investor meetings - cerved company€¦ · investor meetings london, ... 11 years of tmt industry...

TRANSCRIPT

Investor Meetings

London, 17-18 September, 2014

CERVED INFORMATION SOLUTIONS S.p.A.

Disclaimer

1

This presentation and any materials distributed in connection herewith (together, the “Presentation”) do not constitute or form a part of, and should not be construed as, an offer for sale or subscription of or solicitation of any offer to purchase or subscribe for any securities, and neither this Presentation nor anything contained herein shall form the basis of, or be relied upon in connection with, or act as an inducement to enter into, any contract or commitment whatsoever. The information contained in this Presentation has not been independently verified and no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness, reasonableness or correctness of the information or opinions contained herein. None of Cerved Information Solutions S.p.A., its subsidiaries or any of their respective employees, advisers, representatives or affiliates shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this Presentation. The information contained in this Presentation is provided as at the date of this Presentation and is subject to change without notice.

Statements made in this Presentation may include forward-looking statements. These statements may be identified by the fact that they use words such as “anticipate”, “estimate”, “should”, “expect”, “guidance”, “project”, “intend”, “plan”, “believe”, and/or other words and terms of similar meaning in connection with, among other things, any discussion of results of operations, financial condition, liquidity, prospects, growth, strategies or developments in the industry in which we operate. Such statements are based on management’s current intentions, expectations or beliefs and involve inherent risks, assumptions and uncertainties, including factors that could delay, divert or change any of them. Forward-looking statements contained in this Presentation regarding trends or current activities should not be taken as a representation that such trends or activities will continue in the future. Actual outcomes, results and other future events may differ materially from those expressed or implied by the statements contained herein. Such differences may adversely affect the outcome and financial effects of the plans and events described herein and may result from, among other things, changes in economic, business, competitive, technological, strategic or regulatory factors and other factors affecting the business and operations of the company. Neither Cerved Information Solutions S.p.A. nor any of its affiliates is under any obligation, and each such entity expressly disclaims any such obligation, to update, revise or amend any forward-looking statements, whether as a result of new information, future events or otherwise. You should not place undue reliance on any such forward-looking statements, which speak only as of the date of this Presentation. It should be noted that past performance is not a guide to future performance. Please also note that interim results are not necessarily indicative of full-year results.

Today’s Presenters

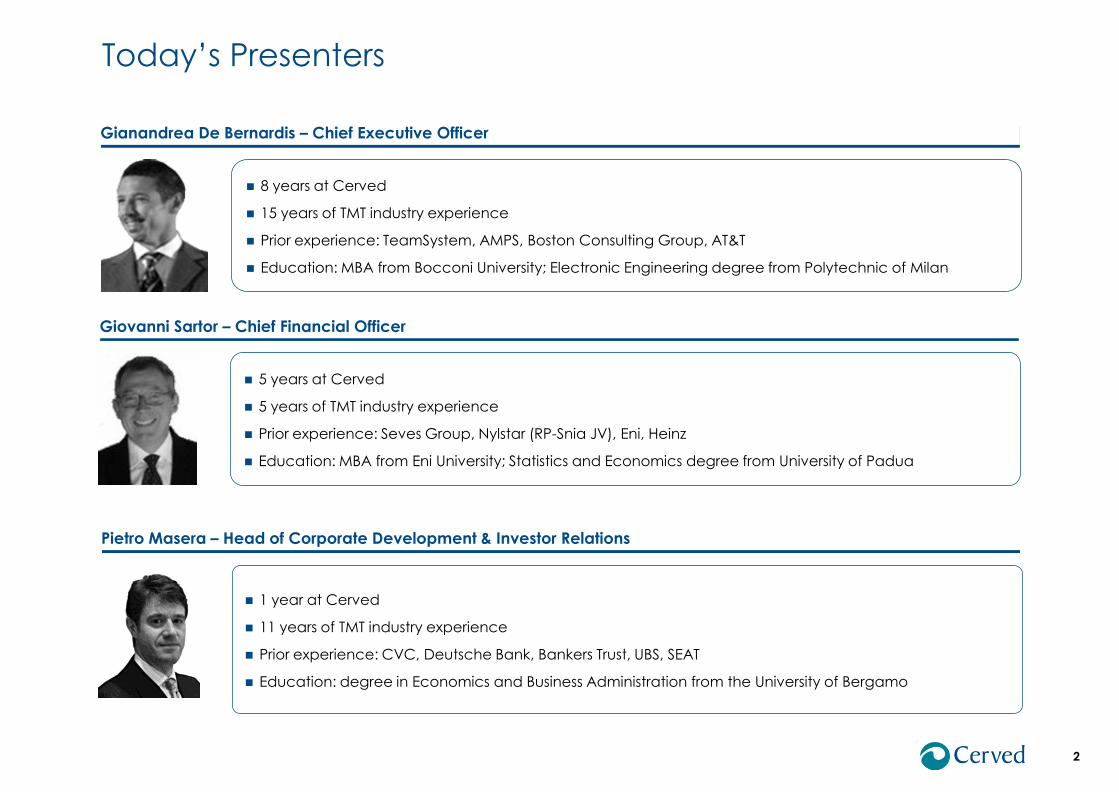

Giovanni Sartor – Chief Financial Officer

5 years at Cerved

5 years of TMT industry experience

Prior experience: Seves Group, Nylstar (RP-Snia JV), Eni, Heinz

Education: MBA from Eni University; Statistics and Economics degree from University of Padua

Pietro Masera – Head of Corporate Development & Investor Relations

1 year at Cerved

11 years of TMT industry experience

Prior experience: CVC, Deutsche Bank, Bankers Trust, UBS, SEAT

Education: degree in Economics and Business Administration from the University of Bergamo

Gianandrea De Bernardis – Chief Executive Officer

8 years at Cerved

15 years of TMT industry experience

Prior experience: TeamSystem, AMPS, Boston Consulting Group, AT&T

Education: MBA from Bocconi University; Electronic Engineering degree from Polytechnic of Milan

2

Table of Contents

3

Investment Case 3

Overview 1

Appendices 4

Current Trading 2

4

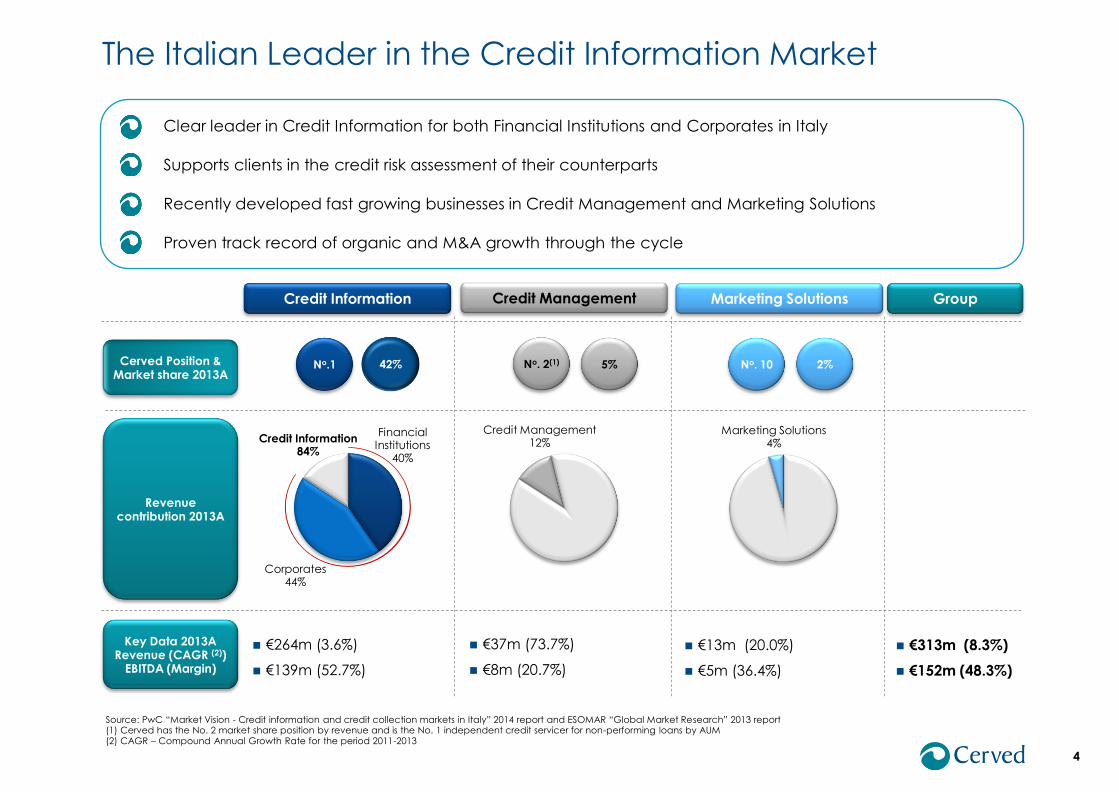

The Italian Leader in the Credit Information Market

Credit Information

€264m (3.6%)

€139m (52.7%)

Credit Information 84%

42% No.1

Credit Management

€37m (73.7%)

€8m (20.7%)

Credit Management 12%

5% No. 2(1)

Marketing Solutions

€13m (20.0%)

€5m (36.4%)

Marketing Solutions 4%

2% No. 10

Source: PwC “Market Vision - Credit information and credit collection markets in Italy” 2014 report and ESOMAR “Global Market Research” 2013 report (1) Cerved has the No. 2 market share position by revenue and is the No. 1 independent credit servicer for non-performing loans by AUM (2) CAGR – Compound Annual Growth Rate for the period 2011-2013

Group

Key Data 2013A Revenue (CAGR (2))

EBITDA (Margin)

€313m (8.3%)

€152m (48.3%)

Revenue contribution 2013A

Corporates 44%

Financial Institutions

40%

Cerved Position & Market share 2013A

Clear leader in Credit Information for both Financial Institutions and Corporates in Italy

Supports clients in the credit risk assessment of their counterparts

Recently developed fast growing businesses in Credit Management and Marketing Solutions

Proven track record of organic and M&A growth through the cycle

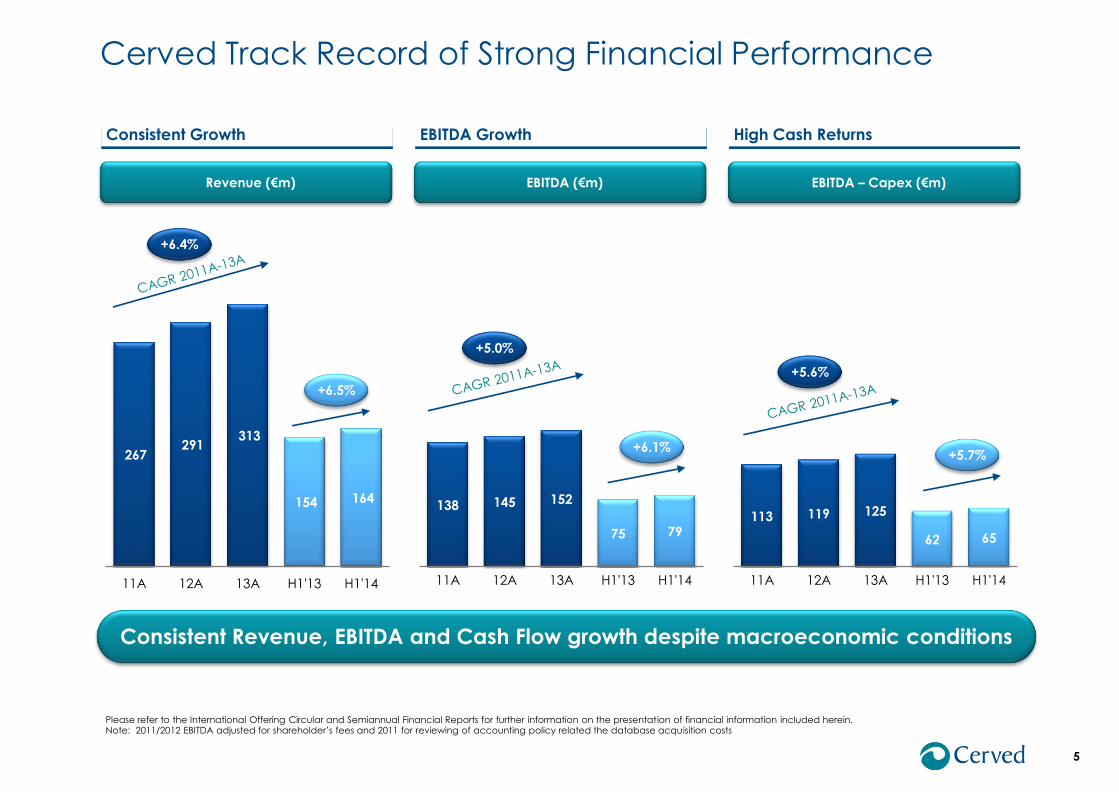

113 119 125

62 65

11A 12A 13A H1'13 H1'14

Cerved Track Record of Strong Financial Performance

5

Consistent Growth EBITDA Growth High Cash Returns

Revenue (€m) EBITDA (€m) EBITDA – Capex (€m)

Consistent Revenue, EBITDA and Cash Flow growth despite macroeconomic conditions

138 145 152

75 79

11A 12A 13A H1'13 H1'14

267 291

313

154 164

11A 12A 13A H1'13 H1'14

+6.4%

+6.5%

+5.0%

+6.1%

Please refer to the International Offering Circular and Semiannual Financial Reports for further information on the presentation of financial information included herein. Note: 2011/2012 EBITDA adjusted for shareholder’s fees and 2011 for reviewing of accounting policy related the database acquisition costs

