islamic private debt securities and syndicated financing

TRANSCRIPT

STRICTLY PRIVATE & CONFIDENTIAL

Islamic Private Debt Securities and Syndicated Financing

Mashitah Hj OsmanDirector, Corporate Investment Banking

Page 1

Introduction to Islamic Private Debt Securities Introduction to Islamic Private Debt Securities

Islamic Private Debt Securities (“Islamic PDS”) or Sukuk (“Sukuk”) are securities structured based on Islamic financing principles. Islamic PDS are similar to conventional PDS, albeit with certain additional steps involved to incorporate the Islamic financing principles.

Sukuk is frequently referred to as an Islamic bond, but a more accurate translation of the Arabic word would be an Islamic Investment Certificate.

The Securities Commission Malaysia (“SC”) defines Islamic PDS as any securities issued pursuant to any Shariah principles and concepts approved by the Shariah Advisory Council (“SAC”) of the SC. Sukuk or its singular, Sak, is a document or certificate which represents a value of an asset.

The Sukuk must have an intrinsic value. The Sukuk may represent debt obligations and may be issued for a pool of receivables.

Page 2

Types of Islamic Securities Instruments and Their FeaturesTypes of Islamic Securities Instruments and Their Features

1. Islamic Commercial Papers (“CPs”)

To meet the short term financing requirements such as for working capital requirement;Normally issued on a tender basis and may either be issued at a discount, at par or premium to the face value;CPs are issued under a Programme not exceeding 7 years; andCPs can be issued for maturities between 1 month to 12 months.

2. Islamic Medium Term Notes (“MTNs”)

To meet the medium-term to long-term financing requirements such as for capital expenditure requirement;May be issued at par, discount or premium to face value; Where MTNs are issued under a Programme which is coupled with CPs, the tenor for such Programme must not exceed 7 years. Otherwise, the tenor restriction is not applicable on the MTN Stand alone Programme; andThe minimum tenor of the MTNs is 1 year;

Page 3

Types of Islamic Securities Instruments and Their Features Types of Islamic Securities Instruments and Their Features (cont(cont’’d)d)

3. Islamic Bonds (“Bonds”)

To meet medium and long-term financing requirement;Typically used for capital expenditure requirement or under a project financing structure;Can be issued without prospectus by way of private placement, “bought-deal” and/or open tender basis;The maturity is more than one (1) year and may be issued in series to match the cashflow profile of the issuer; andNo exposure to interest/profit rate fluctuations as the interest/profit rate is locked-in upfront.

Typical Shariah Concepts and Principles for the Islamic Securities Instruments:

1.Bai Bithaman Ajil (deferred payment sale);2.Ijarah (leasing), Istisna’ (purchase order); 3.Mudharabah (profit-sharing); and 4.Musyarakah (profit and loss-sharing).

