investor presentation · 2020-02-27 · a world of difference. investor presentation february 27,...

TRANSCRIPT

Inspired Packaging. A World of Difference.

Investor PresentationFebruary 27, 2020

©2020 Graphic Packaging International 2

FORWARD LOOKING STATEMENTS

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Any statements of the Company’s expectations in these slides, including but not limited to the amount of net organic volume growth per year, the start-up timing of the new

paperboard machine in Kalamazoo, MI and projected productivity improvements, expected increases in sales due to pricing and volume performance improvements, Adjusted

EBITDA and cash flow, as well as expected capital spending, pension expense and settlement charges, timing for payment of U.S. federal taxes, depreciation and amortization,

pension amortization, interest expense, effective tax rate, and net leverage, as well as targeted reductions in water usage, energy consumption, green house gases and low-density

polyethylene usage constitute "forward-looking statements" as defined in the Private Securities Litigation Reform Act of 1995. Such statements are based on currently available

information and are subject to various risks and uncertainties that could cause actual results to differ materially from the Company's present expectations. These risks and

uncertainties include, but are not limited to, inflation of and volatility in raw material and energy costs, cutbacks in consumer spending that reduce demand for the Company’s

products, continuing pressure for lower cost products, the Company’s ability to implement its business strategies, including productivity initiatives, cost reduction plans, and

integration activities, as well as currency movements and other risks of conducting business internationally, and the impact of regulatory and litigation matters, including the

continued availability of the Company’s net operating loss offset to taxable income, and those that impact the Company’s ability to protect and use its intellectual property. Undue

reliance should not be placed on such forward-looking statements, as such statements speak only as of the date on which they are made and the Company undertakes no

obligation to update such statements except as required by law. Additional information regarding these and other risks is contained in the Company's periodic filings with the SEC.

NON-GAAP FINANCIAL MEASURES

This presentation includes certain financial measures that exclude or adjust for charges or income associated with business combinations, facility shutdowns, extended mill

outages, sales of assets and other special charges or income. The Company’s management believes that the presentation of these financial measures provides useful information

to investors because these measures are regularly used by management in assessing the Company’s performance. These financial measures are not calculated in accordance

with generally accepted accounting principles in the United States (“GAAP”) and should be considered in addition to results prepared in accordance with GAAP, but should not be

considered substitutes for or superior to GAAP results. In addition, these non-GAAP financial measures may not be comparable to similarly-titled measures utilized by other

companies, since such other companies may not calculate such measure in the same manner as we do. A reconciliation of these measures to the most relevant GAAP measure is

available in our latest earnings press release which can be found in the Investors section on the Graphic Packaging website at www.graphicpkg.com.

GRAPHIC PACKAGING: INVESTMENT CASE

• REDEFINING INDUSTRY LEADERSHIP WITH VISION 2025

• CAPTURING SUSTAINABILITY SUPPORTED ORGANIC GROWTH

• CLEAR PATH TO DELIVER PRODUCTIVITY DRIVEN MARGIN IMPROVEMENT

• STRONG FINANCIAL FLEXIBLITY TO ACHIEVE VISION 2025

• BALANCED CAPITAL ALLOCATION MAXIMIZING STOCKHOLDER RETURN

©2020 Graphic Packaging International 3

©2020 Graphic Packaging International4

FOOD, BEVERAGE, FOODSERVICE & CONSUMER PRODUCTS PAPERBOARD PACKAGING LEADER

$6.2B2019 SALES

87% 11% 2%Americas Europe ROW

9 68 3.8MPaperboard Mills Converting

Plants

Tons

Produced

MARKETS

Food

Beverage

Foodservice

Consumer

37%

20%

23%

20%

©2020 Graphic Packaging International 5

KEY CUSTOMERS ACROSS FOOD, BEVERAGE, FOODSERVICE & CONSUMER PRODUCTS MARKETS

37%of all folding cartons

in North America

30%

©2020 Graphic Packaging International 6

SUSTAINED MARKET LEADERSHIP

#2 SBS Producer

22%5.4M ton U.S. market

#1 CUK Producer

58%2.8M ton U.S. market

#1 CRB Producer

52%1.9M ton U.S. market

of all paper cups in the U.S.

