ira seminars open forthe is registrationc.ymcdn.com/.../august_newsletter_2015.pdf · 2015-16event....

TRANSCRIPT

Wyoming Bankers Assodatlon2015-16 Event.

Mark Your Calendar!

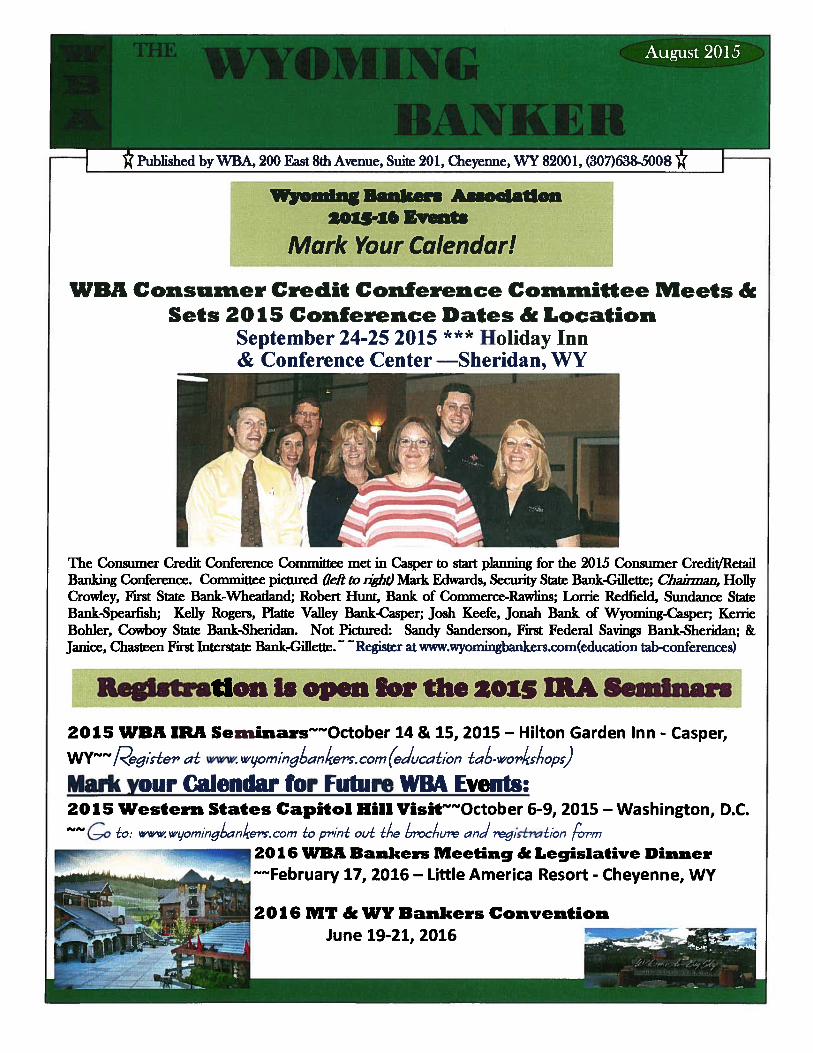

WBA Consumer Credit Conference Committee Meets &Sets 2015 Conference Dates & Location

September 24-25 2015 *** Holiday Inn& Conference Center —Sheridan,_WY

The Consumer Credit Conference Committee met in Casper to start planning for the 2015 Consumer Credit/RetailBanking Conference. Committee pictured (left to iight) Mark Edwards, Security State Bank-Gillette; Chain’nan, HollyCrowley, First State Bank-Wheatland; Robert Hunt, Bank of Commerce-Rawlins; Lorrie Redfield, Sundance StateBank-Spearfish; Kelly Rogers, Platte Valley Bank-Casper; Josh Keefe, Jonah Bank of Wyoming-Casper; KerrieBohier, Cowboy Slate Bank-Sheridan. Not Pictured: Sandy Sanderson, First Fedemi Savings Bank-Sheridan; &Janice, Chasteen First Interstate Bank-Gifiette. - Register at www.wyomingbankers.com(education tab-conferences)

Registration is open for the 2015 IRA Seminars

2015 WBA IRA SeminarsOctober 14 & 15, 2015 — Hilton Garden Inn - Casper,

WY’’Reqicter at www wyorninq/anherc. corn (education taL4-worIchopc)Mark your Calendar for Future WBA Events:2015 Western States Capitol Hill Visit”October 6-9, 2015 — Washington, D.C.

I )( Published byWBA, 200 East 8th Avenue, Suite 201, Cheyenne, WY 82001, (307)638-5008 )

to: www wjoming/,anherc. corn to pr/nt out titie !,roc/,ure and regictration form

2016 WBA Bankers Meeting & Legislative Dinner‘‘February 17, 2016 — Little America Resort - Cheyenne, WY

2016 MT & WY Bankers ConventionJune 19-21, 2016

WBA President, William Iluppert piesents the WB/i PAC check to the ABA President John Ikard.

Bankers attend the 2015 FDIC community Bankers Workshop in Cheyenne on July 7’s.

NBAWNebraska Bankers Association

News Briefs From Washington

Compliance Officers Say Growing BegBurden Limits Products, Services

Growing regulatory compliance burdens have lednearly half of banks to reduce their offerings offinancial products and services, according to ABA’sbiannual Survey of Bank Chief Compliance Officers.A combined 46.3 percent said their banks had cutofferings for loan accounts, deposit accounts, both,or for other services—up slightly from 2011 and2013 and up substantially from the 21.9 percent whoreported exiting a product line or channel due toregulatory burdens in 2009. Just over 55 percent saycompliance budgets have risen since 2013, mostlydue to hiring more staff and handling a growingregulatory burden. View the survey results atwww.aba.com/Comp1iance/Mem/Documents/2O15BCOSurvev.pdf

ABA Seeks Input on Departmentof labor Overtime Proposal

ABA is seeking banker input on how the Departmentof Labor’s controversial overtime proposal wouldimpact their banks. The proposal would more thandouble the current salary necessary for employees tobe exempt from overtime andwill affect most banks in thecountry. Informationprovided will be sharedanonymously in ABA’scomment letter on the rule.

In particular, ABA seeks informationabout the number of currently exempt employeeswho do not earn $50,544 annually, their length oftime being exempt and their percentage of theworkforce; projected costs of overtime; moraleproblems; and the effects of losing flexibility.Contact Cris Naser at the ABA at [email protected].

Read ABA’s staff analysis at www.aba.com/Tools/Ebulletins/Mem/Docurnents/2015-DOL-Proyosal-Staff-Analvsis.pdf.

First De Novo Since 2013 OfficiallyOpens in New Hampshire

With final authorization from the New HampshireDepartment of Banking this week, Primary Bank inBedford, N.H., became the newest U.S. bank to openfor business. The bank startup is the first since theBank of Bird-in-Hand, Bird-in-Hand, Pa., waschartered in 2013, and only the second de novocharter since 2010.

ACCESSbank of Omaha was the last bank charteredin Nebraska; it was established in December 2007.

GAO: Federal Agencies Must ssessEffects of QM and QRM Regulations

In planning for review of the qualified mortgage(QM) and qualified residential mortgage (QRM)regulations, the agencies responsible for theregulations have not included elements importantfor conducting retrospective reviews necessary tobetter understand the effects of these regulations andidentify unintended consequences, according to astudy by the U.S. Government Accountability Office(GAO). Existing data lack important information for

performing these reviews, such as loanperformance and borrower debt to income. TheConsumer Financial Protection Bureau (CFPB)proposed expanding Home Mortgage DisclosureAct (HMDA) data reporting requirements toextract the extra data, but enhanced data wouldnot be available before 2017.

The GAO recommends that the CFPB, HUD, andthe six agencies responsible for the QRM regulationsshould complete plans to review these regulationsincluding identifying specific metrics, baselines, andanalytical methods.

Read the GAO report at www.gao.gov/products/GAO-15-185.

News Source: American Bankers Association

2 NBA Update • www.nebankers.org • 7-29-2015 onna.y Setuke [ori oranay Mcm6cii

News Briefs From Washington

New Exam Procedures on TRIP

The FDIC has issued revised interagency examprocedures for the TILA-RESPA integrateddisclosures (TRID) rule now to take effect onOct. 3. The procedures include updates related tothe CFPB’s ability-to-repay, servicing, and high-priced mortgage loan rules. Read more athttp://bit. lv/RegZ-X.

Cybersecurity Self-Assessment Tool

The FFIEC has released a free cybersecurity self-assessment tool to help banks of all sizes identifycyber risks and assess their preparedness. Theassessment will become part of cybersecurityexams this year. The FFIEC said it will update theassessment as the cyber risk environment evolvesand will solicit public comments on theassessment. Access the assessment tool atwww.ffiec.gov/cyberassessmenttool.htm.

P01 Proposal Would Raise Salary Thresholdfor Non-Exempt Workers

The Department of Labor has released a proposalrevising the requirements for employees to be exemptfrom overtime pay under the Fair Labor Standards Act(FLSA). The proposal would more than double the salarybasis test—the level below which all employees must bepaid overtime beyond 40 hours per week, regardless oftheir duties—from the current level of $455 per week (or$23,660 per year) to $921 per week (or $47,892 per year).The proposal also would increase the total annualcompensation requirement for highly compensatedemployees to $122,148 and establish a mechanism forautomatically updating the salary and compensationlevels going forward. DoL did not propose changes to theduties tests under FLSA, but it did request comment onwhether the tests should be changed. Comments are due60 days after publication in the Federal Register. To helpbankers understand the proposal, ABA will host anonline briefing on July 30 at 2 p.m. EDT. Read more atwww.dol.gov/whd/overtime/NPRM2O15/factsheet.htm.

News Source: American Bankers Association

WBA WELCOMES NEW ASSOCIATE MEMBER

Byaii BrOoks Appraisal Services, Inc. -www.bryanbrooks.net

Bryan Brooks & Associates specializes in aggregate, asphalt, mining and construction equipment. We bring

together over 50 years combined experience in the construction industry.