Page 4

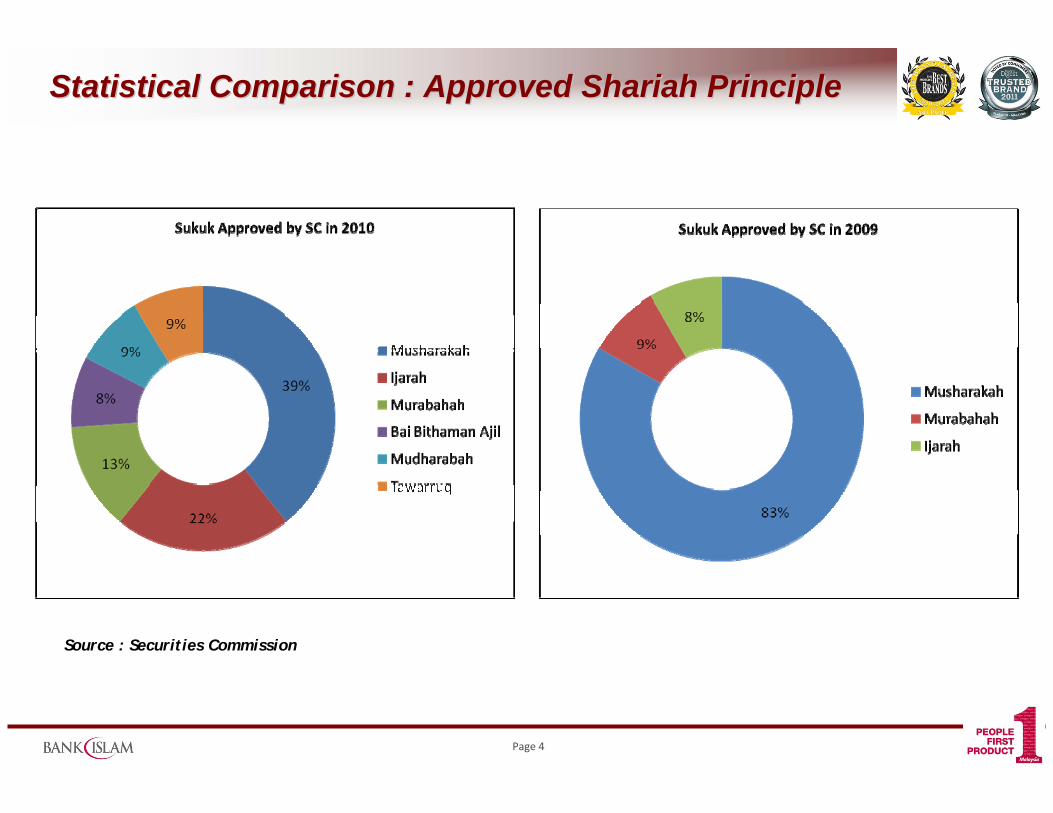

Source : Securities Commission

Statistical Comparison : Approved Shariah PrincipleStatistical Comparison : Approved Shariah Principle

Page 5

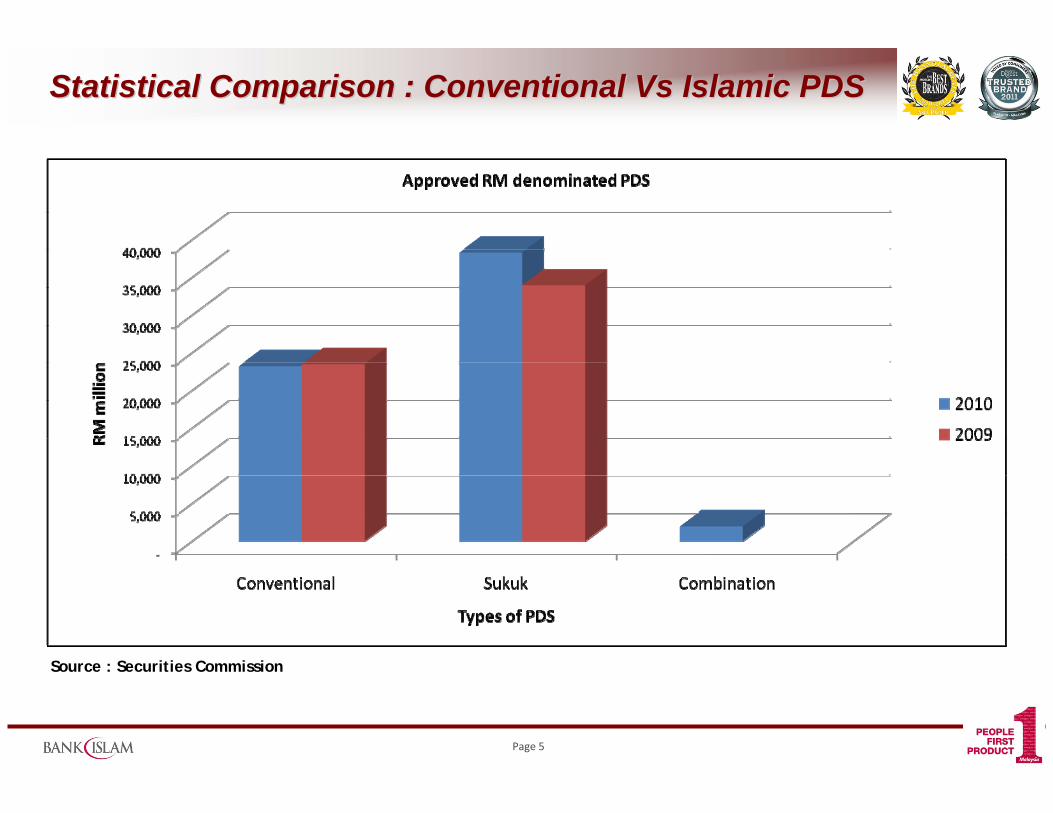

Source : Securities Commission

Statistical Comparison : Conventional Vs Islamic PDSStatistical Comparison : Conventional Vs Islamic PDS

Page 6

Investors’ Perspective

Provides investors with the opportunity to invest in an alternative fixed income instrument that is Shariah-compliant with stable returns and at the same time helps to diversify their investment portfolio; and

Provide investors the opportunity to invest in liquid instruments.

