investment - kpmg | de · the information contained herein is of a general nature and is not...

TRANSCRIPT

Investment in Korea KPMG IN KOREA

AUDIT ▪ TAX ▪ ADVISORY

This booklet has been prepared by: Samjong KPMG ERI, Inc. 10th Fl., Star Tower 737 Yeoksam-dong, Gangnam-gu Seoul 135-984 Republic of Korea Tel: 82 2 2122 0001 Fax: 82 2 2122 0002 The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation. © 2007 Samjong KPMG Inc., Korean member firm of KPMG International, a Swiss cooperative. All rights reserved. Printed in Korea.

Preface

Investment in Korea is one of a series of booklets prepared by KPMG and designed to provide information of interest to those considering investing or doing business in various countries. This publication has been prepared by Samjong KPMG Inc., located in South Korea. The information presented in this publication is of a general nature and should only be used as a guide for preliminary planning purposes. The Korean businesses and the regulatory environments are rapidly developing and changing. The information in this booklet is current as of January 2007; however changes in laws and regulations subsequent to publication could effect the information provided herein. Comprehensive professional advice should be obtained before embarking on any plan of investment. KPMG would be pleased to assist you. For further information on investing in Korea or other publications on taxation, industries or regulations in Korea, please contact any of our offices. Samjong KPMG Inc. Seoul, January 2007

Why Invest in South Korea? According to the Ministry of Finance and Economy (www.investkorea.org) there are 10 reasons why investors choose Korea. 1. Talented Human Resources 97% of Korea’s work force has acquired at least a high school diploma, while people entering tertiary forms of schooling is constantly on the rise. 2. Substantial Domestic Economy

Foreign Exchange Holdings USD 210.4billion 4th in the World GDP USD 787.5billion 12th among OECD

Export USD 284.4billion 12th among OECD Import USD 261.2billion 13th among OECD

Source: InvestKOREA (KOTRA), 2004 3. Excellent Profitability According to the Samsung Economic Research Institute (SERI), the net profit rate of Korea’s top 100 companies was at 6.7%, 1.3% higher than the top 100 global companies. 4. Advanced IT Environment

Digital Access Index 0.82 4th in the World

Internet Users 33.9million (67% of population)

7th in the World

Information Society Index*

20th in Computer 1st in Telecom 5th in Internet 23rd in Social

Overall 8th in the World

Source: InvestKOREA 2004, * - IDC Worldwide IT 2006

Why Invest in South Korea? (cont…) 5. Strategic Regional Location Korea located between Japan and China, has access to more than 51 cities with populations more than 1 million all within a 4 hour flight time. Some of the major players that surround Korea include Beijing, Shanghai, Hong Kong, Tokyo, and Vladivostok. 6. Creativity & Innovation

R & D Capability USD 10.15billion 6th in the World Total Expenditure % of GDP 2.6% 8th in the World

Patents Granted to Residents 29,363 3rd in the World Patent Productivity 187 3rd in the World

Source: InvestKOREA (KOTRA), 2004 7. State-of-the-Art Infrastructure

International Airports

Incheon International

2004 Best Airport 6th Largest Cargo Handler

13th Largest Passenger Handling Incheon Port 13.9% Annual Growth

Busan Port 3rd Largest Port Worldwide 9.9% Annual Growth Ports

Gwangyong Port

10.9% Annual Growth

Ground Transportations KTX 5th High Speed Train in World Made

2.5 Hours distance throughout Korea Source: InvestKOREA (KOTRA), 2004

Why Invest in South Korea? (cont…) 8. World-Class Multinational Companies 12 Korean companies are listed in the Top 500 Global as of July 2006. The list includes: Samsung Electronics, LG, Hyundai Motors, SK, Samsung Life Insurance, POSCO, Korea Electric Power, Kookmin Bank, Hanwha, KT, Samsung, and SK Networks. 9. Strong Government Support Acts including the Foreign Investment Promotion Act (FIPA) and the Restriction of Preferential Taxation Act (RPTA) stand to support foreign investment. As explained in more detail in subsequent chapters, the Government has setup various Free Economic Zones or Sites with various incentives for foreign investors to choose Korea as their site of investment. The government is additionally moving forward to provide Investment Ombudsman, which aims to foster a favorable business environment, and to upgrade living conditions. 10. Stimulating Lifestyle As a former host of the World Cup in 2002 and the Olympics in 1988 (with a possibility of hosting the Winter Olympics in 2014), Korea has clearly been demonstrating prosperity and unity. Korea is also in the processing of establishing easier methods by which foreigners can obtain housing, foreign medical services and immigration in addition to the services currently already provided such as foreign schools. NOTE: The data contained on this list has been obtained from the Invest KOREA website (www.investkorea.org). For further information, please refer to the website.

Contents

Chapter 1 Overview of South Korea 1 Geography and Climate .................................................... 1 Population and Language ................................................. 1 Currency ........................................................................... 2 Historical Background....................................................... 2 Government...................................................................... 3 Religions........................................................................... 4

Chapter 2 Economy of South Korea 5 Overview .......................................................................... 5 Financial Services............................................................. 7 Information Technology................................................... 16 Travel & Tourism.............................................................. 17 Consumer & Retail Markets ........................................... 18 Automotive ..................................................................... 19 Utilities & Energy............................................................ 20 Healthcare ...................................................................... 22

Chapter 3 Investment Incentives in Korea 23 General Information........................................................ 23 Foreign Investment Promotion Act (FIPA) ...................... 23 Foreign Exchange Transactions Act................................. 25 Foreign Trade in Korea .................................................... 26 Foreign Investment Procedures ..................................... 27 Industries to Invest In..................................................... 29 Investment Tax Incentives .............................................. 29 Advanced Technology Incentives .................................... 30 Special Zones for Investments ....................................... 30 Foreign Investment Zones (FIZ)...................................... 30 Industrial Complex FIZ’s ................................................. 32 Free Trade Zones (FTZ) ................................................... 34 Free Economic Zones (FEZ)............................................ 36 Other Incentives............................................................. 38

Chapter 4 Doing Business in Korea 40 Introduction .................................................................... 40 Legal Environment.......................................................... 40 Protection of Intellectual Property Rights....................... 45 Forms of Business Enterprise ........................................ 47 Insolvency Proceedings.................................................. 51 Accounting and Auditing................................................. 53

Chapter 5 Korean Taxation 55 I. Tax Overview .............................................................. 55 Tax Administration .......................................................... 57 Tax Treaties ..................................................................... 57 II. Taxation of Individuals.............................................. 58 Resident Income Taxation............................................... 58 Non-Resident Income Taxation ....................................... 58 Tax Rates & Credits ........................................................ 59 Withholding Taxes........................................................... 61 III. Taxation of Businesses ............................................ 63 Overview ........................................................................ 63 Taxpayer ......................................................................... 63 Permanent Establishment .............................................. 64 Place of Tax Payment...................................................... 64 Taxable Income............................................................... 65 Tax Gains ........................................................................ 65 Tax Losses...................................................................... 65 Double Taxation on Dividend on Income ........................ 66 Tax Base ......................................................................... 67 Tax Rates & Credits ........................................................ 68 Tax Returns & Payments ................................................ 68 Withholding Taxes........................................................... 69 Taxation of Liquidation Income....................................... 69 Taxes on Foreign Companies.......................................... 70 Transfer pricing ............................................................... 72 Thin Capitalization........................................................... 72 IV. Value Added Tax (VAT) ............................................. 73 V. Other Taxes................................................................ 75

Chapter 6 Labor Regulations 76 Introduction .................................................................... 76 Labor Regulations........................................................... 76 Hours & Wages .............................................................. 78 Women & Minors ........................................................... 79

Fringe Benefits ............................................................... 79 Vacation / Leave.............................................................. 79 Retirement ..................................................................... 80 Social Insurance ............................................................. 81 Other Employment Issues ............................................. 82

Chapter 7 Life in Korea 85 General Information........................................................ 85 Cultural Considerations .................................................. 85 Work and Residence Permits ......................................... 89 Customs Clearance of Household Effects...................... 89 Postal Service................................................................. 90 Hotels Accommodations ................................................ 90 Major Holidays................................................................ 91 Foreign Schools .............................................................. 91 Housing in Korea ............................................................ 91 Transportation................................................................. 92 Medical Facilities ............................................................ 93

