investmentbankers to the e nergyindustry s immons & c ompany international colin welsh thursday,...

TRANSCRIPT

Investment Bankersto the Energy Industry

SIMMONS & COMPANYINTERNATIONAL

Colin Welsh

Thursday, 27 October 2005

Chief Executive OfficerSimmons & Company International Limited

SIMMONS & COMPANYINTERNATIONAL

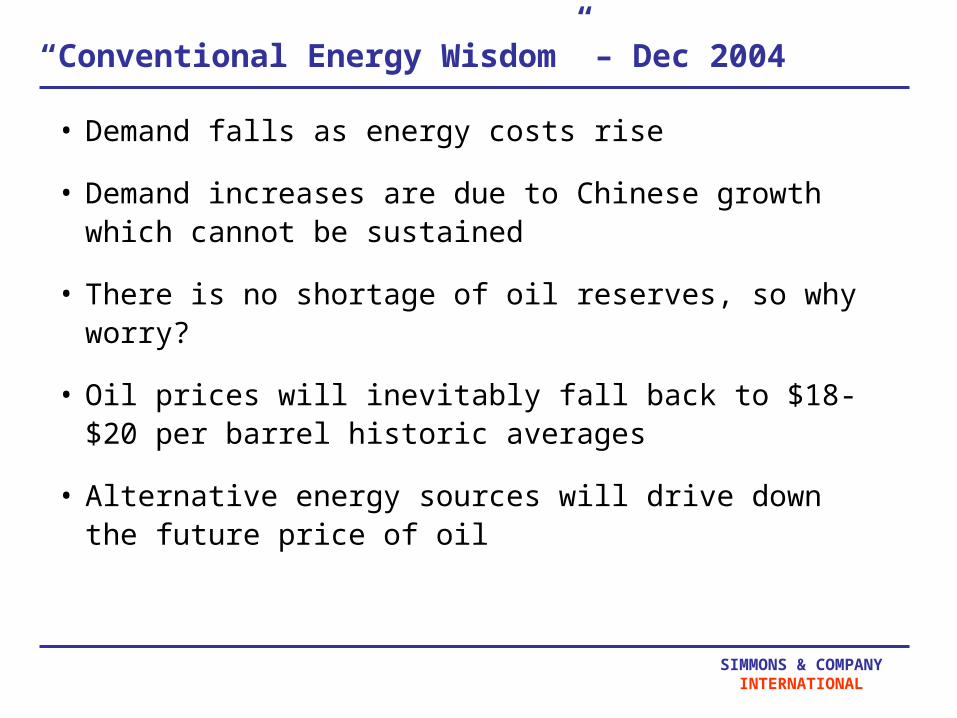

“Conventional Energy Wisdom” – Dec 2004

• Demand falls as energy costs rise

• Demand increases are due to Chinese growth which cannot be sustained

• There is no shortage of oil reserves, so why worry?

