investor presentation - chinabankchinabank.ph/pdf/chib-ir-2q2015.pdfthis presentation may not be...

TRANSCRIPT

0 0

Investor Presentation

1 1

This presentation has been prepared by China Banking Corporation solely for your information and for use at the

presentation by the Bank and has not been independently verified.

This presentation may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or

published, in whole or in part, by any medium or for any purpose. “Presentation” means this document, any oral

presentation, the question and answer session and any written or oral material discussed or distributed at the meeting

where this presentation is made. By attending such meeting, or by accepting a copy of this presentation, you

acknowledge and agree to be bound by the following limitations and (1) will hold in confidence the information

contained herein; (2) will not distribute or reproduce this presentation, in whole or in part; (3) are (a) outside the United

States, (b) accustomed to receiving the type of information contained in this presentation and (c) a person into whose

possession this presentation may be lawfully delivered in accordance with the laws of the jurisdiction in which it is

located.

The information included in this presentation is current as of the date hereof and is subject to updating, completion,

revision and amendment, and such information may change materially. No person is under any obligation to update or

keep current the information contained in the presentation, and any opinions expressed in relation thereto are subject

to change without notice. This presentation should not be construed as legal, tax investment or other advice.

Investor Relations

Alexander C. Escucha, Senior Vice President and Head of Investor and Corporate Relations

28/F, Equitable Tower

8751 Paseo De Roxas, Makati City

Phone (632) 885-5601

E-mail: [email protected]

Legal Disclaimer

2 2

Company Profile

Sector Overview

Key Investment Merits

Financial Highlights

Management & Board of Directors

Q&A

Agenda

3 3

Company Profile

4 4

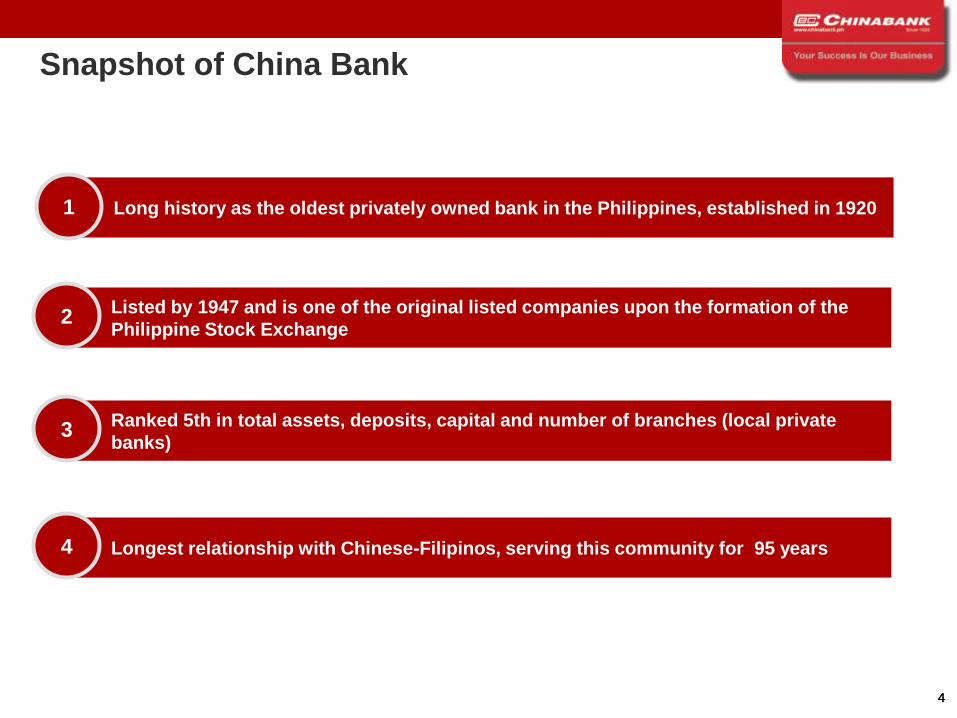

Snapshot of China Bank

Long history as the oldest privately owned bank in the Philippines, established in 1920 1

Listed by 1947 and is one of the original listed companies upon the formation of the

Philippine Stock Exchange 2

Ranked 5th in total assets, deposits, capital and number of branches (local private

banks) 3

Longest relationship with Chinese-Filipinos, serving this community for 95 years 4

