iv sample paper-i accountancy class xii - crpf · pdf file... iv sample paper-i accountancy...

TRANSCRIPT

SAMPLE PAPER-I - IV

SAMPLE PAPER-I ACCOUNTANCY

CLASS XII

Q1. What is the nature of Receipts & Payments Account? (1 Mark)

Q2. A and B are partners sharing profits in the ratio of 2:1. C is admitted for 1/4th share. Calculate new and

sacrificing ratio. (1 Mark)

Q3. Name the two items that would appear in credit side of Partner’s Capital account when capitals are

fixed. (1 Mark)

Q4. How is provision for doubtful debt treated at the time of dissolution of firm? (1 Mark)

Q5. State any two purposes for which Securities Premium A/c can be utilized. (1 Mark)

Q6. How will you deal with the Donation while preparing the final accounts for the year ending on 31/3/08

in each of the following cases: (3 Mark)

(a) During the year 2007-08, donation received Rs.50,000 and it is treated as capital item as per the policy

of the club.

(b) During the year 2007-08, donation received Rs.50,000 and 60% of the donation is to be capitalized as

per the policy of the club.

Q7. 500 shares of Rs.100 each issued at a discount of 10% were forfeited for non-payment of allotment

money of Rs.50 per share. The first and final call of Rs.10 per share on these shares was not made. The

forfeited shares were reissued at Rs.80 per share fully paid up. Journalise.(3 Mark)

Q8. A company redeemed its Rs.2,00,000 debentures at 10% premium out of profits. The company has

sufficient profits for the purpose. Pass necessary journal entries.(3 Mark)

Q9. A, B and C are partners sharing profits and losses in the ratio 5:3:2. Their capital on 1/1/09 were

Rs.1,00,000, Rs.80,000 and Rs.60,000 respectively. They withdrew Rs.500 each on first day of every

month. According to their partnership agreement they are allowed interest on capital @ 5% and charged

interest on drawings @ 6% per year. The profits for the year 2009 as per Profit and Loss A/c amounted to

Rs.1,50,000 out of which Rs.10,000 were transferred to General Reserve. A and B were entitled to a salary

of Rs.2,500 and Rs.2,000 per year and C is entitled to a commission of 5% on net divisible profit after

charging such commission. Prepare Profit and Loss Appropriation A/c and show your workings clearly.

(4 Mark)

Q10. P, Q and R were sharing profits in the ratio of 5:3:2. They decided to share future profits in the ratio

of 2:3:5 with effect from 1/4/2009. They decided to record the effect of the following without affecting the

book value of Profit & Loss A/c (Cr.) Rs.24,000 and Advertisement Suspense A/c Rs.12,000. Pass the

necessary adjusting entry. (4 Mark)

Q11. XYZ Ltd. purchased sundry assets worth Rs.3,81,000 and assumed liabilities of Rs.81,000 from ABC

Ltd. The purchase consideration was agreed at Rs.2,80,000. The amount was to be paid by 8%debentures

of Rs.100 each at a premium of 25%. Give necessary journal entries. (4 Mark)

Q12. X Ltd. Issued 2,00,000 shares of Rs.10 each payable as Rs.2.50 on application (on 1/1/09),

Rs.2.50.on allotment ( on 1/4/09), Rs.3 on first call ( on 1/7/09) and Rs.2 on second & final call (on

1/10/03). All the shares were subscribed and all the sums were duly received. Amit, a shareholder, who had

1,000 shares paid the amount of first and second calls with the allotment.Whereas Sumit, another

shareholder, paid the amount of first call with the second call. Company adopted Table A for interest on calls

in arrears and calls in advance. Pass necessary journal entries. (6 Mark)

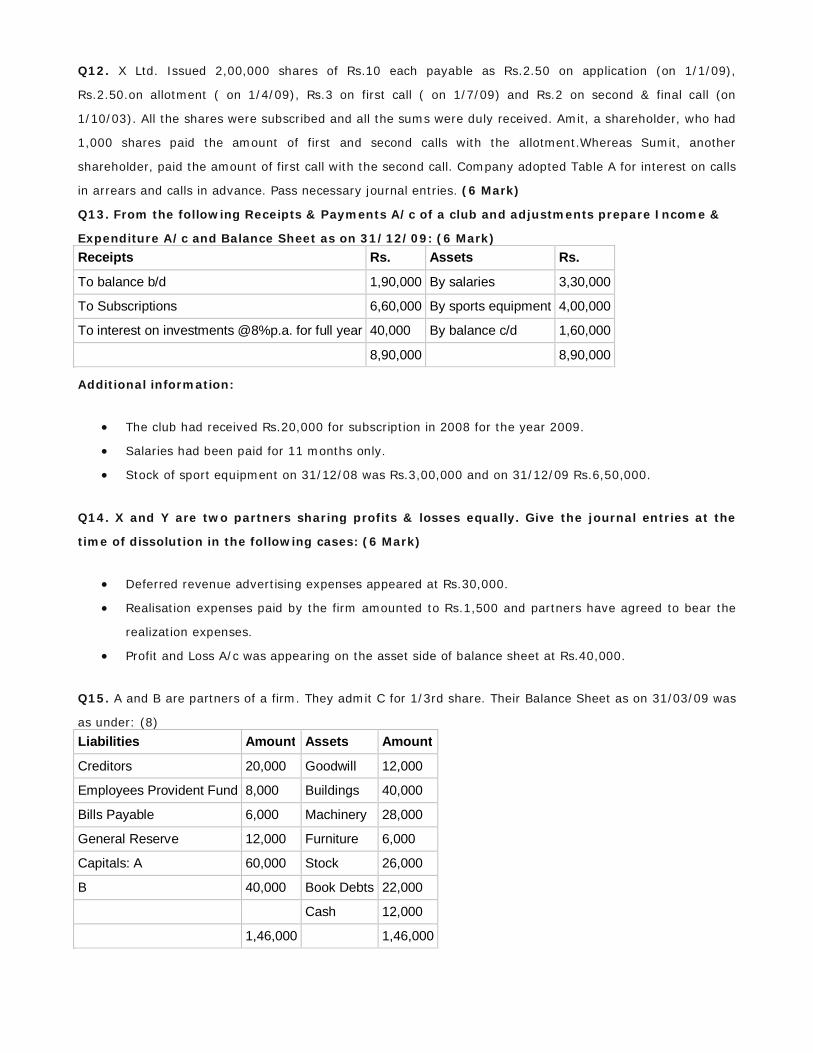

Q13. From the following Receipts & Payments A/c of a club and adjustments prepare Income &

Expenditure A/c and Balance Sheet as on 31/12/09: (6 Mark)

Receipts Rs. Assets Rs.

To balance b/d 1,90,000 By salaries 3,30,000

To Subscriptions 6,60,000 By sports equipment 4,00,000

To interest on investments @8%p.a. for full year 40,000 By balance c/d 1,60,000

8,90,000 8,90,000

Additional information:

The club had received Rs.20,000 for subscription in 2008 for the year 2009.

Salaries had been paid for 11 months only.

Stock of sport equipment on 31/12/08 was Rs.3,00,000 and on 31/12/09 Rs.6,50,000.

Q14. X and Y are two partners sharing profits & losses equally. Give the journal entries at the

time of dissolution in the following cases: (6 Mark)

Deferred revenue advertising expenses appeared at Rs.30,000.

Realisation expenses paid by the firm amounted to Rs.1,500 and partners have agreed to bear the

realization expenses.

Profit and Loss A/c was appearing on the asset side of balance sheet at Rs.40,000.

Q15. A and B are partners of a firm. They admit C for 1/3rd share. Their Balance Sheet as on 31/03/09 was

as under: (8)

Liabilities Amount Assets Amount

Creditors 20,000 Goodwill 12,000

Employees Provident Fund 8,000 Buildings 40,000

Bills Payable 6,000 Machinery 28,000

General Reserve 12,000 Furniture 6,000

Capitals: A 60,000 Stock 26,000

B 40,000 Book Debts 22,000

Cash 12,000

1,46,000 1,46,000

On C’s admission it was agreed:

C should bring Rs.1,00,000 as capital and Rs.5,000 as his share of goodwill.

Goodwill appearing in the books should be written off.

Provision for loss on stock and provision for bad debts is to be made at 10% and 5% respectively.

The value of building is to be taken at Rs.50,000.

Total capitals of the firm has been fixed at Rs.3,00,000 and Partners Capital A/cs are to be adjusted in the

profit sharing ratio. Any excess is to be transferred to current a/cs and deficit is to be brought in cash.

OR

The Balance Sheet of X,Y and Z who shared profits in the ratio of 4:3:2 as on 31/03/200 was as

follows:

Liabilities Amount Assets Amount

Creditors 7,700 Cash at Bank 6,300

General Reserve 1,800 Debtors 6,000

Capitals: Less: Provision 300 5,700

X 19,000 Stock 7,000

Y 14,000 Plant & Machinery 10,500

Z 12,000 Buildings 25,000

54,500 54,500

Y retired on the above date and it was agreed that:

Stock to be depreciated by 5% and building be appreciated by 5%.

A provision of Rs.320 be made for legal charges.

Goodwill of the firm is valued at Rs.14,400 but no goodwill account is to be raised.

X and Z to share future profits in the ratio 5:3.

Y to be paid Rs.5,000 in cash and balance to be transferred to his loan account.

X and Z to maintain their capitals in the new profit sharing ratio and to bring in or withdraw cash for the

purpose. Capital of the new firm be fixed at Rs.28,000. Prepare ledger accounts and balance sheet of the

firm after Y’s retirement.

Q16. X Ltd. was registered with a nominal capital of Rs.2,00,000 divided into 2,000 equity shares of Rs.100

each. 1,000 shares were issued as fully paid to the vendors for purchase of fixed assets. The remaining

1,000 shares were offered for public subscription at a premium of Rs.5 per share payable as Rs10 per share

on application, Rs.25 per share (including premium) on allotment, Rs.40 per share on first call and Rs.30

per share on final call. Applications were received for 900 shares which were duly allotted. At the time of the

first call, a shareholder who held 100 shares failed to the first call money and his shares were forfeited.

These shares were reissued at Rs.60 per share, Rs.70 paid up. Final call was not made. Pass necessary

journal entries. (8 Mark)

OR

Abhishek Ltd. invited applications for 50,000 shares of Rs.10 each at a discount of Rs.2 per share

payable as Rs.2 on application, Rs.3 on allotment, Rs.2 on first call and Rs.1 on final call.

Applications were received for 70,000 shares. Allotment was made as under:

To applicants of 10,000 shares - in full

To applicants of 20,000 shares - 15,000 shares

To applicants of 40,000 shares - 25,000 shares

The shares were fully called and paid up except amounts on allotment, first and final call not paid by those

who applied for 2,000 shares out of group applying for 20,000 shares. These shares were forfeited and

1,200 of these shares were reissued @ Rs.7 per shares. Journalise.

PART B

(ANALYSIS OF FINANCIAL STATEMENTS)

Q17. Name two parties who may be interested in analysis of financial statements. (1 Mark)

Q18. How will you treat increase in share capital while preparing cash flow statement as per AS-3 (revised).

(1 Mark)

Q19. What are the two major inflow and outflows of cash from investing activities? (1 Mark)

Q20. Under what heading will you classify the following items in the balance sheet of a

Company? (3 Mark)

(i) Advances to suppliers

(ii) Goodwill

(iii) Deposit with Custom Authorities

(iv)Debenture Suspense A/c

(v) Acceptances

(vi) Provision for Provident Fund

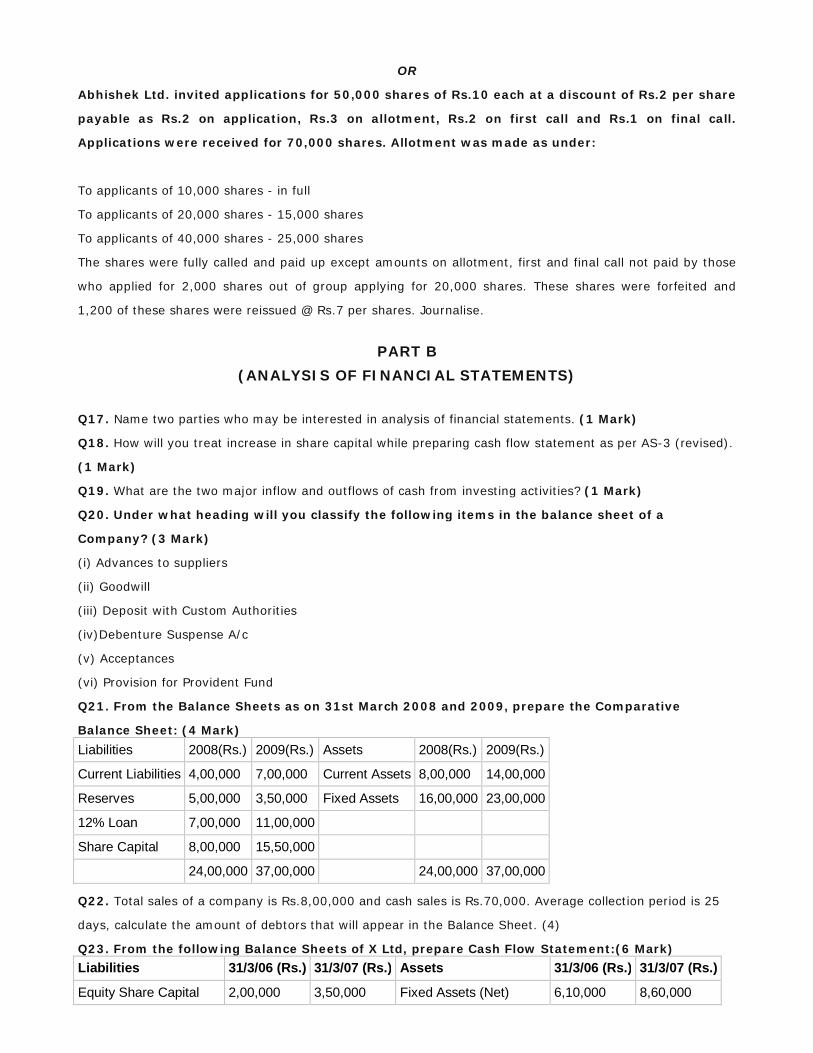

Q21. From the Balance Sheets as on 31st March 2008 and 2009, prepare the Comparative

Balance Sheet: (4 Mark)

Liabilities 2008(Rs.) 2009(Rs.) Assets 2008(Rs.) 2009(Rs.)

