investor day 2014: strategic progress - home –...

TRANSCRIPT

Investor Day 2014:

Strategic progressACIS turnaround underway

10 March 2014 Davinder Chugh, CEO ACIS, member of the GMB

Marc Vereecke, COO ACIS

AM Temirtau

AM South Africa

AM Kryviy Rih

DisclaimerForward-Looking Statements

This document may contain forward-looking information and statements about

ArcelorMittal and its subsidiaries. These statements include financial projections and estimates

and their underlying assumptions, statements regarding plans, objectives and expectations with

respect to future operations, products and services, and statements regarding future performance.

Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,”

“target” or similar expressions. Although ArcelorMittal’s management believes that the

expectations reflected in such forward-looking statements are reasonable, investors and holders

of ArcelorMittal’s securities are cautioned that forward-looking information and statements are

subject to numerous risks and uncertainties, many of which are difficult to predict and generally

beyond the control of ArcelorMittal, that could cause actual results and developments to differ

materially and adversely from those expressed in, or implied or projected by, the forward-looking

information and statements. These risks and uncertainties include those discussed or identified in

the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de

Surveillance du Secteur Financier) and the United States Securities and Exchange Commission

(the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal’s Annual Report on Form

20-F for the year ended December 31, 2013 filed with the SEC. ArcelorMittal undertakes no

obligation to publicly update its forward-looking statements, whether as a result of new

information, future events, or otherwise.

Non-GAAP Financial Measures

This presentation may contain supplemental financial measures that are or may be non-

GAAP financial measures. Definitions of such supplemental financial measures and a discussion

of the most directly comparable IFRS financial measures can be found on ArcelorMittal's