CONTACT:

Scott ForkeSenior Appraiser1916 South Coffman StreetLongmont, CO 80504Phone: 720-684-9678Email: [email protected]

rowley Fleck PLLP -www.crowleyfleck.com

Crowley Fleck PLLP is one of the oldest and largest firms in our region. The firm counts over 150 lawyerspracticing in the areas of commercial litigation, insurance defense litigation, natural resources, mining, andenergy law, healthcare, commercial transactions, banking and finance, creditors rights, real estatetransactions and development, tax and estate planning and administration, intellectual property matters,employment law, governmental affairs and lobbying. The firm has offices throughout Montana, NorthDakota, and Wyoming, including offices in Billings, Bozeman, Butte, Helena, Kalispell, and Missoula,Montana; Bismarck and Williston, North Dakota; and Casper, Cheyenne, and Sheridan, Wyoming.

CONTACT:

James Beicher152 North Durbin St., Ste. 220Casper, WY 82601Phone: 307-265-2279Email: [email protected]

CROWLEY FLEC KPLLPA T T 0 R N F Y S

Ditech Lendfrig—wwwcorrespondent.ditech.com

Look to bolster your business by leveraging the power •of the ditech brand and our team of experiencedmortgage professionals. Together, we can save you time and money. Here’s how:

• Best-in-class training on ditech products and processes for your staff, including live webinars, self-paced courses and personalized training

• Consistent support, quality service and knowledgeable answers from your dedicated client managerand a team of ditech experienced professionals

• A wide spectrum of products that include conforming, Jumbo, FHA and VA loans• A full suite of delivery options that include rate sheet forwards, live trades, AOT and bulk MSR

acquisitions• A commitment to working only with top-rated mortgage servicers

t ditech

CONTACT:

Brent NicholsSales Director1100 Virginia DriveFort Washington, PA 19034Phone: 801-615-6291Email: [email protected]

Every Bank NeedsSegregation of Duties

Without segregation of duties, the consequences can be disastrous for both banks and customers. For example, at a certainbank, a trust officer controlled every aspect of his elderly clients’ banking needs. But one day, when he was on vacation, acustomer came in to sell a U.S. Treasury note so he could lend $50,000 to his son.

The bank personnel told the customer he did not have anything in safekeeping. Flabbergasted, the customer produced hissafekeeping receipts of $300,000. As the bank investigated the matter, it discovered that the trust officer had been issuingsafekeeping receipts but never recorded their existence in the bank. The trust officer also stole customers’ funds instead ofpurchasing investments. Going on for eight years, the embezzlement total was over $1 .5 million.

THIS IS ARTICLE 3 OF 1FRAUD IN THE WORKPLACE SERIES

STAY TUNED FOR MORE

Segregation of duties is simple butvital in the banking world. In short, segregation of duties means setting up a process so asingle transaction is neverfully controlled by one employee —there are always two or more employees involved. While this issimple in concept, the actual maintenance and execution can be extremely difficult.

In a well-run bank, all employees and managers think regularly about separation of responsibilities. At a minimum, theresponsibilities of authorizing transactions, having custody of cash or other assets, and the reconciliation functions should allbe separate — or at least rotated.

Banks hold the public’s money and are, therefore, in an important position of trust. To earn and deserve that trust, banks haveto ensure they use and update all procedures to keep money secure with the changing times.

Let’s say the cashier’s check account needs to be balanced. Rather than having one person assig ned to that duty, banks shouldhave two or three people responsible for it. Each employee would balance the account for one month and then rotate to adifferent duty.This would ensure that one person didn’t have complete control of the cashier’s check account balancing.

A teller introduces a trickier situation because a single person does a customer’s entire transaction electronically. There’s nobookkeeping function to separate thatjob, but there are still controls that can be put into place to achieve segregation.

Banks must have someone to consider which employees are in control of which tasks and analyze when processes goout-of-date. Otherwise, the bank will not only destroy its credibility, but also negatively affect the public’s money.

luckily, these problems are easily preventable with the implementation of segregation of duties. With a reliable system, bankscan retain the public’s trust and have complete confidence that each task is being carried out with integrity.

Gain access to enhanced KBS content:Subscribe at http://tinyurl.com/kbssubscribe

Connect with us on social media:twitter.com/kbsforbanks linkedin.com/company!kbsforbanks

Call KBS (785) 228- 0000 to discuss thisarticle and other loss prevention topics orproducts to help protect your bottom line.

•

HUNTON&WILLIAMS

DOJ Reiterates Cooperation toObtain Full Credit and Avoid Penalties

by Peter Weinstock, John Delionado, and Abigail Lyle’

For the second time in recent weeks, the head of the Department of Justice’s criminaldivision has reiterated the government’s expectation that companies fully cooperate duringcriminal investigations if they hope to obtain full credit and avoid penalties. First, duringremarks to NYU Law School in April, and then again in May during the New York City Bar’sfourth annual White Collar Crime Institute, Assistant Attorney General Leslie Caidwell offered atelling description of what “cooperation” means to the Department of Justice.

Against the backdrop of recent investigations of systemically important financialinstitutions overseas that resulted in historic penalties and were offered as examples of “noncooperation,” Ms. Caidwell explained that, to obtain full credit for cooperation, companies mustconduct thorough internal investigations, identify culpable individuals, and turnover evidence ofwrongdoing to prosecutors in a timely and complete manner. Ms. Caldwell conceded that whilethere is no one-size-fits-all investigation, each company must tailor its investigation to thealleged misconduct at issue.

From her remarks we can glean that conducting an internal investigation is no longer acheck-the-box activity for companies hoping to obtain credit and avoid penalties. Instead,regardless ofwhether the company ultimately decides to fight the allegations or resolve thematter with the Department of Justice, the Department of Justice expects a robust internalinvestigation if the company hopes to separate itself from the alleged individual frauds.

Peter Weinstock, John Delionado, and Abigail Lyle are members of the Consumer Financial Complianceand Litigation practice group at Hunton & Williams LLP, and regularly represent businesses and individualsinvestigated by the government in criminal and civil matters. This article presents the views ofMr. Weinstock, Mr.Delionado, and Ms. Lyle and do not necessarily reflect those ofHunton & Williams or its clients. The informationpresented isfor general information and education purposes. No legal advice is intended to be conveyed; readersshould consult with legal counsel with respect to any legal advice they require related to the subject matter of thearticle. Mr. Weinstock, Mr. Delionado, and Ms. Lyle may be reached at (214) 468-3395, (305) 536-2752, (214)979-8219, pweinstock(ahunton. co, /delionado(ëihunton. corn, or alyleCa)hunton. corn.

1

Accordingly, in conducting an internal investigation, companies must keep the followingin mind:

• Voluntary disclosure ofmisconduct is not enough. The Department of Justiceexpects companies to take the additional step by actually identifying theresponsible individuals to avoid liability for the company. In fact, Ms. Caldwellindicated that chief among the “hallmarks of all good internal investigations,” isidentification of wrongdoers.

• Investigations must be independent. This means, that the goal of the investigationmust be to uncover the truth, not circle the wagons. Ms. Caldwell indicated thatin weighing the company’s “cooperation,” prosecutors will test the results of theirinvestigation against the fmdings of the company to determine whether theinternal investigation was adequate.

• Appropriately tailor the scope of the investigation. Ms. Caidwell explained thatthe length or cost of the internal investigation does not equate to evidence ofcooperation. In fact, she cautioned that overly-lengthy internal investigations canactually have the opposite effect by delaying the Department of Justice’sinvestigation. With respect to scope, if, for example, a company discovered anFCPA issue in just one country, with no basis to suspect violations occurredelsewhere, Ms. Caldwell explained that she would not, expect the investigation toexpand beyond that country. In contrast, however, if the individuals involved inthe misconduct operated in other countries, then she would expect a broaderinvestigation.

• Focus the investigation on the Department ofJustice areas of interest. Ms.Caldwell encouraged an open dialogue between companies and prosecutors sothat prosecutors can identify the areas of interest. Cooperating companies canthen use that information to appropriately tailor their internal investigation.

From the recent examples cited by Ms. Caldwell in her remarks, failing to conduct aninvestigation that meets the Department of Justice’s expectations not only eliminates theopportunity for the company to obtain credit, but may result in the imposition of sizeablesanctions against the companies themselves, not just the individual wrongdoers. For example,the DOJ’s recent investigation of a financial institution based overseas resulted in a multibilliondollar forfeiture, over $100 million in fines, and five years ofprobation for what the Departmentof Justice viewed as “intransigence” by hindering the Department of Justice’s investigation ofthe individual wrongdoers.

Although Ms. Caldwell’s remarks appear not to take us all the way back to the days of the 2003“Thompson Memorandum” — which resulted in the consistent pressuring of companies to waiveattorney-client privileges and work-product protections over the results of their internalinvestigations in order to demonstrate cooperation with the government’s investigation — herremarks show that the Department of Justice will be aggressively evaluating the quality of theclaimed cooperation and its utility to furthering the Department of Justice’s investigation. The

2

Department of Justice has made clear that the need for robust internal programs to not onlyidentify potential misconduct, but also respond through carefully targeted investigations thatidentify the wrongdoers cannot be over-emphasized. As companies wade through these issues,where cooperation and candidness with prosecutors is demanded by the government, companiesmust be sure these expectations are communicated to employees and that it retains experiencedadvisers to achieve the desired result.

3

Kansas Ci -.

Kansas City Convention Center

Uncertain times are inevitable. The challenge isdeveloping the agility to position yourself for growthand profitability—no matter what the economic climatemay be.

Join ABA and agricultural bankers from across theU.S. this October as we shed light on the opportunitiesrooted in developing real strategies to manage risk,work smarter and strengthen customer relationshipsthat will prepare you for a successful—andsustainable—transition from a predictable businessclimate to one with new challenges.

Register today.

a ba.com/AgConference2Ol 5

140years

American Bankers Association

)

6

Rent or Buy: 5 Questions Consumers Should Ask Themselves

WASHINGTON — During American Housing Month in June, the AmericanBankers Association Foundation is reminding consumers that their local bankercan help navigate challenges associated with choosing a home, includingdeciding what is affordable and whether to rent or buy.

“Housing markets vary across the country. Your local banker can help younavigate housing options in your community and provide direction based on yourindividual financial situation and long-term financial goals,” said Frank Keating,ABA president and CEO.