Current Liabilities 4,00,000 7,00,000 Current Assets 8,00,000 14,00,000

Reserves 5,00,000 3,50,000 Fixed Assets 16,00,000 23,00,000

12% Loan 7,00,000 11,00,000

Share Capital 8,00,000 15,50,000

24,00,000 37,00,000 24,00,000 37,00,000

Q22. Total sales of a company is Rs.8,00,000 and cash sales is Rs.70,000. Average collection period is 25

days, calculate the amount of debtors that will appear in the Balance Sheet. (4)

Q23. From the following Balance Sheets of X Ltd, prepare Cash Flow Statement:(6 Mark)

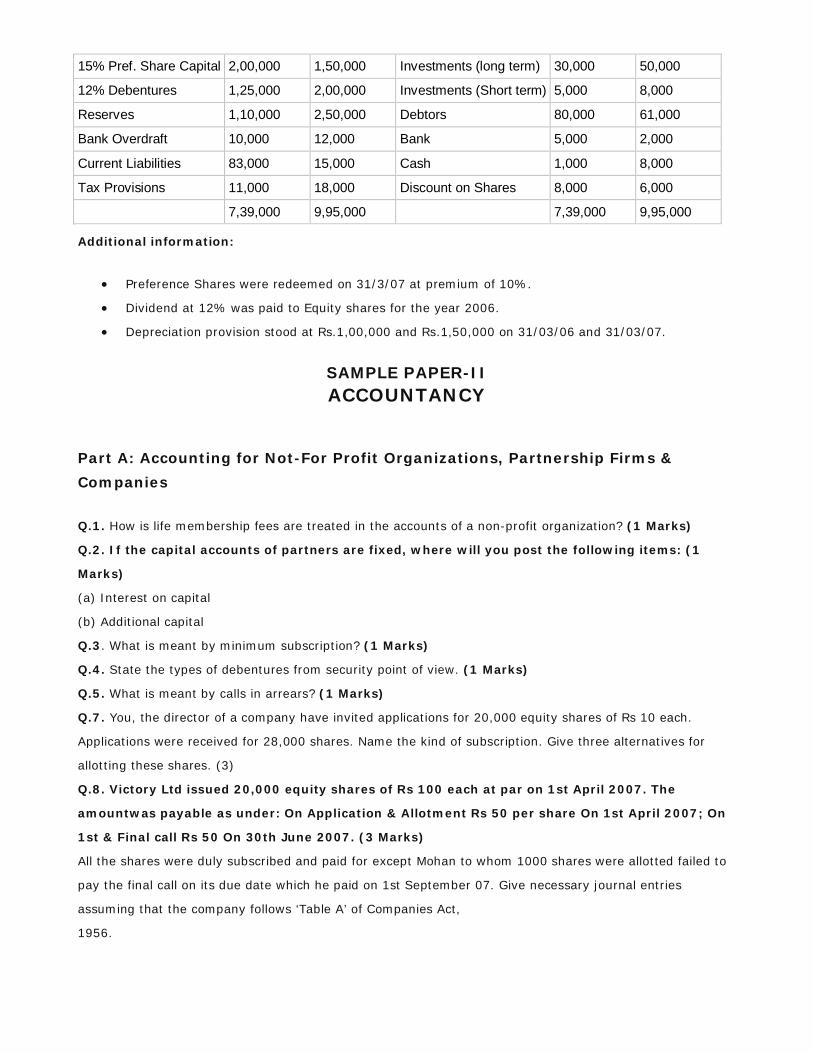

Liabilities 31/3/06 (Rs.) 31/3/07 (Rs.) Assets 31/3/06 (Rs.) 31/3/07 (Rs.)

Equity Share Capital 2,00,000 3,50,000 Fixed Assets (Net) 6,10,000 8,60,000

15% Pref. Share Capital 2,00,000 1,50,000 Investments (long term) 30,000 50,000

12% Debentures 1,25,000 2,00,000 Investments (Short term) 5,000 8,000

Reserves 1,10,000 2,50,000 Debtors 80,000 61,000

Bank Overdraft 10,000 12,000 Bank 5,000 2,000

Current Liabilities 83,000 15,000 Cash 1,000 8,000

Tax Provisions 11,000 18,000 Discount on Shares 8,000 6,000

7,39,000 9,95,000 7,39,000 9,95,000

Additional information:

Preference Shares were redeemed on 31/3/07 at premium of 10%.

Dividend at 12% was paid to Equity shares for the year 2006.

Depreciation provision stood at Rs.1,00,000 and Rs.1,50,000 on 31/03/06 and 31/03/07.

SAMPLE PAPER-II ACCOUNTANCY

Part A: Accounting for Not-For Profit Organizations, Partnership Firms &

Companies

Q.1. How is life membership fees are treated in the accounts of a non-profit organization? (1 Marks)

Q.2. If the capital accounts of partners are fixed, where will you post the following items: (1

Marks)

(a) Interest on capital

(b) Additional capital

Q.3. What is meant by minimum subscription? (1 Marks)

Q.4. State the types of debentures from security point of view. (1 Marks)

Q.5. What is meant by calls in arrears? (1 Marks)

Q.7. You, the director of a company have invited applications for 20,000 equity shares of Rs 10 each.

Applications were received for 28,000 shares. Name the kind of subscription. Give three alternatives for

allotting these shares. (3)

Q.8. Victory Ltd issued 20,000 equity shares of Rs 100 each at par on 1st April 2007. The

amountwas payable as under: On Application & Allotment Rs 50 per share On 1st April 2007; On

1st & Final call Rs 50 On 30th June 2007. (3 Marks)

All the shares were duly subscribed and paid for except Mohan to whom 1000 shares were allotted failed to

pay the final call on its due date which he paid on 1st September 07. Give necessary journal entries

assuming that the company follows ‘Table A’ of Companies Act,

1956.

Q.9. A Ltd issued 5,000, 9% Debentures of Rs 100 each at par and also raised a loan of Rs 3,00,000 from

bank collaterally secured by Rs 4,00,000, 9% debentures. How will you show the Debentures in the Balance

Sheet of the company assuming that the company has recorded the issue of Debentures as collateral

security in its books? (3 Marks)

Q.10. Shiv and Shanker were partners in a firm sharing profits in the ratio of 3:2. Their fixed

capitals were Rs 1,70,000 and Rs 2,10,000 respectively. The partnership deed provides for the

following; (4 Marks)

(a) Interest on capital @ 12% p.a.

(b) Interest on drawings @ 18% p.a. Shiv drew Rs 12,000 on 30.06.06 and Shanker drew Rs 18,000 pm

30.09.06. The profit for the year ended 31st March 2007 was Rs 97,000, which was distributed among the

partners without providing for the above adjustments. Pass adjustment entry.

Q.11. A, B & C were partners in the ratio of 2:2:1. The books are closed on 31st March each year.

B died on 1st June 2006. As per the terms of deed deceased partner’s share in current accounting

year was to be calculated on the basis of average profit of last four years preceding the death of

partner. The profits and losses were as under: (4 Marks)

2001-02 Rs 30,000 Profit

2002-03 Rs 20,000 Profit

2003-04 Rs 60,000 Profit

2004-05 Rs 40,000 Profit

2005-06 Rs 10,000 Profit

Goodwill of the firm was to be twice the profits amount credited to deceased partner’s account in last five

years. You are required to calculate deceased partner’s share in current year’s profit & goodwill & pass

necessary journal entries to record this.

Q.12. X Ltd has a balance of Rs 5,00,000 in the profit and loss Account. The company decides to forego the

payment of dividend and instead utilizes the profits to repay 12% Debentures of Rs 3,50,000 on June 30th

2008 at a premium of 10%. Debentures interest is payable annually on 31st March. The company also has a

balance of Rs 2,00,000 in the Debenture Redemption Reserve Account. Journalize the above transactions in

the books of X Ltd. (6 Marks)

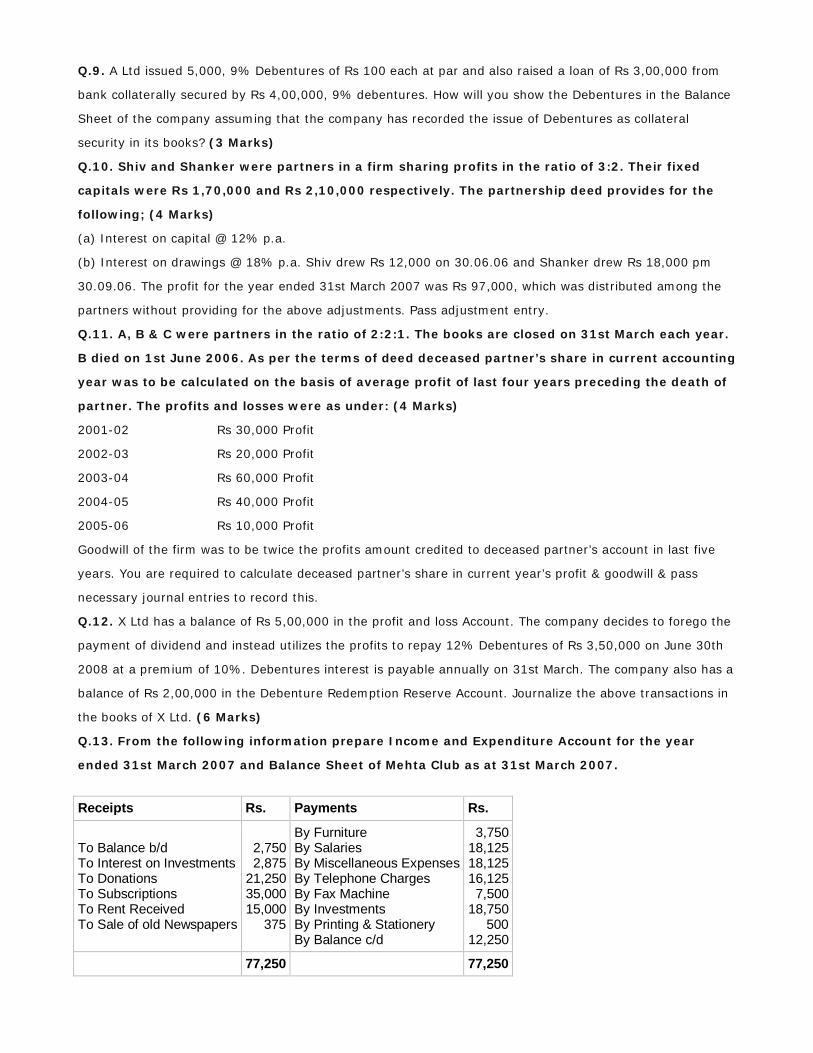

Q.13. From the following information prepare Income and Expenditure Account for the year

ended 31st March 2007 and Balance Sheet of Mehta Club as at 31st March 2007.

Receipts Rs. Payments Rs.

To Balance b/d To Interest on Investments To Donations To Subscriptions To Rent Received To Sale of old Newspapers

2,750 2,875

21,250 35,000 15,000

375

By Furniture By Salaries By Miscellaneous Expenses By Telephone Charges By Fax Machine By Investments By Printing & Stationery By Balance c/d

3,750 18,125 18,125 16,125 7,500

18,750 500

12,250

77,250 77,250

Additional Information:

Subscriptions received included Rs. 750 for 2007-08. The amount of Subscriptions

Outstanding on 31.032007 was Rs. 625; Salaries during 2006-07 unpaid were Rs. 875 and

Rent receivable was Rs. 250, 60% of the Donations were to be capitalized. Capital Fund as at

31st March 2006 was Rs. 12,750 and club also had investments of Rs. 10,000.

Q.14. A & B were partners in the ratio of 3:2. Due to heavy losses they decided to dissolve their

business. Give journal entries for each of the following transactions: (Assume that assets other

than cash & Bank and External liabilities have been transferred to Realization Account) (6 Marks)

(a) Furniture of the book value Rs 40,000 was realized at 85%.

(b) Stock appeared in the books at Rs 30,000,1/2 of which was taken over by B at 5% discount.

(c) The remaining stock was accepted by Bank against their loan of Rs 18,000.

(d) B agreed to pay off his wife’s loan of Rs 3,000 and took away unrecorded investments of Rs 2,000 at an

agreed valuation of Rs 1,800.

(e) The general reserve appeared in the books at 7,200

(f) The loss on realization amounted to Rs 4,500.

Q15. (a) FAST Ltd forfeited 100 shares of Rs 10 each (Rs 8 called up) for non-payment of allotment of Rs 2

per share & first call of Rs 3 per share. These shares were issued at 5% discount. Of these 75 shares were

reissued at Rs 6 per share.

(b) FAST Career Ltd forfeited 100 shares of Rs 10 each (Rs 8 called up) for non payment of allotment of Rs

2 per share & first call of Rs 3 per share. These shares were issued at 5% discount. Of these 75 shares were

reissued at Rs 6 per share as fully paid up.

(C) FAST Academic Research Center forfeited 100 shares of Rs 10 each (Rs 9 called up) for non-payment of

allotment of Rs 2 per share & first call of Rs 2 per share. These shares were issued at 10% discount. Of

these 80 shares were reissued at Rs 6 per share as Rs 8 paid up. (8 Marks)

Part B: Analysis of Financial Statements

Q.17. State any two objectives of preparing cash flow statement. (1 Marks)

Q.18. The Debt equity ratio of a company is 2:3.State which of the following would

increase/decrease/not change the

existing ratio: (1 Marks)

(a) Issue of equity shares for cash Rs 1,00,000

(b) Payment to creditors Rs 54,500 in full settlement of Rs 60,000.

Q.19. Calculate the amount of Tax paid from the following information; (1 Marks)

Provision for taxation at the end of the year Rs 31,000

Provision for taxation at the beginning of the year Rs 15,000

Income tax provision created during the year was Rs 43,000.

