investor presentation february 2012 - mol … and data contained in this presentation and the...

TRANSCRIPT

INVESTOR PRESENTATION

February 2012

DISCLAIMER

"T"This presentation and the associated slides and discussion contain forward-looking statements. These statements are naturallysubject to uncertainty and changes in circumstances. Those forward-looking statements may include, but are not limited to,th di it l l d it l dit h fl t i d bt d d d i ti di lthose regarding capital employed, capital expenditure, cash flows, costs, savings, debt, demand, depreciation, disposals,dividends, earnings, efficiency, gearing, growth, improvements, investments, margins, performance, prices, production,productivity, profits, reserves, returns, sales, share buy backs, special and exceptional items, strategy, synergies, tax rates,trends, value, volumes, and the effects of MOL merger and acquisition activities. These forward-looking statements are subjectto risks uncertainties and other factors which could cause actual results to differ materially from those expressed or implied byto risks, uncertainties and other factors, which could cause actual results to differ materially from those expressed or implied bythese forward-looking statements. These risks, uncertainties and other factors include, but are not limited to developments ingovernment regulations, foreign exchange rates, crude oil and gas prices, crack spreads, political stability, economic growth andthe completion of ongoing transactions. Many of these factors are beyond the Company's ability to control or predict. Giventhese and other uncertainties, you are cautioned not to place undue reliance on any of the forward-looking statements contained, y p y gherein or otherwise. The Company does not undertake any obligation to release publicly any revisions to these forward-lookingstatements (which speak only as of the date hereof) to reflect events or circumstances after the date hereof or to reflect theoccurrence of unanticipated events, except as maybe required under applicable securities laws.

Statements and data contained in this presentation and the associated slides and discussions, which relate to the performanceof MOL in this and future years, represent plans, targets or projections."

2

KEY FIGURESKEY FIGURES

bn USD EBITDA generation in 2011 (+18%), >70% from Upstream, >50% from international operation3

organic reserve replacement rate in last year2P reserves at 682 MMboe*

over

200%

Bboe Recoverable Resource Potential (WI) in 11 countriesmore than 50% in Kurdistan1.4

wells to be drilled in Kurdistan Region of Iraq in 2012-20139

t in European refinery ranking with the two largest assetshaving diesel gearing

Net debt / EBITDA ratio no additional financing need in 20121 4

top

5%

ExecutiveNet debt / EBITDA ratio, no additional financing need in 2012CAPEX should be fully financed by operating cash-flow

year MOL is in the Dow Jones Sustainability World Index

1.4

2nd

e summ

ary

3

uniquely in the region2nd

*MOL estimate

UPSTREAM-DRIVEN, INTEGRATED COMPANYOver 50% international contribution to USD 3bn EBITDA in 2011Over 50% international contribution to USD 3bn EBITDA in 2011

REGION EBITDA 2011 DATA 2011

► Field development driven growth in short ► 682 Mmboe* SPE 2P

GROWTH DRIVERS & COMPETITIVE ADVANTAGE

Ups

trea

m

p gterm (RUS)► Transforming of existing exploration assets to production in the mid term (KAZ)► Long term growth based on exploration-

reserves► 219%* organic reserve replacement ratio► 147 mboepd production► Production in 8,

led strategy (Kurdistan Region of Iraq)exploration in 12 countries

► Largest assets with high net cash margin► 5 refineries, 470 thbpd

Dow

nstr

eam

margin ► Strong landlocked market position

with outstanding captive market► Maintain leading position & improve

profitability: efficiency improvement

► 20.5 Mtpa sales

► 1,600+ filling stations

► 2 petrochemical plants RefineryRefineryPetchemPetchem unitunit

am

and reshape smaller assets

► Gas Transmission: 5,560 km pipeline in

► Growing international transit► Good geographical position

Executive

Gas

Mid

stre

a

MMBF UGS

► Gas Storage capacity: 1.9 bcm

, p pHungary

► Good geographical position

► Secured EUR-base return on storage

e summ

ary

4

Previous pipeline developments

*MOL estimate

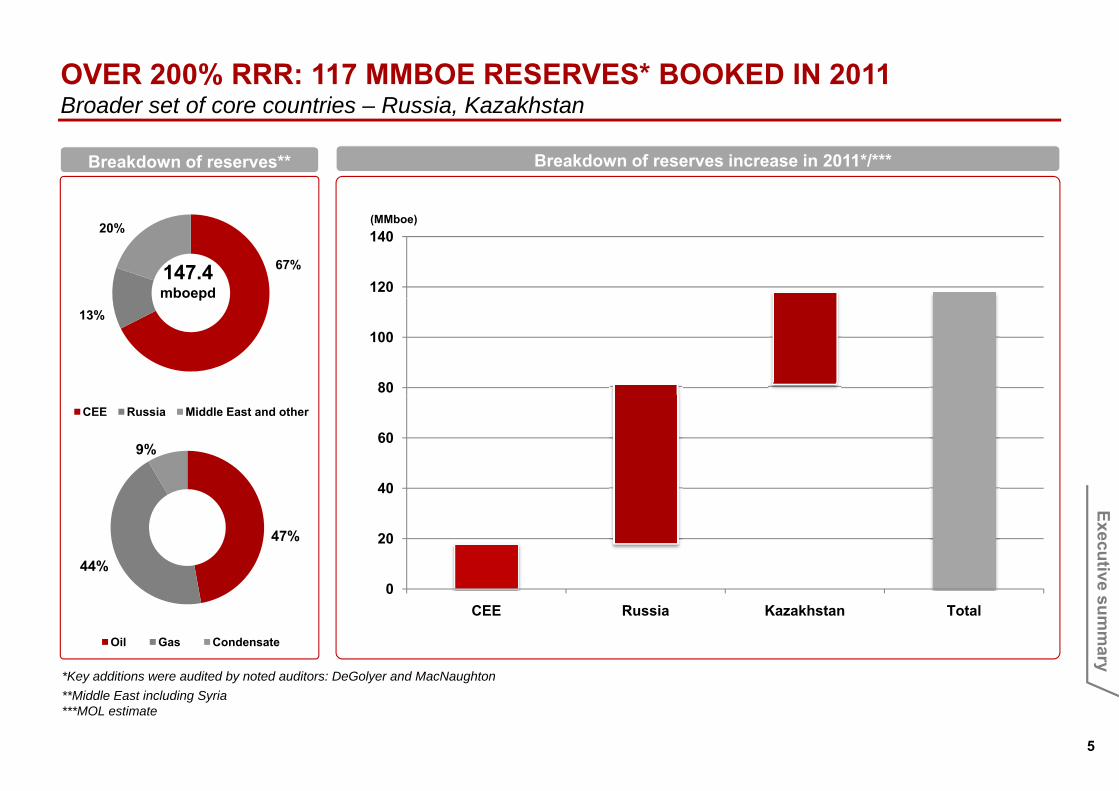

OVER 200% RRR: 117 MMBOE RESERVES* BOOKED IN 2011Broader set of core countries Russia KazakhstanBroader set of core countries – Russia, Kazakhstan

Breakdown of reserves increase in 2011*/***Breakdown of reserves**

120

140(MMboe)

67%

20%

147.4mboepd

80

10013%

p

40

609%

CEE Russia Middle East and other

0

20

40

47%

44%

Executive

0CEE Russia Kazakhstan Total

*Key additions were audited by noted auditors: DeGolyer and MacNaughton

Oil Gas Condensate

e summ

ary

5

**Middle East including Syria***MOL estimate

2012 PRODUCTION: 135 MBOEPD, IN NORMAL BUSINESS ENVIRONMENT3-4% production growth from 20143 4% production growth from 2014

Total hydrocarbon production by countries (mboepd)* Total hydrocarbon production by products (boepd)*

150 150150 150

100 100

50 50

-2012 2013 2014

02012 2013 2014

Executive

CEE Russia Middle East and other Oil Gas Condensate

Largest contributors Short term growth is expected from Russia

e summ

ary

6

*Middle East including Syria

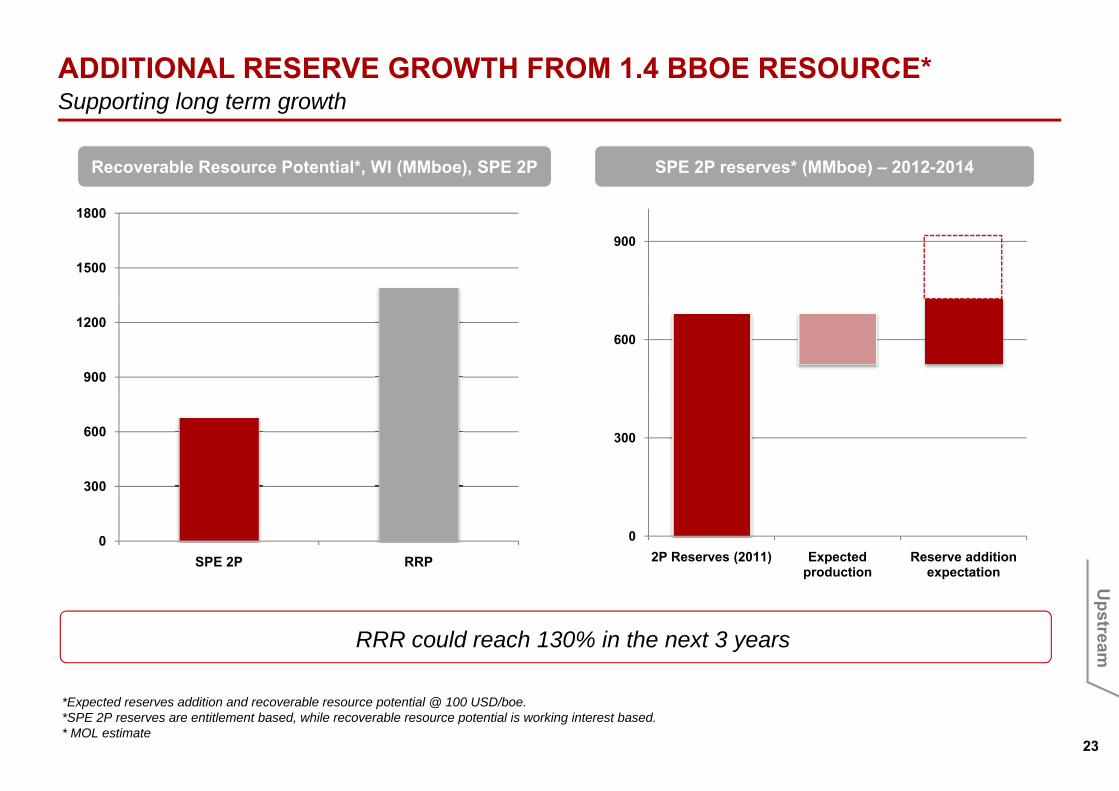

ADDITIONAL RESERVE GROWTH FROM 1.4 BBOE RESOURCE*Supporting long term growthSupporting long term growth

Recoverable Resource Potential*, WI (MMboe), SPE 2P SPE 2P reserves* (MMboe) – 2012-2014

900

1500

1800

600

900

1200

300

300

600

02P Reserves (2011) Expected

productionReserve addition

expectation

0SPE 2P RRP

Executive

Largest contributors

*Expected reserves addition and recoverable resource potential @ 100 USD/boe.

RRR could reach 130% in the next 3 years

e summ

ary

7

p p @*SPE 2P reserves are entitlement based, while recoverable resource potential is working interest based.* MOL estimate

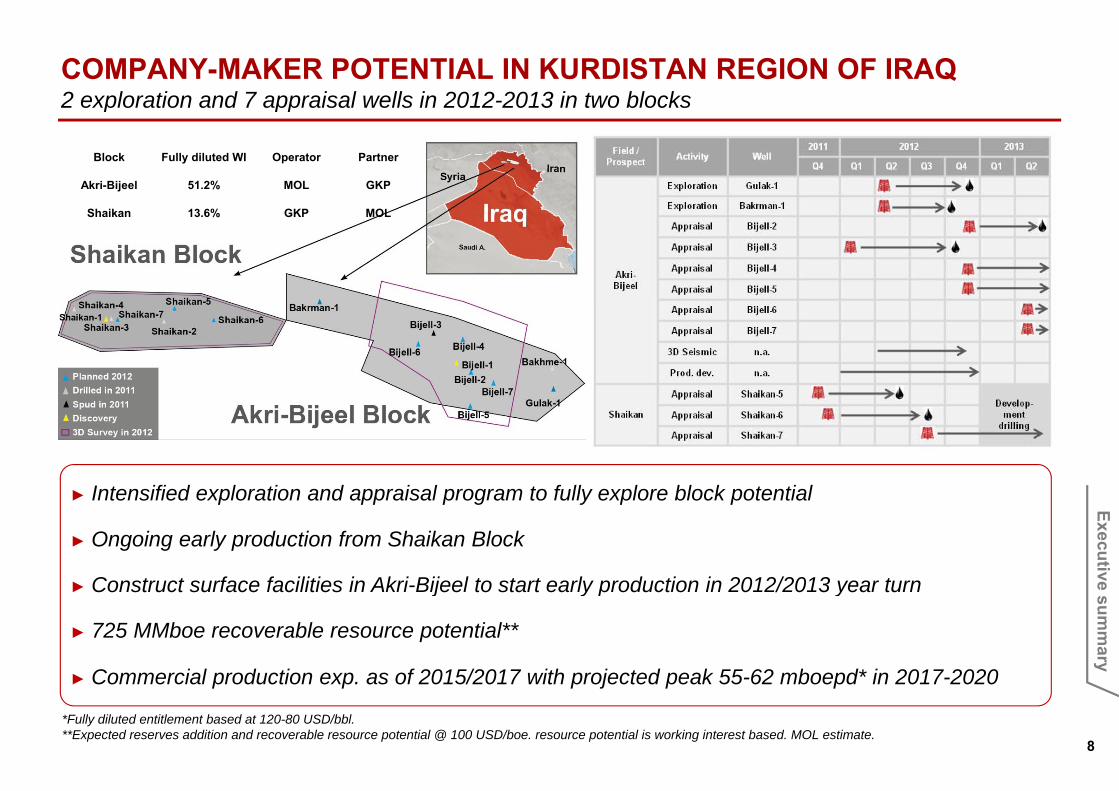

COMPANY-MAKER POTENTIAL IN KURDISTAN REGION OF IRAQ 2 exploration and 7 appraisal wells in 2012-2013 in two blocks2 exploration and 7 appraisal wells in 2012 2013 in two blocks

Block Fully diluted WI Operator Partner

Akri-Bijeel 51.2% MOL GKP

Shaikan 13.6% GKP MOL

► Intensified exploration and appraisal program to fully explore block potential

Largest contributors

► Intensified exploration and appraisal program to fully explore block potential

► Ongoing early production from Shaikan Block

► Construct surface facilities in Akri-Bijeel to start early production in 2012/2013 year turn

ExecutiveLargest contributors ► Construct surface facilities in Akri Bijeel to start early production in 2012/2013 year turn

► 725 MMboe recoverable resource potential**

► Commercial production exp. as of 2015/2017 with projected peak 55-62 mboepd* in 2017-2020

e summ

ary

8

p p p j p p

*Fully diluted entitlement based at 120-80 USD/bbl.**Expected reserves addition and recoverable resource potential @ 100 USD/boe. resource potential is working interest based. MOL estimate.

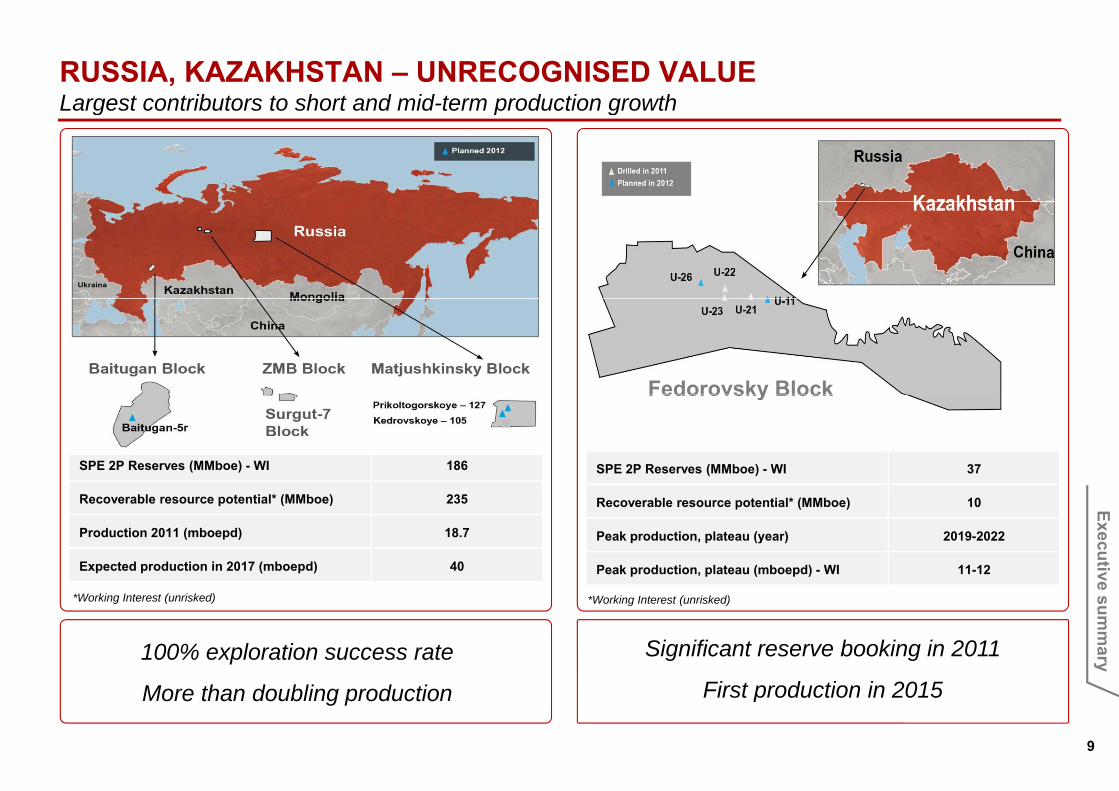

RUSSIA, KAZAKHSTAN – UNRECOGNISED VALUE Largest contributors to short and mid-term production growthLargest contributors to short and mid-term production growth

