investor presentation march 2015

TRANSCRIPT

Investor presentation March 2015

\ 2

Important notice

Forward-looking statements This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and

Section 21E of the Securities Exchange Act of 1934. All statements, other than statements of historical facts, included in this

presentation that address activities, events or developments that Markit Ltd. (“Markit” or the “Company”) expects, believes or

anticipates will or may occur in the future are forward-looking statements. Without limiting the generality of the foregoing, forward-

looking statements contained in this presentation may include the expectations of management regarding plans, strategies,

objectives and anticipated financial and operating results of the Company. Markit’s estimates and forward-looking statements are

mainly based on its current expectations and estimates of future events and trends, which affect or may affect its businesses and

operations. Although Markit believes that these estimates and forward-looking statements are based upon reasonable

assumptions, they are subject to several risks and uncertainties and are made in light of information currently available to Markit.

When used in this presentation, the words “anticipate,” “believe,” “intend,” “expect,” “plan,” “will” or other similar words are

intended to identify forward-looking statements. Such statements are subject to a number of assumptions, risks and uncertainties,

many of which are beyond the control of Markit, which may cause actual results to differ materially from those implied or

expressed by the forward-looking statements. Further information on such assumptions, risks and uncertainties is available in

Markit’s filings with the United States Securities and Exchange Commission (“SEC”). Markit’s SEC filings are available at

www.sec.gov or on the investor relations section of its website, www.markit.com. Markit undertakes no obligation and does not

intend to update these forward-looking statements to reflect events or circumstances occurring after the date of this presentation.

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press

release. All forward-looking statements are qualified in their entirety by this cautionary statement.

Non-IFRS financial measures This presentation also includes measures defined by the SEC as non-IFRS financial measures. Markit believes that these non-

IFRS measures can provide useful supplemental information to securities analysts, investors and other interested parties

regarding financial and business trends relating to its financial condition and results of operations when read in conjunction with

the company’s reported results. Definitions and reconciliations of these non-IFRS measures to most directly comparable IFRS

financial measures are available in the Appendix of this presentation and in Markit’s Annual Report on form 20-F.

Copyright ©2015, Markit Group Limited. All rights reserved and all intellectual property rights are retained by Markit.

