irp advisory group - puget sound energy · irp advisory group meeting june 18, 2015 time topic...

TRANSCRIPT

IRP Advisory Group

June 18, 2015

2

IRP Advisory Group Meeting

June 18, 2015

Time Topic Presenter

9:00 – 9:15 Introduction/Review Action Items Lyn Wiltse (facilitator)

9:15 – 9:30 Process Check-In Phillip Popoff

9:30 – 10:30 Draft Gas Portfolio Results Gurvinder Singh

10:30 – 10:45 BREAK

10:45 – 11:30 Resource Adequacy Villamor Gamponia

& Lloyd Reed

11:30 – 12:00 LUNCH

12:00 – 12:45 Electric Portfolio Sensitivities Elizabeth Hossner,

Bob Williams & Janet Phelps

12:45 – 1:15 Stochastic Model Villamor Gamponia

1:15 – 2:15 Electric Stochastic Results Elizabeth Hossner

2:15 – 2:30 Review Open Items & Wrap Up Lyn Wiltse (facilitator)

Gas Portfolio Analysis Gurvinder Singh

June 18, 2015 IRPAG

4

• Gas Resource Need

• Resource Assumptions

• Draft Portfolios

• Gas Sensitivities

• Next Steps

June 18, 2015 IRPAG

Agenda

5

IRP Process

June 18, 2015 IRPAG

Resource Needs

Planning Assumptions &

Resource Alternatives

Analysis of Alternatives

Portfolio Analysis

Analysis of Results

Decisions

Commitment to “Action”

6

2015 IRP - December Peak Day Need Before

DSR

June 18, 2015 IRPAG

7

Supply Side Resource Alternatives

June 18, 2015 IRPAG

Option #1 – Purchase BC gas at Station 2 and transport via existing or expanded

capacity on Westcoast, along with an expansion of Northwest Pipeline (NWP).

Option #1a – Purchase short term NWP TF-1 capacity from Sumas (2016-18)

Option #2 – Purchase AECO gas and transport via existing or expanded capacity on

NGTL (Nova) and Foothills pipelines, along with the proposed Fortis BC Kingsvale -Oliver

Reinforcement Project (KORP) and a NWP expansion.

Option #3 – Purchase AECO gas and transport via existing or expanded capacity on

NGTL, Foothills, GTN, along with a new Cross-Cascades pipeline with a NWP expansion.

(N-MAX, Palomar/Blue Bridge).

Option #4 – Purchase gas at Malin, transport by back-haul on GTN and transport on a

new Cross-Cascades pipeline with a NWP expansion.

Option #5 – Develop an on-system LNG peaking resource in combination with a plant

serving transportation market.

Option #6 – Develop a stand-alone on-system LNG peaking resource MIST Storage –

lease capacity from NW Natural with discounted redelivery to PSE Service territory.

Option #7 – Upgrade the existing Swarr LP-air facility and return to service.

8

Supply Side Resource Alternatives

June 18, 2015 IRPAG

9

Demand Side Resource Alternatives -

Energy

June 18, 2015 IRPAG

Includes 10%

conservation

credit

10

Demand Side Resource Alternatives - Peak

June 18, 2015 IRPAG

11

Compare Total Achievable Technical

Potential

June 18, 2015 IRPAG

12

Gas Prices - Sumas

June 18, 2015 IRPAG

13

Gas Peak Day Load Forecast –

Base/High/Low

June 18, 2015 IRPAG

14

Scenarios

Gas

CO2

Demand

Mid Gas

Mid CO2

Mid Demand

Gas

CO2

Demand

Low

Gas

High

Gas

No

CO2

High

CO2

Low

Demand High

Demand One-Off

Scenarios

Fully Integrated

Scenarios

Very

High

Gas

1

2

3

4

5

6

7 8

9 10

June 18, 2015

IRPAG

15

2015 IRP Scenarios

June 18, 2015 IRPAG

Scenario Demand Gas Price CO2 Price

1 Low Low Low None

2 Base Mid Mid Mid

3 High High High High

4 Base + Low Gas Price Mid Low Mid

5 Base + High Gas Price Mid High Mid

6 Base + Very High Gas Price Mid Very High Mid

7 Base + No CO2 Mid Mid None

8 Base + High CO2 Mid Mid High

9 Base + Low Demand Low Mid Mid

10 Base + High Demand High Mid Mid

16

2015 IRP Gas Sensitivities

June 18, 2015 IRPAG

• Compare Cost-effective DSR using alternate discount rate

versus the WACC.

• Developed an alternate weighted discount rate using long term T-bill

and WACC (DSR TAG Meeting April 7th 2014)

• Test “lumpiness” of pipeline capacity timing:

• “In the next IRP, PSE should conduct a second run of its model once

the appropriate blocks of pipeline capacity are selected, to assess

whether early acquisition of pipeline blocks impacts the timing of the

selection of other resources.” -- Attachment A Utilities and Transportation Commission Comments on Puget

Sound Energy’s 2013 Integrated Resource Plan Dockets UE-120767 & UG-

120768 Section IV Natural Gas page 10.

17

Gas Draft Portfolios

June 18, 2015 IRPAG

18

Gas Draft Portfolios - Base Scenario

June 18, 2015 IRPAG

19

Gas Draft Portfolios – DSR Results

June 18, 2015 IRPAG

Bundles Low

2015 IRP

Base High

Base +

Low Gas

Base +

High Gas

Base + V

High Gas

Base + No

CO2

Base +

High CO2

Base +

Low

Demand

Base +

High

Demand

Residential Firm B1 C1 D C1 C1 D C D C1 C1

Commercial Firm B1 D E C D D C D D D

Commercial Interruptible 0 0 0 0 0 0 0 0 0 0

Industrial Firm A2 A2 A2 A2 A2 A2 A2 A2 A2 A2

Industrial Interruptible A2 A2 A2 A2 A2 A2 A2 A2 A2 A2

20

Gas Draft Portfolios – DSR Results

June 18, 2015 IRPAG

21

Gas Draft Portfolios – DSR Results

June 18, 2015 IRPAG

Not

Selected??

22

Gas Draft Portfolios – DSR Peak

June 18, 2015 IRPAG

23

Portfolios – Compare Cummulative

Savings

June 18, 2015 IRPAG

24

Portfolios – Compare Incremental

Savings

June 18, 2015 IRPAG

25

Portfolios – Incremental Codes &

Standards

June 18, 2015 IRPAG

• Water Heater

Standards in 2015 IRP

26

Gas Draft Portfolios - Low Scenario

June 18, 2015 IRPAG

27

Gas Draft Portfolios - High Scenario

June 18, 2015 IRPAG

28

Gas Draft Portfolios – DSR Sensitivity

June 18, 2015 IRPAG

Composite Discount Rate =

Residential Savings Share*Average 3 month of LT CMT + C&I Savings Share*WACC

2014-15 Bienial TargetsSector Therms Percent

Residential 4,020,500 58%

Commercial & Industrial 2,920,000 42%

WACC 7.77%

Ave 3 Month LT CM 30 Yr 2.87%

Composite Discount Rate 4.93%

Dec 09,2014;

Rate as of Jun

17, 2015 is

3.09%

29

Gas Draft Portfolios – DSR Sensitivity

June 18, 2015 IRPAG

30

Gas Draft Portfolios – Resource

Lumpiness

June 18, 2015 IRPAG

31

Gas Draft Portfolios – Resource

Lumpiness

June 18, 2015 IRPAG

20 year 10 year

Base Scenario $9,343,219 $5,056,839

Base Annual Additions >2026 $9,280,246 $5,056,839

Delta $62,973 $0

• NPV using WACC over the 20 years and the first ten

years.

