is there cross-border tax planning after schering-plough

TRANSCRIPT

1

Is ThereIs ThereCrossCross--Border Tax PlanningBorder Tax Planning

After After ScheringSchering--PloughPloughAnd Other Recent Cases?And Other Recent Cases?

Orrin TilevitzJuno Investments LLC

Mark LeedsGreenberg Traurig

International Tax Institute March 10, 2010

2

Disclaimers•• ANY TAX ADVICE IN THIS PRESENTATION IS NOT INTENDED OR WRITTEN ANY TAX ADVICE IN THIS PRESENTATION IS NOT INTENDED OR WRITTEN

TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN. HEREIN.

•• You (and your employees, representatives, or agents) may disclose to any and all You (and your employees, representatives, or agents) may disclose to any and all persons, without limitation, the tax treatment or tax structure, or both, of any transaction persons, without limitation, the tax treatment or tax structure, or both, of any transaction described in the associated materials we provide described in the associated materials we provide to you, including, but not limited to, you, including, but not limited to, any tax opinions, memoranda, or other tax analyses contained in those materials.any tax opinions, memoranda, or other tax analyses contained in those materials.

•• The information contained herein is of a general nature and based on authorities that are The information contained herein is of a general nature and based on authorities that are subject to change. Applicability of the information to specific situations should be subject to change. Applicability of the information to specific situations should be determined through consultation with your tax adviser.determined through consultation with your tax adviser.

3

Background—Tax Shelters and Other Structured Transactions

• 1986: Congress outlaws retail tax shelters (it thinks) with enactment of § 469

• 1989: ACM contingent installment sale• 1991-2: Schering-Plough repatriation• 1992: Compaq ADR transaction• 1993: Winn-Dixie leveraged COLI transaction• 1997: Con Ed enters LILO transaction• 1999: IRS issues BOSS notice• 2000: IRS issues “son of BOSS” notice• 2001: Palm Canyon MLD transaction• 2002-3: Southgate’s distressed debt transaction• 2003: IRS issues revised tax shelter registration and disclosure

regulations• 2005: KPMG indictment

4

The Cases As We See Them (Overview)

• Schering Plough –Method of cash repatriation lacks connection with taxpayer’s business. Is this (a) as the court held, like ACM(or Palm Canyon X) or (b) permissible tax structuring of business transaction?

• Palm Canyon X – No connection whatsoever between transaction generating the tax benefits and business of the taxpayer. No economic substance found.

• Wells Fargo – De minimis connection between transaction generating tax benefits and business of the taxpayer did not justify permitting tax benefits.

• Southgate – Substantial connection between business of taxpayer and tax benefits did not justify unwarranted results. Court bifurcated away substantial business motivation and analyzed transaction structure alone.

• Con Ed – Transaction facially related to core business activities found to have economic substance. Question: is this relation real?

5

Schering PloughSchering Plough,,651 F.Supp.2d 219 (DNJ 2009651 F.Supp.2d 219 (DNJ 2009))

Cash RepatriationCash Repatriation

Background, Review and AnalysisBackground, Review and Analysis

6

Schering-Plough—Dramatis Personae• Katharine S. Hayden, U.S.D.J.

– Appointed to federal bench 1997– Previously NJ AUSA, matrimonial practice, and NJ family

court judge. Married to criminal defense attorney– First reported tax case other than summons enforcement and

criminal tax fraud trial• Johannes den Baas, ABN VP. See Saba, Boca, ASA, ACM. • Rabobank. See Enbridge (midco)• Merrill Lynch. See Boca, Saba, ACM• ABN. See Marriott International Resorts, L.P (T-bill short

sale); BB&T Corp. (LILO), Boca, Nicole Rose (midco), Saba, ASA, ACM, Wells Fargo (SILO), Con Edison, Salina (T-bill short sale)

• Deloitte & Touche, SP “independent auditor”. DISCLOSURE: Both speakers are former DT Employees.

7

Background on Early Swap Strategies•• Before 1989, many tax advisors believed that a payment to a swap counterparty Before 1989, many tax advisors believed that a payment to a swap counterparty

in exchange for an its rights to receive payments under a notional principal in exchange for an its rights to receive payments under a notional principal contract generated immediate income to the seller.contract generated immediate income to the seller.

•• It was believed that certain companies utilized this technical position to shift It was believed that certain companies utilized this technical position to shift income to Puerto Rican subsidiaries. The PR subsidiaries were entitled to a income to Puerto Rican subsidiaries. The PR subsidiaries were entitled to a lower rate of tax than their domestic parents under Code lower rate of tax than their domestic parents under Code §§ 936. For example, 936. For example, PR subsidiary would enter into an interest rate swap. It would then sell its PR subsidiary would enter into an interest rate swap. It would then sell its rights to receive payments to its US parent. The PR subsidiary would claim the rights to receive payments to its US parent. The PR subsidiary would claim the amount received as income and the US parent would amortize the payment, amount received as income and the US parent would amortize the payment, creating US tax deductions. Alternatively, the strategy could be used to refresh creating US tax deductions. Alternatively, the strategy could be used to refresh NOLS.NOLS.