\ 3

Markit overview

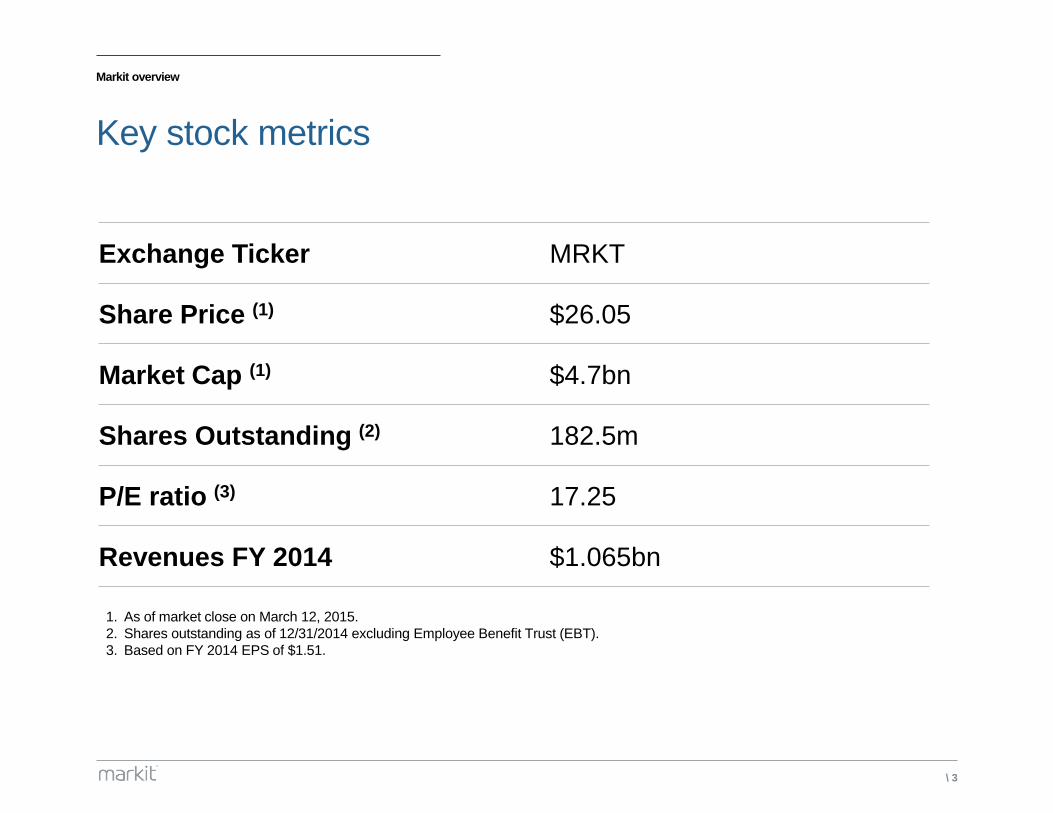

Key stock metrics

Exchange Ticker MRKT

Share Price (1) $26.05

Market Cap (1) $4.7bn

Shares Outstanding (2) 182.5m

P/E ratio (3) 17.25

Revenues FY 2014 $1.065bn

1. As of market close on March 12, 2015.

2. Shares outstanding as of 12/31/2014 excluding Employee Benefit Trust (EBT).

3. Based on FY 2014 EPS of $1.51.

\ 4

2014 overview

Key achievements in 2014

─ Strong full year 2014

financial performance

─ Successful IPO listing on Nasdaq

─ Continued innovation through

product enhancements and new

product launches to address the

needs of our customers

─ Completed two acquisitions –

thinkFolio and CTI

Well positioned to deliver on our longterm financial objectives

\ 5

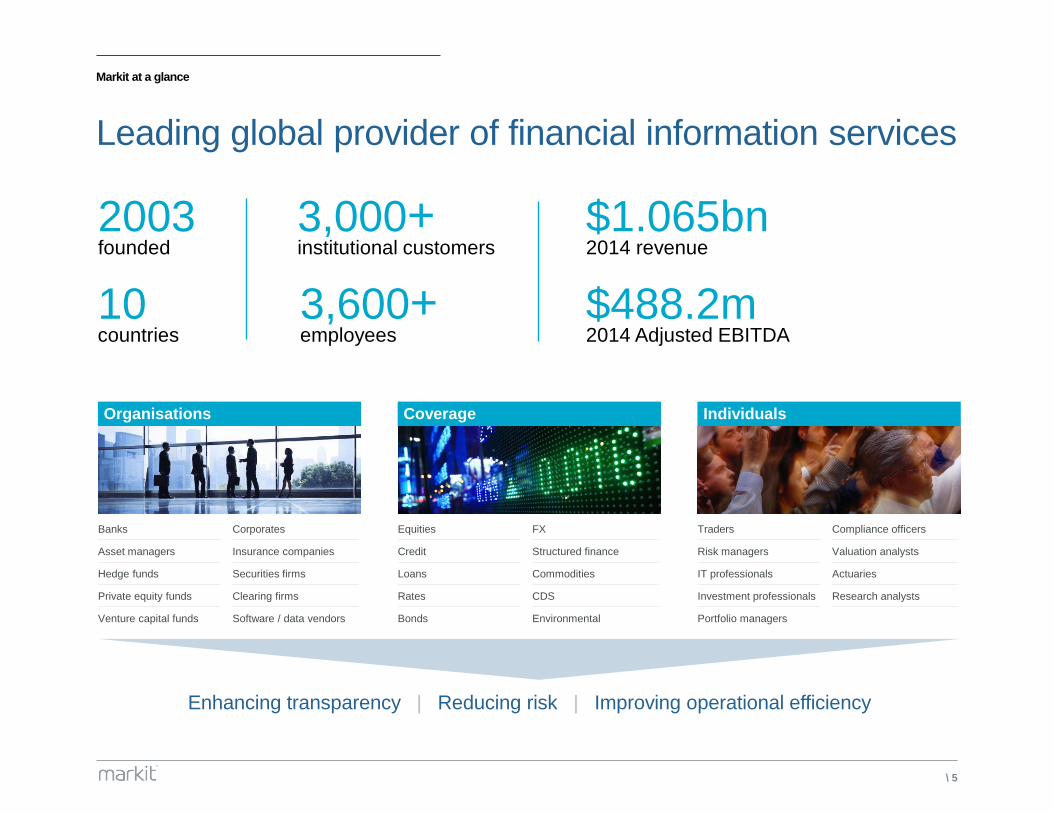

Markit at a glance

Leading global provider of financial information services

Enhancing transparency | Reducing risk | Improving operational efficiency

Organisations Individuals Coverage

Banks Corporates

Asset managers Insurance companies

Hedge funds Securities firms

Private equity funds Clearing firms

Venture capital funds Software / data vendors

Equities FX

Credit Structured finance

Loans Commodities

Rates CDS

Bonds Environmental

Traders Compliance officers

Risk managers Valuation analysts

IT professionals Actuaries

Investment professionals Research analysts

Portfolio managers

2003 founded

10 countries

3,000+ institutional customers

3,600+ employees

$1.065bn 2014 revenue

$488.2m 2014 Adjusted EBITDA

\ 6

Our divisions

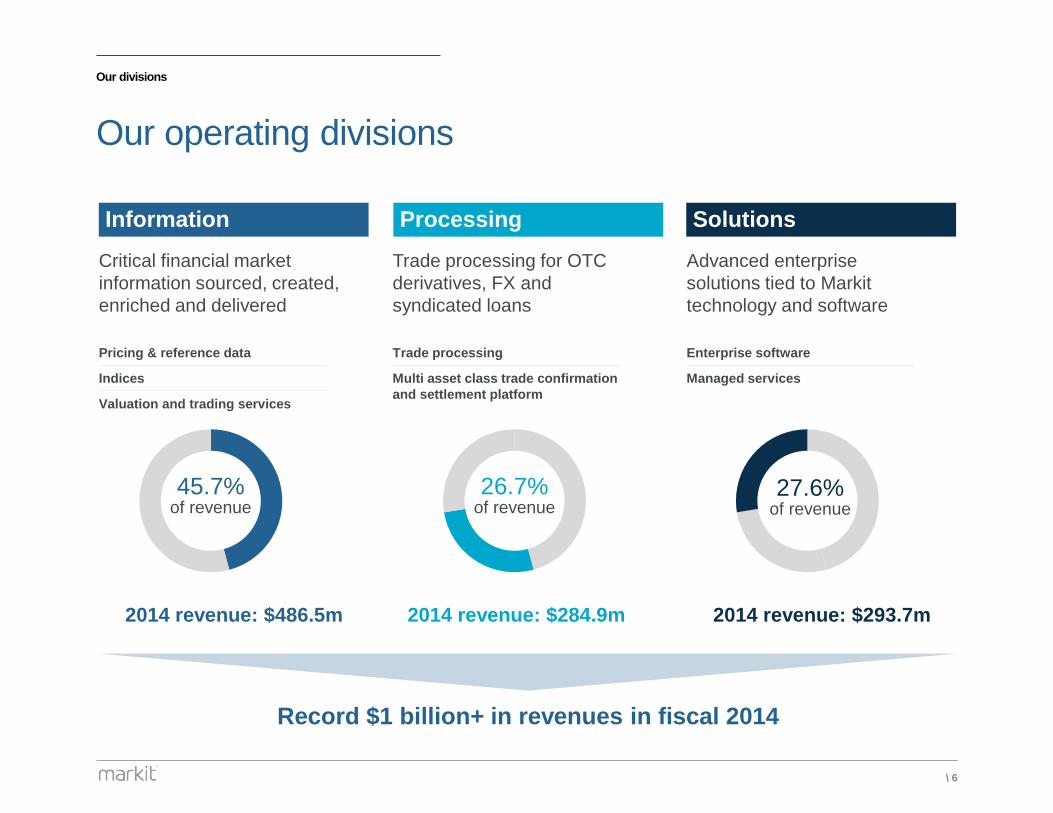

Our operating divisions

Critical financial market

information sourced, created,

enriched and delivered

Trade processing for OTC

derivatives, FX and

syndicated loans

Advanced enterprise

solutions tied to Markit

technology and software

Information Processing Solutions

45.7% of revenue

26.7% of revenue

27.6% of revenue

Pricing & reference data

Indices

Valuation and trading services

Trade processing

Multi asset class trade confirmation

and settlement platform

Enterprise software

Managed services

2014 revenue: $486.5m 2014 revenue: $284.9m 2014 revenue: $293.7m

Record $1 billion+ in revenues in fiscal 2014

\ 7

Customer focus

Deeply embedded in our customers’ systems

and workflows

Create solutions to suit

customer workflow

Develop and

adapt products

Work closely

with customers

Leverage existing

expertise and insights

Work closely with customers to develop new offerings to enhance transparency,

reduce risk and improve operational efficiency

SUCCESSFUL COLLABORATIONS WITH CUSTOMERS

Fixed Income Pricing

INDUSTRY DRIVER

Prudent valuation

Standardised capital requirement for large

banking organisations. Widespread need

for robust inputs into exposure calculation.

Portfolio Valuations

INDUSTRY DRIVER

Independent valuations

Fully hosted OTC derivative valuation

and risk services to support accounting,

regulatory and investor reporting requirements.

Markit | Genpact KYC Services

INDUSTRY DRIVER

KYC AML

Financial institutions need solution to

standardize and streamline client onboarding

─ Liquidity metrics, independent fixed income

pricing data and information on underlying

pricing inputs to simplify the sourcing of data

for additional valuation adjustments (AVA)

calculations

─ AVA calculation allowing customers to access

Markit’s centralised data hub to industrialise

reports in a timely and cost efficient manner.

─ Developed cross asset class coverage with

transparency into mark-to-market inputs and

market data available via a web front-end

─ Accounting credit valuation adjustment

(CVA) service launched in 2014 to help

customers measure and calculate impact

of counterparty risk

─ Developed partnership with four global banks:

Citi, Deutsche Bank, HSBC and Morgan Stanley

─ Service designed to collect, enrich and centrally

administer legal entity data and documents

required by banks from their clients to comply

with KYC and other regulations, including Dodd-

Frank, Emir, Fatca and Mifid

─ Launched Markit Genpact KYC Services in

May 2014

Providing two million+ aggregated data

points across Fixed Income pricing

330+ direct customers, five million+

independent valuations per month

1,000+ buyside institutions, six G14

global banks actively looking to

implement service as of March 2015

\ 8

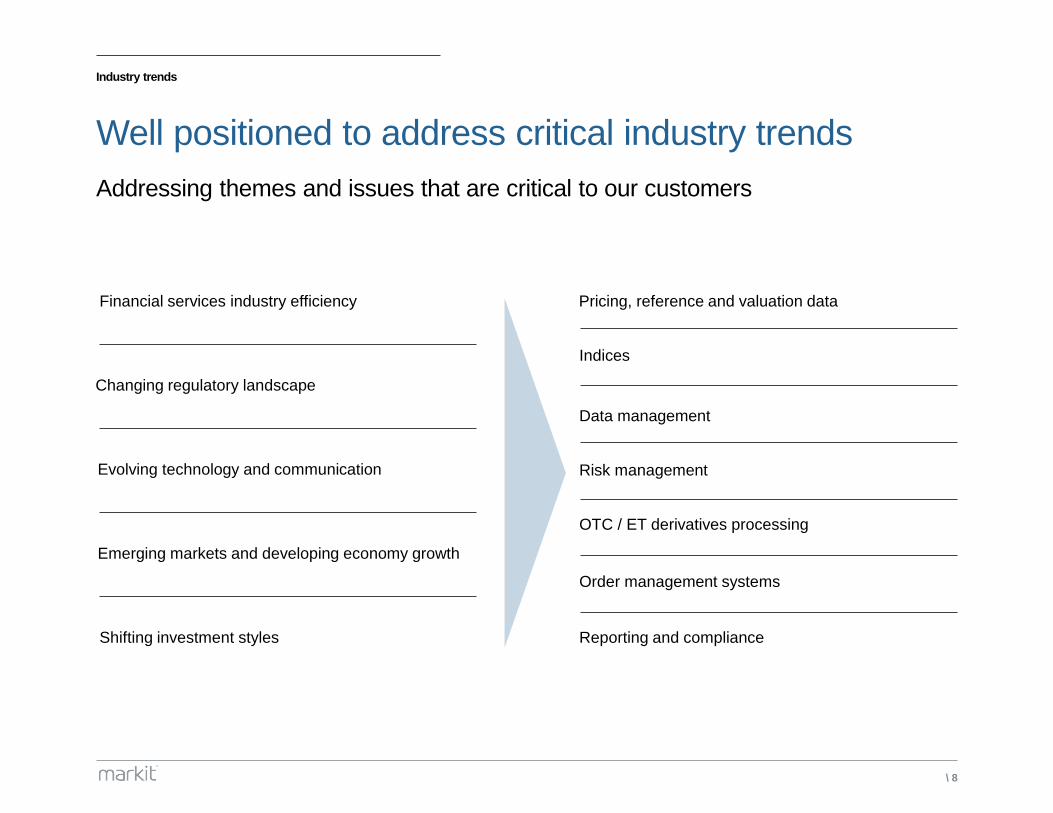

Industry trends

Well positioned to address critical industry trends

Addressing themes and issues that are critical to our customers

Financial services industry efficiency

Emerging markets and developing economy growth

Shifting investment styles

Changing regulatory landscape

Evolving technology and communication

OTC / ET derivatives processing

Reporting and compliance

Data management

Risk management

Order management systems

Indices

Pricing, reference and valuation data

\ 9

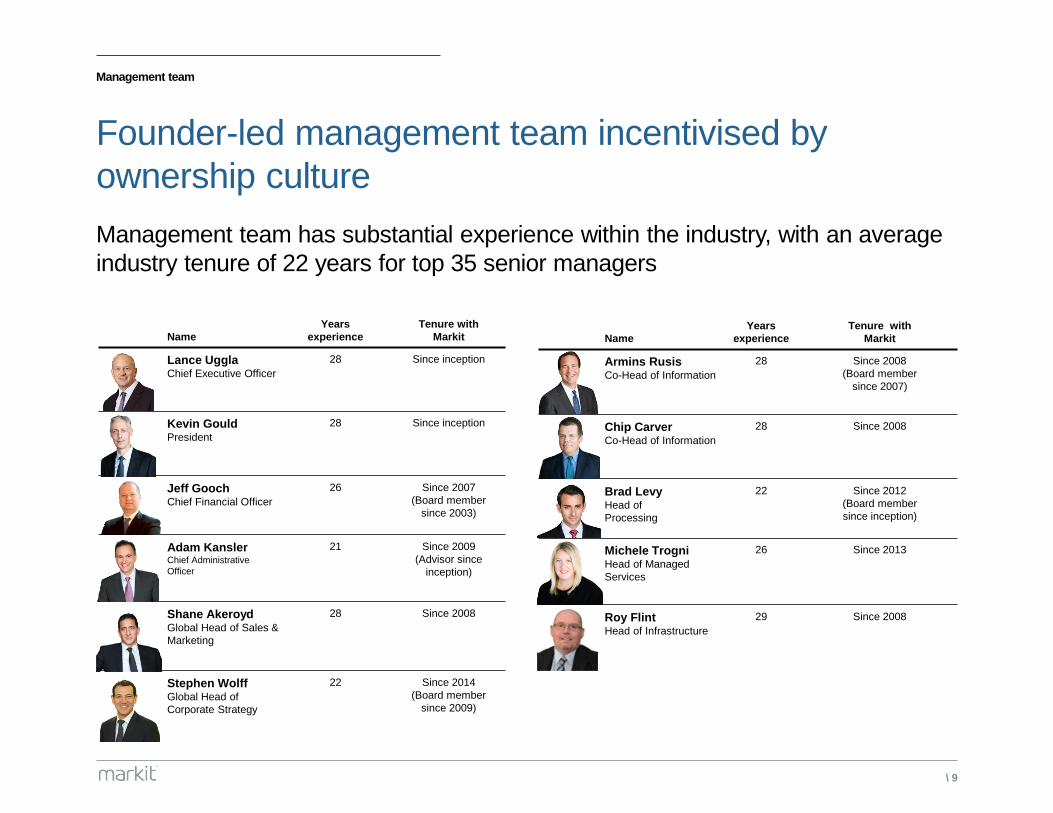

Management team

Founder-led management team incentivised by

ownership culture

Management team has substantial experience within the industry, with an average

industry tenure of 22 years for top 35 senior managers

Name

Years

experience

Tenure with

Markit

Armins Rusis Co-Head of Information

28 Since 2008

(Board member

since 2007)

