investors’ day 2007

TRANSCRIPT

Investors’ Day 2007

Michael Reuther

Member of the Board of Managing DirectorsFrankfurt, September 20th, 2007

Public Finance

& Treasury: Transforming

public

finance

and managing the

challenges

of the

current

market

environment

2 / 26

Agenda

1. Figures H1 2007 Public Finance & Treasury

2. Public Finance

4. Outlook

3. Group Treasury

3 / 26

Key figures Public Finance and Treasury H1 2007Figures segment1)

1) Q1 2006 results

including

Pro-forma

integration

of Eurohypo

Operating

profitin € m

2006 2007Q1 Q2 Q3 Q4 Q1 Q2 H1 H1

Operating

RoEin %

Q1 Q2 Q3 Q4 Q1 Q2 H1 H12006 2007

Revenues

incl. LLPsin € m

2006 2007 2006 2007Q1 Q2 Q3 Q4 Q1 Q2 H1 H1

CIRin %

112134

67 82103

246

14891

44 47

11277

203

95

Q1 Q2 Q3 Q4 Q1 Q2 H1 H12006 2007

16.433.1

2006 2007

2006 2007 2006 2007

4518

37.6

16.2

Public Finance and Treasury 1. 2. 3. 4.

6.1

26.317.416.7

42.033.3

51.9

24.1

40.231.1

15.517.5

4 / 26

Agenda

1. Figures H1 2007 Public Finance & Treasury

2. Public Finance

4. Outlook

3. Group Treasury

5 / 26

Current

initiatives and next

steps

to optimize

public

finance business

within

Commerzbank Group

•

Capital Market Issuance Committee established•

Public Finance Management board established•

Active management of country limits across legal entities•

Cross fertilization of public finance entities

•

Coordination of risk profile for public finance entities•

Revision of Essen Hyp’s

business model

Current

initiatives

Next Steps

Public Finance 1. 2. 3. 4.

6 / 26

Public finance

market

worldwide

Global market

potential virtually

unlimited

547

USA

1,107

8,370

7,835

142

Russia

82

1,256 thereof

Germany

bn

USD

Public debt

including

social

insurance; Source: IMF, own

calculation

Public Finance 1. 2. 3. 4.

7,029

South Africa

Australia, New Zealand

Asia/Pacific

127

Japan

EU-15/EFTA

1,883

MEE, Turkey

Latin America, South America

7 / 26

Different business

model

positionings

in public

finance

Product specialist Local financier

•

Specific product know-

how

•

Deal-related acquisitions

•

Loan as introductory product, cross-selling

•

Main bank status based on local presence

Business approach

Portfolio manager

•

Focus on loan and securities business with high secondary market proportion

•

Centrally managed contacts with customers

•

Commission income

•

Low operating risks

•

Net interest income and commission income

•

High operating risks; market and credit risks

Earnings

/ risks

•

Primary net interest income and trading results

•

Market-

and credit-risks

Portfolio manager with focus on risk-return optimization

Product specialist incl. non-credit business

Main bank for public

authorities

Public Finance 1. 2. 3. 4.

8 / 26

Risk management

approach

Traditional mortgage bank approach Target risk management approach

No separation

of market, liquidity

and credit

risks

•

Public finance

business

as basis

for

expansion

of treasury

activities

•

Performance is

dominated

of interest

rate development

Separation of different risk

classes

Credit risk

management

Market-/liquidity

risk

management

Origination of dedicated

earnings

contribution

from

credit

risk

management

as main

objective

Additional clearly

separable

and identifiable

management

of market

risks

Public Finance 1. 2. 3. 4.