“Bankers are well-suited to talk to their customers about their housing options,”said Corey Carlisle, senior vice president, ABA’s Bank Community EngagementFoundation. “Bankers finance everything from single-family homes to apartmentbuildings giving them valuable perspective for customers searching for a newhome.”

Before pursuing a rental or homeownership opportunity, consumer shouldconsider the following questions:

How much money do you have saved up?Start with an evaluation of your financial health. Figure out how muchmoney you have for a down payment or deposit on a rental. Downpayments are typically 5 to 20 percent of the price of the home. Securitydeposits on rentals are usually about one month of rent and more if youhave a pet. But be sure to keep enough in savings for an emergency fund.It’s a good idea to have three to six months of living expenses to coverunexpected costs.

How much debt do you have?Consider all of your current and expected financial obligations like your carpayment and insurance, credit card debt and student loans. Make sureyou will be able to make all the payments in addition to the cost of yournew home. Aim to keep total rent or mortgage payments plus utilities toless than 25 to 30 percent of your gross monthly income. Recentregulatory changes limit debt to income (DTI) ratio on most mortgageloans to 43 percent.

• What is your credit score?A high credit score indicates strong creditworthiness. Both renters andhomebuyers can expect to have their credit history examined. A low creditscore can keep you from qualifying for the rental you want or a low interestrate on your mortgage loan, If your credit score is low, you may want totake steps to raise your score, which could improve the terms you’reoffered, before entering a loan or rental agreement. For tips on improving

your credit score, visit aba.com/consumers.

Have you factored in all the costs?Create a hypothetical budget for your new home. Find the average cost ofutilities in your area, factor in gas, electricity, water and cable. Find out ifyou will have to pay for parking or trash pickup. Consider the cost of yardmaintenance and other basic maintenance costs like replacing the air filterevery three months. If you are planning to buy a home, factor in realestate taxes, mortgage insurance and possibly a home owner associationfee. Renters should consider the cost of rental insurance.

How long will you stay?Generally, the longer you plan to live someplace, the more it makes senseto buy. Over time, you can build equity in your home. On the other hand,renters have greater flexibility to move and fewer maintenance costs.Carefully consider your current life and work situation and think about howlong you want to stay in your new home.

ABA’s Foundation is also providing resources to help bankers across the countryengage with their communities. For more information, visit aba.com/housinc.

The American Bankers Association represents banks of all sizes and chartersand is the voice for the nation’s $14 trillion banking industry and its two millionemployees. The majority of ABA’s members are banks with less than $185million in assets. Learn more at aba.com.

Through its leadership, partnerships, and national programs, ABA’s CommunityEngagement Foundation, a 501(c)3, helps bankers provide financial education toindividuals at every age, elevate issues around affordable housing andcommunity development, and achieve corporate social responsibility objectivesto improve the well-being of their customers and their communities.

###

ACTIONS YOU CAN TAKE TOHELP PREVENT FRAUD

The 2013 Marpuet Report On Embezzlement, issued

in December 2014, analyzes US fraud and

embezzlement cases resulting in losses of $100K or

more. Listed below from the report are specific

preventive strategies and tactics to address the

problem of employee theft; the complete Marquet

Report can be accessed here:

http://www.marguetinternational.com/reports.htm

(site registration required).

• Do not allow a single individual access to all aspects

of company finances and accounting. Make sure

there is a division of duties between the financial

operations (especially check processing) and the

accounting for financial activities

• Regularly rotate responsibilities for accounting

personnel.

• Require accounting and financial personnel to take

time off and vacations. Embezzlers often take little

or no vacations to perpetrate their schemes.

• Do not allow those responsible for cutting checks to

take work home.

• Require two signatories on outgoing checks above a

certain nominal amount. One of these signatories

should be from outside the finance and accounting

functions. Segregate the reconciliation of all

checking accounts from check processing, check

authorization and check signing functions. Examine

cancelled checks regularly during reconciliation and

have the reconciliation process spot checked by the

outside auditors. One common method of

embezzlement involves the forgery of checks.

Another is to have them payable to the embezzler or

their personal vendors.

• Maintain unused checks in a lockbox. Be sure all

checks, purchase orders and invoices are numbered

consecutively and reconcile any of those missing.

• Conduct regular as well as random audits. Owners

should take a hands-on management approach by

physically spending time with the bookkeeping

department.

I BAJCBEIRVEL. Insurance Agency

• Audit petty cash regularly.

• Audit company credit card charges regularly.

• Audit expense reports regularly.

• Be sure each payment, electronic or otherwise, is

backed up with appropriate documentation.

• Backup financial records daily.

• Make and reconcile daily deposits. Use a “for deposit

only” stamp for check deposits. The person

recording cash receipts should be different from the

one making the actual deposits.

• Bank reconciliations should be made by a different

person than those that handle cash receipts and

cash disbursements.

• Know who your vendors are. Embezzlers often

create phony vendors and submit fraudulent

invoices for payment.

• Examine payroll records regularly. Some embezzlers

issue themselves extra paychecks and bonuses

through the payroll system.

• Investigate customer and vendor complaints

promptly. If vendors are not being paid as expected,

it may be a sign that the payment checks are being

diverted.

• Conduct pre-employment background checks for all

personnel with fiduciary duties.

• Conduct employee background checks on current

employees on a periodic basis, particularly those in

financial positions.

• Both the HR and legal departments should pay close

attention to the employee grapevine and any

suggestions that someone has a gambling problem

should be immediately addressed.

• Prosecute perpetrators, creating a permanent record

future employers can find.

(Reprinted with permission. Berkley FinSecure, a W.R.Berkley Company. Copyright 2014 MarquetInternational, LTD.)

Call or email Tempi Ruth at (800)541-5126 orternpi@bancserve. Corn for more information

Insuring banks for 25 years.Go with experience & expertise

Financial Institution Bond, Director & Officer Liability, Cyber Liability, Bank CardProtector, Property, Auto, Workers Compensation, Lenders Single Interest,

Mortgage E&O, Foreclosed/Force Placed Property & Flood Coverage.

The Marquet Report on EmbezzlementBerkley FinSecure recently reviewed valuable reports that help provide you with a closer look at the who, what, when, where andcost of fraud. Part Two of this two-part series summarizes some of the highlights of the Marguet Report on Embezzlement whichclosely examines domestic fraud cases. Providing valuable insights into the motivations and sources of fraud and embezzlement, thereport also outlines a number of measures to help mitigate losses.

The recently released report by Marquet International analyzes US fraud and embezzlement cases that resulted in losses of $100K ormore in 2013. There were 554 such cases in 2013, a new (unfortunate) record. As they say, This figure represents a rate of morethan 10 Y2 cases per week - a staggering amount.”

The report continues, “We believe that our data shows that poor economies and economic downturns are drivers for potentialembezzlers. However, this is not the only factor. Indeed, our data suggests that the primary motivating factor for perpetrators oflong-term embezzlements is not because the money is needed for dire financial circumstances, but rather to obtain and maintain alifestyle beyond what they would otherwise be able to attain.”

Some of the more interesting statistics taken from The 2013 Marguet Report on Embezzlement include:• The average loss for 2013 was about $1.1 million; the median loss was $325,000 and the average scheme lasted 4.6 years;• More than 2/3 of the incidents (71%) were committed by employees who held finance/bookkeeping & accounting

positions;• The most common embezzlement scheme involved the issuance of forged or unauthorized company checks;• The financial services industry suffered the greatest number and the greatest losses due to major embezzlements;• Credit Unions continue to be a major target/victim of large embezzlement schemes;• Government entities were the second most frequent victim after Financial entities, followed by the combined group of

Non-profits and religious organizations

The Marquet Report concludes with a number of specific measures to help minimize fraud and embezzlement losses as part of acomprehensive organizational control and governance strategy. See newsletter insert for actions you can take to help prevent fraud.Also, the complete Marquet Report can be accessed at: http://www.marguetinternational.com/reports.htm (site registrationrequired).

(Reprinted with permission. Berkley FinSecure, a W.R. Berkley Company. Copyright 1D2014 Marquet International, LTD.)

Call or email Tempi Ruth at (800,)541-5126 or tempibancsene.corn for more information

Insuring banks for 25 years.••I••• Go with experience & expertise

a.ricsE R • Financial Institution Bond, Director & QffIcer Liability, Cvber Liability.Bank Card Protector, Property. Auto, Workers Compensation, LendersJn!urnc gencv

_____________________________________

Single Interest, Mortgage E&O, Foreclosed/Force Placed Property &Flood Coverage.

ABA Survey: Regulatory Burden Limiting Bank Products and Services

WASHINGTON — Growing regulatory compliance burdens have led nearly halfof all banks to reduce their offerings of financial products and services, accordingto the American Bankers Association’s 2015 Survey of Bank ComplianceOfficers. A combined 46.3 percent of respondents said their bank had cutofferings for loan accounts, deposit accounts, or other services because ofregulatory effects.

Additionally, 46 percent of bank Have compliance regulatory burdenscompliance officers reported caused your institution to reducetheir institution had decided not consumer financial products or services?to launch a product, open anew channel, or had held off onentering a new market

—temporarily or permanently—

due to compliance concerns, depositaccounts

“It’s clear that the compliance16.9%

burden brought on by Dodd-537%

Frank has had an impact notonly on banks, but more Yes, forimportantly on the customers loan

accountsand communities they serve, onlysaid Frank Keating, ABA 22.7%

president and CEO. “Thisregulatory overcorrection haslimited the loans, products andservices available toconsumers.”

Further evidence of regulations’ effect on customers can be seen in the one-third(33.8 percent) of banks that turned down otherwise creditworthy mortgageborrowers in an effort to comply with the Ability-to-Repay Rule. The rule’s impactwas felt most by banks with between $1 and $10 billion in assets. Approximatelyone-third (33.2 percent) of banks now make exclusively Qualified Mortgageloans.

The survey also reviewed trends in banks’ risk assessment processes. More than75 percent (76.6) of respondents perform enterprise-wide risk assessments, amajority of which are done annually. Results showed that as bank asset sizeincreases, so does the percentage of institutions performing enterprise-wide riskassessments.

In other findings, an increasing number of banks are relying on social mediamonitoring as a portion of their consumer complaint management process. Just

Yes, forotherI 0.7%

Yes, for depositaccounts oniy

3.4%

over 50 percent (51.3) of respondents use social media or other internet sites asa way to review comments about their bank — an increase from the 42.2 percentthat did so in 2013.