Q.20. What is a contingent liability explain with suitable example. (3 Marks)

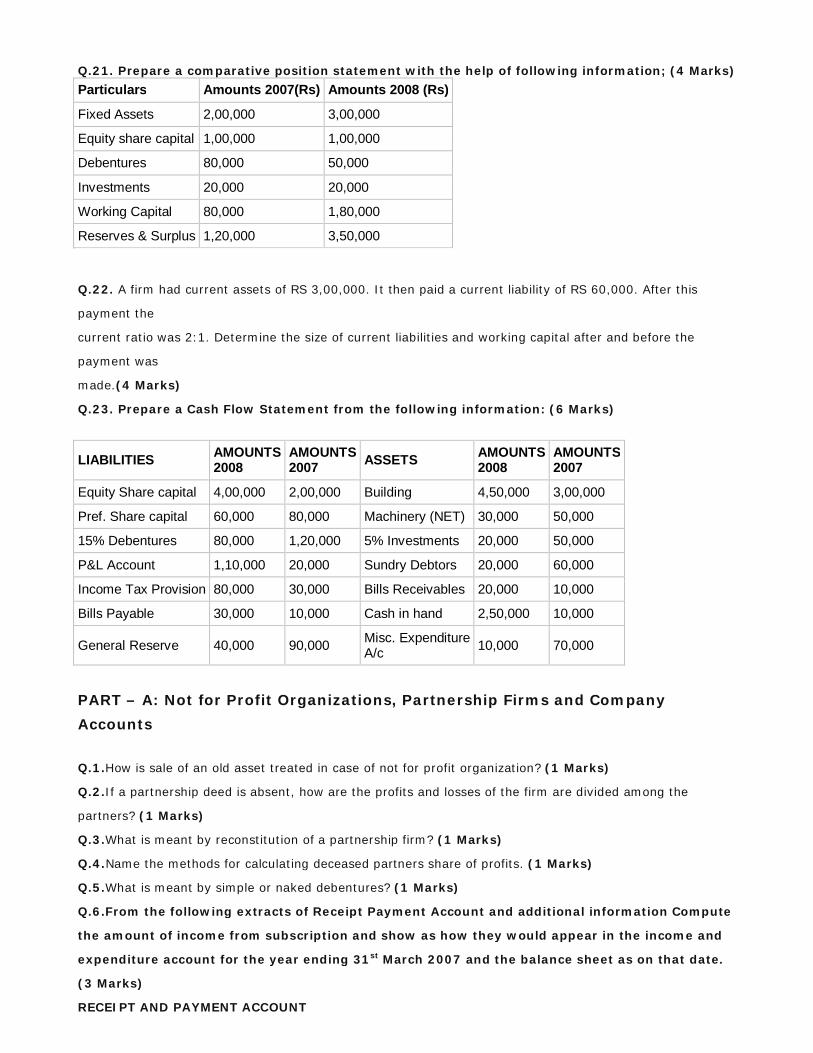

Q.21. Prepare a comparative position statement with the help of following information; (4 Marks)

Particulars Amounts 2007(Rs) Amounts 2008 (Rs)

Fixed Assets 2,00,000 3,00,000

Equity share capital 1,00,000 1,00,000

Debentures 80,000 50,000

Investments 20,000 20,000

Working Capital 80,000 1,80,000

Reserves & Surplus 1,20,000 3,50,000

Q.22. A firm had current assets of RS 3,00,000. It then paid a current liability of RS 60,000. After this

payment the

current ratio was 2:1. Determine the size of current liabilities and working capital after and before the

payment was

made.(4 Marks)

Q.23. Prepare a Cash Flow Statement from the following information: (6 Marks)

LIABILITIES AMOUNTS 2008

AMOUNTS 2007 ASSETS AMOUNTS

2008 AMOUNTS 2007

Equity Share capital 4,00,000 2,00,000 Building 4,50,000 3,00,000

Pref. Share capital 60,000 80,000 Machinery (NET) 30,000 50,000

15% Debentures 80,000 1,20,000 5% Investments 20,000 50,000

P&L Account 1,10,000 20,000 Sundry Debtors 20,000 60,000

Income Tax Provision 80,000 30,000 Bills Receivables 20,000 10,000

Bills Payable 30,000 10,000 Cash in hand 2,50,000 10,000

General Reserve 40,000 90,000 Misc. Expenditure A/c 10,000 70,000

PART – A: Not for Profit Organizations, Partnership Firms and Company

Accounts

Q.1.How is sale of an old asset treated in case of not for profit organization? (1 Marks)

Q.2.If a partnership deed is absent, how are the profits and losses of the firm are divided among the

partners? (1 Marks)

Q.3.What is meant by reconstitution of a partnership firm? (1 Marks)

Q.4.Name the methods for calculating deceased partners share of profits. (1 Marks)

Q.5.What is meant by simple or naked debentures? (1 Marks)

Q.6.From the following extracts of Receipt Payment Account and additional information Compute

the amount of income from subscription and show as how they would appear in the income and

expenditure account for the year ending 31st March 2007 and the balance sheet as on that date.

(3 Marks)

RECEIPT AND PAYMENT ACCOUNT

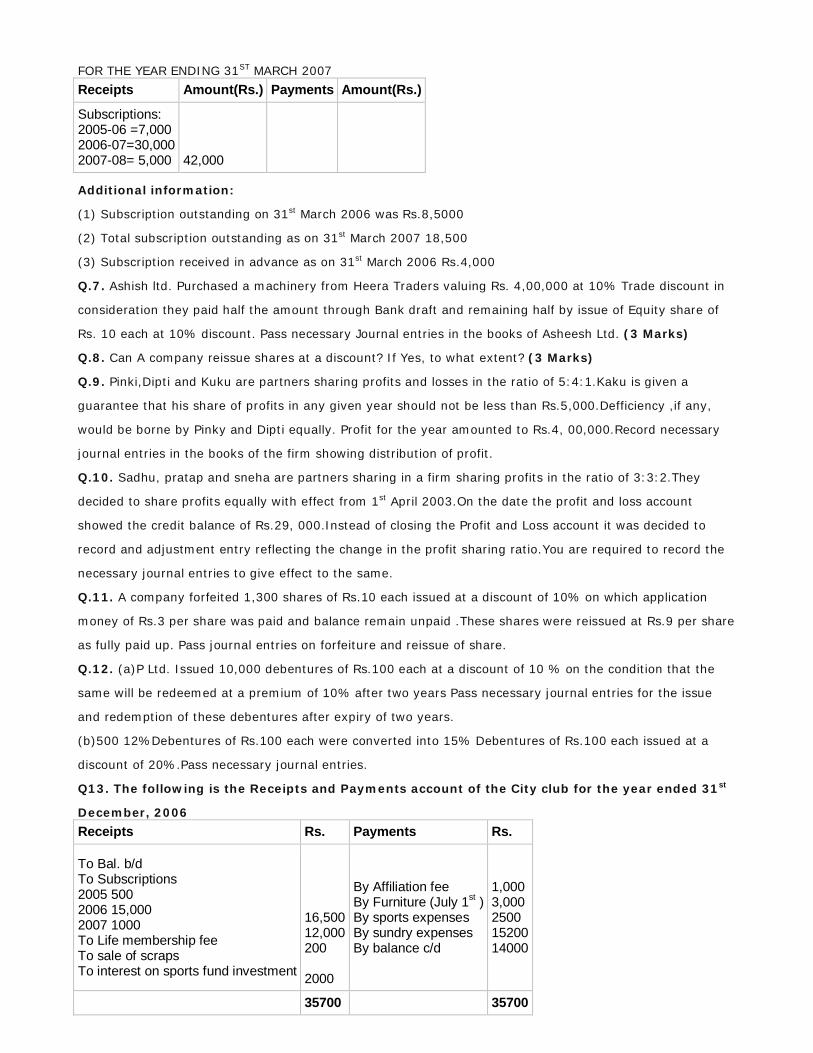

FOR THE YEAR ENDING 31ST MARCH 2007

Receipts Amount(Rs.) Payments Amount(Rs.)

Subscriptions: 2005-06 =7,000 2006-07=30,000 2007-08= 5,000

42,000

Additional information:

(1) Subscription outstanding on 31st March 2006 was Rs.8,5000

(2) Total subscription outstanding as on 31st March 2007 18,500

(3) Subscription received in advance as on 31st March 2006 Rs.4,000

Q.7. Ashish ltd. Purchased a machinery from Heera Traders valuing Rs. 4,00,000 at 10% Trade discount in

consideration they paid half the amount through Bank draft and remaining half by issue of Equity share of

Rs. 10 each at 10% discount. Pass necessary Journal entries in the books of Asheesh Ltd. (3 Marks)

Q.8. Can A company reissue shares at a discount? If Yes, to what extent? (3 Marks)

Q.9. Pinki,Dipti and Kuku are partners sharing profits and losses in the ratio of 5:4:1.Kaku is given a

guarantee that his share of profits in any given year should not be less than Rs.5,000.Defficiency ,if any,

would be borne by Pinky and Dipti equally. Profit for the year amounted to Rs.4, 00,000.Record necessary

journal entries in the books of the firm showing distribution of profit.

Q.10. Sadhu, pratap and sneha are partners sharing in a firm sharing profits in the ratio of 3:3:2.They

decided to share profits equally with effect from 1st April 2003.On the date the profit and loss account

showed the credit balance of Rs.29, 000.Instead of closing the Profit and Loss account it was decided to

record and adjustment entry reflecting the change in the profit sharing ratio.You are required to record the

necessary journal entries to give effect to the same.

Q.11. A company forfeited 1,300 shares of Rs.10 each issued at a discount of 10% on which application

money of Rs.3 per share was paid and balance remain unpaid .These shares were reissued at Rs.9 per share

as fully paid up. Pass journal entries on forfeiture and reissue of share.

Q.12. (a)P Ltd. Issued 10,000 debentures of Rs.100 each at a discount of 10 % on the condition that the

same will be redeemed at a premium of 10% after two years Pass necessary journal entries for the issue

and redemption of these debentures after expiry of two years.

(b)500 12%Debentures of Rs.100 each were converted into 15% Debentures of Rs.100 each issued at a

discount of 20%.Pass necessary journal entries.

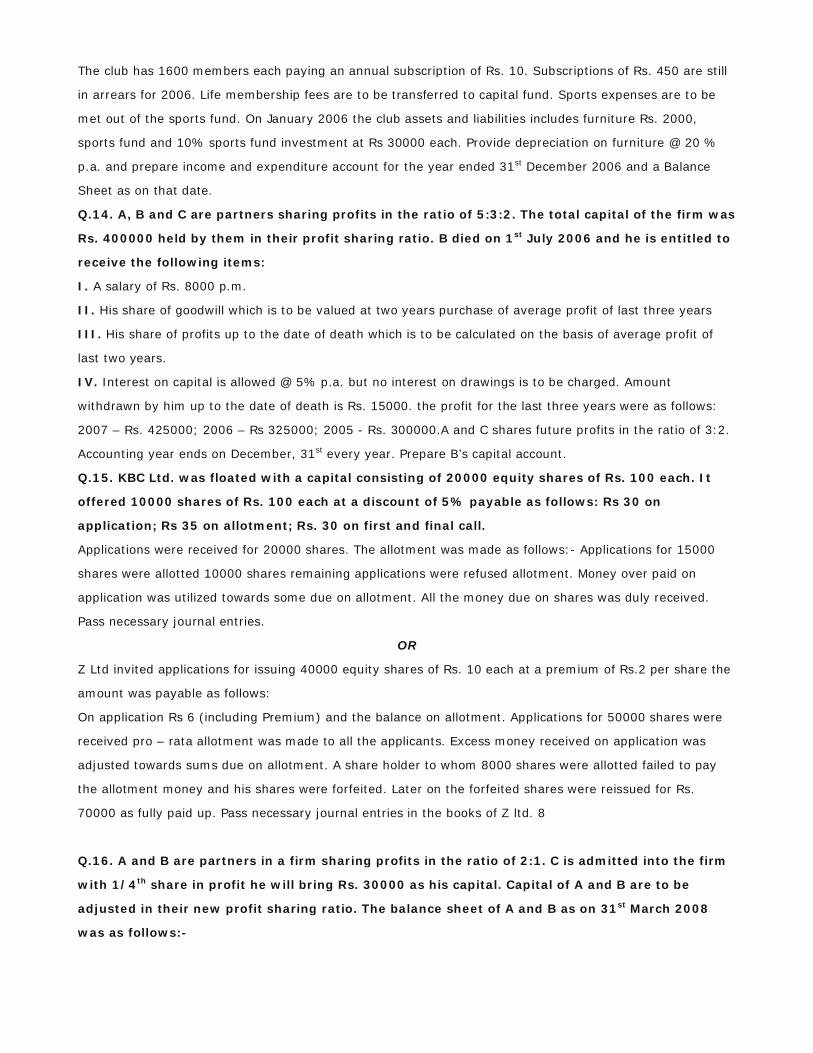

Q13. The following is the Receipts and Payments account of the City club for the year ended 31st

December, 2006

Receipts Rs. Payments Rs.

To Bal. b/d To Subscriptions 2005 500 2006 15,000 2007 1000 To Life membership fee To sale of scraps To interest on sports fund investment

16,500 12,000 200 2000

By Affiliation fee By Furniture (July 1st ) By sports expenses By sundry expenses By balance c/d

1,000 3,000 2500 15200 14000

35700 35700

The club has 1600 members each paying an annual subscription of Rs. 10. Subscriptions of Rs. 450 are still

in arrears for 2006. Life membership fees are to be transferred to capital fund. Sports expenses are to be

met out of the sports fund. On January 2006 the club assets and liabilities includes furniture Rs. 2000,

sports fund and 10% sports fund investment at Rs 30000 each. Provide depreciation on furniture @ 20 %

p.a. and prepare income and expenditure account for the year ended 31st December 2006 and a Balance

Sheet as on that date.

Q.14. A, B and C are partners sharing profits in the ratio of 5:3:2. The total capital of the firm was

Rs. 400000 held by them in their profit sharing ratio. B died on 1st July 2006 and he is entitled to

receive the following items:

I. A salary of Rs. 8000 p.m.

II. His share of goodwill which is to be valued at two years purchase of average profit of last three years

III. His share of profits up to the date of death which is to be calculated on the basis of average profit of

last two years.

IV. Interest on capital is allowed @ 5% p.a. but no interest on drawings is to be charged. Amount

withdrawn by him up to the date of death is Rs. 15000. the profit for the last three years were as follows:

2007 – Rs. 425000; 2006 – Rs 325000; 2005 - Rs. 300000.A and C shares future profits in the ratio of 3:2.

Accounting year ends on December, 31st every year. Prepare B’s capital account.

Q.15. KBC Ltd. was floated with a capital consisting of 20000 equity shares of Rs. 100 each. It

offered 10000 shares of Rs. 100 each at a discount of 5% payable as follows: Rs 30 on

application; Rs 35 on allotment; Rs. 30 on first and final call.

Applications were received for 20000 shares. The allotment was made as follows:- Applications for 15000

shares were allotted 10000 shares remaining applications were refused allotment. Money over paid on

application was utilized towards some due on allotment. All the money due on shares was duly received.

Pass necessary journal entries.

OR

Z Ltd invited applications for issuing 40000 equity shares of Rs. 10 each at a premium of Rs.2 per share the

amount was payable as follows:

On application Rs 6 (including Premium) and the balance on allotment. Applications for 50000 shares were

received pro – rata allotment was made to all the applicants. Excess money received on application was

adjusted towards sums due on allotment. A share holder to whom 8000 shares were allotted failed to pay

the allotment money and his shares were forfeited. Later on the forfeited shares were reissued for Rs.

