investoer guide for turkey

DESCRIPTION

Investor Guide FOR TURKEYTRANSCRIPT

INVESTOR’S GUIDE

FOR TURKEY

2

Establishing a Business in Turkey ..................................................3

Cost of Doing Business in Turkey ...................................................4 Incentives......................................................................................7 1. The Investment Incentive System in Turkey....................................................... 7

1.a. General Investment Incentive Regime ...................................................................... 7 1.b Incentives for Priority Development Regions .............................................................. 7 1.c Incentives Granted to Small and Medium Sized Enterprises (SME Incentives) ................. 9 1.d Research and Development Supports ........................................................................ 9 1.e Technology Development Zones’ Supports ............................................................... 10 1.f State Incentives for Export ..................................................................................... 10

Taxes ...........................................................................................11 1. Taxes .......................................................................................................... 11

1.b Taxes on Expenditure............................................................................................ 12 1.c Taxes on Wealth ................................................................................................... 12

2. Tax Incentives.............................................................................................. 14 3. Tax Exemptions and Allowances ..................................................................... 14

Special Investment Zones............................................................15 Demography and Labor Force ......................................................18 1. DEMOGRAPHY .............................................................................................. 18 2. LABOR FORCE .............................................................................................. 19

Business Environment..................................................................24 AUTONOMOUS BODIES ..................................................................................... 24

1. Competition Authority ............................................................................................. 24 2. Energy Market Regulation Authority .......................................................................... 24 3. Banking Regulation and Supervision Agency .............................................................. 24 4. Telecommunication Authority ................................................................................... 25 5. Tobacco, Tobacco Products and Alcoholic Beverages Market Regulation Board................ 25 6. Privatization Authority............................................................................................. 25

ENVIRONMENTAL STANDARDS........................................................................... 26 TURKISH LABOR MARKET .................................................................................. 26 EMPLOYMENT OF EXPATRIATES.......................................................................... 26

1. How to get a work permit in Turkey .......................................................................... 26 2. Main categories of work permits ............................................................................... 27

RESEARCH AND DEVELOPMENT ACTIVITIES ........................................................ 27 1. TUBITAK ............................................................................................................... 27 2. TTGV .................................................................................................................... 27 3. KOSGEB ................................................................................................................ 28

Infrastructure ..............................................................................29

Economic Outlook ........................................................................34 1. MACROECONOMIC INDICATORS ..................................................................... 34

1.a Changes in price levels .......................................................................................... 35 1.b Balance of Payments ............................................................................................. 36

2.FDI IN TURKEY.............................................................................................. 41 3. INTERNATIONAL TRADE ................................................................................ 46

Business Legislation.....................................................................52

3

Establishing a Business in Turkey

Turkey's regulatory environment is extremely business-friendly. You can establish a business in Turkey irrespective of nationality or place of residence. The registration and establishment of a company in Turkey can be completed in one day. The process is handled by one ministry which acts as the coordinator between all authorities. The first step in establishing a business in Turkey is to fill out the "Business Registration Form" at the local Trade Registry Office located at the local Chamber of Commerce. Here are the steps to follow: • Submit the notarized 'Articles of Association'. • Deposit 0.04% of the capital into either a State Bank or the Turkish Central Bank. • Complete the “Company Establishment Form” and register with the Trade Registry Office. International companies may start their activities in Turkey in various forms depending on the investors' development strategies. The most common types of legal entities in Turkey are : • Limited Liability Company (Ltd.Sti.) • Joint-Stock Company (A.S) • Branch Office • Liaison Office

4

Cost of Doing Business in Turkey

Minimum Monthly Wage (Gross and Net)

USD

Net Minimum Wage 297.29

- Social Security Premium Payment (14%) 58.08

- Payment for Unemployment Insurance Fund (1%) 4.14

- Income Tax (15%) 52.90

- Stamp Tax (6%) 2.48

Gross Minimum Wage 414.89

Total Deduction 117.60

Cost for Employer

Gross Minimum Wage 414.89

Employer Share of Social Security Premium (19.5%) 80.90

Employer's Payment for Unemployment Insurance Fund

(2%) 8.29

Total Cost for Employer 504.08

Source: Ministry of Labor and Social Security, Valid for the year

2007.

35,6% of the labor force work on the minimum wage which is the highest rate in the EU.

For more than four years, the electricity cost remain at the same tariff. The cost policy was adopted by

Turkish Government in order to maintain the stability of the competiveness of national productivity.

5

Cost of Electricity

Cost of Electricity USD/kwh

Active Energy

Daytime Night

Cent/kWh Cent/kWh

Double Term Tariff

Industry Mid

Voltage 0.070 0.035

Single Term Tariff

Mid Voltage 0.081 0.046

Source: Tedaş, Valid for the year 2007

Cost of Water for Industrial Use

Type of

Customer USD/m3

Water Waste

Water Total VAT (%)

Industry 2.41 0 2.41 8

Org.Ind.Zone 1.57 0 1.57 8

Source: ĐSKĐ, valid for the year 2007.

Cost of natural gas for industrial purposes

Price per kwh (USD)

Disengaged Consumer Engaged Consumer

0.030743 USD/kwh 0.034992 USD/kwh

Engaged Consumer: The group of consumers who must purchase

gas from the local supplier company.

Disengaged Consumer: The group of consumers who consumes

more than 1 million m3 annually and qualified to purchase gas

from other suppliers.

Source: IGDAŞ, Valid for the year 2007.

6

Cost of Telephone Use

USD

Fixed Cost (per Month) 25.17

CALL CHARGES- YTL/min

Local Peak 0.039

Local Off-Peak(2) 0.019

Long Distance 0.056

Source: Turk Telecom, valid for the year 2007.

7

Incentives

1. The Investment Incentive System in Turkey

The investment incentives scheme was amended in 2006 to promote investment in manufacturing

services and the energy sector as well as to encourage exports. Local and foreign investors have equal

access to these incentives.

1.a. General Investment Incentive Regime

The general incentive regime is mainly a tax benefit program yet in certain cases there are credit

possibilities. It is applied varyingly according to the location, scale, and subject of the investment.

The Major Incentives Instruments

• Exemption from Customs Duties and Fund Levies;

• Custom Tax exemption for locally purchased or imported machinery and equipment

• VAT Exemption for Imported or Locally Purchased Machinery and Equipment;

• VAT exemption for locally purchased or imported machinery and equipment for projects

Interest Support:

The Treasury covers selected parts of the investment credits’ interest rate. Interest support is provided

for

• SME’s

• R&D Projects

• Environmental Projects

• Projects in 50 Prioritized Development Provinces

1.b Incentives for Priority Development Regions

Incentives are provided in 50 provinces

8

Province List

Incentives provided are as below;

• Free Land

• Income Tax Relief

• Employer’s Share for Social Security Relief

• Energy Support

Free land allocation provided in 4 provinces

9

INCENTIVE TYPE FOR COMPANIES OIZ’s AND

INDUSTRIAL ZONES OTHERS

INCOME TAX RELIEF 100 % 80 %

COMPANSATION FOR THE EMPLOYERS SOCIAL

SECURITY CONTRIBIUTION 100 % 80 %

ENERGY SUPPORT VARIES MIN. 20% - 50% VARIES MIN. 20%

- 50%

FREE LAND ALLOCATION AVAILABLE AVAILABLE

1.c Incentives Granted to Small and Medium Sized Enterprises (SME Incentives)

• Custom Duties Exemption

• VAT Exemption

• Interest Support

KOSGEB support of SME’s; The Small and Medium Industry Development Organization (KOSGEB) makes

significant contributions to strengthen SME’s by various support instruments in financing, R&D, common

facilities, market research, investment site, marketing, export and training.

1.d Research and Development Supports

TÜBĐTAK (Scientific and Technological Research Council of Turkey) and TTGV (Turkish Technology

Development Foundation) both reimburse and/or grant R&D related expenses and capital loans for R&D

projects.

Projects eligible for TÜBĐTAK Incentives cover:

• Concept Development

• Technological Research and Technical Feasibility Research

• Laboratory Studies in the transformation of a concept to a design

• Design and Sketching Studies

• Prototype Production

• Construction of pilot facilities

• Test production

• Patent and License studies

• Activities related to post-sale problems stemming from product design

10

1.e Technology Development Zones’ Supports

• Infrastructure facilities are provided.

• Profits derived out software and R&D activities are exempt from income and corporate taxes until

31.12.2013.

• The wages of researchers, software and R&D personnel employed in the zone are exempt from all

taxes until 31.12.2013.

• VAT exemption during the exemption period of income and corporate taxes is provided for IT specific

sectors.

• Exemption from customs and duties as well as fund levies.

1.f State Incentives for Export The principle aims of this scheme are to encourage export and to increase the competitiveness of firms in international markets. This specific package covers mainly R&D activities, market research, participation in exhibitions and international fairs, expenditures for patents, trademarks and industrial design.

11

Taxes

1. Taxes

Turkey has one of the most competitive corporate tax rates in the OECD region. The new Corporate Tax

law that was enacted on June 21, 2006 has made some important amendments to the current

applications and also included new concepts in the tax legislation. With the new Corporate Tax Law in

place, the Turkish corporate tax legislation has noticeably clearer, more objective and greater

harmonized provisions which are in-line with international standards.

The Turkish tax regime can be classified under three main headings:

1.a Income Taxes

Income taxes in Turkey are levied on all income, including domestic as well as foreign individuals and

corporations residing in Turkey. Non-residents earning income in Turkey through employment, ownership

of property, business transactions, or any other activity which generates income are also subject to

taxation, but only on the income earned in Turkey.

1.a.1 Corporate Income Taxes

In Turkey, the basic corporate income tax rate levied on business profits is 20%.

Withholding Taxes On Selected Payments of Resident Corporations

- Dividends are subject to 15%.

- Interest on treasury-bill and treasury bonds derived by resident corporations is subject to 10%.

- Interest on other bonds and bills derived by resident corporations is subject to 10%.

- Bank deposits are subject to 15%.

- Profit shares paid by participation banks in consideration of participation account are subject to 15%.

- REPO agreements are subject to 15%.

Withholding Taxes On Selected Payments of Non-Resident Corporations

- Dividends are subject to 15%.

- Interest on treasury-bill and treasury bonds derived by non-resident corporations is subject to 0%.

- Interest on other bonds and bills derived by non-resident corporations is subject to 0%.

- Bank deposits are subject to 15%.

- Profit shares paid by participation banks in consideration of participation account are subject to 15%.

- REPO agreements are subject to 15%.

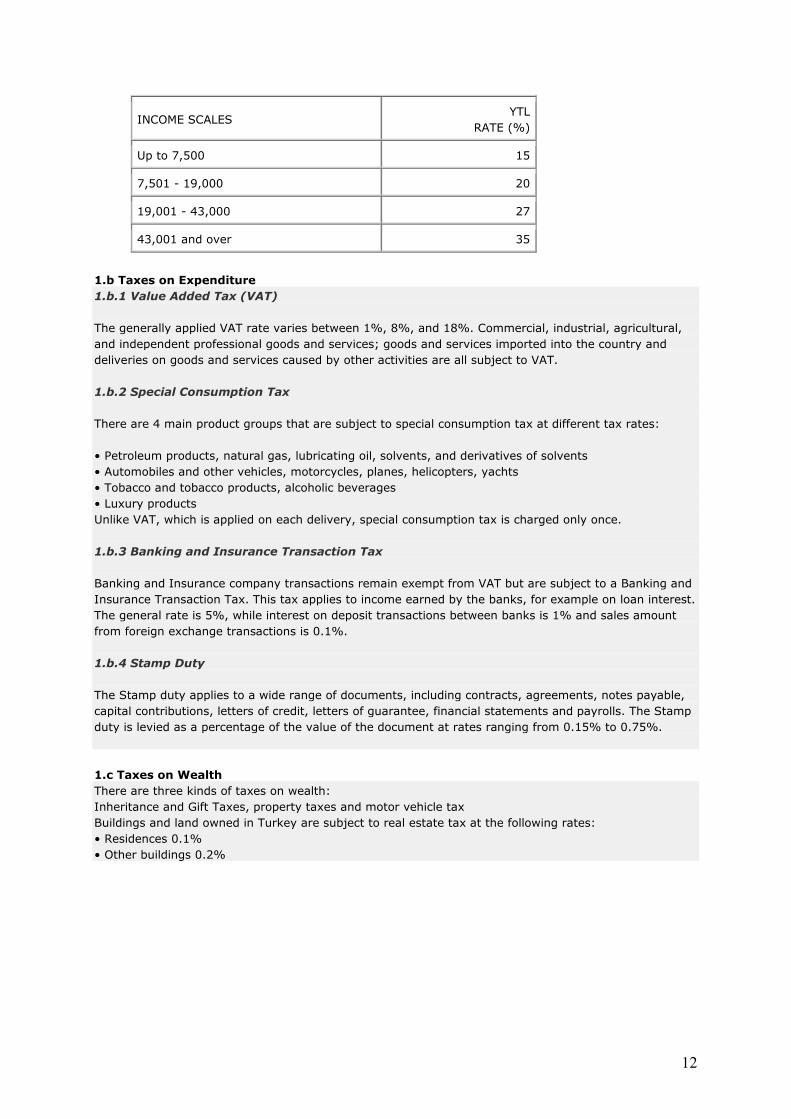

1.a.2 Individual Income Tax

The personal income tax rate varies from 15% to 35%.

Income tax rates applicable to yearly gross earnings from 2007 are as follows:

12

1.b Taxes on Expenditure

1.b.1 Value Added Tax (VAT)

The generally applied VAT rate varies between 1%, 8%, and 18%. Commercial, industrial, agricultural,

and independent professional goods and services; goods and services imported into the country and

deliveries on goods and services caused by other activities are all subject to VAT.

1.b.2 Special Consumption Tax

There are 4 main product groups that are subject to special consumption tax at different tax rates:

• Petroleum products, natural gas, lubricating oil, solvents, and derivatives of solvents

• Automobiles and other vehicles, motorcycles, planes, helicopters, yachts

• Tobacco and tobacco products, alcoholic beverages

• Luxury products

Unlike VAT, which is applied on each delivery, special consumption tax is charged only once.

