jakarta market report 4 q 2012

TRANSCRIPT

jakarta rEaL EStatE research & forecast report

www.colliers.com

4Q 2012 i the knowledge

Property Sector Overviewoffice sectorthe office sector stole the limelight in 2012 with a y-o-y increase of 47.6% for US dollar denominatedbuildings and 33.2% for rupiah buildings. the average asking base rental rates at the end of the year wereUS$31.30/sq m/month and IDr169,859/sq m/month respectively. Meanwhile, new office space will be limitedin 2013 but leasing demand should continue to be buoyant. On the strata-title office front where stock for salewas limited, the y-o-y office asking prices edged up by 31.3% and 26.2%, respectively for rupiah and USdollars, i.e. to IDr27.8 million/sq m and US$3,313/sq m. the limited supply of new office space in 2013 foreither lease or sale will further strengthen the landlords position in rental negotiation and increase rents.

apartment sectorDemand for high-rise residential units has been growing quite significantly since early 2012. Due to this trendand limited stock in sub-markets like the CBD and South jakarta, rupiah prices went up by 25.1% (to IDr29.8million/sq m) and20.5% (to IDr20.7 million/sq m), respectively. In terms of the annual of new apartmentstock, 2012 saw a historic high with a total of 19,706 apartment units coming on the market in jakarta. We stillanticipate seeing a substantial number of apartment units expected to be finished in 2013 and 2014.

resiDentiaL eXpatriate hoUsinG sectorthe rental tariff for expatriate housing generally climbed the range of 15% to 30% per unit for 2H 2012 period. rentals were up mainly due to strong and abundant inquiries for expatriate living accommodation but on theother hand the number of such properties available is increasingly limited - in particular those that meet expatstandards regarding size, location, quality, furniture and facilities available in one house. Such conditions haveled to a landlord market where home owners have a strong bargaining position. Searching for aquality homethat meets a required budget is very challenging, particularly in high-demand locations like Pondok Indah,kebayoran Baru (certain areas which are close to the CBD) and kuningan.

retaiL sectorasking base rent for non-anchor, non-ground floor tenants in sizeable shopping malls increased 18.5% during2012, and was recorded at an average IDr461,399/sq m/month. We anticipate further growth in rental ratesgiven the very limited amount of new retail space and the fact that pre-committed occupancy for underconstruction projects is high.

inDUstriaL estate sectorIndustrial land prices in Greater jakarta increased significantly by 44% in karawang to an average ofUS$155.80/sq m. Meanwhile, a 37% YoY increase was also seen in Bekasi with the average price atUS$206.20/sq m and in Serang with a 32% increase (average price at US$114.60/sq m). On the sales front,the total industrial sales in 2012 only amounted to 51% (636.4 hectares) of the total sales in 2011, not becauseof slow demand but mainly because of a lack of industrial land stock.

office sectorSupply

jakarta office cUmULatiVe sUppLY

Colliers International Indonesia - research

cbD During 2012, total new office space in the CBD totalled 289,514 sq m, representing a jump jump by twice compared the total annual supply in 2011. In the middle of 2012, three high-rise buildings, i.e. aXa tower, Multivision, Office 8 and two mid-rise buildings, i.e. Indosurya Plaza and 18 Office Park tower D were in operation bringing a total of 144,073 sq m of new office space to the CBD. In the following quarter, there was the addition of around 57,000 sq m from the operation of the World trade Center II. Subsequent to that, a total of 88,441 sq m was contributed from the operation of tower One at the City Center and tower C at 18 Office Park. Meanwhile, two buildings are being refurbished this quarter, namely Bina Mulia I and II with the building façades being renovated. Bina Mulia II will be renamed tempo Pavilliun I and will begin operations around april 2013, while Bina Mulia I will begin operations in august 2013. a reduction of supply will also take place in jalan jendral Gatot Subroto where the Wisma Putra

kalimantan buildings are to be demolished and replaced with a brand new building .

total office space in the CBD as of 4Q 2012 is 4.62 million sq m, representing an increase of 6% over that at the end of 2011.

Since 3Q 2012, we had forecast that Menara Palma 2 would be the only supply for 2013, but then two office buildings, which had previously been planned for operations in 2012, rescheduled their completions to early 2013. this includes an office building in Setiabudi, South jakarta, which, at the end of 2012, was still completing the façade work. another building is DBS tower, which decided to reschedule operations to early 2013 and three mid-rise office towers of 18 Office Park project. thus, from the previously projected 40,000 sq m of office space at Menara Palma 2, there will be a total of 145,332 sq m of new office space in the CBD by 2013.

JAKARTANew office space supply in jakarta (CBD and the outside CBD area) showed a significant increase during 2012. By the end of 2012, there was 547,070 sq m of additional office space (supplied by 16 office buildings) which is the largest annual supply since the economy crisis in 1998. Meanwhile, three office buildings located in the CBD stopped operating due to refurbishment, they area Wisma Putra kalimantan, Bina Mulia I and Bina Mulia II removing around 27,175 sq m of the total office stock. the dynamic events in the office supply during the year brought the cumulative supply to 6.75 million sq m.

the office supply in jakarta is projected to continue growing. though it will be far less in 2013, the annual supply is projected to increase rapidly from 2014 to 2016. During that time, it is projected that the annual supply will be 40 - 60% more than in 2012.

Based on marketing scheme, the jakarta office market is still dominated by offices for lease. Currently, 81.2% of the 6.75 million sq m of jakarta office space is offered as office for lease.

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,0008,000,0009,000,000

10,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

F

2013

F

2014

F

2015

F

2016

F

sq m

Existing Supply annual Supply

p. 2 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

composition of cbD office sUppLY baseD on GraDe

Colliers International Indonesia - research

In the CBD, 81% of the existing 4.62 million sq m registered in 2012 is marketed for lease. the supply of offices for lease should continue to grow at least until 2014. Of 531,755 sq m of new supply that will be operational in 2013 - 2014, 317,717 sq m or 61% will be marketed for lease.

In addition, there are 21 new office developments that have been announced will be built in the CBD during 2013 - 2015 in the CBD, 18 of which started construction in 2012. Meanwhile, some new names have also been introduced like Satrio tower 2, Bahana Office tower, World Capital tower, World trade Center III, Sequis Life tower 2 and Gatot Subroto Office tower.

annUaL cbD office sUppLY baseD on area

Colliers International Indonesia - research

oUtsiDe cbD the year 2010 was the momentum of office market in the outside the CBD area showed rapid growth. In 2010 and 2011, the total office supply reached over 100,000 sq m annually. In 2012, the annual supply in the outside the CBD area has grown to twice that of the previous year. During 2012, eight new office buildings contributed 257,556 sq m, bringing the

cumulative supply to 2.13 million sq m in the outside the CBD area. Four office buildings that began operating in early 2012 were Menara Satu, Wisma Pondok Indah 3, Grand Slipi tower and Sovereign Plaza. another four were PHE tower, Eighty8, trihamas and Menara Merdeka.

Premium, 335,918 sq m

Grade a, 1,759,864 sq m

Grade B, 1,513,140 sq m

Grade C, 1,012,052 sq m

0 100,000 200,000 300,000 400,000 500,000

thamrin

Sudirman

rasuna Said

Mega kuningan

Gatot Subroto

Satrio

s q m2009 2010 2011 2012 2013F

coLLiers internationaL | p. 3

JAKARTA | 4q 2012 | oFFiCe

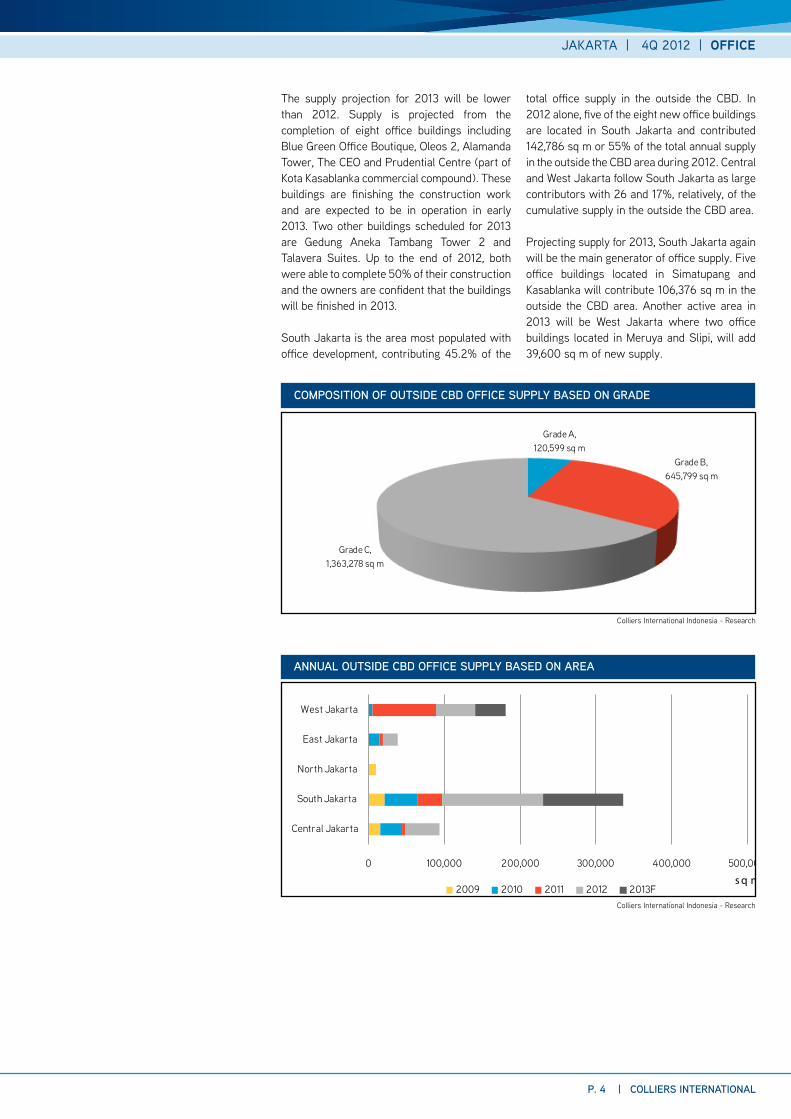

the supply projection for 2013 will be lower than 2012. Supply is projected from the completion of eight office buildings including Blue Green Office Boutique, Oleos 2, alamanda tower, the CEO and Prudential Centre (part of kota kasablanka commercial compound). these buildings are finishing the construction work and are expected to be in operation in early 2013. two other buildings scheduled for 2013 are Gedung aneka tambang tower 2 and talavera Suites. Up to the end of 2012, both were able to complete 50% of their construction and the owners are confident that the buildings will be finished in 2013.