Islamic Capital Market

Increases the breadth and depth of the Islamic capital market;

Global acceptance structure, especially to the Middle Eastern investors; and

Creates an alternative form of investment instruments.

Issuers’ Perspective

Enhances issuer’s profile;Tap wider investor including conventional investors; and

More cost effective of raising fund as the issuer is able to deduct expenses such as arrangement fee, rating fee, etc from taxable income.

Stamp duty exemptions on the legal documentation, subject to the approved Shariah principles.

Benefits of Islamic PDSBenefits of Islamic PDS

Page 7

Process/Activities

(Completion: 3 to 4 months)

- Structure Islamic PDS + Shariah Approval

- Rating

- Submission to Securities Commission

- Information Memorandum

IssuerPrimary Subscribers/Investors

Secondary Market Trading

Trustee

Reporting Accountant

Rating Agency

Other Advisers

Arranger

Shariah Adviser

Due Diligence Working Group

Legal Counsel

Due Diligence

Events to IssuanceEvents to Issuance

Page 8

The cost of financing is directly correlated with the credit standing of a debt issue;

A higher credit risk debt would command a higher financing cost;

Debt rating is a process of assessing the likelihood of timely payment of the principal and interest/profit over the duration of a particular debt;

In essence, the rating is graded into two broad categories i.e. Investment Grade and Non-Investment Grade; and

The Investment Grade comprise ratings of AAA, AA, A and BBB, whilst the Non-Investment Grade comprise ratings of BB, B, C and D.

General Overview On RatingGeneral Overview On Rating

Page 9

Project Sponsor/ManagementIntegrity, experience/track records and level of commitment to meet any cost-overruns, etc.

Viability of Project CashflowRobustness and certainty of cashflow.

Principal Project AgreementsNo restriction conditions to facilitate the raising of financing via Islamic structure. For example : Prohibition to transfer/sale the rights/assets under the agreements.

Construction RiskAppointment of reputable contractor to mitigate delay in completion and variation in project costs.

Rating ConsiderationsRating Considerations

Page 10

Operational RiskRelates to operation and maintenance of the Project upon post-completion.

Demand/Offtake RiskCredit strength of the pay-master and timeliness of payment.

Issue StructureCovenants to enhance the rating e.g. Finance Service Cover Ratio; Debt to Equity Ratio; Order of priority in payment waterfall; Dividend restriction; Designated Accounts; Legal Structure, etc.

Financing structure or security enhancement includes (without limitation to) the provision of guarantee from a parent company where the financial standing is better than the Issuer stand-alone rating.

Rating Considerations (contRating Considerations (cont’’d)d)