website at http://www.arcelormittal.com/corp/investors/presentations/

1

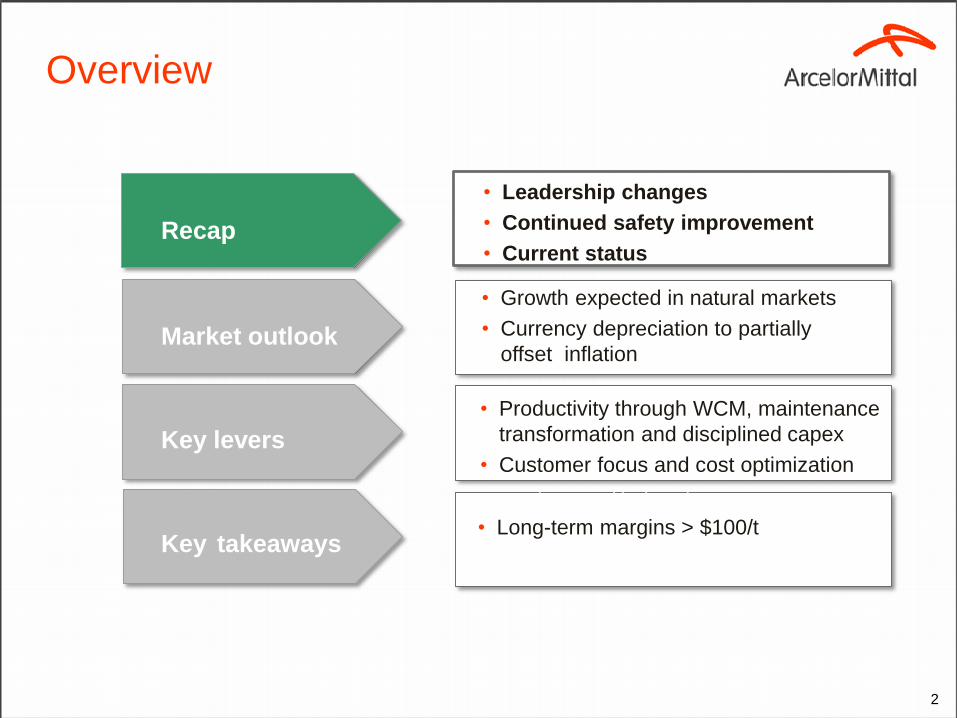

Overview

2

Recap

Market outlook

Key takeaways

• Leadership changes

• Continued safety improvement

• Current status

• Growth expected in natural markets

• Currency depreciation to partially

offset inflations

Key levers

• Productivity through WCM, maintenance

transformation and disciplined capex

• Customer focus and cost optimization

growth opportunities intensity

• Long-term margins > $100/t

opportunities intensity0

3GMB: Group Management Board; VP: Vice President; GM: General Manager

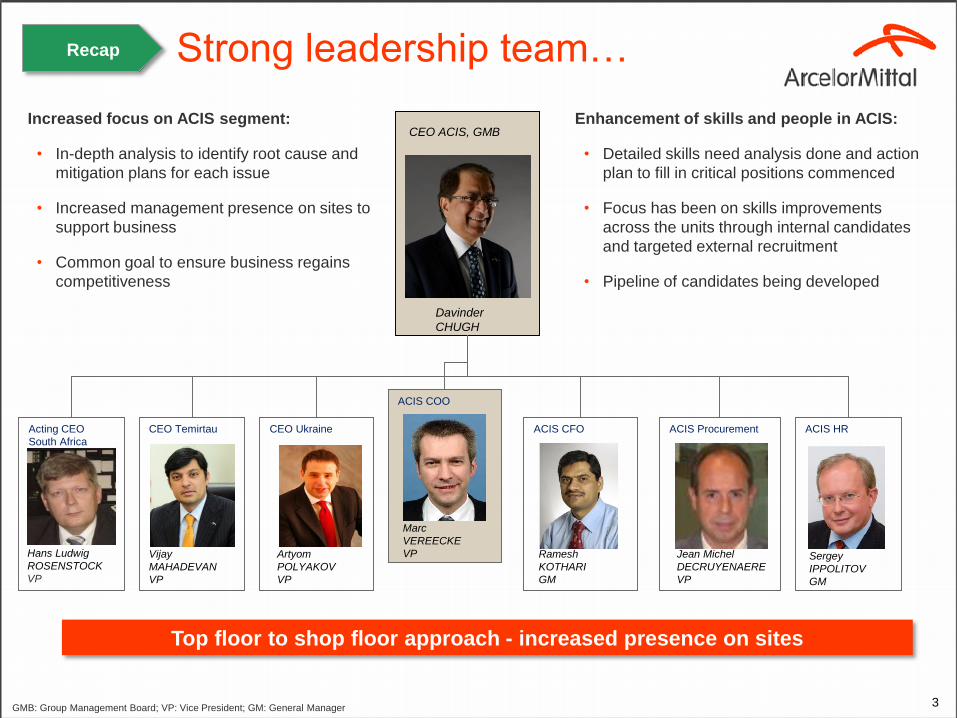

Strong leadership team…

Top floor to shop floor approach - increased presence on sites

CEO Temirtau ACIS HRACIS CFOActing CEO

South Africa

CEO ACIS, GMB

Davinder

CHUGH

ACIS ProcurementCEO Ukraine

Hans Ludwig

ROSENSTOCK

VP

Vijay

MAHADEVAN

VP

Artyom

POLYAKOV

VP

Ramesh

KOTHARI

GM

Jean Michel

DECRUYENAERE

VP

ACIS COO

Marc

VEREECKE

VP

Enhancement of skills and people in ACIS:

• Detailed skills need analysis done and action

plan to fill in critical positions commenced

• Focus has been on skills improvements

across the units through internal candidates

and targeted external recruitment

• Pipeline of candidates being developed

Increased focus on ACIS segment:

• In-depth analysis to identify root cause and

mitigation plans for each issue

• Increased management presence on sites to

support business

• Common goal to ensure business regains

competitiveness

Sergey

IPPOLITOV

GM

Recap

4

Health and safety performance improved overall

• Company is focused on further reducing the rate of severe

injuries and fatality prevention

• In 2014, specific attention will be on contractor performance

and on the main causes for 2013 fatal accidents

Health and safety lost time injury frequency rate (LTIF)*

ACIS steel, employees and contractors

Key focus areas and developments:

• Continue Journey to Zero fatalities through

fatality prevention program and improving

the culture of Health and Safety within the

segment

• Special focus on contractor management,

education and training

• Shop floor audits and proactive preventive

measures being implemented

• Lessons learnt exchanged with peers and

benchmarking (internal and external)

• Daily inspection and safety mindset

reinforcement campaign

• Efforts on absenteeism reduction paying off

Safety is the No.1 priority; Our goal is to be the safest steel company

* WSA: LTIF = Lost time injury frequency defined as Lost Time Injuries per 1.000.000 worked hours; based on own personnel and contractors