5 5

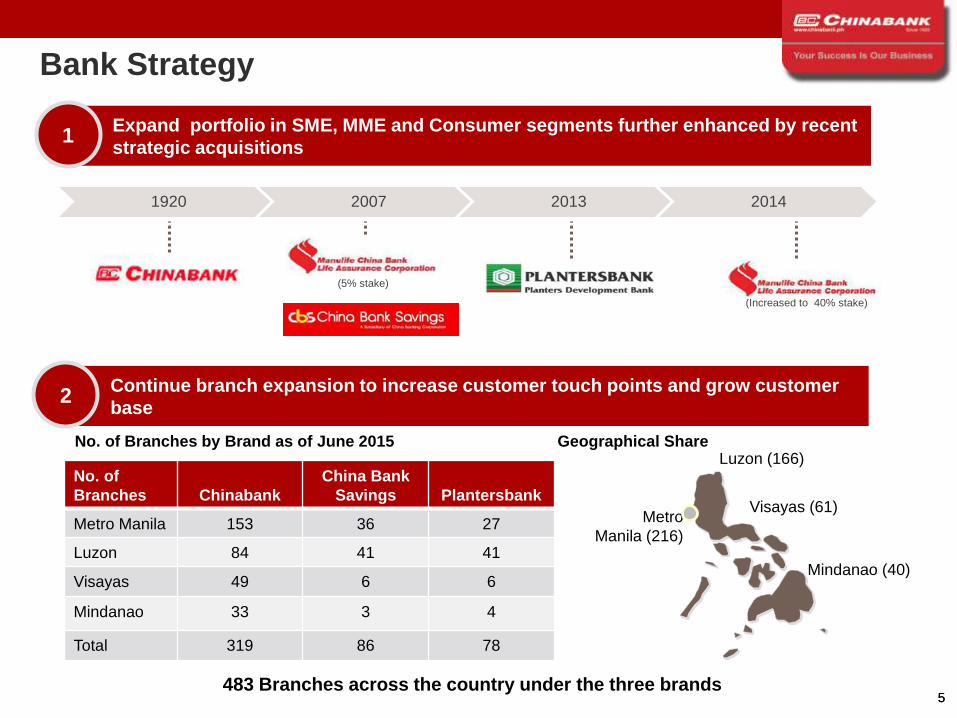

No. of

Branches Chinabank

China Bank

Savings Plantersbank

Metro Manila 153 36 27

Luzon 84 41 41

Visayas 49 6 6

Mindanao 33 3 4

Total 319 86 78

Visayas (61) Metro

Manila (216)

Luzon (166)

Mindanao (40)

Geographical Share

1920 2007 2013 2014

(Increased to 40% stake)

Bank Strategy

No. of Branches by Brand as of June 2015

483 Branches across the country under the three brands

Expand portfolio in SME, MME and Consumer segments further enhanced by recent

strategic acquisitions 1

Continue branch expansion to increase customer touch points and grow customer

base 2

(5% stake)

66

Comprehensive Financial Services Platform

China Bank’s organization anchored on three engines of growth:

Relationship Banking

Retail Banking Business

Lending Segment

Financial Capital Markets and Investment

Savings Banks and Other Business Units

China Bank Savings, Inc.

Manulife-China Bank Life Assurance Corporation

(MCBLife)

Focused growth aims to accelerate business expansion and to ensure efficient client servicing and product delivery

Planters Development Bank

China Bank Insurance Brokers, Inc.

1 2 3

Investment Banking

Private Banking

Treasury

Branch Banking

BinondoBusiness

Center

Institutional Banking

Commercial Banking

Corporate Banking

Consumer Banking

- Consumer Banking

- Remittance Business

- Credit CardTrust

7 7

Sector Overview

8 8

External vulnerabilities are low and policy space is flexible in Philippines and the rest of Asia

Macroeconomic Environment (1/4)

Source: Moody’s Investors Service as of February 2015

Emerging Market Sovereign External Vulnerability Summary Heatmap

Vulnerability Indicators Policy Space

Moody's Sovereign

Credit Rating

Current Account

Balance

(%GDP 2015F)

Enternal

Vulnerability

Indicator

(2015F)

Gross

Borrowing

Requirement

(%GDP, 2015F)

Government

Foreign

Currency

Debt/Total

Government Debt

CPI Inflation,

(Dec/Dec

%, 2015F)

General

Government

Debt

(%GDP, 2015F)

Loan to

Deposits

(%, 1H 2014)

ASIA

China Aa3 Stable 1.5% 19.6% 6.1% 0.5% 3.0% 33.8% 71.0%

India Baa3 Stable -2.0%

77.1%

77.1% 11.3% 6.3% 6.5% 64.2% 83.0%

Indonesia Baa3 Stable -2.7% 57.7%

3.8%

3.8% 45.3% 5.2% 25.6%

91%

91.0%

Korea Aa3 Stable 3.6%

44.4%

44.4% 2.6% na 2.5%

36.9%

36.9% 103.0%

Malaysia A3 Positve 2.7% 112.4%

9.3%

9.3% 2.6% 4.1% 53.6% 88.0%

Pakistan Caa1 Stable -1.6% 112.1% 30.6% 33.1% 8.0% 65.1% na

Philippines Baa2 Stable 3.2%

31.4%

31.4% 6.6% 35.3% 4.0%

38.7%

38.7% 66.0%

Taiwan Aa3 Stable 11.4%

42.6%

42.6% 5.8% 1.9% 42.8% 84.0%

Thailand Baa1 Stable -0.8%

44.6%

44.6% 8.5% 2.1% 2.6%

33.4%

33.4% 96.0%

Vietnam B1 Stable 4.4%

42.6%

42.6% na 41.9% 5.5%

45.8%

45.8% 84.0%

EMERGING MARKET (MEDIAN VALUE)

EM Asia Baa1 Stable 2.1%

44.5%

44.5% 6.6% 19.7% 4.1% 40.8% 84.0%

Latin America Ba1 Stable -2.6% 98.5%

6.9%

6.9% 42.5% 3.2%

35.5%

35.5% 101.0%

EMEA A3 Stable 0.9%

79.8%

79.8% 8.2%

22.8%

22.8% 3.2%

31.2%

31.2% 101.0%

Minimal vulnerability, considerable flexibility Moderate vulnerability, moderate flexibility Elevated vulnerability, diminished flexibility

