investor day - nexans.com · the current strategic plan, ... this should allow for external growth...

TRANSCRIPT

NexansInvestor DayDecember 13, 2017

Disclaimer

Paced For Growth 2018-20222

The current strategic plan, the current 2017 outlook, and all initiatives mentioned withinthis document are based on assumptions and hypothetical scenarios. Theseassumptions and scenarios are exposed to all risk factors described in the 2016Financial statements and Registration document of the Group. Moreover, certainprojects considered in the current strategic plan will be further analyzed prior to decidingtheir implementation, and when needed, those decisions will be submitted to relevantlegal bodies.

Executive summary

Paced For Growth 2018-20223

Meeting tomorrow’s challenges today

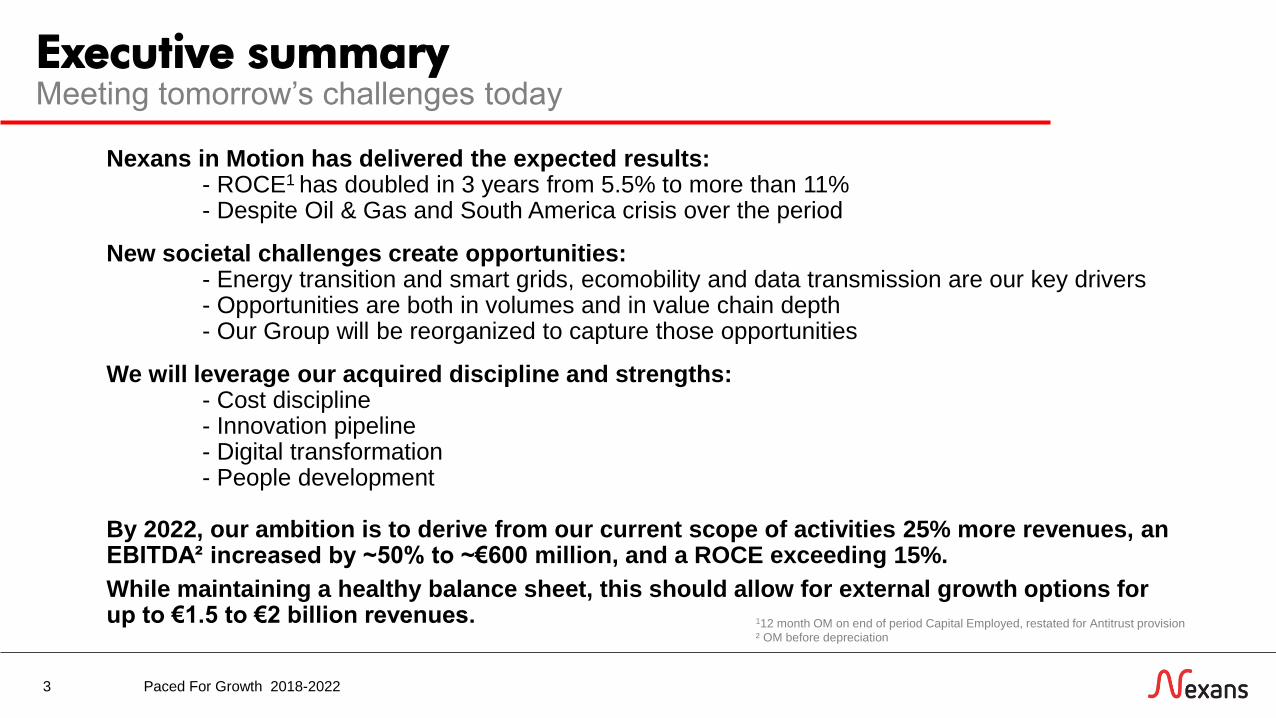

Nexans in Motion has delivered the expected results:- ROCE1 has doubled in 3 years from 5.5% to more than 11%- Despite Oil & Gas and South America crisis over the period

New societal challenges create opportunities:- Energy transition and smart grids, ecomobility and data transmission are our key drivers- Opportunities are both in volumes and in value chain depth- Our Group will be reorganized to capture those opportunities

We will leverage our acquired discipline and strengths:- Cost discipline- Innovation pipeline- Digital transformation- People development

By 2022, our ambition is to derive from our current scope of activities 25% more revenues, an EBITDA² increased by ~50% to ~€600 million, and a ROCE exceeding 15%.

While maintaining a healthy balance sheet, this should allow for external growth options for up to €1.5 to €2 billion revenues. 112 month OM on end of period Capital Employed, restated for Antitrust provision

² OM before depreciation

Agenda

4

Enablers & Actions

Ambition 2022

FinancialsBusiness Ambitions

Intro Conclusion

Paced for Growth 1. Building & Territories

2. High Voltage & Projects

3. Telecom & Data

4. Industry & Solutions

5. Beyond cables

1. Innovation, Digital & Sales

2. Costs competitiveness & Operational efficiency

3. Organization & People

1. Purpose

2. Nexans in Motion: Key learnings

3. Vision

Paced For Growth 2018-2022

Intro

5

1 Purpose

2 Nexans in Motion 2015-2017

3 Vision

Paced For Growth 2018-2022

By bringing energy and information to life, we are the critical link

6

OUR EXPERTISE

Cable maker

Producing cables, we are the material

link at the heart of industry with

high performance characteristics

developed through constant

innovation for over 120 years.

OUR MISSION

Beyond cables

Our systems deliver energy & data,

building the essential link that

transports information & power

everywhere to everyone.

OUR PURPOSE

Life link

Our purpose is to support

development, social contacts through

essential links. Without us, there can

be no communities, exchanges,

communications, energy,

modern life.

Paced For Growth 2018-2022

STANDARD SALES1

(€M)

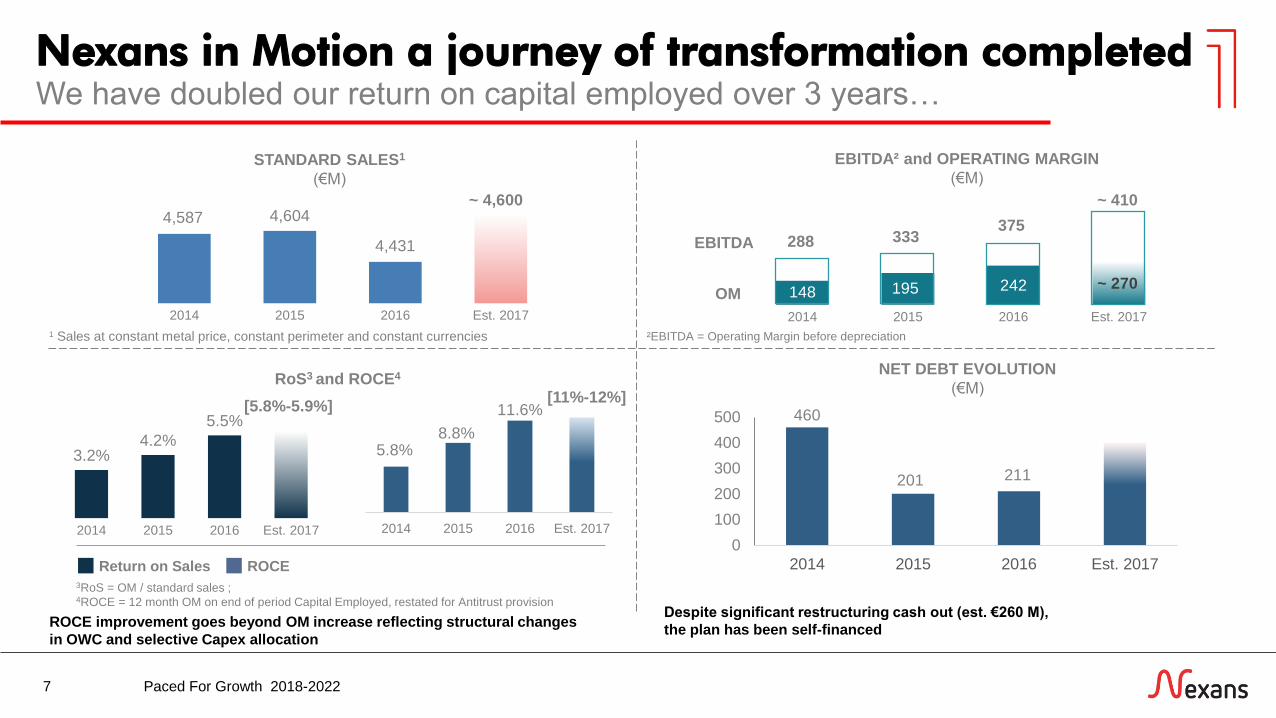

Nexans in Motion a journey of transformation completed

7

We have doubled our return on capital employed over 3 years…

RoS3 and ROCE4

~ 4,600

[5.8%-5.9%][11%-12%]

148 195 242

2014 2015 2016 Est. 2017

3RoS = OM / standard sales ; 4ROCE = 12 month OM on end of period Capital Employed, restated for Antitrust provision

3.2%4.2%

5.5%

2014 2015 2016 Est. 2017

Despite significant restructuring cash out (est. €260 M),

the plan has been self-financed

NET DEBT EVOLUTION

(€M)

Return on Sales ROCE

EBITDA² and OPERATING MARGIN

(€M)

EBITDA375

~ 410

333288

~ 270OM

ROCE improvement goes beyond OM increase reflecting structural changes

in OWC and selective Capex allocation

460

201 211

0

100

200

300

400

500

2014 2015 2016 Est. 2017

1 Sales at constant metal price, constant perimeter and constant currencies

5.8%8.8%

11.6%

2014 2015 2016 Est. 2017

4,587 4,604

4,431

2014 2015 2016 Est. 2017

²EBITDA = Operating Margin before depreciation

Paced For Growth 2018-2022

CO

RE

CH

AN

GE

S

Delivering on turnaround

8

…offsetting price cost squeeze through transformation focus

2014 2017

Rationalized footprint:

– Turnaround Europe:

industrial cables’

rationalization

– Optimization of footprint in

China and Australia

– Portfolio adjustments:

Sell: Argentina, Russia;

Closed: Elm City

Support functions

Europe (SHAPE):

– Footprint optimization

in Utilities

– Reduction of indirect

costs in plants

– Redesign of support

functions: e.g. finance,

purchasing, IS, HR

Product Customer

Optimization initiatives

(SHIFT):

– SHIFT in Europe

– Product Customer

Optimization across

multiple geographies:

MERA, SAM, NAM

Innovation:

– Expansion of production

capabilities in HV, incl. MI

capacity (Halden) and

XLPE developments

– Cable dynamic designs for

floating wind turbines

– Improved safety with

Fire retardant cables

▪ Significant impact of the O&G and mining crises, with est. €50 M operating margin toll from 2014 to 2017, mostly outside of Europe

▪ Adverse events in South America

In a challenging environment:

▪ Significant Price Cost Squeeze impact of est. €75 M p.a.

