investment strategy webinar - aon · investment strategy webinar may 15, 2013. 2 presenters russ...

TRANSCRIPT

Investment Strategy Webinar

May 15, 2013

2

Presenters

Russ Ivinjack, Senior PartnerHead of Specialty Services &Resource IntegrationPhone: 312.715.3330Email: [email protected]

John Geissinger, CFA, PartnerInvestment SolutionsPhone: 203-523-8898Email: [email protected]

Adrian Kurniadjaja, CFA, Senior ConsultantGlobal EquityPhone: 312-715-3305Email: [email protected]

Duncan Lamont, CFA, PrincipalGlobal Asset AllocationPhone: 011 +44 207 086 9168Email: [email protected]

Chris Riley, Associate PartnerGlobal Head of Equity ResearchPhone: 312-715-3339Email: [email protected]

3

Discussion Topics

Opening Remarks & Recently Released Research Market Update with a Focus on Bond Yields Rethinking Fixed Income Hiring Underperforming Equity Managers Closing RemarksQ&A Session

4

Entries in the HEK Blog (www.hekblog.com) – In Case You Missed It

Five New Viewpoints Defined Contribution Plan Re-Enrollment: Responsible Redirection or Wrong

Direction? Do Hedge Fund of Funds have a future? PBS Frontline “The Retirement Gamble” Segment Recent Case Law Development Regarding ERISA Fees and 401(k) Plan

Investments Alternative Investments in DC Plans

Several Pieces of Intellectual Capital on Weekly Update Postings Corporate pension liability hedging views (4/22/2013) Quarterly investment outlook (4/29/2013) Three new white papers (5/8/2013) Liability discount rate update (5/13/2013) Stable value quarterly (5/13/2013) Week in markets summary (every week)

5

Subscribing to the HEK Blog

Go to www.hekblog.com Enter your email address where it says “subscribe” Get ~2 emails per week

