investment strategy - s3-eu-west-1.amazonaws.com · recomposed ¨franco-german¨ axis leadership...

TRANSCRIPT

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

1

Strategy

Investment strategy May 11th, 2017

Interference

A delicate second round for Trump administration The ideological segment of Trump candidate’s program is seriously compromised. Immigration remains a stone in his garden. We are also gravitating towards the elusive repeal of Obamacare. Border tax adjustment is a permanent subject of contention. The debt ceiling issue was only bypassed at the expense of symbolic measures (say the wall) … All these adventures have little importance per se. Still, on the negative, they might reduce the odds of lower private sector taxes and delay large infrastructure plans. But on the positive, Trump phantom administration is proving more pragmatic than feared, as many disruptive ideologues have now left. This pave the way for a better calibrated budget after the summer break, with funding process, and little need for protectionist measures. Repatriation is a … ¨trump¨card, which may find bi-partisan support. IT and pharmaceutical juggernauts would thereby be incentivized to invest back billions of USD in the US (or buy back stocks). So far, so bad for D. Trump, but… so good for markets! Indeed, the risks of a too strong USD and too high rates have vanished

Europe: the worst outcome is never guaranteed… Neither Nexit, nor Frexit did actually occur, and a fortunate deconstruction of traditional (sclerotic) political systems has started. New coalitions need to be formed. Granted, the parliamentarian base of Macron may prove fragile and Italy still needs to be anchored properly to the EU. But in short, the ball is now in the court of pro-integration leaders (Macron and Merkel/Schulz). A two-speed Europe may ultimately emerge. Important obstacles to fiscal, banking unions in the core have now dissipated. A common defence, a lower propensity for austerity and a higher one for risk mutualisation are possible. The EU homogenous posture against the UK, in recent Brexit talks, is a symbol of the renewed credibility of the EU construction. Centrifugal forces are coming to an end in the EU. An Impetus from the EU, of important magnitude, is echoing the US one

Asset price reflation: getting closer to an end of the story? In spite of Fed stall speed since late 2014, we are still in a global financial repression mode. Major developed countries ’ central banks remain very accommodative and real yields stay unusually low. This extreme monetary policy framework is a factor of asset price inflation (but not of economic - actual consumer prices - reflation). For long, investors have primarily questioned the consequential distortions on government bonds. But other assets, acting as a generating substitute to fixed income, are also concerned, namely real estate / housing. For instance, Canada, Australia and China, experienced irrational exuberance. Authorities have been trying to address it through macro-prudential measures (i.e. administrative). This gave temporarily relief, but didn’t curb the speculative trend, yet. US policymakers acknowledged for the need to normalise monetary policy, including shrink the $4,5tn Fed balance sheet. Two looming issues have delayed this process a) the ¨dramatic¨ leverage of investors (remember taper tantrum 2013?) and b) the interdependence with the Fed Funds rates. By chance, a bold stimulation coming from the fiscal (Trumponomics) side is no longer on 2017 agenda. This benign scenario, including tame USD and US yields, prefigures a welcome tailwind for the Fed, when it comes to engineer a subtle mix of restriction in monetary conditions. The ECB and the BoJ are at different stages of their monetary cycles. They will probably not accommodate and expand much further by 2018. China is also contemplating a lesser friendly monetary framework. Such a scenario would result next year in a different investment regime, where the importance of fiscal policy finally takes over from everything else. An end to financial repression is not in sight before 2018 earliest. A US soft patch is welcome for the Fed in its gradual normalisation process. It is conductive of pretty benign conditions for financial markets

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

2

Global framework is ok, but... G-20 economies are improving... A global and synchronized recovery is underway. The traction is pretty well-balanced between developed and emerging countries. A likely stabilization of the USD, coupled with a reasonable rise of interest rates, should not interfere with its continuation in H2 2017. A Trump-induced regime change will however not take place before H1 2018. The solid and nascent Eurozone recovery is spreading. Its size and scope may surprise if French and German elections go ¨well¨. A recomposed ¨Franco-German¨ axis leadership would turnaround private demand and investment. Policy-makers have ample room to stimulate without generating inflation, considering the stage of the business cycle (large output gap). A banking union would allow for better transmission of monetary policy. Japan is doing ok, experiencing a cyclical - but non-inflationary - recovery. China will deliver a solid H1 2017, though cyclical and structural challenges lie ahead.