+5.6%

+5.7%

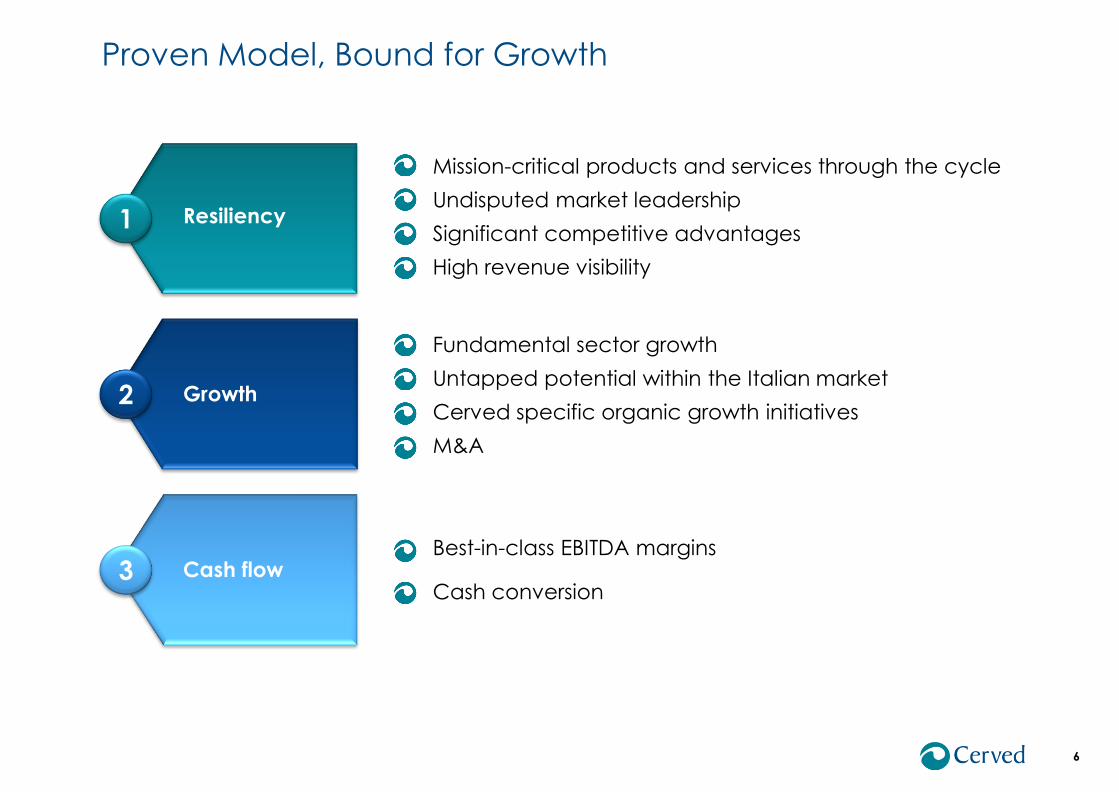

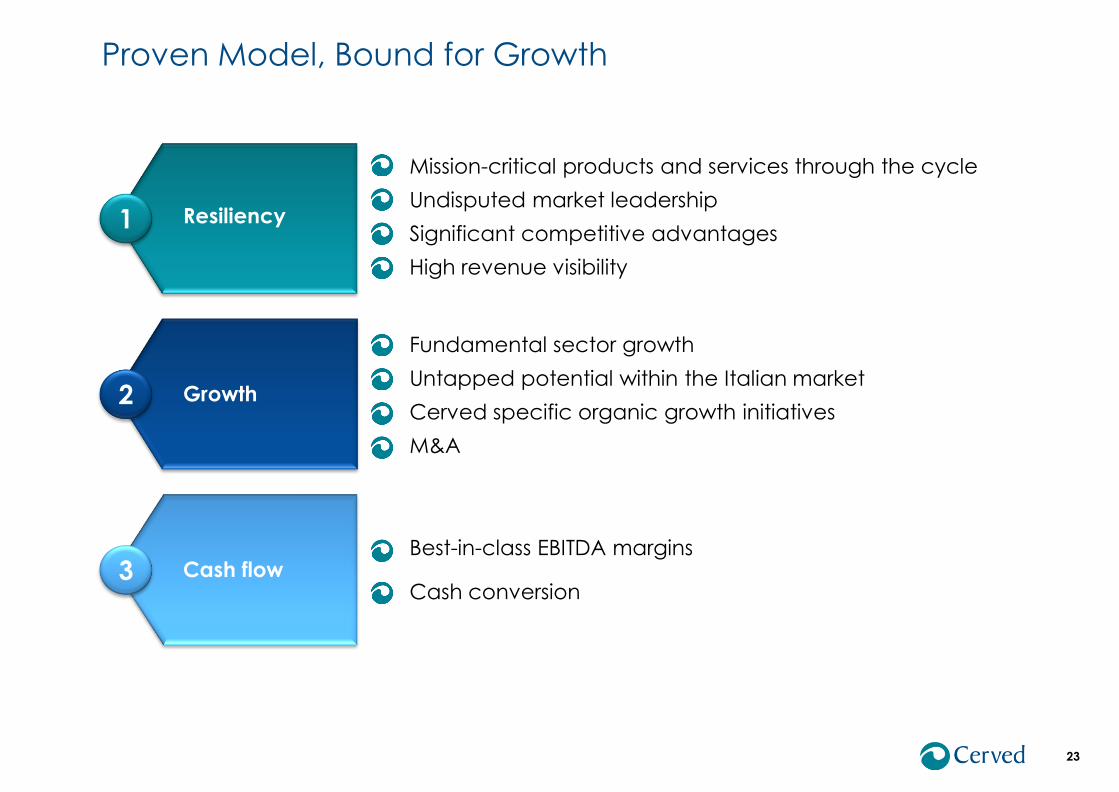

Proven Model, Bound for Growth

6

Mission-critical products and services through the cycle

Undisputed market leadership

Significant competitive advantages

High revenue visibility

Fundamental sector growth

Untapped potential within the Italian market

Cerved specific organic growth initiatives

M&A

Best-in-class EBITDA margins

Cash conversion

2 Growth

3 Cash flow

1 Resiliency

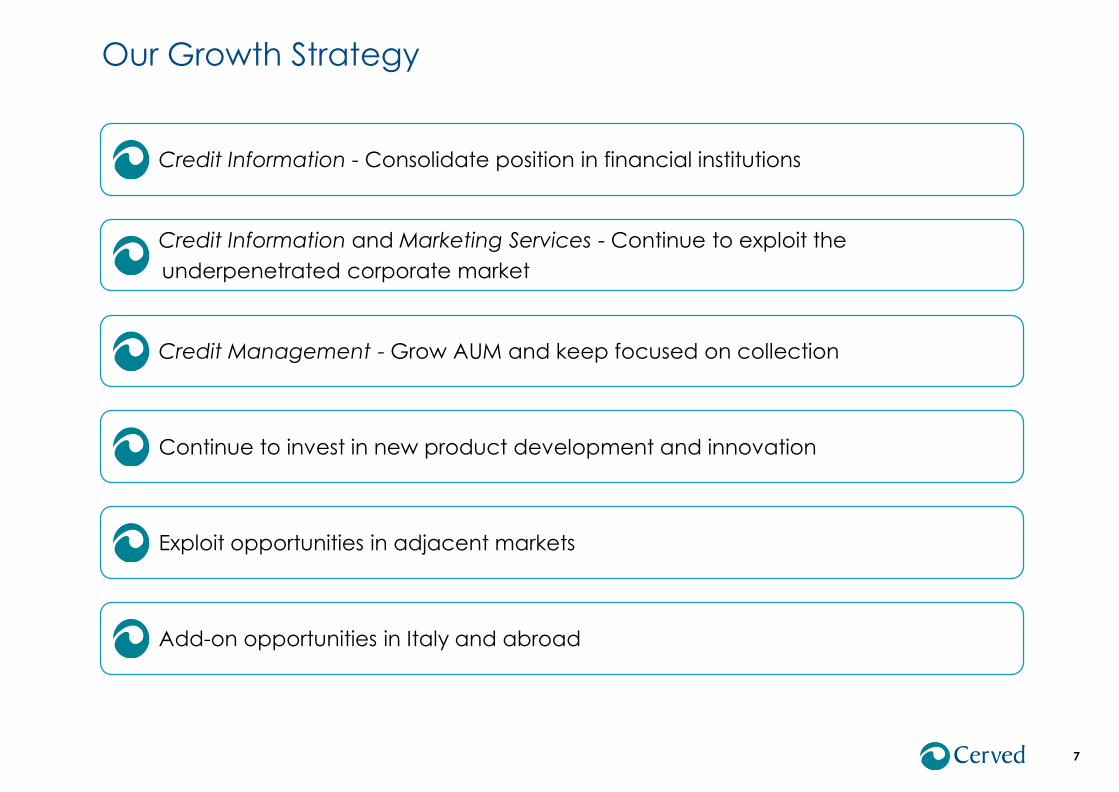

Our Growth Strategy

7

Credit Information - Consolidate position in financial institutions

Credit Information and Marketing Services - Continue to exploit the

underpenetrated corporate market

Exploit opportunities in adjacent markets

Credit Management - Grow AUM and keep focused on collection

Continue to invest in new product development and innovation

Add-on opportunities in Italy and abroad

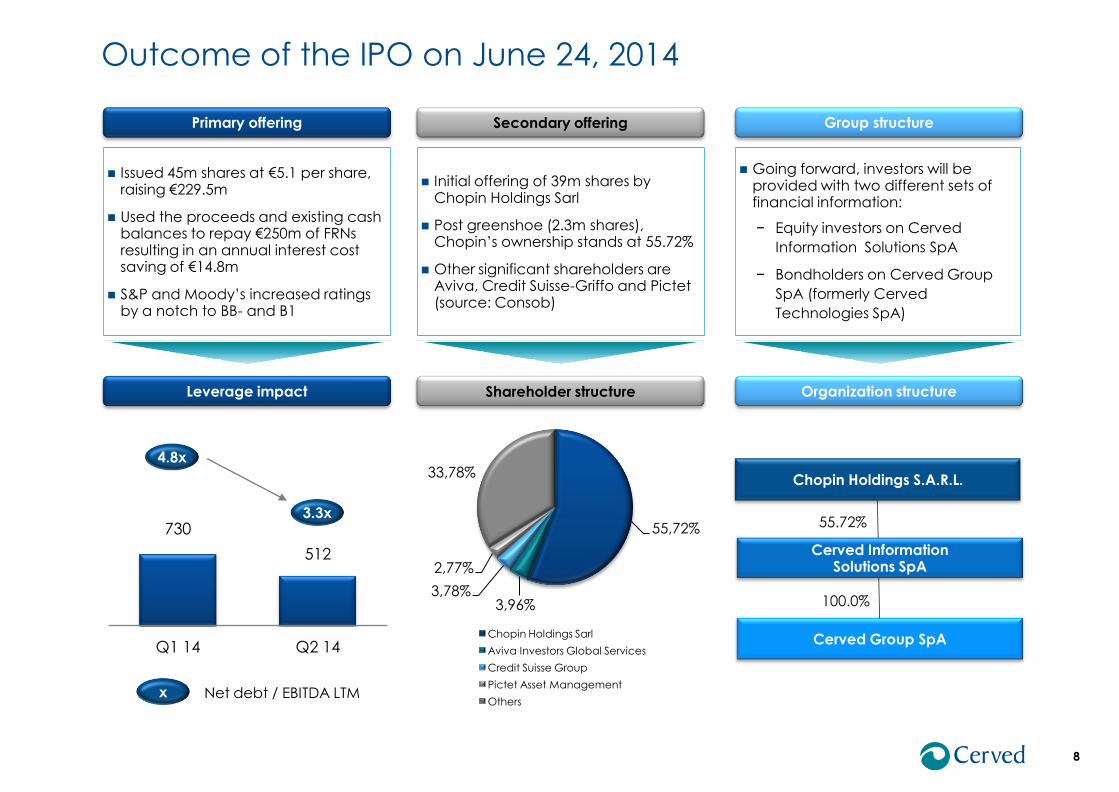

Outcome of the IPO on June 24, 2014

8

Group structure

Organization structure

Going forward, investors will be provided with two different sets of financial information:

− Equity investors on Cerved

Information Solutions SpA

− Bondholders on Cerved Group

SpA (formerly Cerved

Technologies SpA)

Cerved Group SpA

Chopin Holdings S.A.R.L.

Cerved Information Solutions SpA

55.72%

100.0%

Primary offering

Issued 45m shares at €5.1 per share, raising €229.5m

Used the proceeds and existing cash balances to repay €250m of FRNs resulting in an annual interest cost saving of €14.8m

S&P and Moody’s increased ratings by a notch to BB- and B1

Leverage impact

730

512

Q1 14 Q2 14

Net debt / EBITDA LTM

4.8x

x

3.3x 55,72%

3,96% 3,78%

2,77%

33,78%

Chopin Holdings Sarl

Aviva Investors Global Services

Credit Suisse Group

Pictet Asset Management

Others

Secondary offering

Shareholder structure

Initial offering of 39m shares by Chopin Holdings Sarl

Post greenshoe (2.3m shares), Chopin’s ownership stands at 55.72%

Other significant shareholders are Aviva, Credit Suisse-Griffo and Pictet (source: Consob)

Table of Contents

9

Investment Case 3

Overview 1

Appendices 4

Current Trading 2

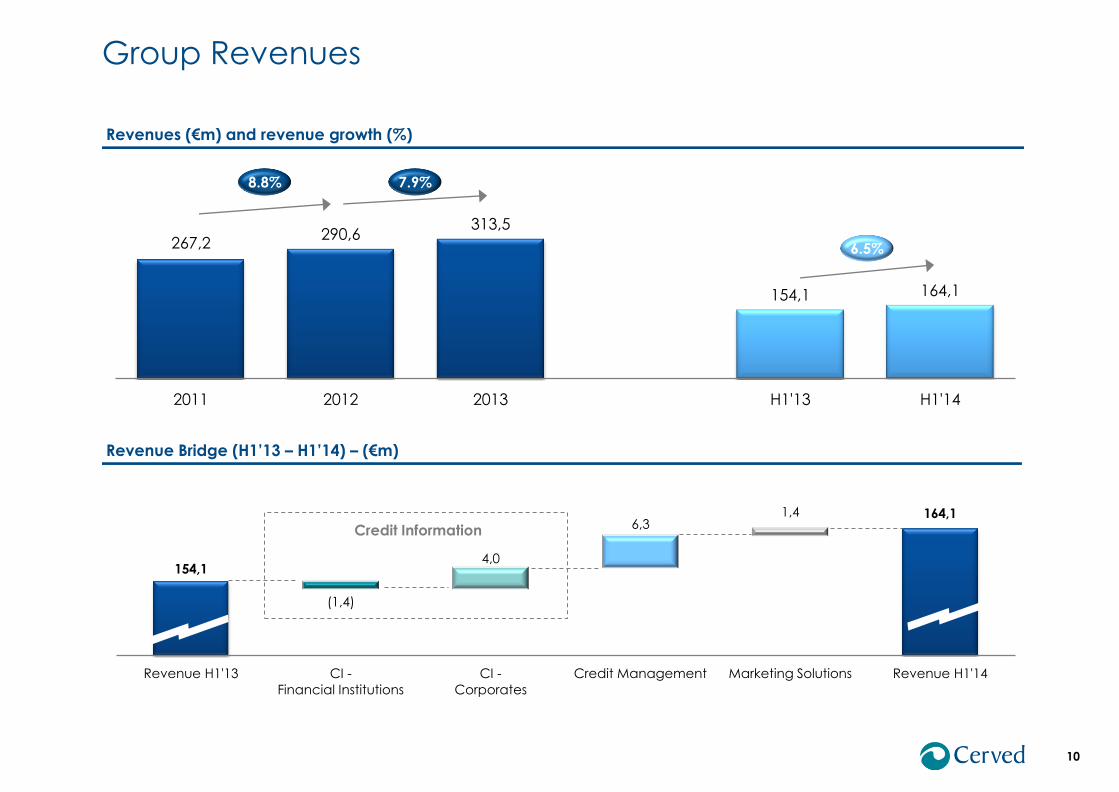

Group Revenues

10

Revenues (€m) and revenue growth (%)

267,2 290,6

313,5

154,1 164,1

2011 2012 2013 H1'13 H1'14

7.9% 8.8%

6.5%

Revenue Bridge (H1’13 – H1’14) – (€m)

154,1

164,1

(1,4)

4,0

6,3 1,4

Revenue H1'13 CI -

Financial Institutions

CI -

Corporates

Credit Management Marketing Solutions Revenue H1'14

Credit Information

74,8

79,3

1,3

2,1

1,1

EBITDA H1'13 Credit

Information

Credit Management Marketing

Solutions

EBITDA H1'14

Group EBITDA

11

EBITDA Bridge (H1’13 – H1’14) – (€m)

EBITDA (1) (€m) and EBITDA margin (%)

138,0 144,7 151,5

74,8 79,3

2011 2012 2013 H1'13 H1'14

4.7% 4.9%

6.1% 48.3% 49.8% 51.6%

48.5% 48.3%

(1) FY 2011 EBITDA is adjusted for Database Acquisition Costs and Shareholder Fees; FY 2012 EBITDA only for Shareholder Fees

