january 2019 convenience retailing conference · personal care & beauty personal hygiene...

TRANSCRIPT

Dimitra Katsipi

Sales Director

Convenience Retailing

Conference

January 2019

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 2

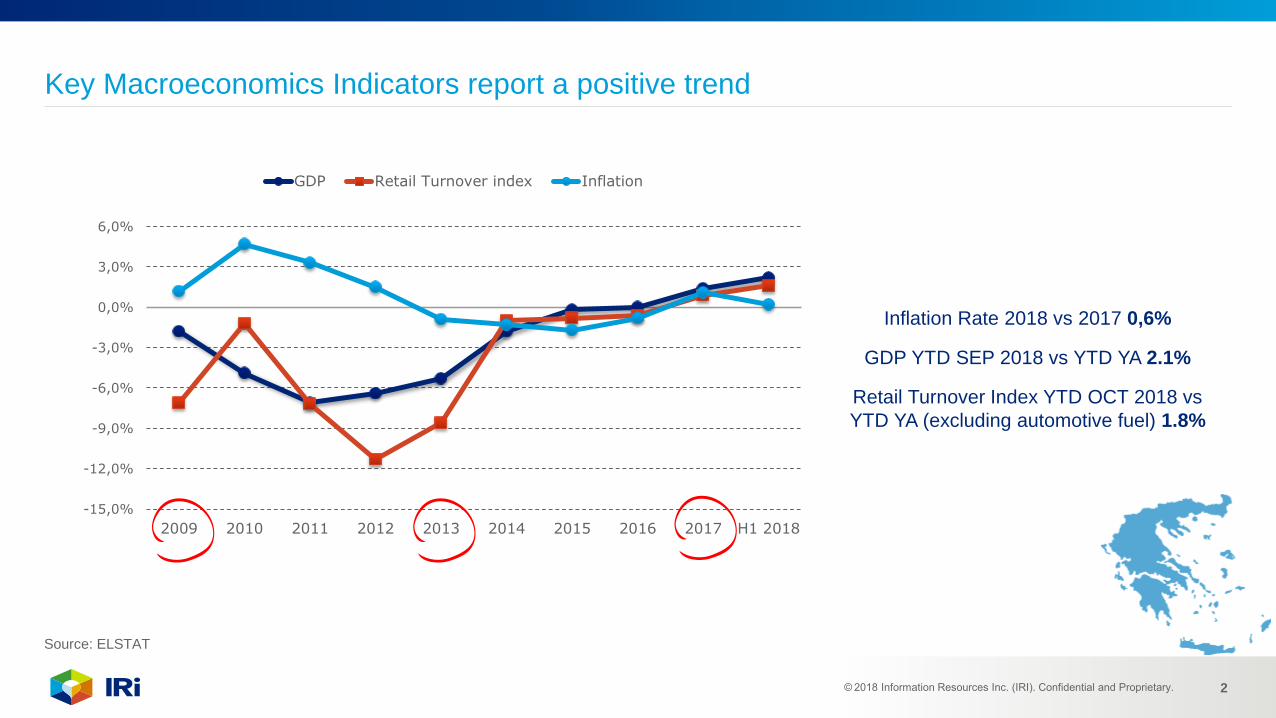

Key Macroeconomics Indicators report a positive trend

Source: ELSTAT

Inflation Rate 2018 vs 2017 0,6%

GDP YTD SEP 2018 vs YTD YA 2.1%

Retail Turnover Index YTD OCT 2018 vs

YTD YA (excluding automotive fuel) 1.8%

-15,0%

-12,0%

-9,0%

-6,0%

-3,0%

0,0%

3,0%

6,0%

2009 2010 2011 2012 2013 2014 2015 2016 2017 H1 2018

GDP Retail Turnover index Inflation

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 3

Key Macroeconomics Indicators report a positive trend

100

98

95

90

86

82

81

79

80

2009

2010

2011

2012

2013

2014

2015

2016

2017

Average spend per capita Index (Reference Year = 2009)

Source: ELSTAT

10,6%

14,8%

21,0%

26,9%

27,5%

26,5%

25,0%

23,5%

21,5%

2009

2010

2011

2012

2013

2014

2015

2016

2017

Unemployment Rate

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 4

6.100

5.480 5.430 5.3005.000 5.100 5.236

2009 2013 2014 2015 2016 2017 2018

FMCG evolution

• FMCG (Food, HBA, Household) | Super/Hyper markets | Value Sales in mio €

Source: IRI InfoScan® FMCG DB. YTD Dec,2018. Bazaar and Random Weight excluded.

