iveco 2010-2014 plan - final - cnh...

TRANSCRIPT

April 21, 2010 Fiat Investor Day 1

Paolo Monferino

Iveco

April 21, 2010 Fiat Investor Day 2

Performance over last plan period

~9.0 ~9.0 ~9.5

640-710 670-740 800-870

7.1-7.9% 7.4-8.2% 8.4-9.2%

Lingotto Plan Targets (Nov 2006)

Net revenues (€bn) Net revenues 2003-2007

CAGR +6.6% Trading profit (€mn)

Trading margin 4.0-7.5% operating margin range

Balocco Plan Targets (Jul 2004)

2007 2009 2008

Net

rev

enues

(€bn)

Trad

ing p

rofit

(€m

n)

2004* 2006 2005

* Pro-forma excluding FPT segment

Trading margin 3.7% 3.9% 6.0% 7.3% 7.7% 1.5%

April 21, 2010 Fiat Investor Day 3

Indust

rial

Oper

atin

g R

esult (€ m

n)

Return on Industrial Sales (%)

FY 2006

Source: Internal elaboration on publicly available information. Iveco excluding FPT Segment

-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

(14) (12) (10) (8) (6) (4) (2) - 2 4 6 8 10 12 14

Scania

Daimler Trucks

Volvo Trucks

Paccar

Man CV

Competition benchmark

April 21, 2010 Fiat Investor Day 4

-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

(14) (12) (10) (8) (6) (4) (2) - 2 4 6 8 10 12 14

Scania

Daimler Trucks

Volvo Trucks

Paccar

Man CV (incl. LA)

Return on Industrial Sales (%)

FY 2009

Source: Internal elaboration on publicly available information. Iveco excluding FPT Segment

Competition benchmark

Indust

rial

Oper

atin

g R

esult (€ m

n)