EN

VIR

ON

ME

NT

Paced For Growth 2018-2022

The world is changing

9

Megatrends are creating new business opportunities…

Innovation acceleration

Evolving consumption

New governance model

Resource constraintsEconomic globalization

Bu

sin

es

s O

pp

ort

un

itie

sfo

r N

ex

an

s

Speed of Change

Energyrevolution

Urbanization &densification

Smart devices &infrastructures

Rise of digital

disruptors

Life sciences

booming

Health and

Wellness

Homing

War for

talents

IndustrySelective

deindustrializationPublic debt

crisis

Anxiety

Natural

disasters

Ageing

society

Low cost/Premiumpolarization

Changing balance of economic power

Rise of Asian & African

middleclass

Growing

world

populatio

n

Digital & Data

Usageeconomy

Globalmobility

Operations

Cable and connectivity production

Evolution of the Energy &

Data Management market€BN, 2015-2030

2020 2025 20302015

System ManagementAsset Management

Cable Services

+9.2%

+2.8%

+4.1%

+3.9%

+3.9%

CAGR

2015-2030

Ecosystem atrisk

Gender gap decreaseNew social network

Autonomous vehicles

Scarcity of natural

ressources

5.6

0

Paced For Growth 2018-2022

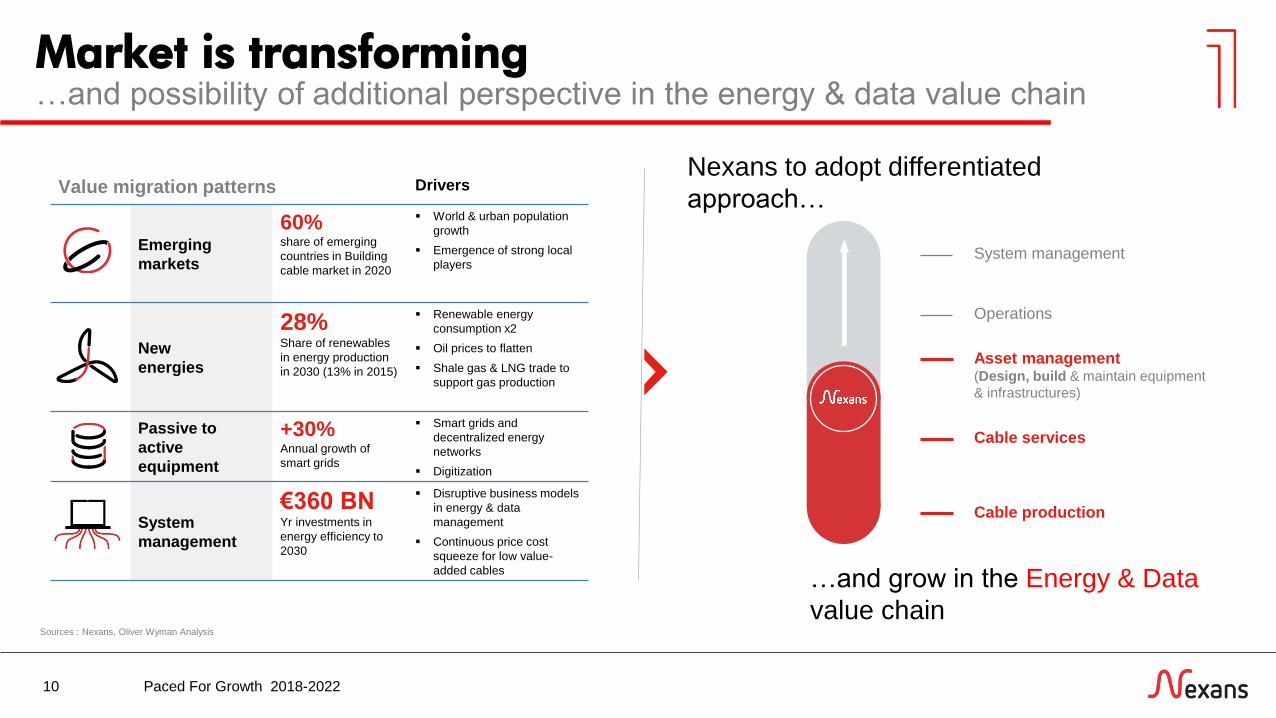

Market is transforming

10

…and possibility of additional perspective in the energy & data value chain

Sources : Nexans, Oliver Wyman Analysis

Value migration patterns Drivers

Emerging

markets

60%share of emerging

countries in Building

cable market in 2020

World & urban population

growth

Emergence of strong local

players

New

energies

28%Share of renewables

in energy production

in 2030 (13% in 2015)

Renewable energy

consumption x2

Oil prices to flatten

Shale gas & LNG trade to

support gas production

Passive to

active

equipment

+30%Annual growth of

smart grids

Smart grids and

decentralized energy

networks

Digitization

System

management

€360 BNYr investments in

energy efficiency to

2030

Disruptive business models

in energy & data

management

Continuous price cost

squeeze for low value-

added cables…and grow in the Energy & Data

value chain

Nexans to adopt differentiated

approach…

Cable production

Cable services

Asset management(Design, build & maintain equipment

& infrastructures)

Operations

System management

Paced For Growth 2018-2022

Aligning Nexans with customers

11

Capturing market opportunities implies a new business structure

Building & TerritoriesProvide reliable cabling and

smarter energy solutions to

support buildings and territories

to become more efficient,

livable and sustainable

High Voltage & ProjectsSupport customers from the

beginning (design, engineering,

funding, asset management) to

the end (system management)

in finding the right cable system

solution to address their

efficiency and reliability

challenges

Telecom & DataHelp customers to easily

deploy optical fiber

infrastructure with “plug-and-

play” cable, connectivity and

solutions

Industry & SolutionsSupport OEMs and industrial

infrastructure projects in

customizing their cabling &

connectivity solutions

addressing their electrification,

digitalization and automation

challenges

Paced For Growth 2018-2022

Paced for GrowthAmbition 2022

12 Paced For Growth 2018-2022

”

>15% ROCE3

Inorganic growth

up to

€1.5 - 2 BNsupporting

megatrends

Nexans Paced for Growth

13

We are opening a period of profitable growth…

Become leader in

advanced cabling and

connectivity solutions,

committed to support its

partners in smart energy

transition, exploding data

transmission and mobility

“ ~ €600 MEBITDA²

~10%

EBITDA/Sales¹

+ 5 % Organic Growth

Nexans revenues¹

up to €6 BN by

2022

> 60% Revenues in HV,

Industry &

Telecom

1 Sales at constant metal price, constant perimeter and constant currencies

² Operating margin before depreciation3 12 month OM on end of period Capital Employed, restated for Antitrust provision

Ambitions by 2022 based on current scope Allowing for external

growth options

Paced For Growth 2018-2022

Paced for Growth: Driving shareholder value

14

…supported by a three axis strategy…

Focus investments on selected

areas with high returns and

promising business prospects.

For mature businesses, focus

on efficiency and lean efforts

to drive competitiveness,

from production to support

areas to erase price cost

squeeze

Develop new offers in the

solution space and accelerate

M&A

Continue to focus on cost

leadership

Build on strengths in

attractive markets

Accelerate growth through portfolio

of activities

C

A B

while respecting all stakeholders and CSR engagements

Paced For Growth 2018-2022

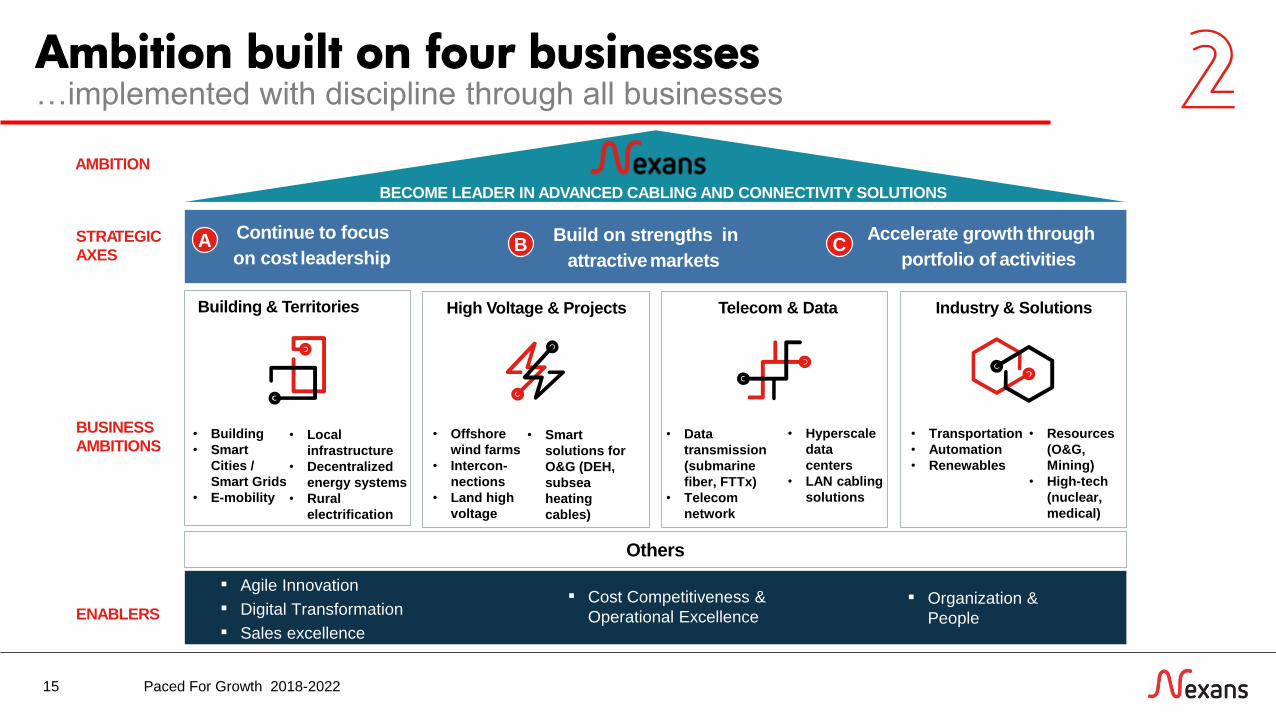

Ambition built on four businesses

15

…implemented with discipline through all businesses

▪ Innovation▪ Organization &

Agility

▪ Digital

Technology

Continue to focus

on cost leadership

Build on strengths in

attractivemarkets

Accelerate growth through

portfolio of activities

STRATEGIC AXES

BECOME LEADER IN ADVANCED CABLING AND CONNECTIVITY SOLUTIONS

BUSINESS AMBITIONS

ENABLERS

Others

AMBITION

Building & Territories

CA B

▪ Organization &

People

▪ Cost Competitiveness &

Operational Excellence

▪ Agile Innovation

▪ Digital Transformation

▪ Sales excellence

High Voltage & Projects Telecom & Data Industry & Solutions

• Local

infrastructure

• Decentralized

energy systems

• Rural

electrification

• Building

• Smart

Cities /

Smart Grids

• E-mobility

• Offshore

wind farms

• Intercon-

nections

• Land high

voltage

• Smart

solutions for

O&G (DEH,

subsea

heating

cables)

• Data

transmission

(submarine

fiber, FTTx)

• Telecom

network

• Hyperscale

data

centers

• LAN cabling

solutions

• Transportation

• Automation

• Renewables

• Resources

(O&G,

Mining)

• High-tech

(nuclear,

medical)

Paced For Growth 2018-2022

Business ambitions

16

1 Building & Territories

2 High Voltage & Projects

3 Telecom & Data

4 Industry & Solutions

5 Beyond cables

.

Paced For Growth 2018-2022

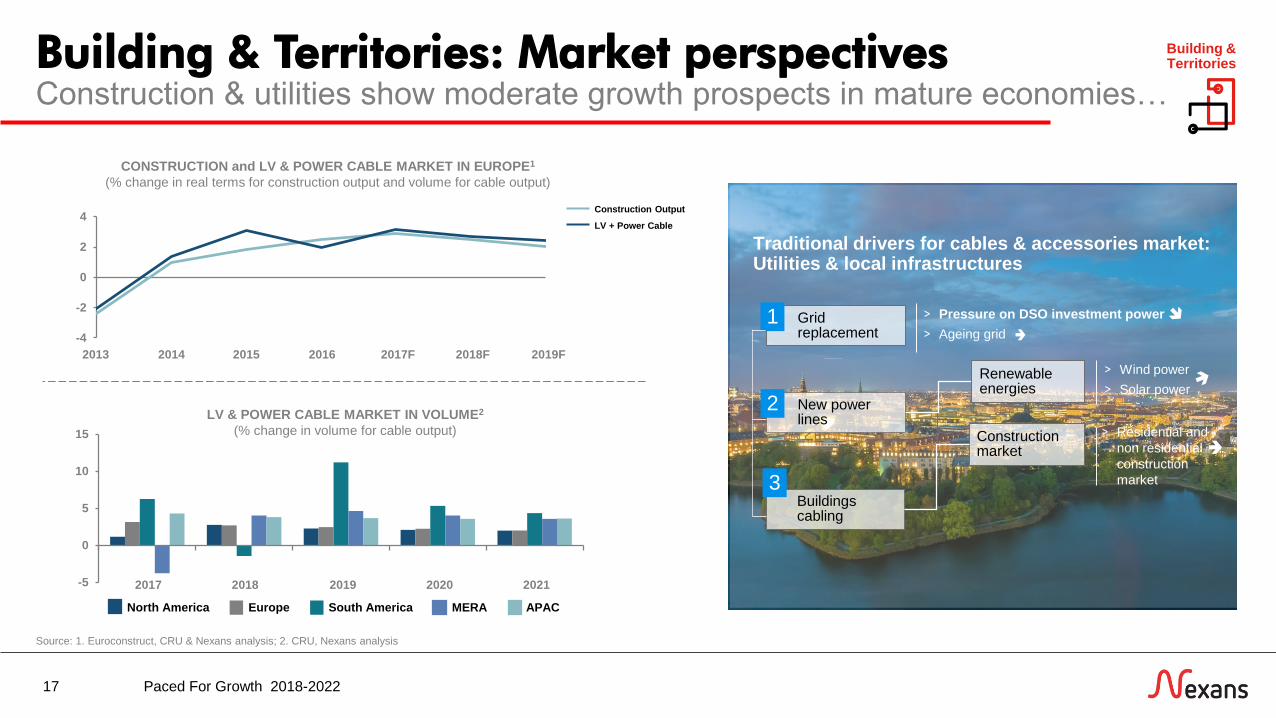

Building & Territories: Market perspectives

17

Construction & utilities show moderate growth prospects in mature economies…

Building & Territories

Source: 1. Euroconstruct, CRU & Nexans analysis; 2. CRU, Nexans analysis

-4

-2

0

2

4

20162015 2018F20142013 2019F2017F

Construction Output

LV + Power Cable

CONSTRUCTION and LV & POWER CABLE MARKET IN EUROPE1

(% change in real terms for construction output and volume for cable output)