9 9

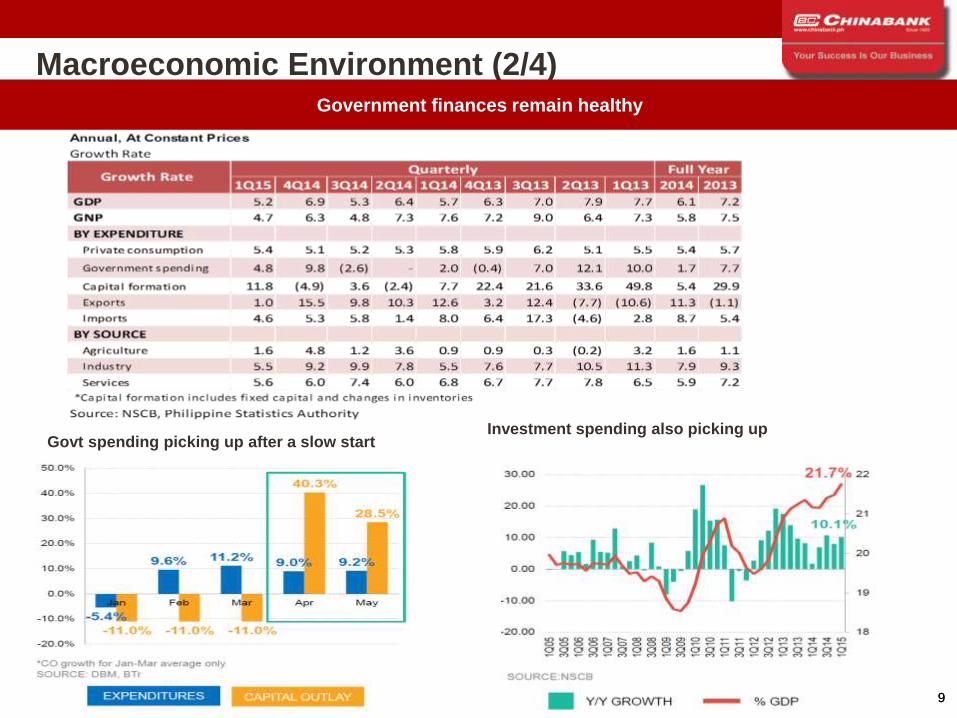

Macroeconomic Environment (2/4) Government finances remain healthy

Govt spending picking up after a slow start Investment spending also picking up

10 10

Macroeconomic Environment (3/4)

Benign inflation environment due to slow increase in food prices and downward adjustments in petroleum prices and electricity rates

July Inflation at 0.8%

Amid strong external position and significant improvement in macroeconomic fundamentals

Strongest sovereign credit ratings for PHL

Resilient Overseas Filipino (OF) Remittances

Stable growth on the back of a sustained demand for skilled Filipino

manpower and continuous efforts of financial institutions for overseas

expansion

Reserves are adequate to cover 10.6 months worth of

imports of goods and payments of services and income

11 11

Macroeconomic Environment (4/4)

* Real lending rate is the difference between the average bank lending rate and inflation Source: BSP, Inflation Report

Interest rates

BSP bucked global trend of monetary easing

- volatile in 2013, increasing in 2014 and steady 2015

Real Lending rate rose to 2.7% in June - due to continuous decline in inflation

Monetary policy & Reserve requirements kept steady

12 12

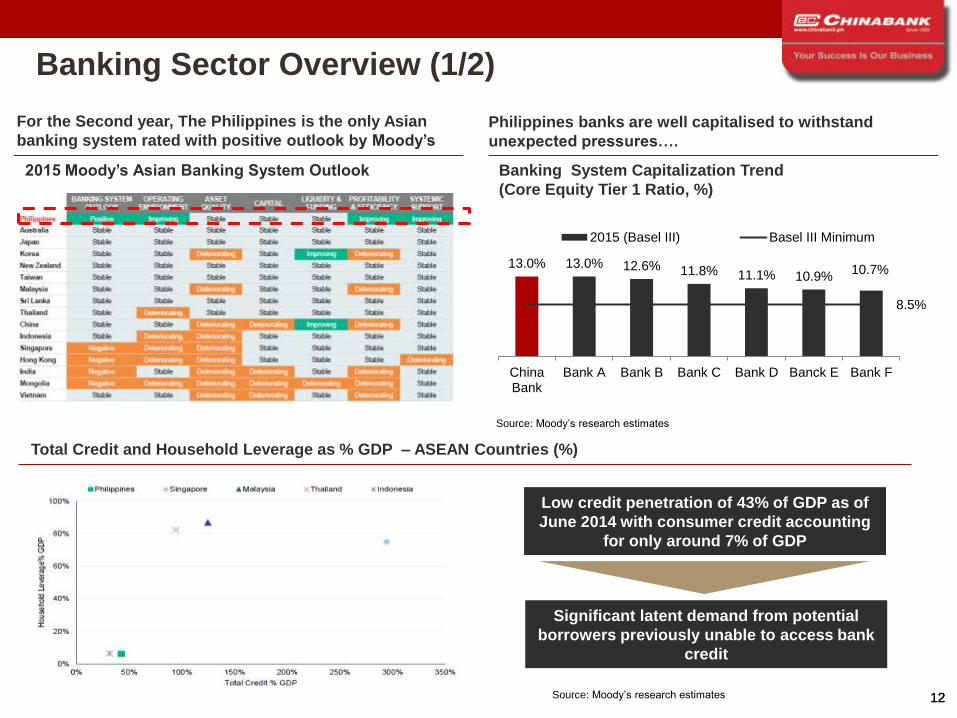

Banking Sector Overview (1/2)