April 21, 2010 Fiat Investor Day 5

Revenues by business area

2006 Net Sales: €9.1bn

2009 Net Sales: €7.2bn

2008 Net Sales: €10.8bn

Enlarged product portfolio providing resilience

Light Medium Heavy Bus Special Vehicles

April 21, 2010 Fiat Investor Day 6

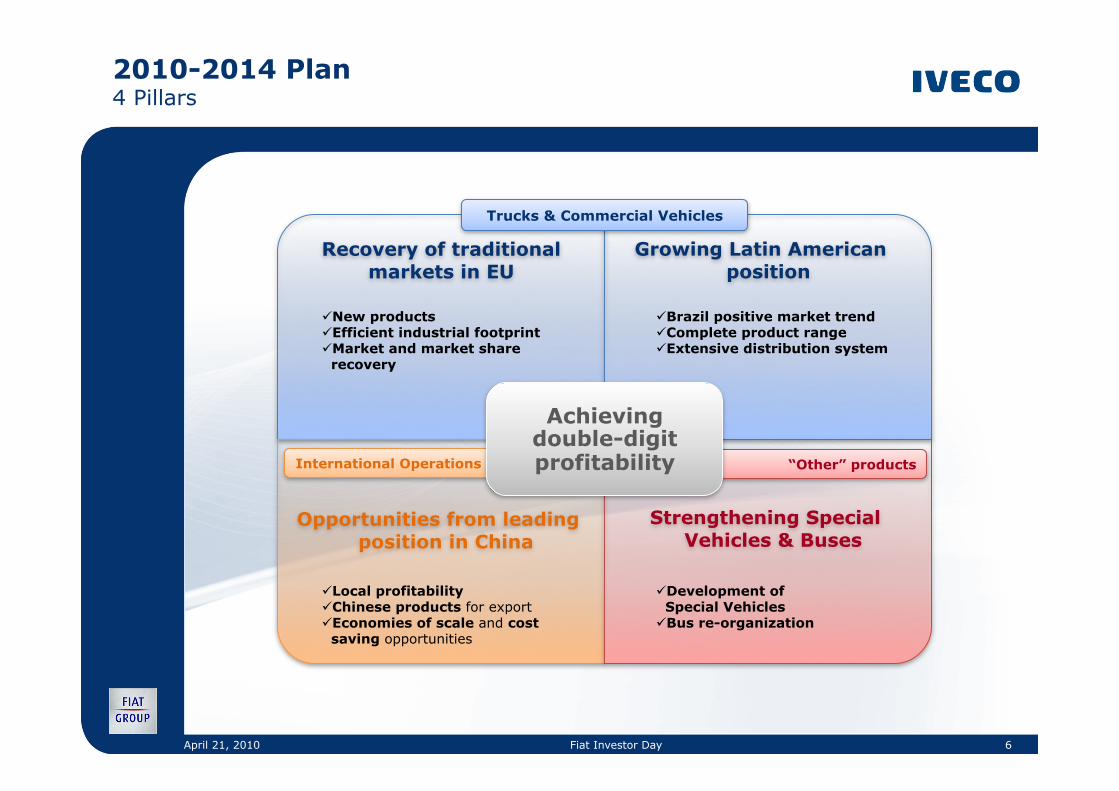

Recovery of traditional markets in EU

Growing Latin American position

Opportunities from leading position in China

Strengthening Special Vehicles & Buses

Local profitability Chinese products for export Economies of scale and cost

saving opportunities

Development of Special Vehicles

Bus re-organization

New products Efficient industrial footprint

Market and market share recovery

Brazil positive market trend Complete product range Extensive distribution system

“Other” products International Operations

Trucks & Commercial Vehicles

Achieving double-digit profitability

2010-2014 Plan 4 Pillars

April 21, 2010 Fiat Investor Day 7

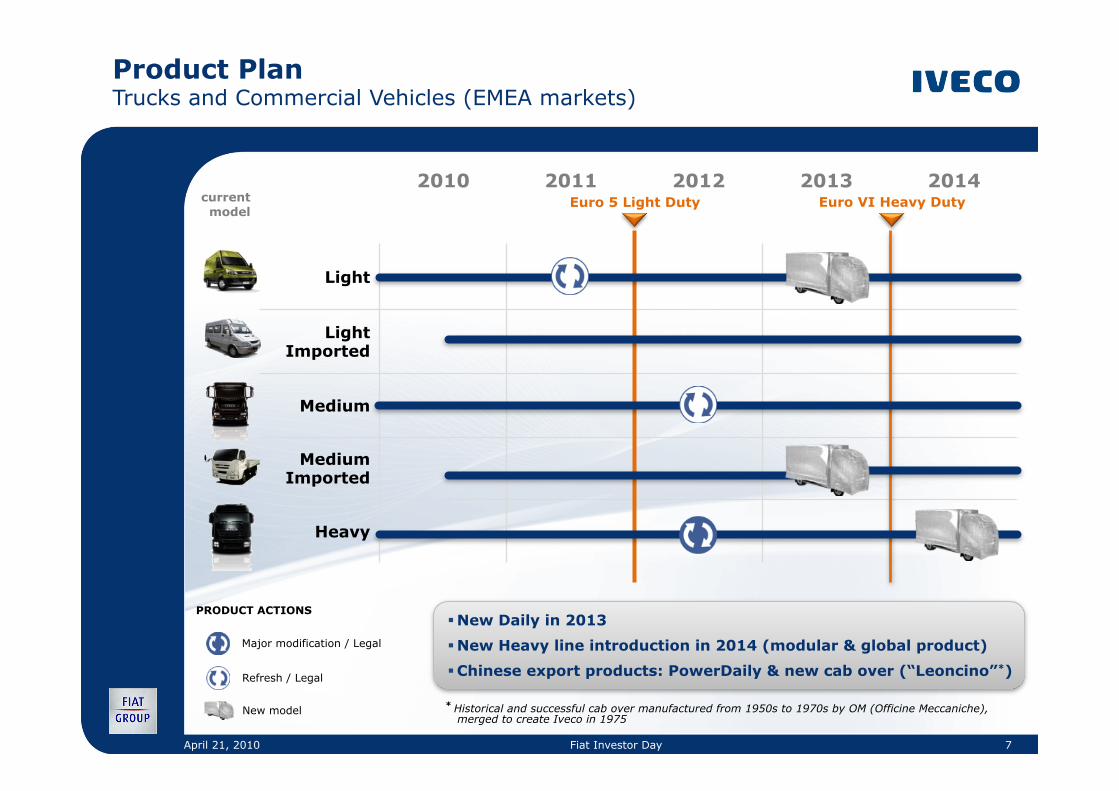

Product Plan Trucks and Commercial Vehicles (EMEA markets)

current model

2010 2011 2012 2013 2014

Light

Light Imported

Medium

Medium Imported

Heavy

PRODUCT ACTIONS

Refresh / Legal

Major modification / Legal

Euro 5 Light Duty Euro VI Heavy Duty

New Daily in 2013

New Heavy line introduction in 2014 (modular & global product)

