ird rfp flexible workforce supply of unisys -

TRANSCRIPT

Request For Proposal

for

Flexible workforce Supply of Unisys

COBOL specialists

Ref: 201206300

Month May 2012

Important note:

Please read all sections of this RFP. Submitting a Response to this RFP is deemed

to be the Participant‟s acceptance of the RFP Rules.

Page 2 of 27 02/05/2012

TABLE OF CONTENTS

TABLE OF CONTENTS ................................................................................... 2

1 INTRODUCTION .................................................................................... 4

1.1 Purpose of this RFP ......................................................................... 4

1.2 Participation ................................................................................... 4

1.3 Inland Revenue .............................................................................. 4

1.4 Introduction to IT Development Capabilities ....................................... 4

1.5 Introduction to this procurement ....................................................... 6

2 Communication about this RFP ................................................................ 8

2.1 Communication channels ................................................................. 8

2.2 Clarifications .................................................................................. 8

3 The RFP Process .................................................................................... 9

3.1 Stages of the RFP............................................................................ 9

3.2 RFP Timeline .................................................................................. 9

3.3 Submission of Proposals ................................................................ 10

3.4 Evaluation of Proposals .................................................................. 10

3.5 RFP Rules ..................................................................................... 11

3.6 Tax Secrecy ................................................................................. 11

3.7 Due diligence tax checks ................................................................ 11

4 Statement of Requirements .................................................................. 12

4.1 Scope of Flexible workforce supply of Unisys COBOL Specialists .......... 12

4.2 Requirements General ................................................................... 12

4.3 Mandatory Requirements ............................................................... 13

4.4 Resource and Relationship Requirements ......................................... 13

4.5 Service Delivery Requirements ....................................................... 13

4.6 Contractual Requirements .............................................................. 13

4.7 Fees and Charges ......................................................................... 14

5 Proposals from Participants .................................................................. 15

5.1 General ....................................................................................... 15

5.2 Acceptance of tender rules ............................................................. 15

5.3 Due diligence tax checks ................................................................ 15

6 RULES ............................................................................................... 16

6.1 Inland Revenue's Right to Accept or Reject Any Proposal ................... 16

6.2 Status of RFP ................................................................................ 16

6.3 Due Date for Proposals and Late Proposals ....................................... 16

6.4 Cost of Proposal ............................................................................ 16

6.5 Proposals to Remain Open.............................................................. 16

6.6 Pricing ......................................................................................... 16

Page 3 of 27 02/05/2012

6.7 Additional Information May be Included ........................................... 16

6.8 Participants to Inform Themselves .................................................. 17

6.9 Validity of Inland Revenue Information ............................................ 17

6.10 Inland Revenue Information ........................................................... 17

6.11 Reliance upon Statements by Participants ........................................ 17

6.12 Confidentiality .............................................................................. 18

6.13 Advertising and Statements ........................................................... 18

6.14 Evaluation Process and Important Factors ........................................ 18

6.15 Requirements ............................................................................... 19

6.16 Standard Contractual Provisions...................................................... 19

6.17 Rights Reserved by Inland Revenue ................................................ 19

6.18 Satisfactory Proposal ..................................................................... 19

6.19 Joint Proposals ............................................................................. 20

6.20 Inland Revenue to Advise of Outcome ............................................. 20

6.21 Indemnity .................................................................................... 20

6.22 Warranties ................................................................................... 20

6.23 Tax Compliance, Criminal and Company Checks ................................ 21

6.24 Public Finance Law Restrictions ....................................................... 21

6.25 No Canvassing .............................................................................. 21

6.26 Ethics .......................................................................................... 21

6.27 Governing Law.............................................................................. 21

6.28 Definitions and Interpretation ......................................................... 21

APPENDIX 1: Cover Letter – provided as a separate document....................... 23

APPENDIX 2: Detailed Requirements - provided as a separate document ......... 24

APPENDIX 3: IR‟s Standard Terms and Conditions - provided as a separate

document ................................................................................................. 25

APPENDIX 4: IR820 - provided as a separate document ................................. 26

APPENDIX 5: IR822 - provided as a separate document ................................. 27

Page 4 of 27 02/05/2012

1 INTRODUCTION

1.1 Purpose of this RFP

Inland Revenue has released this Request for Proposal (RFP) because it is seeking

to identify a supplier to work with Information Technology Operations and

Services (IT) to provide flexible supply of specialised IT Unisys COBOL resources.

We need to secure key skills and capability which will allow IR to have a flexible

and sustained level of resource trained to a level of competence to work on IR‟s

custom-built mainframe business systems on the UNISYS Clearpath platform.

Suppliers responding or intending to respond to this RFP shall be known as

Participants.

1.2 Participation

This is an open invitation to Participants through the Government Electronic

Tenders Services (GETS).

1.3 Inland Revenue

Inland Revenue's primary outcome is improving the economic and social well

being of New Zealanders.

Inland Revenue undertakes a full range of tax administration functions and

collects approximately 85% of the Government's revenue. Inland Revenue along

with other Government departments administers Working for Families Tax

Credits, Child Support, Paid Parental Leave, the Student Loan Scheme and

KiwiSaver.

Inland Revenue's Our Way Forward and Statement of Intent outline the key

strategies for us over the next three to five years. These documents and other

useful information can be found at www.ird.govt.nz.

1.4 Introduction to IT Development Capabilities

The Development Capabilities are made up of development team that support our

core tax and social policy systems on a Unisys Mainframe, integration and

electronic interfaces and channels, Commercial off the Shelf (COTS) systems,

Internet and Intranet based content management system, Business Intelligence,

data warehouse and Enterprise Resource Planning (ERP) systems based around

the SAP platform. The systems are supported by the Service Management and

Technical and Operations and Database Capabilities within the Information

Technology group at Inland Revenue.

Inland Revenue‟s mainframe IT system is a Unisys ClearPath Libra 690 server

located in Auckland and operated by HP. The core tax and social policy systems

run in this environment and is commonly known as FIRST (Future Inland Revenue

Systems Technology). The FIRST development and DR server is also a Unisys

Libra 690 located in Upper Hutt.