Page 11

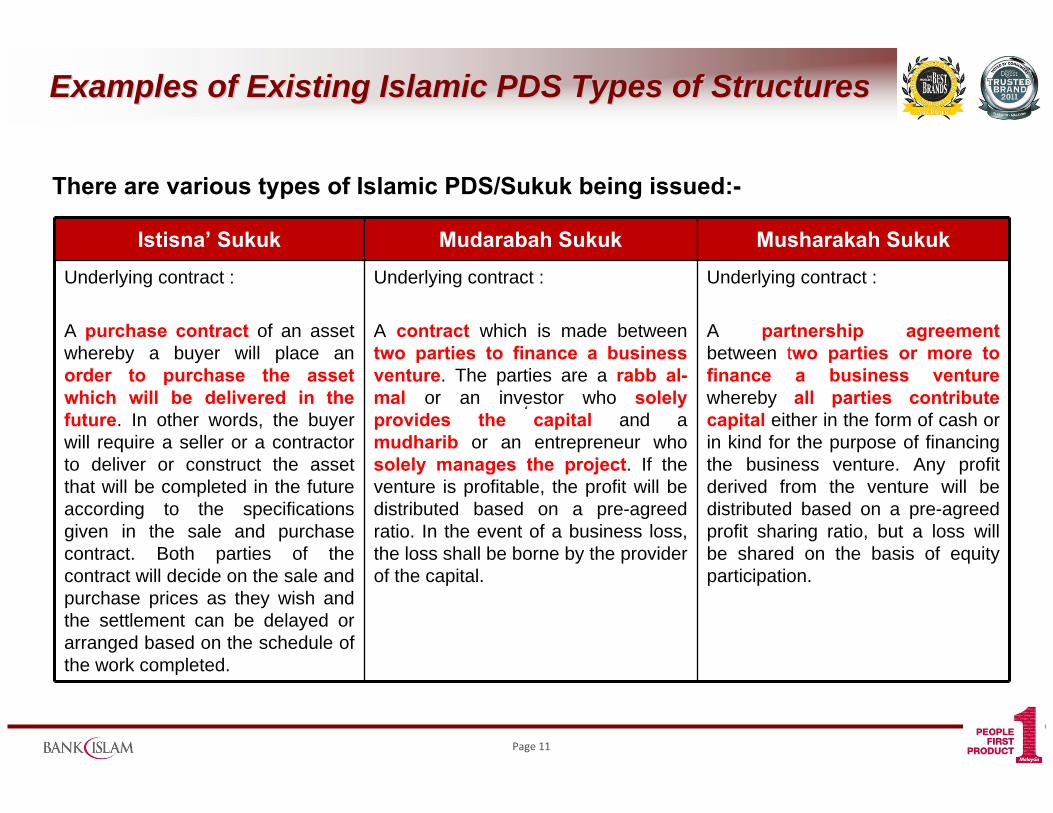

Istisna’ Sukuk Mudarabah Sukuk Musharakah SukukUnderlying contract :

A purchase contract of an asset whereby a buyer will place an order to purchase the asset which will be delivered in the future. In other words, the buyer will require a seller or a contractor to deliver or construct the asset that will be completed in the future according to the specifications given in the sale and purchase contract. Both parties of the contract will decide on the sale and purchase prices as they wish and the settlement can be delayed or arranged based on the schedule of the work completed.

Underlying contract :

A contract which is made between two parties to finance a business venture. The parties are a rabb al-mal or an investor who solely provides the capital and a mudharib or an entrepreneur who solely manages the project. If the venture is profitable, the profit will be distributed based on a pre-agreed ratio. In the event of a business loss, the loss shall be borne by the provider of the capital.

Underlying contract :

A partnership agreement between two parties or more to finance a business venture whereby all parties contribute capital either in the form of cash or in kind for the purpose of financing the business venture. Any profitderived from the venture will be distributed based on a pre-agreed profit sharing ratio, but a loss will be shared on the basis of equity participation.

There are various types of Islamic PDS/Sukuk being issued:-

Examples of Existing Islamic PDS Types of StructuresExamples of Existing Islamic PDS Types of Structures

