jahangir aziz - icrier

TRANSCRIPT

M U M B A I

INDIA: Growth risk and policy spaceINDIA: Growth risk and policy space

ST

RI

CT

LY

PR

IV

AT

EA

ND

CO

NF

ID

EN

TI

AL

Jahangir Aziz

(91) 22-6719-8033 [email protected]

Gunjan Gulati

(91) 22-6639-3125 [email protected]

Vikas Agarwal

(91) 22-6639-2961 [email protected]

Agenda

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Growth risks

How the adjustment might look

Why India got hit

Global Recession

39

Policy space

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Recession goes global

Global Real GDPGlobal Real GDP

12

2008 2009 2010 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09

United States 1.3 -1.8 2.5 -0.5 -3.8 -5.5 -0.5 1.5 2.5

Japan -0.4 -5.7 2.2 -1.8 -9.0 -12.0 -2.5 -1.0 2.0

Euro area 0.8 -2.2 0.8 -0.7 -5.0 -4.0 -1.0 0.0 1.0

United Kingdom 0.7 -2.9 1.0 -2.6 -5.9 -5.0 -1.5 0.0 1.0

Asia ex. Japan 6.0 3.4 6.6 3.6 -4.6 1.3 6.7 8.6 9.0

China 9.0 7.2 8.5 5.5 1.5 5.1 10.0 11.7 12.6

India 6.2 5.5 7.7 8.7 0.3 0.1 4.8 8.9 10.9

Latin America 4.1 -0.4 3.2 4.2 -4.7 -3.2 -0.3 2.7 3.1

Emerging Europe 4.6 -1.1 2.2 5.0 -4.7 -4.1 -1.7 0.1 1.1

Global 1.7 -1.7 2.4 0.1 -4.9 -4.8 -0.1 1.6 2.7

Developed markets 0.8 -2.6 1.8 -0.8 -5.0 -5.9 -1.1 0.5 1.8

Emerging markets 5.2 1.6 4.9 3.9 -4.5 -0.6 3.6 5.8 6.3

Source: JP Morgan Datawatch January 31, 2009

% over year ago % over previous period , saar

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Global downturn deep but short-lived; at least for now!

Real GDP growth Developed and Emerging MarketsReal GDP growth Developed and Emerging Markets

Source: J.P. Morgan economics. Chart shows real GDP growth QoQ saar. Shaded area forecasts.

22

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

-10

-5

0

5

10

15

% q/q, saar

00 02 04 06 08 10

Emerging markets

Developed markets

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

FROM LONDON TO MUMBAIFROM LONDON TO MUMBAI

Why India got hit?

14

TED Spread and India Call Money Rate

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1-Jan-08

15-Jan-08

29-Jan-08

12-Feb-08

26-Feb-08

11-Mar-08

25-Mar-08

8-Apr-08

22-Apr-08

6-May-08

20-May-08

3-Jun-08

17-Jun-08

1-Jul-08

15-Jul-08

29-Jul-08

12-Aug-08

26-Aug-08

9-Sep-08

23-Sep-08

7-Oct-08

21-Oct-08

4-Nov-08

18-Nov-08

2-Dec-08

0

2

4

6

8

10

12

14

16

18

20

TED (LHS)

Call money (RHS)

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Sudden stop in external financing: part coincidental, part structural

Dependence of corporates and banks on external funds

Dependence of non-bank financials (NBFCs) and mutual funds (MFs) on domestic money market and corporate investments

Dependence of SMEs, real-estate, and consumers on NBFCs and MFs

Segmented domestic financial market—regarded as a buffer to shocks—became a key vulnerability, exacerbating price volatility

2468

10121416

2000 2001 2002 2003 2004 2005 2006 2007 2008

% of GDP

Corporates' domestic investment and saving

Investment

Saving

-10

-5

0

5

10

15

Con Gov Inv NetX

India

China

India's investment led growth(Change between 2002-07)

% of GDP

02468

10

2000 2001 2002 2003 2004 2005 2006 2007 2008

% of GDPCorporates' demand for external financing

Investment india

Investment abroad

Foreign fund inflows

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Decoupling anyone? external openness has increased sharply