Some statistics about FIRST:

> 6 million online transactions / day (< 1 sec response time)

Unisys Cobol 74 ( 6,000 programs, 60 million lines of code)

~ 6.965 million Customer Base (individuals, businesses, partnerships,

trusts etc)

> 587,000 Student Loan borrowers

> 1.46 million KiwiSaver members

Page 5 of 27 02/05/2012

> 180,000 Child Support custodians

~ 4,700 Tax Agents (represent 1.7million customers)

> 80 million items of output issued per year

> 8 million Returns processed per year

> 8 million Payments processed per year

> $1.8 billion Debt collected per year

> $347 million Child Support collected per year

> $486 million Student Loans collected per year

> $1.7 billion Family Assistance distributed per year

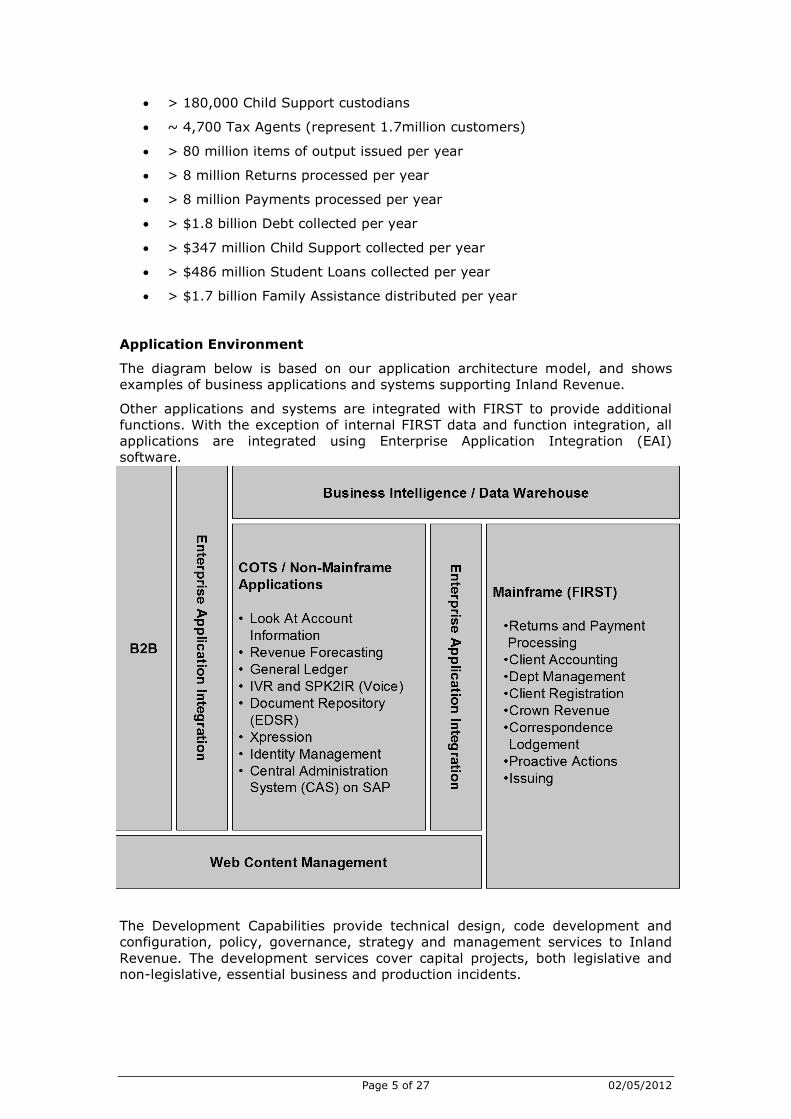

Application Environment

The diagram below is based on our application architecture model, and shows

examples of business applications and systems supporting Inland Revenue.

Other applications and systems are integrated with FIRST to provide additional

functions. With the exception of internal FIRST data and function integration, all

applications are integrated using Enterprise Application Integration (EAI)

software.

The Development Capabilities provide technical design, code development and

configuration, policy, governance, strategy and management services to Inland

Revenue. The development services cover capital projects, both legislative and

non-legislative, essential business and production incidents.

Page 6 of 27 02/05/2012

The Database Capability is responsible for Mainframe DMSII and Oracle databases

including Real Application Cluster (RAC) databases. Applications integrate to this

environment utilising Database access libraries and direct database access.

Supporting the core Unisys based systems are external and internal Portal

applications, utilising IBM Websphere Portal. Integration and middle layer (for

example; B2B and Enterprise Application Integration) using technologies including

JCAPS and Oracle SOA suite and Oracle Weblogic. Customer identities are

integrated using Oracle Identity Manager and access source information from the

core systems. As IR transforms it business and core IT systems, IR will be

exposing its core systems as services and utilising Business Rules authored in

Oracle‟s Rules products.

Key functions are also supported via software package implementation and

configuration and support, including: Seibel, Remedy, Electronic Document

Storage and Retrieval (EDSR), Imaging, xPression, Oracle Enterprise Tax

Management.IR is using Oracle WebLogic Server which forms part of Oracle

Fusion Middleware portfolio and supports Java EE application server, WebLogic

Application Server, Oracle Service Bus (OSB), Enterprise Application Integration

platform and transaction server and infrastructure. IR is running Weblogic server

11gR1 (10.3.4) and SOA Suite 11g (11.1.1.4). As a recent deployment, IR needs

to support projects to integrate solutions into an enterprise architecture solution

for future growth and development, support project demand and support the

support of existing deployments. The design and development specifications

above are applicable for these skills.

Development methodologies followed are waterfall based or a waterfall hybrid,

agile methods are also possible. The methods used are determined by the scope

and nature of the work. The guiding process are defined in IR‟s Business Project

Method (BMP) and Systems Develop Life Cycle (SDLC). Projects are managed via

a programme or project governance group reporting through to an executive

Project Governance & Investment Committee (PGIC). Documentation, process,

stage gates and reporting requirements are maintained electronically on IR‟s

Intranet.

1.5 Introduction to this procurement

The objective is to secure a multi-year term supplier of skilled, experienced and

capable “hit the ground running” resources as required to assist us in meeting the

demands of projects and development service requirements. Objectives of this

procurement process are:

Access to a flexible supply of Unisys COBOL development resource

Retention of IR knowledge through partnering

Sharing risk through partnering

Economies of scale in utilising Third Parties

Reduction of ad-hoc “body shopping”

Introduction of repeatable process through Partnering

We need to secure key skills and capability and the ability to have a sustained

level of resource and a flexible supply trained to a level of competence in IRs

business systems, processes, and technologies .