Source: PPC, AF&PA, RISI, GPI estimates

©2020 Graphic Packaging International 7

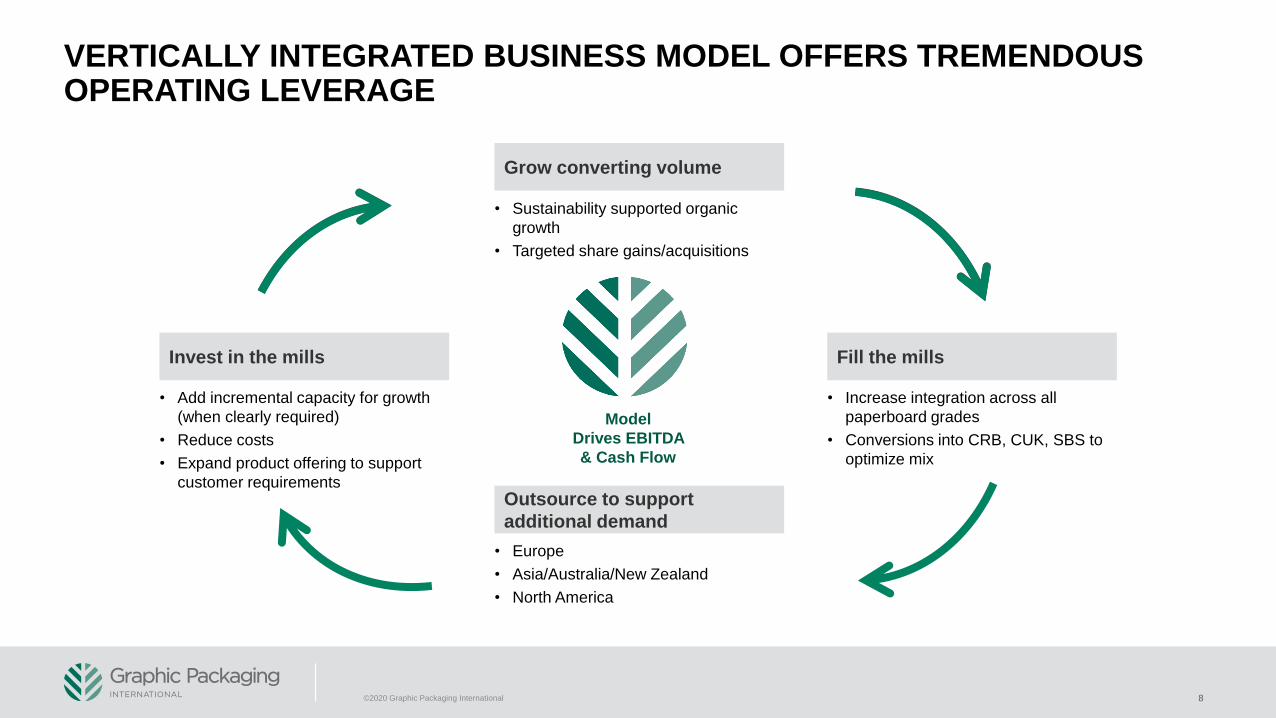

POWERFUL, VERTICALLY INTEGRATED BUSINESS MODEL

PRODUCTS WE USE EVERYDAYHIGHLY EFFICIENT CONVERTING & PACKAGING MACHINERY

68% vertical integration results in best-in-class EBITDA margins; significant opportunities to drive integration rates higher

LOW COST, HIGH QUALITY PAPERBOARD MILLS

Grow converting volume

8

VERTICALLY INTEGRATED BUSINESS MODEL OFFERS TREMENDOUS OPERATING LEVERAGE

• Europe

• Asia/Australia/New Zealand

• North America

• Sustainability supported organic

growth

• Targeted share gains/acquisitions

• Increase integration across all

paperboard grades

• Conversions into CRB, CUK, SBS to

optimize mix

• Add incremental capacity for growth

(when clearly required)