Appendix 94

Chapter 1

Overview of South Korea Geography and Climate The Republic of Korea covers the southern part of a peninsula which juts down from the northeastern edge of Asia. It occupies an area of approximately 99,000 square kilometers, roughly equivalent to the size of Britain. In terms of topography, the low hills in the south and west gradually change to higher mountains toward the east coast and north. It is interesting to note that almost 70% of South Korea is occupied by mountainous areas. Korea’s western and southern coasts are irregular, with many inlets, small peninsulas, and bays, while the eastern coastline is relatively straight. Korea has Russia and China to its north and west, with Japan located to the southeast. South Korea has four distinct seasons. Spring is mostly clear and pleasant with temperatures ranging from 16°C to 19°C. The spring is then followed by a hot and humid summer with a short period of monsoon rains. The daytime high temperature is usually over 30°C. Meanwhile, autumn is crisp and cool and the winters tend to be cold and dry. Annual rainfall average more than 100 centimeters; two-thirds of precipitation falls between June and September when the country is afflicted by typhoons. Population and Language With approximately over 48.5 million people as of 2006, Korea is one of the most densely populated countries in the world. The population is concentrated in the capital city, Seoul, with over 10 million people, followed by the southern port city of Busan with approximately 3.6 million people. Seoul has become one of the largest cities in the world and is the home to nearly one-quarter of the country’s population. Seoul is not only the focus of the administrative, social, and cultural activities in Korea but is also the center of the largest industrial activity.

1

A large number of Korean corporation’s headquarters and government offices are located in Seoul. However, in recent years, there has been a large increase in development outside of Seoul with the government encouraging investments in “special zones.” To address the concerns that accompany rapid population growth, the Korean government is implementing several decentralization programs. Those plans include substantial extension of the Seoul subway system and the relocation of government offices to satellite cities. The official language is Korean. Although Korean includes many Chinese words and is similar in many ways to Japanese grammar, it is actually a distinct language belonging to the Ural-Altaic group. Most educated Koreans speak at least basic English; and little English is spoken outside major cities or industrial areas. A large number of the elderly population is also fluent in Japanese. Currency The basic unit is the Korean won (KRW, ₩) which is issued in paper notes of KRW 1,000, 5,000, and 10,000. Cash equivalent checks valued at KRW 100,000 are also regularly used for larger purchases. Coins are denominated as KRW 10, 50, and 500. The won-dollar exchange rate has fluctuated since the won was pegged to currencies from Korea’s major trading partners. The exchange rate as of December 2006 is approximately KRW 930 to USD 1, and has risen within the last several years. Historical Background Korea has had many notable accomplishments over the centuries including the construction of an astronomy observatory 8th century, the development of the famed blue-green celadon ceramics, the use of movable metals in 1234, the development of the Hangul phonetic alphabet, and the invention of the first ironclad warship in 1592. South Korea is an ancient country with a young industrial tradition. Korea has a documented history that dates back to 2760 B.C. with a legendary origin in which the Tung-i, or eastern bowmen-barbarians, spread through Manchuria to the Korean peninsula in the third millennium B.C. The Koreans have nurtured a district culture in spite of invasions and occupations by the Chinese and Japanese. In 1910, Korea fell under the control of the Japanese and was ruled as a colony until the end of World War II.

2

Following liberation from Japan in 1945, the peninsula was divided at the 38th parallel with the Soviet forces occupying the northern half and the United Nations forces installed in the south. The partition led to the establishment of a communist regime in the north and a constitutional republic in the south. In June of 1950, the Korean War began and lasted for three years. Since the signing of an armistice in 1953, the countries have been separated by a demilitarized zone (DMZ). Government Since 2003, Korea has entered its 16th Presidency. The 17th President will be elected at the end of 2007 by direct popular vote and the new President will begin a single five-year term in 2008. Almost all of the National Assembly members are elected by popular vote for a four-year-term and the rest are appointed by political parties according to a proportional formula. Korea’s government has taken a constitutional form first beginning in 1948, and has lasted until today. The president holds the highest position in the Korean government. The country’s most recent constitution, adopted in a national referendum in late 1987, includes provisions for direct election of the president. Under the constitution, the president is limited to a single five-year term. In 1988, the government initiated a revision of the Local Autonomy Act. The division was made to ease the transition from a centralized system of government to local autonomy. As of 2006, these local administrative heads of government are elected for a four-year term for a maximum of three terms. The president appoints a prime minister, subject to confirmation by the National Assembly. The prime minister then appoints three deputy prime ministers each responsible for Finance & Economy, Education & Human Resources, and Science & Technology. A State Council is then appointed by the President and the National Assembly. The president presides over cabinet meetings and also serves as the commander-in-chief of the Armed Forces. He can exercise emergency powers in case of threats to national security or grave economic crises. However, the National Assembly must concur in the exercise of these powers. Legislative powers rest with the National Assembly, a single body of 299 members who serve four-year terms. 243 members are elected by regional vote and the other remaining 56 are distributed by popular representation.

3

The National Assembly is designed to create and implement new laws. Additionally, the National Assembly’s approval is required to pass the National Budget, authorize the issuance of government bonds, ratify treaties, review the administrative activities of the executive branch, as well as initiate and approve legislation. In its oversight of the administration, the Assembly may require testimony from officials and is empowered to remove them from office. The Constitution also grants the National Assembly the power to impeach the President. The judiciary is a separate branch of government, which is structured in three tiers. Cases are first tried in district courts or the family courts and then in appellate courts. The Supreme Court is the highest judicial tribunal where appeals from the lower courts and from court-martials. The Chief Justice of the Supreme Court is appointed by the President with the consent of the National Assembly. Other Supreme Court judges are appointed by the President. The chief justice appoints all other judges. Korea has adopted a civil law system, which does not utilize a jury. Religions South Korea guarantees the freedom of religion. While there are diverse religious traditions in Korea, the principal religions are Buddhism and Christianity which make up approximately 50% of the population. A small percentage of the population practices Confucianism or Shamanism, while a majority of the rest is non-affiliated.

4

Chapter 2

Economy of South Korea Overview The World Bank has recognized the growth that Korea has experienced from 1962 has been defined as “One of the outstanding success stories of international development.” Korea’s economy was close to the bottom of the international income scale. Without the benefit of principal natural resources; Korea launched itself upon a bold series of 5-year economic development programs and in slightly more than two decades, Korea has transformed from a marginally subsistent agricultural economy into one of Asia’s major industrial nations. Below represents the major economic indicators of South Korea:

Summary of Primary Economic Indicators

Category 2003 2004 2005 2006f Population (mill) 47.9 48.0 48.1 48.3 GDP (USD bil) 608 681 787 - GDP growth 3.1 4.7 4.0 5.0* GDP per capita (USD) 12,720 14,193 16,291 - Exports (USD bil) 193.7 253.7 284.5 327.9** Imports (USD bil) 178.8 224.1 261.3 300.4** Trade Balance (USD bil) 14.9 29.4 23.2 27.5** CPI (% y/y avg) 3.5 3.6 2.7 3.0** Current Acct. Bal.(USD bil) 14.1 32.2 17.0 6.741** Foreign Reserves (USD bil) 137.3 199.1 210.4 235.0** Unemployment Rate 3.6 3.7 3.7 3.5* FDI (USD bill) 6.47 12.79 11.56 11.23* No. of FDI cases 2,564 3,075 3,668 - Source: Korea National Statistical Office * = Ministry of Finance and Economy **=CIA World Factbook (f = forecast)