20253035404550

2000 2001 2002 2003 2004 2005 2006 2007 2008

% of GDPIndia's trade openess has doubled since the early 2000s

Export + Imports

10203040506070

2000 2001 2002 2003 2004 2005 2006 2007 2008

% of GDPIndia's capital account openess has quadrupled since the early 2000s

Inflows + Outflows

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

-5

0

5

10

15

%q/q, saar

00 02 04 06 08

Growth has been increasingly correlated to global conditions

IndiaPartner country wtg avg growth

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

How the adjustment might look: a V-shaped recovery still likely …

GDP: expenditure-side details%y/y, fiscal year beginning April 1

Private cons

Government spending Investment Exports Imports GDP Inflation

2001-02 6.1 2.3 -2.9 5.7 3.4 5.2 3.62002-03 2.7 -0.4 17.0 21.8 10.4 3.8 3.42003-04 5.8 2.6 19.9 5.8 16.8 8.4 5.52004-05 5.2 2.6 19.5 28.1 16.0 8.3 6.52005-06 8.7 5.4 19.4 14.8 45.6 9.2 4.42006-07 7.1 6.2 10.9 18.9 24.5 9.7 5.42007-08 8.3 7.0 13.7 7.5 7.7 9.0 4.62008-09f 5.6 9.1 7.1 8.5 12.1 6.2 8.62009-10f 4.9 9.4 4.8 3.7 3.4 5.5 0.72010-11f 6.5 9.0 14.0 15.0 19.0 7.7 3.1

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

-6-5-4-3-2-101

% point change from T-3

Non-farm GDP growth

T 3 T 2 T 1 T T 1 T 2 T 3

Average of past downturns

Projected current

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

… on investment dynamics

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

-4-3

-2-10

12

% point change from T-3

Private consumption growth

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current downtrun

-8-6

-4-20

24

% point change from T-3

Government consumption growth

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current downtrun

-20-16-12-8-404

-8-6

-4-20

24

% point change from T-3

Investment growth

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current (RHS)

-16

-12

-8

-4

0

4

% point change from T-3

Export growth

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current

-24-20-16-12-8-4048

% point change from T-3

Import growth

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current

-3

-2

-1

0

1

2

% point change from T-3

Current account balance-to-GDP

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Inflation to fall and stay low

0

5

10

15

20

25

Jan 07 Apr 07 Jul 07 Oct 07 Jan 08 Apr 08 Jul 08 Oct 08

%oy a

Manufacturing inflation yet to price in supply-side disinflation

Manufacturing

Raw material

Headline

Energy

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

-6-4-202468

% point change from T-3

Inflation

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Q4 BOP carnage unlikely to be repeated; CA to take over INR dynamics

-20

-10

0

10

20

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

US$ billion

Capital inflows excluding trade balance, FDI, FII portfolio, and ECB

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

-12-10

-8-6-4-20246

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Capital account

Current account

% of GDP

Change in balance of payments

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Credit growth to slow appreciably

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

27

28

29

30

31

32

Jan 08 Apr 08 Jul 08 Oct 08 Jan 09

70717273747576

as % of DepositsCredit has slowed compared to deposit growth

Credit

G-sec holdings

-14

-10

-6

-2

2

6

% point change from T-3

Real non-food credit growth

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Projected current

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

GOI yields to fall; corporate bond could be a pleasant surprise

456789

10

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

% 10-year GOI bond yield

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

012345678

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

% difference from GOI bond y ield Long term corporate bond yields have softened

1-Y commercial paper

5-Y corporate bond

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Growth risks: protracted global recession