South jakarta is the area most populated with office development, contributing 45.2% of the

total office supply in the outside the CBD. In 2012 alone, five of the eight new office buildings are located in South jakarta and contributed 142,786 sq m or 55% of the total annual supply in the outside the CBD area during 2012. Central and West jakarta follow South jakarta as large contributors with 26 and 17%, relatively, of the cumulative supply in the outside the CBD area.

Projecting supply for 2013, South jakarta again will be the main generator of office supply. Five office buildings located in Simatupang and kasablanka will contribute 106,376 sq m in the outside the CBD area. another active area in 2013 will be West jakarta where two office buildings located in Meruya and Slipi, will add 39,600 sq m of new supply.

composition of oUtsiDe cbD office sUppLY baseD on GraDe

Colliers International Indonesia - research

annUaL oUtsiDe cbD office sUppLY baseD on area

Colliers International Indonesia - research

Grade a, 120,599 sq m

Grade B, 645,799 sq m

Grade C, 1,363,278 sq m

0 100,000 200,000 300,000 400,000 500,000

Central jakarta

South jakarta

North jakarta

East jakarta

West jakarta

s q m2009 2010 2011 2012 2013F

p. 4 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

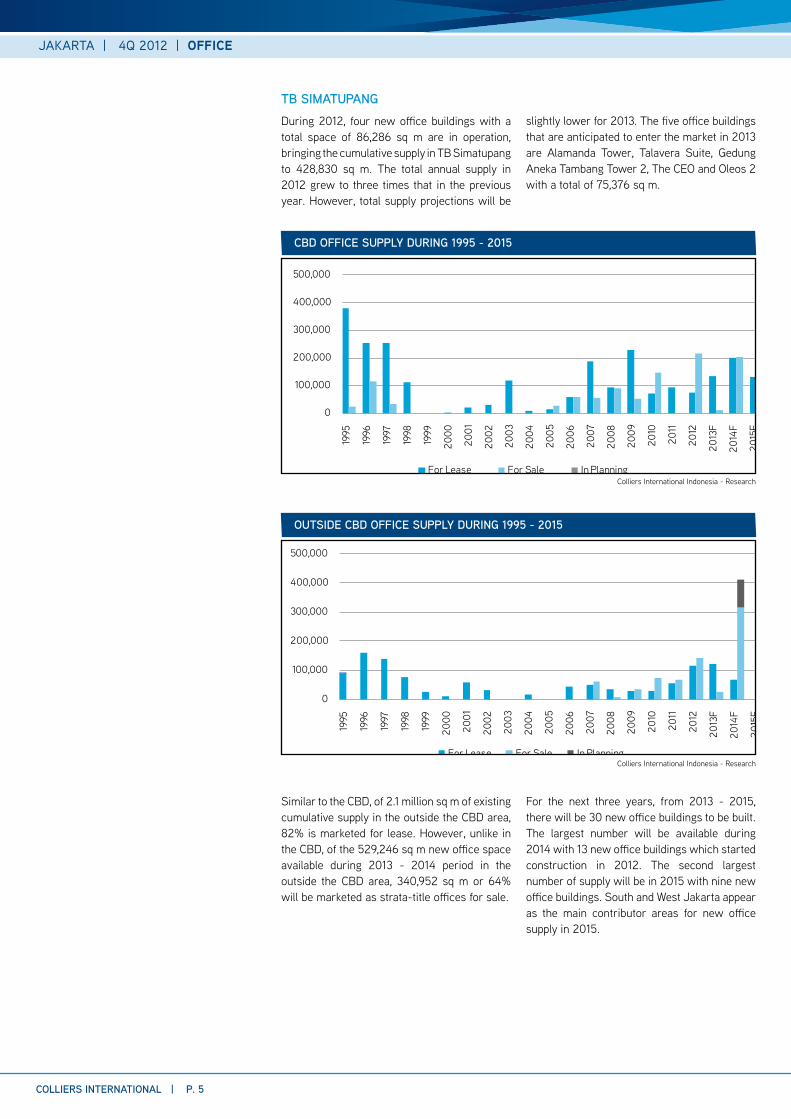

tb simatUpanG During 2012, four new office buildings with a total space of 86,286 sq m are in operation, bringing the cumulative supply in tB Simatupang to 428,830 sq m. the total annual supply in 2012 grew to three times that in the previous year. However, total supply projections will be

slightly lower for 2013. the five office buildings that are anticipated to enter the market in 2013 are alamanda tower, talavera Suite, Gedung aneka tambang tower 2, the CEO and Oleos 2 with a total of 75,376 sq m.

cbD office sUppLY DUrinG 1995 - 2015

Colliers International Indonesia - research

Similar to the CBD, of 2.1 million sq m of existing cumulative supply in the outside the CBD area, 82% is marketed for lease. However, unlike in the CBD, of the 529,246 sq m new office space available during 2013 - 2014 period in the outside the CBD area, 340,952 sq m or 64% will be marketed as strata-title offices for sale.

For the next three years, from 2013 - 2015, there will be 30 new office buildings to be built. the largest number will be available during 2014 with 13 new office buildings which started construction in 2012. the second largest number of supply will be in 2015 with nine new office buildings. South and West jakarta appear as the main contributor areas for new office supply in 2015.

0

100,000

200,000

300,000

400,000

500,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

F

2014

F

2015

F

For Lease For Sale In Planning

oUtsiDe cbD office sUppLY DUrinG 1995 - 2015

Colliers International Indonesia - research

0

100,000

200,000

300,000

400,000

500,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

F

2014

F

2015

FFor Lease For Sale In Planning

coLLiers internationaL | p. 5

JAKARTA | 4q 2012 | oFFiCe

new sUppLY pipeLine

projecteD compLetion

timebUiLDinG name Location sGa

(sQ m) marketinG scheme DeVeLopment statUs*

cbD area2013 DBS tower (Ciputra World jakarta 1) Satrio 64,000 For Lease and For Strata-title Under Conctruction

2013 Menara Prima 2 Mega kuningan 40,000 For Lease Under Conctruction

2013 Perkantoran Setiabudi rasuna Said 11,000 For Strata-title Under Conctruction

2013 18 Park tower a Sudirman 4,814 For Lease Under Conctruction

2013 18 Park tower B Sudirman 4,570 For Lease Under Conctruction

2013 18 Park tower E Sudirman 4,233 For Lease Under Conctruction

2013 tempo Pavilliun I rasuna Said 7,075 For Lease Under Conctruction

2013 tempo Pavilliun II rasuna Said 9,640 For Lease Under Conctruction

2014 Chase tower Sudirman 75,000 For Lease Under Conctruction

2014 Gran rubina tower 1 rasuna Said 31,438 For Strata-title Under Conctruction

2014 Life tower rasuna Said 30,500 For Lease Under Conctruction

2014 Satrio Square Satrio 24,600 For Lease and For Strata-title Under Conctruction

2014 Sahid Sudirman Center Sudirman 126,600 For Strata-title Under Conctruction

2014 the Noble House Office tower Mega kuningan 45,000 For Lease and For Strata-title Under Conctruction

2014 Wisma Mulia 2 Gatot Subroto 70,000 For Lease Under Conctruction

2015 Bahana Office tower Mega kuningan 50,000 For Lease Under Planning

2015 Ciputra World jakarta 2 Satrio 70,000 For Lease and For Strata-title Under Planning

2015 International Financial Center 2 Sudirman 50,000 For Lease Under Conctruction

2015 Mangkuluhur tower B Gatot Subroto 39,356 For Strata-title Under Conctruction

2015 Menara Selaras Sudirman 36,596 For Lease Under Planning

2015 Office tower @St regis Gatot Subroto 90,000 For Strata-title Under Planning

2015 rasuna tower rasuna Said 80,000 For Lease Under Construction

2015 tower two at the City Center kH Mas Mansyur 39,204 For Lease Under Planning

2016 District 8 tower 2 Sudirman 71,545 For Strata-title Under Planning

2016 District 8 tower 3 Sudirman 139,000 For Strata-title Under Planning

2016 Graha Surya Internusa rasuna Said 45,000 For Lease Under Planning

2016 Graha Surya Internusa 2 rasuna Said 45,000 For Strata-title Under Planning

2016 Gran rubina tower 2 rasuna Said 70,000 For Strata-title Under Planning

2016 Gatot Subroto Office tower Gatot Subroto 100,000 For Strata-title Under Planning

2016 Satrio Project Satrio 100,000 For Lease Under Planning

2016 Sequis Life tower 2 Sudirman 80,000 For Lease Under Planning

2016 World trade Center III Sudirman 70,000 For Lease Under Planning

2016 World Capital tower Mega kuningan 90,000 For Strata-title Under Planning

oUtsiDe cbD area (exclude tb simatUpanG)2013 Blue Green Office Boutique Meruya 20,000 For Lease Under Construction