Chinese export products: PowerDaily & new cab over (“Leoncino”*)

* Historical and successful cab over manufactured from 1950s to 1970s by OM (Officine Meccaniche), merged to create Iveco in 1975

New model

April 21, 2010 Fiat Investor Day 8

Focus on network strengths and service level

Customer concentration (change in distribution channel mix)

Road freight dominant

Gradual need for replacement of existing fleet

Emission legislation (Euro VI in 2013)

European market drivers

Our goal: Back to 2008 volumes in a "normalized" market

EU freight by mode

Source: Automotive World – June 2009

Transport needs strongly correlated to GDP

52% 60% 69%

74% 76%

77% 78%

30% 24%

18%

14%

12%

11%

11%

18%

16% 13%

12%

12%

12%

11%

Bill

ion t

ons/

km

April 21, 2010 Fiat Investor Day 9

Trucks & Commercial Vehicles European market trend

Market trend forecast in line with consensus

Western Europe Market ≥3.5T

Eastern Europe Market ≥3.5T

Western Europe

Eastern Europe (ex Russia, CIS countries and Bulgaria)

April 21, 2010 Fiat Investor Day 10

Trucks & Commercial Vehicles European market share

Light (3.5-6.0T)

Heavy (≥16.0T)

Medium (6.01-15.99T)

Western Europe

Eastern Europe (ex Russia, CIS countries and Bulgaria)

… …

… …

… …

April 21, 2010 Fiat Investor Day 11

Trucks & Commercial Vehicles – Africa & Mid-East Market and market share

Increase dealer network coverage from 49 to ~80 points-of-sale by 2014

Light + Imported

products (3.5-6.0T)

Heavy (≥16.0T)

Market (k units) Market share

… …

… …

… …

Medium + Imported

products (6.01-15.99T)