Banking System Capitalization Trend

(Core Equity Tier 1 Ratio, %)

Source: Moody’s research estimates 12

For the Second year, The Philippines is the only Asian

banking system rated with positive outlook by Moody’s

13.0% 13.0% 12.6% 11.8% 11.1% 10.9% 10.7%

8.5%

ChinaBank

Bank A Bank B Bank C Bank D Banck E Bank F

2015 (Basel III) Basel III Minimum

2015 Moody’s Asian Banking System Outlook

Low credit penetration of 43% of GDP as of

June 2014 with consumer credit accounting

for only around 7% of GDP

Total Credit and Household Leverage as % GDP – ASEAN Countries (%)

Significant latent demand from potential

borrowers previously unable to access bank

credit

Philippines banks are well capitalised to withstand

unexpected pressures….

Source: Moody’s research estimates

13 13

Banking Sector Overview (2/2)

Financial Metrics of Philippine Banks (June 2015)

China Bank overtook RCBC as top 5 private bank in terms of Total Assets and Number of Branches

Amt Amt Amt Amt

(in P Bn) (in P Bn) (in P Bn) (in P Bn)

BDO 1,886 17.38% 1,227 21.97% 1,520 18.29% 180 15.42% 13.23% 13.54% 892

MBT 1,630 15.02% 806 14.43% 1,206 14.50% 190 16.25% 10.97% 13.26% 938

BPI 1,414 13.04% 824 14.76% 1,199 14.42% 146 12.48% 13.00% 12.90% 825

PNB 617 5.68% 328 5.87% 456 5.49% 96 8.18% 7.20% 7.50% 662

CHIB 476 4.38% 287 5.13% 400 4.81% 54 4.62% 8.67% 9.08% 483

RCBC 470 4.34% 270 4.83% 322 3.88% 62 5.32% 9.30% 8.93% 450

SECB 441 4.07% 203 3.63% 258 3.10% 51 4.35% 18.83% 17.22% 257

UBP 357 3.29% 165 2.95% 266 3.20% 52 4.46% 10.70% 3/ 13.70% 270

EW 205 1.89% 132 2.36% 158 1.90% 30 2.57% 8.00% 10.60% 410

Gov't Banks 1,556 14.34% 552 9.88% 1,249 15.03% 117 10.03%

LBP 1,091 10.06% 402 7.20% 954 11.48% 75 6.38% 18.74% 2/ 16.54% 2/ 352

DBP 464 4.28% 150 2.68% 294 3.54% 42 3.63% 9.20% 2/ 7.13% 2/ 97

Foreign Banks 984 9.07% 467 8.36% 626 7.53% 89 7.57%

Other Local Banks 813 7.50% 325 5.82% 653 7.85% 102 8.75%

TOTAL 10,849 100% 5,586 100% 8,313 100% 1,169 100%1/

data from SEC 17-Q

2/data from Published SOC

3/ UBP ROE Computed

Institution

ASSETS2/ NET LOANS2/ DEPOSITS2/ CAPITAL2/ ROE1/

BranchesMkt Share

(%)

Mkt Share

(%)

Mkt Share

(%)

Mkt Share

(%)

Jan-Jun

'15

Jan-Jun

'14

14 14

Key Investment Merits

15 15

Key Investment Merits

5

4

3

1

2 6

7 Established

strength in Affluent

Filipino-Chinese

business segment

Strong

balance sheet

with

sustainable

growth

Well diversified

loan portfolio with

quality assets

Strong and

improving capital

levels

Well positioned for

growth with

diversified income

stream, effective cost

management ,

extensive distribution

network and scalable

infrastructure

Strong support

from SM Group

and Experienced

management

Sustained

delivery o f

Shareholder

Returns

16 16

Established Strength in Affluent Filipino-

Chinese Business Segment

Loyal and highly valuable customer

base

Predominantly focused on the

SME/MME segments

Multi-generational relationships Agile and entrepreneurial mindset

Sustainable and profitable niche client relationships

1

17 17

255 258 315

399 405 389 409 2 4

9

15 21 18

24 45

50 46

2010 2011 2012 2013 2014 Jun-14 Jun-15

China Bank (CBC) China Bank Savings (CBS) Planters Development Bank (PDB)