Market Update with a Focus on Bond Yields

Duncan Lamont, CFA

7

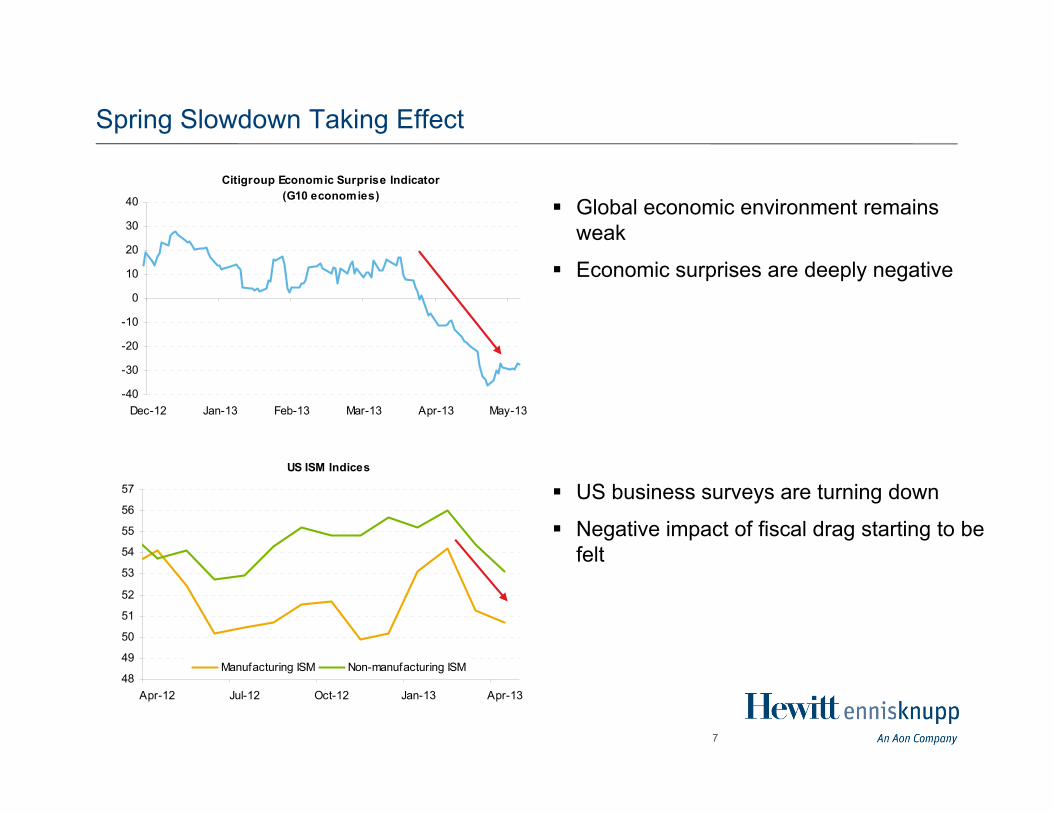

Spring Slowdown Taking Effect

Global economic environment remains weak

Economic surprises are deeply negative

US business surveys are turning down

Negative impact of fiscal drag starting to be felt

Citigroup Economic Surprise Indicator (G10 economies)