5

By the end of 1997, real GNP, growing at an average rate of 7.5% per annum since 1970 (average rate of 11.5% during the years 1991 through 1996), rose from USD 7.9 billion to USD 437 billion based on current prices, while per capita GNP, in current prices, had increased from USD 253 to USD 9,511 one of the highest rates of sustained growth in modern economic history. Although Korea’s rapid growth has clearly been attributable to a number of interacting economic, political and social factors which cannot be easily quantified, it is possible to single out one key element; valuable human resources – namely well educated, highly motivated and industrious people. Additionally, the international trade and export-oriented policy for economic development have played key roles in maintaining the rapid growth of the Korean economy. This rapid growth during the last decade has resulted in inflationary effects on the domestic economy, which monetary planners have tried to control. The consumer price index at the end of 1998 had increased by 7.5% over the 1997 year-end level. However, a tight monetary policy limited the increase in price levels to 0.8% during 1999, 2.3% during 2000 and to 4.1% during 2001. As of 2005 the CPI stood at 2.7%, and decreased to about 2.5% in 2006. Korea applied to join the Organization for Economic Cooperation and Development (OECD) in 1995 and was admitted in 1996. To comply with OECD requirements, the Korean government has been taking steps toward trade and foreign exchange liberalization. These steps include the 1992 membership status within the General Agreement on Tariffs and Trade (GATT), lifting the quantitative import restrictions permitted to be imposed on developing countries. Korea also became an Article 8 member of International Monetary Fund (IMF) in 1989. Due to the excessive expansion of the private sector, funded in part by excessive loans from financial institutions without proper scrutiny, Korea encountered a period of financial difficulty. From late 1997, the nation experienced its worst financial crisis since 1980 with nose-diving stock prices, a soaring foreign exchange rate, and the winding up of troubled companies and ailing financial institutions. The nation and its people struggled to overcome the crisis. In December 1997, Korea received assistance from the IMF. This is dramatically exemplified by the participation of many people in a nationwide campaign to collect gold for export (to secure foreign currency liquidity). As a result, the nation's foreign currency reserves started to build and by the end of 1998, the economy started to recover. With the complete repayment of its IMF bailout loan of USD 19.5 billion in August 2001, Korea completed the IMF workout program. Reflecting this improvement in 2002, economic indicators have also recovered to pre-currency crisis levels. For example, the nation’s GDP growth rate recorded 10.7% in 1999, 8.7% in 2000 and 3.0% in 2001, after

6

marking negative 6.7% in 1998. The unemployment rate was recorded at 6.8% in 1998, 6.3% in 1999, 4.1% in 2000 and 3.4% in 2001. The unemployment rate as of 2005 stands at 3.6~3.7%. The year of 2004 marked a significant jump in recent years, where GDP growth peaked over 4.7% from 2004, and continues to sustain a reasonable GDP growth. Also, Foreign Direct Investment (FDI) has had a significant increase, almost doubling in the total amount of foreign investing in 2003. In 2005, the overall growth rate of GDP was at a respectable 4.0% along with a per capita GDP that reached over USD 16,000. The economy for 2006 to 2007 continues on a relatively stable path, facing major issues such as the Free Trade Agreement with the United States and new growth opportunities in the global markets. Financial Services The financial services industry in Korea has been on the rise over the years after the financial crisis in 1997. The sector has clearly undergone consolidation on a large-scale where stronger firms have merged or acquired weaker ones, while firms that failed to sustain growth were eventually forced to close. Nevertheless, the financial service industry provides a wide array of opportunities in financial markets, banking, and insurance.

Total Assets of the Financial Market Sector (Unit: KRW Billion)

2005 2006 Sector Q2 Q3 Q4 Q1 SQ2

Banking* 750,485 773,907 774,825 809,071 840,172 Life Insurance 217,071 224,031 234,766 239,362 246,073

Property / Casualty 45,122 46,763 49,019 49,407 51,032 Securities 64,865 70,071 73,060 68,227 88,144

Futures 995 1,164 1,177 1,273 1,365 Asset Management 1,500 1,593 1,622 1,798 1,842

Investment Management 189 207 239 264 281

Credit Cards 26,923 27,418 29,487 29,424 30,016 Source: FSIS (Financial Statistics Information System), * - Commercial Banks Only

7

Financial Market Share by Sector

(Basis: 2006 (Q1 & Q2), Share in Total Assets)

Life Ins., 19.05%Property/Casualty

3.94%

Securities, 6.14%

Futures, 0.10%

Asset Mgmt.,0.14%

Investment Mgmt.,0.02%

Credit Cards,2.33%

Mut. Sav. Bank,3.56%

Banking*, 64.72%

Source: FSIS (Financial Statistics Information System), * - Commercial Banks Only Financial Markets The Korea Exchange (KRX) was formed under the Korea Stock & Futures Exchange Act. Under the KRX, there exist three primary markets which include the Korea Stock Exchange, Korea Securities Dealer Automated Quotations (Kosdaq), and Korea Futures Exchange (KOFEX). KSE is the primary securities market for the trading of stocks and bonds, while Kosdaq is geared more towards supporting high-tech companies and small and medium-sized enterprises (SME) to raise funds. There are currently 731 companies listed on the Korea Stock Exchange (KSE) with a market capitalization of KRW 704.6 trillion as of December 2006 and 963 listed companies on Kosdaq with a market capitalization of KRW 72.14 trillion. The size of foreign investors on the Korea Stock Exchange (KSE) is KRW 262.5 trillion and this is a 0.88% (KRW 2.3 trillion) increase from December 2005.

8

Number of Registered Foreign Investors

Category 2002 2003 2004 2005 2006 Individual Investors 5,024 5,242 5,538 5,836 6,235 Institutional Investors 9,104 10,093 11,361 12,663 14,400

Investment Company 6,190 6,752 7,464 8,193 9,008 Pension Fund 874 990 1,131 1,255 1,413 Security Company 388 422 449 489 513 Banks 387 412 435 465 501 Insurance Company 250 268 281 305 321 Other 1,015 1,249 1,601 1,956 2,644

Total 14,128 15,335 16,899 18,499 20,635 Source: FSIS (Financial Statistics Information System) As shown above, the number of foreign investors is dramatically increasing and the current status displays over 20,000 cases. This status is to be reflected by belief that South Korea’s stock market, with the emergence of the three markets, increased the participation of foreign institutions. The overall presence of investors investing in Korea’s securities is also continuously growing. Heightening Prudential Regulation To compete in a fierce global financial environment, Korea adopted major regulatory and institutional changes as a result from their financial crisis in 1997. A single integrated regulatory body, the Financial Supervisory Commission (FSC) was established in 1998 to regulate financial institutions within the domestic sector. Recently, continuous infrastructure reform is focused on consolidating the existing financial acts into the Financial Investment Services and Capital Market Act (FISCMA, Provisional). The separate laws to be consolidated include:

Securities and Exchange Act; Futures Trading Act; Collective Investment (Asset Management) Act; Trust Service Act; Korea Exchange (KRX) Act; Merchant Banking Act; and Corporate Restructuring Vehicle (CRV) Act.

Studying and applying global benchmarks including the Financial Services Act (“Big Bang”) 1986 (UK), Financial Services Reform Act 2001 (Australia), Securities and Futures Act 2002 (Hong Kong, Singapore) and the Financial Instruments and Exchange Law 2006 (Japan), FISCMA is expected to be

9

enforced in 2008 as Korea’s capital market reform legislation. The areas of financial reform act will consolidate include:

Deregulating the scope of investment services; Broadening the definition of investment products; Changing regulatory concepts; and Increasing investors’ protection.

Improving Corporate Governance of Financial Institutions Major regulatory and supervisory reform measures were conducted to enhance corporate governance in financial sectors, especially in the banking industry during the post-crisis period. In December 1997, bank ownership regulations were amended and foreign investors were permitted to own commercial bank shares. Foreign investors in turn were given the authority to own more than the 4% limit which applied to domestic investors. Additionally, in May 1998, the appointment of foreign bank executives was permitted. Non-executive outside directors, audit committees and compliance officer systems were introduced in January 2000 to strengthen governance structure and internal control procedures within commercial banking organizations. Furthermore, the Banking Act was amended in April 2002 to reform bank ownership structure, permitting investors to own up to 10% of bank shares in the case of non-industry linked domestic residents. Various reform measures have also been implemented to upgrade accounting and disclosure systems for commercial banks in order to facilitate monitoring by depositors and investors. The following is a chart of an overall chart of the governance institutions of commercial banks.

10

Governance Institutions of Commercial Banks

Category Board of Directors

Audit Committee

Compliance Officer

Risk Mgmt. Committee

Main Function

Planning and evaluation of management

goals and strategies

Business and accounting

audit

Internal control and monitoring

Establishing and

monitoring of risk

management framework

Compensation Requirement

Three or more non-executive directors(non-

executive directors 50%

or more)

2/3 or more non-

executive directors

One independent

officer -

Appointed by General

shareholders’ meeting

Board of Directors

CEO Board of Directors

Nomination

Nomination committee for non-executive directors(non-

executive directors 50%

or more)

Nomination committee for Audit

Committee members(all

non-executive directors)

- -

Statutory Basis

Commercial Code and

Banking Act

Commercial Code and

Banking Act Banking Act

FSC Regulation

on Supervision of Banking business

Source: The Bank of Korea Banking The overall banking sector in Korea has been undergoing significant changes in recent years, which include the attempt towards the globalization and the merging of commercial banks. Online banking services including internet banking has also increased which has helped Korea to become one of the world leaders.