... but US and China are losing steam Our proprietary index of macro risks is deep into a ¨no-recession¨ zone. But looking ahead, the situation is a bit less sanguine. US cycle is very mature. Recent moderation in fiscal stimulation, absence of liquidity injection by the Fed, and the relative overvaluation of the USD translate into a neutral policy stance. Credit is giving serious signs of slowdown, and a rebound of corporate investment requires tax reform (delayed to Q4?). The weakness of Q1 GDP is not alarming, as seasonal. A stalemate between administration and Congress is likely over summer. It may ultimately result in more balanced talks after summer holidays, with a better prepared government team!? China was the most important pillar of 2016/17 global reflation and of the stabilization in commodity prices and economic activity in certain emerging countries. But China will slow in H2, as the excessive credit-fuelled stimulus is over. A mild tightening mode is developing, featured by interbank rates rise, credit containment and macro-prudential measures (housing). The rebalancing based on reduction of excess capacity and stronger private sector (demand and investment) is slowly going on, but positively. It will need more time and actions (controlling corporate leverage and financial system activities). Latest IMF projections for the next 5 years seem realistic: advanced economies will deliver 2% real on average, developing 4,5% to 5%, translating into global growth of 3.5%

Measured current inflation, benign near-term perspectives The recent spike of US headline PCE above 2% does not feature a regime change, or a warning signal for the Fed. Firstly, it is not confirmed at all by core PCE figures, which stay resiliently close to 1,5%. Main explanation lies in a base effect and energy prices. Secondly, the latest soft US macro data as well as wage related metrics all proved muted. In Europe, the same sort of base - energy related - effect is taking place, moderating the momentum of inflation. More fundamentally, the output gap position of EU is very comfortable: a lot of slack remains present, which would provide a shelter if the economy was to exceed its growth potential for several quarters. In China, the strength of PPI over past quarters is good news as a confirmation of lower disinflation pressure linked to excess manufacturing capacity. If confirmed, Chinese domestic disinflationary pressure would durably be reduced. Ultimately, global inflation may benefit if China actually was to stop exporting its disinflation

Shrinking the $4,5tn Fed Balance Sheet... The Fed engaged late 2014 in the very, very gradual normalization of its unconventional and extreme monetary policy. In a first long cautious mode, it stopped injecting massive liquidity and then rose, at an homeopathic pace, the Fed funds. Now the central bank also wants to address the issue of its gigantic balance sheet, but remains haunted by the stigma of the 2013 ¨taper tantrum¨. It takes special care about this eventual process by a) pre-announcing it long before to markets, and b) acknowledging the collateral impact on Fed funds. We think that shrinking the balance sheet is inevitable and that the earlier will prove the better. This will inevitably impact nominal and real rates, on the upside. This must therefore definitely be considered as a means of tightening US monetary conditions. This might bring an element of insecurity to economic agents. But the Fed is well aware of the risks. On the positive, it will restore liquidity in markets and remove asset price distortions.

Macroeconomy

May 11th, 2017

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

3

Fed hikes and toppish USD

Global liquidity stays ample Markets are focusing on the monetary policies outlook and specifically, on the prospect of a gradual, endless policy normalization process across the major economies. Global liquidity conditions do not only depend on central bank policy tightness or looseness, but also on the willingness of commercial banks to expand their balance sheets. The combination of central and commercial bank liquidity is what counts. Supportive global liquidity conditions may allow the Fed to hike rates in June without derailing the risky assets rally. With the Fed willingness to remain as long as possible “behind the curve” in this tightening cycle, it is hard to avoid a conclusion that the EUR has the most to gain within the G3 currencies from this normalization.

Back to theory The USD is driven by the growth differentials. The relationship is that when the US growth outpaces that of the rest of the world by more than 1%, the USD tends to rally. On the other side, when US growth significantly underperforms the rest of the world, the USD tends also to strengthen thanks to its safe haven status. In between, when economies are synchronized, the USD should depreciate. 2017-year will be the first year of DM & EM synchronous growth recovery since 2010.This simultaneous improvement is creating positive feedback loops for global growth. Outside the US, developed activity data has surprised to the upside. As such, the dollar has had little reason to outperform even more so when the long USD positioning remains elevated and the currency still overvalued by c. 15% in real terms.