Table: NPV Delta in 2016$ (000’s)

32

Next Steps

June 18, 2015 IRPAG

• Analyze the portfolio results

• Complete Monte Carlo Analysis

• Gas for Power Portfolio

PSE’s Market Reliance

and Resource Adequacy Villamor Gamponia and Lloyd Reed

June 18, 2015

34

Agenda:

June 18, 2015

PSE’s resource adequacy in the presence of risks in

market reliance

Analytical approach used

Genesys – PNW Resource Adequacy Model

PSE’s Wholesale Purchase Curtailment Model (WPCM)

PSE’s Resource Adequacy Model (RAM)

Impacts of risks in market reliance on PSE’s resource

adequacy

Risk metrics

Benefits and costs of reliability to customers

35

Analytical Tool : GENESYS

June 18, 2015

Chronological hourly simulation using Monte Carlo method

Random Variables:

• Hydro: 1929-2008

• Temperature: 1929-2005

• Thermal Forced Outage Rates

• Wind: Correlated with 20 temperature profiles

Operating Year: October 2020 – September 2021

Number of Games: 6,160

Risk Metrics: LOLP, LOLE/LOLH, EUEs

36

Genesys Assumptions for 2020-2021

June 18, 2015

Coal Retirement Case by Power Planning Council

Boardman(600MW) and Centralia 1(730MW) are retired

Total Firm plus Spot SW Imports for Winter Capacity:

2,925MW (Spot = 2,500MW)

Outputs from BPA’s Genesys model version were

utilized(Feb 2015 Assessment) http://www.nwcouncil.org/media/7148951/30915-raac-steering-2021-coal-retirement-

bpa.pdf

LOLP Net of Standby Resources = 8.1%, LOLP Before

Standby Resources = 11.1%

MW needed to reach 5% =1,150MW

37

Genesys Assumptions for 2020-2021

June 18, 2015

The average PNW load curtailment (in the Genesys draws with curtailments) is 1,950 MW.

The hourly PNW load curtailments from the Genesys model range from 0.2 MW to 10,133 MW.

The maximum hourly PNW curtailment used in the PSE studies was limited to 6,000 MW.

Allocation of Regional Deficits

to PSE Lloyd Reed

External Consultant

June 18, 2015

39

Today’s Topics

June 18, 2015

Introduction/Background

Need for PSE’s Wholesale Purchase Curtailment

Model (WPCM)

WPCM Data Inputs and Assumptions

WPCM Results

WPCM Model Output/Links to Other PSE IRP models

Questions/Discussion

40

Introduction/Background

June 18, 2015

PSE’s 2013 IRP assumed an infinite supply of power is available for PSE to purchase in the PNW wholesale markets under all conditions.

PSE needs to purchase up to approximately 1,600 MW of wholesale capacity and energy to meet its winter season peak load needs.

The changing load/resource situation in the PNW could lead to potential shortages in capacity and energy being available for purchase by PSE and other PNW load-serving utilities.

Over 2,000 MW of regional coal-fired generation will be retired by 2025.

PSE’s wholesale purchases could be limited to amounts significantly less than 1,600 MW during PNW regional load curtailment events.

Key Question: How can the impacts of PNW regional load curtailment events be quantified and included in PSE’s 2015 IRP resource adequacy analysis?

41

Need for PSE’s Wholesale Purchase Curtailment Model

June 18, 2015

PNW Resource Adequacy studies performed by the NWPCC and BPA

are conducted on an aggregated region-wide basis.

It is not possible to isolate on impacts to individual utilities.

Lack of other available modeling tools to translate PNW-wide regional

load curtailments to an individual utility level.

No PNW IOU attempted to quantify potential regional load curtailment

impacts in their respective 2013 IRPs.

Conclusion: PSE needs to develop a new modeling tool for use in the

2015 IRP to quantify the impacts of PNW-wide load curtailment events

on PSE’s power system.

Impacts will be quantified via reductions in PSE’s wholesale market

purchases under its long-term Mid-C transmission rights.

42

WPCM Data Inputs and Assumptions

June 18, 2015

Genesys Model Output

The hourly regional load curtailment volumes determined in the Genesys model (limited to 6,000 MW) were used as an input to PSE’s WPCM.

PSE Specific Data

PSE’s set of initial wholesale power purchases (as determined in PSE’s RAM model) under all of the draws from the Genesys model that contain PNW regional load curtailments.

No PNW load curtailment = No reduction in PSE’s initial wholesale purchase

amount.

PSE’s hourly wholesale purchases vary slightly due to the variable generation of PSE’s Wild Horse and Mid-C plants in the RAM model.

PSE’s initial hourly wholesale purchases average slightly less than 1,600 MW and are limited only by the available amount of PSE’s long-term Mid-C transmission import rights.

43

WPCM Data Inputs and Assumptions (Cont.)

June 18, 2015

PNW Regional Load/Resource Data

The surplus/deficit position of other PNW utilities has a direct impact on the amount of PNW-wide load curtailments that are ultimately “allocated” to PSE.

Load and resource data for 2021 was compiled from various sources to determine the net winter capacity surplus or deficiency for multiple PNW utilities.

2013 IRPs for PGE, Pacificorp, Avista and Idaho Power.

BPA’s 2014 Pacific Northwest Loads and Resources Study.

Other forecasted 2021 large PNW purchasers of winter capacity (relative to PSE) include PGE, Pacificorp (West System) and BPA.

Aggregating small capacity purchasers and sellers does not impact the PSE load curtailment allocations.

44

WPCM Data Inputs and Assumptions (Cont.)

June 18, 2015

Load and resource data was used to compute winter 2021 base capacity surplus/(deficiencies) for the above noted utilities, BPA’s public preference customers by category (i.e. PUDs, municipalities, etc.), PNW regional IPPs, and power marketers.

Sensitivities to changes in regional load and resource conditions were determined based upon each entity’s total winter peak load + winter peaking resources. Sensitivity ratios were utilized to sync up the base individual utility

surplus/(deficiencies) to the hourly PNW regional load curtailment amounts from the Genesys model.