Page 12

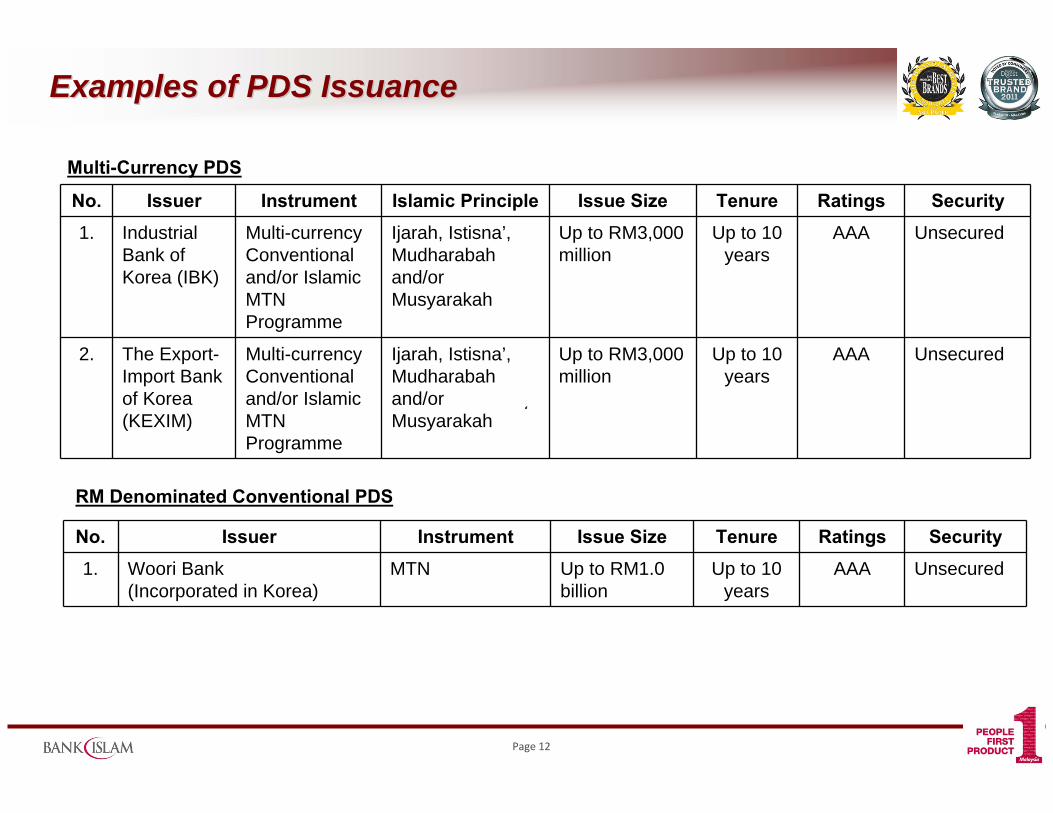

No. Issuer Instrument Islamic Principle Issue Size Tenure Ratings Security 1. Industrial

Bank of Korea (IBK)

Multi-currency Conventional and/or Islamic MTN Programme

Ijarah, Istisna’, Mudharabah and/or Musyarakah

Up to RM3,000 million

Up to 10 years

AAA Unsecured

2. The Export-Import Bank of Korea (KEXIM)

Multi-currency Conventional and/or Islamic MTN Programme

Ijarah, Istisna’, Mudharabah and/or Musyarakah

Up to RM3,000 million

Up to 10 years

AAA Unsecured

Multi-Currency PDS

RM Denominated Conventional PDS

No. Issuer Instrument Issue Size Tenure Ratings Security 1. Woori Bank

(Incorporated in Korea)MTN Up to RM1.0

billionUp to 10

yearsAAA Unsecured

Examples of PDS IssuanceExamples of PDS Issuance

Page 13

No. Issuer Instrument Islamic Principle Issue Size Tenure Ratings Guarantor1. Nestle

Foods (M) Sdn Bhd

CP/MTN Programme

Murabahah Up to RM700 million

7 years AAA/P1 Nestle (M) Berhad

2. Toyota Capital (M) Sdn Bhd

MTN Programme N/A

Up to RM1,200 million

10 years AAA Toyota Motor Finance (Netherlands) BV

3. Tesco Stores (M) Sdn Bhd

Islamic CP/MTN Programme and Conventional CP/MTN Programme

Murabahah/ Musyarakah

Up to RM3,500 million

7 years (for CPs) and 15 years (for MTN)

P1 (for CP) and AAA (for MTN)

Tesco Plc

RM Denominated PDS – Guaranteed by Parent Company

No. Issuer Instrument Islamic Principle Issue Size Tenure Ratings Guarantor1. Esso

Malaysia Berhad

CP Programme

Murabahah Up to RM300 million

7 years P1 -

RM Denominated PDS – Other Multinational Corporations

Examples of PDS Issuance (conExamples of PDS Issuance (con’’t)t)

Page 14

A financing facility granted by a group of financiers.Lead arrange by one or more financiers.Several roles such as Bookrunner(s), Underwriting Financier(s), Security Agent, Facility Agent etc. are accorded to the Lead Arrangers. Financing amount committed by each of the participating financers may differ depending on the title.Wide options on the structure e.g. Corporate Financing, Investment / Acquisition/Financing, Project Financing etc.May entail more than one facility.Documented in a single financing agreement with common terms and conditions.Financing amount required.Creditworthiness/ bankability.Industry segmentation.Customer profile.

About Syndicated Financing

Factors to determine the Obligor

Syndicated FinancingSyndicated Financing

Page 15

Customer to discuss funding requirements with potential Lead Arranger(s).Request for financing proposal.Select the suitable financing proposal and appoint the Lead Arranger(s).Work towards financial close with the Lead Arranger(s).Financing structure tailored made to meet the funding requirements.

Term and/or revolving facility; drawdown period; bullet or amortising payment; early settlement; single or multi-currency denominated; secured or unsecured financing; assignment etc.

