iq issue 36

DESCRIPTION

Issue 36 of IQ Magazine, the leading title for the international live music businessTRANSCRIPT

Live Music inteLLigenceAn ILMC Publication. July 2011, Issue 36

Live Still the Driver: Chris Carey • the Winds of change: shuki Weiss • On the Beat: Derek Smith • survivaL: BoB Paterson

PeoPLe PoWer Social media and its meteoric impact on live reaching the Peaks Stuart Galbraith on 30 years in the business the next diMension? 3D and gigs: perfect match or passing fad? shifting gear Merchandise feels the heat

TalenT ’s GoT BritainI Q Marke t repor t

20

38

32

48

16

News6 In Brief

The main headlines over the last two months

7 In Depth Key stories from around the live music world

Features16 People Power

Social media and its game-changing impact on live music

20 Reaching the Peaks Stuart Galbraith celebrates 30 years in the business

32 The Next Dimension? 3D and concerts: perfect match or passing fad?

38 Talent’s Got Britain IQ’s first market report on Great Britain

48 Shifting Gear Clive Rozario gets into the merchandise game

Comments and Columns12 Live Still the Driver

Chris Carey advises us to look beyond the numbers

13 The Winds of Change Shuki Weiss calls for understanding on Israel

14 On the Beat Derek Smith says the police do like UK festivals, really

15 Survival... Bob Paterson on life for the smaller venue and agent

56 In Focus From conference whoring to rock festival-hopping

57 Insight Academy Music Group CEO

John Northcote reflects the UK venue scene

58 Your Shout Who wants to be a record breaker?

Issue 36, July 2011

Contents

So the festival season is now fully upon us, and in the time it takes these pages to be printed and

posted, protestors could well have rioted at Glastonbury because U2 don’t pay all of their taxes in Ireland. It must be difficult being (a) so very famous; and (b) so virtuous, in that any slight perceived dalliance from the course of righteous truth is splashed across the world’s media. Combine the most famous festival in the world with arguably the world’s biggest band, and it’s a powder keg just waiting for a match, and just one of a thousand stories that now emerge from and around the festival scene every year.

The news that Festival Republic chief Melvin Benn is reigniting his bid to open a festival in the US, while Secret Garden Party organisers are also opening up an event across the Atlantic, does call to question whether America is the next big untapped festival market. It’s certainly a scene that’s driving innovation at the moment, at least if Coachella is anything to go by. Not only did the California favourite beat every European event to the RFID punch, but having announced it’ll run over two consecutive weekends next year, it’s trialling a completely new format.

On the subject of new formats and innovation tips, we’re decidedly tech-focussed this issue. Social media, the watchword of ILMC this year, is explored by Charlotte Mceleny, music specialist for New Media Age (page 16). And hot on the heels of pop outfit JLS taking cinemas by storm, we consider the impact of 3D on live music and ask whether it’s a perfect match or a passing fad (p. 32).

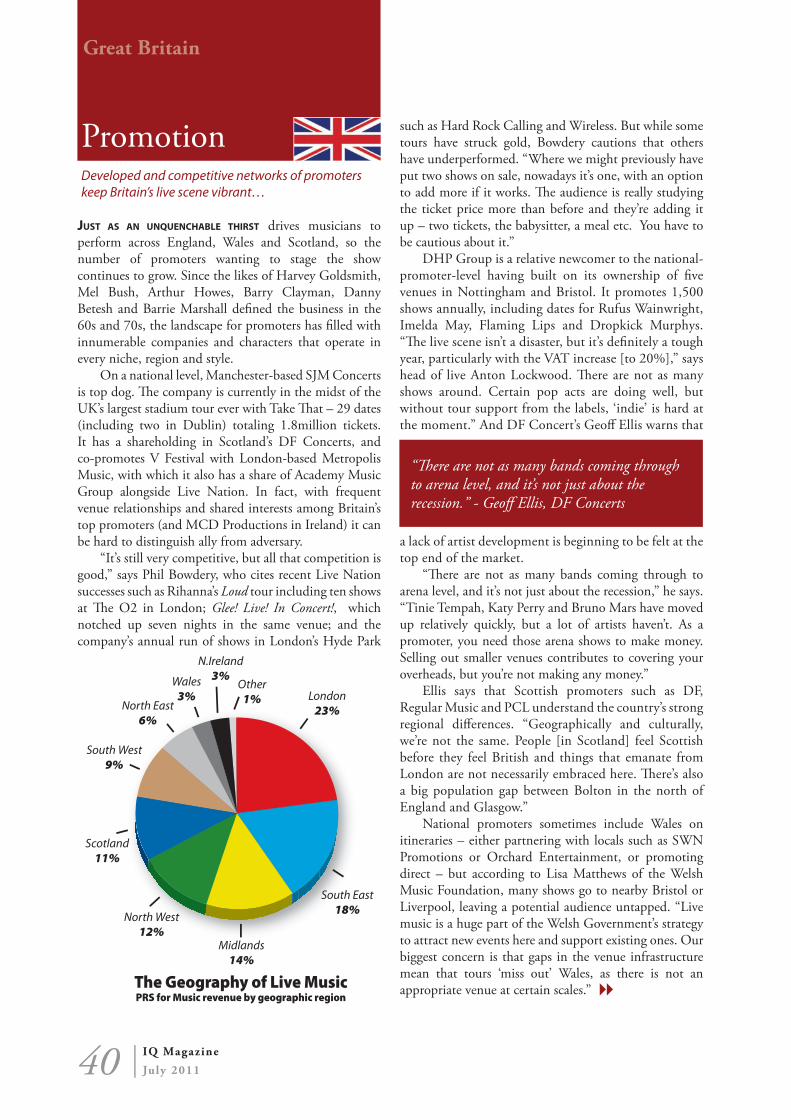

Moving on, as our slightly nationalistic cover suggests, this issue we’re publishing a market report on

Great Britain, the first by any trade publication such as ourselves. We’ve pulled together what available data is out there, and spoken to many of the key players from across the industry to hopefully build up a snapshot of what is such an important market for live music. If we’d just had another 50 pages, we might have been able to do it justice!

Add to that a profile on Sonisphere boss Stuart Galbraith as he celebrates 30 years in the business (p. 20), Clive Rozario’s take on the merchandise game (p. 48), and contributions from Chris Carey, Shuki Weiss and even a chief policeman, and we’ve got more words than Glastonbury has bands.

Oh, and one final word on festivals… this summer I’m setting off on something of a marathon trip to visit a whole bunch. I’ll be writing about it in the next issue, but if you’re interested, please check out www.facebook.com/RidetoLive2011.

Until next time!

As the festival season kicks off, America is where all the action is, writes Greg Parmley…

The Idea Factory

THE ILMC JOURNALLive Music IntelligenceIssue 36, July 2011 IQ Magazine2-4 Prowse Place,London, NW1 9PH, [email protected]: +44 (0)20 7284 5867Fax: +44 (0)20 7284 1870

PublisherILMC and M4 Media

EditorGreg Parmley

Associate EditorAllan McGowan

Marketing& Advertising ManagerTerry McNally

Sub EditorMichael Muldoon

Production AssistantAdam Milton

Editorial AssistantClive Rozario

ContributorsLars Brandle, Chris Carey, Meredith Humphrey, Charlotte Mceleny, John Northcote, Bob Paterson: Clive Rozario Derek Smith, Manfred Tari, Shuki Weiss, Adam Woods.

Editorial ContactGreg Parmley, [email protected]: +44 (0)20 7284 5867

Advertising ContactTerry McNally, [email protected]: +44 (0)20 7284 5867

Design & Production Oyster [email protected]

Editorial

To subscribe to IQ Magazine: +44 (0)20 7284 5867 [email protected] Annual subscription to IQ is £50 (€60) for 6 issues.

As the festival season kicks off, a smorgasbord of deals, disputes and demands keeps the industry on form and as vibrant as ever...

In Brief...April• New Zealand passes a three-strikes

law that allows copyright holders to demand ISPs ban repeat illegal file-sharers.

• Live Nation expresses interest in running the new Copenhagen arena after the tender process is restarted when AEG struggles to raise the necessary funds.

• Dutch theatre producer Stage Entertainment launches a new division to focus solely on international touring.

• LG Arena in Birmingham (UK) and local police confiscate more than £10,000 (€11,400) of bootlegged merchandise at a WWE show.

May• A California court rejects an appeal by

legendary music producer Phil Spector to overturn his murder conviction.

• Speaker manufacturer Klipsch signs a multi-year naming rights deal for Live Nation venues in New York and Miami.