1.b.3 Banking and Insurance Transaction Tax

Banking and Insurance company transactions remain exempt from VAT but are subject to a Banking and

Insurance Transaction Tax. This tax applies to income earned by the banks, for example on loan interest.

The general rate is 5%, while interest on deposit transactions between banks is 1% and sales amount

from foreign exchange transactions is 0.1%.

1.b.4 Stamp Duty

The Stamp duty applies to a wide range of documents, including contracts, agreements, notes payable,

capital contributions, letters of credit, letters of guarantee, financial statements and payrolls. The Stamp

duty is levied as a percentage of the value of the document at rates ranging from 0.15% to 0.75%.

1.c Taxes on Wealth

There are three kinds of taxes on wealth:

Inheritance and Gift Taxes, property taxes and motor vehicle tax

Buildings and land owned in Turkey are subject to real estate tax at the following rates:

• Residences 0.1%

• Other buildings 0.2%

INCOME SCALES YTL

RATE (%)

Up to 7,500 15

7,501 - 19,000 20

19,001 - 43,000 27

43,001 and over 35

13

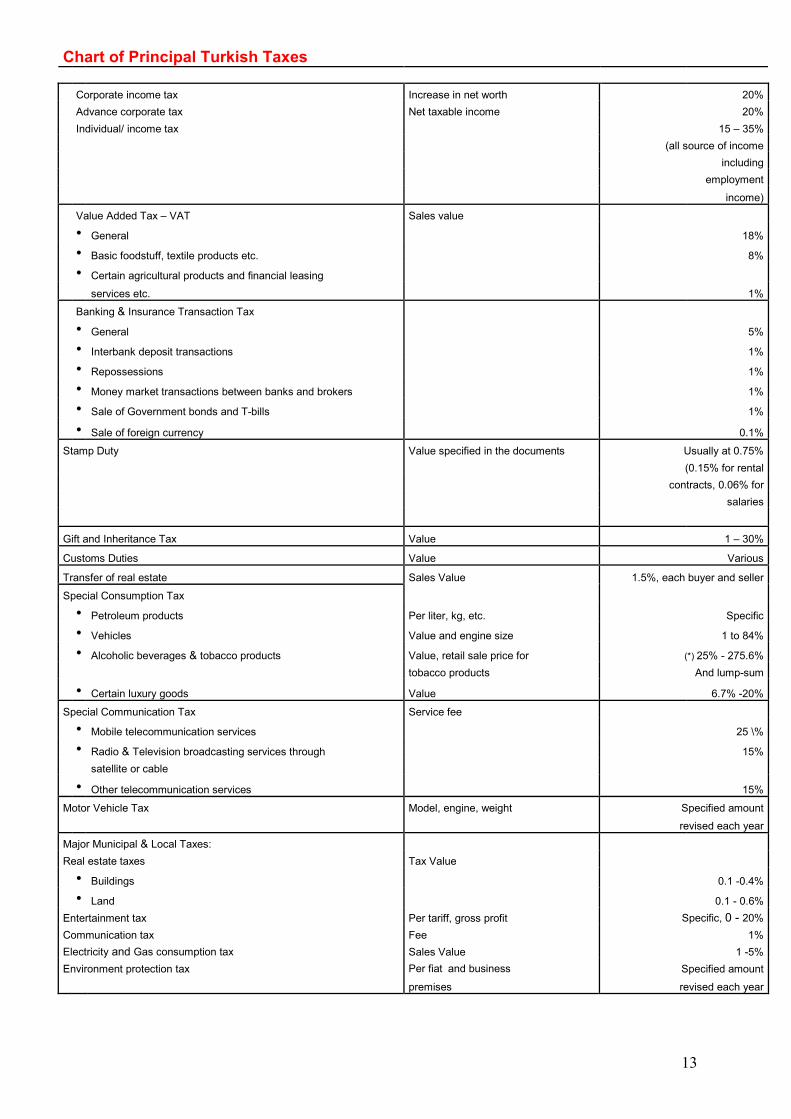

Chart of Principal Turkish Taxes

Corporate income tax Increase in net worth 20%

Advance corporate tax Net taxable income 20%

Individual/ income tax 15 – 35%

(all source of income

including

employment

income)

Value Added Tax – VAT Sales value

• General 18%

• Basic foodstuff, textile products etc. 8%

• Certain agricultural products and financial leasing

services etc. 1%

Banking & Insurance Transaction Tax

• General 5%

• Interbank deposit transactions 1%

• Repossessions 1%

• Money market transactions between banks and brokers 1%

• Sale of Government bonds and T-bills 1%

• Sale of foreign currency 0.1%

Stamp Duty Value specified in the documents Usually at 0.75%

(0.15% for rental

contracts, 0.06% for

salaries

Gift and Inheritance Tax Value 1 – 30%

Customs Duties Value Various

Transfer of real estate Sales Value 1.5%, each buyer and seller

Special Consumption Tax

• Petroleum products Per liter, kg, etc. Specific

• Vehicles Value and engine size 1 to 84%

• Alcoholic beverages & tobacco products Value, retail sale price for (*) 25% - 275.6%

tobacco products And lump-sum

• Certain luxury goods Value 6.7% -20%

Special Communication Tax Service fee

• Mobile telecommunication services 25 \%

• Radio & Television broadcasting services through 15%

satellite or cable

• Other telecommunication services 15%

Motor Vehicle Tax Model, engine, weight Specified amount

revised each year

Major Municipal & Local Taxes:

Real estate taxes Tax Value

• Buildings 0.1 -0.4%

• Land 0.1 - 0.6%

Entertainment tax Per tariff, gross profit Specific, 0 - 20%

Communication tax Fee 1%

Electricity and Gas consumption tax Sales Value 1 -5%

Environment protection tax Per fiat and business Specified amount

premises revised each year

14

(*) Only the percentage tax rate is applied provided that it is not less than the tax calculated by using the minimum lump-sum tax amounts.

Source : KPMG

2. Tax Incentives

• Prioritized Development Zones

• Technology Development Zones

• Organized Industrial Zones

• Free Zones

• Research and Development

• Educational Corporations

• Cultural Investments and Enterprises

3. Tax Exemptions and Allowances VAT exemptions include but are not limited to the following transactions: • Export of goods and services • Roaming services rendered in Turkey for customers outside Turkey (i.e. non-resident customers) in-line with international roaming agreements and which have a reciprocity condition in place • Petroleum exploration activities • International transportation • Deliveries made to diplomatic representatives, consulates and international organizations with tax exemption status and to their employees • The supply of machinery and equipment, including importation to persons or corporations that are VAT taxpayers and that have an investment certificate issued by the relevant authority • Services rendered at harbors and airports for vessels and aircrafts • Social and other exemptions apply to deliveries made to the government and other related organizations for cultural, educational, health and similar purposes • Banking and insurance transactions are exempted from VAT as they are subject to a separate Banking and Insurance Transactions Tax at the rate of 5 % • Tax exemption are provided for earnings derived by corporations from their overseas branches and both their domestic and overseas ventures if they meet certain conditions • Research and Development Allowances • Deductions from the tax base of corporations related to certain donations, aid or sponsorship expenditures for sport activities

15

Special Investment Zones

There are 4 types of special investment zones in Turkey:

1. TECHNOLOGY DEVELOPMENT ZONES - TECHNOPARKS • Technology Development Zones are areas designed to support R&D activities and attract investments in high technology fields. • There are 14 operational TDZ’s and 8 new TDZ’s which have been approved for construction.

ADVANTAGES OF TDZ’s • Offices ready to rent and infrastructure facilities provided. • Profits derived from software and R&D activities are exempt from income and corporate taxes until December 31, 2013. • Deliveries of application software produced exclusively in TDZ’s are exempt from VAT until December 31, 2013. Examples include software for systems management, data management, business applications, different business sectors, Internet, mobile phones and military command control. • Wages of researchers, software and R&D personnel employed in the zone are exempt from all taxes until December 31, 2013. • A VAT exemption during the exemption period of income and corporate taxes is provided for IT specific sectors. • Exemption from customs and duties as well as fund levies. • Academic staff is encouraged to establish companies, participate in a recognized company or join its executive boards as well as conduct research in the zones.

16

2. ORGANIZED INDUSTRIAL ZONES Organized Industrial Zones are designed in a way that allow companies which provide goods and services to operate within approved boundaries with the necessary infrastructure, techno parks and social facilities. • The infrastructure provided in the zones includes roads, water, natural gas, electricity, communications, waste treatment and other services. • There are 93 OIZ’s in 81 provinces with a completed infrastructure. Another 151 OIZ’s are currently under construction throughout Turkey. Number of Organized Industrial Zones in Turkey: Marmara Region (57) Aegean Region (44) Mediterranean Region (17) Central Anatolia Region (42) Black Sea Region (33) Eastern Anatolia Region (20) South Eastern Anatolia Region (13) ADVANTAGES OF OIZ’s have in 54 PRIORITIZED PROVINCES Investors operating in the zones located in 54 selected provinces benefit from the following advantages: • 100% exemption from income tax for employed workers. • 100% exemption from the employer’s share of social security costs. • Free land allocation. • Up to 50% support for electricity costs. • Exemption from real estate tax, waste water charges, building construction duties and the use-of-building. Province List: Provinces with active OIZ’s Adana, Adiyaman, Afyon, Amasya, Ankara, Antalya, Aydın, Balikesir, Bartin, Bayburt, Bilecik, Bolu, Burdur, Bursa, Canakkale, Cankiri, Corum, Denizli, Duzce, Elazıg, Erzincan, Erzurum, Eskisehir, Gaziantep, Hatay, Isparta, Istanbul, Izmir, Karaman, Karabuk, Kars, Kayseri, Kirikkale, Kirklareli, Kirşehir, Kilis, Kocaeli, Konya, Kütahya, Malatya, Manisa, Mardin, Mersin, Niğde, Ordu, Osmaniye, Samsun, Sinop, Sivas, Sanliurfa, Tekirdag, Tokat, Trabzon, Tunceli, Usak, Yozgat, Zonguldak, Van

3. INDUSTRIAL ZONES • Industrial Zones are designed to provide sites suitable for large scale and technology intensive investments. • The Council of Ministers approves the Industrial Zones after the evaluation of the investment sites by the Ministry of Industry and Trade. • The investments carried out in an Industrial Zone should be in a high technology sector and have an investment site of a minimum of 1,500 m2. • Industrial Zones benefit from all of the same advantages provided to OIZ’s.

17

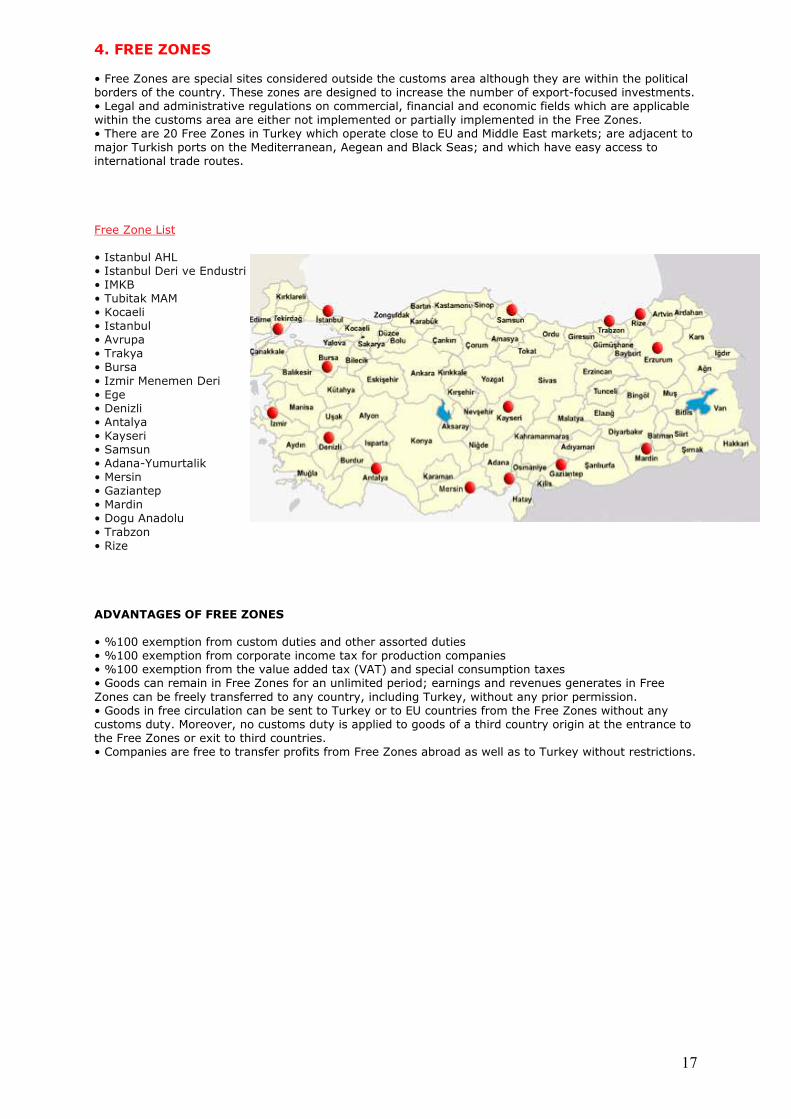

4. FREE ZONES • Free Zones are special sites considered outside the customs area although they are within the political borders of the country. These zones are designed to increase the number of export-focused investments. • Legal and administrative regulations on commercial, financial and economic fields which are applicable within the customs area are either not implemented or partially implemented in the Free Zones. • There are 20 Free Zones in Turkey which operate close to EU and Middle East markets; are adjacent to major Turkish ports on the Mediterranean, Aegean and Black Seas; and which have easy access to international trade routes. Free Zone List • Istanbul AHL • Istanbul Deri ve Endustri • IMKB • Tubitak MAM • Kocaeli • Istanbul • Avrupa • Trakya • Bursa • Izmir Menemen Deri • Ege • Denizli • Antalya • Kayseri • Samsun • Adana-Yumurtalik • Mersin • Gaziantep • Mardin • Dogu Anadolu • Trabzon • Rize ADVANTAGES OF FREE ZONES • %100 exemption from custom duties and other assorted duties • %100 exemption from corporate income tax for production companies • %100 exemption from the value added tax (VAT) and special consumption taxes • Goods can remain in Free Zones for an unlimited period; earnings and revenues generates in Free Zones can be freely transferred to any country, including Turkey, without any prior permission. • Goods in free circulation can be sent to Turkey or to EU countries from the Free Zones without any customs duty. Moreover, no customs duty is applied to goods of a third country origin at the entrance to the Free Zones or exit to third countries. • Companies are free to transfer profits from Free Zones abroad as well as to Turkey without restrictions.

