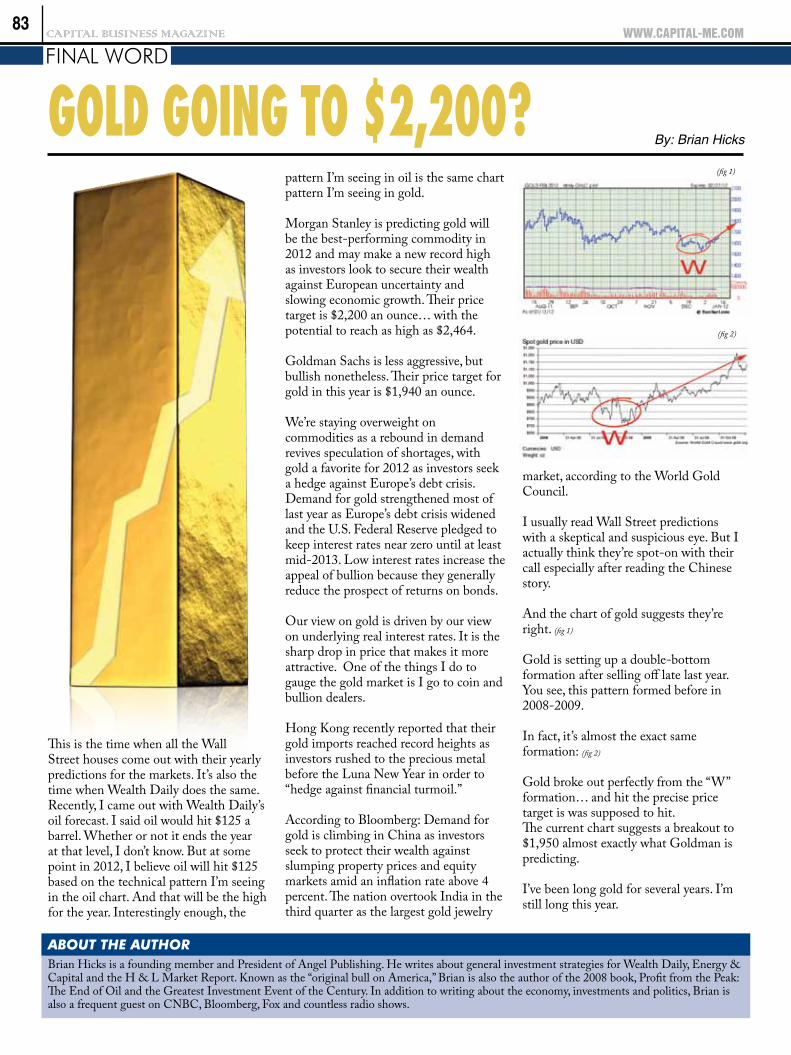

is gold always the ‘gold’ standard

DESCRIPTION

Yasin Ebrahim Capital Business Magazine Is Gold Always The ‘Gold’ Standard? seeks to explore the current status quo 'Gold is Good'. It examines the benefits of investing in gold for individuals, this involves a hedge against inflation, deflation and most particularly currency devaluation. My views simultaneously reflect both the potential benefits and drawbacks of investing in gold for investors.TRANSCRIPT

ww

w.o

meg

awat

ches

.com

PLANET OCEAN"Standing on the Moon looking back at Earth – this lovely place you justcame from – you see all the colours, and you know what they represent.

Having left the water planet, with all that water brings to the Earth interms of colour and abundant life, the absence of water and atmosphere

on the desolate surface of the Moon gives rise to a stark contrast."– Buzz Aldrin, astronaut

More information available atOMEGA Middle East, Emirates TowersDubai, UAE. Tel: +971 4 3300455

ww

w.o

meg

awat

ches

.com

PLANET OCEAN"Standing on the Moon looking back at Earth – this lovely place you justcame from – you see all the colours, and you know what they represent.

Having left the water planet, with all that water brings to the Earth interms of colour and abundant life, the absence of water and atmosphere

on the desolate surface of the Moon gives rise to a stark contrast."– Buzz Aldrin, astronaut

More information available atOMEGA Middle East, Emirates TowersDubai, UAE. Tel: +971 4 3300455

Gold, Gold, Gold. Investors unwavering conviction that when all else fails, bet gold. Investing in gold for the moment is logical because it provides a hedge against inflation, deflation and most importantly currency devaluation.

Statistics released by the World Gold Council support the notion of ‘Gold is good’ as the research confirms that emerging economics such as Mexico, Russia, China, India, Korea and Thailand have increased their holdings of gold, thus, reducing supply and helping to boost market sentiment.

Prior to the gold price spike of March 2008, investors would have earned a healthy profit over a three year period as the value of their investment doubled. Gold as part of an investment portfolio will remain an effective inflationary hedge because it represents real value; as prices start to increase, the value of gold will appreciate. Gold is traded in U.S. dollars; a decline in U.S. dollars would result in an increased amount of U.S. dollars needed to purchase the same quantity of gold which leads to an increase in the value of gold. Prominent investment managers’, Shaun Price and Marc Lubazka of Touchstone

Large Cap Growth Fund and Aurum Advisors respectively, are of the view that investing in gold will not only serve as a hedge against the current economic uncertainty but that gold will provide the long-term growth that has recently been lacking from investors’ portfolios.

Commodity Ownership Ownership of gold, similar to other commodities, comes in two forms - direct or indirect. Direct cash investment (ownership) is expensive and time consuming. Purchasing of the underlying commodity is a rare approach as it involves storage costs, insurance expenses and valuation expenses. In addition, no income is earned representing cash opportunity cost. Returns are only earned when the commodity is sold. Indirect ownership involves investing in commodities through an investment vehicle (intermediary) or purchasing the stock or bonds of a commodity firm such as Rio Tinto. This approach allows access to commodities which would have been previously available due to capital requirements and expertise in managing the investments.

The Myth of ‘the Safe Bet’ The concept of gold being a bubble is not farfetched. As the old adage goes “what goes up must come down”. Prior to the financial meltdown of August 2007, investors’ had utmost confidence in real estate, specifically in residential

real estate investments. The false sense of

security was based on assumptions that house prices

won’t fall and the process

used to rate whether a borrower was a credit risk was flawless. Furthermore, sophisticated financial products such as Mortgage Backed Securities (MBS’s) and Collateral Default Obligations (CDOs) helped repackage these securities making it appear as a ‘riskless’ trade. Similarly, the characteristics of gold may lead investors to believe that in the current economic climate, gold is a ‘safe bet’. Investors must be aware, gold should be held as part of a balanced portfolio for diversification benefits.

To Gold or not to Gold? The U.S. government is set to continue with the quantitative easing approach which has yet to have the desired impact. Consequently, discouraging bond and equity investors with characteristics such as high inflation, high volatility, and low liquidity look set to continue.

Further support of gold investment is that it strengthens the current aims of central banks which involve stimulating growth and diversifying their foreign exchange reserves, amid fears of currency debasement. Subsequently, boosting demand for gold.

Gold as part of a balance portfolio will provide the diversification and hedging needs that investors require during these uncertain economic times of inflation, inept fiscal and monetary policies exacerbated by Euro zone debt crisis. In the near future; ‘As good as gold’ may prevail as the marquee statement among investors. Therefore, investing in gold for the moment is a “Safe Bet”, if there is one.

Is Gold AlwAys The ‘Gold’ sTAndArd? By: Yasin Ebrahim

About the AuthoRYasin Ebrahim is a freelance journalist researching developments in the alternative investment field through exposure in traditional and social media. His background in risk and investment management coupled with leading industry qualifications; Financial Risk Manager (FRM), Chartered Alternative Investment Analyst (CAIA) provide him with a sound background to explore alternative investments.

busInEss PlAnETCAPITAL BusIness MAgAzIne

29

International Colloquium

organised by theFaculty of Business and Commercial Sciencesat the Holy Spirit University of Kaslik

jointly with the Arab Society of Faculties of Business, Economic and Political Sciences

Date : April 2 and 3, 2012 (Official opening session on April 2, 2012 at 10:00 a.m.)Place : John-Paul II Amphitheater – USEK Main Campus

For registration please visit www.usekic2012.com

busInEss PlAnETCAPITAL BusIness MAgAzIne

31

asian coMPanies set to Benefit froM the eurozone crisis

By: FTI Consulting

Asian companies are more intent on finding investment opportunities in Europe than those in the

Middle East or North America, according to research from FTI Consulting, Inc, the global business advisory firm dedicated to helping organisations protect and enhance their enterprise value.

The FTI Eurozone Poll, a survey of 800 business leaders in Asia, the Middle East and North America gauging their response to the Eurozone crisis, found

that 45% of businesses in Asia are either currently doing or looking to make strategic acquisitions in Europe in the next 12 months, compared with just 14% in the Middle East and 7% in North America.

Overall, the research highlighted a buoyant mood in Asia: Sixty seven percent of companies in the region are looking to invest in innovation, and 50% are focused on organic growth. However, it is clear that Europe is seen by Asian companies to provide more fertile ground

for acquisitions, with fewer (35%) looking at strategic acquisitions outside of the Eurozone.

Business leaders in the Middle East and North America claim less exposure towards the economic problems of Europe but are more negative. Seventy percent of executives in North America say their businesses have remained untouched by the Eurozone crisis, but of those where it has had an impact, 25% say it is negative and just 6% positive. Similarly, in the

Middle East, 38%

say the crisis has had an unfavourable impact, compared

with 16% favorable. By contrast, 73% of businesses in Asia have been

impacted, with an even split of positive and negative.