The nature of the resource supply will be to augment current resources in order

for IR to deliver on current and emerging business demands for the organisation.

1.5.1 Relationship to Development Services Panel

This approach will operate in conjunction with the Development Services Panel.

The Panel is aimed at shorter and more tactical resourcing requirements

Page 7 of 27 02/05/2012

compared to this engagement. Being a member of the Panel will not preclude a

supplier from responding or being a supplier for this engagement.

1.5.2 Relationship to RFQ 201206100 Unysis and COBOL Developer

Inland Revenue have recently been to Market for the similar services under an

RFQ on an Open Tender basis. These engagements and are designed to meet a

short term need for the business until this procurement process delivers a more

strategic solution. Suppliers appointed under 201206100 will not be excluded

from tendering for this engagement.

Page 8 of 27 02/05/2012

2 Communication about this RFP

2.1 Communication channels

All enquiries regarding this RFP must be directed via email to

[email protected]. Please quote reference number 201206300 in any

communication.

Please note that Participants, including any existing suppliers, should not discuss

this RFP with, or direct questions to, Inland Revenue personnel. Questions will

only be accepted in writing via email to the above address. Any breach of this

requirement may result in the exclusion of the party from the RFP process.

2.2 Clarifications

Participants are responsible for identifying any further information required to

prepare their RFP Response („Proposal‟). Any clarifications should be made through the process described in this section 2.

Questions and answers to questions may be summarised and published on the

GETS website. However, Inland Revenue reserves the right not to do this.

Inland Revenue may reword questions as appropriate to provide greater clarity or

relevance to other Participants.

Inland Revenue reserves the right not to provide further clarification to, or

answer questions from, Participants.

Page 9 of 27 02/05/2012

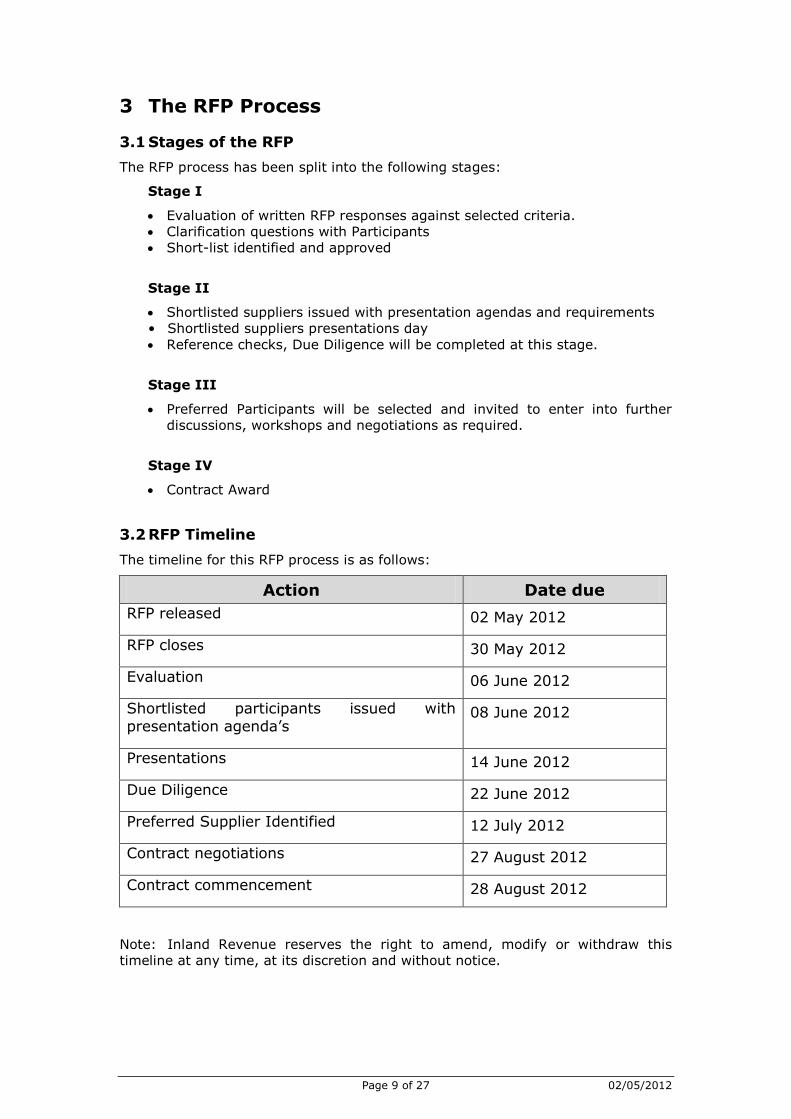

3 The RFP Process

3.1 Stages of the RFP

The RFP process has been split into the following stages:

Stage I

Evaluation of written RFP responses against selected criteria.

Clarification questions with Participants

Short-list identified and approved

Stage II

Shortlisted suppliers issued with presentation agendas and requirements

• Shortlisted suppliers presentations day

Reference checks, Due Diligence will be completed at this stage.

Stage III

Preferred Participants will be selected and invited to enter into further

discussions, workshops and negotiations as required.

Stage IV

Contract Award

3.2 RFP Timeline

The timeline for this RFP process is as follows:

Action Date due

RFP released 02 May 2012

RFP closes 30 May 2012

Evaluation 06 June 2012

Shortlisted participants issued with

presentation agenda‟s 08 June 2012

Presentations 14 June 2012

Due Diligence 22 June 2012

Preferred Supplier Identified 12 July 2012

Contract negotiations 27 August 2012

Contract commencement 28 August 2012

Note: Inland Revenue reserves the right to amend, modify or withdraw this

timeline at any time, at its discretion and without notice.

Page 10 of 27 02/05/2012

3.3 Submission of Proposals

Five numbered and bound Proposals should be submitted in hard copy. A soft

copy must also be provided. Please ensure that all parts, appendices or

schedules, which are required to be included as part of your written response, are

included in the soft copy format. These copies become the property of Inland

Revenue and will not be returned.