18

Demography and Labor Force

1. DEMOGRAPHY

Turkey is located in the GMT+2 time zone, which allows it to communicate with countries from both west

and east in the same working day.

783,562.38 km2

Turkey’s 783,562.38 km2 of land is divided in 7 geographic regions, namely the Marmara, Aegean,

Mediterranean, South East Anatolian, East Anatolian, Central Anatolian and Black Sea. The country is

surrounded by 4 seas: Mediterranean, Aegean, Marmara and Black Sea.

70 MILLION

Turkey has a total population of 70 million, of which 24.6 million people are active in the labor force.

Demographic Structure

Average Age 29

0-14 years 24.9%

15-64 years 68.1%

65 years and over 6.9% (2007 est.)

Population growth rate

1.04% (2007 est.)

Life expectancy at birth

total population 72.88 years

male 70.43 years

female 75.46 years (2007 est.)

Source : TURKSTAT

19

Gender Ratios

At Birth 1.05 m/f

0 – 14 1.038 m/f

15 - 64 1.032 m/f

65 + 0.84 m/f

Total Population 1.019 m/f

Source : www.indexmundi.com

Population Age

0 – 14 24.9% (m 9.03 million / f 8.7 million)

15 - 64 68.1% (m 24.6 million / f 23.8 million)

65 + 6.9% (m 2.2 million / f 2.6 million)

Source : www.indexmundi.com

2. LABOR FORCE

Turkey offers investors a young, talented, motivated and skilled workforce composed of 24.6 million

people, approximately 35% of the total population. This skilled labor force is capable of meeting the

needs of the globally integrated and highly diversified Turkish economy.

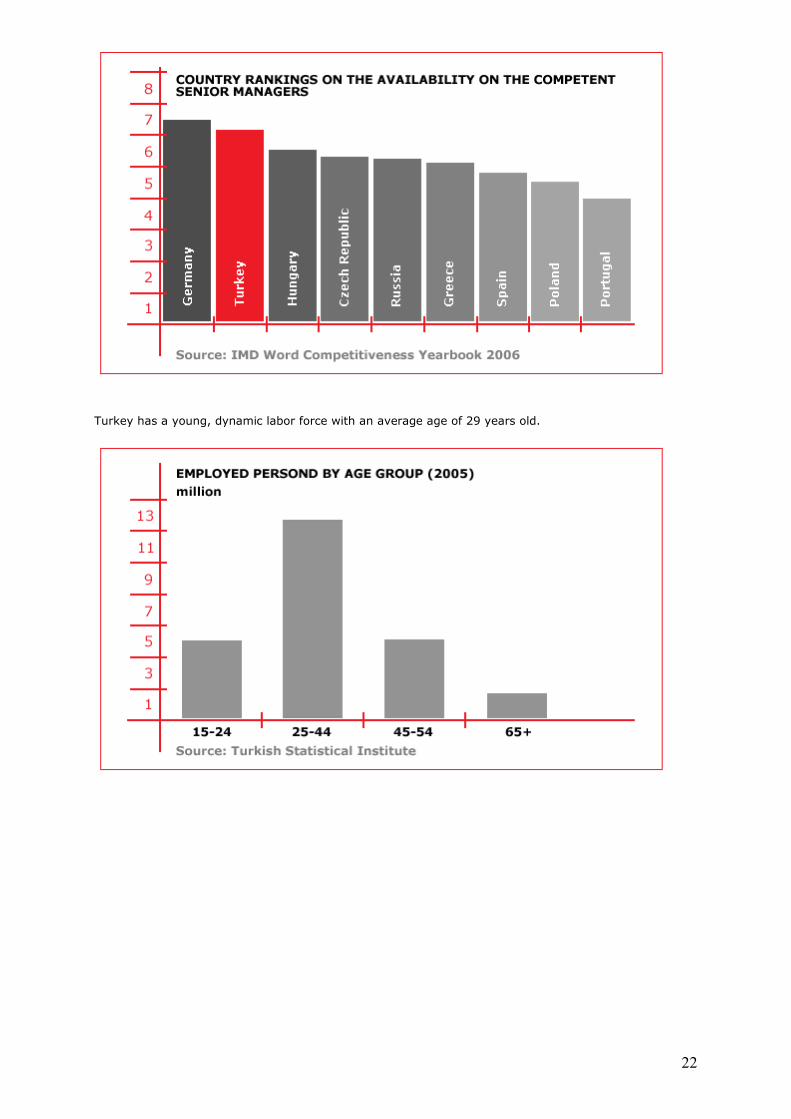

Turkey’s young population is an important source for labor force growth and has helped Turkey to rank

highest among its competitors .

20

The distribution of the workforce among many diverse sectors reflects the wealth of the opportunities

offered to investors.

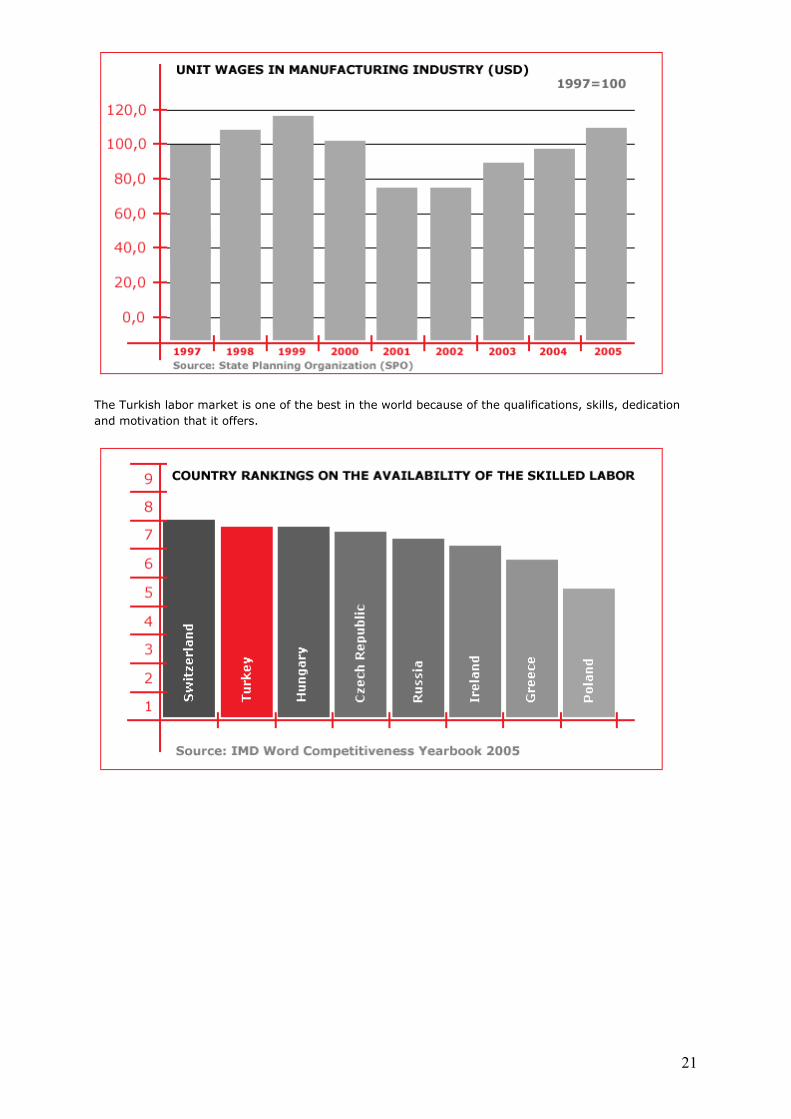

Labor costs in Turkey are very competitive and wages have remained quite stable. As it can be seen from

the table below, the unit wage manufacturing index is still below the 1997 level.

21

The Turkish labor market is one of the best in the world because of the qualifications, skills, dedication

and motivation that it offers.

22

Turkey has a young, dynamic labor force with an average age of 29 years old.

23

A strong work ethic is an important component of the Turkish work culture. The workplace as an

institution is cherished in Turkey because it allows individuals to utilize their skills and to work towards

self advancement. The labor force’s dedication to work is shown via Turkey’s high productivity, low

absenteeism and its top ranked position among working hour rates per year.

EDUCATION At the end of every academic year, nearly 400,000 graduates from 115 universities in Turkey join the labor market. Moreover, about 250,000 students graduate every year from 4,244 vocational and professional high schools; an additional 400,000 students graduate from 3,690 high schools in Turkey. All things considered, Turkey has a labor market which continues to improve dramatically every year, both in quantity and quality.

24

Business Environment

AUTONOMOUS BODIES

Autonomous Bodies are established in order to regulate and monitor different types of markets in

accordance with the requirements of a functioning market economy. The Bodies have both administrative

and fiscal independency. Some of the important entities in Turkey are the Competition Authority, the

Energy Market Regulation Authority, the Banking Regulation and Supervision Authority;

Telecommunication Authority and the Tobacco, Tobacco Products and Alcoholic Beverages Market

Regulation Board.

1. Competition Authority

Competition Authority (CA) is responsible for the full achievement of competition in the markets. Main

responsibilities and powers of the Competition Authority are:

a. To carry out, the examination, inquiry and investigation into activities and official transactions defined

in Competition Code upon application or upon its own initiative; to take the necessary measures to

expunge infringements of the Code; and to impose administrative regulations

b. To evaluate the requests for exemption and to grant an exemption certificate to the appropriate

agreements which may distort competition,

c. To constantly follow the markets to which exemption decisions and negative clearance certificates are

related, and to re-evaluate the applications of those in case changes are established in these markets or

in the positions of the parties

d. To evaluate mergers and acquisition activities and approve them according to determined criteria

www.rekabet.gov.tr

2. Energy Market Regulation Authority

Energy Market Regulation Authority (EMRA) regulates and controls the energy market. The Authority

ensures its independent duties in order to provide sufficient energy sources to consumers at high quality

and at low cost, in a reliable and environmentally friendly manner. The main responsibilities of Energy

Market Regulation Authority are:

a) To regulate and monitor the Electricity, Natural Gas, Petroleum and Liquid Petroleum Gas markets,

b) To establish a financially viable, stable and transparent energy market within a competitive

environment.

www.epdk.gov.tr

3. Banking Regulation and Supervision Agency

Banking Regulation and Supervision Agency (BRSA) safeguards the rights and benefits of depositors;

prevents all kinds of operations and transactions that may risk the orderly and safe operation of banks or

that may harm the economy; facilitates the efficient working of the credit system. The main goals of the

Agency are as follows:

25

a) To enhance the efficiency of the banking sector and its competitiveness

b) To maintain confidence in the banking sector

c) To minimize potential negative effects of banking sector on economy

d) To improve the stability of the banking sector

e) To protect the rights of depositors.

www.bddk.org.tr

4. Telecommunication Authority

Telecommunication Authority undertakes the regulation, the authorization, the reconciliation and the

supervision of activities within the telecommunication market. The main responsibilities of the Authority

are:

a) To prepare the required plans in the telecommunications area and present them to the Ministry of

Transportation,

b) To observe the developments in technology of the telecommunications area in cooperation with the

universities and private establishments,

c) To observe, control, examine and evaluate the telecommunication implementations,

d) To give opinions on the concession contracts to be signed for telecommunication services and/or

infrastructure,

e) To define the general criteria on price tariffs, contract provisions and technical issues to be

implemented for the users of the telecommunication services and infrastructure, and other operators for

their use of interconnections between the telecommunication networks,

f) To define and implement the performance standards considered as a basis for telecommunication

items,

g) To take the required measures to protect the consumer rights.

www.tk.gov.tr

5. Tobacco, Tobacco Products and Alcoholic Beverages Market Regulation Board

Tobacco, Tobacco Products and Alcoholic Beverages Market Regulation Board(TAMRB) establishes

regulatory and supervisory systems in areas dealing with tobacco, tobacco products, alcohol and

alcoholic drinks. The main responsibilities of the Board are as follows:

a) Regulation and supervision of tobacco production; granting of permission for the import of tobacco

seeds; issuing of authorization to trade in tobacco; regulating, monitoring, and supervising tobacco

producers on the basis of a written contract; and buying and selling of tobacco products by public

auctions

b) Granting permissions for setting up tobacco processing plants, controlling their production,

movements, handovers, and closures; monitoring of tobacco stocks and warehouses; and the granting of

compatibility permissions to tobacco warehouses

c) Supervision of companies operating within the sector

d) The granting of production permits, sales permits as well as granting permission to establish factories

aimed at producing tobacco products

e) Regulating the market in Ethyl Alcohol, Methanol, Distilled Alcoholic Drinks, and Fermented Alcoholic

Drinks; preparing national regulation policies; and harmonizing with the EU regulations

www.tapdk.gov.tr

6. Privatization Authority

Privatization Authority does not show the main characteristics of the above mentioned market regulating

autonomous agencies. However, as an independent administrative body fully responsible for privatization

in Turkey, it has a very high importance for the direct investors. The Privatization High Council and

Privatization Administration are responsible for carrying out privatization transactions in Turkey. The

main responsibilities of the Authority are:

a) To decide which enterprises meet the criteria for inclusion in the privatization process,

b) To prepare enterprises for privatization in both fiscal and legal matters,

c) To determine a timeline for the completion of privatization procedures,

d) To prepare the privatization process of enterprises which have been deemed suitable,

e) To decide on the privatization methods required for selected enterprises,

f) To decide on scaling down methods for enterprises that are already in the process of privatization,

26

g) To conclude the activities of enterprises either temporarily or permanently, which are already in the

process of privatization,

h) To make a decision about the possible liquidation of companies in the privatization process.

www.oib.gov.tr

ENVIRONMENTAL STANDARDS

Turkey's policies regarding environmental protection and development are based on the harmonization of

policies and solutions with both EU and international standards, reinforcement of existing legislation,

improvement of environmental management, prevention of pollution and increasing awareness of

environmental issues.