9 / 26

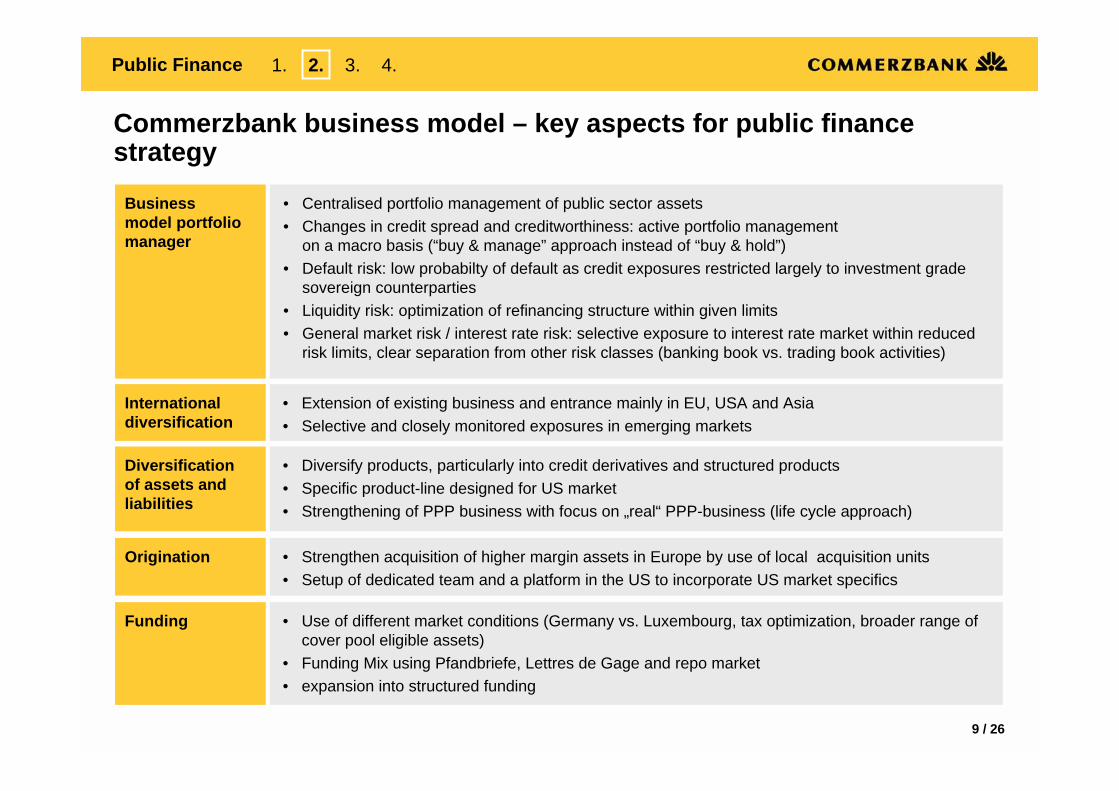

Commerzbank business

model

–

key

aspects

for

public

finance strategy

•

Centralised

portfolio management of public sector assets•

Changes in credit spread and creditworthiness: active portfolio management

on a macro basis (“buy & manage” approach instead of “buy & hold”)

•

Default risk: low probabilty

of default as credit exposures restricted largely to investment

grade sovereign counterparties

•

Liquidity risk: optimization of refinancing structure within given limits•

General market risk / interest rate risk: selective exposure to interest rate market within reduced risk limits, clear separation from other risk classes (banking book vs. trading book activities)

•

Strengthen acquisition of higher margin assets in Europe by use of local acquisition units•

Setup of dedicated team and a platform in the US to incorporate US market specificsOrigination

Business model portfolio manager

International diversification

•

Extension of existing business and entrance mainly in EU, USA and Asia •

Selective and closely monitored exposures in emerging markets

•

Diversify products, particularly into credit derivatives and structured products •

Specific product-line designed for US market•

Strengthening of PPP business with focus on „real“ PPP-business (life cycle approach)

Diversification of assets and liabilities

•

Use of different market conditions (Germany vs. Luxembourg, tax optimization, broader range of cover pool eligible assets)

•

Funding Mix using Pfandbriefe, Lettres

de Gage and repo

market•

expansion into structured funding

Funding

Public Finance 1. 2. 3. 4.

10 / 26

Path

to transform

public

finance

in Commerzbank Group

•

The current portfolio structure

is still dominated by traditional public finance business. Exposure is concentrated in OECD countries containing classical products such as securities and certificated of indebtedness / loans (SSD). Sovereigns account for a percentage of nearly 25%. Germany exposure reduced to 53% (2004: 70%) of total assets due to strengthened international diversification.