EUR liquidity should remain supportive too The French election outcome has seen bank stocks rallying and with bank shares now trading closer to book value, banks' balance sheet consolidation pressure should ease. European economic conditions have improved with core countries leading the way. However, the ECB may have to be cautious when reducing monetary accommodation. The ECB may stay behind the curve too, keeping its own monetary conditions accommodative. The ECB may reduce accommodation only when it has become confident enough that Italy will be able to deal with the consequences of tighter monetary conditions. What the market is not anticipating yet. Speculators have already scaled down their short EUR exposure but not fully yet. The EUR remains still undervalued by 10%. The JPY correction has been fast and exceeds what real rate differentials would suggest. There could be a quick reversal. The long-term inflation outlook looks robust and the BoJ is already quietly reducing its QQE. Yield differential tightening will support a higher JPY, mainly when the currency is 20% undervalued. The CHF will continue its gradual decline, mainly driven by the EUR leg. It is becoming increasingly evident that the SNB will continue to intervene in FX markets over major risk events. This policy stops CHF from strengthening for now. The EURUSD will also remain a driver of the EURCHF. The UK Prime Minister May announcement of a snap general election on June 8th is a game-changer for the GBP. This early general election is the only way to resolve the political impasse the UK government faces in conducting Brexit negotiations. This is the best default scenario, as it makes the deadline to deliver a "clean" Brexit far less pressing, it dilutes the influence of hard Brexit partisans, and it strengthens the PM. This reduces downside risks for the UK growth outlook over Brexit negotiations. Long-term investors are still short, which needs to adjust. On the long term, valuation metrics are still highlighting a large discount.

Tighter Chinese monetary conditions will impact its trading partners The most exposed are the commodity related currencies. Tighter financial conditions in China to spill over first to Australia. The AUD breaking below 0.7450 has added a technical bearish momentum factor for this pair, on top of falling iron ore prices. According to the CFTC, the market is currently long AUD, which we think needs to adjust. The PBoC has eased restrictions on cross border flows considering the improving external growth and higher interbank rates. With the easing of capital restrictions and a repricing of Fed hikes going into the June meeting, the RMB will stabilize. However, a cyclical weakening of growth and PPI in China could weaken the yuan.