• Reduce costs

• Expand product offering to support

customer requirementsOutsource to support

additional demand

Fill the millsInvest in the mills

Model

Drives EBITDA

& Cash Flow

©2020 Graphic Packaging International

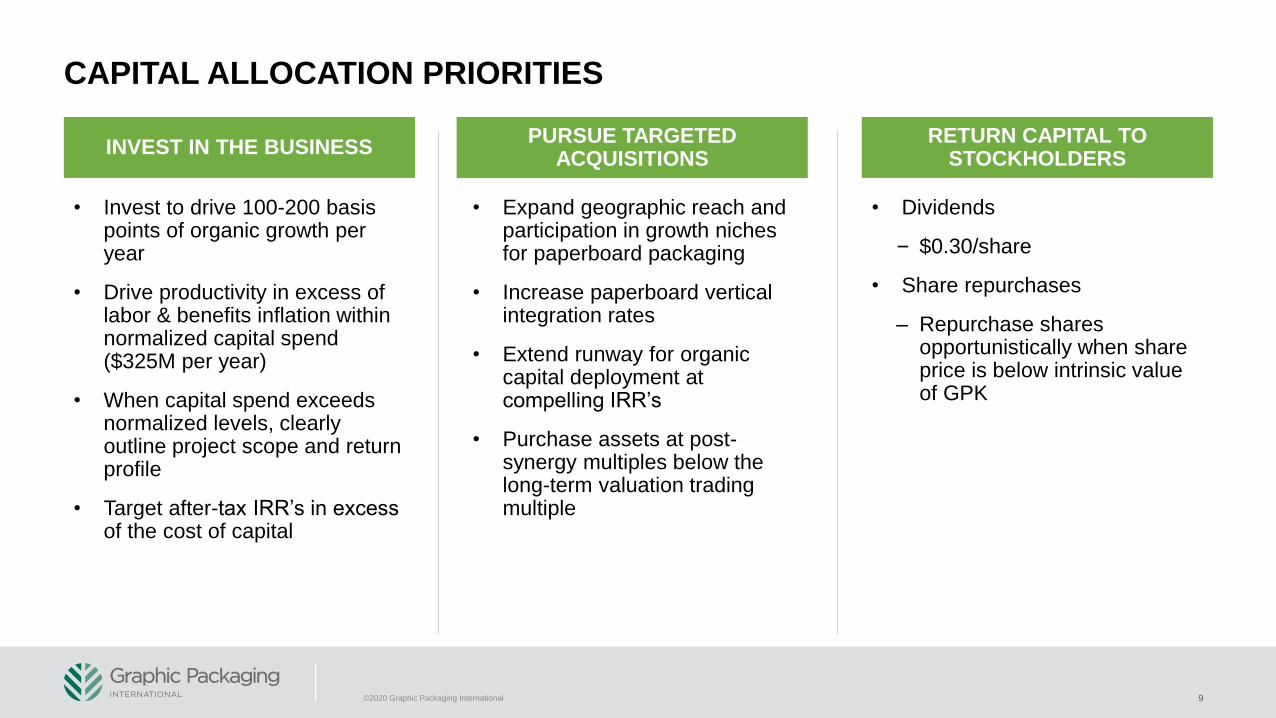

INVEST IN THE BUSINESSPURSUE TARGETED

ACQUISITIONS

9

RETURN CAPITAL TO STOCKHOLDERS

• Invest to drive 100-200 basispoints of organic growth peryear

• Drive productivity in excess oflabor & benefits inflation withinnormalized capital spend($325M per year)

• When capital spend exceedsnormalized levels, clearlyoutline project scope and returnprofile

• Target after-tax IRR’s in excessof the cost of capital

• Expand geographic reach andparticipation in growth nichesfor paperboard packaging

• Increase paperboard verticalintegration rates

• Extend runway for organiccapital deployment atcompelling IRR’s

• Purchase assets at post-synergy multiples below thelong-term valuation tradingmultiple

• Dividends

– $0.30/share

• Share repurchases

‒ Repurchase sharesopportunistically when share price is below intrinsic value of GPK

CAPITAL ALLOCATION PRIORITIES

©2020 Graphic Packaging International

CAPITAL INVESTMENTS & PRODUCTIVITY(2) TARGETED ACQUISITIONS

10

BALANCED APPROACH TO CAPITAL ALLOCATIONFROM 2015 TO 2019, $3.4B IN ADJ(1) OPERATING CASH FLOW

NET DEBT LEVERAGE RATIORatio consistently in desired 2.5x–3.0x range

STOCKHOLDER RETURNReturned significant value to stockholders

430M 538M ~11%Dividends Share

repurchases

Net reduction in

share count

$ $

Invested $1.5B in capital

~6% of sales driving $355M in productivity

$244 $295

$260

$395 $353

$74 $73 $57 $77 $74

2015 2016 2017 2018 2019

Acquired 14 businesses for ~$900M at compelling post synergy valuations

Combined with IP’s Consumer Packaging business in 2018 adding ~$200M in ADJ EBITDA and ~$75M synergies

Multiples

(Pre/Post)~8.5X ~5.6X

ADJ EBITDA

($M)~$100 ~$170

1.7B 4.2%Liquidity Current weighted

avg. interest rate

$ 2.6xYE19

(2) 2018 productivity includes $35m in synergies; 2019 productivity excludes $36M of incentives & pension

(3) Includes $23M for CRB consolidation

(5) (5)

(1) Operating cash flow in 2018 and 2019 adjusted to recognize net cash from receivables program

(4) Includes distributions to GPIP partner

(5) Share repurchases through 4Q’19

(3)

©2020 Graphic Packaging International

(4)

PRICE / COST RECOVERY OCCURRING

11

100-200 BPS / YEAR NET ORGANICVOLUME GROWTH MATERIALIZING

POISED FOR SALES, VOLUME, MARGIN & CASH GENERATION GROWTH

($8)

$131

($124)

($33)

