investment innovations: raising the bar - citi.com · innovation innovation linked to business...

TRANSCRIPT

Investment Innovations: Raising the BarNovember 2011

Jervis SmithManaging Director, Global Head of Client Executive

Global Transaction Services, Citi,

Amin RajanCEO, CREATE-Research

November 2011

Executive SummaryThis presentation summarises the results of the 2011 Create Research annual global survey that

Sponsored by Citi and Principal Global Investors

This presentation summarises the results of the 2011 Create Research annual global survey that took place in April / May 2011

Create is an independent research firm we have worked with for six years. Headed by Professor Amin Rajan.

Focusing on the last decade, the report assessed the impact of Innovation on the basis of two global surveysOne involved 108 pension plans– One involved 108 pension plans

– The other involved 396 asset managers, pension consultants, third party administrators and distributors from 30 countries

Together the surveyed firms represent a combined AUM of around US$29 trillion Together, the surveyed firms represent a combined AUM of around US$29 trillion

Survey and one-on-one interviews

Four key questions:y q– What innovations worked/ did not work, and why?– What improvements are essential?– What should the main thrust for innovations be over the next three years?– What specific actions do they call for?

1

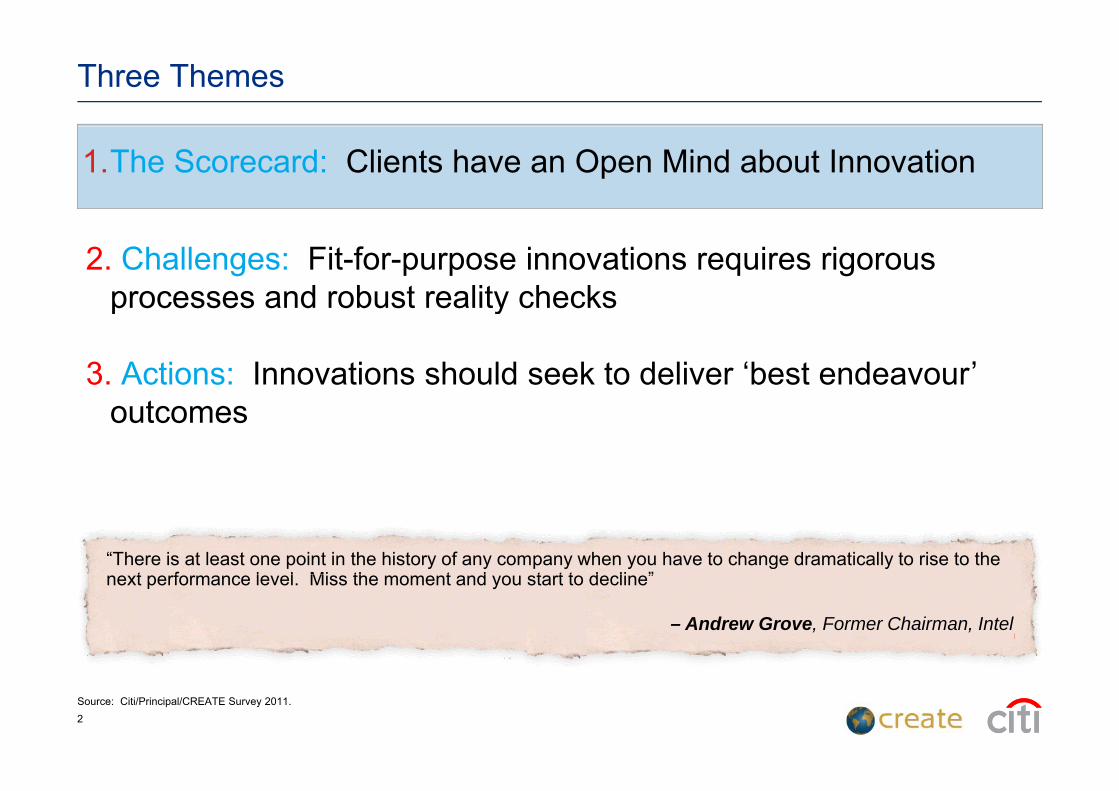

Three Themes

1.The Scorecard: Clients have an Open Mind about Innovation

2. Challenges: Fit-for-purpose innovations requires rigorous processes and robust reality checksprocesses and robust reality checks