• In the UK, Live Nation and Festival Republic announce that they will begin posting out tickets soon after purchase in an attempt to cut-down on fraud.

• Pollstar reports that a three-year partnership between Charmenko’s Nick Hobbs and Borek Jirik’s Berlin-based Transmusic dissolves with losses of “hundreds of thousands of Euros”.

• Live Nation partners with discount specialist Groupon to form a new concert ticketing site – GrouponLive.

• Organisers of the UK Festival Awards announce that this year’s festivals will be judged by journalists attending each festival

anonymously and marking them on set criteria.

• The principal associations representing the UK’s live music industry unite to form the UK Live Music Group, with its nominated chair, Paul Latham, taking a seat on the board of trade body UK Music.

• Former See Tickets MD Nick Blackburn is announced as the head of CTS Eventim’s UK operation.

• Azerbaijan wins the 56th Eurovision Song Contest with Running Scared at the event in Düsseldorf ’s Fortuna Arena.

• Galaxy Macau opens for business on Macau’s Cotai Strip. Owners of the HKD 14.9billion (€1.4bn) development pledge to increase the number of concerts by foreign artists.

• US ticketing company Eventbrite (which integrates social media and mobile) announces a $50million (€35m) influx of venture capital finance.

• Demand for downloading Lady Gaga’s latest album Born This Way for 99cents from Amazon brings down the online retail giant’s servers.

• Irish promoter Denis Desmond is paid the $2.95m (€2.08m) in damages he is owed for a cancelled Prince show in 2008, just as the artist announces two European festival shows this summer.

• The ticket service run by German promoter Karsten Jahnke is voted most customer-friendly in the country by a top consumer body.

• Gil Scott-Heron dies in New York at the age of 62.

June• Moroccan activists carry out a

campaign of online and street protests against the government and sponsor-funded Mawazine world music festival, describing it as a “waste of money”.

• Banks bailout beleaguered UK music retailer HMV with a £220m (€251m) refinancing lifeline, subject to high exit fees and interest charges of between £10-15m (€11-17m) per year.

• The insurer of Michael Jackson’s This Is It shows sues AEG Live and the late singer’s estate to nullify the policy it issued for the string of 2009 London shows.

• UK ticket operation CrowdSurge sells what it claims is the first ticket via a fully integrated Facebook app.

• Two festival-goers die of heat-related conditions at US festival Bonnaroo after temperatures at the Tennessee event stretch into the 90s.

• Simon Fuller and ex-Island Records boss Chris Blackwell announce Blackwell Fuller, a new venture focussed on monetising artist content.

• The Dutch government cuts its arts budget by 30% just before VAT in tickets rises from 6% to 19% on 1 July.

6 IQ Magazine

July 2011

News

Below: XL Video’s Des Fallon who sadly passed away in May at the age of 40Top Right: Eddie Van Halen Far Below Right: Jonathan Brown

News

Australian promoter AJ Maddah is testing the theory that there’s an

insatiable demand for the harder side of live. Maddah, the mastermind behind

A u s t r a l i a ’ s b e h e m o t h S o u n d w a v e touring fest, is launching the S o u n d w a v e Revolution festival.

Van Halen, Alice Cooper and Bad Religion will headline the new event, which begins the first of five dates 24 September in

Brisbane’s RNA Showgrounds, and will play a host of non-traditional rock ‘n’ roll venues.

Social networking has played a big role in building the buzz for Revolution. Organisers whipped-up a frenzy when they discretely leaked names from the Revolution bill through Twitter ahead of the official announcement. Maddah was upfront about the considerable cost to stage Revolution, announcing on the micro-blogging site that he had stumped up

AUD$12.4m (€9.2m). The launch of Revolution

flies in the face of the general industry consensus that Australia’s festival circuit has already reached saturation point. That was proved wide of the mark when Staple Group’s Destroy All Lines launched the six-date Australasian hard-rock and alternative No Sleep ‘Til Fest in December 2010, which sold more than 40,000 tickets nationally, according to co-founder Jaddan Comerford.

Eighteen months after merging with Ticketmaster, Live Nation Entertainment (LNE) executive chairman Irving Azoff is reportedly considering privatisation with the company’s largest shareholder Liberty Media.

According to the New York Post, privatisation is only one of the possible moves being discussed by Azoff and Liberty Media boss John Malone. Currently

Liberty Media owns 20% of the company.

At its current price, $3.6billion (€2.5bn) would be needed to finance a buyout. News of the discussion saw LNE’s stock price rise 6%, then fall 3% and comes after LNE narrowed its Q1 losses to $48.5million (€34.2m) from a loss of $122m (€86,), over the same period in 2010.

Colombian record label Discos Fuentes and concert promoter AG Producciones, have become partners in a bid to cross-promote and develop their respective artists.

Discos Fuentes will now use AG to help promote and manage its artists – which include Latin Brothers, La Sonora Dinamita, and Osmar Pérez y los Chiches Vallenatos – while Fuentes will release

albums by AG’s touring artists, which include La Misma Gente.

The new partnership will initially focus on recordings and concerts around new soap opera El Joe La Leyenda, which is based on the life of Joe Arroyo, the Colombian salsa star. Arroyo is not currently signed to Fuentes but most of his catalogue was recorded with Discos Fuentes.

Aussie Festival Revolution

This July will see the Society of Ticket Agents & Retailers (STAR) launch a new Kitemark to help consumers identify legitimate ticket agents in both the primary and secondary markets. Designed to combat rising levels of ticket fraud, the campaign will involve posting a trademark hologram on all STAR member websites so that customers know ticket inventory has been authorised and is safe.

In order to include all the UK’s major primary retailers, STAR recently changed its terms and conditions. Previously, See Tickets was not a member because it refuses to refund booking fees in the event of a show cancellation.

According to secretary Jonathan Brown, the campaign will roll-out in two stages, with a trade launch on 4 July followed by a press and consumer launch in early

September. Sites will begin using the mark in July so that the public can identify it immediately after the consumer launch.

“The trademark will have legal protection,” Brown tells IQ. “Each will have an inscription on the logo to show its authenticity.” The awareness campaign will then continue with STAR working alongside other trade bodies and running online advertisements.

STAR Launches Kitemark

Live Nation’s Private Chats Colombian Discos Partner Up

News

8 IQ Magazine

July 2011

2012’s Olympic Legacy for Live Music

Following London’s 2012 Games, three new venues will be available to host live music events, bringing a new range of options for live music in the capital.

According to the Olympic Park Legacy Company’s recently appointed director of venues Peter Tudor, the 2012 Stadium, Multi-Use Arena and outdoor park in Stratford, East London, will all have the potential to host live music events from the spring of 2013 onwards.

“There is real potential for promoters and artists to

reach new audiences in East London,” says Tudor. “We are still looking at the different shows that the Multi-Use Arena will be able to accommodate, and there will be excellent transportation links developed as well.”

Tudor, who previously worked as senior director of sales at Ticketmaster and as general manager of Wembley Arena, says that following the games, the Multi-Use Arena will be the most versatile venue, with the ability to host seated concerts or shows standing

in the round with a capacity of 7,500.

It was announced in February that West Ham Football Club and their partner Live Nation would take over the 2012 Stadium after the games, but the decision is subject to legal action by football club Tottenham Hotspur and local club Leyton Orient. AEG, which had also bid for the stadium with Tottenham, is now said to be interested in operating the £300million (€342m) aquatics centre and 6,000-capacity handball centre.

Live Nation, which was chosen in February to run live entertainment during the Olympics in London’s Trafalgar Square and three city parks, may also be considering the outdoor park at the Stratford site which can accommodate up to 40,000 people.

Tickets and T-shirts for Tesco

Switzerland’s Paléo Festival Nyon is helping combat black market secondary ticket sales by encouraging ticket-buyers to use print-at-home tickets and by releasing larger numbers of day tickets every morning of the 19-24 July event.

According to Paléo’s head of press and media Christophe Platel, print-at-home tickets are more difficult to resell online because customers know they can easily be copied or printed multiple times. The 23,000-capacity festival will also sell 1,500 tickets each morning for that night’s events – an increase

from the 1,000 sold each day in 2009 and 2010.

Further safeguarding against secondary sales, on 4 May Paléo launched their sixth annual Bourse aux Billets platform allowing fans to sell or buy their tickets in a safe and fair environment. “The platform is just one of our ways to fight against the black market which is illegal in Switzerland,” Platel tells IQ. “It is a service to our

spectators – it allows people to get tickets if they couldn’t during the initial sale as everything was sold out in 48 hours.”

