j. k. dietrich - fbe 432 – fall, 2002 overview of finance week 1 – august 26 and 28, 2002

TRANSCRIPT

J. K. Dietrich - FBE 432 – Fall, 2002

Overview of Finance

Week 1 – August 26 and 28, 2002

J. K. Dietrich - FBE 432 – Fall, 2002

Financial Analysis, Functions, and Careers

August 28, 2002

J. K. Dietrich - FBE 432 – Fall, 2002

FBE 432 Objectives

Analyze and communicate implications of financial theory using cases

Understand finance careers and functions Refine and expand specific financial

analytical skills Responsibility for learning is with you Requirements are clear: review, prepare, and

participate

J. K. Dietrich - FBE 432 – Fall, 2002

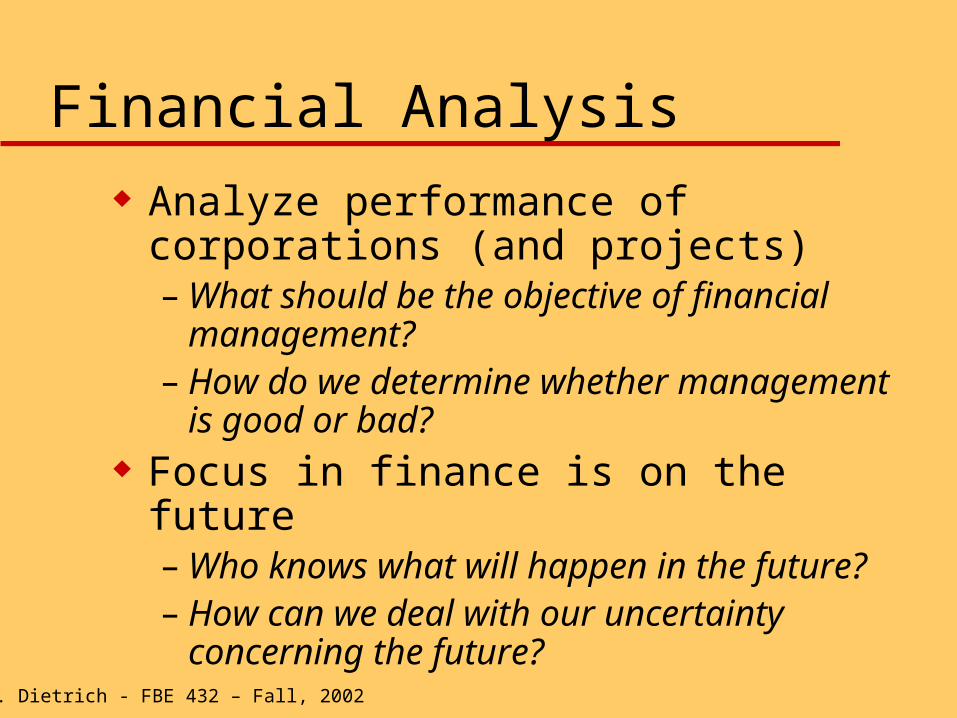

Financial Analysis

Analyze performance of corporations (and projects) – What should be the objective of financial

management?– How do we determine whether management is

good or bad? Focus in finance is on the future

– Who knows what will happen in the future?– How can we deal with our uncertainty

concerning the future?

J. K. Dietrich - FBE 432 – Fall, 2002

Financial Functions

All finance is concerned with value Corporate decision-making

– Investments, including mergers and acquisitions and divestitures (disinvestment)

– Growth and financing needs – Management of working capital

Chief financial officer is responsible for these decisions– Requires project analysts, treasury assistants

J. K. Dietrich - FBE 432 – Fall, 2002

Investment Banking

Investment bankers assist corporations in their dealings with financial markets– Issuing securities

» Initial public offerings (IPOs) or secondary offerings

» Issuing debt or preferred stock to private investors (private placements) or to public markets