•

Setup of the market entities

Public finance strategy not set to offer operation or product range of a full service bank to its customers. However, it will generate direct acquisitions by maintaining decentralised

origination acitivities.

•

Active portfolio management Buy & manage strategy.

•

Extension of US business activities

Establishment of an acquisition team and dedicated platform in New York in order to generate assets and to implement new product-lines (i.e. tender option bond etc.) .

•

Credit derivatives

Setup of a CDS portfolio in high potential countries and increase of synthetic credit-

exposure to US Munis

(total return swaps).

•

Structured transactions / PPP

Increasing cooperation with Commerzbank (joint bidding), diversification of portfolio product base into structured transactions to increase risk return ratio. Selective acquisitions partially using own origination activities (multichannel

strategy).

•

High yielding public finance business within Commerzbank Group

Benefit from group affiliation, e.g. client relationships of the “Mittelstandsbank” and competence of Commerzbank’s

Corporates

& Markets unit to realise

cross-selling results and synergies within origination and transaction services.

•

Financial objectives

Stable and growing results (dominated by net interest income).

•

Market objectives Public finance unit to reach top three position in Europe and become major market participant worldwide.

•

International activities

Regional market analysis in relevant markets supported by local specialists (New York, Singapore, Tokyo).

≥

20082007≤

2006

Present

situationCurrent

activities

Objectives

Public Finance 1. 2. 3. 4.

11 / 26

Sophistication

and optimization

of public

finance

portfolio

structure

Present structure Target structure

complexity

/ risk complexity

/ risk

attr

activ

enes

s

attr

activ

enes

s

Germany –

plain

vanilla

EU15 –

sovereignsJapan

EU15 –

subsovereigns

US –

tax munis

& student

loans

EU15 –

structured

Germany –

plain

vanilla

Japan EU15 –

sovereigns

EU15 –

subsovereigns

US –

tax munis

& student

loansEU15 –

structured

US –

new

product

lines

Eastern Europe

–

Subsovereigns

High potential CDS

Germany –

PPP /infrastructure

Eastern Europe sovereigns

Eastern Europe

–

Subsovereigns

High potential CDS

Germany –

PPP /infrastructure

Eastern Europe sovereigns

growingstableshrinking

Public Finance 1. 2. 3. 4.

12 / 26

0

Creditspread-Risko

in %

Mar

ge p

.a. i

n B

ps.

Strong

Public Finance Business significantly

improves

risk

/ return profile

within

Commerzbank Group

Efficient

frontier Government bonds

vs. corporate

bonds

Data: Month

end dates

since

January

1998Corporates: 100% ML EMU Corporate Index APublic Finance: 95% ML EU-Gov

Index 5% JP-Morgen

EMBI Index

Creditspread-Risk

in %

Public Finance 1. 2. 3. 4.

•

Empirical

negative correlation

between

public

finance

risks

and corporate

bond

market

(reasons: e.g. safe-haven

demand, flight-to-quality)

•

Exposure

to both

risk

classes

has risk

reducing

effect•

Compared

to a 100% investment

in corporate

assets, a portfolio

with

significant

exposure

to public

finance

assets

achieves

higher

returns

with

equal

risk

profile

(i.e. equivalent

returns

at lower

risk)

Mar

gin

p.a.

in b

ps.

100%PF

100%Corp

13 / 26

Commerzbank Group on track

to build

leading

public

finance

business

Build European top tier public finance business within characterized by market orientation and value creation potential for Commerzbank

•

Diversification

–

both

in products

and regionally

–

well on track Reduction

of plain-vanilla

business

and shift

towards

innovative and more

valuable

products

initiated, portfolio

structure

shifted

from

local

to global focus

•

Development of origination

activities

started Local

activities

in New York have

been

started, Tokyo and Singapore

to follow

•

Group affiliation

provides

unparalleled

backing

for

public

finance

business Local

group entities

serve

as acquisition

and distribution

channel

for

public

finance

products. Cross-selling

potential can

be

lifted

for

other

group entities. Synergies

from

Group‘s

funding expertise

and Group‘s

global market

potential provide

support.