“It’s easy for businesses outside of Europe to view the crisis with a mixture of relief that they are outside of the zone yet still fear the contagion may infect their own markets”, said Mark Malloch-Brown, EMEA Chairman, FTI Consulting. “But in any period of systemic dislocation, there will be winners and losers. Asset prices now are significantly lower than they had been, meaning significant benefits for those investors alert and prepared for the risks. The next 12 months will see massive shifts in corporate ownership, creating opportunities and risks for companies both in and out of the Eurozone.”

“Our research highlights that Asian businesses have the right business fundamentals and, more important, the right mentality to take advantage of the changing landscape,” he added.

Other findings from the FTI Eurozone Poll Significant minority think the euro will not survive 2012

While the FTI Consulting research highlights that the majority of business leaders outside of the Eurozone think the euro will survive, a significant majority are less confident of its future. Nearly a third (31%) of respondents strongly or slightly agree that the euro will not last the year, with a further 64% thinking that at least one of the 17 members will stop using the currency by the end of 2012, and that sentiment was evenly spread across

the three main regions. Certainly, many companies are preparing for the worst. Sixty-three percent have or would request changes in contracts with Eurozone countries to include scenarios for exit. Furthermore, the stability of the euro is seen as a critical issue by nearly two-thirds (61%) of respondents.

The UK’s status elevated in response to the Eurozone crisis

The research from FTI Consulting highlights that the UK’s reputation amongst executives outside of Europe has risen, as the UK’s continental counterparts are seen to be more impacted by the sovereign debt crises and concerns over the currency. In total 72% of respondents to the FTI Consulting survey agree that the UK will increase in importance as a gateway to Europe, split across the regions as follows: 78% in Asia, 71% in North America and 64% in the Middle East.

While the findings support the idea of the United Kingdom as a safe haven for foreign investors, it is far from clear that the data represents a ringing endorsement for the UK government’s decision to separate itself from the euro problem. The research establishes that many executives outside of Europe want greater stability in the Eurozone, and that an overwhelming majority (83%) now believe that Germans will lead the recovery.

When asked about the performance of the leaders of the major European economies, the survey highlighted ambivalence and indicated little variation between the Big Three: German Chancellor Angela Merkel rated highest with a performance rating of 6.3 out of 10, compared with 5.6 out of 10 for both David Cameron, UK Prime Minister, and Nicolas Sarkozy, the French president.

Businesses call on their political leaders to help Europe’s economy

Business leaders outside of the Eurozone are surprisingly supportive of intervention from their own political leaders, according to the FTI Consulting research. In total, 69% of respondents agree that their

country’s leaders should support the European Union in its recovery process. The sentiment is felt strongest in Asia, where a large majority (78%) support intervention, unsurprising given its own exposure and commercial interest in the region. However, there is still strong support in North America (63%) for government intervention, even as the United States gears up for its presidential race, indicating that businesses in the United States and Canada will still feel an economic chill if the Eurozone crisis deepens.

Furthermore, there are split views on the responsibilities of business and governments to provide a solution to the crisis. A slight majority, 56%, favor the market as opposed to a government-led solution, with the Asians and North Americans most supportive at 60% and 56%, respectively, and the Middle East businesses split almost equally.

www.capital-me.com32

About FtI consultIngFTI Consulting, Inc. is a global business advisory firm dedicated to helping organisations protect and enhance enterprise value in an increasingly complex legal, regulatory and economic environment. With more than 3,800 employees located in 23 countries, FTI Consulting professionals work closely with clients to anticipate, illuminate and overcome complex business challenges in areas such as investigations, litigation, mergers and acquisitions, regulatory issues, reputation management, strategic communications and restructuring. The company generated $1.4 billion in revenues during fiscal year 2010. More information can be found at www.fticonsulting.co.uk.

About the FtI euRozone PollResearch was conducted online by the Strategy Consulting and Research team at FTI Consulting from 9 to 16 January 2012 with more than 800 C-suite executives involved in strategic decisions for their private organisation. Respondents were drawn from affiliate panel databases. The three regions and countries within were selected based upon the known amount of trade they presently conduct with countries in the European Union and prospects for increased prominence. Respondents from each of the three key regions totalled 351 in Asia, 236 in the Middle East and 221 in North America. A breakdown of responses by each country involved is possible where the total number of respondents exceeds 50.

busInEss PlAnETCAPITAL BusIness MAgAzIne

33

a Pivotal year ahead By: SEI Investment Management Unit

There is no denying that the past year was a trying one for investors. Global equity markets

were mostly lower. Global bond markets saw extreme volatility, with the debt of a few select countries (the U.S., Germany, the U.K. and Canada, to mention the most important ones) registering the only healthy returns in an investment environment that swung from risk-on to risk-off with unnerving frequency and ferocity.

Global financial markets remain fragile and subject to sharp moves. With Europe on the cusp of recession, China labouring through the downside of a property bubble, and the U.S. heading towards its most important election cycle in decades, there will be no quick end to the uncertainty that has made investing a difficult enterprise.

Europe on the RopesEconomic indicators in the Eurozone have taken a turn for the worse in recent months. Countries that use the euro as their national currency are seeing signs of outright recession. Only Germany’s composite purchasing manager indices are above the recession line. Retail sales in the Eurozone have been in negative territory for several months. Labour-market indicators have deteriorated as well, with the number of unemployed rising for six consecutive months through October and the Eurozone unemployment rate rising to 10.3%.

A Generation Without a PlaceMost worrisome is the sharp rise in the unemployment rate of younger workers (24 years old and younger). At 21.4%, Europe’s youth unemployment is more than twice the Eurozone’s overall average. Youth unemployment has risen to an astounding 48.9% in Spain and Greece is not far behind at 45.1%.

fOuRTH quARTER EcOnOMIc OuTlOOk

In Exhibit 2, we note the competitive rankings of various countries based on the WEF’s 12 pillars of competitiveness.

Exhibit 2: Greece Reaps the Bitter Fruits Austerity

1 2 3 4 5 6 7 8 9 10 11 12 13 15 16 18 19 26 29

36 41 43 45

53 56 66

90

Nat

iona

l Com

petit

iven

ess

Ran

k Sources: World Economic Forum, SEI Rankings consist of 142 countries in total. Blue columns denote eurozone nations.

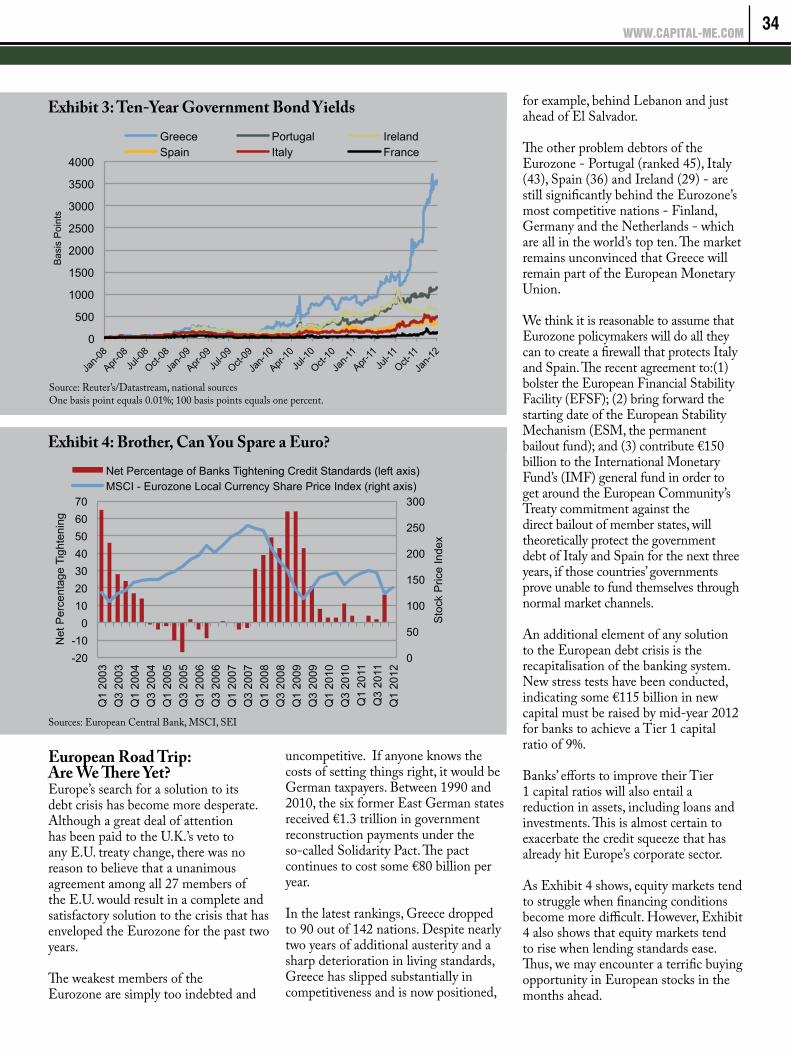

European Road Trip: Are We There Yet?Europe’s search for a solution to its debt crisis has become more desperate. Although a great deal of attention has been paid to the U.K.’s veto to any E.U. treaty change, there was no reason to believe that a unanimous agreement among all 27 members of the E.U. would result in a complete and satisfactory solution to the crisis that has enveloped the Eurozone for the past two years.

The weakest members of the Eurozone are simply too indebted and

uncompetitive. If anyone knows the costs of setting things right, it would be German taxpayers. Between 1990 and 2010, the six former East German states received €1.3 trillion in government reconstruction payments under the so-called Solidarity Pact. The pact continues to cost some €80 billion per year.

In the latest rankings, Greece dropped to 90 out of 142 nations. Despite nearly two years of additional austerity and a sharp deterioration in living standards, Greece has slipped substantially in competitiveness and is now positioned,

for example, behind Lebanon and just ahead of El Salvador.