The base PNW winter 2021 capacity surpluses/(deficiencies) and sensitivity ratios utilized in the PSE WPCM model are shown in the following table:

45

WPCM Data Inputs and Assumptions (Cont.)

June 18, 2015

PNW Entity Base 2021 Winter Capacity Surplus/(Deficiencies) and

Sensitivity Ratios

Entity Sur/(Def) Sensitivity

MW Ratios

PSE (1,584.1) 0.15

PGE (789.0) 0.11

PACW (1,175.9) 0.11

BPA (797.0) 0.30

Other (635.0) 0.21

PNW IPP+IPC 3,188.0 0.12

Total (1,793.0) 1.00

46

WPCM Data Inputs and Assumptions (Cont.)

June 18, 2015

PNW Load Curtailment Allocation Methodology

The WPCM only evaluates physical power system impacts – it does not evaluate financial impacts. Some of the outputs from the WPCM, however, are used as input to other PSE IRP

financial models.

The WPCM incorporates a simplified version of the PNW wholesale market that includes PSE (a capacity purchaser), one net capacity seller (including imports from California), and four other PNW utility capacity purchasers. Power marketers with no generation or end-use loads are assumed to have no

impact on the physical load curtailment allocation.

The model assumes that all purchasers of power during a PNW regional capacity shortage/load curtailment event have equal access and opportunity to purchase capacity from sellers in the PNW wholesale markets.

The model assumes that all purchasers during a PNW regional capacity shortage/load curtailment event are willing to pay up to the same price to avoid having to curtail their own customers.

47

WPCM Data Inputs and Assumptions (Cont.)

June 18, 2015

The model incorporates impacts from both forward-market purchases and spot-market purchases. Forward-market purchases are assumed to be initiated well in advance of a PNW

load curtailment event (i.e. under “normal” market conditions).

Spot-market purchases are assumed to be initiated on a day-ahead or day-of basis (i.e. under “non-normal” capacity scarcity conditions).

A utility that manages to purchase more capacity than it needs to meet its own need (i.e. to avoid a load curtailment to its own customers) will make that surplus capacity available to other (still deficit) PNW capacity purchasers.

Under PNW capacity shortage/load curtailment events, BOTH forward-market wholesale purchases and spot-market wholesale purchases could be subject to curtailment. In general, forward-market purchases do not have a priority over spot-market

purchases.

It is in the seller’s discretion as to which wholesale sales it may choose to curtail if required.

48

WPCM Results

June 18, 2015

No limitations on PSE’s ability to purchase wholesale

power: PSE’s average wholesale purchase amount – 1,584 MW

PSE’s minimum wholesale purchase amount – 1,365 MW

PSE’s maximum wholesale purchase amount – 1,696 MW

PSE’s hourly wholesale purchases limited due to PNW

load curtailment events (Base Case): PSE’s average wholesale purchase amount – 857 MW

PSE’s minimum wholesale purchase amount – 10 MW

PSE’s maximum wholesale purchase amount – 1,675 MW

49

WPCM Model Output/Links to Other PSE IRP models

June 18, 2015

For each hourly PNW load curtailment event (as determined in the

Genesys model) the primary outputs from the WPCM model are:

PSE’s initial hourly wholesale market purchase (in MW).

The reduction to PSE’s initial hourly wholesale market purchase that

incorporates the PNW load curtailment/capacity scarcity event (in MW).

PSE’s final hourly wholesale market purchase (in MW).

The final set of PSE hourly wholesale market purchases in then used

as an input into the second and final run of PSE’s RAM model.

PNW load curtailment impacts on PSE across the 6,160 Genesys

draws are “translated” to the 250 draw datasets that are utilized in

the PSE financial models.

Wholesale power prices are adjusted in PSE’s IRP financial models to

incorporate PNW regional scarcity pricing impacts.

50

PSE’s Resource Adequacy Model (2015 IRP

Version) > = <

Thermal System Load

Forced Outages Temperature Sensitivity

Seasonal Capacities

Maintenance Schedules DSR

Adjustments: Weather Sensitive EE Savings

Hydro Contingency Reserves Base EE Savings

Hydro Conditions Balancing Reserves EISA/DE and DR

Mly/Hrly Shapes (WECC Stds)

Sustained Peaking Simulation Approach(SAS code):

- 6,160 draws for a study year

Wind using Genesys chronological order

Hourly Generation - event is a draw with

Contracts loads > resources for any hour

Seasonal Exchanges - reserve sharing means 1st hr

Mid-C and Non Mid-C Contracts of event is covered by NW pool

- LOLP = Ʃ Draws with an event/6160

Transmission (Market Reliance) - 5% LOLP target same as region

Owned + BPA Contracts Random Variables

Adjustments for: Weather (Temps,Hydro,Wind)

PNW Regional Load Curtailment Thermal Plant Outages

MidC Hydro

Spinning Reserves Planning Margin =

Balancing Reserves (Resources + DSR - Reserves) /

Wild Horse Wind Normal Peak Load

MidC Contracts

Transport Customers(Sch 449)

RESOURCES - - - - - - - - - - - > < - - - LOADS

51

PSE’s Resource Adequacy Model (Updates

to the 2015 IRP Version)

June 18, 2015

Based on F14 load forecasts(lower by 120MW in

2020 from F13)

Consistency with Genesys draws:

Same study period: Oct 2020 to Sep 2021

Chronological simulation of weather and temperature

years (Hydro:1929-2008; Temperature: 1929-2005)

Forced outage assumptions for expected FOR and

mean time to repair are the same for PSE thermals

Hourly reductions in market purchase capability

from WPCM in Genesys games with curtailments

52

Reliability Metrics for 2020-2021

June 18, 2015

Planning Margin

@5% LOLP

No Risk in Market Reliance 13%

With Risk in Market Reliance 14%

*Risks in market reliance are based on shortages from the regional adequacy model with coal retirements in 2020.

**For games with any interruption, similar to SAIFI(interruptions)/SAIDI(duration).PSE Targets:SAIFI=1.3,SAIDI=5.33

Risk in market reliance significantly increases the expected unserved

energy or EUE even with added capacity to achieve the same LOLP.

53

Peak Contribution of Wind

June 18, 2015

ICE – Incremental Capacity Equivalents, if we add or subtract a resource,

what level of gas peaking capacity needs to be subtracted or added

respectively to keep the 5% LOLP. The ratio of the change in gas peaking

capacity to the capacity of the new added or subtracted resource gives an

estimate of the peak contribution of a resource.