Largest contributors Fedorovsky Block

SPE 2P Reserves (MMboe) - WI 37SPE 2P Reserves (MMboe) - WI 186

Fedorovsky Block

Recoverable resource potential* (MMboe) 10

Peak production, plateau (year) 2019-2022

Peak production, plateau (mboepd) - WI 11-12

Recoverable resource potential* (MMboe) 235

Production 2011 (mboepd) 18.7

Expected production in 2017 (mboepd) 40

Executive

Largest contributors Largest contributors 100% exploration success rate

M th d bli d ti

*Working Interest (unrisked)

Significant reserve booking in 2011

First production in 2015

*Working Interest (unrisked)

e summ

ary

9

More than doubling production First production in 2015

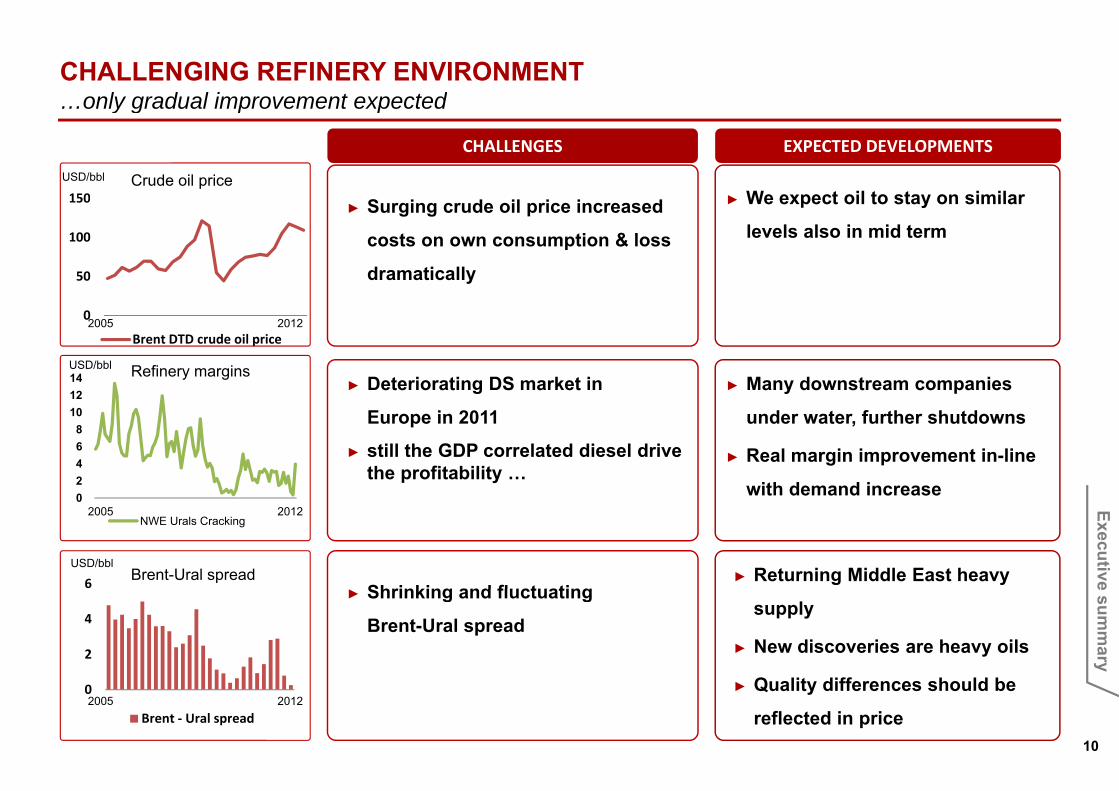

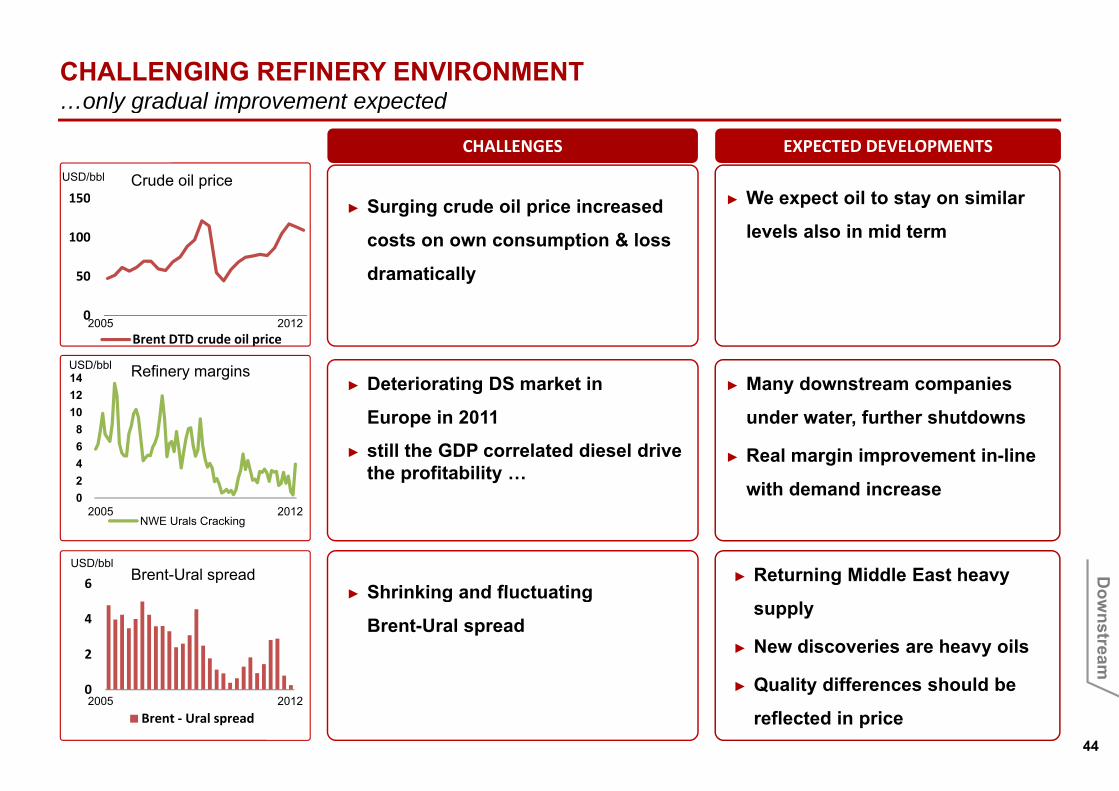

CHALLENGING REFINERY ENVIRONMENTonly gradual improvement expected…only gradual improvement expected

150

USD/bbl

S i d il i i d ► We expect oil to stay on similarCrude oil price

CHALLENGES EXPECTED DEVELOPMENTS

50

100

150► Surging crude oil price increased

costs on own consumption & loss

dramatically

► We expect oil to stay on similar

levels also in mid term

► Deteriorating DS market in 1214 Refinery marginsUSD/bbl

► Many downstream companies

0

Brent DTD crude oil price2005 2012

► still the GDP correlated diesel drive the profitability …

Europe in 2011

2468

1012

under water, further shutdowns

► Real margin improvement in-line

with demand increase0

NWE Urals Cracking

with demand increase

Shrinking and fluctuating► Returning Middle East heavy 6 Brent-Ural spread

USD/bbl

2005 2012 Executive

► Shrinking and fluctuating

Brent-Ural spread supply

► New discoveries are heavy oils

► Quality differences should be0

2

4

e summ

ary

10

► Quality differences should be

reflected in price0

Brent ‐ Ural spread2005 2012

DEMAND SUFFERS FROM ECONOMIC CRISIS, BUT…long term growth potential remains in the region…long term growth potential remains in the region

Gasoline demand changein %

SHORT TERM CRISIS EFFECT LONG TERM POTENTIAL REMAINS

Car penetration curve

► GRADUAL 500

600

700

800

ItalyFrance

AustriaGermany

C h RPoland

1,00

0 in

habi

tant

5

10

15

Gasoline demand changein % Car penetration curve

► Regional car penetration is still well bellow EU

IMPROVEMENT IN DIESEL PER CAPITA COMSUMPTION WITH

GDP GROWTH0

100

200

300

400 Czech Rep.

SlovakiaCroatia

RussiaRomania

Serbia

China

PakistanIndia HUNGARY

Car

s pe

r

10

-5

0

5average

► Room for additional gasoline demand

Hungary

0 5000 10000 15000 20000 25000 30000 35000 40000 45000

GDP per Capita (PPP in USD)

700

-102005 2006 2007 2008 2009 2010 2011

Domestic markets CEE region

Diesel demand changein % Diesel consumption per capita

300400500600700

5

10

15 ► GDP growth potential of the region remains

liter

/ ca

pita

Executive

0100200

-5

0

5

Domestic markets CEE region

► Significant additional diesel demand is expected in the CEE

e summ

ary

11

CEE North West Europe-102005 2006 2007 2008 2009 2010 2011

Domestic markets CEE region

Source: Woodmac and MOL estimates.

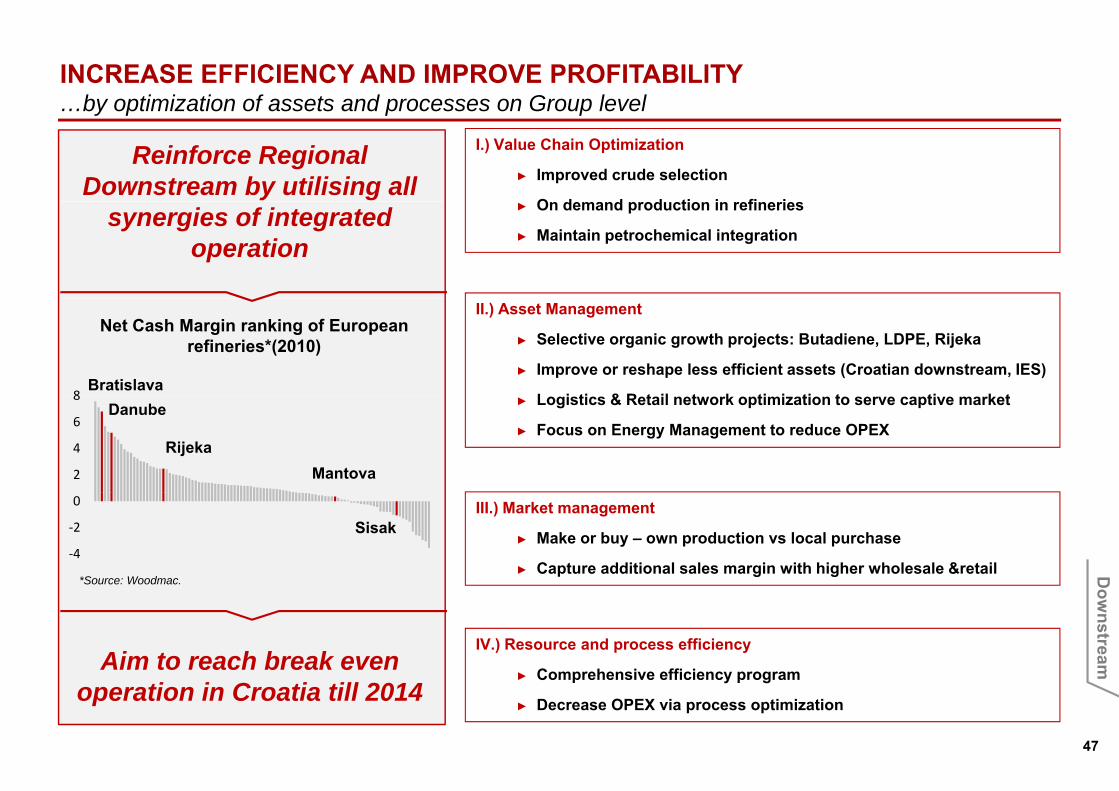

INCREASE EFFICIENCY AND IMPROVE PROFITABILITY by optimization of assets and processes on Group level…by optimization of assets and processes on Group level

Reinforce Regional Downstream by utilising all

I.) Value Chain Optimization

► Improved crude selection

O d d d ti i fi isynergies of integrated operation

► On demand production in refineries

► Maintain petrochemical integration

Net Cash Margin ranking of European refineries*(2010)

Bratislava8

II.) Asset Management

► Selective organic growth projects: Butadiene, LDPE, Rijeka

► Improve or reshape less efficient assets (Croatian downstream, IES)

L i ti & R t il t k ti i ti t ti k t

2

4

6

8Danube

RijekaMantova

► Logistics & Retail network optimization to serve captive market

► Focus on Energy Management to reduce OPEX

‐4

‐2

0

SisakIII.) Market management

► Make or buy – own production vs local purchase

► Capture additional sales margin with higher wholesale &retail *Source: Woodmac.

Executive

IV.) Resource and process efficiency

► Comprehensive efficiency programAim to reach break even ti i C ti till 2014

e summ

ary

12

► Decrease OPEX via process optimizationoperation in Croatia till 2014

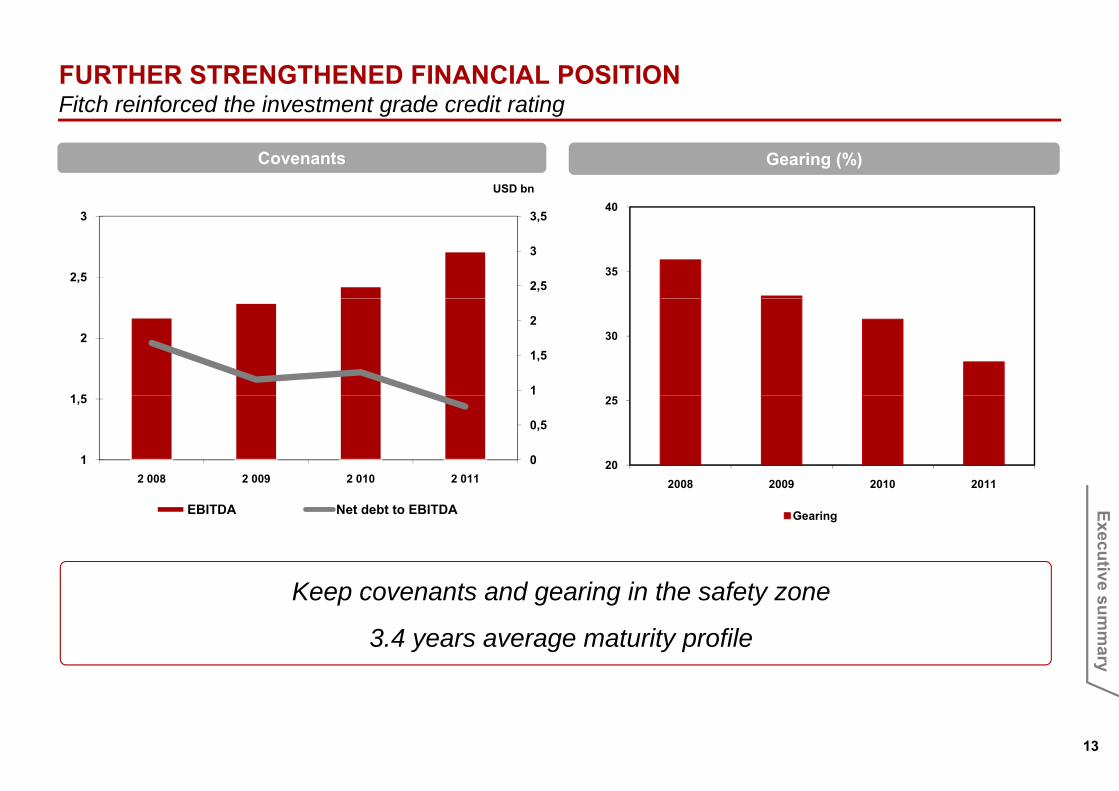

FURTHER STRENGTHENED FINANCIAL POSITIONFitch reinforced the investment grade credit rating

Covenants

Fitch reinforced the investment grade credit rating

USD bn

Gearing (%)

2,5

3

3,5

2,5

3

35

40

1

1,5

2

1 5

2 30

0

0,5

1

1,5

2 008 2 009 2 010 2 01120

25

2008 2009 2010 2011

EBITDA Net debt to EBITDA

Keep covenants and gearing in the safety zone

Gearing

Executive

Largest contributors Keep covenants and gearing in the safety zone

3.4 years average maturity profile

e summ

ary

13

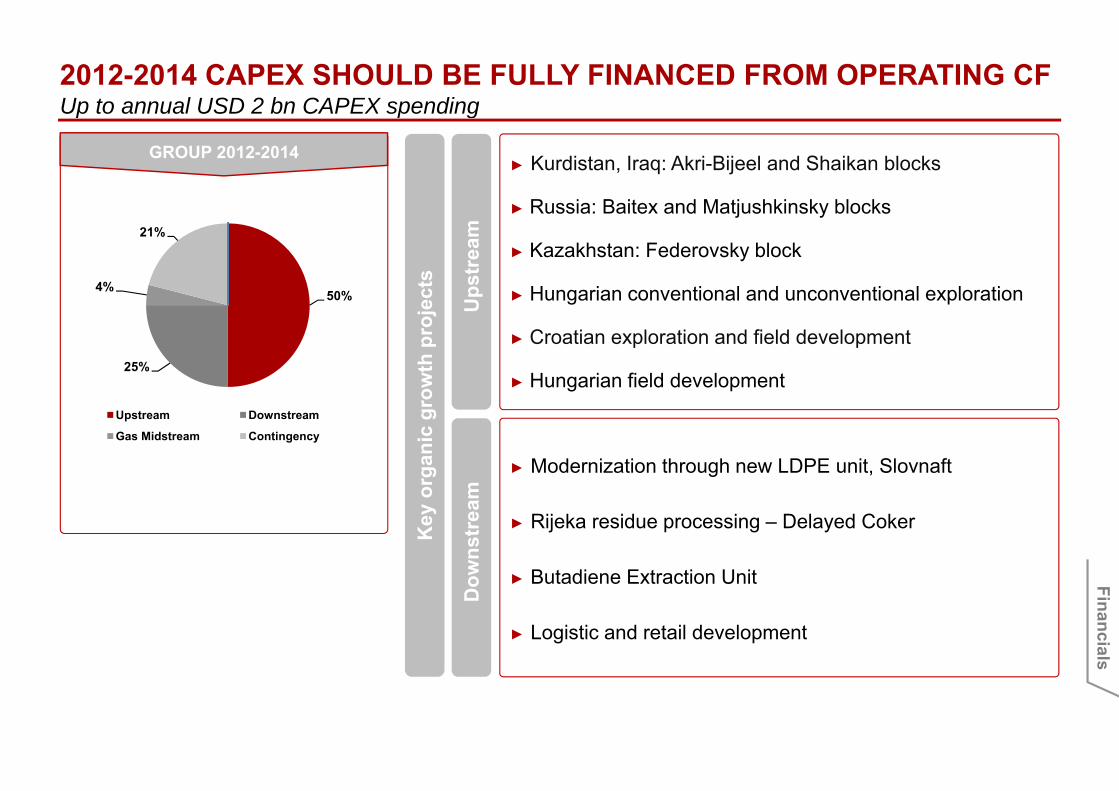

2012-2014 CAPEX SHOULD BE FULLY FINANCED FROM OPERATING CFUp to annual USD 2 bn CAPEX spending