11

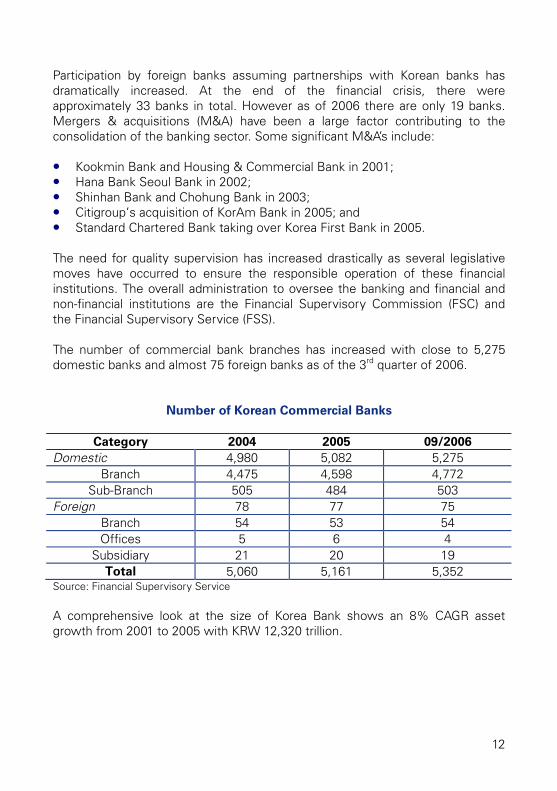

Participation by foreign banks assuming partnerships with Korean banks has dramatically increased. At the end of the financial crisis, there were approximately 33 banks in total. However as of 2006 there are only 19 banks. Mergers & acquisitions (M&A) have been a large factor contributing to the consolidation of the banking sector. Some significant M&A’s include:

Kookmin Bank and Housing & Commercial Bank in 2001; Hana Bank Seoul Bank in 2002; Shinhan Bank and Chohung Bank in 2003; Citigroup’s acquisition of KorAm Bank in 2005; and Standard Chartered Bank taking over Korea First Bank in 2005.

The need for quality supervision has increased drastically as several legislative moves have occurred to ensure the responsible operation of these financial institutions. The overall administration to oversee the banking and financial and non-financial institutions are the Financial Supervisory Commission (FSC) and the Financial Supervisory Service (FSS). The number of commercial bank branches has increased with close to 5,275 domestic banks and almost 75 foreign banks as of the 3rd quarter of 2006.

Number of Korean Commercial Banks

Category 2004 2005 09/2006 Domestic 4,980 5,082 5,275

Branch 4,475 4,598 4,772 Sub-Branch 505 484 503

Foreign 78 77 75 Branch 54 53 54 Offices 5 6 4

Subsidiary 21 20 19 Total 5,060 5,161 5,352

Source: Financial Supervisory Service A comprehensive look at the size of Korea Bank shows an 8% CAGR asset growth from 2001 to 2005 with KRW 12,320 trillion.

12

Return on Assets and Return on Equity

Category 2002 2003 2004 2005 BIS 10.81 10.52 10.40 11.26

ROA, Return on Assets 0.59 0.1 0.89 1.23 ROE, Return on Equity 11.67 2.16 17.96 20.33

Source: Financial Supervisory Service A total of 37 foreign banks are operating services and 13% CAGR asset growth shows a significant improvement in the overall banking sector with respect to both profitability and soundness.

Current M/S of foreign banks in Korea (Basis: Total Assets in 2005)

JP Morgan Chase

9%

Caly on8%

Deutsche8%

ING

7% UBS7%

others

47%

HSBC

14%

Source: Financial Supervisory Service With regard to the adoption of Basel II, the FSS(Financial Supervisory Service) announced that the implementation of the advanced approaches of the New Basel Accord – the advanced internal ratings-based approach (IRB) for credit risk and the advanced measurement approach (AMA) for operational risk – will be required by January 1, 2009 for all domestic banks. The implementation date for the standardized and foundation IRB approaches will remain January 1, 2008, but banks may opt to follow the current capital requirements until the end of 2008.

13

Insurance Korea’s insurance industry stands at the center of dramatic change and innovation. The increase in the number of senior citizens, pensions, health and variable insurances has led to the expansion of the insurance market. The presence of Korea’s insurance industry in the life insurance sector stands to be one of the top in Asia, behind only Japan. There were approximately 22 major insurance companies as of December 2006 and the total premium income for 2005 stood at approximately KRW 47.78 trillion. The following chart shows the overall return on assets for the life insurance and non-life insurance industries.

Return on Assets for Insurance (Return on Assets, ROA)

Category 2003 2004 2005 06/2006

Life Insurance 6.13 7.16 5.5 5.39 Non-Life Insurance 4.11 4.87 4.85 4.1

Source: Financial Supervisory Service According to the graph provided below, Samsung Life Insurance is the largest provider of life insurance services in Korea.

Top Life Insurance Companies by Total Assets (2005) (Unit: KRW Trillion)

101.413

41.742

39.363

8.512

8.204

5.953

5.643

5.616

5.531

4.687

0 20 40 60 80 100 12

Samsung

Korea

Kyobo

Allianz

ING

Dongyang

Mirae Asset Group

Hungkuk

Shinhan

Kumho

0

Source: Financial Supervisory Service

14

Samsung Life has a significant market share lead on competitors such as Korea Life Insurance and even global insurance companies, like that of Germany-based Allianz Life. There were 24 non-life insurance companies operating as of December 2006. In the non-life insurance sector, Samsung Fire and Marine dominates the domestic market with approximately KRW 19.936 trillion in assets. Behind Samsung are Hyundai Fire and Marine followed by Dongbu. Foreign presence in the non-life insurance industry is relatively small compared to other industries. The following is a chart of the top non-life insurance companies by total assets:

Top Non-Life Insurance Companies by Total Assets (2005) (Unit: KRW Trillion)

6.466

5.912

5.651

3.911

3.239

2.77

1.326

1.187

1.032

16.936

0 5 10 15 20

Samsung

Hyundai

Dongbu

LIG

Seoul

Meritz

Korean Reinsurance

Jaeil (First)

Shindonga

Hungkuk Ssangyong

Source: Financial Supervisory Service

In January 2007, the FSS announced that Risk Assessment and Application System (RAAS) for insurance supervision will be implemented beginning in April 2007. RAAS has been pursued since 2003 as part of a wide-ranging plan to shift to risk-based insurance supervision. RAAS will help the insurance industry carry out individually tailored supervision based on the key factors affecting the safety and soundness of insurance companies.

15

Information Technology The information technology (IT) sector within Korea stands as one of the top industries that drive the economic growth of Korea. More importantly, developing technology and being at the forefront of innovation stands as one of the government’s main objectives. As a result, many policies were implemented to promote the growth of the IT sector. During the last decade, the role of the IT industry has also had a helping hand in Korea’s growth in several relative industries making IT an even more essential element to Korea’s economy. Korean ministries like the Ministry of Information and Communications (MIC) actively seek to promote the development of information technology. Technology Statistics The Korean mobile communications market is one of the most advanced in the Asia-Pacific region. As of May 2006, the number of mobile phone service subscribers and Internet users in Korea recorded 39.1 million and 33.0 million respectively. The development of the IT industry in Korea has also resulted in spill-over effects such as stimulating e-commerce, digitalizing the contents industry and revolutionizing distribution. Korea also has one of the largest internet markets (only behind countries like that of the US, Japan, China, and Germany) with close to 33.6 million users which is 68.35% of the total population. The following chart provides some insight into overall internet availability and the technological advancement of Korea.