– Mergers and acquisitions– Advising and valuing firms

This services are corporate finance or investment banking services

J. K. Dietrich - FBE 432 – Fall, 2002

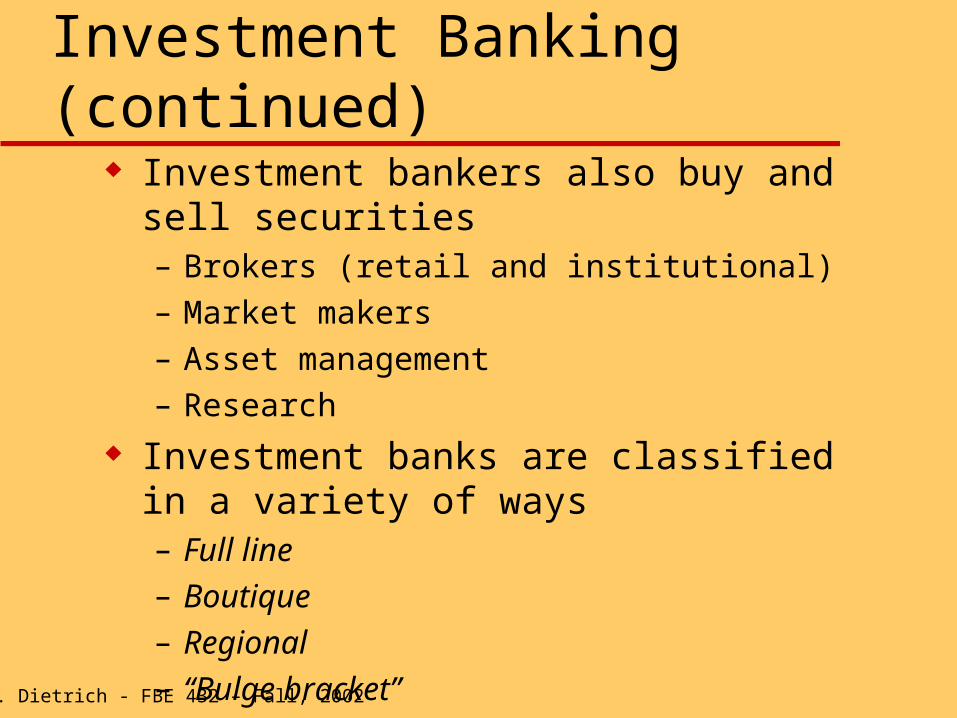

Investment Banking (continued) Investment bankers also buy and sell securities

– Brokers (retail and institutional)

– Market makers

– Asset management

– Research

Investment banks are classified in a variety of ways– Full line

– Boutique

– Regional

– “Bulge bracket”

J. K. Dietrich - FBE 432 – Fall, 2002

Investment Banking (continued)

Investment bankers need many types of financial skills – Analysts for research– Analytical support in doing deals– Traders – Marketing securities to retail and institutional

markets Investment banks hire junior analysts and

associates at entry level

J. K. Dietrich - FBE 432 – Fall, 2002

Investment Banking and Markets

Investment bankers assist corporations (and governments) in designing securities for sale to public or private markets

Employees of investment banks are usually called are said to work on the sell side of a securities firm, or are called sell side analysts or sell side traders or brokers

J. K. Dietrich - FBE 432 – Fall, 2002

Investors

Individuals and institutions invest savings in securities (and other investments)

Individuals are usually divided into the retail market (small investors) and affluent investors (private banking)

Buying and selling securities in the retail market Advising and investing for individuals is financial

advising and asset management Individuals often invest in mutual funds and save

in pension plans

J. K. Dietrich - FBE 432 – Fall, 2002

Institutional Investors

Pension funds, mutual funds, insurance companies, and specialized investment vehicles for wealthy investors (e.g. hedge funds) are called institutional investors

Institutional investors require analysts and portfolio managers to invest funds

Employees of institutional investors are usually said to be on the buy side, as for example a buy-side analyst or a buy-side trader

J. K. Dietrich - FBE 432 – Fall, 2002

Specialized Investment Vehicles

Venture-capital firms provide financing to new firms, often firms in new technologies, requiring both technical and financial skills

Hedge funds are unregistered investment vehicles for wealthy investors’ or institutional funds, often using complex investment strategies requiring sophisticated financial analytical skills

J. K. Dietrich - FBE 432 – Fall, 2002

Developments in Finance

Financial theory has developed to value financial instruments like options and swaps

Technology has developed to enable accounting and trading for complex financial claims like collateralized mortgage obligations (CMOs)

Trading and valuing these instruments and advising corporations on how to use them to manage risk demands highly developed research departments

J. K. Dietrich - FBE 432 – Fall, 2002

Commercial Banking

Commercial banks make loans to corporations and individuals

Corporate commercial bankers provide a variety of services to corporations, including cash management and lending