► Kurdistan, Iraq: Akri-Bijeel and Shaikan blocks

R i B it d M tj hki k bl k

GROUP 2012‐2014

Up to annual USD 2 bn CAPEX spending

► Russia: Baitex and Matjushkinsky blocks

► Kazakhstan: Fedorovsky block

► Hungarian conventional and unconventional explorationpstr

eam

50%4%

21%

cts

► Hungarian conventional and unconventional exploration

► Croatian exploration and field development

► Hungarian field development

U50%

25%

owth

pro

je

m► Modernization through new LDPE unit, Slovnaft

Upstream Downstream

Gas Midstream Contingencyor

gani

c gr

o

Dow

nstr

eam

► Rijeka residue processing – Delayed Coker

► Butadiene Extraction Unit

Key

o Executive

D

► Logistic and retail development

e summ

ary

14

MOL is committed to Sustainable DevelopmentSUSTAINABILITY IS A TOP PRIORITY IN MOL GROUPThe only CEE company in Dow Jones Sustainability Index

position taken among European refineries in CO2-efficiency*Top 20% Climate Change

The only CEE company in Dow Jones Sustainability Index

decrease in lost-time injury frequency (LTIF) since 200644%Health & Safety

teams from 62 countries participated in MOL’s online competition aiming to attract best talents596Human Capital

recycling/reuse rate achieved in waste management 56%Environment

mn USD social investment projects in 2010 to supportlocal communities in the field of education, health, environment and culture~10Communities

Executive

average customer satisfaction level in Wholesalein core markets89%Economic sustainability

e summ

ary

15*excluding INA’s refineries

EXPLORATION AND PRODUCTIONFocus on exploration and active portfolio managementFocus on exploration and active portfolio management

Upstream

16

UPSTREAM – 75 YEARS EXPERIENCE AND OUTSTANDING EXPLORATION SUCCESS RATECompetitive advantagesCompetitive advantages

KEY STRENGTHS TO BUILD UPON

► Promising E&P portfolio

OUTSTANDING EXPLORATION SUCCESS RATE (2008-2011)

35No. of wells

► Organic growth on existing exploration portfolio

► Proven track record in successful portfolio development and project execution

1015202530

67%60%

► Leading European low cost on-shore producer

► MOL and INA complementary skill base

1930 1940 1950 1960 1970 1980 1990 201020092008200720062005

05

CEE InternationalTotal drillings Successful drilling

2011

Predeccessor of MOL started to explore hydrocarbons in the begining of 1930’ in Hungary

Using EOR/IOR techniques since 1970

1930 1940 1950 1960 20021970 1980 1990 201020092008200720062005 2011

First international production (Kazakhstan, 1993)

MOL built up a sizeable international portfolio

Increased multinational E&P portfolioIncreased multinational E&P portfolioand workforce with INA

Major project execution: the consortium, led by MOL provide 7-8% gas consumption of Pakistan

Major discoveries in Kurdistan Region of Iraq and Kazakhstan(2008-2010)

Upstream

1717

( )

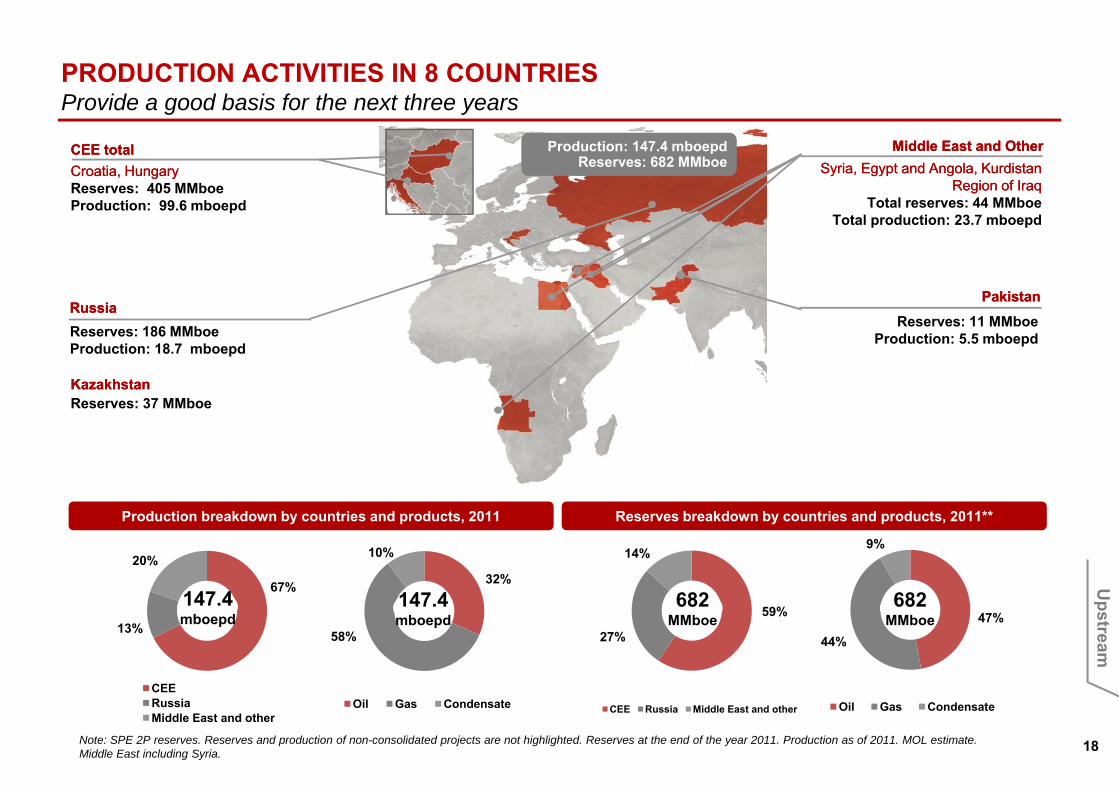

PRODUCTION ACTIVITIES IN 8 COUNTRIES Provide a good basis for the next three yearsProvide a good basis for the next three years

Croatia, HungaryCroatia, HungaryReserves: 405 MMboeP d ti 99 6 b d

CEE CEE totaltotal MiddleMiddle EastEast and and OtherOtherSyriaSyria, , EgyptEgypt and Angola, and Angola, KurdistanKurdistan

RegionRegion of of IraqIraqTotal reserves: 44 MMboe

Production: 147.4 mboepdReserves: 682 MMboe

Production: 99.6 mboepd

PakistanPakistan

Total reserves: 44 MMboeTotal production: 23.7 mboepd

Reserves: 186 MMboeProduction: 18.7 mboepd

Reserves: 11 MMboeProduction: 5.5 mboepd

PakistanPakistanRussiaRussia

KazakhstanKazakhstanReserves: 37 MMboe

Production breakdown by countries and products, 2011 Reserves breakdown by countries and products, 2011**

9%

67%

20%32%

10% 14%

47%

44%

67%

13%

CEE

58%

59%

27%

147.4mboepd

147.4mboepd

682MMboe

682MMboe

Upstream

18Note: SPE 2P reserves. Reserves and production of non-consolidated projects are not highlighted. Reserves at the end of the year 2011. Production as of 2011. MOL estimate.Middle East including Syria.

Oil Gas CondensateCEERussiaMiddle East and other

Oil Gas Condensate CEE Russia Middle East and other

1,4 BBOE* EXPLORATION POTENTIAL OF CURRENT ASSETSto secure organic mid-term growth

KazakhstanKazakhstan

RussiaRussia

to secure organic mid-term growthCEE onshore, offshore, CEE onshore, offshore, unconventionalunconventional

Matjushkinskiy, Surgut-7, Baitex BlocksHungary, Croatia, RomaniaHungary, Croatia, Romania

245280

KazakhstanKazakhstan

PakistanPakistan

Fedorovskoye Block

T l K k M l &Kurdistan Region of IraqKurdistan Region of Iraq 40

725 Tal, Karak, Margala & Margala North Blocks

Other InternationalOther International

Egypt Syria CameroonEgypt Syria Cameroon

Akri-Bijeel, Shaikan Blocks

110

725

Egypt, Syria, CameroonEgypt, Syria, Cameroon, , Angola, OmanAngola, Oman

Estimated recoverable resource potential*MMboe

Increasing exploration activity with new focus areas Recoverable resource potential*, MMboe (2012-2014)

USD mn Exploration CAPEXExploration CAPEX

160180200

1200

1500

20406080

100120140

0

300

600

900M

Mbo

e Upstream

19*Working Interest (unrisked). Exploration potential of current assets at the end of 2011.

02000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

International Hungary

0Kurdistan CEE CIS Pakistan Other Total Resources

UPSTREAM - POSITIONING AS A STRONG GROWTH PILLAR OF MOL GROUP Exploration-led strategy increasing reserve and maintaining production at elevated levelsExploration-led strategy, increasing reserve and maintaining production at elevated levels

I.) Dynamic exploration strategy

► Competency based target setting

IV.) Active management of the portfolio

► Most of our existing prospects will be drilled within three years

► Opening towards higher impact elements, aiming to add further elements to the portfolio

► a geographically and life-cycle-wise

► Continuous monitoring of inorganic growth opportunities

DevelopmentAA

SSP TP T

KZKZKKSS KAKA

CEE – Exploration Russian exploration (M)

Pakistan – Karak block

Kurdistan Region of Iraq – Akri Bijeel block

CECERDRD

EBITDA

CAPEX

P P AA

RERE

Discovery

Appraisal

MaturityOO

KKAA R R OO ZMBZMB

KZKZ

The majority of value creation RERE

P TP T

Kurdistan Region of Iraq – SShaikan block

Pakistan – Tal block

Russia – MOL’s operated portfolio

Kazakhstan

R R OO

KZKZ

KSKSUpstream cash cycleP P AA

CECE

j yhappens in exploration phase however the risk is also higher.

Dominantly geological, technical, political risks during the different phases

while marketability risk also appears

Time

AA

OO

ZMBZMB

Kazakhstan

Russia Development – Matyushinsky, Baitex

Russia – ZMB

CEE Onshore production

CEE Adriatic offshore

RDRD

y ppTime

SS Syria – Hayan block

III.) Focus on field development with short-term impactII.) Transforming of existing exploration assets to

production in the mid term

Upstream

2020

production in the mid-term

OVER 200% RRR: 117 MMBOE RESERVES* BOOKED IN 2011Broader set of core countries Russia KazakhstanBroader set of core countries – Russia, Kazakhstan

Breakdown of reserves increase in 2011*/***Breakdown of reserves**

120

140(MMboe)

67%

20%

147.4mboepd

80

10013%

p

40

609%

CEE Russia Middle East and other

0

20

40

47%

44%0

CEE Russia Kazakhstan Total

*Key additions were audited by noted auditors: DeGolyer and MacNaughton

Oil Gas Condensate

Upstream

21

**Middle East including Syria***MOL estimate

2012 PRODUCTION: 135 MBOEPD, IN NORMAL BUSINESS ENVIRONMENT3-4% production growth from 20143 4% production growth from 2014

Total hydrocarbon production by countries (mboepd)* Total hydrocarbon production by products (boepd)*

150 150150 150

100 100

50 50

-2012 2013 2014

02012 2013 2014

CEE Russia Middle East and other Oil Gas Condensate

Largest contributors Short term growth is expected from Russia

Upstream

22

*Middle East including Syria

ADDITIONAL RESERVE GROWTH FROM 1.4 BBOE RESOURCE*Supporting long term growthSupporting long term growth

Recoverable Resource Potential*, WI (MMboe), SPE 2P SPE 2P reserves* (MMboe) – 2012-2014

900

1500

1800

600

900

1200

300

300

600

02P Reserves (2011) Expected

productionReserve addition

expectation

0SPE 2P RRP

Largest contributors RRR could reach 130% in the next 3 years

Upstream

23

*Expected reserves addition and recoverable resource potential @ 100 USD/boe. *SPE 2P reserves are entitlement based, while recoverable resource potential is working interest based.* MOL estimate

KEY UPSTREAM PROJECTS

Upstream

24

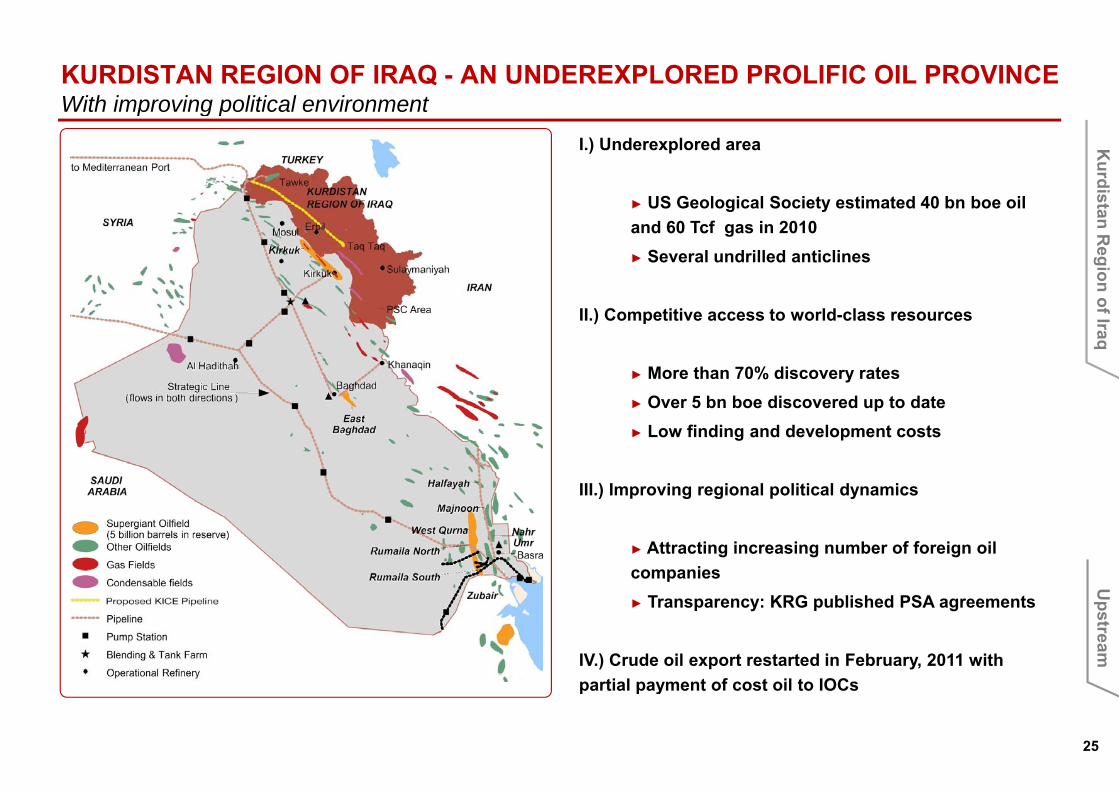

KURDISTAN REGION OF IRAQ - AN UNDEREXPLORED PROLIFIC OIL PROVINCE With improving political environmentWith improving political environment

I.) Underexplored area

► US Geological Society estimated 40 bn boe oil

Kurdis

► US Geological Society estimated 40 bn boe oil and 60 Tcf gas in 2010► Several undrilled anticlines

stanR

egion o

II.) Competitive access to world-class resources

► More than 70% discovery rates

of Iraq

► Over 5 bn boe discovered up to date► Low finding and development costs

III ) Improving regional political dynamicsIII.) Improving regional political dynamics

► Attracting increasing number of foreign oil companies ► Transparency: KRG published PSA agreements

IV.) Crude oil export restarted in February, 2011 with partial payment of cost oil to IOCs

Upstream

25

partial payment of cost oil to IOCs

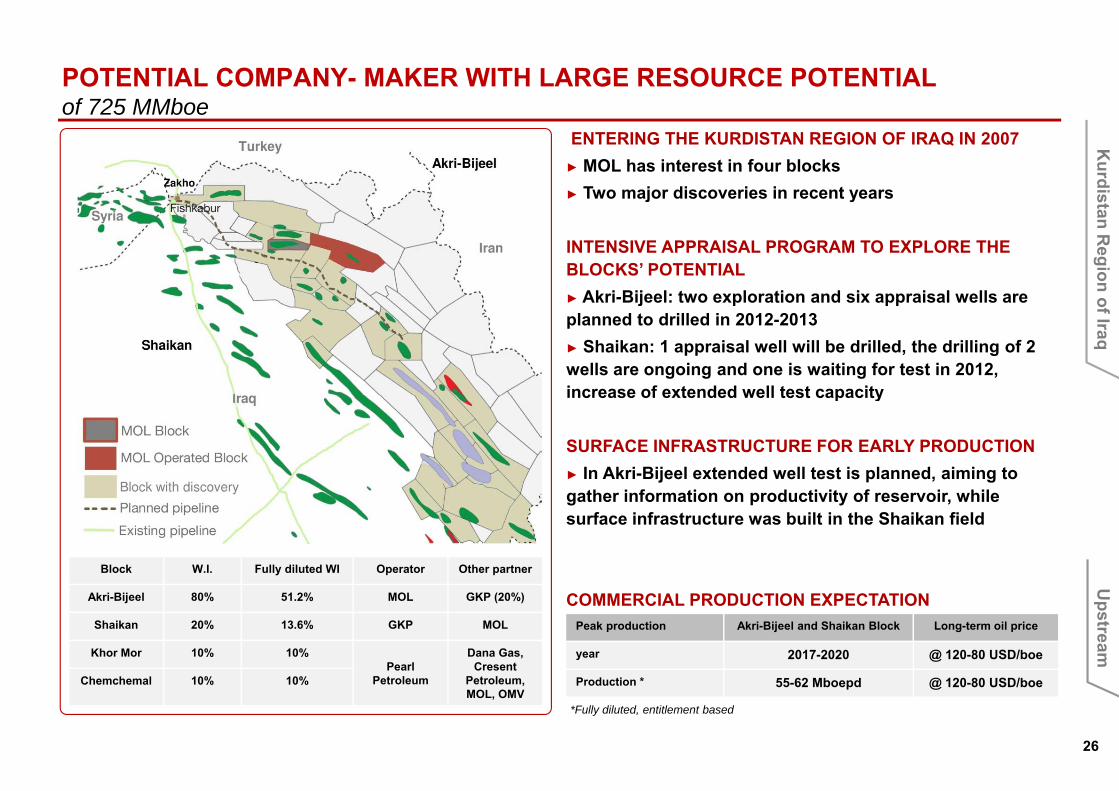

POTENTIAL COMPANY- MAKER WITH LARGE RESOURCE POTENTIALof 725 MMboeof 725 MMboe

ENTERING THE KURDISTAN REGION OF IRAQ IN 2007► MOL has interest in four blocks► Two major discoveries in recent years