2013 DIPO Business Park Slipi 19,600 For Strata-title Under Construction

2013 Prudential Centre Casablanca 31,000 For Lease Under Construction

2014 GP Plaza Slipi 12,204 For Strata-title Under Construction

2014 Menara Sentraya Blok M 52,072 For Lease and For Strata-title Under Construction

2014 the Suites Pantai Indah kapuk 13,200 For Strata-title Under Construction

2014 Wisma 77 tower 2 Slipi 24,200 For Strata-title Under Construction

2014 kirana two Sunter 17,563 For Lease and For Strata-title Under Construction

2014 Sky 18 tower kalibata 27,500 For Strata-title Under Construction

p. 6 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

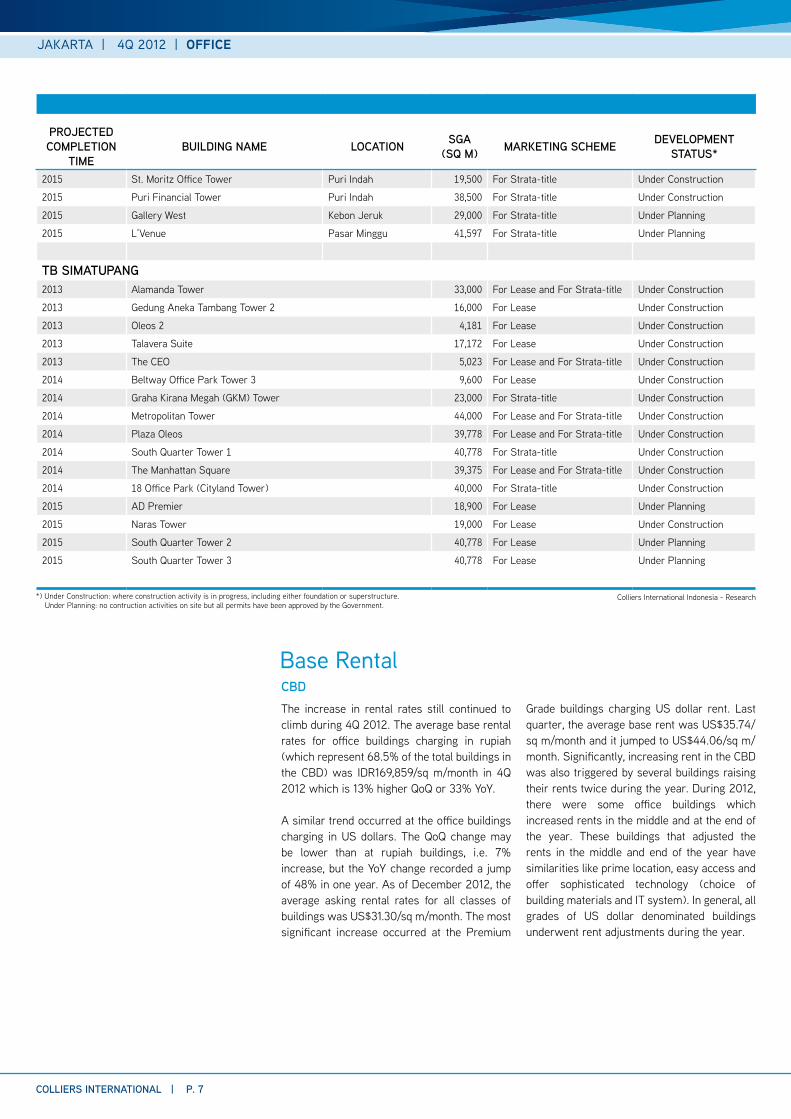

cbD the increase in rental rates still continued to climb during 4Q 2012. the average base rental rates for office buildings charging in rupiah (which represent 68.5% of the total buildings in the CBD) was IDr169,859/sq m/month in 4Q 2012 which is 13% higher QoQ or 33% YoY.

a similar trend occurred at the office buildings charging in US dollars. the QoQ change may be lower than at rupiah buildings, i.e. 7% increase, but the YoY change recorded a jump of 48% in one year. as of December 2012, the average asking rental rates for all classes of buildings was US$31.30/sq m/month. the most significant increase occurred at the Premium

Grade buildings charging US dollar rent. Last quarter, the average base rent was US$35.74/sq m/month and it jumped to US$44.06/sq m/month. Significantly, increasing rent in the CBD was also triggered by several buildings raising their rents twice during the year. During 2012, there were some office buildings which increased rents in the middle and at the end of the year. these buildings that adjusted the rents in the middle and end of the year have similarities like prime location, easy access and offer sophisticated technology (choice of building materials and It system). In general, all grades of US dollar denominated buildings underwent rent adjustments during the year.

Colliers International Indonesia - research*) Under Construction: where construction activity is in progress, including either foundation or superstructure. Under Planning: no contruction activities on site but all permits have been approved by the Government.

Base Rental

projecteD compLetion

timebUiLDinG name Location sGa

(sQ m) marketinG scheme DeVeLopment statUs*

2015 St. Moritz Office tower Puri Indah 19,500 For Strata-title Under Construction

2015 Puri Financial tower Puri Indah 38,500 For Strata-title Under Construction

2015 Gallery West kebon jeruk 29,000 For Strata-title Under Planning

2015 L’Venue Pasar Minggu 41,597 For Strata-title Under Planning

tb simatUpanG2013 alamanda tower 33,000 For Lease and For Strata-title Under Construction

2013 Gedung aneka tambang tower 2 16,000 For Lease Under Construction

2013 Oleos 2 4,181 For Lease Under Construction

2013 talavera Suite 17,172 For Lease Under Construction

2013 the CEO 5,023 For Lease and For Strata-title Under Construction

2014 Beltway Office Park tower 3 9,600 For Lease Under Construction

2014 Graha kirana Megah (GkM) tower 23,000 For Strata-title Under Construction

2014 Metropolitan tower 44,000 For Lease and For Strata-title Under Construction

2014 Plaza Oleos 39,778 For Lease and For Strata-title Under Construction

2014 South Quarter tower 1 40,778 For Strata-title Under Construction

2014 the Manhattan Square 39,375 For Lease and For Strata-title Under Construction

2014 18 Office Park (Cityland tower) 40,000 For Strata-title Under Construction

2015 aD Premier 18,900 For Lease Under Planning

2015 Naras tower 19,000 For Lease Under Construction

2015 South Quarter tower 2 40,778 For Lease Under Planning

2015 South Quarter tower 3 40,778 For Lease Under Planning

coLLiers internationaL | p. 7

JAKARTA | 4q 2012 | oFFiCe

the average rent for both US dollar and rupiah rent (combined) for all grades of buildings showed that thamrin and Sudirman sub-markets had the highest rent. average rental rates in thamrin and Sudirman were IDr286,805 (US$29.87) and IDr256,568 (US$26.73) per sq m per month, respectively. Meanwhile Satrio and Mega kuningan were at IDr194,125 (US$20.22) and IDr174,979 (US$18.23) per sq m per month. Gatot Subroto and rasuna Said placed the lowest at IDr166,894 (US$17.38) and IDr133,528 (US$13.91), respectively, per sq m per month. the average rent in the rasuna Said sub-market was somewhat low because some small

and old office buildings populated this area; however, given increasingly higher land prices and higher site coverage, newer and future buildings are built with Grade a quality.

In general, office buildings in operation between 2009 and 2012 experienced the highest increase in average asking rental rates achieving IDr175,455 for rupiah denominated buildings and US$36.10 / sq m / month for US dollar. to date, most large new office buildings operating in the CBD area are of Grade a quality and they somewhat raised the overall average rental rates for the last two years.

oUtsiDe cbD average rental rates in the outside the CBD area moved upward significantly during the quarter recording an increase of 23% QoQ at an average of IDr123.312/sq m/month. Comparing YoY figures, this reflected an increase by 33%. Such a substantial increase during the quarter was mainly fuelled by the operation of three new office buildings: PHE tower, trihamas and Eighty8 at kota kasablanka.

Similarly, the overall asking rental rates in US dollars also rose this quarter by 12% to US$15.50 / sq m / month, primarily triggered by the adjustment of one office park located in the tB Simatupang area and the new operation of Merdeka tower. During the first three quarters, rental rates in US dollar denominated buildings are quite marginal and therefore the YoY increase was recorded at 16%.

In popular office areas like Slipi (West jakarta) and Mt Haryono (East jakarta), rental rates were recorded at IDr96,818/sq m/month and IDr97,500/sq m/month, respectively. Meanwhile, at preferred commercial locations in South jakarta like in kasablanka, kebayoran Baru, kemang, Permata Hijau and Gandaria, the average rental rates were registered at IDr101,455/sq m/month.

In the growing commercial areas like tB Simatupang and Pondok Indah, an increase in the US dollar rates was generated particularly because arcadia Office Park raised their rent by as much as 20% QoQ following Menara talavera which initiated the adjustment in the early part of 2012. average rental rates in US dollar denominated buildings in tB Simatupang were US$15.45/sq m/month which represents an increase of 12% over the previous quarter. the average rental tariff in rupiah was IDr117,183/sq m/month.

aVeraGe askinG rentaL rates in the cbD DUrinG 1995 - 2012

Colliers International Indonesia - research

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

IDr 0

IDr 48,000

IDr 96,000

IDr 144,000

IDr 192,000

IDr 240,000

IDr 288,000

IDr 336,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

IDr US$

p. 8 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

Strata-Title Offices CBDa total of 805,829 sq m of strata-titled office space is recorded in the CBD as of 4Q 2012. the latest strata-titled office building entering the market is tower One at the City Center with total semi-gross area of around 84,000 sq m. During 2012 there were four strata-title buildings completed and in operation including, Multivision tower, aXa tower, Office 8 and the City Center.

New strata-titled office space of 214,995 sq m during 2012 was the highest annual supply since 1990 but 2013 will only see a very limited supply of 11,000 sq m from one building which was previously projected to be completed in 2012 but which postponed operations until 2013. On the contrary, around six strata-titled office buildings are predicted to flood the market in 2014 - 2015 with around 400,000 sq m of strata-titled office space. two of these buildings, Gran rubina and Sahid Sudirman Center are currently under construction, while others, like Ciputra World jakarta 2, the Noble House and Office at St. regis have confirmed that they will

start construction soon.

the sales performance of strata-titled office has been quite astonishing with the current take-up rate of 98.9% (leaving only 1% space unsold or less than 10,000 sq m). this is likely to continue in 2013 since 66% of the projected supply for that year has been pre-committed. Such conditions will lead prices to see further adjustment next year.