The other problem debtors of the Eurozone - Portugal (ranked 45), Italy (43), Spain (36) and Ireland (29) - are still significantly behind the Eurozone’s most competitive nations - Finland, Germany and the Netherlands - which are all in the world’s top ten. The market remains unconvinced that Greece will remain part of the European Monetary Union.

We think it is reasonable to assume that Eurozone policymakers will do all they can to create a firewall that protects Italy and Spain. The recent agreement to:(1) bolster the European Financial Stability Facility (EFSF); (2) bring forward the starting date of the European Stability Mechanism (ESM, the permanent bailout fund); and (3) contribute €150 billion to the International Monetary Fund’s (IMF) general fund in order to get around the European Community’s Treaty commitment against the direct bailout of member states, will theoretically protect the government debt of Italy and Spain for the next three years, if those countries’ governments prove unable to fund themselves through normal market channels.

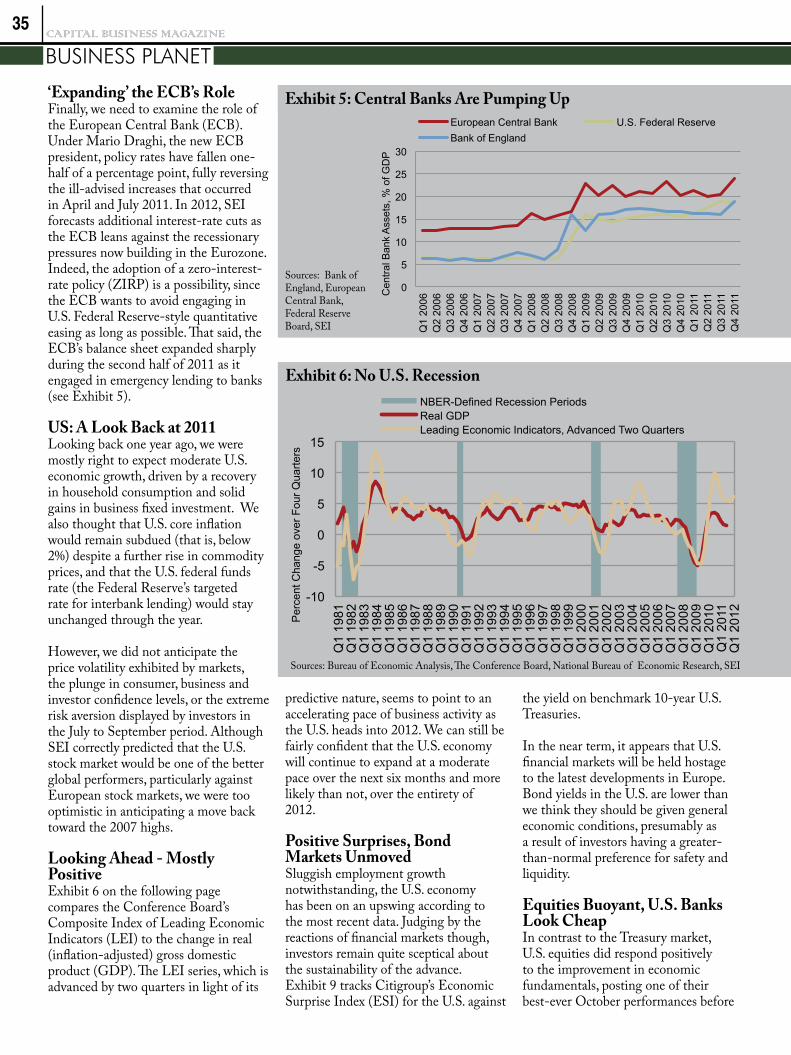

An additional element of any solution to the European debt crisis is the recapitalisation of the banking system. New stress tests have been conducted, indicating some €115 billion in new capital must be raised by mid-year 2012 for banks to achieve a Tier 1 capital ratio of 9%.

Banks’ efforts to improve their Tier 1 capital ratios will also entail a reduction in assets, including loans and investments. This is almost certain to exacerbate the credit squeeze that has already hit Europe’s corporate sector.

As Exhibit 4 shows, equity markets tend to struggle when financing conditions become more difficult. However, Exhibit 4 also shows that equity markets tend to rise when lending standards ease. Thus, we may encounter a terrific buying opportunity in European stocks in the months ahead.

www.capital-me.com34

Exhibit 3: Ten-Year Government Bond Yields

Source: Reuter’s/Datastream, national sources One basis point equals 0.01%; 100 basis points equals one percent.

0

500

1000

1500

2000

2500

3000

3500

4000

Bas

is P

oint

s

Greece Portugal Ireland Spain Italy France

Exhibit 4: Brother, Can You Spare a Euro?

Sources: European Central Bank, MSCI, SEI

0

50

100

150

200

250

300

-20 -10

0 10 20 30 40 50 60 70

Q1

2003

Q

3 20

03

Q1

2004

Q

3 20

04

Q1

2005

Q

3 20

05

Q1

2006

Q

3 20

06

Q1

2007

Q

3 20

07

Q1

2008

Q

3 20

08

Q1

2009

Q

3 20

09

Q1

2010

Q

3 20

10

Q1

2011

Q

3 20

11

Q1

2012

Sto

ck P

rice

Inde

x

Net

Per

cent

age

Tigh

teni

ng

Net Percentage of Banks Tightening Credit Standards (left axis) MSCI - Eurozone Local Currency Share Price Index (right axis)

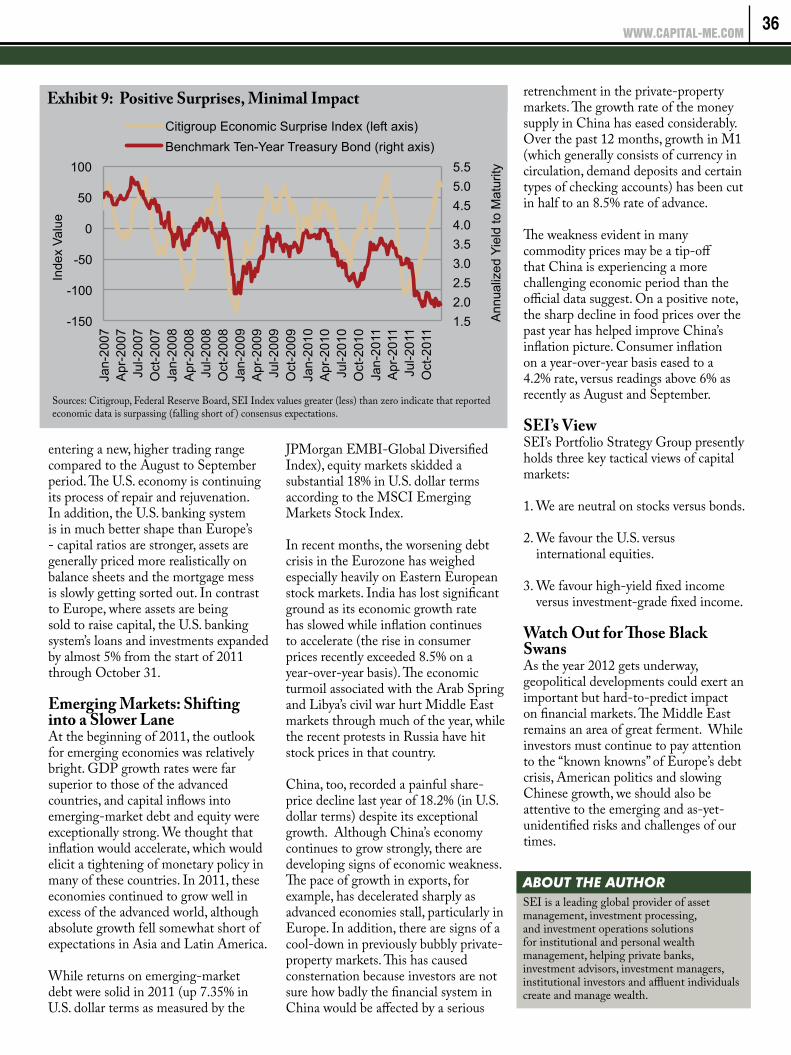

‘Expanding’ the ECB’s RoleFinally, we need to examine the role of the European Central Bank (ECB). Under Mario Draghi, the new ECB president, policy rates have fallen one-half of a percentage point, fully reversing the ill-advised increases that occurred in April and July 2011. In 2012, SEI forecasts additional interest-rate cuts as the ECB leans against the recessionary pressures now building in the Eurozone. Indeed, the adoption of a zero-interest-rate policy (ZIRP) is a possibility, since the ECB wants to avoid engaging in U.S. Federal Reserve-style quantitative easing as long as possible. That said, the ECB’s balance sheet expanded sharply during the second half of 2011 as it engaged in emergency lending to banks (see Exhibit 5).

US: A Look Back at 2011Looking back one year ago, we were mostly right to expect moderate U.S. economic growth, driven by a recovery in household consumption and solid gains in business fixed investment. We also thought that U.S. core inflation would remain subdued (that is, below 2%) despite a further rise in commodity prices, and that the U.S. federal funds rate (the Federal Reserve’s targeted rate for interbank lending) would stay unchanged through the year.

However, we did not anticipate the price volatility exhibited by markets, the plunge in consumer, business and investor confidence levels, or the extreme risk aversion displayed by investors in the July to September period. Although SEI correctly predicted that the U.S. stock market would be one of the better global performers, particularly against European stock markets, we were too optimistic in anticipating a move back toward the 2007 highs.

Looking Ahead - Mostly PositiveExhibit 6 on the following page compares the Conference Board’s Composite Index of Leading Economic Indicators (LEI) to the change in real (inflation-adjusted) gross domestic product (GDP). The LEI series, which is advanced by two quarters in light of its

predictive nature, seems to point to an accelerating pace of business activity as the U.S. heads into 2012. We can still be fairly confident that the U.S. economy will continue to expand at a moderate pace over the next six months and more likely than not, over the entirety of 2012.