Incrementa l Capacity Equiva lent(Re la tive to a Peaker)

ICE Va lue

Existing Wind 12.5%

SW WA Generic Wind 7.0%

MT Generic Wind 55.0%

• SW Washington Wind profile is based on historical Hopkins Ridge lagged 10

minutes

• MT Generic Wind profile is based on 2 years of historical Judith Gap wind data

• EUE based incremental capacity equivalent could be different

54

Impacts of Added SW Imports and Resource

Reductions due to Non-Firm Gas Supply

June 18, 2015

No Risk in

Market

Reliance

With Risk in

Market

Reliance*

With Risk in Market

Reliance + Full SW

Import(+475MW)

With Risk in Market Reliance

+ Capacity Drop for Non-

Firm Fuel(-650MW)

LOLP 5% 5% 5% 5%

LOLE/LOLH(Hrs) 0.20 0.25 0.23 0.29

Expected Unserved Energy(MW-Hrs) 26.2 49.6 41.6 61.2

TVar90 of Unserved Energy(MW-Hrs) 262 496 416 612

Exp Number of Interruptions/Year** 1.9 2.0 1.9 2.1

Exp Duration/Interruption(Hrs)** 2.14 2.55 2.45 2.75

* Risks in market reliance are based on shortages from the regional adequacy model

with coal retirements in 2020-2021. Assumes Boardman and Centralia 1 are retired in 2020.

** For games with any interruption, similar to SAIFI(interruptions)/SAIDI(duration).PSE targets:SAIFI=1.3,SAIDI=5.33

55

Market Reliance Risks and Value of Lost Loads

June 18, 2015

Risks in market reliance increase unserved energy and

customer interruptions

Need to evaluate benefits/costs of reliability

Inputs required:

PSE’s Resource Adequacy Model produces system lost

loads by month/day/hour and by duration

Interruption cost estimates per event by customer type

are available from DOE, based on LBL compilation of

surveys(www.icecalculator.com)

Costs of adding a frame peaker to meet reliability is

available from PSM

56

Benefit-Cost of Reliability

57

Benefit-Cost of Reliability – Risks to Customers

June 18, 2015

Capacity

Addition

(MW)

Total Levelized

Cost of Added

Capacity

($mil/yr)

Incremental

Reliability Cost

($mil/yr)

Expected

VOLL

($mil/yr)

Incremental

Reliabiltiy Benefit

Lower Cost Lost

Load ($mil/yr)

Benefit/Cost

Ratio

TailVar90 of

VOLL

($mil/yr)

Change

in

TailVar90

0 0 101.85$ 1,032$

100 15.65$ 15.65$ 57.10$ 44.75$ 2.86 568$ 464$

200 31.30$ 15.65$ 36.11$ 20.99$ 1.34 355$ 212$

300 46.95$ 15.65$ 23.61$ 12.50$ 0.80 240$ 116$

400 62.60$ 15.65$ 15.71$ 7.90$ 0.50 155$ 85$

500 78.24$ 15.65$ 9.78$ 5.93$ 0.38 99$ 56$

Cost of Reliability

Benefit of Reliability with Risk in

Market Reliance

Electric Portfolio Analysis

Elizabeth Hossner

June 18, 2015 IRPAG

59

Draft Portfolio Builds - Base

June 18, 2015 IRPAG

Annual

Builds (MW) CCCT

Frame

Peaker WA Wind Biomass PBA Battery DSR DR

2016 - - - - - - 75 18

2017 - - - - - - 64 12

2018 - - - - - - 67 41

2019 - - - - - - 64 14

2020 - - - - - - 79 43

2021 - - - - - - 62 2

2022 - - - - 25 - 66 12

2023 - 228 100 - - - 56 2

2024 - - 100 - - - 55 3

2025 - - - - - - 53 2

2026 - 455 - - - - 27 2

2027 - - 100 - - - 27 2

2028 - 228 - - - - 27 3

2029 - - - - - - 23 2

2030 - - - - - - 23 2

2031 - 228 - - - - 27 2

2032 - - - - - - 32 2

2033 - - - 15 - - 29 2

2034 - - - - - - 25 2

2035 - - - - - 80 24 2

Total - 1,138 300 15 25 80 906 172

Winter - 1,138 24 - 25 80 906 172

60

Meeting Peak Capacity - Base

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Pe

ak C

apac

ity

(MW

)

Demand Side Resources

Fixed PPA

Batteries

MT Wind

Solar

Biomass

WA Wind

Peaker - Recip

Peaker - Aero

Peaker - Frame

CCGT

Mid-C Transmission Available

Existing Resources (full capacity)

Dec Peak Load + PM + Op Reserves

61

Meeting RPS - Base

June 18, 2015 IRPAG

0

500

1000

1500

2000

2500

3000

3500

4000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Tota

l REC

s G

Wh

Meeting the RPS

Generic Solar

Generic MT Wind

Generic Biomass

Generic WA Wind

Hydro Upgrades

Existing Resources

REC Need ('000)

62

Meeting Annual Energy - Base

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Ann

ual E

nerg

y (a

MW

)

Colstrip Natural Gas Contracts

Hydro Wind Generic Natural Gas

Generic Wind Generic Biomass Demand - 2015 IRP Base before DSR

Demand - 2015 IRP Base After DSR

Net Market Purchases = 806 aMW

Net Market Purchases = 1,536 aMW

63

Portfolio Builds across Scenarios

385

1156

385

385

771

385

2312

771

771

1156

1542

228

228

683

228

683

683

228

228

683

455

1138

455

1138

1138

455

455

683

300

200

200

600

200

200

200

200

300

200

400

200

300

1000

300

300

600

300

400

200

500

100

80

80

403

411

411

411

411

435

411

428

403

428

654

669

669

669

669

713

669

701

654

701

888

906

906

906

906

968

906

956

888

956

131

131

131

131

131

131

131

131

131

198

154

152

154

152

152

152

152

152

154

225

174

172

174

172

172

172

172

172

174

254

15

15

15

0 500 1000 1500 2000 2500 3000 3500 4000 4500 5000

Low

Base

High

Base + Low Gas Price

Base + High Gas Price

Base + Very High Gas Price

Base + No CO2

Base + High CO2

Base + Low Demand

Base + High Demand

Low

Base

High

Base + Low Gas Price

Base + High Gas Price

Base + Very High Gas Price

Base + No CO2

Base + High CO2

Base + Low Demand

Base + High Demand

Low

Base

High

Base + Low Gas Price

Base + High Gas Price

Base + Very High Gas Price

Base + No CO2

Base + High CO2

Base + Low Demand

Base + High Demand

2021

2026

2035

Nameplate Additions (MW)

CCCT

Frame Peaker

Wind

PBA

Battery

DSR

DR

Biomass

64

Draft Portfolios – Portfolio Sensitivities

65

Portfolio Sensitivities

June 18, 2015 IRPAG

Sensitivities Alternatives Analyzed

A Market Reliance Risk

What if continuing to rely on short-term market purchases becomes too risky?

Baseline – Continue to rely on 1,600 MW of

market purchases

1.

B Gas Transport for Peakers

What if peakers cannot rely on oil for

backup fuel and must have firm gas supply instead?

Baseline – Non-firm pipeline capacity with oil

backup

2. Firm pipeline capacity with no oil backup

C Solar Penetration

What if customers install significantly more rooftop solar than expected?