LV & POWER CABLE MARKET IN VOLUME2

(% change in volume for cable output)

-5

0

5

10

15

20212017 20192018 2020

APACMERANorth America South AmericaEurope

Traditional drivers for cables & accessories market:Utilities & local infrastructures

New power lines

Grid replacement

1

2

> Pressure on DSO investment power

> Ageing grid

Construction market

Renewable energies

> Wind power

> Solar power

> Residential and

non residential

construction

market

Buildings cabling

3

Paced For Growth 2018-2022

Growth will come from new markets

18

…but future challenges are creating new opportunities

Building & Territories

Sources: 1.World Energy Investment Outlook, IEA, 2016; 2. TechNavio Analysis; 3. Bloomberg New Energy Finance

9630

70

382

118

278

APAC EMEA AM

GLOBAL IOT MARKET BY GEO2

$BN, 2014 vs. 2019

20192014

629

11232

234 268

APAC MERA SAM NAM Europe

PV SOLAR INVESTMENT BY GEO1

$BN, 2014-2035

Shift in city infrastructure

and smart buildings

CUMULATIVE NUMBER OF

PUBLIC EV CHARGING POINTS3

Thousand units installed, 2011-2016

28

98137 151

225

363

2011 2012 2013 2014 2015 2016

Changing topology of the

Grid MV and LV networksBooming integration of e-mobility

in the local infrastructures

Source: Oliver Wyman Analysis Source: CENEX

Decentralized

power generation

Source: Nexans, desk research, Roland Berger

Paced For Growth 2018-2022

Continue to focus on cost

leadership

Build on strengths in

attractive markets

Accelerate growth through portfolio

of activities

C

A B

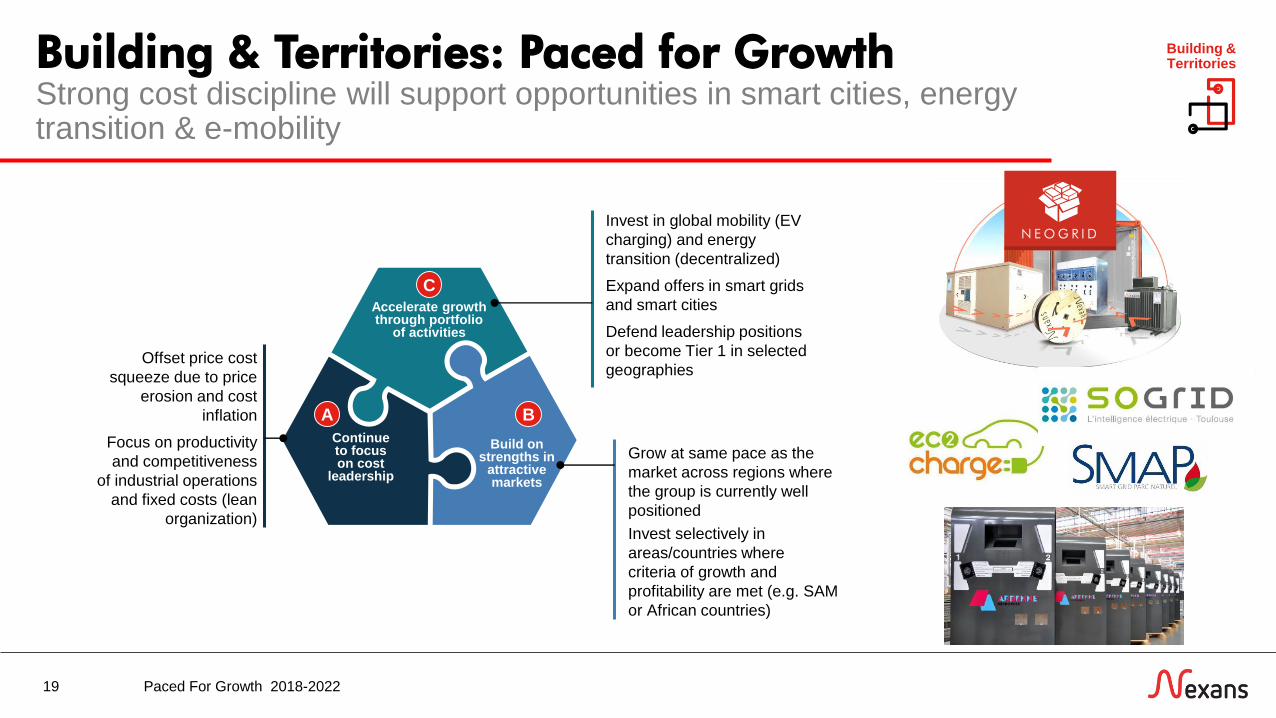

Building & Territories: Paced for Growth

19

Strong cost discipline will support opportunities in smart cities, energy transition & e-mobility

Building & Territories

Grow at same pace as the

market across regions where

the group is currently well

positioned

Invest selectively in

areas/countries where

criteria of growth and

profitability are met (e.g. SAM

or African countries)

Offset price cost

squeeze due to price

erosion and cost

inflation

Focus on productivity

and competitiveness

of industrial operations

and fixed costs (lean

organization)

Invest in global mobility (EV

charging) and energy

transition (decentralized)

Expand offers in smart grids

and smart cities

Defend leadership positions

or become Tier 1 in selected

geographies 17%

N EOG R I D

Paced For Growth 2018-2022

Building & Territories: Key Financials

20

Leaner operations & market leadership will drive performance

Building & Territories

1 Sales at constant metal price, constant perimeter and constant currencies

² 12 month OM on end of period Capital Employed, restated for Antitrust provision3 OM before depreciation

• Nexans performs far better in countries where it holds tier 1 position

• Overall B&T performance will be improved with targeted actions in

competitiveness, leaner operations and increased market leadership

(pricing, differentiation and logistics)

2017 Est.Ambition

2022

Sales (€BN) ~1.75 ~ 2.0

Ogranic growth (5 years CAGR) ~ 2.5%

EBITDA3 / Sales > 7% ~ 9.5%

CAPEX / Depreciation 100% 100%

Key Figures1

Key Performance levers

0

ROCE²

Sa

les / C

E

RoS0

Un

de

rperf

orm

ers

Tra

din

g

Market leaders

0A

Focus on Cost

leadership

B

Build on

strengths in

attractive

markets

C

Accelerate

growth through

portfolio of

activities

Price Cost

Squeeze

Impact +++ + + ---

Paced For Growth 2018-2022

Business ambitions

21

.

1 Building & Territories

2 High Voltage & Projects

3 Telecom & Data

4 Industry & Solutions

5 Beyond cables

Paced For Growth 2018-2022

High Voltage & Projects: Market perspectivesEnergy transition in Europe, NAM & APAC will drive growth…

22

High Voltage & Projects

Key macro-indicators and trends

GLOBAL MARKET SALES OF HV CABLES1

€BN, 2017-2022

17

26+9% p.a.

11%

8%

Submarine HV Land HV XX CAGR

2017 2022

Source: 1. McKinsey analysis; Technavio Industry report; 2. World Energy Investment Outlook, IEA, 2016; 3. Bloomberg New Energy Finance, 2017; 4. IEA 2017 World Energy Investment

OFFSHORE WIND INVESTMENTS2

$BN, 2014-2035

HVDC TRANSMISSION & INTERCONNECTOR

PROJECTS (by status and commissioning yr)3

KM, 2017-2022

Announced Permitted

2017 2018 2019 2020 2021 2022

3,237

13,917

5,5785,159

1,732

212

14 9

94

231

APAC MEA SAM NAM Europe

WORLD UPSTREAM O&G INVESTMENTS4

$BN, 2011-2017

Upstream O&G investment

Exploration % of total (right axis)

0

200

400

600

800

1000

10%

12%

14%

16%

18%

20%

2011 2012 2013 2014 2015 2016 2017

5,268

Paced For Growth 2018-2022

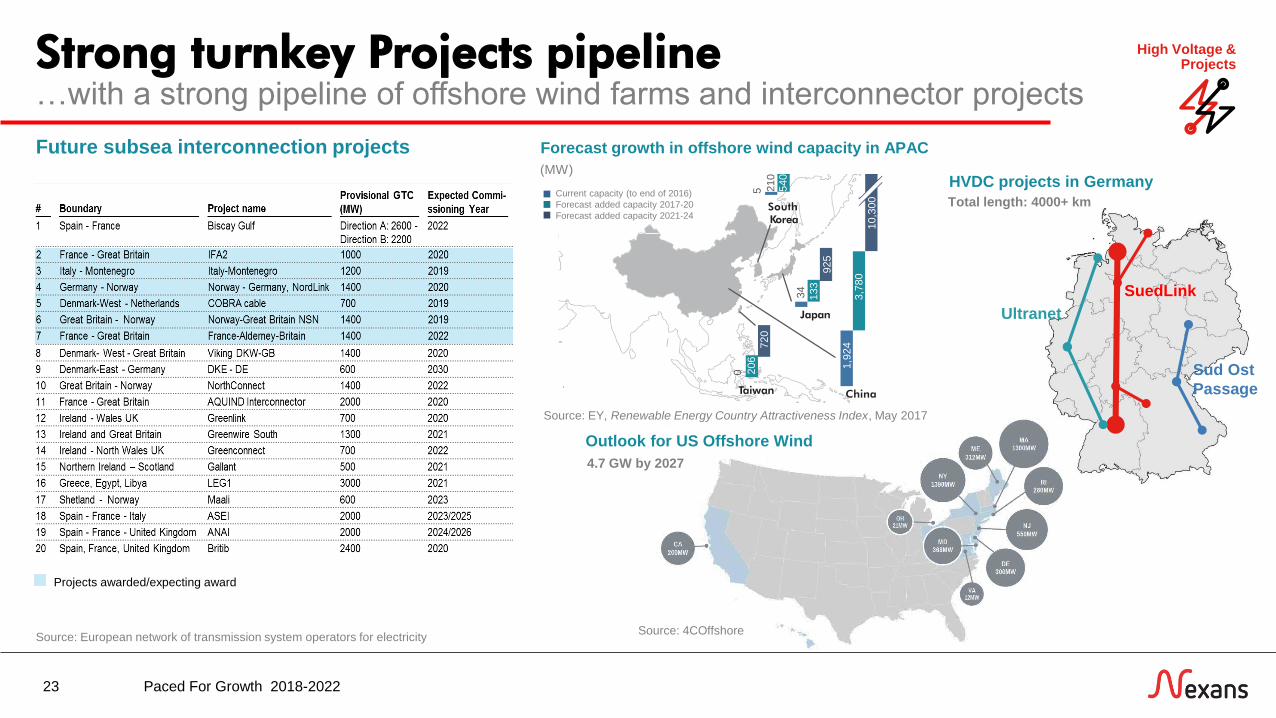

Strong turnkey Projects pipeline…with a strong pipeline of offshore wind farms and interconnector projects

23

SuedLink

Sud Ost

Passage

Ultranet

High Voltage & Projects

Future subsea interconnection projects

Projects awarded/expecting award

Total length: 4000+ km

HVDC projects in Germany

Source: European network of transmission system operators for electricity

4.7 GW by 2027

Outlook for US Offshore Wind

Source: 4COffshore

Forecast growth in offshore wind capacity in APAC

Taiwan

0

Japan

China

South Korea

Current capacity (to end of 2016)

Forecast added capacity 2017-20

Forecast added capacity 2021-24

206

720

210

5 540

34

133

925

1,9

24

3,7

80

10,3

00

(MW)