Continued improvement in safety

0,51

2011

0,68

2010

0,92

2009

1,09

2008

1,16

2007

1,80

2013 Target

-71%

2012

0,53

Recap

5

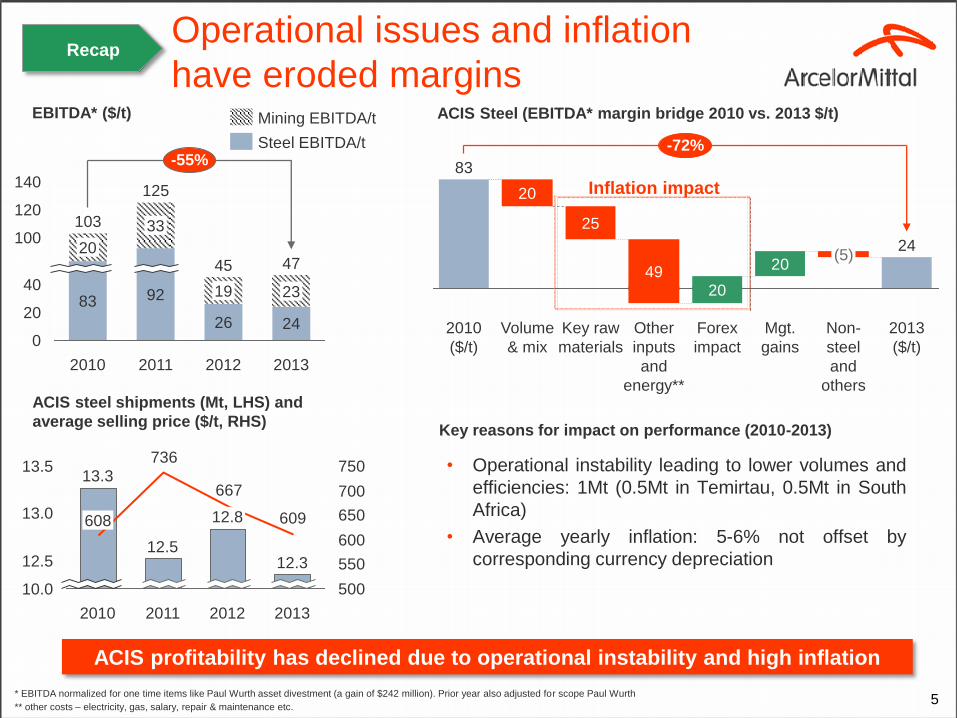

EBITDA* ($/t)

* EBITDA normalized for one time items like Paul Wurth asset divestment (a gain of $242 million). Prior year also adjusted for scope Paul Wurth

** other costs – electricity, gas, salary, repair & maintenance etc.

ACIS profitability has declined due to operational instability and high inflation

Operational issues and inflation

have eroded marginsACIS Steel (EBITDA* margin bridge 2010 vs. 2013 $/t)

25

Volume

& mix

20

2010

($/t)

83

-72%

2013

($/t)

24

Non-

steel

and

others

(5)

Mgt.

gains

20

Forex

impact

20

Other

inputs

and

energy**

49

Key raw

materials

Inflation impact

• Operational instability leading to lower volumes and

efficiencies: 1Mt (0.5Mt in Temirtau, 0.5Mt in South

Africa)

• Average yearly inflation: 5-6% not offset by

corresponding currency depreciation

26 24

140

120

100

40

20

0

-55%

2013

47

23

2012

45

19

2011

125

92

33

2010

103

83

20

Key reasons for impact on performance (2010-2013)

Steel EBITDA/t

Mining EBITDA/t

609

667

736

500

550

600

650

700

75013.5

13.0

12.5

10.0

2013

12.3

2012

12.8

2011

12.5

2010

13.3

608

ACIS steel shipments (Mt, LHS) and

average selling price ($/t, RHS)

Recap

6

Recap

Market outlook

Key takeaways

• Leadership changes

• Continued safety improvement

• Current status

• Growth expected in natural markets

• Currency depreciation to partially

offset inflations

Key levers

• Productivity through WCM, maintenance

transformation and disciplined capex

• Customer focus and cost optimization

growth opportunities intensity

• Long-term margins > $100/t

opportunities intensity0

7

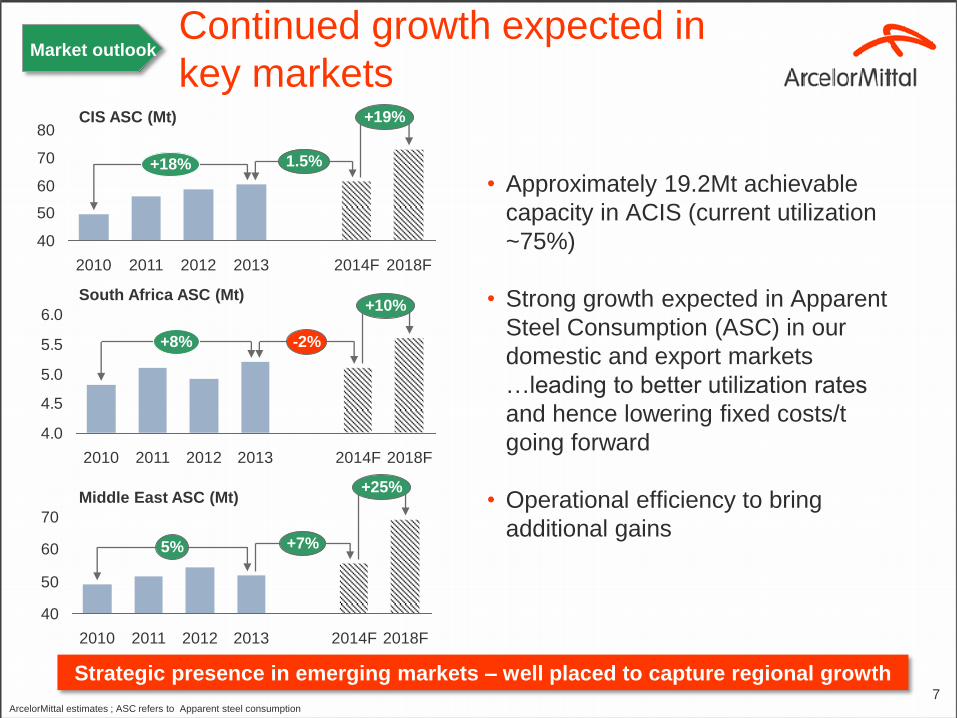

Continued growth expected in

key markets

Strategic presence in emerging markets – well placed to capture regional growth

CIS ASC (Mt)