Please note that Inland Revenue may, in its discretion, treat either the hard copy

or soft copy version of the Proposal as the public record for the purposes of the

Public Records Act 2005. If there is any discrepancy between the two, Inland

Revenue may, in its discretion, choose which of the two takes precedence, and

that one will be the public record.

All Proposals must be received by Procurement by 12.00 Midday on 30 May 2012

Proposals are to be delivered to:

Inland Revenue

Level 4, Asteron House

55 Featherston Street

Wellington

Attention: Procurement - RFP 201206300

If your soft copy is not too large to be e-mailed, please e-mail it to

[email protected] and quote reference number 201206300 in the subject line.

Otherwise, submit it with the hard copies on a CD.

Inland Revenue's requirements about the form of Proposals and the information

which must be included in them are set out in section 5 below.

3.4 Evaluation of Proposals

3.4.1 Evaluation criteria

Inland Revenue will evaluate each Proposal based on how well it meets Inland

Revenue's requirements. Inland Revenue has identified the following factors as

being important in the evaluation process:

Participant‟s proposed approach to the delivery of a flexible supply for

Unisys COBOL specialist services including the qualifications and/or

experience of proposed personnel, including details of currency with

technology sets (Working with applicable versions used in IR) and

technology used with IR‟s environment.

Participant‟s experience, capability and capacity in delivering to the

requirements, the ability to increase or decrease the resource supply

based on demand;

Participant‟s proven track record in Government or relevant industry

sector;

Participant‟s security and management processes including contingency

and risk mitigation strategies;

Participant‟s proposed level of investments in IR knowledge of IR systems

and process until such time as the group is at an appropriate level to work

autonomously.

Acceptance by the Participant of the form of Agreement attached as

Appendix 3 of this Proposal or the extent to which the Participant wishes

to depart from it.

The above list of evaluation criteria is not exhaustive, and the criteria are not

listed in any order of priority or with any indication as to relative weightings.

3.4.2 Changes to evaluation criteria

Page 11 of 27 02/05/2012

Inland Revenue may, at any time (including after receipt of Proposals), change

the criteria listed in section 3.4.1 and/or the weighting it places on each criterion

without notifying Participants. Inland Revenue will determine (in its sole

discretion) how the evaluation of any Proposal will be undertaken.

3.5 RFP Rules

The Rules that will apply to and throughout this RFP Process are provided in

section 6. If there is any conflict between the Rules and any other part of

this RFP, the Rules take precedence.

3.6 Tax Secrecy

As part of the RFP Process, Inland Revenue may need to share information with

the Participants that is considered tax secret under the Tax Administration Act

1994.

To ensure that tax secret information can be shared with you, please have all

personnel involved in preparing your bid complete the certificate of secrecy form

(IR820) attached in Appendix 4 and return those IR820 forms with your Tender

Response.

3.7 Due diligence tax checks

As part of Inland Revenue‟s due diligence process the chosen supplier or suppliers

will be required to be reviewed for tax compliance.

Please complete the attached IR 822 form at Appendix 5 that authorises Inland

Revenue to review your taxation records and return this with your proposal.

Page 12 of 27 02/05/2012

4 Statement of Requirements

4.1 Scope of Flexible workforce supply of Unisys COBOL Specialists

4.1.1 In Scope

The following Deliverables are in scope:

Provision of specialist resources with key skills and capability which will

allow IR to have a flexible and sustained level of resource trained to a

level of competence to work on IR‟s custom-built mainframe business

systems on the UNISYS Clearpath platform.

Augment IR resources in order for IR to deliver on current and emerging

business demands for the organisation.

Maintain a training program for inducting developers with standard Unisys

COBOL 74 and utilities (e.g. WFL, Cande, ERGO, etc.1 ) and the IR system

and development environment. This may include the development,

update and maintenance of a training program based on IR ad-hoc

collateral.

The management of the retained knowledge, training and pipeline

information.

Participants will be invited to provide details in their RFP response of other

reporting and management approaches they provide which could benefit IR.

Inland Revenue will consider proposals that utilise a resourcing delivery model

that achieves the outcomes of the RFP and provides a cost effective model,

including but not limited to the ability to provide services on-site at IR.

4.1.2 Out of Scope

For the avoidance of doubt, the following is not in scope for supply:

Unisys Mainframe Hardware, Database or Mainframe Software and

Mainframe Operations Services.

Detailed requirements are contained in Appendix 2

4.2 Requirements General

All requirements are set out (as shown below) in the table attached at Appendix

2. Participants must use this table to respond to the requirements listed and

return this completed appendix with other supporting documentation as described

in section 5.