Baseline – Rooftop solar growth based on

forecast

3. Maximum potential capture of rooftop solar

66

Portfolio Sensitivities Continued

June 18, 2015 IRPAG

Sensitivities Alternatives Analyzed

D Energy Storage/Flexible Resource

What is the cost difference between a

portfolio with and without and energy storage or Flexible Resource?

Baseline – Batteries economically chosen as

part of least cost portfolio

4. Add 80 MW Battery in 2023 instead of Peaker

5. Add 80 MW Pumped Storage Hydro in 2023

instead of Peaker

6. Update Costs for Recip Engine (75 MW)

7. Add 75 MW Recip Engine in 2023 E Demand-side Resources (DSR)

How much does DSR reduce cost, cost risk and emissions?

Baseline – All cost-effective DSR per RCW

19.285 requirements

8. No DSR. All needs met with supply-side resources

F Carbon Reduction

How does increasing renewable resources

and DSR beyond requirements affect carbon reduction and portfolio costs?

Baseline – Renewable resources and DSR per

RCW 19.285 requirements

9. Add 300 MW of wind in 2021 beyond

renewable requirements

10. Add 300 MW of utility scale solar in 2021

beyond renewable requirements

11. DSR increased beyond requirements

67

Portfolio Sensitivities Continued

June 18, 2015 IRPAG

Sensitivities Alternatives Analyzed

G Gas Plant location

What if the gas plants were built in Eastern

Washington instead of PSE service territory?

Baseline – Gas plants located in PSE Service

territory

12. Model gas plants with gas transport costs and transmission costs from Eastern Washington

H MT Wind

Update transmission cost for Montana

Wind to be more optimistic if Colstrip

continues to operate. Will MT Wind be

chosen in lowest cost portfolio?

Baseline – Cost estimate for transmission

upgrades from Montana

13. Low transmission cost estimate from Bill

Pascoe

I Thermal Mix

How does changing the mix of resources

effect the portfolio cost and risk?

Baseline – Resources chosen as part of least

cost portfolio

14. Mix of CCCT and Frame Peaker

15. All CCCT Portfolio

68

Portfolio Sensitivity D – Energy Storage/Flexibility

June 18, 2015 IRPAG

• Baseline Assumption: Batteries economically chosen as part of

least cost portfolio

• Sensitivity:

1. Add 80 MW Battery in 2023 instead of a Frame Peaker

2. Add 80 MW of Pumped Storage Hydro in 2023 instead of

Frame Peaker

3. Increment Recip Engines in 75 MW (4 engines) instead of

220 MW (12 engines) with updated (lower) cost estimate

from Wartsila

4. Add 75 MW of Recip Engines in 2023 instead of a Frame

Peaker with updated cost estimate from Wartsila

69

Portfolio Sensitivity D – Recip Assumptions

June 18, 2015 IRPAG

Updated costs on Reciprocating Engines from Wartsila. Cost estimates provided by Burns and McDonnell for a plant in the Seattle/PSE area.

Current EPC estimate for a 18V50SG (18.7 MW each):

4 x 18V50SG (74.8 MW): $72 million ($962/KW)

6 x 18V50SG (112.2 MW): $95.4 million ($850/KW)

10 x 18V50SG (187 MW): $152 million ($812/KW)

Assumptions:

• Air-cooled radiators installed on the ground

• No piles required for foundations

• SCR included

• Separate contracts for Wartsila gensets and engineering/construction

• Does not include cost of transmission interconnect

PSE adds 40% for outside-the-fence, project development, project financing, and escalation

70

2015 IRP- Reciprocating Engines Resources

2014 $ Units Recip Engine

(Base)

Recip Engine

(Small Size)

Recip Engine

(Large Size)

Recip Engine

Flexibilty

(Small Size)

Recip Engine

Flexibilty

(Large Size)

ISO Capacity Primary MW 220 75 224 75 224

Winter Capacity Primary MW 220 75 224 75 224

Capacity DF MW

Capital Cost $/KW $1,599 $1,404 $1,175 $1,404 $1,175

O&M Fixed $/KW-yr $5.31 $5.31 $5.31 ($12.92) ($12.92)

71

Portfolio

CPS2

Score

Proxy

(%)*

Spin

Capacity

Shortfall

(%)

Spin

Capacity

Shortfall

(aMW)

Unserved

Energy

(aMW)

Excess

Energy

(aMW)

Expected

Annual

Balancing

Savings

($)

Expected

Annual

Bal.

Savings

($/kW

Capacity)

2018 Base 97% 0.1% 2.0 5.9 12.5 -- --

2018 Base +

CCCT 97% 0.1% 1.8 5.7 12.2 $800,000 $2.33

2018 Base +

Frame CT 97% 0.1% 1.9 5.9 12.1 $1,037,000 $4.69

2018 Base +

Recip CT 97% 0.1% 1.8 5.9 12.1 $328,000 $18.23

Figure G-13

Summary Results from Flexibility Analysis,

50 Simulations

APPENDIX G – OPERATIONAL FLEXIBILITY

Source: 2013 IRP

72

(A) (B) (C) (D) (E)=(A)-(C) (F) (G) (H)=(A)-(G)

Difference

from base

Difference

from base

Difference

from base

Portfolio Costs

Benefit/

(Cost) Portfolio Costs

Benefit/

(Cost)

Value of

Flexibility to

the Portfolio

Portfolio

Costs

Benefit/

(Cost)

Value of

Flexibility to

the Portfolio

Base Case $12,276,911 $12,221,360 $55,551 $12,221,360 $55,551

Reciprocating Engines 75 MW* $12,263,289 $13,622 $12,201,832 $19,528 $61,457 $12,207,549 $13,810 $55,740

Reciprocating Engines 75 MW in 2023 $12,281,901 ($4,990) $12,211,855 $9,504 $70,046 $12,220,589 $770 $61,311

Reciprocating Engine 224 MW in 2023 $12,354,297 ($77,386) $12,234,783 ($13,424) $119,513 $12,260,986 ($39,626) $93,311

*Replaces battery in 2035 as a cheaper alternative

No Flexibility Benefit

Sensitivity of Reciprocating Engines

Flexibility Benefits 50% for RecipsFlexibility Benefits

73

Portfolio cost Increase from Base

Base $12,276,911

80 MW Pumped Storage in 2023 $12,478,039 $201,129

200 MW Pumped Storage in 2023 $12,915,303 $638,392

80 MW Batteries in 2023 $12,373,801 $96,891

80 MW Batteries in 2023 with $150/KW Flexibilty Value* $12,276,911 $0

*Represents the tipping point for the flexibility value to bring batteries in line with the Base Portfolio

Storage Results

74

Portfolio Sensitivity F – Carbon Reduction

June 18, 2015 IRPAG

• Baseline Assumption: Renewable resources and DSR per RCW

19.285

• Sensitivity:

1. Add 300 MW of wind in 2021 beyond renewable

requirements

2. Add 300 MW of utility scale solar in 2021 beyond renewable

requirements

3. DSR increased beyond requirements

75

What is the cost of carbon abatement?