40

50

60

70

80

20112010

+19%

+18% 1.5%

2018F2014F20132012

Middle East ASC (Mt)

40

50

60

70

2010

+25%

+7%5%

2018F2014F201320122011

South Africa ASC (Mt)

4.0

4.5

5.0

5.5

6.0+10%

+8%

2010

-2%

2018F2014F201320122011

• Approximately 19.2Mt achievable

capacity in ACIS (current utilization

~75%)

• Strong growth expected in Apparent

Steel Consumption (ASC) in our

domestic and export markets

…leading to better utilization rates

and hence lowering fixed costs/t

going forward

• Operational efficiency to bring

additional gains

ArcelorMittal estimates ; ASC refers to Apparent steel consumption

Market outlook

8

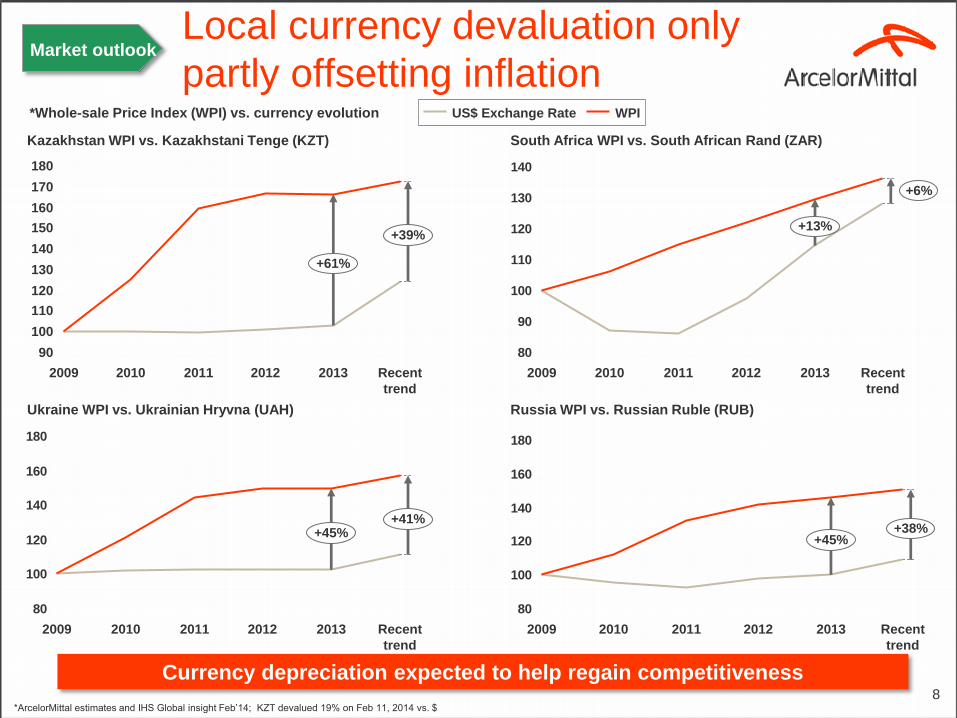

Local currency devaluation only

partly offsetting inflation

Currency depreciation expected to help regain competitiveness

Kazakhstan WPI vs. Kazakhstani Tenge (KZT)

Ukraine WPI vs. Ukrainian Hryvna (UAH)

South Africa WPI vs. South African Rand (ZAR)

*Whole-sale Price Index (WPI) vs. currency evolution

*ArcelorMittal estimates and IHS Global insight Feb’14; KZT devalued 19% on Feb 11, 2014 vs. $

80

100

120

140

160

180

+41%+45%

Recent

trend

20132012201120102009

110

100

90

180

170

160

150

140

130

120

+39%

+61%

Recent

trend

20132012201120102009

80

90

100

110

120

130

140

+6%

+13%

Recent

trend

20132012201120102009

WPIUS$ Exchange Rate

80

100

120

140

160

180

20102009

+38%+45%

Recent

trend

201320122011

Russia WPI vs. Russian Ruble (RUB)