Currently, the average selling price of strata-titled office space in the CBD is IDr27.8 million/sq m and US$3,313/sq m for office buildings charging in US dollars. this indicates that asking prices for office buildings in rupiah have experienced an escalation by 5.4% compared to the previous quarter and in one year prices have climbed by 23.3%. Meanwhile, the price discrepancy QoQ in US dollars was somewhat higher, i.e. up by 12.9% or 31.3% YoY. Given the vibrant market, the current asking price ranging from IDr30 to 45 million/sq m will strongly move ahead in 2013.

aVeraGe askinG rentaL rates in the oUtsiDe cbD DUrinG 2005 - 2012

Colliers International Indonesia - research

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

IDr 0

IDr 19,200

IDr 38,400

IDr 57,600

IDr 76,800

IDr 96,000

IDr 115,200

IDr 134,400

IDr 153,600

2005 2006 2007 2008 2009 2010 2011 2012

rp US$

coLLiers internationaL | p. 9

JAKARTA | 4q 2012 | oFFiCe

oUtsiDe cbD Strata-titled offices are becoming more popular, not only in the downtown area but also in the outside the CBD area where 92% of the total 404,243 sq m was sold out. During 2012, there was a total of 132,980 sq m of new strata-titled space available but this did not reduce the take-up level because pre-commitment absorption was high. Furthermore, the pre-committed take-up level for future office buildings projected to begin operations in 2013 - 2014 has reached 28% as of 4Q 2012. this situation has stimulated asking prices to edge higher. Currently, the asking price for office space in

rupiah increased by 2.6% QoQ while the YoY change shows a substantial figure of 24.6%. Furthermore, the rapid increase also triggered the future strata-titled offices to adjust their prices. the chart below presents the price difference between the average asking price in early 2012 and the average current price at the end of 2012 which demonstrates an increase of 15 to 20% in one year. the average price shown in the chart is the combination of the average price of new and future strata-titled buildings being marketed in 2012.

the Gap between initiaL anD cUrrents aVeraGe price DUrinG 2012 of new anD fUtUre office bUiLDinG

Colliers International Indonesia - research

rp15

,000

,000

rp17

,000

,000

rp19

,000

,000

rp21

,000

,000

rp23

,000

,000

rp25

,000

,000

rp27

,000

,000

rp29

,000

,000

rp31

,000

,000

rp33

,000

,000

rp35

,000

,000

CBD

Outside CBD

aVeraGe askinG rentaL rates in the oUtsiDe cbD DUrinG 2005 - 2012

Colliers International Indonesia - research

$0

$521

$1,042

$1,562

$2,083

$2,604

$3,125

$3,646

IDr 0

IDr 5,000,000

IDr 10,000,000

IDr 15,000,000

IDr 20,000,000

IDr 25,000,000

IDr 30,000,000

IDr 35,000,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

CBD (IDr) Outside (IDr) CBD (USD)

South and West jakarta are two areas that currently have quite a few strata-titled office buildings both existing and under construction. the average asking price for office buildings in West jakarta was IDr23.4 million / sq m. Strata-title office buildings located in Slipi, West

jakarta are currently offered at between IDr18.0 and 26.0 million / sq m. Besides that, Puri Indah and kebun jeruk, also in West jakarta, appear to be a more popular area for strata-titled offices where asking prices range from IDr24.0 to 25.0 million/sq m.

Colliers International Indonesia - research

p. 10 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

cbD the occupancy level in 2011 was one of the highest in office market history. In 2012 where the combination of limited supply and continued demand happened, occupancy level as at the end of the year rose to 97.3%. total annual office space during 2012 alone has been 95% absorbed and thus total annual office absorption in the CBD reached around 422,000 sq m. Since 2009, total annual absorption of office space has went up gradually following the increasing business expansion. the year 2013 will be quite challenging for office market because total new office stock is only 45% of the total supply in 2012. On the other hand such situation will maintain the occupancy level at high level because currently the total projected supply for 2013 has been 40% absorbed. Based on area, all corridors in the CBD have very high occupancy rates particularly in Mega kuningan, Gatot Subroto and thamrin where occupancy rates have reached over 98%. Other sub market also showed good occupancy performance for example, Sudirman with high quality office building reached 97.1%, rasuna Said where new high quality buildings will be

located with 95.7% occupancy and Satrio with 93.3%.

Going forward, the population of new office buildings will be concentrated in Satrio and Mega kungingan sub markets where 31% of the total future offices supply will be located. Meanwhile only 10% of future office stock will be located in Sudirman and rasuna Said. It would be a challenge for Mega kuningan and Satrio to maintain occupancy level should all of these projects be completed.

High occupancy cost in the Premium and Grade a buildings do not preclude tenants from expanding office space in these buildings and in fact, it is very hard to find large spaces. Of all new office buildings completed in 2012, only two buildings have an occupancy level below 90%. Brisk performance of Premium and Grade a office buildings brought the average occupancy rates to 97.6% for this office segment in 2012. While the lower class, several office buildings still had occupancy rates below 70%.

the occUpancY

serVice charGes While base rental rates trended upward during the year, services charges were relatively stable. thus far, there has not been any trigger to stimulate tariff increases. But the market is anticipating a different story for next year, given some adjustment plans which will take effect toward operational cost.

In the CBD, the overall service charges initially started at IDr55,086/sq m/month early in 2012 before reaching IDr56,938/sq m/month in 4Q 2012. On the US dollar front, service charges were up from US$6.31/sq m/month a year ago to US$6.37/sq m/month in 4Q 2012.

Nothing changed much in the Premium and Grade a office buildings. Service charges were only adjusted modestly by 6% YoY to US$6.68/sq m/month. Meanwhile, in the US dollar, Grade a office buildings, service charges were on average IDr60,745/sq m/month in 4Q 2012 which indicate an increase of 9% over the year.

In the same pattern, the average service charge in the outside CBD was relatively stable both in rupiah and US dollars. In 4Q 2012, service charges stood at IDr42,405/sq m/ month and US$5.25 / sq m / month which represent a YoY change of 5 and 7%.

Meanwhile, the tB Simatupang area is still the main supplier for strata-titled office buildings in South jakarta. there are currently six strata-title office buildings being built in this corridor with the average asking price of IDr22.4 million/sq m. In addition to tB Simatupang,

there are also two under construction strata-titled office buildings located in kebayoran and kasablanka, South jakarta. Prices in this area were at IDr30 - 35 million/sq m due to their proximity to the main commercial area.

p. 11 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

space aVaiLabLe anD space committeD in the cbD (2013 - 2015)

Colliers International Indonesia - research

0 100,000 200,000 300,000 400,000 500,000

2015F

2014F

2013F

sq m

Space absorbed annual Supply

oUtsiDe cbD However, the inflow of new office supply edged down the occupancy rates slightly to 92.8% in 4Q 2012. Based on area, office buildings located in North and East jakarta recorded the highest average occupancy rates. But in fact, this is mostly as a consequence of the limited supply of office buildings in both of these areas. On the contrary, despite a lower occupancy rate, West and South jakarta were the most active areas to contribute new office supply in the last two years. In West jakarta, slow absorption experienced by large buildings located in this area maintained an average occupancy rate of

only around 90%. Meanwhile in South jakarta, the average occupancy rate was 93.4%.

In active sub-markets like tB Simatupang, finding ample office space is tough, evidenced by the current occupancy rate of 97.5%. During the year, new transactions were dominated by deals in new buildings and will only affect the overall occupancy when the buildings go into operation. Pre-commitment levels for buildings scheduled to be in operation in 2013 in tB Simatupang area have reached 55%, signalling that the market will remain vibrant in 2013.

annUaL office space absorption in the cbD

Colliers International Indonesia - research

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

p. 12 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

Given auspicious economic projections, business activity is projected to carry on in 2013. Further, an independent report issued by PWC and the Urban Land Institute called “ Emerging trends in real Estate asia Pacific 2013” placed jakarta as the number one investment and development destination. Investors’ positive perception will help the real estate market to perform. Corporations with local market oriented products like finance, banking, insurance, FMCG and automotive enjoy their growing period and will likely expand their business operations. On the other hand, new office stock will be limited in 2013. Combining this limited supply and demand (continued inquiries for office space) would be an unavoidable factor for rental rates to move forward. after all, the occupancy cost (base rental rates and service charge) would soar given the government plan to increase the electricity tariff, parking tariff, minimum regional wages and fuel price.

On the other hand, the heightening occupancy

cost must have been a torment for export-oriented businesses amid the shadow of the European economic slowdown. We have heard that some tenants have opted to be cost-efficient in anticipation of the rising rental cost by reconfiguring office space (putting more hot desktops for mobile employees) or relocating to lower cost premises.

the rising rental rates have been a blessing for the strata-titled market particularly, in the CBD area. With the current rental rates, having a strata-title should be feasible for either investment or owner-occupation. the monthly cost of renting office space is now somewhat equal to paying monthly instalments (principal at the currently low lending rate) when buying strata-titled office space using a bank loan. another advantage is that the premises will become the owner’s asset at the end. We have started seeing either tenants shift their leasing plans to owning a strata-titled asset while occupying it or investors buying strata-titled space for leasing it out.

Outlook

space aVaiLabLe anD space committeD in the oUtsiDe cbD (2013 - 2015)

Colliers International Indonesia - research

0 100,000 200,000 300,000 400,000 500,000

2015F

2014F

2013F

sq m

Space absorbed annual Supply

annUaL office space absorption in the oUtsiDe cbD

Colliers International Indonesia - research

0

50,000

100,000

150,000

200,000

250,000

300,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

p. 13 | coLLiers internationaL

JAKARTA | 4q 2012 | oFFiCe

Colliers International Indonesia - research

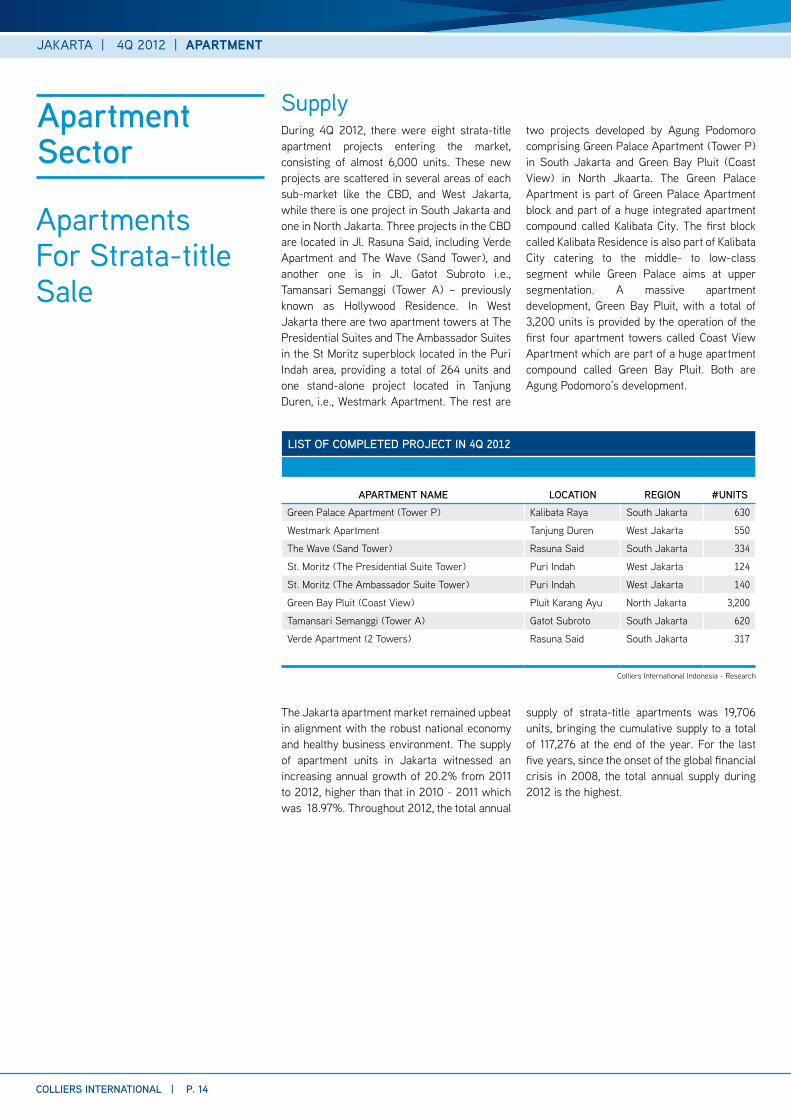

During 4Q 2012, there were eight strata-title apartment projects entering the market, consisting of almost 6,000 units. these new projects are scattered in several areas of each sub-market like the CBD, and West jakarta, while there is one project in South jakarta and one in North jakarta. three projects in the CBD are located in jl. rasuna Said, including Verde apartment and the Wave (Sand tower), and another one is in jl. Gatot Subroto i.e., tamansari Semanggi (tower a) – previously known as Hollywood residence. In West jakarta there are two apartment towers at the Presidential Suites and the ambassador Suites in the St Moritz superblock located in the Puri Indah area, providing a total of 264 units and one stand-alone project located in tanjung Duren, i.e., Westmark apartment. the rest are