•• IRS ended this strategy in 1989 with the issuance of Notice 89IRS ended this strategy in 1989 with the issuance of Notice 89--21. Notice 8921. Notice 89--21 required recognition of the sale of the receipt leg of a swap over the life of 21 required recognition of the sale of the receipt leg of a swap over the life of the swap.the swap.

•• Parties in Parties in Schering PloughSchering Plough relied on Notice 89relied on Notice 89--21 to conclude that sale of right 21 to conclude that sale of right to receive payment under a swap was not a loan and transaction would not to receive payment under a swap was not a loan and transaction would not generate subpart F income. Today, Treas. Reg. generate subpart F income. Today, Treas. Reg. §§ 1.4461.446--3(h)(4)) treats swap 3(h)(4)) treats swap assignment as loan or nonperiodic payment, depending on economic substance assignment as loan or nonperiodic payment, depending on economic substance to each party.to each party.

8

20-Year Interest Rate Swap

ABN

ABN Schering-Plough

LIBOR

Federal Funds Rate

MerrillLynch

LIBOR Federal Funds Rate + .10

(Basis Swap)

9

Some Background on the Basis Swap• Limited had $498M of untaxed earnings that it desired to

repatriate tax-free.• Court noted that SP relied on ML to design “tax-beneficial

investment vehicles and ML had placed SP into a failed CINS (contingent installment note sale) transaction. The CINS deal had not been audited at the time the swap was executed. CINS counsel was also swap counsel.

• Court concludes that swap is ML’s idea. Upfront fee payment of $2.2M. Transaction was repeated in 1992.

• Transaction size was “back-solved” so that the amount to be paid by Limited would be equal to the untaxed earnings.

• SP did not study whether swap would reduce interest rate exposure before entering into transaction “and incurred significant losses while attempting to mitigate the adverse effects of the hedge.”

10

Assignment of Payments for Yrs. 6-20

ABNSchering-

PloughLIBOR

Schering(NJ)

SPInt’l

Schering-Plough

Ltd.

SchericoLtd.

EssexChemie

U.S.

Switzerland

Payment Rights Yrs 6-20

advance

cash

Sherico held a put optionallowing it to force SP toreacquire the payment rights

LIBOR

Fed Funds

11

Court’s Analysis• Is transaction really a loan or a sale (substance

over form)?– For SP to prevail, court must find that “transactions

were the economic equivalent of sales of future income streams”

• Does it have sufficient economic substance or is it a sham transaction?– SP must have entered into them with objectives beyond

tax avoidance AND that net economic position appreciably altered as a result.

• Does it duly comport with the relevant taxation scheme implemented by Congress?– Transaction must be “consistent with Congress’s

legislative intent”.

12

Transaction Is A Loan Because . . .• PhD economists testify that it is loan, financing device.• PV of receivables=amt paid by Swiss subs, amt to be paid ABN exceed nominal

value of pmts to SP, the economic equivalent of interest. Although return to Swiss subs could vary b/t $33MM & $54MM, repayment of initial advance was not an issue.

• Reacquisition of leg reflects accelerated principal reduction.• Documentary evidence calling things “loans”, “principal” and “interest”• SP controlled cash flows consistent with indirect obligation to repay Swiss subs

and consistently made repayment to Swiss subs through ABN.• Contrary cases didn’t involve “meticulously crafted”, tax-motivated, related-

party transactions between a parent corporation and its controlled subsidiary”• Dr. David Larue testify in parent-subsidiary situation, labels may not comport

with economic nature.• ABN a mere conduit, citing Enbridge.• Court does not discuss benefits and burdens of ownership.

Cases Court Relied On

Mapco Inc. v. U.S., 556 F2d 1107 (Ct. Cl. 1977)

Chemical Bank

Rock Creek

Mapco

Pipeline Revenues

$4M loan

$4M p’mt Assigned 75% of pipeline revenue until $4M

Chemical CDs

13

Mapco, Cont.• Bank deposits CD proceeds into Mapco’s account, transfer

enough to pay Rock Creek its profit, and keep the rest against its loan

• Customers continue to pay Mapco• Mapco admits that sole purpose of transaction is to refresh

expiring NOL• Note: parties unrelated• Case cited only 2 other times:

– Andantech, T.C. Memo, 2002-97 a sale-leaseback tax shelter

– Watts Copy Systems, Inc., T.C. Memo. 1994-124, holding that the taxpayer correctly reported a sale of a lease revenue stream to a bank as a non-taxable loan, looking to the “benefits and burdens of ownership.”

14

Mapco, Cont.• Case cited only 2 other times:

– Andantech, T.C. Memo, 2002-97 a sale-leaseback tax shelter

– Watts Copy Systems, Inc., T.C. Memo. 1994-124, holding that the taxpayer correctly reported a sale of a lease revenue stream to a bank as a non-taxable loan, looking to the “benefits and burdens of ownership.”