Turkey participates in 76 international agreements concerning environmental protection and

management as well as 25 bilateral agreements.

On January 28, 2003, the Republic of Turkey ratified an act between Turkey and European Union

countries regarding Turkey's participation in the European Environment Agency and the European

Information and Observation Network. Furthermore, most of the legislation on the environment has

already been harmonized with the exception of certain legislation that is at the last stage of full

harmonization with the EU law.

TURKISH LABOR MARKET

Turkey has been a member of the International Labor Organization (ILO) since 1932. Since it became a

member, Turkey has approved 56 ILO Agreements. Moreover, Turkey has signed Bilateral Social Security

Agreements with 22 countries.

According to the Turkish Constitution, the State is responsible for creating a suitable environment to

prevent unemployment and to provide a peaceful labor environment.

The minimum wage is to be determined annually by the Ministry of Labor and Social Security. According

to the Social Insurance Code, the social security services for employees are handled by the Social

Insurance Agency. Recently, the Social Security Agency has been reorganized with the ultimate goals of

consolidating all Social Security and Social Support Organizations into one single body; standardizing

the regulations and principles of all social security institutions; and keeping track of the fiscal position

and financial records of the institutions.

Is-Kur, a governmental body, is responsible for the domestic and international matching of jobs with

employees; carrying out workforce planning; as well as safeguarding and developing employment. There

is a large amount of private employment agencies in the market working effectively with employees and

employers. It is also possible to find employment and employees via private employment agencies.

EMPLOYMENT OF EXPATRIATES

1. How to get a work permit in Turkey

Expatriates are required to obtain a work permit before they start to work dependently or independently

in Turkey.

The Ministry of Labor and Social Security is responsible for:

• Processing the applications of companies that wish to employ expatriates

• Issuing work permits for expatriates

• Extending and/or restricting the term of work permits in accordance with the relevant legislation

27

Applications for work permits can be made both inside and outside of Turkey:

• Expatriates residing outside of Turkey need to apply to the relevant Turkish Consulate in either their

residential country or their country of citizenship

• Expatriates with valid residence permits (a minimum 6 month period, with the exception of residence

permits for educational purposes) can apply directly to the Ministry of Labor and Social Security

Other legal procedures regarding work permits are as follows:

• A work permit is valid only when a work visa and/or residence permit is also granted

• Applications are processed and answered within a fixed 90 day period by the Ministry. For key

personnel of large foreign direct investors, this period is at most 15 days

2. Main categories of work permits

Work permits are divided into 4 categories:

• Dependent work permits for a definite period of time

• Dependent work permits for an indefinite period of time

• Independent work permits

• Exceptional work permits

Exceptional work permits can be granted under certain conditions stipulated in Law. This type of work

permit can be issued to an expatriate living in Turkey who is married to a Turkish citizen, to one who will

temporarily come to Turkey with the aim of scientific and/or cultural activities, or to one employed by

ministries, public authorities or other similar organizations.

RESEARCH AND DEVELOPMENT ACTIVITIES

1. TUBITAK

In Turkey, public institutions and universities play an important role in R&D activities. The Scientific and

Technological Research Council of Turkey is the public agency in charge of promoting, developing,

organizing, conducting and coordinating research and development in different fields of natural sciences.

This research is in line with the national targets for economical development and technical progress. The

Council also makes important contributions to the relations between universities and industries.

The institution provides certain incentives in order to increase the scientific and technological

competitiveness of Turkey; develop methods to rapidly transform scientific research into technological

innovations; and provide an active contribution from the private sector into research and development.

www.tubitak.gov.tr

2. TTGV

The Turkish Technology Development Foundation was set up to raise the industrial sector's awareness of

R&D and to support technological development projects in the Turkish Industry through the funds

provided by the Under Secretariat of Treasury from the resources of the World Bank. This Foundation

continues its activities as a successful example of Private and Public Sector cooperation. In this respect,

the Foundation promotes the R&D activities of the industrial sector; contributes to the creation of the

necessary infrastructure for technology to produce a commercial and marketable product, system or

service; provides financial support; and undertakes studies aimed at improving the legislative and

institutional framework for R&D.

www.ttgv.org.tr/

28

3. KOSGEB Another institution, which conducts R&D research in Turkey, is the Small and Medium-sized Industry Development Organization (SMSIDO - KOSGEB). KOSGEB is focused on helping small and medium-sized industrial companies to adapt quickly to technological innovations; increasing their competitiveness and contributions to the economy; as well as improving their efficiency. www.kosgeb.gov.tr

29

Infrastructure

ENERGY INFRASTRUCTURE

1. ENERGY STRATEGY:

• Turkey’s strategy in the energy sector is to supply security and higher service quality to the consumer.

• In addition to unused energy resources such as hydrologic and lignite, Turkey’s renewable energy

potential is a great opportunity for investors. The new law which supports renewable energy encourages

these types of investment and makes them even more attractive.

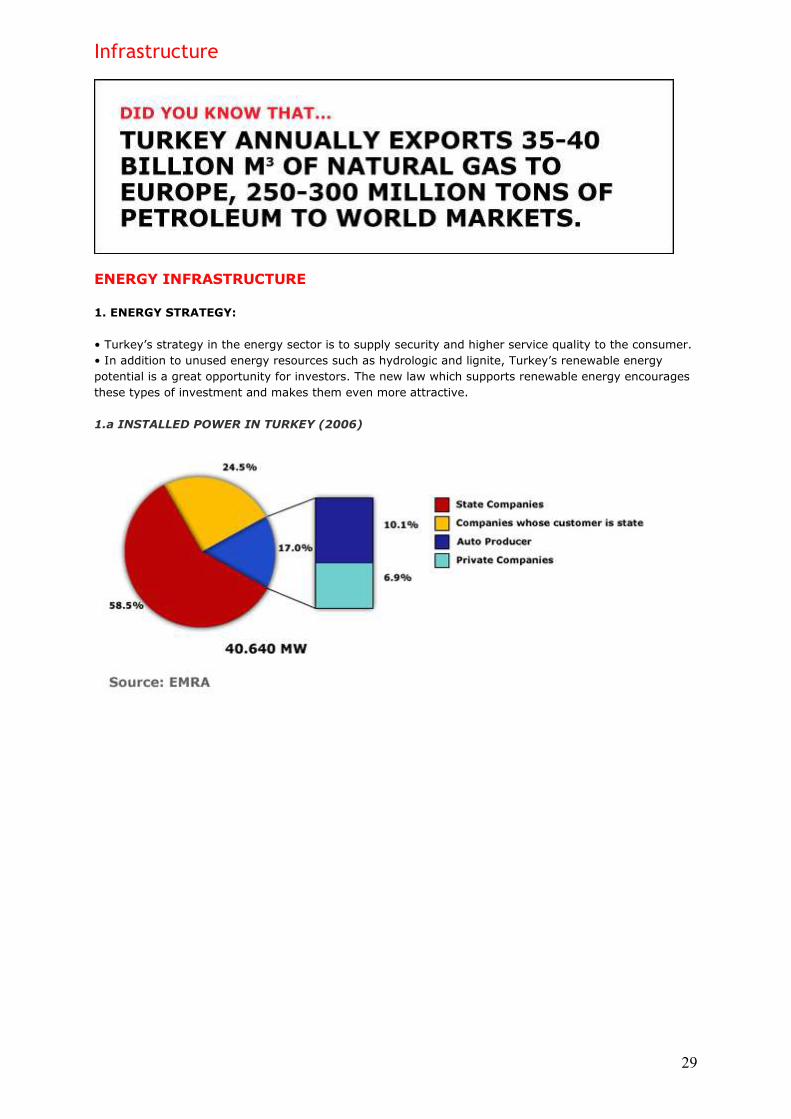

1.a INSTALLED POWER IN TURKEY (2006)

30

1.b RESOURCES USED TO PRODUCING ENERGY (2006)

1.c COMPARISON OF ELECTRICITY PRICES FOR INDUSTRIAL USERS (2006)

Energy prices in Turkey, presently at 8.32 €¢/kWh, are very competitive with respect to the global

market.

(Source: EMRA)

31

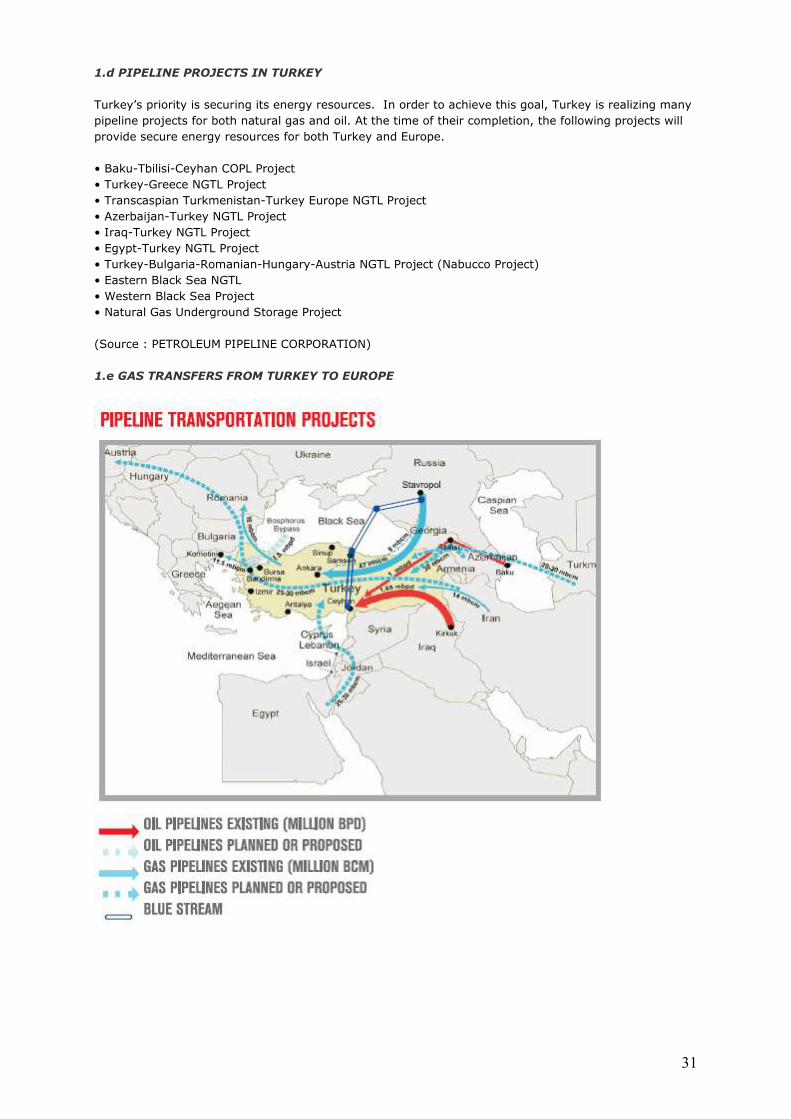

1.d PIPELINE PROJECTS IN TURKEY

Turkey’s priority is securing its energy resources. In order to achieve this goal, Turkey is realizing many

pipeline projects for both natural gas and oil. At the time of their completion, the following projects will

provide secure energy resources for both Turkey and Europe.

• Baku-Tbilisi-Ceyhan COPL Project

• Turkey-Greece NGTL Project

• Transcaspian Turkmenistan-Turkey Europe NGTL Project

• Azerbaijan-Turkey NGTL Project

• Iraq-Turkey NGTL Project

• Egypt-Turkey NGTL Project

• Turkey-Bulgaria-Romanian-Hungary-Austria NGTL Project (Nabucco Project)

• Eastern Black Sea NGTL

• Western Black Sea Project

• Natural Gas Underground Storage Project

(Source : PETROLEUM PIPELINE CORPORATION)

1.e GAS TRANSFERS FROM TURKEY TO EUROPE

32

2. Telecommunications Infrastructure

Telecommunications Infrastructure - 2006

Mobile Telephone Subscribers 54.7 mil

Public Telephone Switched Users 18.8 mil

Internet Users 18.0 mil

Broadband Subscribers 3.5 mil

Source: Telecommunications Authority - Turk Telekom A.Ş

The Telecommunication sector in Turkey has evolved considerably in recent years and began with the

privatization of 55% of Turk Telekom stock. The diversification of services within the telecommunication

sector via mobile phones and the internet has created new economies which are attractive as areas for

further investment.

3. Transportation Infrastructure

The proximity Turkey has to major markets such as CIS, the Middle East and North Africa means that 1.2

billion consumers can be easily reached.

Turkey’s advantages also include its logistics industry which has developed significantly since its entry

into the EU Customs Union. Its geographic, physical and corporate infrastructure is one of the key

attractions for potential investors.

Transportation Infrastructure

Number of Passengers

Internal Flights 28.8 mil

External Flights 32.8 mil

Number of Airports

Rail Way 10.948 km

Sea Way 243.5 million tons/year

Source: Ministry of Transportation - 2006

Turkey meets all the requirements for the efficient and cost effective shipment of goods with its high performance structure, reliable and on-time transportation services and its strategic location in the region.