Public Finance 1. 2. 3. 4.

14 / 26

Agenda

1. Figures H1 2007 Public Finance & Treasury

2. Public Finance

4. Outlook

3. Group Treasury

15 / 26

Safeguard the Group‘s solvency in normal and stress situations; fulfill regulatory requirements

Fund the Group at lowest possible cost and highest possible funding source diversification

Optimise

balance sheet structure and structural interest income via implementation of investment and refinancing models; interest income distributed to business lines

Profit-oriented management of interest rate and currency risks from the

commercial banking book; fixed amount of interest income is distributed to business segments

Asset Liability Management of Pension Funds via Pension Committee;

economic results reflected in IAS notes

Frequent communication with central banks, regulators, investors

and

market participants

Group Treasury 1. 2. 3. 4.

Core functions of Group Treasury

16 / 25

•

Ensure Group liquidity after Eurohypo acquisition (balance sheet volume doubled)

•

Reduce wholesale funding dependency•

Separation of Public Finance and Treasury activities within Eurohypo

Challenges

Achieve- ments

Fully integrated Group Treasury of Commerzbank and Eurohypo

BaFin waiver allows flexible cross-financing between entities; net reduction of approx. € 15bn of wholesale funding“One funding curve” concept for all unsecured funding; money market funding centralised in CB, secured funding in EurohypoFunding synergies fully on track (€ 14m in 2008)

Next Steps Projects

Finalisation of “Refi-Register” for cheaper funding

Seek official approval of our Group-internal liquidity model from regulators; replacing current Grundsatz II regulation

Align Group-wide hedge accounting

Key hirings

in 2007

!

Eurohypo integration: Efforts

on track, stress test successfully

mastered

!!

Group Treasury 1. 2. 3. 4.

17 / 26

•

Clear coordination procedures implemented and process defined•

Group issuance and roadshow

calendars adopted•

Investor survey conducted –

very positive feedback received•

Leveraging #1 position of Group in Pfandbrief

market

Milestones in the first year

Capital Markets CommitteeCapital Markets Committee

-

Systematic issuance by Group members gives clear guidance -

Tier 1, Tier 2, Tier 3Öffentliche Pfandbriefe Lettres de Gage Hypothekenpfandbriefe Senior Unsecured

6.5

bn

0.8 bn

79.4 bn

152.4 bn

31.9 bn

* total outstanding issuances in € bn

as of June

2007 (Treasury Database)

Group Treasury 1. 2. 3. 4.

Capital Market Committee manages

€ 270bn* of Group capital

market

issuance

70%

30%

26%

22%38%

3%

11% 91%

2% 1%6%

93%

2% 5%

50%50%

18 / 26

Implementation of Funding plan for distressed market environment

• No Jumbo Pfandbriefe

for the remaining year

• Only limited requirements for unsecured debt

• Direct placements with institutional clients of Commerzbank

Group Treasury 1. 2. 3. 4.

Group funding plan adjustment to current market environment

Residual Funding needs(Sept. until year end)

Funding generated as of June 30: €

22.5bn

Funding Plan 2007 approx. €

40bn

Commerzbank Group funding plan 2007

65 –

75 %

€ 14.2bn

25 –

35 %

€ 8.3bn Approx€ 4bn

Funding planreduction

Funding done in Q3 y-t-d

20% 40% 60% 80% 100%

Reduced capital markets funding regards due to

• Increase in customer deposits

• Sufficient liquidity portfolios

• Increase in money market secured financing

Covered

Bonds Unsecured

debt

19 / 26

•

Funding cost of commercial loan business (approx. € 210bn) only to be affected by up to 4-5 bp (increase extended over several years)

•

Positive impact of widening credit margins on Group’s lending business likely to match increased funding cost

•

No evidence for customer deposits to become more expensive•

Issuance cost of Pfandbriefe

higher than recent lows but impact limited as more expensive Pfandbrief

issues will expire•

Spreads of Group’s senior unsecured capital markets funding to increase in line with markets movements. First expectations of impact: 20-25 bp

•

Total outstanding unsecured debt € 60bn, to be reduced by roughly € 12 bn

due to use of “refinancing register”•

Funding cost to increase over several years. Effects in 2008 € 10-15m (€ 30-35m in 2010)

What will happen?