15

Mapco, Cont.—Why Is It a Loan

• Certainty of repayment• Looks like loan• Interest rate is standard prevailing interest rate—

not reflect any transfer of risks of ownership• CD indicates that Mapco indirectly guaranteed

repayment• Rock Creek lacks dominion or control over

revenue stream and no risks or benefits of property ownership

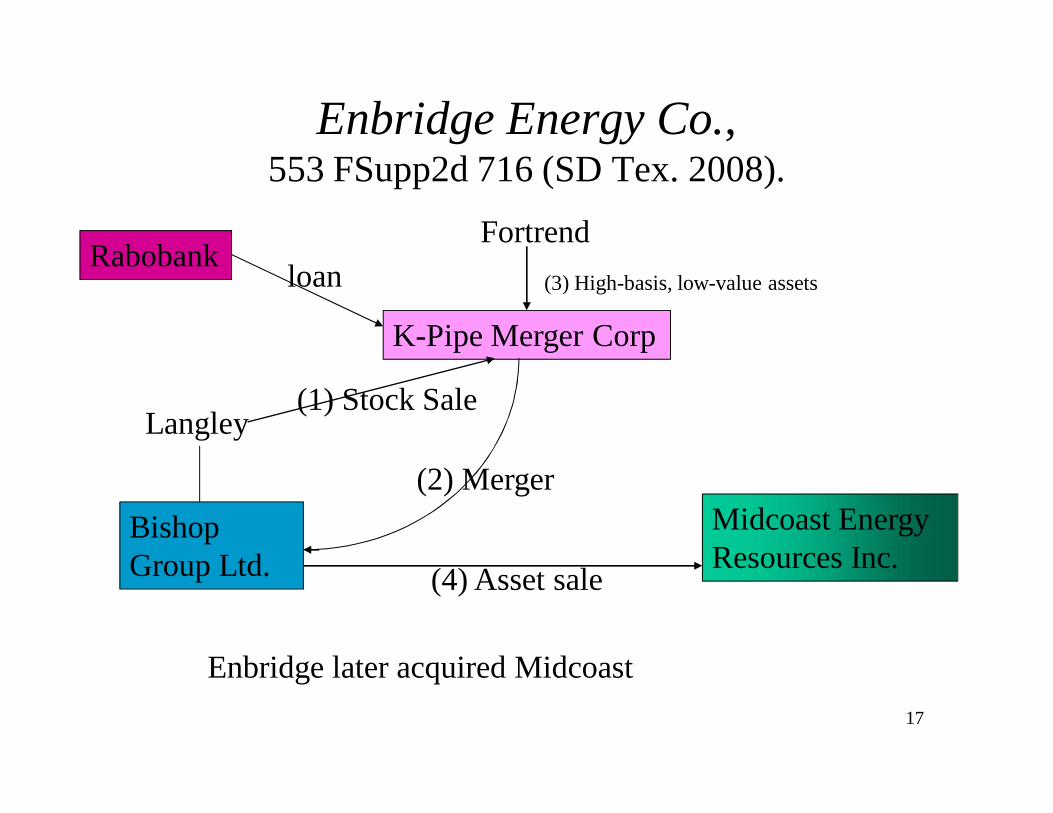

Enbridge Energy Co.,553 FSupp2d 716 (SD Tex. 2008).

Bishop Group Ltd.

Midcoast Energy Resources Inc.

Langley

K-Pipe Merger Corp

(1) Stock Sale

Fortrend(3) High-basis, low-value assets

(2) Merger

(4) Asset sale

Rabobank loan

Enbridge later acquired Midcoast17

Enbridge, Cont.--Facts

• Asset sale closes one day after stock sale• Midcoast had begun negotiating stock sale; PWC

brought in Fortrend to “bridge the gap”• All communications involved Midcoast and its

advisor insisted on certain “good facts”, including that Bishop not be liquidated for at least 2 years

• K-Pipe’s obligations indemnified by Midcoast• After transaction K-Pipe engage in virtually no

business activity, and sole purpose was to allow basis step-up in assets

18

Enbridge, Cont.—Holdings & Rationale

• K-Pipe should be disregarded• Midcoast purchased stock, not assets,

because seller would not have sold assets• Court not address fact that Bishop not

liquidated; apparently, constructive liquidation

19

20

Loan—Substance over Form Factors• SP set forth 17 reasons why substance was an assignment of

income, including that Swiss subs only had recourse against ABN and subs could sell receipt legs.

• “Simply be breaking up he obligations using an intermediary, SP cannot defeat the reality that is subsidiaries advanced it a lump sum and were later funneled money via a third party.”

• Swaps and assignment were prearranged parts of broader picture intended to repatriate funds

• Court found the fact that the transactions were routed through Scherico to be suspect – Sherico had no untaxed earnings and was used as a conduit for repatriating Limited’s untaxed earnings.

• Therefore, reorder swap and assignment as assignment-loan and establishment of payment obligation.

• Problem: step transaction doctrine can’t be used to reorder steps and, in the presenters’ view, citing to this doctrine muddied the analysis.