April 21, 2010 Fiat Investor Day 12

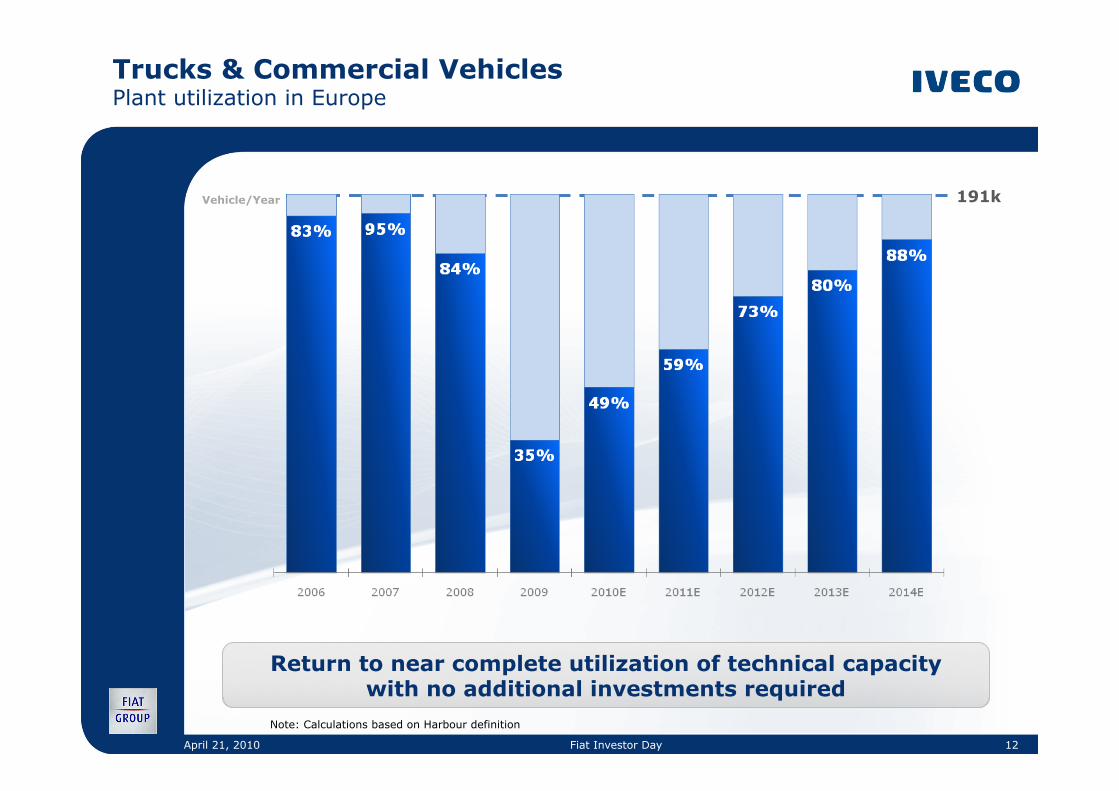

Trucks & Commercial Vehicles Plant utilization in Europe

Return to near complete utilization of technical capacity with no additional investments required

191k Vehicle/Year

Note: Calculations based on Harbour definition

April 21, 2010 Fiat Investor Day 13

Trucks & Commercial Vehicles Industrial flexibility in Europe

Fixed industrial cost / Production volumes (Base 100 = 2009)

7% average YoY efficiency improvement over the plan (mainly on the back of WCM program)

April 21, 2010 Fiat Investor Day 14

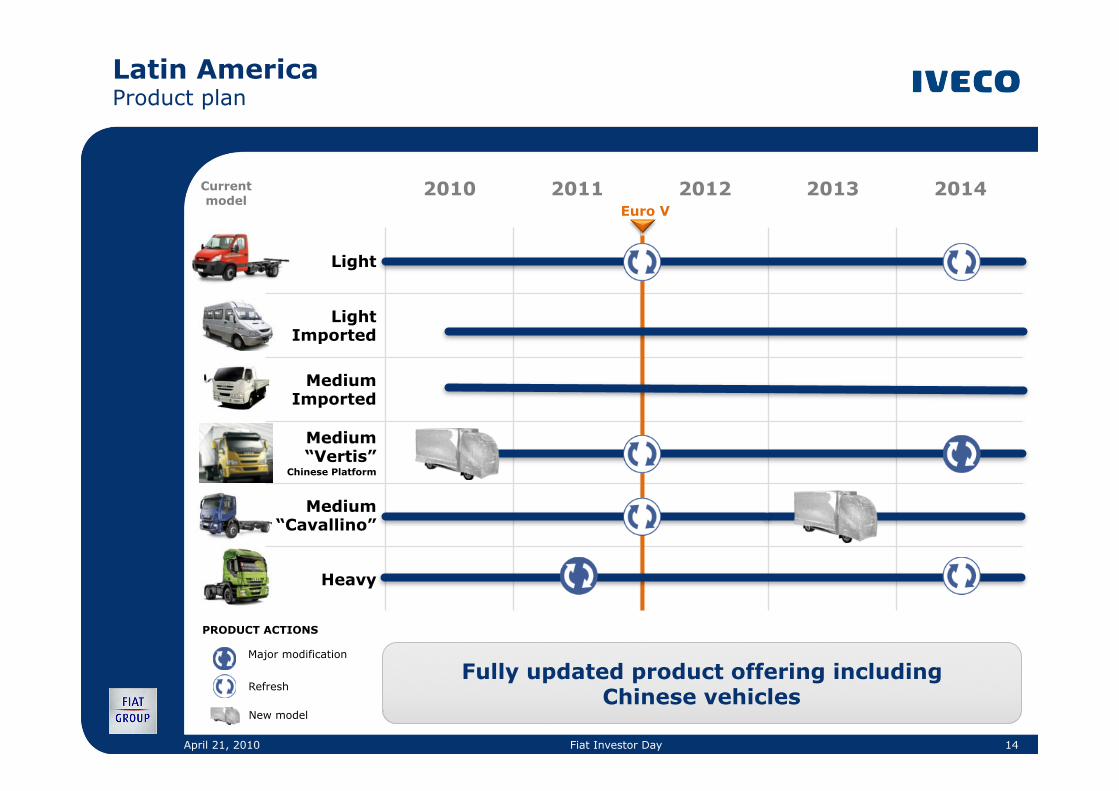

Latin America Product plan

PRODUCT ACTIONS

Refresh

Major modification

New model

Fully updated product offering including Chinese vehicles

Current model

2010 2011 2012 2013 2014

Light

Light Imported

Medium Imported

Medium “Vertis”