Source: EY, Renewable Energy Country Attractiveness Index, May 2017

Paced For Growth 2018-2022

Continue to focus on cost

leadership

Build on strengths in

attractive markets

Accelerate growth through portfolio

of activities

C

A B

24

High Voltage & Projects

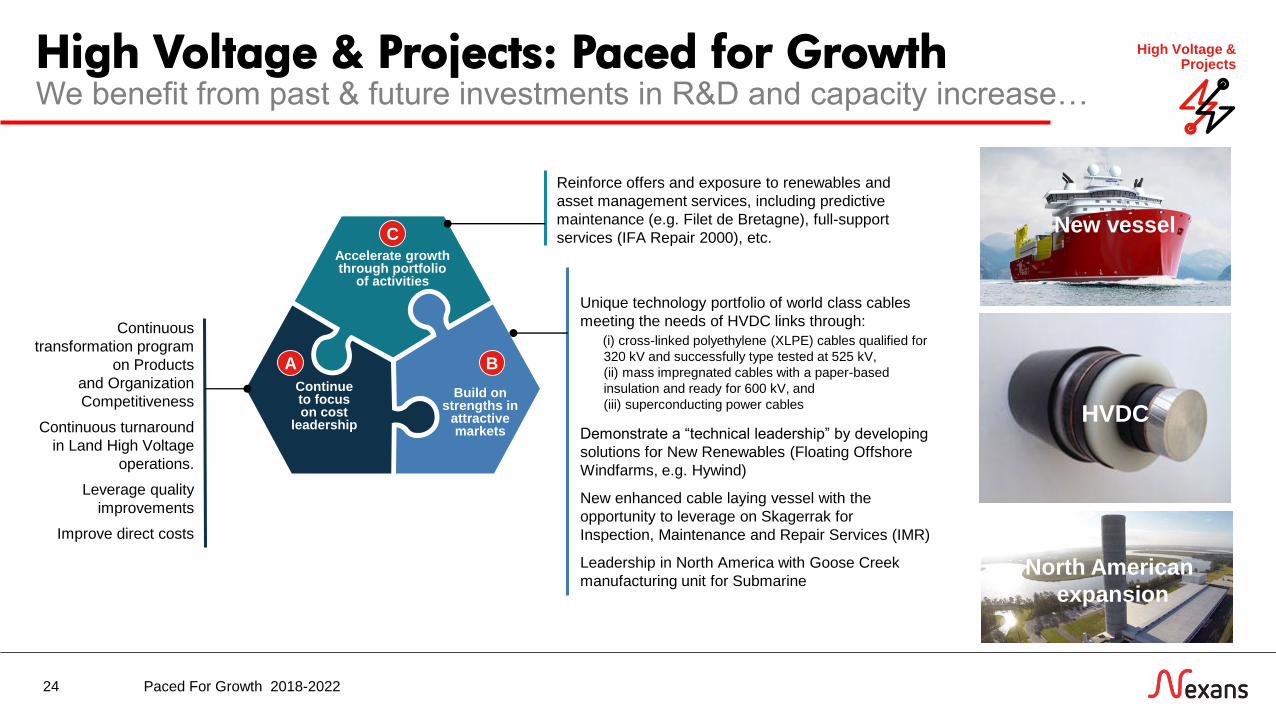

Unique technology portfolio of world class cables

meeting the needs of HVDC links through:

(i) cross-linked polyethylene (XLPE) cables qualified for

320 kV and successfully type tested at 525 kV,

(ii) mass impregnated cables with a paper-based

insulation and ready for 600 kV, and

(iii) superconducting power cables

Demonstrate a “technical leadership” by developing

solutions for New Renewables (Floating Offshore

Windfarms, e.g. Hywind)

New enhanced cable laying vessel with the

opportunity to leverage on Skagerrak for

Inspection, Maintenance and Repair Services (IMR)

Leadership in North America with Goose Creek

manufacturing unit for Submarine

Continuous

transformation program

on Products

and Organization

Competitiveness

Continuous turnaround

in Land High Voltage

operations.

Leverage quality

improvements

Improve direct costs

Reinforce offers and exposure to renewables and

asset management services, including predictive

maintenance (e.g. Filet de Bretagne), full-support

services (IFA Repair 2000), etc.

High Voltage & Projects: Paced for GrowthWe benefit from past & future investments in R&D and capacity increase…

New vessel

North American

expansion

HVDC

Paced For Growth 2018-2022

High Voltage & Projects: Key Financials

25

…leading to significant growth outlook

Sales of turnkey projects manufactured in Goose Creek (USA) to

start by 2020 and reach full sales potential by 2022 when

qualifications are completed

New cable laying vessel available for operations starting Q4 2020

Key Performance levers

Sales

202220212020201920182017

Other areas

NAM

A

Focus on Cost

leadership

B

Build on

strengths in

attractive

markets

C

Accelerate

growth through

portfolio of

activities

Price Cost

Squeeze

Impact + +++ + -

High Voltage & Projects

1 Sales at constant metal price, constant perimeter and constant currencies

² OM before depreciation

Key Figures1

2017 Est.Ambition

2022

Sales (€BN) ~ 0.9 ~ 1.3

Organic growth (5 years CAGR) ~ 8%

EBITDA² / Sales ~ 13% ~ 15%

CAPEX / Depreciation 160% 160%

Paced For Growth 2018-2022

Business ambitions

26

.

1 Building & Territories

2 High Voltage & Projects

3 Telecom & Data

4 Industry & Solutions

5 Beyond cables

Paced For Growth 2018-2022

Telecom & Data: Market perspectives

27

Telecom &Data

Telecom & data cabling infrastructure must meet expectations…

Source: CRU report – July 17 update; McKinsey analysis, BISRIA (March 2016), Discerning Analytics (May 2016)

Data centers having over 100,000 nodes

2016-2022 GLOBAL MARKET

INTERNAL TELECOM AND DATA CABLES,

€BN

2017 2022

Data CenterOther LAN

9.19.9

1.11.4

8.08.6

5%

1%

2016-2022 ZOOM ON DATA

CENTER SUB-MARKET,

€BN

2017 2022

Enterprise Large Hyperscale

1.1

1.4

15%

7%

-5%

2017-2022 GLOBAL MARKET

TELECOM AND DATA CABLES,

€BN

2017 2022

External Copper Telecom

Internal Telecom/Data

Fiber Optic

20.220.7

2.0 1.4

9.19.9

9.09.4

-7%

2%

1%

Paced For Growth 2018-2022

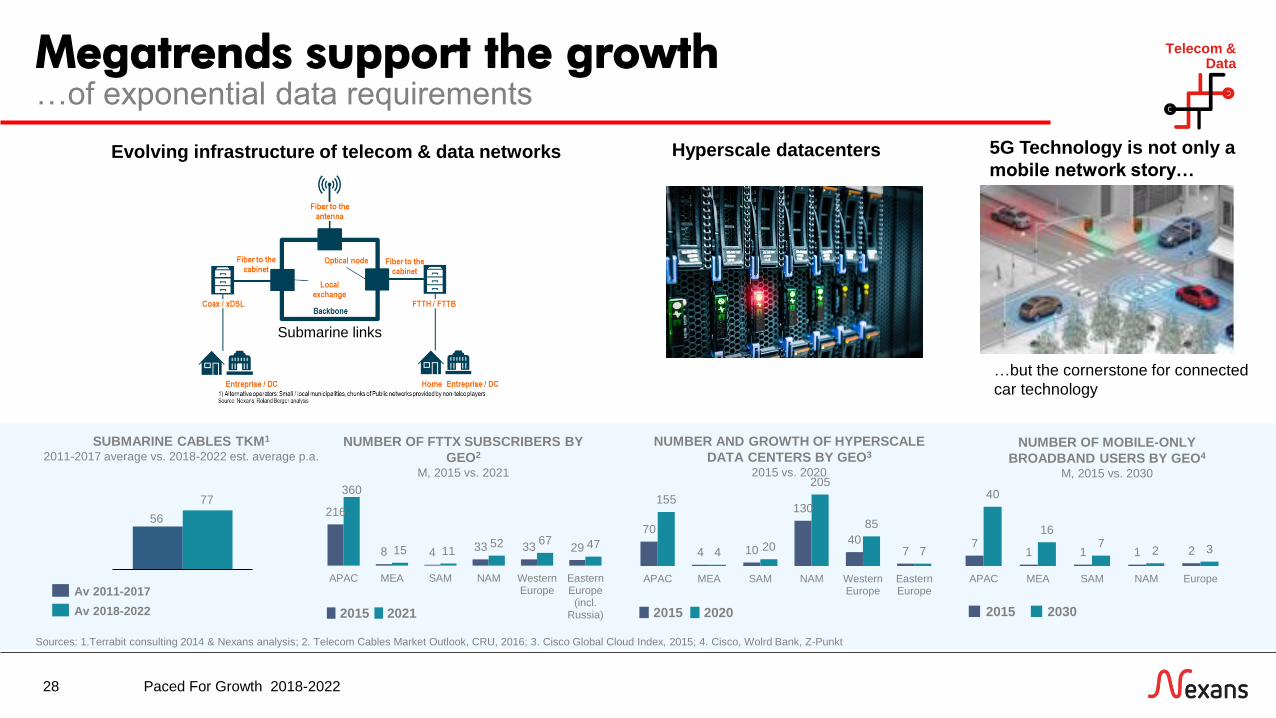

Megatrends support the growth Telecom &Data

…of exponential data requirements

Sources: 1.Terrabit consulting 2014 & Nexans analysis; 2. Telecom Cables Market Outlook, CRU, 2016; 3. Cisco Global Cloud Index, 2015; 4. Cisco, Wolrd Bank, Z-Punkt

SUBMARINE CABLES TKM1

2011-2017 average vs. 2018-2022 est. average p.a.

70

4 10

130

407

155

4 20

205

85

7

APAC MEA SAM NAM WesternEurope

EasternEurope

NUMBER AND GROWTH OF HYPERSCALE

DATA CENTERS BY GEO3

2015 vs. 2020

2015 2020

216

8 4 33 33 29

360

15 1152 67 47

APAC MEA SAM NAM WesternEurope

EasternEurope(incl.

Russia)

NUMBER OF FTTX SUBSCRIBERS BY

GEO2

M, 2015 vs. 2021

2015 2021

71 1 1 2

40

167

2 3

APAC MEA SAM NAM Europe

NUMBER OF MOBILE-ONLY

BROADBAND USERS BY GEO4

M, 2015 vs. 2030

2015 2030

…but the cornerstone for connected

car technology

5G Technology is not only a

mobile network story… Hyperscale datacenters

Submarine links

Evolving infrastructure of telecom & data networks

77

56

Av 2011-2017

Av 2018-2022

28 Paced For Growth 2018-2022

Telecom &Data

29

Match growing demand

through increased

production capacity

Develop “Ready-to-

install” cable &

connectivity solutions

and full turnkey solutions

for submarine fiber

installation

“Tailor approach” for

data centers: easy and

quick installation, cost-

efficiency and

optimization space

utilization

Maintain appropriate

fixed cost

productivity while

supporting growth

Create trust-based

partnerships to deploy

optical fiber networks

Increase share of

integrated systems and

connectivity solutions

Telecom & Data: Paced for GrowthNexans will double its presence in the market…

Continue to focus on cost

leadership

Build on strengths in

attractive markets

Accelerate growth through portfolio

of activities

C

A B

5G

FTTxHyperscale

Data Centers

Submarine

backbone

Paced For Growth 2018-2022

Telecom & DataTelecom & Data: Key Financials

30

…with a unique point to point connectivity offer

Key Performance levers

A

Focus on Cost

leadership

B

Build on

strengths in

attractive

markets

C

Accelerate

growth through

portfolio of

activities

Price Cost

Squeeze

Impact + +++ +++ -

All 3 sub-segments will contribute to organic growth

M&A needed to significantly accelerate Nexans’ exposure to

high growing telecom & data markets

Three Main Sub-segments

1 Sales at constant metal price, constant perimeter and constant currencies

² Approx. 100 M€ for CAPEX and OPEX 3 OM before depreciation

Telecom Operators

Special Telecom Subsea

LAN Cables & SystemsCAGR

5%

7%

12%

20222017

Key Figures1

2017 Est.Ambition

2022

Sales (€BN) ~ 0.5 ~ 0.8

Organic growth (5 years CAGR) ~ 10%

EBITDA3 / Sales ~ 12% ~ 15%

CAPEX / Depreciation 100% 110%²

Paced For Growth 2018-2022

Business ambitions

31

.