Banks require financially trained individuals to call on corporations and analyze corporate customers

J. K. Dietrich - FBE 432 – Fall, 2002

Finance Career Paths Many individuals move between financial

functions in corporations and investment banking, asset management, commercial banking, and financial advising over the course of their careers

Research, marketing (selling), deal-making, and advising require varying levels of interpersonal skills

Risk tolerance and energy requirements vary in different finance career paths

J. K. Dietrich - FBE 432 – Fall, 2002

Next Time – August 28

Review valuation approaches Read for practice, The Union Carbide Deal

(Abridged)– Outline issues at issue in the case– What role do investment bankers play?– How are they compensated?

J. K. Dietrich - FBE 432 – Fall, 2002

Introduction to Valuation and Review

August 28, 2002

J. K. Dietrich - FBE 432 – Fall, 2002

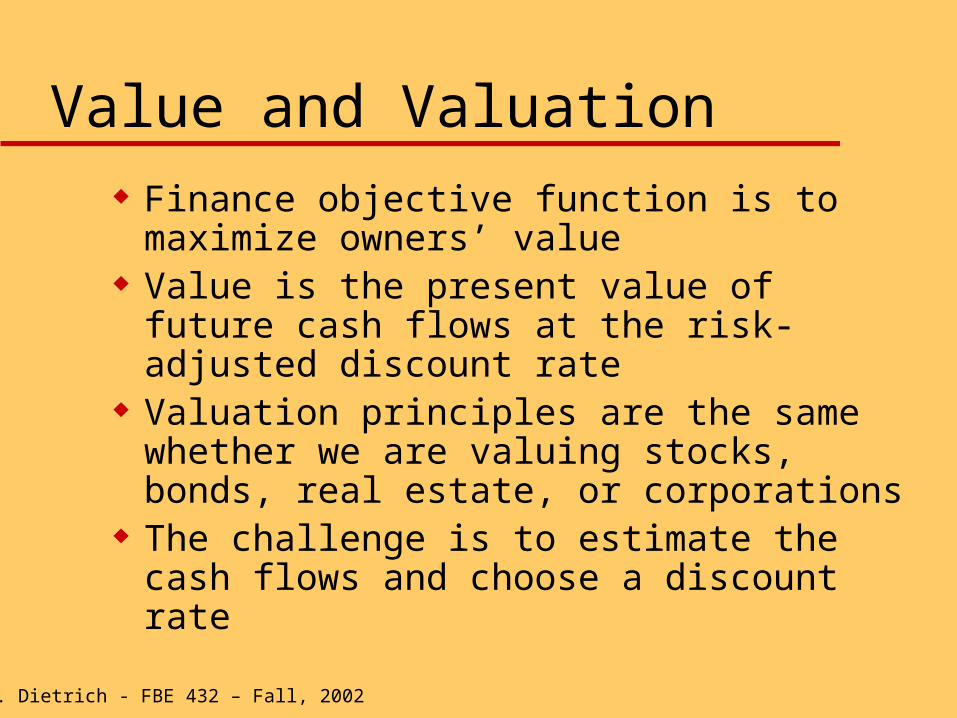

Value and Valuation

Finance objective function is to maximize owners’ value

Value is the present value of future cash flows at the risk-adjusted discount rate

Valuation principles are the same whether we are valuing stocks, bonds, real estate, or corporations