Chip Carver Co-Head of Information

28 Since 2008

Brad Levy Head of

Processing

22 Since 2012

(Board member

since inception)

Michele Trogni Head of Managed

Services

26 Since 2013

Roy Flint Head of Infrastructure

29 Since 2008

Name

Years

experience

Tenure with

Markit

Lance Uggla Chief Executive Officer

28 Since inception

Kevin Gould President

28 Since inception

Jeff Gooch Chief Financial Officer

26 Since 2007

(Board member

since 2003)

Adam Kansler Chief Administrative

Officer

21 Since 2009

(Advisor since

inception)

Shane Akeroyd Global Head of Sales &

Marketing

28 Since 2008

Stephen Wolff Global Head of

Corporate Strategy

22 Since 2014

(Board member

since 2009)

\ 10

Key corporate events

Track record of acquiring and growing

complementary businesses

CDS Pricing

CDS Reference

Entity Identifiers

Dividend

Forecasting

Index

Management

OTC Derivatives

Sell-Side

Valuations

Loan Pricing

Daily Equity &

Commodities Data

ABS Pricing

Credit Event

Auctions

OTC Derivatives

Buy-Side

Valuations

Metrics

Research

Aggregation

Instant Messaging

Desktop and Data

Feed Solutions

OTC Derivative

Trade Processing

Portfolio

Reconciliation

Structured

Finance Cashflow

Modeling

Loan CDS Indices

& Pricing

Bespoke Indices

Document

Management

Macroeconomic

Data

Portfolio

Compression

Syndicated

Loan Portfolio

Management

Software

Trade

Confirmations

Loan Mapping

Service

Environmental

Registry

Evaluated Bond

Pricing

Credit Trade

Confirmation

Market Share

Analysis

Loan Settlement

Valuations

Management

Entity Identifiers

Mobile

Applications

Broker Voting

SmartText

Online Advertising

Manager

Liquidity Metrics

Loan

Processing

Risk Analytics

Quantitative

Research

and Trading

Analytics

FX Trade

Processing

Commission

Management

Loan Index

Securities Finance

Enterprise Data

Management

Credit Factors

Instrument

Reference Data

ETF Data &

Analytics

ISDA Amend

TD bank spin off

RED acquired

Nine banks invest

Totem & DaDD

acquired

LoanX acquired

Hedge funds

invest

Chasen acquired

Communicator

acquired

MarketXS

acquired

Three banks

invest

BOAT acquired

CDS IndexCo

acquired

International Index

Company

acquired

NTC Economics

acquired

FCS acquired

SwapsWire

acquired

DTCC DerivSERV

joint venture

created

TZ1 acquired

ClearPar acquired

STORM acquired

General Atlantic

invests

Wall Street on

Demand

acquired

QuIC acquired

Logicscope

acquired

QSG acquired

Data Explorers

Acquired

Cadis acquired

26 90+ 140+ 300+ 400+ 1,000+ 1,400+ 2,000+ 2,400+ 2,800+ 3,000+

CLO Pricing

RMBS Index

Tri- Party Repo

and Data Analysis

Corporate Actions

Private Equity

Valuations

Loan Analytics

Credit Checking

Tax Document

Management

Collaboration

Remaining 50% of

MarkitSERV

acquired

GCA acquired

Temasek invests

Credit Indices

European ABS

Performance

Monitoring

European Equity

Trade Reporting

Platform

Quote

Parsing

Operational

Benchmarking

2004 2005

2006

2008

2009

2011

2012

2013

2007

2010

2003

Investment

management

solutions

Social media

research signals

Flash

manufacturing

Japanese PMI

KYC services

Intraday iNAVs

Tax compliance

services

Messaging

software

RMB bond index

2014

thinkFolio

acquired

IPO

Acquired majority

stake in CTI

3,600+ Employees

Revenues

\ 11

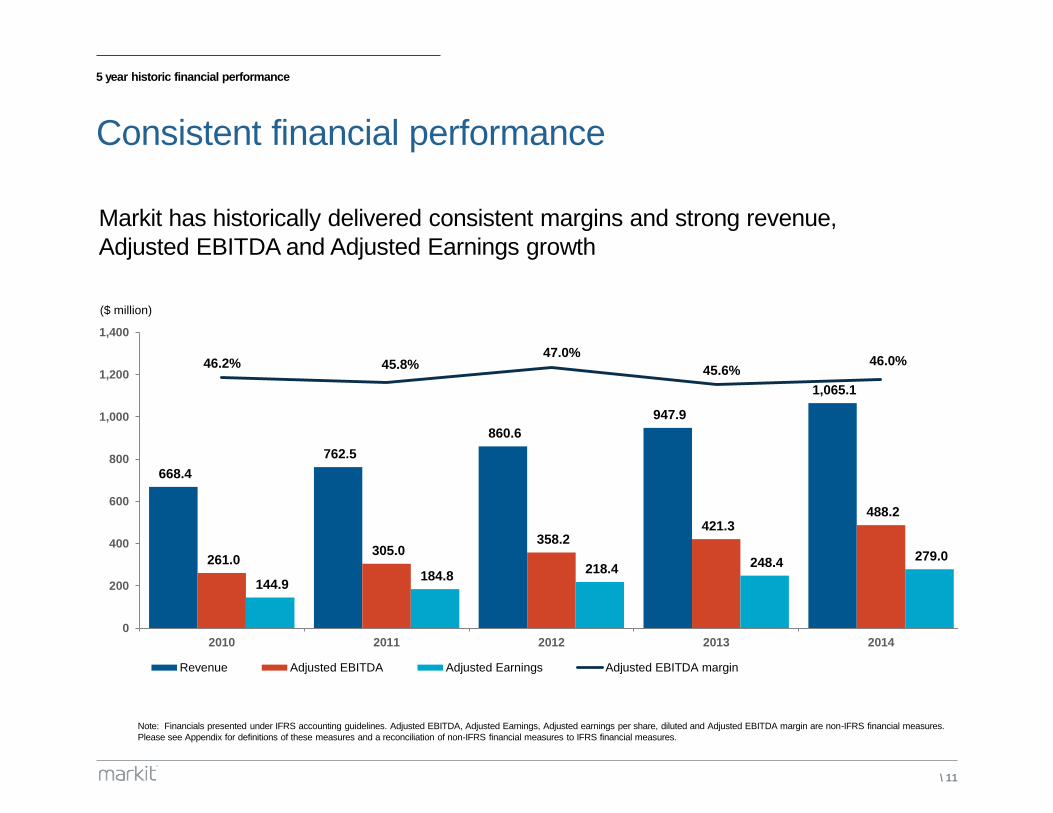

5 year historic financial performance

Consistent financial performance

Note: Financials presented under IFRS accounting guidelines. Adjusted EBITDA, Adjusted Earnings, Adjusted earnings per share, diluted and Adjusted EBITDA margin are non-IFRS financial measures.

Please see Appendix for definitions of these measures and a reconciliation of non-IFRS financial measures to IFRS financial measures.

($ million)

668.4

762.5

860.6

947.9

1,065.1

261.0 305.0

358.2 421.3

488.2

144.9 184.8

218.4 248.4

279.0

46.2% 45.8% 47.0%

45.6% 46.0%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

1,400

2010 2011 2012 2013 2014

Revenue Adjusted EBITDA Adjusted Earnings Adjusted EBITDA margin

Markit has historically delivered consistent margins and strong revenue,

Adjusted EBITDA and Adjusted Earnings growth

\ 12

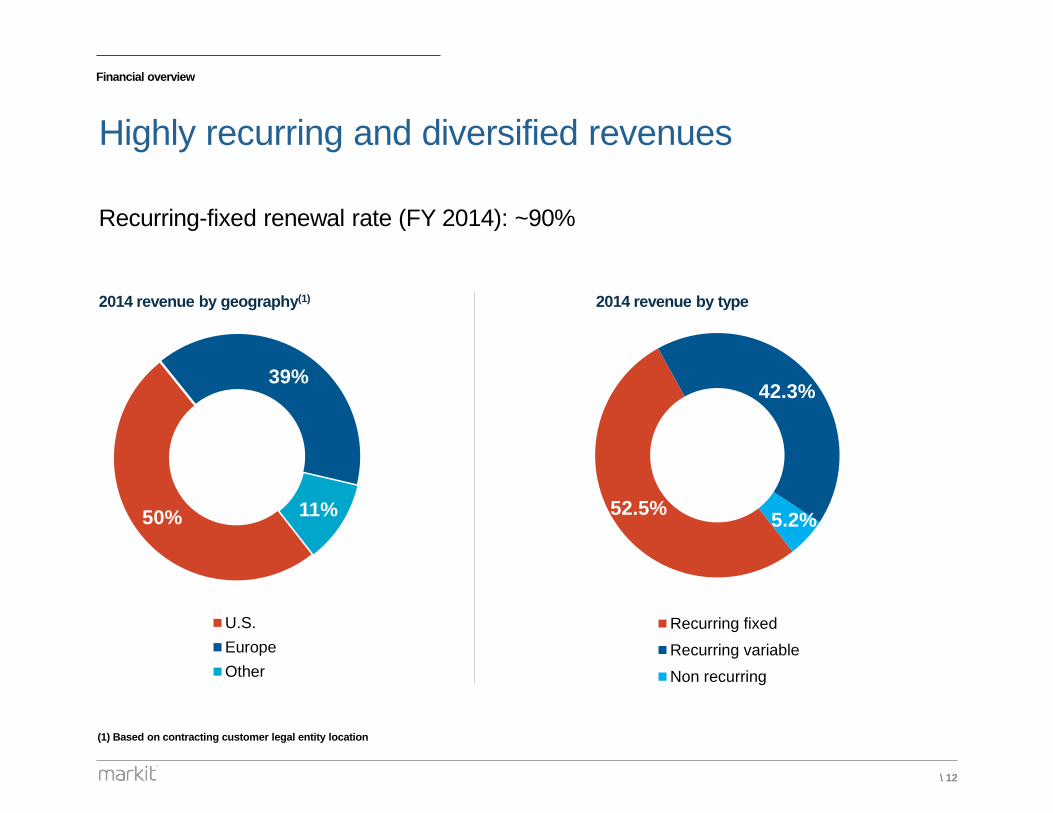

Financial overview

Highly recurring and diversified revenues

Recurring-fixed renewal rate (FY 2014): ~90%

(1) Based on contracting customer legal entity location

52.5%

42.3%

5.2%

Recurring fixed

Recurring variable

Non recurring

50%

39%

11%

U.S.