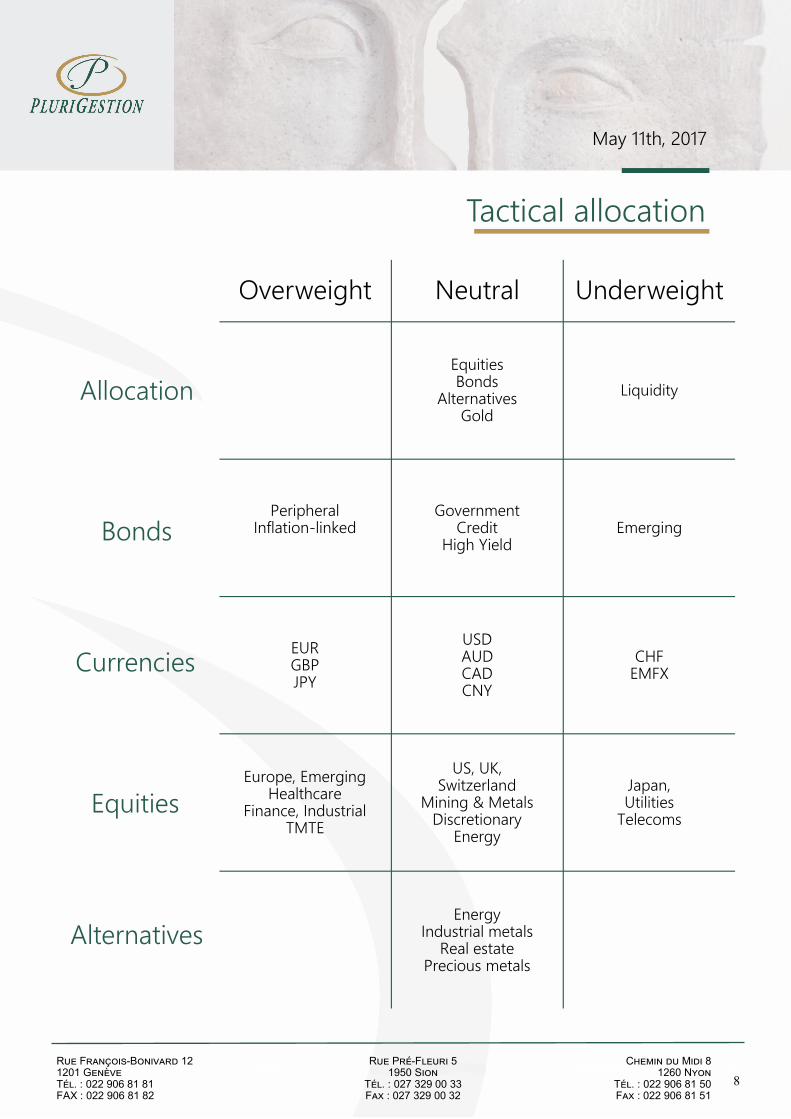

Overweight

EUR, GBP, JPY

Neutral

USD, AUD, CAD, CNY

Underweight

CHF, EM FX

May 11th, 2017

Currencies

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

4

The reflation trade is not over yet In our previous publications, we argued that the Q4/Q1 bond sell-off would pause and that market should experience a gradual setback. We argued that the bond market had got ahead of itself when pricing in ECB rate hikes this year and having fully embraced the Fed’s rate scenario. Furthermore, we highlighted the risk of a setback in risk appetite. The market was already positioned for higher bond yields, the speculative positioning reached multi-year short level, and expectations of economic data strengthening were high. It seems that many manufacturing indicators are at, or close to, record-high levels and it is almost inevitable that they will recede somewhat. The bond market has already discounted this mean-reverting process. In that context, we got a strong global bond rally. 10-year German yields have traded as low as 0.15% and 10-year US Treasury yields have fallen from above 2.60% at the peak in March to below 2.30%. The question now is whether this bond rally is mature or will continue. We believe that yields have corrected enough and will not continue to fall. We continue to see 2 more rate hikes from the Fed in 2017 and ongoing discussions regarding the Fed changing its reinvestment policy. The latter would work as a tightening of the monetary policy and push long-dated yields higher. Expectations around the ECB tightening are also clearly too low. A month ago, many investors were positioned for a move higher in rates particularly in the US. According to positioning data, investors were caught on the wrong foot as yields started to move lower. The short covering probably accelerated to move yields lower. Positioning is back to “long” exposure. It means it is more difficult to push yields lower once all investors are well loaded. Now, there is room for yields to move higher. At the same time, the BoJ has just begun a silent tapering. While it kept its guidance to purchase JGBs at the rate of 80 trillion yen per year, the current pace is more around 70. Unclear monetary policy communication will not drive supportive inflows in the asset class.

The stoplight for reflation has turned positive again… Market conditions for break-evens were mixed. Risk sentiment is supported by the renewed focus on the possibility of tax reform in the US, on robust economic data and the outcome of the French presidential election. Against that, crude oil prices fell back towards the lows seen in Q4 2016, putting downward pressure on near term inflation expectations. Euro area inflation increased to 1.9% in April from 1.5% in March, while core inflation jumped to 1.2% from 0.7%, thereby reaching the highest level in 4 years. The higher core inflation reflected higher service price inflation. The question remains whether the higher service price inflation reflects a rise in underlying price pressure, which would change the ECB monetary policy stance. The higher service price inflation is clearly good news for the ECB, but given that much of the rise seems to be due to the seasonality it is not structural yet. We need a confirmation. If the trend is confirmed, the next step will be another reduction of the ECB monthly purchases. Market expectations make inflation linked bonds still attractive, as well as European peripheral government debts.

There is more to come on the credit The credit markets finally broke out of the ranges where they had been stuck for months and rallied sharply following the French election results. After weeks of barely moving the credit market tightened. Higher beta corporate sectors fared even better than the HY market and will continue to do so. We do not hide our preference for the high beta sectors (including the Cocos) against the HY market which we consider expensive at current levels, due to liquidity squeeze. The credit market rally should continue, as there are no major hurdles to hamper its progress. We see nothing on the horizon other than the ECB’s decision to further reduce its QE. The US market also gained ground but by a much smaller amount, highlighting its distance from the recent uncertainty sources. Still, we expect the market to improve gradually as there is little to hamper the rally.