33

Quantities by Transportation Type

DETAILED QUANTITIES BY TRANSPORTATION TYPE

2004 2005 2006

QUANTITY (tons) VALUE $

QUANTITY (tons) VALUE $

QUANTITY (tons) VALUE $

000. TON % 000. $ % 000. TON % 000. $ % 000. TON % 000. $ %

SEA TRANSPORT 150.453,0 86,4 80.876.384,0 50,4 159.221,0 86,1 102.167.289,0 53,8 178.079,0 87,6 122.747.456,0 55,3

RAILWAY TRANSPORT 2,1 1,2 1.845.728,0 1,1 2.168,0 1,2 2.573.457,0 1,4 2.162,0 1,1 3.086.501,0 1,4

ROAD TRANSPORT 19.790,0 11,4 58.234.461,0 36,3 21.845,0 11,8 60.271.018,0 31,8 21.165,0 10,4 67.415.308,0 30,4

AIRWAY TRANSPORT 237,0 0,1 16.201.418,0 10,1 275,0 0,1 17.050.735,0 9,0 275,0 0,1 18.332.136,0 8,3

OTHERS 1.648,0 0,9 3.466.590,0 2,2 1.431,0 0,8 7.719.220,0 4,1 1.705,0 0,8 10.362.749,0 4,7

TOTAL 172.130,1 100,0 160.624.581,0 100,0 184.940,0 100,0 189.781.719,0 100,0 203.386,0 100,0 221.944.150,0 100,0

Source. TURKSTAT

The national road and railway network are completely integrated into the Eurasian infrastructure. The Silk Road connection project will ensure a uniform railway connection between Europe, the Middle East, the Turkic Republics and the Far East throughout Turkey. Regular truck transportation and Ro-Ro ferry routes are continuing to increase logistic services capacity.

34

Economic Outlook

Fiscal discipline and a tight fiscal policy continue to be the main pillars of Turkey’s economic program and have contributed a great deal to disinflation as well as to a strong growth performance. In addition to the sound macroeconomic policies, Turkey has implemented a comprehensive and far-reaching structural reform agenda. Compared with the experiences of other countries, Turkey’s success has been remarkable primarily because of the speed with which it has conducted structural and institutional changes. Indeed, Turkey has made large strides in restructuring its financial sector as well as improving public sector governance and its business environment.

1. MACROECONOMIC INDICATORS

The Turkish economy has had a steady growth rate for the last 20 quarters. GNP and GNP per capita

figures highlight the strength and the stability of the national economy as well as its integration to

macroeconomic global trends.

GNP (Current

price in billions

of USD)

GNP Per Capita

(Current Price in

USD)

Growth

(Real)

(%)

2007 ( I. Period) 91.8 6.7

2006 399.7 5,477 6.0

2005 360.9 5,008 7.6

2004 299.5 4,172 9.9

2003 239.2 3,383 5.9

2002 180.9 2,598 7.9

2001 145.7 2,123 -9.5

2000 200.0 2,965 6.3

1999 185.3 2,879 -6.1

1998 206.5 3,255 3.9

1997 192.4 3,079 8.3

Source: Turkish Statistical Institution (TURKSTAT)

35

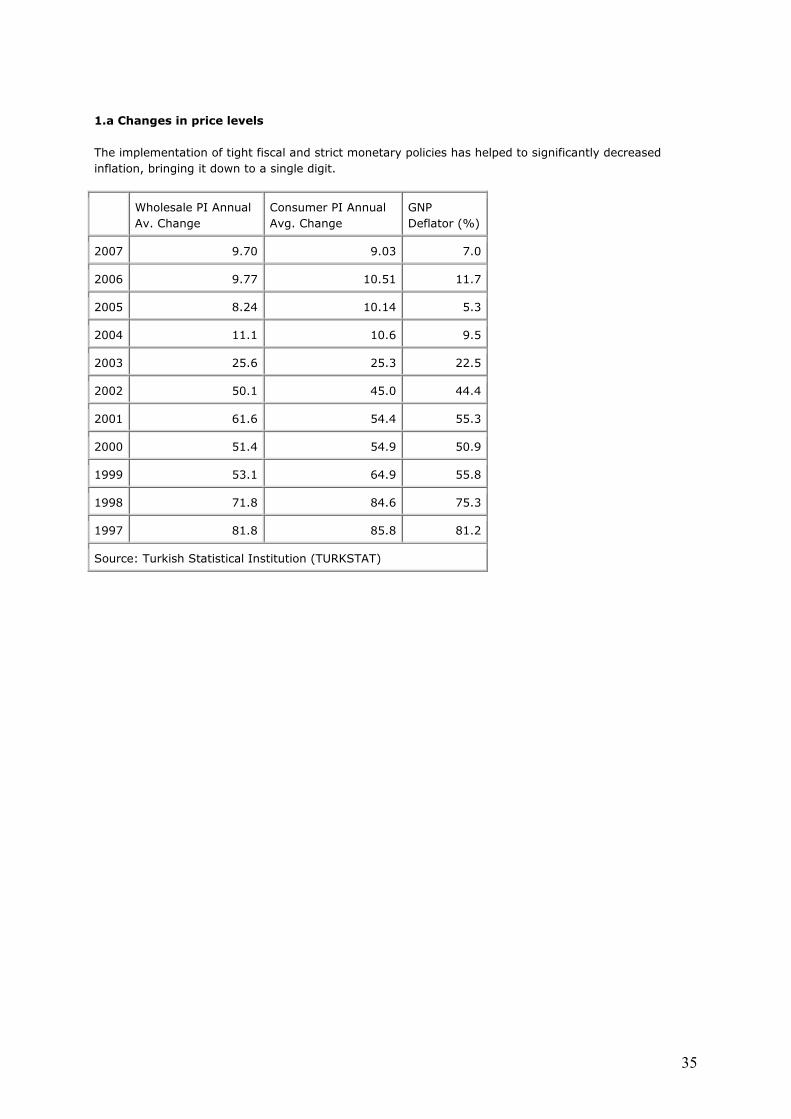

1.a Changes in price levels

The implementation of tight fiscal and strict monetary policies has helped to significantly decreased

inflation, bringing it down to a single digit.

Wholesale PI Annual

Av. Change

Consumer PI Annual

Avg. Change

GNP

Deflator (%)

2007 9.70 9.03 7.0

2006 9.77 10.51 11.7

2005 8.24 10.14 5.3

2004 11.1 10.6 9.5

2003 25.6 25.3 22.5

2002 50.1 45.0 44.4

2001 61.6 54.4 55.3

2000 51.4 54.9 50.9

1999 53.1 64.9 55.8

1998 71.8 84.6 75.3

1997 81.8 85.8 81.2

Source: Turkish Statistical Institution (TURKSTAT)

36

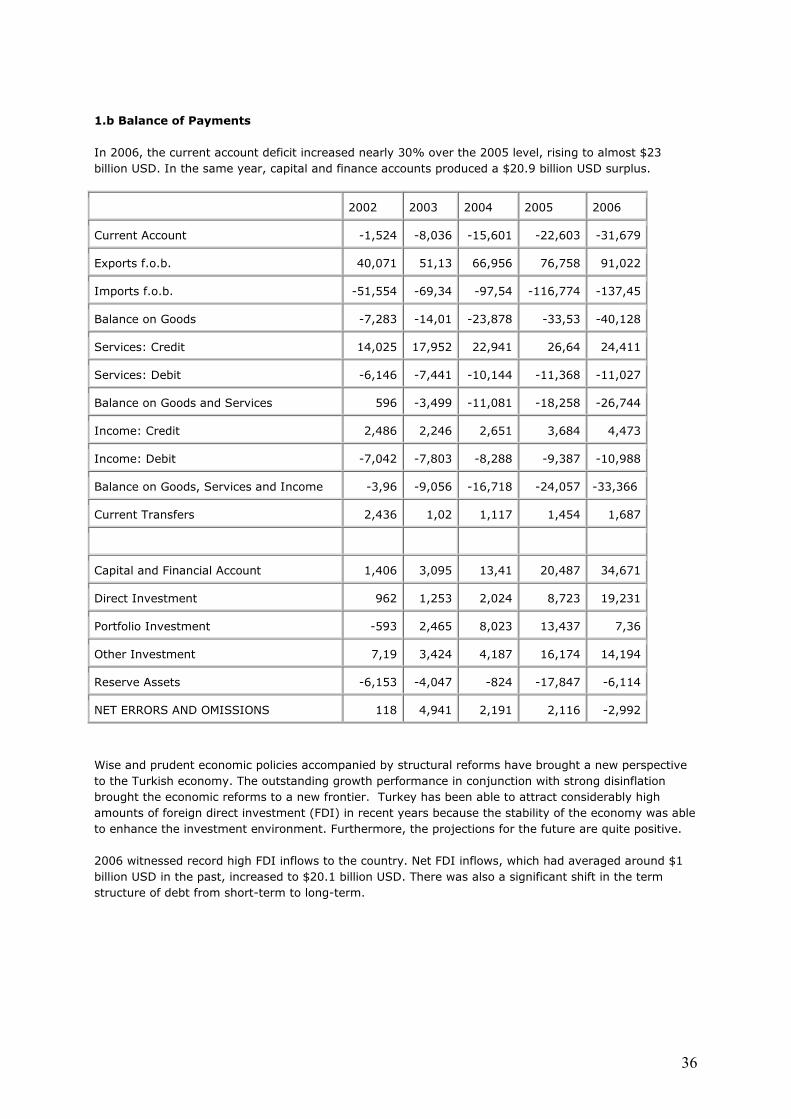

1.b Balance of Payments

In 2006, the current account deficit increased nearly 30% over the 2005 level, rising to almost $23

billion USD. In the same year, capital and finance accounts produced a $20.9 billion USD surplus.

2002 2003 2004 2005 2006

Current Account -1,524 -8,036 -15,601 -22,603 -31,679

Exports f.o.b. 40,071 51,13 66,956 76,758 91,022

Imports f.o.b. -51,554 -69,34 -97,54 -116,774 -137,45

Balance on Goods -7,283 -14,01 -23,878 -33,53 -40,128

Services: Credit 14,025 17,952 22,941 26,64 24,411

Services: Debit -6,146 -7,441 -10,144 -11,368 -11,027

Balance on Goods and Services 596 -3,499 -11,081 -18,258 -26,744

Income: Credit 2,486 2,246 2,651 3,684 4,473

Income: Debit -7,042 -7,803 -8,288 -9,387 -10,988

Balance on Goods, Services and Income -3,96 -9,056 -16,718 -24,057 -33,366

Current Transfers 2,436 1,02 1,117 1,454 1,687

Capital and Financial Account 1,406 3,095 13,41 20,487 34,671

Direct Investment 962 1,253 2,024 8,723 19,231

Portfolio Investment -593 2,465 8,023 13,437 7,36

Other Investment 7,19 3,424 4,187 16,174 14,194

Reserve Assets -6,153 -4,047 -824 -17,847 -6,114

NET ERRORS AND OMISSIONS 118 4,941 2,191 2,116 -2,992

Wise and prudent economic policies accompanied by structural reforms have brought a new perspective

to the Turkish economy. The outstanding growth performance in conjunction with strong disinflation

brought the economic reforms to a new frontier. Turkey has been able to attract considerably high

amounts of foreign direct investment (FDI) in recent years because the stability of the economy was able

to enhance the investment environment. Furthermore, the projections for the future are quite positive.

2006 witnessed record high FDI inflows to the country. Net FDI inflows, which had averaged around $1

billion USD in the past, increased to $20.1 billion USD. There was also a significant shift in the term

structure of debt from short-term to long-term.

37

A Sustainable Growth Path

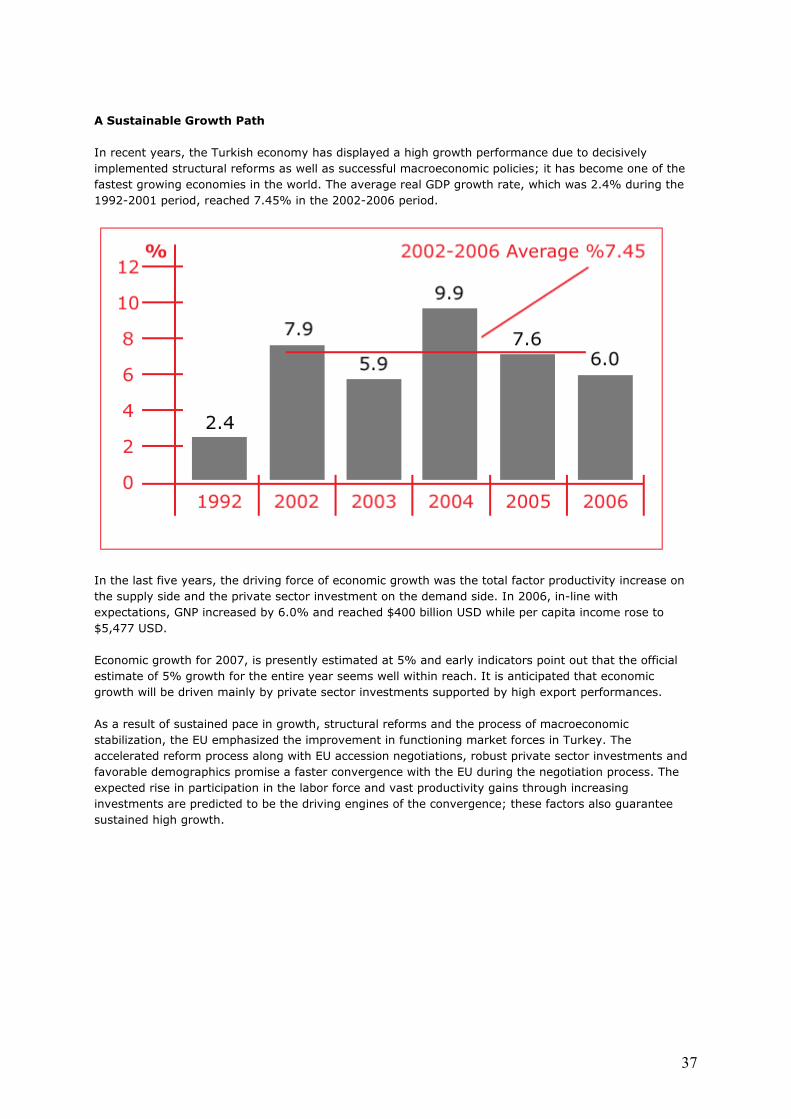

In recent years, the Turkish economy has displayed a high growth performance due to decisively

implemented structural reforms as well as successful macroeconomic policies; it has become one of the

fastest growing economies in the world. The average real GDP growth rate, which was 2.4% during the

1992-2001 period, reached 7.45% in the 2002-2006 period.