• Oil prices will inevitably fall back to $18-$20 per barrel historic averages

• Alternative energy sources will drive down the future price of oil

SIMMONS & COMPANYINTERNATIONAL

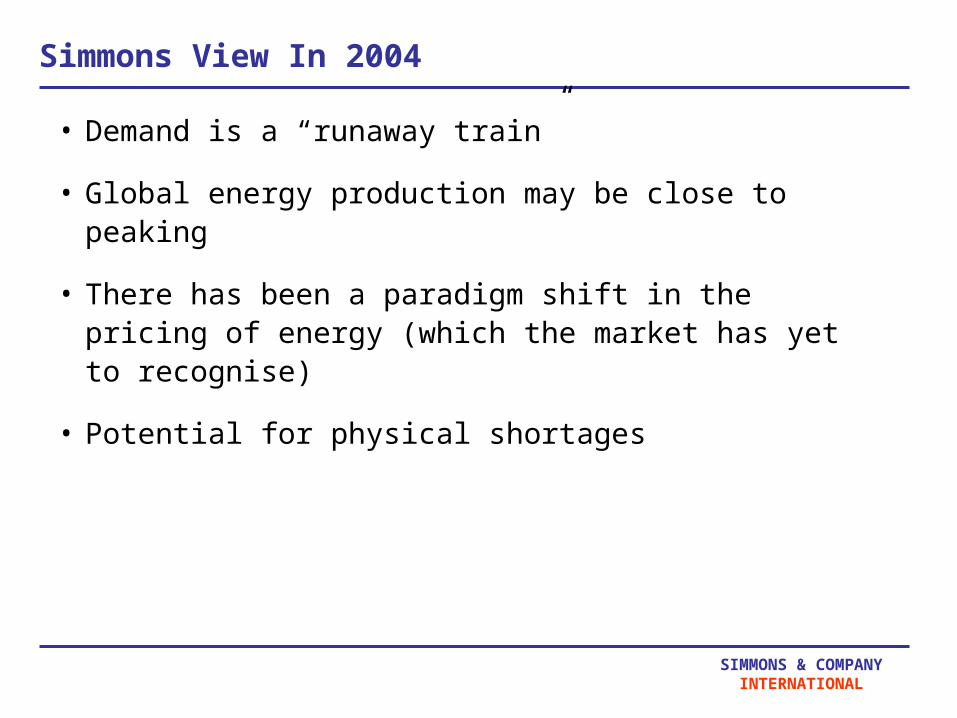

Simmons View In 2004

• Demand is a “runaway train”

• Global energy production may be close to peaking

• There has been a paradigm shift in the pricing of energy (which the market has yet to recognise)

• Potential for physical shortages

SIMMONS & COMPANYINTERNATIONAL

Where Were We In Dec 04?

WTI Oil Price, Spot And Forward

SIMMONS & COMPANYINTERNATIONAL

Where To Next?

SIMMONS & COMPANYINTERNATIONAL

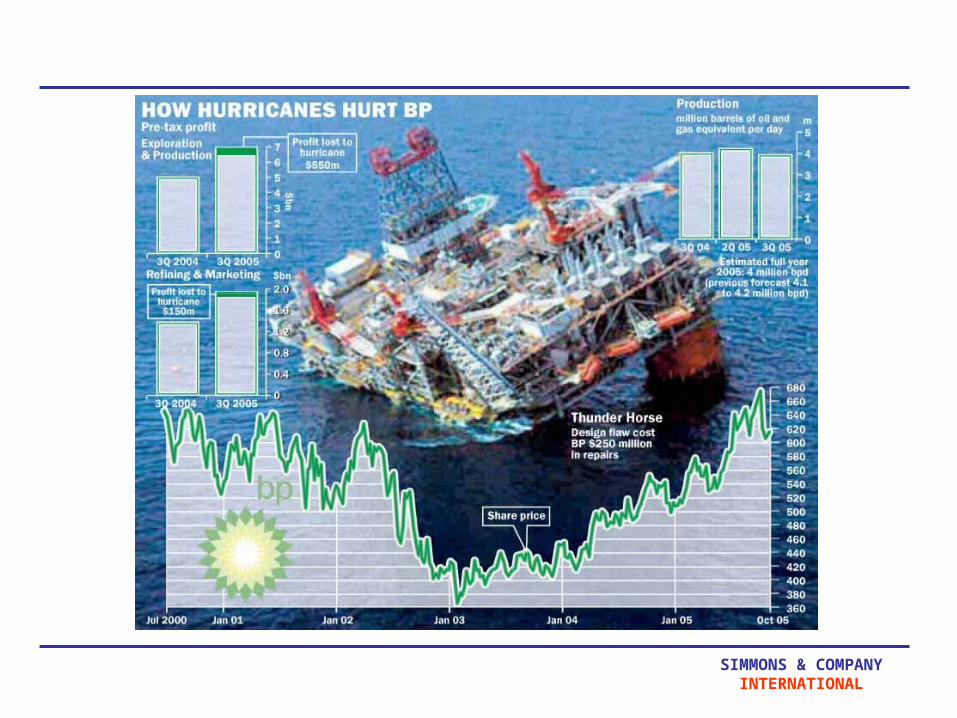

Hurricanes Katrina & Rita

SIMMONS & COMPANYINTERNATIONAL

SIMMONS & COMPANYINTERNATIONAL

U.S. Total Oil Production(Alaska & Lower States)