94 67 70

112 84 86 97

117 145

190

221 290 264 289 46 50

64

81

97 108

93

Securities/Treasury Assets Net Loans Others

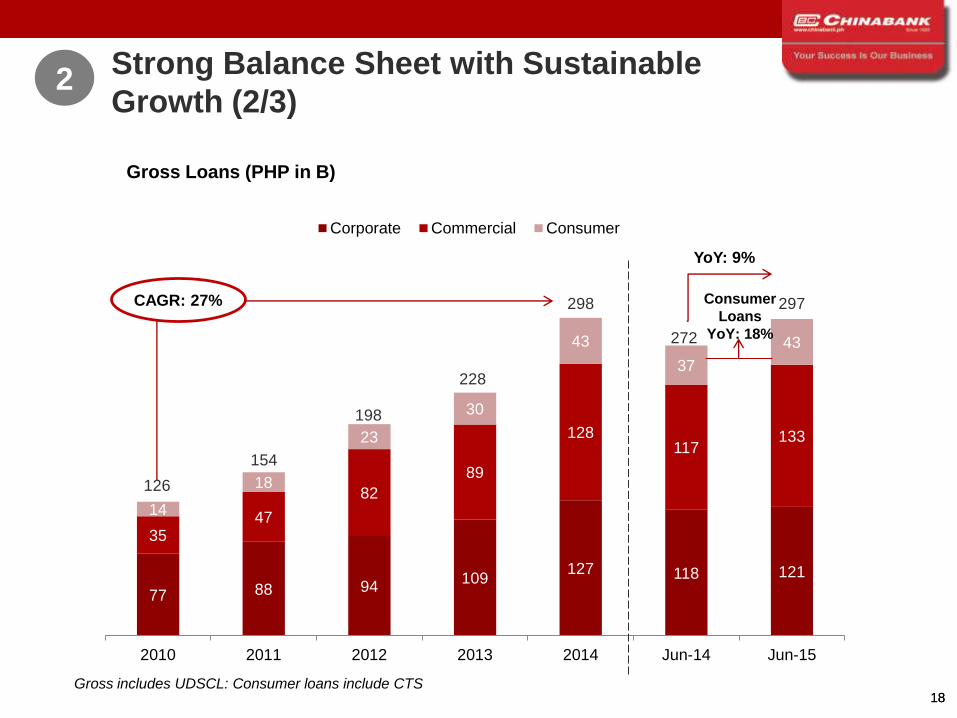

Strong Balance Sheet with Sustainable

Growth (1/3)

471

257 262

479

414

324

457

2

Steady Increase in Assets Through Sustainable Organic Growth and Strategic Inorganic Expansions

YoY: 5%

CAGR:16%

Total Assets (PHP in B)

18 18

Strong Balance Sheet with Sustainable

Growth (2/3)

Gross Loans (PHP in B)

2

77 88 94 109

127 118 121

35 47

82

89

128 117

133

14

18

23

30

43

37

43

2010 2011 2012 2013 2014 Jun-14 Jun-15

Corporate Commercial Consumer

126

154

198

228

298

272

297 CAGR: 27%

YoY: 9%

Gross includes UDSCL: Consumer loans include CTS

Consumer

Loans

YoY: 18%

19 19

70 82 90 137

179 164 188 89 86

128

146

147 161 141

53 48

54

71

73 63 70

2010 2011 2012 2013 2014 Jun-14 Jun-15

CASA High Cost FCDU

Peso Deposits (PHP in B)

Loan-to-Deposit (%)

Strong Balance Sheet with Sustainable

Growth (3/3) 2

Funding (PHP in B)

213 216

272

354

399 388

399 CAGR: 17%

YoY: 3%

160 167

218

283

327 325 330

2010 2011 2012 2013 2014 Jun-14 Jun-15

49 67 70 62 73 68 72

Peso CASA as % Total Peso Deposits (%)

44 49 42 48 55 50 57

20 20

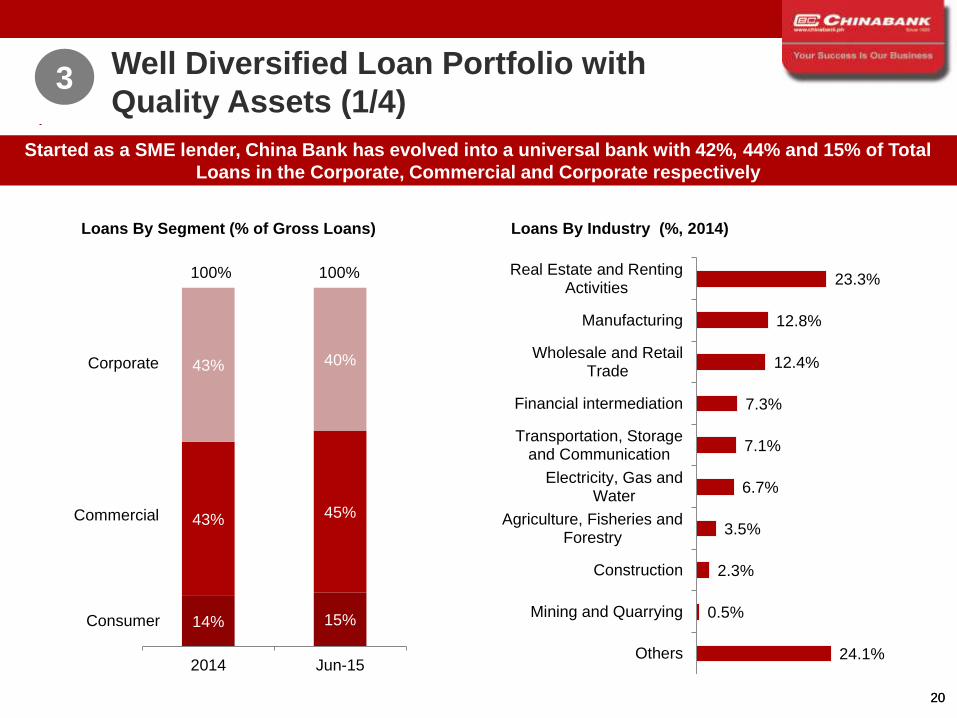

Loans By Industry (%, 2014)