70000 as fully paid up. Pass necessary journal entries in the books of Z ltd. 8

Q.16. A and B are partners in a firm sharing profits in the ratio of 2:1. C is admitted into the firm

with 1/4th share in profit he will bring Rs. 30000 as his capital. Capital of A and B are to be

adjusted in their new profit sharing ratio. The balance sheet of A and B as on 31st March 2008

was as follows:-

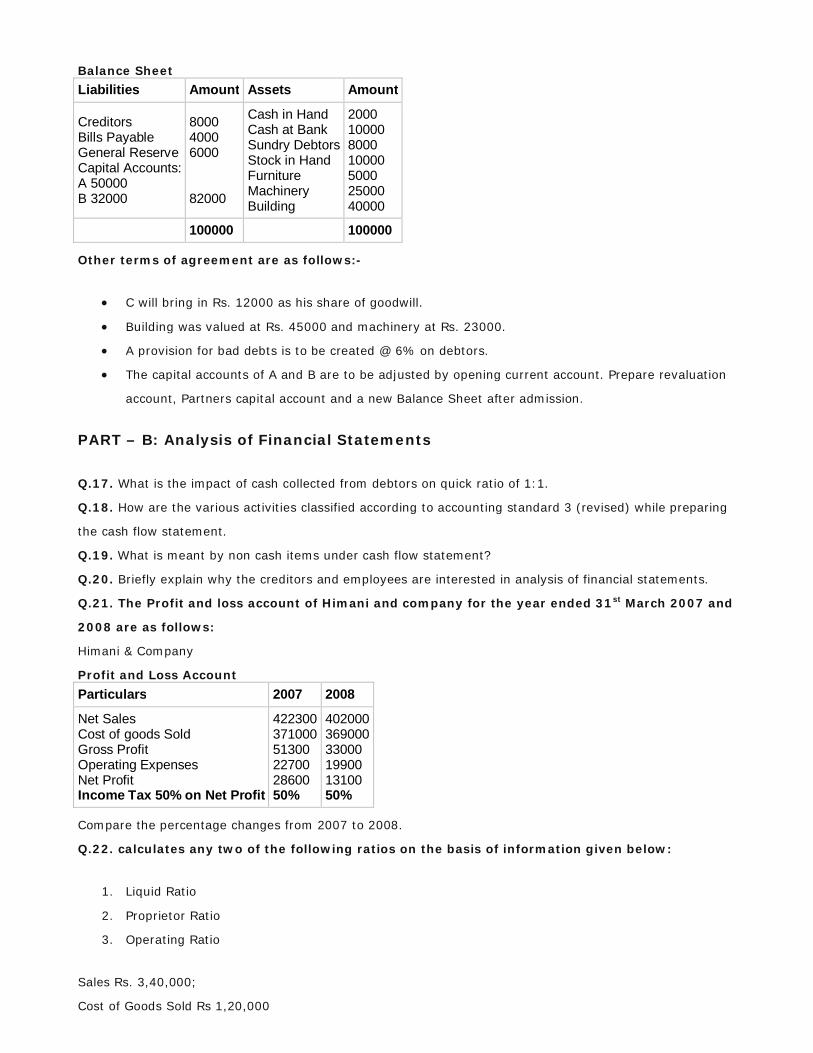

Balance Sheet

Liabilities Amount Assets Amount

Creditors Bills Payable General Reserve Capital Accounts: A 50000 B 32000

8000 4000 6000 82000

Cash in Hand Cash at Bank Sundry Debtors Stock in Hand Furniture Machinery Building

2000 10000 8000 10000 5000 25000 40000

100000 100000

Other terms of agreement are as follows:-

C will bring in Rs. 12000 as his share of goodwill.

Building was valued at Rs. 45000 and machinery at Rs. 23000.

A provision for bad debts is to be created @ 6% on debtors.

The capital accounts of A and B are to be adjusted by opening current account. Prepare revaluation

account, Partners capital account and a new Balance Sheet after admission.

PART – B: Analysis of Financial Statements

Q.17. What is the impact of cash collected from debtors on quick ratio of 1:1.

Q.18. How are the various activities classified according to accounting standard 3 (revised) while preparing

the cash flow statement.

Q.19. What is meant by non cash items under cash flow statement?

Q.20. Briefly explain why the creditors and employees are interested in analysis of financial statements.

Q.21. The Profit and loss account of Himani and company for the year ended 31st March 2007 and

2008 are as follows:

Himani & Company

Profit and Loss Account

Particulars 2007 2008

Net Sales Cost of goods Sold Gross Profit Operating Expenses Net Profit Income Tax 50% on Net Profit

422300 371000 51300 22700 28600 50%

402000 369000 33000 19900 13100 50%

Compare the percentage changes from 2007 to 2008.

Q.22. calculates any two of the following ratios on the basis of information given below:

1. Liquid Ratio

2. Proprietor Ratio

3. Operating Ratio

Sales Rs. 3,40,000;

Cost of Goods Sold Rs 1,20,000

Selling Expenses Rs. 80,000

Administrative Expenses Rs 40,000

Current assets Rs 1,50,000

Current Liabilities Rs 1,05,000

Closing stock Rs 10,000

Fixed Assets Rs 2,80,000

Equity Share Capital Rs. 2,75,000

General Reserve Rs 2,00,000

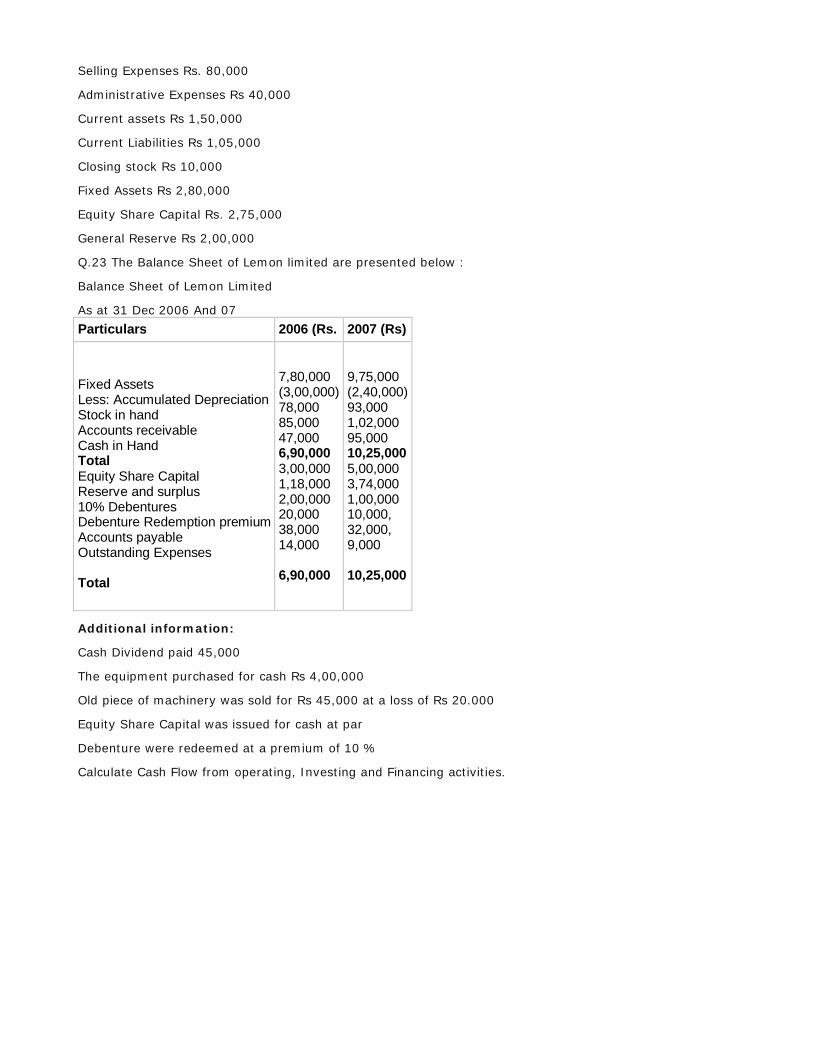

Q.23 The Balance Sheet of Lemon limited are presented below :

Balance Sheet of Lemon Limited

As at 31 Dec 2006 And 07

Particulars 2006 (Rs. 2007 (Rs)

Fixed Assets Less: Accumulated Depreciation Stock in hand Accounts receivable Cash in Hand Total Equity Share Capital Reserve and surplus 10% Debentures Debenture Redemption premium Accounts payable Outstanding Expenses Total

7,80,000 (3,00,000) 78,000 85,000 47,000 6,90,000 3,00,000 1,18,000 2,00,000 20,000 38,000 14,000 6,90,000

9,75,000 (2,40,000) 93,000 1,02,000 95,000 10,25,000 5,00,000 3,74,000 1,00,000 10,000, 32,000, 9,000 10,25,000

Additional information:

Cash Dividend paid 45,000

The equipment purchased for cash Rs 4,00,000

Old piece of machinery was sold for Rs 45,000 at a loss of Rs 20.000

Equity Share Capital was issued for cash at par

Debenture were redeemed at a premium of 10 %

Calculate Cash Flow from operating, Investing and Financing activities.

SAMPLE PAPER-III

ACCOUNTANCY

PART-A : Accounting for Not for profit Organisation, Partnership and Company

Q.1. How do you treat amount received from individual as per will in the final Accounts of Not For Profit

Organisation. (1 Marks)

Q.2. A partners becomes insolvent,what will be the faith of the firm? (1 Marks)

Q.3.A and B are partners with capital of Rs 200000 and Rs150000.As per the deed they are entitled for

interest on capital @ 10%.During the year the firm made a profit of Rs 10000 before appropriation. What is

the amount of interest to be allowed to the partners? (1 Marks)

Q.4.What is the utility of Debenture Redemption Reserve? (1 Marks)

Q.5. If a partner wants to retire and balance sheet shows a debit balance of Profit and loss Account of Rs

12000,how it should be treated? (1 Marks)

Q.6. Show the following items in the final Account of Not For Profit Organisation. (3 Marks)

Particulars 31/3/07 31/3/08

Outstanding Locker Rent 2650 3720

Advance Rent Received 900 1300

Locker Rent Received during the year 2007-08 is Rs 9000

Q.7. Sony Ltd reissued 1200 shares out of 2000 forfeited shares at Rs 8 as Rs 9 paid up. These shares were

forfeited for non payment of Final call of Rs 2 .Pass Journal entries to Reissue the shares and calculate the

amount to be transfer to the capital Reserve. (3 Marks)

Q.8. JK Ltd Purchased machine worth Rs 320000 from Amrit Ltd. Payment was made as Rs 50000 cash and

remaining amount by issue of equity shared of the face value of Rs 100 each fully paid at an issue price of

Rs 90 each. Pass journal entries in the books of JK Ltd for the above transaction. (3 Marks)

Q.9. A and B are the partners sharing profits in the ratio of 7:5. They agree to admit C their manager, into

partnership who is to get 1/6th share in the business which he acquires 1/24th from A and 1/8th from B.C

brings in Rs 10000 for his share of capital and required cash for Goodwill. On C ‘s admission goodwill of the

firm was valued at Rs 18000.The profit for thr first year after C’s admission was Rs 30000.Give journal

entries in connection to C’s admission and distribution of the profit among partners. (4 Marks)

Q.10. Rolic Ltd redeemed 1000, 15% debentures of Rs 100 each by converting them into 12% Preference

shares of Rs 50 each at 25% premium and 500 15% debentures were purchasing from open market at Rs

97 for immediate cancellation. Pass Journal entries. (4 Marks)

Q.11. M, N and O are partners in a firm having fixed capital of Rs. 1,50,000; Rs. 75,000 and Rs. 60,000

respectively sharing 5 : 3 : 2. The rate of interest on capital was agreed at 10% per annum but was wrongly

credited to them as 12% p.a. Give the necessary adjustment entry to adjust then balances of partner’s

capital account (4 Marks)

Q.12. Delta Ltd issued Rs 2000000, 8% debentures on 1st April 2008 of the face value Rs 100 at Rs 98

redeemable after 5 years at Rs 104.Iterest paid on these debentures on 30th September and 31st March

every year. Income tax deducted is 20%of the amount of interest. Pass journal entries in the books of the

company for 2008-09 (6 Marks)

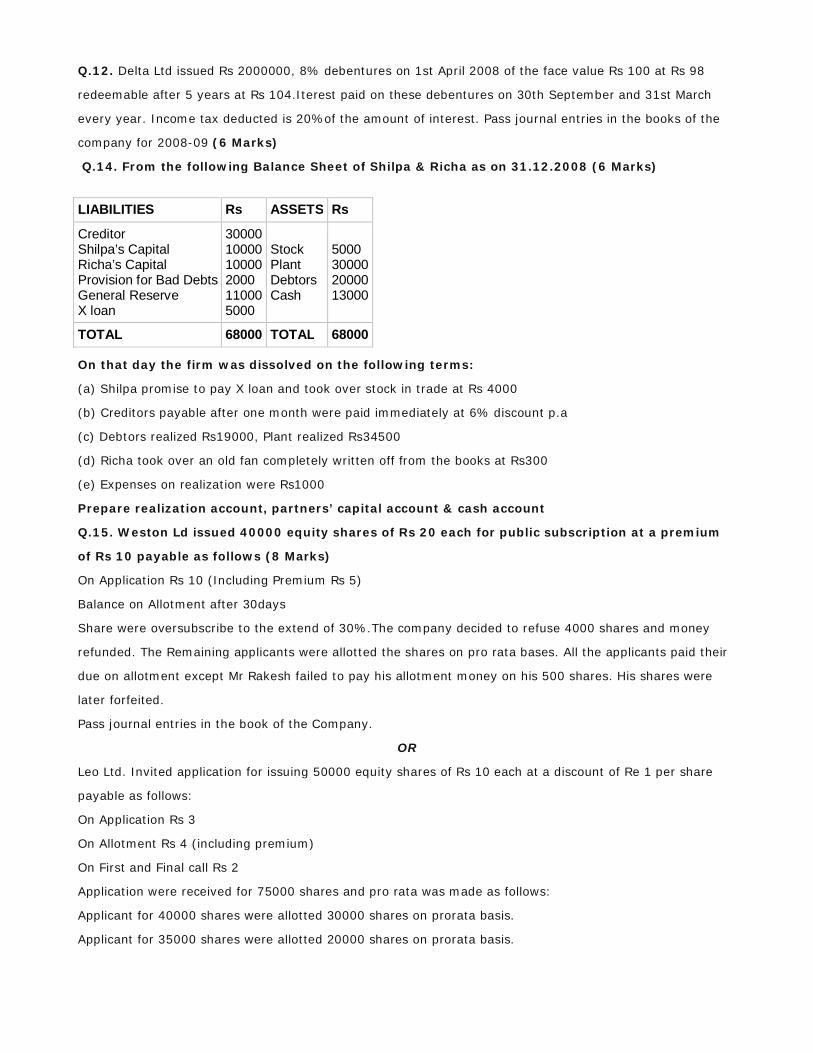

Q.14. From the following Balance Sheet of Shilpa & Richa as on 31.12.2008 (6 Marks)

LIABILITIES Rs ASSETS Rs

Creditor Shilpa’s Capital Richa’s Capital Provision for Bad Debts General Reserve X loan

30000 10000 10000 2000 11000 5000

Stock Plant Debtors Cash

5000 30000 20000 13000

TOTAL 68000 TOTAL 68000

On that day the firm was dissolved on the following terms:

(a) Shilpa promise to pay X loan and took over stock in trade at Rs 4000

(b) Creditors payable after one month were paid immediately at 6% discount p.a

(c) Debtors realized Rs19000, Plant realized Rs34500

(d) Richa took over an old fan completely written off from the books at Rs300

(e) Expenses on realization were Rs1000

Prepare realization account, partners’ capital account & cash account

Q.15. Weston Ld issued 40000 equity shares of Rs 20 each for public subscription at a premium

of Rs 10 payable as follows (8 Marks)

On Application Rs 10 (Including Premium Rs 5)

Balance on Allotment after 30days

Share were oversubscribe to the extend of 30%.The company decided to refuse 4000 shares and money

refunded. The Remaining applicants were allotted the shares on pro rata bases. All the applicants paid their

due on allotment except Mr Rakesh failed to pay his allotment money on his 500 shares. His shares were

later forfeited.