Korea’s Internet Information

Category 2005 Data Additional Information Number of Internet Users (mill

ppl) 33.58 7th in the World

Percentage of Internet Users 68.35% 4th in World Number of Domains

Registered (.kr) 703,925

Number of High-Speed Internet Users

26.4/100 users 4th in World

Source: National Internet Development Agency of Korea (NIDA)

16

IT Imports & Exports Exports of Korea's IT industry increased from $9.2 billion in 1990 to $78 billion in 2005. At the same time, imports increased from $7.5 billion in 1990 to $44.3 billion in 2005, recording a continuing surplus in the sector's trade balance. The major IT export items are semiconductors, mobile handsets, and LCD panels. In terms of market share, Korean DRAM semiconductors, LCD panels and CDMA standard mobile handsets rank as one of the top in the world. Korean companies like Samsung, LG, or Hynix are spreading their wings overseas playing important roles in the technology sector on a more global scale. The following is a chart of Korea’s IT industry imports and exports which shows a significant increase in exports within the past couple of years.

Korean IT Industry's Imports/Exports (Unit: USD 100 million)

Category 2002 2003 2004 2005 Jan.~May, 2006 Exports 463 572 743 780 441 Imports 309 363 407 443 238 Balance 154 209 336 337 203

Source: Ministry of Communication and Information Travel & Tourism The World Cup in Korea-Japan 2002 has given the chance for Korea’s reputation to expand on a global scale. After the World Cup, the overall number of travelers and tourists who visited Korea has increased steadily reaching over 6 million total visitors in 2005. The travel/tourist market in Korea is at a decent size where in 2004 the number of visitors totaled 5.8 million visitors and reached over 6 million visitors in the year 2005. Overall foreign funds inbound had reached over KRW 6 billion in 2004, showing a modest but nonetheless significant amount of income in the travel/tourism sector. The following is an overall table of the number of visitors from various countries worldwide:

17

Inbound Foreign Travel (by country) and Funds

(Unit: * - USD 1000, No. People) Category/Country 2002 2003 2004 2005

Foreign Funds* 5,918,800 5,343,400 6,053,100 5,649,800 America 459,362 421,602 511,170 530,629 Japan 2,320,837 1,802,542 2,443,070 2,439,809

Overseas Koreans 314,829 287,531 299,895 280,453 Taiwan 136,921 194,586 304,908 351,421

UK 66,696 60,600 65,981 72,581 Other 2,048,823 1,985,901 2,193,114 2,346,871

Total Visitors 5,347,468 4,752,762 5,818,138 6,021,764 Source: Korea Tourist Organization, Korean National Statistical Office Korea’s overall success in the travel & tourism sector is bound to improve as Korea has in recent years built a state-of-the-art airport facility in the Incheon area, establishing itself in a perfect position between China and Japan. In addition to Incheon airport, Korea’s ports have also undergone much development and remained a key factor in the economic development of South Korea. Korea also provides other various tourist attractions such as special ski resorts, shopping districts etc. demonstrating great potential to increase the amount of tourism and foreign investments coming into Korea. Consumer & Retail Markets Korea’s population and relatively high per capita income makes it one of the most attractive countries for consumer goods. Korea’s overall consumer market competition has increased with foreign discount stores entering the Korean market. The number of small supermarkets has been falling and turnover stagnant since the mid-1990s due to the economic recession and the rapidly growing discount store sector. Convenience stores were first introduced in 1988 and grew steadily in numbers until 1997. During the economic crisis, they lost market share to other retailers and many went bankrupt. As of today, many different department stores face consolidation where the large retailers and chains are growing at the expense of smaller neighborhood stores. Small and local stores consist of the majority of retailers in Korea. The liberalization of the retail market has led to major changes in the overall consumer market. Retail markets have changed significantly with the introduction of discount stores operated by foreign chains like that of Carrefour, Wal-Mart, Tesco, and Costco. However, the three giant Korean department

18

stores Lotte, Hyundai, and Shinsegae, remain the largest players and take a bulk of the market share. In recent developments, some foreign chains failed to adapt resulting in US based Wal-Mart’s buyout by the market leader E-mart, and Carrefour also bought out by E-land. Other distribution channels include TV home shopping networks, e-commerce (gmarket, dnshop, auction.co.kr, etc.), door to door sales and catalog sales which is usually linked with TV home shopping. Korea’s highly developed e-commerce makes Korea one of the highest ranked countries in the overall online shopping market. According to the National Statistical Office of Korea, the total in e-commerce sales hit a record high of KRW 13.45 trillion (USD 14.29 billion) with close to 4,531 online businesses. Automotive The Korean automobile market’s production volume is the fifth largest in the world. The recent automobile industry in Korea has increased drastically within the past several years driven by the overseas sales of domestic cars from companies like that of Hyundai-Kia or GM Daewoo. The industry has also undergone much change since the financial crisis in 1997, mainly through mergers & acquisitions demonstrating consolidation in the automotive sectors where Hyundai acquired Kia, Renault acquired Samsung Motors (70% stake), and then GM acquired Daewoo. As a result of Korea’s small domestic market, the export of automobiles is essential for these Korean car companies, making the industry heavily geared towards exports. Hyundai-Kia also account for a majority of the car sales in Korea and also in exports. The following is an overall view of Korea’s production and export market share:

Production M/S Export M/S

Hyundai43.7%

GM Daewoo21.1%

Kia32.4%

RN Samsung0.1%

Ssanyong2.5%

others0.1%

Hyundai45.5%

GM Daewoo17.5%

Kia29.9%

Ssanyong3.7%

RN Samsung3.2% others

0.3%

Source: Korea Automobile Manufactures Association

19

Some characteristics of the overall industry indicate that passenger cars dominate the overall industry making up close to 90% of overall production. The following chart provides an overview of how the Korean automobile industry stands:

Korean Automobile Market

Category 2003 2004 2005 2006*

Total Production 3,177,870 3,469,464 3,699,350 3,493,565 Domestic Sales 1,318,312 1,093,652 1,142,562 1,042,561

Exports 1,814,938 2,379,563 2,586,088 2,404,195 Import 27,441 34,712 46,221 50,563

*2006: January ~ November Source: Korea Automobile Manufacturer Association Utilities & Energy The demand for utilities & energy is very high in comparison to other OECD countries. Oil represents approximately half of all energy sources consumed in Korea, with coal, nuclear power, gas and hydroelectric power occupying the other half. Korea is also heavily reliant on external sources of oil importing an amount equivalent to USD 51,735 million with a majority of imports coming from the Middle East. Daily oil consumption as of 2005 is close to 2,086,000 barrels per day. The following chart is an overall picture of the energy state of Korea from the year 2002 through to 2005.

Energy Overview of Korea (TOE = Tons of Oil Equivalent)

Category 2002 2003 2004 2005 Total primary energy

consumption (TPES) (1000 TOE) 208,636 215,067 220,238 229,333

Total final energy consumption (1000 TOE)

160,451 163,995 166,009 172,137

Electric power consumption per capita (KWh per capita)

5,845 6,126 6,491 6,883

Total Energy Imports (USD mil) 32,290 38,306 49,600 66,697 Daily Oil Consume (1000 barrel/day) 2,090 2,090 2,061 2,086

Oil imports (USD mil) 25,415 30,407 38,274 51,735 Source: Ministry of Commerce, Industry and Energy; Korea Energy Management Corporation

20

The primary sources of utilities and energy are provided by the Korea Gas Corporation (KOGAS) and the Korea Electric Power Corporation (KEPCO). Another important agency to note is the Korea Energy Management Corporation (KEMCO) which is dedicated to developing energy conservation and efficiency in an effort to alleviate energy burdens. Korea’s growth and demand for energy has greatly increased in the past couple of years with the total primary energy consumption in 2005 at approximately 229 million TOE. In January 1999, the Ministry of Commerce, Industry and Energy (“MOCIE”) announced the Restructuring Plan to introduce competition to the Korean electricity industry and to promote consumer convenience through the expansion of consumer choice. The Government promulgated the Law on Promotion of Restructuring of Electricity Industry (the “Restructuring Law”) and amended the Electricity Business Law on December 23, 2000. Under the original terms, the law was supposed to undergo several phases of development. During Phase I, which lasted from January 1999 until April 2001, KEPCO split its generating capacity into five wholly owned generation subsidiaries. During Phase II, the Government introduced a competitive bidding pool system. Under the pool system, each generation company would enter bids to supply power on a day to day basis for specified time segments within each day, with the price for each segment determined by the highest clearing bid. KEPCO anticipates that consumers would purchase power from KEPCO at prices upon the resulting bid price plus transmission and distribution fees. During Phase III, which is expected to run from 2003 to 2009, the distribution companies, including KEPCO’s distribution subsidiaries, would purchase power directly from the generation companies through the competitive bidding pool system. Phase IV will be the final phase of the Restructuring Plan and contemplates allowing consumers to choose their power source from any distribution company on market terms. However, under the current president Mr. Roh Moo-Hyun, the plan has seen setbacks primarily from the opposition of unions. Recent developments have also been moving towards the promotion of the developing nuclear energies to decrease the dependency that Korea has on its external oil sources.