+2,7%

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 5

TRENDS PER SHOP TYPE - YTD 2018

0-400 sqm

2500+ sqm

400-1000 sqm

1000-2500 sqm

• % Value Contribution: 13,1%

• Value sales trend: +0,8%

• % Value Contribution: 11,7%

• Value sales trend: +15,9%

• % Value Contribution: 39,4%

• Value sales trend: +1,6%

• % Value Contribution: 35,8%

• Value sales trend: +0,8%

Source: IRI InfoScan, HM/SM, YTD: Jan – December 2018

Hyper markets increase intensively their sales

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 6

HM/SM VALUE SALES TREND 2017 2018

2,7%

1,3%

4,0%

FOOD

HBA

HOUSEHOLD

All Giga-Categories are increasing in 2018

Source: IRI InfoScan, HM/SM, YTD: Jan – December 2018

3,3%

-1,2%

-0,6%

FOOD

HBA

HOUSEHOLD

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 7

HM/SM UNIT SALES TREND 2017 2018

3,3%

2,3%

1,8%

FOOD

HBA

HOUSEHOLD

Unit sales

Source: IRI InfoScan, HM/SM, YTD: Jan – December 2018

2,2%

2,8%

3,5%

FOOD

HBA

HOUSEHOLD

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 8

HM/SM VALUE SALES TREND 2018

2,7%

6,4%

0,6%

2,0%

3,9%

6,2%

2,8%

7,3%

-4,7%

4,0%

-0,2%

HOUSEHOLD CLEANERS & DETERGENTS

OTHER HOUSEHOLD PRODUCTS

PERSONAL CARE & BEAUTY

PERSONAL HYGIENE

PACKAGED FOOD

SNACKS

DAIRY

FROZEN FOOD

COOKING AIDS, INGREDIENTS & CONDIMENTS

NON ALCOHOLIC BEVERAGES

ALCOHOL DRINKS

Source: IRI InfoScan, HM/SM, YTD: Jan – December 2018

All Categories are growing in YTD except Cooking Aids, Ingredients &

Condiments

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 9

HM/SM UNIT SALES TREND YTD 2018

2,0%

5,1%

3,3%

2,2%

3,8%

6,3%

0,9%

8,8%

-3,8%

1,8%

0,2%

HOUSEHOLD CLEANERS & DETERGENTS

OTHER HOUSEHOLD PRODUCTS

PERSONAL CARE & BEAUTY

PERSONAL HYGIENE

PACKAGED FOOD

SNACKS

DAIRY

FROZEN FOOD

COOKING AIDS, INGREDIENTS & CONDIMENTS

NON ALCOHOLIC BEVERAGES

ALCOHOL DRINKS

Same case in Unit Sales

Source: IRI InfoScan, HM/SM, YTD: Jan – December 2018

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 10

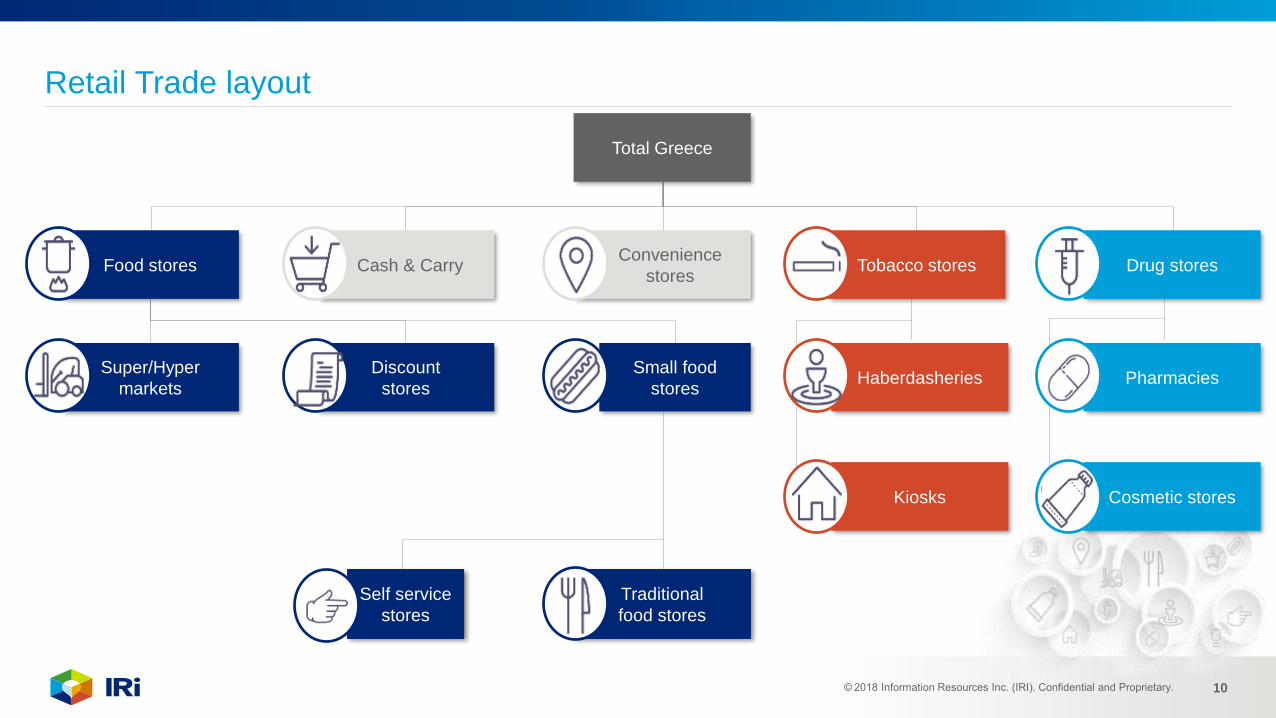

Retail Trade layout

Drug stores

Total Greece

Food stores Cash & CarryConvenience

storesTobacco stores

Super/Hyper

markets

Discount

stores

Small food

stores

Traditional

food stores

Self service

stores

Haberdasheries Pharmacies

Kiosks Cosmetic stores