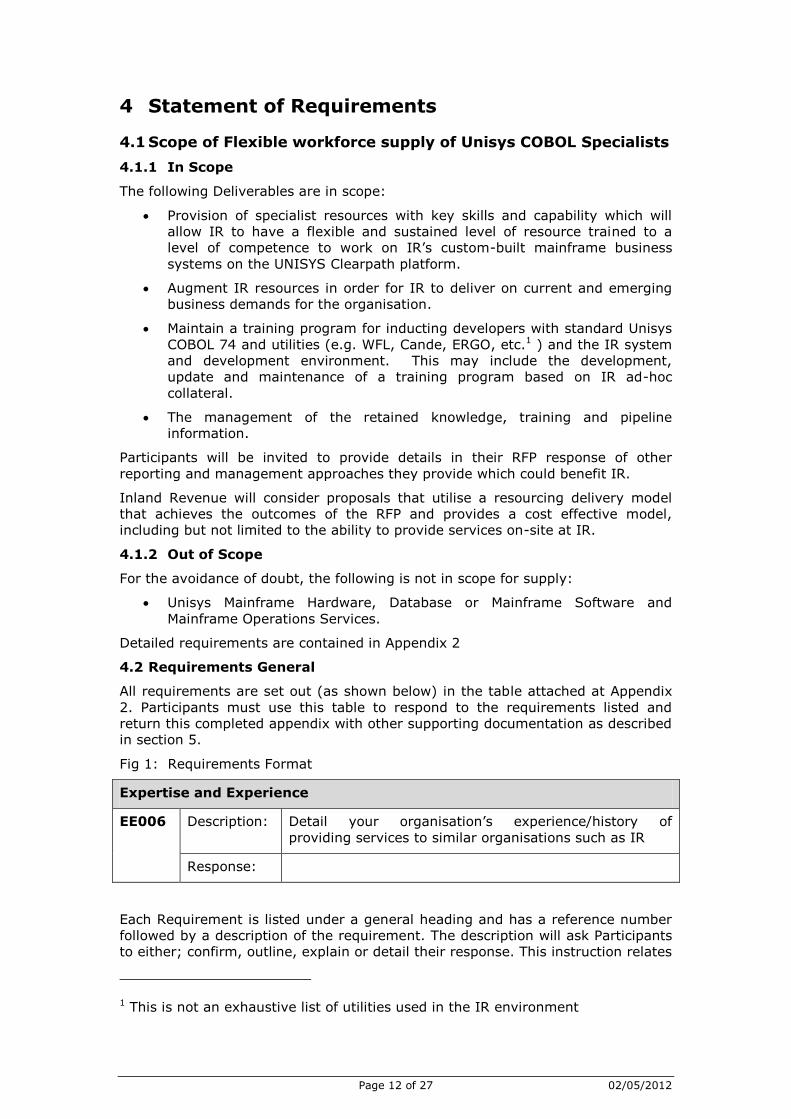

Fig 1: Requirements Format

Expertise and Experience

EE006 Description: Detail your organisation‟s experience/history of

providing services to similar organisations such as IR

Response:

Each Requirement is listed under a general heading and has a reference number

followed by a description of the requirement. The description will ask Participants

to either; confirm, outline, explain or detail their response. This instruction relates

1 This is not an exhaustive list of utilities used in the IR environment

Page 13 of 27 02/05/2012

to the amount of written information that the participant should provide as

follows:

Confirm – This may be a yes/no answer, or where requested a sentence

confirming the requirements or providing the information

Outline – A summary or paragraph[s] relating to the requirement, within

half a page of A4 or 300 words

Explain – A full response to the requirement within two pages of A4 or

1000 words

Detail – Requiring a full, detailed response covering the requirement.

Where the instruction asks for a separate document Participants must

cross reference this with the requirement reference

The final box must be used for participant responses, including any cross

referencing to separate documents.

4.3 Mandatory Requirements

Some of the requirements outlined in the Statement of Requirements in Appendix

2 are Mandatory Requirements. This means that these requirements are

considered essential to Inland Revenue in the provision of flexible workforce

supply of Unisys COBOL Specialists.

4.4 Resource and Relationship Requirements

IR will require the following competencies and skills of the specialist resources:

A high level of technical knowledge, expertise and leadership, with

advanced analysis and design ability in IR‟s business systems

environment, incorporating integration across a number of information

systems and platforms to ensure the delivery of quality IT solutions to

meet the business requirements;

A driving attitude for collaboration and success;

A solid and proven understanding of the software development lifecycle

and Inland Revenues project management practices, methodologies,

industry standards, IT security and Enterprise Architecture;

Comprehensive written and verbal communication skills, including the

ability to understand different forums and communicate appropriately;

Excellent people and relationship management skills;

Facilitation, negotiation and problem resolution skills; and

Highly developed organisational skills to ensure deadlines and quality

objectives are met.

The requirements of the service provider defined in Appendix 2 details how the

service provider proposes to manager the account, the resources provided, the

approach to staff training and knowledge management and how the organisation

communicates to ensures everyone in the environment is informed as required.

4.5 Service Delivery Requirements

Requirements outlined in the Statement of Requirements in Appendix 2 are for

the provision of services from organisations that have experience/history of

providing the proposed services to New Zealand government or large corporate

organisations. The expectation of the service provider is that the service includes

work management and leadership of the team as well as the expectation that the

people allocated to do the work within the reporting lines and are capable and

experienced to deliver the types of activity defined.

4.6 Contractual Requirements

Appendix 3 of this RFP provides a copy of Inland Revenue‟s Standard Contractual

Provisions. Participants are to read these provisions and confirm their agreement

Page 14 of 27 02/05/2012

to them or, using the table format below, identify those provisions you wish to

discuss with a clear indication of the particular points of concern. Participants

agree that they will not attempt to negotiate any changes to Inland Revenue's

Standard Contractual Provisions which have not been raised in their Proposal.