-40

-30

-20

-10

0

10

20

30

40

Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13

US ISM Indices

48

49

50

51

52

53

54

55

56

57

Apr-12 Jul-12 Oct-12 Jan-13 Apr-13

Manufacturing ISM Non-manufacturing ISM

8

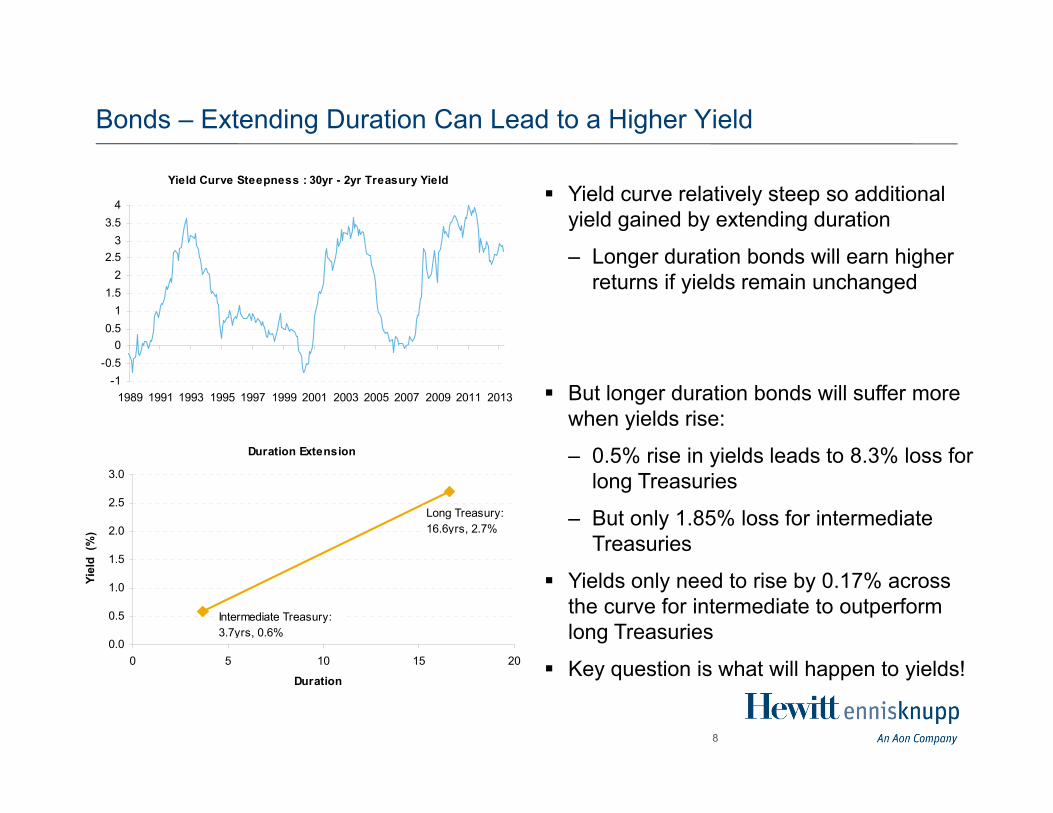

Bonds – Extending Duration Can Lead to a Higher Yield

Yield Curve Steepness : 30yr - 2yr Treasury Yield

-1-0.5

00.5

11.5

22.5

33.5

4

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Duration Extension

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0 5 10 15 20

Duration

Yiel

d (%

)

Intermediate Treasury:3.7yrs, 0.6%

Long Treasury:16.6yrs, 2.7%

Yield curve relatively steep so additional yield gained by extending duration

– Longer duration bonds will earn higher returns if yields remain unchanged

But longer duration bonds will suffer more when yields rise:

– 0.5% rise in yields leads to 8.3% loss for long Treasuries

– But only 1.85% loss for intermediate Treasuries

Yields only need to rise by 0.17% across the curve for intermediate to outperform long Treasuries

Key question is what will happen to yields!