The challenge is to estimate the cash flows and choose a discount rate

J. K. Dietrich - FBE 432 – Fall, 2002

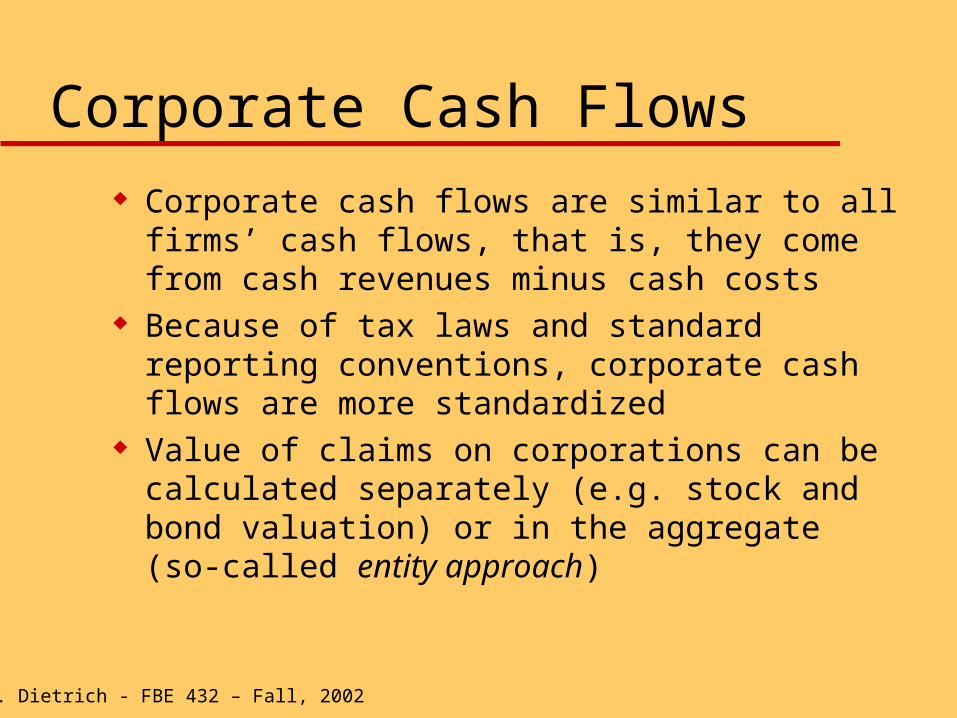

Corporate Cash Flows

Corporate cash flows are similar to all firms’ cash flows, that is, they come from cash revenues minus cash costs

Because of tax laws and standard reporting conventions, corporate cash flows are more standardized

Value of claims on corporations can be calculated separately (e.g. stock and bond valuation) or in the aggregate (so-called entity approach)

J. K. Dietrich - FBE 432 – Fall, 2002

Future Corporate Cash Flows

Since value comes from future cash flows and the future is unknown, future cash flows must be estimated

The future is usually divided into two or more parts– Forecast period and continuing value period– Rapid growth period and normal growth period

Choice of division depends on case and data available

J. K. Dietrich - FBE 432 – Fall, 2002

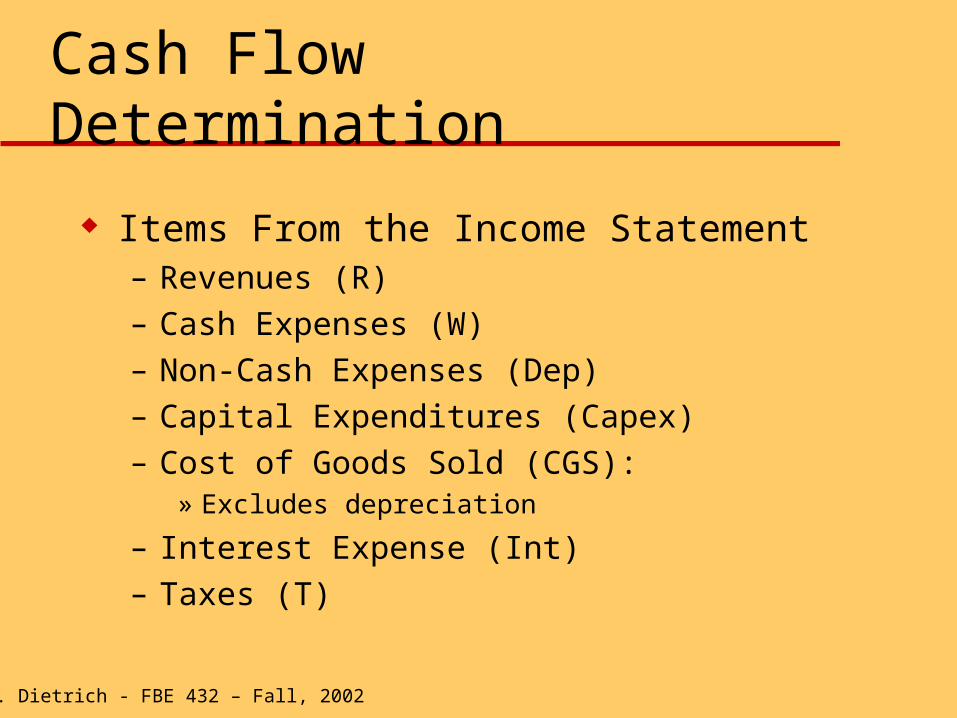

Cash Flow Determination

Items From the Income Statement – Revenues (R)