3. Actions: Innovations should seek to deliver ‘best endeavour’ outcomes

“There is at least one point in the history of any company when you have to change dramatically to rise to the t f l l Mi th t d t t t d li ”next performance level. Miss the moment and you start to decline”

– Andrew Grove, Former Chairman, Intel

Source: Citi/Principal/CREATE Survey 2011.2

Which Innovations Were Widely Adopted in the 2000s and who were the early pioneers?

Global equities Emerging market equities Convertible bonds

New Asset Classes Derivatives for hedging

unrewarded risks ETFs

New enhancing tools

ues

Hedging

High yield bonds Emerging market bonds Commodity funds Currency funds

Hedge funds Portable alpha Leverage Shortingon

Tec

hniq

& R

eturns-

Risk parity portfolios Real assets

Outsourcing of back office Outsourcing of distribution

New business models

US, Canada, UK, Switzerland

set A

lloca

ti-enhancing

US, UK, Holland, Australia, Singapore

LDI Distressed debt

New Asset Techniques Fiduciary management Multi-boutique models Client service models Innovation models

SRI Environment

New product themes

ses

and

As Tools and P

GTAA Age-based retirement funds Risk-based retirement funds Unconstrained mandates

Water Renewable energy Shari’ah Capital protection

T ffi iAss

et C

lass

Product The

US, EU, Switzerland

Tax efficiency

US, EU, Malaysia, Canada, Singapore

emes

US, UK, Holland, Switzerland

Source: Citi/Principal/CREATE Survey 2011.3

In the Last Decade, Which Innovations in the Three Sub Sets Delivered Most Value to Defined Benefit Pensions and Which Delivered Least Value?