Pass journal entries in the book of the Company.

OR

Leo Ltd. Invited application for issuing 50000 equity shares of Rs 10 each at a discount of Re 1 per share

payable as follows:

On Application Rs 3

On Allotment Rs 4 (including premium)

On First and Final call Rs 2

Application were received for 75000 shares and pro rata was made as follows:

Applicant for 40000 shares were allotted 30000 shares on prorata basis.

Applicant for 35000 shares were allotted 20000 shares on prorata basis.

M to whom 1500 shares were allotted out of the group applying for 40000 shares failed to pay allotment and

P to whom 600 shares were allotted under the group applying for 35000 shares paid his entire due on

allotment. However M paid his due along with his Call money.

Pass journal entries in the books of the company for the above transactions

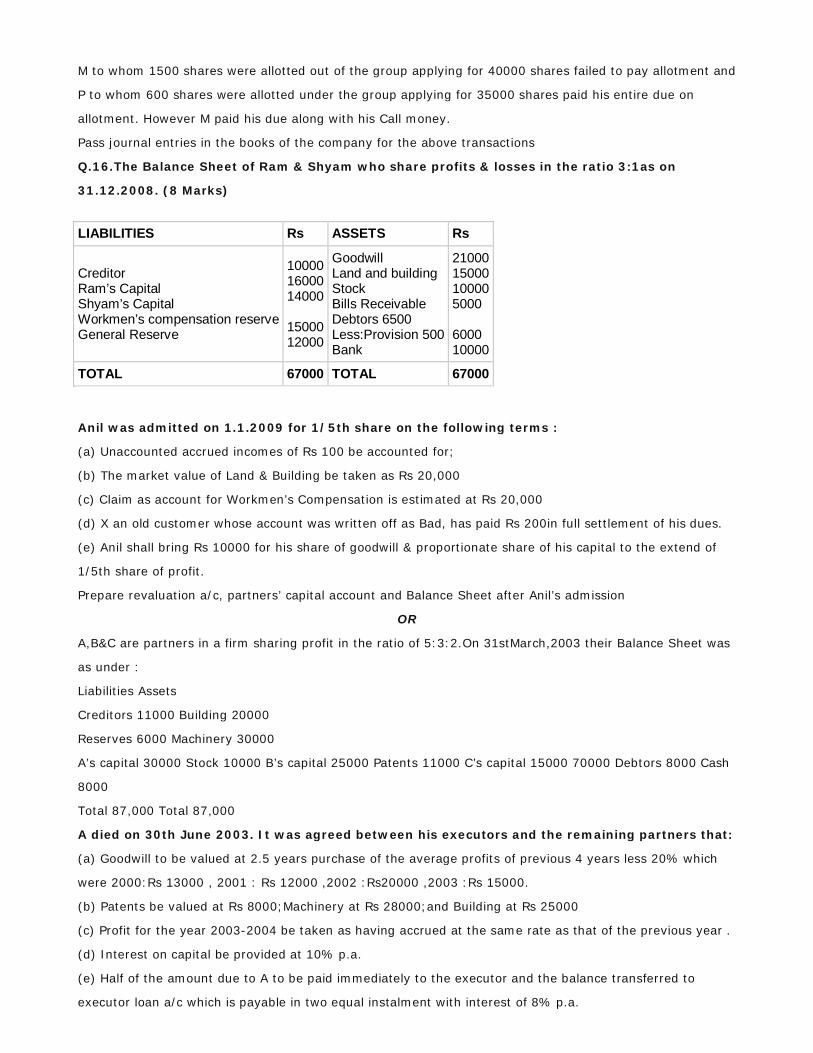

Q.16.The Balance Sheet of Ram & Shyam who share profits & losses in the ratio 3:1as on

31.12.2008. (8 Marks)

LIABILITIES Rs ASSETS Rs

Creditor Ram’s Capital Shyam’s Capital Workmen’s compensation reserve General Reserve

10000 16000 14000 15000 12000

Goodwill Land and building Stock Bills Receivable Debtors 6500 Less:Provision 500 Bank

21000 15000 10000 5000 6000 10000

TOTAL 67000 TOTAL 67000

Anil was admitted on 1.1.2009 for 1/5th share on the following terms :

(a) Unaccounted accrued incomes of Rs 100 be accounted for;

(b) The market value of Land & Building be taken as Rs 20,000

(c) Claim as account for Workmen’s Compensation is estimated at Rs 20,000

(d) X an old customer whose account was written off as Bad, has paid Rs 200in full settlement of his dues.

(e) Anil shall bring Rs 10000 for his share of goodwill & proportionate share of his capital to the extend of

1/5th share of profit.

Prepare revaluation a/c, partners’ capital account and Balance Sheet after Anil’s admission

OR

A,B&C are partners in a firm sharing profit in the ratio of 5:3:2.On 31stMarch,2003 their Balance Sheet was

as under :

Liabilities Assets

Creditors 11000 Building 20000

Reserves 6000 Machinery 30000

A’s capital 30000 Stock 10000 B’s capital 25000 Patents 11000 C’s capital 15000 70000 Debtors 8000 Cash

8000

Total 87,000 Total 87,000

A died on 30th June 2003. It was agreed between his executors and the remaining partners that:

(a) Goodwill to be valued at 2.5 years purchase of the average profits of previous 4 years less 20% which

were 2000:Rs 13000 , 2001 : Rs 12000 ,2002 :Rs20000 ,2003 :Rs 15000.

(b) Patents be valued at Rs 8000;Machinery at Rs 28000;and Building at Rs 25000

(c) Profit for the year 2003-2004 be taken as having accrued at the same rate as that of the previous year .

(d) Interest on capital be provided at 10% p.a.

(e) Half of the amount due to A to be paid immediately to the executor and the balance transferred to

executor loan a/c which is payable in two equal instalment with interest of 8% p.a.

Prepare A’s capital a/c , A’s executor a/c and A’s executor a/c Loan Account till loan is paid.

PART-B :ANALYSIS OF FINANCIAL STATEMENT

Q.17. How will you classify Loans given by Tata Finance Company in its Cash Flow Statement. (1 Marks)

Q.18. Give two example of significant non cash transaction. (1 Marks)

Q.19. The market Price of shares of HCCL was Rs 36 per share. If its Price Earning Ratio is 8 times ,

Calculate the EPS of the company. (1 Marks)

Q.20. Explain the advantages of Analysis of Financial Statement. (3 Marks)

Q.21. Prepare the Common Size Income Statement from the following information. (4 Marks)

Particular 31st March 2006 31st March 2007

Gross Sales Sales Return Cost of Goods Sold Operating Expenses Income Tax Rate

106000 6000 70% of Sales 8000 50%

110000 10000 74.8% of sales 9800 50%

Q.22. a)Cash sale of a company are 1/3rd oft the credit sales. Stock Turnover Ratio is 5 times.

Closing stock is Rs 8000 more than the opening Stock and Closing debtors are 2/3rd of opening

debtors. Closing Debtors are Rs 4000 and Opening Stock was Rs 60000.Gross Profit is 20% of

Sales. Calculate Debtors Turn over Ratio.

b) Calculate Debt Equity ratio from the following information: (4 Marks)

Total Assets Rs 1500000

Current Liabilities Rs 600000

Total Debts Rs 1200000 Q.1. What are the features of Receipts and Payments Account? (1 Marks)

Q.2. What is meant by Guarantee of profit to a partner? (1 Marks)

Q.3. Mention any two provisions of the Partnership Act, in the Absence of Partnership deed?(1 Marks)

Q.4. Why is P & L appropriation A/c prepared by partnership firm? (1 Marks)

Q.5. What do you mean by limited liability? (1 Marks)

Q.6. From the following informations calculate the amount of subscriptions for the year 2008-09.

(3 Marks)

Rs.

subscriptions received during the year 90000

subscriptions outstanding 31 March 2008 20000

subscriptions outstanding 31 March 2009 20000

subscriptions received in advance on 31 March 2008 20000

subscriptions received in advance on 31 March 2009 20000

subscription of Rs. 5000 are still in arrears for the year 2007-08.

Q.7. X limited forfeited 100 shares of Rs. 10 each, Rs. 6 called up, issued at a discount of 10% to Mahesh

on which he had paid Rs. 2 per share. Out of these 80 shares were reissued at Rs. 6/- per share to Suresh.

Rs. 8 paid up. (3 Marks)

Q.8. B Ltd. issued 2,00,000 shares of rs. 10 each payable as follows :

Rs. 2.50 on Application (on 1 Jan)

Rs. 2.50 on Allotment (on 1 April)

Rs. 3.00 on First Call (on 1 July)

Rs. 2.00 on Second & Final Call (on 1 Oct)

All the shares were subscribed and all the sums were duly received. Shareholder, Aditya who had 1,000

shares paid the amount of first and second calls with the allotment. Interest was paid to Mr. Aditya on 1 Oct

2009. 3

Q.9. A & B started a partnership business on 1 January, 2008. Their capital contributions were

Rs. 2,00,000 and Rs. 1,50,000 respectively. The partnership deed provided inter alias that :

(a) Interest on capitals at 10% p.a.

(b) A to get a salary of Rs. 2,000 p.m. and B Rs. 3,000 p.m.

(c) Profits are to shared in the ratio of 3:2.

The profits for the year ended 31 Dec, 2008 before making above appropriations were Rs. 2,16,000.

Interest on drawings amounted to Rs. 2,200 for A and Rs. 2,500 for B. 3

Q.10. (2 x 2)= 4

(A) A & B are partners with capitals of Rs. 18,000 and Rs. 16,000 respectively. They admit C as a partner

with 1/5 share in the profits of the firm. C brings Rs. 16,000 as his share of capital. Give Journal entries to

record goodwill.

(B) A, B & C are partners sharing profit and losses in the ratio of 6 :5 :3. They admit D into the firm. The

new partner gets 3/7th share, equally from all the three partners. Calculate new and sacrificing ratio.

Q.11. Journalise the following transactions assuming that the face value of each debenture is Rs.

100.

(i) 150 debentures issued at Rs. 95 each, repayable at Rs. 100.

(ii) 100 debentures issued at Rs. 95 each, repayable at Rs. 105.

(iii) 80 debentures issued at Rs. 100 each, repayable at Rs. 105.

(iv) 120 debentures issued at Rs. 105 each, repayable at Rs. 100. 4

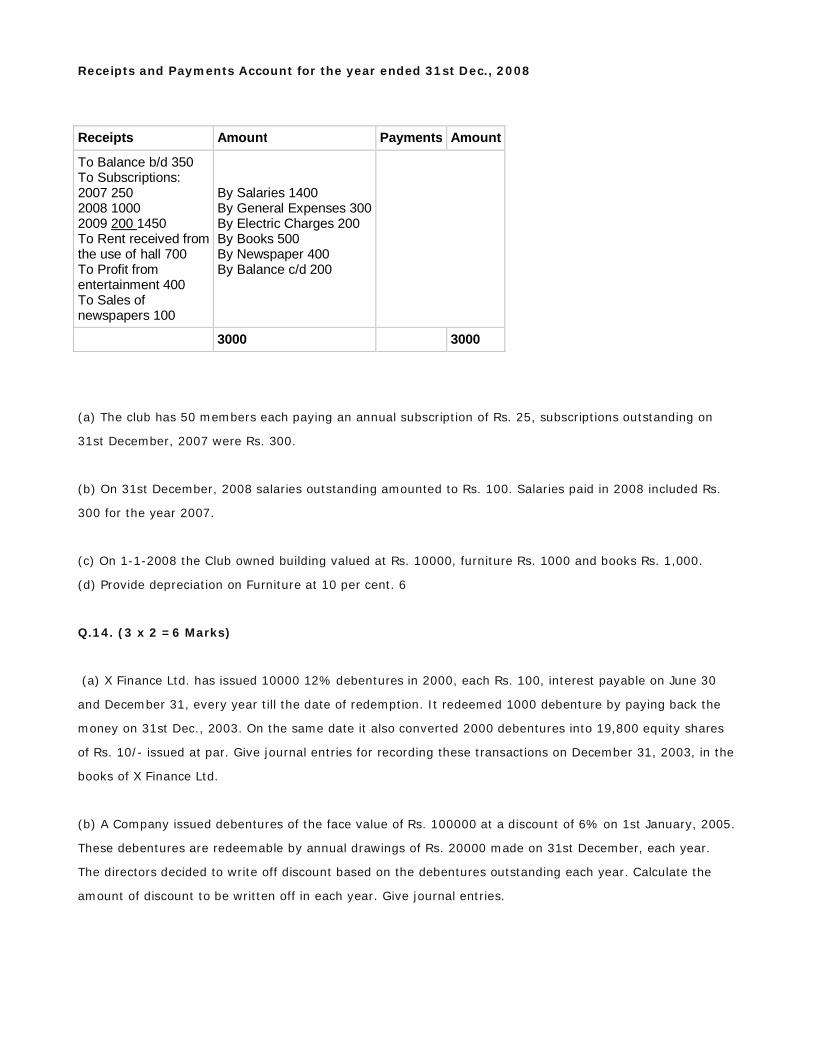

Q.12. From the following Receipts and Payments account of a club and from the information,

prepare an Income and Expenditure account for the year ended 31st December, 2004 and the

Balance Sheet as on that date:

Receipts and Payments Account for the year ended 31st Dec., 2008

Receipts Amount Payments Amount

To Balance b/d 350 To Subscriptions: 2007 250 2008 1000 2009 200 1450 To Rent received from the use of hall 700 To Profit from entertainment 400 To Sales of newspapers 100

By Salaries 1400 By General Expenses 300 By Electric Charges 200 By Books 500 By Newspaper 400 By Balance c/d 200

3000 3000

(a) The club has 50 members each paying an annual subscription of Rs. 25, subscriptions outstanding on

31st December, 2007 were Rs. 300.

(b) On 31st December, 2008 salaries outstanding amounted to Rs. 100. Salaries paid in 2008 included Rs.

300 for the year 2007.

(c) On 1-1-2008 the Club owned building valued at Rs. 10000, furniture Rs. 1000 and books Rs. 1,000.

(d) Provide depreciation on Furniture at 10 per cent. 6

Q.14. (3 x 2 =6 Marks)

(a) X Finance Ltd. has issued 10000 12% debentures in 2000, each Rs. 100, interest payable on June 30

and December 31, every year till the date of redemption. It redeemed 1000 debenture by paying back the

money on 31st Dec., 2003. On the same date it also converted 2000 debentures into 19,800 equity shares

of Rs. 10/- issued at par. Give journal entries for recording these transactions on December 31, 2003, in the

books of X Finance Ltd.