Overweight

Peripheral Inflation-linked

Neutral

Government Credit

High Yield

Underweight

Emerging

May 11th, 2017

Bonds

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

5

Equity markets in risk-on mode

Investors are not willing to visit the dark side of the force, the risk-off Some indices have surpassed or are on their historic highs such as the Dow Jones, Nasdaq, S&P 500, FT100, SPI, DAX, Sensex and OBX, which could raise fears of an imminent correction of stock market indices. This argument alone is not sufficient, neither from a technical nor a fundamental point of view.

With the election of Donald Trump, there is of course a rupture - perhaps not the one expected - where everything and the opposite are said, but that drives investors to keep shares in case of Donald Trump would manage to concretize one of its measures, including its tax reform announced in broad outline. The dominant fear today is the fear of missing future gains rather than a major correction! On the European side, the elections in France and Germany could have an impact on a new governance of Europe. Without minimizing the geopolitical risks and uncertainties associated with Donald Trump, the environment remains favorable to equities. In addition, the calm returning on the dollar and on US interest rates is a positive factor that reduces volatility for the stock markets. Regarding emerging equities, the current consolidation/correction of industrial metal and oil prices, as well as signs of a slowing economic growth in China, should warrant more caution in the short term.

Valuations (PE ratios) are high for some indices, as for the US, Switzerland, Mexico, New Zealand, but not in bubble zones. Moreover, in an environment of rising profits and contained inflation, PER levels are justified and could even increase further. Growth in profits and revenues in the first quarter of 2017 proved to be stronger than anticipated. In the United States, profits will grow by more than 14% and revenues by more than 8%. In Europe, growth rates will be even higher. The same trend is expected in the second quarter. For 2017 and 2018, analysts expect annual profits to increase between 8% and 10% in developed countries and between 10% and 12% in emerging ones. The rise in profits is the driving force behind stock markets. The zero to negative stock market performance between April 2015 and October 2016 was explained by a recessionary period of profits. Today, we are in a phase of accelerating earning growth. Emerging equities are globally more attractive in terms of PER, between 8x (Russia, Eastern Europe) and 14x (Latin America) 2017 profits. The euro area is also interesting with 15.5x 2017, and it is in the process of reducing its risk premium linked to European problems (Brexit, governance, immigration). Although the valuation of the US stock market is high, we have increased our S&P 500 target level from 2,490 to 2,560 in 2017. The Euro Stoxx 50 index can reach the highest historical levels in 2018, based on a new European governance after the shock of the Brexit and the rise of populist movements; if conditions are met, a Euro Stoxx 50 returning on 4'900 (+35%) is possible.

In a still low interest rate environment, even though the Fed will very gradually normalize its monetary policy, equity markets remain attractive in comparison to bond markets in terms of both dividend yields and earning yields (1/PER). It would require a significant increase in interest rates to put stock markets at risk; we are far away. The ratios are so in favor of shares: it would take the US 10-year around 4% to endanger the bull market started 8 years ago.

The European stock market has clearly been penalized in recent years because of the risks linked to bad governance in Europe. Since the beginning of the bull market (March 10, 2009), the S&P 500 has increased by 224% against 80% for the Euro Stoxx 50. With the arrival of new political leaders and waning fears of populist movements taking over, there is renewed hope for a more integrated Europe. A new European project would be a positive element for the stock exchanges, with one of the big beneficiaries being the banking sector. In 2017, the Swiss stock market outperformed its European peers, but strongly influenced by the strong performances of the small and mid-cap market segment. Switzerland is relatively expensive and it becomes more difficult to find attractive equities. The safe-haven premium for Swiss assets is expected to fall with better prospects in the euro area. In conclusion, we overweight euro area assets due to the evacuation of political risks and systemic risk on the euro. Defence is certainly a topical issue. The geopolitical risks and the under-equipment of certain armies, in Europe in particular, result in an increase in defence expenditure. We favor growth sectors, Pharma and Technology, less sensitive to economic cycles. Luxury seems to emerge from the crisis.