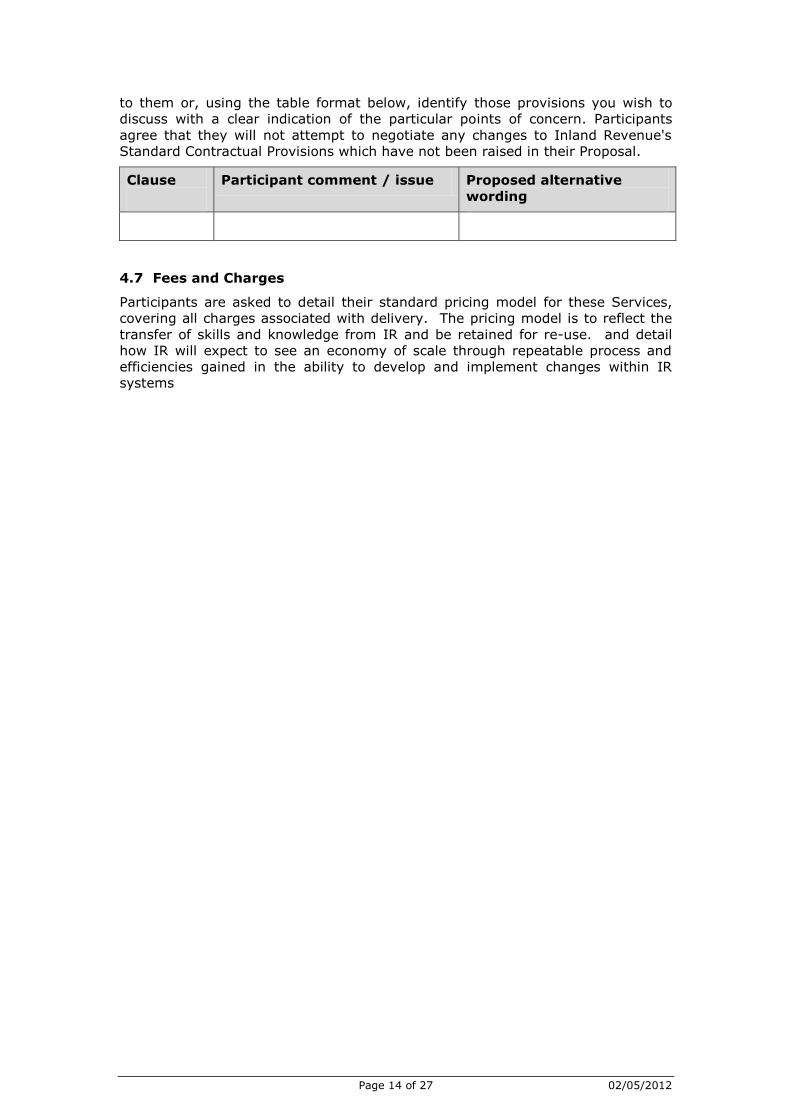

Clause

Participant comment / issue Proposed alternative

wording

4.7 Fees and Charges

Participants are asked to detail their standard pricing model for these Services,

covering all charges associated with delivery. The pricing model is to reflect the

transfer of skills and knowledge from IR and be retained for re-use. and detail

how IR will expect to see an economy of scale through repeatable process and

efficiencies gained in the ability to develop and implement changes within IR

systems

Page 15 of 27 02/05/2012

5 Proposals from Participants

5.1 General

5.1.1 RFP responses (Proposals) must:

have a cover letter in the form attached to this RFP as Appendix 1;

Detailed requirements response form Appendix 2;

Mandatory Forms Appendix 4 and 5;.

5.1.2 Proposals must be submitted in accordance with section 3.3.

5.1.3 The Proposal must follow the structure set out in the table contained in

Appendix 2, with Proposal content presented in the format provided.

5.1.4 A response must be provided for every requested item of information in

this RFP.

5.1.5 If an answer to a question in one section is identical for another,

Participants should repeat the relevant text in the question response area.

Do not refer to an answer provided in another section, e.g. “see question

1.1 for response”.

5.1.6 Where additional information about Inland Revenue, its systems, policies

and/or infrastructure is needed before an adequate response can be made

to any question, please attempt to obtain that information from Inland

Revenue through the process outlined at section 2.2 rather than including

assumptions in your Proposal. Your Proposal must, however, identify

where you have made assumptions, and the impact of those assumptions.

A response which is too general, like “it depends upon Inland Revenue” or

“more information required”, will be considered inadequate.

5.2 Acceptance of tender rules

Section 6 provides the Rules that will apply to and throughout this RFP Process.

Participants are to review these Rules and confirm compliance with them. In the

event of any uncertainty or concerns, the Participant is asked to contact Inland Revenue using the procedure outlined in section 2 and detail the comments /

concerns. If there is any inconsistency between the Rules and the rest of this RFP,

the Rules will take precedence.

5.3 Due diligence tax checks

Please complete the attached IR 822 form that authorises Inland Revenue to

review your taxation records.

Page 16 of 27 02/05/2012

6 RULES

These Rules have been drafted in consultation with Corporate Legal and cannot

be changed without prior consultation with Corporate Legal or National

Procurement.

The following Rules apply to the RFP process. By submitting a Proposal or

otherwise participating in the RFP process each Participant accepts that it is

bound by the Rules.

6.1 Inland Revenue's Right to Accept or Reject Any Proposal

Inland Revenue reserves the right to accept or reject any Proposal, regardless of

whether it conforms with, or is submitted in accordance with, the requirements of

this RFP. Inland Revenue further reserves the right to vary or cancel the RFP

process and/or reject all or any of the Proposals at any time prior to signing of

any Agreement.

6.2 Status of RFP

This RFP does not constitute an offer by Inland Revenue to acquire any Goods or

Services or enter into an Agreement with any Participant for the supply of all or

part of any related Goods or Services.

6.3 Due Date for Proposals and Late Proposals

6.3.1 Inland Revenue may extend the due date for any Proposal or any part of it

at its discretion. Inland Revenue reserves the right to accept or decline

late Proposals at its discretion.

6.3.2 Inland Revenue reserves the right to vary the RFP timetable described in

this RFP (including the activities and timing) at any time in its absolute

discretion. Inland Revenue may vary the timetable applicable for any

particular Participant, without having to make any such variation for all of

the Participants.

6.4 Cost of Proposal

Each Participant shall be responsible for all costs associated with the development

and submission of its Proposal.

6.5 Proposals to Remain Open

Each Proposal must remain open for consideration by Inland Revenue for a

minimum period of six months after the due date for Proposals stipulated in this

RFP.

6.6 Pricing

6.6.1 Each Participant must guarantee that the pricing for its Proposal will be

valid for the validity period set out in Section Error! Reference source not found. . All prices must be in New Zealand dollars and exclusive of

GST.

6.6.2 Where a Participant has made any assumption that Inland Revenue or any

third party will incur any set up cost for the proposed Deliverable, or in

relation to the ongoing provision of the Service, the Participant must

clearly state what those activities are and estimate the likely costs of such

activities.

6.7 Additional Information May be Included

Information not specifically requested in the RFP but believed by the Participant

to be of value in evaluating its Proposal should be included as an addendum to

Page 17 of 27 02/05/2012

the Proposal or any other written response to this RFP process. Where there is

reference to published manuals, the relevant extracts only from those manuals

should be placed in the addendum. The addendum must not include any

advertising brochures or similar materials.

6.8 Participants to Inform Themselves

6.8.1 Each Participant will be responsible for ensuring that it has:

a. examined this RFP, any documents referenced by this RFP and any

other information made available by Inland Revenue to it;

b. identified and obtained any additional information it may require to

cost and provide firm pricing for the Services which meets Inland

Revenue's requirements;

c. considered all the risks, contingencies and other circumstances

having an effect on any Proposal; and

d. satisfied itself as to the correctness of any Proposal and of the

costing stated in any Proposal and the sufficiency of the Services

proposed in any Proposal to meet Inland Revenue's Requirements.

6.8.2 If a Participant has any doubts as to the meaning of any part of this RFP it

must immediately communicate that doubt to Inland Revenue‟s designated

contact. If, for any reason, this is not possible, the Participant should,

when submitting its Proposal, set out in a covering notification the

interpretation it has used. Any assumption made in the preparation of a

Proposal must be documented.