Kurdisj y

INTENSIVE APPRAISAL PROGRAM TO EXPLORE THE BLOCKS’ POTENTIAL► Akri-Bijeel: two exploration and six appraisal wells are

stanR

egion o► Akri-Bijeel: two exploration and six appraisal wells areplanned to drilled in 2012-2013► Shaikan: 1 appraisal well will be drilled, the drilling of 2 wells are ongoing and one is waiting for test in 2012, increase of extended well test capacity

of Iraq

increase of extended well test capacity

SURFACE INFRASTRUCTURE FOR EARLY PRODUCTION► In Akri-Bijeel extended well test is planned, aiming to

th i f ti d ti it f i hilgather information on productivity of reservoir, while surface infrastructure was built in the Shaikan field

Block W.I. Fully diluted WI Operator Other partner

COMMERCIAL PRODUCTION EXPECTATIONAkri-Bijeel 80% 51.2% MOL GKP (20%)

Shaikan 20% 13.6% GKP MOL

Khor Mor 10% 10%Pearl

Petroleum

Dana Gas, Cresent

Petroleum, Chemchemal 10% 10%

Peak production Akri-Bijeel and Shaikan Block Long-term oil price

year 2017-2020 @ 120-80 USD/boe

Production * 55-62 Mboepd @ 120-80 USD/boe

Upstream

26

,MOL, OMV

55 62 Mboepd @ 120 80 USD/boe

*Fully diluted, entitlement based

TWO MAJOR DISCOVERIES IN THE LAST YEARS Shaikan and Akri Bijeel

HIGHLIGHTS

► In 2010 the Bijell-1 exploratory well showed very promising case hole test results from Jurassic formations with a daily test production of 3,700barrels of oil and 100 boe of gas, which gave the Group the prospect of a fields with an in place volume of 2.4 billions of barrels (OIIP).

Shaikan and Akri Bijeel

Kurdis

► The Shaikan Block is the scene of intense drilling after the discovery in 2009 of several billion barrels’ worth of heavy oil-in-place.

► After the discoveries was announced, the Kurdistan Regional Government gave permission to start the appraisal program of the fields.

stanR

egion o

SHAIKAN-1 BIJELL-1 SHAIKAN-3 SHAIKAN-2 BEKHME-1 SHAIKAN-4

SHAIKAN-5

SHAIKAN-6

► The preparation works for Extended well test were started in October 2010 for Shaikan discovery, and in 2011 for the Bijell-1 discovery.

of Iraq

1000m

SPUD27 April,

2009

SHAIKAN DISCOVERYAugust, 2009

2009 2010 2011

SPUD11 December,

2009

BIJELLDISCOVERYMarch, 2010

SPUD2 September,

2010

SPUD1 December,

2010

SPUD23 March,

2011

SPUD21 May,

2011

SPUDOct, 2011

SPUDDec, 2011

2000m

3000m

4000m

TOTAL DEPTH2,950m

November, 2009

TOTAL DEPTH1,518m

December, 2010

TOTAL DEPTH EXPECTED EST. EST.

MILESTONES

5000mTOTAL DEPTH

4,377mNovember, 2010

O3,300m

August, 2011TOTAL DEPTH

5,000mOctober ,2011

CTD:

3,400m

STD:

3,500m

STD:

3,800m

Upstream

27

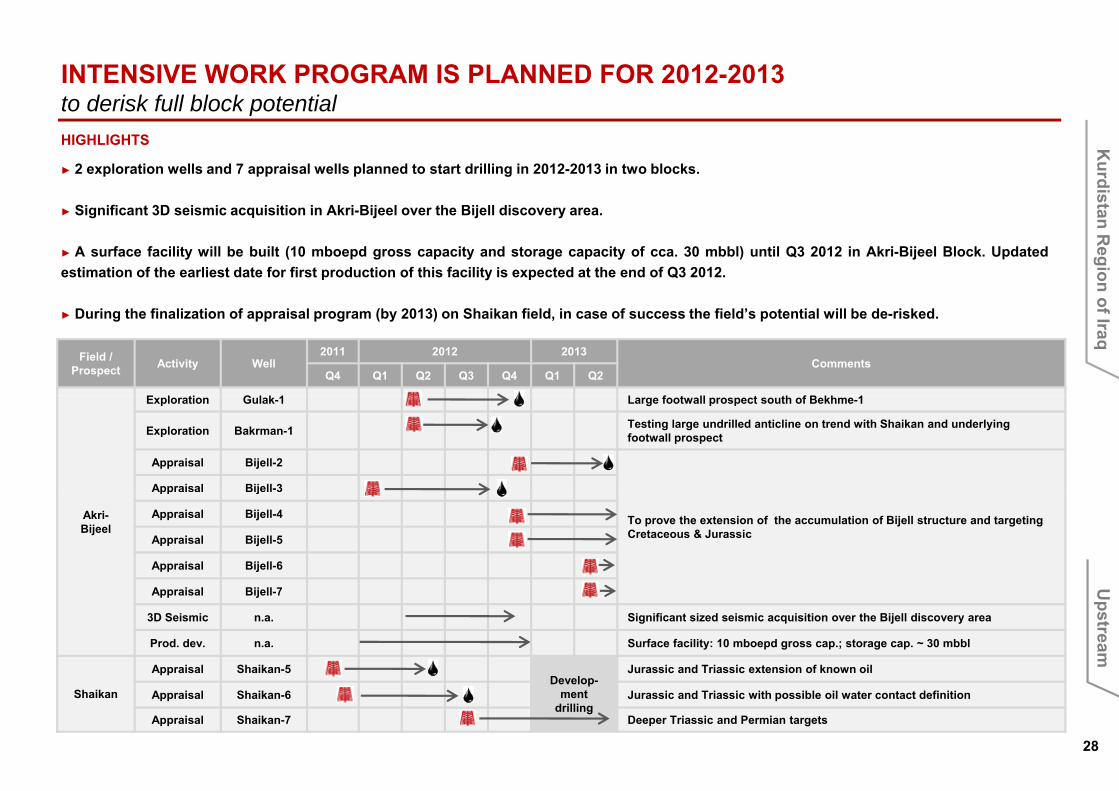

INTENSIVE WORK PROGRAM IS PLANNED FOR 2012-2013 to derisk full block potentialto derisk full block potentialHIGHLIGHTS

► 2 exploration wells and 7 appraisal wells planned to start drilling in 2012-2013 in two blocks.

Kurdis

► Significant 3D seismic acquisition in Akri-Bijeel over the Bijell discovery area.

► A surface facility will be built (10 mboepd gross capacity and storage capacity of cca. 30 mbbl) until Q3 2012 in Akri-Bijeel Block. Updatedestimation of the earliest date for first production of this facility is expected at the end of Q3 2012.

stanR

egion o

Field / Prospect Activity Well

2011 2012 2013Comments

Q4 Q1 Q2 Q3 Q4 Q1 Q2

► During the finalization of appraisal program (by 2013) on Shaikan field, in case of success the field’s potential will be de-risked.

of Iraq

Exploration Gulak-1 Large footwall prospect south of Bekhme-1

Exploration Bakrman-1 Testing large undrilled anticline on trend with Shaikan and underlying footwall prospect

Appraisal Bijell-2

Appraisal Bijell-3

Akri-Bijeel

To prove the extension of the accumulation of Bijell structure and targeting Cretaceous & Jurassic

pp j

Appraisal Bijell-4

Appraisal Bijell-5

Appraisal Bijell-6

A i l Bij ll 7Appraisal Bijell-7

3D Seismic n.a. Significant sized seismic acquisition over the Bijell discovery area

Prod. dev. n.a. Surface facility: 10 mboepd gross cap.; storage cap. ~ 30 mbbl

Appraisal Shaikan-5Develop-

Jurassic and Triassic extension of known oil

Upstream

28

Shaikanp

ment drilling

Appraisal Shaikan-6 Jurassic and Triassic with possible oil water contact definition

Appraisal Shaikan-7 Deeper Triassic and Permian targets

PLANNED WORK PROGRAM FOR 2012PLANNED WORK PROGRAM FOR 2012

Kurdisstan

Region oof Iraq

Upstream

29

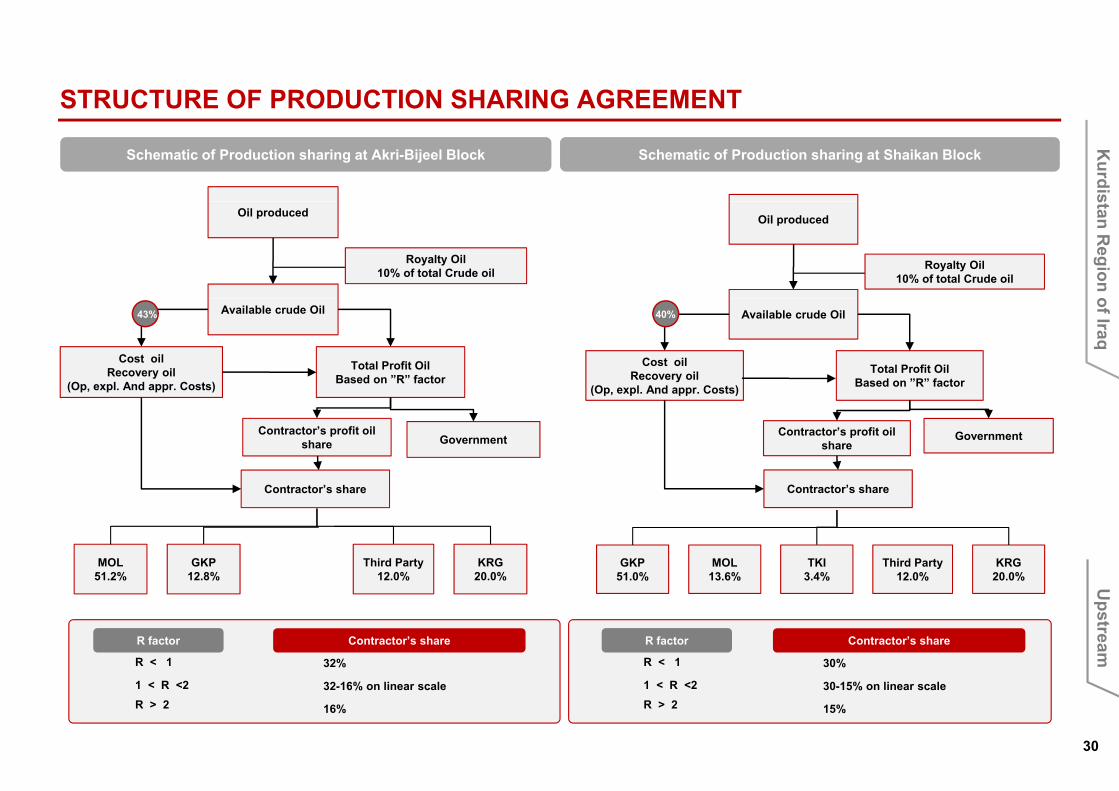

STRUCTURE OF PRODUCTION SHARING AGREEMENTSTRUCTURE OF PRODUCTION SHARING AGREEMENT

Schematic of Production sharing at Akri-Bijeel Block Schematic of Production sharing at Shaikan Block

Kurdis

Oil produced

Royalty Oil10% of total Crude oil

Oil produced

Royalty Oil10% of total Crude oil

stanR

egion o

Available crude Oil

Cost oilRecovery oil

(Op, expl. And appr. Costs)

Total Profit OilBased on ”R” factor

Available crude Oil

Cost oilRecovery oil

(Op, expl. And appr. Costs)

Total Profit OilBased on ”R” factor

43% 40%

of Iraq

Contractor’s profit oil share Government

( p, p pp )

Contractor’s profit oil share

Government

Contractor’s share Contractor’s share

MOL51.2%

GKP12.8%

Third Party12.0%

KRG20.0%

GKP51.0%

MOL13.6%

TKI3.4%

Third Party12.0%

KRG20.0%

Contractor s share Contractor s share

Contractor’s shareR factor

R < 1 30%

1 < R <2 30 15% on linear scale

Contractor’s shareR factor

R < 1 32%

1 < R <2 32 16% on linear scale

Upstream

30

1 < R <2 30-15% on linear scale

15%R > 21 < R <2 32-16% on linear scale

16%R > 2

RUSSIA – CORE COUNTRY WITH SHORT AND MID TERM PRODUCTION GROWTHIntensive work program in the coming yearsIntensive work program in the coming years

EXPERIENCES► Primary target region: Volga-Ural, Western Siberia►10 years experience ensures technical capability in field development-rejuvenation and exploration

FOUR BLOCKS IN DIFFERENT PROJECT PHASES –SIGNIFICANT UNDEVELOPED RESOURCE/RESERVE

► ZMB: developed field (mature) cash cow”

Russia

► ZMB: developed field (mature) – „cash-cow”► Baitugan field: under development – low risk, exploration► Matyushkinsky block: under development and intensive exploration

2P reserves (2011): 186 MMboeProduction (2011): 18.7 mboepd

intensive exploration► Surgut-7: exploration block

INTENSIFICATION OF PRODUCTION ( ) p

Estimated recoverable resource potential: 235 MMboeExpected production in 2017: 40 mboepd

OPERATIONAL COST REDUCTION

POSITIVE CHANGE IN LEGISLATION (60/66)Block W.I. Operator Other partner

ZMB 50% Russneft MOL (50%) 2012-2014► Our plan to spend USD 150-200 mn CAPEX yearly for field development and exploration.► It is expected that MOL will drill yearly 50-60 production and injection wells and yearly 2 3 exploration wells in the

ZMB 50% Russneft MOL (50%)

Baitugan 100% MOL -

Matjushkinsky 100% MOL -

Surgut-7 100% MOL -

Upstream

31

and injection wells and yearly 2-3 exploration wells in the next 3 years*Working Interest (unrisked)

MATYUSHINSKY BLOCK Exploration upside: 7 10 prospects

BAITEX BLOCKSignificant reserves accessible for production

Russia

Legend

Oil field

Block boundary

Exploration upside: 7-10 prospects Significant reserves accessible for production

RussiaOil pipeline

Gas pipeline

Transneft pipeline

Russia

The Komalkariver

Road

0 10 20 30 40 50km

0 10 20 30 miles

Baitugan FieldBaitugan OTU

The Baltuganriver

Acquired by MOL plc in Dec, 2006Operator : MOL, 100%2P reserves: 112 MMbbl (2011)2011 production: 4.8 mboepdOil quality: 26 0 API

Acquired by MOL plc in April, 2007Operator: MOL, 100%2P reserves: 28 MMbbl (2011)2011 production: 3.3 mboepdOil quality: 34 0 API

Planned pipeline in 2012 (40km)Further pipeline construction

Central Processing StationTransneft pipeline is located 90 km from the Central Processing Station.

Transneft pipeline is located on Western part of the field, The field is connected tothe oil pipeline .

Oil wellOil gathering unit

License area border

Transneft pipeline

Upstream

32

Oil quality: 26 API

Area: Western Siberia, with sizable acreage (3,200 km2) Area: Volga-Ural region (70 km2)

Oil quality: 34 API g

MATYUSHINSKY BLOCK Exploration upside: 7 10 prospects

BAITEX BLOCKSignificant reserves accessible for productionExploration upside: 7-10 prospects

COMPLEX BLOCK► Sizeable acreage► Producing assets: 46 production and 8 injection wells in two fields► However in recent years MOL found three oil fields and identified 7-10

INTENSIVE DEVELOPMENT RESULTED RESERVES BOOKING► An intense construction and investment program was launched in 2007 with the goal of fully rehabilitating the field (more than 200 production and injection wells)

Significant reserves accessible for production

► However in recent years MOL found three oil fields and identified 7 10 prospects which will be further explored in the next years

INTENSIVE DEVELOPMENT TO RAMP UP PRODUCTION► 100% exploration success rate with three wells

Oil d ti f 0 6 b d (2007) t 4 4 b d (Q4 2011)

injection wells)► Oil production increased from 1.8 mboepd (2007) to 4.9 mboepd (Q4 2011). ► Due to newly gained data during the production intensification, the closing SPE 2P reserves significantly (81%) increased in 2011 y-o-y

DECLINING COSTS OF OPERATION IN THE RECENT YEARS

Russia

► Oil production up from 0.6 mboepd (2007) to 4.4 mboepd (Q4 2011) ► It is expected that MOL will drill yearly 20-30 production wells to increase production, pipeline construction (40 km)

HUGE EXPLORATION POTENTIAL

DECLINING COSTS OF OPERATION IN THE RECENT YEARS► Baituganskoye oilfield is located in one of Russia’s most developed oil and gas province► Shallow, compact field with developed infrastructure support low energy and operational costs

Ledovoye 101 (M)Kvartovoye-11 (M)

Prikoltogorskoye (M) Baitugan-5r (B)

Kedrovoye (M)

Verkhne Laryeganskoy (M)

► Due to the sizeable acreage at least 7-10 undrilled prospects► MOL plans to drill 2-3 exploration wells yearly UPSIDE POTENTIAL

► Further exploration potential in deeper zones

7-10.th Exploration

ll (M B)

1000m

Ledovoye-101 (M)

SPUDFebruary,

2008

2008 2010 2012SPUDApril, 2008

Prikoltogorskoye (M), Baitugan-5r (B)

SPUDFebr, 2012

SPUDMarch, 2012

SPUDFebruary,

2013

2009 2011 2013 2014

Verkhne Laryeganskoy (M)

SPUDApril, 2011

Verkhne

wells (M,B)

SPUDNov, 2012

1000m

3000m

TOTAL DEPTH

LedovoyeDISCOVERY

July, 2008

TOTAL DEPTH

KvartovoyeDISCOVERYNovember,

2008EXPECTED

TD:EST.TD:

EST.TD:

TOTAL DEPTH2860m

Verkhne Laryeganskoye

DISCOVERYAug, 2011

EST.TD:

It is expected that MOL will drill 100-150 production and injection wells to increase

significantly the production level in the next three years.