About the surveyThe web-based, biennial survey was conducted from February through March2015 to collect information about compliance officers and the compliancefunction practices at their bank. Over 450 financial institutions —78.5 percent ofwhich reported to be community banks -- participated in the 70-question survey.

The American Bankers Association is the voice of the nation’s $16 trillion bankingindustry, which is composed of small, regional and large banks that togetheremploy more than 2 million people, safeguard $12 trillion in deposits and extendmore than $8 trillion in loans. Learn more at aba.com.

###

What do you need to know about the EFIECCybersecurity Assessment Tool?

Written by:Jon Waidman — Partner, Secure Banking Solutions, LLCSecure Banking Solutions, LLC

As promised in their 2014 Cybersecurity Observations publication, the FFIEC has released new guidancein the form of a Cybersecurity Assessment Tool. As one would expect, it has a heavy focus on CEO andBoard level involvement, as well as tying controls to other FFIEC and NIST resources in order to assemblea set of expectations for financial institutions based on their size and complexity.

However, this new assessment tool not only provides financial institutions a method to evaluate thematurity of their Information Security Program to address cyber threats, but it also gives examiners amethod to create a risk-based cyber examination process. If you think about the old FFIEC handbooks,which don’t really delineate between institutions of different size and complexities... that’s exactly whatthe FFIEC appears to be doing here on the cybersecurity side of the information security world.Interestingly enough, this new tool is also very prescriptive in that inherent risk and maturityexpectations are outlined in specific detail, which is another (welcome) change from traditionalguidance. It’s essentially giving institutions examination procedures that they can use to point to exactlywhere they are in the realm of cybersecurity, as well as exactly where institutions need to be regardingthe implementation of controls. For those who have completed the FDIC IT Officers questionnaire in thepast, this tool resembles that process very closely with two significant differences: the FDIC Officer’sQuestionnaire has a signature line for accountability but does not have a risk-based scoping process tovary expectations on institutions based on size and complexity.

Another significant question that needs to be addressed is how this new assessment affects whatinstitutions are currently doing regarding a documented Information Security Program. Please be sure tounderstand — this new Cybersecurity Assessment Tool is not a replacement for any current riskmanagement process; it’s an addition to current Information Security Program processes that ensuresfinancial institutions have adequate controls in place to mitigate the risk of cyber-specific threats. Thisdoesn’t replace anything from a standard or traditional ISP, including an asset-based IT Risk Assessment.It’s a different vantage point that should allow Senior Management and the Board of Directors to betterunderstand the institution’s maturity when it comes to preparing for and mitigating risk around theincreasing cybersecurity attacks that are affecting networks and organizations on a much more regularbasis.

So, what are the big takeaways for those that need to understand this new tool at your own financialinstitutions? First, the assessment tool identifies and creates a baseline of (inherent) cybersecurity riskfor the institution. It then compares the current maturity level of the intuition against risk-basedexpectations and identifies gaps in the cybersecurity controls needed to meet the maturity expectations.If the institution does not meet the identified cybersecurity maturity levels, then the assessmentsuggests improvements to existing risk management and information security program components.

The FDIC has also released this FFIEC Cybersecurity Assessment Tool as FIL-28-2015 and states that theuse of this new tool is “voluntary;’thowever, we have seen many times in the past that voluntaryprocesses or items-not-mandated are still used in examination processes. Technically, all of the FFIEC ITBooklets are voluntary resources. It’s important that each financial institutions quickly get familiar withthis new Cybersecurity Awareness Tool and understand where their institution stands in terms ofinherent risk and cybersecurity maturity. Once you understand your inherent risk and maturity levels,your next step is to develop a list of next-steps to improve gaps in the cybersecurity maturity n-iodelidentified by the FFIEC. Examiners will likely not expect full compliance with these identifiedcybersecurity controls tomorrow, but there will certainly be an expectation that institutions startleveraging this resource and making steps toward the identified goals.

SBS is quickly working to automate this manual assessment tool into a freely available resource thatfinancial institutions can use to quickly and easily perform their own Cybersecurity Assessment. If you’reinterested in pre-registering for this free web-based application, please visit our website here:https://www.protectmybank.com/register/

For more information about the FFIEC Cybersecurity Assessment Tool, you can find links to theresources and a copy of the tool at www.protectmybank.com. SBS will continue to provide additionalarticles and updates on educational opportunities on our website, so stay tuned... we aim to keep youup-to-date on everything Cybersecurity Assessment related!

7 his newsletter is an instrument of

the Enterpi icing Rural Families

Making It l/Vori< program of

iirsvers!tv of Vyoming Es tension.

ror further information concernina

the Eiiterpr s/nq Rural Families

program or on-line course contact

ThformationeRuraiFamiIies.org or

go to http://eRuralFamiIies.org/

Tip of the Month

Tools for determining and about the community and can ac- • Asset Mapping — Identifyingmeasuring community needs. curately identify priority needs and resources or things of value

concerns. (assets) in the community. It is aninventory of the businesses, or-

• Existing Data — Using existing • Community Forum — Public ganizations, and resources thatstatistical data to obtain insights meeting(s) held for community help create a community.about the well-being of people. members to discuss issues facing

the community, prioritizing needs, • Observation — Systematically• Attitude Survey — Information and how to address the needs. selecting, watching, and recordingis gathered from a representative behavior of living beings, objects,sample of community residents • Focus Group Interview— A or phenomena. Participant obserabout issues related to their well- group of people selected for their vation (taking part in the situationbeing. experience, views, or position are he/she observes) and non-

asked a series of questions about participant observation (watching• Key Informants — Identifying a topic or issue to gather their the situation—openly or con-community leaders and decision opinions. cealed—but not participating).makers who are knowledgeable

Enterprising Rural FamiliesTM

6

An Online Newsletter Volume XI, Issue 7 July 2015

Cultivating Ethical Leadership in the WorkplaceBy Hannah Swanbom, Community Development Area Educator,University of Wyoming Extension

Cultivating ethical leaders in our work place can be a difficult task to accomplish for a multi

tude of reasons. One of those reasons being everyone has a different definition and idea of

what the terms ethical and leadership look like in action. In order to understand and culti

vate our co-workers, employees, and employers to act as ethical leaders it is imperative to

have a general understanding of both terms. According to the Webster’s Dictionary the defi

nition of leadership is: “a position or function of a leader of a group, organization...”. Web

ster’s definition for ethics is: “rules of behavior based on ideas about what is

morally good and bad.” “Ethical behavior, in its simplest terms, is knowing and

doing what is right. The difficulty is in defining what is right” (Rabinowitz, 2014).

The term ethical leadership can create confusion and disagreements. In this

article we will attempt to construct a definition of what ethical leadership is and

how to implement it into your working situation.

Lthic. i<.nowlng tIlC dIflcrcncckciwccn what: 1)OLI kavc a right to

d0 and what i right to d0.- rotlcr)tcwart

“Ethics refers to the desirable and appropriate values and morals according to

an individual or the society... Ethics serve as guidelines for analyzing ‘what is good or bad’

in a specific scenario” (Management Study Guide, 2013). A leader is an individual who has

often-characteristic traits, which makes their behavior appealing and effective. Traits that

are often associated with leaders include: intelligent, good communicator, objective, confi

2

“The first step to cultivating ethical leadership in your

organization begins with finding employees who share

and carry out ethical behavior that is in compliance with

your organization’s ethical code.”

dent, and approachable. Individuals who are described as ethical leaders are often described with these traits: honest,

integrity, respectful, and uses good judgment to make decisions.

Recipe for Ethical Leadership

Serving Size: 1

1-part ethical traits

1-part leadership traits

= Ethical leader

Ethical Leadership

How to practice ethical leadership:

TMEnterprising Rural FamiliesJuly 2015 Volume Xl, Issue 7

A leadership strategy withoutethical clarity produces moral

and economic bankruptcy.— Bill Donahuc

Ethical leadership has two elements according to research. The first element is leaders must act and make decisions ethi

cally like ethical people in general. Secondly, ethical leaders must lead in an ethical manner. Ethical leaders must lead

ethically- in the ways they treat people in everyday interaction, in their attitudes, in the way they encourage, and in the di

rections in which they steer their organizations or institutions or initiatives,” (Rabinowilz, 2014). It is important to under

stand- ethical leaders are ethical all the time and they are consistently ethical overtime, proving lime and time again that

ethics are essential to the perception and framework they use to understand and communicate to the world.

Ethical leaders time after time make decisions that are in the best interest of the greater good rather than making decisions

that solely benefit themselves. Being open to feedback, different opinions, and challenges to ideas and actions. Ethical

leaders encourage others to become leaders as well as accept responsibility and accountability for their actions. Perhaps

most importantly, “ethical leaders understand the power of leadership and use it well--sharing it as much as possible, nev

er abusing it, and exercising it only when it will benefit the individuals or organization they work with, the community, or

society,” (Rabinowitz, 2014).

Ethical leadership requires a clear and coherent ethical framework which they draw upon in making decisions and taking

action. Individuals develop their ethical framework based upon experiences, background, education, and the actions of

role models. Your ethical framework essentially is everything that has gone into creating who you are. Leaders of organi

zations need to have the same ethical framework, vision and mission of the organization. An organization cannot be led

effectively by a leader who doesn’t share and value the same things as the company (Rabinowitz, 2014). In addition to

leading organizations ethically, ethical leaders surround themselves with ethical employees who have a similar ethical

framework and are able to support and carry out the mission of the company. Leaders should also celebrate with their em

ployees when positive ethical moments occur. “Managers should talk about what positive ethics looks like in practice as

often as they talk about what to avoid. Take time to celebrate positive ethical choices,” (Brooks, 2013).

3

THERE ISNO RIGHT WAYTODOA WRONG THING.

It is recommended that the ethics of an organization and ethics of

— everyone who are part of it be frequently discussed. Everyone’s

ethical assumptions, including the leaders’, should be open to discussion. “Talk about ethics as an ongoing learning journey,

not something you have or don’t have. Recognize that the world changes constantly, and that ethical conduct requires that eve

ryone remain vigilant,” (Brooks, 2013). Take advantage of these on-going opportunities to talk about ethics to grow and learn

and build you organization rather than a yearly mandatory training program.