6.9 Validity of Inland Revenue Information

6.9.1 While Inland Revenue has used reasonable efforts in compiling this RFP, it

will not be liable to any Participants or any third party for any inaccuracy

or omission in this RFP or any additional information Inland Revenue may

provide during the RFP process.

6.9.2 No assurances or representations are made by Inland Revenue generally,

whether before or after the issue of this RFP or during the RFP process,

and each Participant acknowledges that it has not relied upon any express

or implied statement, representation or warranty as to the truth, accuracy

or completeness of the information contained in this RFP or otherwise

provided by Inland Revenue to the Participant.

6.10 Inland Revenue Information

6.10.1 Except to the extent required by law, Inland Revenue may withhold any

information from any Participant and will not be responsible to any person

for any information. However, Inland Revenue will attempt to provide

information reasonably required by a Participant to assist in the

preparation of its Proposal where this is requested by the Participant.

6.10.2 Inland Revenue may, in its sole discretion, distribute some or all of the

details of any request for further information from a Participant together

with some or all of Inland Revenue's response, but Inland Revenue is

under no obligation to distribute any such details.

6.11 Reliance upon Statements by Participants

6.11.1 Inland Revenue may rely upon all statements made by any Participant in

any part of its Proposal and in subsequent correspondence or negotiations

with Inland Revenue or its representatives.

Page 18 of 27 02/05/2012

6.11.2 Each Participant will notify Inland Revenue of any inaccuracy in relation to

its Proposal (or any additional information provided by the Participant) as

soon as it becomes aware of the inaccuracy.

6.11.3 Upon learning that a Participant's Proposal contains a material inaccuracy,

Inland Revenue may, in its discretion, disengage from negotiations with

the Participant (if relevant). The Participant will be responsible for all

costs and expenses incurred by Inland Revenue in connection with the

inaccuracy.

6.12 Confidentiality

Each Participant will maintain confidentiality at all times, and will not at any time,

directly or indirectly:

a. disclose or permit to be disclosed to any person;

b. use for itself; or

c. use to the detriment of Inland Revenue;

any Confidential Information except:

d. as is already or becomes public knowledge and is obtained from

that public source otherwise than as a result of a breach by the

party disclosing or using that Confidential Information of any

provision of this RFP; or

e. for the purpose of providing a Proposal (and only to the extent

absolutely necessary for that purpose) and, without limiting the

effect of this clause, a Participant may disclose Confidential

Information only to those of its officers, employees, professional

advisers and agents on a "need to know" basis, as is required for

the purpose of providing a Proposal.

6.13 Advertising and Statements

No advertising, press release, public statement or other information relating to

this RFP, any Proposal or any Agreement shall be published in any newspaper,

magazine, journal or other medium without the prior written consent of Inland

Revenue.

6.14 Evaluation Process and Important Factors

6.14.1 Evaluation criteria are provided in section 3.4.1 of this RFP. This

information is provided to ensure the Participant has the best possible

understanding of Inland Revenue‟s Requirements. However, as set out in

section 3.4, the evaluation criteria set out in 3.4.1 are not exhaustive,

may be changed by Inland Revenue, and are not set out in order of

priority or with any indication of relative weighting.

6.14.2 Inland Revenue may cease assessing any Proposal or Participant at any

time during the RFP process.

6.14.3 Information relating to the evaluation and comparison of Proposals is

confidential to Inland Revenue.

6.14.4 To assist in the examination and evaluation of Proposals, Inland Revenue

may, at its discretion, seek further details or clarifications from a

Participant about any aspect of its Proposal. Inland Revenue will not be

obliged to seek the same clarification or additional information from each

Participant.

Page 19 of 27 02/05/2012

6.14.5 Each Participant authorises Inland Revenue to collect any information from

the Participant and relevant third parties (such as referees) and to use

that information in evaluating the relevant Proposal.

6.15 Requirements

The Requirements specified in this RFP reflect those known to Inland Revenue at

the time of releasing this RFP. Inland Revenue reserves the right to vary or add

to the Requirements prior to completion of any Agreement.

6.16 Standard Contractual Provisions

Inland Revenue reserves the right to amend the Standard Contractual Provisions

annexed to this RFP in its sole discretion at any time prior to the contract which

incorporates them being executed by Inland Revenue and the successful

Participant. Such amendments may be substantial.

6.17 Rights Reserved by Inland Revenue

Without limiting any other Rule, Inland Revenue reserves the right to at any

time:

a. apply, or change any criteria relating to participation in this RFP

process or evaluation of Proposals;

b. exclude or include any Participant in this RFP process for any

reason at any time, without notice;

c. restrict or deny the supply of, or access to, any Inland Revenue site

or any other property or any of Inland Revenue's personnel,

information or property to any person;

d. change any Rule for all or any of the Participants;

e. enter negotiations with any Participant at any time and on any

terms and conditions;

f. re-advertise this RFP in whole or in part;

g. provide any assistance, information or equipment (including

software) to any Participant or any other person at any time

without providing this to, or involving or doing the same with any

other Participant (whether before, during or after this RFP process);

h. not accept the lowest price for any Proposal, or enter into any

Agreement, and/or not give any reason for any rejection, failure or

otherwise of any Proposal, or any suspension or cancellation of this

RFP process.

6.18 Satisfactory Proposal

6.18.1 Inland Revenue reserves the right to:

a. select individual components offered in a Proposal (subject to the

Participant's Agreement where the Participant has specifically

indicated in the Proposal that certain components must be taken

collectively);

b. propose the composition of a consortium based on the Proposals

received; and

c. negotiate directly with any consortium member included in the

Proposal.

6.18.2 A Participant must not restrict Inland Revenue's ability to exercise these

rights.

Page 20 of 27 02/05/2012

6.19 Joint Proposals

6.19.1 Joint proposals submitted by more than one Participant may be accepted

provided that:

a. no ROI process preceded the RFP which required qualification of the

Participants by Inland Revenue; or

b. both parties qualified through the ROI process.

6.19.2 Inland Revenue prefers all Participants which are party to a joint Proposal

to indicate their willingness to negotiate independently with Inland

Revenue should Inland Revenue wish to separate the joint Proposal.