The National, Robert Plant, Jack Johnson and The Strokes are among the artists scheduled to perform at the 36th anniversary event, while previous headliners include Iggy and The Stooges, Massive Attack and the Arctic Monkeys.

UK retailing giant Tesco has entered the ticketing market, selling tickets for 23 open-air concerts through its Tesco Entertainment website. Coupled with several recent retail exclusives on artist merchandise (it already runs its own record label, with exclusive releases having included Simply Red and Faithless), it marks a move into the live music space for the world’s third largest retailer.

Partnering with concert production company the Liz Hobbs Group, the tickets are being sold for shows at various events at Jockey Club Racecourses across the UK between 8 June and 23 August. Ticket prices will start at £12 (€14) and will be capped at £33 (€38) with a maximum of ten per customer. All transactions are offered free of booking fees and credit card charges.

“We know customers want to buy tickets for live music events but are often faced with unexpected and additional fees,” says Tesco’s entertainment director Rob Salter. “We wanted an offer that was really simple – one ticket, one price, no hidden costs.”

In addition to offering online ticket sales, Tesco has moved into the merchandising channel, offering retail exclusives with several artists (see page 48). Meanwhile, Tom Jones, Scissor Sisters, James Blunt, Alexandra Burke and Scouting for Girls are among the artists scheduled to perform across racecourses including Haydock Park, Newmarket, Epsom Downs, Carlisle and Sandown Park.

Paléo Fights Black Market

Top left: Peter Tudor Centre: The StrokesTop right: Eilen Jewell

News

Shock Stops Live Arm

Coachella: So Good They’ll Run it Twice?

A reshuffle at Australia’s Shock Entertainment means that their fledgling touring division, Ragged Company, will be wound up, and the GM of the past two years, George Hatzigeorgiou has been let go.

Based in Melbourne, Ragged has toured the likes of Kitty Daisy & Lewis, The Charlatans, Eilen Jewell, Hawkwind, Rodney Crowell, The Hotclub of Cowtown,

Elana James, and in recent months, the American singer-songwriter John Grant. Hatzigeorgiou, who also handled national publicity duties for Shock Entertainment, is now “pursuing new opportunities” outside the Shock Entertainment family.

Shock launched Ragged Company in October 2008, taking its name from a lyric in the Rolling Stones’ track

Dead Flowers. The following month, Ragged brought The Charlatans down under for their first Australian tour. However, the touring arm was never seen as a core asset, and failed to find a foothold in Australia’s super-competitive live scene.

Founded in 1988 as an import business, parent Shock Entertainment came to symbolise innovation in the independent music scene. But it emerged last year that the group nearly went bust

with more than AUD $4million (€3m) owed to creditors, and the brand was essentially rescued when it was bought out by CD and DVD replicator Regency Media.

Having successfully trialled new RFID access control systems this year, Coachella Valley Music and Arts Festival is going one better next year by launching an entirely new festival format. With demand

mounting, organisers have announced that the 2012 edition will run twice, over back-to-back weekends –13-15 and 20-22 April – with an identical line up.

“We had too many people who wanted to go [this

year],” says Paul Tollet, the festival’s founder and Goldenvoice president. “It was hard watching people be upset that they couldn’t go last year because tickets were going for $500-$600 and that’s just not right.” A weekend pass for 2010 was $269.

Tollett told Billboard that he toyed with increasing the capacity, but was concerned it would spoil the dynamic of the Indio, Californian event. “I didn’t want to ruin the show by putting 40,000 more people in per day,” he said.

News

10 IQ Magazine

July 2011

Production Sector Faces Consolidation

GO for Green Group

A series of recent mergers, acquisitions and partnerships in the production world points to the beginning of widespread consolidation of the sector, according to some industry experts. The statements come after a number of smaller owner-operated companies were snapped up by multinational outfits over the last year, operations that are increasingly offering one-stop shop solutions.

Last month saw New York-based Production Resource Group (PRG) announce the acquisition of Nocturne Productions, a leading concert touring video production company that has previously worked with Lady Gaga, Paul McCartney, Bon Jovi, Madonna and Elton John. The past year also saw PRG acquire Germany’s Showtec Beleuchtungs, Procon (formerly ETF Event Engineering), and Belgium’s EML Productions. “Our companies have been on the same tours and shared clients for years, so combining forces is a logical next step,” says Nocturne’s co-president Bob Brigham.

In April, three leading audio rental companies in Italy came together to form

All Access. The new company has made a significant investment in Martin Audio’s Multi-cellular Loudspeaker Array and plans to compete with it on an international

playing field. And in May, Pennsylvania’s Tait Towers announced a strategic alliance with staging giant Stageco when the two companies opened a joint London office in time for the 2012 Games. “It’s a natural collaboration of our relationship because we now have an office together in Manheim, Pennsylvania, just outside Lidditz where our main office is,” says Tait’s president James ‘Winky’ Fairorth. “It made sense for Stageco to have a

presence there as well because we’re constantly collaborating on shows.”

The ongoing increase in multinationals and companies forging increasingly close alliances is

allowing for significant cost-cutting on some productions. Australian pop princess Kylie Minogue’s current Aphrodite: Les Folies tour (see IQ Issue 35) has taken advantage of this new opportunity by using only two companies for the tour, which spans Europe, Australia, Mexico and South Africa.

Tait Towers was able to provide the aquatic-themed Aphrodite tour with all water effects, staging, set, automation and performer flying, while all rigging,

lighting, audio and video was provided by Montreal-based Solotech – making Kylie’s tour the first international production of its size to strike such a deal. “There are economies of scale with them providing all the personnel and all the equipment,” production manager Kevin Hopgood said.

In Belgium, Ampco Flashlight Group – itself the product of a merger between two leading rental companies – also offers a one-stop shop service. And while others stress the importance of relationships and track record, marketing director Marcel Albers says: “If you look at the music industry as a whole, you see that in a lot of territories worldwide, 80% of business is taken by four major companies. If you look at agents and promoters, that’s also the case. It’s a fact that you’re either small, and very small; or big, and very big.”

“It’s an inevitability,” agrees John Penn, MD of SSE Audio (who oversaw the merger between SSE and Canegreen in August 2008). “It’s the way that things are going and a commercial reality.”

The Green Operations (GO) Group, the independent think tank created to encourage the European event industry to become greener, held its first workshop from 23-24 May in Amsterdam.

A total of 35 festival managers, promoters and sustainability experts from

eight European countries descended upon both the ID&T headquarters (the Dutch entertainment enterprise acting as co-host) and the Amsterdam Arena for the event. The first day of the workshop was dedicated to energy related issues, while the

second day was geared towards effective audience communication tools.

The GO Group was initiated in November 2010 by Bucks University, GreenEvents Conference, Green Music Initiative, and Yourope with the aim of highlighting the importance of sustainability within the music festival and event

industry. Participants included Festival Republic, WWF, Melt! Festival, Øya Festival, and Roskilde.

The GO Group is currently planning the next workshop for spring 2012, and will act as a partner for the second GreenEvents Europe Conference in Bonn, Germany, from 2-4 November 2011.

Above: Kylie Minogue live in Paris. Photo: Christie Goodwin 2011 Right: Of Montreal

News

Festival Promoters Go Abroad

A number of new entrants and major moves are keeping the French concert business in a state of flux. At the beginning of May, French investment company Fimalac Développement announced its acquisition of a 40% stake in the concert company Auguri Productions. Fimalac already has a 40% stake in both Gilbert Coullier Productions, the market leader in the French concert business; and Groupe Lucien Barrière which

promotes approximately 2,500 shows annually via its subsidies Barrière and Fouquets.

Also entering the live market is Lagardère Media Group (LMG), which opened a new division, Lagardère Unlimited Live Entertainment, in April. The company, which last year turned over €7.9billion in 2010, will promote tours and concerts and already holds a related stake in the Zénith concert hall in Paris. LMG’s entrance into the

market is considered as a move that could easily drive consolidation in the market.

Meanwhile, record labels, which are historically active in the live business – as evidenced when Warner Music bought Camus Productions in 2008 and Sony music purchased Arachnée Productions two years ago – are no less busy. Independent distributor Discograph just launched its own booking department (D-Tour); and the largest French independent label

Wagram Music launched a new website last month, Wspectacle.com, adding a booking department with two agents.

The ticketing industry in France has also seen the arrival of the corporates of late with Live Nation’s purchase of No 2 ticketer Ticknet in November last year. And at the end of 2011, Vivendi Universal took over ticketing provider Digitick, paying €45m for the e-ticket market leader.