Terms and conditions need to meet the requirements of both the customer and financiers.Mainly domestic and international financial institutions.Takaful operators & insurance companies.Pension, retirement and pilgrimage funds and-quasi governments agencies.

Access the Syndicated Financing

Market

Financiers

Financing Structure

Syndicated Financing (conSyndicated Financing (con’’t)t)

Page 16

Difficult and large deals still get done.

Limited disclosure/ Disclosure is limited to several parties only.

Not complicated and more expedient as compared to Sukuk/ Bonds issuance.

Suitable for refinancing purposes.

Allows the company to develop banking relationship in the market place.

For customer/obligor of a lesser credit/financial standing, lower cost of borrowings can be achieved with the parent company’s guarantee (of a stronger credit/financial).

Why Syndicated Financing Why Syndicated Financing

Page 17

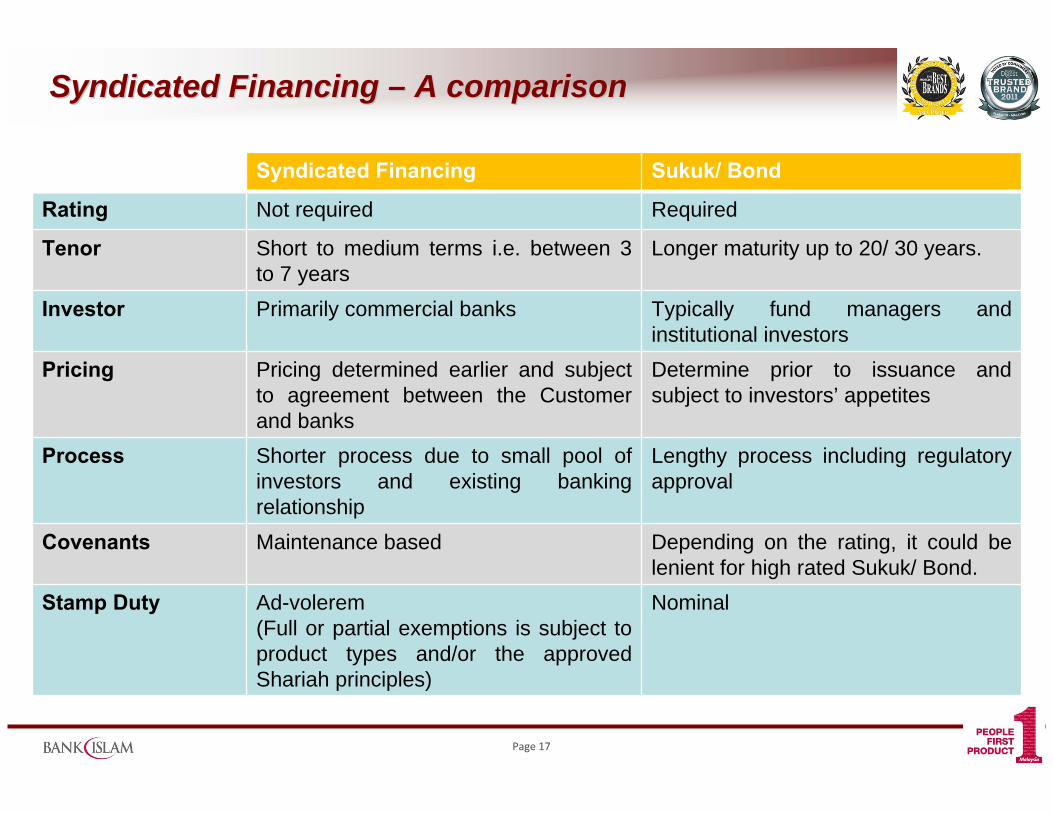

Syndicated Financing Sukuk/ Bond

Rating Not required Required

Tenor Short to medium terms i.e. between 3 to 7 years

Longer maturity up to 20/ 30 years.

Investor Primarily commercial banks Typically fund managers and institutional investors

Pricing Pricing determined earlier and subject to agreement between the Customer and banks

Determine prior to issuance and subject to investors’ appetites

Process Shorter process due to small pool of investors and existing banking relationship

Lengthy process including regulatory approval

Covenants Maintenance based Depending on the rating, it could be lenient for high rated Sukuk/ Bond.