6.19.3 For any joint proposals, a primary contact point must be identified as the

single point of contact for all matters relating to this RFP and RFP process,

including, for the avoidance of doubt, the negotiation of all contractual

arrangements if the joint proposal is selected.

6.19.4 Where a joint proposal is submitted, both Participants accept that they are

jointly and severally liable in relation to their joint proposal.

6.20 Inland Revenue to Advise of Outcome

6.20.1 Inland Revenue will advise each Participant of the outcome of its Proposal.

Inland Revenue shall be under no obligation to give any reasons for its

rejection of any Proposal.

6.20.2 During the RFP process, Inland Revenue may, if it decides to proceed with

the completion of the RFP process, select a preferred Participant(s). The

preferred Participant(s) will, if required by Inland Revenue, enter into good

faith negotiations with Inland Revenue in respect of an Agreement for the

provision of the Deliverables described in this RFP.

6.20.3 Notification of selection of any preferred Participant or Proposal will not

give rise to any binding legal obligation between the relevant parties.

6.20.4 Inland Revenue will not be liable (in contract or tort, including negligence

or otherwise) for any direct or indirect costs, damages or losses (including

loss of profits or business) to any Participant or other person in relation to

this RFP or the RFP process.

6.21 Indemnity

If a Participant breaches any Rule, any warranties given under these Rules or

otherwise given in the RFP process, or any other condition of the RFP and, as a

result of that breach, Inland Revenue incurs costs or losses (including, without

limitation, the cost of any investigations, procedural impairment, repetition of all

or part of the RFP process or enforcement of Intellectual Property rights or

confidentiality obligations), then that Participant shall indemnify Inland Revenue

against such costs or losses.

6.22 Warranties

6.22.1 Each Participant warrants that:

a. all information provided by it is complete and accurate in all

material respects, and

b. the provision of information to Inland Revenue, and the copying

and other use of it by Inland Revenue for the evaluation of

Proposals and for the negotiation of any resulting contractual

agreement, will not breach any third party Intellectual Property

rights.

Page 21 of 27 02/05/2012

6.23 Tax Compliance, Criminal and Company Checks

In recognition of the unique requirements of doing business with Inland Revenue,

a Participant or any of its personnel may be required to undergo a tax

compliance, criminal and/or company check. Participation in this RFP process by

a Participant authorises Inland Revenue to undertake a tax compliance, criminal

and/or company check of that Participant or its personnel if desired. This

requirement includes any subcontractors nominated by the Participant in their

Proposal.

6.24 Public Finance Law Restrictions

Each Participant accepts Inland Revenue is restricted by laws controlling Inland

Revenue incurring credit (including prepayments), entering finance leases and in

respect of the giving of guarantees, indemnities and other contingent liabilities.

6.25 No Canvassing

Participants must not attempt to influence the outcome of the RFP Process by

canvassing, lobbying or otherwise directly or indirectly seeking support of Inland

Revenue personnel.

6.26 Ethics

Each Participant represents and warrants that it has not and will not engage in

any practices that give one Participant an improper advantage over another,

and/or engage in any unfair and unethical practices, including, in particular, any

collusion, secret commissions or such other improper practices.

6.27 Governing Law

This RFP will be construed according to and governed by New Zealand law and

each Participant agrees to submit to the non-exclusive jurisdiction of New

Zealand courts in any dispute concerning this RFP process or any Proposal.

6.28 Definitions and Interpretation

6.28.1 The following definitions apply to this document:

Agreement means any contract or contracts to be signed by any successful

Participant and Inland Revenue.

Confidential Information means any information (regardless of the form of

disclosure or medium of storage):

contained in or relating to this RFP or the RFP process;

relating to Inland Revenue and/or its business, operations, Participants,

taxpayers, systems and/or personnel;

disclosed by Inland Revenue in relation to this RFP process; or

relating to Inland Revenue which, due to its nature, might reasonably be

expected by any party to be kept confidential.

Deliverables mean the Goods and Services specified in the Requirements.

Goods means all tangible products, equipment, parts and other items being

proposed for supply to Inland Revenue.

Inland Revenue means Her Majesty the Queen in Right of New Zealand acting

by and through the Commissioner of Inland Revenue or his or her duly authorised

delegate.

Intellectual Property means patents, registered designs, trade marks

(including logos, get up and trade dress), domain names, copyright, personality

rights, know-how and trade secrets, confidential information and all other

Page 22 of 27 02/05/2012

intellectual property, in each case whether registered or unregistered (including

applications for the grant of any of the foregoing) and all rights or forms of

protection having equivalent or similar effect to any of the foregoing which may

subsist anywhere in the world.

Participant means any person or company participating in this RFP process.

Proposal means the quotation/proposal developed and submitted by a

Participant in response to this RFP including any other written response or

information provided by that Participant during the RFP process.

Requirements are the requirements of Inland Revenue, as detailed in this RFP

document.

RFP means this document and all of its schedules, appendices and attachments.

RFP process means the end to end process described in this RFP by which

Inland Revenue may, or may not, select a supplier or suppliers.

Rules means the rules set out in this section 6.

Services means all Services in scope, or being proposed, for supply to Inland

Revenue.

6.28.2 Headings in this RFP are inserted for convenience only and shall be

ignored in construing this RFP.

6.28.3 Except to the extent that the context otherwise requires, any reference in

this RFP to a "person" includes an individual, company, corporation, local

authority, an association of persons whether corporate or not, a trust or a

state or agency of a state whether of central government or local

government (in each case, whether or not having separate legal

personality).

6.28.4 Except to the extent that the context otherwise requires, in this RFP:

a. words denoting the singular number also include the plural and vice

versa and words denoting any gender include all genders; and

b. an example or an inclusion does not limit what else may be

included.

Page 23 of 27 02/05/2012

APPENDIX 1: Cover Letter – provided as a separate

document

Page 24 of 27 02/05/2012

APPENDIX 2: Detailed Requirements - provided as a

separate document

Page 25 of 27 02/05/2012

APPENDIX 3: IR’s Standard Terms and Conditions

- provided as a separate document

Page 26 of 27 02/05/2012

APPENDIX 4: IR820 - provided as a separate

document

Page 27 of 27 02/05/2012

APPENDIX 5: IR822 - provided as a separate

document