– Cash Expenses (W)

– Non-Cash Expenses (Dep)

– Capital Expenditures (Capex)

– Cost of Goods Sold (CGS): » Excludes depreciation

– Interest Expense (Int)

– Taxes (T)

J. K. Dietrich - FBE 432 – Fall, 2002

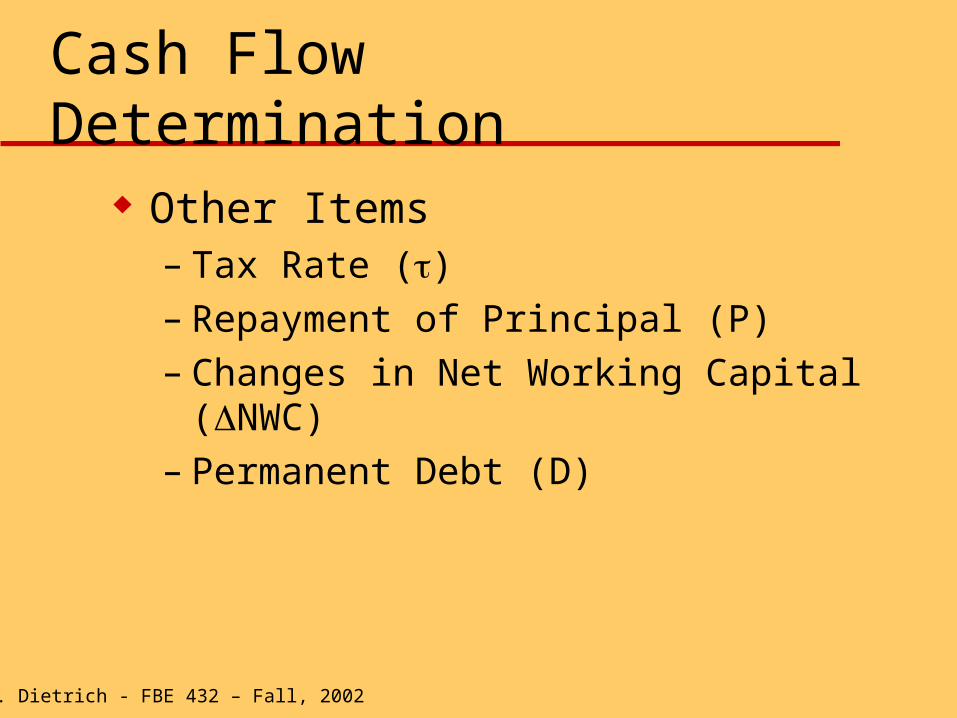

Cash Flow Determination

Other Items – Tax Rate ()– Repayment of Principal (P)– Changes in Net Working Capital (NWC)– Permanent Debt (D)