Source: Citi/Principal/CREATE Survey 2011.4

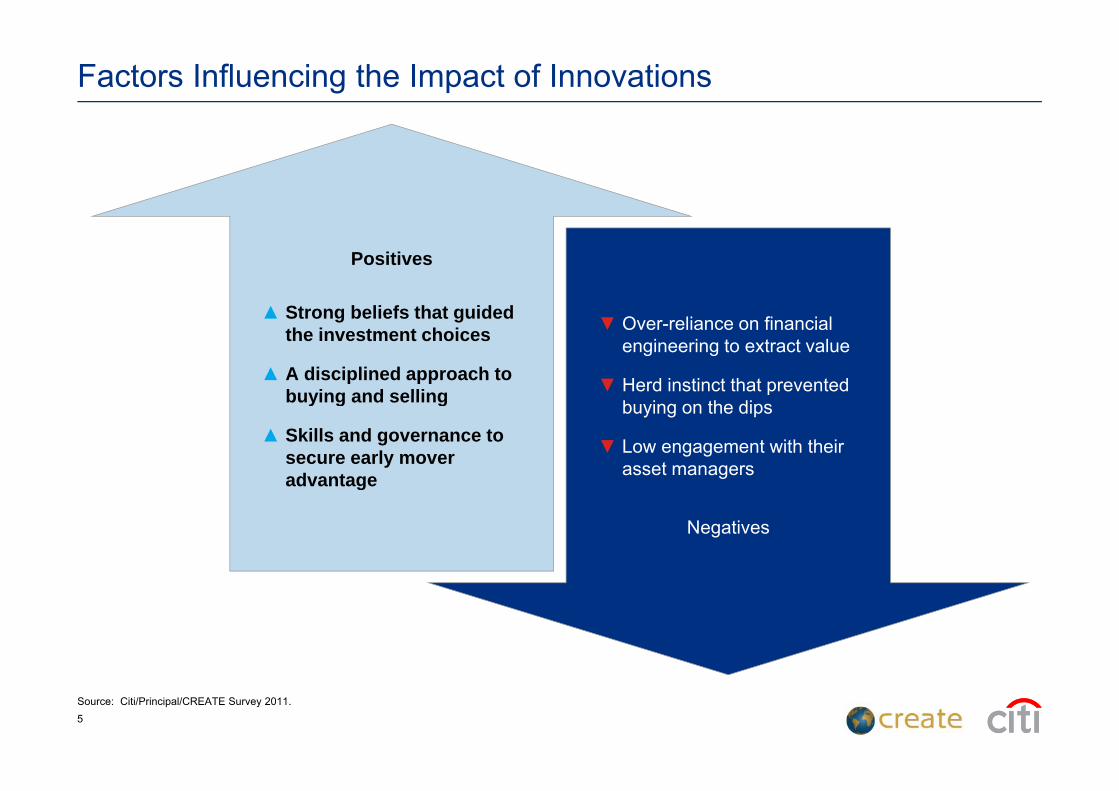

Factors Influencing the Impact of Innovations

▲ St b li f th t id d

Positives

▲ St b li f th t id d▲ Strong beliefs that guided the investment choices

▲ A disciplined approach to buying and selling

▼ Over-reliance on financial engineering to extract value

▼ Herd instinct that prevented

▲ Strong beliefs that guided the investment choices

▲ A disciplined approach to buying and sellingbuying and selling

▲ Skills and governance to secure early mover advantage

buying on the dips

▼ Low engagement with their asset managers

buying and selling

▲ Skills and governance to secure early mover advantageadvantage

Negatives

advantage

Source: Citi/Principal/CREATE Survey 2011.5

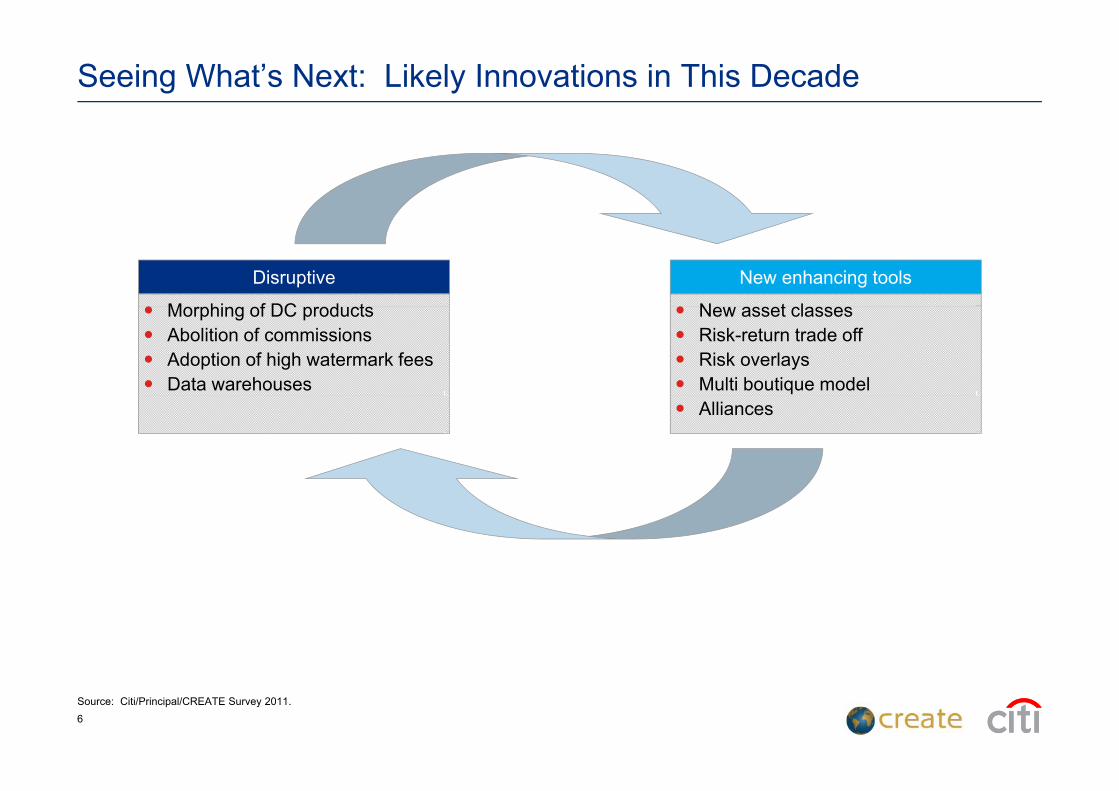

Seeing What’s Next: Likely Innovations in This Decade

M hi f DC d t N t l

Disruptive New enhancing tools

Morphing of DC products Abolition of commissions Adoption of high watermark fees Data warehouses