21

Healthcare Korea’s overall health has improved dramatically over the past three decades where in 1960 life expectancy was at a mere 51 years for males and 54 for females. These figures have improved reaching 74 years for males and 81 years for females being almost equivalent to countries like the US or Japan. Development of the overall healthcare sector can be directly related to improvements in diet as well as an improvement in the availability of health and medical services. Health care in the form of medical insurance and medical assistance was first introduced in 1977 with only 29.5% of the population having health insurance coverage until 1980. Overall health insurance coverage has heightened to over 96% in recent years. People are increasingly relying on medicine and medical services and the share of medical costs to total household expenditures. According to the OECD, the overall spending per person has also been on the rise. In 1990, national health expenditure per capita was USD 377 which has increased to around USD 1,100 in recent years. The supply of hospitals and medical personnel has continuously increased. The total number of hospitals and clinics in the nation (including Oriental medicine hospitals and clinics) was 11,188 in 1975, which increased to 49,187 in 2005. Meanwhile, the number of licensed doctors that totaled 16,800 in 1975 has increased to 81,998 in 2004. The Ministry of Health and Welfare (MOHW) is the primary government organization responsible for all aspects of health services providing planning in the maintenance and promotion of national health and social welfare. The annual budget of the MOHW has also been increasing in recent years. In 2005, overall spending amounted to KRW 8,906 trillion (approximately US$9 billion) or 5.6% of GDP. The number of healthcare professionals has also shown drastic improvements as there is approximately one physician for every 500 persons, one dentist for every 2,320 and one pharmacist for every 899 persons. Although several multinational pharmaceutical companies have operations in Korea (Pfizer, Merck & Co., GlaxoSmithKline, Novartis, Sanofi-Aventis, etc.), there are a large number of domestic pharmaceutical firms (Hanmi, ChoongWae, DaeWoong, Dong-A, Yuhan, etc.). Healthcare is still undergoing much legal reforms as hospitals and healthcare providers alike are trying to accommodate more to consumer needs and promote a healthier environment for all health businesses.

22

Chapter 3

Investment Incentives in Korea General Information Foreign investments since the financial crisis in 1997 have been at the center of policy changes easing the financial burden and making South Korea an even more appealing candidate for foreign investments. The restructuring that followed the wake of the 1997 economic crisis brought with it a major shift not only in attitudes in favor of foreign investment, but also a change in policy that has been described in some literature as a change from “control and regulation” to “promotion and support.” Invest KOREA, an investment promotion agency for the national Korea Trade Investment Promotion Agency (KOTRA), is the primary organization facilitating investments made in Korea by foreigners. Information provided in this chapter, can be seen in more detail by visiting the Invest KOREA website (www.investkorea.org). Through KOTRA and Invest KOREA, the government has provided numerous ways of investing by providing exemptions for advanced technology investments, Industrial Complexes, Foreign Investment Zones (FIZ), Foreign Economic Zones (FEZ), and Free Trade Zones (FTZ). These following incentives will be discussed in detail in this chapter, along with other regulations and tax incentives which will prove valuable for investors. Foreign Investment Promotion Act (FIPA) Overview The Foreign Investment Promotion Act (FIPA) is the primary act that governs overall foreign investments which regulates foreign equity investment, foreign loans, technology inducement, licensing, tax incentives, repatriation of capital, and remittance of dividends. The FIPA was first enacted in 1998, and was designed in order for investors to take full advantage of Korea’s resources and

23

encourage foreigners to invest in Korea. Additionally, the Foreign Exchange Transactions Act (FETA) which will be discussed later outlines the process of foreign corporations establishing a branch office or a representative office. Additional acts investors should acquaint themselves with include the Customs Act, the Commercial Code, the Foreigner’s Land Acquisition Act and various other tax laws, as well as Korea’s acts of general applicability that may effect foreign investment. Important Definitions The FIPA provides legal provisions for any foreigner who intends to make an investment in any corporation legally established in South Korea. Overall, a report must be filed with the Ministry of Commerce, Industry and Energy in return for a certificate which will indicate the completion of the report. Under FIPA, a “foreigner” is:

An individual with foreign citizenship; A company established under laws of a foreign country; or A company established under an international economic cooperation

organization. Essentially, to qualify as a “foreign investment” a foreign investor must:

Invest at least KRW 50 million or more; Retain at least 10% or more of the voting shares or equity of the invested

company; Enters into a contract allowing the foreigner to dispatch or elect officers

(directors, partners, auditors); Enter a contract term of one year or more for the delivery or purchase of

raw materials or products; and Enter a contract for the supply or introduction of technology or for joint

technology R&D projects. A “foreign investment” is:

Purchase of stocks of a Korean corporation or a company run by a national of South Korea; or

A loan with maturity of at least five years given to a foreign-capital invested company by an overseas holding company or a holdings company of capital investment.

24

Foreigners can invest or contribute in the following types of investments:

Foreign means of payment outlined by FETA, or domestic means of payment;

Capital goods; Proceeds from shares or equity under FIPA; Industrial/Intellectual property rights; Assets after the liquidation of a branch company or office; Redemption of loans provided to foreign-invested company by the foreign-

invested company; Stocks or shares of a foreign company listed with a foreign stock exchange; Real estates located in Korea owned by a foreigner; or Other domestic payments.

Liberalization of Investments Except otherwise noted, foreigners may invest or engage in any activity within Korea. However, activities that either threaten national security or public order, harms public health or the environment, go against decency and morality of Korean standards, or are in any contradiction with Korean laws and regulations are not permitted to conduct business in Korea. Foreign Exchange Transactions Act All transactions involving foreign exchange in Korea or flows of capital between Korean residents and non-residents are controlled according to the provisions outlined in the Foreign Exchange Transactions Act (FETA). The FETA applies to all domestic companies, including branches, agencies, representative offices and other offices of foreign companies operating in the Republic of Korea. In essence, inflows and outflows of foreign exchange are regulated under the FETA, foreign exchange earnings from external transactions are regarded as coming under the jurisdiction of the Republic of Korea. As stated above, foreign investors who comply with the notification requirements of the FIPA are guaranteed the right to remit dividends and repatriate capital through a designated foreign exchange bank. Liberalization The FETA, which was enacted in September 1998, liberalizes the highly restrictive and regulated exchange policy under the previous Foreign Exchange Management Act (FEMA). The FETA originally called for complete liberalization of capital transactions as part of the implementation of a second stage of liberalization to have commenced on January 1, 2001. Since the inception of the

25

FETA, the emphasis on promotion of Korea’s international competitiveness and standard of living through the liberalization of foreign exchange has been subordinated to concerns over recent changes in international market conditions and the maintenance of order within capital markets. Accordingly, approval requirements relating to capital transactions have been extended to an additional term of three (3) years as part of a step-by-step or gradual approach to liberalization. Foreign Trade in Korea Total exports equaled to an amount of USD 284.5 billion in 2005 with imports equaling approximately USD 261.3 billion. The following information, taken from the Economy section of this booklet, outlines the amount of foreign trade within Korea:

Import/Exports of Korea

Category 2003 2004 2005 Exports (USD bil) 193.7 253.7 284.5 Imports (USD bil) 178.8 224.1 261.3

Trade Balance (USD bil) 14.9 29.4 23.2 Source: Korea National Statistical Office Since joining the General Agreement on Tariffs and Trade (GATT) in the 1967 and entering the World Trade Organization (WTO) in 1995, Korea has benefited tremendously. As mentioned in previous chapters, Korea is also undergoing negotiations with the US to form a Free Trade Agreement (FTA). Through Korea’s inception into organizations like that of GATT clearly demonstrates Korea’s willingness to stay committed with multilateral rules and to maintain an overall free and open market. Korea continues to keep its open market as regulations within Korea continues to transitions its economy to accommodate more FDI. Much progress after the crisis of 1997 shifted Korea’s attention to liberalization in addition to the focus on increasing FDI. Economic reforms continued to assist foreign trade, and the government eventually established the Ministry of Foreign Affairs and Trade (MOFAT) in 1998, which was designed to create policies to improve foreign trade. From this, government agencies have also been lifting restrictions in most sectors except for that in the agricultural products. Import and export authorization in turn has changed from positive to negative orientation.