Market outlook

9

Recap

Market outlook

Key takeaways

• Leadership changes

• Continued safety improvement

• Current status

• Growth expected in natural markets

• Currency depreciation to partially offset

inflations

Key levers

• Productivity through WCM, maintenance

transformation and disciplined capex

• Customer focus and cost optimization

growth opportunities intensity

• Long-term margins > $100/t

opportunities intensity0

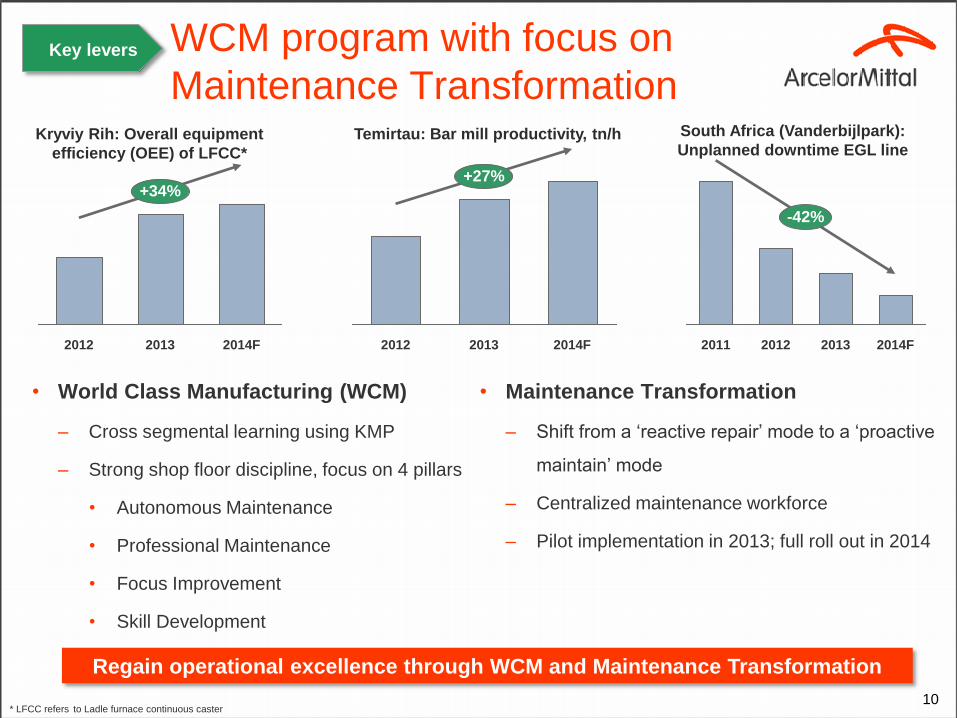

• World Class Manufacturing (WCM)

– Cross segmental learning using KMP

– Strong shop floor discipline, focus on 4 pillars

• Autonomous Maintenance

• Professional Maintenance

• Focus Improvement

• Skill Development

WCM program with focus on

Maintenance TransformationTemirtau: Bar mill productivity, tn/h

Regain operational excellence through WCM and Maintenance Transformation

10

+27%

2014F20132012

South Africa (Vanderbijlpark):