12

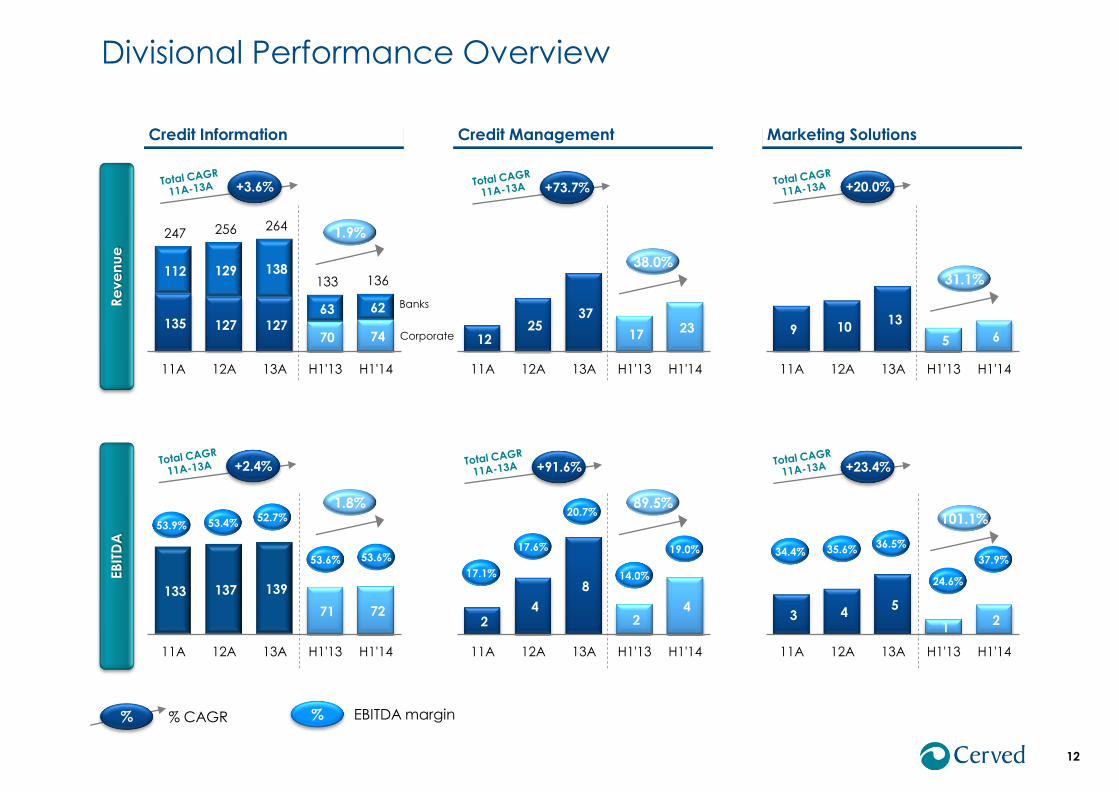

Credit Information Credit Management Marketing Solutions

135 127 127 70 74

112 129 138

63 62

247 256 264

133 136

11A 12A 13A H1'13 H1'14

+3.6%

Re

ve

nu

e

EB

ITD

A

133 137 139

71 72

11A 12A 13A H1'13 H1'14

12 25

37

17 23

11A 12A 13A H1'13 H1'14

2 4

8

2 4

11A 12A 13A H1'13 H1'14

9 10 13

5 6

11A 12A 13A H1'13 H1'14

3 4 5

1 2

11A 12A 13A H1'13 H1'14

34.4% 35.6% 36.5%

24.6%

% EBITDA margin % CAGR

Divisional Performance Overview

+73.7% +20.0%

+2.4% +91.6% +23.4%

37.9%

17.1%

17.6%

20.7%

14.0%

19.0%

53.9% 53.4% 52.7%

53.6% 53.6%

%

38.0%

31.1%

1.9%

89.5% 101.1%

1.8%

Banks

Corporate

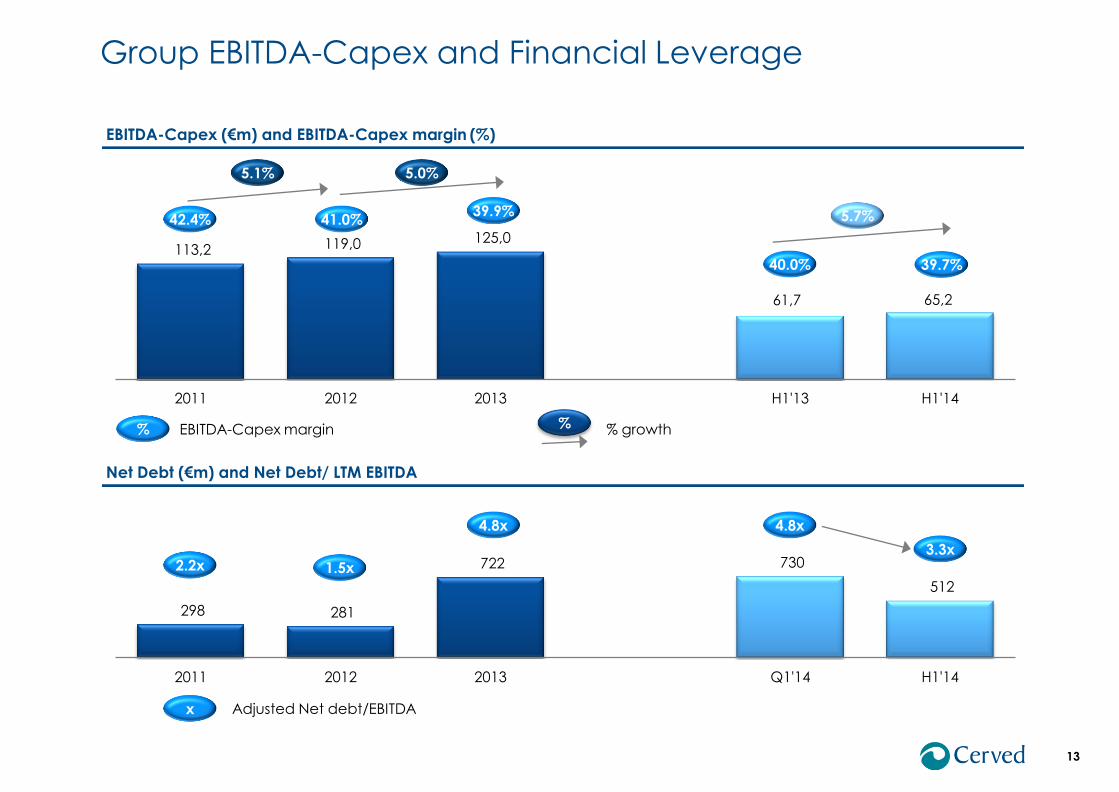

Group EBITDA-Capex and Financial Leverage

13

EBITDA-Capex (€m) and EBITDA-Capex margin (%)

61,7 65,2

113,2 119,0 125,0

2011 2012 2013 H1'13 H1'14

5.0% 5.1%

5.7% 39.9% 41.0% 42.4%

40.0% 39.7%

% EBITDA-Capex margin % % growth

Net Debt (€m) and Net Debt/ LTM EBITDA

298 281

722 730

512

2011 2012 2013 Q1'14 H1'14

2.2x 1.5x

4.8x

x Adjusted Net debt/EBITDA

4.8x

3.3x

1 0 2

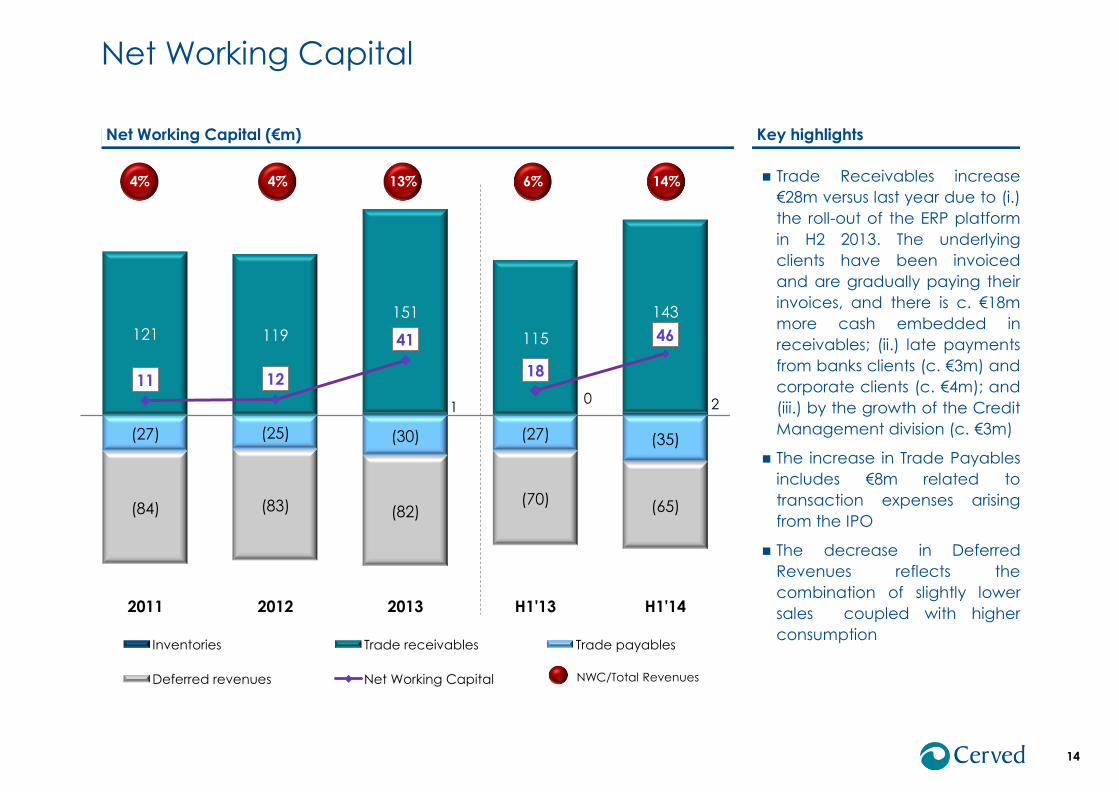

121 119

151

115

143

(27) (25) (30) (27) (35)

(84) (83) (82) (70) (65)

11 12

41

18

46

2011 2012 2013 H1'13 H1'14

Inventories Trade receivables Trade payables

Deferred revenues Net Working Capital

14

4% 4% 13%

NWC/Total Revenues

6% 14% Trade Receivables increase

€28m versus last year due to (i.)

the roll-out of the ERP platform

in H2 2013. The underlying

clients have been invoiced

and are gradually paying their

invoices, and there is c. €18m

more cash embedded in

receivables; (ii.) late payments

from banks clients (c. €3m) and

corporate clients (c. €4m); and

(iii.) by the growth of the Credit

Management division (c. €3m)

The increase in Trade Payables

includes €8m related to

transaction expenses arising

from the IPO

The decrease in Deferred

Revenues reflects the

combination of slightly lower

sales coupled with higher

consumption

Net Working Capital

Key highlights Net Working Capital (€m)

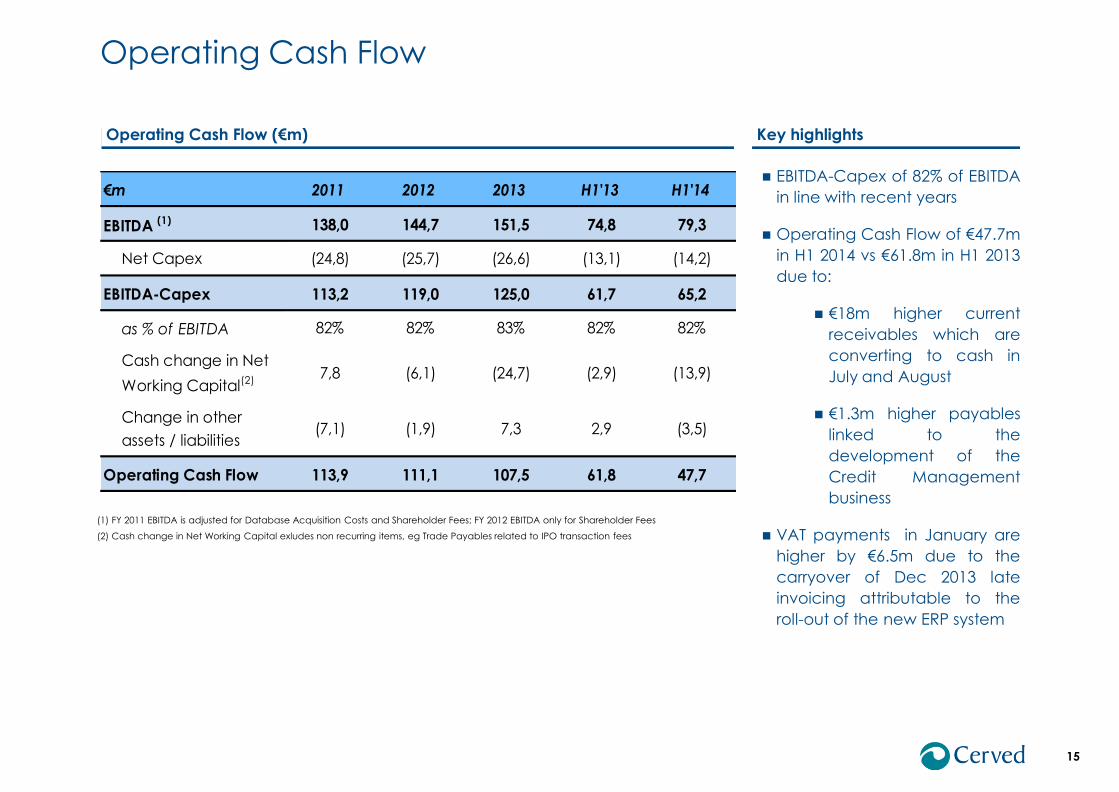

EBITDA-Capex of 82% of EBITDA

in line with recent years

Operating Cash Flow of €47.7m

in H1 2014 vs €61.8m in H1 2013

due to:

€18m higher current

receivables which are

converting to cash in

July and August

€1.3m higher payables

linked to the

development of the

Credit Management

business

VAT payments in January are

higher by €6.5m due to the

carryover of Dec 2013 late

invoicing attributable to the

roll-out of the new ERP system

Key highlights Operating Cash Flow (€m)

Operating Cash Flow

15

(1) FY 2011 EBITDA is adjusted for Database Acquisition Costs and Shareholder Fees; FY 2012 EBITDA only for Shareholder Fees

(2) Cash change in Net Working Capital exludes non recurring items, eg Trade Payables related to IPO transaction fees

€m 2011 2012 2013 H1'13 H1'14

EBITDA (1) 138,0 144,7 151,5 74,8 79,3

Net Capex (24,8) (25,7) (26,6) (13,1) (14,2)

EBITDA-Capex 113,2 119,0 125,0 61,7 65,2

as % of EBITDA 82% 82% 83% 82% 82%

Cash change in Net

Working Capital(2)7,8 (6,1) (24,7) (2,9) (13,9)

Change in other

assets / liabilities(7,1) (1,9) 7,3 2,9 (3,5)

Operating Cash Flow 113,9 111,1 107,5 61,8 47,7

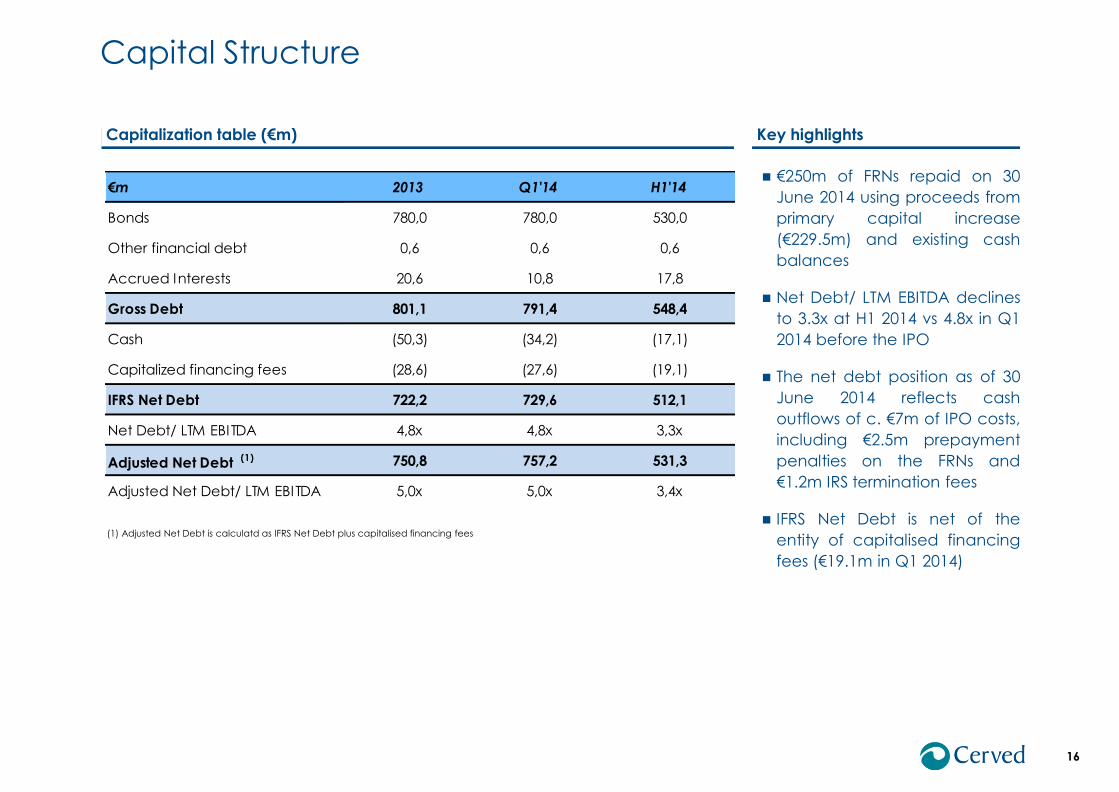

€250m of FRNs repaid on 30

June 2014 using proceeds from

primary capital increase

(€229.5m) and existing cash

balances

Net Debt/ LTM EBITDA declines

to 3.3x at H1 2014 vs 4.8x in Q1

2014 before the IPO

The net debt position as of 30

June 2014 reflects cash

outflows of c. €7m of IPO costs,

including €2.5m prepayment

penalties on the FRNs and

€1.2m IRS termination fees

IFRS Net Debt is net of the

entity of capitalised financing

fees (€19.1m in Q1 2014)

Capital Structure

16

(1) Adjusted Net Debt is calculatd as IFRS Net Debt plus capitalised financing fees

Key highlights Capitalization table (€m)

€m 2013 Q1'14 H1'14

Bonds 780,0 780,0 530,0

Other financial debt 0,6 0,6 0,6

Accrued Interests 20,6 10,8 17,8

Gross Debt 801,1 791,4 548,4

Cash (50,3) (34,2) (17,1)

Capitalized financing fees (28,6) (27,6) (19,1)

IFRS Net Debt 722,2 729,6 512,1

Net Debt/ LTM EBITDA 4,8x 4,8x 3,3x

Adjusted Net Debt (1) 750,8 757,2 531,3

Adjusted Net Debt/ LTM EBITDA 5,0x 5,0x 3,4x

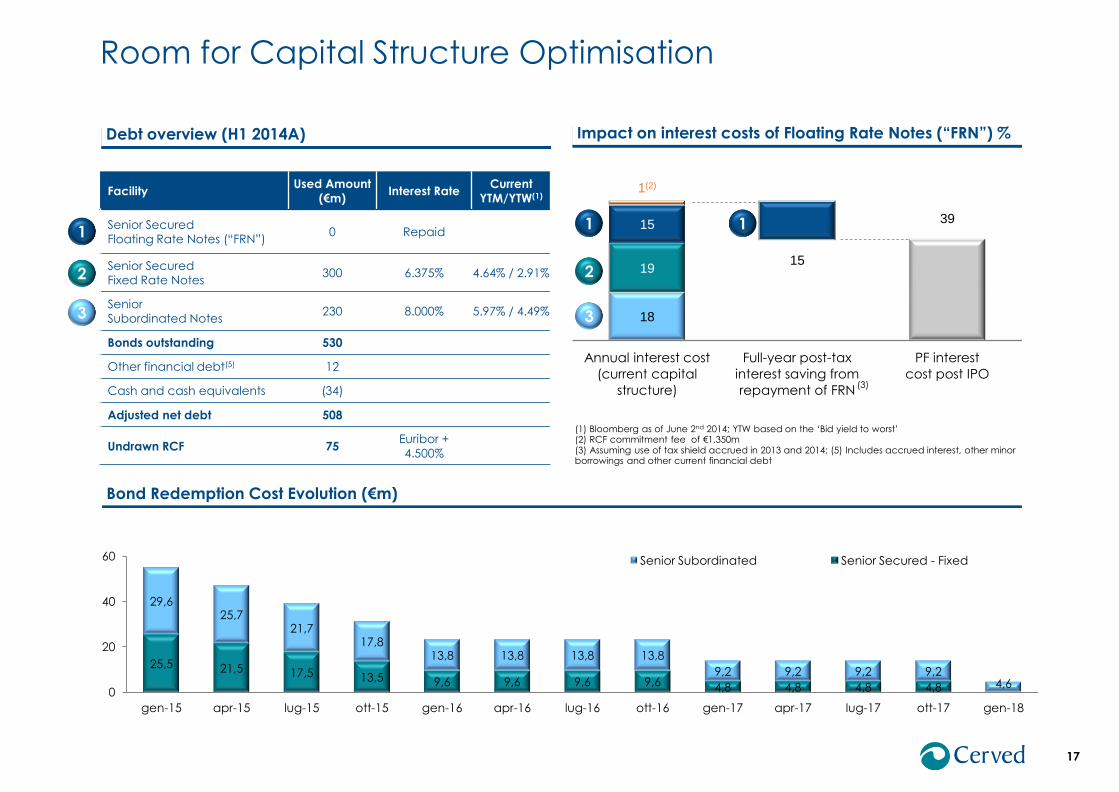

39

18

15 19

15

1(2)