24.1%

0.5%

2.3%

3.5%

6.7%

7.1%

7.3%

12.4%

12.8%

23.3%

Others

Mining and Quarrying

Construction

Agriculture, Fisheries andForestry

Electricity, Gas andWater

Transportation, Storageand Communication

Financial intermediation

Wholesale and RetailTrade

Manufacturing

Real Estate and RentingActivities

Well Diversified Loan Portfolio with

Quality Assets (1/4) 3

Loans By Segment (% of Gross Loans)

14% 15%

43% 45%

43% 40%

2014 Jun-15

Consumer

Commercial

Corporate

100% 100%

Started as a SME lender, China Bank has evolved into a universal bank with 42%, 44% and 15% of Total

Loans in the Corporate, Commercial and Corporate respectively

21 21

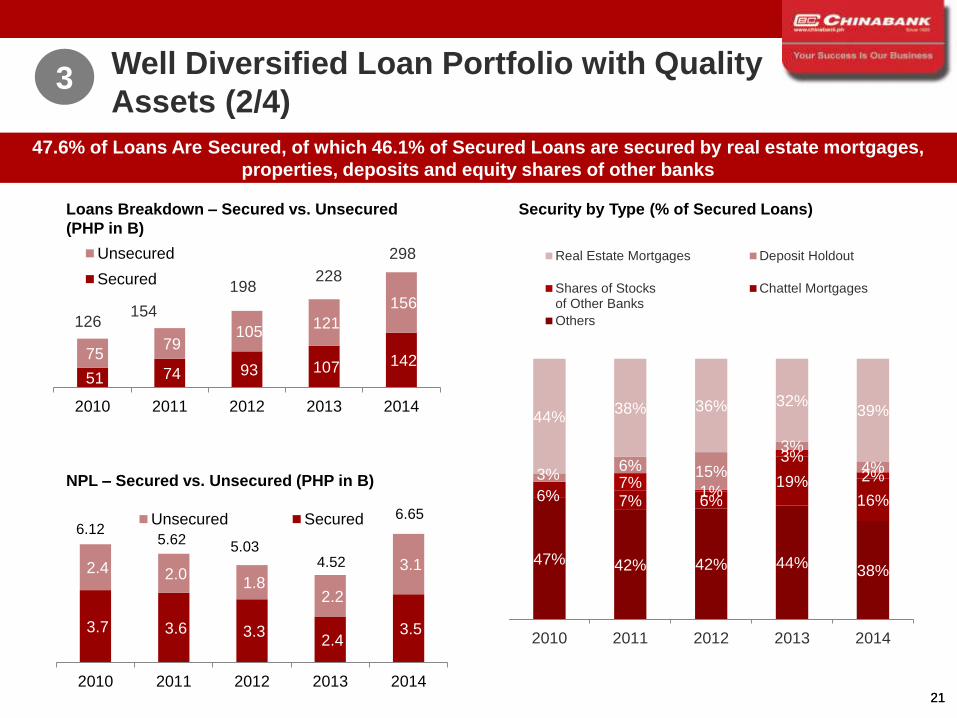

NPL – Secured vs. Unsecured (PHP in B)

6.12 5.62

5.03 4.52

6.65

Loans Breakdown – Secured vs. Unsecured

(PHP in B)

51 74 93 107 142 75 79

105 121

156

2010 2011 2012 2013 2014

Unsecured

Secured

Security by Type (% of Secured Loans)

126 154

198 228

298

Well Diversified Loan Portfolio with Quality

Assets (2/4) 3

47.6% of Loans Are Secured, of which 46.1% of Secured Loans are secured by real estate mortgages,

properties, deposits and equity shares of other banks

47% 42% 42% 44% 38%

6% 7% 6%

19%

16% 7%

1%

3%

2% 3% 6% 15%

3%

4%

44% 38% 36% 32%

39%

2010 2011 2012 2013 2014

Real Estate Mortgages Deposit Holdout

Shares of Stocksof Other Banks

Chattel Mortgages

Others

3.7 3.6 3.3 2.4

3.5

2.4 2.0 1.8

2.2

3.1

2010 2011 2012 2013 2014

Unsecured Secured

22 22

NPA and NPL Ratios (%) - Group

Well Diversified Loan Portfolio with Quality

Assets (3/4) 3

Continuous improvement in assets and loan provisions and steady coverage

7.9% 6.6%

5.6%

4.2% 3.8% 3.6% 3.7%

2.2% 3.0% 3.0% 3.2%

6.5% 5.8%

5.2% 4.1%

3.9% 2.9% 2.6% 2.0% 2.2% 3.0% 2.5%

2006 2007 2008 2009 2010 2011 2012 2013 2014 Jun-14 Jun-15

96.9% 91.2% 92.1%

122.2% 128.9% 134.7% 134.9% 146.6%

101.3% 99.1% 92.6%

2006 2007 2008 2009 2010 2011 2012 2013 2014 Jun-14 Jun-15

Loan Loss Coverage Ratio (%) - Group

Parent at

128.18%

23 23

Source: BSP and Company data

Credit Cost (%)