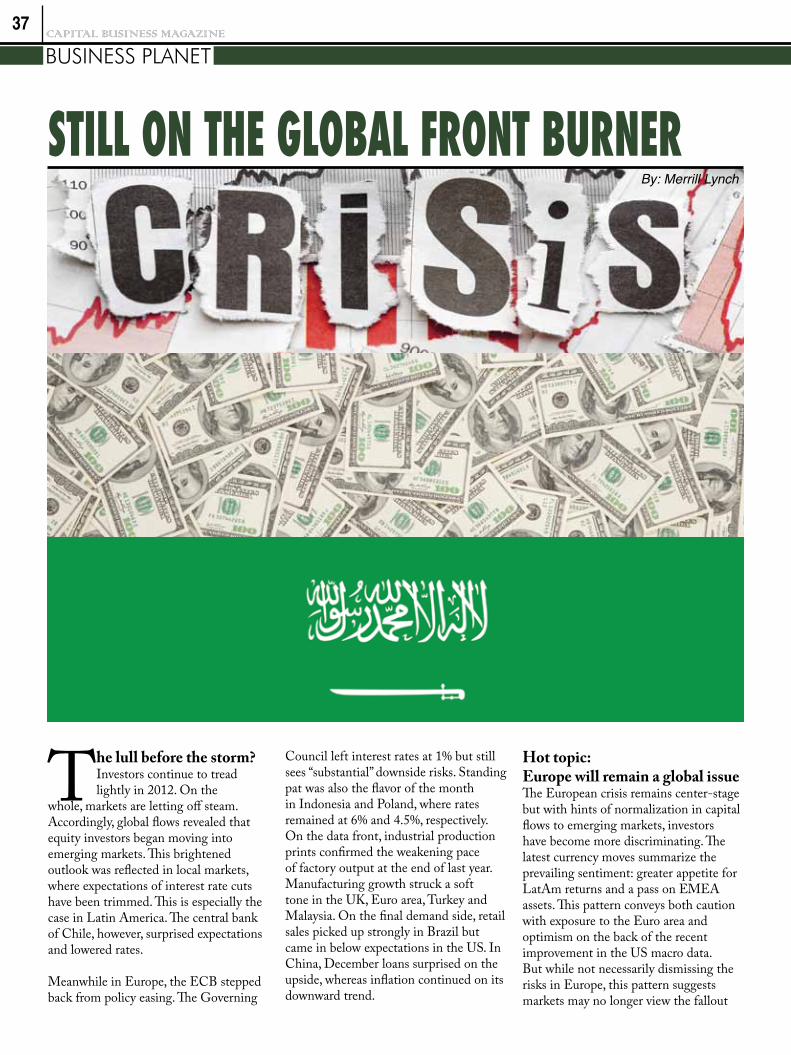

Positive Surprises, Bond Markets UnmovedSluggish employment growth notwithstanding, the U.S. economy has been on an upswing according to the most recent data. Judging by the reactions of financial markets though, investors remain quite sceptical about the sustainability of the advance. Exhibit 9 tracks Citigroup’s Economic Surprise Index (ESI) for the U.S. against

the yield on benchmark 10-year U.S. Treasuries.

In the near term, it appears that U.S. financial markets will be held hostage to the latest developments in Europe. Bond yields in the U.S. are lower than we think they should be given general economic conditions, presumably as a result of investors having a greater-than-normal preference for safety and liquidity.

Equities Buoyant, U.S. Banks Look CheapIn contrast to the Treasury market, U.S. equities did respond positively to the improvement in economic fundamentals, posting one of their best-ever October performances before

busInEss PlAnETCAPITAL BusIness MAgAzIne

35

Exhibit 6: No U.S. Recession

-10

-5

0

5

10

15

Q1

1981

Q

1 19

82

Q1

1983

Q

1 19

84

Q1

1985

Q

1 19

86

Q1

1987

Q

1 19

88

Q1

1989

Q

1 19

90

Q1

1991

Q

1 19

92

Q1

1993

Q

1 19

94

Q1

1995

Q

1 19

96

Q1

1997

Q

1 19

98

Q1

1999

Q

1 20

00

Q1

2001

Q

1 20

02

Q1

2003

Q

1 20

04

Q1

2005

Q

1 20

06

Q1

2007

Q

1 20

08

Q1

2009

Q

1 20

10

Q1

2011

Q

1 20

12

Per

cent

Cha

nge

over

Fou

r Qua

rters

NBER-Defined Recession Periods Real GDP Leading Economic Indicators, Advanced Two Quarters

Sources: Bureau of Economic Analysis, The Conference Board, National Bureau of Economic Research, SEI

Sources: Bureau of Economic Analysis, The Conference Board, National Bureau of Economic Research, SEI

Exhibit 5: Central Banks Are Pumping Up

Sources: Bank of England, European Central Bank, Federal Reserve Board, SEI

0

5

10

15

20

25

30

Q1

2006

Q

2 20

06

Q3

2006

Q

4 20

06

Q1

2007

Q

2 20

07

Q3

2007

Q

4 20

07

Q1

2008

Q

2 20

08

Q3

2008

Q

4 20

08

Q1

2009

Q

2 20

09

Q3

2009

Q

4 20

09

Q1

2010

Q

2 20

10

Q3

2010

Q

4 20

10

Q1

2011

Q

2 20

11

Q3

2011

Q

4 20

11 Cen

tral B

ank

Ass

ets,

% o

f GD

P

European Central Bank U.S. Federal Reserve Bank of England

entering a new, higher trading range compared to the August to September period. The U.S. economy is continuing its process of repair and rejuvenation. In addition, the U.S. banking system is in much better shape than Europe’s - capital ratios are stronger, assets are generally priced more realistically on balance sheets and the mortgage mess is slowly getting sorted out. In contrast to Europe, where assets are being sold to raise capital, the U.S. banking system’s loans and investments expanded by almost 5% from the start of 2011 through October 31.

Emerging Markets: Shifting into a Slower LaneAt the beginning of 2011, the outlook for emerging economies was relatively bright. GDP growth rates were far superior to those of the advanced countries, and capital inflows into emerging-market debt and equity were exceptionally strong. We thought that inflation would accelerate, which would elicit a tightening of monetary policy in many of these countries. In 2011, these economies continued to grow well in excess of the advanced world, although absolute growth fell somewhat short of expectations in Asia and Latin America.

While returns on emerging-market debt were solid in 2011 (up 7.35% in U.S. dollar terms as measured by the

JPMorgan EMBI-Global Diversified Index), equity markets skidded a substantial 18% in U.S. dollar terms according to the MSCI Emerging Markets Stock Index.

In recent months, the worsening debt crisis in the Eurozone has weighed especially heavily on Eastern European stock markets. India has lost significant ground as its economic growth rate has slowed while inflation continues to accelerate (the rise in consumer prices recently exceeded 8.5% on a year-over-year basis). The economic turmoil associated with the Arab Spring and Libya’s civil war hurt Middle East markets through much of the year, while the recent protests in Russia have hit stock prices in that country.

China, too, recorded a painful share-price decline last year of 18.2% (in U.S. dollar terms) despite its exceptional growth. Although China’s economy continues to grow strongly, there are developing signs of economic weakness. The pace of growth in exports, for example, has decelerated sharply as advanced economies stall, particularly in Europe. In addition, there are signs of a cool-down in previously bubbly private-property markets. This has caused consternation because investors are not sure how badly the financial system in China would be affected by a serious

retrenchment in the private-property markets. The growth rate of the money supply in China has eased considerably. Over the past 12 months, growth in M1 (which generally consists of currency in circulation, demand deposits and certain types of checking accounts) has been cut in half to an 8.5% rate of advance.

The weakness evident in many commodity prices may be a tip-off that China is experiencing a more challenging economic period than the official data suggest. On a positive note, the sharp decline in food prices over the past year has helped improve China’s inflation picture. Consumer inflation on a year-over-year basis eased to a 4.2% rate, versus readings above 6% as recently as August and September.

SEI’s ViewSEI’s Portfolio Strategy Group presently holds three key tactical views of capital markets:

1. We are neutral on stocks versus bonds.

2. We favour the U.S. versus international equities.

3. We favour high-yield fixed income versus investment-grade fixed income.

Watch Out for Those Black SwansAs the year 2012 gets underway, geopolitical developments could exert an important but hard-to-predict impact on financial markets. The Middle East remains an area of great ferment. While investors must continue to pay attention to the “known knowns” of Europe’s debt crisis, American politics and slowing Chinese growth, we should also be attentive to the emerging and as-yet-unidentified risks and challenges of our times.

www.capital-me.com36

Exhibit 9: Positive Surprises, Minimal Impact

1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5

-150

-100

-50

0

50

100

Jan-

2007

A

pr-2

007

Jul-2

007

Oct

-200

7 Ja

n-20

08

Apr

-200

8 Ju

l-200

8 O

ct-2

008

Jan-

2009

A

pr-2

009

Jul-2

009

Oct

-200

9 Ja

n-20

10

Apr

-201

0 Ju

l-201

0 O

ct-2

010

Jan-

2011

A

pr-2

011

Jul-2

011

Oct

-201

1

Ann

ualiz

ed Y

ield

to M

atur

ity

Inde

x Va

lue

Citigroup Economic Surprise Index (left axis) Benchmark Ten-Year Treasury Bond (right axis)

Sources: Citigroup, Federal Reserve Board, SEI Index values greater (less) than zero indicate that reported economic data is surpassing (falling short of ) consensus expectations.