Annual interest cost

(current capital

structure)

Full-year post-tax

interest saving from

repayment of FRN

PF interest

cost post IPO

17

Debt overview (H1 2014A)

Bond Redemption Cost Evolution (€m)

Impact on interest costs of Floating Rate Notes (“FRN”) %

25,5 21,5 17,5 13,5 9,6 9,6 9,6 9,6 4,8 4,8 4,8 4,8

29,6 25,7

21,7 17,8

13,8 13,8 13,8 13,8

9,2 9,2 9,2 9,2 4,6

0

20

40

60

gen-15 apr-15 lug-15 ott-15 gen-16 apr-16 lug-16 ott-16 gen-17 apr-17 lug-17 ott-17 gen-18

Senior Subordinated Senior Secured - Fixed

Facility Used Amount

(€m) Interest Rate

Current

YTM/YTW(1)

Senior Secured

Floating Rate Notes (“FRN”) 0 Repaid

Senior Secured

Fixed Rate Notes 300 6.375% 4.64% / 2.91%

Senior

Subordinated Notes 230 8.000% 5.97% / 4.49%

Bonds outstanding 530

Other financial debt(5) 12

Cash and cash equivalents (34)

Adjusted net debt 508

Undrawn RCF 75 Euribor + 4.500%

(1) Bloomberg as of June 2nd 2014; YTW based on the ‘Bid yield to worst’ (2) RCF commitment fee of €1.350m (3) Assuming use of tax shield accrued in 2013 and 2014; (5) Includes accrued interest, other minor borrowings and other current financial debt

1

2

3

1

2

3

1

(3)

Room for Capital Structure Optimisation

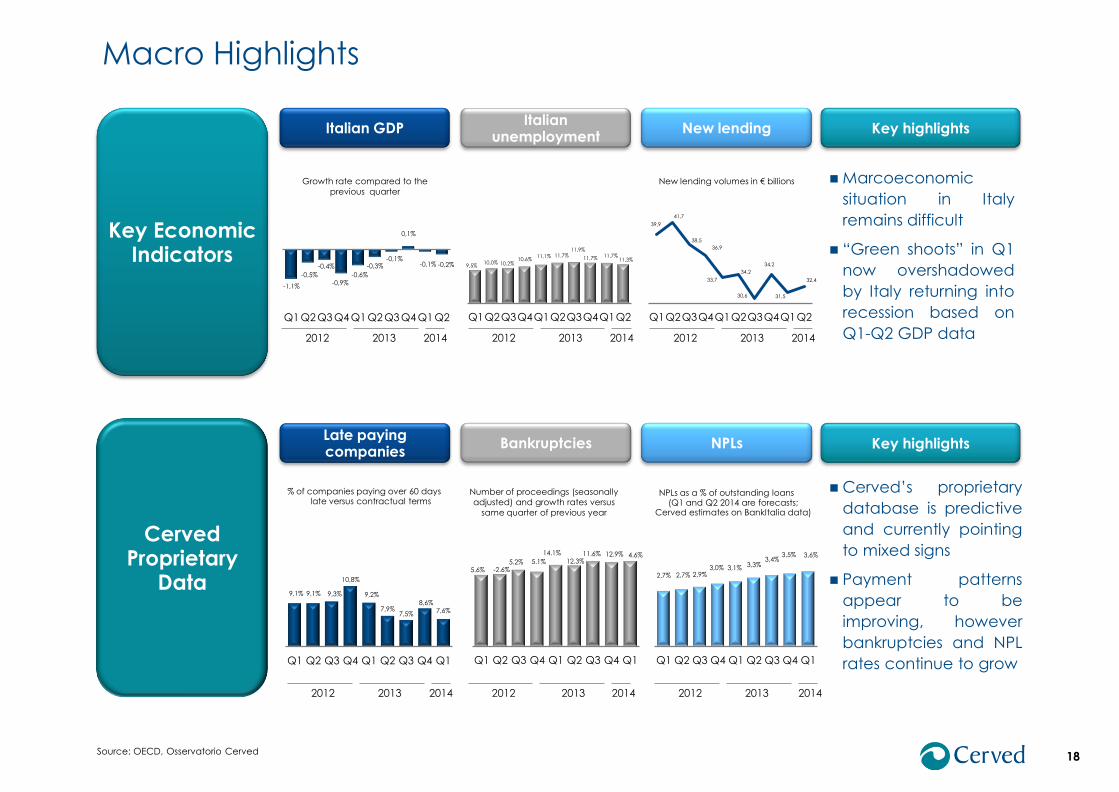

9,1% 9,1% 9,3%

10,8%

9,2%

7,9% 7,5%

8,6% 7,6%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

9,5% 10,0% 10,2%

10,6% 11,1% 11,7%

11,9%

11,7% 11,7% 11,3%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

-1,1%

-0,5%

-0,4%

-0,9% -0,6%

-0,3% -0,1%

0,1%

-0,1% -0,2%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

39,9

41,7

38,5

36,9

33,7

34,2

30,6

34,2

31,5

32,4

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

5.6% -2.6% 5.2% 5.1%

14.1%

12.3% 11.6% 12.9% 4.6%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2,7% 2,7% 2,9% 3,0% 3,1% 3,3%

3,4% 3,5% 3,6%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

Macro Highlights

18

Key Economic Indicators

Cerved Proprietary

Data

Italian unemployment

Italian GDP New lending

Bankruptcies Late paying companies

NPLs

% of companies paying over 60 days late versus contractual terms

Number of proceedings (seasonally

adjusted) and growth rates versus

same quarter of previous year

NPLs as a % of outstanding loans (Q1 and Q2 2014 are forecasts;

Cerved estimates on BankItalia data)

Marcoeconomic

situation in Italy

remains difficult

“Green shoots” in Q1

now overshadowed

by Italy returning into

recession based on

Q1-Q2 GDP data

Key highlights

Cerved’s proprietary

database is predictive

and currently pointing

to mixed signs

Payment patterns

appear to be

improving, however

bankruptcies and NPL

rates continue to grow

Key highlights

Growth rate compared to the

previous quarter

New lending volumes in € billions

2014 2013 2012 2014 2013 2012 2014 2013 2012

2014 2013 2012 2014 2013 2012 2014 2013 2012

Source: OECD, Osservatorio Cerved

Table of Contents

19

Investment Case 3

Overview 1

Appendices 4

Current Trading 2

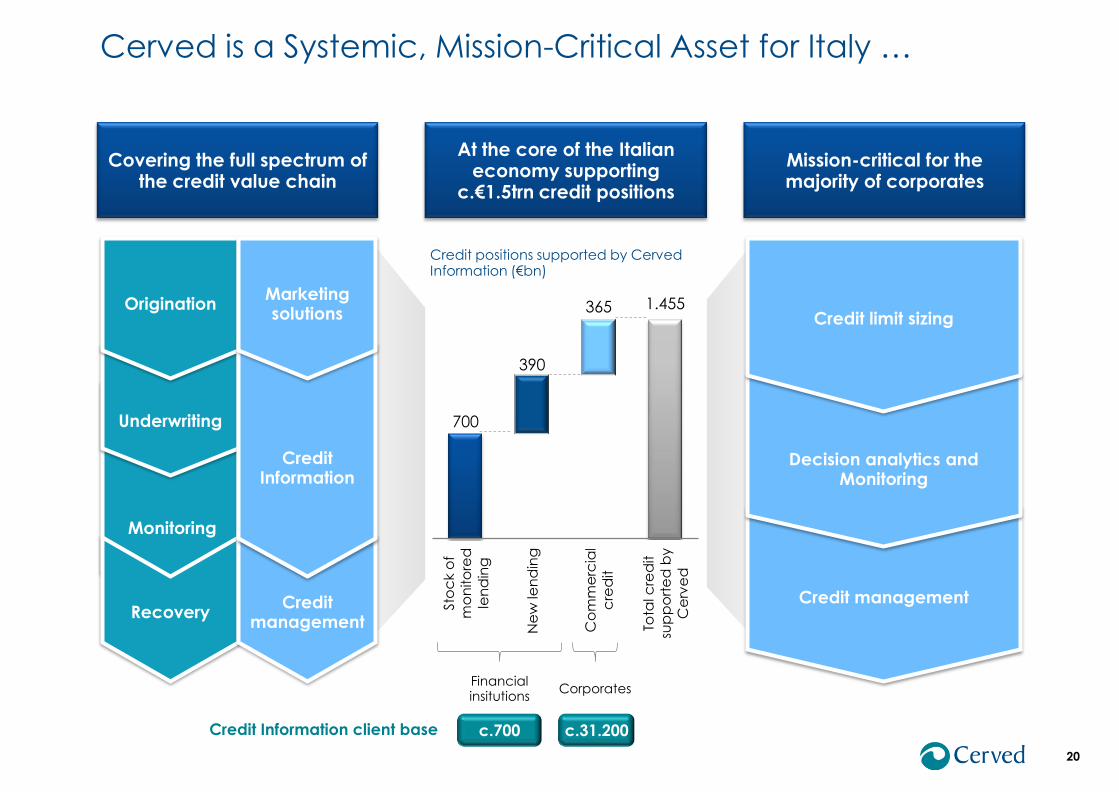

Cerved is a Systemic, Mission-Critical Asset for Italy …

20

Mission-critical for the majority of corporates

At the core of the Italian economy supporting

c.€1.5trn credit positions

700

1.455

390

365

Sto

ck o

f

mo

nito

red

len

din

g

Ne

w le

nd

ing

Co

mm

erc

ial

cre

dit

Tota

l cre

dit

sup

po

rte

d b

y

Ce

rve

d

Credit positions supported by Cerved Information (€bn)

Monitoring

Covering the full spectrum of the credit value chain

Recovery

Underwriting

Origination

c.700 c.31.200 Credit Information client base

Financial insitutions

Corporates

Credit management

Credit Information

Marketing solutions

Credit management

Decision analytics and Monitoring

Credit limit sizing

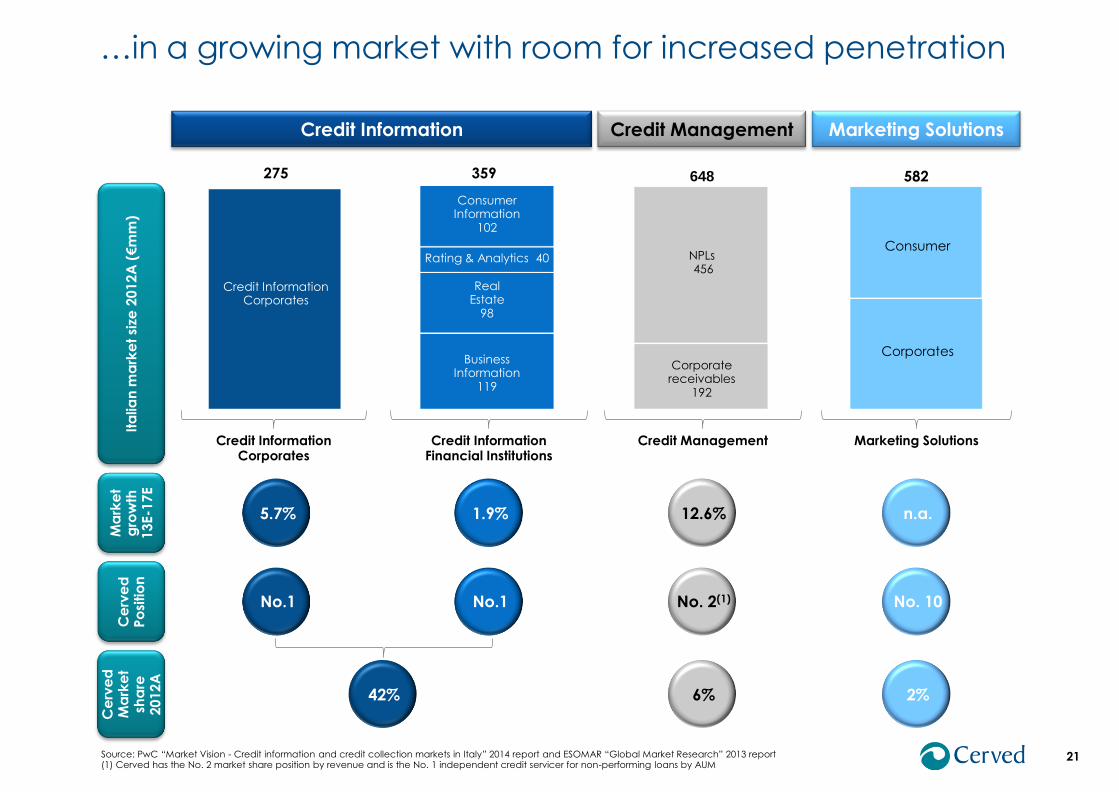

…in a growing market with room for increased penetration

21 Source: PwC “Market Vision - Credit information and credit collection markets in Italy” 2014 report and ESOMAR “Global Market Research” 2013 report (1) Cerved has the No. 2 market share position by revenue and is the No. 1 independent credit servicer for non-performing loans by AUM

2% 42%

Credit Information Marketing Solutions Credit Management

Credit Information Corporates

275

Credit Information Corporates

582 648

Ce

rve

d

Ma

rke

t sh

are

2012A

Ce

rve

d

Po

sitio

n

359

2% 42% 6%

Credit Information Financial Institutions

Credit Management Marketing Solutions

Consumer

Corporates

n.a. 5.7% 12.6% 1.9%

No. 10 No.1 No. 2(1) No.1

Business Information Financial Institutions

119

Real Estate Financial Institutions

98

Consumer Information

Financial Institutions 102

Rating & Analytics Financial Institutions 40

Business Information

119

Real Estate

98

Consumer Information

102

Rating & Analytics 40 Consumer

Corporates

Ita

lian

ma

rke

t si

ze 2

012A

(€m

m)

Ma

rke

t g

row

th

13E-1

7E

NPLs 456

Corporate receivables

192

22

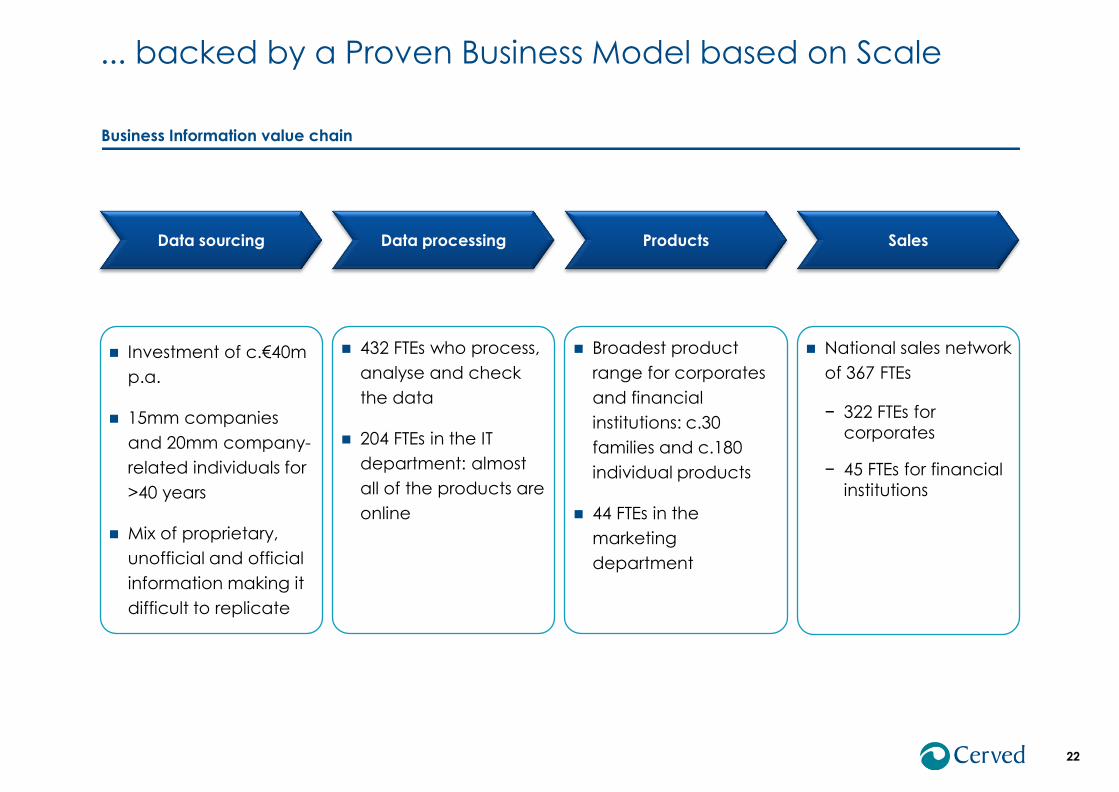

Data sourcing Data processing Products Sales

Business Information value chain

Investment of c.€40m

p.a.