02468

101214

99Q1 00Q1 01Q1 02Q1 03Q1 04Q1 05Q1 06Q1 07Q1 08Q1 09Q1

%oy a

GDP and industrial production

IP

GDP

-10-505

10152025

%oy a

Transportation indicators confirm the slowdown

2006 2007 2008

Port traffic

Railway freight

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

0

5

10

15

20

3-month av erage grow th

As do demand indicators

00 02 04 06 08

Real cash balance

IP Consumer goods

-10

0

10

20

30

40

3m av erage grow th

00 02 04 06 08

IP Capital goods

Real non-food credit demand

And bank credit growth

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

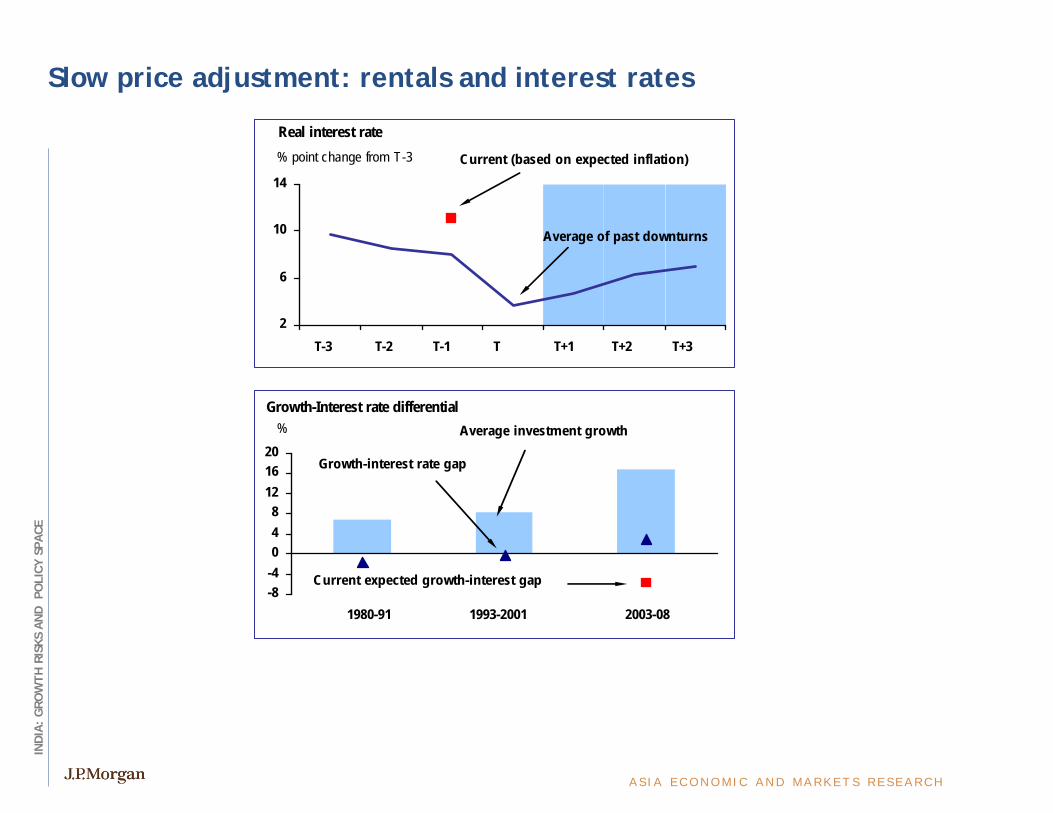

Slow price adjustment: rentals and interest rates

2

6

10

14

% point change from T-3

Real interest rate

T-3 T-2 T-1 T T+1 T+2 T+3

Average of past downturns

Current (based on expected inflation)