21

Loans Under Subpart F

• See Jt. Comm. Expl. of TRA 1976 at 228-229, amendment to § 956 to exclude stock and debt of unrelated parties (investment by foreign sub in debt of related U.S. person, but not unrelated person makes funds available for use by U.S. shareholders and therefore constitutes effective repatriation that should be taxed)

22

No Economic Substance Under ACM Because• Transaction not change economics: repatriated funds do no

constitute appreciable economic effect.• Interest rate exposure purposely inflicted by tax counsel

and so doesn’t count.• Minimal effect on ABN’s financial position.• Transaction had no business purpose: that SP had good

uses for the cash doesn’t matter, citing varies COLI cases.• Court dismisses hedging, cash management and yield

enhancement arguments.• Transaction tax-motivated: reasonable taxpayer would not

have taken roundabout route to achieve straightforward ends.

23

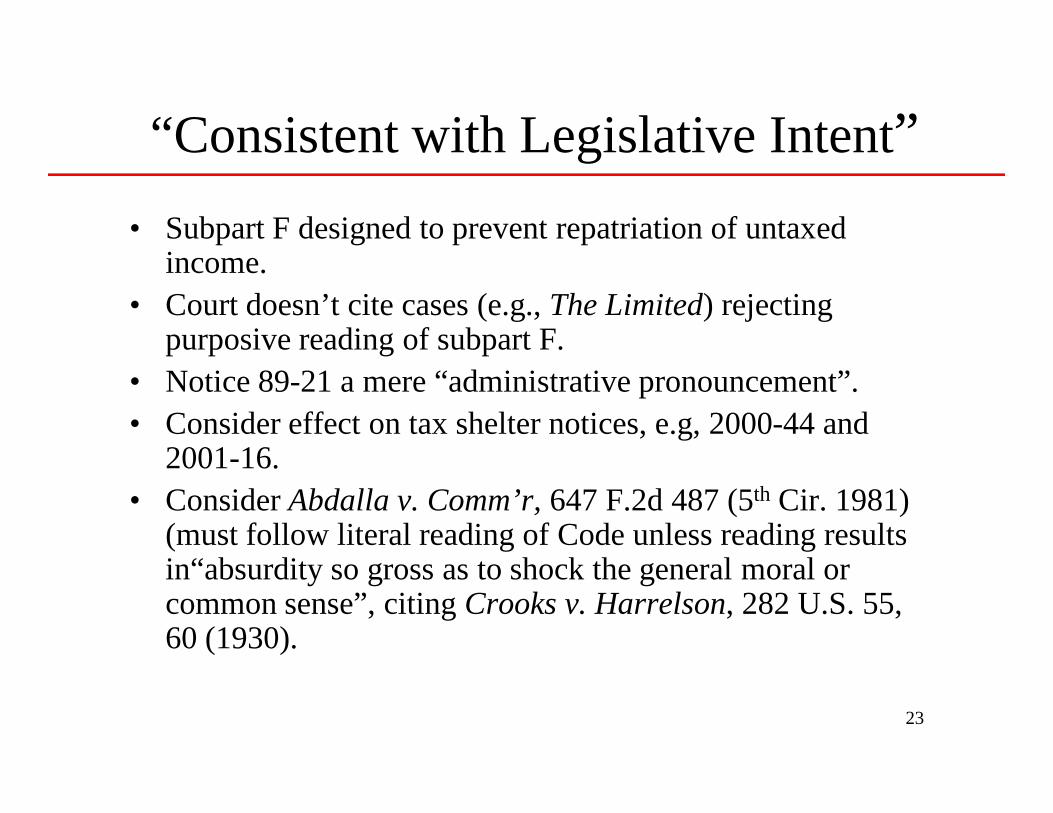

“Consistent with Legislative Intent”• Subpart F designed to prevent repatriation of untaxed

income.• Court doesn’t cite cases (e.g., The Limited) rejecting

purposive reading of subpart F.• Notice 89-21 a mere “administrative pronouncement”.• Consider effect on tax shelter notices, e.g, 2000-44 and

2001-16.• Consider Abdalla v. Comm’r, 647 F.2d 487 (5th Cir. 1981)

(must follow literal reading of Code unless reading results in“absurdity so gross as to shock the general moral or common sense”, citing Crooks v. Harrelson, 282 U.S. 55, 60 (1930).

24

Palm Canyon X Investments Palm Canyon X Investments LLCLLC

TC Memo. 2009TC Memo. 2009--288288

“Market Linked Deposits”“Market Linked Deposits”

Background, Review and Background, Review and AnalysisAnalysis

25

Palm Canyon X- Taxpayer Due Diligence

• Strategy promoted to taxpayer as a “high end tax product for big losses.

• Taxpayer was given a tax opinion from a nationally prominent law firm to review.

• Taxpayer hires independent counsel to review opinion who was “skeptical” of conclusion.– Opinion was deemed aggressive but technically accurate.

• Taxpayer investigated promoters.• Taxpayer hired promoter counsel to prepare opinion.• Deduction for option premium reported as FX trading loss.

26

Palm Canyon X --Structure

AHI

Bank

Offsetting Market-Linked Deposits

99%

CF Advisors

1%

Hamels

Palm Canyon

“Bull” ¥Deposit

“Bear” ¥Note

Bank pays 3.6% Fixed

If ¥≥124.67, Bank pays $8M

If ¥≤124.67, no bonus

If ¥=124.65 or 6, Bank pays $8M

Palm pays 3.6% Fixed

If ¥≥124.67, Palm pays $7.9M

If ¥≤124.67, no bonus

If ¥=124.65 or 6, Palm pays -0-

Cash did not change hands. Palm paid net premium of $55k.