9

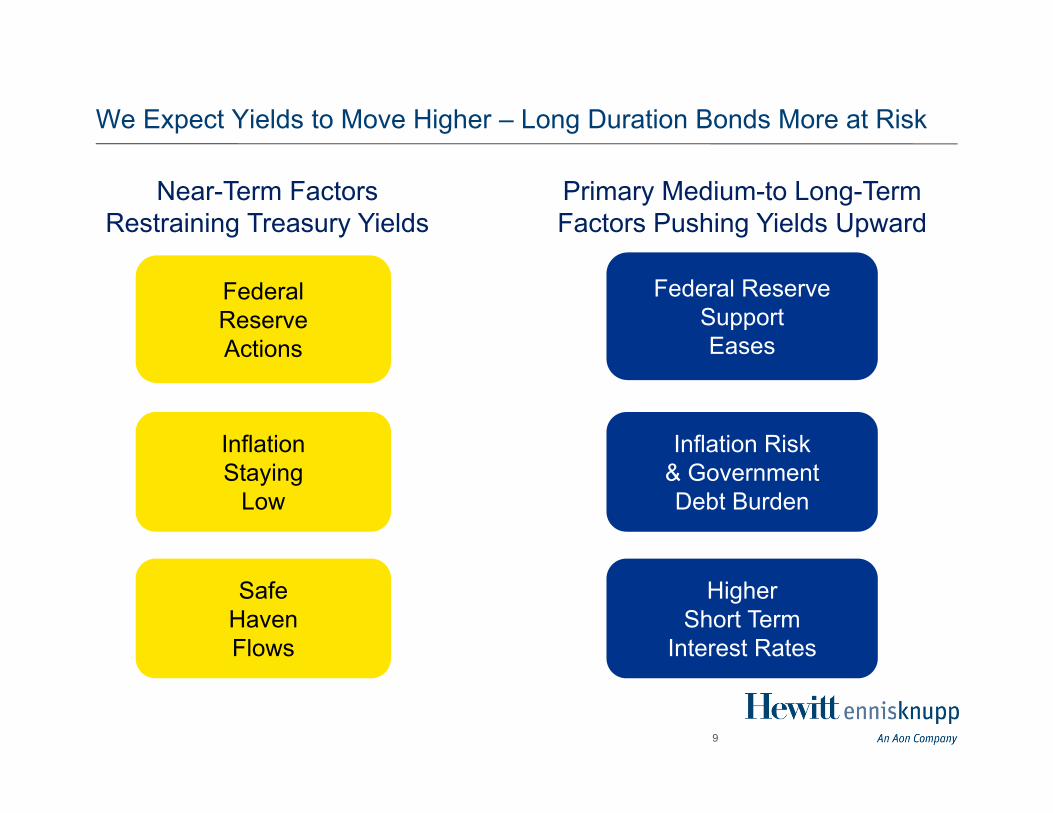

We Expect Yields to Move Higher – Long Duration Bonds More at Risk

FederalReserveActions

InflationStaying

Low

SafeHavenFlows

Federal ReserveSupportEases

Inflation Risk& GovernmentDebt Burden

HigherShort Term

Interest Rates

Near-Term Factors Restraining Treasury Yields

Primary Medium-to Long-Term Factors Pushing Yields Upward

10

Medium Term Outlook on Interest Rates

Market Expectation Increase from today MTV Expectation Increase from todayNow 2.8% 2.8%In 3yrs 3.4% 0.5% 3.9% 1.1%In 5yrs 3.6% 0.8% 4.4% 1.6%

Market Expectations for Yield Curves

0%

1%

2%

3%

4%

1 3 5 7 9 11 13 15 17 19 21 23 25

Duration

Yield curve at April 30, 2013

Projected yield curve at April 30, 2016

Projected yield curve at April 30, 2018

We expect yields to rise by more than priced into the marketRecommend tilting portfolios to short of target duration

11

Summary of Medium-Term Market Views

Equities Gains to slow significantly, but prefer to bonds Non-US markets should outperform on currency hedged

basis Now prefer emerging markets to developed Neutral growth/value Retain preference for large cap

Bonds Continue with negative view Negative view on US treasuries Take profits on credit - move back to target Cautious on high yield, still prefer loans Local emerging market currency debt preferred to dollar

denominatedAlternative Asset Classes Favor real estate, hedge funds, infrastucture and

selected private equity investments

Rethinking Fixed Income

John Geissinger, CFA

13

Focus on Risk Reducing Portfolio

We have discussed many ways to enhance the return seeking portfolio; for example, “Go Big or Go Home”, and “Conviction in Equity Investing.”

In an era of low expected returns, we also must invest in the most efficient risk-reducing portfolio.

Corporate Defined Benefit plans are encouraged to de-risk through the use of a hedge portfolio.

Other investors-Public Defined Benefit, Endowment, Foundation and Sovereign Wealth-should move away from the broad based bond benchmarks to fine tune the risk-reducing properties of fixed income.

14

Risk Reducing Properties

There are several desired characteristics for a risk reducing portfolio:– Low correlation– Low volatility– High volatility, IF correlation is negative– Downside protection: perform when the return-seeking, predominantly equity,

portfolio experiences negative returns Achieving these properties at minimum cost is preferable.

15

Intermediate versus Long Treasury Market

We disaggregated the Treasury Index into the intermediate sector (1-10 years) and long sector (10+ years) to compare the risk-reducing qualities of both maturity sectors of the fixed income market.

The Treasury Index was utilized to focus exclusively on the duration positioning of the risk-reducing portfolio.

16

Volatility and Correlation Comparison

Even though short-term interest rates are more volatile than long-term interest rates, the intermediate sector has less volatility than the long sector.

The volatility of the long sector can be similar to the equity volatility. The intermediate sector has less correlation to the equity market than the long sector.