(b) A Company issued debentures of the face value of Rs. 100000 at a discount of 6% on 1st January, 2005.

These debentures are redeemable by annual drawings of Rs. 20000 made on 31st December, each year.

The directors decided to write off discount based on the debentures outstanding each year. Calculate the

amount of discount to be written off in each year. Give journal entries.

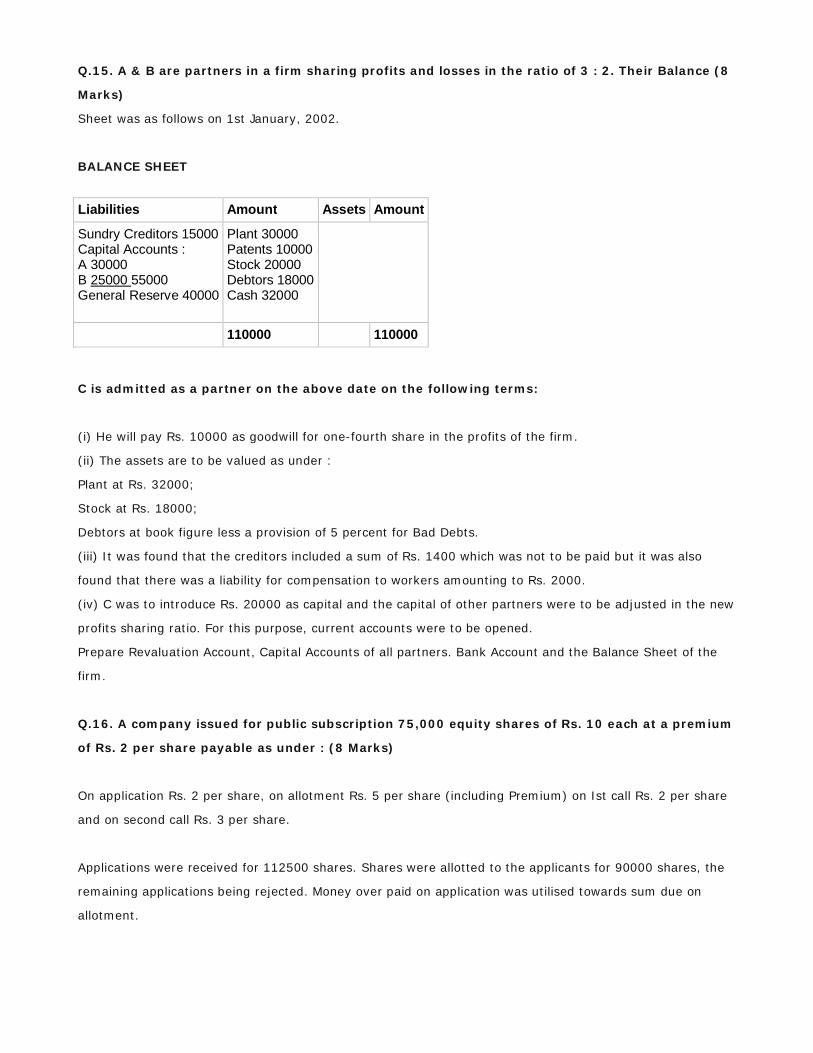

Q.15. A & B are partners in a firm sharing profits and losses in the ratio of 3 : 2. Their Balance (8

Marks)

Sheet was as follows on 1st January, 2002.

BALANCE SHEET

Liabilities Amount Assets Amount

Sundry Creditors 15000 Capital Accounts : A 30000 B 25000 55000 General Reserve 40000

Plant 30000 Patents 10000 Stock 20000 Debtors 18000 Cash 32000

110000 110000

C is admitted as a partner on the above date on the following terms:

(i) He will pay Rs. 10000 as goodwill for one-fourth share in the profits of the firm.

(ii) The assets are to be valued as under :

Plant at Rs. 32000;

Stock at Rs. 18000;

Debtors at book figure less a provision of 5 percent for Bad Debts.

(iii) It was found that the creditors included a sum of Rs. 1400 which was not to be paid but it was also

found that there was a liability for compensation to workers amounting to Rs. 2000.

(iv) C was to introduce Rs. 20000 as capital and the capital of other partners were to be adjusted in the new

profits sharing ratio. For this purpose, current accounts were to be opened.

Prepare Revaluation Account, Capital Accounts of all partners. Bank Account and the Balance Sheet of the

firm.

Q.16. A company issued for public subscription 75,000 equity shares of Rs. 10 each at a premium

of Rs. 2 per share payable as under : (8 Marks)

On application Rs. 2 per share, on allotment Rs. 5 per share (including Premium) on Ist call Rs. 2 per share

and on second call Rs. 3 per share.

Applications were received for 112500 shares. Shares were allotted to the applicants for 90000 shares, the

remaining applications being rejected. Money over paid on application was utilised towards sum due on

allotment.

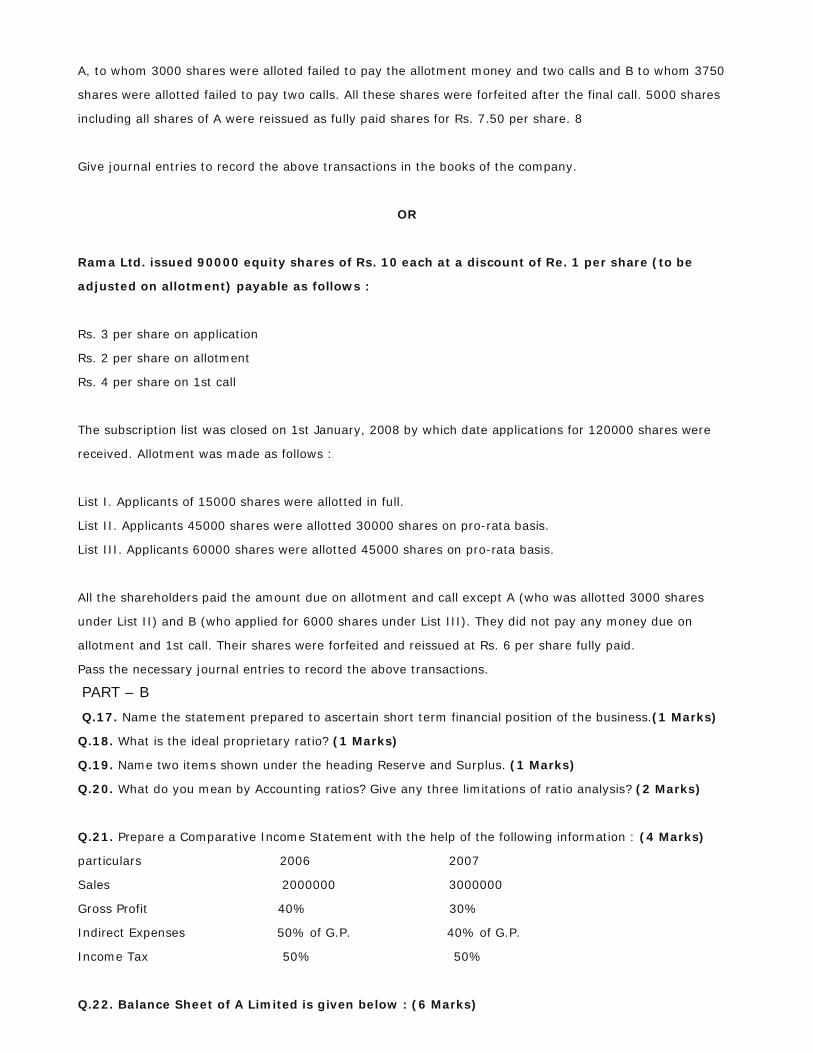

A, to whom 3000 shares were alloted failed to pay the allotment money and two calls and B to whom 3750

shares were allotted failed to pay two calls. All these shares were forfeited after the final call. 5000 shares

including all shares of A were reissued as fully paid shares for Rs. 7.50 per share. 8

Give journal entries to record the above transactions in the books of the company.

OR

Rama Ltd. issued 90000 equity shares of Rs. 10 each at a discount of Re. 1 per share (to be

adjusted on allotment) payable as follows :

Rs. 3 per share on application

Rs. 2 per share on allotment

Rs. 4 per share on 1st call

The subscription list was closed on 1st January, 2008 by which date applications for 120000 shares were

received. Allotment was made as follows :

List I. Applicants of 15000 shares were allotted in full.

List II. Applicants 45000 shares were allotted 30000 shares on pro-rata basis.

List III. Applicants 60000 shares were allotted 45000 shares on pro-rata basis.

All the shareholders paid the amount due on allotment and call except A (who was allotted 3000 shares

under List II) and B (who applied for 6000 shares under List III). They did not pay any money due on

allotment and 1st call. Their shares were forfeited and reissued at Rs. 6 per share fully paid.

Pass the necessary journal entries to record the above transactions.

PART – B

Q.17. Name the statement prepared to ascertain short term financial position of the business.(1 Marks)

Q.18. What is the ideal proprietary ratio? (1 Marks)

Q.19. Name two items shown under the heading Reserve and Surplus. (1 Marks)

Q.20. What do you mean by Accounting ratios? Give any three limitations of ratio analysis? (2 Marks)

Q.21. Prepare a Comparative Income Statement with the help of the following information : (4 Marks)

particulars 2006 2007

Sales 2000000 3000000

Gross Profit 40% 30%

Indirect Expenses 50% of G.P. 40% of G.P.

Income Tax 50% 50%

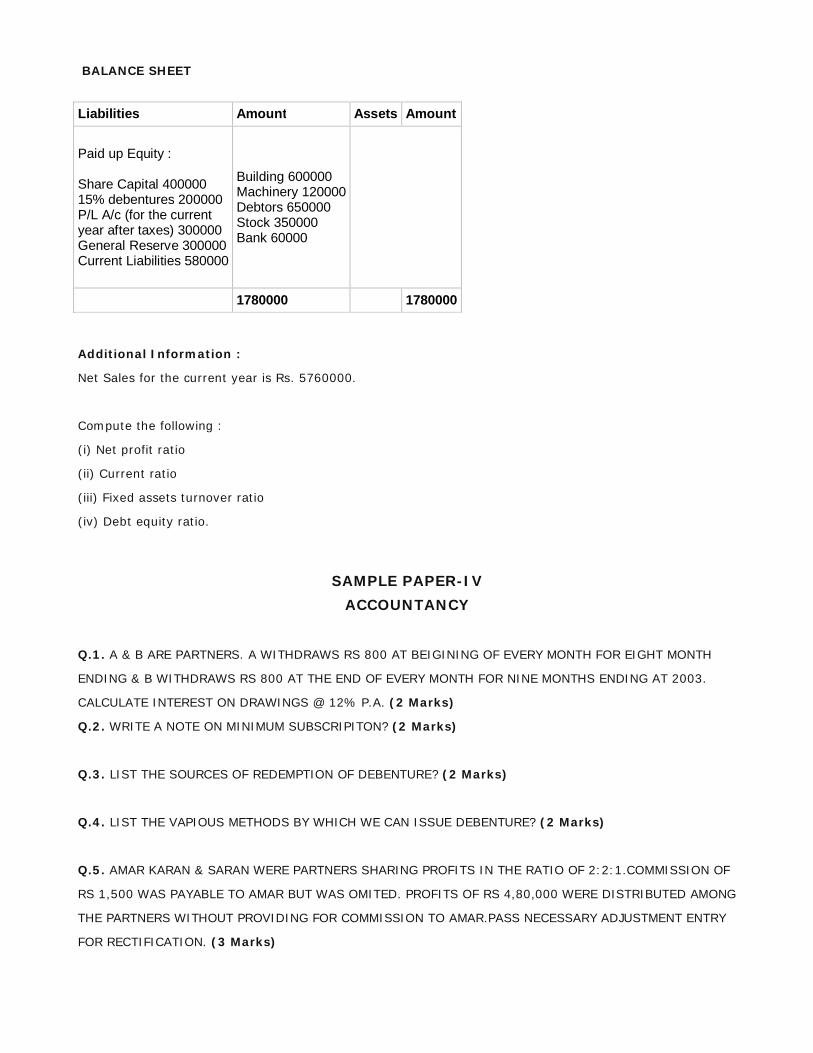

Q.22. Balance Sheet of A Limited is given below : (6 Marks)

BALANCE SHEET

Liabilities Amount Assets Amount

Paid up Equity : Share Capital 400000 15% debentures 200000 P/L A/c (for the current year after taxes) 300000 General Reserve 300000 Current Liabilities 580000

Building 600000 Machinery 120000 Debtors 650000 Stock 350000 Bank 60000

1780000 1780000

Additional Information :

Net Sales for the current year is Rs. 5760000.

Compute the following :

(i) Net profit ratio

(ii) Current ratio

(iii) Fixed assets turnover ratio

(iv) Debt equity ratio.

SAMPLE PAPER-IV

ACCOUNTANCY

Q.1. A & B ARE PARTNERS. A WITHDRAWS RS 800 AT BEIGINING OF EVERY MONTH FOR EIGHT MONTH

ENDING & B WITHDRAWS RS 800 AT THE END OF EVERY MONTH FOR NINE MONTHS ENDING AT 2003.