two projects developed by agung Podomoro comprising Green Palace apartment (tower P) in South jakarta and Green Bay Pluit (Coast View) in North jkaarta. the Green Palace apartment is part of Green Palace apartment block and part of a huge integrated apartment compound called kalibata City. the first block called kalibata residence is also part of kalibata City catering to the middle- to low-class segment while Green Palace aims at upper segmentation. a massive apartment development, Green Bay Pluit, with a total of 3,200 units is provided by the operation of the first four apartment towers called Coast View apartment which are part of a huge apartment compound called Green Bay Pluit. Both are agung Podomoro’s development.

Supplyapartment sector

Apartments For Strata-title Sale

the jakarta apartment market remained upbeat in alignment with the robust national economy and healthy business environment. the supply of apartment units in jakarta witnessed an increasing annual growth of 20.2% from 2011 to 2012, higher than that in 2010 - 2011 which was 18.97%. throughout 2012, the total annual

supply of strata-title apartments was 19,706 units, bringing the cumulative supply to a total of 117,276 at the end of the year. For the last five years, since the onset of the global financial crisis in 2008, the total annual supply during 2012 is the highest.

coLLiers internationaL | p. 14

JAKARTA | 4q 2012 | apartment

List of compLeteD project in 4Q 2012

apartment name Location reGion #UnitsGreen Palace apartment (tower P) kalibata raya South jakarta 630

Westmark apartment tanjung Duren West jakarta 550

the Wave (Sand tower) rasuna Said South jakarta 334

St. Moritz (the Presidential Suite tower) Puri Indah West jakarta 124

St. Moritz (the ambassador Suite tower) Puri Indah West jakarta 140

Green Bay Pluit (Coast View) Pluit karang ayu North jakarta 3,200

tamansari Semanggi (tower a) Gatot Subroto South jakarta 620

Verde apartment (2 towers) rasuna Said South jakarta 317

List of new strata-titLe apartment sUppLY in 2012

apartment name Location reGion DeVeLoper #Unit

Denpasar residence (tower kintamani) Satrio CBD agung Podomoro Group 550Denpasar residence (tower Ubud) Satrio CBD agung Podomoro Group 550tamansari Semanggi (tower a) Gatot Subroto CBD Wika realty 620thamrin Executive residence kebon kacang CBD agung Podomoro Group 400the Wave (Coral tower) rasuna Said CBD Bakrieland Develoopment 324the Wave (Sand tower) rasuna Said CBD Bakrieland Develoopment 334Verde apartment (2 tower) rasuna Said CBD Far Point 317Menteng Square (3 towers) Proklamasi Central jakarta Bahama Development 1,600Cervino Village (2 towers) Casablanca South jakarta Pakkodian 518Green Palace apartment (6 towers) kalibata South jakarta agung Podomoro Group 3,780One Park residence (3 towers) Gandaria South jakarta Intiland 379residence 8 at Senopati (2 towers) Senopati South jakarta agung Sedayu Group 650Senopati Suites Senopati South jakarta Mahkota asia Graha 103Gading Nias residence (Grand Emerald) Pegangsaan Dua North jakarta agung Podomoro Group 747Green Bay Pluit (Coast View) 4 towers Pluit karang ayu North jakarta agung Podomoro Group 3,200regatta (tower rio De janeiro) Pantai Mutiara North jakarta Intiland 110East Park apartment (tower B) krt radjiman East jakarta Cakra Sarana Persada 550Belmont residence (tower Everest) Meruya Ilir West jakarta Gapura Prima 553Central Park residence (tower adeline) S. Parman West jakarta agung Podomoro Group 350City Garden residence Cengkareng West jakarta agung abadi Group 600Puri Park View (2 towers) Pesanggrahan West jakarta kSO Pt Pelaksana jaya Mulia

& Pt alam jaya Perkasa1,723

Season City (tower C) Grogol West jakarta agung Podomoro Group 714St. Moritz (the ambassador Suite tower) Puri Indah West jakarta Lippo karawaci 140St. Moritz (the Presidential Suite tower) Puri Indah West jakarta Lippo karawaci 124St. Moritz (the royal Suite tower) Puri Indah West jakarta Lippo karawaci 220Westmark apartment S. Parman West jakarta Cowell Development 550

strata-titLe apartment cUmULatiVe sUppLY

Colliers International Indonesia - research

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2005 2006 2007 2008 2009 2010 2011 2012

Un

its

p. 15 | coLLiers internationaL

JAKARTA | 4q 2012 | apartment

Colliers International Indonesia - research

new sUppLY pipeLine

apartment name Location reGion #Unit DeVeLopment statUs

2013ambassade residence (tower a) Puri Denpasar CBD 234 Under ConstructionBelmont residence (tower Montblanc) Meruya Ilir West jakarta 350 Under ConstructionLuxurious raffles residence Satrio CBD 88 Under ConstructiondGreen Pramuka (tower Faggio & tower Pino) jend. a. Yani Central jakarta 2,900 Under ConstructionEast Park apartment (tower a) krt radjiman East jakarta 550 Under ConstructionGP Plaza Gatot Subroto CBD 320 Under ConstructionGreen Central (tower Cerberra) Gajah Mada West jakarta 420 Under ConstructionGreen lake Sunter (2 towers) Sunter North jakarta 2,400 Under ConstructionGreen Palace apartment (tower S) kalibata South jakarta 630 Under ConstructionGreen Palace apartment (tower V) kalibata South jakarta 630 Under Constructionkebagusan City tower B kebagusan South jakarta 548 Under Constructionkemang Village (the Infinity) Pangeran antasari South jakarta 175 Under Constructionkemang Village (the tiffany) Pangeran antasari South jakarta 240 Under ConstructionMyHome apartment Satrio CBD 136 Under ConstructionPakubuwono terrace (tower I) Ciledug South jakarta 750 Under ConstructionPancoran riverside (tanjung kalibata) Pengadegan timur South jakarta 1,900 Under ConstructionPasar Baru Mansion (2 towers) Pasar Baru Central jakarta 520 Under Constructionrusunami Delta Cakung (tower 1) Cakung East jakarta 1,700 Under ConstructionSentra timur residence (Stage 2) Pulogebang East jakarta 1,000 Under ConstructionSt. Moritz (New royal Suite tower) Puri Indah West jakarta 150 Under ConstructionSunter Icon (2 towers) Sunter North jakarta 600 Under Constructionthe East at Essence Dharmawangsa South jakarta 244 Under Constructionthe Grove Suite Hr rasuna Said CBD 151 Under Constructionthe H tower Hr rasuna Said CBD 9 Under Constructionthe residences at Dharmawangsa 2 Dharmawangsa South jakarta 89 Under Constructionthe royal Springhill (tower Magnolia) kemayoran Central jakarta 256 Under Constructionthe royal Springhill (tower Marygold) kemayoran Central jakarta 128 Under Constructionthe Windsor (2 towers) Puri Indah West jakarta 340 Under Constructiontitanium Square Pasar rebo East jakarta 725 Under ConstructionVerde apartment (tower East) Hr rasuna Said CBD 114 Under Construction

2014Botanica apartment (3 towers) Simprug South jakarta 626 Under ConstructionCasa Grande residence (Montana tower) Casablanca CBD 284 Under ConstructionCasa Grande residence (Montreal tower) Casablanca CBD 313 Under ConstructionCasablanca East residence Pahlawan revolusi East jakarta 1,500 Under ConstructionDukuh Golf residence (aurora tower) kemayoran Central jakarta 522 Under ConstructionDukuh Golf residence (Bellavista tower) kemayoran Central jakarta 612 Under ConstructionGading Greenhill Pegangsaan Dua North jakarta 700 Under ConstructionGreen Bay Pluit (Bay View) Pluit karang ayu North jakarta 3,096 Under Constructionkemang Village (the Intercontinental) Pangeran antasari South jakarta 400 Under Constructionkemang Village (the Metropolitan) Pangeran antasari South jakarta 150 Under ConstructionLa City apartment (tower a) Lenteng agung South jakarta 980 Under Construction

continued

p. 16 | coLLiers internationaL

JAKARTA | 4q 2012 | apartment

apartment name Location reGion #Unit DeVeLopment statUs

continuationLa Maison Barito Barito South jakarta 80 Under ConstructionLa Venue - South tower Pasar Minggu South jakarta 341 Under ConstructionMetro Park residence kebon jeruk West jakarta 1,200 Under ConstructionNorthern ancol residence ancol North jakarta 800 Under ConstructionPakubuwono terrace (tower II) Ciledug South jakarta 720 Under ConstructionPluit Seaview (tower Maldives) Pluit North jakarta 940 Under ConstructionSetiabudi Sky Garden (tower 1) Setiabudi CBD 426 Under ConstructionSherwood apartment (3 towers) kelapa Gading North jakarta 320 Under ConstructionSignature Park Grande Mt Haryono East jakarta 1,100 Under ConstructionSky terrace Lagoon kalideres West jakarta 525 Under ConstructionSt. Moritz (the New ambassador Suite tower) Puri Indah West jakarta 200 Under ConstructionSt. Moritz (the New Presidential Suite tower) Puri Indah West jakarta 200 Under ConstructionSt. Moritz (the New royal Suite tower) Puri Indah West jakarta 196 Under ConstructionSudirman Suites Sudirman CBD 380 Under Constructionthe aspen Fatmawati South jakarta 860 Under Constructionthe Bellevue Pondok Indah South jakarta 60 Under Constructionthe Grove Hr rasuna Said CBD 438 Under Constructionthe H residence Mt Haryono East jakarta 383 Under Constructionthe Hive @tamansari DI Panjaitan East jakarta 422 Under Constructionthe Pakubuwono Signature Pakubuwono South jakarta 188 Under ConstructionSenopati Penthouse Senopati South jakarta 63 Under ConstructionCapitol Park apartment Salemba Central jakarta 400 Under PlanningElpis residence Gunung Sahari Central jakarta 791 Under PlanningSt. regis (Previously the Icon) Gatot Subroto CBD 284 Under Planningteluk Intan (tower Saphire) teluk Gong North jakarta 350 Under Planning