Other ethical leadership practices include: taking leadership positions seriously, maintaining perspective while keeping a sense of

humor. Honoring the golden rule; one should treat others as one would like to be treated. Collaborate often; collaborating helps

spread power and responsibility throughout the organization. Work to maintain communication channels and continue to grow

and develop interpersonal skills. Finally, the hardest task for most ethical leaders is recognizing when an organization needs

new leadership (Rabinowtz, 2014). Just like anything else an organization is a living entity and requires new leaders to help it

grow and thrive.

Organizations, big or little, all need ethical leaders to help achieve their goals. Ethical leadership, like any other form of leader

ship, needs to be consistent and always evolving and growing. The first step to cultivating ethical leadership in your organization

begins with finding employees who share and carry out ethical behavior that is in compliance with your organization’s ethical

code - continue to hold everyone to those ethical expectations (Brooks, 2013). “Like so many other important tasks, maintaining

ethical leadership is ongoing, like only a few others, it can last a lifetime,” (Rabinowitz, 2014).

Resources

Brooks, Chad. “7 Steps to Ethical Leadership.” businessnewsdaily. BusinessNewsDaily., 02 December 2013. Web. 9 Jun 2015.

<http:Ilwww. businessnewsdaily. com/5537-how-to-be-ethical-leader. html>.

Management Study Guide, . “Leadership.” Management Study Guide. Management Study Guide, n.d. Web. 27 May 2015.

<http:llmanagementstudyguide.com/qualities_of_a_leader. htm>.

Rabinowitz, Phil. “Section 8. Ethical Leadership “Orienting Ideas in Leadership. 2014. Print. <http://ctb.ku.edu/enltable-of

contentslleadershiplleadership-ideas/ethical- leadershiplmain>.

Enterprising Rural FamiIiesT’1Juy2O15VoumeXl, Issue 7

Your qualifying delivery order of $125 or more.

COUPON CODE: 64202218Exciudestechnology. Offervalid through 8/10/15

0

ceDEPOT.

All your school supplies.All in one place!

$a

3J

H

Iv

Have an account? Visit:busness otfceoepot cor

Need an account? Register at:

https://odams.officedepot.com/registrations/synergybai.php

Parents and teachers know that heading back to school requires a diverse

selection of supplies. From little ones getting on the bus for the first day ofkindergarten to college students ready for the next semester, we haveaccessories and essentials for every grade and age level. Complete anyschool supplies list with choices from our assortment of must-have items.

*EDITORS ABA Chief Economist James Chessen can be scheduled forinterviews by calling 202-663-5471.

Consumer Delinquencies Fall Slightly in First QuarterLower Home-Related Delinquencies Lead Dedilne

WASHINGTON — Delinquencies in closed-end loans and bank cards fell in thefirst quarter, highlighted by a significant drop in home equity loan and homeequity line delinquencies, according to results from the American BankersAssociation’s Consumer Credit Delinquency Bulletin. Delinquencies fell in five ofthe 11 individual loan categories while delinquencies in two categories — directauto loans and marine loans — remained unchanged.

The compositeratio, which

500tracksdelinquencies ineight closed-end 4,00

installment loancategories, fellone basis point tol1.53 percent ofall accounts — 200

continuing athree-year trendof remaining wellunder the 15-year average of 000

2.28

_____

percent. (SeeHistorical Graphic.) The ABA reportthat is 30 days or more overdue.

“It’s highly encouraging that consumers continued to improve their financialsituations even during a quarter where the economy contracted,” said JamesChessen, ABA’s chief economist. “This speaks to sustained consumer disciplineas Americans continue to use and manage their debt responsibly.”

Delinquencies in all three home-related categories fell in the fourth quarter, withhome equity loan delinquencies falling 11 basis points to 3.12 percent, homeequity line of credit delinquencies falling 6 basis points to 1.42 percent andproperty improvement loan delinquencies falling three basis points to 0.90percent.

“Home equity loan and line delinquencies are tracking the slow and steadyimprovements in the housing market,” said Chessen. “As property values

Installment Loan Delinquencies Stay Near Record lows

15-Year Average: 2.28%End of 0.1 2015: 1.53% — Composite — — 15-Year Aserate

1.53%

e.l m La

defines a delinquency as a late payment

improve, fewer people have negative equity in their homes. Greater householdwealth and income gives consumers more breathing room to meet their financialobligations.”

Bank card delinquencies fell slightly in the first quarter, dropping three basispoints to 2.49 percent of all accounts. They remain well below their 15-yearaverage of 3.76 percent and have varied by only 14 basis points since the fourthquarter of 2012.

“Delinquencies for credit cards have remained remarkably stable at historicallylow rates,” said Chessen.

Chessen expects the delinquency levels to hold near record lows amid a stableeconomy and continued financial vigilance among consumers.

“Falling unemployment, steady job gains and higher incomes may have drivendelinquencies rates down to about as low as they can go,” saidChessen. “Maintaining these low delinquency levels is possible as long asconsumers remain focused on managing their level of debt. People have done agreat job over the last few years and hopefully the lessons of the past willcontinue to pay dividends well into the future.” (See Economic Charts.)

The first quarter 2015 composite ratio is made up of the following eight closed-end loans. All figures are seasonally adjusted based upon the number ofaccounts.

CLOSED-END LOANS

• Personal loan delinquencies rose from 1.42 percent to 1.48 percent.• Direct auto loan delinquencies remained at 0.71 percent.• Indirect auto loan delinquencies rose from 1.53 percent to 1.58 percent.• Mobile home delinquencies fell from 3.60 percent to 3.52 percent.• RV loan delinquencies rose from at 0.98 percent to 1.01 percent.• Marine loan delinquencies remained at 1.17 percent.• Property improvement loan delinquencies fell from 0.93 percent to 0.90

percent.• Home equity loan delinquencies fell from 3.23 percent to 3.12 percent.

In addition, ABA tracks three open-end loan categories:

OPEN-END LOANS

• Bank card delinquencies fell from 2.52 percent to 2.49 percent.• Home equity lines of credit delinquencies tell from 1.48 percent to 1.42

percent.

• Non-card revolving loan delinquencies rose from 1.80 percent to 1.91percent.

Consumer TipsFor borrowers having trouble paying down debts, ABA advises taking action --

sooner rather than later -- to solve debt problems. Proven tips are listedbelow. Additional consumer information on budgeting, saving, managing creditand more is available at ABA.com/Consumers.

• Talk with creditors — the sooner you talk to them, the more options youhave;

• Don’t charge more purchases until your problems are solved;• Avoid bankruptcy — it’s a short-term solution with long-term consequences;

and• Contact Consumer Credit Counseling Services at 1-800-388-2227.

GlossaryIndirect auto loan: loan arranged through a third party such as an auto dealer.Direct auto loan: loan arranged directAy through a bank.Delinquency: late payment that is 30 days or more overdue.Bank card: a credit card provided by a bank.Closed-end loan: a loan for a fixed amount of money with a fixed repaymentperiod and regularly scheduled payments.Open-end loan: a loan with a fixed amount of available credit but a balance thatfluctuates depending on usage such as a line of credit.

The American Bankers Association is the voice of the nation’s $15 trillion bankingindustiy, which is composed of small, regional and large banks that togetheremploy more than 2 million people, safeguard $11 trillion in deposits and extendmore than $8 trillion in loans.

###

2015 WM llankPac Is

Mi

Unerwfly!

___

BankPac

BANKERSTom Abernathy - Wyoming Community Bank, RivertonAnn Anderson — Pinnacle Bank, CodyStephanie Arnold - Bank of Commerce, RawlinsKevin S. Bailey - First Federal Savings Bank, SheridanJohn Barto Jr. - Bank of Commerce, RawlinsThomas Bass - Wyoming Bank & Trust, CheyenneJim Belcher — Crowley Heck, PLLPJeff Benson — Bankers’ Bank of the WestJennifer Booth - Pinnacle Bank, TorringtonWade Bruch - Pinnacle Bank, TorringtonPaul Brunkhorst - The Bank of Buffalo, BuffaloJennifer Burns - First State Bank, WheatlandCheryl Callies - First Interstate Bank, CasperBill Chandler - Bank of Commerce, RawlinsTheresa Christensen - First Interstate Bank, CasperGary Conatser - Bank of Commerce, RawhnsDavid Conrad - The Bank of Buffalo, BuffaloJohn J. Coyne UI - Big Horn Federal Savings BankGary Crum - Wyoming State Bank, LararnieDarold Destefano - Bank of Sheridan, SheridanRichard Destefano - First Interstate Bank, SheridanKaren Deveraux - First Interstate Bank, CasperJim Durfee - Sundance State Bank, SundanceTrudy Durfee - Sundance State Bank, SundanceMichael D. Edelman - First Interstate Bank, RivertonScott Estep — Wyoming Community Bank, LanderFaron Ferguson - Pinnacle Bank, MoorcroftDavid J. Ferries - First Federal Savings Bank, SheridanLisa Foster — Pinnacle Bank, NewcastleRobert Foster - Wyoming Community Bank, RivertonCopper France - Bank of Commerce, RawlinsSherrod France - Bank of Commerce, RawlinsMichael Geesey - Wyoming Bankers AssociationKeith Geis - Platte Valley Bank, WheatlandStig Hallingbye - Security First Bank, CheyenneEric Hailman - ICBADavid Hansen - Pinnacle Bank, TorringtonBen Hansen - RSNB Bank, Rock SpringsJohn Hay - RSNB Bank, Rock SpringsKeith Hay - RSNB Bank, Rock SpringsJanet Hayek - First Interstate Bank, CasperKelly Hayworth - Sundance State Bank, SundanceRobert Hunt - Bank of Commerce, RawlinsBill Huppert - First Interstate Bank, SheridanMark Huston - WSCNLora Jeffs - Pinnacle Bank, CodyMark Johnson — Kansas Bankers SuretyGregg Jones - Jonah Bank of Wyoming, CheyenneLea.Ann Jones - Sundance State Bank, SundanceCraig Kerrigan - Oregon Trail Bank, CheyenneArchie Kirsch - Bank of Commerce, RawlinsTy flell - Sundance State Bank, SundanceJohn Linton - Wyoming Community Bank, LanderLas Malson - First Interstate Bank, Gillette