French Market Gets Busy

TWO UK FESTIVAL promoters setting up shop across the Atlantic this summer is said to be part of a wider trend as the increasingly swamped festival market forces organisers to look beyond borders.

This August will see Secret Garden Party founder Fred Fellowes introduce the 5,000-capacity boutique festival Escape to New York, while Festival Republic’s Melvin Benn is organising a

new 50,000-capacity festival in Florida, Orlando Calling, in November. Orlando Calling is his second attempted foray into the US after 2008’s Vineland Festival failed to launch.

According to Benn – the UK’s leading festival promoter whose other international events include Electric Picnic in Ireland, Hove in Norway and Berlin Music Week – the decision to go stateside is not a unique trend on the rise,

but a natural step for experienced promoters working in crowded markets.

“It’s not only the British going to America – German promoters are starting events in Denmark and American events are expanding,” he says. “Lollapalooza has expanded into Chile and wants to go to Europe next year. The UK and German markets are both very crowded so it’s hardly surprising that we would look to expand overseas.”

Fellowes had no plans to expand to the US until a chance meeting at SXSW led to contacts with the Native American tribes on New York’s Shinnecock Reservation. Normal US permit laws do not apply to Indian reservations, meaning that despite some large insurance premiums, Fellowes can run a European-style festival with alcohol and tobacco consumed in the open.

“The decision to expand

came as the result of a chance contact with the Indian tribes in Southampton, USA. It is a unique legal position on a reservation which made it a very attractive position,” says Fellowes, who admits that he’s wary about entering the world’s largest entertainment market. “It’s not the easiest place to break. Many people have found licensing an event in America very challenging and a catalogue of events have fallen foul this year.

“Still there is a huge chasm between us and Coachella (75,000) and the Burning Man (51,000) festival where we need to build up our position to,” he says.

Escape to New York headliners include Best Coast, Patti Smith, Edward Sharpe & The Magnetic Zeros, and Of Montreal with tickets ranging from $100 (€70) to $289 (€202). Acts for Orlando Calling will be announced later this month.

12 IQ Magazine

July 2011

PRS for Music economist Chris Carey says to look beyond the numbers...

Live Still the Driver

Comment

35%

60s

19%

6%

40%

Pollstar’s Top Grossing Tours of the Decade, by Age

of Lead Singer in 201150s 40s 30s

2010 was a blip, and 2011 will bounce backAfter incredible growth over the last decade, UK live music revenues dipped in 2010 with revenue from primary ticket sales falling 6.7% compared to 2009. Whilst primary ticket sales are a key driver of live music revenue, this single statistic needs to be considered in context.

The good news is that this fall is a function of supply, not as a result of falling consumer demand. There was a relative shortage of bands on the road in 2010 and some of those on the road (sensibly) opted to play smaller venues in order to limit their risk. When the big bands get back on the road and they start playing the bigger venues, the demand is there and revenues will bounce back. More good news is that not everyone experienced a drop in 2010. At The Great Escape festival in Brighton (UK), Jessica Koravos (MD, AEG Live) was quick to point out that revenues at The O2 arena were up in 2010, and she was expecting further growth in 2011.

2010 was a difficult year for the UK recorded music industry too, which saw trade values fall by 11% in the year, against the backdrop of a strong 2009. What was interesting to note for recorded music was that five of the official bestselling artist albums of 2010 were not released in 2010. (Michael Bublé’s Crazy Love; Paolo Nutini’s Sunny Side Up; Florence and the Machine’s Lungs; and Mumford & Sons Sigh No More were released in 2009, with Lady Gaga’s The Fame first released in 2008.)

It would be too easy for the live industry to look at its relative strength and rest on its laurels. At ILMC 23, Flemming Schmidt (CEO, Live Nation Denmark), was at pains to warn against complacency and overconfidence, stating that live music risked “being where the labels were ten years ago”. The live industry’s imperative to build for the future is captured perfectly by Deloitte Research charting Pollstar’s Top Grossing Tours of the Decade by age of lead singer, and revealing that 40% will be in their sixties this year, with a further 35% in their fifties (see chart).

Festivals: Growing in value, reach, & seasonEuropean festivals performed strongly in 2010,

with IQ’s European Festival Report showing growth in supply (16% growth in festival capacity) and in demand (6% growth in attendances). In the UK, the number of festivals grew 16%, with festivals accounting for 25% of UK ticket sales in 2010.

Not unlike the football season, the festival season seems to start earlier every year and go on for longer, and we have yet to see what impact it has on the rest of the live music market; and whether the two can grow together.

Tickets: Purchase decisions & price signallingTicketing is a complex area, and from an

economist’s 30,000-feet perspective there are some interesting dynamics at work.

Broadly speaking, there are two types of live music ticket buyers: the ‘die hard fans’ who will always prioritise time for a gig and queue for a ticket, and the ‘late arrivers’ who wait to seek out a ticket and principally drive demand in the secondary market.

However, the introduction of widespread secondary ticketing means that two key market signals (price and quantity) are increasingly difficult for consumers to understand. The ‘face value’ of a ticket does not always reflect the price at which a ticket can

be purchased and ‘sold out’ simply means the search moves to the secondary market.

This growing uncertainty is difficult for the market to maintain, and could go some way towards explaining the difficult experience of the US live music market in 2010. It is certainly important for the live industry to help consumers make informed choices, and particularly to encourage them to buy sooner, rather than later, in order to ease the cash flow burdens and mitigate risk.

Finally, we often (understandably) hear outcry at tickets selling at well above face value. However, I suggest that the tickets that sell for less than face value are a far greater concern for the health of the live music industry, as the cheap tickets bought at the last minute may deter consumers from paying face value next time around.

Above: Source - Deloitte TMT Predictions, 2011

Comment

The Winds of ChangeVeteran promoter Shuki Weiss calls for more

understanding of the needs of Israeli music fans…

The Middle East is seeing some turbulent times, as it has for 63 years since the state of Israel was founded to provide a home for a people that know a thing or two about persecution. Regional politics has never been trickier, but over the last few months it at least seems like democracy is trying to shine a little light on the area.

We’ve seen questionable leadership in several of the world’s leading nations this last decade (without pointing any fingers), and that didn’t stop artists from continuing to play for their fans, and from expressing their opinions whilst on stage. From my particular point of view, as an active promoter for 35 years – in Israel for the most part – we’ve been waiting for this particular wind of change for some time now.

For as long as I can remember it was the sun, the beaches, the sights and the audiences’ passion for rock ‘n’ roll that brought artists to Israel, even if over the last few years, unexpected and changeable aspects have made such visits a little less stable. That said, Israel remains an exotic, modern, and democratic destination, with a warm, enthusiastic crowd hungry for music and eager to express their love for the artists that ‘dare’ to visit and play in their country, paying them the respect they deserve. The touring acts that come this way recognise this loving audience – often describing them as one of the best crowds they’ve seen.

Recently, several touring artists unfortunately chose to pass on Israel, or even worse, to cancel confirmed shows, under pressure from organisations looking to delegitimise Israel and its current policies. I say ‘unfortunately’, not because I necessarily agree with current Israeli policy, but rather because these cancellations do nothing to affect policy, ending up punishing and hurting the fans. These cancellations have hit the local music industry hard, causing enormous financial damage to promoters and many others employed in the live music business.

In fact, we’re seeing cynical use of the arts and entertainment to advance political goals, and, controversial as this may be, on a personal level, I do not see the justification for this. I’d much rather see music used as the means of communication we know it can be: bringing people together under an umbrella of culture and ideas.

Over the last few months, talking with colleagues in

different parts of the world I’ve been happy to discover that most of us agree that it is crucial to allow the artists they represent the freedom they need to create and to connect with audiences wherever they deem fit. Playing Israel is not a political decision, or a question of conscience. It is a matter of establishing a relationship with the fans, and inspiring them to do good – as music so often can. In Israel, a few weeks ago, British novelist Ian McEwan told Reuters: “If you didn’t go to countries whose foreign policy or domestic policy is screwed up, you’d never get out of bed… No, let us come and engage, keep talking. The worst thing that is going to happen is when everyone stops talking.”

Indeed, over the last few years we’ve worked on projects looking to inspire positive change by influencing music fans, such as artist workshops in Israel and the West Bank with colleagues from Palestine and the international community teaching kids to use music as dialogue rather than let hatred and fear rule, or simply live music events giving artists the stage in order to pass on their message, whatever that message may be.