About the AuthoRSEI is a leading global provider of asset management, investment processing, and investment operations solutions for institutional and personal wealth management, helping private banks, investment advisors, investment managers, institutional investors and affluent individuals create and manage wealth.

still on the gloBal front BurnerBy: Merrill Lynch

The lull before the storm?Investors continue to tread lightly in 2012. On the

whole, markets are letting off steam. Accordingly, global flows revealed that equity investors began moving into emerging markets. This brightened outlook was reflected in local markets, where expectations of interest rate cuts have been trimmed. This is especially the case in Latin America. The central bank of Chile, however, surprised expectations and lowered rates.

Meanwhile in Europe, the ECB stepped back from policy easing. The Governing

Council left interest rates at 1% but still sees “substantial” downside risks. Standing pat was also the flavor of the month in Indonesia and Poland, where rates remained at 6% and 4.5%, respectively. On the data front, industrial production prints confirmed the weakening pace of factory output at the end of last year. Manufacturing growth struck a soft tone in the UK, Euro area, Turkey and Malaysia. On the final demand side, retail sales picked up strongly in Brazil but came in below expectations in the US. In China, December loans surprised on the upside, whereas inflation continued on its downward trend.

Hot topic: Europe will remain a global issueThe European crisis remains center-stage but with hints of normalization in capital flows to emerging markets, investors have become more discriminating. The latest currency moves summarize the prevailing sentiment: greater appetite for LatAm returns and a pass on EMEA assets. This pattern conveys both caution with exposure to the Euro area and optimism on the back of the recent improvement in the US macro data. But while not necessarily dismissing the risks in Europe, this pattern suggests markets may no longer view the fallout

busInEss PlAnETCAPITAL BusIness MAgAzIne

37

from the ongoing crisis as having global repercussions.

Confidence in the potential for a US decoupling is rising. According to the IMF, the US accounts for about one-third of both global stock and bond market capitalization. But in terms of turnover, the clout of US markets can reach two-thirds of the global total. Arguing for less anxiety on the US exposure to Europe are better economic momentum and greater policymaking efforts to redistribute liquidity. The expansion of FX swap line agreements, the ECB’s offer of unlimited long-term refinancing, and the European Council announcement that EU and other countries would channel resources to the IMF have improved the actual and prospective liquidity situation in Europe. But are these factors enough to restrainthe global reach of the European crisis?

The bigger pictureEurope matters because of its size and the euro’s reserve currency status. The Euro area’s systemic relevance means that its governance crisis is a global menace. Europe is rightly being held to account for fiscal mismanagement, but there may be bigger cracks in the background. A fundamental issue is the international allocation of liquidity. Liquidity crises are typically generated by solvency concerns. In a global context, however, this raises questions of international cost sharing. In practice, the IMF is the institution with the legitimacy to dilute the burden across its members and channel official liquidity to troubled parts of the system.

Saudi Arabia: A supportive 2012 budgetWhile the higher budgeted expenditure appropriations broadly reflect the permanent nature of the current expenditure part of the Arab-unrest related stimulus, the focus next year will be on achieving a better quality of spending. This will occur as housing appropriations and capital injections to specialized lending institutions increasingly filter into the economy. Also, this would most likely entail an increase in credit disintermediation, as recognized in the budget, but a robust non-oil

economy is likely to support continued broader banking sector loan growth.

A very strong macro performance in 2011The preliminary outturns for macro indicators for the past year, show growth was strong as a buoyant private sector expansion was underpinned by the government stimulus. The decomposition of growth however is better than expected with much stronger growth from the non-oil sector than projected. The non-hydrocarbon sector grew by 7.8% in 2011 vs our forecast of 4.9%. To put it into perspective, the reported non-oil sector growth is the highest in the last three decades. Also, unlike the 2009 stimulus where the non-oil government sector expanded by 5.2% to cushion the downturn amid weak private sector, private sector growth was buoyant and broad based. Note that the oil sector is however reported to have expanded by just 4.3% whereas crude oil production likely grew by c10% in 2011.

Large fiscal surplus achieved despite record expendituresThe MoF reports the preliminary fiscal balance was SAR306 billion (14.1% of GDP), vs our projections of SAR165 billion (7.7% of GDPe). The difference stems mainly from higher revenues (SAR1,110 billion vs SAR989 billion anticipated).

Non-oil revenues were in line with our projections (SAR77.7 billion) but oil revenues were higher than expected, due to higher than projected oil prices and production. Stimulus spending appears to have been on track, comfortably financed by high oil prices and production. The decision to allocate SAR250 billion from this year’s fiscal surplus into a dedicated account at SAMA to finance the construction of 500,000 residential units could help expedite the process and put the onus on execution of the capital spending appropriations. This also treats the transfer as an off-budgetary item in the budget presentations, conveniently bringing down the fiscal breakeven oil price by $27/bbl.

2012 budget is the highest on recordThe 2012 budgeted expenditure is the largest on record (19% increase over 2011 budget) but is below preliminary actual 2011 spending. Budgeted revenues are also the largest on record. This fits with the fact that budgeted capital expenditures are at similar levels to 2010 and 2011 budgets (though 33% higher than the last disclosed realized capex in 2010).

The increase in appropriations thus likely reflects higher current spending, in line with the continuing impact of the permanent portions of the Arab unrest-related stimulus. Fiscal revenues are budgeted at SAR702 billion, expenditures at SAR690 billion, meaning a surplus of SAR12 billion is actually being budgeted in contrary to the past few years. Capital expenditures are budgeted at SAR265 billion while current spending is budgeted at SAR425 billion.

Disclosed decomposition of spending shows appropriations for education are the largest at 24% of total (includes construction of 742 new schools), followed by health and social affairs (13% of total, includes construction of 17 new hospitals).

Fiscal stance to remain expansionary in 2012We still expect the fiscal stance to remain supportive of growth next year. We expect total actual expenditures to amount to SAR750 billion in 2012. This would represent 9% overspending (slightly below the norm given more realistic budgeting and shift of supplemental housing appropriations off-budget) and would be 6.7% lower than realized 2011 spending as one-off items from stimulus packages wane.

Our revenue and spending projections are consistent with a fiscal breakeven oil price of $78.5/bbl in 2012. We expect GDP growth of 3.3% in 2012 on higher base effect and drag from oil sector. We see a fiscal surplus of 8.6% of GDP, based on oil production of 9.3mn bpd and oil in $100/bbl handle.

www.capital-me.com38

Master accoMPlishMent

cOVER sTORyCAPITAL BusIness MAgAzIne

39

www.capital-me.com40

“My Business” is a Joint Collaboration on Entrepreneurship Program for Arab Youth between INJAZ Al-Arab and MASTERCARD Worldwide.

MasterCard, a payment industry giant, has taken the initiative to join hands with INJAZ Al-Arab, a non-profit organization in the Middle East and co-member of Junior Achievement Worldwide, both collaborating on a corporate volunteering program to

provide experiential education and training to Arab youth in work readiness, financial literacy and entrepreneurship. MasterCard will support INJAZ Al-Arab’s ‘It’s My Business’, a leading entrepreneurial mentorship program developed for youth in Lebanon and countries across the Middle East and North Africa (MENA).

The announcement was made February 8th, 2012 at an event MasterCard and INJAZ Al-Arab held at the Intercontinental Phoenicia Hotel, Beirut, marked by the attendance of H.E. Mr. Walid Daouk, Lebanese Minister of Information, Soraya Salti, INJAZ Al-Arab Regional Director and Junior Achievement Senior Vice President, MENA, Patricia Devereux, Group Head, Corporate Philanthropy and Citizenship, Michael Miebach, President, Middle East and Africa, MasterCard Worldwide, Chady Zein, Principal at Booz & Co., and Basel El Tell, Vice President and Regional Manager, Levant, MasterCard Worldwide.

“All young people deserve an opportunity to reach their full potential,” said Miebach. “MasterCard is proud to work with INJAZ Al-Arab to launch the ‘It’s My Business’ program, which we believe is a great investment in youth in Lebanon and across the MENA. Equipping the youth with entrepreneurship skills will enable them to pursue their own business, thus reducing unemployment rates and allowing them to build stronger futures for themselves and their families while positively contributing to the economic development of their countries.”

The program also has the full endorsement of the Lebanese government, allowing a mostly underprivileged public school sector to benefit from international expertise that would otherwise be of scarce availability if not an impossibility. “The introduction of ‘It’s My Business’ program in Lebanon, will provide our youth with a wealth of knowledge on financial literacy and business-related skills, which will allow them to thrive when they enter the real world.,” said H.E., Walid Daouk, Minister of Information, Lebanon.

Carrying forward the vision and inspiration behind INJAZ Al-Arab, is a profoundly committed Salti who said: “Youth unemployment in the MENA region currently stands at 25%, which is double the world average.”

Moreover, research from Booz & Company shows that on average, youth are waiting five years after graduation

MasterCard’s support to INJAZ Al Arab’s entrepreneurship program deepens its commitment to further financial inclusion through the power of entrepreneurship.

cOVER sTORyCAPITAL BusIness MAgAzIne

41

to find their first job. Receiving support from MasterCard allows us to address this youth unemployment crisis by improving the workforce readiness, entrepreneurship, and financial literacy skills of Arab youth. The pilot of this initiative will be implemented in Egypt, Lebanon, Morocco and Saudi Arabia, after which the curriculum will be made available throughout the INJAZ network of 14 countries.

MasterCard, having a deep corporate commitment to a philanthropy agenda, entrepreneurial education, financial education and inclusion, was also intensifying its presence and investment in the MENA region. “We looked at INJAZ and saw that they wanted to expand their core program, which had been the age range of 14-18, down to the age of 11, and this is our sweet spot,” Miebach told the

magazine. “This particular pilot program already has scale. We can’t expect 3000 students to become entrepreneurs, but we can expect them to think out of the box, take initiatives, and become positively disposed to do something about their own future. At the same time, it’s important to extend the range upwards, as students go to university, and refresh the concepts to encourage them to do something about all the things they had learned before.”