U.S. Total Oil Demand

SIMMONS & COMPANYINTERNATIONAL

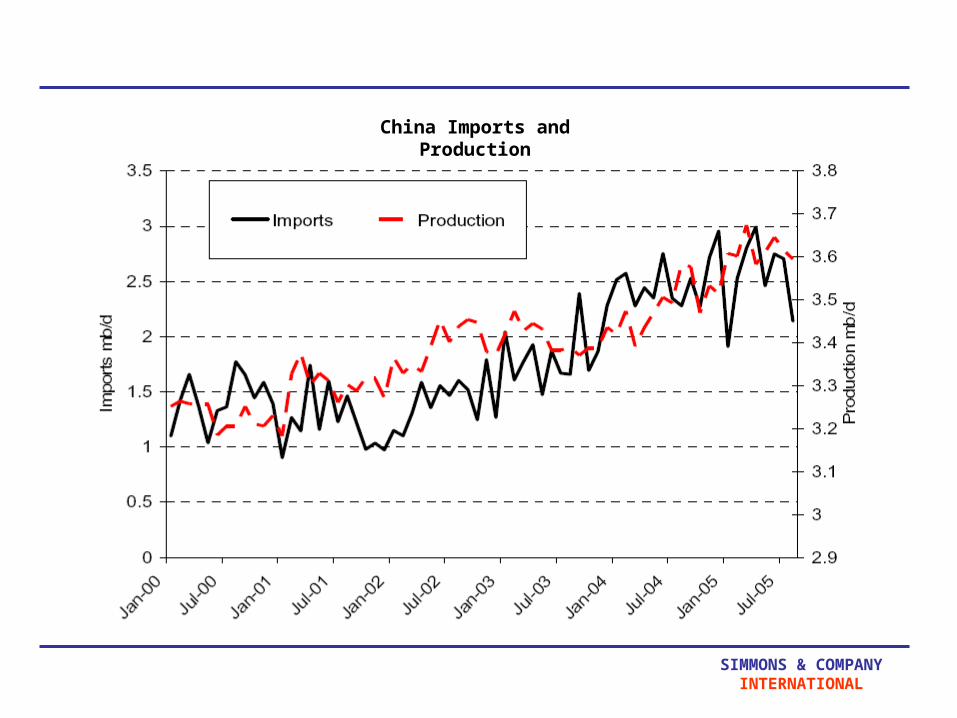

China Imports and Production

SIMMONS & COMPANYINTERNATIONAL

OPEC Spare Capacity vs. Worldwide Demand

SIMMONS & COMPANYINTERNATIONAL

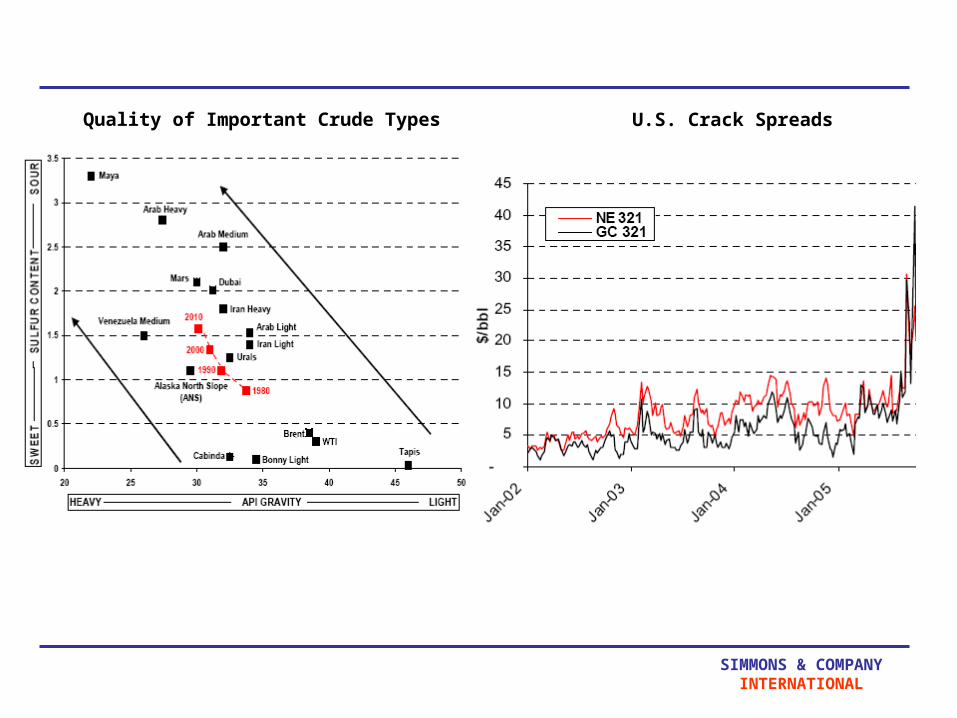

Quality of Important Crude Types U.S. Crack Spreads

SIMMONS & COMPANYINTERNATIONAL

Conclusion

• The principles of supply and demand dictate that lack of refinery capacity will result in an inability to satisfy the worlds increasing demands for refined products.

• So we can expect significantly higher refined product prices – US gasoline prices have risen by 30%, but more significantly we can expect physical shortages.

• That will be good news for investment in alternative energy and new technologies – unconventional oil, GTL, clean coal and natural gas.

• But it may be bad news for the world economy as spiralling transportation costs drive inflation and dampens demand.

• So predictions for next year:-– Continued high commodity prices,

– Very high petrol, diesel and heating oil prices,

– Record investment in the sector.

SIMMONS & COMPANYINTERNATIONAL

SIMMONS & COMPANYINTERNATIONAL

Investment Bankersto theEnergy

Industry