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

12/1

/197

712

/1/1

980

12/1

/198

312

/1/1

986

12/1

/198

912

/1/1

992

12/1

/199

512

/1/1

998

12/1

/200

112

/1/2

004

12/1

/200

712

/1/2

010

Correlation

Rolling 5 Yr Correlation with Equity

Intermediate

Long

17

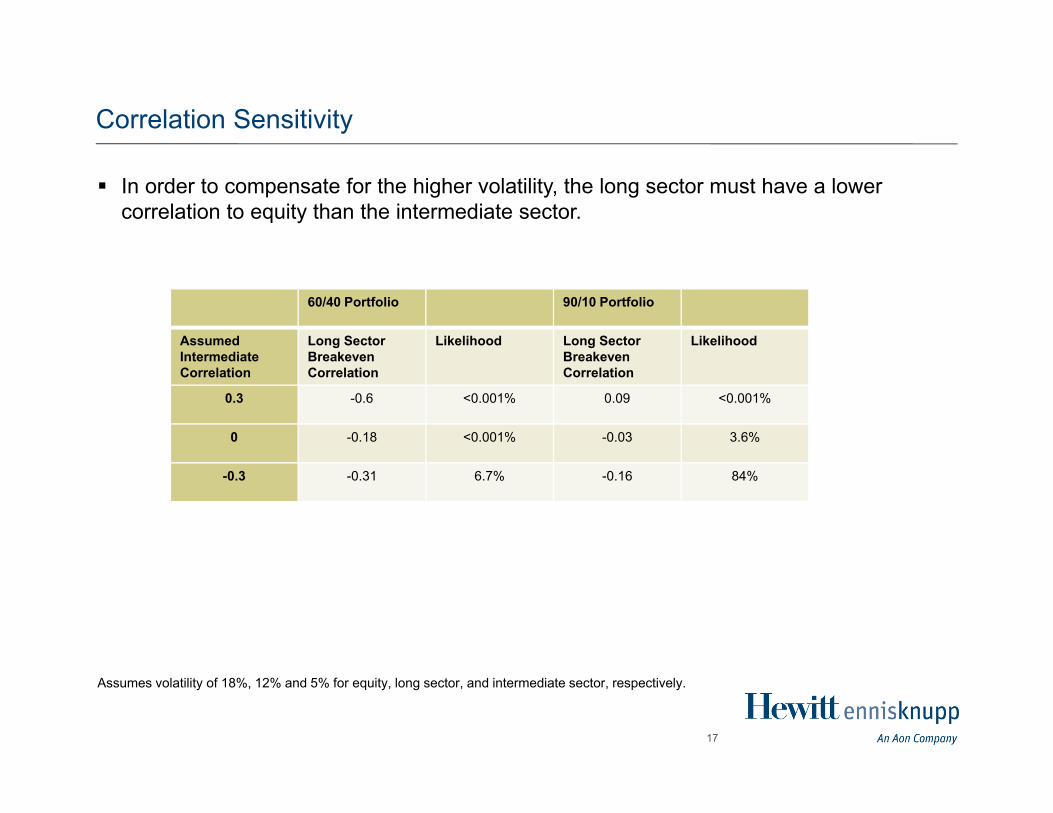

Correlation Sensitivity

In order to compensate for the higher volatility, the long sector must have a lower correlation to equity than the intermediate sector.

Assumes volatility of 18%, 12% and 5% for equity, long sector, and intermediate sector, respectively.