Stamp Duty Ad-volerem (Full or partial exemptions is subject to product types and/or the approved Shariah principles)

Nominal

Syndicated Financing Syndicated Financing –– A comparisonA comparison

Page 18

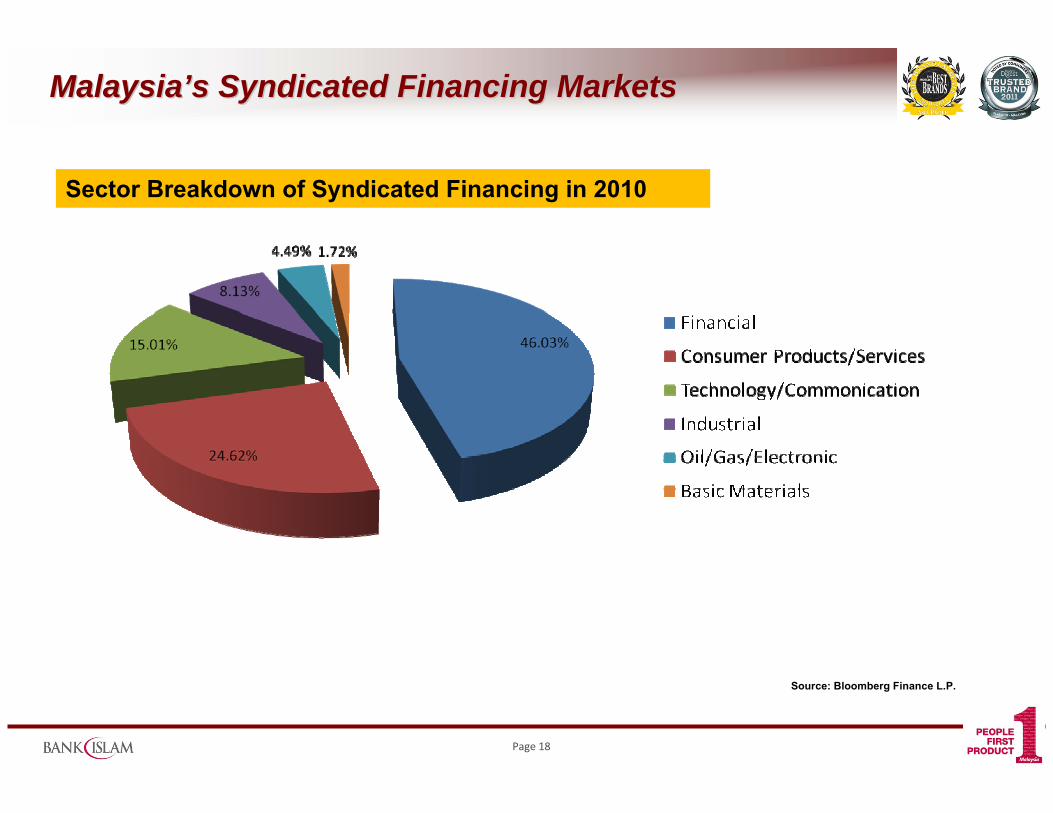

Sector Breakdown of Syndicated Financing in 2010

Source: Bloomberg Finance L.P.