Brett MaIns - Platte Valley Bank, TorringtonAndrea Mattock - Pinnacle Bank, TorringlonGil McEndree - Pinnacle Bank, WorlandRick Malone - ANB Bank, LaramieLynne Michelena - First Interstate Bank, BuffaloAndy Miller - Sundance State Bank, SundanceMinnie Miller — Pinnacle Bank, ThermopolisRebecca Miller - AI’4B Bank, LaraxnieDan Moline - Wyoming Community Bank, RivertonPamela Mosser - Security First Bank, CheyenneBrent Mullock - Pinnacle Bank, TorringtonGary Negich - First Interstate Bank, LararnieRuby Ogden - Bank of Commerce, RawlinsCortney Parker - Bank of Commerce, RawlinsMary Penland - Bank of Commerce, RawlinsTodd Peterson - Pinnacle Bank- TorringtonJohn Heifer - Bank of Commerce, RawlinsMatt Pope - First Interstate Bank, CheyenneShawn Porter - First Interstate Bank, CasperTanya Raile - Pinnacle Bank, CodySteven Reimann - AEB Bank, BuffaloRegina Rentfro - Bank of Commerce, RawlinsCharles Ruwart - Oregon flail Bank, GuernseyDusty Schutzman - Pinnacle Bank, CodyLeonard Scoleri - Oregon Trail Bank, GuernseySynthia Scoleri - Oregon Trail Bank, GuernseyScott Sexson — Central States Health & Life CompanyKent Shurtleff — Wyoming Community Bank, RivertonDerrick Sisson - First State Bank, GuernseyJana Stafford - Pinnacle Bank, CodyMary Margaret Stockton - Wyoming Community Bank, RivertonSusan Stokes - Wyoming Community Bank, RivertonColleen Stratton - Bank of Commerce, RawlinsSharon Streitz - First Interstate Bank, CasperNedalyn Testolin - Oregon Trail Bank, ChugwaterJustin Tystad — Pinnacle Bank, NewcastleRon Van Voast - Security First Bank, CheyenneDana Wallace - First Interstate Bank, CasperDouglas Weedin - Pinnacle Bank, CodyMark Westerhold - Pinnacle Bank, CodyKen Wright — Big Horn Federal Savings BankRonald E. Wright - Platte Valley Bank, Casper

The 2015 WBA BartkPac campaign is in full Swing. To date 97 individuals from 36 banks & branches and 7 businesspartners have contributed $12,030 to the current campaign. The following is a list of WBA members and their bankswho have contributed as of July 31, 2015.

Banks/Associate MembersANB Bank — Buffalo, Lararnie Platte Valley Bank — Casper, Torrington,Bank of Commerce — Rawlins WheatlandBank of Sheridan Pinnacle Bank — Cody, Moorcroft, Worland,Bankers’ Bank of the West Tordngton, Newcastle, ThermopolisBig Horn Federal Savings Bank - Greybull RSNB Bank — Rock SpringsCentral States Health & Life Company Security First Bank - CheyenneFirst Federal Savings Bank - Sheridan Sundance State Bank - SundanceFirst Interstate Bank — Buffalo, Casper, Cheyenne, The Bank ot Buffalo

Gilleffe, Laramie, Riverton, Sheridan WSCNFirst State Bank — Guernsey, Wheatland Wyoming Bankers AssociationICBA Wyoming Bank & Trust - CheyenneJonah Bank of Wyoming - Cheyenne Wyoming Community Bank — Lander,Kansas Bankers Surety RivertonOregon Trail Bank — Cheyenne, Chugwater, Wyoming State Bank - Lararnie

Guernsey

WBA Bank Pac is the nonpartisan political action committee of the Wyoming Bankers Association. All contributions are voluntary. Absolutely no form ofcoercion may be used to solicit a contribution. No employee will be favored, disadvantaged, or retaliated against based on their contribution amount or theirdecision not to contribute. A suggested contribution is only a suggestion. Corporate contributions are prohibited. Contributions to WBA BanicPac are notdeductible for state or federal income tax purposes. Federal 1_aw requires political action committees to obtain written authorization to solicit and to use bestefforts to report the name, mailing address, occupation, and name of employer for each individual whose contributions aggregate an excess of $200 in itscalendar year. State law requires political action committees to use best efforts to report the name, mailing address, occupation, and name of employer foreach individual whose contributions aggregate an excess of $100 in a reporting period.

uLk uD

Ron Boyd Retires as CEORon has been with Security State Bank for over 34 years. Ron and his wife Kathy, will continue to livein the Basin area and Ron is going to continue to serve on the Security State Bank Board and work forthe bank part time to include managing an internal appraisal department, managing some accounts, andhelp share his wealth of banking knowledge. Security State Bank held a retirement party for Ron onThursday, July 16, 2015 at the Basin City Arts Center.

Employment Opportunities

THERawlinsNATIONAL BANK Commercial Lender — Rawlins, WYCommunity Minded.

just like you

The Rawlins National Bank has an exciting career opportunity for an experienced Commercial Lender tojoin our team. The Commercial Loan Officer is responsible for originating new commercial loans,maintaining an existing loan portfolio and developing customer relationships through communityinvolvement and business development activities.

Qualified candidates must possess a Bachelor’s Degree and 3-5 years commercial lending experience.This position requires strong analytical, organizational and communication skills. Training programs areavailable with promotion potential to Assistant Vice President, then Vice President. This careeropportunity is based out of our Rawlins, WY location and may require occasional travel. The RawlinsNational Bank has branch locations in Wyoming and Colorado.

Rawlins offers many scenic and recreational places to live and work. Rawlins is a recent national awardwinner for its downtown, and has been highly ranked within the top 20 in Outdoor Life’s magazine top200 towns for outdoor recreation, as has Carbon County.

If you are interested in joining our team of experienced professionals at The Rawlins National Bank,please send your resume to:

The Rawlins National Bank Or deliver in person to:Attn: Human Resources The Rawlins National BankP0 Box 100 220 Fifth St.Rawlins, WY 82301 Rawlins, WY 82301

The Rawlins National Bank is an Equal Opportunity Employer

ThE WYOMiNG BANKERShare your news with the Wyoming Bankers Association!

Whenever your financial institution has a newsworthy event such as a promotion or appointment, a retirement, an anniversary celebration, a branchopening, a community contribution, or any other item of interest, we want to hear from you. Complete the form below and return it to the WBA, or

send us a press or news clipping. Your item will be published in the next issue of The Wyoming Banker.

Name

Institution

Address

City/State/Zip

Phone

Here’s our story: (Must be typed)

Mail, fax, or email your news items to:The Wyoming Banker Editor

Wyoming Bankers Association, P0 Box 2190, Cheyenne, WY 82003Phone: 307-638-5008 * Fax: 307-638-5013 * Email: [email protected]

Wyoming BrkersAssn. August2015

N1WSPAPER CLIPPINGSClick on the headline to read full article

Congratulations, David Hubert!