60/40 Portfolio 90/10 Portfolio

AssumedIntermediate Correlation

Long Sector Breakeven Correlation

Likelihood Long Sector Breakeven Correlation

Likelihood

0.3 -0.6 <0.001% 0.09 <0.001%

0 -0.18 <0.001% -0.03 3.6%

-0.3 -0.31 6.7% -0.16 84%

18

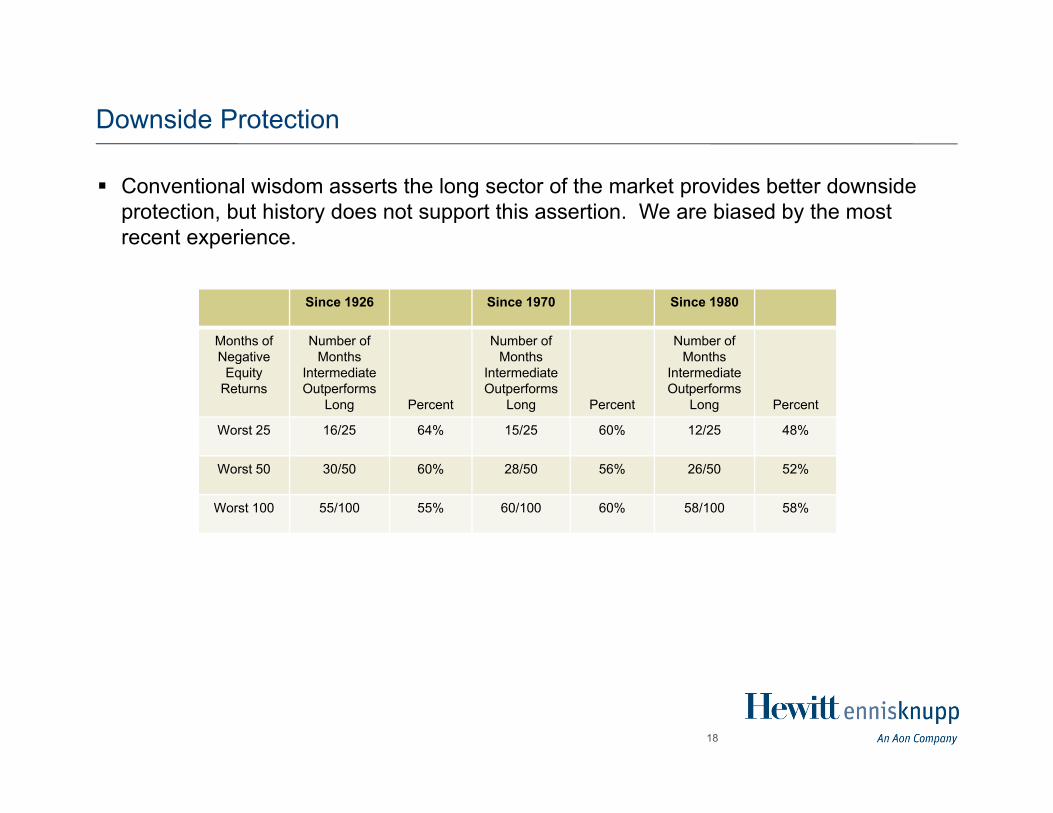

Downside Protection

Conventional wisdom asserts the long sector of the market provides better downside protection, but history does not support this assertion. We are biased by the most recent experience.

Since 1926 Since 1970 Since 1980

Months of Negative

Equity Returns

Number of Months

IntermediateOutperforms

Long Percent

Number of Months

IntermediateOutperforms

Long Percent

Number of Months

IntermediateOutperforms

Long Percent

Worst 25 16/25 64% 15/25 60% 12/25 48%

Worst 50 30/50 60% 28/50 56% 26/50 52%

Worst 100 55/100 55% 60/100 60% 58/100 58%

19

Does the Long Sector Compensate for Additional Volatility

In a word, NO!

-4

-2

0

2

4

6

8

10

12/1

/199

38/

1/19

944/

1/19

9512

/1/1

995

8/1/

1996

4/1/

1997

12/1

/199

78/

1/19

984/

1/19

9912

/1/1

999

8/1/

2000

4/1/

2001

12/1

/200

18/

1/20

024/

1/20

0312

/1/2

003

8/1/

2004

4/1/

2005

12/1

/200

58/

1/20

064/

1/20

0712

/1/2

007

8/1/

2008

4/1/

2009

12/1

/200

98/

1/20

104/

1/20

1112

/1/2

011

8/1/

2012

Rolling 5 Year Return Difference

Risk Adj Inter Less Long

Inter Less Risk Adj Long

20

One Explanation for Lack of Risk Premium in Long Sector

0

0.5

1

1.5

2

2.5

3

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21Duration

Yield

Long end pulled downby long liabilityhedging

21

Portfolio Implications

Investors looking to manage the volatility of the return-seeking portfolio should invest the risk-reducing portfolio in intermediate fixed income.