p. 17 | coLLiers internationaL

Colliers International Indonesia - research

DistribUtion of apartments sUppLY in 2012 baseD on Location

Colliers International Indonesia - research

JAKARTA | 4q 2012 | apartment

CBD 18.60%

Central jakarta6.98%

South jakarta34.88%

North jakarta13.95%

East jakarta2.33%

West jakarta23.26%

all of 19,706 apartment units during 2012 are provided by 22 apartment projects comprising of 42 new apartment towers. Quite a few of these developments were targeted at the middle class segment offering a price per sq m of between IDr 11 million/sq m and IDr 18 million/sq m . the composition of apartment projects

during 2012 was mainly located at South jakarta area, dominated by middle-low class apartment with price ranging from IDr 7.5 million/sq m to IDr 8.2 million/sq m. Meanwhile, only one apartment project being built in East jakarta and this apartment intends for lower segment of market.

the location of new apartment development has been shifting to the outside of the CBD area for the last five years. as seen in the chart above, since 2007, the number of apartment units in the CBD (including the areas like Sudirman, Mega kuningan, rasuna Said, SCBD, and thamrin) has dwindled. Prior to 2007, the CBD had been flooded by upper-class apartment development due to its proximity to the main business locations and premium shopping malls. as vacant land is becoming scarce in the CBD area, land prices have accordingly jumped significantly over the last two years. therefore, looking at supply composition over the next two years, less and less apartment developments will be built in the CBD.

In South jakarta, apartment development started mushrooming in 2008 with the influx of four apartment projects. In 2010, South jakarta provided around 13% of the total units in jakarta with favourite apartment locations like kemang, terogong and Permata Hijau, dominated by middle- to upper-class apartments. In 2011, the area became more populated with the completion of massive projects like kalibata City and the area will continue to grow into 2015 with a concentration in the Pancoran, kemang and Senopati areas.

coLLiers internationaL | p. 18

JAKARTA | 4q 2012 | apartment

2006 2012

sUppLY apartment in jakarta baseD on area (#Units)

Colliers International Indonesia - research

CBD 28.39%

Central jakarta19.92%

South jakarta10.91%

North jakarta19.07%

East jakarta0.35%

West jakarta21.35%

CBD 19.08%

Central jakarta12.06%South

jakarta17.60%

North jakarta20.89%

East jakarta5.10%

West jakarta25.28%

DistribUtion of apartment baseD on Location DUrinG 2006 - 2014f

Colliers International Indonesia - research

0%

20%

40%

60%

80%

100%

2006 2007 2008 2009 2010 2011 2012 2013F 2014F

CBD Central jakarta South jakarta North jakarta East jakarta West jakarta

the East jakarta area started seeing a robust market in 2009 with the operation of Menara Cawang. Since then, three projects entered the market, particularly within the jalan Mt Haryono – Cawang corridor including Signature Park, Mt Haryono Square and Mt Haryono residence. In 2013, the upcoming projects will mainly be located in the Cakung and Pulo Gebang areas, while in 2014, the Mt Haryono – Cawang corridor will see three middle-class projects such as the H residence, Signature Park Grande and the Hive @ tamansari. Other areas, like Cipinang will have projects lke Casablanca East residence.

apartment development in areas like South jakarta and West jakarta is becoming more active over the last two years with more new projects. In South jakarta, huge projects with

massive units include kalibata residence and Green Palace apartment, while Seasons City, royal Mediterania Garden residence and Central Park apartment have been dominating West jakarta’s apartment supply for the last two years. During 2012, the agung Podomoro Group continues to be the most active development group in building a number of apartment projects like Green Palace apartment, Green Bay Pluit, and Denpasar residence which are scattered around different areas. Intiland Development ranked second with four apartment towers, i.e. three from One Park residences, located in Gandaria, South jakarta and one from regatta (rio de janeiro), located in Pantai Mutiara, North jakarta.

Based on our database, we anticipate further supply growth up to 2014 with an additional 39,147 units scheduled to be on the market. as mentioned earlier, the new apartments will be concentrated in the area outside of the CBD. In East jakarta, growing areas like Mt. Haryono – Cawang corridor will have an additional 7,784 units of strata-title apartments. Since 2010, East jakarta has been consistently growing as an apartment location compared to the other

five municipalities in jakarta. along the Mt. Haryono – Cawang corridor, there are three apartment projects including the H residence, the Hive and Signature Park Grande, which will be targeted at the middle- to upper-class segments while other areas in East jakarta (further east), like Cakung and jatinegara, have rusunami Delta Cakung and East Park apartment which are targeted at the low-class segment.

apartment market in 2013 - 2014

p. 19 | coLLiers internationaL

JAKARTA | 4q 2012 | apartment

most actiVe DeVeLopers DUrinG 2012 (baseD on nUmber of projects)

Colliers International Indonesia - research

agung Podomoro Group38%

Intiland10%

Lippo karawaci7%

Bahama Development7%

Other7%

Bakrieland5%

agung Sedayu Group5%

Pakkodian5%

Farpoint realty5%

agung abadi Group

3%Wika realty

2%

Mahkota asia Graha2% Gapura Prima

2% Cowell Development2%

aVeraGe take-Up comparison Y-o-Y

reGion 4Q 2011 4Q 2012 QoQCBD 86.4% 87.7% 1.2%

South jakarta 75.2% 86.1% 11.1%

Outside CBD 73.9% 79.6% 5.7%

Colliers International Indonesia - research

the jakarta apartment market performed somewhat well in 2012 on the back of solid domestic demand. In line with the growth of supply, the absorption rate of strata-title apartments this year showed an upward trend. Overall, at the end of 2012, take-up rates of strata-title apartments reached 82.2%, increasing by 6% compared to 2011. the take-up rates in 2012 is the best ever in apartment history.

the under-construction apartment projects recorded good sales compared to last quarter, increasing by 3.4%. Based on area, the CBD has the highest absorption rate of 87.7%,

followed by South jakarta and non-CBD (outside of the CBD and South jakarta areas) with 86.1 and 79.6%, respectively. South jakarta showed a significant year-on-year (YoY) increase, representing a rise of 11.2% over last year’s figure. this significant YoY increase was dominated by the pre-sales performance of under-construction apartment projects. Senopati, Permata Hijau, Pakubuwono, Simprug and Gandaria continue to be the most preferable locations in the South jakarta area. Overall, around 67% of the total approximately 39,000 units proposed for completion between 2013 and 2014 have been reported as sold, leaving about 13,000 units available for sale.

Demand

coLLiers internationaL | p. 20

JAKARTA | 4q 2012 | apartment

DistribUtion of fUtUre apartment Units in jakarta UntiL 2014

Colliers International Indonesia - research

CBD 16.63% Central

jakarta12.64%

South jakarta19.28%

North jakarta21.55%

East jakarta8.76%

West jakarta21.14%

among other factors that stimulate apartment buying is a growing economy is the growing middle class who are now thinking of buying an apartment either as a full-time residence, occasional living, leasing or for investment. the growing economy also creates traffic, particularly in the business area. this promotes apartment living in town that reduces time travelling to the work place. On the other hand, the increasing land prices in jakarta, especially in prime areas, also provides the foundation for apartment price appreciation. Meanwhile, the corporate activities remained vigorous for the last two years which potentially leads to the creation of more leasing demand. this will potentially become a pulling factor for investors to buy apartments, especially in premium areas, such as Sudirman, SCBD, Gatot Subroto,

thamrin, rasuna Said and kuningan. Colliers International Indonesia noted a yield for apartments in jakarta ranging from 5 to 9%. the increasing demand for apartments is also fuelled by several promotional programmes offering various incentives such as three years cash instalments without interest, direct prizes and “buyer get buyer” bonuses whereby buyers referring another buyer will get a discounted price. Further ahead, the strata-title apartment market will receive a total 39,147 units during 2013 and 2014. the competition for the next two years seems to be intense, however, with pre-commitment sales so far reaching 67%, the remaining sales work will be a lot easier.

aVeraGe take-Up comparison Q-o-Q of UnDer constrUction apartment projects

reGion 3Q 2012 4Q 2012 QoQCBD 73.6% 77.9% 4.38%

South jakarta 65.7% 76.2% 10.40%

Outside CBD 64.9% 66.2% 1.27%

Colliers International Indonesia - research

coLLiers internationaL | p. 21

saLes rate in 2012 anD pre-commitment saLes rate for sUppLY in 2013 - 2014 perioD

Colliers International Indonesia - research

JAKARTA | 4q 2012 | apartment

11,629

14,497

17,979

20,850

18,297

19,706

0 5,000 10,000 15,000 20,000 25,000

2014

2013

2012

Supply absorbed

Units

the above graph shows pre-sales effort made before the apartment is ready to occupy. thus far, of the total approximately 18,297 apartments which will be completed in 2013, 79.2% have been absorbed. the middle- to upper-class projects such as MyHome apartment, located in the CBD; the residence at Dharmawangsa 2, in South jakarta; Springhill residence and St.Moritz (New royal Suite tower) located in the outside area are some successful projects which will be in operation in 2013. On the other hand, of the available units projected to be in operation in 2014, 56% have been absorbed. Some projects which have good absorption rates are from upper- and middle-to upper–class developments. the upper class projects

such Setiabudi Sky Garden, located in CBD, and Botanica apartment, located in Simprug, South jakarta area, recorded 75 - 78% pre-committed take-up rates, while in the outside the CBD area, Sherwood apartment of a middle- to upper-class project, which is located in kelapa Gading, North jakarta, has reported selling around 85% of the total units. Overall, the South jakarta area saw better sales performance than the CBD and non-CBD areas, increasing by 10.4% compared to the previous quarter. Meanwhile, the CBD still maintains the highest take-up rate, with 78% having been sold.