New asset classes Risk-return trade off Risk overlays Multi boutique model Alliances

Source: Citi/Principal/CREATE Survey 2011.6

Theme 2

1.The Scorecard: Clients have an Open Mind about Innovation

2. Challenges: Fit-for-purpose innovations requires rigorous processes and robust reality checksp y

3. Actions: Innovations should seek to deliver ‘best endeavour’ toutcomes

“Which asset managers can claim Apple’s historic run of successes?” A I t i Q t– An Interview Quote

Source: Citi/Principal/CREATE Survey 2011.7

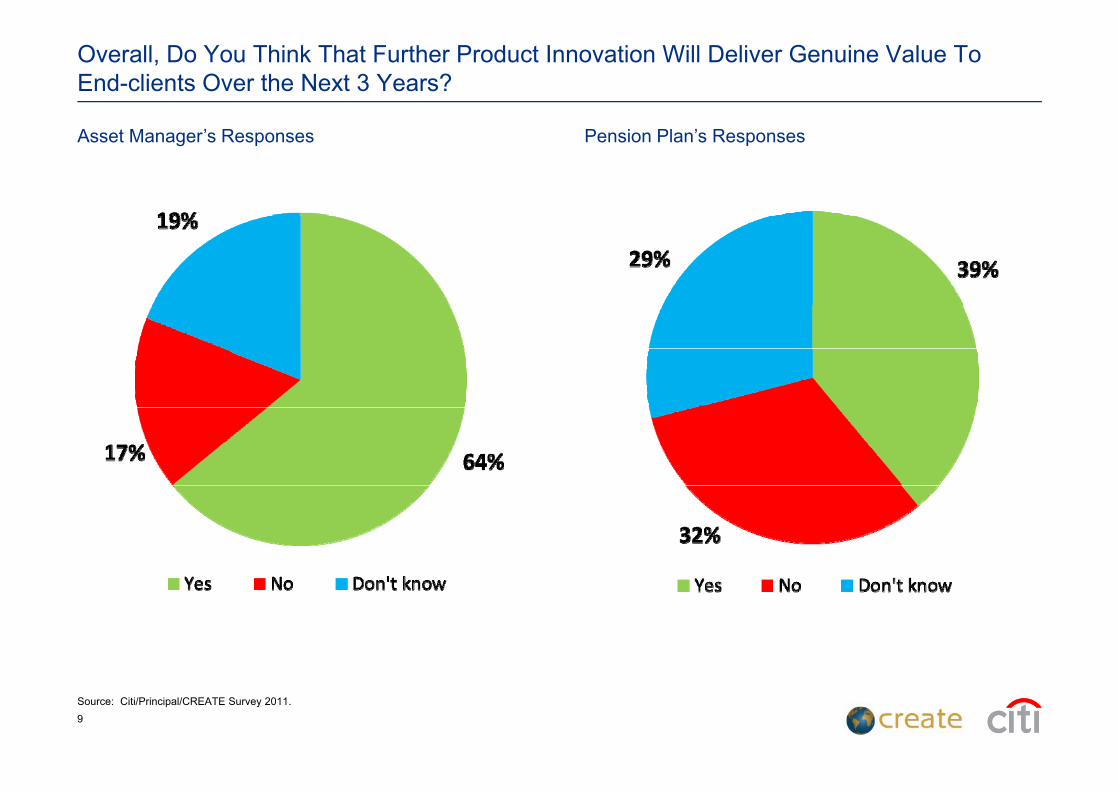

Overall, Do You Think That Further Product Innovation Will Deliver Genuine Value To End-clients Over the Next 3 Years?