MasterCard employees will bring their skills set and market experience to the classroom, not to talk about the payments industry, but about their knowledge, transferring it to students, helping them think differently of the world. “The fundamental skills of how to set up a company, how to think about customers, how to differentiate yourself from the market, are all brought using basic concepts that these

students understand,” Miebach added. INJAZ depends on these volunteer networks that provide expertise. “We encourage volunteering and CSR within MasterCard. We free up time for our people with good incentives, and encourage entrepreneurship within MasterCard; it is about people empowerment and risk taking,” added Miebach.

MasterCard believes that economic growth and sustainability cannot be achieved without addressing youth unemployment, creating more jobs through SMEs and tangible business models that work.

Booz& Co. identified 10 imperatives that all stakeholders in the entrepreneurial ecosystem should follow to influence and improve the entrepreneurial ecosystem in the MENA region:

1. Offer a helping hand. Established entrepreneurs should give time, advice and seed funding to aspiring entrepreneurs.

2. Change behaviors and evolve the culture. Discuss entrepreneurship every day and generate hype around a handful of success stories.

3. Bring entrepreneurship to the classroom. Everyone in high school and university should learn entrepreneurial principles.

4. Bring entrepreneurship to the office. Companies should encourage employees to unleash their own talent.

5. Do not imitate Silicon Valley. Identify and leverage your country’s own unique resources.

6. Welcome new ideas. Engage domestic and foreign workers to encourage a free flow of expertise and enterprise.

7. Break the stereotype. Great entrepreneurial ideas can come from anyone in any industry.

8. Embrace the Diaspora. Tap successful entrepreneurs living abroad for their advice and connections.

9. Eliminate red tape. Governments should give many kinds of support to all types of entrepreneurs.

10. Expand the venture capital (VC) model. VCs need to go beyond funding and provide a support structure for entrepreneurs.

Zein of Booz & Co. highlighted some of the MENA’s shortcomings in terms of youth unemployment, entrepreneurship and future needs for regional nations to promote a vibrant entrepreneurial ecosystem and become globally competitive, based on a summary of ideas discussed at the World Economic Forum Special Meeting on Economic Growth and Job Creation in the Arab World, held last October in Jordan.

One of the Arab world’s top priorities in the coming years is job creation. According to the WEF, the region needs to create 75 million jobs by 2020 just to

keep employment close to current levels. The key to accelerating job creation will be fostering a business environment in which entrepreneurs can easily start new companies, spread innovation and spur economic activity in general.

Booz & Co. said that more than one-half of the population in the MENA region is under the age of 25, posing both enormous opportunities and giant challenges. But, unemployment rates are in the high double digits in most MENA countries, including a staggering 35% in Yemen.

A key to accelerating job creation in the MENA region is fostering an entrepreneurial environment. Once start-ups mature into SMEs, they become significant contributors to employment and gross domestic product (GDP). (See Exhibit 1)

Entrepreneurial ventures are driven by one or a combination of three factors:

• Lifestyle or passion: Entrepreneurs who are motivated in this way create businesses in fields where they have a particular interest, talent or knowledge. • Social good: These individuals are motivated by a social problem and use entrepreneurial principles to create, organize and manage a venture that will bring about socio-economic change for a particular group. • Fame and fortune: These entrepreneurs aim big and are driven strongly by the profit motive. In addition, Booz & Co. identified three external forces that drive entrepreneurship:

In addition, there are three external forces or circumstances that drive entrepreneurship: • Innovation: Some entrepreneurs create new demand by nourishing an innovative idea they have conceived or acquired. • Opportunity: Entrepreneurs who recognize a demand/supply gap in the market, an unmet need or an opportunity for change can seize that opportunity. • Necessity: Entrepreneurs in this category have been forced by their environment to seek self-sufficiency and satisfy their basic needs of food, shelter and security.

At first glance, the MENA region’s entrepreneurial activity today seems robust, says Booz & Co. About 13% of the region’s working population is engaged in entrepreneurial activity, far more than in the US, Germany or Japan. (see Exhibit 2)

However, this apparent entrepreneurial vigor is deceptive. More than 80% of entrepreneurs in the MENA region have very small-scale operations, with

www.capital-me.com42

Percentage of Total Employment in SMEs

Exhibit 1: SME Contribution to Economies

SME Contribution to GDP

Note: Selected Countries (2008)Source: European Commission SME Performance Review; US Department of Statistics; OECD; UNECE; World Bank; Zawya; Booz & Company

UK 54%

US 55%

Germany 60%

61%

38%Egypt

UAE

Saudi Arabia 25%

Hungary

France

42%

71%

54%

2

32%

1

63%

3

21 3Averages Low-Income Countries Middle-Income Countries High-Income Countries

UK

US

Germany

Egypt

UAE

Saudi Arabia

Hungary

France

16%

51%

52%

53%

54%

50%

33%

30%

25%

39% 52%

1 2 3

Exhibit 2: Early-stage Entrepreneurial Activity(% of Adult Population, 2009)

3%4%4%4%4%5%5%6%6%8%8%9%9%

10%

12%12%13%

15%15%16%17%

19%

22%24%

Arab Countries

Yem

en

Col

ombi

a

Chi

na

Mor

occo

Bra

zil

Leba

non

UA

E

Tuni

sia

Iran

Jord

an

Nor

way

Syr

ia

US

A

Sw

itzer

land

Sou

th A

frica

Uni

ted

Kin

gdom

Finl

and

Sau

di A

rabi

a

Fran

ce

Ger

man

y

Rus

sia

Italy

Japa

n

Alg

eria

Arab Countries Average = 13%

Note: The percentage of the population performing early-stage entrepreneurial activity are those people who are involved in setting up a business orowners-managers of new businesses (less than 42 months).Source: Global Entrepreneurship Monitor,2009; Booz & Company

Entrepreneurial activity in Arab countries is decep-tively high, as it is mostly

driven by necessity

cOVER sTORyCAPITAL BusIness MAgAzIne

43

enterprise value of less than $15,000. The high level of entrepreneurship is mainly driven by necessity – shop owners, farmers and cart sellers trying to satisfy their basic needs of food, shelter and security. Booz & Co. says there are currently about 150 existing initiatives that encourage entrepreneurial activity in the MENA region. These initiatives include technology incubators, government (25%), non-governmental organizations (NGOs 62%), networking associations for aspiring entrepreneurs and university programs dedicated to entrepreneurship. The entrepreneurial ecosystem has four success elements: personal enablers, financial enablers, business enablers and environmental enablers.

A. Personal EnablersThe first ring in the ecosystem affects the entrepreneur’s individual development, says Booz & Co. These personal enablers include:

Mentors/Advisers: Typically other entrepreneurs willing to share knowledge and real-life lessons. Informal Education: Informal education is available through various sources, such as seminars and networking events.Formal Education: Universities around the world offer entrepreneurship courses and programs to nurture a spirit of entrepreneurship.

Fewer than 10% of the universities in the MENA region offer entrepreneurial courses and a mere five actually offer a major in entrepreneurship.

B. Financial EnablersThese financial enablers or financiers include:

Equity Investors: Equity investors include family and friends, angel investors and venture capital funds Banks and SME Financing: Debt financing from banks requires collateral and usually involves a lengthy approval process since start-ups lack a track record. Microfinancing: These lenders offer very small loans to aspiring entrepreneurs in poor regions. Government Programs: These programs include funds, short-term loans, guarantees and other financing initiatives for specific industries.

The MENA region’s financial enablers are underdeveloped in particular the network of equity investors, a critical source for start-up capital in the West, which is still nascent in the MENA region, according to Booz & Co. Only 20% of local SMEs have a loan or a line of credit, the lowest percentage of any region in the world; and only 10% of their investment expenditures are financed by a bank loan, also among the lowest worldwide. C. Business EnablersThe third ring in the entrepreneur’s ecosystem consists of professional enablers and includes:

Professional Services: This is a large category that includes marketing companies, media associations, consulting firms and accounting firms. Incubators: Incubators provide office space and back-office support for start-ups, usually in return for a nominal fee and/or equity stake in the firm, until they achieve sufficient scale to afford these services on their own. Network Associations: Network associations connect entrepreneurs with experienced business people and/or consultants who serve as mentors or more formal advisers to help the entrepreneur tackle business challenges.

www.capital-me.com44

Over the past 20 years, about 60 initiatives have been launched within the MENA region to promote business support.

D. Environment EnablersThe final outer ring in the entrepreneurship ecosystem involves a diverse group of environment enablers: the regulatory framework, infrastructure, lobbying organizations, prevailing culture and media. Booz& co. reports:

Regulatory Framework: Government agencies and private chambers of commerce can stimulate entrepreneurship by simplifying rules and providing incentives for start-ups. However, much more reform is needed across the region in many areas. Infrastructure: The existing infrastructure in MENA countries needs upgrading to improve the start-up and business environment in general. The Internet is used by just 24% of the population in the Arab states versus 79% in the US and 67% in Europe, with average Internet speed in the MENA region (2.73 Mbps) a mere fraction of the global average of 8.69 Mbps.Prevailing Culture: Most people in the workforce value the stability of a lifetime government job over the excitement of risk taking or innovating. A survey of young people in the Gulf showed that only 9% said that “opening their own business” was their top priority in life.

About mAsteRcARDMasterCard (NYSE: MA) is a global payments and technology company operating in more than 210 countries and territories.

About InJAz- Al ARAbINJAZ Al-Arab, a regional branch of JA Worldwide®, is an organization that works with young people in the Middle East and North Africa region providing them with entrepreneurship, financial literacy and work-readiness skills.