Chinese Platform

Medium “Cavallino”

Heavy

Euro V

April 21, 2010 Fiat Investor Day 15

Latin America Market and market share

Significant growth opportunities leveraging on Brazil volumes

Light (2.8-7.9T)

Medium (8.1-31.0T)

Heavy (>31.0T)

Market (k units) Market share

… …

… …

… …

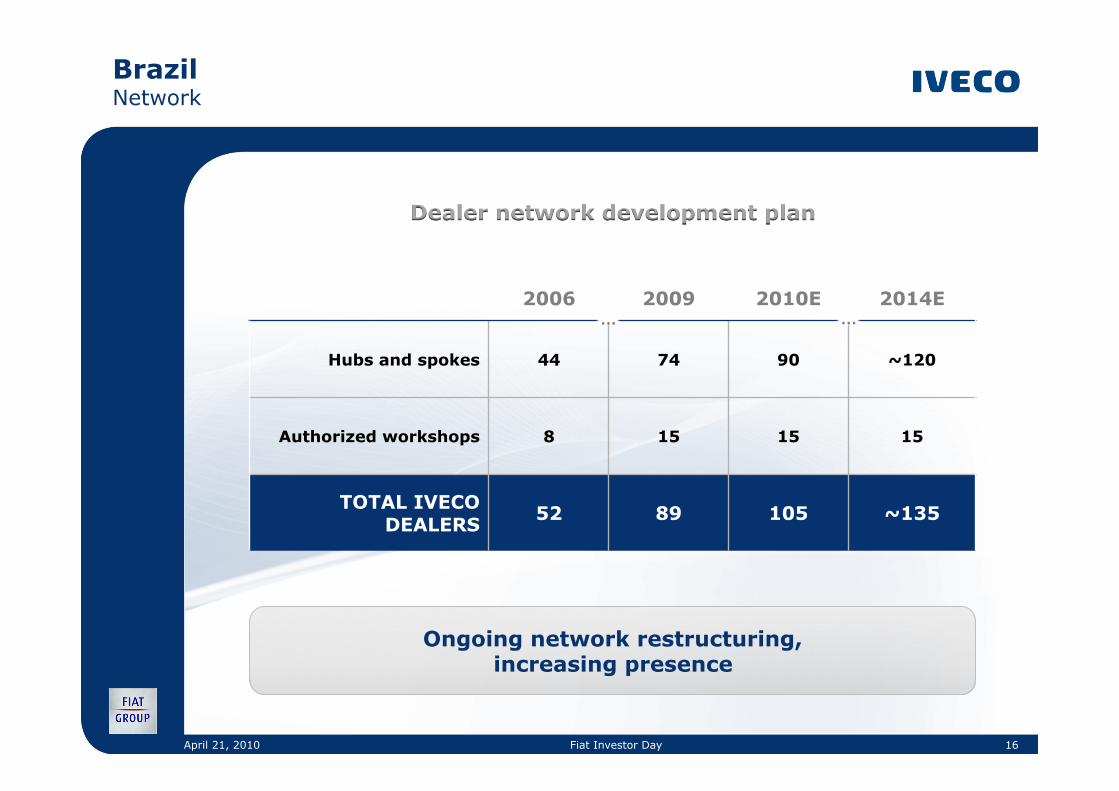

April 21, 2010 Fiat Investor Day 16

Brazil Network

Ongoing network restructuring, increasing presence

2006 2009 2010E 2014E

Hubs and spokes 44 74 90 ~120

Authorized workshops 8 15 15 15

TOTAL IVECO DEALERS

52 89 105 ~135

Dealer network development plan

… …

April 21, 2010 Fiat Investor Day 17

Special Vehicles Key objectives

Defence • Consolidate technological leadership in Protection

Systems and Mobility Performance

• Multirole product range completion

• Growth outside traditional markets (€2.5bn contract with Brazilian Ministry of Defence)