15mm companies

and 20mm company-

related individuals for

>40 years

Mix of proprietary,

unofficial and official

information making it

difficult to replicate

432 FTEs who process,

analyse and check

the data

204 FTEs in the IT

department: almost

all of the products are

online

Broadest product

range for corporates

and financial

institutions: c.30

families and c.180

individual products

44 FTEs in the

marketing

department

National sales network

of 367 FTEs

− 322 FTEs for

corporates

− 45 FTEs for financial

institutions

... backed by a Proven Business Model based on Scale

Proven Model, Bound for Growth

23

Mission-critical products and services through the cycle

Undisputed market leadership

Significant competitive advantages

High revenue visibility

Fundamental sector growth

Untapped potential within the Italian market

Cerved specific organic growth initiatives

M&A

Best-in-class EBITDA margins

Cash conversion

2 Growth

3 Cash flow

1 Resiliency

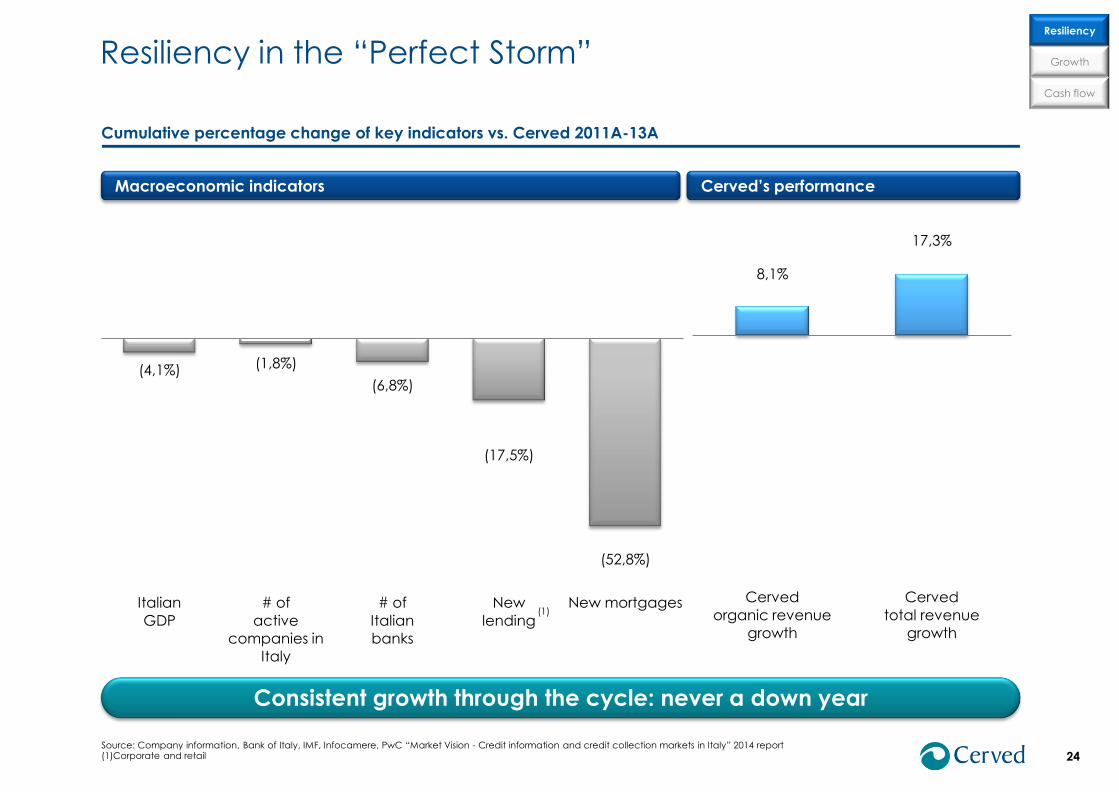

(4,1%) (1,8%)

(6,8%)

(17,5%)

(52,8%)

Italian

GDP

# of

active

companies in

Italy

# of

Italian

banks

New

lending

New mortgages

24

8,1%

17,3%

Cerved

organic revenue

growth

Cerved

total revenue

growth

Macroeconomic indicators

Cumulative percentage change of key indicators vs. Cerved 2011A-13A

Cerved’s performance

Consistent growth through the cycle: never a down year

(1)

Source: Company information, Bank of Italy, IMF, Infocamere, PwC “Market Vision - Credit information and credit collection markets in Italy” 2014 report (1)Corporate and retail

Resiliency

Cash flow

Growth Resiliency in the “Perfect Storm”

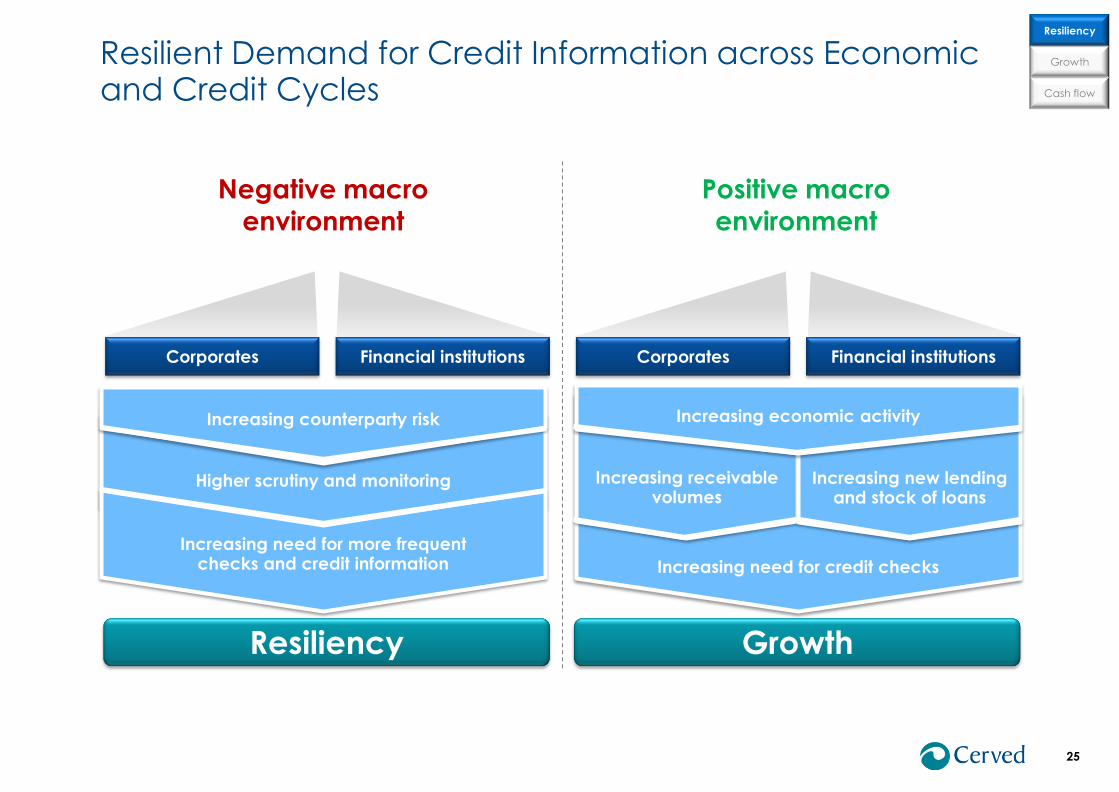

Resilient Demand for Credit Information across Economic and Credit Cycles

25

Increasing need for credit checks

Increasing receivable volumes

Increasing new lending and stock of loans

Increasing economic activity

Higher scrutiny and monitoring

Increasing need for more frequent checks and credit information

Resiliency Growth

Negative macro

environment

Positive macro

environment

Increasing counterparty risk

Corporates Financial institutions Corporates Financial institutions

Resiliency

Cash flow

Growth

26

RMS(1)

Cerved CAGR 11A-13A

Market CAGR 11A-13E

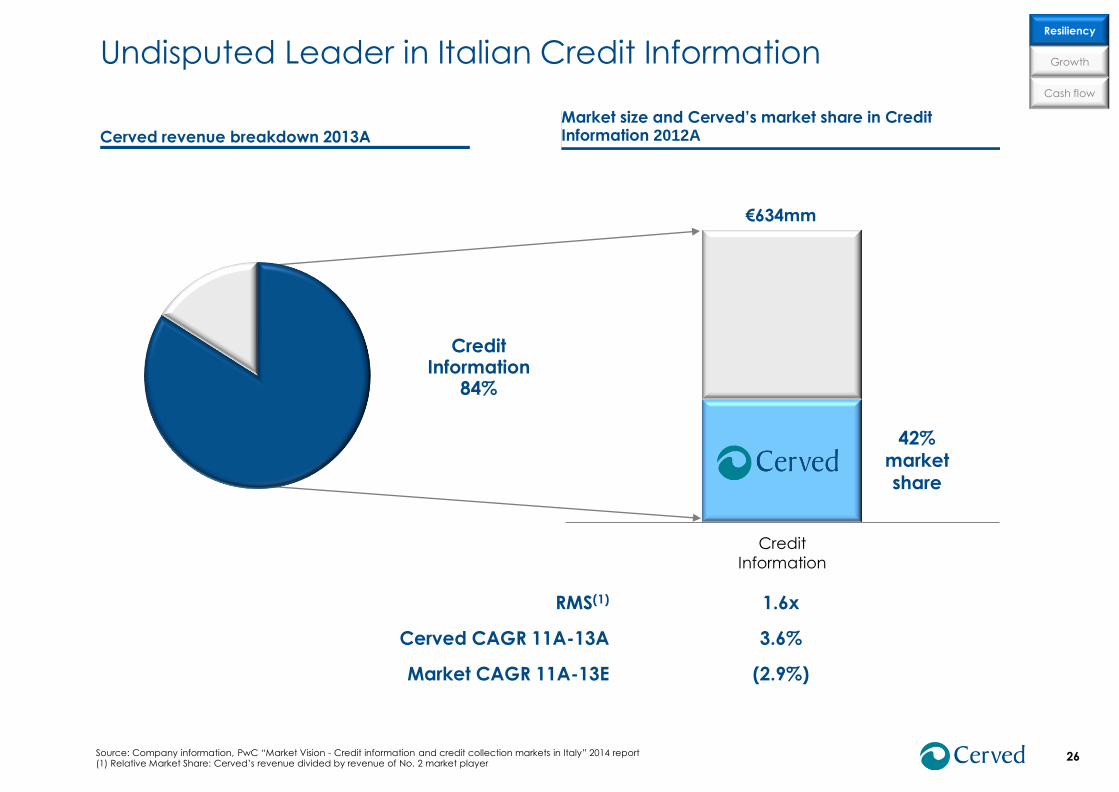

Source: Company information, PwC “Market Vision - Credit information and credit collection markets in Italy” 2014 report (1) Relative Market Share: Cerved’s revenue divided by revenue of No. 2 market player

Credit

Information

1.6x

3.6%

(2.9%)

€634mm

Credit Information

84%

Market size and Cerved’s market share in Credit Information 2012A Cerved revenue breakdown 2013A

42% market share

Resiliency

Cash flow

Growth Undisputed Leader in Italian Credit Information

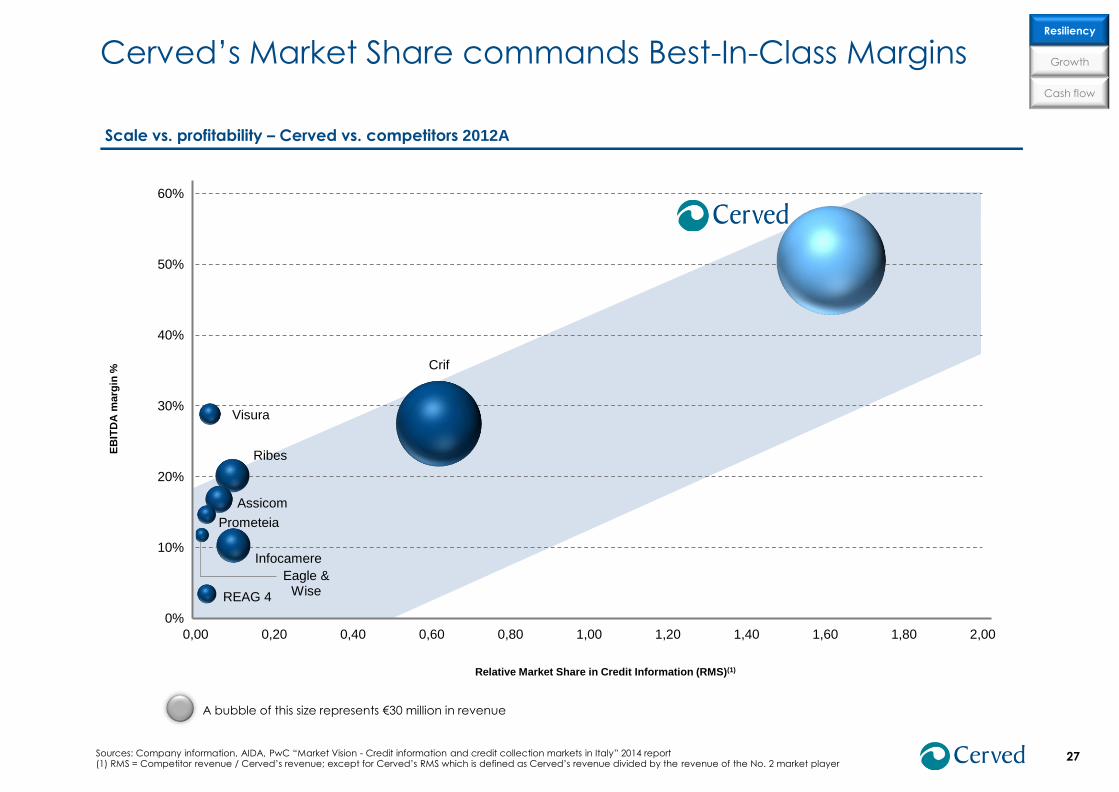

Crif

Infocamere

Ribes

Assicom

Visura

REAG 4

Prometeia

Eagle & Wise

0%

10%

20%

30%

40%

50%

60%

0,00 0,20 0,40 0,60 0,80 1,00 1,20 1,40 1,60 1,80 2,00

EB

ITD

A m

arg

in %

Relative Market Share in Credit Information (RMS)(1)

27 Sources: Company information, AIDA, PwC “Market Vision - Credit information and credit collection markets in Italy” 2014 report (1) RMS = Competitor revenue / Cerved’s revenue; except for Cerved’s RMS which is defined as Cerved’s revenue divided by the revenue of the No. 2 market player

Scale vs. profitability – Cerved vs. competitors 2012A

A bubble of this size represents €30 million in revenue

Resiliency

Cash flow

Growth Cerved’s Market Share commands Best-In-Class Margins

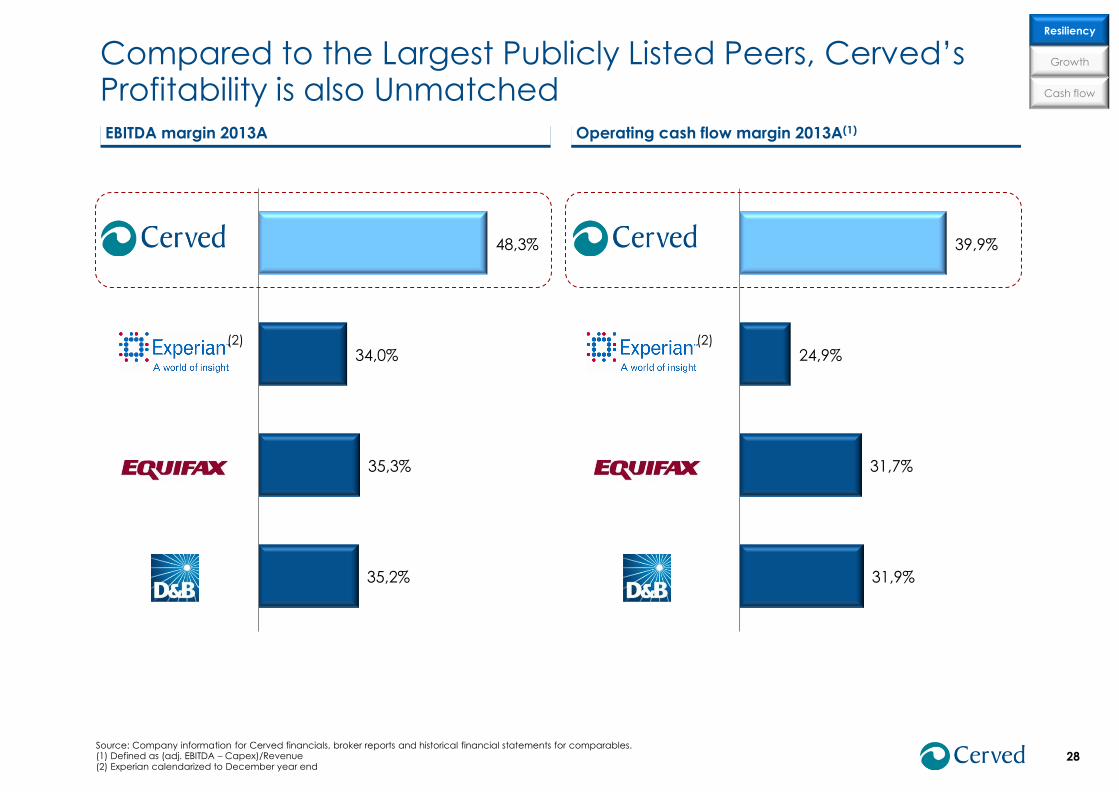

35,2%

35,3%

34,0%

48,3%

28

EBITDA margin 2013A Operating cash flow margin 2013A(1)