In the last five years, the driving force of economic growth was the total factor productivity increase on

the supply side and the private sector investment on the demand side. In 2006, in-line with

expectations, GNP increased by 6.0% and reached $400 billion USD while per capita income rose to

$5,477 USD.

Economic growth for 2007, is presently estimated at 5% and early indicators point out that the official

estimate of 5% growth for the entire year seems well within reach. It is anticipated that economic

growth will be driven mainly by private sector investments supported by high export performances.

As a result of sustained pace in growth, structural reforms and the process of macroeconomic

stabilization, the EU emphasized the improvement in functioning market forces in Turkey. The

accelerated reform process along with EU accession negotiations, robust private sector investments and

favorable demographics promise a faster convergence with the EU during the negotiation process. The

expected rise in participation in the labor force and vast productivity gains through increasing

investments are predicted to be the driving engines of the convergence; these factors also guarantee

sustained high growth.

38

Declining Inflation...

One of the most striking aspects of the recent performance of the Turkish economy has been the

substantial decline in inflation in a strong growth environment with soaring energy prices. Annual

inflation rate declined from a level near 70% at the beginning of 2002 to 7.5% in October 2005, the

lowest level in 35 years. To further support disinflation, the Central Bank of Turkey shifted to formal

inflation targeting in 2006. The 2007 end-year CPI target was determined at 5% with a 2 percentage

point uncertainty range around this target.

Prudent Fiscal Policy

Fiscal discipline continues to be the cornerstone of the macroeconomic performance of the Turkish

economy. By sustaining historically high levels of total public sector primary surpluses over GNP,

averaging more than 6.5% annually for the past four years, Turkey reduced its debt stock and positively

affected the expectations of the market towards a stable economic growth environment and low inflation

rate.

39

Looking at External Accounts...

The 2006 current account deficit was realized at 7.9% of GNP. The current account deficit was easily

financed in 2006 and the share of long term and non-debt creating capital inflows demonstrated an

increasing trend. The FDI inflows reached $20.1 billion USD in 2006, the highest ever in Turkish

economic history. The receipts from FDI are expected to continue in future years with the acceleration of

the EU accession process and efforts to improve the investment environment.

The current account deficit in 2007 is projected to decline to about 7% of GNP mainly due to high export

performance, privatization receipts, and rising FDI.

40

In Conclusion

Thanks to prudent fiscal and monetary policies as well as comprehensive structural reforms, economic

fundamentals and balance sheets have strengthened considerably in recent years, making the economy

much more resilient to adverse shocks. In order to move forward, Turkey still faces important

challenges. In this respect, Turkey is determined to continue and to accelerate the structural reforms on

all fronts and transform into a well developed country in every aspect.

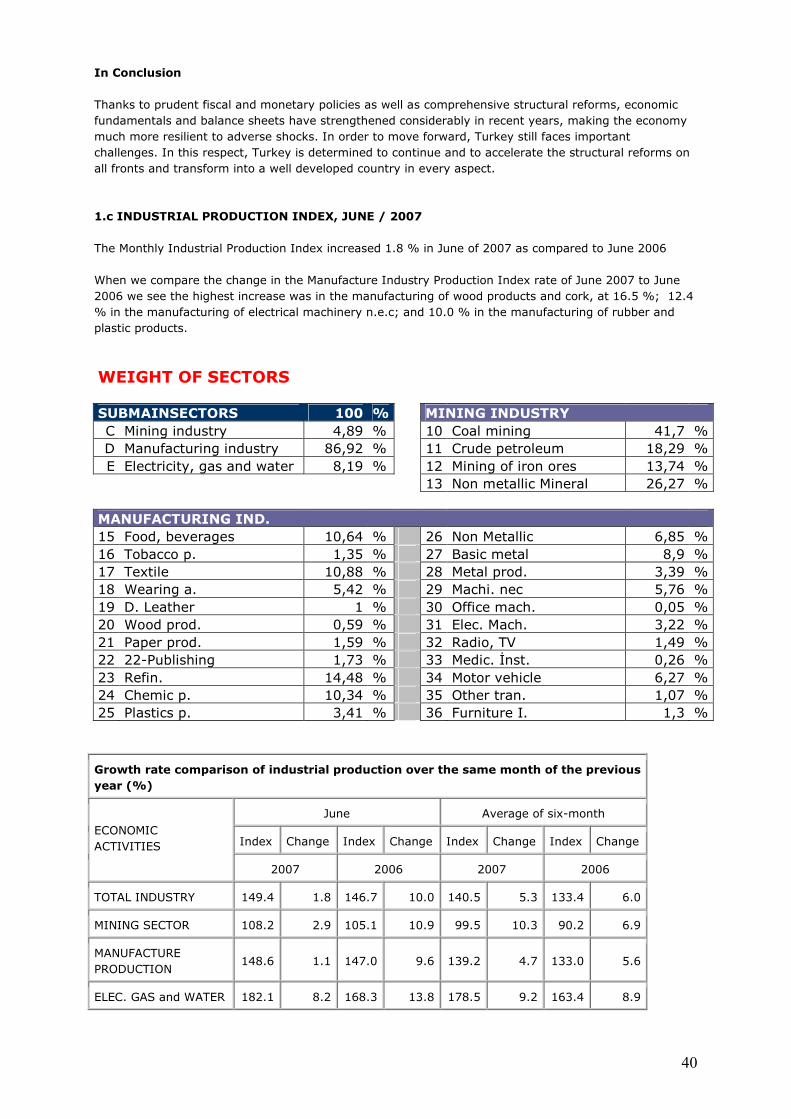

1.c INDUSTRIAL PRODUCTION INDEX, JUNE / 2007

The Monthly Industrial Production Index increased 1.8 % in June of 2007 as compared to June 2006

When we compare the change in the Manufacture Industry Production Index rate of June 2007 to June

2006 we see the highest increase was in the manufacturing of wood products and cork, at 16.5 %; 12.4

% in the manufacturing of electrical machinery n.e.c; and 10.0 % in the manufacturing of rubber and

plastic products.

WEIGHT OF SECTORS SUBMAINSECTORS 100 % MINING INDUSTRY

C Mining industry 4,89 % 10 Coal mining 41,7 % D Manufacturing industry 86,92 % 11 Crude petroleum 18,29 % E Electricity, gas and water 8,19 % 12 Mining of iron ores 13,74 %

13 Non metallic Mineral 26,27 % MANUFACTURING IND.

15 Food, beverages 10,64 % 26 Non Metallic 6,85 % 16 Tobacco p. 1,35 % 27 Basic metal 8,9 % 17 Textile 10,88 % 28 Metal prod. 3,39 % 18 Wearing a. 5,42 % 29 Machi. nec 5,76 % 19 D. Leather 1 % 30 Office mach. 0,05 % 20 Wood prod. 0,59 % 31 Elec. Mach. 3,22 % 21 Paper prod. 1,59 % 32 Radio, TV 1,49 % 22 22-Publishing 1,73 % 33 Medic. Đnst. 0,26 % 23 Refin. 14,48 % 34 Motor vehicle 6,27 % 24 Chemic p. 10,34 % 35 Other tran. 1,07 % 25 Plastics p. 3,41 % 36 Furniture I. 1,3 %

Growth rate comparison of industrial production over the same month of the previous

year (%)

June Average of six-month

Index Change Index Change Index Change Index Change ECONOMIC

ACTIVITIES

2007 2006 2007 2006

TOTAL INDUSTRY 149.4 1.8 146.7 10.0 140.5 5.3 133.4 6.0

MINING SECTOR 108.2 2.9 105.1 10.9 99.5 10.3 90.2 6.9

MANUFACTURE

PRODUCTION 148.6 1.1 147.0 9.6 139.2 4.7 133.0 5.6

ELEC. GAS and WATER 182.1 8.2 168.3 13.8 178.5 9.2 163.4 8.9

41

2.FDI IN TURKEY

2.a. Turkey is the 13th most attractive country in the world for FDI

2.b. International Direct Investment (Inflows)

(Million $of USD)

Jan.-Sept.

2000 2001 2002 2003 2004 2005 2006

2006 2007

International Direct

Investment Total

(Net)

982 3,352 1,133 1,752 2,883 10,029 29,968 13,127 15,334

International Direct

Investment 982 3,352 1,133 754 1,542 8,188 17,046 10,798 13,156

Equity Investment

(Net) 982 3,352 617 737 1,191 8,137 17,038 10,783 12,862

Inflows 1,707 3,374 622 745 1,291 8,538 17,695 11,345 12,921

Liquidation

Outflows -725 -22 -5 -8 -100 -401 -657 -562 -59

Intra Company

Loans* -- -- 516 17 351 51 8 15 294

Real Estate (Net) -- -- -- 998 1,343 1,841 2,922 2,329 2,178

*Loans which companies with foreign capital take from foreign partners

Provisional Data

Source: Central Bank of the Republic of Turkey

42

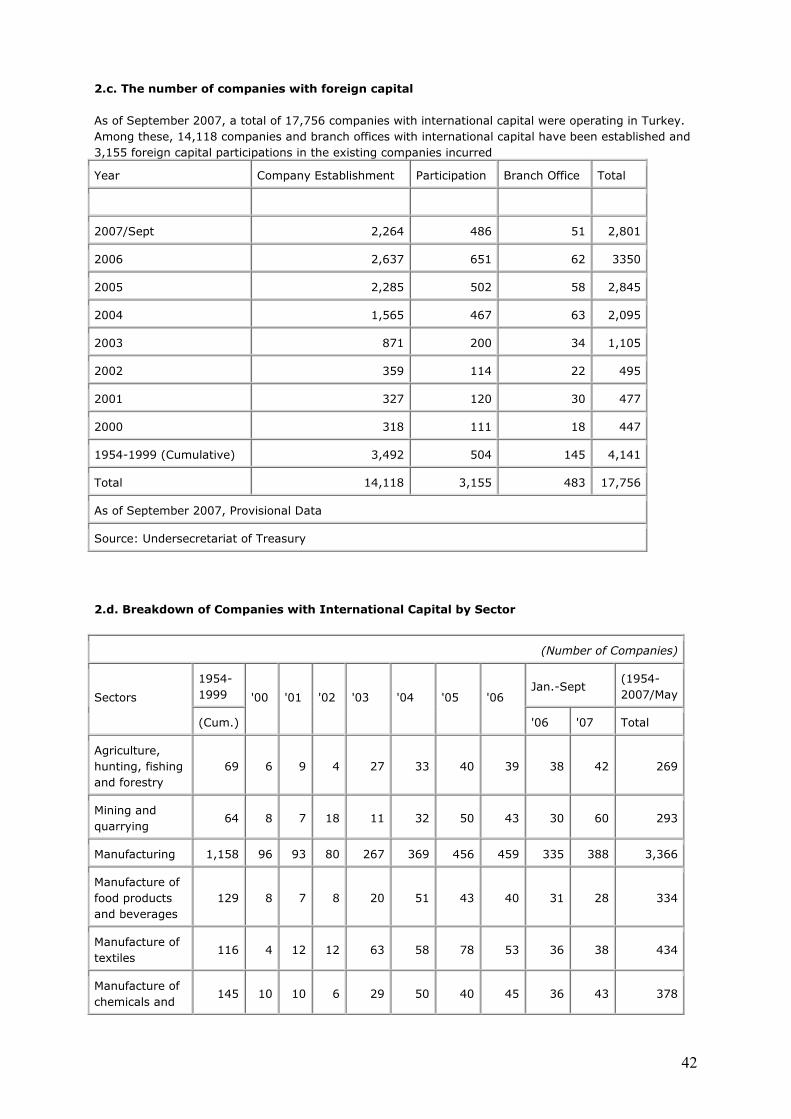

2.c. The number of companies with foreign capital

As of September 2007, a total of 17,756 companies with international capital were operating in Turkey.