2016-18 2019

Price

Cost Cost

From 9 to 6 months

Price

PRICE LAGS REDUCED

©2020 Graphic Packaging International

12

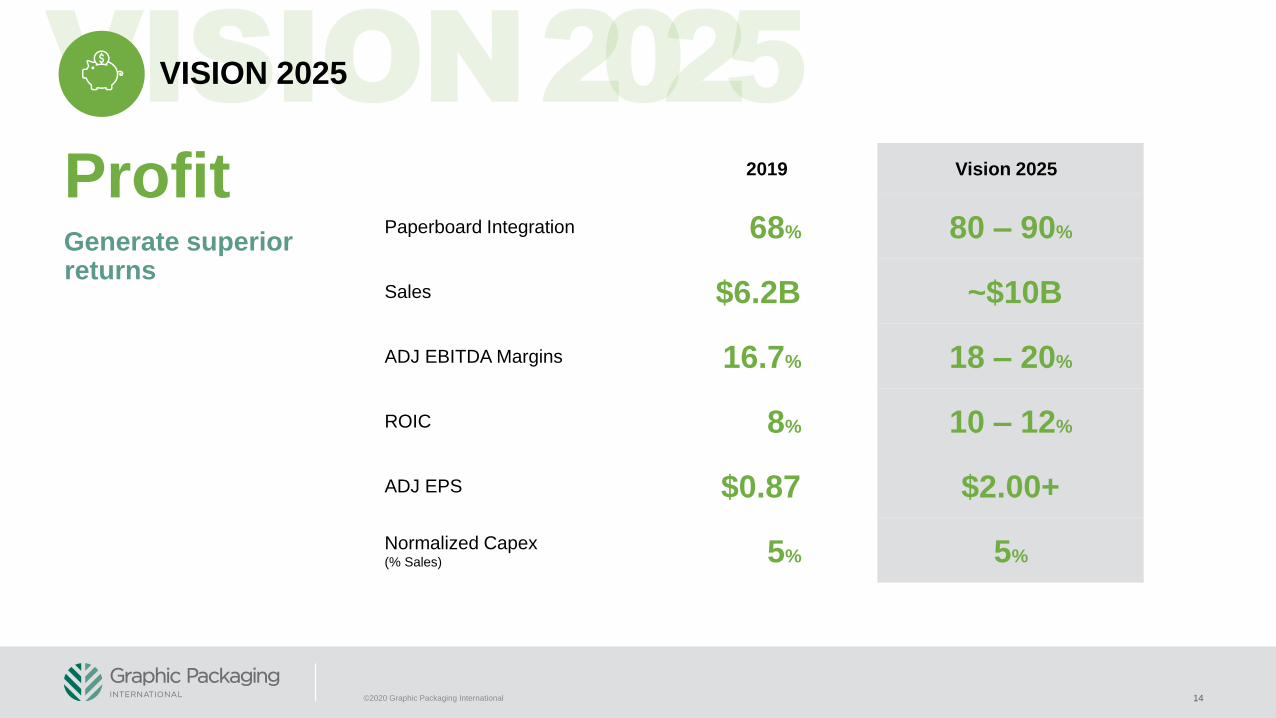

VISION 2025

Partners

People

Profit

Planet

GROW WITH THE BEST CUSTOMERS IN THE BEST MARKETS

GENERATE SUPERIOR RETURNS

LEVERAGE SUSTAINABILITY PROFILE & REDUCE ENVIRONMENTAL IMPACT

ENGAGE EMPLOYEES IN A HIGH-PERFORMANCE CULTURE

©2020 Graphic Packaging International

13

VISION 2025

PartnersGrow with the best customers in the best markets

#1 paperboard market

share in North America &

Europe

$400M – $700M net new

product sales 2020-2025

included in organic growth

100 – 200 bps/year

sustainability supported,

organic growth

Strategic,

high return M&A

$400M – $500M in

productivity 2020-2025

to drive margin growth

©2020 Graphic Packaging International

14

VISION 2025

ProfitGenerate superior returns

2019 Vision 2025

Paperboard Integration 68% 80 – 90%

Sales $6.2B ~$10B

ADJ EBITDA Margins 16.7% 18 – 20%

ROIC 8% 10 – 12%

ADJ EPS $0.87 $2.00+

Normalized Capex (% Sales) 5% 5%

©2020 Graphic Packaging International

15

VISION 2025

Reduce water

usage by 15%

Reduce LDPE usage

by 40%

Reduce green house

gases by 15%

PlanetLeverage industry leading sustainability profile, reducing impact on the environment

4

Reduce energy

consumption by 15%

GPI products

100% recyclable

©2020 Graphic Packaging International

16

VISION 2025

PeopleEngage employees in a high-performance culture

Top quartile

engagement scores

Reduce LTIR from

0.3 to 0.2 (Safety)

GPI University

30 hours of training per

employee, per year

Attract and retain the right

talent

Play on a winning team

©2020 Graphic Packaging International

17

SUSTAINABILITY HAS BECOME A GLOBAL PHENOMENON & MANDATEWHAT BRANDS ARE SAYING….

Source: Goldman Sachs

“Tackling plastic waste is one of my top priorities and I take this challenge personally. We are doing our part to address the issue head on by reducing, recycling and reinventing our packaging.”

—Ramon Laguarta, CEO PepsiCo

Soft drink giants Coca-Cola & PepsiCo have announced they are cutting ties with a trade association representing the plastic industry over concerns their memberships contradict a commitment to reducing waste.