Upstream

33

DEPTH2722mMarch, 2008

DEPTH3054mJune, 2008

TD:2900-3500m

TD:3365m 2960mMay, 2011 2960m

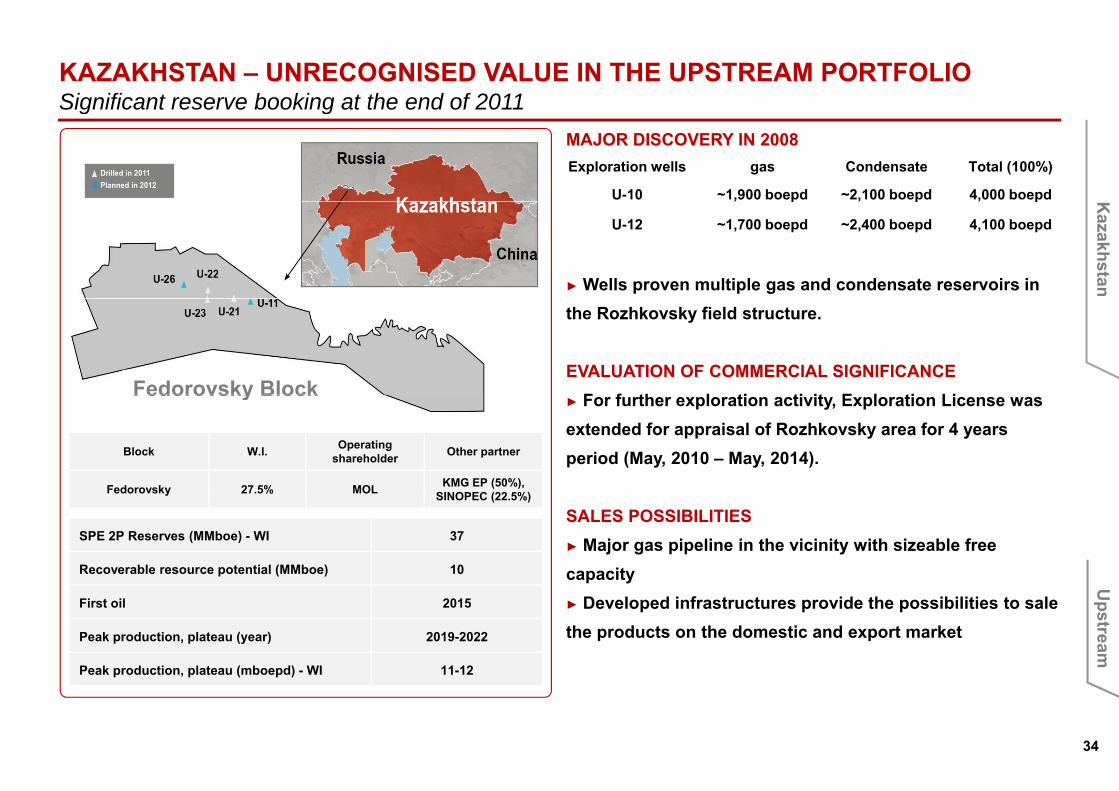

KAZAKHSTAN – UNRECOGNISED VALUE IN THE UPSTREAM PORTFOLIOSignificant reserve booking at the end of 2011

Exploration wells gas Condensate Total (100%)

U-10 ~1,900 boepd ~2,100 boepd 4,000 boepd

Significant reserve booking at the end of 2011MAJOR DISCOVERY IN 2008

, p , p , p

U-12 ~1,700 boepd ~2,400 boepd 4,100 boepd

► Wells proven multiple gas and condensate reservoirs in

Kazakhstan

the Rozhkovsky field structure.

EVALUATION OF COMMERCIAL SIGNIFICANCEF f th l ti ti it E l ti LiFedorovsky Block

► For further exploration activity, Exploration License was extended for appraisal of Rozhkovsky area for 4 years period (May, 2010 – May, 2014).Block W.I. Operating

shareholder Other partner

Fedorovsky 27.5% MOL KMG EP (50%), SINOPEC (22 5%)

Fedorovsky Block

SALES POSSIBILITIES► Major gas pipeline in the vicinity with sizeable free capacity

Fedorovsky 27.5% MOL SINOPEC (22.5%)

SPE 2P Reserves (MMboe) - WI 37

Recoverable resource potential (MMboe) 10

► Developed infrastructures provide the possibilities to sale the products on the domestic and export market

First oil 2015

Peak production, plateau (year) 2019-2022

Peak production, plateau (mboepd) - WI 11-12

Upstream

34

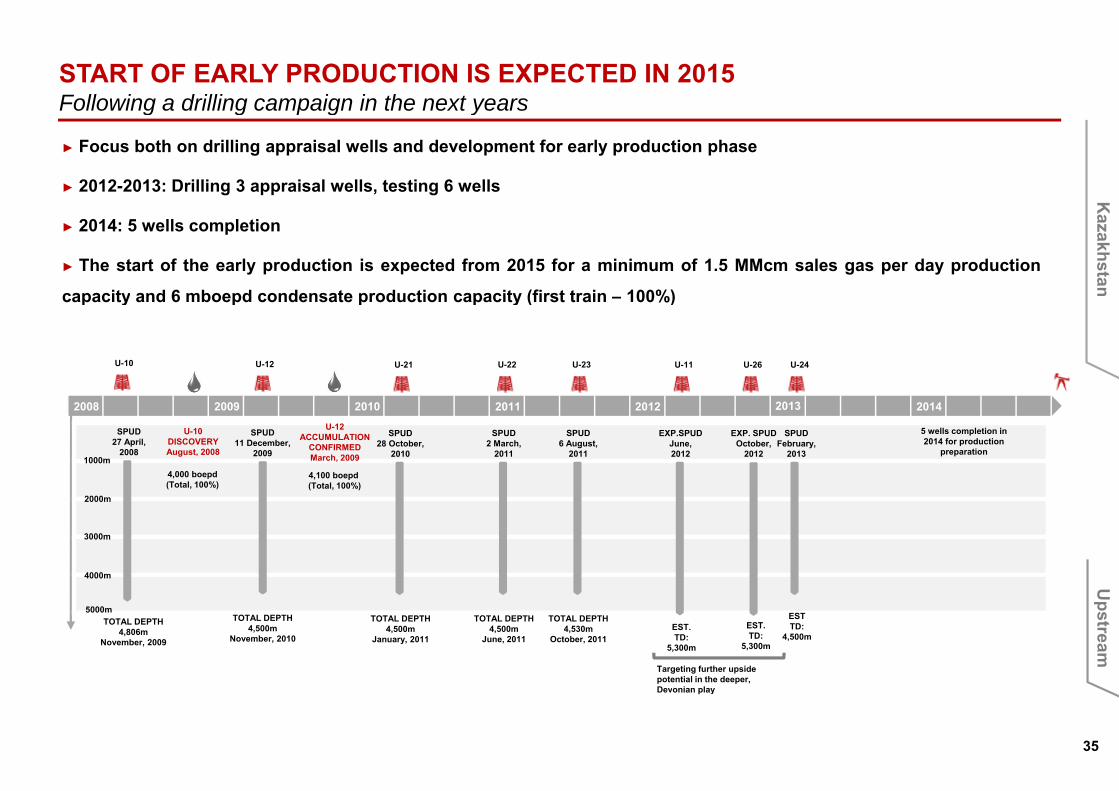

START OF EARLY PRODUCTION IS EXPECTED IN 2015 Following a drilling campaign in the next yearsFollowing a drilling campaign in the next years

► Focus both on drilling appraisal wells and development for early production phase

► 2012-2013: Drilling 3 appraisal wells, testing 6 wells

► 2014: 5 wells completion

► The start of the early production is expected from 2015 for a minimum of 1.5 MMcm sales gas per day production

capacity and 6 mboepd condensate production capacity (first train – 100%)

Kazakhstan

capacity and 6 mboepd condensate production capacity (first train – 100%)

U-10 U-12 U-21 U-11 U-26 U-24U-22 U-23

1000m

SPUD27 April,

2008

U-10 DISCOVERYAugust, 2008

2008 2010 2012

SPUD11 December,

2009

U-12ACCUMULATION

CONFIRMEDMarch, 2009

SPUD28 October,

2010

EXP.SPUDJune, 2012

EXP. SPUDOctober,

2012

SPUDFebruary,

2013

2009 2011 2013 2014

SPUD2 March,

2011

SPUD6 August,

2011

4,000 boepd(Total, 100%)

4,100 boepd(Total, 100%)

5 wells completion in 2014 for production

preparation

2000m

3000m

4000m

5000mTOTAL DEPTH

4,806mNovember, 2009

TOTAL DEPTH4,500m

November, 2010

TOTAL DEPTH4,500m

January, 2011

ESTTD:

4,500mEST.TD:

5,300m

EST.TD:

5,300m

TOTAL DEPTH4,500m

June, 2011

TOTAL DEPTH4,530m

October, 2011

Targeting further upside potential in the deeper,

Upstream

35

Devonian play

PAKISTAN – INTENSIVE SIMULTANEOUS ACTIVITY FROM EXPLORATION TO PRODUCTIONOutstanding exploration success over the last 11 yearsOutstanding exploration success over the last 11 years

TAL BLOCK

► The aim is to continue appraisal activity on recent

di i (M iKh l M i M k i E ddiscoveries (MamiKhel, Maramzai, Makori East and

Tolanj) and to continue exploration of remaining

potential of the block.

Increase reserve base and production in the next years

Pakistan

► Increase reserve base and production in the next years

► Increase capacity of the surface facilities to be able to

handle growing production

2P reserves (2011): 11 MMboeProduction (2011): 5.5 mboepd

KARAK BLOCK

► Oil discovery in Q4 2011 (1,700 bbl/d; - 100% WI)

► 2012-2013: tie-in of well to early production, drilling ofEstimated recoverable resource potential* targeted 40 MMboeEstimated peak production*: 17-18 mboepd between 2017-2020

► 2012 2013: tie in of well to early production, drilling of

1 appraisal well

MARGALA AND MARGALA NORTHBlock W.I. Operator Other partner

Tal 10% (expl.) MOL PPL, OGDCL,

*Working Interest (unrisked)

► Interpretation of ongoing 2D seismics

► In case of prospectivity, drilling of 1 exploration well

8.42% (dev.) POL, GHPL

Karak 40% Mari Gas MOL (40%)

Margala, MN 70% MOL POL (30%)

Upstream

36

Working Interest (unrisked)

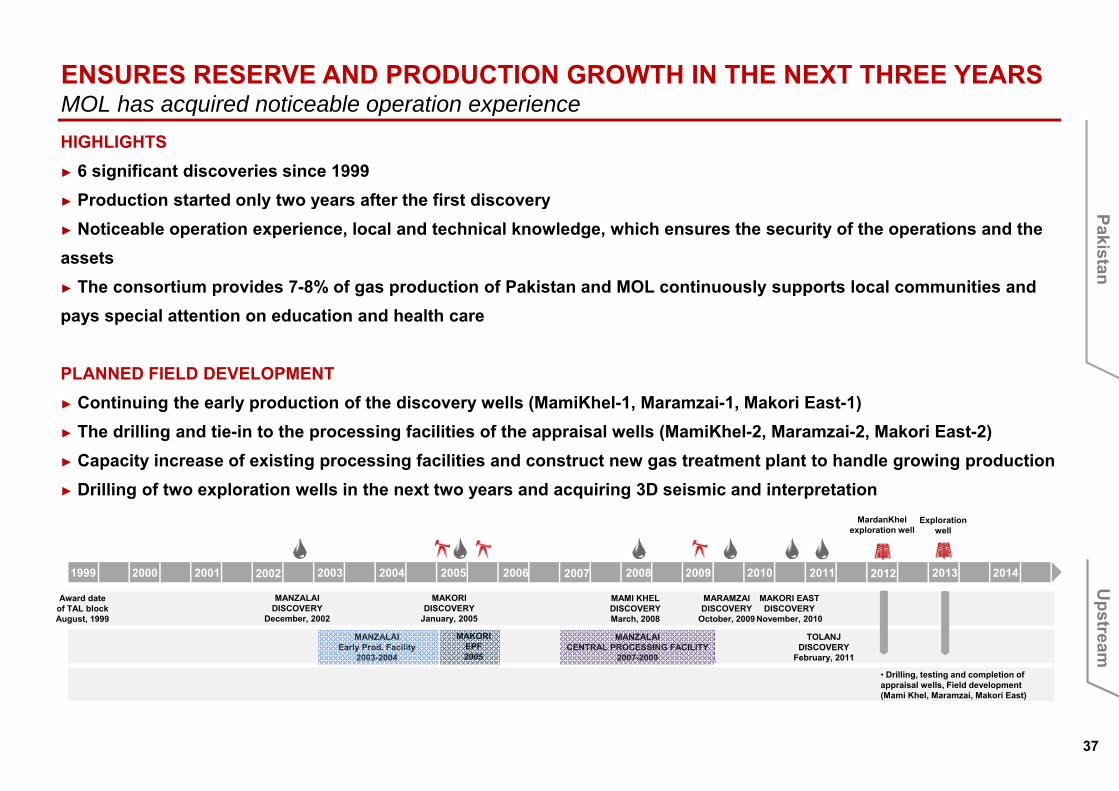

ENSURES RESERVE AND PRODUCTION GROWTH IN THE NEXT THREE YEARS MOL has acquired noticeable operation experienceHIGHLIGHTS► 6 significant discoveries since 1999► Production started only two years after the first discovery

MOL has acquired noticeable operation experience

► Production started only two years after the first discovery► Noticeable operation experience, local and technical knowledge, which ensures the security of the operations and the assets ► The consortium provides 7-8% of gas production of Pakistan and MOL continuously supports local communities and

Pakistan

pays special attention on education and health care

PLANNED FIELD DEVELOPMENT► Continuing the early production of the discovery wells (MamiKhel-1, Maramzai-1, Makori East-1)► The drilling and tie-in to the processing facilities of the appraisal wells (MamiKhel-2, Maramzai-2, Makori East-2) ► Capacity increase of existing processing facilities and construct new gas treatment plant to handle growing production► Drilling of two exploration wells in the next two years and acquiring 3D seismic and interpretation

1999

MardanKhelexploration well

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exploration well

► Drilling of two exploration wells in the next two years and acquiring 3D seismic and interpretation

Award date of TAL blockAugust, 1999

MANZALAIDISCOVERY

December, 2002

MAKORIDISCOVERY

January, 2005

MAMI KHELDISCOVERYMarch, 2008

MARAMZAIDISCOVERY

October, 2009

MAKORI EASTDISCOVERY

November, 2010

TOLANJDISCOVERY

February, 2011

MANZALAIEarly Prod. Facility

2003-2004

MAKORIEPF2005

MANZALAICENTRAL PROCESSING FACILITY

2007-2009

• Drilling, testing and completion of appraisal wells Field development

Upstream

37

appraisal wells, Field development (Mami Khel, Maramzai, Makori East)

CEE: MAXIMIZE RECOVERY RATES FROM EXISTING FIELDS AND MITIGATE DECLINE RATEOnshore and offshore field development (2012)Onshore and offshore field development (2012)

FIELD DEVELOPMENTS AND EOR/IOR PROJECTS

► ~130 producing fields

CEEp g

► 14 field developments in progress

► 20 new field development projects

E -Developm

► EOR project implementation in the next years

► 20-25 new field development projects,

20 25 MMb dditi l t ti l

ment

FIELD DEVELOPMENTS AND EOR/IOR PROJECTS

► close to 60 producing fields

► 20-25 MMboe additional reserve potential2011 reserves* (SPE 2P): 405 MMboeProduction (2011): 99.6 mboepdCAPEX (2012): USD 255 mn

► close to 60 producing fields

► 5 new wells (three new wells and two new reentry wells)

► EOR project implementation on Ivanic and Zutica fields:

► Close to USD 100 mn investments in the next 3 years► Close to USD 100 mn investments in the next 3 years

► Increasing total production volume by 3.4 million tons

of oil and 600 million cubic meters of gas in the

following 2 decades (total: 28 MMboe) by

Upstream

38

g ( ) y

*MOL estimate

280 MMBOE TARGETED RECOVERABLE RESOURCE POTENTIAL CEE exploration (2012) – outstanding success ratio in the region

► Number of licenses, acreage exposure: 33; 37,400 km2

► 2012: 13 conventional and 3 tight gas (unconventional) drillings and tests

CEE exploration (2012) outstanding success ratio in the region

CE

► 2 3D seismic measurements► Exploration expenditure for 2012 (USD mn): ~USD 133 mn► Plan to secure acreage position in the next years as majority of the licenses will expire by 2013

E -Exploratiexpire by 2013

► Number of licenses, acreage exposure: 5; 41,876 km2

► Drilling 6 wells (included 1unconventional) and 1 well: Zalata-1 East in Hungary (INA 50%)

ion

(INA 50%).► Offshore-drilling: 3 wells are expected; Ilena-1 Dir, Ivna-1 (optional) and Irina SW (optional), study program to prepare following drilling campaign► Plan to regain the exploration licenses as INA remains the only entity currently in Croatia which has the necessary equipment experience knowledge and projects

► 70% MOL operator (after ratification by state), 30% Expert Petroleum ► Number of licenses acreage exposure: 3; 3 400 km2

Croatia, which has the necessary equipment, experience, knowledge and projects prepared ready to drill to accelerate exploration activities

► Number of licenses, acreage exposure: 3; 3,400 km2

► Blocks are located in the vicinity of successful Hungarian fields► Compulsory work program (2012-2014):

► 600 km of 2D seismic,

Upstream

39

► 1700km2 of 3D seismic ► 19 exploration wells (including unconventional well)

UNCONVENTIONAL: TEST COMMERCIAL PRODUCTION AT DERECSKE BASINDrilling an other exploration well to increase proven hydrocarbon volumeDrilling an other exploration well to increase proven hydrocarbon volume

Derecske Basin

TIGHT GAS PROJECT WAS INTENSIFIED IN 2010

► Drilling of two wells (Beru-4, Beru-3).