Fire Fighting • Enlarge product range (Aircrash) to keep worldwide

leadership

Astra • Leveraging construction sector recovery

Net revenues of ~ €1.4bn by 2014 (+40% vs. 2009)

Keep on developing business by leveraging success of recent products and extending offering and geographical presence

April 21, 2010 Fiat Investor Day 18

Buses Key objectives

Product range rationalization

• Product standardization and cost reduction

• Overlapping vehicles to be discontinued

• New entry-level coach to gain additional volumes

Re-balancing industrial footprint

• Industrial cost optimization

• WCM to improve efficiency

Entering new markets

• New Citybus versions to compete in non-domestic markets

• Direct distribution in major markets

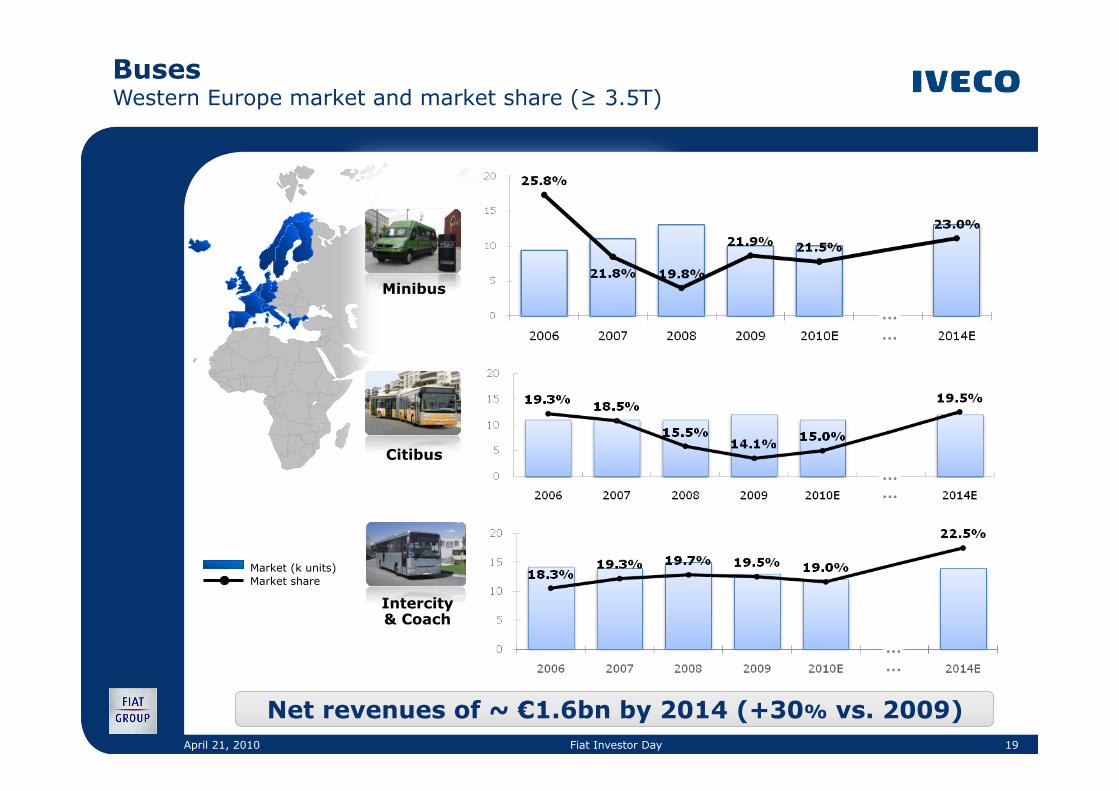

April 21, 2010 Fiat Investor Day 19

Buses Western Europe market and market share (≥ 3.5T)

Net revenues of ~ €1.6bn by 2014 (+30% vs. 2009)