Contributionof Palm interest

AHI purchases CF Advisors’ interest, causing deemed distribution of positions.

27

Palm Canyon X- Features of the Trade

• Digital option purchased by Palm had a value of $5M.• Digital option sold by Palm had a value of $4.95M.• Cash did not trade hands in respect of the options.• Investor’s interest was purchased by Taxpayer in the same

year in which it was initially acquired by Investor.• No basis reduction for short option, but basis credit for long

option.• “Inflated basis” transferred to other FX positions held by

Palm upon liquidation.

28

Palm Canyon X Economics• Variation of Notice 2000-44 option transaction undertaken

after Notice was issued.• $55G net investment to make $33G net profit, $8 million if

“sweet spot” hit.• Actual $6G profit, before fees.• $345G in fees paid.• Taxpayer claims outside basis in partnership equals $5M

premium paid, not reduced by $4.945 premium received, (Helmer v. Comm’r).

• Palm Canyon then started FX trading (4 trades & $2k of profit).

• Transaction settled on a net basis. Principal did not change hands.

29

Palm Canyon X, Court’s Approach

• Court’s analysis:– Courts have reached inconsistent conclusions as to

whether short position here is a “liability” under § 752; assume it is not and go to economic substance.

– Whether Regs. § 1.752-6T can be applied retroactively is unclear; assume it cannot and go to economic substance.

– Need not decide whether partnership anti-abuse regulations apply.

30

Palm Canyon X —Economic SubstanceSubjective prong failed: no business purpose absent tax

benefits.• Taxpayer asserted that transactions were part of strategy to

become adept at FX hedging for Thighmaster sales business.

• Court found no foreseeable need to hedge FX.– “Self-serving memoranda prepared on eve of MLD transaction”.– Fees were disproportionate to advice received.

• No investigation into FX aspects of contracts.– “Window dressing” research to avoid penalties.

• Long and short premiums were inflated.• CF Advisors’ membership solely to facilitate tax benefit.

– Buy-out docs were prepared at transaction inception.• Transaction developed as a tax shelter.

31

Palm Canyon X,—Economic Substance

Objective prong failed: no reasonable prospect of earning a profit.

• No realistic chance of hitting “sweet spot” (1.3% chance maximum, or 0.11-0.13% chance).– Bank, as calculation agent, could assure sweet spot

was not hit; range was closer than normal bid-ask spread.

• Fees nullify potential profit.

32

Importance of Palm Canyon X• Court states that it must first analyze whether TP

literally complied with Code, and if so only then whether economic substance doctrine changes result; but.

• Law was unclear and courts took disparate positions. Since result would be nullified even transaction worked, court assumed that it did & went directly to economic substance.

• 40% gross valuation misstatement penalty sustained.• Negligence found as well, notwithstanding tax opinion.• Substantial understatement b/c no substantial authority

for positions taken. Opinion did not provide reasonable cause.

33

Southgate Master Fund LLCSouthgate Master Fund LLC651 F.Supp.2d 596 (ND Tex. 2009651 F.Supp.2d 596 (ND Tex. 2009))

HighHigh--Basis Distressed DebtBasis Distressed Debt

Background, Review and AnalysisBackground, Review and Analysis

34

Southgate – Background on Chinese Distressed Debt Transaction

• Taxpayer operated a bank as an S corporation that had a significant track record in distressed debt investing, including in developing markets.

• Deutsche Bank introduced Taxpayer to China Cinda, a government-owned entity charged with working out and disposing of non-performing loans (“NPLs”) originated by China Construction Bank.

• Court found that Taxpayer acted as a prudent investor, studied the market and investigated the loan portfolio.

35

Southgate – Formation Transactions

ChinaCinda

Eastgate(Delaware)

NPLs

MCA, LLC(Delaware)

Taxpayer

Southgate LLC(Delaware)

99%1%

NPLs

$100k &$99k Note

ServicingAgreement

36

Southgate – Next Steps• Eastgate (Cinda) sold 90% of Southgate to “Beal” for $19.4MM over

all-in cost of approximately $10MM.• Court found investor “entered into the NPL investment for legitimate

purposes with a reasonable possibility of making a profit.”• As part of a reasonable business strategy, NPLs with a face of amount

of $253MM was sold for net proceeds of $1MM in 2002.• Code § 704(d), however, would have limited Beal’s losses to his basis

in Southgate.• Beal “sold” $180MM of Treasuries to UBS in a sale/repurchase

transaction and contributed the cash received in the sale to Southgate to create additonal basis. He retained liability to UBS, even though not required to do so by UBS.

• Taxpayers undertook a second transaction after it became clear that first transaction was a pre-tax loser; court inferred that 2nd transaction was undertaken solely for tax benefits.