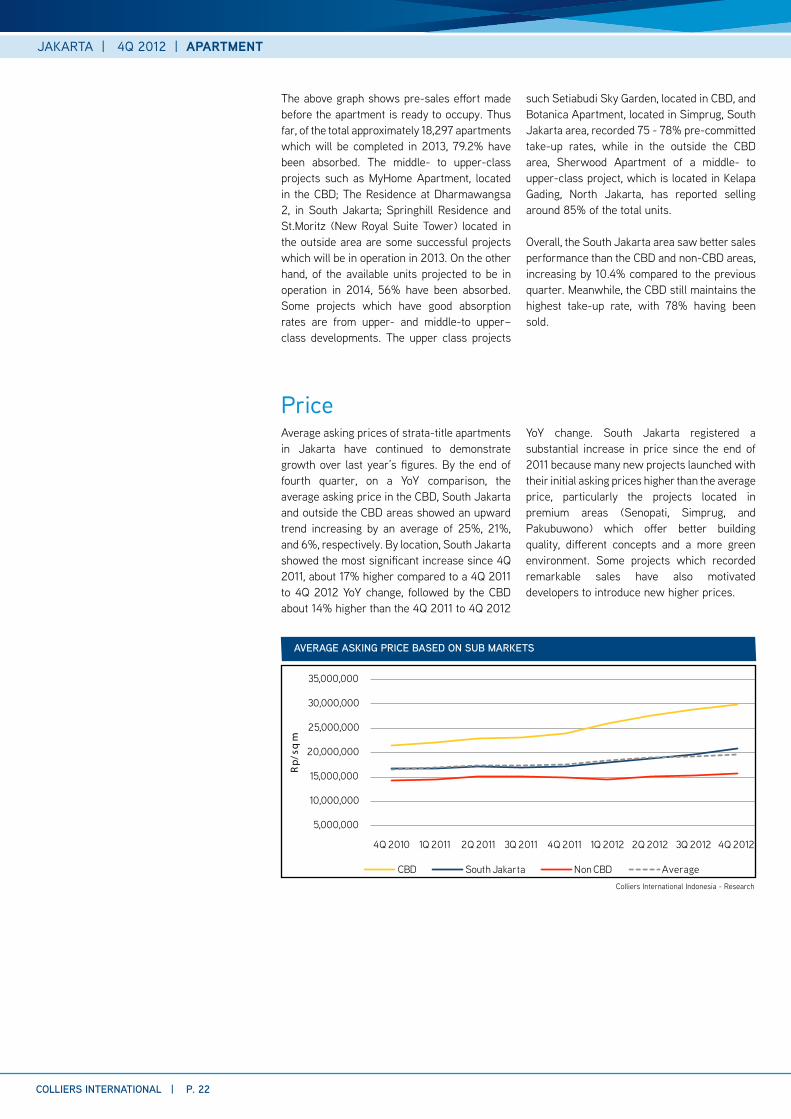

average asking prices of strata-title apartments in jakarta have continued to demonstrate growth over last year’s figures. By the end of fourth quarter, on a YoY comparison, the average asking price in the CBD, South jakarta and outside the CBD areas showed an upward trend increasing by an average of 25%, 21%, and 6%, respectively. By location, South jakarta showed the most significant increase since 4Q 2011, about 17% higher compared to a 4Q 2011 to 4Q 2012 YoY change, followed by the CBD about 14% higher than the 4Q 2011 to 4Q 2012

YoY change. South jakarta registered a substantial increase in price since the end of 2011 because many new projects launched with their initial asking prices higher than the average price, particularly the projects located in premium areas (Senopati, Simprug, and Pakubuwono) which offer better building quality, different concepts and a more green environment. Some projects which recorded remarkable sales have also motivated developers to introduce new higher prices.

Price

coLLiers internationaL | p. 22

aVeraGe askinG price baseD on sUb markets

Colliers International Indonesia - research

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

4Q 2010 1Q 2011 2Q 2011 3Q 2011 4Q 2011 1Q 2012 2Q 2012 3Q 2012 4Q 2012

Rp/

sq m

CBD South jakarta Non CBD average

JAKARTA | 4q 2012 | apartment

Overall, three circumstances have led to the increasing prices. among them are high absorption of strata-title apartments in jakarta; the climbing land values, particularly in the CBD and South jakarta (due to the scarcity of land in those areas); and rising construction costs. In general, the overall price climb during 2012 was mainly due to the influx of new apartments with prices above the average market price and the under-construction apartment projects with high prices. as explained in the demand section above, South jakarta became the most preferable location during 2012 with new projects catering to the upper segment.

the positive perception toward residential property products which led to a continued increase in sales inspired developers to adjust apartment price. among projects in South jakarta that introduced increased asking prices are Pakubuwono Signature, Senopati Suites 2,

kentjana residence, the residence at Dharmawangsa 2, Botanica apartment, Providence Park and 1 Park avenue. On the other front, with a limited number of units available, the CBD managed to maintain the highest average asking price up to the end of 2012. In the outside the CBD area, where quite a few developments offered a massive number of units, leaving many available units, has made the average asking price relatively stable.

Cash instalments is the most common payment method opted for by apartment buyers, after hard cash payment and bank loan (Indonesian term for kredit Pemilikan apartemen or kPa). Cash instalments was chosen because people have cash and for privacy reasons, they do not want to go through convoluted procedures when borrowing using a bank mortgage. Meanwhile, hard cash is preferred by buyers to benefit from big discounts.

aVeraGe askinG price in Different sUb markets

area 4Q 2010 4Q 2011 4Q 2012 2010 Vs 2011 2011 Vs 2012CBD rp 21,443,924 rp 23,828,588 rp 29,817,588 11.12% 25.1%

South jakarta rp 16,556,357 rp 17,189,527 rp 20,717,032 3.82% 20.5%

Outside CBD rp 14,385,630 rp 14,812,173 rp 15,656,812 2.97% 5.7%

average rp 16,479,008 rp 17,493,209 rp 19,572,483 6.15% 11.9%

Colliers International Indonesia - research

coLLiers internationaL | p. 23

preferreD paYment methoD for apartment bUYer

Colliers International Indonesia - research

JAKARTA | 4q 2012 | apartment

kPa (Mortgage)19%

Hard Cash24%

Cash Instalment During Construction

57%

historicaL apartment price bY sUb markets

area 2010 2011 2012 2013fCBD rp 21,443,924 rp 23,828,588 rp 29,817,081 rp 36,362,582

South jakarta rp 16,556,357 rp 17,189,527 rp 20,717,032 rp 25,167,739

Outside CBD rp 14,385,008 rp 14,812,173 rp 15,656,812 rp 16,920,083

average rp 16,479,008 rp 17,493,209 rp 19,572,483 rp 21,725,457

Colliers International Indonesia - research

By our assessment, the average price of apartment units in 2013 will increase by 11%. the most significant increment is anticipated for apartment projects in the CBD followed by South jakarta, due to high demand from end-users and investors, especially since those areas have a very strong expatriate rental market. as for the CBD, we expect to see further growth in apartment prices of around 22% over 2013. the increase will be triggered by projects which are still under construction

and some projects which are approaching their scheduled hand-over dates, such as raffles residence and MyHome apartment form Ciputra World jakarta. Meanwhile, with quite a few projects offering large numbers of units in the outside the CBD area, prices will likely remain relatively stable. However, the overall price in the outside the CBD area will increase moderately with the influx of upper-class apartment projects such as St Moritz and the Windsor in Puri Indah, West jakarta.

coLLiers internationaL | p. 24

aVeraGe apartment price

Colliers International Indonesia - research

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

2010 2011 2012 2013F

Pri

ce/s

q m

JAKARTA | 4q 2012 | apartment

Apartment For Lease (Serviced and Non-serviced)

Only one new development of apartments for lease (non-serviced) in jakarta entered the market during the last quarter of 2012, i.e. apartemen Plaza Senayan (towers C and D) which is the extension of apartemen Plaza Senayan (towers a and B), comprising 217 leased apartment units and offering a range of one-, two-, three-bedroom and penthouse units. With the influx, the cumulative supply of non-serviced apartments is 3,565 units. Overall, the total units of apartment for lease (both serviced and non-serviced) in jakarta was

8,246, of which around 57% are operated as serviced apartments.

Overall, the development of apartments for lease in jakarta has been limited for the past few years. Since 2010, a total of four apartment for lease projects comprising 348 units (non-serviced) were taken out from our database of apartment for lease as they underwent major refurbishment and some of them have been converted to strata-title apartments.

Colliers International Indonesia - research

Supply

List of refUrbisheD apartments for Lease projects (2010 - 2012)

apartment name Location reGion cateGorY #UnitsMenara Budi rasuna Said CBD Non-Serviced 157

ratu Plaza Sudirman CBD Non-Serviced 46

Pasadena Pulomas Pulomas East jakarta Non-Serviced 50

Puri apartment Puri Indah West jakarta Non-Serviced 95

the number of future projects of apartments for lease is quite limited compared to apartments for sale. Only a few potential projects are in the planning stages. Meanwhile, there are three apartment for lease projects in the pipeline which are estimated to enter the rental apartment market in the next two years. ascott kuningan and Fraser residence Menteng are

predicted to open in 2013, while Frasers Suites jakarta, part of the Ciputra World 2 commercial compound, will be open in 2014. Other than the influx of future apartment units, kempinski Serviced apartment is planning to close 40 serviced apartment units, from january to March 2013, due to renovation works.

Colliers International Indonesia - research

List of fUtUre apartments for Lease projects

apartment name Location reGion cateGorY #Unitsascott kuningan Satrio CBD Serviced 186

Fraser residence Menteng Menteng Central jakarta Serviced tBa

Fraser Suites jakarta Satrio CBD Serviced 200

p. 25 | coLLiers internationaL

JAKARTA | 4q 2012 | apartment

apartments for lease commonly target the corporate leasing market, which particularly demand their hospitality services and flexibility in leasing term. In general, occupancy levels of apartments for lease experienced a minor decrease at the end of 2012 to an average of 78.3%, down from the previous quarter at 79.1%. this situation occurred mainly because of the additional supply of 217 units of non-serviced apartments which affected the overall

calculations. In the non-serviced apartment market, the occupancy level dropped quite a bit to 80.6% from the previous 88%, mainly due to the operation of apartment Plaza Senayan mentioned above. Meanwhile, serviced apartments performed well at the end of 2012. Demand for serviced apartments was largely from new expatriates from newly established companies in jakarta and or from expanding companies.