MalaysiaMalaysia’’s Syndicated Financing Marketss Syndicated Financing Markets

Page 19

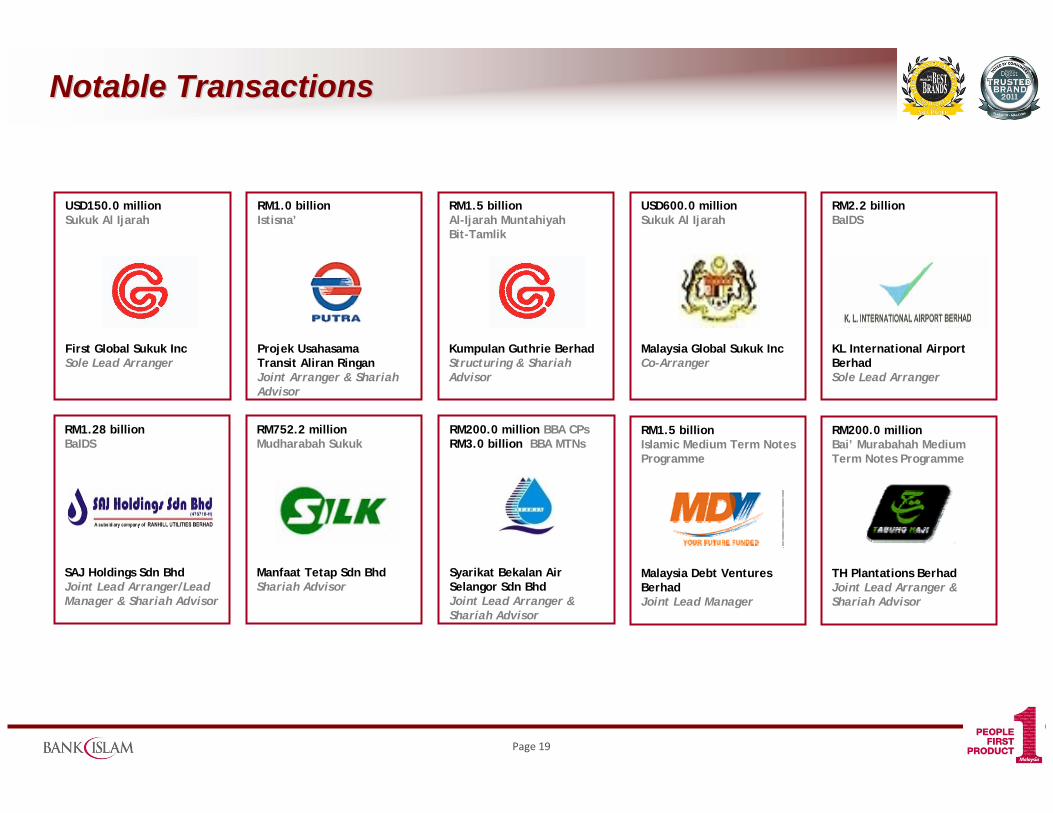

RM1.0 billionIstisna’

Projek Usahasama Transit Aliran RinganJoint Arranger & Shariah Advisor

RM2.2 billionBaIDS

KL International Airport BerhadSole Lead Arranger

RM1.5 billionAl-Ijarah Muntahiyah Bit-Tamlik

Kumpulan Guthrie BerhadStructuring & Shariah Advisor

USD150.0 millionSukuk Al Ijarah

First Global Sukuk IncSole Lead Arranger

USD600.0 millionSukuk Al Ijarah

Malaysia Global Sukuk IncCo-Arranger

RM1.28 billionBaIDS

SAJ Holdings Sdn BhdJoint Lead Arranger/Lead Manager & Shariah Advisor

RM752.2 millionMudharabah Sukuk

Manfaat Tetap Sdn BhdShariah Advisor

RM200.0 million BBA CPs RM3.0 billion BBA MTNs

Syarikat Bekalan Air Selangor Sdn BhdJoint Lead Arranger & Shariah Advisor

RM1.5 billion Islamic Medium Term Notes Programme

Malaysia Debt Ventures BerhadJoint Lead Manager

RM200.0 million Bai’ Murabahah Medium Term Notes Programme

TH Plantations BerhadJoint Lead Arranger & Shariah Advisor

Notable TransactionsNotable Transactions

Page 20

RM4.0 billionIjarah Medium Term Notes Programme

Syarikat Prasarana Negara BerhadCo-Manager

RM500.0 millionBank Guaranteed Sukuk Ijarah

Aras Sejagat Sdn BhdJoint Lead Arranger &Joint Lead Manager

RM4.0 billionSukuk Musyarakah

Plus SPV BerhadJoint Book Runner

RM327.0 millionSyndicated Islamic Financing Facility

Prolintas Expressway Sdn BhdLead Arranger

RM330.0 millionSyndicated Islamic Financing Facility

Kedah Sato Sdn BhdLead Arranger

USD150.0 million*Syndicated Islamic Financing Facility

Qatar Airways Q.C.S.CArranger

*Ijarah deal of the year 2009 – Islamic Finance News*Qatar deal of the year 2009 – Islamic Finance News*Best Islamic Structured Financing – The Asset Triple A Islamic Finance Awards 2010

RM10.0 billionIslamic Medium Term Notes Programme

Aman Sukuk BerhadJoint Lead Manager &Shariah Advisor

RM800.0.0 millionSyndicated Islamic Financing Facilities

Aura Bayu Sdn BhdSenior Manager

RM667.5 millionSyndicated Project Financing Facilities

Ranhill Powertron II Sdn BhdSenior Manager

Notable Transactions Notable Transactions (cont(cont’’d)d)

Page 21

Wassalamوالسالموالسالم

Thank You

شكرا جزيالشكرا جزيال