Source: Company information for Cerved financials, broker reports and historical financial statements for comparables. (1) Defined as (adj. EBITDA – Capex)/Revenue (2) Experian calendarized to December year end

31,9%

31,7%

24,9%

39,9%

(2) (2)

Resiliency

Cash flow

Growth Compared to the Largest Publicly Listed Peers, Cerved’s Profitability is also Unmatched

29

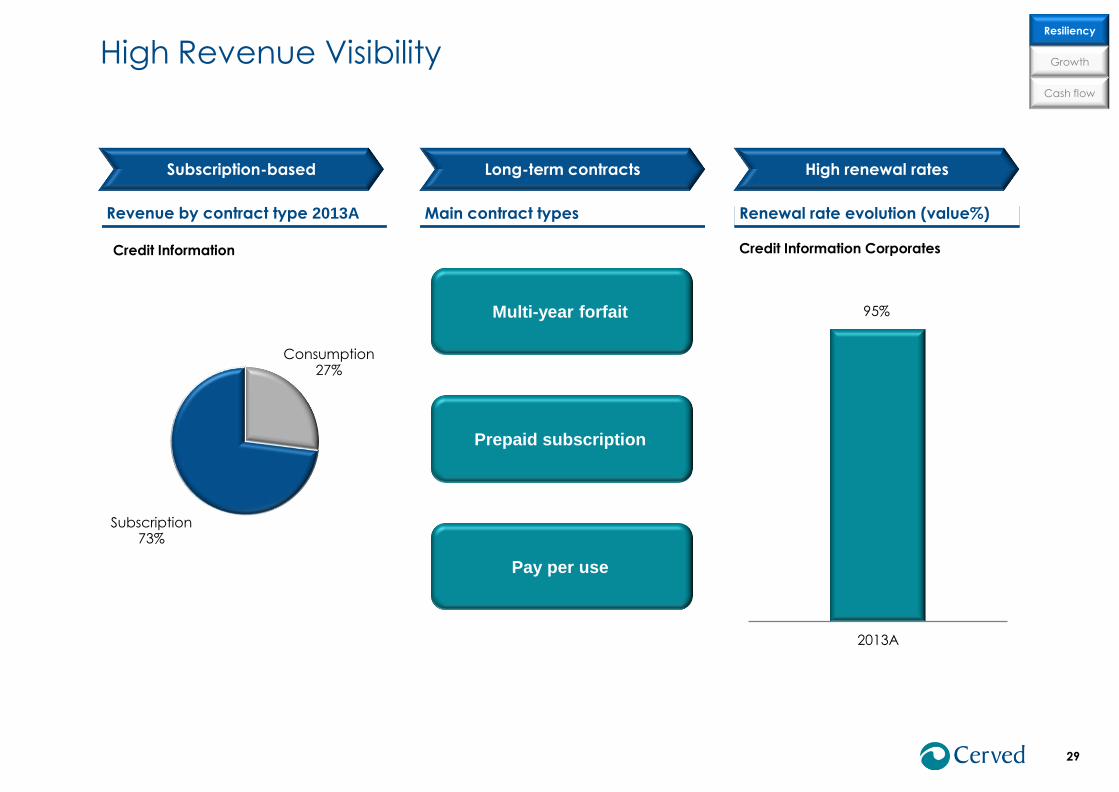

Subscription-based

Revenue by contract type 2013A

Consumption 27%

Subscription 73%

Credit Information

Long-term contracts

Main contract types

High renewal rates

95%

2013A

Credit Information Corporates

Renewal rate evolution (value%)

Multi-year forfait

Prepaid subscription

Pay per use

Resiliency

Cash flow

Growth High Revenue Visibility

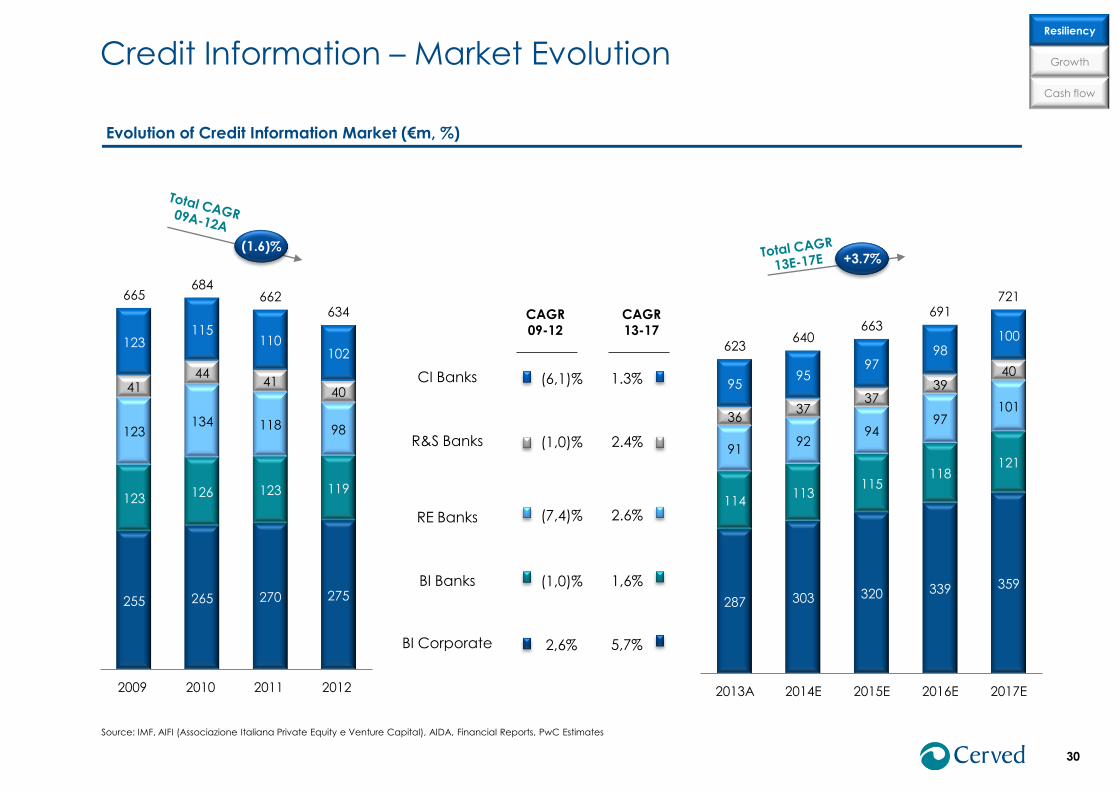

255 265 270 275

123 126 123 119

123 134 118 98

41 44

41 40

123 115

110 102

665 684

662 634

2009 2010 2011 2012

287 303 320 339 359

114 113

115 118

121 91

92 94

97 101

36 37

37 39

40 95

95 97

98 100

623 640

663 691

721

2013A 2014E 2015E 2016E 2017E

Credit Information – Market Evolution

30

Resiliency

Cash flow

Growth

Evolution of Credit Information Market (€m, %)

(6,1)%

(1,0)%

(7,4)%

(1,0)%

2,6%

CAGR

13-17

1.3%

2.4%

2.6%

1,6%

5,7%

+3.7%

CAGR

09-12

Source: IMF, AIFI (Associazione Italiana Private Equity e Venture Capital), AIDA, Financial Reports, PwC Estimates

CI Banks

R&S Banks

RE Banks

BI Banks

BI Corporate

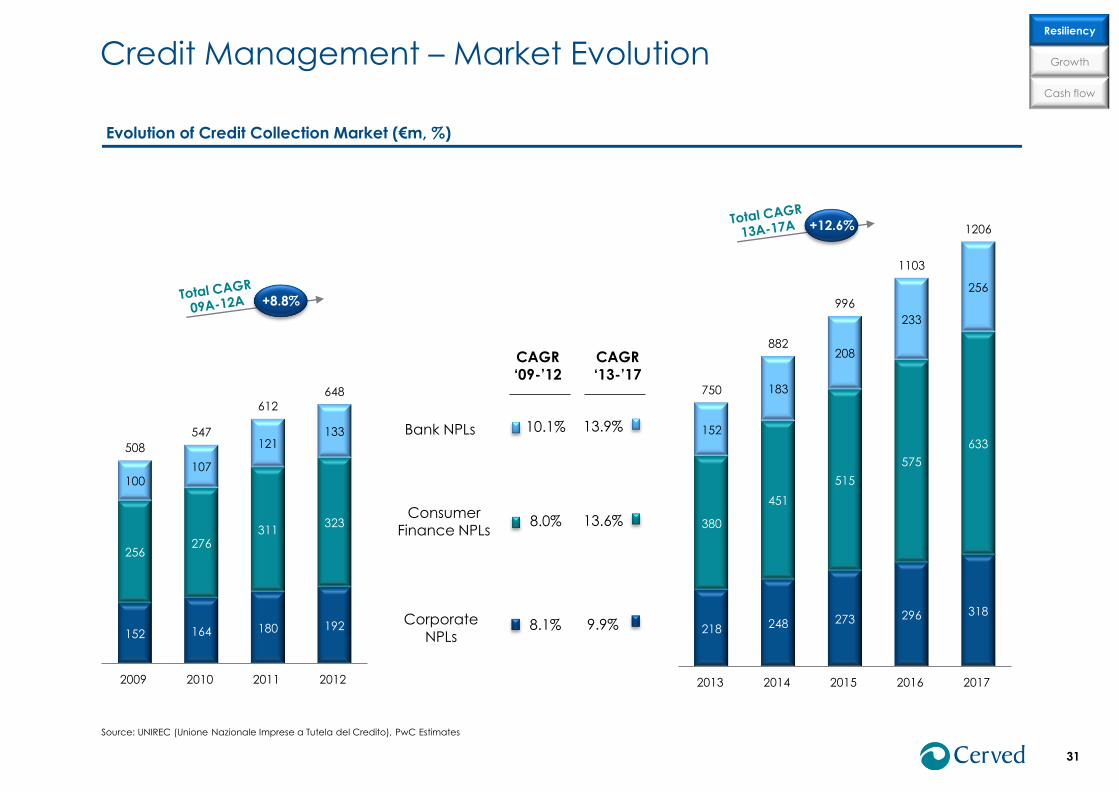

Credit Management – Market Evolution

31

Resiliency

Cash flow

Growth

Evolution of Credit Collection Market (€m, %)

152 164 180 192

256 276

311 323

100 107

121 133

508

547

612

648

2009 2010 2011 2012

Source: UNIREC (Unione Nazionale Imprese a Tutela del Credito), PwC Estimates

218 248 273 296 318

380

451

515

575

633 152

183

208

233

256

750

882

996

1103

1206

2013 2014 2015 2016 2017

+8.8%

+12.6%

10.1%

8.0%

8.1%

CAGR ‘13-’17

13.9%

13.6%

9.9%

CAGR ‘09-’12

Bank NPLs

Consumer Finance NPLs

Corporate NPLs

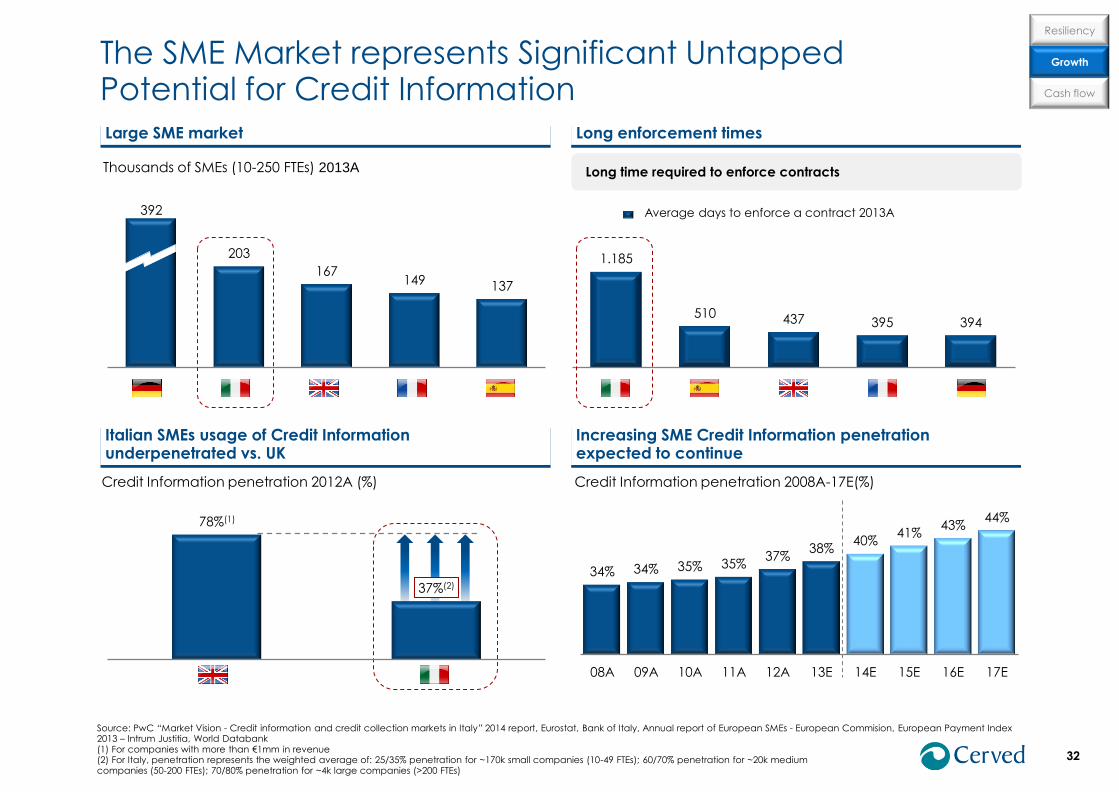

Increasing SME Credit Information penetration expected to continue

1.185

510 437 395 394

The SME Market represents Significant Untapped Potential for Credit Information

Large SME market

Thousands of SMEs (10-250 FTEs) 2013A

Long enforcement times

Long time required to enforce contracts

34% 34% 35% 35% 37%

38% 40%

41% 43%

44%

08A 09A 10A 11A 12A 13E 14E 15E 16E 17E

Source: PwC “Market Vision - Credit information and credit collection markets in Italy” 2014 report, Eurostat, Bank of Italy, Annual report of European SMEs - European Commision, European Payment Index 2013 – Intrum Justitia, World Databank (1) For companies with more than €1mm in revenue (2) For Italy, penetration represents the weighted average of: 25/35% penetration for ~170k small companies (10-49 FTEs); 60/70% penetration for ~20k medium companies (50-200 FTEs); 70/80% penetration for ~4k large companies (>200 FTEs)

392

203

167 149 137

Credit Information penetration 2012A (%) Credit Information penetration 2008A-17E(%)

32

Italian SMEs usage of Credit Information underpenetrated vs. UK

Average days to enforce a contract 2013A

Resiliency

Cash flow

Growth

78%(1)

37%(2)