Unplanned downtime EGL line

2012

-42%

20132011 2014F

Kryviy Rih: Overall equipment

efficiency (OEE) of LFCC*

• Maintenance Transformation

– Shift from a ‘reactive repair’ mode to a ‘proactive

maintain’ mode

– Centralized maintenance workforce

– Pilot implementation in 2013; full roll out in 2014

+34%

2014F20132012

* LFCC refers to Ladle furnace continuous caster

Key levers

Higher investment to ensure assets run full, stable and improve reliability

395433

613

515

2010 2011

489

Long

term*

> 550

>39%-120

2012 2013

Capex ($million)Major projects ongoing and planned

• Learning from fire incident in Vanderbijlpark

(“Vdp”): Risk identification mapping and mitigation

plans ongoing

• 3 major blast furnace relines in 2014/15

– Temirtau, Kryviy Rih and Newcastle

• Higher self sufficiency in energy supply

– PCI unit in Ukraine

– Power plant revamping in Temirtau

• Upgrade coke oven battery in Ukraine

• 2013 Capex $395m, average 2010–

2013 at ~$489m

• 2014 Capex > $550m; includes major

reline projects

Capex allocated to improve asset

availability and reliability

11

• Fewer breakdowns and unplanned downtime will

result in improvement in stability

• Modernization of our plants improving productivity

• Readiness to ramp up production to capture

growth

*Long term: 3-5 years

Key levers

12

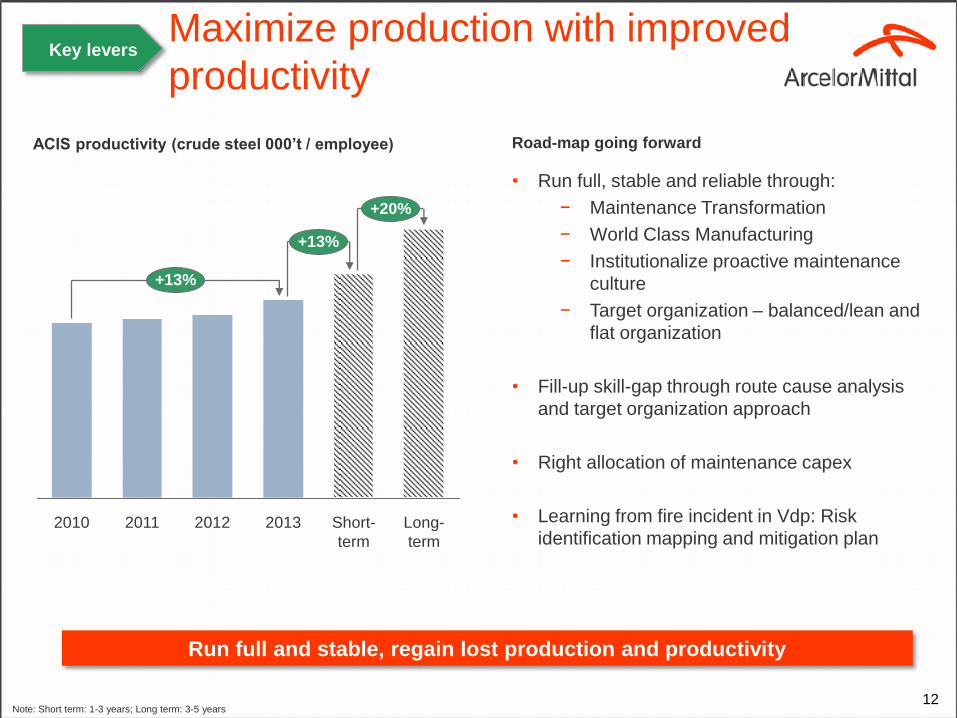

Maximize production with improved

productivity

ACIS productivity (crude steel 000’t / employee)

Note: Short term: 1-3 years; Long term: 3-5 years

Run full and stable, regain lost production and productivity

• Run full, stable and reliable through:

− Maintenance Transformation

− World Class Manufacturing

− Institutionalize proactive maintenance

culture

− Target organization – balanced/lean and

flat organization

• Fill-up skill-gap through route cause analysis

and target organization approach

• Right allocation of maintenance capex

• Learning from fire incident in Vdp: Risk

identification mapping and mitigation plan

Road-map going forward

+20%

2011 2012

+13%

Long-

term

+13%

Short-

term

20132010

Key levers

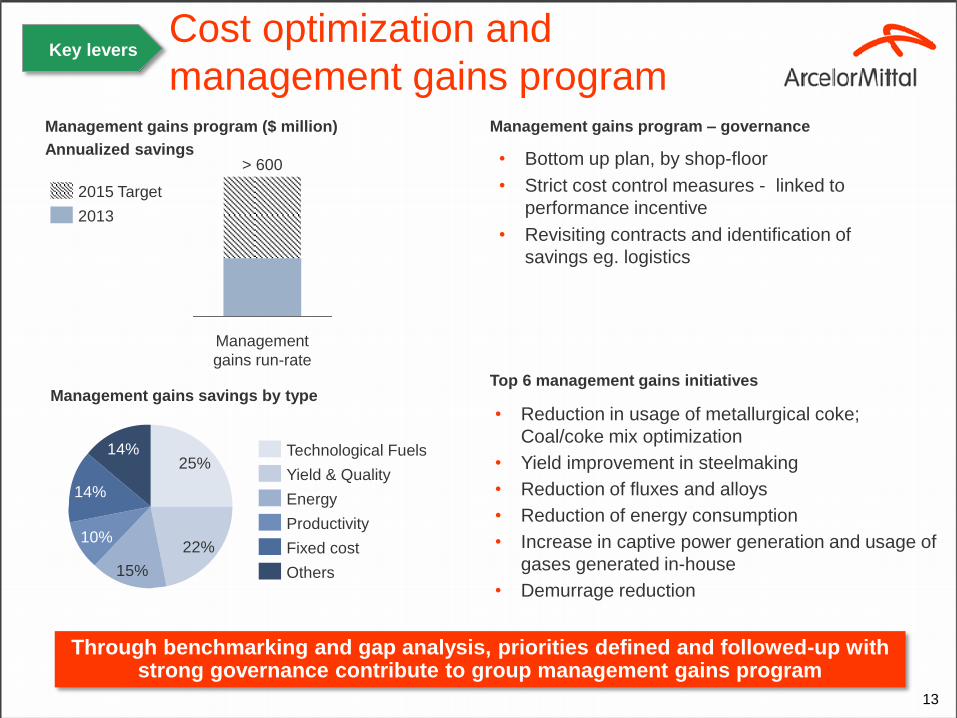

Through benchmarking and gap analysis, priorities defined and followed-up with strong governance contribute to group management gains program

13

Management gains program ($ million)

Annualized savings• Bottom up plan, by shop-floor

• Strict cost control measures - linked to

performance incentive

• Revisiting contracts and identification of

savings eg. logistics

Cost optimization and

management gains programManagement gains program – governance

• Reduction in usage of metallurgical coke;