About JunIoR AchIevement Junior Achievement Worldwide is the world’s largest organization committed to inspiring and preparing young people to succeed in a global economy, catering to 9.3 million students annually.

Making Cash FlowAn interview with Michael Bach, President of Middle East and Africa, MasterCard Worldwide, reveals the inner workings of a regional giant who sees but only one competitor: cash!

“Clearly there is significant growth potential in the payment industry. MasterCard is bringing solutions to displace cash; that is what we do for a living and what we do well. We drive growth into the markets, and the key competitor that we see out there is cash, which we try to displace every single day, simply through payment tools; smart and safe payment tools. That’s our focus,” Miebach explained.

MasterCard’s business plan is to first target banks, their traditional customers and then acquirers and merchants. This 3rd party model has been established for years, and it’s undergoing change.

“You have other players entering the payment industry, you have mobile operators coming in, have merchants extending beyond immediate merchant business models into adjacent business models, so that’s a massive trend out there,” said Miebach. Though the B2B model is what drives the company’s growth, the final consumer is ever present on the corporate mindset of MasterCard. “The MasterCard brand reflects security and trust, and there is a relationship that this brand has with the consumer. We work with the market stakeholders that we talked about and all of them talk to consumers. What do these consumers need? We are truly driven by consumer needs and we try to educate on what these needs are and could be. It’s a virtual circle, more like a B2B2C.”

MasterCard is a technology company, in the payment industry, providing payment tools to various sectors including debit cards, charge cards, pre-paid cards, mobile payment, and more. “We are bringing the benefits of payments to society and the economy.”

“It’s about access, transactions, and driving commerce. As far as running a credit card business, that’s what banks do,” clarified Miebach. In reality, banks are the ones positioned to handle responsible lending to individuals regardless of age and profession. “But generally in the region, regulators have, after 2008, driven regulations across countries in the MENA region, specifically in GCC, to enhance rules that foster responsible lending. And banks are seeking ways to balance their business models to differentiate themselves with payments vis-a-vis the consumer rather than with the credit proposition, with cards that bring mileage, give access to lounges, and other true benefits, to drive value to businesses and consumers.”

Transaction security has accompanied the payment industry early on trying to combat fraud and prevent loss to both providers and end-users. “You have the highest risk of fraud when you are not in the electronic payment world but rather the cash world. In the cash world, there is no control or transparency. In electronic payments, there are still a set of risks associated, but MasterCard has been driving security solutions that prevent fraud,” affirmed Miebach. MasterCard has pioneered industry leading tools and mechanisms to ensure authentication on the internet. “With a clear set of established rules, MasterCard brings the clarity of rules that are rigorously tested, for each business, merchant and consumer.”

The payment industry has also been paying close attention to the rise of Islamic banking. “Islamic finance is the fastest growing sector in this region. We have taken a look at that. We are a payment company with different sets of products, and by definition, a debit or a prepaid card qualifies under Islamic considerations. As we work with banks, their interest in addressing their Islamic customer set, specifically Islamic countries where you have to choose either or, such as Qatar for example, induces us to work jointly in driving their product set, specifically to their customers.”

InfORMATIOn TEcHnOlOGyCAPITAL BusIness MAgAzIne

45

cashing in on ict By: Booz & Co.

THE EnTERPRIsE OPPORTunITy fOR MEnA TElEcOM OPERATORs TO IncREAsE

The number of enterprises in the MENA region will increase, and so will their spending on

ICT, until it approaches that of their peers in Europe and the U.S. Operators can leverage their strengths to grab share in the rapidly growing SME segment, lock in key large accounts and large-scale digitization projects, and benefit from converging consumer and enterprise offerings.

The spending increase by enterprises is driven by a sea change in mobility and cloud computing needs, as well as the desire for unified and collaborative services such as enterprise social media, as smart phones and tablet PCs have gained popularity. Competition will be intense; business communication equipment vendors, systems integrators, software and online service providers all will seek to grab a share of the MENA region’s fast-growing enterprise ICT opportunity.

Telecom operators can capitalize on core capabilities to secure a share of the enterprise opportunity.

Their multiplatform network infrastructure, established relationships, wide reach, reputed brands, and access to capital will be key assets.

“Despite those advantages, MENA operators will not automatically win enterprise customers. Operators will need to approach the business market in a fundamentally new manner and create a new value proposition. They will need to refocus efforts to capture the opportunity presented by the creation of millions of new small and medium-sized enterprises (SMEs) over the next several years.

They need to expand their offering to lock in key accounts and leverage their incumbent position with government agencies,” said Bahjat El-Darwiche, Partner, Booz & Company.

ENTERPRISE CUSTOMERS: A GROWING OPPORTUNITYAs many MENA consumer telecom markets approach saturation, MENA operators hope to continue growing by putting new emphasis on their efforts in the enterprise segment. The ICT segment for enterprises in the MENA region is significantly underserved. Although enterprises account for as much as 6.5 percent of all mobile SIMs in some European countries, they average less than 1 percent in the MENA region. Yet, the MENA enterprise ICT market is growing rapidly. It will almost double within five years, from an estimated $14.8 billion market in 2010 to $26.1 billion in 2015.

Increases in both the number of enterprises and the expected ICT spend per enterprise will drive that rapid growth. According to Booz & Company, an expected number of enterprises in the MENA region will grow at a 10 percent annual rate through 2014: this will add almost 4 million new businesses to the current base of 8.25 million.

That growth substantially outpaces the growth rate of businesses in both Europe and North America. Nevertheless, ICT spending per MENA enterprise, currently one-fifth that in Western Europe and one-tenth that in the US, is bound to increase.

TAKING ADVANTAGE OF OPERATORS’ STRENGTHS Telecom operators can capitalize on six core capabilities to secure a share of the enterprise opportunity. Each

Bahjat EL DarwichePartner, Booz & Company

Hadi RaadPrincipal, Booz & Company

of these six core capabilities provides MENA telecom operators with an edge over competitors in approaching the enterprise business.

A combination of some or all of these capabilities adds up to a potent competitive advantage with enterprise customers:

1. Multi-platform network infrastructure • Telecom operators can use their multi-platform network infrastructure to deliver services on a variety of devices.

2. Established customer relationships •Through their current offerings and interactions, telecom operators have access to an established enterprise customer base.

3. Wide reach • Telecom operators use a variety of sales channels and have a strong presence across the geography they serve.

4. Large-scale program management experience • Many established telecom operators have broad experience in managing large-scale infrastructure deployment and service delivery programs with many stakeholders and interdependencies.

5. Trusted brands • Many telecom operators enjoy established brand recognition, typically in the consumer market where they have ample experience.

6. Access to capital • Particularly in the MENA region, telecom operators are

cash rich and have the means to invest in long-term, capital-intensive projects.

PREPARING TO COMPETE IN THE ENTERPRISE ICT MARKETWith stiff competition almost certain to emerge for the enterprise ICT market, MENA telecom operators need to consider the business market in a fundamentally new manner and adopt differentiated approaches to succeed in securing and maintaining clients – whether SMEs, large enterprises, or government agencies.

Telecom operators will have the ability not only to gain a foothold in these emerging businesses, but also solidify ties with individuals who work in these organizations, bolstering their consumer business.

www.capital-me.com46

FOCUS ON SMEs TO CAPTURE EMERGING OPPORTUNITYTo serve the SME segment effectively, regional telecom operators will first need to group customers based on behavioral characteristics such as telecom expenditures and service sophistication. “Operators need to design bundled and converged solutions that offer SMEs a one-stop-shop experience. Telecom operators could also provide SMEs software-as-a-service (SAAS) cloud applications, allowing them to meet their business needs with minimal up-front investments,” explained Hadi Raad, Principal, Booz & Company.

Because SMEs are scattered throughout the region and not clustered in one city, they are hard to reach through retail outlets. As a result, operators might consider using outbound telesales, as well as resellers that have the widespread coverage necessary to reach SMEs.

LOCK IN LARGE ACCOUNTS WITH TURNKEY SOLUTIONSLarge enterprises and key accounts typically have a large number of employees and will likely spend significantly on ICT. These customers increasingly demand turnkey solutions that address their specific business needs, such as increasing productivity, improving customer satisfaction, and cutting costs. They typically prioritize service levels over price. Large enterprises and key accounts also expect a differentiated sales and customer service experience that only dedicated account and service managers can deliver.

“To service large enterprises effectively, regional telecom operators will need to migrate from being providers of basic voice and data services to providing full ICT solutions. That entails initially expanding their product portfolio and service

offerings to deliver complete, targeted ICT solutions. The portfolio offerings need to be comprehensive and specific. In targeting large enterprises, telecom operators also need to shift from a typical account manager sales approach to a consulting relationship, acting as partners with the customers and designing turnkey solutions rather than offering off-the-shelf services,” stated El-Darwiche.

LEVERAGE GOVERNMENT RELATIONSHIPS TO CAPTURE DIGITIZATION OPPORTUNITIESBeyond the traditional enterprise market opportunity, regional incumbent telecom operators should also seek to position themselves as enablers for digital economies by leveraging their privileged government relationships and becoming the provider of choice for government ICT requirements.

Raad commented, “Applications such as smart metering, intelligent transport systems, ehealth, and education are driving transformation in traditional economic sectors. To capture large-scale projects, telecom operators need to build a deep knowledge of the economic sector they would be serving and propose ICT solutions to address their specific needs.”

USE ENTERPRISE RELATIONSHIPS TO BOLSTER CONSUMER OFFERINGSTelecom operators can ride the popularity of some end-user devices (such as iPads or BlackBerrys) and the adoption of services by key decision makers in the enterprise to promote their business applications. For instance, they can provide and promote mobile- or tablet- based applications to monitor sales performance.