Overall funding cost to increase moderately

Funding spreads and credit margins in general may remain at higher levels even after stressed liquidity situation of banking sector will have calmed down

Impact on assets

Group Treasury 1. 2. 3. 4.

Outlook: Impact of increased credit spreads on Group’s P&L expected to be positive

20 / 26

Group balance sheet shows sound funding structure ...Total Assets € 638bn Total Liabilities € 638bn

•

Core business & assets not liquid within 1 year funded long term (average term to maturity of bonds over 3.5 yrs)

•

Remaining unsecured and capital funding calendar until year end: € 1.5bn

•

Customer deposits on the rise

Dedicated liquidity portfolio and liquid assets larger than short term liabilities

Balance sheet prudently funded

Cover pool

eligible

Not eligible

for

cover

pool

Liquid trading

assets/ reverse

repos

& fair values

of derivative

hedging

instruments

Covered

bonds

Capital/ senior unsecured

funding & core

customer

deposits

Trading liabilities/ repos

& fair values

of derivative

hedging

instruments

Money market

instrum.& liabilities

to banks

Other

commercial

banking

assets

& other

assets

Non core

customer

deposits

& other

liab.

12%

28%

31%33%

22%

Cor

ebu

sine

ssor

notl

iqui

d w

ithin

1yr

24%

Cash/ interbk. lending

& dedicated

liquidity

portfolio41%

Group Treasury 1. 2. 3. 4.

21 / 26

Unsecured funding matrix

0-1Y 1-2Y 2-3Y 3-4Y 4-5Y 5-6Y 6-7Y 7-8Y 8-9Y 9-10Y > 10Y

0-1Y

1-2Y

2-3Y

3-4Y

4-5Y

5-6Y

6-7Y

7-8Y

8-9Y

9-10Y

> 10Y

Breakdown Group position “Liabilities to banks”

Liab

ilitie

s to

ban

ks

Rep

os&

col

late

ral

Ope

n m

arke

top

erat

ion

with

cen

tral

bank

Reg

iste

red

cove

red

bond

s

Pass

thro

ugh

loan

sfr

om K

fW, E

IB, e

tc.

Schu

ldsc

hein

darle

hen

plac

ed w

ith b

anks

Dep

osits

of c

entr

alba

nk c

usto

mer

s

Dep

osits

from

com

mer

cial

ban

ks

Maturing

assets

> liabilities

Maturing

liabilities

> assets

Assets

Liab

ilitie

s

Data Source: interim report

& Treasury data

as per 06/30/07

Group Treasury 1. 2. 3. 4.

... in all maturity buckets

Maturing assets > liabilities

Maturing liabilities > assets

0

40

80

120

bnEU

R

22 / 26

141%147

928

110

Liabilities to customers thereof repos & cash collateral thereof registered covered bondsUnsecured liabilities to customers

29915

10615.6

7155

Claims on customers thereof reverse repos & cash collateral thereof cover pool eligible claims thereof pass through loans from KfW, EIB, etc. thereof loan loss provisionsunsecured funded loans to customers

Group Treasury 1. 2. 3. 4.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50D

euts

che

CS

Gro

up

UB

S

Post

bank

Uni

Cre

dit

HSB

C

Inte

saSP

I

SocG

en

Dre

ba

Erst

eB

ank

Bar

clay

s PL

C DZ

RB

S

AB

N A

mro

Cre

dit A

gric

ole

LBB

W

BN

P Pa

ribas

BB

VA

Lloy

ds T

SBC

omm

erzb

ank

adju

sted

Wes

tLB

Alli

ed Ir

ish

SEB

Sant

ande

r

Nor

dLB

Hel

aba

Bay

LaB

a

Nor

dea

HB

OS

HVB

Com

mer

zban

kLB

B

HSH

Sach

senL

B

Aar

ealB

ank

Dep

fa

Group’s adjusted loan/deposit ratio in mid range of European banks

Adjustment Commerzbank Group (€ bn)

Data Source: Based

on annual

report

information

23 / 26

Conclusion: Group liquidity

situation

Group Treasury 1. 2. 3. 4.