The Result: A Credit Cost That is Consistently Lower Than Industry Year Over Year

Well Diversified Loan Portfolio with Quality

Assets (4/4) 3

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

1.00%

2007 2008 2009 2010 2011 2012 2013 2014 1Q2015 1S2015

China Bank Average of universal and commercial banks in the Philippines

24 24

Strong and Improving Capital Levels

The Only Major Bank without Hybrid Tier-2 Notes Issuances to comply with Basel II Capital Requirement

4

Total Equity (PHP in B)

23.6%

16.0%

13.5% 12.8%

16.6% 17.8%

16.0% 15.4% 14.8% 16.2%

14.5%

22.0%

15.1% 12.6%

11.9%

15.7% 17.0% 15.2% 14.6% 14.0% 14.8%

13.6%

18.5% 15.9% 15.7% 16.0%

17.3%

17.7% 19.0% 18.9%

16.7% 16.7% 17.0%

Capital Adequacy Ratio (CAR) Tier-1 Ratio Industry Average CAR

25 27 26 30

35 39 42 45

57 55 59

2006 2007 2008 2009 2010 2011 2012 2013 2014 Jun-14 Jun-15

P8BN stock rights in

2014

Basel II

implementation

25 25

8,633 8,552 8,062 9,936

14,089

6,789 7,423

1,587 1,503 1,602

1,577

1,813

866 993

1,751 1,469 2,916

1,905

535

202 346

1,348 1,221

1,275 1,679

2,411

895 709

2010 2011 2012 2013 2014 Jun-14 Jun-15

Net Interest Income Fee Income Trading & Securities Others

Operating Income by Income Type (PHP in M)

13,319 12,744

13,856

15,097

18,848

8,752

Well Positioned for Growth Diversified

Income Stream… (1/3) 5

CAGR: 9.1%

YoY: 8.22%

9,471

26 26

…Effective Cost Management…(2/3) 5

Despite massive expansion, cost parameters compare well with its peers in the Philippines

Cost to Income – Philippine Banks (%, 2014)

Cost to Average Assets – Philippine Banks

(%, 2014)

68.1% 64.5% 62.2% 60.1% 60.0% 56.1% 54.6% 48.2% 47.3%

BankA

BankB

ChinaBank

BankC

BankD

BankE

BankF

BankG

BankH

5.41%

3.24% 3.15% 2.74% 2.74% 2.65% 2.49% 2.33%

1.51%

BankA

BankB

BankC

BankD

BankE

ChinaBank

BankG

BankH

BankH

53.5% 55.2% 59.2% 59.0% 62.2% 65.0% 63.5%

2010 2011 2012 2013 2014 Jun-14 Jun-15

Cost to Income – China Bank (%)

2.90% 2.71% 2.82% 2.41% 2.65% 2.61% 2.54%

2010 2011 2012 2013 2014 Jun-14 Jun-15

Cost to Average Assets – China Bank (%)

27 27

5th Largest Distribution Network in the Philippines

(No. of Branches, as of 30 June 2015) Ongoing Network Expansion Plan

(No. of Branches and ATMs)

Robust and Scalable Infrastructure Platform

…and Extensive Distribution Network and

Scalable Infrastructure Platform (3/3) 5

938 892 825

662

483 450 410

270 257

BankA

BankB

BankC

BankD

ChinaBank

BankE

BankF

BankG

BankH

314 319 364 384 404 424 484 78 86

151 158 165 172 180

78 78

661 676 801 842 883 925 967

2014 Jun-15 2015F 2016F 2017F 2018F 2019F

PDB CBS CHB ATMs

470 483 515 542 569 596 664

28 28

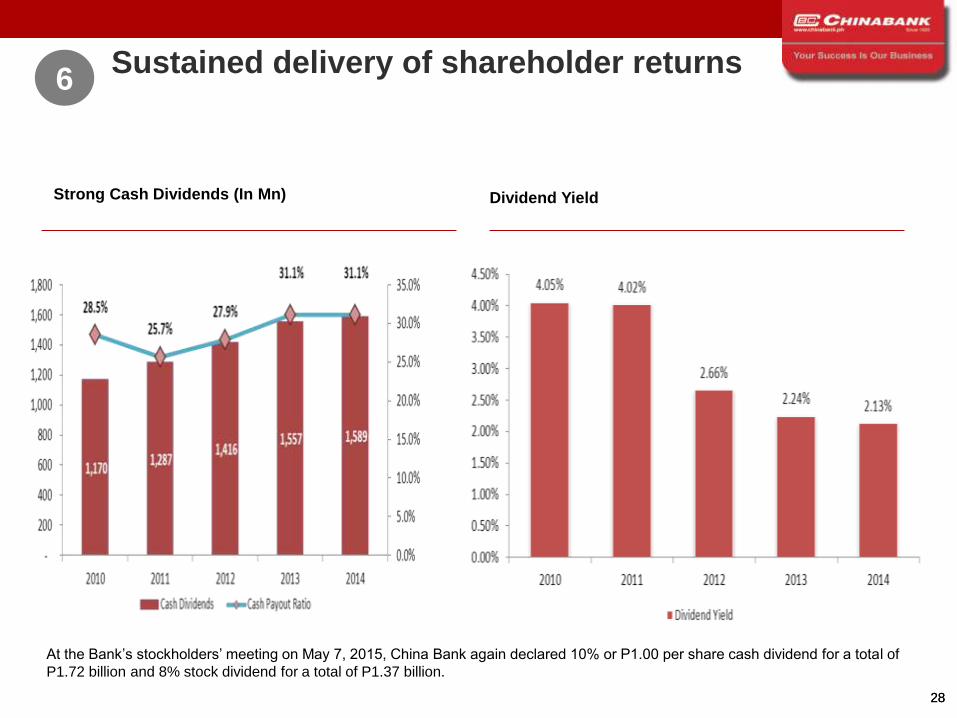

Strong Cash Dividends (In Mn)