CEE -

1

B 1

Beru-4

Beru 6

2

2

Beru-ÉNy-1

Zala Basin

Drava Basin Makó Basin

Békés Basin ► MOL found (Beru-4) the expected formation in the targetzone with strong gas shows.

IN 2011-2012 THE FOCUS IS

i ) th b tt iti f th b i ith t t f

-Unconvent

2

3

Beru-1

Beru-2

Beru-M-1

Beru-3

Beru-6

Beru-7i.) the better position of the basin with test for

commerciality proved by fracturing (Beru-4)

ii.) and drilling to increase proved hydrocarbonvolume (Beru-6).

tional

( )

► The fracturing of the formation was finalized byHalliburton in Q4 2011. Well test and pilot production isexpected in H1 2012.

1 – Földes-East - Field analogyTargets of exploration program:2 – Structural prospects3 – Non - structural position

Beru-2 Drilled wells Beru-7 Planned wells

Beru-6 Well under drilling

Beru-4 Under FracturingBeru-ÉNy-1 Alternate plan

of Beru-7

► In 2012 the exploration program aims to continue theevaluation of unconventional potential with drilling of two(Beru-7, Beru-M-1) and testing of one (Beru-6) well.

IN CASE OF SUCCESSIN CASE OF SUCCESS

► In the next years MOL will explore the potential of thebasis, while in case of success production could startaround 2015-2017.

► MOL focuses on the smaller, but more promisingDerecske basin in the vicinity of already producingwells.

Upstream

40

SYRIA – IN LINE WITH SANCTIONS MAINTAINING ECONOMIC INTEREST Negative effects due to tightening sanctions and security issuesNegative effects due to tightening sanctions and security issues

TIGHTENING US AND EU SANCTIONS DURING 2011-2012► Embargo on Syrian oil export

Two production cuts in September and December 2011► Two production cuts in September and December 2011 in a sum of 2.8 mboepd due to the local requirements► The restrictive measures might have additional adverse effects.

Syria

Production (2011): 20.3 mboepd, NEGATIVE EFFECT OF THE RESTRICTIVE MEASURES► Encountering significant obstacles in the collection of

Hayan Block: development phase, 100% INA; operator

Aphamia Block: exploration phase, 100% INA

receivables from the Syrian partner for its share of hydrocarbon production; ► There has been no improvement in this situation since October 2011.

CURRENT SECURITY SITUATION► Adapting the numbers of its staff to the current security

EXPLORATION AND FIELD DEVELOPMENT

► Exploration activity started in 1998 and was completed in 2007.

First oil production started in 2005 on Jihar Field, first gas

production started in 2006 on Palmyra Field. ► Adapting the numbers of its staff to the current security situation: temporarily withdraw the employees who are not required for the continuation of the daily operations

PEAK PRODUCTION IN 2011

► Gas Treatment Plant operating from 2011, resulting in significant

increase in oil, condensate and gas production.

Upstream

41

DOWNSTREAMReinforce Regional Stronghold PositionReinforce Regional Stronghold Position

Dow

nstream

42

TWO LARGEST ASSETS WITH HIGH COMPLEXITYIntegrated operation in adjacent marketsIntegrated operation in adjacent markets

KEY STRENGTH

► Strong land-locked market presence – 21% motor fuel

market share in the CEE

► Region-wide Logistics, Wholesale and Retail network serve

the market - above 55% end-user share

Mantova

Bratislava

Danube

Sisak

Rij k

3%9%

23%4%

6%4%4%

LPGNaphthaMototre GasolineMiddle Distillates

y yi

eld

2012

E

over 80%hit dRijeka

48%

Fuel OilBitumenOtherOther chemical prds.

Refining Logistics

Ref

iner

y

Marketing

white prd.

Retail Network• 1,600+ FS• 3.5 Mt total fuel sales• Avrergae throughput: 2.7 Mlpa

RefiningWholesale

• 19 Mt external sales • 21% regional market share• Market leader in 4 countries

Logistics

Refinery Mtpa thbpd NCI

MOL Group 23.5 470 9.9

Danube 8 1 161 10 6

Marketing

D

g g p p• 18% captive market for refineries

1.5 Mt external sales volume

• 27% end-user sales

Petrochemicals

Capacity (ktpa) TVK SPC

Danube 8.1 161 10.6

Bratislava 6.1 122 11.5

Rijeka 4.5 90 9.1

Mantova 2 6 52 8 4

Key

fact

s

Logistics

ownstream

43

13% captive market for RefiningEthylene 660 220

Polymer 765 435

Mantova 2.6 52 8.4

Sisak 2.2 44 6.1

CHALLENGING REFINERY ENVIRONMENTonly gradual improvement expected…only gradual improvement expected

150

USD/bbl

S i d il i i d ► We expect oil to stay on similarCrude oil price

CHALLENGES EXPECTED DEVELOPMENTS

50

100

150► Surging crude oil price increased

costs on own consumption & loss

dramatically

► We expect oil to stay on similar

levels also in mid term

► Deteriorating DS market in 1214 Refinery marginsUSD/bbl

► Many downstream companies

0

Brent DTD crude oil price2005 2012

► still the GDP correlated diesel drive the profitability …

Europe in 2011

2468

1012

under water, further shutdowns

► Real margin improvement in-line

with demand increase0

NWE Urals Cracking

with demand increase

Shrinking and fluctuating► Returning Middle East heavy 6 Brent-Ural spread

USD/bbl

2005 2012

D

► Shrinking and fluctuating

Brent-Ural spread supply

► New discoveries are heavy oils

► Quality differences should be0

2

4

ownstream

44

► Quality differences should be

reflected in price0

Brent ‐ Ural spread2005 2012

DEMAND SUFFERS FROM ECONOMIC CRISIS, BUT…long term growth potential remains in the region…long term growth potential remains in the region

Gasoline demand changein %

SHORT TERM CRISIS EFFECT LONG TERM POTENTIAL REMAINS

Car penetration curve

► GRADUAL 500

600

700

800

ItalyFrance

AustriaGermany

C h RPoland

1,00

0 in

habi

tant

5

10

15

Gasoline demand changein % Car penetration curve

► Regional car penetration is still well bellow EU

IMPROVEMENT IN DIESEL PER CAPITA COMSUMPTION WITH

GDP GROWTH0

100

200

300

400 Czech Rep.

SlovakiaCroatia

RussiaRomania

Serbia

China

PakistanIndia HUNGARY

Car

s pe

r

10

-5

0

5average

► Room for additional gasoline demand

Hungary

0 5000 10000 15000 20000 25000 30000 35000 40000 45000

GDP per Capita (PPP in USD)

700

-102005 2006 2007 2008 2009 2010 2011

Domestic markets CEE region

Diesel demand changein % Diesel consumption per capita

300400500600700

5

10

15 ► GDP growth potential of the region remains

liter

/ ca

pita

D

0100200

-5

0

5

Domestic markets CEE region

► Significant additional diesel demand is expected in the CEE

ownstream

45

CEE North West Europe-102005 2006 2007 2008 2009 2010 2011

Domestic markets CEE region

Source: Woodmac and MOL estimates.

LONG-TERM TENDENCIES JUSTIFY COMPLEXITY AND DIESEL FOCUSFavourable balance of landlocked CEE marketFavourable balance of landlocked CEE market

5

Supply-Demand Balance - 2012 / 2016 / 2020(including refinery and bio supply in Mt) Supply-Demand Balance of the CEE region

‐5

0

North-West Europe

GasolineDiesel22 28 31

-16 -29 -26

3 4 4

‐15

‐10

Gasoil Balance Gasoline Balance

CEE- MOL’s Core region

3 4 4

-7 -8 -10

16 18 18

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

Other Mediterranean*-30 -29 -29

► Diesel demand supported by favourable long term regional GDP growth

► Increasing diesel shortage provides room for further mid-term diesel projects (Rijeka DC, Duna HCK) D

Largest contributors

► Stable gasoline surplus requires keeping existing flexibility through refining-petrochemical integration (new LDPE unit)

ownstream

46Source: Woodmac and MOL estimates.

INCREASE EFFICIENCY AND IMPROVE PROFITABILITY by optimization of assets and processes on Group level…by optimization of assets and processes on Group level

Reinforce Regional Downstream by utilising all

I.) Value Chain Optimization

► Improved crude selection

O d d d ti i fi isynergies of integrated operation

► On demand production in refineries

► Maintain petrochemical integration

Net Cash Margin ranking of European refineries*(2010)

Bratislava8

II.) Asset Management

► Selective organic growth projects: Butadiene, LDPE, Rijeka

► Improve or reshape less efficient assets (Croatian downstream, IES)

L i ti & R t il t k ti i ti t ti k t

2

4

6

8Danube

RijekaMantova

► Logistics & Retail network optimization to serve captive market

► Focus on Energy Management to reduce OPEX

‐4

‐2

0

SisakIII.) Market management

► Make or buy – own production vs local purchase

► Capture additional sales margin with higher wholesale &retail *Source: Woodmac.

D

IV.) Resource and process efficiency

► Comprehensive efficiency program

ownstreamAim to reach break even

ti i C ti till 2014

47

► Decrease OPEX via process optimizationoperation in Croatia till 2014

SELECTIVE INVESTMENTS TO MAINTAIN LEADING POSITION…and improve profitability…and improve profitability

LOGISTICS AND RETAIL INVESTMENTS Growth in high margin captive market

Largest contributors ► New logistics, depots ensure better market reach

► Retail investments focuses on growth markets and sites with favourable position

SELECTIVE PETROCHEMICAL DEVELOPMENTS Ensure flexibility & capture profitable niche segment

Largest contributors

Exploit high margin butadiene market

► New 130 ktpa butadiene unit: caa. EUR 100 mn CAPEX; ~EUR 50 mn EBITDA improvement

Maintain synergies from Refining – Petrochemicals integration

► Shut down 3 old subscale LDPE units new 220 ktpa LDPE unit CAPEX: cca EUR 260 mn► Shut down 3 old, subscale LDPE units, new 220 ktpa LDPE unit, CAPEX: cca EUR 260 mn

► Increased flexibility - higher naphtha off-take from refineries (plus cca. 120 ktpa)

Aim to reach break-even operation till 2014 with gradual improvementCROATIAN DOWNSTREAM D

Largest contributors

► Short term efficiency actions: OPEX cut, logistics & retail network rationalization► On-demand operation of refineries

N i li ti b t fi i f fl ibl ti ti

p g p ownstream

48

► New pipeline connection between refineries for flexible, synergetic operation► Preparation for residue disruption (new Coker unit)

FOCUSING ON MOST PROFITABLE SALES IN KEY LANDLOCKED COUNTRIESCapturing regional growth opportunities by differentiated geographic focusCapturing regional growth opportunities by differentiated geographic focus

FOCUS ON PRINCIPAL EXTENSIVE GROWTH AREAS

► ‘Hold fast’: maintain market share in HUN, ITA, while increase in SK, regain in CRO and BIH, , , g

► ‘Go for it’: further growth on key export markets AUT, CZ, expansion in West-ROM, SRB, SLO

► ‘Keep up’: maintain and build up market presence on markets ensuring optimum flexibility to refining assets

HARMONIZED DEVELOPMENT OF LOGISTICS, COMMERCIAL AND RETAIL TO SUPPORT SALES► Focus on growing markets & keep leading position in domestic countries

D b ttl ki th l i ti t

Largest contributors

► Increasing retail presence on growth markets

INCREASE RETIAL NETWORK EFFICIENCY

► Debottlenecking the logistics system

► Greenfield investments

► Opportunistic network acquisitions

► Improve brand perception & increase non-fuel revenue D

► Increase avr. throughput per site to 3.0 Mlpa► Dispose inefficient sites

ownstream

49

Keep and strenghten locational benefit: margin-driven sales optimization with end-user focus

Financials

FFinancials

50

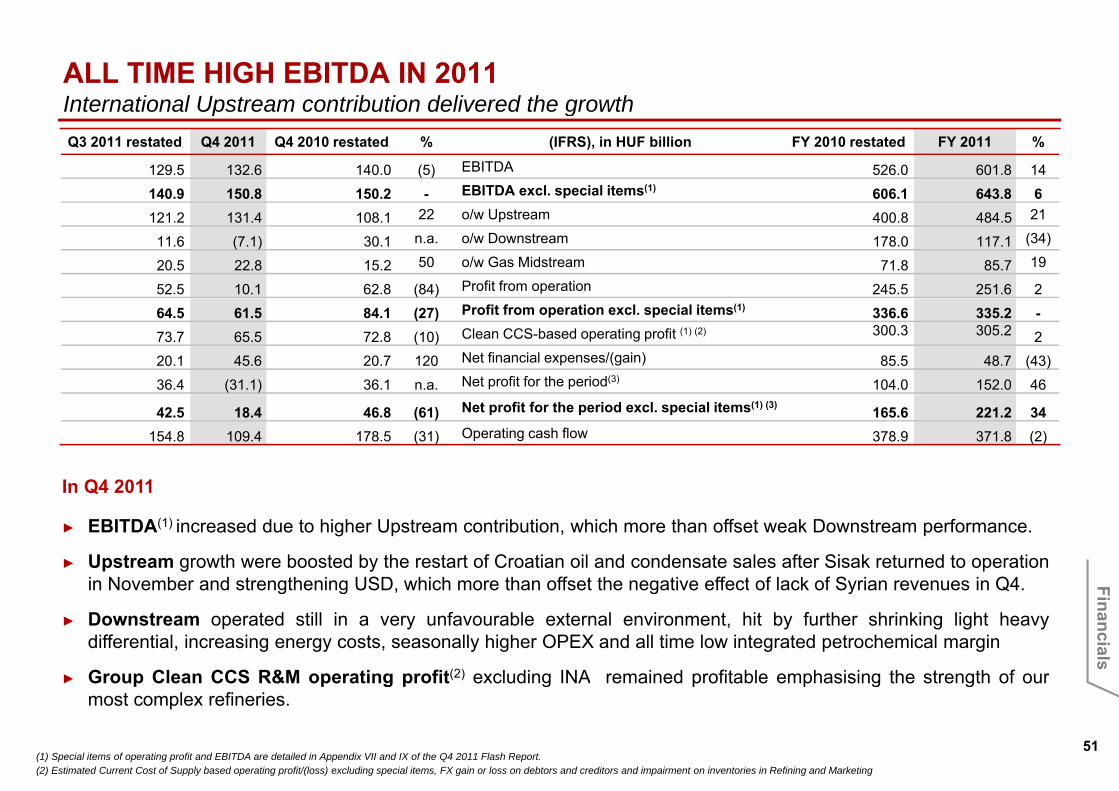

ALL TIME HIGH EBITDA IN 2011 International Upstream contribution delivered the growthInternational Upstream contribution delivered the growthQ3 2011 restated Q4 2011 Q4 2010 restated % (IFRS), in HUF billion FY 2010 restated FY 2011 %

129.5 132.6 140.0 (5) EBITDA 526.0 601.8 14140.9 150.8 150.2 - EBITDA excl. special items(1) 606.1 643.8 6121.2 131.4 108.1 22 o/w Upstream 400.8 484.5 21

11.6 (7.1) 30.1 n.a. o/w Downstream 178.0 117.1 (34)

20.5 22.8 15.2 50 o/w Gas Midstream 71.8 85.7 19

52.5 10.1 62.8 (84) Profit from operation 245.5 251.6 264.5 61.5 84.1 (27) Profit from operation excl. special items(1) 336.6 335.2 -73.7 65.5 72.8 (10) Clean CCS-based operating profit (1) (2) 300.3 305.2 220.1 45.6 20.7 120 Net financial expenses/(gain) 85.5 48.7 (43)36.4 (31.1) 36.1 n.a. Net profit for the period(3) 104.0 152.0 46

In Q4 2011

42.5 18.4 46.8 (61) Net profit for the period excl. special items(1) (3) 165.6 221.2 34154.8 109.4 178.5 (31) Operating cash flow 378.9 371.8 (2)

In Q4 2011

► EBITDA(1) increased due to higher Upstream contribution, which more than offset weak Downstream performance.

► Upstream growth were boosted by the restart of Croatian oil and condensate sales after Sisak returned to operationin November and strengthening USD, which more than offset the negative effect of lack of Syrian revenues in Q4. Fin November and strengthening USD, which more than offset the negative effect of lack of Syrian revenues in Q4.

► Downstream operated still in a very unfavourable external environment, hit by further shrinking light heavydifferential, increasing energy costs, seasonally higher OPEX and all time low integrated petrochemical margin

► Group Clean CCS R&M operating profit(2) excluding INA remained profitable emphasising the strength of our

Financials

51

p p g p g p p g gmost complex refineries.