Commerzbank well positioned

•

Commerzbank well prepared

due

to regular

updates

of stress scenarios•

Integrated

Treasury (Commerzbank/Eurohypo) allows

active

management•

Refinancing

structure

of the

Group restructured

since

Eurohypo acquisition

Commerzbank as liquidity

provider

•

Commerzbank acted as liquidity provider of the German banking system•

Supply of € 4.5bn term money (1-3 months) to German banks in late August/September

Liquidity

of conduits

assured

•

Exposure to Commerzbank conduits € 8.5bn, thereof € 5.5bn funded•

Liquidity assured at all times

No deterioration

expected

•

Interbank

deposits without significant changes •

Increase in client deposits by € 6bn since August•

But:

Risk of market turbulences remains

Further contingency

measures initiated

•

Market Risk Controlling and Group Treasury identified potential to generate additional liquidity from business lines

24 / 26

…but a volatile element will always be part of the risk management business

Objective: Stable revenue stream for the Group…

Similar to other Service and Support depart-

ments

in the Group

Allocation of Treasury results reflects dual function

•

Fund the Group •

Optimise

balance sheet structure •

Optimise structural interest income (investment models)

•

Advise and support business units

•

…

Active management of the commercial banking interest rate risk

Allocation of P&L

Allocation of cost to business segments

Service and Support Function

Risk Management Function

Fixed amount of operating profit (representing an ave-

rage treasury interest

income over the cycle) is distributed to business segments

Remaining result (positive or negative) is shown in Public Finance and Treasury

H1 07

€

86.5m

€ 58m

€

-28.5m

Operating Profit Group Treasury

Group Treasury 1. 2. 3. 4.

1.

2.