Israel is blessed with some of the world’s most unique venues and rising standards of equipment and expertise have recently helped establish a wonderful reputation for this market. Also, some of the industry’s leading companies have now set up shop here, such as Eventim Israel, who

bring the latest global ticketing technology and know-how to the country, improving the fans’ concert-going experience and the promoters’ real time access to information.

This has also enabled us to market more tourist packages throughout Europe and the world, inviting the international community to see their favourite artists in some very unusual and stunning venues.

In September, we’ll have 3,000(!) tourists from Brazil travelling to see Roberto Carlos play in Jerusalem’s Sultan’s Pool – beneath the Tower of David, with the walls of Jerusalem’s old city as a magnificent backdrop.

In a region desperately looking for answers, the arts should be leading the way; inspiring change rather than ignoring reality. Peace begins with education, not delegitimisation.

Our hope is to be inspired through connection with the world’s artistic community.www.shuki.co.il

14 IQ Magazine

July 2011

Derek Smith, Association of Chief Police Officers Lead on Charging for Policing looks at the relationship between the festival industry and the Police in the UK…

On the Beat

Comment

Survival...

You know – most of us like most of you! The perceptions of the police from festival organisers (and vice versa) are often shaped more by urban myth than reality and, on both sides, are more influenced by history than the present.

Let’s be clear: the festival industry is growing. Attendance at festivals in the UK has been increasing quickly in recent years. The number of festivals has also grown to well over 700 for 2011. As a result, the festival industry is a thriving commercial business. The top 20 festivals generate some £500million (€575m) – including tickets; food and drink; memorabilia, and accommodation. It is clearly very successful. But there is a range of threats and risks that continue to require police input. And these have changed over the years. There has always been less of a tribalism threat for public order than has existed within football, but as the number of festival-goers rises, so there are safety and crowd control issues that must be addressed.

Similarly, the ‘free spirit’ days of old have changed in character. There are still undoubtedly risks related to drug selling and using at festivals and some public order issues related to alcohol. Equally, on the sites there is likely to be the normal range of personal crimes. These can cover the full spectrum of offences but for the most part, they are thankfully, low level. The majority of people go to the events to experience being at a festival and to see and hear their favourite performers.

As festival promoters and organisers, you have a number of issues and concerns:a) There is a wide disparity in the perception of the role of police and promoter. Some feel over policed as a result, not only onsite but outside. b) There is a wide disparity in the cost of policing involved and charged. National police guidance seems to be inconsistently applied. It is also true that forces are inconsistent in charging practices which leads to confusion. Some events that should be charged for are not.c) There is little negotiation – promoters often get told what policing is required. There is seldom any approach to risk mitigation that will help to offset the need for officers. This could be cost substitution where equipment (eg CCTV cameras) or stewards are used to reduce

potential police costs.From the service’s viewpoint, all of these events

mean additional preparation and policing. Each festival represents a new policing demand every time. There is no magic formula to deal with the relative risks at festivals. They reflect different numbers of different attendees at each event and each is affected by its own geography. This not only affects the sites but often the immediate communities. We shouldn’t underestimate the impact that festivals can, and do, have on neighbours.

The limits of police cost recovery have been tested in the past and the service accepts that even where there is a

policing requirement that stems from the existence of the event – where it is remote from the site – the

policing may not be chargeable.Thankfully, the number of arrests and public

order incidents at festivals remains relatively low. However, there needs to be an acceptance of the relevant roles that are required to deliver safe and trouble-free events. And this should be on both sides! An event that results in very few incidents requiring police intervention may be considered

by the organisers to be over-policed, but it must be remembered that a police presence acts as a significant deterrent. A delicate balance needs to be struck regarding police numbers that must include a good degree of professional judgement. The requirements can be and should be honed by

proper consultation and planning, and should be carried out on a risk-based approach, with agreement

on what is the best way of dealing with each risk. In most significant events, policing will be part of

the solution but it need not always be the whole solution. There is scope for alternative ways of addressing some risk. Policing is an expensive resource. Nobody has ever complained about being undercharged(!), but being under-policed at times could be a tremendous risk to the public.

I want the service to engage properly and consistently with the industry professionals. The national guidance has been amended to allow a proper dialogue to take place that will try to eliminate some of the inconsistency currently seen. I hope that it can help shape the future approach to what is a very successful entertainment industry for the country. I also hope it encourages perceptions to change.

We do like you – really.

My background is in radio – Radio 1, Radio 2 and GLR, working with Johnnie Walker and Bob Harris and hosting my own show on various stations, but I became an agent in 1999 having promoted gigs in small clubs in London (The 12-Bar Club and The Spitz). Leaving the big city in 2002 to live in Suffolk I identified a gap in the market for quality live music, reacquiring the promoting bug in 2004, and then using the 120-capacity High Barn in Great Bardfield, Essex. Now, as Movers & Shakers Promotions we promote the likes of The Ukulele Orchestra of Great Britain, Bellowhead, Ralph McTell, Show of Hands, and Al Stewart, throughout the county.

The smaller end of the market has never been easy, but the last two years of economic problems and restrictive licensing laws have been the toughest, with established promoters, venues and agents not taking any chances. This has opened the door for amateur promoters and with the internet, lesser known musicians and bands have found new ways of booking tours, over-saturating the market and driving down ticket prices. There is still an appetite for smaller gigs but with more competition, acts that tour too often are suffering and punters are attracted by the cheaper ticket to see something new or to save money for the special high priced ticket in exotic venues.

Smaller venues and promoters have had to adapt and many have become very savvy. Some operate early-bird tickets to entice punters to purchase in advance as some are still waiting until the last minute for concerts they think won’t sell out. You can easily detect when there is a buzz on an act and those shows sell out fast. Most now use online ticketing, with systems like WeGotTickets seeming to be the most user-friendly as the punter, not the promoter, pays the commission.

But as the giant promoters still somehow manage to lose enormous sums of money, the smaller operators are still out there, and whilst we have seen a large number of venues close and festivals cancel over the last few years, we have also seen many flourishing. I would say that the present period could certainly be described as Darwinian during which the good ones are managing to survive.

Survival...Bob Paterson of BPA Live on life for the UK’s smaller regional agents, venues and promoters...

“ Smaller venues and promoters have had to adapt and many have become very savvy.”

16 IQ Magazine

July 2011

A AH B H

A AH B H

Social media has evolved enormously in two years, but its full impact on live music is yet to be discovered, argues Charlotte Mceleny...

PEOPLE POWERlmost two years ago there was a lot of talk about social media, as MySpace was ousted as global frontrunner by Facebook, but while it excited

many, a large shadow of doubt hung over the seemingly fickle audiences. Since then, there has been a seismic shift in the attitude towards social media by brands and companies, which has in turn started to bring in a sizeable increase in investment.

Fast forward to the end of 2010 and spend on social media advertising topped $2.1billion (€1.5bn) worldwide, according to media analysts BIA/Kelsey, and is expected to grow to $7.7bn (€5.3bn) by 2015. No longer an afterthought, most companies, celebrities, musicians and organisations have in some cases opted against launching websites altogether in favour of a Facebook page. For most companies, the past two years

have been a process of getting the basics in place and then experimenting. But the next phase will see integration and, according to experts, the most exciting and effective use of social media will come from innovations in mobile, advertising formats, e-commerce, video and data.

esitation over adopting social media has been based around concerns for consumers, particularly around technology such as mobile.

For live music, the increasingly close tie between social media and mobile has only intensified its importance as it helps to link social media activity with physical events and venues. But while check-ins, QR codes and near field communication technologies have been nascent in the past, that giants such as Facebook are now wading into the game with their own versions can only help to

A AH B H

“We are of the view that social media is not an add-on. Our mindset is that social has to be a part of everything.” – Steve Jenner, Kilimanjaro Live

Social Media

encourage mainstream adoption.Dominic Cook, a former marketing and content director

at MySpace (after 12 years in the music industry at Virgin and EMI) has now set up social media marketing and social tech PR agency, 33Seconds. He says that while the music industry has always been more tech-savvy than many, it has yet to get to grips with localisation and targeting.

“Bands in general have always been forward thinking in this space,” he says. “From the late 90s, bands were building online communities and talking direct to their audience. MySpace helped take this to a new level and Facebook, Twitter and YouTube have taken it even further. Other industries can learn a lot from the music industry about how bands connect to their fans and give them a reason to engage and build a two-way relationship.”