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 11

Retail Trade layout

Total Greece

Food stores Cash & Carry Convenience

stores Tobacco stores

Super/Hyper

markets

Discount

storesSmall food

stores

Traditional

food stores

Self service

stores

Haberdasheries

KiosksSuper / Hyper 0-400m2

2009 2013 2017 Diff.

16.793 12.747 12.788

2009 2013 2017 Diff.

2.502 2.440 2.422

2009 2013 2017 Diff.

1.058 1.058 934

2009 2013 2017 Diff.

574 207 221 2009 2013 2017 Diff.

13.717 10.100 10.145

2009 2013 2017 Diff.

- 5.426 5.732

2009 2013 2017 Diff.

- 4.674 4.413

2009 2013 2017 Diff.

- 105 1212009 2013 2017 Diff.

12.828 8.391 7.998

2009 2013 2017 Diff.

17.418 11.438 9.982

2009 2013 2017 Diff.

8.699 5.931 5.089

2009 2013 2017 Diff.

8.719 5.507 4.893

Diff. 2017 vs. 2013

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 12

Attica 1,875

Salonica 1,249

North 1,815

Centre 1,683

Peloponnese 1,010

Crete 366

Total Convenience Stores 7,998

YEAR 2016

23,4%

15,6%

22,7%

21,1%

12,6%

4,6%

31,6%

12,9%

17,0%

22,4%

11,3%

4,8% Attica

Salonica

North

Centre

Peloponnese

Crete

WEIGHTED

1,973

1,313

1,885

1,731

1,138

387

8,427

Convenience stores: Number of stores & contribution by geographical area

YEAR 2017

NUMERICAL

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 13

Shoppers have visited approx. 6 different store types last week and 7 last month

99

83 79

73 69

64 65

49

39 43

37

26 20

14 17 15 16 17

10

95

79 76

62 60 59 57

47

36 34 31

22 20 19 16

13 12 10 7

2017 2018

%

Store types visited last month

Source: IRI Shopper Research 2017-2018, Apr 2018

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 14

Challenges

SCALE

Optimum

Assortment

and Category

FINANCIAL

BARRIERS

Limited Space

ONLINE

Competition

Promo

Activities

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 15

Promotions

Out of Stock

Shoppers

Turnover

Unemployment

Macroeconomics

Inflation

Location

Competition Store Layout

AssortmentEmployees

The Retail Environment is …

Price

Store Execution

© 2018 Information Resources Inc. (IRI). Confidential and Proprietary. 16

THANK YOU!

For More Information, Contact Us…

IRI Greece

31 Spartis Street, 114 52, Metamorfosi, Athens, Greece [email protected]

+30 210 27 87 698

Follow us on Twitter: @IRIworldwide