25 / 26

Agenda

1. Figures H1 2007 Public Finance & Treasury

2. Public Finance

4. Outlook

3. Group Treasury

26 / 26

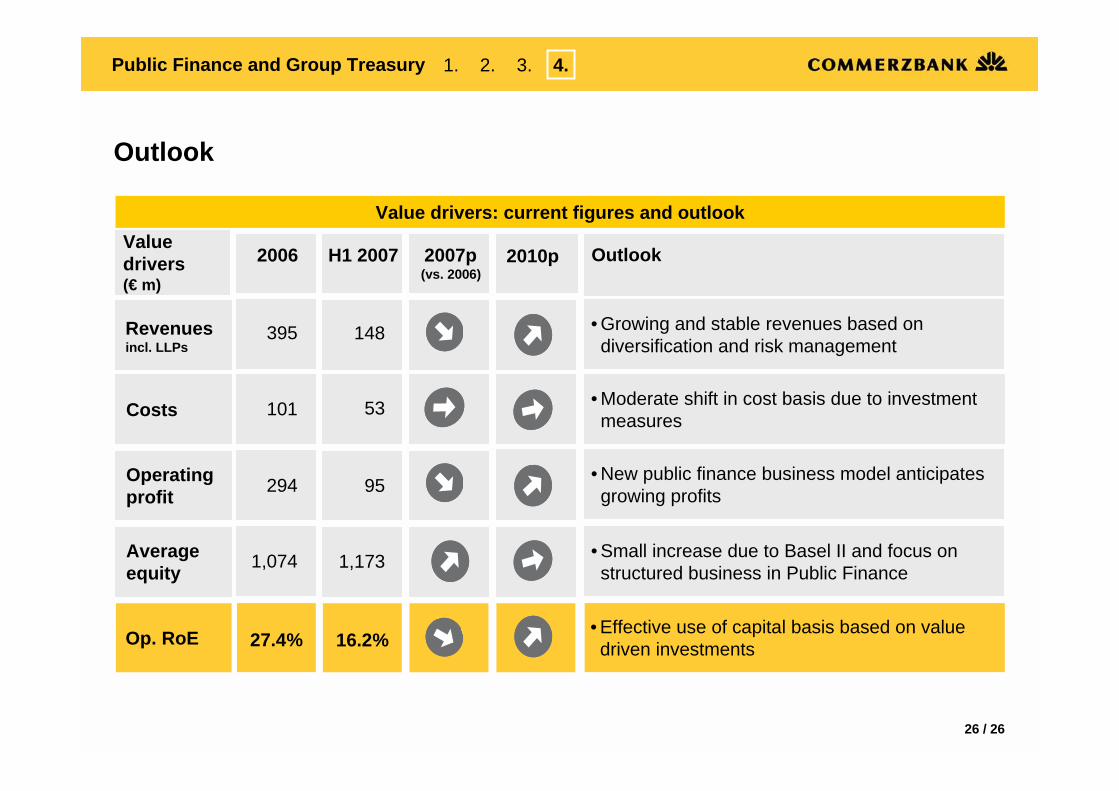

Outlook

Public Finance and Group Treasury 1. 2. 3. 4.

Revenuesincl. LLPs

Costs

Operating

profit

Average

equity

Op. RoE 16.2%

148

53

95

1,173

27.4%

395

101

294

1,074

Value drivers: current figures and outlook

2006 H1 2007 2007p (vs. 2006)

2010p Outlook

•

Growing and stable revenues based on diversification and risk management

•

Moderate shift in cost basis due to investment measures

•

New public finance business model anticipates growing profits

•

Small increase

due

to Basel II and focus

on structured

business

in Public Finance

•

Effective use of capital basis based on value driven investments

Value drivers (€ m)

27 / 26

DisclaimerAll presentations shown at Investors’ Day based on new group reporting as published per H1

2007.

This presentation has been prepared and issued by Commerzbank

AG. This publication is intended for professional and institutional investors only

.

Any information in this presentation is based on data obtained from sources considered to be reliable, but no representations or guarantees are made by Commerzbank

AG and/or its subsidiaries and/or affiliates (herein described as Commerzbank

Group)

with regard to the accuracy of the data. This

presentation

also contains forward-looking statements that reflect our current views and expectations about future events. The words “anticipate,” “assume,” “believe,” “estimate,” “expect,” “intend,” “may,” “plan,” “project,” “should” and similar expressions are used to identify forward-looking statements. These statements are based on plans, estimates and projections as they are currently available to the management of

Commerzbank

AG. Forward-looking statements therefore speak only as of the date they are made, and we undertake no obligation to update publicly any of them in light of new information or future events.

By their very nature, forward-

looking statements involve risks and uncertainties. A number of important factors could therefore cause actual results to differ materially from those contained in any forward-looking statement. This presentation is for information purposes; it is not intended to be and should not be construed as an offer or solicitation to acquire, or dispose of any of the securities or issues mentioned in this presentation.

Commerzbank

Group accepts no responsibility or liability whatsoever for any

expense, loss or damages arising out of, or in any way connected with, the use of all or any part of this presentation.

Copies of this document are available upon request or can be downloaded from www.ir.commerzbank.com

28 / 26

Jürgen

Ackermann

(Head of IR)P: +49 69 136 22338M: [email protected]

Sandra Büschken

(Deputy Head of IR)P: +49 69 136 23617M: [email protected]

Wennemar

von BodelschwinghP: +49 69 136 43611M: [email protected]

Ute Heiserer-JäckelP: +49 69 136 41874M: [email protected]

Simone NuxollP: +49 69 136 45660M: [email protected]

Stefan PhilippiP: +49 69 136 45231M: [email protected]

For more information, please contact Commerzbank´s

IR-team:

Karsten

SwobodaP: +49 69 136 22339M: [email protected]

Andrea Flügel

(Assistant)P: +49 69 136 22255M: [email protected]

www.ir.commerzbank.com