26

Recent developments continue to find new ways to decrease tariffs and trade barriers. As FTA negotiations with the US continue, trade is bound to show significant growth potential. Foreign Investment Procedures Overview A foreigner can establish a domestic business entity in four different ways which includes a company, a sole proprietorship, a branch office or a representative office. The company and sole proprietorship are both governed by the Foreign Investment Promotion Act (FIPA), while the branch office and representative office is governed by the Foreign Exchange Transactions Act (FETA). A more detailed explanation on these separate entities will be discussed in a later chapter titled “Business Environment.” The general process for setting up a foreign investment is initiated with an investment report, followed by company registration, and finally completing the process with a foreign-invested company registration. Procedures for foreign investment can be divided into two types where one set of procedures apply to all lines of businesses and the other applies to manufacturing businesses. Procedures Foreign investment reporting begins at either the Invest KOREA offices or a foreign exchange bank where the confirmation is given, followed by the registration of incorporation and business registration processed at a court or at Invest KOREA, and finally registering a foreign invested company. The procedure for applying for manufacturing business is also relatively similar. The process starts with the selection of an industrial location with Invest KOREA or a municipal office, followed by an approval of the establishment of the plant or entry into an occupancy agreement with the municipal office or industrial complex, then with the municipal offices receiving a building permit and ending with the registration of the plant. Overall, all types of acquisition must be made to a foreign exchange bank, a designated foreign bank, or Invest KOREA. The process by which long-term loans must be carried out is very similar to that of share acquisitions. The following is a chart based on information for reporting and to assist in assessing the types of acquisitions:

27

Type of Acquisition

Reporting Sector Additional Information

New shares

Any branch of a foreign exchange bank, a

designated foreign bank, or Invest KOREA

1. Establishment of new corporation,

2. Participation in the capital increase of an existing domestic

company or foreign invested company

Issued and

outstanding shares

Any branch of a foreign exchange bank, a

designated foreign bank, or Invest KOREA

Only in case of defense-industry business, approval of the Ministry

of Commerce, Industry and Energy is needed

Merger

Any branch of a foreign exchange bank, a

designated foreign bank, or Invest KOREA

Notification must be filed within 30 days after

Long- term loan

Any branch of a foreign exchange bank, a

designated foreign bank, or Invest KOREA

A loan with a maturity of 5 years or more is extended to a foreign-

invested company

Source: Invest KOREA Factories and Land Acquisition For the overall establishment of factories or land acquisition, the following acts must be considered when conducting business in Korea:

Industrial Cluster Development and Factory Establishment Act; Factory Establishment Administration Guidelines; Industrial Location and Development Act; Industrial Site Development Guidelines; National Land Planning and Utilization Act; Farmland Act; Highlands Act; Building Act; and Clean Air Conservation Act.

Generally, a foreigner may acquire land by filing a notice unless permission is required. These preceding acts and guidelines serve as an overall guide in terms of how investors must proceed with land use and construction methods. As for land acquisition, in addition to the FIPA and FETA, the Foreigner’s Land Acquisition Act provides the regulations and procedures as to how foreigners

28

acquire any land in Korea. For further information, please refer to each of these acts. Industries to Invest In In Korea, there are various industries and lines of business to invest in. The government also provides comprehensive incentive programs for investors with interest in these industries which the Invest KOREA website outlines in relative detail:

Logistics; SOC; Bio-technology; IT; R&D; Semiconductor; Venture; Tourism; M&A; Auto Industry; Aerospace Industry; and Nano Industry.

Investment incentives in Korea will increase as South Korea transitions into being a major economic hub of northeast Asia and as its infrastructure develops providing a more investor friendly environment. Investment Tax Incentives Korea provides numerous tax incentives through the FIPA. Under certain situations there are special conditions in which taxes may be reduced which will be outlined in the sections herein. To compete with other developing nations in attracting foreign investors and to channel investment into favored industries, Korea provides a number of tax incentives that is based on geographical location or given out based on a related industry. Corporate income tax, individual income tax, acquisition tax, registration tax, property tax, value added tax, customs duty and special consumptions tax may be exempt or reduced for investments which introduce advanced technology or is located in a Foreign Investment Zone (FIZ). Other tax information can be referred to in the individual and business taxation portion of this booklet.

29

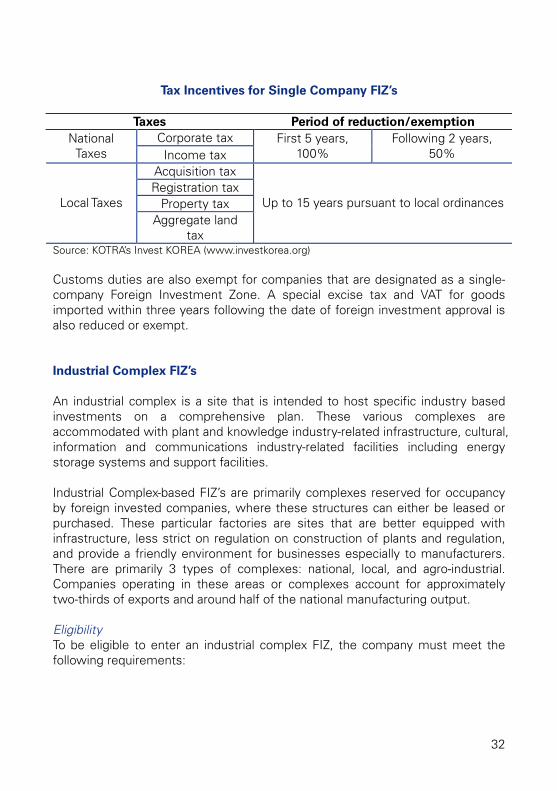

In addition to the previous mentioned tax incentives, the government also provides an array of various “economic zones” and industrial complexes designed specifically for foreign investments. These economic zones are distinguished based on their incentives for trade, location, and the type of industry which is being invested in. The following information can be viewed in more detail at KOTRA’s Invest KOREA website (www.investkorea.org). Advanced Technology Incentives Investments in certain industries such as that of advanced technology is promoted and outlined in the table below.

Tax Incentives for Advanced Technology FDI

Tax Incentives Individual

Corporate income tax Full exemption for 5 years, 50% reduction for next

2 years Local taxes: acquisition, property, aggregate land,

registration

Full exemption for 5 years, 50% reduction for next 2 years (local governments can extend the

applicable period up to 15 years) Customs duties, special

excise tax, value-added tax Full exemption for 3 years on imported capital

goods by foreign-invested companies Source: Ministry of Finance and Economy Special Zones for Investments Introduction South Korea provides many different types of incentives depending on the industry of investment, the location of the special site, the types of requirements, and the scope of investment. Generally, there are primarily four different regions and types of investment zones which consist of a Single-company Foreign Investment Zone, Industrial Complex-based Foreign Investment Zone, Free Trade Zones, and Free Economic Zones. Foreign Investment Zones (FIZ) Single-company Economic Zones Single-company foreign investment zones are essentially for either individual

30

plants, offices, or other facilities of foreign-invested companies. To be eligible, under the FIPA, the foreign investment zones have specific criteria which must be met. Refer to the chart provided by KOTRA’s Invest KOREA for further detailed information on requirements for eligibility to enter into these special zones.

Eligibility Requirements

Investment Size Types of Business Nature of Investment

≥US $30million Manufacturing

High-tech industries Industrial support services

Construction of plant & facilities

≥US $20million

Tourist hotels overwater tourist hotels Resort facilities, International Convention

centers – Construction of business facilities

≥US $10million

Freight terminals, Contract warehousing & shipping facilities, Port facilities,

Logistics business for airports & ports, SOC building projects

Building business premises

≥US $5million R&D Institutions (must employ 10 or

more researchers with 3 or more years of experience in given research fields)

Building & expanding

R&D facilities Source: KOTRA’s Invest KOREA (www.investkorea.org) These foreign economic zones are highly regarded as the benefits include rent-free buildings for any company meeting the requirements for up to 50 years. Tax Incentives Numerous tax incentives are available on various types of taxes. The following is a chart outlining the overall tax incentives that are provided for investments in Single-company FIZ’s.