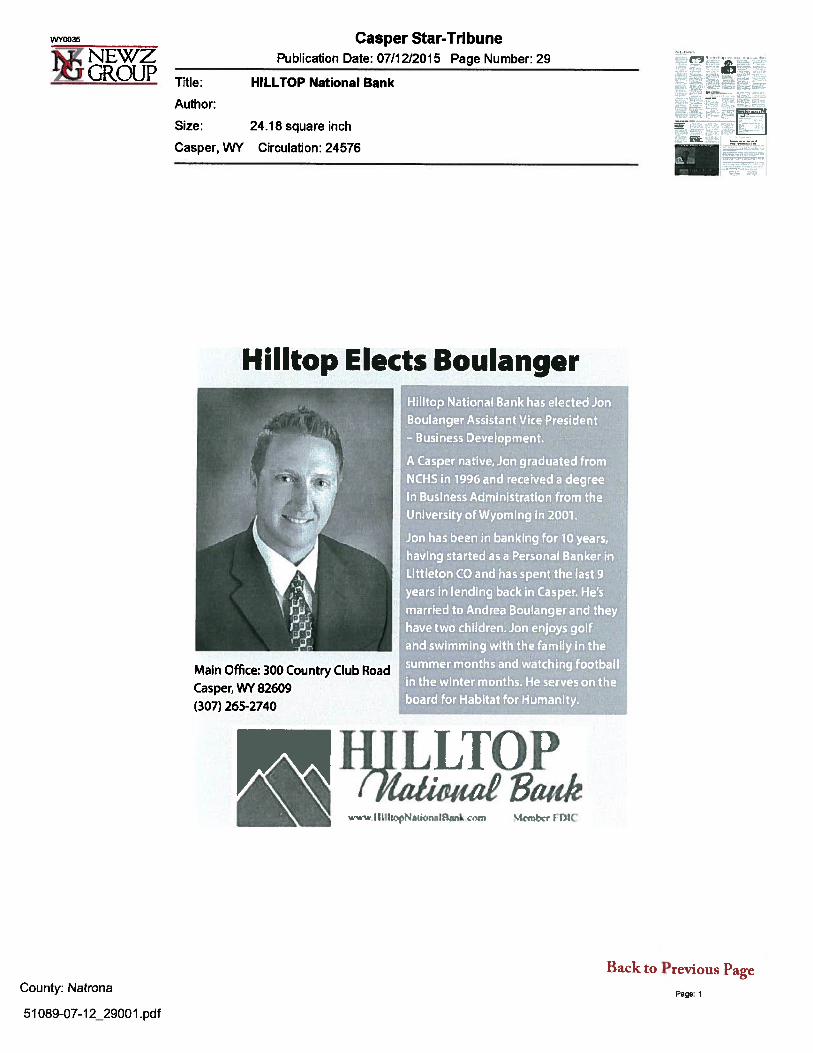

Hilltop Elects Boulanger

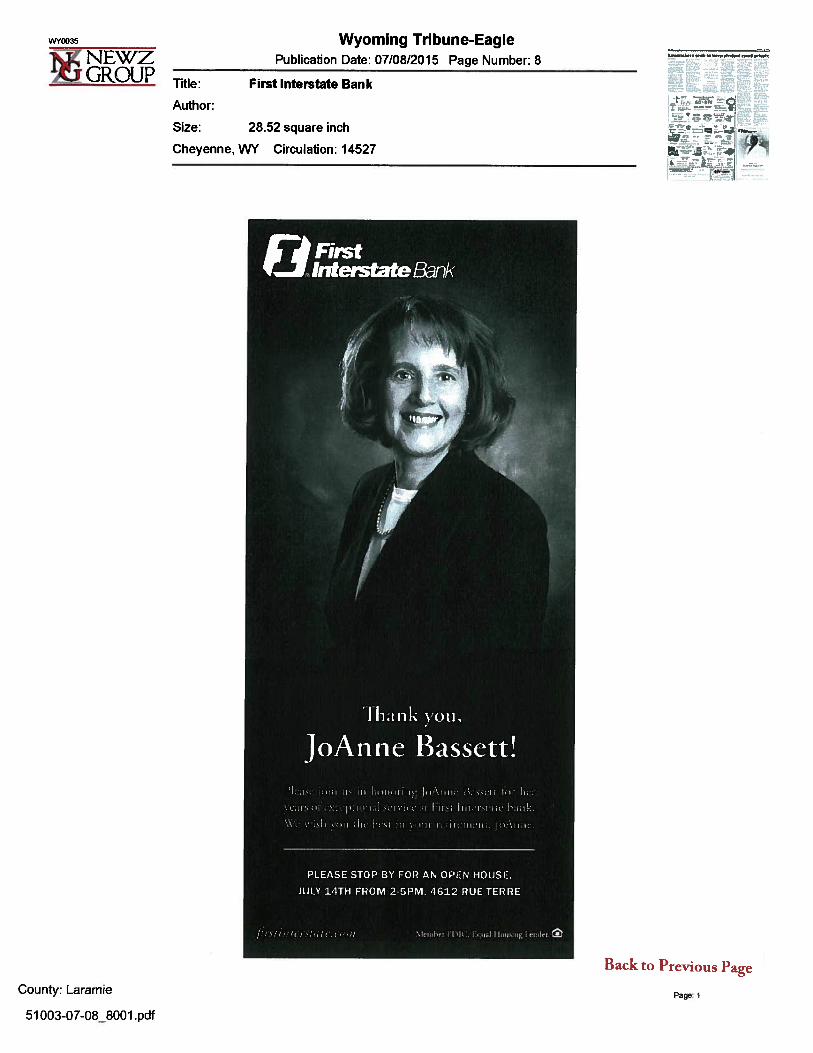

Thank you, JoAnne Bassett!

1st bank is pleased to announce a new Board Chairman

• Todd Ernst to Lead Pinnacle Bank — Powell

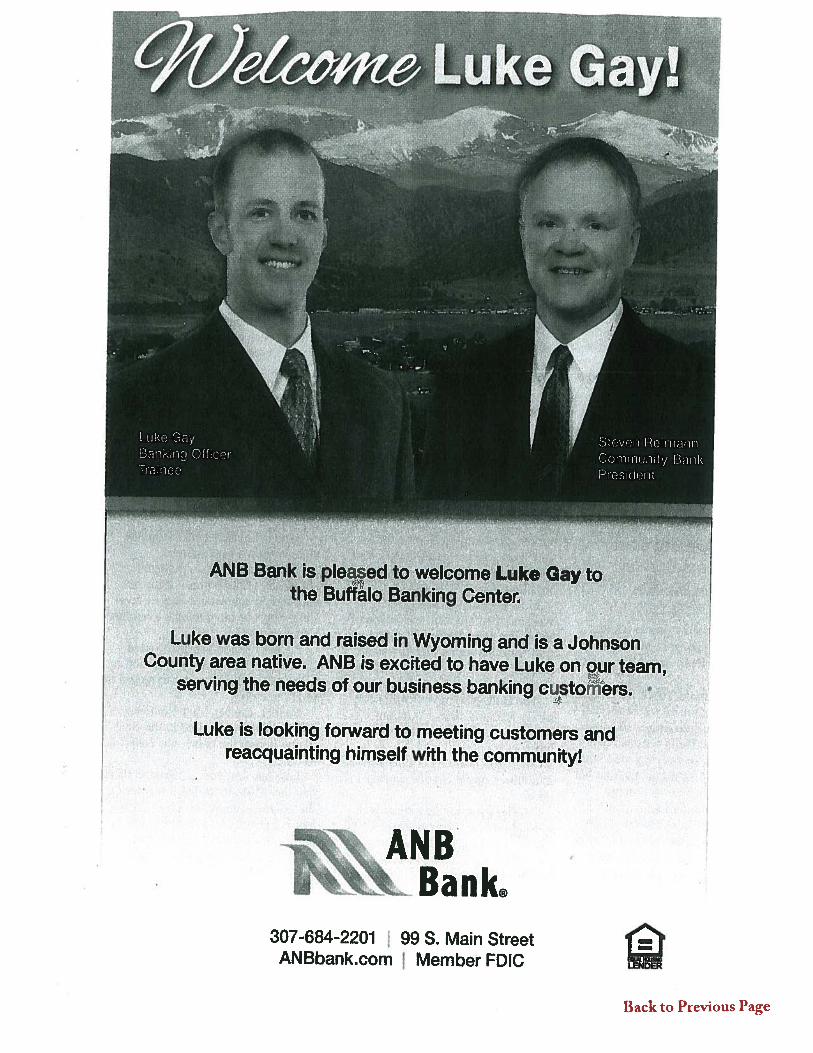

Welcome Luke Gay!

Jean Georges

Sharon Ferguson

• Grace Nadine Mong Brown

• Cherie M. Quealy

• Wells Fargo gives $100K

• New Computer for Lions

• SAFV Task Force gets donation from RMP

• Banking boom

• Find the best bank for you, your needs

VVYOO35

NEWZGROUP Title:

Sheridan PressPublication Date: 07/23/2015 Page Number: 8

First Interstate Bank

Author:

Size: 40.3 square inch

Sheridan, WY Circulation: 5750

County: Sheridan

5101 5-07-23_8001 .pdf

Back to Previous Page

Page: 1

WY0035

NEWZyGROUP

Casper Star-TribunePublication Date: 07/12/2015 Page Number: 29

HILLTOP National Bank

Author:

Size: 24.18 square inch

Casper, WY Circulation: 24576

-

Hilltop Elects Boulanger

Main Office: 300 Country Club RoadCasper, WY 82609(307) 265-2740

Back to Previous PageCounty: Natrona

Page: 1

Hilltop National Bank has elected JonBoulanger Assistant Vice President— Business Development.

A Casper native, Jon graduated fromNCHSin 1996 and received a degreeIn Business Administration from theUniversity of Wyoming In 2001.

Jon has been in banking for 10 years,having started as a Personal Banker inUttleton CO and has spent the last 9years in lending back in Casper. He’smarried to Andrea Boulanger and theyhave two children Jon enjoys golfand swimming with the family in thesummer months and watching footballin the winter months He serves on theboard for Habitat for Humanity

HILLTOP[&liiwP Bau,

ww Ii I fti,.nk ..e.m \kii,kr I[1i(

51089-07-1 2_29001 .pdf

WY0035

NEWZGROUP Title:

Wyoming Tribune-EaglePublication Date: 07/08/2015 Page Number: 8

First Interstate Bank

Author:

Size: 28.52 square inch

Cheyenne, WY Circulation: 14527

i—zeze

--

I

County: Laramie

Back to Previous Page

Page: I

51 003-07-08_8001 .pdf

WY0035

‘ NEWZ

___

3GROUP Title:

Author:

Uinta County HeraldPublication Date: 06/26/2015 Page Number: 7

I ST BANNK

JN( Bank is pleased to announce a new Board ChairmanDave Madia, from Evanston Wyoming, has been elecied Chairman by ihe Board of

I )irecl ors; elkcl ive .1 uly 21” 2015. 1 )ave has becim on (lie 1 Bank Hoard since I 99()

and will 1w icplacimig Jerry (ioiildiiig, Jerry (lomilding, froni 1\fton Wyoiiiing, loishweii a Ditector for 1’ Bank since 1995 and has served as Clniiimnan since 2007.

He will he lesiglillig omi .IuIv 21 .

Kim (loirles, froni Moimimlain View Wyoming, was elected Vice (Thairmiman amid

Tim Heppler, from Evanston Wyoming, will conlimitme to serve as Board Secretary.1’ Bank Board immenibers also iiiclitde Climis Bitmiiiig, froni Rock Springs,

I)avici Rich, from Morgan Utah, Harry Johnston, from Big Fork Montana,

Brent Sanders and F)oiig Nissen from Evanston.

1’ Bank is a Division of Glacier Bank with 150 eiiiploces iii 9 biamiclies located iii

E’aiistoii. Mountain View, Keiimnwrcr, Rock Springs, Piiiedale. Alpine, amid iIioii

Wymimig; ‘si organ and Mommntaimi Green ( tali.

Back to Previous PageCounty: Uinta

51 033-06-26_7001 .pdf

Page: 1

Size: 41.54 square inch

Evanston, VVY Circulation: 3200

Call the Uinta County Herald news desk at:News tip? Story idea? (307) 789-6560

News Release

FOR IMMEDIATE RELEASE

Todd Ernst to Lead Pinnacle Bank — Powell

July 23, 2015 — Pinnacle Bank is pleased to announce ToddErnst has been promoted to Market President of the Powellbranch.

In Ernst’s new position, he is responsible for new businessdevelopment, consumer and business lending, managingpersonnel and overseeing the day-to-day operations of thebranch.

Ernst has been in the banking industry since 1987, having served in many capacities for localcommunity banks in the Powell market.

A well-known figure in banking, business and community affairs, Ernst serves on the PowellEconomic Partnership Advisory Board and the Powell Chamber of Commerce Board ofDirectors. He also works with youth through AWANA club and Camp Wannabe. Ernst holdsa bachelor’s of science degree in Range Management from the University of Wyoming andhas resided in Powell for the past 22 years. He and his wife, Cheri, have two children, Sheenaand Tyler.

“I am very pleased Todd has accepted the position of Market President,” said DustySchutzman, Regional President. “Todd’s experience, broad perspective and passion fordelivering outstanding service to our customers will serve us well as we continue to grow.”

About Pinnacle Bancorp, the subsidiary owner of Pinnacle Bank:Family-owned since the 1938, Pinnacle Bancorp, Inc., is an $8 billion financial holdingcompany operating over 125 community banks in eight states. For more information, log ontowypinnbank.com.