Advanced customer relationship management systems and data mining techniques have changed the field radically over the last 18 months, with many promoters, ticketing companies and artists are now beginning to deliver targeted messages and product to fans. But a common issue for a lot of social media activity is that there needs to be a steady flow of communication in order to maintain a relationship with consumers. This is something festivals or venues, with strong communities or narrow genres, are able to do with ease, but for venues that one night have a pop act but the next have classical, it is not an easy balance to strike. The commitment to creating the content and assets, beyond posting event links and information, is a challenge for some because the broad variety of music and tastes makes it incredibly transient. The more niche the offering, the easier it is to relate.

Sonisphere festival, run by Kilimanjaro Live, is one of the biggest festivals on Facebook with over 600,000 fans worldwide. Steve Jenner, digital director of the company and founder of Virtual Festivals says social media is the company’s primary method for disseminating news and updates to its audience. “It is basically used as the first port of call for getting content out as you instantly get 130,000 in the UK, for example, seeing it in their newsfeed,” he says. “As a free source, you cannot beat it. We are of the view that social media is not an add-on. Our mindset is that social has to be a part of everything.”

Ministry of Sound (MoS) runs a large majority of its

artists’ social media activity and says that utilising the increasing amount of assets that record companies hold is key in helping to promote live shows. Lucy Blair, digital marketing manager, says: “At the moment we help with social networks for our artists. A lot of them tend to tweet themselves and I tend to do the Facebook pages and blogs. For us, live music is an increasingly important part of our business.”

lair reports that some promoters are “savvy” to using social media, while others “aren’t so fussed”. But with ever-growing demand from

fans for multimedia content, she says, “we have a wealth of content we can share, so we try and send over videos about what the acts are up to, for example, to help promote the event. The more you can do to convey the personality of the artist the better... push artists to do as much as they can.”

Better collaboration between artists, management, labels and promoters is a key issue, but even once the content that will help drive engagement with fans is established, the large range of social media sites and social music services is growing and more complex than ever. According to web measurement firm Nielsen, Facebook is the dominant platform by a long shot. Globally, Facebook has over 600million users. Nielsen figures suggest that in its global statistics (which include the US, UK, France, Germany, Spain, Italy, China, Australia and Brazil), Facebook has 280million active monthly users, representing a reach of 63%. The social networking behemoth is still growing at a rate of 25% year-on-year according to stats, while Twitter has only grown 23% in the same time, to reach 52million users worldwide.

“Bands have a number of platforms and tools that can help them reach their fanbase and ‘socialise’ their gig dates, their music, their videos, their products,” says Cook. “SoundCloud, Topspin, Bandcamp, ReverbNation, Music Glue are all tools and platforms that help bands reach their fans more effectively. For fans trying to discover live music, Facebook and Twitter are still leading the space in terms of volume and reach. While sites like Songkick are trying to provide a focused service.”

Facebook has recently launched a Facebook for Musicians page, which includes tabs to help bands and venues get to grips with using the platform. A spokesperson for Facebook tells IQ: “Music has always been social. We all grew up sharing mixed tapes or CDs, going to concerts and movies with friends. Those experiences and conversations with friends are now being brought online, and Facebook is providing the platform. From up-and-coming bands, to chart superstars, Facebook provides the tools for any musician to create an engaging social experience.”

18 IQ Magazine

July 2011

Top 10 Music Sites, ‘global’ unique audience (9 key markets*) from home and work computers, March 2011

Mar-11 Mar-10

Rank NameAudience

ReachActive Reach

Audience ActiveReach

YOY audiencechange

1 VEVO 54,157,358 12.30% 2,162,085 0,51% 2405%

2 AOL Music 23,146,367 5.26% 28,588,709 6.69% -19%

3 Yahoo! Music 16,983,043 3.86% 21,415,427 5.01% -21%

4 MTV Networks Music 14,297,823 3.25% 13,727,421 3.21% 4%

5 Terra Musica 13,678,796 3.11% 10,745,105 2.51% 27%

6 Jango Music Network 10,499,631 2.38% 11,155,302 2.61% -6%

7 CBS Interactive Music Group 9,692,132 2.20% n/a n/a n/a

8 Pandora.com 7,897,287 1.79% 5,267,383 1.23% 50%

9 iG Música 7,696,069 1.75% n/a n/a n/a

10 Sony Music Entertainment 5,764,098 1.31% 6,618,677 1.55% -13%

A AH B H

One site that is on the rise, particularly in use by my music brands is Tumblr. Nielsen figures reveal that the site has increased its global audience by 189% in the past year, from 9.18million in March 2010 to 17.38million in March 2011. Amy Kean, director of social media at media and advertising group Havas Media, says, “Tweeting can restrict creativity so Tumblr is a good alternative.” The link between Tumblr and music is getting closer as the blogging platform announced in June that it was allowing SoundCloud users to directly record and upload their music. Similarly, SoundCloud has also linked up with Songkick, tying the connection with recorded music to the live experience.

In February, SoundCloud announced it had reached 3million users and David Adams, head of content and music relations, says, “our players can be embedded across the web and connected to third party applications. So users may be on SoundCloud, listening to a SoundCloud player on an artist’s site, or streaming a track via SoundCloud on an artist’s app; we put the audio at the heart of how fans research and discover acts.” Indeed, the SoundCloud and Songkick collaboration is just one way in which social media is evolving beyond a tool to publish and promote gigs, to being a link between real sales and physical experiences.

White label ticketing company CrowdSurge claims to have just sold the first ticket in Facebook, and currently has dates on sale for the likes of Kaiser Chiefs, White Lies and Coldplay. Founder Matt Jones, says the company has spent over six months planning the Facebook application which allows consumers to purchase tickets without leaving the social media platform. “The response from the industry has been good – it has little barriers to entry and you can share events and purchases directly from it with friends,” he says. “White Lies initially launched in

the UK but will now follow in the US, while we are now rolling it out worldwide and for merchandise.

“You get people when they are most receptive,” he continues. “If you look at an artist like Lady Gaga on Facebook, she has a huge captive audience but they need to be monetised. Direct purchases through Facebook make sense, particularly as almost 20% of online time is spent there now.” Jones also outlines how the CrowdSurge app gives users the ability to share and hold tickets for friends, allowing them to buy tickets in adjacent seats at a venue. But while such ideas are pushing the curve, the speed of evolution in the social media space is leaving many to catch up.

avas Media’s Amy Kean, who works with high profile brands including Domino’s Pizza, Santander, L’Oréal and Heinz, says there is an

increasing pressure to innovate in order to gain cut-through with audiences. “Everyone has done the housekeeping by getting their pages but we are now hitting a phase of that not being enough,” she says.“From a PR point of view, you’ll get no headlines for just having a Facebook page and consumers are not wowed by just another competition. There is now a pressure to go above and beyond to create something that has longevity, facilitating social occasions. And a page is not an occasion.”

Kean highlights a recent campaign by Heineken which created Bluetooth bottle openers that automatically created an event on Facebook once a beer was opened. The branded event then invited people to join in having a beer, and the event with the most attendees each week won a free case to enjoy together the following week. And with engagement through social media increasingly coming from events and offline situations, the role of the mobile phone is growing rapidly.

Top 10 Music Communities, global unique audience (9 key markets*)from home and work computers, March 2011

Mar-11 Mar-10

Name AudienceActiveReach

AudienceActiveReach

YOY changein audience

Facebook 280,333,570 63.67% 223,897,157 52.38% 25%

Blogger 119,514,370 27.14% 110,982,968 25.96% 8%

WordPress 56,879,947 12.92% 49,547,834 11.59% 15%

Twitter 52,276,383 11.87% 42,632,241 9.97% 23%

Myspace 34,707,981 7.88% 60,898,286 14.25% -43%

LinkedIn 31,092,260 7.06% 23,305,579 5.45% 33%

Orkut 30,246,759 6.87% 28,143,712 6.58% 7%

Tumblr 17,380,696 3.95% 6,007,966 1.41% 189%

Badoo 15,428,692 3.50% 9,187,629 2.15% 68%

Yahoo! Pulsa 12,985,233 2.95% n/a n/a n/a

A AH B H

“You’ll get no headlines for just having a Facebook page and consumers are not wowed by just another competition.” – Amy Kean, Havas Media

Social Media

Charts: Source - Nielson, March 2011*US, UK, France, Germany, Spain, Italy, Switzerland, Australia, Brazil

“Mobile is very exciting as up to 20% of our traffic now comes via a mobile device, so it is a big deal,” says Kilimanjaro’s Jenner. “As a result, all our sites are mobile enabled and we’re looking into launching iPad and tablet versions. QR codes are another way we are looking to expand our marketing. At the moment print ads are expensive and you have no way of telling how many people have seen them but QR codes can capture that by linking people and tracking how they arrive on your site.”