J. K. Dietrich - FBE 432 – Fall, 2002

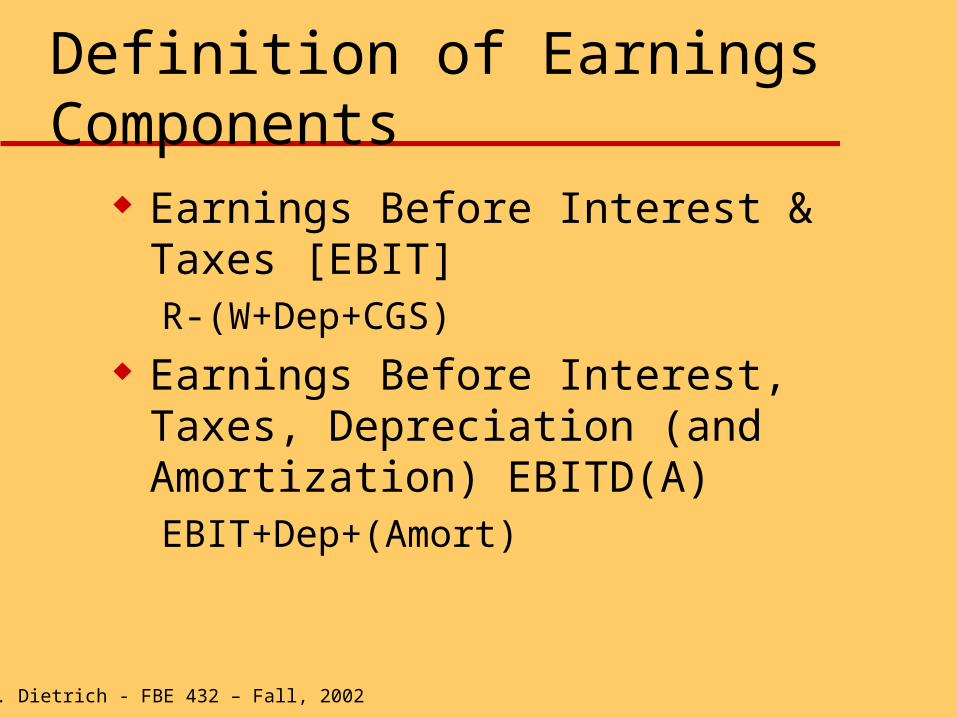

Definition of Earnings Components

Earnings Before Interest & Taxes [EBIT]R-(W+Dep+CGS)

Earnings Before Interest, Taxes, Depreciation (and Amortization) EBITD(A)EBIT+Dep+(Amort)

J. K. Dietrich - FBE 432 – Fall, 2002

Definitions of Earnings Components

Pre-Tax Income – [EBIT-Int]

Tax Bill [T]– (EBIT-Int)

Net Income – NI =Pre-Tax Income - T

J. K. Dietrich - FBE 432 – Fall, 2002

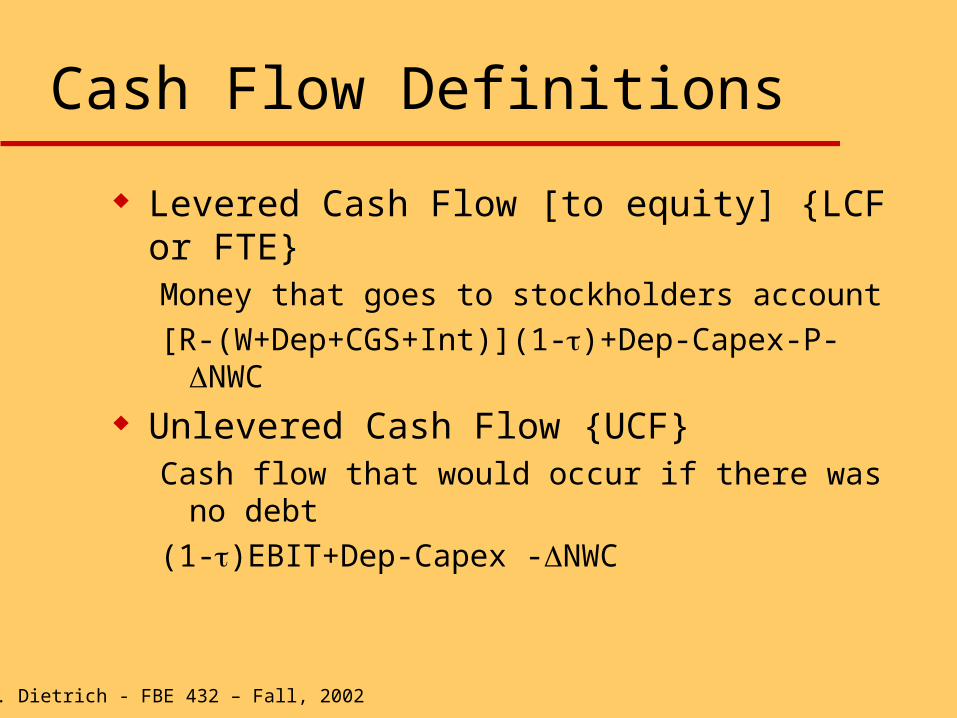

Cash Flow Definitions

Levered Cash Flow [to equity] {LCF or FTE}Money that goes to stockholders account

[R-(W+Dep+CGS+Int)](1-)+Dep-Capex-P-NWC

Unlevered Cash Flow {UCF}Cash flow that would occur if there was no debt

(1-)EBIT+Dep-Capex -NWC

J. K. Dietrich - FBE 432 – Fall, 2002

Next Week – September 4

Review valuation techniques and relate to case materials

Prepare Eskimo Pie Case Form groups for group case analyses

following Eskimo Pie