Marketing Solutions Credit Management

3,9

2,6

2,0

0,6 0,4

€648mm

Credit Information 84%

Cerved revenue breakdown 2013A

Marketing Solutions

4%

Credit Management

12%

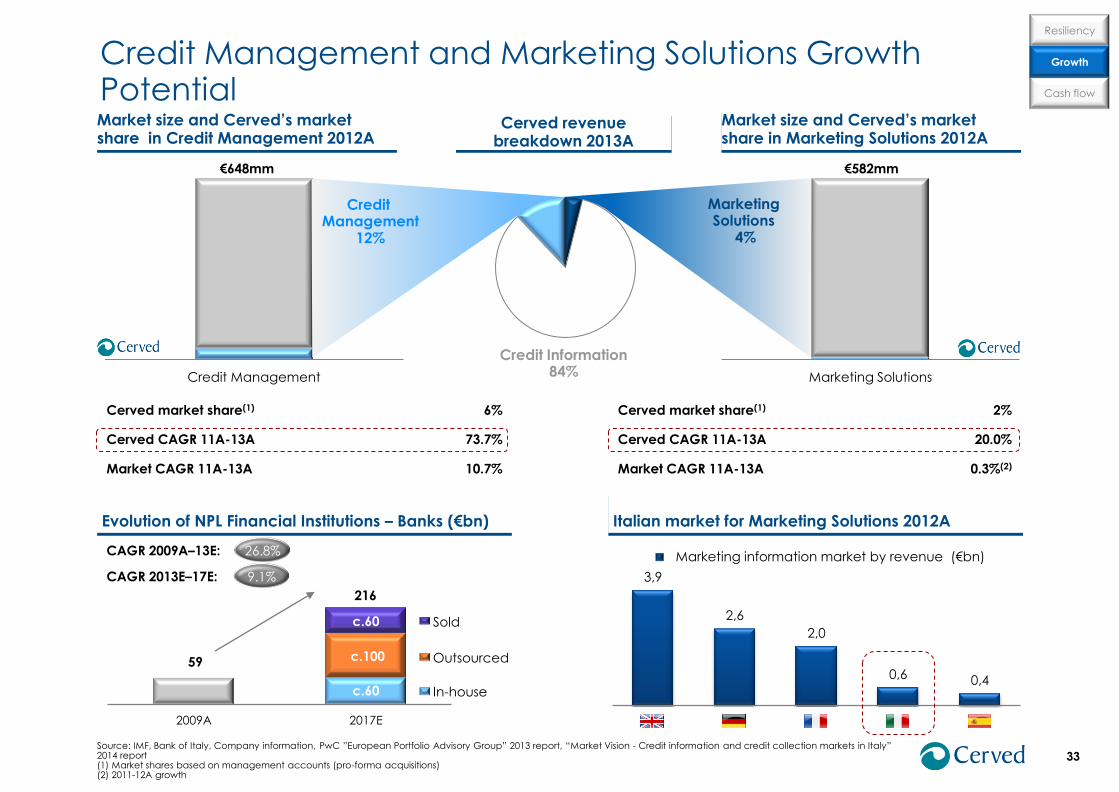

Credit Management and Marketing Solutions Growth Potential

33

Market size and Cerved’s market share in Credit Management 2012A

Cerved market share(1)

Cerved CAGR 11A-13A

Market CAGR 11A-13A

6%

73.7%

10.7%

€582mm

Italian market for Marketing Solutions 2012A

Source: IMF, Bank of Italy, Company information, PwC ”European Portfolio Advisory Group” 2013 report, “Market Vision - Credit information and credit collection markets in Italy” 2014 report (1) Market shares based on management accounts (pro-forma acquisitions) (2) 2011-12A growth

Market size and Cerved’s market share in Marketing Solutions 2012A

2%

20.0%

0.3%(2)

Cerved market share(1)

Cerved CAGR 11A-13A

Market CAGR 11A-13A

Evolution of NPL Financial Institutions – Banks (€bn)

59

c.60

c.100

c.60

2009A 2017E

216

26.8%

9.1%

CAGR 2009A–13E:

CAGR 2013E–17E:

In-house

Outsourced

Sold

Resiliency

Cash flow

Growth

Marketing information market by revenue (€bn)

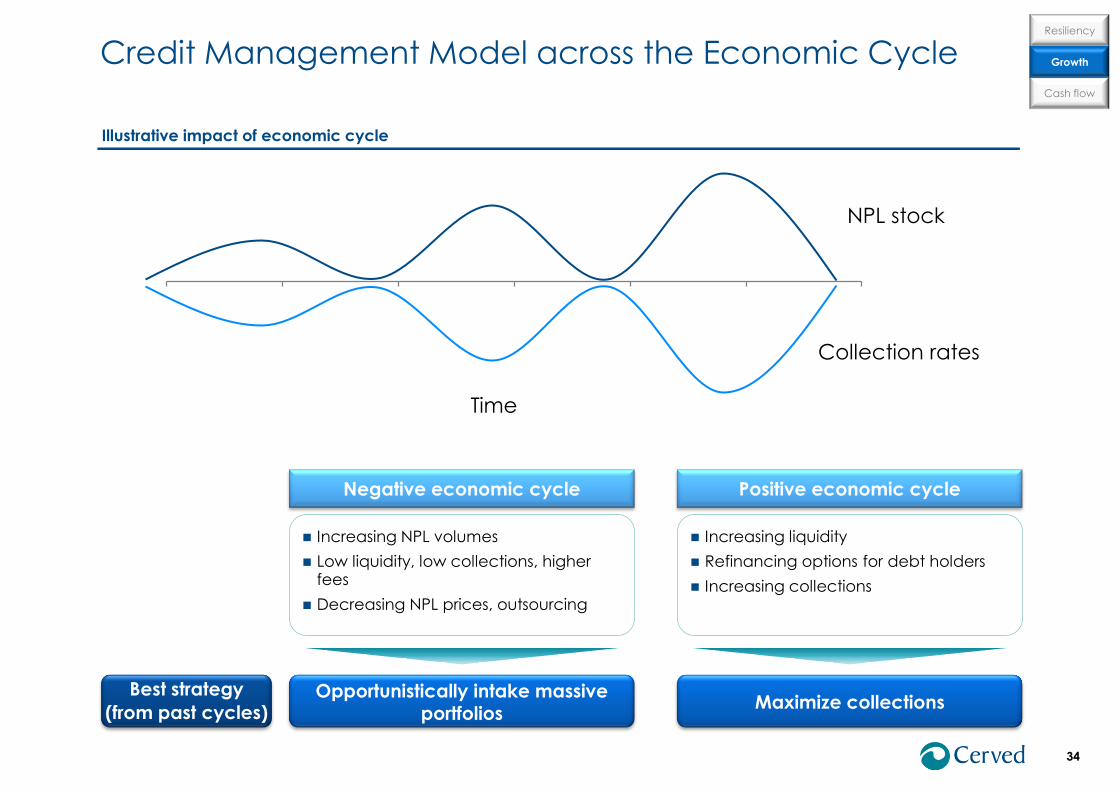

Increasing NPL volumes

Low liquidity, low collections, higher fees

Decreasing NPL prices, outsourcing

Credit Management Model across the Economic Cycle

34

Negative economic cycle

Opportunistically intake massive portfolios

Maximize collections Best strategy

(from past cycles)

Positive economic cycle

Increasing liquidity

Refinancing options for debt holders

Increasing collections

Resiliency

Cash flow

Growth

Illustrative impact of economic cycle

NPL stock

Collection rates

Time

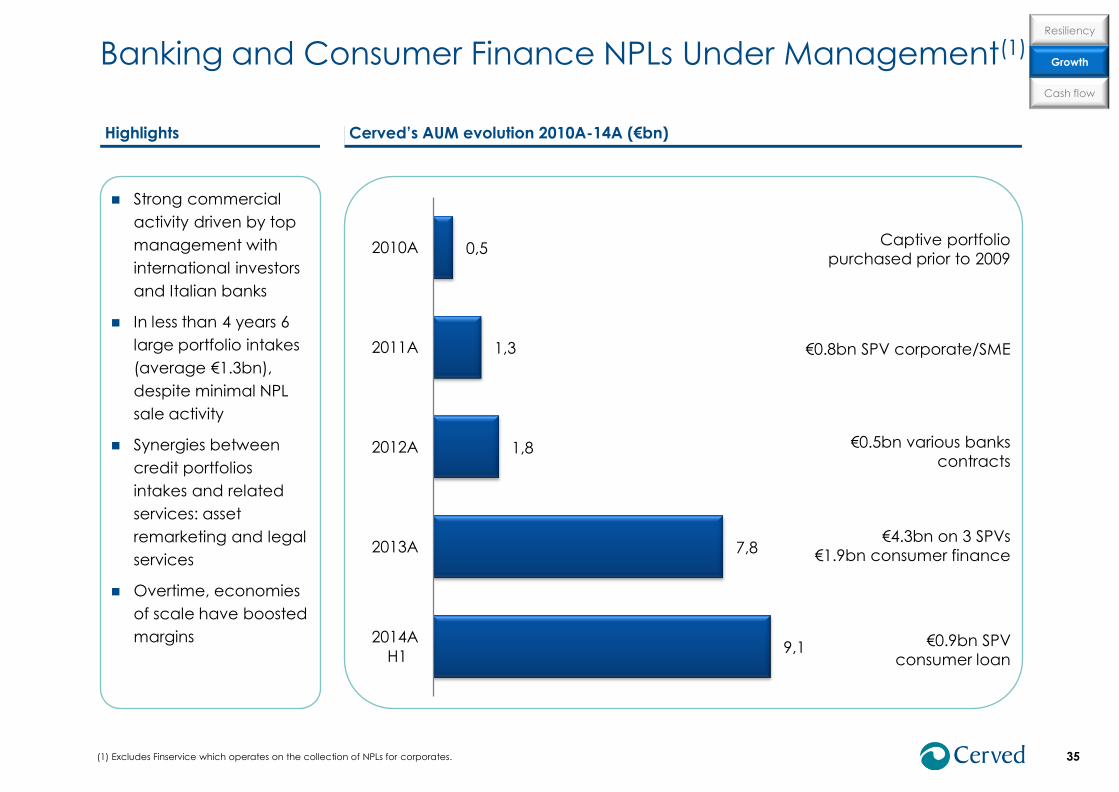

35

Highlights

Strong commercial

activity driven by top

management with

international investors

and Italian banks

In less than 4 years 6

large portfolio intakes

(average €1.3bn),

despite minimal NPL

sale activity

Synergies between

credit portfolios

intakes and related

services: asset

remarketing and legal

services

Overtime, economies

of scale have boosted

margins 9,1

7,8

1,8

1,3

0,5

2014A

H1

2013A

2012A

2011A

2010A Captive portfolio

purchased prior to 2009

€0.8bn SPV corporate/SME

€0.5bn various banks

contracts

€4.3bn on 3 SPVs

€1.9bn consumer finance

€0.9bn SPV

consumer loan

Cerved’s AUM evolution 2010A-14A (€bn)

Banking and Consumer Finance NPLs Under Management(1) Resiliency

Cash flow

Growth

(1) Excludes Finservice which operates on the collection of NPLs for corporates.

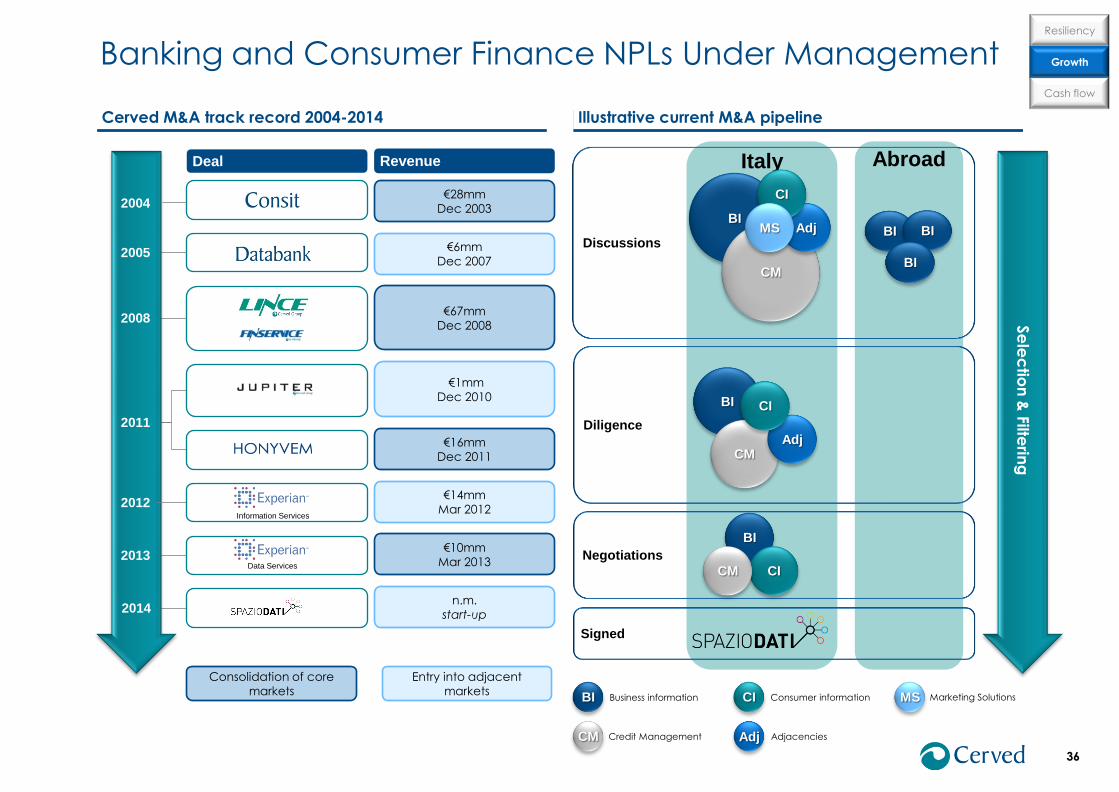

Consolidation of core

markets

36

Deal Revenue

€28mm

Dec 2003

€6mm

Dec 2007

€67mm

Dec 2008

€16mm

Dec 2011

€10mm

Mar 2013

n.m.

start-up

€1mm

Dec 2010

Data Services

Cerved M&A track record 2004-2014

2004

2005

2008

€14mm

Mar 2012 Information Services

2012

2011

2013

2014

Abroad Italy

Illustrative current M&A pipeline

Discussions

Diligence

Signed

Negotiations

BI

CM

BI

CM

BI

Adj

Adj

CI

CI

CI

MS

BI Business information CI Consumer information MS Marketing Solutions

CM Credit Management Adj Adjacencies

CM

Resiliency

Cash flow

Growth

BI BI

BI

Entry into adjacent

markets

Banking and Consumer Finance NPLs Under Management Se

lec

tion

& F

ilterin

g

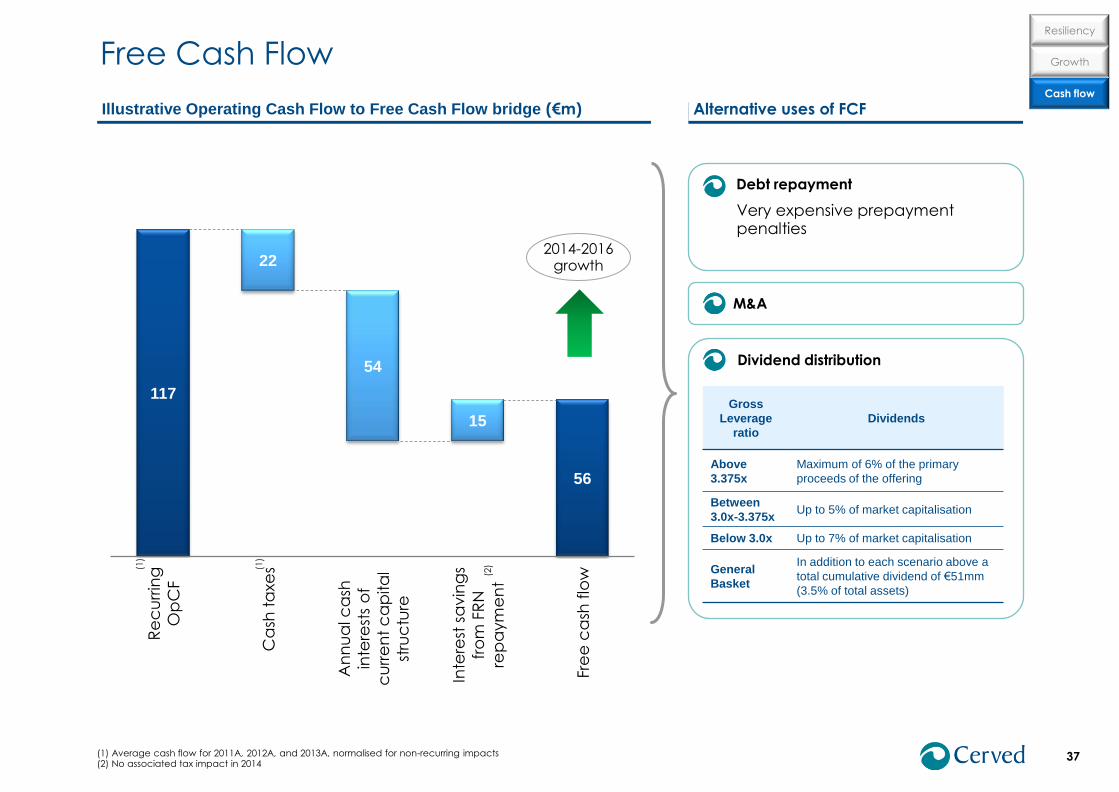

Free Cash Flow

Debt repayment

Very expensive prepayment penalties

Dividend distribution

37

Illustrative Operating Cash Flow to Free Cash Flow bridge (€m)

117

56

22

54

15

Re

cu

rrin

g

Op

CF

Ca

sh t

axe

s

An

nu

al c

ash

inte

rest

s o

f

cu

rre

nt

ca

pita

l

stru

ctu

re

Inte

rest

sa

vin

gs

fro

m F

RN

rep

aym

en

t

Fre

e c

ash

flo

w

Alternative uses of FCF

2014-2016 growth

Gross

Leverage

ratio

Dividends

Above

3.375x

Maximum of 6% of the primary

proceeds of the offering

Between

3.0x-3.375x Up to 5% of market capitalisation

Below 3.0x Up to 7% of market capitalisation

General

Basket

In addition to each scenario above a

total cumulative dividend of €51mm

(3.5% of total assets)