“It is extremely important to make the connection from the online to the physical space,” adds SoundCloud’s Adams, “If you are playing a show, why not privately send a track to all those who signed up to your mailing list from last night’s show? It’s not just a track that is your only promotional tool but other forms of audio can help push social media to promote your live show such as an audio tweet or audio tour diary. Max Roachford recently audio-tweeted during a sound check at the Royal Albert Hall to excite fans about the show that evening.”

longside mobile, the most talked about trend in social media at the moment is social commerce, or f-commerce, as the majority of

activity has so far been carried out on Facebook. There has been a broad reluctance to launch Facebook pages as there is concern from many companies that consumers have doubts about their privacy on the site, slowing adoption. Kilimanjaro’s Jenner says that although they have a Facebook store, they aren’t getting much use of it from consumers, although he believes that making the investment was important because consumers will warm to the idea of transacting on there. Similarly, UK music retailer and venue owner HMV has also set up a Facebook store but only sells CDs and DVDs as it does

not want to invest in the back-end support for tickets until sure of a bigger demand from consumers.

Matt Potter, online content manager at HMV, says he isn’t yet persuaded to add the full product range. “It’s not huge but we’re seeing it work already,” he says. “For big-ticket events, the most important place to announce is via Facebook, but we link back to the site because they go so quickly. We don’t want to give our Facebook followers a worse experience.”

HMV’s response highlights what an interesting stage social media is currently at for businesses. It has proved itself to be essential, yet the innovation and technology that will successfully monetise it are still developing. Because the barriers to entry are lower, it’s easy to be in the social media space, but as a promotional channel for promoters and artists, there are still more questions than answers. While Facebook is a dominant force in the market and will help to push key emerging trends for live music (such as location-based services) smaller start ups such as SoundCloud and Tumblr are also paving the way with easy-to-use services. The foundations have now been laid, and the future for social media is bright if not a little hazy. The challenge, however, will be to stay ahead of the curve; to innovate and arrive where consumers spend time before the competition.

Reaching the Peaks

Stuart Galbraith had been due to ski Mont Blanc the week before he spoke to IQ about his 30-year career. In the event, a cold he thought he had shaken off

came back with a vengeance when he reached altitude. So he went climbing instead. “This is where we were.” He waves a print of a terrifying spike of vertiginous rock on which a man stands, waving his arms. “That’s not me,” he notes. “I didn’t stand – I crouched.”

It would have made sense to ask why climbing this thing was somehow easier than skiing down the snowy mountainside. Instead, we talk about stamina, which, according to Galbraith, is what climbing is all about.“I don’t think it’s any coincidence that most really renowned climbers are in their 50s and 60s,” he says. “Psychologically and physically, I think you embody stamina much more as you get older. Life’s not a sprint by that point.”

Galbraith founded Kilimanjaro Live after he explosively left Live Nation not quite four years ago, naming it after another successful climbing

project. On the subject of stamina, the company he calls ‘Kili’ is clearly not just a means for a veteran promoter to keep his hand in. Described by Galbraith as a boutique promoter, Kili nonetheless sets itself big targets. Its travelling rock festival, Sonisphere, visits 12 markets this summer, with Metallica, Iron Maiden and Slipknot atop the bill. Kili is also the sole owner of Cardigan Bay’s wakeboarding and music festival Wakestock.

The company’s touring artists include Placido Domingo, Grace Jones, Josh Groban, Katy Perry, Red

Hot Chili Peppers, Metallica and Wilco. Among its rising acts are Marina and the Diamonds, Band Of Skulls, Wolf Gang, Mona, and Ed Sheeran. As a joint venture with AEG, Kili also puts shows into the European O2 network, bringing the Royal Horse Gala, Festival New Orleans and Ozzfest in recent years. These four areas: festivals, touring, artist development and O2 spectaculars account for the full Kilimanjaro portfolio. Having launched on 1 January 2008, Kili inched over into profit after a couple of years of anticipated losses, and from his corner-office sofa in Southwark, London, Galbraith professes himself very pleased.

“I am definitely having more fun now than I have ever had in my whole career, because the position I have got is very, very varied,” he says. “The good thing about Kili is it’s almost the best of both worlds for me, because we are able to be small and nimble, but equally if I need to draw upon the partnership with AEG, and the funds and global influence that they have, we can do so very quickly.”

Having promoted Simply Red, Def Leppard, Guns N’ Roses, U2, Simple Minds and AC/DC, with MCP; and Bon Jovi, REM and the Red Hot Chili Peppers in his Live Nation days, Galbraith might perhaps have picked up a couple of big clients and operated as that kind of boutique promoter. But that would be to disregard the festivals – from Monsters of Rock to Download, Wireless and Hyde Park – which remain his abiding passion. Festivals need small bands as well as big ones, and so the four-pronged strategy was, he says, a straightforward choice.

“For me, they are all interlinked,” he says. “I

Climbing mountains, competing in triathlons, building superstars and international touring festivals…there are very few promoters like Stuart Galbraith, writes Adam Woods...

Above: Galbraith in June 2011 Photo: Awais

22 IQ Magazine

July 2011

Stuart Galbraith

have been involved with festivals since 1984, when I started at MCP, and I did Monsters of Rock until 1996. Without sounding clichéd, it’s in my blood. I know how to run festivals; I like running festivals.

“But you can’t build a festival just on big bands. You have to have small bands, and you have to have a development team to book them. And there is no point me trying to book small bands, because I don’t eat, live,

sleep, breathe rock music, because I have got such a varied portfolio. People like [Kili bookers] Alan Day, Mark Walker, Steve Tilley and Sam Thomas do, and they know that genre collectively inside out.

“It was never, for me, an option, just trying to do big bands, because if you want longevity and you want a broad base, you have to break new talent. It is brilliant for me that we are involved with things like Ed Sheeran or Wolf Gang and probably 20 or 30 other acts that we are breaking through, and those are our festival headliners in five years time.”

There is no doubt that the shape into which Galbraith has moulded Kilimanjaro can tell us a lot about the parts of his career he has relished,

and those he hasn’t. Having taken the time-honoured route from university social secretary (at Leeds, from 1980 to 1984) to promoter at MCP, for 15 years thereafter, he himself isn’t shy to spell it out. “Kili is almost a combination of my previous two situations,” he offers. “MCP was just four of us, and we sat in a room, decided what we wanted to do and got on and did it, very, very quickly. Against the situation I ended up in at Live Nation, where we were obviously a

Ian Grenfell – Quietus Management9 Sept 2010, 8.15pmGrand Couloir, 3300metres, Mont Blanc descentSo we’ve been on our feet since 4am having had minimal sleep at the Tete Rousse Hut. Ninety mountaineers in four rooms, no running water, one toilet, dehydration, exhaustion, altitude sickness, elation. The snow is falling heavily now. It’s dark so we have head torches. The final danger is the Grand Couloir, a 100m pass, famous for stone-fall catching unsuspecting climbers. I’m first across. In an instant, a rock the size of a grapefruit hits me on the side of the head. It feels like a gunshot. I’m wearing a helmet so I’m shaken but alive. I look up and there’s Stuart – he’s just dislodged the rock unwittingly. Maybe he thinks he’ll get a better Simply Red commission rate with me dead.

I first met Stuart in 1992 on Simply Red’s Stars tour and since then we have worked on many arena tours with the band and occasionally conspired on other business ideas. I’ve not met a promoter without a healthy ego but in my experience Stuart doesn’t let that get in the way. Issues come and issues go but I don’t think I have ever doubted Stuart’s advice regarding the UK live music business.

As well as encouraging me to climb Mont Blanc, probably my hardest physical challenge so far, he cajoled me into doing a triathlon last year (he beat me in every discipline) .He is fiercely competitive, ambitious and open to new ideas. He can come across as hard-nosed but he’s as sensitive as the next man and is never happier than when he is talking about his daughters achievements.

Dean James – Mama GroupStuart is a good guy in an industry not known for good guys.

Rob Prinz – United TalentI first met Stuart in the early 90s when he was working for MCP and we did a string of Bon Jovi shows together in the UK. He seemed quite a fresh and ambitious young man and I could immediately tell he was someone you could rely on (except when he’s climbing a mountain somewhere and claims no cell reception!).