—Newsweek, July 2019

Starbucks is aiming to double the recycled content in [their] cup by 2022. It’s also testing more than 12 greener technologies for paper cup liners.

—CNN, February 2019

Pepsi has committed to using only recyclable, compostable or biodegradable packaging by 2025.

—CNN, July 2019

In Germany, Aldi scrapped single-use bags. Aligned to its pledge to cut down plastic packaging by 25% by 2024, the new compostable bags are made of biodegradable material.

—Forbes, July 2019

The Kellogg Company is expanding its global sustainability commitments to include a goal of working towards 100% reusable, recyclable or compostable packaging by the end of 2025.

—Kellogg Company PR, October 2018

[McDonald’s] wants to have 100% of its customer packaging come from renewable, recycled, or certified sources and have recycling available in all its restaurants [by 2025].

—USA Today, January 2018

©2020 Graphic Packaging International

18

GPI SUSTAINABILITY INITIATIVES SUPPORT CUSTOMER ASPIRATIONS

Source: Goldman Sachs; Molson Coors Sustainability Report 2019

100% by 2025

Renewable / Recyclable Sources

100% by 2025

PBP Recyclable / Reusable / Compostable

17% by 2025

PBP Recycled Content

100% by 2025

Recyclable / Reusable Materials

100% by 2024

Elimination of 10 Problematic Plastics

100% by 2025

Recyclable / Reusable / Compostable

25% by 2025

Recycled Content

100% by 2025Reusable / Recyclable / Compostable / Biodegradable

30% by 2025Recycled Content

100% by 2030Recyclable Packaging

50% by 2030Recycled Content

100% by 2025Recyclable Products

-15%

Water Usage

-15%

Green house gases

-15%

Energy

-40%

LDPE usage

©2020 Graphic Packaging International

19

PAPERBOARD PACKAGING WILL EMERGE AS A WINNERAMONG THE SOLUTIONS PREFERRED BY CONSUMERS

Paperboard Packaging

©2020 Graphic Packaging International

20

LARGE $5 BILLION ADDRESSABLE MARKET ESTIMATED IN NORTH AMERICA AND EUROPE FOR PAPERBOARD CONVERSIONS

Foam Cups Plastic Cups Foam Containers

Beverage Packaging CPET Trays, Bowls Stand-up Pouches

$ $ $

$ $ $

1B 1B 1B

1B 500M 250M

CURRENT MARKET OFFERING

©2020 Graphic Packaging International

21

TARGETING 100-200 BASIS POINTS OF NET ORGANIC GROWTH PER YEAR(10-15% OF ADDRESSABLE MARKET FROM 2020 TO 2025)

Paperboard

bowls

Microwave

cooking

solutions

Insulated

paperboard cups

(hot & cold)Packaging

machinery &

beverage

carriers

Packaging

machinery &

food can

containers

PE-free

cups

High strength

packaging

Food

containers

Ship in own

container (SIOC)

TARGETED, INNOVATIVE SOLUTIONS

Compostable

cups

©2020 Graphic Packaging International

22

GPI WILL SELL A PE-FREE CUP IN 2020 THAT IS COMMERCIALLY VIABLE FOR THE MARKETPLACE

Foam Cups

Major customers announced exits from foam Next gen plant-based lined cup; now more

cost effective

PE Coated Paperboard Cups PE-Free Cups (100% Plant-Based)

+40% cost premium to foam +50% cost premium to PE coated,

reduced to +10% to +15% at scale

Cost premium for 100% plant-based cup is currently ~50% more than a PE coated paper cup.

Expect to reduce the premium to 10-15% at scale with next gen PLA

2013 2019 2020

Recyclable

Renewable

Compostable

90% Renewable

Recyclable

Compostable

90% Renewable

Recyclable

Commercially

Compostable

©2020 Graphic Packaging International

CUMULATIVE GROWTH PLAN (CUSTOMER COMMITTED)

23

INSULATED PAPERBOARD CUP AND BOWL GROWTH IS ACCELERATING

• Consumers’ negativeperception of foam and plasticare driving replacementactions

• Lowest cost option with similarfunctional characteristics

$13M

$50M

$100M

$130M

2019 2020 Est. 2021 Est. 2022 Est.

Customer A Customer B Customer C Other

~$50MConversion from foam

food containers

~$10MPlastic bowl conversion

~$50MHot cup from foam to

paperboard

~$20MSingle wall paper and

polypropylene cups to

double wall cold cup

VALUE DRIVERS

©2020 Graphic Packaging International

CUMULATIVE GROWTH PLAN (CUSTOMER COMMITTED)

24

BEVERAGE PACKAGING GROWTH IN EUROPE IS ACCELERATING

• Beverage brands focused oneliminating plastic & waste

• Improved sustainability profile

• Enhanced premium impact /brand messaging

• Efficient high-speedmachinery solutions

$24M

$50M

$75M

$100M

$1M

$15M

$25M

$40M

2019 2020 Est. 2021 Est. 2022 Est.