37

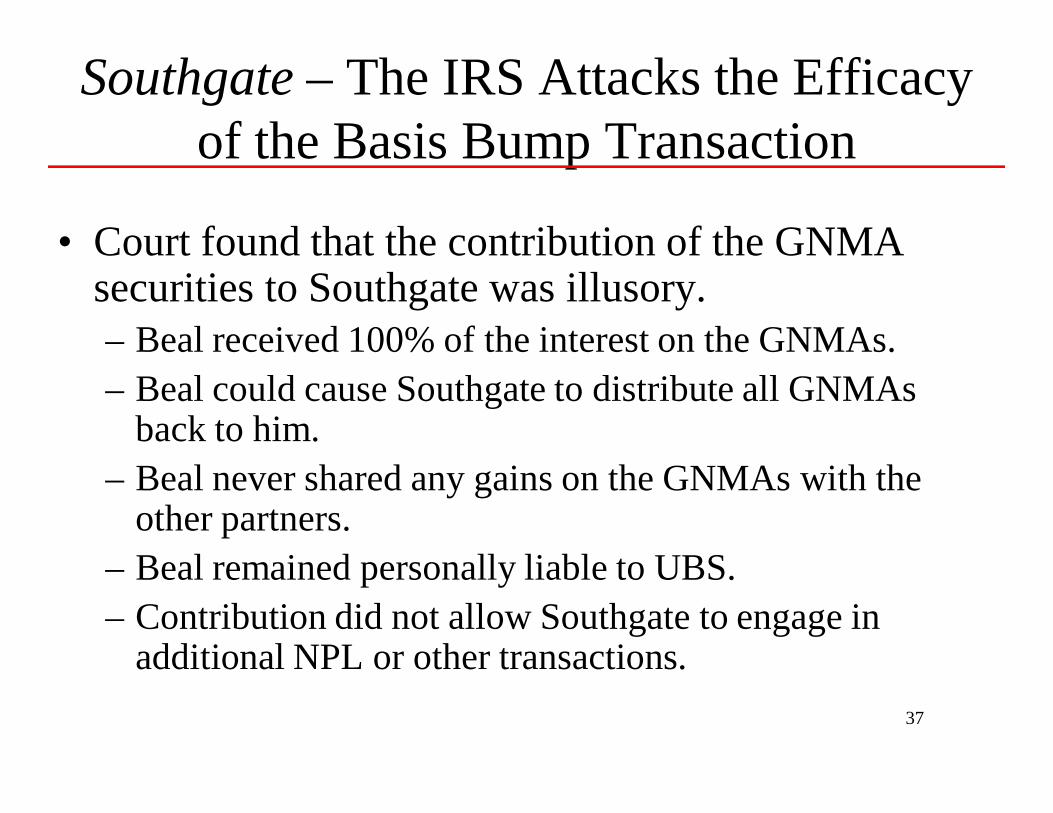

Southgate – The IRS Attacks the Efficacy of the Basis Bump Transaction

• Court found that the contribution of the GNMA securities to Southgate was illusory.– Beal received 100% of the interest on the GNMAs.– Beal could cause Southgate to distribute all GNMAs

back to him.– Beal never shared any gains on the GNMAs with the

other partners.– Beal remained personally liable to UBS.– Contribution did not allow Southgate to engage in

additional NPL or other transactions.

38

Southgate – Tax Lawyer Conduct

• Court noted that law firm did not sell the transactions as a pre-packaged product.

• Law firm employed qualified tax lawyers.• Law firm opined on a more-likely-than-not basis.• Accounting firm provided a like opinion.• Court found opinions met penalty-avoidance

standards of Code § 6662.• Transactions met technical Code requirements.

39

Southgate – IRS Attacks

• NPLs were worthless when contributed.– Facts did not bear this out and court dismissed argument.

• Cinda was a dealer in securities and was required to mark-to-market its portfolio.– Again, no borne out by facts and dismissed.

• Code § 482 required a re-allocation of the loss.– No common control between Cinda and US taxpayers, so

argument was rejected.• So the taxpayer wins, right?

– No, but the burden of proof shifted to the government under Code § 7491.

40

Southgate – Court Invokes Economic Substance Doctrine

• Court bifurcated transaction for eco substance test – one as to the formation and operation of Southgate and then to basis bump transaction.

• Formation and operation of Southgate had economic substance.

• Basis bump failed economic substance test.– Southgate did not have a reasonable prospect of profiting from

GNMAs.– “Proffered reasons read like afterthoughts designed to disguise the

true purpose.– Court refrained from applying partnership anti-abuse regulation.– Court found penalties were not warranted.

41

Wells Fargo & Co.Wells Fargo & Co.U.S. Court of Claims (Jan 2010)U.S. Court of Claims (Jan 2010)

SILOSILO

Background, Review and Background, Review and AnalysisAnalysis

42

Wells Fargo –Loop Debt Structure

Wells

Fargo

Tax

Exempt

Head lease

Triple net sublease Sublease purchase option

Lender

Nonrecourse loan

Treated as a sale

Sublease rent

Lender

Affiliate

At termination, Wells had the right to force a service contractor any sort of forced renewal.