Sustained delivery of shareholder returns 6

Dividend Yield

At the Bank’s stockholders’ meeting on May 7, 2015, China Bank again declared 10% or P1.00 per share cash dividend for a total of

P1.72 billion and 8% stock dividend for a total of P1.37 billion.

29 29

Shareholding Support from SM Group

Retail Financial Services

Property

Mutually Beneficial to the SM Group’s ecosystem of merchants,

suppliers and contractors

Priority rights to place branches and ATMs in SM shopping malls

Superior network locations for opening mini-branches in SM

Group’s Savemore supermarkets

Access to SM Group’s retail network to promote new products

such as its upcoming payment cards products

Distinct Benefits for China Bank as a

member of the SM Group

Strong Support from SM Group and

Experienced Management Team (1/3)

27%

10%

26%

37%

% Shareholding in China Bank

100%

(SMIC@17%)

7

Sy Group and

SM Group

Foreign

Shareholders

Dee Group

Others

30 30

Highly respected senior management

team in the industry…

…with over 20 years of Industry

experience on average…

…and successful track record of

managing acquisitions and achieving

financial results …

Strong Support from SM Group and

Experienced Management Team (2/3) 7

31 31

Recipient of the Bell Award for Corporate Governance for the 3rd

consecutive year by PSE

Recipient of Gold Award for Outstanding company from Institute of

Corporate Directors (ICD)

Asia’s Outstanding Company on Corp Governance

awarded by Corporate Governance Asia

Strong Support from SM Group and

Experienced Management Team (3/3) 7

• Award top 5 listed companies, out of 260

• Only bank among top 5 (2012, 2013 and 2014)

• Gold (2011 and 2012)

• Ranked among the top 50 publicly-listed companies in the ASEAN

Corporate Governance Scorecard Country Reports and Assessments

2013-2014

…The Result: Recognition of China Bank’s Strength in Corporate Governance

32 32

Financial Performance Highlights

33 33

Financial Highlights (1/2)

Income Statement(In Millions)

FY 2013 FY 2014 Amt % Jun-14 Jun-15 Amt %

Net interest Income 9,936 14,089 4,153 41.8 6,789 7,423 634 9.3

Non-Interest Income 5,160 4,759 (401) (7.8) 1,963 2,048 85 4.3

Total Operating Income 15,096 18,848 3,752 24.9 8,752 9,471 719 8.2

Total Operating Expenses 9,321 12,170 2,849 30.6 5,876 6,266 390 6.6

Income before Income Tax 5,775 6,678 903 15.6 2,876 3,205 329 11.4

Provision for Income Tax 675 1,565 890 131.9 672 691 19 2.8

Net Income 5,100 5,113 13 0.3 2,204 2,514 310 14.1

Attributable to:

Equity Holders of the Parent Bank 5,103 5,116 13 0.3 2,226 2,514 289 13.0

Non-contorlling Interest (3) (3) - - (22) (0) 21 (97.9)

Ratios:

Net Interest Margin (%) 3.00 3.30 3.18 3.36

Cost-to-Income Ratio (%) 59.00 62.22 65.01 63.46

Cost To Assets Ratio (%) 2.41 2.65 2.61 2.54

Return on Average Equity (%) 11.30 9.91 9.08 8.67

Return on Average Assets (%) 1.50 1.12 0.98 1.06

Change Change

34 34

Financial Highlights (2/2)

Balance Sheet

In Millions

FY2013 FY2014 Amt % Jun-14 Jun-15 Amt %

Total Assets 413,698 470,940 57,242 13.8 457,400 479,289 21,889 4.8

Loans & Receivables (Net) 220,541 290,419 69,878 31.7 264,044 289,323 25,279 9.6

Total Deposits 354,268 399,302 45,034 12.7 387,678 399,446 11,768 3.0

Low Cost Deposits 155,724 193,230 37,506 24.1 176,907 202,502 25,594 14.5

Time Deposits 198,544 206,071 7,527 3.8 210,770 196,944 (13,826) (6.6)

Total Equity 45,400 56,566 11,166 24.6 55,275 58,808 3,533 6.4

Ratios:

Loans to Deposits 62.25 72.73 68.11 72.43

Non-Performing Loans 2.00 2.24 3.04 2.53

NPL Coverage 146.60 101.25 99.13 92.64

Car Tier / CET 1 14.50 13.95 14.78 13.58

CAR Total 15.39 14.88 16.24 14.49

Change Change

35 35

China Bank: Board of Directors

36 36

China Bank: Board of Directors

37 37

China Bank: Management

38 38

China Bank: Management

39 39

Q&A