Coal/coke mix optimization

• Yield improvement in steelmaking

• Reduction of fluxes and alloys

• Reduction of energy consumption

• Increase in captive power generation and usage of

gases generated in-house

• Demurrage reduction

Top 6 management gains initiatives

Management

gains run-rate

> 600

2013

2015 Target

15%

22%

25%14%

14%

10%Productivity

Energy

Yield & Quality

Technological Fuels

Fixed cost

Others

Management gains savings by type

Key levers

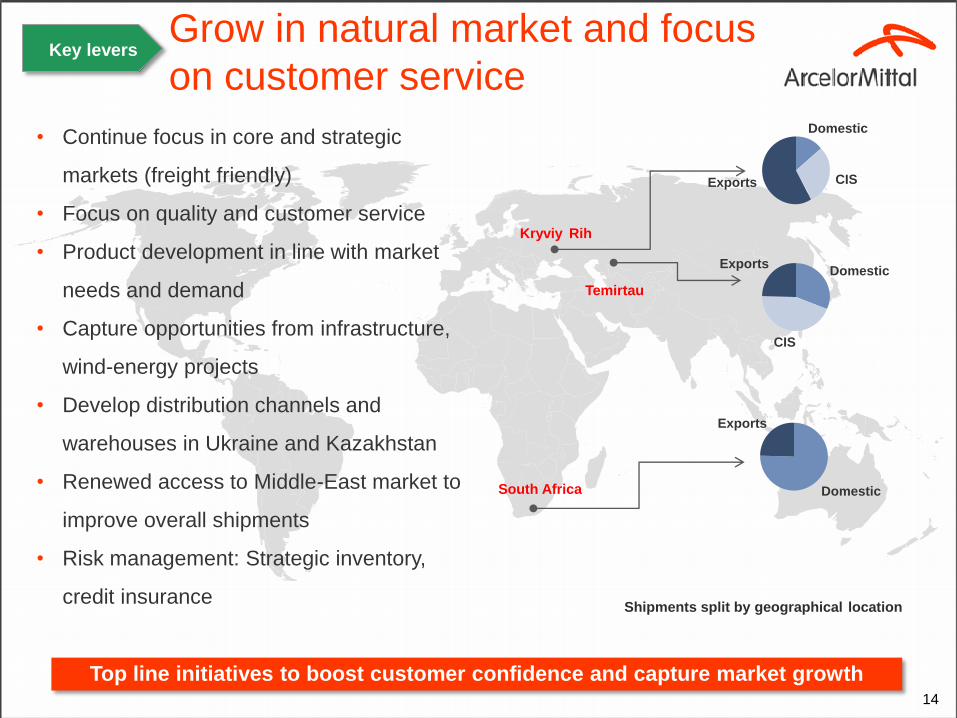

Top line initiatives to boost customer confidence and capture market growth 14

• Continue focus in core and strategic

markets (freight friendly)

• Focus on quality and customer service

• Product development in line with market

needs and demand

• Capture opportunities from infrastructure,

wind-energy projects

• Develop distribution channels and

warehouses in Ukraine and Kazakhstan

• Renewed access to Middle-East market to

improve overall shipments

• Risk management: Strategic inventory,

credit insurance

Grow in natural market and focus

on customer service

Exports CIS

Domestic

Shipments split by geographical location

Exports

CIS

Domestic

Exports

DomesticSouth Africa

Key levers

Temirtau

Kryviy Rih

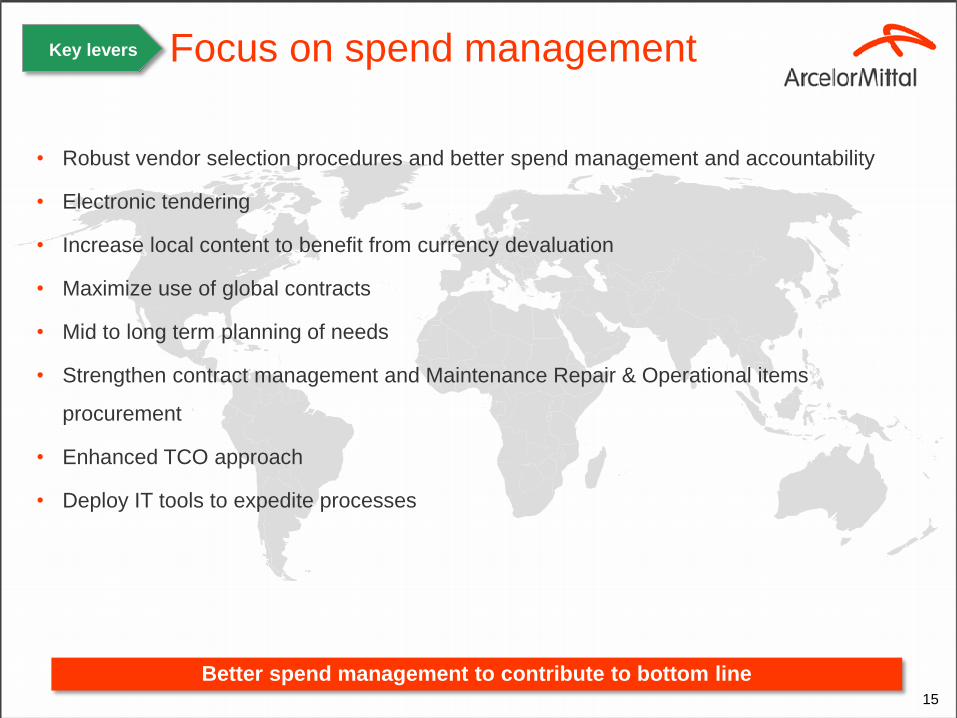

Better spend management to contribute to bottom line15

Focus on spend management

• Robust vendor selection procedures and better spend management and accountability