For those that are concerned about cash flow yield, recognize the yield reduction relative to the volatility reduction is minimal:– Reposition from Aggregate Index to Intermediate Aggregate Index,– Shorten duration by 1.35 years,– Yield reduction of 30 basis points,– One year breakeven yield change is only 22 basis points.

Hiring Underperforming Equity Managers

Chris RileyAdrian Kurniadjaja, CFA

23

Manager Decisions

Hiring managers to succeed in the long term is not just about hiring the best performing manager in the search process– Be cognizant of the manager’s style and tendencies before making a decision

• Style biases• Size biases• Macro economic conditions that may have impacted performance• If these conditions reverse, how will the manager perform?

A similar decision needs to be made when evaluating current managers within an investment program that have underperformed their respective benchmark

The market environment over the last few years has been volatile where a variety of active management strategies have not worked– Low quality rally– Value out of favor– Europe/Japan– Correlation of U.S. securities

24

Terminating an Investment Manager – Is Now the Right Time?

Benchmark-relative performance is just one of several factors to consider when contemplating the replacement of an investment manager

Other considerations include:– Stability of key investment staff

• Did they become dumb overnight

– Stability of investment firm• Are they unfocused?

– Has the process changed?• Including execution of the process

– Is the manager’s style in favor or out of favor?

25

Examination of Buy-Rated Managers

We analyzed buy-rated equity managers to determine if there was any patterns of performance that are meaningful to assist with these critical decisions– Time periods analyzed were three years through 3/31/2010 and the subsequent

three-year period

A few patterns emerged:– Strong outperformance of a subset of buy-rated managers was followed with

weakness– Conversely, underperforming periods for managers was followed by outperformance

Implications for client investments– Given the strong mean reversion, consider recently underperforming managers

when hiring a new manager• Don’t hire the manager with the best short-term performance

– Have a little more patience with the managers that underperform

26

Analysis

Alphas are cyclical. – For the three years to 3/31/10, the medians performed strongly– For the three years to 3/31/13, alpha was much harder to achieve– Only emerging markets, EAFE and Global managers saw improved alphas; EM

and Global outperformed during both examined time periods.

-3

-2

-1

0

1

2

3

4

SM

IDV

SM

IDG

SM

IDC

MC

V

MC

G

MC

C

LCV

LCG

LCC

EM

Glo

bal

EA

FE

Median excess return for three years to 3/31/10Median excess return for three years to 3/31/13

27

Findings

Managers that underperform their medians exhibit stronger returns over the next three years; Further, managers that were out-performing their medians exhibit weaker returns over the next

three years Directionally, 75% of underperforming managers experienced an improvement relative to median,

while close to 80% of outperforming managers saw their excess returns falling relative to median

-1.8

2.6

-0.1

0.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Bel

owm

edia

n

abov

em

edia

n3 years to 3/31/10 3 years to 3/31/13

28

Client Implications

We have all heard the phrase “buy low, sell high.” This needs to be considered more when hiring and firing investment managers within the institutional framework.

Implications for client manager decisions– Given the strong mean reversion noted within our universe of Buy-rated equity

managers, clients should strongly consider managers underperforming their benchmark when hiring a new manager• Don’t hire the manager with the best short-term performance

– During reviews of existing managers, consider the reasons for underperformance• If the reasons for the manager’s hiring remain (strong team, unique process,

investment culture, etc.), examine the reasons for the underperformance In most cases where the qualities of an investment manager remain

consistent, the performance issues are likely environmental or not conducive to the manager’s process

Data has shown mean reversion which should lead to outperformance in the future if patient

Closing Remarks

Russ Ivinjack

30

Question & Answer

Questions may be submitted at any time during the web seminar by typing the question in the "Ask a Question" text field and clicking "Submit." Questions will be answered live as time permits during the question and answer session.

31

Our next investment strategy update call is scheduled for Wednesday, June 19th, at 10 a.m. CDT.