Among these, 14,118 companies and branch offices with international capital have been established and

3,155 foreign capital participations in the existing companies incurred

Year Company Establishment Participation Branch Office Total

2007/Sept 2,264 486 51 2,801

2006 2,637 651 62 3350

2005 2,285 502 58 2,845

2004 1,565 467 63 2,095

2003 871 200 34 1,105

2002 359 114 22 495

2001 327 120 30 477

2000 318 111 18 447

1954-1999 (Cumulative) 3,492 504 145 4,141

Total 14,118 3,155 483 17,756

As of September 2007, Provisional Data

Source: Undersecretariat of Treasury

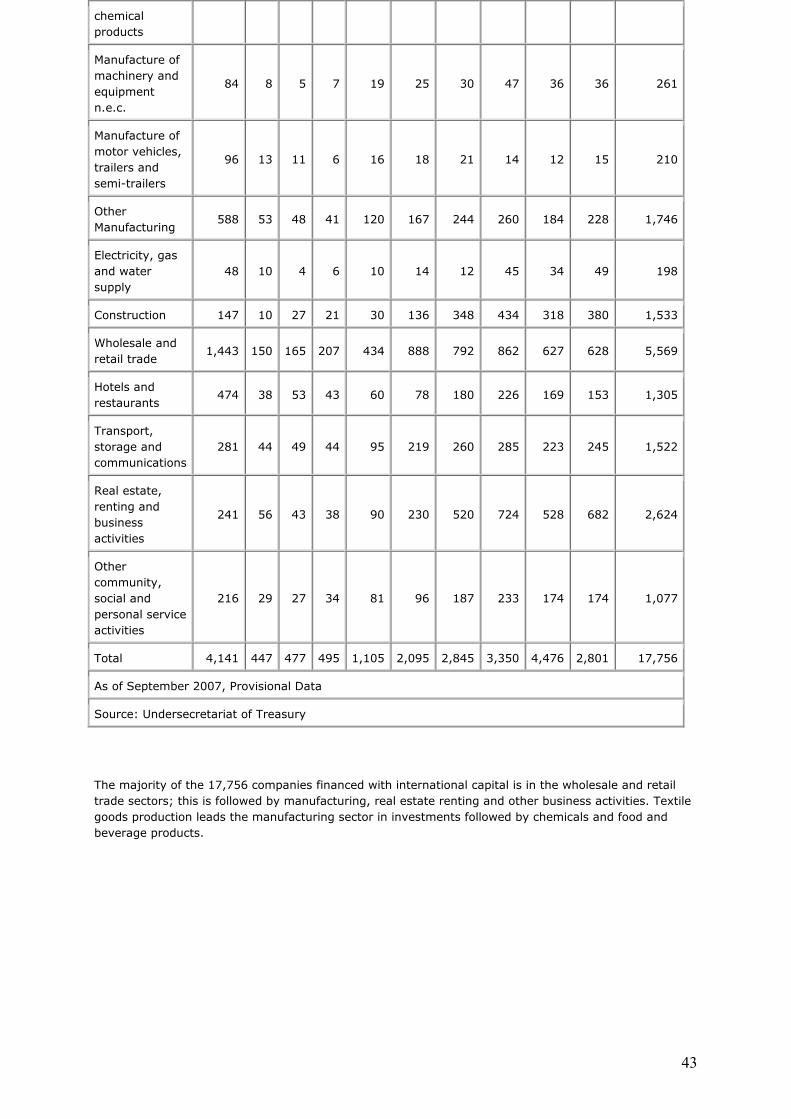

2.d. Breakdown of Companies with International Capital by Sector

(Number of Companies)

1954-

1999 Jan.-Sept

(1954-

2007/May Sectors

(Cum.)

'00 '01 '02 '03 '04 '05 '06

'06 '07 Total

Agriculture,

hunting, fishing

and forestry

69 6 9 4 27 33 40 39 38 42 269

Mining and

quarrying 64 8 7 18 11 32 50 43 30 60 293

Manufacturing 1,158 96 93 80 267 369 456 459 335 388 3,366

Manufacture of

food products

and beverages

129 8 7 8 20 51 43 40 31 28 334

Manufacture of

textiles 116 4 12 12 63 58 78 53 36 38 434

Manufacture of

chemicals and 145 10 10 6 29 50 40 45 36 43 378

43

chemical

products

Manufacture of

machinery and

equipment

n.e.c.

84 8 5 7 19 25 30 47 36 36 261

Manufacture of

motor vehicles,

trailers and

semi-trailers

96 13 11 6 16 18 21 14 12 15 210

Other

Manufacturing 588 53 48 41 120 167 244 260 184 228 1,746

Electricity, gas

and water

supply

48 10 4 6 10 14 12 45 34 49 198

Construction 147 10 27 21 30 136 348 434 318 380 1,533

Wholesale and

retail trade 1,443 150 165 207 434 888 792 862 627 628 5,569

Hotels and

restaurants 474 38 53 43 60 78 180 226 169 153 1,305

Transport,

storage and

communications

281 44 49 44 95 219 260 285 223 245 1,522

Real estate,

renting and

business

activities

241 56 43 38 90 230 520 724 528 682 2,624

Other

community,

social and

personal service

activities

216 29 27 34 81 96 187 233 174 174 1,077

Total 4,141 447 477 495 1,105 2,095 2,845 3,350 4,476 2,801 17,756

As of September 2007, Provisional Data

Source: Undersecretariat of Treasury

The majority of the 17,756 companies financed with international capital is in the wholesale and retail

trade sectors; this is followed by manufacturing, real estate renting and other business activities. Textile

goods production leads the manufacturing sector in investments followed by chemicals and food and

beverage products.

44

2.e. International Direct Investment Inflow by Sector

During last 5 years, the highest FDI attracting sectors are manufacturing, financial services and energy

fields

(Million $)

Jan.-May Sectors 2002 2003 2004 2005 2006

2006 2007

Agriculture, hunting and forestry -- 1 4 5 5 -- --

Fishing -- -- 2 2 1 -- 3

Mining and quarrying 2 14 75 40 122 76 318

Manufacturing 110 448 214 788 1,868 1,214 2,810

Manufacture of food products and

beverages 14 249 78 68 609 580 255

Manufacture of textiles 10 8 14 183 26 14 187

Manufacture of chemicals and

chemical products 9 9 39 174 602 305 896

Manufacture of machinery and

equipment n.e.c. 13 17 8 13 54 52 24

Office machinery and computers 2 4 2 13 53 41 76

Manufacture of motor vehicles,

trailers and semi-trailers 33 145 35 106 63 46 66

Other Manufacturing 19 14 38 227 461 176 1,306

Electricity, gas and water supply 68 86 69 4 112 111 537

Construction 3 8 23 80 278 161 246

Wholesale and retail trade 89 92 103 68 1,167 1,139 111

Hotels and restaurants 0 4 1 42 23 22 12

Transport, storage and

communications 1 2 639 3,285 6,700 4,887 504

Financial intermediation 260 51 69 4,016 6,957 3,423 7,870

Real estate, renting and business

activities 0 6 3 29 93 58 481

Health and social work 5 23 53 74 265 180 17

Other community, social and personal

service activities 84 10 36 86 104 84 12

Total 622 745 1,291 8,536 17,695 11,345 12,921

Provisional Data Source: Central Bank of the Republic of Turkey

45

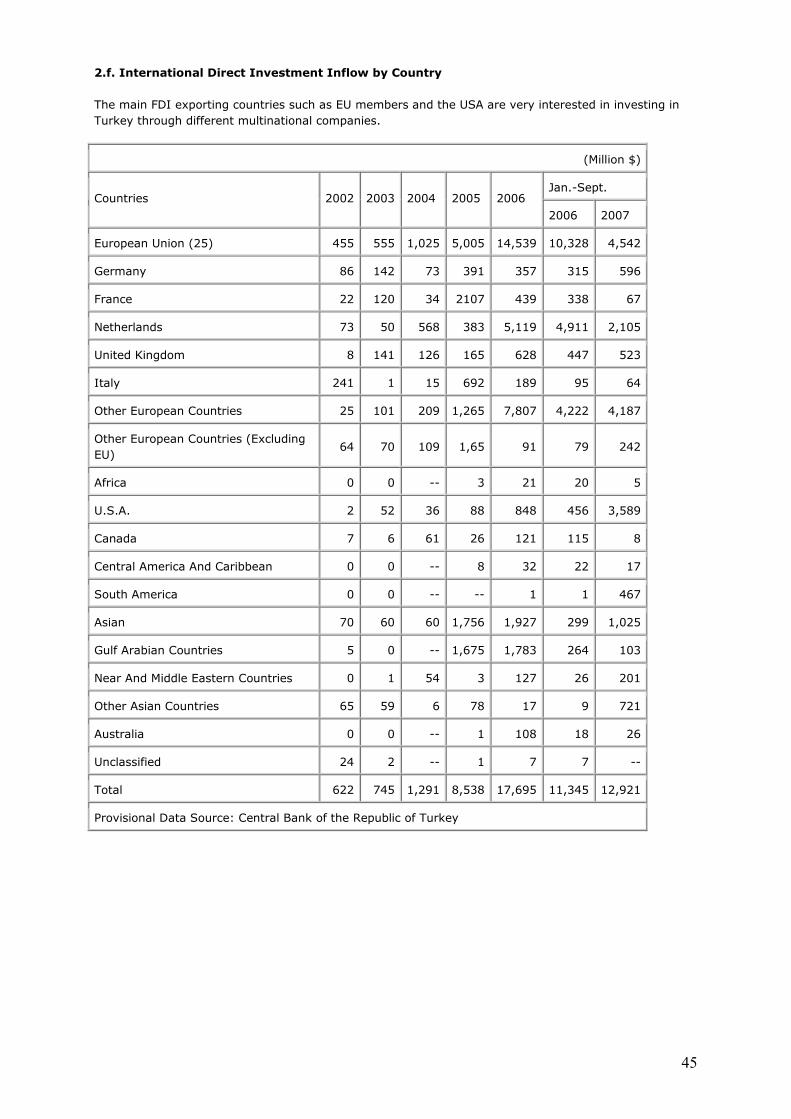

2.f. International Direct Investment Inflow by Country

The main FDI exporting countries such as EU members and the USA are very interested in investing in

Turkey through different multinational companies.

(Million $)

Jan.-Sept. Countries 2002 2003 2004 2005 2006

2006 2007

European Union (25) 455 555 1,025 5,005 14,539 10,328 4,542

Germany 86 142 73 391 357 315 596

France 22 120 34 2107 439 338 67

Netherlands 73 50 568 383 5,119 4,911 2,105

United Kingdom 8 141 126 165 628 447 523

Italy 241 1 15 692 189 95 64

Other European Countries 25 101 209 1,265 7,807 4,222 4,187

Other European Countries (Excluding

EU) 64 70 109 1,65 91 79 242

Africa 0 0 -- 3 21 20 5

U.S.A. 2 52 36 88 848 456 3,589

Canada 7 6 61 26 121 115 8

Central America And Caribbean 0 0 -- 8 32 22 17

South America 0 0 -- -- 1 1 467

Asian 70 60 60 1,756 1,927 299 1,025

Gulf Arabian Countries 5 0 -- 1,675 1,783 264 103

Near And Middle Eastern Countries 0 1 54 3 127 26 201

Other Asian Countries 65 59 6 78 17 9 721

Australia 0 0 -- 1 108 18 26

Unclassified 24 2 -- 1 7 7 --

Total 622 745 1,291 8,538 17,695 11,345 12,921

Provisional Data Source: Central Bank of the Republic of Turkey

46

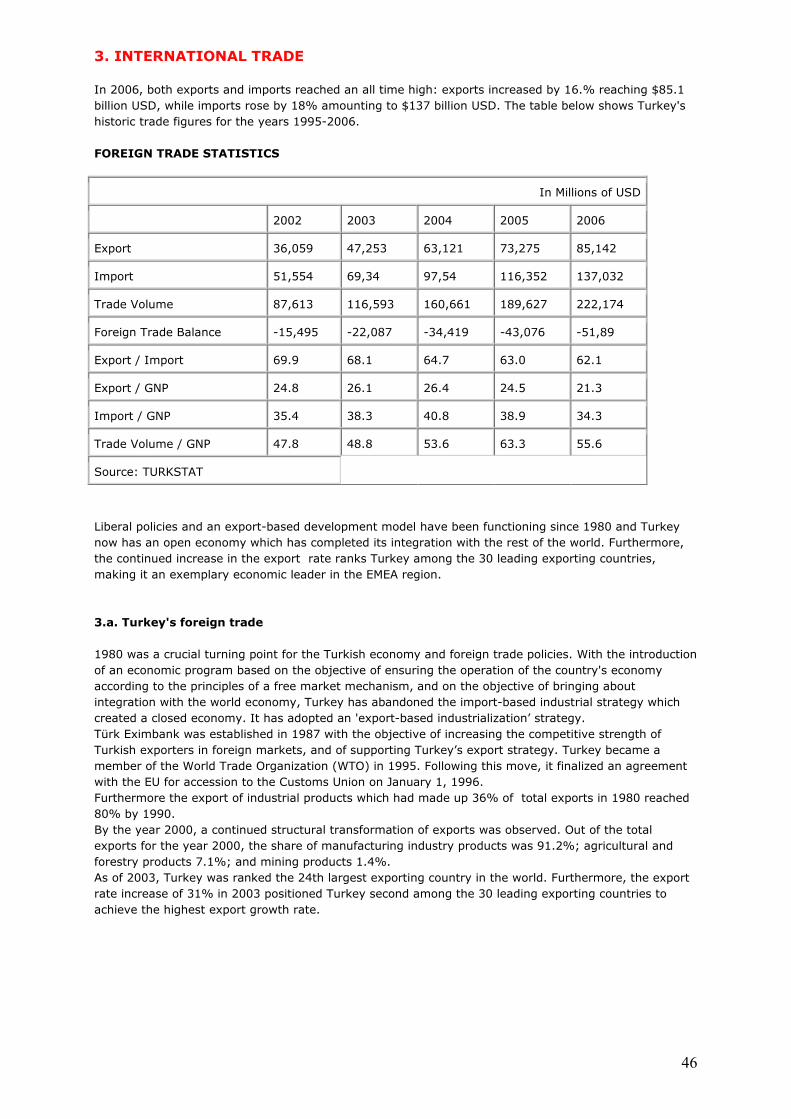

3. INTERNATIONAL TRADE

In 2006, both exports and imports reached an all time high: exports increased by 16.% reaching $85.1

billion USD, while imports rose by 18% amounting to $137 billion USD. The table below shows Turkey's

historic trade figures for the years 1995-2006.

FOREIGN TRADE STATISTICS

In Millions of USD

2002 2003 2004 2005 2006

Export 36,059 47,253 63,121 73,275 85,142

Import 51,554 69,34 97,54 116,352 137,032

Trade Volume 87,613 116,593 160,661 189,627 222,174

Foreign Trade Balance -15,495 -22,087 -34,419 -43,076 -51,89

Export / Import 69.9 68.1 64.7 63.0 62.1

Export / GNP 24.8 26.1 26.4 24.5 21.3

Import / GNP 35.4 38.3 40.8 38.9 34.3

Trade Volume / GNP 47.8 48.8 53.6 63.3 55.6

Source: TURKSTAT

Liberal policies and an export-based development model have been functioning since 1980 and Turkey

now has an open economy which has completed its integration with the rest of the world. Furthermore,

the continued increase in the export rate ranks Turkey among the 30 leading exporting countries,

making it an exemplary economic leader in the EMEA region.