Carton Machine

VALUE DRIVERS

©2020 Graphic Packaging International

TRACK RECORD OF ONGOING PRODUCTIVITY CRB MILL CONSOLIDATION

25

TWO MAJOR SOURCES OF SIGNIFICANT PRODUCTIVITY IMPROVEMENT AND MARGIN GROWTH

Mill Curtain Coaters Automation

Monroe Facility

50-70MPer Year

$ 100MAdditional Per Year

$

Kalamazoo

870kT

K1: 370kT

K2: 500kT

East Angus

100kT

White Pigeon

70kT

~1,050kTTotal CRB capacity

Kalamazoo

500kT

K1: 370kT

K3: 130kT

Battle

Creek

210kTEast Angus

100kT

Middletown

170kT

White

Pigeon

70kT

©2020 Graphic Packaging International

SNEEK FACILITY MONROE FACILITY

26

CURTAIN COATERS

ONGOING COMMITMENT TO GENERATING $50-70M IN PRODUCTIVITY EVERY YEAR

• Invested Capital: $25M

• Most productive and flexible folding carton

manufacturing facility in Europe

• Increase sales capacity by $40M to support

conversions from shrink/plastic to paperboard

• Expect ~$10M run-rate EBITDA

• Invested Capital: $180M

• State Of The Art Fully Automated

1.3M ft2 of manufacturing & warehouse space

• Strategically located near West Monroe

paperboard mill to reduce logistics costs

• 400K converting tons per year

• Expect ~$30M run-rate EBITDA

• Invested Capital: ~$115M

• Macon and Kalamazoo investments in place

• West Monroe planned over the next two years

• Significant reduction in Latex and TiO2 usage

• Expect ~$40M run-rate EBITDA

TRACK RECORD OF ONGOING PRODUCTIVITY

©2020 Graphic Packaging International

CURRENT CRB MILL SYSTEM POST CRB MILL CONSOLIDATED SYSTEM

27

CONSOLIDATE FROM 5 TO 3 CRB MILLS, RETAIN OPTIONALITY FOR FURTHER CONSOLIDATION OR GROWTH

Note: Currently purchase ~70kT annually to support existing Mexico converting operations

Kalamazoo500kT

K1: 370kTK3: 130kT

Battle Creek210kT

East Angus100kT

Middletown170kT

Kalamazoo870kT

K1: 370kTK2: 500kT

East Angus100kT

White Pigeon70kT

White Pigeon70kT

~1,050kTTotal CRB capacity

~1,050kTTotal CRB capacity

CRB MILL CONSOLIDATION

©2020 Graphic Packaging International

• Lowest basis weight andcaliper profile in NorthAmerica

• Higher quality paperboardenables internalconverting improvementsand external customerbenefits

• Significantly enhancessustainability profile

28

• Rare opportunity for alarge, highlydifferentiating investment

• Fully supports customermandates for high qualitysustainable paperboard

• High return on capitalemployed with valuedriven by cost reduction

• World-class paperboardtechnology

• Best in class coststructure

• Lowest ongoingmaintenance capital

• Leverage digitally nativetalent pool as populationof skilled machinistsshrinks

• Operating one large andtwo small mills focusesand simplifies operations

• One large mill reducesfinancial impact ofongoing maintenancedowntime and mill systemcomplexity

HIGHLY STRATEGIC AND UNIQUE OPPORTUNITY TO INVEST IN OUR CRB PLATFORM

CRB MILL CONSOLIDATION

AN INVESTMENT

IN THE COREMORE

“FUTURE-PROOF”

FOCUSED, SIMPLIFIED

OPERATIONS

HIGHEST QUALITY

PRODUCT

©2020 Graphic Packaging International

ANNUAL FIXED COSTS VARIABLE COSTS

29

$100M REDUCTION IN ANNUAL FIXED AND VARIABLE COSTS

CRB MILL CONSOLIDATION

~$70MCost Savings

~$30MCost Savings

©2020 Graphic Packaging International

30

UNMATCHED CRB COST STRUCTURE POST INVESTMENT

Source: RISI

GPI Mills

Competitor Mills

CRB MILL CONSOLIDATION

GP

I K

ala

ma

zo

o

GP

I W

hite P

ige

on

GP

I E

ast A

ngu

s

GPI $400/ton

Competitors (Avg)

$532/ton

~$130/ton

advantage

Production = ~2.1M tons

©2020 Graphic Packaging International

QUANTIFIED BENEFITS FINANCIAL RETURNS

31

HIGHLY STRATEGIC AND UNIQUE OPPORTUNITY TO INVEST IN OUR CRB PLATFORM

Note (1) WACC = 7%

Not a material U.S. cash taxpayer until 2022

Fixed Cost Reduction

• ~$70M, versus today’s

footprint

—Close Middletown

—Close Battle Creek

—Close K3 machine

—300+ reduction in

workforce

Variable Cost Reduction

• ~$30M, at today’s

volumes

• Reduced commodity input

consumption

—Freight

—Chemicals

—Energy

—Coatings

—Fiber

CRB MILL CONSOLIDATION

310M 12%

NPV IRR (after tax)