43

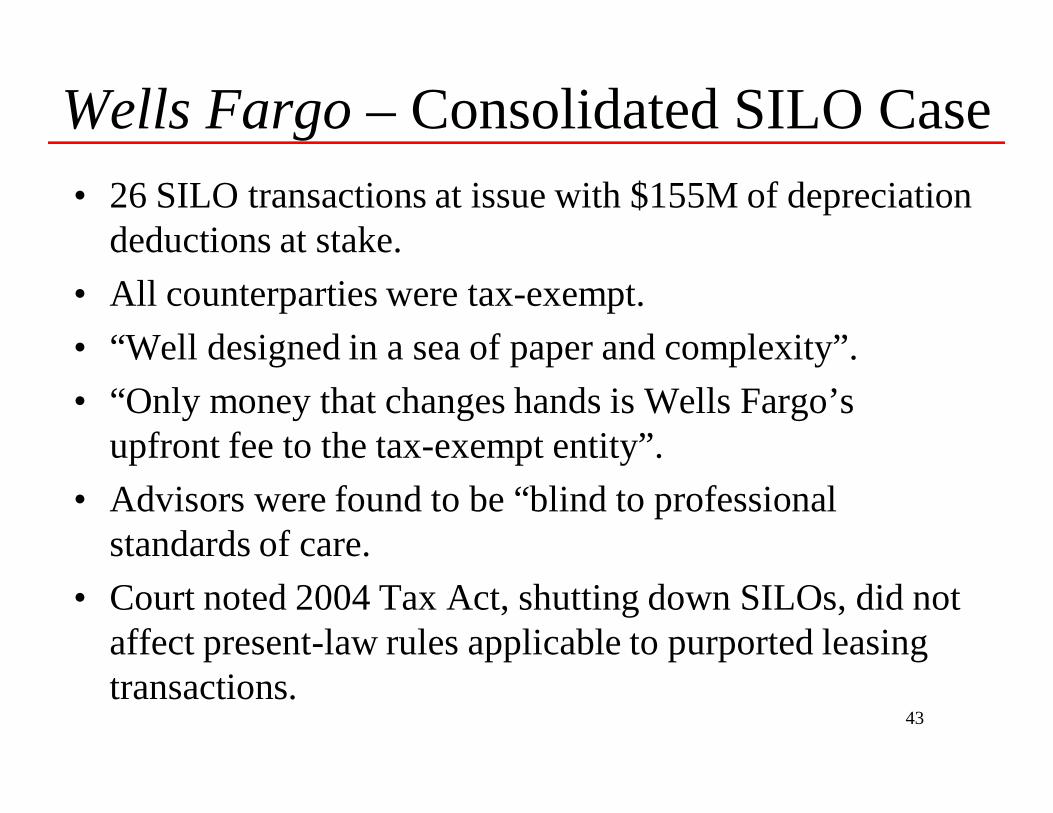

Wells Fargo – Consolidated SILO Case• 26 SILO transactions at issue with $155M of depreciation

deductions at stake.• All counterparties were tax-exempt.• “Well designed in a sea of paper and complexity”.• “Only money that changes hands is Wells Fargo’s

upfront fee to the tax-exempt entity”.• Advisors were found to be “blind to professional

standards of care.• Court noted 2004 Tax Act, shutting down SILOs, did not

affect present-law rules applicable to purported leasing transactions.

44

Wells Fargo – Significant Leasing Activities

• Wells and other predecessors had a huge history of financing leasing transactions.

• Tax Department confirmed for each transaction that Wells had sufficient tax capacity to use interest and depreciation deductions.

• Although transactions had a 2.6% return without tax benefits, this yield was less than Wells’ cost of funds.

45

Wells Fargo – SILO Executions

• Inflated property values were used to turbo-charge tax depreciation and interest deductions.

• All transactions involved property being used by tax-exempt entity before SILO was executed.

• All purchase options were pre-funded by Wells (Wells received its own money back); court found the options to be more in the nature of forward contracts. The service contract right enabled Wells to force exercise of the option.

• None of the transactions had any cash flow during the term of the transaction.

46

Wells Fargo – Economic Substance Analysis

• “The only purpose was for Wells Fargo to pay an inducement fee to a tax-exempt entity and thereby acquire tax deductions of offset other Wells Fargo taxable income.”

• Court found Wells Fargo did not acquire benefits and burdens of ownership.– Wells had no risk of loss, either on lease or residual.– 100% loop debt.– Lender accounted for debt and rent as offsetting

entries.

47

Wells Fargo – Economic Substance Analysis

• Court found that Wells Fargo did not incur a liability and denied it any deductions for interest.

• Objective economic substance analysis – failed test because the source of the pre-tax economic benefit to Wells was the return of its own money at the end of the transaction. And transaction had negative pre-tax economics.

• Subjective non-tax business purpose – belied by lack of arms’ length negotiations. Valuation reports were suspect.