-8-4048

121620

% Growth-Interest rate differential

1980-91 1993-2001 2003-08

Growth-interest rate gap

Average investment growth

Current expected growth-interest gap

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

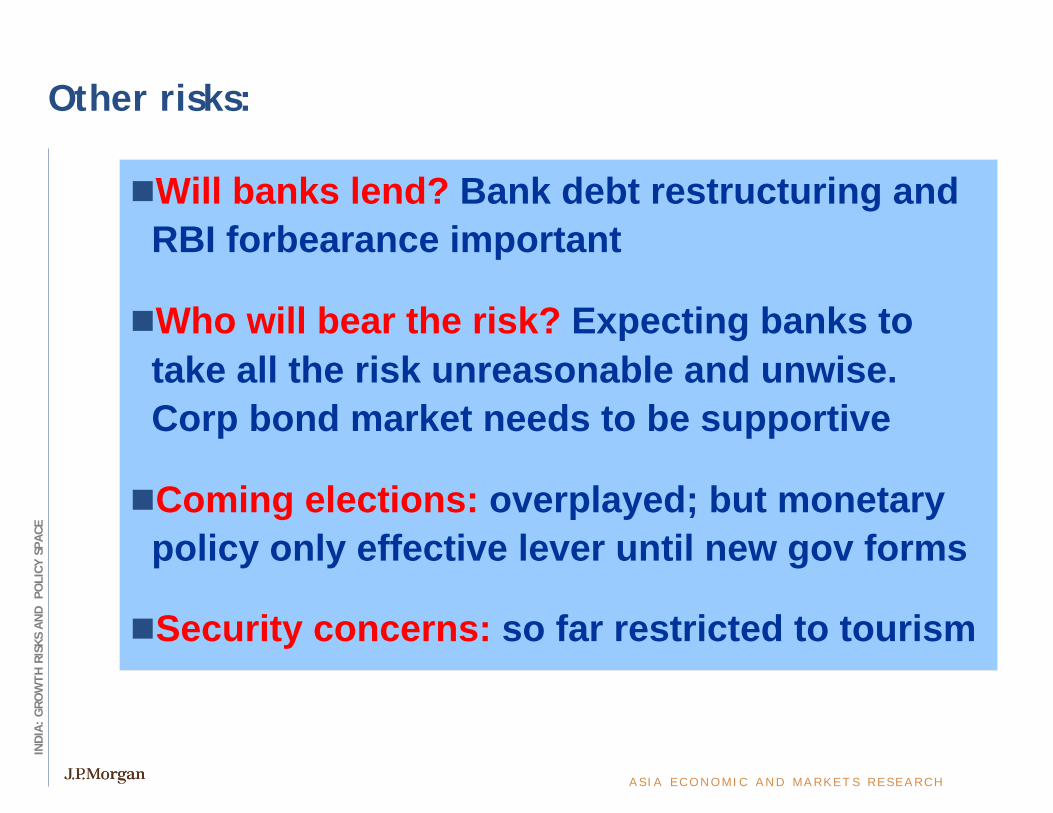

Other risks:

Will banks lend? Bank debt restructuring and RBI forbearance important

Who will bear the risk? Expecting banks to take all the risk unreasonable and unwise. Corp bond market needs to be supportive

Coming elections: overplayed; but monetary policy only effective lever until new gov forms

Security concerns: so far restricted to tourism

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

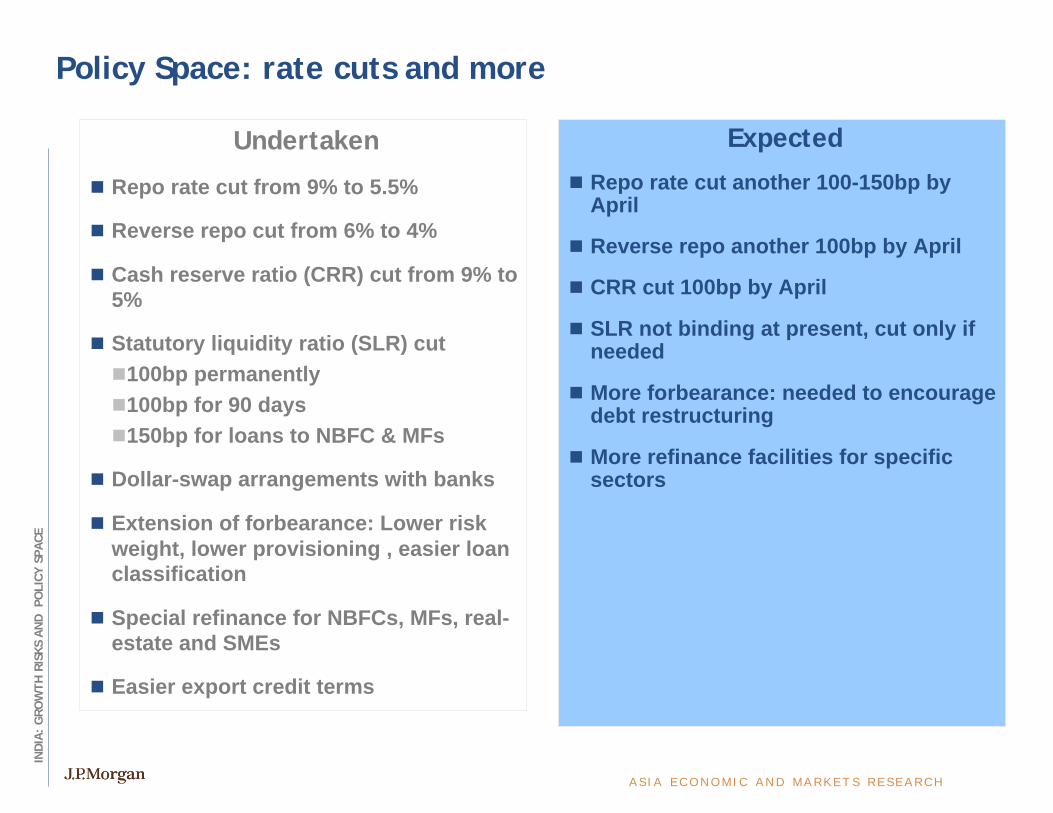

Policy Space: rate cuts and more

Undertaken

Repo rate cut from 9% to 5.5%

Reverse repo cut from 6% to 4%

Cash reserve ratio (CRR) cut from 9% to 5%

Statutory liquidity ratio (SLR) cut100bp permanently100bp for 90 days150bp for loans to NBFC & MFs

Dollar-swap arrangements with banks

Extension of forbearance: Lower risk weight, lower provisioning , easier loan classification