Roy Morley – Event LogisticsI worked for Stuart at MCP for ten years and he guided me through the hurdles of organising outdoor events. This was prior to the Popcode but at the time MCP pretty well led the field in pushing standards to a higher level regarding organisation and planning of outdoor events. This was an amazing opportunity for me and I’ve been using the knowledge gained ever since. In

Above: Summit of Mont Blanc, 9 Sept 2010 (L to r): Ian Ramage, Stuart Galbraith, Andy Perkins (guide), Ian Grenfell, John Cude and Tim Blakemore

“I am definitely having more fun now than I have ever had in my whole career.”

Stuart Galbraith

multinational with a staff of 120 by the time I left, and things took somewhat longer.”

This corporate heft isn’t the element of Live Nation that Galbraith wishes to capture at Kilimanjaro Live, but the sense of building something from scratch and by force of will.

When MCP was acquired by Robert Sillerman’s SFX in 1999, independent promoters that sold out to the incoming Americans were not popular people. “We were despised within the industry,” Galbraith recalls. “We had sold out and we couldn’t get arrested on a street level. Slowly but surely, we brought in a booking

team and we grew it. It was a case of plugging away for three years until we got the team built. You need to earn trust; you need to prove you are a good new promoter.”

MCP was part of a shopping spree by SFX that autumn which also included Barry Clayman Concerts and Apollo Leisure, as well as Mojo Concerts in the Netherlands, and Galbraith vividly recalls the hostility. “I remember the ILMC in 2000, when the topic of the entire conference was how SFX was the end of the live industry as we knew it,” he says. “And sure enough, it has certainly changed the face of live music, without a shadow of a doubt.”

Spectaculars aside, Galbraith derives his greatest satisfaction, he says, from building a team. Promoters such as Andy Copping, Steve Homer, John Dunn, Toby Leighton-Pope and others came up under his watchful eye in the Clear Channel/Live Nation days. “And now with Sam, Mark, Alan and Steve here, we are doing exactly the same again,” he says. “Each one of them has a musical genre they specialise in, and between them they make a great team. I like seeing the guys building their own rosters, helping them and providing a platform, the way I have done a couple of times already in my career.”

With AEG on board, with the funds and support that implies, and in a market that has long since reconciled itself to corporate creatures,

Kilimanjaro Live wasn’t born into the same adversity and ill-will as SFX in its British incarnation. All the same, Galbraith’s abrupt split from Live Nation in September 2007 hovers persistently over the conversation. It is something the man himself has never publicly discussed, but rumours have certainly flown: that Galbraith was sacked when he was found to have been planning an

Above: Terrorvision © PG Brunelli

between the ruthless efficiency we did occasionally manage to enjoy a few moments and I particularly remember going to pick him up outside the hotel in Milton Keynes (while we were looking after a couple of mad weekends with Guns N’ Roses and Metallica) at the appointed hour to find he’d been ‘playing golf’ all night. This match involved hitting the ball over the hotel...obviously a 100% success rate wasn’t achieved...

Jim MacDonald – G4SStuart is very much the successful entrepreneur – everything he touches seems to turn to gold; everywhere he goes success follows him. Wakestock has been growing since we got involved and to say that Sonisphere is successful is an understatement because it’s sold out where other festivals haven’t – it gives you an idea of the level of Stuart’s expertise.

Javier Arnaiz – Last Tour InternationalThe day before the first Spanish Sonisphere in Barcelona, John Jackson called to say James Hetfield had suffered

“You need to earn trust; you need to prove you are a good new promoter.”

26 IQ Magazine

July 2011

Stuart Galbraith

exodus to AEG (which never transpired); that he was given five minutes to clear his desk.

He isn’t about to dish the dirt now. Although he is happy to discuss Live Nation, his pride in his achievements there and its role in his current thinking, legal undertakings prevent him from discussing the split in all but the vaguest detail. “Obviously, the departure wasn’t perhaps as I wanted it to be,” he says. “In fact, it definitely wasn’t as I wanted it to be. The fact is, in building Kili, I will learn from the mistakes we have made elsewhere.”

He reveals that he thrashed out the terms of his joint venture with AEG in less than 48 hours, though he won’t say precisely when. “I was able to achieve within 48 hours with AEG what I had not been able to achieve with Live Nation in nine months,” is the summary he offers. And regardless of the birthing process, the company emerged fully formed. “The discussion with AEG was to set up the partnership with the four strands,” he says. “They made it very clear that their priority was filling The O2, and now filling their European network.

“The festivals help us do that. The development of new talent helps us do that. We can point to examples, whether it’s Katy Perry, who is already playing The O2 – in that particular instance, Live Nation promoted her there; we do the Midlands – or whether it be taking Ozzy Osbourne and Ozzfest in there.”

As Kili’s proud declaration of its boutique status

Left: Monsters of Rock at Donington

an injury during a show in Portugal and our show was at risk. The only thing we could do was keep our fingers crossed, and wait. It was a tough night but Stuart told me not to worry.

The next day, he said had found a solution. If the band cancelled, we would flip a coin to decide which one of us would announce the cancellation on stage in front of 40,000 fans... then he turned around and went for breakfast. Luckily, James managed to recover and the show was just perfect. Stuart must have known something, mustn’t he?!

Ewald Tatar – Nova MusicStuart is a very nice and straight forward partner and also a friend. When you speak to him you can be 100% sure that he knows what he is talking about and his personal opinion and know-how is always appreciated. He’s a very innovative businessman and promoter with lots of news ideas and concepts, which is definitely one of the secrets of his success.

Jordan Berliant – The CollectiveStuart is an incredible promoter and I look forward to the next 30 years.

Rob Markus – WME EntertainmentStuart has always been a fair and responsible promoter and handles situations with grace – probably all reasons why he has been around for so long!

Charlie Lister – William G Search LimitedIt was July 1993 when I first heard from Stuart, a date that’s hard to forget as it helped reshape my career. Nothing particularly unusual, just a fax asking for a quote for cabins and toilets. What was unusual for us was that it was for U2’s Zoo TV concert in Roundhay Park. It proved to be both the start of a lasting friendship between us and the beginning of our role as a major supplier to the music industry.

I’ll always remember Stuart ringing me the day before our first Monsters of Rock to say Aerosmith would like a toilet and shower fitting in their cabin. Still a little green I recall saying “But you didn’t order one.” The reply was typical of the man: “I know, but they insist on having one... get it sorted and welcome to the world of rock and roll!” It’s been both a privilege and fun to work with Stuart over the years and he was certainly instrumental in my involvement in the business and for that I will always be grateful.

When and if he ever leaves the event industry I’d urge him to consider a role as a trainer in advanced negotiating techniques. You know when he calls and mentions the great sold out gigs of the past, that

Stuart Galbraith

indicates, Galbraith is not terribly covetous of corporate scale. “I think there does come a point where scale becomes a restriction to momentum and actually provides inertia,” he adds. “It is not my ambition to see Kili become too big. We are currently 20 employees. I can’t see that we will become more than 30, maximum.”

Sonisphere has its conceptual roots in the Live Nation days, and Galbraith offers it as an illustration of what he can do now. The original plan was to take the Download model and put it on the road, but with established Live Nation festivals in so many territories, it made no sense from a business point of view. Sometime later, in the company of John Jackson of K2 Agency, he took the proposal to other overseas promoters and then to AEG, who provided the funding. “Sure enough, year one, we lost money; year two, we have just about broken even; and year three, we will be developing it as per our business plan.

“Working in partnership with a private company has given us much more flexibility and the opportunity to try things that are not possible within the rigid structure of a public company,” he concludes. The Sonisphere concept came together at the Led Zeppelin show in December 2007, when K2 Agency’s John Jackson, who had been thinking along much the same lines, proposed a partnership.

Three years in, Sonisphere still has to fulfil the global implications of its name, but Jackson says a number of promoters are already lined up for dates outside Europe. He takes particular pride in the rapid growth of the Knebworth UK flagship event, and credits the Kili team for much of its success.

“Stuart and his team run the best festivals I have ever attended, end of story,” says Jackson. “Everyone who attends Knebworth says what a fantastic atmosphere we have, and that has to be down to Stuart and his brilliant team.”

Galbraith speaks to his AEG colleagues, including AEG Live chief executive Randy Phillips, on a daily basis, and anticipates that the next 18

months in the life of the company will be particularly interesting. “[Incoming European CEO] Jay Marciano has just arrived, and he is three offices along, with the primary function of knitting together buildings and content providers in the AEG family,” he says. “Then there’s

Above: Rammstein set the festival alight Photo: PG Brunelli