Europe

Other

2014 revenue by type 2014 revenue by geography(1)

\ 13

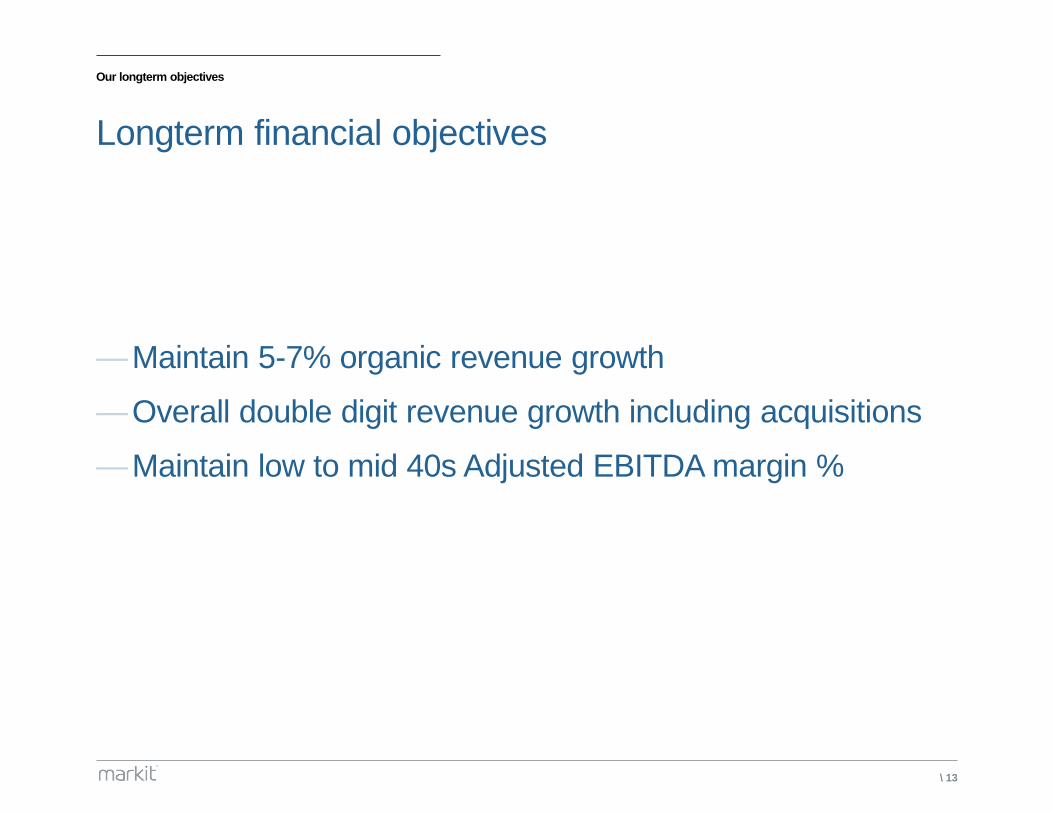

Our longterm objectives

Longterm financial objectives

—Maintain 5-7% organic revenue growth

—Overall double digit revenue growth including acquisitions

—Maintain low to mid 40s Adjusted EBITDA margin %

\ 14

Key investment highlights

Why invest in Markit?

— Trusted partner for diversified, global customer base

— Well positioned to address critical industry trends

— Founder-led experienced management team incentivised

by ownership culture

— Demonstrated ability for product innovation and

accretive acquisitions

— Attractive financial model

\ 15

Business segment overview

\ 16

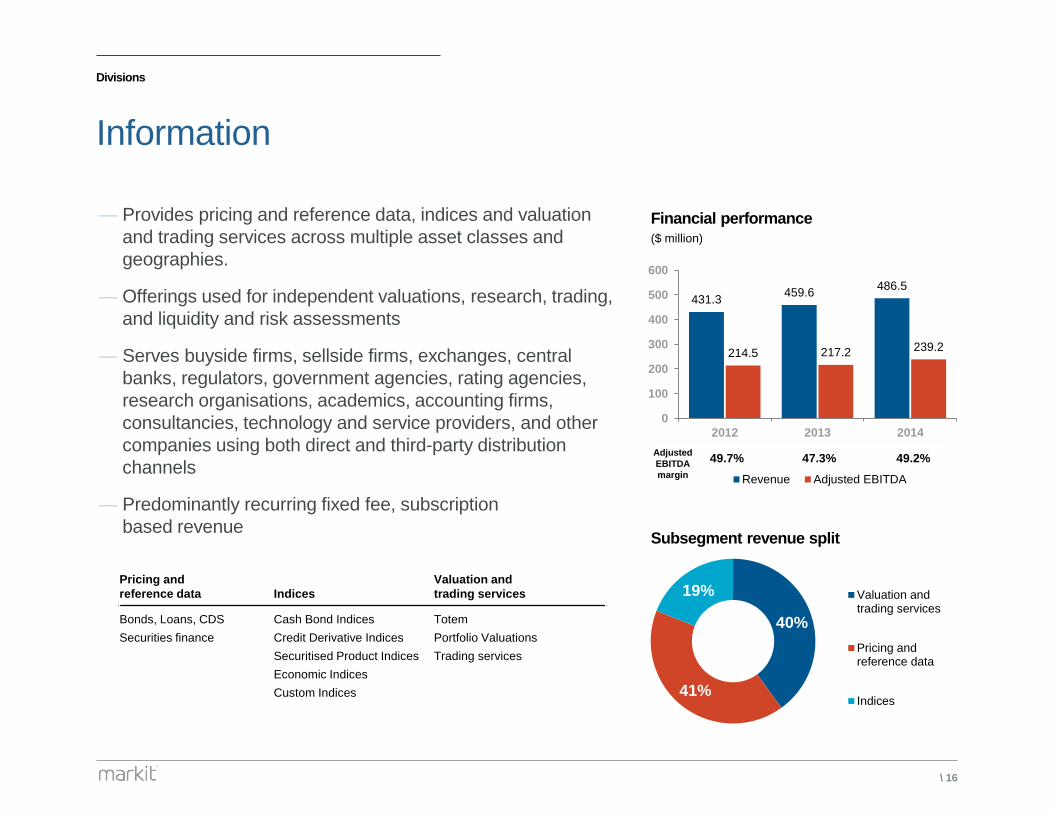

Divisions

Information

431.3 459.6

486.5

214.5 217.2 239.2

0

100

200

300

400

500

600

2012 2013 2014

Revenue Adjusted EBITDA

— Provides pricing and reference data, indices and valuation

and trading services across multiple asset classes and

geographies.

— Offerings used for independent valuations, research, trading,

and liquidity and risk assessments

— Serves buyside firms, sellside firms, exchanges, central

banks, regulators, government agencies, rating agencies,

research organisations, academics, accounting firms,

consultancies, technology and service providers, and other

companies using both direct and third-party distribution

channels

— Predominantly recurring fixed fee, subscription

based revenue

49.7% 47.3% 49.2%

Financial performance ($ million)

40%

41%

19% Valuation andtrading services

Pricing andreference data

Indices

Subsegment revenue split

Pricing and

reference data Indices

Valuation and

trading services

Bonds, Loans, CDS

Securities finance

Cash Bond Indices

Credit Derivative Indices

Securitised Product Indices

Economic Indices

Custom Indices

Totem

Portfolio Valuations

Trading services

Adjusted

EBITDA

margin

\ 17

Divisions

Processing

— Offers trade processing solutions globally for OTC

derivatives, FX and syndicated loans

— Enables inter-dealer brokers, buyside and sellside firms,

to confirm transactions rapidly and increase efficiency by

optimizing post-trade workflow

— Reduces operational risk, facilitates compliance with

global reporting regulations and supports clearing

connectivity to 16 OTC clearing houses

— Predominantly recurring variable-fee revenue model

MarkitServ Loan Settlement

Rates

Credit

Equities

FX

US Syndicated Loans

European Syndicated Loans

238.8

265.3

284.9

124.5

138.1

156.6

0

50

100

150

200

250

300

2012 2013 2014

Revenue Adjusted EBITDA

Financial performance ($ million)