1 Building & Territories

2 High Voltage & Projects

3 Telecom & Data

4 Industry & Solutions

5 Beyond cables

Paced For Growth 2018-2022

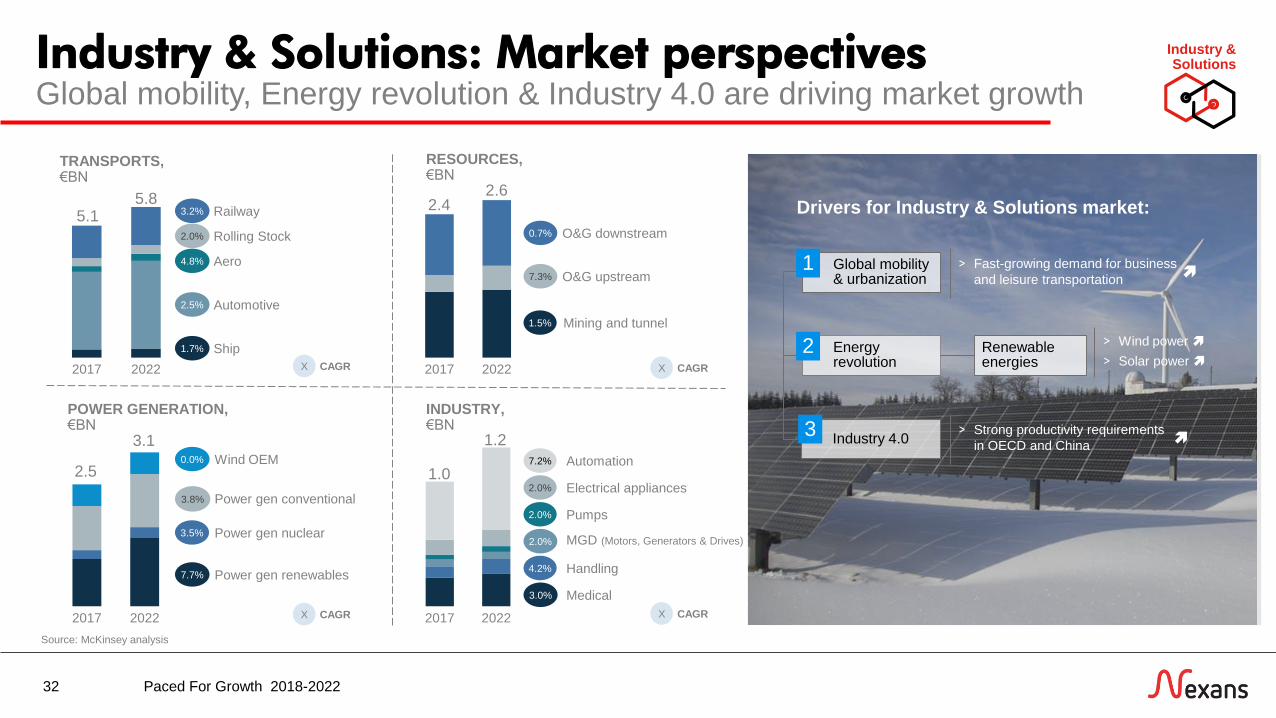

Industry & Solutions: Market perspectivesGlobal mobility, Energy revolution & Industry 4.0 are driving market growth

Industry &Solutions

Source: McKinsey analysis

32

Drivers for Industry & Solutions market:

> Fast-growing demand for business

and leisure transportation

Renewable energies

> Wind power

> Solar power

> Strong productivity requirements

in OECD and China

Global mobility & urbanization

1

Energy revolution

2

Industry 4.03

2017 2022

1.02.0%

2.0%

4.2%

2.0%

7.2% Automation

Electrical appliances

Pumps

MGD (Motors, Generators & Drives)

Handling

Medical3.0%

2017 2022

2.50.0%

3.5%

7.7%

3.8% Power gen conventional

Power gen nuclear

Power gen renewables

INDUSTRY, €BN

1.23.1Wind OEM

POWER GENERATION, €BN

RESOURCES, €BN

TRANSPORTS,€BN

2017 2022

5.12.0%

2.5%

1.7%

4.8%

3.2%5.8

Railway

Rolling Stock

Aero

Automotive

Ship

2017 2022

2.4

7.3%

1.5%

0.7%

2.6

O&G downstream

O&G upstream

Mining and tunnel

X CAGR

X CAGR

X CAGR

X CAGR

Paced For Growth 2018-2022

Nexans will focus on most attractive segments

33

Industry &SolutionsIndustry & Solutions: Selective growth

Active portfolio management is required to address the complexity of the Industry & Solutions business…

Handling Mining Nuclear & Conventional Oil & Gas Upstream Shipbuilding & Navy

Automation Oil & Gas Downstream Railway Infrastructure & Rolling Stock

Renewables& Wind OEMs

Aerospace

Gro

wLevera

ge

…while defending historical strong market share

Automotive

Paced For Growth 2018-2022

34

Industry &SolutionsIndustry & Solutions: Paced for Growth

We mobilize global leverage & innovation providing connectivity for added customer value…

Grow our market share on the most

attractive segments:

• Customer focus / key account

management

• Product range extension

• Market reach in NAM & APAC

Defend our historic strong market

share and ensure to leverage the

expected partial recovery of certain

markets such as Shipyards, O&G

upstream and Mining

Secure efficient

operations and

competitiveness

through 3 levers:

• Design

excellence

• Leverage most

competitive

manufacturing

sites

• Factory

performance &

modernization

Accelerate growth in renewable

energy:

• Contracting activities on extended

electrical package

Develop services in priority growth

markets:

• Supply Chain

• Engineering

• Connectivity / cable kits

Continue to focus on cost

leadership

Build on strengths in

attractive markets

Accelerate growth through portfolio

of activities

C

A B

Paced For Growth 2018-2022

Industry & SolutionsIndustry & Solutions: Key Financials

35

…and we smartly shift portfolio to grow most promising segments

Smart shift of portfolio to grow most promising and profitable

industrial market segments

Key Performance levers

0

Sa

les/C

E

RoS

ROCE2

Downcycle units

(O&G, Shipyard,

Mining)

Market leaders

A

Focus on Cost

leadership

B

Build on

strengths in

attractive

markets

C

Accelerate

growth through

portfolio of

activities

Price Cost

Squeeze

Impact +++ +++ ++ ---

1 Sales at constant metal price, constant perimeter and constant currencies

² 12 month OM on end of period Capital Employed, restated for Antitrust provision (excl. harnesses)3 OM before depreciation

Key Figures1

2017 Est.Ambition

2022

Sales (€BN) ~1.1 ~ 1.6

Organic growth (5 years CAGR) ~ 7.5 %

EBITDA3 / Sales ~ 8% ~ 9.5%

CAPEX 120% 120%

Paced For Growth 2018-2022

36

.

1 Building & Territories

2 High Voltage & Projects

3 Telecom & Data

4 Industry & Solutions

5 Beyond cables

Business ambitions

Paced For Growth 2018-2022

Cable added-value

Cable

production

Cable

Services

Asset

management

Operations

System

management

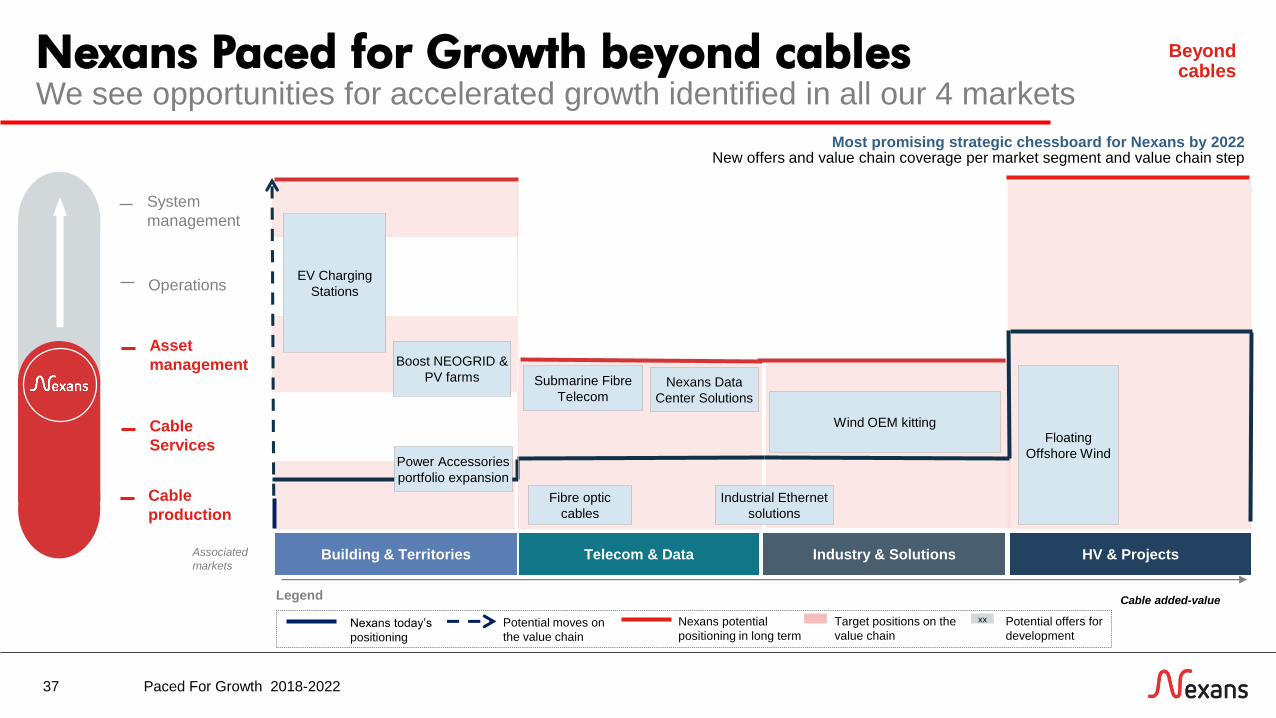

Nexans Paced for Growth beyond cables

37

We see opportunities for accelerated growth identified in all our 4 markets

Most promising strategic chessboard for Nexans by 2022New offers and value chain coverage per market segment and value chain step

Legend

Nexans today’s

positioning

Potential moves on

the value chain

Nexans potential

positioning in long term

Target positions on the

value chain

xx Potential offers for

development

Industry & SolutionsPower network utilitiesBuilding & Territories HV & ProjectsTelecom & DataAssociated

markets

Submarine Fibre

Telecom

Power Accessories

portfolio expansion

Industrial Ethernet

solutions

Nexans Data

Center Solutions

EV Charging

Stations

Boost NEOGRID &

PV farms

Floating

Offshore Wind

Fibre optic

cables

Wind OEM kitting

Beyond cables

Paced For Growth 2018-2022

Enablers & Actions

38

1 Digital, Innovation & Sales

2 Costs competitiveness &

Operational Efficiency

3 Organization & People

..

Paced For Growth 2018-2022

Innovation pipeline Paced for Growth

39

Our key asset to generate growth is our innovation pipeline…

High performance

operation at Low

temperature (- 65°C)

for Oil & Gas platforms

High mechanical

resistance

Supporting wind power generation from

deep offshore areas Cable dynamic designs for floating turbines off

the coasts (e.g. Hywind)

Ecodesign to decrease global warming

potentialEDRMAX by Nexans™ won 2 awards in December 2016:

> Ecoproduct for Sustainable Development

> [avniR] Ecodesign award

Improved safety with

Fire retardant cables

for buildings and tunnels

CPR European Regulation

compliance

(C)UL Certification

More distance and more power in grid

interconnectors, offshore wind parks and remote

O&G offshore platforms

HVDC submarine MI cables up to 600kV – 1.5GW

HVDC underground extruded cables – 320kV qualified

HVDC underground extruded cables ongoing

qualification 525kV

Electrical insulation

Tensile strength

Elongation

Abrasion resistance

Oil resistance

Fire reaction

High permittivity

Heat resistance

UV resistance

Core innovation: 70% of investments

To optimize core existing products for existing customers

Paced For Growth 2018-2022

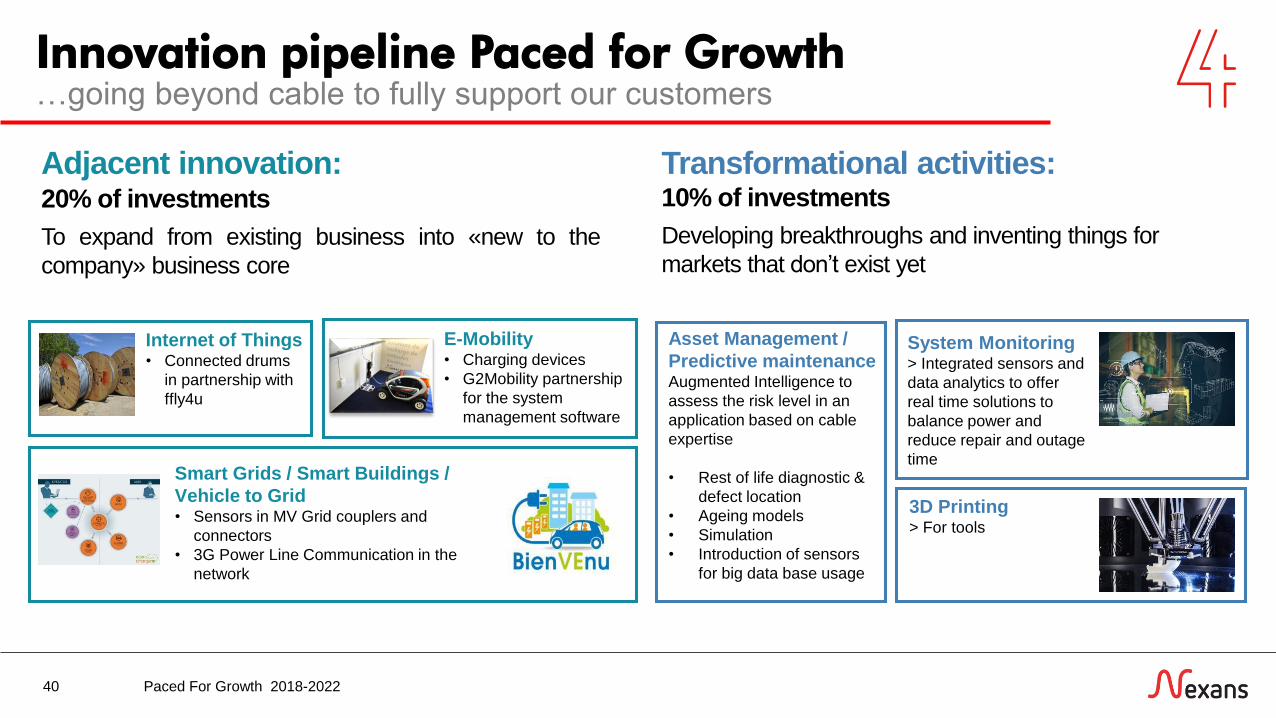

Innovation pipeline Paced for Growth

40

…going beyond cable to fully support our customers

Internet of Things• Connected drums

in partnership with

ffly4u

Smart Grids / Smart Buildings /

Vehicle to Grid• Sensors in MV Grid couplers and

connectors

• 3G Power Line Communication in the

network

E-Mobility • Charging devices

• G2Mobility partnership

for the system

management software

Adjacent innovation:20% of investments

To expand from existing business into «new to the

company» business core

Transformational activities: 10% of investments

Developing breakthroughs and inventing things for

markets that don’t exist yet

Asset Management /

Predictive maintenanceAugmented Intelligence to

assess the risk level in an

application based on cable

expertise

• Rest of life diagnostic &

defect location

• Ageing models

• Simulation

• Introduction of sensors

for big data base usage

System Monitoring> Integrated sensors and

data analytics to offer

real time solutions to

balance power and

reduce repair and outage

time

3D Printing> For tools

Paced For Growth 2018-2022

Scale Digital for business impact Digital transformation will support sales growth & cost performance…

41

GrowthPerformance GrowthPerformance

Paced For Growth 2018-2022

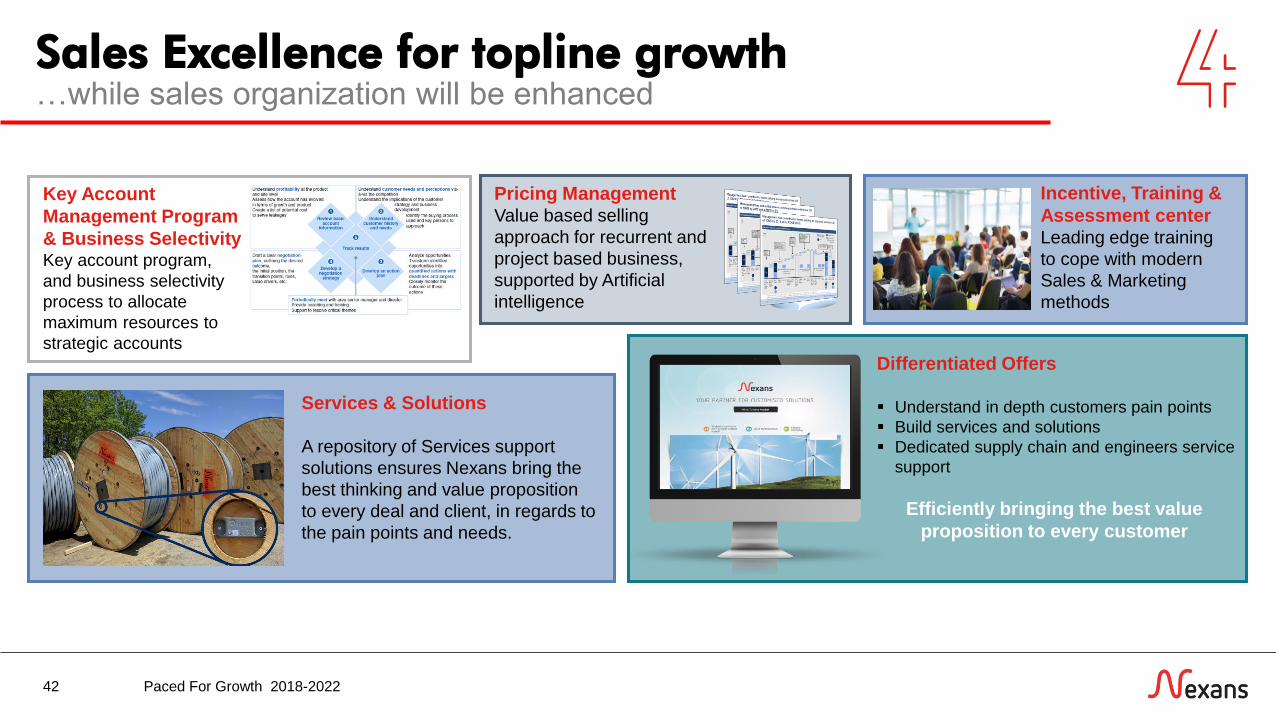

Sales Excellence for topline growth

42

…while sales organization will be enhanced

Incentive, Training &

Assessment centerLeading edge training

to cope with modern

Sales & Marketing

methods

Differentiated Offers

Understand in depth customers pain points

Build services and solutions

Dedicated supply chain and engineers service

support

Pricing ManagementValue based selling

approach for recurrent and

project based business,

supported by Artificial

intelligence

Services & Solutions

A repository of Services support

solutions ensures Nexans bring the

best thinking and value proposition

to every deal and client, in regards to

the pain points and needs.

Key Account

Management Program

& Business SelectivityKey account program,

and business selectivity

process to allocate

maximum resources to

strategic accounts

Efficiently bringing the best value

proposition to every customer

Paced For Growth 2018-2022

43

.Enablers & Actions

1 Digital, Innovation & Sales

2 Costs competitiveness &

Operational Efficiency

3 Organization & People

.

Paced For Growth 2018-2022

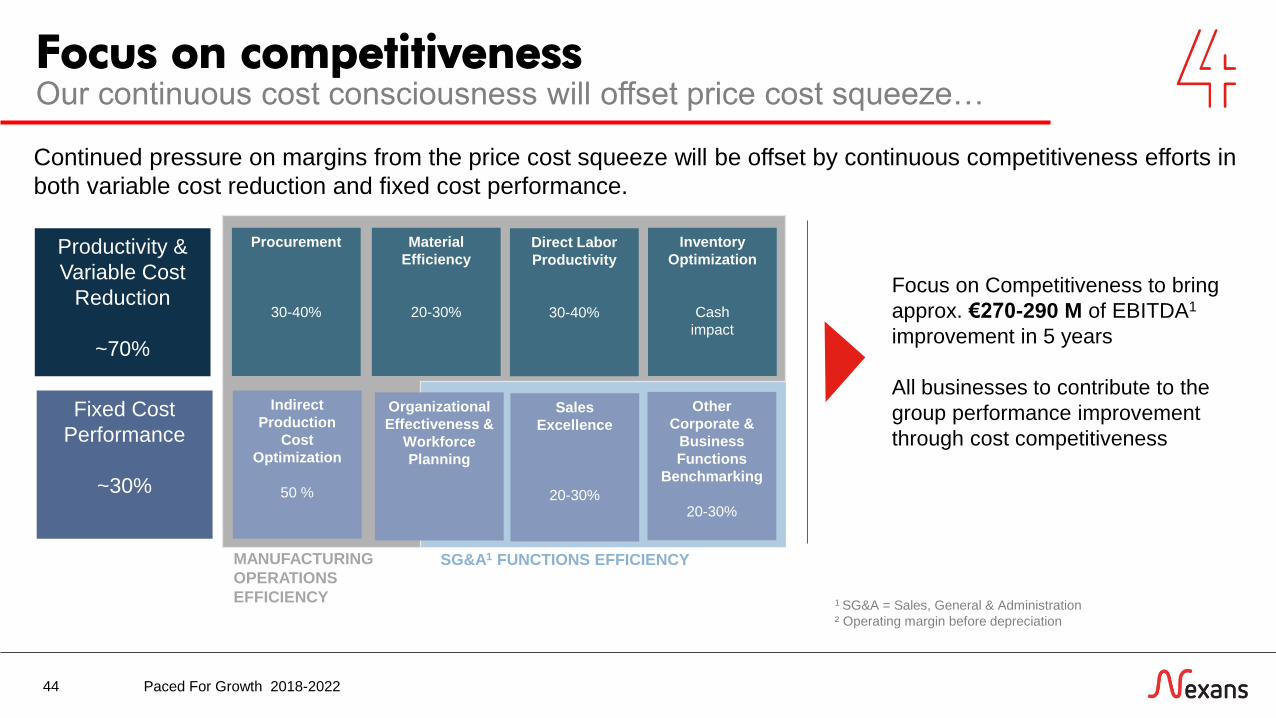

Our continuous cost consciousness will offset price cost squeeze…

44

Focus on competitiveness

Continued pressure on margins from the price cost squeeze will be offset by continuous competitiveness efforts in

both variable cost reduction and fixed cost performance.

Productivity &

Variable Cost

Reduction

~70%

Fixed Cost

Performance

~30%

Procurement

30-40%

Material

Efficiency

20-30%

Direct Labor

Productivity

30-40%

Inventory

Optimization

Cash

impact

Indirect

Production

Cost

Optimization

50 %

Sales

Excellence

20-30%

Other

Corporate &

Business

Functions

Benchmarking

20-30%

MANUFACTURING

OPERATIONS

EFFICIENCY

SG&A1 FUNCTIONS EFFICIENCY

Focus on Competitiveness to bring

approx. €270-290 M of EBITDA1

improvement in 5 years

All businesses to contribute to the

group performance improvement

through cost competitiveness

1 SG&A = Sales, General & Administration

² Operating margin before depreciation

Organizational

Effectiveness &

Workforce

Planning

Paced For Growth 2018-2022

Manufacturing operations efficiency…transforming our assets will increase productivity…

NEXANS 2018-22

OPERATIONS

RELIABILITY

AGILE BUSINESS

MODEL

▪ Excellence in

Safety

▪ Predictive

Quality and

Maintenance

▪ Deliver value

through leading

factories

▪ Customer-driven

Demand

Management

▪ Highly motivated

workforce

▪ Learning

organization

through training

WORKFORCE

TRANSFORMATION

CUSTOMER CENTRIC

FOOTPRINT

▪ Drive rapid

innovation

▪ Secure from

external disruption

45

2017

PE

RF

OR

MA

NC

E

2018 2020 2022

FACTORYOF THE FUTURE

FOCUSED PROCESS & PRODUCT IMPROVEMENTS

STANDARD CORE INITIATIVES

Paced For Growth 2018-2022

46

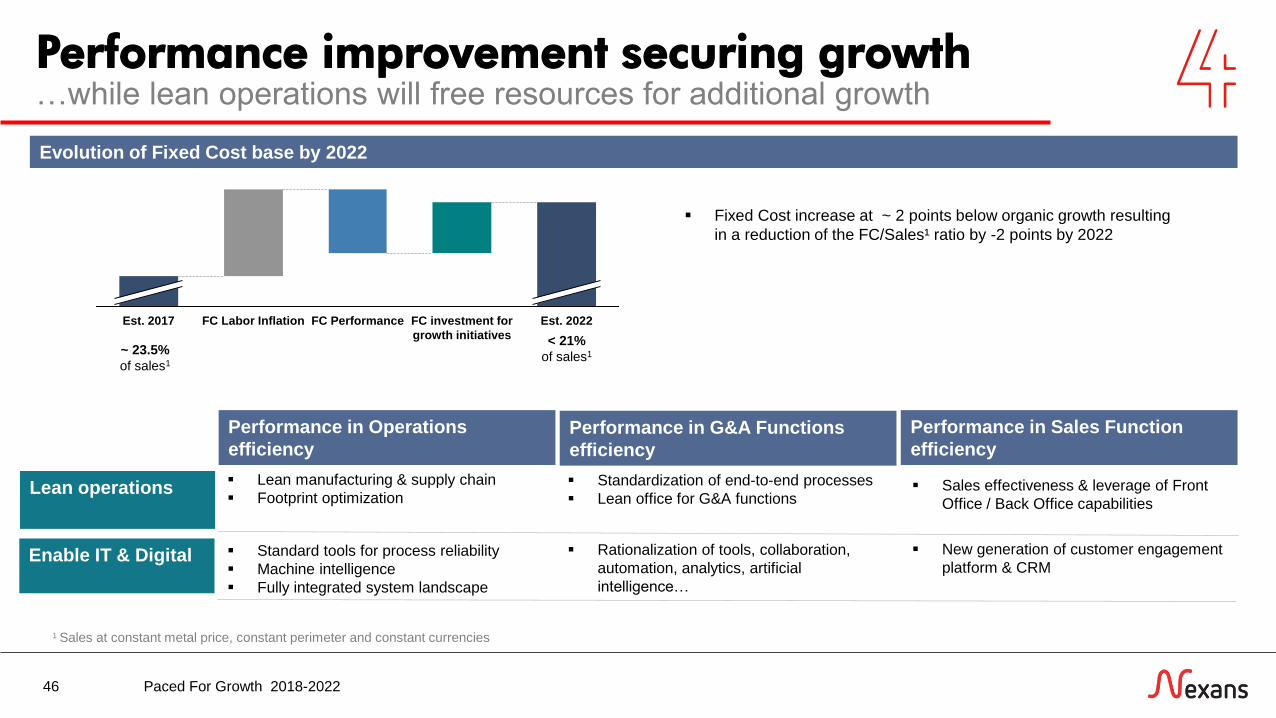

Performance improvement securing growth…while lean operations will free resources for additional growth