Minibus

Intercity & Coach

Citibus

Market (k units) Market share

… …

… …

… …

April 21, 2010 Fiat Investor Day 20

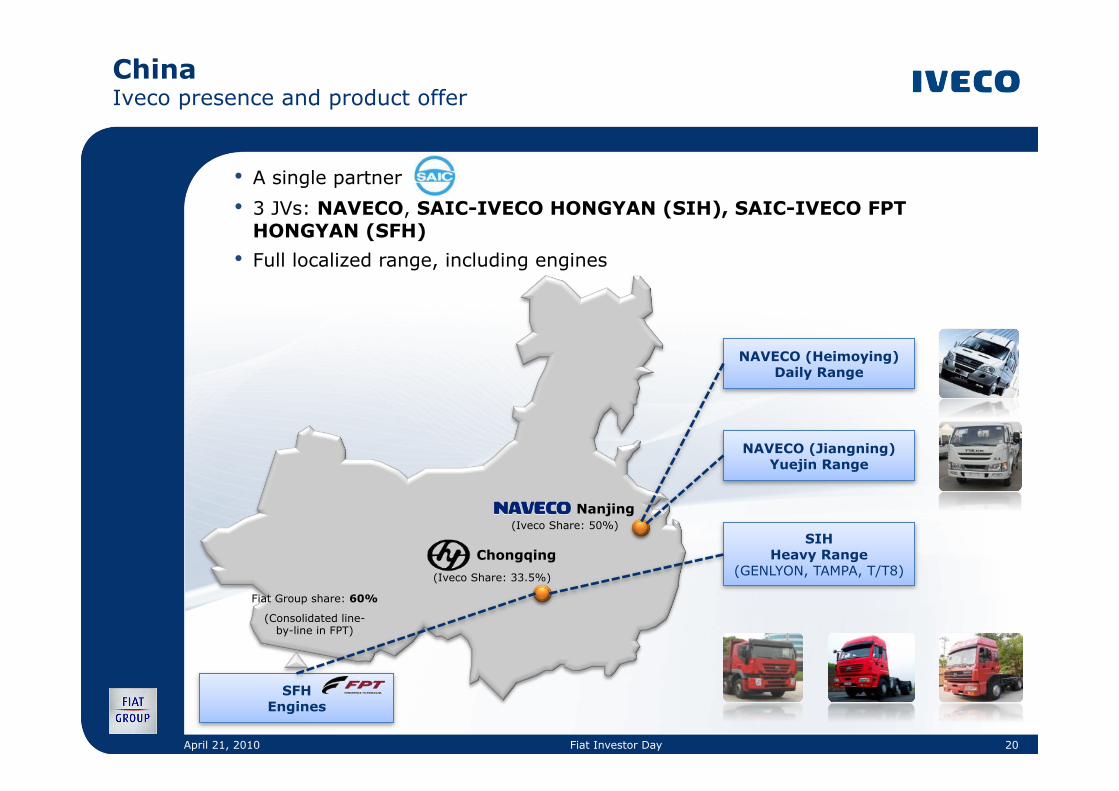

NAVECO (Heimoying) Daily Range

China Iveco presence and product offer

Chongqing�SIH

Heavy Range (GENLYON, TAMPA, T/T8)

NAVECO (Jiangning) Yuejin Range

Nanjing �

• A single partner

• 3 JVs: NAVECO, SAIC-IVECO HONGYAN (SIH), SAIC-IVECO FPT HONGYAN (SFH)

• Full localized range, including engines

(Iveco Share: 50%) �

(Iveco Share: 33.5%) �

SFH Engines

Fiat Group share: 60%

(Consolidated line- by-line in FPT)

April 21, 2010 Fiat Investor Day 21

China Strong platform for growth

Serving domestic market

Increasing Network territory coverage

2009 2014E

JV Exports (units)* 1 k 24 k

Exporting to international markets

Leveraging supplier base for global sourcing

Targeting €300mn Annual Purchase Value in 2014

*Included in Iveco consolidated sales

Sales volumes by segment (k units)

Hongyan

CAGR (2006-2014E)

11.5%

9.2%

7.1%

Yuejin

Power Daily

3,293

2,581 2,576

1,923 2,154

1,632

… …

…

Iveco estimates

April 21, 2010 Fiat Investor Day 22

China JV performance

Iveco interest recognised under equity method

2006 2007 2008 2009 2010E 2014E

Wholesale units (k units) TOTAL JVs

20 95 92 107 130 235

Net Revenue (€ bn) TOTAL JVs

0.3 1.0 1.0 1.2 ~1.5 ~3.2

Net Profit (€ mn) IVECO Interest

9 6 13 4 10 80+

…

April 21, 2010 Fiat Investor Day 23

k units

2014E

Looking at Iveco from a wider perspective Iveco + Chinese JVs consolidated volumes (pro-forma)