(1) Average cash flow for 2011A, 2012A, and 2013A, normalised for non-recurring impacts (2) No associated tax impact in 2014

(1)

(1)

M&A

(2)

Resiliency

Cash flow

Growth

Table of Contents

38

Investment Case 3

Overview 1

Appendices 4

Current Trading 2

Basis for Financial Information

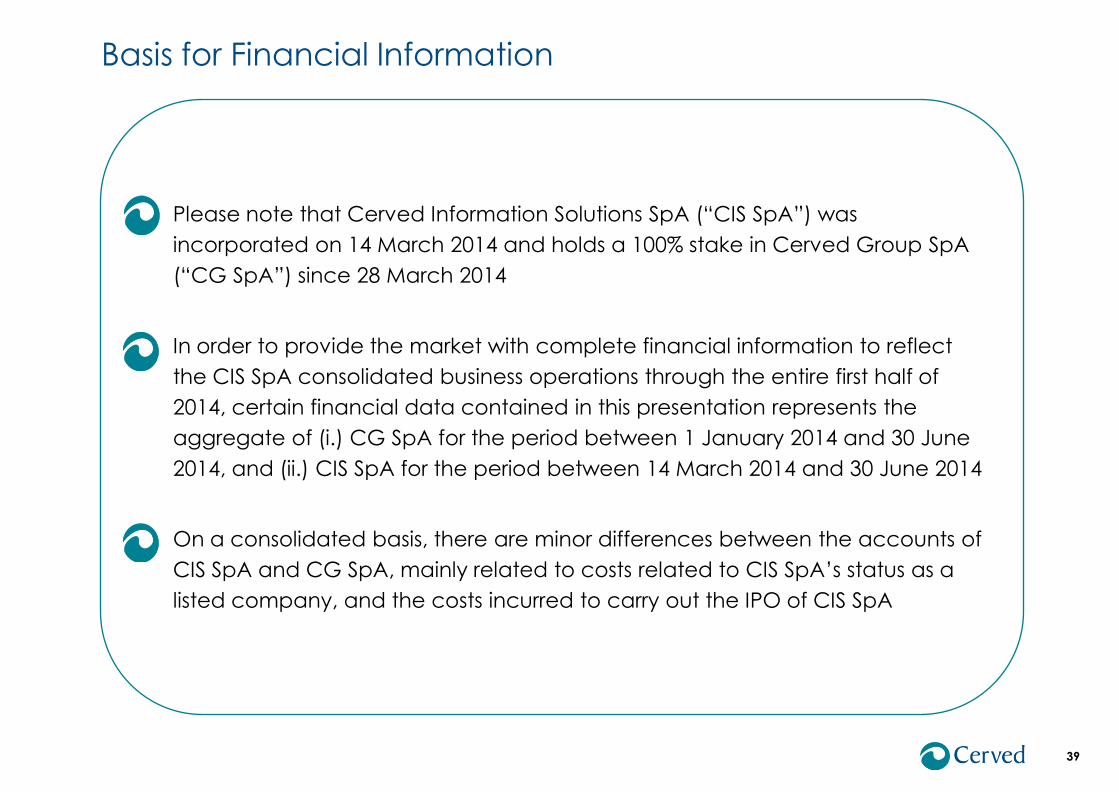

39

Please note that Cerved Information Solutions SpA (“CIS SpA”) was

incorporated on 14 March 2014 and holds a 100% stake in Cerved Group SpA

(“CG SpA”) since 28 March 2014

In order to provide the market with complete financial information to reflect

the CIS SpA consolidated business operations through the entire first half of

2014, certain financial data contained in this presentation represents the

aggregate of (i.) CG SpA for the period between 1 January 2014 and 30 June

2014, and (ii.) CIS SpA for the period between 14 March 2014 and 30 June 2014

On a consolidated basis, there are minor differences between the accounts of

CIS SpA and CG SpA, mainly related to costs related to CIS SpA’s status as a

listed company, and the costs incurred to carry out the IPO of CIS SpA

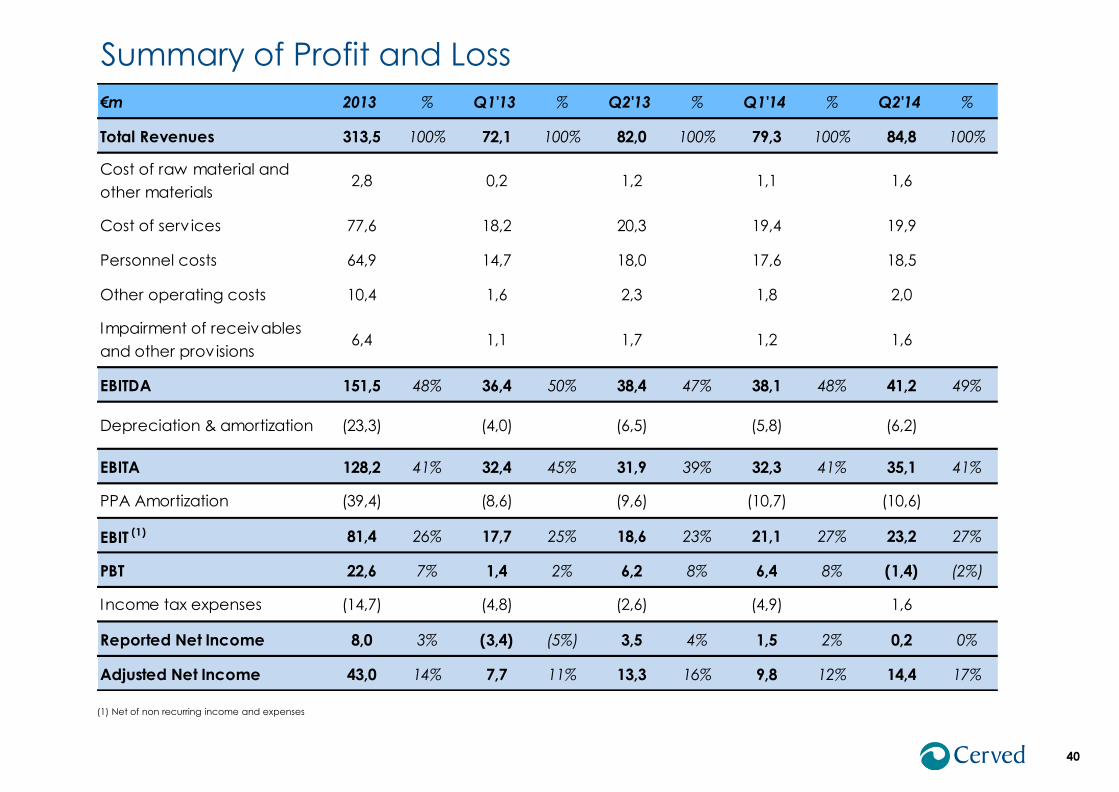

Summary of Profit and Loss

40

€m 2013 % Q1'13 % Q2'13 % Q1'14 % Q2'14 %

Total Revenues 313,5 100% 72,1 100% 82,0 100% 79,3 100% 84,8 100%

Cost of raw material and

other materials2,8 0,2 1,2 1,1 1,6

Cost of serv ices 77,6 18,2 20,3 19,4 19,9

Personnel costs 64,9 14,7 18,0 17,6 18,5

Other operating costs 10,4 1,6 2,3 1,8 2,0

Impairment of receivables

and other provisions6,4 1,1 1,7 1,2 1,6

EBITDA 151,5 48% 36,4 50% 38,4 47% 38,1 48% 41,2 49%

Depreciation & amortization (23,3) (4,0) (6,5) (5,8) (6,2)

EBITA 128,2 41% 32,4 45% 31,9 39% 32,3 41% 35,1 41%

PPA Amortization (39,4) (8,6) (9,6) (10,7) (10,6)

EBIT (1) 81,4 26% 17,7 25% 18,6 23% 21,1 27% 23,2 27%

PBT 22,6 7% 1,4 2% 6,2 8% 6,4 8% (1,4) (2%)

Income tax expenses (14,7) (4,8) (2,6) (4,9) 1,6

Reported Net Income 8,0 3% (3,4) (5%) 3,5 4% 1,5 2% 0,2 0%

Adjusted Net Income 43,0 14% 7,7 11% 13,3 16% 9,8 12% 14,4 17%

(1) Net of non recurring income and expenses

41

Source: Company Information (2011 and 2012 restated financials; 2013 aggregate financials) (1) Non cash item (2) Net of capitalized financing fees

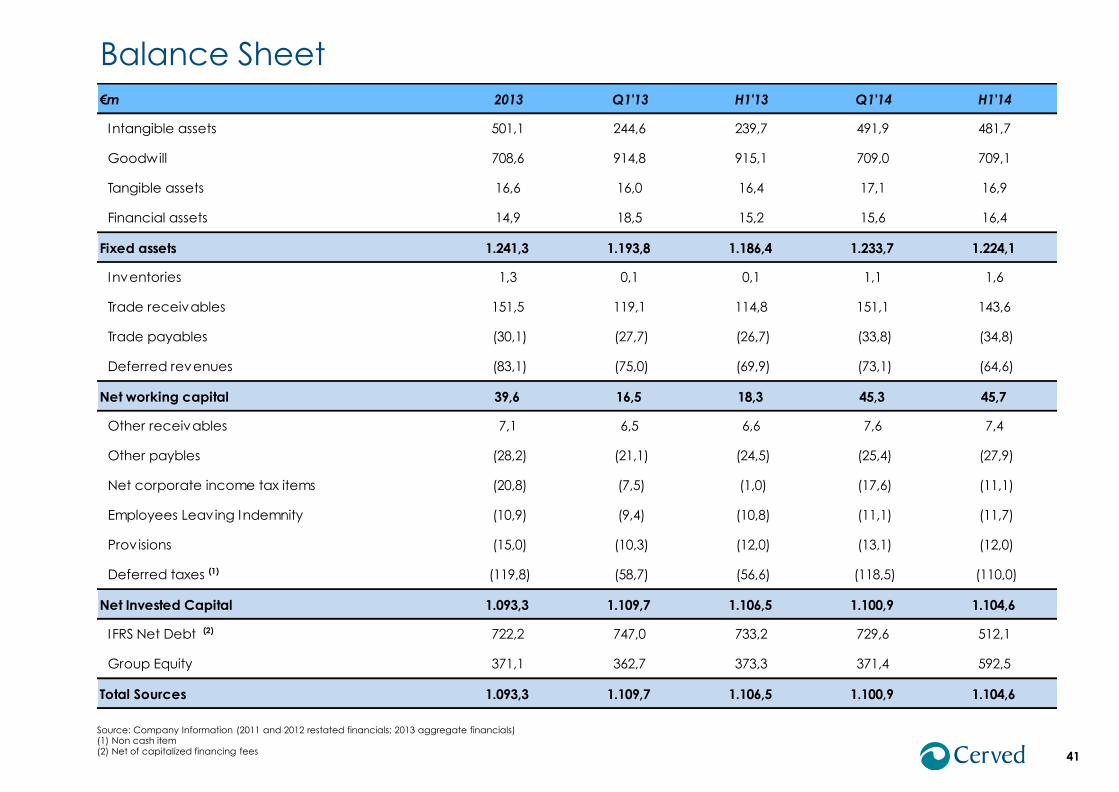

Balance Sheet

€m 2013 Q1'13 H1'13 Q1'14 H1'14

Intangible assets 501,1 244,6 239,7 491,9 481,7

Goodwill 708,6 914,8 915,1 709,0 709,1

Tangible assets 16,6 16,0 16,4 17,1 16,9

Financial assets 14,9 18,5 15,2 15,6 16,4

Fixed assets 1.241,3 1.193,8 1.186,4 1.233,7 1.224,1

Inventories 1,3 0,1 0,1 1,1 1,6

Trade receivables 151,5 119,1 114,8 151,1 143,6

Trade payables (30,1) (27,7) (26,7) (33,8) (34,8)

Deferred revenues (83,1) (75,0) (69,9) (73,1) (64,6)

Net working capital 39,6 16,5 18,3 45,3 45,7

Other receivables 7,1 6,5 6,6 7,6 7,4

Other paybles (28,2) (21,1) (24,5) (25,4) (27,9)

Net corporate income tax items (20,8) (7,5) (1,0) (17,6) (11,1)

Employees Leaving Indemnity (10,9) (9,4) (10,8) (11,1) (11,7)

Provisions (15,0) (10,3) (12,0) (13,1) (12,0)

Deferred taxes (1) (119,8) (58,7) (56,6) (118,5) (110,0)

Net Invested Capital 1.093,3 1.109,7 1.106,5 1.100,9 1.104,6

IFRS Net Debt (2) 722,2 747,0 733,2 729,6 512,1

Group Equity 371,1 362,7 373,3 371,4 592,5

Total Sources 1.093,3 1.109,7 1.106,5 1.100,9 1.104,6

42

(1) (1) Cash change in Net Working Capital exludes non recurring items, eg Trade Payables related to IPO transaction fees (2) (2) Includes cash contributed by acquired companies

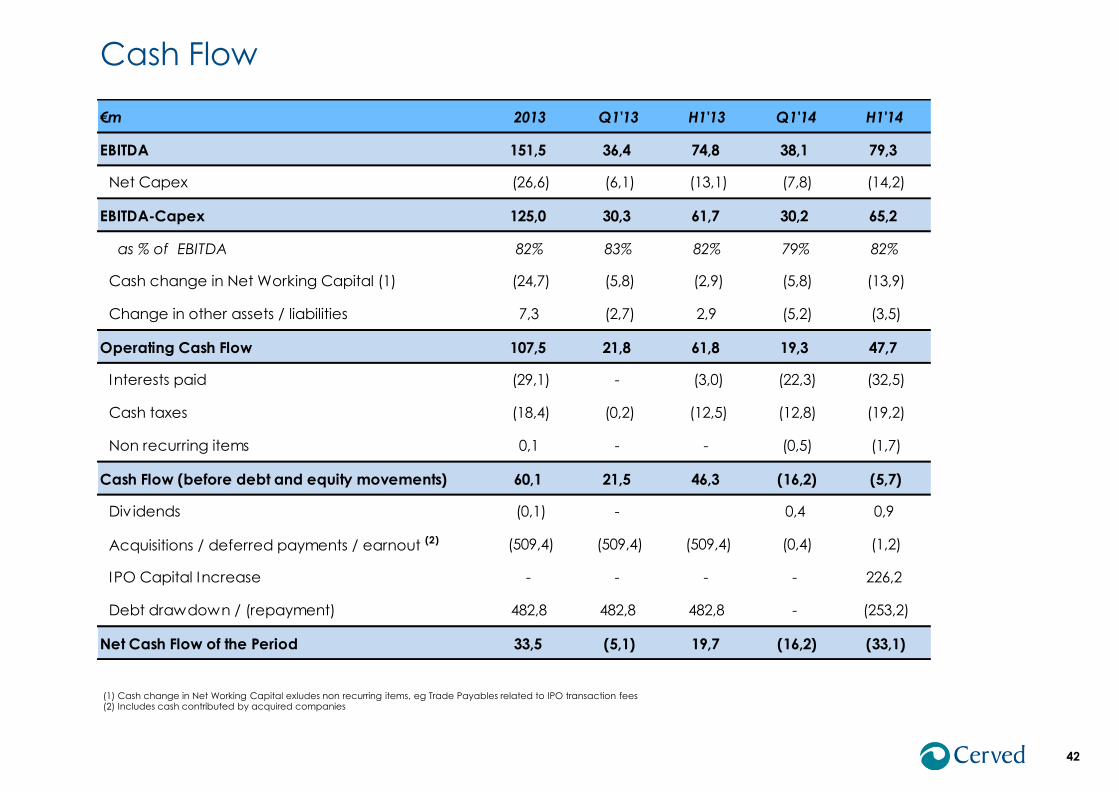

Cash Flow

€m 2013 Q1'13 H1'13 Q1'14 H1'14

EBITDA 151,5 36,4 74,8 38,1 79,3

Net Capex (26,6) (6,1) (13,1) (7,8) (14,2)

EBITDA-Capex 125,0 30,3 61,7 30,2 65,2

as % of EBITDA 82% 83% 82% 79% 82%

Cash change in Net Working Capital (1) (24,7) (5,8) (2,9) (5,8) (13,9)

Change in other assets / liabilities 7,3 (2,7) 2,9 (5,2) (3,5)

Operating Cash Flow 107,5 21,8 61,8 19,3 47,7

Interests paid (29,1) - (3,0) (22,3) (32,5)

Cash taxes (18,4) (0,2) (12,5) (12,8) (19,2)

Non recurring items 0,1 - - (0,5) (1,7)

Cash Flow (before debt and equity movements) 60,1 21,5 46,3 (16,2) (5,7)

Div idends (0,1) - 0,4 0,9

Acquisitions / deferred payments / earnout (2) (509,4) (509,4) (509,4) (0,4) (1,2)

IPO Capital Increase - - - - 226,2

Debt drawdown / (repayment) 482,8 482,8 482,8 - (253,2)

Net Cash Flow of the Period 33,5 (5,1) 19,7 (16,2) (33,1)