52.1% 52.1% 55.0% Adjusted

EBITDA

margin

\ 18

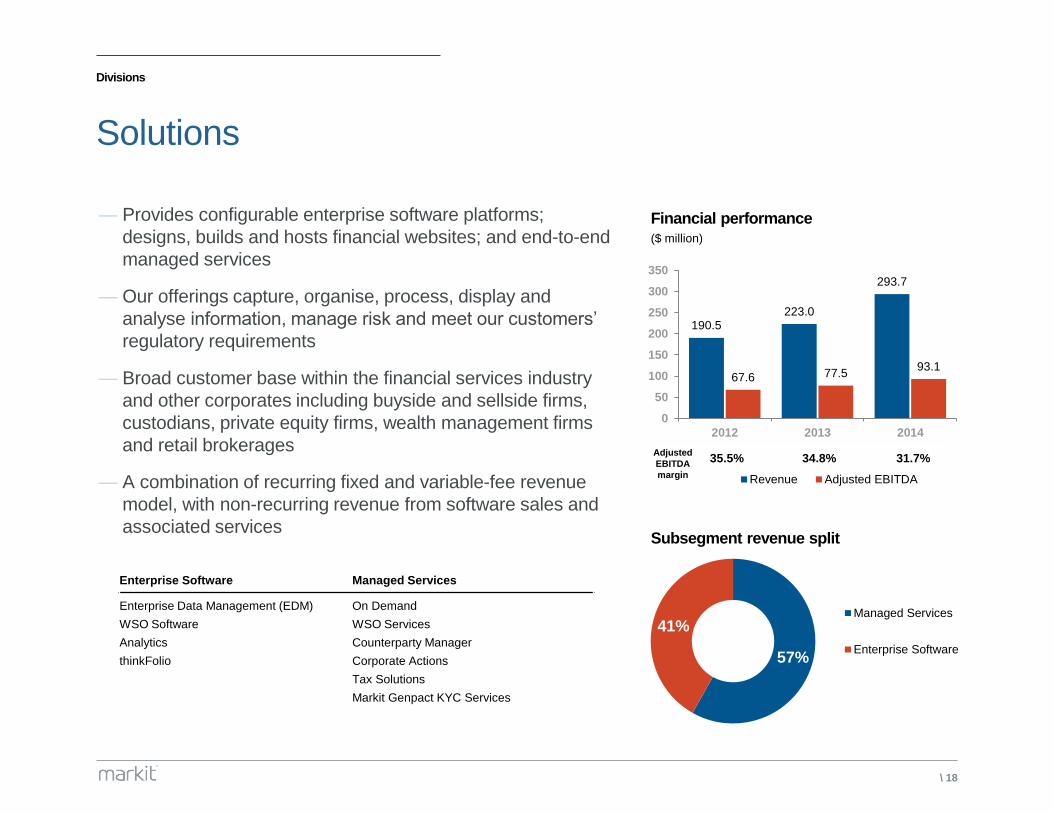

Divisions

Solutions

190.5 223.0

293.7

67.6 77.5 93.1

0

50

100

150

200

250

300

350

2012 2013 2014

Revenue Adjusted EBITDA

— Provides configurable enterprise software platforms;

designs, builds and hosts financial websites; and end-to-end

managed services

— Our offerings capture, organise, process, display and

analyse information, manage risk and meet our customers’

regulatory requirements

— Broad customer base within the financial services industry

and other corporates including buyside and sellside firms,

custodians, private equity firms, wealth management firms

and retail brokerages

— A combination of recurring fixed and variable-fee revenue

model, with non-recurring revenue from software sales and

associated services

Financial performance ($ million)

57%

41% Managed Services

Enterprise Software

Subsegment revenue split

Enterprise Software Managed Services

Enterprise Data Management (EDM)

WSO Software

Analytics

thinkFolio

On Demand

WSO Services

Counterparty Manager

Corporate Actions

Tax Solutions

Markit Genpact KYC Services

35.5% 34.8% 31.7% Adjusted

EBITDA

margin

\ 19

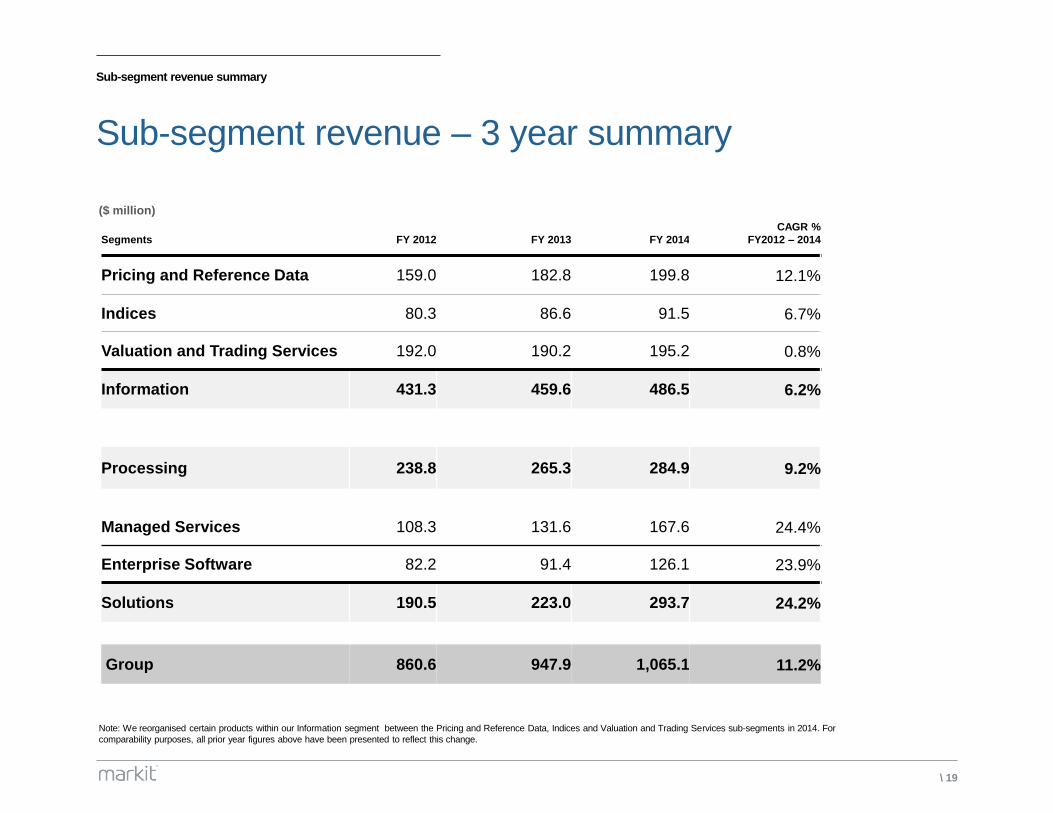

Sub-segment revenue summary

Sub-segment revenue – 3 year summary

Segments FY 2012 FY 2013 FY 2014

CAGR %

FY2012 – 2014

Pricing and Reference Data 159.0 182.8 199.8 12.1%

Indices 80.3 86.6 91.5 6.7%

Valuation and Trading Services 192.0 190.2 195.2 0.8%

Information 431.3 459.6 486.5 6.2%

Processing 238.8 265.3 284.9 9.2%

Managed Services 108.3 131.6 167.6 24.4%

Enterprise Software 82.2 91.4 126.1 23.9%

Solutions 190.5 223.0 293.7 24.2%

Group 860.6 947.9 1,065.1 11.2%

Note: We reorganised certain products within our Information segment between the Pricing and Reference Data, Indices and Valuation and Trading Services sub-segments in 2014. For

comparability purposes, all prior year figures above have been presented to reflect this change.

($ million)

\ 20

Q4 and FY 2014 financial results

\ 21

Q4 and FY 2014 financial results

Summary financial results

1. Adjusted EBITDA is defined as profit for the period from continuing operations before income taxes, net finance costs, depreciation and amortisation on fixed assets and

intangible assets (including acquisition related intangible assets), acquisition related items, exceptional items, share based compensation and related items, net other

gains or losses, including Adjusted EBITDA attributable to joint ventures and excluding Adjusted EBITDA attributable to non-controlling interests.

2. Adjusted EBITDA margin is defined as Adjusted EBITDA divided by revenue, excluding revenue attributable to non-controlling interests.

3. Adjusted Earnings is defined as profit for the period from continuing operations before amortisation of acquired intangibles, acquisition related items, exceptional items,

share based compensation, net other gains or losses and unwind of discount, less the tax effect of these adjustments and excluding Adjusted Earnings attributable to

non-controlling interests.

4. Adjusted EPS diluted is defined as Adjusted Earnings divided by the weighted average number of shares used to compute earnings per share diluted.100101

Q4 2014 Q4 2013 YoY% FY 2014 FY 2013 YoY%

Revenue 271.4 243.8 11.3% 1,065.1 947.9 12.4%

Constant currency growth – – 12.4% – – 10.9%

Adjusted EBITDA (1) 124.7 108.4 15.0% 488.2 421.3 15.9%

Adjusted EBITDA margin (2) 46.3% 44.5% N/A 46.0% 45.6% N/A

Adjusted Earnings (3) 69.1 65.4 5.7% 279.0 248.4 12.3%

Adjusted EPS diluted (4) $0.37 $0.37 - $1.51 $1.41 7.1%

Weighted average number of shares

used to compute earnings per share,

diluted

187.3 176.7 6.0% 184.5 175.6 5.1%

($ million)

\ 22

Q4 and FY 2014 financial results

Revenue growth

$243.8

$21.6

$8.6 $(2.6) $271.4

$200

$210

$220

$230

$240

$250

$260

$270

$280

Q4 2013revenue

Organicgrowth

Acquiredgrowth

FX /Currency

impact

Q4 2014revenue

+8.9%

+3.5%

(1.1)%

+11.3%

$947.9

$73.4

$29.2 $14.6

$700

$750

$800

$850

$900

$950

$1,000

$1,050

$1,100

FY 2013revenue

Organicgrowth

Acquiredgrowth

FX /Currency

impact

FY 2014revenue

+7.8%

+3.1%

+1.5%

+12.4%

Q4 2014 vs. Q4 2013 FY 2014 vs. FY 2013

$1,065.1

($ million)

\ 23

Q4 and FY 2014 financial results

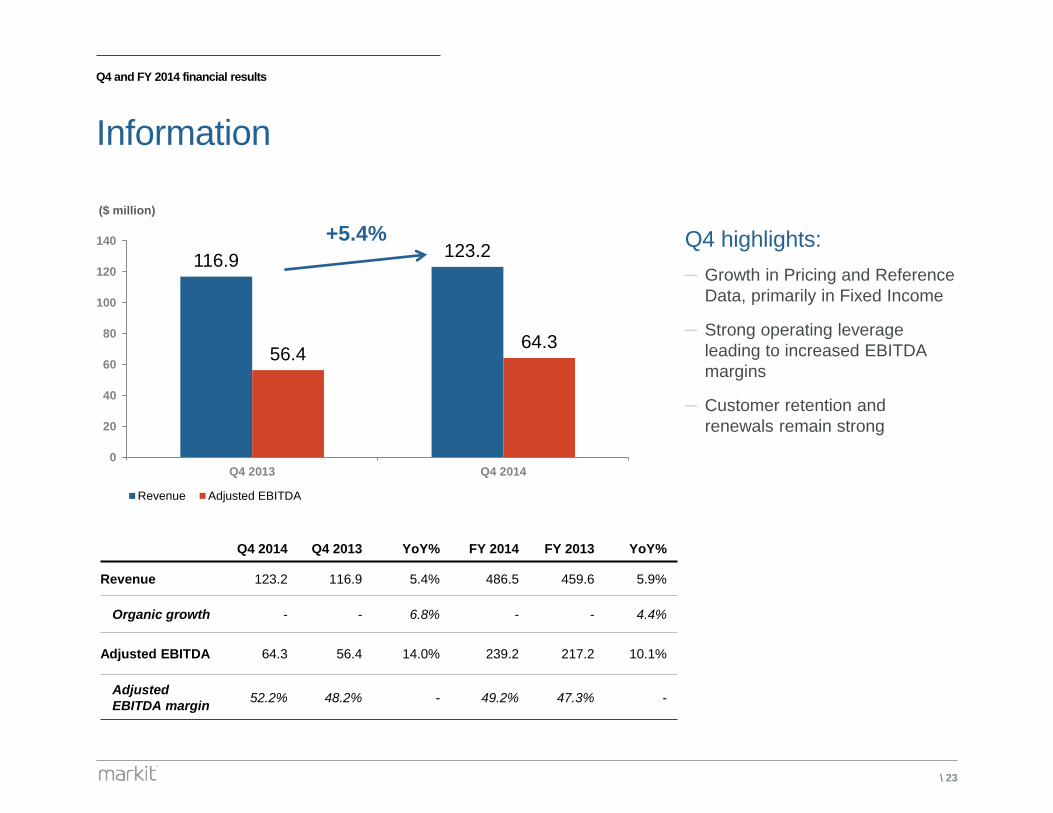

Information

116.9 123.2

56.4 64.3

0

20

40

60

80

100

120

140

Q4 2013 Q4 2014

Revenue Adjusted EBITDA

+5.4% Q4 highlights:

─ Growth in Pricing and Reference

Data, primarily in Fixed Income

─ Strong operating leverage

leading to increased EBITDA

margins

─ Customer retention and

renewals remain strong

($ million)

Q4 2014 Q4 2013 YoY% FY 2014 FY 2013 YoY%

Revenue 123.2 116.9 5.4% 486.5 459.6 5.9%

Organic growth - - 6.8% - - 4.4%

Adjusted EBITDA 64.3 56.4 14.0% 239.2 217.2 10.1%

Adjusted

EBITDA margin 52.2% 48.2% - 49.2% 47.3% -

\ 24

Q4 and FY 2014 financial results

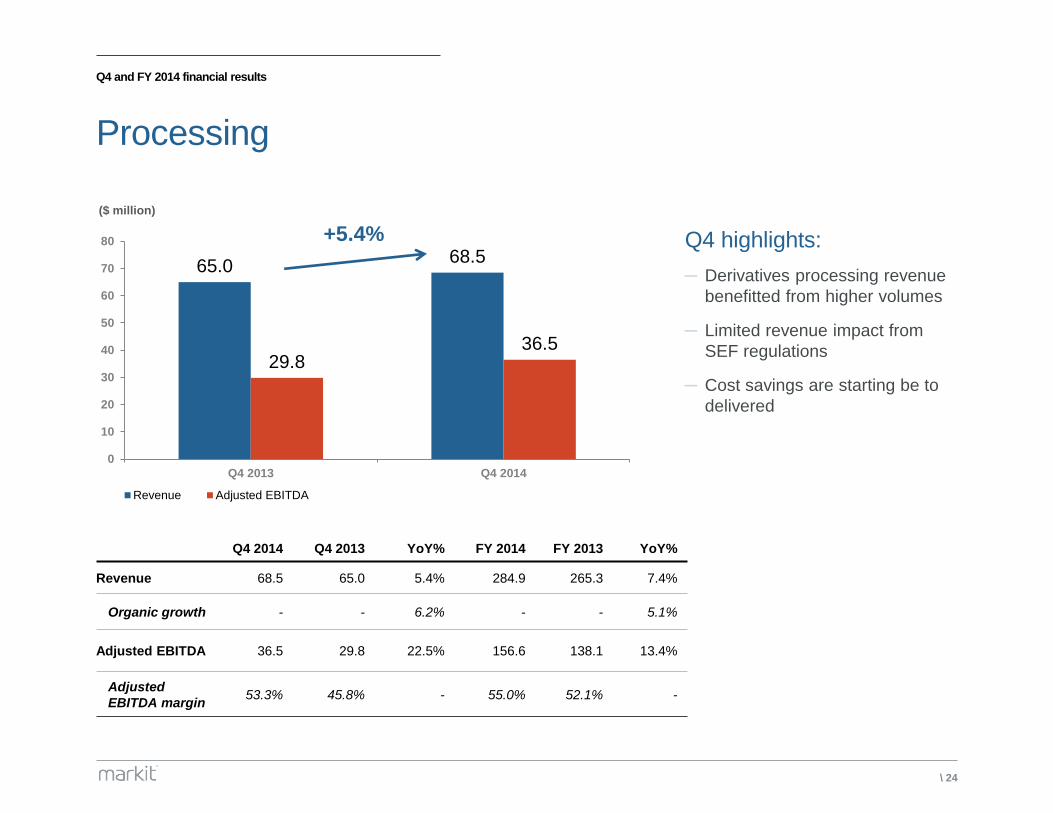

Processing

Q4 highlights:

─ Derivatives processing revenue

benefitted from higher volumes

─ Limited revenue impact from

SEF regulations

─ Cost savings are starting be to

delivered

65.0 68.5

29.8 36.5

0

10

20

30

40

50

60

70

80

Q4 2013 Q4 2014

Revenue Adjusted EBITDA

+5.4%

Q4 2014 Q4 2013 YoY% FY 2014 FY 2013 YoY%

Revenue 68.5 65.0 5.4% 284.9 265.3 7.4%

Organic growth - - 6.2% - - 5.1%

Adjusted EBITDA 36.5 29.8 22.5% 156.6 138.1 13.4%

Adjusted

EBITDA margin 53.3% 45.8% - 55.0% 52.1% -

($ million)

\ 25

Q4 and FY 2014 financial results

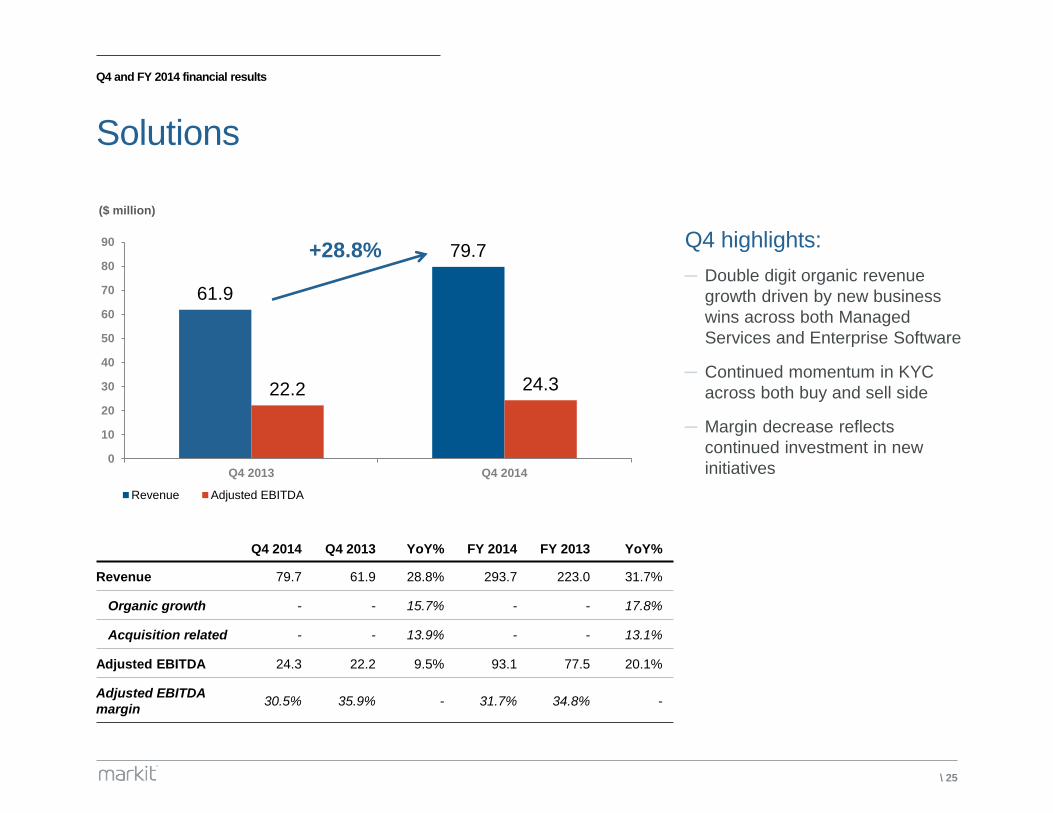

Solutions

61.9

79.7

22.2 24.3

0

10

20

30

40

50

60

70

80

90

Q4 2013 Q4 2014

Revenue Adjusted EBITDA

+28.8%

Q4 2014 Q4 2013 YoY% FY 2014 FY 2013 YoY%

Revenue 79.7 61.9 28.8% 293.7 223.0 31.7%

Organic growth - - 15.7% - - 17.8%

Acquisition related - - 13.9% - - 13.1%

Adjusted EBITDA 24.3 22.2 9.5% 93.1 77.5 20.1%

Adjusted EBITDA

margin 30.5% 35.9% - 31.7% 34.8% -

Q4 highlights:

─ Double digit organic revenue

growth driven by new business

wins across both Managed

Services and Enterprise Software

─ Continued momentum in KYC

across both buy and sell side

─ Margin decrease reflects

continued investment in new

initiatives

($ million)

\ 26

Q4 and FY 2014 financial results

Net debt / leverage

December

31st 2014

December

31st 2013

Bank borrowings 224.5 268.0

Share buyback 211.1 306.6

Total borrowings 435.6 574.6

Cash and cash equivalents (117.7) (75.3)

Net debt 317.9 499.3

Adjusted EBITDA 488.2 421.3

Leverage

(Net debt/ Adjusted EBITDA) 0.65x 1.19x

Highlights:

─ Operating cash flow was $369.9

million for the full year 2014, up

8.9% year on year

─ Capital expenditure full year 2014

was $124.9 million, down 4.3% or

$5.6 million year on year

─ Net debt down 36.3% or $181.4

million

($ million)