Occupancy

occUpancY for non-serViceD apartment

reGion 3Q 2012 4Q 2012CBD 88.03% 86.65%

South jakarta 79.23% 79.72%

Outside CBD 76.02% 75.96%

Colliers International Indonesia - research

the overall occupancy rate in South jakarta commenced as the highest in both market i.e. non-serviced and serviced apartment. Inquiries during the reviewed quarter were largely from manufacturing companies, followed by contractors and consultant groups from japan. all in all, with the expectation of a rosy economy in 2013, inquires for leased apartments is anticipated to ameliorate along with greater corporate activity and an improving number of

expatriates and business travellers to jakarta. Nevertheless, such a situation would be difficult to be applicable for apartments for lease located in the non-CBD areas since the majority of the developments are old projects and lack the amenities which newer developments offer. On the contrary, demand will be concentrated on selected quality projects, such as serviced apartments managed by international hotel operators and located in preferred areas like the CBD and South jakarta.

occUpancY for serViceD apartment

reGion 3Q 2012 4Q 2012CBD 84.07% 84.55%

South jakarta 83.93% 87.10%

Outside CBD 60.24% 61.36%

Colliers International Indonesia - research

p. 26 | coLLiers internationaL

JAKARTA | 4q 2012 | apartment

Nothing changed during the quarter and the average rental rates of apartments for lease remained stable. However, since the majority of apartments for lease are offered in US dollars while the remainder are offered in local currency, the average rental rates in US dollars dropped somewhat due to the strengthening US dollar against the rupiah during this quarter. this is because all rupiah rates have to be converted to US dollars to get the overall average asking rental rates. Furthermore, the average asking rental rates of apartments for lease (both serviced and non-serviced) have a

depreciation rate of less than 0.1% compared to the previous quarter. all in all, by location, serviced apartments in the CBD maintained average asking rental rates at USD27.52/sq m/month, while the non-CBD area, including South jakarta, stood at USD21.16/sq m/month. For non-serviced apartments, those in the CBD and non-CBD areas including South jakarta have average asking rental rates of USD17.02 and 12.25/sq m/month, respectively.

Rental Rates

rentaL rate/sQ m/month

reGion 3Q 2012 4Q 2012CBD $23.72 $23.70

Outside CBD $14.75 $14.75

Colliers International Indonesia - research

coLLiers internationaL | p. 27

JAKARTA | 4q 2012 | apartment

aVeraGe rentaL rates for serViceD apartment

Colliers International Indonesia - research

aVeraGe rentaL rates for non-serViceD apartment

Colliers International Indonesia - research

$10.00$12.00$14.00$16.00$18.00$20.00$22.00$24.00$26.00

1Q 2009

2Q 2009

3Q 2009

4Q 2009

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

4Q 2012

Ren

tal R

ate/

sq m

/mon

th

CBD Non CBD

$10.00$12.00$14.00$16.00$18.00$20.00$22.00$24.00$26.00

1Q 2009

2Q 2009

3Q 2009

4Q 2009

1Q 2010

2Q 2010

3Q 2010

4Q 2010

1Q 2011

2Q 2011

3Q 2011

4Q 2011

1Q 2012

2Q 2012

3Q 2012

4Q 2012

Ren

tal R

ate/

sq m

/mon

th

CBD Non CBD

However, over the next year, quite a few serviced apartments, particularly those located in the CBD and operated by international hotel operators, are planning to increase asking rental rates. Optimistic about their high demand, they confidently raised their asking prices by 8 - 10% per unit, or USD50 - 500. On the other hand, several apartments for lease in South

jakarta increased their asking rental rates dominated by upgrades to the indoor and outdoor facilities and room furnishings, such as sofa, television and bed. Meanwhile, most landlords of older developments chose to maintain their current rates and were reluctant to increase them for fear that they could lose their current tenants.

On the back of a growing economic performance, the apartment market foresees a promising outlook in 2013. the apartment market was very much fuelled by the vigorous domestic market where such property products are perceived to have better returns than other banking products. On the other hand, supply will be adequate in the future, providing a liberty for buyers to opt for different kinds of developments. Despite there being a substantial number of units in the next two years, the market should be in a healthy situation because pre-commitment levels at upcoming developments are quite high. Furthermore, the increasing middle-class urban population will help maintain the apartment market at least at the current level. Besides jakarta, buyers are potentially coming from wealthy people in other cities in Indonesia like Medan, Surabaya, kalimantan and Makassar.

In the leasing market, demand will still be underpinned by requested from corporations, in particular large-scale overseas companies. the challenge remains for existing apartment for lease projects (both serviced and non-serviced) in jakarta that such developments are getting older, there is limited stock and most of them are lacking amenities that are offered by newer strata-title developments. thus, in the leasing market, apartments for lease directly compete with strata-title apartments offered for lease. this opportunity has been grabbed by developers to build strata-title apartments which meet expatriate standards like building specifications, large units, advanced security systems and more facilities.

Outlook

p. 28 | coLLiers internationaL

JAKARTA | 4q 2012 | apartment

residential expatriate housing sector

Expatriate Housing

With strong underlying fundamentals and business confidence in Indonesia in line with the growing national economy, the number of multinational companies operating in this country is increasing. this is generally marked by an increasing number of expatriates hired by those companies mainly from western and asian countries. It has been a common pattern in the expatriate housing market that sales activity slows down in the last three months of the year, particularly because expatriates shift their focus to the year-end long vacation. Nevertheless, home searching activities were surprisingly quite solid in terms of numbers during that period of time. Some expats were actively searching for landed houses and apartments as preparation for starting work in january – March 2013. Generally, the expats have to secure their home before they get a work permit.

rental rates of selected expatriate-standard houses and apartments showed an upward trend during second semester (2H) of 2012. rentals were up mainly due to strong and abundant inquiries for expatriate living accommodation but on the other hand the number of such properties is becoming limited, in particular those that meet expat standards like size, location, quality, furniture and facilities available in one house. Such conditions have led to landlord markets where home owners have a strong bargaining position. Searching for a quality home that meets a required budget

is very challenging, particularly in high-demand locations like Pondok Indah, kebayoran Baru (certain areas which are close to the CBD) and kuningan. these areas are favourite locations for top management executives with budgets higher than US$4,500/month. For a big house within those areas, the rental per month could reach as high as US$15,000/unit/house. Meanwhile those with budgets ranging from US$3,500 to US$5,000/month have the option of locations like kemang, Cipete, Cilandak or even Pejaten. During our review in the last six months of 2012, the rental tariff generally climbed in the range of US$500 to the highest of US$3,000/unit house/month.

Menteng would be an interesting option for embassy-related expatriates as it provides proximity to the business area; however the stock of good quality houses is limited and hard to find. However, most expatriates working in jakarta would opt for South jakarta because it is within the catchment of many international schools, international clubs, international hospital, entertainment centres, shopping spots, offices and other points of interest for expatriates. Having proximity to an international school is one of the utmost considerations when choosing home locations for expatriates with a family.

the table below gives a brief description of average land price for residential use in some preferred expatriate locations:

aVeraGe LanD prices in seVeraL resiDentiaL Locations

LocationsaVeraGe LanD price/sQ m

in iDr in Us$ (eQUiVaLent)kuningan 21.4 million 2,490

kebayoran Baru 19.3 million 2,240

Menteng 19.1 million 2,220

Pondok Indah 17.6 million 2,050

Permata Hijau 15.7 million 1,830

kemang 8.4 million 980

Cipete 7.4 million 860

Pejaten 7.3 million 850

Cilandak 6.5 million 760

Colliers International Indonesia - residential tenant representation Services

Supply and Rental Rates

coLLiers internationaL | p. 29

JAKARTA | 4q 2012 | residential expat housing

eXpatriate hoUsinG rentaL rates

Locations size (sQ m) rentaL rates (in Us$/Unit)kuningan

4 - 5 Bedroom House 500 - 900 3,500 - 11,500

kebayoran Baru 4 - 5 Bedroom House 600 - 1,500 4,500 - 15,000

3 - 4 Bedroom townhouse/complex 250 - 700 3,500 - 8,000

menteng 4 - 5 Bedroom House 500 - 1,200 4,000 - 15,000

pondok indah 4 - 5 Bedroom House 550 - 1,000 4,500 - 15,000

permata hijau, simpruk 4 - 5 Bedroom House 400 - 1,500 3,500 - 12,000

3 - 4 Bedroom townhouse/complex 220 - 240 2,750 - 4,500

kemang 4 Bedroom townhouse/complex 400 - 700 3,500 - 5,500

3 Bedroom House 400 - 750 3,000 - 5,000

4 - 5 Bedroom House 550 - 1,000 3,500 - 7,000

Cipete 3 Bedroom townhouse/complex 200 - 300 2,500 - 3,500

4 Bedroom townhouse/complex 400 - 700 3,500 - 6,000

3 Bedroom House 300 - 500 2,500 - 3,500

4 - 5 Bedroom House 400 - 800 3,500 - 7,000

pejaten 3 Bedroom townhouse/complex 400 - 600 3,500 - 7,000

4 Bedroom House 500 - 900 3,000 - 7,000

Cilandak 4 Bedroom townhouse/complex 300 - 700 3,500 - 6,500

3 + 1 Bedroom House 300 - 600 3,000 - 5,500

4 - 5 Bedroom House 450 - 750 3,500 - 7,000

On the demand side, there were no changes in the types of industries that were looking for expatriate-standard housing. Several lines of businesses such as oil and gas, consultancy (finance and management consultants), and contractors (mostly from japan) were actively

looking during the second half of 2012.

In term of area preferences, locations adja¬cent to international schools are most attractive for expatriates with family and thus residential areas like Pondok Indah are in high demand.

Demand

Colliers International Indonesia - residential tenant representation Services

p. 30 | coLLiers internationaL

JAKARTA | 4q 2012 | residential expat housing

ApartmentsDuring the second half of 2012, the average rental tariff for selected expatriate apartments experienced minor increases. Overall, rental tariffs are relatively flat for some periods, except for high-demand apartments like Pakubuwono residence, Pakubuwono View and Dharmawangsa residence which introduced an increase of US$250 – US$750/month/unit.

Demand for selected apartments for expatriates is in line with demand for landed houses as some new companies established their presence in jakarta. Meanwhile, some existing multinational companies have also expanded,