June 18, 2015 IRPAG

• Addition of demand side or renewable

resources to portfolio changes revenue

requirement and emissions

• Other elements of portfolio change to

accommodate added resource

76

Carbon Abatement from DSR

June 18, 2015 IRPAG

• Start with base scenario without demand side resources (DSR)

and base with bundle D

• Calculate change in annual revenue requirement over 20 years,

take NPV

• Calculate change in annual emissions over 20 years, take NPV

• Divide to get incremental cost in $ / ton of emissions

• Run base scenario in PSM forcing in bundle E and reoptimize

• Calculate changes in revenue requirement and emissions from

results between bundles D and E

• Do the same for bundles F and G

77

Incremental Cost by Bundle

June 18, 2015 IRPAG

78

Carbon Abatement by Bundle

June 18, 2015 IRPAG

79

Impacts of Changing DSR

Changes to portfolio cost and emissions reflect impacts of multiple changes to portfolios. Increments are calculated

relative to portfolio with previous bundle.

Scenario

NPV 20 Year

Portfolio

Cost ($000)

Total 20

Year

Emissions

(Millions of

Tons)

Total 20

Year

Carbon

Abatement

(Millions of

Tons)

Incremental

Cost

(Benefit) /

Ton

Base No DSR $12,339,055 245.00

Base Bundle D $11,019,322 228.89 16.11 $(202)

Bundle E $11,077,321 227.99 0.90 $173

Bundle F $11,075,068 227.74 0.25 $(23)

Bundle G $11,155,377 226.52 1.22 $157

80

Carbon Abatement from Wind or Solar

June 18, 2015 IRPAG

• Start with base scenario (with bundle D)

• Examine 3 scenarios

• Add 300 MW of wind in 2021 without reoptimizing

• Add 300 MW of wind in 2021 and reoptimize

• Add 300 MW of solar in 2021

• Calculate incremental revenue requirement per ton of

emissions compared with base for each scenario

• Two approaches to math

81

Incremental Cost Calculation for Wind or

Solar

June 18, 2015 IRPAG

• Levelized emissions approach:

• Calculate change in annual revenue requirement over 20 years, take

NPV

• Calculate change in annual emissions over 20 years, take NPV

• Divide to get incremental cost in $ / ton of emissions

• Average emissions approach:

• Calculate change in annual revenue requirement over 20 years, take

NPV, levelize to get annual payment

• Calculate change in annual emissions over 20 years, take 20-year

average

• Divide levelized payment by average emissions to get incremental

cost in $ / ton of emissions

82

Incremental Cost for Wind and Solar

June 18, 2015 IRPAG

83

Carbon Abatement from Wind or Solar

June 18, 2015 IRPAG

84

Impacts of Wind or Solar Additions

June 18, 2015 IRPAG

Changes to portfolio cost and emissions reflect impacts of multiple changes to portfolios. Increments for both wind

and solar are calculated relative to base scenario.

Scenario

NPV 20

Year

Portfolio

Cost ($000)

Total 20

Year

Emissions

(Millions

of Tons)

Total 20

Year

Carbon

Abatement

(Millions

of Tons)

Incremental

Cost

(Benefit) /

Ton

Base Bundle D $11,019,322 228.89

300 MW Wind (Not

Reoptimized)

$11,239,345

223.98

4.91

$115

300 MW Wind

(Reoptimized)

$11,111,563 223.98 4.91 $36 - 38

300 MW Solar $11,423,572 226.11 2.78 $362 - 374

85

Portfolio Sensitivity H – Montana Wind

June 18, 2015 IRPAG

• Baseline Assumption: Cost estimate for transmission upgrades

from Montana

• Sensitivity: Low transmission cost estimate based on

conversations with Bill Pascoe

• Follow-up with Bill on details

86

2014 $ WA Wind MT Wind Base MT Wind Update

Capital Cost Facility ($/kW) $1,703 $1,703 $1,703

Sales Tax ($/kW) $123

Transmission/Substations ($/kW) $2,813 $507

AFUDC ($/kW) $141 $396 $171

Total Capital Cost ($/kW) $1,968 $4,913 $2,381

Northwestern Line Losses 4.0% 2.7%

PSEI Colstrip Line Losses 2.7% 2.7%

Montana Losses 6.7% 5.4%

BPA Line Losses 1.9% 1.9% 1.9%

Total line losses 1.9% 8.6% 7.3%

Capacity Factor 34% 41% 41%

O&M Variable ($/MWh) $3.15 $3.15 $3.15

Variable Transmission ($/MWh) $1.84 $1.84 $1.84

Northwestern to Broadview $3.30 $0.00

PSE tariff - Broadview to Townsend $9.16 $9.16

BPA tariff - Townsend to Garrison $7.36 $7.36

BPA tariff - Garrison to PSE $35.23 $35.23 $35.23

Total Fixed Transmssion Cost ($/kW-yr) $35.23 $55.05 $51.75

O&M Fixed ($/kw-yr) $27.12 $27.12 $27.12

Wind Costs

87

Difference

from base

Peak Capacity

Credit

Portfolio

Costs

Benefit/

(Cost)Base Case $12,276,911

MT Wind 2023 300 MW 55% $12,461,758 ($184,847)

MT Wind 2023 300 MW 50% $12,473,556 ($196,645)

MT Wind 2023 300 MW 45% $12,482,803 ($205,893)

MT Wind 2023 300 MW 40% $12,502,560 ($225,649)

Montana Wind Results

88

Portfolio Sensitivity I – Thermal Mix

June 18, 2015 IRPAG

Annual

Builds (MW) CCCT

Frame

Peaker All Others CCCT

Frame

Peaker All Others CCCT

Frame

Peaker All Others

2016 - - 93 - - 95 - - 93

2017 - - 76 - - 79 - - 76

2018 - - 108 - - 112 - - 108

2019 - - 78 - - 82 - - 78

2020 - - 122 - - 127 - - 122

2021 - - 64 - - 70 - - 64

2022 - - 78 - - 84 - - 78

2023 - 228 159 - - 263 - 228 159

2024 - - 158 385 - 62 - - 158

2025 - - 55 - - 60 - - 55

2026 - 455 29 385 - 30 385 - 29

2027 - - 129 - - 32 385 - 129

2028 - 228 30 - - 132 - - 30

2029 - - 25 - - 27 - - 25

2030 - - 26 385 - 27 - - 26

2031 - 228 29 - - 31 - - 29

2032 - - 35 - - 37 - - 35

2033 - - 46 - - 48 - 228 46

2034 - - 27 - - 28 - - 27

2035 - - 106 - - 27 - - 26

Total - 1,138 1,473 1,156 - 1,454 771 455 1,393

Total

Nameplate

Portfolio NPV

($000)