Special refinance for NBFCs, MFs, real-estate and SMEs

Easier export credit terms

Expected

Repo rate cut another 100-150bp by April

Reverse repo another 100bp by April

CRR cut 100bp by April

SLR not binding at present, cut only if needed

More forbearance: needed to encourage debt restructuring

More refinance facilities for specific sectors

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Monetary policy transmission weak but still effective

2

6

10

14

18

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Policy CorridorCall Rate

In percentMoney market and policy rates

-8

-4

0

4

8

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Tight liquidityEasy liquidityIn Rs trillion

RBI's Discount Window Operations

95

100

105

110

0

4

8

12

16

April 02=100

Monetary conditions and industrial growth%saar

2002 2003 2004 2005 2006 2007 2008

3-M lagged Monetary indexdowntrun

3-M avg industrial growth

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Fiscal policy: more space than meets the eye

Undertaken

October: 3.3% of GDP1.9% of GDP in cash1.4% of GDP in bonds

December: 0.5-0.7% of GDPExpenditure 0.4% of GDPTax cuts of 0.15% of GDPSupport for export, textile, housing, SMECuts in retail gasoline price

January: 1.5-1.8% of GDP (budget + other)Infrastructure refinancing Rs 400bn SPV for NBFCs worth Rs 250bnState borrowing Rs 300bn

Central government deficit could rise to 6.5% of GDP from 3.7% of GDP last year

Borrowing in Q1 09 Rs1.1tn (3% of deposit)

Window for more support closed for FY09

Expected

FY10 budget deficit 6.2-6.5% of GDP

Less oil and fertilizer subsidy opens up 1.5-2% of GDP space

Debt high (82% of GDP by FY09), but so are assets; divesting when cash strapped typically weakens political opposition

Lower GOI interest rates will help stabilize debt dynamics

Fears of crowding out overplayed in H1 FY10, concern in H2 FY10

FRBM-II likely in FY10

Consolidation not before FY11

Divestment important to balance stimulus with sustainable debt

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

Capital controls: time for regime change

Undertaken

Cap on ECB interest removed but approval still needed

ECB extended to NBFCs to refinance infra loans

Cap on NRI deposit raised

FII limit on corporate bond raised to $15bn from $6bn

Expected

Gradual removal of NRI deposit cap

Gradual removal of FII limit in corporate bonds

Some increase in FII limit in GOI bonds (likely with SLR reduction)

Gradual removal of sector restrictions for VC and PE

Move towards QFI from FII regime

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE

A S I A E C O N O M I C A N D M A R K E T S R E S E A R C H

[This presentation was prepared exclusively for the benefit and internal use of the JPMorgan client to whom it is directly addressed and delivered (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating, on a preliminary basis, the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by JPMorgan. Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of JPMorgan.

The information in this presentation is based upon any management forecasts supplied to us and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. JPMorgan’s opinions and estimates constitute JPMorgan’s judgment and should be regarded as indicative, preliminary andfor illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. In addition, our analyses are not and do not purport to be appraisals of the assets, stock, or business of the Company or any other entity. JPMorgan makes no representations as to the actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other effects.

Notwithstanding anything herein to the contrary, the Company and each of its employees, representatives or other agents may disclose to any and all persons, without limitation of any kind, the U.S. federal and state income tax treatment and the U.S. federal and state income tax structure of the transactions contemplated hereby and all materials of any kind (including opinions or other tax analyses) that are provided to the Company relating to such tax treatment and tax structure insofar as such treatment and/or structure relates to a U.S. federal or state income tax strategy provided to the Company by JPMorgan.

JPMorgan’s policies prohibit employees from offering, directly or indirectly, a favorable research rating or specific price target, or offering to change a rating or price target, to a subject company as consideration or inducement for the receipt of business or for compensation. JPMorgan also prohibits its research analysts from being compensated for involvement in investment banking transactions except to the extent that such participation is intended to benefit investors.

IRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

JPMorgan is a marketing name for investment banking businesses of JPMorgan Chase & Co. and its subsidiaries worldwide. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by a combination of J.P. Morgan Securities Inc., J.P. Morgan plc, J.P. Morgan Securities Ltd. and the appropriately licensed subsidiaries of JPMorgan Chase & Co. in Asia-Pacific, and lending, derivatives and other commercial banking activities are performed by JPMorgan Chase Bank, N.A. JPMorgan deal team members may be employees of any of the foregoing entities.

This presentation does not constitute a commitment by any JPMorgan entity to underwrite, subscribe for or place any securities or to extend or arrange credit or to provide any other services.

eneral

IND

IA:

GRO

WTH

RIS

KS A

ND

PO

LICY

SPA

CE