3.a. Turkey's foreign trade

1980 was a crucial turning point for the Turkish economy and foreign trade policies. With the introduction

of an economic program based on the objective of ensuring the operation of the country's economy

according to the principles of a free market mechanism, and on the objective of bringing about

integration with the world economy, Turkey has abandoned the import-based industrial strategy which

created a closed economy. It has adopted an 'export-based industrialization’ strategy.

Türk Eximbank was established in 1987 with the objective of increasing the competitive strength of

Turkish exporters in foreign markets, and of supporting Turkey’s export strategy. Turkey became a

member of the World Trade Organization (WTO) in 1995. Following this move, it finalized an agreement

with the EU for accession to the Customs Union on January 1, 1996.

Furthermore the export of industrial products which had made up 36% of total exports in 1980 reached

80% by 1990.

By the year 2000, a continued structural transformation of exports was observed. Out of the total

exports for the year 2000, the share of manufacturing industry products was 91.2%; agricultural and

forestry products 7.1%; and mining products 1.4%.

As of 2003, Turkey was ranked the 24th largest exporting country in the world. Furthermore, the export

rate increase of 31% in 2003 positioned Turkey second among the 30 leading exporting countries to

achieve the highest export growth rate.

47

These developments contributed greatly to Turkey being considered an attractive investment region; this

is particularly because trade and investments exhibit complementary features. Also, the open economy

indicator calculated as the GNP/foreign trade ratio is accepted as a significant determining factor for

foreign direct investors in identifying their investment areas. With its economic structure integrated with

the world economy, Turkey has not only increased its trade volume and exports but also has created an

export product range with an emphasis on industrial products of high added value which require

advanced technology. This was all made possible by ensuring a structural transformation in its exports.

Furthermore it has continued to diversify its target markets.

Turkey currently exports over 7,000 products to 170 countries and for 2007, will reach nearly $100

billion USD in exports.

3.b. Foreign Trade by Economic Activities

In line with the policies implemented within the framework of the export-led development model that has

been followed since 1980, exportation has become important to Turkey both qualitatively and

quantitatively.

Starting particularly in 1980 and continuing up to the mid-1990s, very important developments have

been observed in the market share of labor-intensive industrial products such as the manufacture of

textiles and of clothing; iron and steel; and foodstuffs.

In 1996, with the establishment of a Customs Union with the European Union, Turkey's exportation

entered a new structural transformation process. Developments in recent years show that production and

export have increased significantly in high technology sectors such as electrical and electronic machinery

and equipment as well as automobile manufacture. In this respect, it is also seen that the export market

share of the manufacture of industrial products has increased in the period from 1999 to 2006.

Between 1980 and 2006 there have been important changes made in the distribution of imports within

different sectors.

Since 1990, the manufacturing industry has became the leading importer. Including the sub-sectors of

the manufacturing industry, it is apparent that the import share of iron and steel, as well as chemicals in

total imports has not changed significantly. However, the import of machinery and transportation

vehicles, as well as that of textile products sectors has increased.

3.c. Foreign Trade in terms of Countries

In terms of both imports and exports, members of the European Union are Turkey's most important

trade partners.

Imports by Country

With respect to Turkey's imports by country groups, EU members have maintained the highest position

since 1980. Between 1999 and 2005, while it was observed that imports from EU members rose from

around 44% to 52%, there was also a marked increase in imports from Asia, the Black Sea Economic

Cooperation Member Countries, and the Common Wealth of Independent States which has attracted

significant attention.

In 2005, the share of imports to OECD countries was 56.6%. The highest position among the OECD

countries was held by the EU members with a total market share of 42.2%. In 2005 the top 5 countries

in terms of imports were Germany, Russia, Italy, China and France. The overall share of these 5

countries in imports was 40.1%.

48

2002 2003 2004 2005

Million

USD

% of

Total

Million

USD

% of

Total

Million

USD

% of

Total

Million

USD

% of

Total

OECD Countries 32984,5 64 43898,6 43898,6 59492,4 61 65896,5 56,6

EU Countries 23321 45,2 33494,7 33494,7 45373,1 46,5 49047,6 42,2

EFTA Countries 2512 4,9 3395,7 3395,7 3888,7 4 4437,3 3,8

Other OECD

Countries 7151,4 13,9 7008,2 7008,2 10230,6 10,5 12845,1 11

Turkish Free

Zones 574,5 1,1 588,9 588,9 809 0,8 756,8 0,7

Non OECD

Countries 17994,8 34,9 24852,2 24852,2 37238,4 38,2 49698,4 42,7

European

Countries 6342,8 12,3 8910 8910 14411,3 14,8 19274 16,6

African Countries 2696,2 5,2 3338 3338 4779,3 4,9 6032,9 5,2

American

Countries 592,3 1,1 1082 1082 1359 1,4 1798,1 1,5

Middle East

Countries 3681,5 7,1 4059 4059 5121,8 5,3 7372,9 6,3

Other Asian

Countries 4366,5 8,5 6801 6801 10636,2 10,9 14457,8 12,4

Other Countries 315,5 0,6 651 651 930,9 1 762,6 0,7

Selected Country Groups

Black Sea Econ.

Cooperation 6576,6 12,8 9297,7 9297,7 15263,1 15,6 20401,3 17,5

Economic

Cooperation Org. 1548,2 3 2735,7 2735,7 3208,1 3,3 5101,5 4,4

Commonwealth

of

Indep.States 5554,5 10,8 7777,1 7777,1 12848,2 13,2 17178,4 14,8

Turkish

Republics 467,8 0,9 623,3 623,3 940,9 1 1262,3 1,1

Islamic

Conference Org. 6770,1 13,1 8481,5 8481,5 10565,9 10,8 14426,8 12,4

Selected Countries*

Germany 7041,5 13,7 9453 13,6 12515,7 12,8 13594,8 11,7

49

Russia 3891,7 7,5 5451,3 7,9 9033,1 9,3 12856,8 11

Italy 4097 7,9 5471,5 7,9 6865,8 7 7539,8 6,5

China 1368,3 2,7 2610,3 3,8 4476,1 4,6 6848,2 5,9

France 3052,7 5,9 4164,1 6 6201,3 6,4 5874,8 5

USA 3099,1 6 3495,8 5 4745,2 4,9 5360,6 4,6

Switzerland 2142,7 4,2 2968,2 4,3 3404,5 3,5 4053 3,5

United Kingdom 2438,3 4,7 3500 5 4317,1 4,4 4681,4 4

Spain 1419,2 2,8 2003,7 2,9 3253,7 3,3 3540,1 3

Southern Korea 900,4 1,7 1312,4 1,9 2572,5 2,6 3475,7 3

Iran 921 1,8 1860,7 2,7 1962,1 2 3469 3

Japan 1465,5 2,8 1927,1 2,8 2684,3 2,8 3102,3 2,7

Ukraine 991,1 1,9 1331,5 1,9 2509,4 2,6 2632,4 2,3

Belgium-

Luxemburg 1150 2,2 1523,6 2,2 1991,7 2 2224,3 1,9

Netherlands 1311,3 2,5 1656,7 2,4 1908,1 2 2138,6 1,8

Saudi Arabia 793,8 1,5 969,1 1,4 1231,5 1,3 1886,5 1,6

Sweden 535,1 1 822,2 1,2 1118,4 1,1 1423,6 1,2

T o t a l 51553,8 100 69339,7 100 97539,8 100 116351,7 100

Source: SPO

* The countries are chosen according to the total import values in the previous years.

Exports by Country

Between 1980 and 2005, the share of Turkish exports to European Union members was around 50%;

these countries maintained their place as the group to which Turkey exports most. Between 1999 and

2005, it was observed that while the share of exports made to the EU countries changed from around

51% to 54%, there was also an increase in exports made to Black Sea Economic Cooperation Countries,

to countries of the Islamic Conference Organization, and to the Commonwealth of Independent States.

In 2005, the share of exports to OECD countries was 60.4 %. The highest position among the OECD

countries was held by the EU members with an overall share of 52.3%. In 2004, the top 5 countries for

exports were Germany, the UK, Italy, the USA and France. The overall share of exports by these 5

countries was 40.6%.

50

2002 2003 2004 2005

Million

USD

% of

Total

Million

USD

% of

Total

Million

USD

% of

Total

Million

USD

% of

Total

OECD Countries 23,553.1 65.3 30.422.4 64.4 40.332.2 63.9 44.280.0 60.4

EU Countries 18,458.5 51.2 25,898.7 54.8 34,309.9 54.4 38,349.6 52.3

EFTA Countries 409.0 1.1 538.0 1.1 655.5 1.0 819.9 1.1

Other OECD

Countries 4,685.5 13.0 3,985.6 8.4 5,366.8 8.5 6,009.7 8.2

Turkish Free

Zones 1,438.5 4.0 1,928.3 4.1 2,529.1 4.0 2,963.8 4.0

Non OECD

Countries 11,067.5 30.7 14,902.2 31.5 20,259,6 32.1 26,031.5 35.5

Europe + CIS

Countries 3,447.4 9.6 4,720.0 10.0 5,922.2 9.4 7,920.2 10.8

African Countries 1,696.7 4.7 2,131.2 4.5 2,951.5 4.7 3,625.8 4.9

American

Countries 241.2 0.7 256.0 0.5 373.0 0.6 520.7 0.7

Middle East

Countries 3,575.7 9.9 5,131.5 10.9 7,237.6 11.5 9,268.8 12.6

Other Asian

Countries 1,939.8 5.4 2,604.0 5.5 2,864.0 4.5 3,486.7 4.8

Other Countries 166.7 0.5 59.5 0.1 911.3 1.4 1,209.3 1.7

Selected Country Groups

Black Sea

Economic

Cooperation

3,476.9 9.6 5,044.4 10.7 6,736.3 10.7 8,604.0 11.7

Economic

Cooperation

Organization

1,041.9 2.9 1,569.2 3.3 2,186.5 3.5 2,658.9 3.6

Commonwealth

of Independent

States

2,278.9 6.3 2,962.6 6.3 3,932.7 6.2 5,046.6 6.9

Turkish Republics 619.3 1.7 899.1 1.9 1,186.1 1.9 1,406.0 1.9

Islamic

Conference

Organization

5,195.9 14.4 7,341.8 15.5 10,141.2 16.1 12,988.8 17.7

51

Selected Countries*

Germany 5,868.8 16.3 7,484.9 15.8 8,745.3 13.8 9,448.8 12.9

United Kingdom 3,024.9 8.4 3,670.1 7.8 5,543.9 8.8 5,916.1 8.1

Italy 2,375.7 6.6 3,193.2 6.8 4,640.3 7.3 5,606.2 7.7

USA 3,356.1 9.3 3,751.6 7.9 4,848.6 7.7 4,887.3 6.7

France 2,134.6 5.9 2,826.1 6.0 3,668.4 5.8 3,791.0 5.2

Spain 1,125.1 3.1 1,789.5 3.8 2,618.4 4.1 3,009.1 4.1

Iraq 0.0 0.0 0.0 0.0 1,820.8 2.9 2,724.7 3.7

Netherlands 1,055.6 2.9 1,525.9 3.2 2,138.0 3.4 2,467.3 3.4

Russia 1,172.0 3.3 1,367.6 2.9 1,859.2 2.9 2,374.4 3.2

Romania 566.5 1.6 873.3 1.8 1,235.5 2.0 1,783.6 2.4

U. A. E 457.3 1.3 702.9 1.5 1,143.7 1.8 1,669.4 2.3

Israel 861.4 2.4 1,083.0 2.3 1,313.9 2.1 1,462.5 2.0

Belgium

Luxembourg 693.3 1.9 885.6 1.9 1,183.2 1.9 1,291.1 1.8

Bulgaria 380.3 1.1 621.7 1.3 894.3 1.4 1,178.5 1.6

Greece 590.4 1.6 920.4 1.9 1,170.8 1.9 1,124.1 1.5

Saudi Arabia 554.6 1.5 741.5 1.6 768.5 1.2 961.2 1.3

Iran 334.0 0.9 533.8 1.1 813.0 1.3 905.4 1.2

Poland 342.6 1.0 480.0 1.0 697.7 1.1 829.3 1.1

T o t a l 36.059.1 100.0 47,252.8 100.0 63,120.9 100.0 73,275.3 100.0

Source: SPO

* The countries are chosen according to the total export values in the last year.

TURKEY MEMBERSHIPS IN INTERNATIONAL TRADE ORGANIZATIONS

Turkey has been a member of World Trade Organization, since 1995. Its commitment to intergrating with

regional and international trade norms is seen in its participation in and membership of various

organizations such as: Economic Cooperation Organization (ECO), UNCTAD, Black Sea Economic

Cooperation Organization, World Customs Organization, International Chamber of Commerce, Islamic

Cooperation Organization, D-8 , Stability Pact, and various other organization.

52

Business Legislation

Turkey offers a simple business legislation system with international standards through which all

investors enjoy equal treatment. Recent amendments to the existing law will assist Turkey even further

with its present improvements in the investment environment.

Turkey offers:

1. Legal Framework for Foreign Direct Investment

2. Bilateral Agreements, Double Taxation Prevention Treaties and Social Security Agreements

3. Bilateral Free Trade Agreements

Legal Framework of Foreign Direct Investment

The aim of Foreign Direct Investment Law is:

• To encourage FDI’s in the country

• To protect foreign investors’ rights

• To bring the investors and investments in line with international standards

• To establish a notification-based rather than approval-based system for FDI’s

• To increase the volume of FDI’s through established policies

The Foreign Direct Investment Law provides a definition of foreign investors and foreign direct

investments. Additionally, it explains the important principles of FDI’s such as freedom to invest, national

treatment, expropriation and nationalization, transfers, access to real estate, dispute settlement,

valuation of non-cash capital, employment of expatriates, and liaison offices.

The Regulation for the implementation of the Foreign Direct Investment law consists of:

• Specifying the procedures and principles of the issues that are laid down in Foreign Direct Investment

(FDI) Law.