(1) Special items of operating profit and EBITDA are detailed in Appendix VII and IX of the Q4 2011 Flash Report.(2) Estimated Current Cost of Supply based operating profit/(loss) excluding special items, FX gain or loss on debtors and creditors and impairment on inventories in Refining and Marketing

FURTHER STRENGTHENED FINANCIAL POSITIONFitch reinforced the investment grade credit rating

Covenants

Fitch reinforced the investment grade credit rating

USD bn

Gearing (%)

2,5

3

3,5

2,5

3

35

40

1

1,5

22 30

0

0,5

1

1

1,5

2 008 2 009 2 010 2 01120

25

2008 2009 2010 2011

EBITDA Net debt to EBITDA

Keep covenants and gearing in the safety zone

Gearing

F

Largest contributors Keep covenants and gearing in the safety zone

3.4 years average maturity profile

Financials

52

2012 CAPEX: STRONG FOCUS ON UPSTREAMUp to USD 2 bn CAPEX spendingUp to USD 2 bn CAPEX spending

12% 21%

UPSTREAM (2012) DOWNSTREAM (2012)

3%13%

MOL GROUP (2012)

25%

5%

4%

47%

3%

21%

17%

16%

Hungary Croatia

60%19%

Refining and Marketing

37%

Upstream Downstream

► Strict control on maintenance; focus► Increasing share of exploration: speed

Kurdistan, Iraq RussiaSyria PakistanOther

RetailPetrochemicalsGas Midstream C&O

P t ti l i t t th h i

L t t ib t

► Strict control on maintenance; focus on safe operation

► Improve flexibility and extend value chain in Petchem

► Increasing share of exploration: speed up in Kurdistan Region of Iraq

► Exploration with international focus is targeting reasonable resource base

► Potential investment on the horizon

► Conservative and flexible approach

F

Largest contributors ► Increase retail presence and logistic developments to secure enduser market

► Focus on developments in Russia, Kazakhstan and Pakistan

► Mitigating natural decline in the CEE

Financials

53

region

2012-2014 CAPEX SHOULD BE FULLY FINANCED FROM OPERATING CFUp to annual USD 2 bn CAPEX spending

► Kurdistan, Iraq: Akri-Bijeel and Shaikan blocks

R i B it d M tj hki k bl k

GROUP 2012‐2014

Up to annual USD 2 bn CAPEX spending

► Russia: Baitex and Matjushkinsky blocks

► Kazakhstan: Federovsky block

► Hungarian conventional and unconventional explorationpstr

eam

50%4%

21%

cts

► Hungarian conventional and unconventional exploration

► Croatian exploration and field development

► Hungarian field development

U50%

25%

owth

pro

je

m► Modernization through new LDPE unit, Slovnaft

Upstream Downstream

Gas Midstream Contingencyor

gani

c gr

o

Dow

nstr

eam

► Rijeka residue processing – Delayed Coker

► Butadiene Extraction Unit

Key

o

F

D

► Logistic and retail development

Financials

54

NO PRESSURE FOR FURTHER FINANCING IN 2012Stable maturity profile more than EUR 2 bn available liquidity

3000

Stable maturity profile, more than EUR 2 bn available liquidity

2000

2500

2014

2013

1500

2016

2014

mn

EUR

500

1000m

500

0

Deposits Undrawn facilities Available liquidity 2012 2013 2014

F

-1000

-500

Financials

55

2012-2014 CAPEX SHOULD BE FULLY FINANCED FROM OPERATING CFUp to annual USD 2 bn CAPEX spending

► Kurdistan, Iraq: Akri-Bijeel and Shaikan blocks

R i B it d M tj hki k bl k

GROUP 2012-2014

Up to annual USD 2 bn CAPEX spending

► Russia: Baitex and Matjushkinsky blocks

► Kazakhstan: Federovsky block

► Hungarian conventional and unconventional explorationpstr

eam

50%4%

21%

cts

► Hungarian conventional and unconventional exploration

► Croatian exploration and field development

► Hungarian field development

U50%

25%

owth

pro

je

m► Modernization through new LDPE unit, Slovnaft

Upstream Downstream

Gas Midstream Contingencyor

gani

c gr

o

Dow

nstr

eam

► Rijeka residue processing – Delayed Coker

► Butadiene Extraction Unit

Key

o

F

D

► Logistic and retail development

Financials

NATURAL HEDGE POSITION IN FXUSD and EUR denominated business mixUSD and EUR denominated business mix

► Both in Upstream and Downstream operating cash flow is mainly driven by USD and EUR 3%

Total debt – YE 2011

► CAPEX is also linked mainly to USD, EUR27%

► Weaker local currencies is slightly beneficial70%

► FX structure of indebtedness naturally decreases the above exposures

EUR USD HUF and other currency

FFinancials

57

APPENDIX

AAppendix

58

ALL TIME HIGH EBITDA IN 2011 International Upstream contribution delivered the growthInternational Upstream contribution delivered the growthQ3 2011 restated Q4 2011 Q4 2010 restated % (IFRS), in HUF billion FY 2010 restated FY 2011 %

129.5 132.6 140.0 (5) EBITDA 526.0 601.8 14

140.9 150.8 150.2 ‐ EBITDA excl. special items(1) 606.1 643.8 6

121.2 131.4 108.1 22 o/w Upstream 400.8 484.5 21

11.6 (7.1) 30.1 n.a. o/w Downstream 178.0 117.1 (34)

20.5 22.8 15.2 50 o/w Gas Midstream 71.8 85.7 19

52.5 10.1 62.8 (84) Profit from operation 245.5 251.6 2

64.5 61.5 84.1 (27) Profit from operation excl. special items(1) 336.6 335.2 ‐

73.7 65.5 72.8 (10) Clean CCS‐based operating profit (1) (2) 300.3 305.2 2

20.1 45.6 20.7 120 Net financial expenses/(gain) 85.5 48.7 (43)

36.4 (31.1) 36.1 n.a. Net profit for the period(3) 104.0 152.0 46

In Q4 2011

42.5 18.4 46.8 (61) Net profit for the period excl. special items(1) (3) 165.6 221.2 34

154.8 109.4 178.5 (31) Operating cash flow 378.9 371.8 (2)

In Q4 2011

► EBITDA(1) increased due to higher Upstream contribution, which more than offset weak Downstream performance.

► Upstream growth were boosted by the restart of Croatian oil and condensate sales after Sisak returned to operationin November and strengthening USD, which more than offset the negative effect of lack of Syrian revenues in Q4. Ain November and strengthening USD, which more than offset the negative effect of lack of Syrian revenues in Q4.

► Downstream operated still in a very unfavourable external environment, hit by further shrinking light heavydifferential, increasing energy costs, seasonally higher OPEX and all time low integrated petrochemical margin

► Group Clean CCS R&M operating profit(2) excluding INA remained profitable emphasising the strength of our

Appendix

59

p p g p g p p g gmost complex refineries.

(1) Special items of operating profit and EBITDA are detailed in Appendix VII and IX of the Q4 2011 Flash Report.(2) Estimated Current Cost of Supply based operating profit/(loss) excluding special items, FX gain or loss on debtors and creditors and impairment on inventories in Refining and Marketing

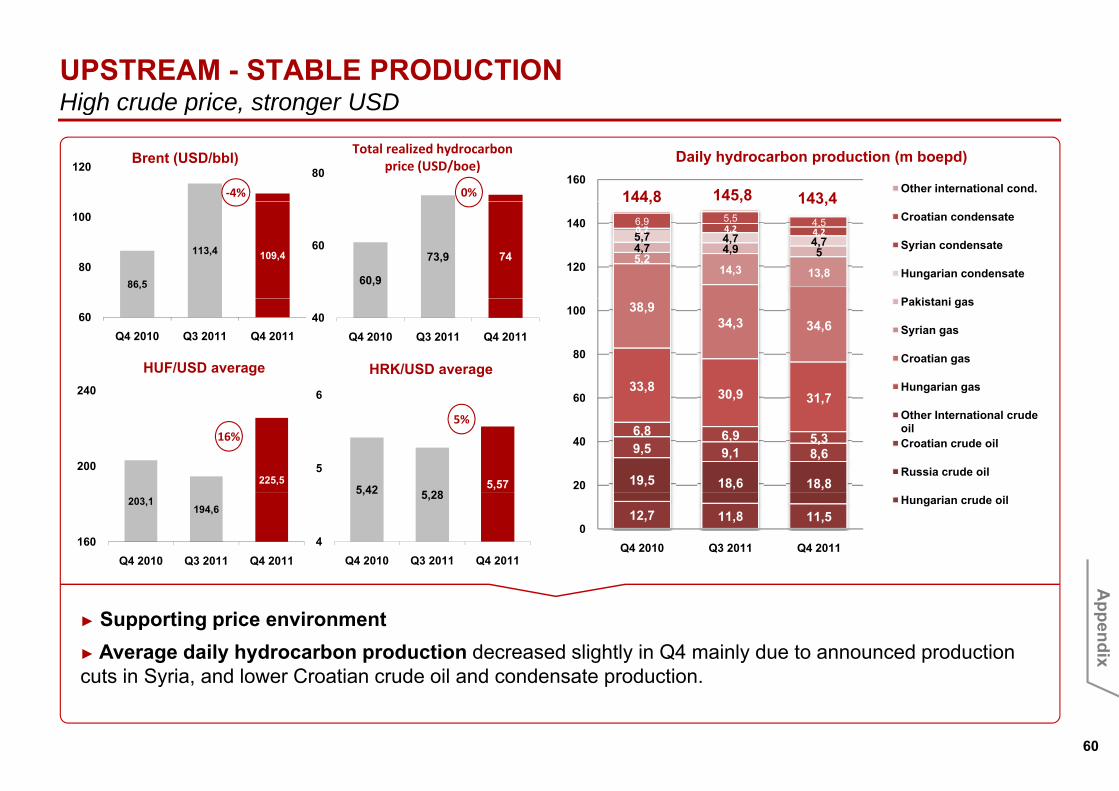

UPSTREAM - STABLE PRODUCTIONHigh crude price stronger USD

160

Daily hydrocarbon production (m boepd)

Other international cond.

High crude price, stronger USD

120 Brent (USD/bbl)

‐4%

80

Total realized hydrocarbonprice (USD/boe)

0% 145,8144,8 143,4

5,214,3 13,8

4,7 4,9 55,7 4,7 4,70,7 4,2 4,26,9 5,5 4,5

120

140 Croatian condensate

Syrian condensate

Hungarian condensate

P ki t i86,5

113,4 109,480

100

60,9

73,9 7460

,144,8 143,4

33,8 30 9 31 7

38,934,3 34,6

60

80

100Pakistani gas

Syrian gas

Croatian gas

Hungarian gas HUF/USD average

240

60Q4 2010 Q3 2011 Q4 2011

40Q4 2010 Q3 2011 Q4 2011

6

HRK/USD average

19,5 18,6 18,8

9,5 9,1 8,6

6,8 6,9 5,3

30,9 31,7

20

40

60Other International crude oilCroatian crude oil

Russia crude oil

16

225,5200

5,42 5 285,57

5

6

5%16%

12,7 11,8 11,50

Q4 2010 Q3 2011 Q4 2011

Hungarian crude oil 203,1194,6

160Q4 2010 Q3 2011 Q4 2011

5,42 5,28

4Q4 2010 Q3 2011 Q4 2011

A

► Supporting price environment► Average daily hydrocarbon production decreased slightly in Q4 mainly due to announced production cuts in Syria, and lower Croatian crude oil and condensate production.

Appendix

60

y p

UPSTREAM RESULT WAS RECORD HIGH IN Q4UPSTREAM RESULT WAS RECORD HIGH IN Q4…

EBITDA* (HUF bn)

Positive effects of

► Restart of Croatian oil and condensate sales to Si k (b k t ti i N b )131 4

120

130

140

+8%

Sisak (back to operation in November)

► Strengthening USD against HUF108,1

121,2131,4

100

110

Q4 2010 Q3 2011 Q4 2011

were moderated by negative effects of

► Lack of Syrian revenues90

100

Operating profit* (HUF bn)

- ► Lack of Syrian revenues

► Severe impact of regulated Hungarian natural gas price for household costumers

► Slight production decrease82,4 81,3

8770

80

907%

A► Slight production decrease60

Q4 2010 Q3 2011 Q4 2011

Appendix

61* Excluding special items

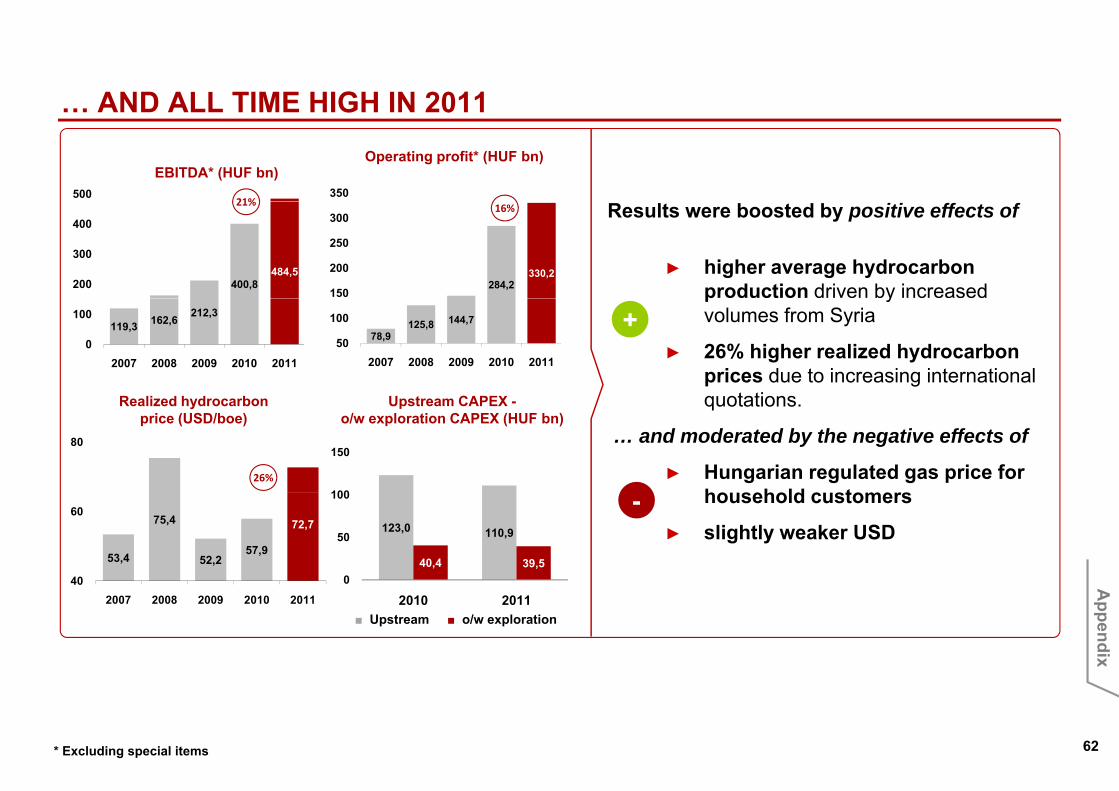

AND ALL TIME HIGH IN 2011… AND ALL TIME HIGH IN 2011

350

Operating profit* (HUF bn)

500

EBITDA* (HUF bn)

21%

284,2330,2

150

200

250

300 Results were boosted by positive effects of

► higher average hydrocarbon production driven by increased 400,8

484,5200

300

40016%21%

78,9125,8 144,7

50

100

2007 2008 2009 2010 2011

p yvolumes from Syria

► 26% higher realized hydrocarbon prices due to increasing international

t ti

119,3 162,6212,3

0

100

2007 2008 2009 2010 2011

+

quotations.

… and moderated by the negative effects of

► Hungarian regulated gas price for h h ld t

80

Realized hydrocarbonprice (USD/boe)

100

150

Upstream CAPEX -o/w exploration CAPEX (HUF bn)

26%

household customers

► slightly weaker USD53,4

75,4

52,257,9

72,7

40

60 -123,0 110,9

40,4 39,50

50

100

A

2007 2008 2009 2010 2011 2010 2011■ Upstream ■ o/w exploration

Appendix

62* Excluding special items

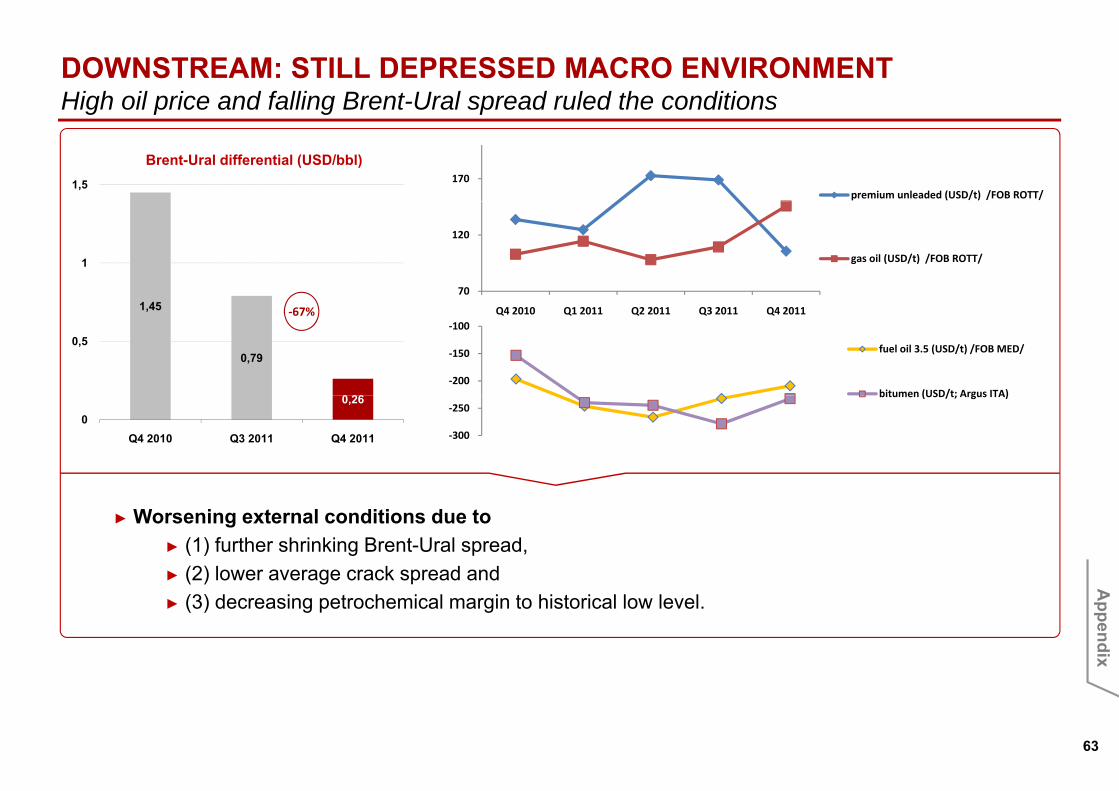

DOWNSTREAM: STILL DEPRESSED MACRO ENVIRONMENTHigh oil price and falling Brent-Ural spread ruled the conditionsHigh oil price and falling Brent Ural spread ruled the conditions

Brent-Ural differential (USD/bbl)1,5 170

premium unleaded (USD/t) /FOB ROTT/

1

70

120

gas oil (USD/t) /FOB ROTT/

1,45

0,79

0 26

0,5

Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011

‐200

‐150

‐100

fuel oil 3.5 (USD/t) /FOB MED/

bitumen (USD/t; Argus ITA)

‐67%

0,26

0Q4 2010 Q3 2011 Q4 2011 ‐300

‐250bitumen (USD/t; Argus ITA)

► Worsening external conditions due to ► (1) further shrinking Brent-Ural spread, ► (2) lower average crack spread and A

► (3) decreasing petrochemical margin to historical low level.