$

($200)

($150)

($100)

($50)

$0

$50

$100

$150

$200

$250

2019 2024 2029 2034 2039 2044 2049

Unlevered Free Cash Flow from CRB Mills

©2020 Graphic Packaging International

32

COMPELLING POSITIVE ENVIRONMENTAL IMPACT

*Information based on Legacy GPI / Source: Schneider Electric and GPK Management Estimates

CRB MILL CONSOLIDATION

Current Future % Change

Green House Gases (Metric Tons)

497K 419K - 16%

Water Usage(Gallons/Ton)

916 614 - 33%

Purchased Energy(KWH/Ton)

1,901 1,562 - 18%

ANNUAL CRB PROFILE

©2020 Graphic Packaging International

FULL YEAR 2019 FINANCIAL RESULTS

(US$ M) 2019 2018 % Chg

Net Sales $6,160 $6,029 +2%

Adj. EBITDA $1,030 $971 +6%

Adj. EBITDA Margin 16.7% 16.1% +60bps

Adj. EPS $0.87 $0.81 +7%

Adj. Cash Flow $528 $469 +13%

Global Liquidity $1,710 $1,280 ------

Integration Rate(1) 68% 67% +100bps

2019 GROWTH & INVESTMENT

• Adj. EBITDA met upwardly revised target,growing +6% y/y

• Adj. EPS increased +7% y/y to $0.87

• Volume driven by acquisitions &sustainability supported net organicgrowth

• Price to commodity input cost relationshipimproved $98 million

• Capital investment back into business of$353M including initial $23M intransformational CRB investment

• $1.7B in global liquidity

• Integration rate increased 100bps to 68%

Adjusted figures represent non-GAAP measures. Please refer to Q4 and full year 2019 earnings press release for

reconciliations to equivalent GAAP measures.

(1) Integration rate is defined as paperboard we produce which is converted in manufacturing facilities we operate.

33©2020 Graphic Packaging International

2020 Est. Adj EBITDA $1,050M – $1,100M

Components

Price $10M – $20M

Volume(1)

Commodity Costs

Net Performance

L&B / Other(2)

$15M – $25M

($0M – $10M)

$65M – $75M

($50M – $60M)

FX $0M

34

(1) Includes EBITDA from Quad folding carton facility acquisition

(2) Other primarily includes inflation associated with insurance and property taxes

(3) Cash interest range assumes Company executes two acquisitions of $250M of minority interest in 2020

1Q 2Q 3Q 4Q

$0 ($55M) +$30M +$25M

Y/Y Net Maintenance Outage Cost Impact to Adj EBITDA

2020 EBITDA & CASH FLOW GUIDANCE COMPONENTS

2020 Est. Cash Flow $200M – $275M

Components

Cap Ex ($600M – $625M)

Interest ($140M – $160M)

Tax ($30M – $40M)

Working Capital ($10M – $30M)

Pension ($10M – $20M)

(3)

©2020 Graphic Packaging International

$353 $600 - $625

2019 2020E 2021E

$600

Normalized

$325

Cash flow expected to meaningfully increase in 2022

ACQUISITION OVERVIEW

• $40M purchase price; estimated $7M ofannualized EBITDA w/ synergies over 24 months

• Approximately 40K tons of paperboardconsumed annually, predominately CRB

• >100 basis point increase in paperboardintegration rate (68% to 69%) upon execution

• Facility strategically located close to manyexisting food, beverage and industrial customers

• Complementary food, beverage and industrialmarket participation

• Compelling post-synergy multiple and above costof capital return

QUAD/GRAPHICS, INC. OMAHA, NE FOLDING CARTON FACILITY ACQUISITION

©2020 Graphic Packaging International 35

TIMING AND LIQUIDITY

36

• Acquiring initial $250M of minority ownership interest per the agreement

• 15.1M partnership units at a price of $16.50

• To be funded from domestic revolving credit facility by 01/31/20

• Next potential $250M transaction is July 2020 per the agreement

• Assuming IP continues to reduce the ownership interest per the agreement, GPK does not expect to be a material U.S. Federal cash taxpayer until 2024

GPK/IP PARTNERSHIP

GPK/IP Partnership

Units

As of

12/31/19

% of

Ownership

Interest

As of

01/31/20

% of

Ownership

Interest

GPK Units 290.2 78.4% 290.2 81.7%

IP Units 79.9 21.6% 64.8 18.3%

Total 370.1 100.0% 355.0 100.0%

©2020 Graphic Packaging International

INITIAL $250M ACQUISITION RESULTS IN A 4% REDUCTION IN TOTAL PARTNERSHIP UNITS

37

MITIGATING EXPOSURE to MARKET and DEMOGRAPIC CHANGES

• Settling approximately $900M in pension obligations related to its largest U.S. pension plan