Overweight

Europe, Emerging Healthcare, Energy

Finance, Industrial, TMTE

Neutral

US, UK, Switzerland

Mining & Metals Discretionary

Underweight

Japan Utilities, Telecoms

May 11th, 2017

Equities

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

6

Bonds & FX valuations are a source of concern Emerging market corporate ratings will not improve in 2017 despite an improvement in many of the fundamentals that drove the downgrades in 2016. EM will still face a set of challenges over the coming years. In 2016, EM corporate downgrades outnumbered upgrades by 3 to 1. On the commodities front, we believe that the mini-boom in many hard commodities in early 2017 was overstated, but that prices will not fall back as far as their recent lows. EM corporates will also see new challenges in the coming months with the “America First” Trump policy. So far, it appears that policies will be more targeted than initially suggested, but the situation is still unclear. Expectations of rising US rates are likely to lead to rising borrowing costs for some EM borrowers. This could challenge debt service and refinancing capacity of EM hard currency borrowers where there are not appropriate hedges with hard currency earnings. The prospects for EM corporate ratings remain much more negative than for developed market entities. At end-2016, a net 18% of EM ratings were on negative outlook, indicating the likely direction of rating activity in the next months. EM credit valuations are too expensive compared to fundamentals and alternative credit investments.

External environment has supported EM FX… With stable developed markets rates, a relatively weak USD, a robust global growth and reduced risks of US trade protectionism measures, EM currencies could benefit from this favorable landscape. That being said, EM FX has already significantly rallied and we are turning more cautious/selective due to unattractive positioning and valuation. Many high yielding currencies have already significantly rallied over the past year, now exhibiting overvaluation and stretched positioning, or higher political risks. Furthermore, current expectations for US fiscal policy implementation are low and market pricing for the Fed over the next year is relatively dovish, so the risk is skewed towards a negative surprise. Therefore, in spite of offsetting factors such as a broadly supportive external environment, the positioning/valuation concerns lead us to become more selective in our choice of EM longs. While there is probably some more room for EM FX to rally, the next (potentially last) leg of the rally will be concentrated in the few currencies which still have attract ive valuations, limited positioning and have lagged the EM FX rally thus far.

The stability of the US dollar and interest rates, as well as strong economic growth in China in Q1 and the good behavior of commodity prices, enabled emerging equities to outperform developed countries. In the short term, three factors could force a consolidation in emerging markets: 1) the Chinese economy appears to be slowing down due to government action to calm overheated real estate, 2) industrial metal and oil prices are in a corrective phase and could affect emerging assets and 3) the Fed is expected to increase rates in June. Equities Asia. China. After a strong Q1 thanks to real estate and infrastructure spending, the Chinese economy is expected to slow down. The latest activity indicators, from consumer and business surveys, indicate a slowdown, triggered by a liquidity squeeze from the PBoC to contain the rise in real estate prices and to slow down the issuance of new financial products. In the long run, the strategy of increasing China's influence in world trade will require enormous infrastructure projects. China has a $900 billion investment plan, One Belt, One Road (Obor), to link Europe and Africa by trains and ships, a geo-economic plan that should change the center of gravity of trade world. In the short term, the CSI300 index lost 4% in one month, in line with industrial and oil prices. The liquidity squeeze by the PBoC may still weigh on commodity prices, hence on Chinese equities. There is a positive potential factor: in June, MSCI will decide whether or not to integrate domestic Chinese equities into global indices. India. We remain positive, as its stock market is less correlated to commodities and more focused on economic fundamentals. After a successful demonetization, the government and the central bank are tackling non-performing bank loans. The Sensex index has broken out its resistance. Equities Russia/Eastern Europe. Russia. The Russian index has declined by 12% over the last 3 months, which corresponds to the end of the rally on oil prices. Again, emerging stock markets are correlated with commodity prices. Russian shares are cheap, but the lack of visibility on the evolution of oil urges to be cautious. Eastern Europe. We favor this region whose good economic performance is reflected in the rise in currencies. As for Russia, valuations are low, but visibility is better. Equities. Latin America. Mexico remains under pressure with the renegotiation of the NAFTA agreement. The current government is unpopular and is not in a position of strength vis-à-vis the United States. Brazil is undergoing a very controversial overhaul on pension funds by the population, which could lead to a major crisis, while the IMF considers this overhaul indispensable.