Est. 2022FC investment for

growth initiatives

FC PerformanceFC Labor InflationEst. 2017

Fixed Cost increase at ~ 2 points below organic growth resulting

in a reduction of the FC/Sales¹ ratio by -2 points by 2022

Evolution of Fixed Cost base by 2022

Performance in Operations

efficiencyPerformance in G&A Functions

efficiency

Lean manufacturing & supply chain

Footprint optimization

Standard tools for process reliability

Machine intelligence

Fully integrated system landscape

Performance in Sales Function

efficiency

Sales effectiveness & leverage of Front

Office / Back Office capabilities

New generation of customer engagement

platform & CRM

Lean operations

Enable IT & Digital

Standardization of end-to-end processes

Lean office for G&A functions

Rationalization of tools, collaboration,

automation, analytics, artificial

intelligence…

1 Sales at constant metal price, constant perimeter and constant currencies

~ 23.5%

of sales1

< 21%

of sales1

Paced For Growth 2018-2022

47

.Enablers & Actions

1 Digital, Innovation & Sales

2 Costs competitiveness &

Operational Efficiency

3 Organization & People

.

Paced For Growth 2018-2022

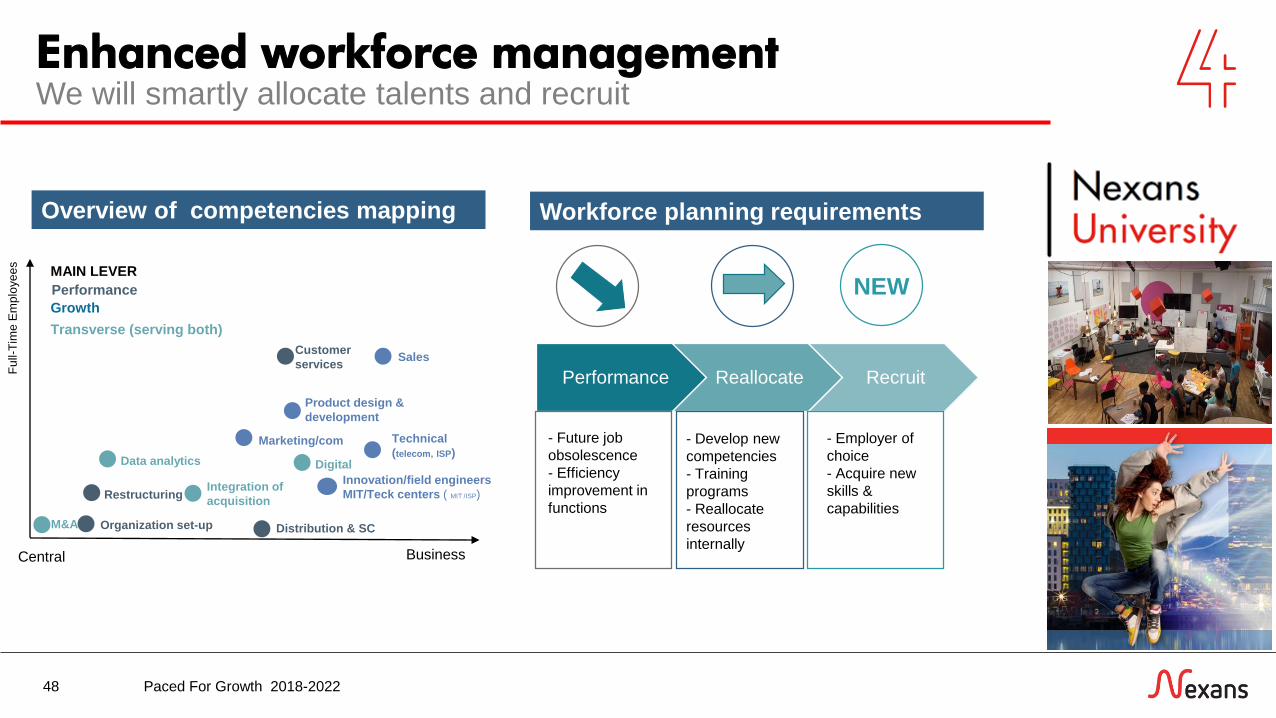

We will smartly allocate talents and recruit

48

Enhanced workforce management

Overview of competencies mapping

Performance Reallocate Recruit

NEW

- Future job

obsolescence

- Efficiency

improvement in

functions

- Develop new

competencies

- Training

programs

- Reallocate

resources

internally

- Employer of

choice

- Acquire new

skills &

capabilities

Workforce planning requirements

Central Business

Technical

(telecom, ISP)

M&A

Restructuring

Organization set-up

Marketing/com

Customer

servicesSales

Innovation/field engineers

MIT/Teck centers ( MIT /ISP)

Product design &

development

Integration of

acquisition

DigitalData analytics

Distribution & SC

Performance

Growth

MAIN LEVER

Transverse (serving both)

Fu

ll-T

ime

Em

plo

ye

es

Paced For Growth 2018-2022

Financials

Nexans 2018-224949 Paced For Growth 2018-2022

Aligned with market growth

Financials by Market

50

We will grow in HV, Telecom & Industry…

Organic Growth1 by segment

Building &

Territories

High

Voltage &

Projects

Telecom &

Data

Industry &

Solutions

Building

Utilities

Land High Voltage

Submarine High Voltage

Umbilicals

Operators

Special Telecom

LAN cables & systems

Transportation (incl. Harnesses)

Resources

Other speciatlies

Sub - segments CAGR 2018-19 2020-22

~ 2.5%

~ 8%

~ 10%

~ 7.5%

Group Organic Growth1 by 2022

Total Group 5% 3%

1 Sales at constant metal price, constant perimeter and constant currencies

6%

Acceleration in 2020-22 with commissioning of US plant and new cable

laying vessel operating at full speed

Robust growth across the cycle for the 3 sub-segments (LAN cables &

systems, telecom operators and special telecom subsea)

Acceleration in 2020-22 driven by completed shift of portfolio and recovery

of the O&G upstream and shipbuilding businesses

Paced For Growth 2018-2022

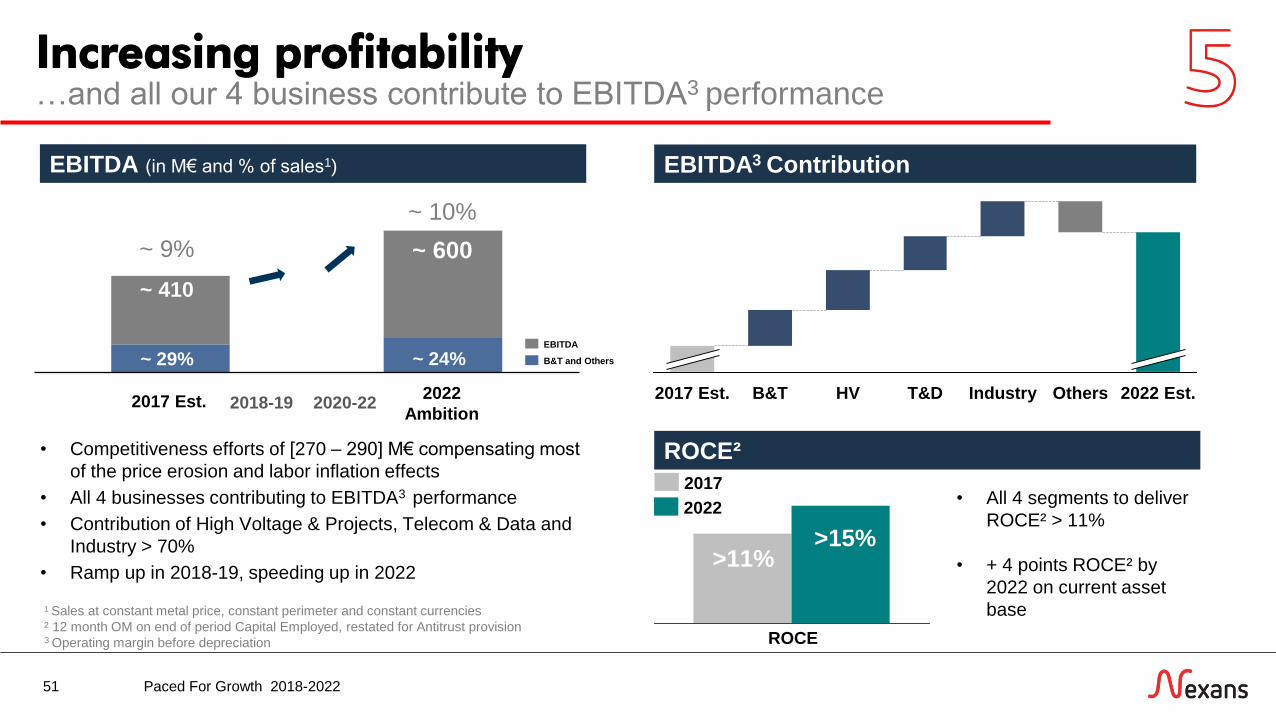

Increasing profitability

51

…and all our 4 business contribute to EBITDA3 performance

EBITDA (in M€ and % of sales1)

400 - 420580 - 620

ROCE²

2022

Ambition2017 Est.

~ 410

~ 600

ROCE

2022

2017

>11%>15%

• All 4 segments to deliver

ROCE² > 11%

• + 4 points ROCE² by

2022 on current asset

base

~ 9%

~ 10%

• Competitiveness efforts of [270 – 290] M€ compensating most

of the price erosion and labor inflation effects

• All 4 businesses contributing to EBITDA3 performance

• Contribution of High Voltage & Projects, Telecom & Data and

Industry > 70%

• Ramp up in 2018-19, speeding up in 2022

B&T and Others

EBITDA

1 Sales at constant metal price, constant perimeter and constant currencies

² 12 month OM on end of period Capital Employed, restated for Antitrust provision3 Operating margin before depreciation