• Approximately $150M in pension obligations settled through lump sum payments in Q4 2019

• Approximately $750M in pension obligations to be transferred to annuity provider in Q1 2020

• Non-cash settlement charge of $39M in Q4 2019 related to lump sum payments; anticipate a

non-cash settlement charge of approximately $150M in Q1 2020 related to the transfer of the

liability to the annuity provider

U.S. PENSION PLAN SETTLEMENT

©2020 Graphic Packaging International

38

CONTINUED FOCUS ON A BALANCED CAPITAL ALLOCATION STRATEGY WILL BE KEY ENABLER OF ACHIEVING VISION 2025

2015–2019 Adjusted(1) Operating Cash Flow $3.4B

Capital, $1.5B, 45%

Acquisitions, $0.9B, 27%

Share Repurchases,

$0.5B, 15%

Dividends, $0.4B, 13%

$3.4B

(1) Operating cash flow in 2018 and 2019 adjusted to recognize net cash from receivables program. Reconciliation can be found in Company’s Q4 2019 press release.

©2020 Graphic Packaging International

39

EBITDA GROWTH DRIVERS

• Price/commodity input cost recovery

• 100 to 200 basis points of net organic volume growth

• Productivity greater than labor/benefits inflation

• Strategic capital investments in the business to drive significant cost reduction

• Strategic M&A to drive paperboard integration rates at returns above the cost of capital

MULTIPLE EBITDA GROWTH DRIVERS – ANNUALIZED ADJ. EBITDA >$1B

$971

$1,030

$1,050-$1,100

2018 2019 2020E

Adj. EBITDA $s in millions

©2020 Graphic Packaging International

APPENDIX

COMMODITY ANNUAL CONSUMPTION 2019 REVENUE BY CURRENCY

41

SUPPLEMENTAL INFORMATION

Categories Units

Wood (Million tons)

10

Recycled Fiber (Million tons)

1

Natural Gas (MMBTU)

22

Caustic Soda (000, tons)

40

Starch (Million lbs.)

150

TiO2 (Million lbs.)

25

Polyethylene (Million lbs.)

105

80.7%

2.2%

0.4%

0.8%

2.6%0.4%

2.0%5.6% 4.6% 0.7%

USD AUD NZD BRL CAD

CNY MXN GBP EUR JPY

©2020 Graphic Packaging International

Nearly 100% of revenue from defensive end-markets

• Food – 37%

• Beverage – 20%

• Foodservice – 23%

• Non-food consumer staples folding cartons and Other –20%

• North America – 85% of revenues

• Integrated mill to converting network

What happened in 2009?

• Core paper folding carton volume declined 3.6%

• Adj EBITDA improved $81M y/y to $556 million or 14%

─Altivity acquisition closed in March 2008 and added $26 million to EBITDA

─Excluding Altivity, EBITDA increased by $54 million y/y driven by positive price/cost spread, productivity, synergies realization

Adjusted EBITDA and Converting Volume

Beverage,

20%

Food, 37%

Foodservice,

23%

Non-food,

20%

End-Market ExposureRECESSION RESISTANT MODEL

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

0.0

200.0

400.0

600.0

800.0

1000.0

Yo

Y %

Ch

an

ge

US

$,

M

Adjusted EBITDA Net Tons Sold Y/Y % Chg.

©2020 Graphic Packaging International 42

Note: SBS demand was down mid-to-high single digits in 2009, largely recovered in 2010

VISION 2025

GROW WITH THE BEST CUSTOMERS IN THE BEST MARKETS

GENERATE SUPERIOR RETURNS

LEVERAGE INDUSTRY LEADING SUSTAINABILITY PROFILE, REDUCING IMPACT ON THE ENVIRONMENT

ENGAGE EMPLOYEES IN A HIGH-PERFORMANCE CULTURE

2019 Vision 2025

Paperboard Integration 68% 80% – 90%

Sales $6.2B ~$10B

ADJ EBITDA Margin 16.7% 18% – 20%

ROIC 8% 10% – 12%

ADJ EPS $0.87 $2.00+

Normalized Capex

(% of Sales) 5% 5%

#1 paperboard

market share in

North America

and Europe

$400M - $700M

net new product

sales 2020-2025

included in

organic growth

100 - 200

bps/year

sustainability

supported, organic

growth

Strategic, high

return M&A

$400M - $500M in

productivity 2020-

2025 to drive

margin growth

Reduce water

usage by 15%Reduce LDPE

usage by 40%

Reduce green

house gases

by 15%

4

Top quartile

engagement

scores

Play on a winning

team

Reduce LTIR from

0.3 to 0.2 (Safety)

GPI

University

30 hours

of training per

employee, per year

Attract and retain

the right talentReduce energy

consumption

by 15%

GPI products 100%

recyclable

©2020 Graphic Packaging International 43