31

Tax Incentives for Single Company FIZ’s

Taxes Period of reduction/exemption

Corporate tax National Taxes Income tax

First 5 years, 100%

Following 2 years, 50%

Acquisition tax Registration tax

Property tax Local Taxes Aggregate land

tax

Up to 15 years pursuant to local ordinances

Source: KOTRA’s Invest KOREA (www.investkorea.org) Customs duties are also exempt for companies that are designated as a single-company Foreign Investment Zone. A special excise tax and VAT for goods imported within three years following the date of foreign investment approval is also reduced or exempt. Industrial Complex FIZ’s An industrial complex is a site that is intended to host specific industry based investments on a comprehensive plan. These various complexes are accommodated with plant and knowledge industry-related infrastructure, cultural, information and communications industry-related facilities including energy storage systems and support facilities. Industrial Complex-based FIZ’s are primarily complexes reserved for occupancy by foreign invested companies, where these structures can either be leased or purchased. These particular factories are sites that are better equipped with infrastructure, less strict on regulation on construction of plants and regulation, and provide a friendly environment for businesses especially to manufacturers. There are primarily 3 types of complexes: national, local, and agro-industrial. Companies operating in these areas or complexes account for approximately two-thirds of exports and around half of the national manufacturing output. Eligibility To be eligible to enter an industrial complex FIZ, the company must meet the following requirements:

32

100% foreign-owned companies or joint-ventures companies where foreign equity holding exceeds 30% (10% for Daebul and Pyeongdong areas), involving a foreign investment with at least KRW 50 million.

The size may not exceed the area corresponding to 50% of the value of foreign investment in a tenant company (100% for Daebul and Pyeongdong).

Industries and order of priority are:

(1) High tech industries; (2) Cutting-edge technologies and manufacturing; (3) General manufacturing; which involves new technologies with NT mark; (4) Corporate R&D facilities; and (5) Freight terminals/Warehousing & distribution center projects.

When two applicants are applying at the same time, precedence is based on:

(1) Which company invests more money; (2) Higher level of foreign equity holding; and (3) Larger employer.

Low Rent Another benefit that occupants are given are low rents which is equivalent to 1/100 of the purchase price of land. Rent may also be completely removed or reduced by 75% depending on the type of business which a tenant firm is engaged. General manufacturing firms, investing USD 5 million will receive a reduction in rent by 75%. Tax Reduction For various tax reductions in the particular Industrial Complex-based FIZ’s, will be based on the minimum amount of investment.

Minimum Amount of Investment along with Industry

Minimum Amount Investment Industry USD10 million Construction of a Manufacturing Plant

USD 5 million Freight,, terminals; contract,

warehousing, and manufacturing

Construction of related facilities

Source: KOTRA’s Invest KOREA (www.investkorea.org)

33

The various tax incentives for the type of tax and the period of reduction or exemption can be seen in the following table:

Tax Incentives for Industrial Complex-based FIZ’s

Taxes Period of reduction/exemption Corporate tax National

Taxes Income tax First 3 years,

100% Following 2 years, 50%

Acquisition tax Registration tax

Property tax Local Taxes Aggregate land

tax

Up to 15 years in accordance with local ordinances

Source: KOTRA’s Invest KOREA (www.investkorea.org) Free Trade Zones (FTZ) General FTZ’s are special zones benefiting from exemption or reduction of customs duties and taxes, which are usually developed primarily for manufacturing, trade, logistics, and distribution. These zones are usually considered to be outside Korean customs territory, therefore customs duties on foreign goods and selected domestic goods are deferred, and VAT is rated at zero. These FTZ’s are designed to bring most benefit to large foreign invested companies specializing in manufacturing and logistics operations. FTZ’s are strategically located to enhance the trade process and also provide a comprehensive administrative portal processing of all the needed steps from reporting on investments, moving into the zone, permission to build a plant, and obtaining export licenses. These zones are usually located near airports or ports, and also based in industrial complexes. The following chart provides some information on these special FTZ’s:

34

Type of FTZ’s

Type of Zone Location Governing Administration

Industrial-Complex Zones

Masan Iksan

Gunsan Daebul

Ministry of Industry, Commerce, and Energy

Airports Incheon Int’l Airport

Ministry of Construction and Transportation

Ports

Port of Gwangyang Port of Incheon Port of Gunsan Port of Busan

Ministry of Maritime Affairs and Fisheries

Source: KOTRA’s Invest KOREA (www.investkorea.org) Eligibility To be eligible to invest in these zones, there are several requirements which depend on the type of FTZ investors plan. For industrial complex-based FTZ’s to become eligible:

The investors must be investing in the manufacturing sector; Wholesalers who trade internationally; or Logistics companies in loading & unloading, transportation, warehousing,

and storage & exhibition. Furthermore, there is an order of priority:

(1) Cutting edge technology sectors included in the Ministry of Industry, Commerce and Energy Notice;

(2) High-tech sectors specified in Restriction on Special Taxation Act; (3) Priority industrial sectors in accordance with the regional assigned

industries; and (4) Manufacturing sectors with high technology transfer and job creation.

For airports, the requirements are:

The annual freight handling capacity must be at least 500,000 tons; The combined area of the facility must be at least 500,000 square meters.

For the ports, the requirements are:

35

Ships must regularly serve international container ships with a handling capacity of 10million tons;

The pier is reserved for container ships of 30,000 tons and heavier; The port and hinterland must be at least 500,000 square meters in area.

Occupant Benefits The land rent in FTZ’s is very affordable ranging from KRW 80 to KRW 130 per square meter each month. In some areas such as Gunsan, 50% of rent is discounted for companies in machinery and the automobile industries, while in Daebul companies in shipbuilding and machinery industries receive such benefits. Rent can also be completely rent-free for investments that meet special conditions and the FTZ also provide standard plants for lease for immediate start of production. The FTZ’s also benefits occupants (manufacturers who invest USD 10 million or logistics companies investing USD 5 million) in deductions or exemptions for certain taxes in these FTZ’s as seen in the chart below:

FTZ’s Tax Reduction or Exemption

Taxes Period of reduction/exemption Corporate tax National

Taxes Income tax First 3 years,

100% Following 2 years, 50%

Acquisition tax Registration tax

Property tax Local Taxes

Aggregate land tax

First 3 years full exemption and 50% exemption the following 2 years. (Up to 15 years in accordance with local ordinances)

Source: KOTRA’s Invest KOREA (www.investkorea.org) Free Economic Zones (FEZ) Free Economic Zones (FEZ’s) are designated areas that exploit Korea’s strategic location in Northeast Asia. These FEZ’s provide a location where businesses can handle all administrative tasks and all formalities at a single location. With the establishment of the FEZ’s, the government has taken another step towards arranging itself to be Asia’s major economic hub. FEZ’s were designated in Busan, Jinhae, Incheon, and the Gwangyong area, which are all equipped with an airport and port. The development of FEZ’s is an ongoing project in Korea, currently bringing in major IT, BT and logistics sectors to migrate into these zones until 2008. By 2009, these FEZ’s hope to be highly advanced cities enabled with autonomous urban functions. Additionally, to provide an optimal environment for investors to live in, the government promotes the development

36

of various types of infrastructure with foreign capabilities (foreign schools, foreign speaking hospitals etc.). It also should be noted that foreign currencies are also accepted here. Tax Incentives Tax benefits are provided for manufacturers of tourism-related businesses investing USD 10 million or more, which includes the construction of a plant hotel, resort, or international convention facility. Benefits are also given to logistics related businesses investing USD 5 million or over, and this includes construction of an airport or port. The following table provides a detailed view of the tax deductions available for investors in FEZ’s:

FEZ’s Tax Reduction or Exemption

Taxes Period of reduction/exemption Corporate tax National

Taxes Income tax First 3 years,

100% Following 2 years, 50%

Acquisition tax Registration tax

Property tax Local Taxes

Aggregate land tax

First 3 years full exemption and 50% exemption the following 2 years. (Up to 15 years in