\ 27

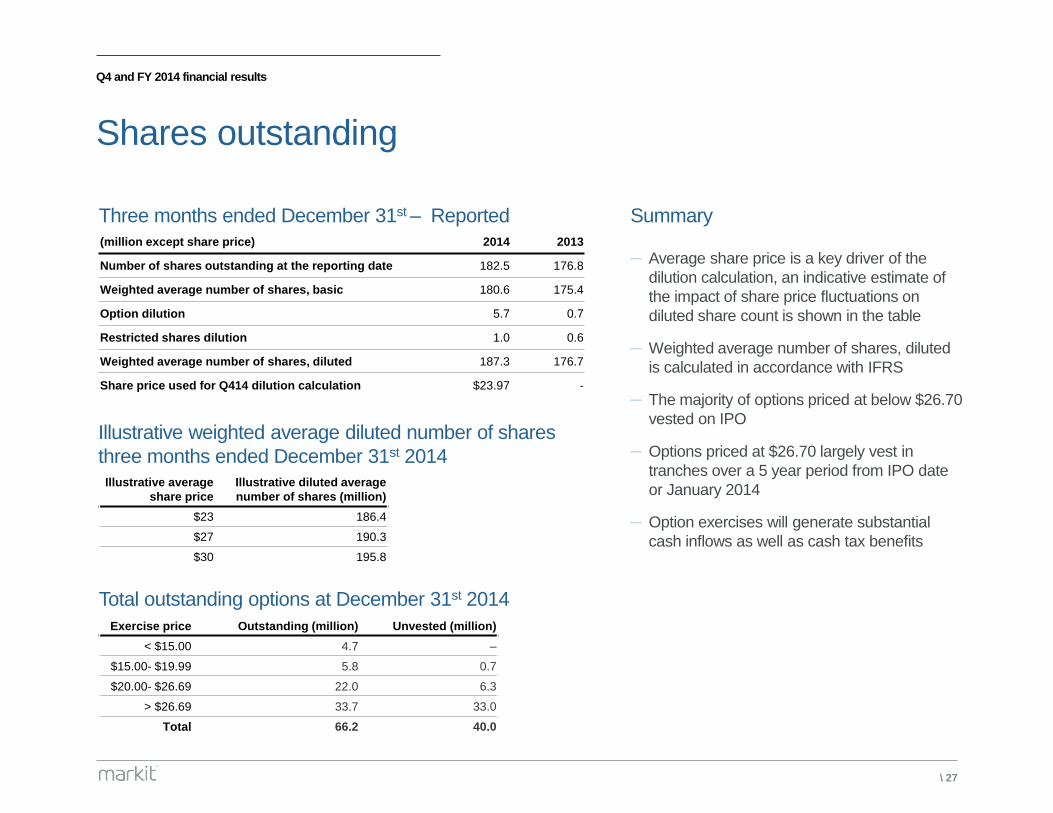

Q4 and FY 2014 financial results

Shares outstanding

Summary

─ Average share price is a key driver of the

dilution calculation, an indicative estimate of

the impact of share price fluctuations on

diluted share count is shown in the table

─ Weighted average number of shares, diluted

is calculated in accordance with IFRS

─ The majority of options priced at below $26.70

vested on IPO

─ Options priced at $26.70 largely vest in

tranches over a 5 year period from IPO date

or January 2014

─ Option exercises will generate substantial

cash inflows as well as cash tax benefits

(million except share price) 2014 2013

Number of shares outstanding at the reporting date 182.5 176.8

Weighted average number of shares, basic 180.6 175.4

Option dilution 5.7 0.7

Restricted shares dilution 1.0 0.6

Weighted average number of shares, diluted 187.3 176.7

Share price used for Q414 dilution calculation $23.97 -

Illustrative average

share price

Illustrative diluted average

number of shares (million)

$23 186.4

$27 190.3

$30 195.8

Exercise price Outstanding (million) Unvested (million)

< $15.00 4.7 –

$15.00- $19.99 5.8 0.7

$20.00- $26.69 22.0 6.3

> $26.69 33.7 33.0

Total 66.2 40.0

Three months ended December 31st – Reported

Illustrative weighted average diluted number of shares

three months ended December 31st 2014

Total outstanding options at December 31st 2014

\ 28

Appendix

\ 29

North America – 1,600+

Europe – 1,000+

Asia Pacific – 900+

Global presence

22 offices

3,600+ total headcount

Locations and headcount

\ 30

Industry recognition

Innovation of the Year

Credit Event Fixings \ 2006

Trading Initiative of the Year

Credit Event Fixings \ 2006

Industry Platform of the Year

PortRec \ 2008

Industry Platform of the Year \

Compression \ 2009

Lifetime Achievement \

Lance Uggla \ 2012

OTC Infrastructure Service of the Year

MarkitSERV \ 2013

Back Office Technology Product of the

Year

Markit Counterparty Manager \ 2013

Risk Management System of the Year

Integrated resource management \ 2014

Asia Risk

—Technology Development of the Year \ 2011

AsianInvestor

—Best Tradable Index \ 2013

The Asset

—Rising Star Index Provider \ 2011

—Best Index Provider \ 2013

Banking Technology

—Best EDM Platform \ 2013

Buy-Side Technology

—Best Pricing/Valuation Service \ 2007

—Best Data Management Product \ 2007

—Best Pricing/Valuation Service \ 2008

—Best Overall Product \ 2008

—Best Data Management Product \ 2008

—Best Data Management Product \ 2009

—Best Pricing/Valuation Service \ 2010

—Best Data Management Product \ 2010

—Best Pricing/Valuation Service \ 2011

—Best Data Management Product \ 2011

—Best TCA Provider to the Buy-Side \ 2012

—Best Overall Buy-Side Technology Provider \

2012

—Best Pricing/Valuation Service \ 2012

—Best Data Management Product \ 2012

—Best Pricing/Valuation Service \ 2013

—Best Data Management Product \ 2013

—Best Buy-Side Pricing\ Valuation Service \ 2014

—Best Data Management Provider \ 2014

Credit

—Best Operational Support Provider \ 2006

—Best Operational Support Provider \ 2007

— Innovation of the Year \ 2008

—Best Operational Support Provider \ 2008

—Best Third Party Asset Valuation Provider \

2009

—Best Operational Support Provider \ 2009

—Best Third Party Asset Valuation Provider \

2010

—Best Third Party Asset Valuation Provider \

2011

GlobalCapital (Derivatives Intelligence)