Appendix

63

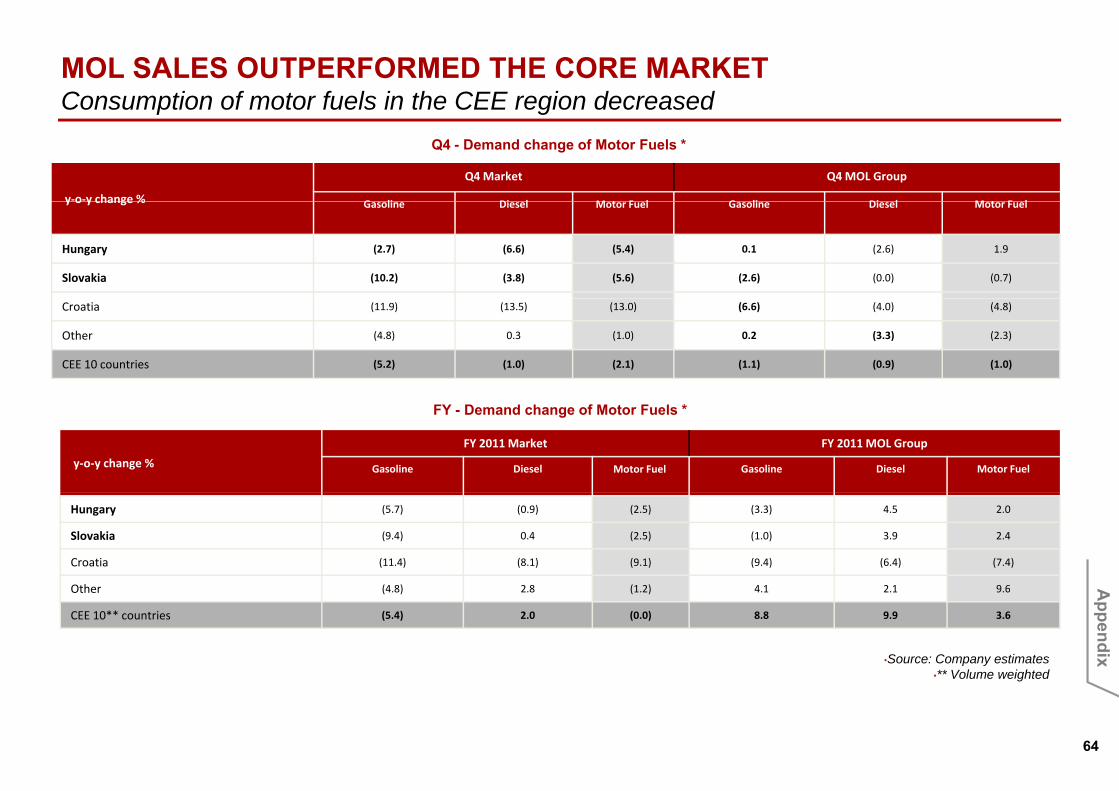

MOL SALES OUTPERFORMED THE CORE MARKETConsumption of motor fuels in the CEE region decreased

y‐o‐y change %

Q4 Market Q4 MOL Group

G li Di l M t F l G li Di l M t F l

Q4 - Demand change of Motor Fuels *

Consumption of motor fuels in the CEE region decreased

y o y change % Gasoline Diesel Motor Fuel Gasoline Diesel Motor Fuel

Hungary (2.7) (6.6) (5.4) 0.1 (2.6) 1.9

Slovakia (10.2) (3.8) (5.6) (2.6) (0.0) (0.7)

Croatia (11.9) (13.5) (13.0) (6.6) (4.0) (4.8)

Other (4.8) 0.3 (1.0) 0.2 (3.3) (2.3)

CEE 10 countries (5.2) (1.0) (2.1) (1.1) (0.9) (1.0)

y‐o‐y change %

FY 2011Market FY 2011 MOL Group

Gasoline Diesel Motor Fuel Gasoline Diesel Motor Fuel

FY - Demand change of Motor Fuels *

Hungary (5.7) (0.9) (2.5) (3.3) 4.5 2.0

Slovakia (9.4) 0.4 (2.5) (1.0) 3.9 2.4

Croatia (11.4) (8.1) (9.1) (9.4) (6.4) (7.4)

Other (4 8) 2 8 (1 2) 4 1 2 1 9 6 AOther (4.8) 2.8 (1.2) 4.1 2.1 9.6

CEE 10** countries (5.4) 2.0 (0.0) 8.8 9.9 3.6

•Source: Company estimates•** Volume weighted

Appendix

64

DOWNSTREAM in Q4 2011 – SUFFERED FROM EXTERNAL ENVIRONMENTClean CCS R&M profit** excluding INA is still positive

External refined product and petrochemical sales (Mt)

Clean CCS R&M profit excluding INA is still positive

DownstreamEBITDA* (HUF bn)

30 6

EBITDA* turned to negative

► challenging Downstream environment

30,1

11 610

20

30

5,3 5,4 5,24

6‐3%

► challenging Downstream environment

► seasonally higher operating costs (energy

and maintenance costs)

-

11,6

-7,1

-10

0

Q4 2010 Q3 2011 Q4 2011

, 5,2

2Q4 2010 Q3 2011 Q4 2011

CCS-based** R&M operating profit –MOL excl. INA (HUF bn)

CCS-based** R&M operating profit -Group (HUF bn)

► seasonally weaker retail sales

… just slightly moderated by internal efforts

7 710,55

10-8,8 -1,2

-29

-20

-10

0 ► efforts to maintain sales margin +‐60%

A7,7

4,2

0Q4 2010 Q3 2011 Q4 2011

-30Q4 2010 Q3 2011 Q4 2011

* Excluding special item

Appendix

65

Excluding special item** Excluding special items, forex gains on debtors and creditors and impairment on inventories

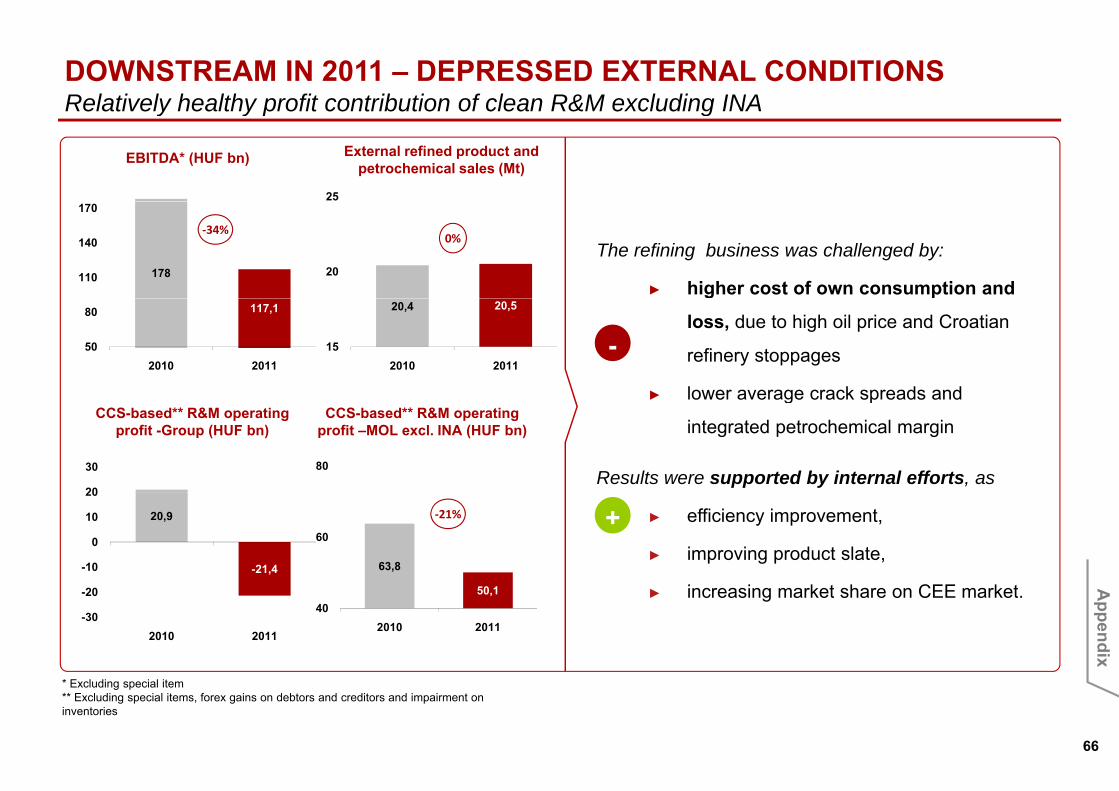

DOWNSTREAM IN 2011 – DEPRESSED EXTERNAL CONDITIONSRelatively healthy profit contribution of clean R&M excluding INA

25

External refined product and petrochemical sales (Mt)

Relatively healthy profit contribution of clean R&M excluding INA

EBITDA* (HUF bn)

The refining business was challenged by:

► higher cost of own consumption and 20178110

140

170

‐34%0%

loss, due to high oil price and Croatian

refinery stoppages

► lower average crack spreads and

20,4 20,5

152010 2011

117,1

50

80

2010 2011-

► lower average crack spreads and

integrated petrochemical margin

Results were supported by internal efforts, as

CCS-based** R&M operating profit –MOL excl. INA (HUF bn)

20

30

CCS-based** R&M operating profit -Group (HUF bn)

80

► efficiency improvement,

► improving product slate,

► increasing market share on CEE market

20,9

-21,4

20

-10

0

10

20

63,8

50 1

60+‐21%

A

► increasing market share on CEE market.

* Excluding special item

-30

-20

2010 2011

50,140

2010 2011

Appendix

66

Excluding special item** Excluding special items, forex gains on debtors and creditors and impairment on inventories

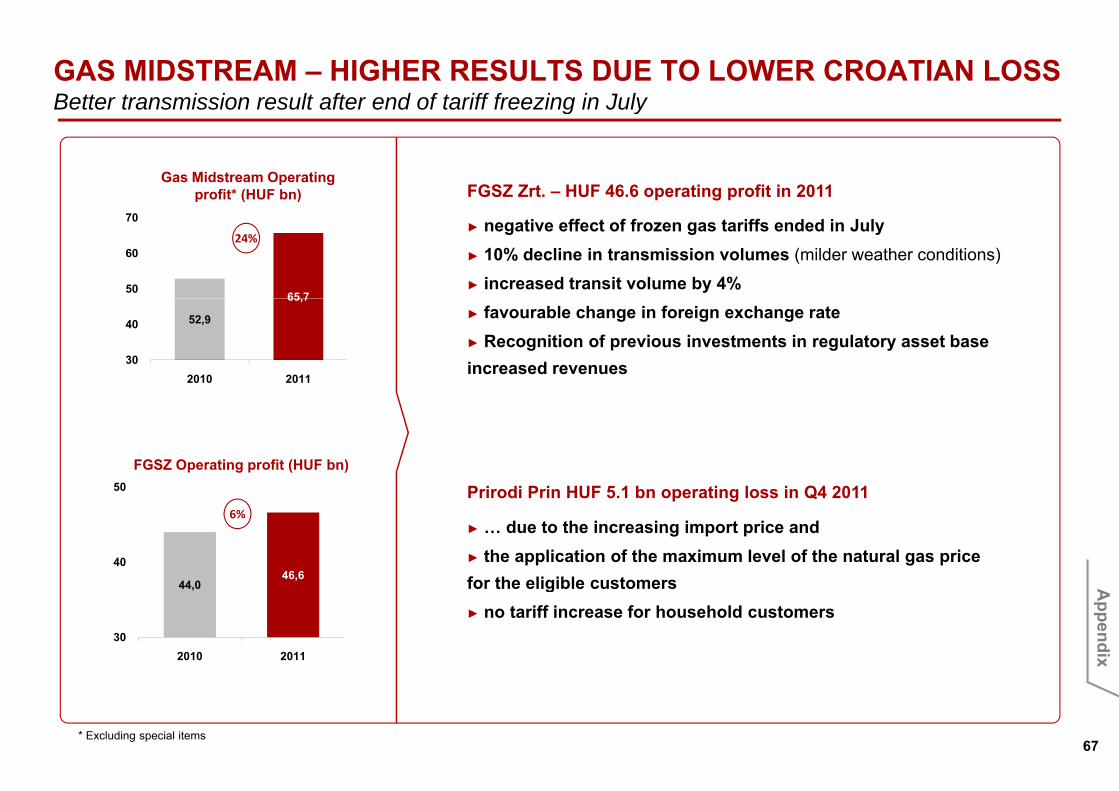

GAS MIDSTREAM – HIGHER RESULTS DUE TO LOWER CROATIAN LOSSBetter transmission result after end of tariff freezing in JulyBetter transmission result after end of tariff freezing in July

FGSZ Zrt. – HUF 46.6 operating profit in 2011Gas Midstream Operating

profit* (HUF bn)

► negative effect of frozen gas tariffs ended in July► 10% decline in transmission volumes (milder weather conditions)

► increased transit volume by 4%65 7

50

60

70

p ( )

24%

► favourable change in foreign exchange rate► Recognition of previous investments in regulatory asset base increased revenues

52,9

65,7

30

40

2010 2011

FGSZ Operating profit (HUF bn)50 Prirodi Prin HUF 5 1 bn operating loss in Q4 2011

44,046,6

40

Prirodi Prin HUF 5.1 bn operating loss in Q4 2011

► … due to the increasing import price and ► the application of the maximum level of the natural gas price for the eligible customers

6%

A,

302010 2011

g► no tariff increase for household customers

Appendix

67* Excluding special items

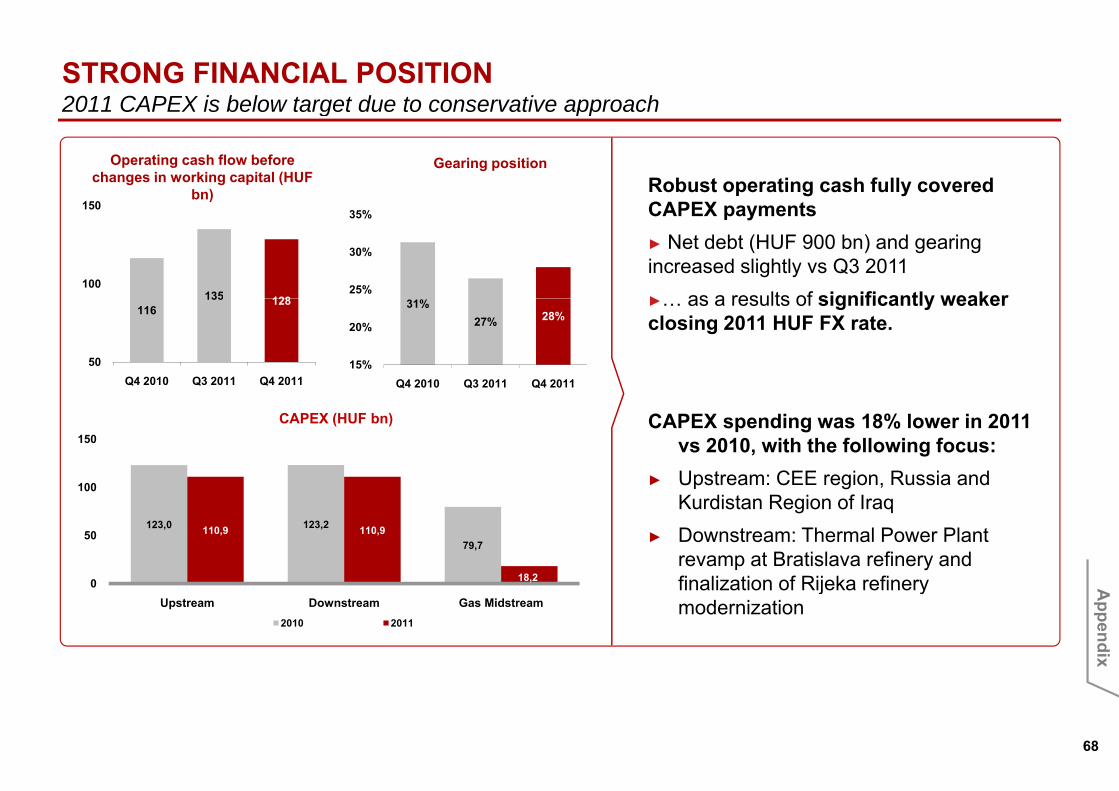

STRONG FINANCIAL POSITION2011 CAPEX is below target due to conservative approach2011 CAPEX is below target due to conservative approach

Robust operating cash fully covered C

Gearing position

150

Operating cash flow before changes in working capital (HUF

bn)CAPEX payments► Net debt (HUF 900 bn) and gearing increased slightly vs Q3 2011► as a results of significantly weaker25%

30%

35%

135 128100

150)

►… as a results of significantly weaker closing 2011 HUF FX rate.

31%27% 28%

15%

20%

Q4 2010 Q3 2011 Q4 2011

116135 128

50Q4 2010 Q3 2011 Q4 2011

CAPEX spending was 18% lower in 2011 vs 2010, with the following focus:

► Upstream: CEE region, Russia and 100

150CAPEX (HUF bn)

Kurdistan Region of Iraq► Downstream: Thermal Power Plant

revamp at Bratislava refinery and finalization of Rijeka refinery

123,0 123,2

79,7110,9 110,9

18,20

50

Afinalization of Rijeka refinery modernizationUpstream Downstream Gas Midstream

2010 2011

Appendix

68