CALCULATE INTEREST ON DRAWINGS @ 12% P.A. (2 Marks)

Q.2. WRITE A NOTE ON MINIMUM SUBSCRIPITON? (2 Marks)

Q.3. LIST THE SOURCES OF REDEMPTION OF DEBENTURE? (2 Marks)

Q.4. LIST THE VAPIOUS METHODS BY WHICH WE CAN ISSUE DEBENTURE? (2 Marks)

Q.5. AMAR KARAN & SARAN WERE PARTNERS SHARING PROFITS IN THE RATIO OF 2:2:1.COMMISSION OF

RS 1,500 WAS PAYABLE TO AMAR BUT WAS OMITED. PROFITS OF RS 4,80,000 WERE DISTRIBUTED AMONG

THE PARTNERS WITHOUT PROVIDING FOR COMMISSION TO AMAR.PASS NECESSARY ADJUSTMENT ENTRY

FOR RECTIFICATION. (3 Marks)

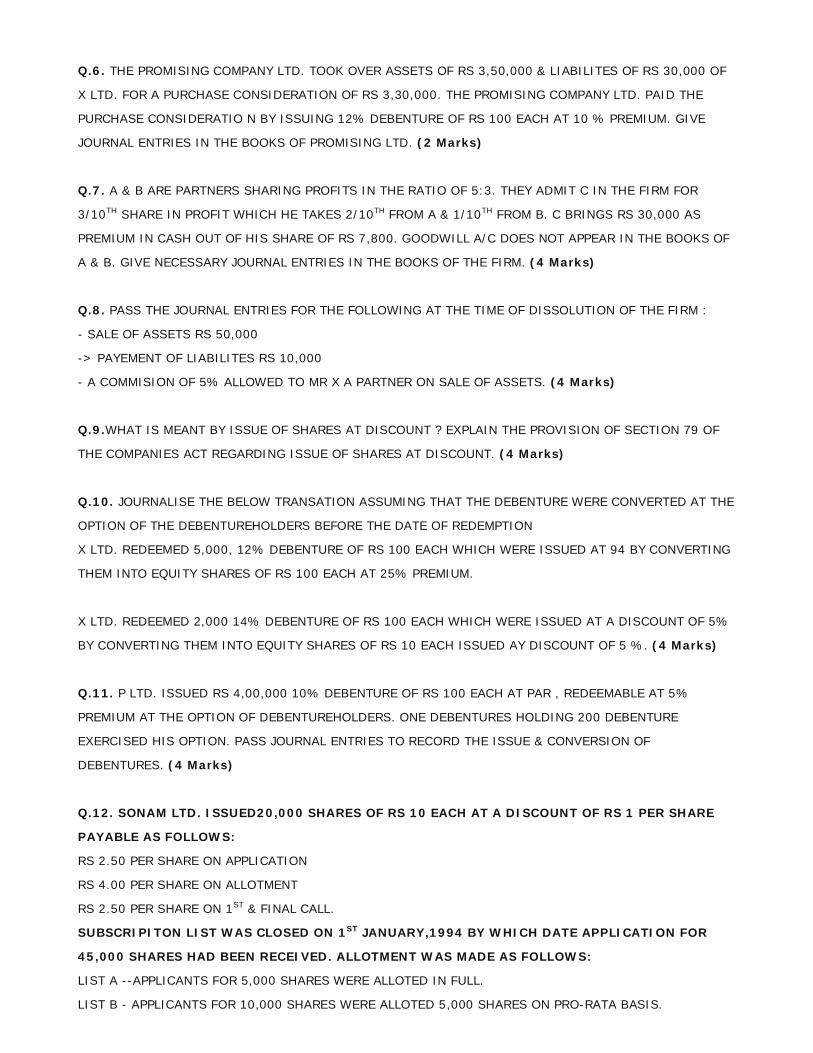

Q.6. THE PROMISING COMPANY LTD. TOOK OVER ASSETS OF RS 3,50,000 & LIABILITES OF RS 30,000 OF

X LTD. FOR A PURCHASE CONSIDERATION OF RS 3,30,000. THE PROMISING COMPANY LTD. PAID THE

PURCHASE CONSIDERATIO N BY ISSUING 12% DEBENTURE OF RS 100 EACH AT 10 % PREMIUM. GIVE

JOURNAL ENTRIES IN THE BOOKS OF PROMISING LTD. (2 Marks)

Q.7. A & B ARE PARTNERS SHARING PROFITS IN THE RATIO OF 5:3. THEY ADMIT C IN THE FIRM FOR

3/10TH SHARE IN PROFIT WHICH HE TAKES 2/10TH FROM A & 1/10TH FROM B. C BRINGS RS 30,000 AS

PREMIUM IN CASH OUT OF HIS SHARE OF RS 7,800. GOODWILL A/C DOES NOT APPEAR IN THE BOOKS OF

A & B. GIVE NECESSARY JOURNAL ENTRIES IN THE BOOKS OF THE FIRM. (4 Marks)

Q.8. PASS THE JOURNAL ENTRIES FOR THE FOLLOWING AT THE TIME OF DISSOLUTION OF THE FIRM :

- SALE OF ASSETS RS 50,000

-> PAYEMENT OF LIABILITES RS 10,000

- A COMMISION OF 5% ALLOWED TO MR X A PARTNER ON SALE OF ASSETS. (4 Marks)

Q.9.WHAT IS MEANT BY ISSUE OF SHARES AT DISCOUNT ? EXPLAIN THE PROVISION OF SECTION 79 OF

THE COMPANIES ACT REGARDING ISSUE OF SHARES AT DISCOUNT. (4 Marks)

Q.10. JOURNALISE THE BELOW TRANSATION ASSUMING THAT THE DEBENTURE WERE CONVERTED AT THE

OPTION OF THE DEBENTUREHOLDERS BEFORE THE DATE OF REDEMPTION

X LTD. REDEEMED 5,000, 12% DEBENTURE OF RS 100 EACH WHICH WERE ISSUED AT 94 BY CONVERTING

THEM INTO EQUITY SHARES OF RS 100 EACH AT 25% PREMIUM.

X LTD. REDEEMED 2,000 14% DEBENTURE OF RS 100 EACH WHICH WERE ISSUED AT A DISCOUNT OF 5%

BY CONVERTING THEM INTO EQUITY SHARES OF RS 10 EACH ISSUED AY DISCOUNT OF 5 %. (4 Marks)

Q.11. P LTD. ISSUED RS 4,00,000 10% DEBENTURE OF RS 100 EACH AT PAR , REDEEMABLE AT 5%

PREMIUM AT THE OPTION OF DEBENTUREHOLDERS. ONE DEBENTURES HOLDING 200 DEBENTURE

EXERCISED HIS OPTION. PASS JOURNAL ENTRIES TO RECORD THE ISSUE & CONVERSION OF

DEBENTURES. (4 Marks)

Q.12. SONAM LTD. ISSUED20,000 SHARES OF RS 10 EACH AT A DISCOUNT OF RS 1 PER SHARE

PAYABLE AS FOLLOWS:

RS 2.50 PER SHARE ON APPLICATION

RS 4.00 PER SHARE ON ALLOTMENT

RS 2.50 PER SHARE ON 1ST & FINAL CALL.

SUBSCRIPITON LIST WAS CLOSED ON 1ST JANUARY,1994 BY WHICH DATE APPLICATION FOR

45,000 SHARES HAD BEEN RECEIVED. ALLOTMENT WAS MADE AS FOLLOWS:

LIST A --APPLICANTS FOR 5,000 SHARES WERE ALLOTED IN FULL.

LIST B - APPLICANTS FOR 10,000 SHARES WERE ALLOTED 5,000 SHARES ON PRO-RATA BASIS.

LIST C -APPLICANTS FOR 30,000 SHARES WERE ALLOTED 10,000 SHARES ON PRO-RATA BASIS.

APPLICATION MONEY IN EXCESS OF THAT REQUIRED ON ALLOTMENT COULD BE UTILIZED FOR CALLS.

ALL THE SHAREHOLDERS PAID THE AMOUNTS DUE ON ALLOTMENT & CALLS EXCEPT Y (WHO WAS

ALLOTTED 400 SHARES UNDER LIST B ) & Z (WHO WAS ALLOTED 200 SHARES UNDER LIST C ). BOTH OF

THESE SHAREHOLDERS PAID ONLY THE APPLICATION MONEY.

THEIR SHARES WERE DULY FORFEITED & WERE RE – ISSUED AT RS 7 PER SHARE FULLY PAID. PASS THE

NECESSARY JOURNAL ENTRIES. (6 Marks)

Q.13. THE BALANCE SHEET OF J,K & L WHO WERE SHARING PROFITS IN 5:3:2,IS GIVEN BELOW

AS ON 31ST/MARCH/2003:

LIABILITES RS ASSETS RS

SUNDRY CREDITORS 78,600 LAND 1,85,000

J’S CAPITAL 5,78,800 BUILDINGS 2,87,000

K’S CAPITAL 3,47,800 PLANT&MACHINERY 3,86,000

L’S CAPITAL 2,37,900 STOCK 1,85,000

DEBTORS 92,100

CASH 1,08,000

12,43,100 12,43,100

L RETIRES ON THE ABOVE DATE & THE FOLLOWING ADJUSTMENTS IN THE VALUE OF ASSETS &

LIABILITES WERE AGREED UPON:

- LAND WAS UNDER VALUED BY RS 1,20,000;PLANT & MACHINERY OVERVALUED BY RS 35,000.

- PROVISION FOR DOUBTFUL DEBT WAS REQUIRED FOR RS 6,000.

- GOODWILL WAS VALUED AT RS 3,00,000 & WAS TO BE ADJUSTED AGAINST THE CAPITAL OF REMAINING

PARTNERS.

- L WAS PAID RS 75,000 IMMEDIATELY & THE BALANCE AMOUNT WAS TO BE TRANSFERRED TO HIS LOAN

A/C. PREPARE CASH A/C; REVALUTION A/C; CAPITAL A/C & BALANCE SHEET OF THE RECONSTITUTED FIRM

ON THE ABOVE DATE. (6 Marks)

OR

A, B&C WERE PARTNERS WHOSE BALANCE SHEET AS ON 31ST/DEC/1987 WAS AS BELOW:

LIABILITES RS ASSETS RS

CREDITORS 7,096 CASH AT BANK 6,496

GENERAL RESERVE 3,000 DEBTORS 9,000

CAPITAL: A’S-8,000 B’S-6,000 C’S-4,000

18,000

STOCK 10,600

FURNITURE 2,000

28,096 28,096

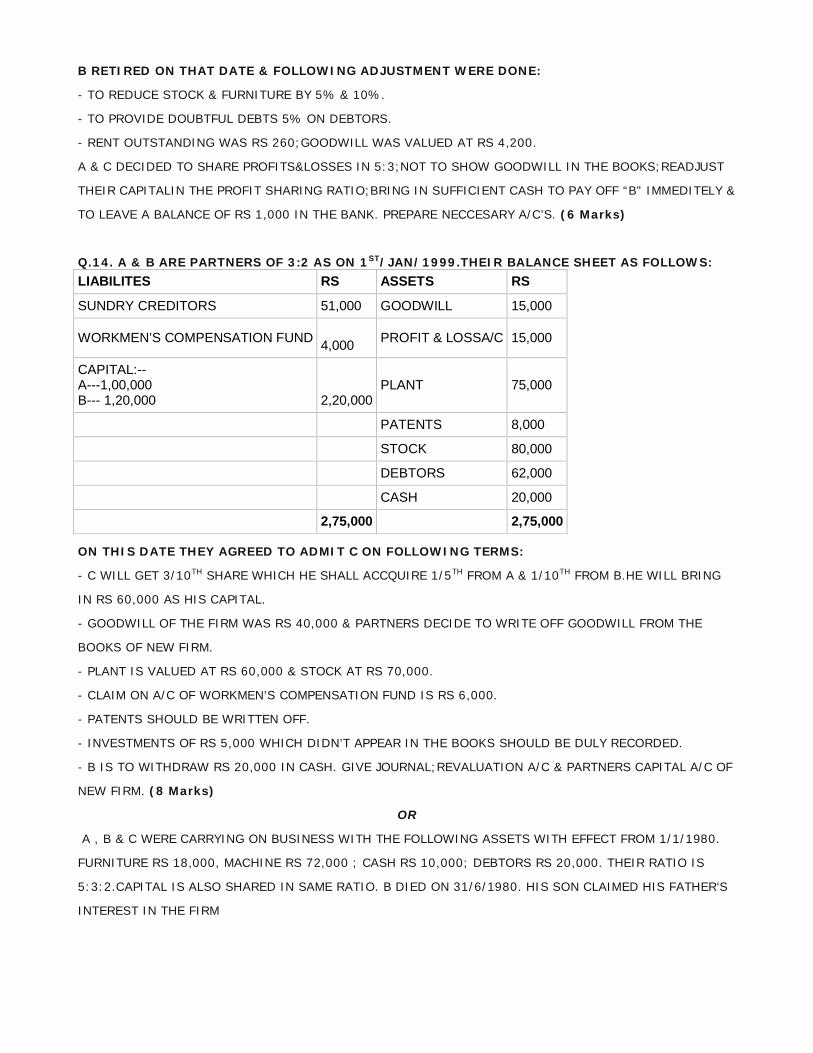

B RETIRED ON THAT DATE & FOLLOWING ADJUSTMENT WERE DONE:

- TO REDUCE STOCK & FURNITURE BY 5% & 10%.

- TO PROVIDE DOUBTFUL DEBTS 5% ON DEBTORS.

- RENT OUTSTANDING WAS RS 260;GOODWILL WAS VALUED AT RS 4,200.

A & C DECIDED TO SHARE PROFITS&LOSSES IN 5:3;NOT TO SHOW GOODWILL IN THE BOOKS;READJUST

THEIR CAPITALIN THE PROFIT SHARING RATIO;BRING IN SUFFICIENT CASH TO PAY OFF “B” IMMEDITELY &

TO LEAVE A BALANCE OF RS 1,000 IN THE BANK. PREPARE NECCESARY A/C’S. (6 Marks)

Q.14. A & B ARE PARTNERS OF 3:2 AS ON 1ST/JAN/1999.THEIR BALANCE SHEET AS FOLLOWS:

LIABILITES RS ASSETS RS

SUNDRY CREDITORS 51,000 GOODWILL 15,000

WORKMEN’S COMPENSATION FUND 4,000 PROFIT & LOSSA/C 15,000

CAPITAL:-- A---1,00,000 B--- 1,20,000

2,20,000

PLANT 75,000

PATENTS 8,000

STOCK 80,000

DEBTORS 62,000

CASH 20,000

2,75,000 2,75,000

ON THIS DATE THEY AGREED TO ADMIT C ON FOLLOWING TERMS:

- C WILL GET 3/10TH SHARE WHICH HE SHALL ACCQUIRE 1/5TH FROM A & 1/10TH FROM B.HE WILL BRING

IN RS 60,000 AS HIS CAPITAL.

- GOODWILL OF THE FIRM WAS RS 40,000 & PARTNERS DECIDE TO WRITE OFF GOODWILL FROM THE

BOOKS OF NEW FIRM.

- PLANT IS VALUED AT RS 60,000 & STOCK AT RS 70,000.

- CLAIM ON A/C OF WORKMEN’S COMPENSATION FUND IS RS 6,000.

- PATENTS SHOULD BE WRITTEN OFF.

- INVESTMENTS OF RS 5,000 WHICH DIDN’T APPEAR IN THE BOOKS SHOULD BE DULY RECORDED.

- B IS TO WITHDRAW RS 20,000 IN CASH. GIVE JOURNAL;REVALUATION A/C & PARTNERS CAPITAL A/C OF

NEW FIRM. (8 Marks)

OR

A , B & C WERE CARRYING ON BUSINESS WITH THE FOLLOWING ASSETS WITH EFFECT FROM 1/1/1980.