—Data Vendor of the Year \ 2013

—Data Vendor of the Year \ 2014

Environmental Finance

—Best Registry Provider \ 2010

—Best Registry Provider \ 2011

—Best Registry Provider \ 2012

—Best Voluntary Carbon Registry \ 2013

—Best Voluntary Carbon Registry \ 2014

Financial News

—Best Data Solution \ Derivatives \ 2005

—Best Derivatives Provider \ 2006

—Best New Vendor Solution \ 2006

—Best Data Service \ 2008

—Best New Data Service \ 2013

—Most Innovative Compliance/ Risk Management

Service \ 2014

FOW

— Innovation for IT: Connectivity \ 2011

—Best Innovation by an ISV: Regulatory Change \

2013

Funds Europe

—European Middle Office Provider \ 2008

—European Middle Office Provider \ 2010

—European Middle Office Provider \ 2013

FX Week

—Vendor e-FX Initiative of the Year \ 2012

Global Investor

—Data Vendor of the Year \ 2008

—Data Firm of the Year \ 2009

Global Custodian

—Most innovative data provider \ 2013

—Best Market data provider \ 2014

HFM Week

—Best information and data vendor (US) \ 2013

—Best Research and data vendor (US) \ 2014

Inside Market Data

—Company to Watch \ 2006

—Most Innovative Market Data Product \ 2007

—Acquisition of the Year \ 2007

—Best New Data Product \ 2008

—Best Data Provider for Derivatives \ 2008

—Best Data Provider for Derivatives \ 2009

—Best Data Provider for Derivatives \ 2010

—Best New Data Provider \ 2014

Inside Reference Data

—Reference Data Provider of the Year \ 2006

—Best Reference Data Provider \ 2007

—Best Evaluated Prices Provider \ 2008

—Best EDM initiative \2009

—Best EDM initiative \ 2011

—Best Evaluated Prices Service Provider \ 2012

—Best Reference Data Provider \ 2012

—Best Evaluated Prices Service Provider \ 2013

—Best Reference Data Initiative \ 2013

Insurance Risk

—Best Data Management Service Provider \ 2012

ISR

—Editor’s Award for Innovation \ 2006

Markets Media

—Best CDS Data \ 2013

— Best Company \ 2014

Operations Management

—Vendor of the year \ 2005

—Operations Leader of the Year \ 2008

—Deal of the Year \ 2008

Profit & Loss

—Best Connectivity \ 2013

Sell-Side Technology

—Best Sell-Side Data Management Product \ 2013

— Sell-Side Technology Provider of the Year \ 2014

— Best Sell-Side Newcomer \ 2014

The Asset Investment Awards

—Rising Star Index Provider \ 2011

The Corporate Engagement Awards

—Best Sponsorship - Employee Engagement \ 2011

—Best Arts-Centred Corporate Sponsorship Activity \

2011

The Trade

—Outstanding Market data provider \ 2014

Waters Technology Rankings

—Best EDM Platform \ 2013

—Best Corporate Actions Service \ 2013

\ 31

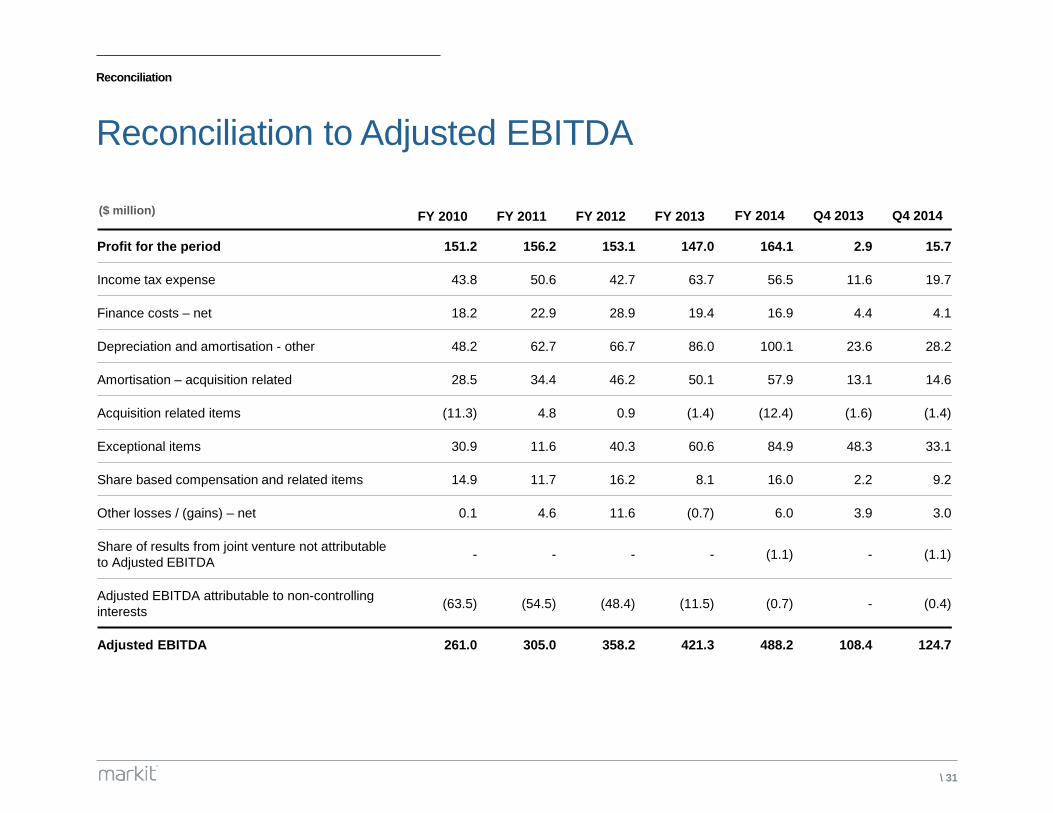

Reconciliation

Reconciliation to Adjusted EBITDA

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 Q4 2013 Q4 2014

Profit for the period 151.2 156.2 153.1 147.0 164.1 2.9 15.7

Income tax expense 43.8 50.6 42.7 63.7 56.5 11.6 19.7

Finance costs – net 18.2 22.9 28.9 19.4 16.9 4.4 4.1

Depreciation and amortisation - other 48.2 62.7 66.7 86.0 100.1 23.6 28.2

Amortisation – acquisition related 28.5 34.4 46.2 50.1 57.9 13.1 14.6

Acquisition related items (11.3) 4.8 0.9 (1.4) (12.4) (1.6) (1.4)

Exceptional items 30.9 11.6 40.3 60.6 84.9 48.3 33.1

Share based compensation and related items 14.9 11.7 16.2 8.1 16.0 2.2 9.2

Other losses / (gains) – net 0.1 4.6 11.6 (0.7) 6.0 3.9 3.0

Share of results from joint venture not attributable

to Adjusted EBITDA - - - - (1.1) - (1.1)

Adjusted EBITDA attributable to non-controlling

interests (63.5) (54.5) (48.4) (11.5) (0.7) - (0.4)

Adjusted EBITDA 261.0 305.0 358.2 421.3 488.2 108.4 124.7

($ million)

\ 32

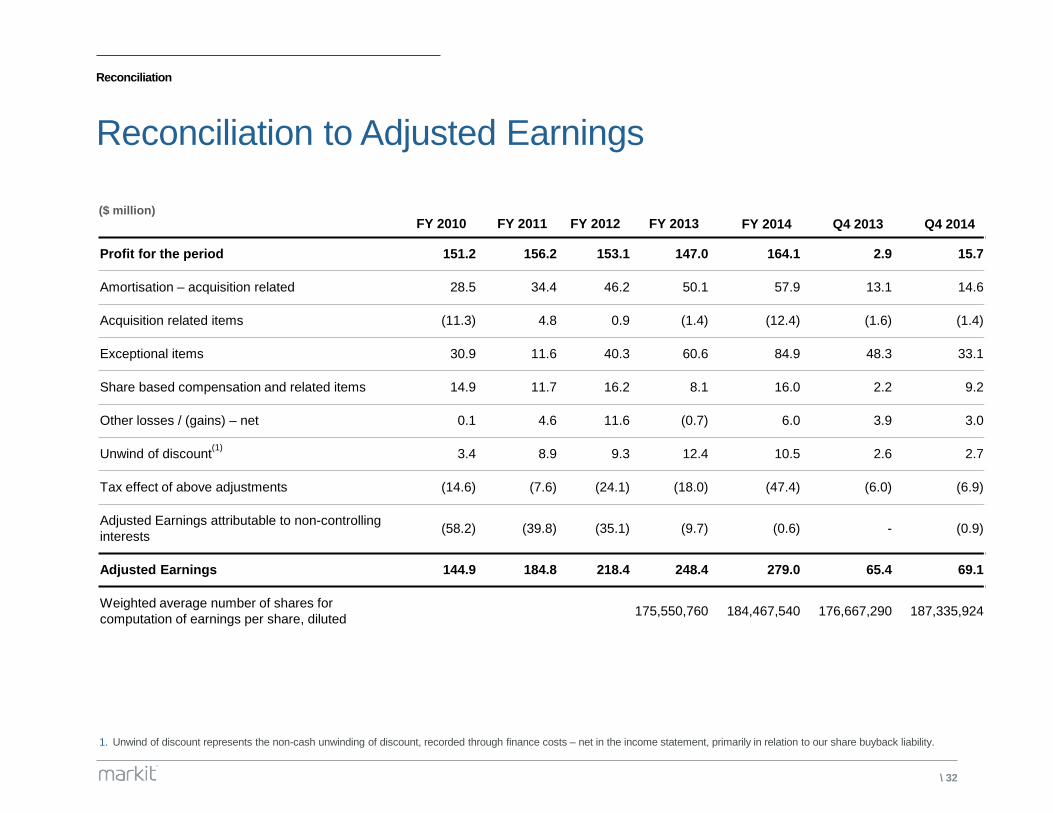

Reconciliation

Reconciliation to Adjusted Earnings

1. Unwind of discount represents the non-cash unwinding of discount, recorded through finance costs – net in the income statement, primarily in relation to our share buyback liability.

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 Q4 2013 Q4 2014

Profit for the period 151.2 156.2 153.1 147.0 164.1 2.9 15.7

Amortisation – acquisition related 28.5 34.4 46.2 50.1 57.9 13.1 14.6

Acquisition related items (11.3) 4.8 0.9 (1.4) (12.4) (1.6) (1.4)

Exceptional items 30.9 11.6 40.3 60.6 84.9 48.3 33.1

Share based compensation and related items 14.9 11.7 16.2 8.1 16.0 2.2 9.2

Other losses / (gains) – net 0.1 4.6 11.6 (0.7) 6.0 3.9 3.0

Unwind of discount(1)

3.4 8.9 9.3 12.4 10.5 2.6 2.7

Tax effect of above adjustments (14.6) (7.6) (24.1) (18.0) (47.4) (6.0) (6.9)

Adjusted Earnings attributable to non-controlling

interests (58.2) (39.8) (35.1) (9.7) (0.6) - (0.9)

Adjusted Earnings 144.9 184.8 218.4 248.4 279.0 65.4 69.1

Weighted average number of shares for

computation of earnings per share, diluted 175,550,760 184,467,540 176,667,290 187,335,924

($ million)

\ 33

Q4 and FY 2014 financial results

Definitions

Revenue growth We measure revenue growth in terms of organic revenue growth, acquisition related revenue growth, foreign currency impact on revenue growth and constant currency revenue growth. We

define these components as follows:

Organic – Revenue growth from continuing operations from factors other than acquisitions and foreign currency fluctuations. We derive organic revenue growth from the development of new

products and services, increased penetration of existing products and services to new and existing customers, price changes for our products and services and market driven factors such as

increased trading volumes or changes in customer assets under management.

Acquisition related – Revenue growth from acquired businesses through the end of the fiscal year following the fiscal year in which the acquisition was completed. This growth results from our

strategy of making targeted acquisitions that facilitate growth by complementing our existing products and services and addressing market opportunities.

Foreign currency – The impact on revenue growth resulting from the difference between current revenue at current exchange rates and current revenue at the corresponding prior period

exchange rates.

Constant currency – Total revenue growth, excluding the impact of exchange rate movements from the prior period to the current period. This is equal to the combination of organic and

acquisition related revenue growth, as described above.

Revenue by type Revenue by type is how we classify the income recognised from the sale of our products and services into three groups as defined below:

Recurring fixed revenue – Revenue generated from contracts specifying a fixed fee for services delivered over the life of the contract. The fixed fee is typically paid annually, semiannually or

quarterly in advance. These contracts are typically subscription contracts where the revenue is recognised across the life of the contract. The initial term of these contracts can range from one to

five years and usually includes auto-renewal clauses.

Recurring variable revenue – Revenue derived from contracts that specify a fee for services which is typically not fixed. The variable fee is typically paid monthly in arrears. Recurring variable

revenue is based on, among other factors, the number of trades processed, assets under management or the number of positions we value. Many of these contracts do not have a maturity

date while the remainder have an initial term ranging from one to five years.

Non-recurring revenue – Revenue that relates to certain software license sales and the associated consulting revenue.

Other Non-IFRS Measures Adjusted EBITDA is defined as profit for the period from continuing operations before income taxes, net finance costs, depreciation and amortisation on fixed assets and intangible assets

(including acquisition related intangible assets), acquisition related items, exceptional items, share based compensation and related items, net other gains or losses, including Adjusted EBITDA

attributable to joint ventures and excluding Adjusted EBITDA attributable to non-controlling interests.

Adjusted EBITDA margin is defined as Adjusted EBITDA divided by revenue, excluding revenue attributable to non-controlling interests.

LTM Adjusted EBITDA is defined as Adjusted EBITDA for the previous twelve month period from date reported.

Adjusted Earnings is defined as profit for the period from continuing operations before amortisation of acquired intangibles, acquisition related items, exceptional items, share based

compensation, net other gains or losses and unwind of discount, less the tax effect of these adjustments and excluding Adjusted Earnings attributable to non-controlling interests.

Adjusted EPS diluted is defined as Adjusted Earnings divided by the weighted average number of shares used to compute earnings per share, diluted.