• Electronic tendering

• Increase local content to benefit from currency devaluation

• Maximize use of global contracts

• Mid to long term planning of needs

• Strengthen contract management and Maintenance Repair & Operational items

procurement

• Enhanced TCO approach

• Deploy IT tools to expedite processes

Key levers

16

Recap

Market outlook

Key takeaways

• Leadership changes

• Continued safety improvement

• Current status

• Growth expected in natural markets

• Currency depreciation to partially

offset inflations

Key levers

• Productivity through WCM, maintenance

transformation and disciplined capex

• Customer focus and cost optimization

growth opportunities intensity

• Long-term margins > $100/t

opportunities intensity0

17

248

753

241

3,413

2,582

61

Q1'11 EBITDA Volume & Mix Selling Price / Cost Non Steel EBITDA* Others** Q2'11 EBITDA

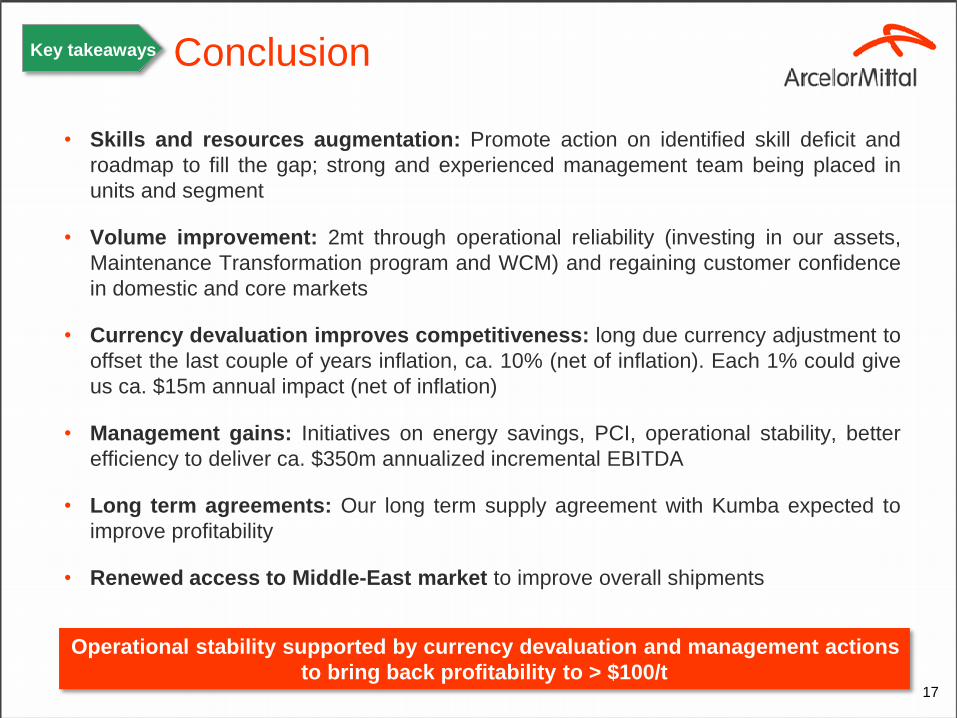

Operational stability supported by currency devaluation and management actions

to bring back profitability to > $100/t

• Skills and resources augmentation: Promote action on identified skill deficit and

roadmap to fill the gap; strong and experienced management team being placed in

units and segment

• Volume improvement: 2mt through operational reliability (investing in our assets,

Maintenance Transformation program and WCM) and regaining customer confidence

in domestic and core markets

• Currency devaluation improves competitiveness: long due currency adjustment to

offset the last couple of years inflation, ca. 10% (net of inflation). Each 1% could give

us ca. $15m annual impact (net of inflation)

• Management gains: Initiatives on energy savings, PCI, operational stability, better

efficiency to deliver ca. $350m annualized incremental EBITDA

• Long term agreements: Our long term supply agreement with Kumba expected to

improve profitability

• Renewed access to Middle-East market to improve overall shipments

ConclusionKey takeaways

Q&A

Contacts

Daniel Fairclough – Global Head Investor Relations

+44 207 543 1105

Hetal Patel – UK/European Investor Relations

+44 207 543 1128

Valérie Mella – European and Retail Investor Relations

+44 207 543 1156

Maureen Baker – Fixed Income/Debt Investor Relations

+33 1 71 92 10 26

Thomas A McCue – US Investor Relations

+312-899-3927

Lisa Fortuna – US Investor Relations

+312-899-3985