GET THE SERVICE RIGHTRegardless of the targeted niche within the enterprise segment, operators

need to differentiate their value proposition by realigning their service delivery approach. For medium-sized businesses, this might mean access to around-the-clock customer service and a help desk with knowledgeable technical support, proactive maintenance, and short resolution times. Larger enterprise customers will require committed service-level agreements (SLAs) for a comprehensive range of mission-critical services.

Raad further said, “Mobile and converged communications, as well as social media and cloud computing, are driving enterprise ICT demand. Operators need to segment within each of the large enterprises, key accounts, and SME markets – and deliver a differentiated raft of services to each segment. They need to extend their portfolio beyond core connectivity services to include tailor-made solutions that address the specific needs of their targeted customers. Strategic acquisitions of providers with geographic or industry expertise is an effective way for operators to gain ground in this business and further penetrate the ICT market.”

For his part, El-Darwiche concluded: “With almost 4 million new businesses over the next 3 years, the enterprise market opportunity in the MENA region could be significant.. Enterprise revenues account as high as 25% of telecom operators’ revenues in some European markets. Operators should leverage their strengths to grab share in the rapidly growing SME segment, lock in key large accounts and large-scale digitization projects, and benefit from converging consumer and enterprise offerings.”

About booz & comPAnyBooz & Company is a leading global management consulting firm, helping the world’s top businesses, governments, and organizations. www.booz.com

InfORMATIOn TEcHnOlOGyCAPITAL BusIness MAgAzIne

47

visit our website:

www.fleminggulf.com

20th - 21st March 2012, Kuala Lumpur

Maximising shutdown efficiency with excellent turnaround strategies & people management

Efficient Plant Shutdown & Turnaround Forum 2012

Media Partner:Endorsing Association:

EVENT BENEFITS

Who WIll aTTENd

COOs, CEOs, VPs, Presidents, Directors, Heads, GMs, Senior Managers, Managers, Assistants, Supervisors, Superintendents and Engineers of Shutdown & Turnaround, Scheduling, Operations, Maintenance, Planning, Procurement, Production, HSE, Quality Assurance, Facilities, Asset Integrity

Gain insights into the best practices today from key industry players

Understand & implement the best plan suited to your organisation

Handle unplanned shutdowns & uncertainties during a shutdown

Learn from your industry peers through our interactive workshop

Maximise the efficiency of your shutdown while minimising turnaround duration

Analyse the effectiveness of your shutdown for future improvement

integrate effectively planning, execution & completion for a successful shutdown

Minimise financial impact while maintaining high quality, integrity and safety standards

EVENT INTRodUCTIoNPlant shutdowns and turnarounds will always have only one objective; executing timely shutdowns with controlled costs while maintaining the highest safety and quality standards. It is a massive undertaking that requires intricate planning and one can never be too prepared. One minor hitch will easily escalate costs and delay shutdown time; bringing huge financial losses. It is imperative that all personnel and departments involved understand their roles and responsibilities well.. The Efficient Plant Shutdown & Turnaround Forum 2012 has been exclusively tailored to address critical issues in scheduling, planning, executing and completing shutdowns. This event will discuss crucial information related to efficient planning and scheduling; maintaining skilled workforce and manpower; as well as cost and time effective methods when executing shutdowns and turnarounds. Learn from the best experts on how to spearhead your most expensive project of the year towards excellence.

adVISoRy PaNEl

SPEaKER PaNEl

azneil Malik, PETRoNaS, Malaysia Head, Turnaround ManagementJohn a. Mclay, P. Eng., JMC Consulting, Canada Chief ExecutiveNaveen Goyal, aditya Birla, India Assistant Vice PresidentV. G. Vachhani, PT South Pacific Viscose, Indonesia Vice President, MaintenanceMohamed daoud, adCo, UaE Manager (Projects Quality), Engineering & Major ProjectsPuli S. Saravanan, Shell, Singapore Regional Turnaround Director - Easth l Gadiyar, Reliance Industries ltd., India Vice President, Head CES Planning Kamarulzaman alassan, huntsman Tioxide, Malaysia Production Managerdr. Zulkipli Ghazali, UTP, Malaysia Senior Lecturerlee Woong youl, SK Energy, Korea Maintenance Planning ManagerSaurabh Sinha, Shell, Brunei Senior Planning Engineer

John a. Mclay, P. Eng., JMC Consulting, Canada Chief Executivedr. Zulkipli Ghazali, Universiti Teknologi PETRoNaS (UTP), Malaysia Senior LecturerM. C. Bhurat, PT South Pacific Viscose, Indonesia Vice President, Expansion ProjectsMohamed daoud, abu dhabi Company for onshore oil operations (adCo), UaE Manager (Projects Quality), Engineering & Major ProjectsNaveen Goyal, aditya Birla Management Corporation Private limited (aditya Birla), India Assistant Vice President

PMPT SPECIal PRoMoTIoN GIVE aWay

Two units of apple iPads (16GB) pre-loaded with the

“Turnaround Management System Checklists”

with 50 categories of turnaround management containing over

2800 checklist items.

InfORMATIOn TEcHnOlOGyCAPITAL BusIness MAgAzIne

49

don’T leT securITy MIsconcepTIons ‘cloud’ your JudGeMenT

By: Steve Bailey

What comes to mind when you think about cloud security? Do you think

about application security or protecting corporate data? Perhaps you fear virus or phishing attacks? For the past several years, cloud security has been one of the biggest concerns among IT decision makers as they consider the best way to transition applications and data out of the corporate data center and into the cloud. The real question is one of perception versus reality.

A perceived lack of cloud security can sometimes stop an IT organization dead in its tracks when they look at the cloud as an option for data storage. Many industries, like healthcare and financial services, have always been held to a higher standard than other organizations when it comes to regulatory

compliance and data retention, which prevents them from taking a “risk” on the cloud. This unjustified fear of lax cloud security also means they lose out on all of the business, cost and operational benefits that can come with storing data in the cloud.

The reality is that all of the pieces are in place to enable secure and compliant cloud-based storage environments, and

the technology is sound. It’s time that IT organizations rethink their position on cloud security by looking at the facts.

Making the Case for Cloud StorageThe economic benefits that come with storing data in the cloud are too great to ignore for any IT organization struggling with data management. Because cloud

www.capital-me.com50

storage providers leverage multi-tenant architectures, infrastructure costs are shared across many users. This helps lower costs substantially versus on-site solutions, which require additional provisioning, power, cooling costs, and more.

As data volumes continue to increase, many companies find themselves pushing the capacity, cooling and power limitations of their existing data centers. Meanwhile, regulations require many businesses to keep ever-growing amounts of data for compliance purposes. This three-way balancing act between capacity, compliance and cost requires a flexible, multi-tier approach that makes cloud storage an attractive alternative.

Operational BenefitsWhile many organizations benefit today from keeping online, deduplicated data copies available for fast recovery, massive growth will still require more disk and tape to contain exploding amounts of data. Cloud storage offers a low-cost tier of storage that enables several new compliance, disaster recovery, and data backup solutions. More readily available than offline vaulted data, cloud-based storage delivers these key use cases to help solve today’s data management problems, including:

• Tiering data retention to cloud storage, alleviates the need to expand data center capacity or operational costs

• Archiving stale data to cloud-based storage to free up existing space within the data center

• Cost-effective Disaster Recovery for Small-and-Medium Enterprises without large upfront and operational investment

• Content indexing data before moving to cloud to meet Compliance requirements and minimize search/retrieval times during eDiscovery operations

• Remote office backup directly to cloud-based storage

But is My Data Safe?There are many aspects to securing data in the cloud. People who move application and email servers into the cloud are concerned with spam, hackers and phishing attacks. Those who are considering the cloud to store data for long-term archiving/retention or disaster recovery are concerned with others gaining access or visibility into vital corporate data. In healthcare, organizations are concerned with regulatory compliance. There is also physical security and the specter of some nameless individual strolling into a cloud service provider’s data center and walking away with a jump drive full of intellectual property. Many IT decision-makers are worried about all of the above.

Think about the data in terms of your own data center. You have anti-virus and filtering software tools that monitor and prevent email attacks as well as

encryption and data storage technologies to meet your needs for compliance, recovery and retention. And it’s a safe bet that cloud service providers have guards protecting their physical sites.

There are a few things that you should look for, however, to ensure that your data is being protected in the cloud. Your cloud solution should include:

• Embedded encryption that secures data backup and archive data in-flight or stored within cloud storage

• Integrated alerting, reporting, and data verification functionality to help ensure that data has safely reached the cloud without the risk associated with manual scripting or standalone gateway appliances

• Native REST/HTTP integration to deliver seamless data and information management across on-site and cloud-based storage architectures

• Integrated features like deduplication and compression to enable efficient movement of backup and archive data across a network for long-term cloud storage

It is inevitable that IT organizations will turn to the cloud to keep pace with business demands. It may take time to overcome the fear inherent in handing over control of your data to someone else, but consider this, there was a time when using a credit card online invoked the same type of fear. Nobody wanted to be first to dip their toe in the pool. The technology needed to keep secure, protected and recoverable is here today and adoption will grow. It’s just a matter of time.

About the AuthoRSteve Bailey is the Regional Operations Director at CommVault covering the Emerging Markets region (Middle East, India, Russia/CIS, Eastern and South Eastern Europe). Steve’s responsibilities cover the presales and professional services functions in addition to CommVault channel development, education and growth across the Emerging Region. He has been with CommVault for a little over 10 years and has worked in many functions, both regional and at an EMEA level, most recently heading up CommVault’s EMEA Product Management function.

InfORMATIOn TEcHnOlOGyCAPITAL BusIness MAgAzIne

51