2,611 2,611

Mix CCCT & Peaker

2,619

12,363,387

Base

12,276,911

All CCCT

12,470,600

89

Total Expected Cost of Portfolios

(Difference from Base Scenario $000)

(6,000,000) (4,000,000) (2,000,000) 0 2,000,000 4,000,000 6,000,000

Recip Engine updated cost

Gas Plant Location

Thermal Mix

Energy Storage in 2023

Gas Transport for Peakers

Carbon Reduction

No DSR

Gas Price

CO2 Price

Demand

Scenario

Total Portfolio Cost (Difference from Base $000)

Low

High

Very High

Base = 0Low High

Base + Low Demand

Base + High Demand

Base + No CO2

Base + High CO2

Base + Low Gas Price

Base + Very High Gas Price

Base + High Gas Price

75 MW in 2035

75 MW in 2023

80 MW Battery

80 MW Pumped Hydro

300 MW Wind in 2021

300 MW Solar in 2021

Mix CCCT & Frame

All CCCT

224 MW in 2035

Factors out of

our control

Decisions we

can control

Electric Stochastic

Modeling Villamor Gamponia & Elizabeth Hossner

June 18, 2015 IRPAG

91

Model Overview – Electric Analysis

June 18, 2015 IRPAG

AuroraXMP

Develops scenario prices and dispatched resource outputs, costs and revenues for each input draw

Stochastic Model

Develops distribution of inputs:Electric and Gas Prices

PSE LoadsHydro and Wind Generation

CO2 Cost/PriceThermal Forced Outage Rates

PSM III

Uses PSE financial model to develop optimal portfolio for each

scenario

92

Stochastic Model: Goal

June 18, 2015 IRPAG

• Challenge is to capture risk in a systematic and consistent

way

• Key correlations across risk variables and time

• Identify major sources of risks

• Weather (Temperature, Hydro Conditions, Wind)

• Market (Economic/Population/Gas & Power)

• Regulation – CO2

93

Stochastic Model: Flow Chart

June 18, 2015 IRPAG

Weather Inputs Outputs

Economic/Demographic

Market/Regulatory Inputs

Historical Wind

Historical Hydro

Historical Temperature

Historical Elec/Gas Prices

Population,Economic Conditions

US Gas Storage, WTI Oil Prices

Wind Sims

Hydro Sims

Temp Sims

Wind Draws

Hydro Draws

Temp Draws

PSE LoadModel

Elec Price Model

Gas Price Model

PSE Load Draws

Elec Price Draws

Gas Price Draws

CO2 PriceScenario CO2 Scenario Sims

CO2 ScenarioDraws

Thermal Forced Outage Rate

Aurora Convergent Outage Method

FOR Draws

94

Stochastic Inputs for Portfolio Modeling

June 18, 2015 IRPAG

• 250 Draws for each of the inputs

• Mid-C Power Prices

• Sumas Gas Prices

• CO2 Prices

• Wind Generation

• Hydro Generation

• PSE Demand – Peak and Energy

• Thermal Plant Forced Outage

95

Stochastic Inputs: Power & Gas Price Equations

June 18, 2015 IRPAG

Econometric equations in semi-log form

MidC Price = f(Sumas Price, Regional Temp Devs, Day of Week, Holidays,

MidC Hydro Generation)

Sumas Price = f(US Gas Storage Devs fr 5Yr Avg, WTI, lagged WTI, Trend,

Fracking)

AECO Price = f(Sumas Price)

Data – daily data from 1/2003 to 12/2014

Equations were estimated simultaneously with autocorrelation(to

be shown in the Appendix)

WTI = West Texas Intermediate Oil Price

96

Stochastic Inputs: Power & Gas Price Draws

June 18, 2015 IRPAG

Approach for Gas and Power Price Draws

250 Monte Carlo draws based on estimated equation and parameter error distributions, temp draws, hydro draws, West Texas Intermediate oil price draws

Temperature and hydro draws are consistent with temperature and hydro combination from Genesys; 11% of the draws include regional deficits

Filter draws with extreme daily price(>P99.9 of prices in 2000-2001)

• (0<power<$750/MWH, 0<gas<$40/mmbtu)

Adjust the expected value of the draws to fundamental power and gas prices from the Aurora Model; also adjust the P05 and P95 for Low and High fundamental prices

97

Annual Mid-C Power Price Draws

June 18, 2015 IRPAG 0

25

50

75

100

125

150

175

200

225

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

An

nu

al A

vera

ge M

id-C

Po

wer

Pri

ces

($/M

Wh

)

Average of 250

P95

P05

98

Annual Sumas Gas Price Draws

June 18, 2015 IRPAG 0

2

4

6

8

10

12

14

16

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

Ann

ual A

vera

ge S

umas

Gas

Pri

ce ($

/MM

Btu

)

P95

P05

99

MidC Price Distribution for Operating Year

2020-2021

June 18, 2015 IRPAG

10

0

CO2 Price Draws

June 18, 2015 IRPAG

• CO2 Tax/Price – draws based on cost/price scenarios and

assigned probability (No CO2-33.3%, Mid CO2-33.3%, High CO2-

33.3%)

0

20

40

60

80

100

120

140

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

No

min

al

$/t

on

2015 IRP Low - No CO2 Price

2015 IRP Mid - NPCC CA

2015 IRP High - Wood Mackenzie High

2015 IRP Average of 250 Draws

10

1

Wind Generation

June 18, 2015 IRPAG

• Synchronized daily draws each month using data through 2014 from Hopkins, Wild Horse, and LSR (LSR only has 2 years of operation, so supplemented data with lagged Hopkins data scaled to actual capacity and pro-forma capacity factor). Generic WA Wind based on LSR/Hopkins data.

0

10

20

30

40

50

60

70

30% 31% 32% 33% 34% 35% 36% 37% 38%

Freq

uenc

y (C

ount

)

Annual Capacity Factor (%)

Generic WA Wind

Draws –

Frequency of

Annual Capacity

Factor for 250

Draws

10

2

Generic WA Wind Draws –

Monthly Capacity Factor for 250 Draws

June 18, 2015 IRPAG

0%

10%

20%

30%

40%

50%

60%

70%

1 2 3 4 5 6 7 8 9 10 11 12

Mon

thly

Cap

acit

y Fa

ctor

(%)

Month

Average of 250

10

3

Hydro Generation

June 18, 2015 IRPAG

• Draws of monthly flows/capacity factors based on 80-Year Hydro

from PNCA(Pacific Northwest Coordination Agreement)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1 2 3 4 5 6 7 8 9 10 11 12

Average of 250

Monthly Hydro

Factors for 5 Mid-C

Projects

10

4

Demand Draws

June 18, 2015 IRPAG

• Monte Carlo draws on economic and demographic inputs are

based on historical standard errors of growth in macroeconomic

and key regional inputs into the model such as population,

employment and income;