May 11th, 2017

Emerging

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

7

Precious metals: Neutral

After reaching the $1,290, gold came back to $1,228. Geopolitical tensions (North Korea, Syria) and doubts about the implementation of the Trump program have faded. A better global economy and an increase in Fed Funds in June are negative factors for gold. Nevertheless, gold remains a good diversification as geopolitical insurance. The World Gold Council announced that demand for gold fell by 18% in the Q1 2017 compared to the same period last year. The technical breakdown of the $1'250 support could lead to $ 1'170.

Industrial metals: Neutral

Industrial metal prices decreased with weakening Chinese manufacturing data and liquidity squeeze by the PBoC to curb credit. China accounts for 40%-50% of global demand for industrial metals. Today, the biggest futures contracts on commodities are traded on the Chinese financial place ; therefore, when the financial conditions are accommodative, the Chinese buy and store massively and when the conditions become restrictive, they reduce their purchases and live on the accumulated stocks. In the coming months, industrial metal prices are likely to remain under pressure. But in the long run, prices are structurally in a bull trend: 1) new production capacity projects have never been so few, 2) the Chinese strategic plan, One Belt, One Road (Obor), is gigantic and requires $900 billion in infrastructure spending, and 3) there is the possibility to see the $1 trillion Donald Trump infrastructure spending program.

Energy: Neutral After a rally between January 2016 and January 2017, the crude oil price is in a corrective phase with a recent downward acceleration. Since January 2017, Brent has declined to $49 from $57. The OPEC agreement in December 2017 on a reduction in production only had a very short-term effect. Confidence in OPEC's ability to reduce production is fading, oil inventories are rising and US production from shale gas/oil is much higher than expected. Few investors want to bet on a rise in oil prices, while US shale producers have shown that they can increase their production with lower prices. The fall in oil prices also coincided with a recent weakness in Chinese manufacturing figures, raising fears of lower demand. The political aspect of oil adds uncertainty. On May 25th in Vienna, OPEC will meet on whether or not to renew the agreement on production. However, we will enter into a more favorable period to a decline in inventories with the beginning of the driving season in the United States and the summer approaching that will increase the use of the air conditioners. The technical break of the support at $52 for the Brent opened the door to $45. The decline was accelerated with the unwinding of big long positions on oil coming from hedge funds.

Real estate: Neutral

The MSCI US REITs Index posted negative performance. Investors are opting for a long Amazon (e-commerce)-short traditional retailers bet. Commercial real estate has to be avoided. Residential real estate remains a good alternative in a low interest rate environment. Residential real estate in Canada, that has been overheated for some time, is showing signs of correction. In such an environment, we do not buy Canadian banks. Real estate prices in UK registered their first decline over three months between February and April since 2012: the sector suffers from high prices, a lower job creation and the effects of rising inflation. Otherwise, the MSCI World REITs is doing well, showing that there are still interesting regions such as the euro zone and the US residential.

May 11th, 2017

Alternative Investments

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

8

Allocation

Overweight Neutral Underweight

Equities Bonds

Alternatives Gold

Liquidity

Peripheral Inflation-linked

Government Credit

High Yield Emerging

EUR GBP JPY

USD AUD CAD CNY

CHF EMFX

Europe, Emerging Healthcare

Finance, Industrial TMTE

US, UK, Switzerland

Mining & Metals Discretionary

Energy

Japan, Utilities

Telecoms

Energy Industrial metals

Real estate Precious metals

Bonds

Currencies

Equities

Alternatives

Tactical allocation

May 11th, 2017

Rue François-Bonivard 12 1201 Genève Tél. : 022 906 81 81 FAX : 022 906 81 82

Rue Pré-Fleuri 5 1950 Sion

Tél. : 027 329 00 33 Fax : 027 329 00 32

Chemin du Midi 8 1260 Nyon

Tél. : 022 906 81 50 Fax : 022 906 81 51

9

Disclaimer This document is solely for your information and under no circumstances is it to be used or considered as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. All information and opinions contained herein has been compiled from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to their accuracy or completeness. The analysis contained herein is based on numerous assumptions and different assumptions could result in materially different results. Past performance of an investment is no guarantee for its future performance. This document is provided solely for the information of professional investors who are expected to make their own investment decisions without undue reliance on its contents. This document may not be reproduced, distributed or published without prior au-thority of Plurigestion SA.

May 11th, 2017