48

Consolidated Edison Co. of N.Y.Consolidated Edison Co. of N.Y.90 Fed. Cl. 228 (2009)90 Fed. Cl. 228 (2009)

LILOLILO

Background, Review and Background, Review and AnalysisAnalysis

49

Con Ed--Structure

Con Ed Leasing

EZH (Dutch)

43.2-yr lease

Subject of lease: 47.7% interest in Dutch cogen facility, remaining useful life 54 years

20.1-yr subleaseSublease purchase option

ABB

German sale-

leaseback + put

Sublease Renewal Option

Retention Option

HBU

ABN

Nonrecourse loan

1997 ($120M) & 2041 ($831M) rent p’ments

Result: $937G deduction in 1997, based on prior § 467 regs.

Sublease rent

50

Con Ed--Issues

• Will the form of the transaction be respected for tax purposes?

• Is the loan from HBU to Con Ed bona fide indebtedness that is respected for tax purposes?

• Does the investment by Con Ed in the lease and sublease have economic substance?

51

Con Ed --IRS Position

• No present leasehold interest.• No genuine indebtedness.• Con Ed lacks benefits and burdens of

ownership.• No reasonable expectation of profit and

transaction not motivated by valid non-business purpose.

• Circular financing arrangement.

52

Con Ed Response

• Transaction projected to generate pre-tax profit of at least $61M and incremental income taxes of $21.3M.

• Tax benefit is deferral, not elimination.• Transaction structured to get front-loading

of earnings under FAS 13.

53

Con Ed --Business Reasons• Pursuing new opportunities in deregulated market.• Pre-tax profit.• Expansion into Western European energy markets.• Learning about and sharing technology in its core

competency.• Opportunity to operate the plant if purchase option

not exercised.• Gaining expertise about environmental benefits.• Image building—association with

environmentally-friendly plant.• Favorable accounting treatment—earnings bump.

54

Con Ed --Court’s Reasoning• Test for economic substance is a reasonable chance of making a

reasonable profit apart from tax considerations.• Resolving battle of experts, not inevitable that EZH would exercise

purchase option, and if they didn’t Con Ed would have economic benefits and burdens of ownership.

• Significant risk to Con Ed if EZH does not exercise purchase option.• Potential residual value if EZH does not exercise purchase option.• Gov’t witness on economic didn’t perform detailed analysis.• Court not troubled by nonrecourse debt—common in leveraged leases.• True lease status not automatically disqualified by defeasance account.• Potential profit need not be discounted to present value in comparing

profit on other possible investments. Instead, analysis must depend on specific characteristics of transaction under review.

• BB&T distinguished: lengthy trial, not MSJ; Con Ed proved genuine ownership interest, non-tax business reasons; BB&T is financial services provider entered transaction with wood-pulp manufacturer

• AWG (SILO case) distinguished.

55

DO THE FOLLOWING TRANSACTIONS WORK

UNDER THE TEST IN SCHERING PLOUGH?

56

Basic Foreign Tax Credit Planning

U.S.

F1 F2

High-taxed earnings

Low-taxed earnings

dividend

57

Basic Foreign Tax Credit Planning II

U.S.

F1

High-taxed earnings

Low-taxed earnings

Purchase price

F1 buys F2 stock

58

Basic Foreign Tax Credit Planning III

U.S.

F1 F2

High-taxed earnings

Low-taxed earnings

dividend

1

Bank

Loan

guarantee

2

59

Treaty ShoppingF1

Hungary Corp

U.S. Corp

interest

dividend

60

U.S. Blocker Corporation

U.S. Corp

U.S. business I U.S. business II

Foreign Investors

61

Foreign Blocker Corporation

Caymans Corp

Tax-Exempt Investors

Passive investments

Lenderloan

62

Blocker Partnership

USP

CFC1 CFC2

CFC3

USPS

IRS Notice 2009-7, 2009-3 IRB 312 (transaction of interest)

63

U.S. Sales Affiliate

Foreign Parent

Manufacturing

U.S. SubsidiarySales within U.S.

Is it better or worse if parent moves a responsible official to the U.S.on counsel’s advice that this would help U.S. tax position?

64

Planning Into § 871(g)(1)(B)(i)

F1—Non-treaty Country

S1—U.S.

Short-term cash advances with OID

May F1 extend the term of the advances from 4 to 6 monthsOn advice of tax counsel?

100%

65

References• Silverman and Varma, “The Future of Tax Planning: From Coltec to

Schering-Plough,” Tax Notes, Jan. 18, 2010, p. 341 • Cummings, “The New Normal: Economic Substance Doctrine First,”

Tax Notes, Jan. 25, 2010, p. 521 • Shakow, “Consolidated Edison Turns on the Lights,” Tax Notes, Feb.

1, 2010, p. 625• Bowen, Lee and Morris, “Recent Taxpayer Economic Substance

Victories Provide Blueprint for Success,”, BNA Daily Tax Report, Dec. 10, 2009

• Jackson, “Practitioners Look for Clarification on Losses in Weakened Economy Following Schering-Plough,” 2009 TNT 237-5 (Dec. 14, 2009)

• Elliott and Sheppard, Treasury Speaks Out About Schering-Plough Decision, 2009 TNT 209-3 (Nov. 2, 2009).

• Elliott, Practitioners Express Worry and Confusion Over Ruling in Schering-Plough, 2009 TNT 190-2 (Oct. 5, 2009)