Common components and product investments fully supported by total size

…

…

April 21, 2010 Fiat Investor Day 24

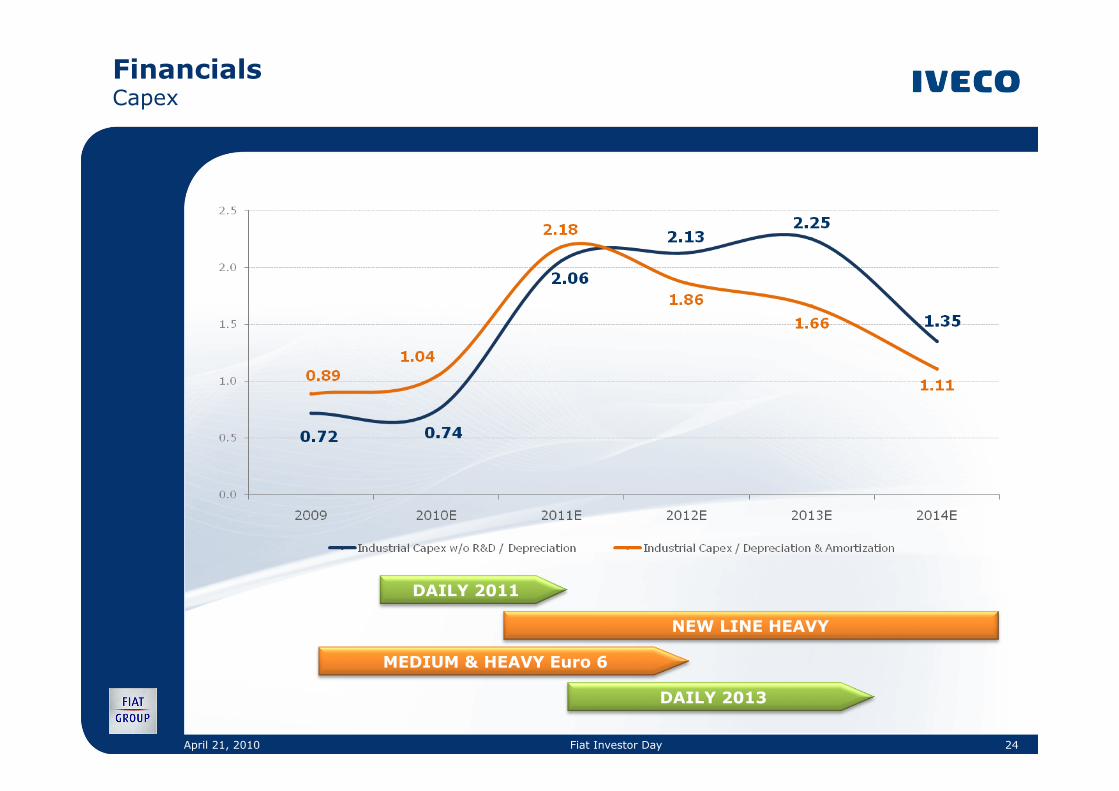

Financials Capex

MEDIUM & HEAVY Euro 6

DAILY 2013

NEW LINE HEAVY

DAILY 2011

April 21, 2010 Fiat Investor Day 25

2010-14 Financial targets

April 21, 2010 Fiat Investor Day 26

Our roadmap to double-digit profitability

• Market Western & Eastern European markets restored to “normalized” level, but

still below 2007 peak

Strengthening our position in Latin America with significant market growth in Light & Medium segments and share gains across range

Full exploitation of Chinese platforms for export to Africa & Mid-East and Latin America

• Substantially overhauled portfolio across all product ranges and geographies including Chinese trucks to complement range

• Major efficiency gains in manufacturing with ~90% capacity utilization by 2014

• Significant growth in Special Vehicles and realignment of product portfolio in Buses resulting in manufacturing efficiencies