• The stochastic simulation also accounts for the error distribution

of the estimated customer counts and use per customer

equations and the estimated equation parameters;

• Temperature draws used on 1929-1947 Portage Bay data (near

UW) and 1948-2005 SeaTac data; HDDs/CDDs based on each

temperature year draw is run through the demand forecast model;

impacts on monthly/hourly profile and use/customer

10

5

Demand Draws – Annual Energy

June 18, 2015 IRPAG 2,000

2,500

3,000

3,500

4,000

4,500

5,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

PSE

Dem

and

(aM

W)

Average of 250

P95

P05

10

6

Demand Draws - Peak

June 18, 2015 IRPAG 4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

PSE

Peak

Dem

and

(MW

)

Average of 250

P95

P05

10

7

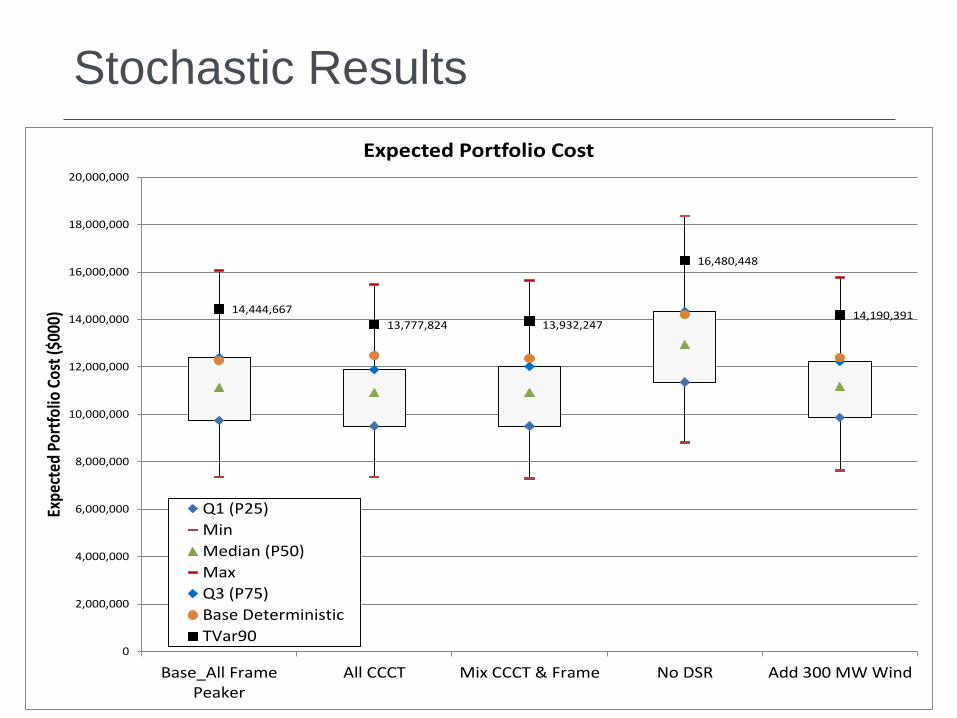

Stochastic Results

10

8

Stochastic Analysis Results

June 18, 2015 IRPAG

NPV ($Millions)

Base

Deterministic

Portfolio Cost

Difference from

BaseTVar90

Difference from

Base

Base (all Frame Peaker) 12,277 14,445

All CCCT 12,471 194 13,778 (667)

Mix Frame & CCCT 12,363 86 13,932 (512)

No DSR 14,208 1,931 16,480 2,036

Add 300 MW Wind 12,384 107 14,190 (254)

Levelized ($Millions)Levelized

Portfolio Cost

Difference from

BaseTVar90

Difference from

Base

Base (all Frame Peaker) 1,203 1,360

All CCCT 1,248 45 1,341 (20)

Mix Frame & CCCT 1,238 35 1,345 (16)

No DSR 1,422 219 1,569 208

Add 300 MW Wind 1,240 37 1,358 (2)

10

9

Stochastic Results

June 18, 2015 IRPAG

14,444,667

13,777,824 13,932,247

16,480,448

14,190,391

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

Base_All FramePeaker

All CCCT Mix CCCT & Frame No DSR Add 300 MW Wind

Expe

cted

Por

tfol

io C

ost (

$000

)

Expected Portfolio Cost

Q1 (P25)

Min

Median (P50)

Max

Q3 (P75)

Base Deterministic

TVar90

11

0

0

20

40

60

80

100

120

140

Fre

qu

en

cy (

Co

un

t)Frequency Histogram of Expected Portfolio Cost (Billions $)

Base Portfolio

Base_No DSR

Base Portfolio mean = $11.1

Base_No DSR mean = $12.9

11

1

(3,000)

(2,500)

(2,000)

(1,500)

(1,000)

(500)

-

500

1,000

1,500

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035

An

nu

al P

ea

k Su

rplu

s/(N

ee

d)

-M

WBase Portfolio Annual Peak Surplus/(Need) - MW

Q1 (P25)

Min

Median

Max

Q3 (P75)

Mean

11

2

Net Cost of Capacity

11

3

Cost of Incremental Capacity

June 18, 2015 IRPAG

Based on PSM for the 2015 IRP

NPV to 2016($000s)

Net Cost w/o

Replacement

Replacement

Cost

Net Cost w

Replacement

Levelized

Cost

Capacity

(MW)

Levelized

Cost/MW

New CCCT 2020 738,139 82,828 820,967 61,862 385 160.68

New Peaker Aero 2020 424,201 41,696 465,897 35,551 203 175.13

New Peaker Frame 2020 385,692 44,890 430,582 32,324 228 141.77

New Peaker Recip 2020 569,848 47,893 617,741 47,758 220 217.08

2. Base - 2015 IRP

NPV to 2016 ($000)

Net Cost w/o

Replacement

Replacement

Cost

Net Cost w

Replacement

Levelized

Cost

Capacity

(MW)

Levelized

Cost/MW

New CCCT 2020 640,446 64,147 704,593 53,674 385 139.41

New Peaker Aero 2020 418,176 40,263 458,439 35,046 203 172.64

New Peaker Frame 2020 390,542 47,680 438,222 32,730 228 143.55

New Peaker Recip 2020 567,329 48,743 616,072 47,546 220 216.12

7. Base + No CO2 - 2015 IRP

11

4

Net Cost Distribution (2020 $/kW – Capacity)

0

50

100

150

200

250

300

350

-110

-100 -9

0

-80

-70

-60

-50

-40

-30

-20

-10 0 10 20 30 40 50 60 70 80 90 100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

260

Freq

uenc

y (C

ount

of 1

000

Tria

ls)

Net Cost ($/kW)

2020 Frame Peaker

2020 CCCT

Wrap Up/Review Action

Items Lyn Wiltse

June 18, 2015 IRPAG

11

6 June 18, 2015 IRPAG

Adjourn