FURNITURE RS 18,000, MACHINE RS 72,000 ; CASH RS 10,000; DEBTORS RS 20,000. THEIR RATIO IS

5:3:2.CAPITAL IS ALSO SHARED IN SAME RATIO. B DIED ON 31/6/1980. HIS SON CLAIMED HIS FATHER‘S

INTEREST IN THE FIRM

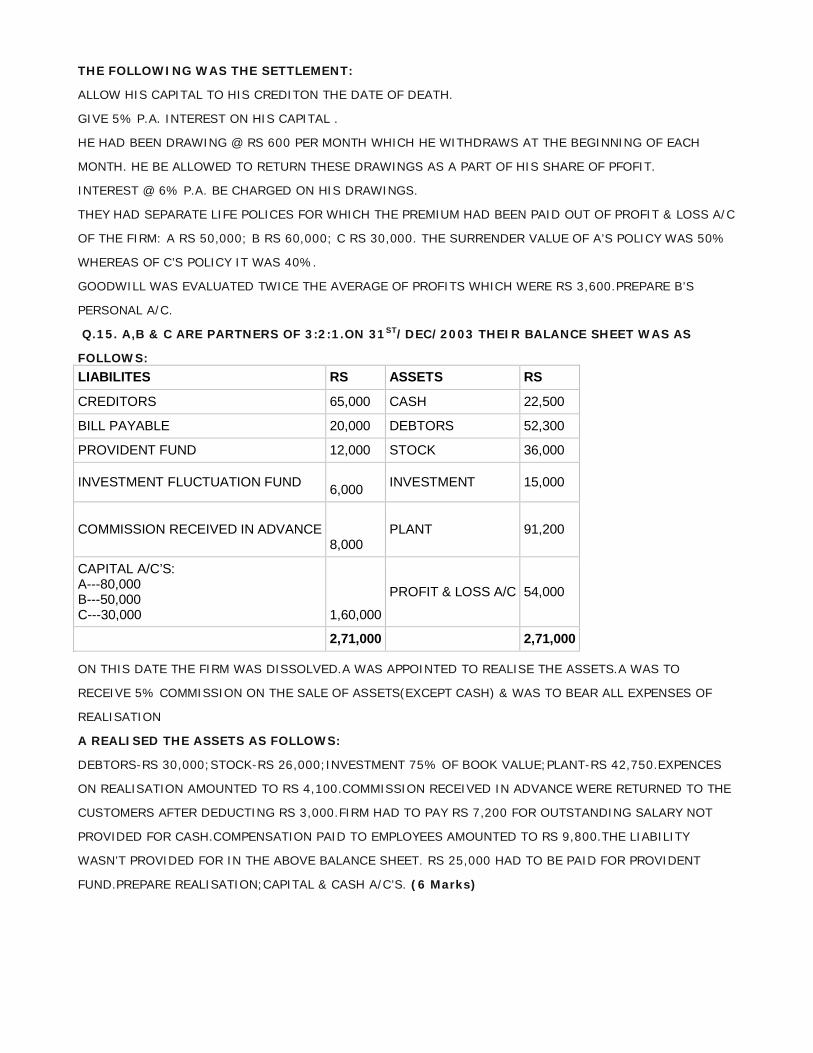

THE FOLLOWING WAS THE SETTLEMENT:

ALLOW HIS CAPITAL TO HIS CREDITON THE DATE OF DEATH.

GIVE 5% P.A. INTEREST ON HIS CAPITAL .

HE HAD BEEN DRAWING @ RS 600 PER MONTH WHICH HE WITHDRAWS AT THE BEGINNING OF EACH

MONTH. HE BE ALLOWED TO RETURN THESE DRAWINGS AS A PART OF HIS SHARE OF PFOFIT.

INTEREST @ 6% P.A. BE CHARGED ON HIS DRAWINGS.

THEY HAD SEPARATE LIFE POLICES FOR WHICH THE PREMIUM HAD BEEN PAID OUT OF PROFIT & LOSS A/C

OF THE FIRM: A RS 50,000; B RS 60,000; C RS 30,000. THE SURRENDER VALUE OF A’S POLICY WAS 50%

WHEREAS OF C’S POLICY IT WAS 40%.

GOODWILL WAS EVALUATED TWICE THE AVERAGE OF PROFITS WHICH WERE RS 3,600.PREPARE B’S

PERSONAL A/C.

Q.15. A,B & C ARE PARTNERS OF 3:2:1.ON 31ST/DEC/2003 THEIR BALANCE SHEET WAS AS

FOLLOWS:

LIABILITES RS ASSETS RS

CREDITORS 65,000 CASH 22,500

BILL PAYABLE 20,000 DEBTORS 52,300

PROVIDENT FUND 12,000 STOCK 36,000

INVESTMENT FLUCTUATION FUND 6,000 INVESTMENT 15,000

COMMISSION RECEIVED IN ADVANCE 8,000

PLANT 91,200

CAPITAL A/C’S: A---80,000 B---50,000 C---30,000

1,60,000

PROFIT & LOSS A/C 54,000

2,71,000 2,71,000

ON THIS DATE THE FIRM WAS DISSOLVED.A WAS APPOINTED TO REALISE THE ASSETS.A WAS TO

RECEIVE 5% COMMISSION ON THE SALE OF ASSETS(EXCEPT CASH) & WAS TO BEAR ALL EXPENSES OF

REALISATION

A REALISED THE ASSETS AS FOLLOWS:

DEBTORS-RS 30,000;STOCK-RS 26,000;INVESTMENT 75% OF BOOK VALUE;PLANT-RS 42,750.EXPENCES

ON REALISATION AMOUNTED TO RS 4,100.COMMISSION RECEIVED IN ADVANCE WERE RETURNED TO THE

CUSTOMERS AFTER DEDUCTING RS 3,000.FIRM HAD TO PAY RS 7,200 FOR OUTSTANDING SALARY NOT

PROVIDED FOR CASH.COMPENSATION PAID TO EMPLOYEES AMOUNTED TO RS 9,800.THE LIABILITY

WASN’T PROVIDED FOR IN THE ABOVE BALANCE SHEET. RS 25,000 HAD TO BE PAID FOR PROVIDENT

FUND.PREPARE REALISATION;CAPITAL & CASH A/C’S. (6 Marks)

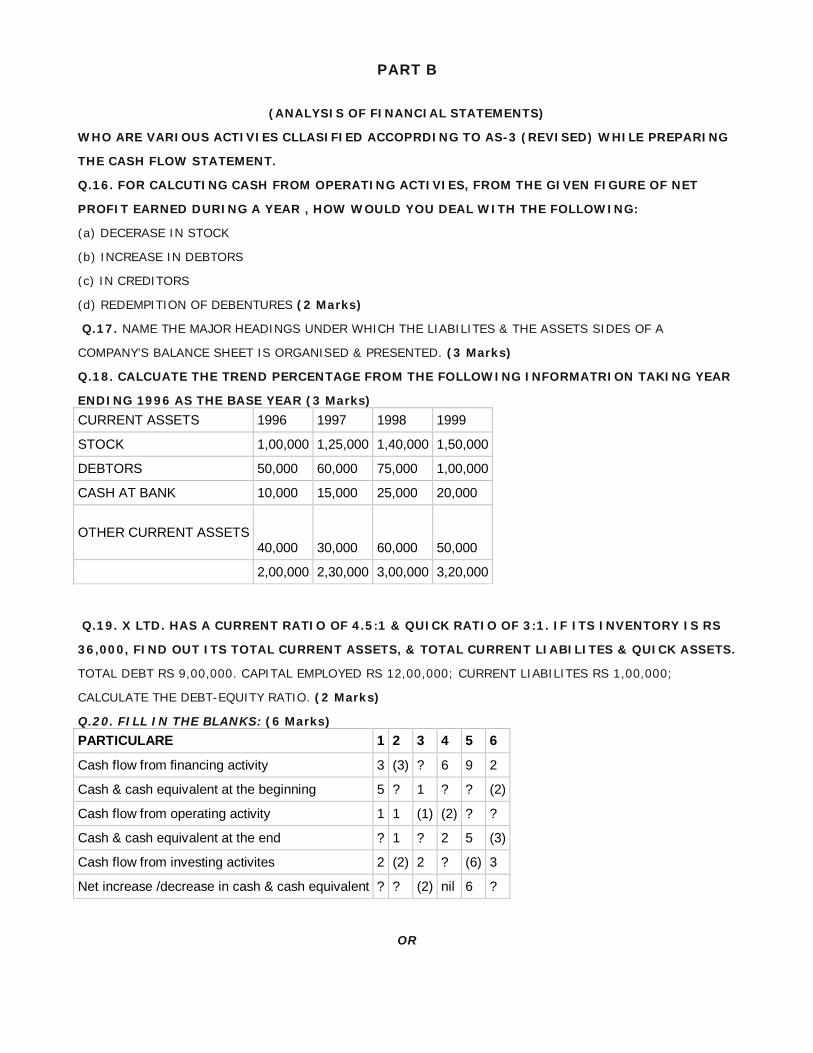

PART B

(ANALYSIS OF FINANCIAL STATEMENTS)

WHO ARE VARIOUS ACTIVIES CLLASIFIED ACCOPRDING TO AS-3 (REVISED) WHILE PREPARING

THE CASH FLOW STATEMENT.

Q.16. FOR CALCUTING CASH FROM OPERATING ACTIVIES, FROM THE GIVEN FIGURE OF NET

PROFIT EARNED DURING A YEAR , HOW WOULD YOU DEAL WITH THE FOLLOWING:

(a) DECERASE IN STOCK

(b) INCREASE IN DEBTORS

(c) IN CREDITORS

(d) REDEMPITION OF DEBENTURES (2 Marks)

Q.17. NAME THE MAJOR HEADINGS UNDER WHICH THE LIABILITES & THE ASSETS SIDES OF A

COMPANY’S BALANCE SHEET IS ORGANISED & PRESENTED. (3 Marks)

Q.18. CALCUATE THE TREND PERCENTAGE FROM THE FOLLOWING INFORMATRION TAKING YEAR

ENDING 1996 AS THE BASE YEAR (3 Marks)

CURRENT ASSETS 1996 1997 1998 1999

STOCK 1,00,000 1,25,000 1,40,000 1,50,000

DEBTORS 50,000 60,000 75,000 1,00,000

CASH AT BANK 10,000 15,000 25,000 20,000

OTHER CURRENT ASSETS 40,000

30,000

60,000

50,000

2,00,000 2,30,000 3,00,000 3,20,000

Q.19. X LTD. HAS A CURRENT RATIO OF 4.5:1 & QUICK RATIO OF 3:1. IF ITS INVENTORY IS RS

36,000, FIND OUT ITS TOTAL CURRENT ASSETS, & TOTAL CURRENT LIABILITES & QUICK ASSETS.

TOTAL DEBT RS 9,00,000. CAPITAL EMPLOYED RS 12,00,000; CURRENT LIABILITES RS 1,00,000;

CALCULATE THE DEBT-EQUITY RATIO. (2 Marks)

Q.20. FILL IN THE BLANKS: (6 Marks)

PARTICULARE 1 2 3 4 5 6

Cash flow from financing activity 3 (3) ? 6 9 2

Cash & cash equivalent at the beginning 5 ? 1 ? ? (2)

Cash flow from operating activity 1 1 (1) (2) ? ?

Cash & cash equivalent at the end ? 1 ? 2 5 (3)

Cash flow from investing activites 2 (2) 2 ? (6) 3

Net increase /decrease in cash & cash equivalent ? ? (2) nil 6 ?

OR

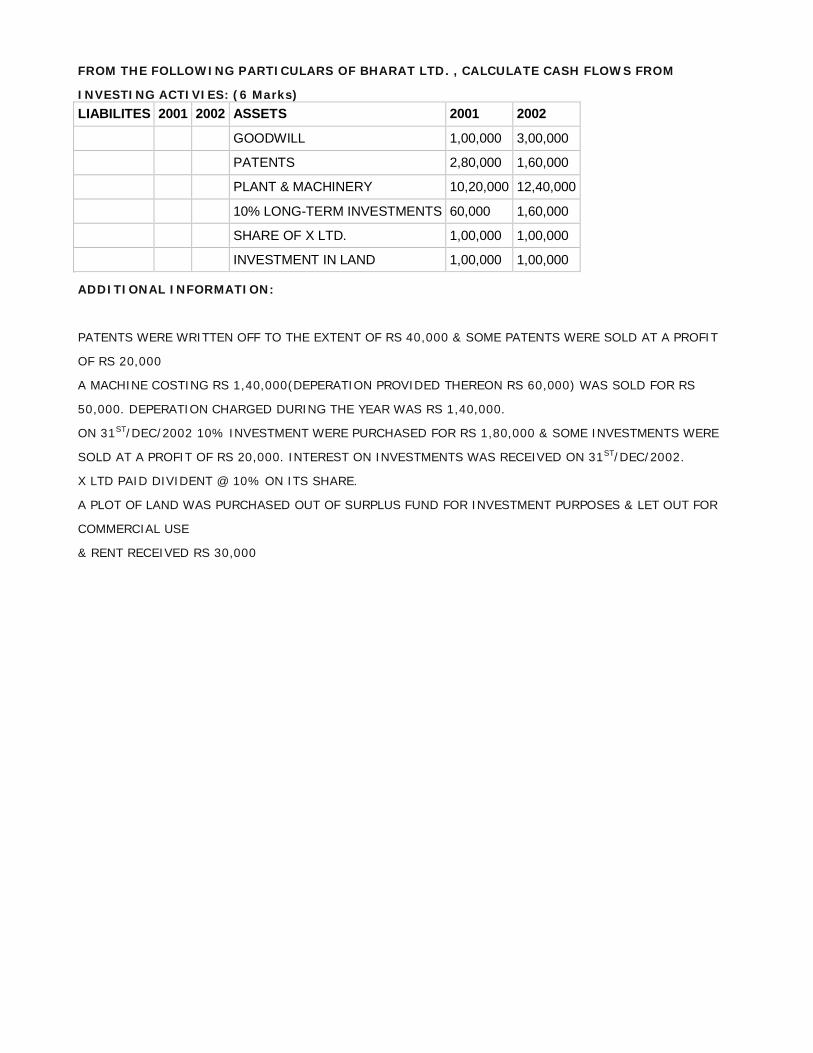

FROM THE FOLLOWING PARTICULARS OF BHARAT LTD. , CALCULATE CASH FLOWS FROM

INVESTING ACTIVIES: (6 Marks)

LIABILITES 2001 2002 ASSETS 2001 2002

GOODWILL 1,00,000 3,00,000

PATENTS 2,80,000 1,60,000

PLANT & MACHINERY 10,20,000 12,40,000

10% LONG-TERM INVESTMENTS 60,000 1,60,000

SHARE OF X LTD. 1,00,000 1,00,000

INVESTMENT IN LAND 1,00,000 1,00,000

ADDITIONAL INFORMATION:

PATENTS WERE WRITTEN OFF TO THE EXTENT OF RS 40,000 & SOME PATENTS WERE SOLD AT A PROFIT

OF RS 20,000

A MACHINE COSTING RS 1,40,000(DEPERATION PROVIDED THEREON RS 60,000) WAS SOLD FOR RS

50,000. DEPERATION CHARGED DURING THE YEAR WAS RS 1,40,000.

ON 31ST/DEC/2002 10% INVESTMENT WERE PURCHASED FOR RS 1,80,000 & SOME INVESTMENTS WERE

SOLD AT A PROFIT OF RS 20,000. INTEREST ON INVESTMENTS WAS RECEIVED ON 31ST/DEC/2002.

X LTD PAID DIVIDENT @ 10% ON ITS SHARE.

A PLOT OF LAND WAS PURCHASED OUT OF SURPLUS FUND FOR INVESTMENT PURPOSES & LET OUT FOR

COMMERCIAL USE

& RENT RECEIVED RS 30,000