For more information contact:Dusty Schutzman307.527.7186

Back to Previous Page

Luke was born and raised in Wyoming and is a JohnsonCounty area native. ANB is excited to have Luke on our team,

serving the needs of our business banking customers

ANBBank®

307-684-2201 99 S. Main Street

____

ANBbank.com Member FDIC

ANB Bank is pleased to welcome Luke Gay tothe Buffalo Banking Centers

Luke is looking forward to meeting customers andreacquainting himself with the community!

Back to Previous Page

WY0035

NEWZGROUP Title:

Wyoming Tribune-EaglePublication Date: 07/08/2015 Page Number: 5

Jean Georges

Author:

Size: 20.30 square inch

Cheyenne, WY Circulation: 14527

-- -.-

‘_V rj

Jean Georges1927-2015

JeanR.Georges,87,ofCheyennediedJuly4inCheyenne.

Shewasborn Dec.

21,1927, in Wellington,Cob., to Dietrich and ClaraRohwer.

She married PerryGeorgeson Sept. 20,1953,in Green River, and togethertheyowned andoperated Grier FurnitureStore. She also was atellerfbookkeeperforAmericanNational Bank.

She was a memberofCheyenne Country Club,where she was an avidgolfer and loved to playbridge, and the MemorialHospital Auxillary. Shealsowas a volunteerfor thePink Boutique.

She loved herfamily andwas very generous to thecommunity, especially inhelpingwith furtheringthe education ofher familyand friends.

She is survived byabrother, Charles RohwerofCheyenne; and numerous nieces andnephews,including Rick Durante of

Cheyenne, who was like ason to her.

She was preceded by herhusband, Perry Georges;herparents; and siblings,Dorothy Nickel andRichard Rohwer.

Visitationwill be fromnoon to 7p.m. today atSchrader, Aragon andJacoby Funeral Home.Funeral services will be at2p.m. Thursday atLakeview Chapel atSchrader, Aragon andJacoby Funeral Homewith Father AugustineCanillo officiating.Intermentwill follow atBeth El Cemetery, whichwill he followed by a reception atSchrader ReceptionCenter.

In lieu offlowers, donations may be made toAlzheimer’s AssociationWyoming, 2232 DellRange Blvd. Suite 220,Cheyenne, WY 82009.

The family would liketo extend heartfelt thanksto Lucille Marx, Jean’scaregiver for the pastyear.

Online condolences maybe made atwww.schradercares.com.

Thisisapt-idobftwaiy.

County: Laramie

Back to Previous Page

Page: 1

51 003-07-085003.pdf

WY0035

‘ NEWZGROUP Title:

Wyoming Tribune-EaglePublication Date: 07/10/2015 Page Number: 5

Sharon Ferguson

Author:

Size: 13.64 square inch

Cheyenne, WY Circulation: 14527

S -

Sharon Fergnson1948-2015

SharonKayFerguson,67, ofCheyennediedJuly 8after alengthybattle with

cirrhosis and livercancer.She was bornMarch 1,

1948, in Rapid City, S.D., toReeford and GladysChariton.

Mrs. Ferguson workedfor 43 years in the clericalfield, 23years ofwhich sheworked forbanks. Her lastnineyears she worked forSecurity FirstBankinCheyenne.

She enjoyed sharinghertalents ofcrafts with family and friends. She lovedanimals andbirds, andenjoyedridingwithherhusband, Red, on hisHarley.

Mrs. Ferguson is sur

vivedbyherhusbandof29years, Edward “Red”Ferguson ofCheyenne;son, Justin Holsworth ofFort Worth, Texas; onegranddaughter; sisters,Joyce OlsonofBox Elder,S.D., and L.aVonne HayesofFort Smith, Ark.; twinsister, Karen Coleman ofLas Vegas; and numerousnieces and nephews.

She was preceded indeath byherparents andsister, Gladys Viola.

She requested herbodybe an anatomical gift donated to the UniversityofColorado AnschutzMedical Campus fororgandonation and research.

Friends may contributeto the Davis HospiceCenteror CheyenneAnimal Shelter.

Graveside services willbe at a later date in RapidCity, officiated by KirkFuneral Home.

County: Laramie

Back to Previous Page

Page: 1

51003-07-1 0_5002.pdf

News-RecordWY0035

NEWZj. GROUP Title:

Publication Date: 07/12/2015 Page Number: A04

Grace Nadine Mong Brown

Author:

Size: 58.74 square inch

Gillette, VVY Circulation: 7200 L

RAID OEITUARYGrace Nadine Mong Brown

Grace Nadine MongBrown was born May29,1929. to Ray andEva Mong at theirhome in Yoder. Shepassed away peacefullyThursday, June 18.2015.in Lakowood, Colorado.from the debilitatingeffects of Alzheimer’sdementia.

The familywill hold amemorial service to celebrate Grace’s lifeat 9:30 am. Aug. 8 at the First PresbyterianChurch, 250 West 22nd St.. Cheyenne, WY82001.

Ray and Eva Mong homesteaded inwestern Nebraska after Ray returned fromserving in the Army during World War I. Hewas appointed rural mail carrier in Yoderand served for 30 years. Eva worked as abookkeeper and played piano in church andaccompanied silent movies.

Grace attended Yoder schools andmoved to Cheyenne after graduating fromhigh school. She took a summer job at theCitizens’ National Bank and then postponedher acceptance of a scholarship at theUniversity of Wyoming to work at the bankfora year. She never made it to Laramie.

On June 3,1948, she married her Yoderschoolmate and lifelong partner, DelbertBrown, at the First Presbyterian Church inTorrington.

Del worked for the local Texaco distributor for the next several years in Torringtoi,.where Grace gave birth to the first two oftheir four sons, Robert and Roger. in 1949and 1952.

In 1954, Grace and Del returned toCheyenne when Del joined the WyomingHighway Patrol and Grace worked part-timeat the Stockgrowers Bank.

After completing his training, Del wastransferred to Gillette for a ‘temporary”assignment that lasted five years and led toa 22-year stay in that community for Graceand Del. Sons Thomas and Richard were

born there in 1956. and 1957.Del went to work at the Stockmens Bank

after leaving the patrol. As the younger boysreached school age, Grace returned to workas a part-time bookkeeper for Ostlunds Inc.and later accepted the position of DeputyCounty Treasurer for Campbell County. Sheserved in that position for seven years untilher election as County Treasurer in 1974.

Grace and Del moved to Cheyenne in1977, where Grace returned to her oldemployer. Stockgrowers Bank (which hadbecome First National Bank), as a mortgageloan officer. She quickly gained experienceand responsibility, serving as Vice Presidentof Mortgage Loans, Vice President ofOperations. Manager of the Mortgage LoanDepartment, Vice President of PersonalBanking and Marketing and Vice Presidentof Marketing and Retail Sales as the bankwent through a series of mergers andname changes (Norwest Bank Cheyenne,Wyoming National Bank, Norwest BankWyoming and eventually becoming part of

Wells Fargo Bank).Grace was excited to finally attend col

lege at the University of Colorado at Boulderfor several weeks each year from 1982 to1984, and again in 1986 and 1987. That’swhere she graduated from professional continuing education programs at the GraduateSchool of Banking and the School of BankMarketing.

After retiring briefly from the bank forthree months in 1992, Grace returnedto work seasonally as a committee secretary in the House of Representativesfor six annual sessions of the WyomingLegislature. She also worked part time forAAA Wyoming and Western Bank.

In 1999, Grace and Del moved to BigFork. Montana, to be near son Tom and hisfamily and to enjoy the beauty and outdoorrecreation of the Flathead Valley,

Grace once again found seasonal andpart-time work with the Big Fork Chamberof Commerce and the Flathead Valley Bankduring their eight years in Montana, Whenthey returned to Cheyenne in 2007, Grace

finally retired from paid work, but continuedto volunteer with the Cheyenne BotanicGardens and the Cheyenne RegionalMedical Center.

In 2012, Grace and Del moved to Golden,Colorado, to be closer to their sons Rogerand Richard and their families.

Awoman of strongand enduring faith,Grace was a lifelong Christian and activemember of the Presbyterian arid Methodistchurches wherever she lived. She heldvolunteer service and leadership positions

too numerous to list. Grace was also activein other community arid service organizations, including PTA, Circle of Friends, Orderof the Eastern Star and PEO International.

Grace enjoyed playing the piano andsinging — joining community and churchchoirs at every opportunity — but sheespecially loved to play and sing with herchildren and grandchildren. Her love ofmusic was infectious and inspired threegenerations of both professional and amateur singers, musicians, performers andmusic lovers.

Above all. Grace loved her family andwas the kind of mother, grandmother andgreat-grandmother that all children shouldhave — playful. loving, caring, attentive,firm-but-forgiving and great at baking cookies. We will miss you, Nana.

During 86 years with us in Wyoming,Montana and Colorado, Grace Brownshared her unrelenting joy and love of lifewherever she went and touched innumerable lives with acts of kindness that werenever random when coming from Grace.

She once wrote,” I don’t care what theywrite on my tombstone as long as it doesn’tsay ‘She meant well!”

She didn’t need to worry. While the radiant light of Grace’s bright spirit no longershines directly on us. it continues to warmthe memories and illuminate the souls ofher family and many, many friends. But thetruly amazing legacy Grace left us is thelight that glimmers in the hearts of so manyothers who felt her glow but never evenknew her name. She wants us to pass it on

County: CampbellPage: 1

51005-07-1 2_A04001 .pdf

News-RecordW’OO35

NE’X”Z Publication Date: 07/12/2015 Page Number: A04GROUP Title: Grace Nadine Mong Brown

Author:

Size: 58.74 square inch

Gillette, WY Circulation: 7200

—with interest.Grace is survived by her blessed husband

of 67 years, Del bert Erven Brown; her luckysons (and devoted daughters-in-law) RobertErven Brown (Kathy) of Phoenix, Arizona,Roger Kelley Brown (Susan) of Golden,Colorado, Thomas Edward Brown (Katie) ofBig Fork, Montana, and Richard Lynn Brownof Lakewood, Colorado; 11 ‘spoiled grandchildren: and four great-grandchildren,