~ 29% ~ 24%

EBITDA3 Contribution

Industry 2022 Est.B&T2017 Est. OthersT&DHV2018-19 2020-22

Paced For Growth 2018-2022

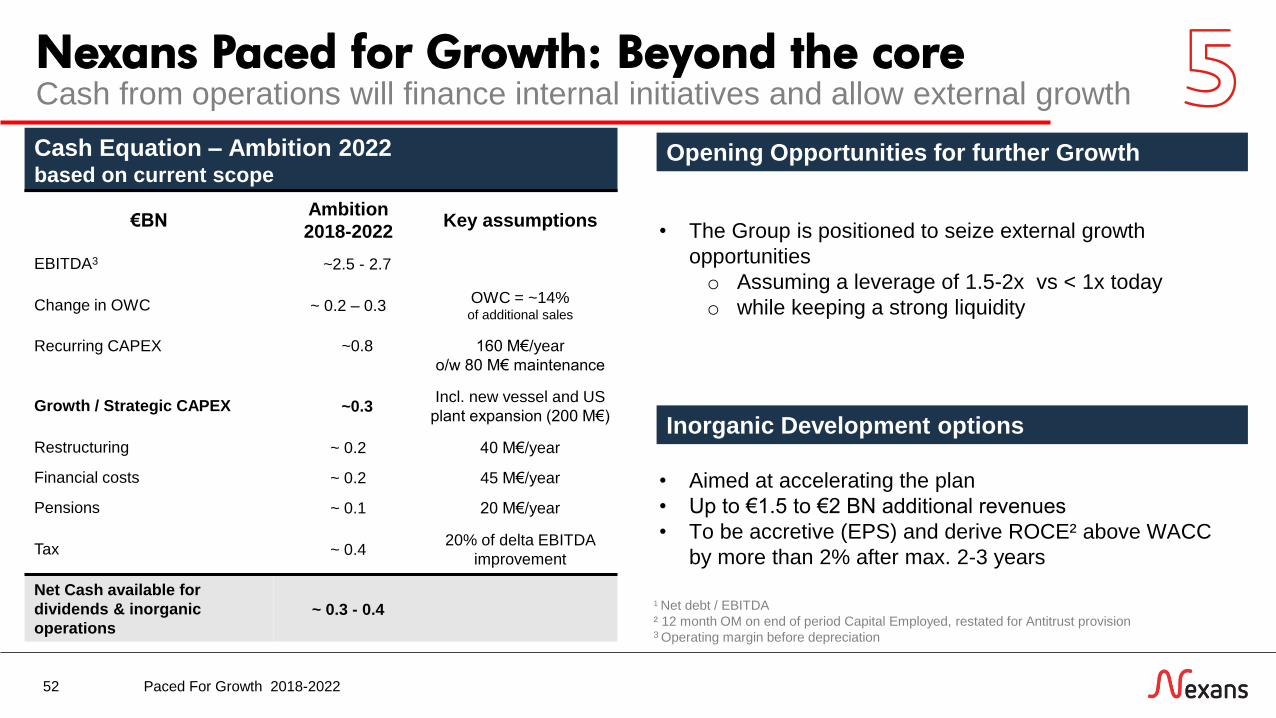

Nexans Paced for Growth: Beyond the core

52

Cash from operations will finance internal initiatives and allow external growth

Cash Equation – Ambition 2022based on current scope

• The Group is positioned to seize external growth

opportunities

o Assuming a leverage of 1.5-2x vs < 1x today

o while keeping a strong liquidity

Opening Opportunities for further Growth

€BNAmbition

2018-2022Key assumptions

EBITDA3 ~2.5 - 2.7

Change in OWC ~ 0.2 – 0.3OWC = ~14% of additional sales

Recurring CAPEX ~0.8 160 M€/year

o/w 80 M€ maintenance

Growth / Strategic CAPEX ~0.3Incl. new vessel and US

plant expansion (200 M€)

Restructuring ~ 0.2 40 M€/year

Financial costs ~ 0.2 45 M€/year

Pensions ~ 0.1 20 M€/year

Tax ~ 0.420% of delta EBITDA

improvement

Net Cash available for

dividends & inorganic

operations~ 0.3 - 0.4

1 Net debt / EBITDA

² 12 month OM on end of period Capital Employed, restated for Antitrust provision3 Operating margin before depreciation

• Aimed at accelerating the plan

• Up to €1.5 to €2 BN additional revenues

• To be accretive (EPS) and derive ROCE² above WACC

by more than 2% after max. 2-3 years

Inorganic Development options

Paced For Growth 2018-2022

Value for our Stakeholders

53

CSR is an integral part of our business strategy

CSR ranking 2014 2017

DC+

‘Prime’

D B

63/1002017:

72/100

PEOPLE

PRODUCTS

PLANET

PARTNERS

BRING INDIVIDUAL AND COLLECTIVE PERFORMANCE

TO OUR BUSINESS

Safety

Ensure health and safety at sites

Human capital

Build people who build business

CSR awareness

Empower our people on CSR

MANAGE THE ENVIRONMENTAL IMPACTS

Environmental management

Maintain a high level of environmental management

(hazardous waste, soil pollution, water)

Energy management

Develop production energy-efficency (reduction in consumption

and reduction of our product energy losses)

Climate strategy

Reduce climate impacts (GHG emissions for our activities and

for the product usage, resilience to extreme climate events)

EMBEDDING LEADERSHIP BASED

ON VALUES AND ETHICS

Business ethics

Maintain a compliant framework and fair business practices

Stakeholders

Maintain a sustainable stakeholder relationship

Nexans Foundation

Help underprivileged communities to access to energy

MANAGE IN A COMPETITIVE AND INNOVATIVE

SUSTAINABLE BUSINESS MODE

Energy transition: Engage with customers to contribute to a

more sustainable economy (energy transition, electric mobility,

smarter grids and renewable energy)

Innovation management: Guarantee an innovative collaboration

with stakeholders

Sustainable products: Increase resource-efficiency (materials

sourcing, recyclability, life cycle assessment and circular economy)

KPI Target 2022

SafetyWorkplace accident

frequency rate<1

Womenin management positions 25%

Environmental

certificationssites certified EHP and/or

ISO 14001

97%

OTIFincluding logistic and

plants data94%

Paced For Growth 2018-2022

Conclusion

54 Paced For Growth 2018-2022

Paced for Growth

55

By bringing energy and information to life, we are the critical link.

InnovationPeopleSustainable

growth

The ‘Paced for Growth’ strategic plan will allow us to go further in the innovationand differentiation of our activities in markets with high-potential on a globalscale.

Being a cable leader is the core of our activity but today we have the ability togo beyond that to become a critical link, the one capable of providing womenand men around the world with the energy and information they need.

Paced For Growth 2018-2022

Q&A

56 Paced For Growth 2018-2022

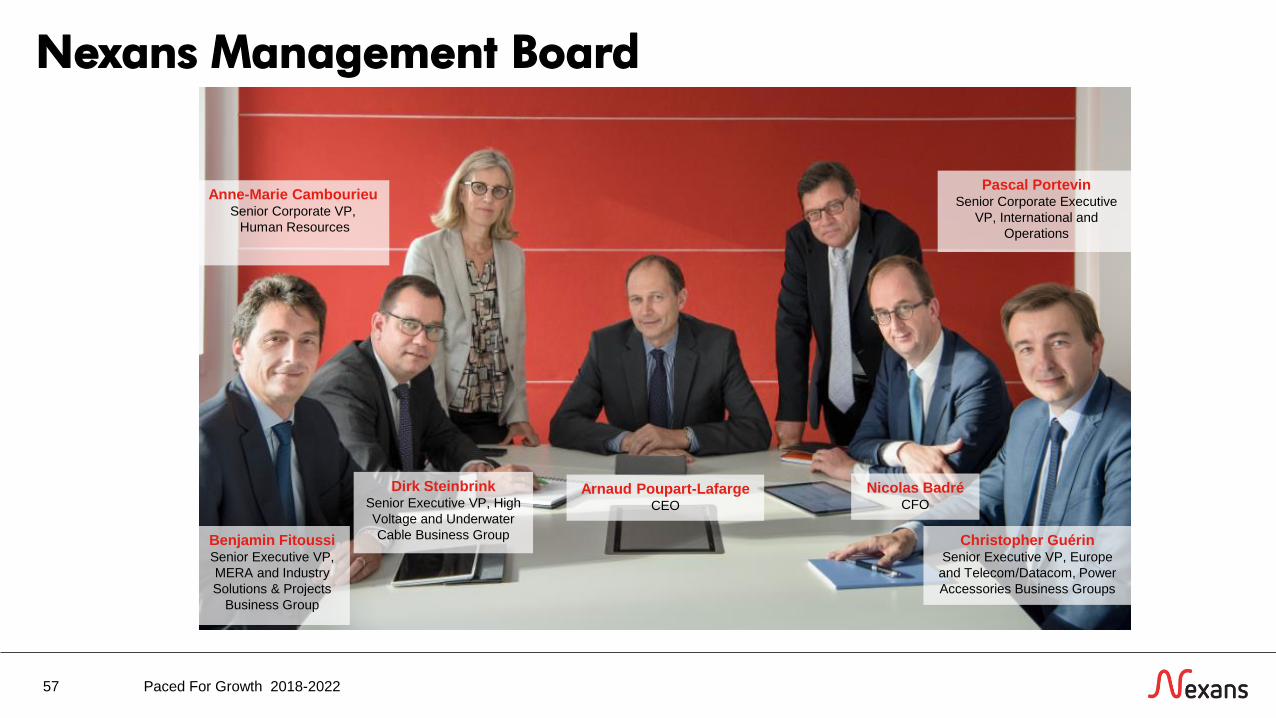

Nexans Management Board

57

Arnaud Poupart-LafargeCEO

Pascal PortevinSenior Corporate Executive

VP, International and

Operations

Anne-Marie CambourieuSenior Corporate VP,

Human Resources

Nicolas BadréCFO

Christopher GuérinSenior Executive VP, Europe

and Telecom/Datacom, Power

Accessories Business Groups

Benjamin FitoussiSenior Executive VP,

MERA and Industry

Solutions & Projects

Business Group

Dirk SteinbrinkSenior Executive VP, High

Voltage and Underwater

Cable Business Group

Paced For Growth 2018-2022

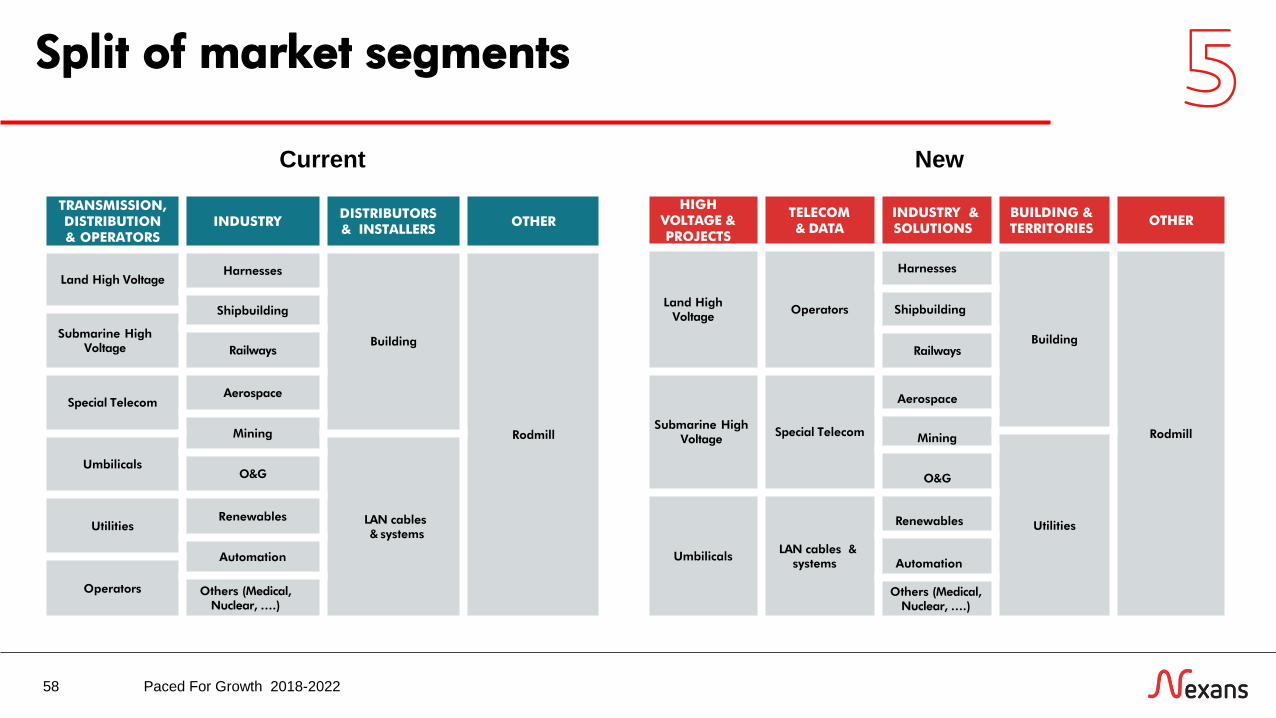

Split of market segments

58

Current New

TRANSMISSION,DISTRIBUTION& OPERATORS

INDUSTRYDISTRIBUTORS & INSTALLERS

OTHER

Land High VoltageHarnesses

Building

Rodmill

Shipbuilding

Submarine High Voltage Railways

Special TelecomAerospace

Mining

Umbilicals

LAN cables & systems

O&G

UtilitiesRenewables

Automation

Operators Others (Medical, Nuclear, ….)

HIGH VOLTAGE & PROJECTS

TELECOM & DATA

INDUSTRY & SOLUTIONS

BUILDING & TERRITORIES

OTHER

Land HighVoltage

Operators

Harnesses

Building

Rodmill

Shipbuilding

Railways

Submarine High Voltage

Special Telecom

Aerospace

Mining

Utilities

O&G

UmbilicalsLAN cables &

systems

Renewables

Automation

Others (Medical, Nuclear, ….)

Paced For Growth 2018-2022

NEXANS 2018-2259