Asset Manager’s Responses Pension Plan’s Responses

Source: Citi/Principal/CREATE Survey 2011.9

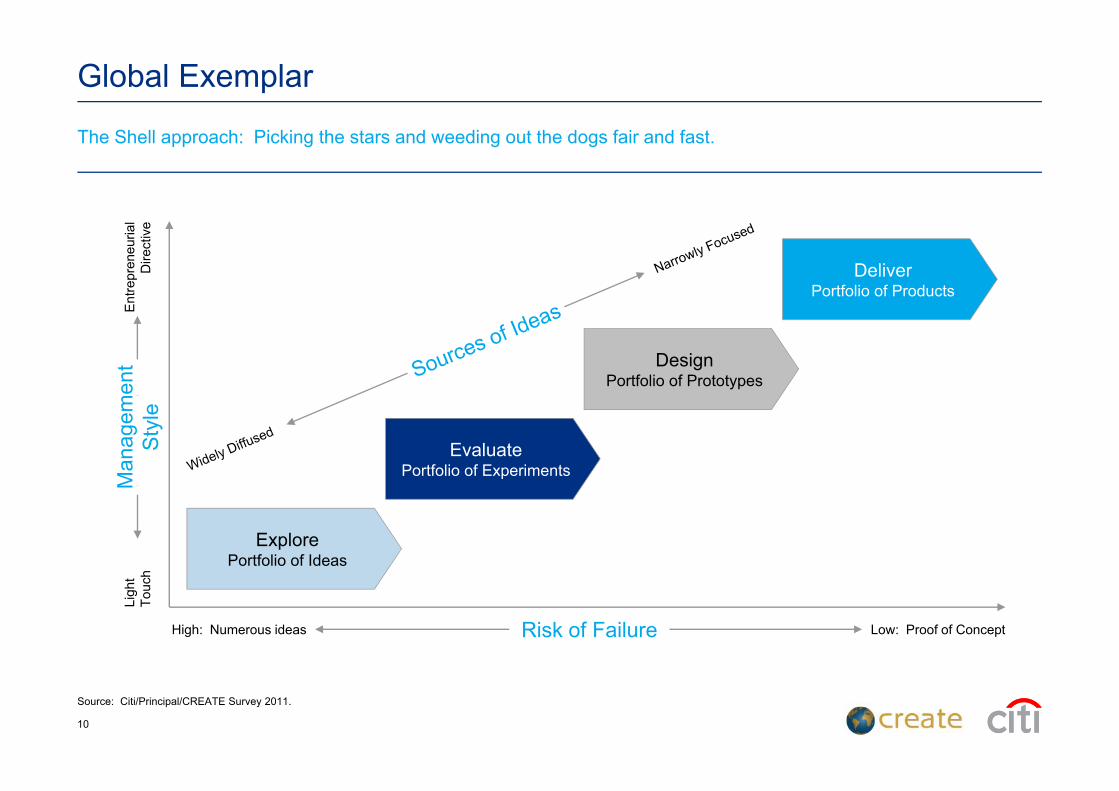

Global Exemplar

The Shell approach: Picking the stars and weeding out the dogs fair and fast.

DeliverPortfolio of Products

Entre

pren

euria

l D

irect

ive

DesignPortfolio of Prototypes

Een

t

EvaluatePortfolio of ExperimentsM

anag

emS

tyle

ExplorePortfolio of Ideas

hM

High: Numerous ideas Low: Proof of ConceptRisk of Failure

Ligh

tTo

uch

Source: Citi/Principal/CREATE Survey 2011.

10

Lesson 1

Choose the right tools to deliver a culture of innovation.

Nature of InnovationCustomer-driven Culture-driven Deliver value to clients

Alignment of interests

Incremental changes

Step changes

Nature of Innovation Breaking the current

boundaries on new products,geographies & customers

Metrics on new boundaries

Customer driven Strong business values on

innovation

Innovation linked to business strategy and PBS

Culture driven

Cre

ativ

ityU

nstructure

Step changes Customer engagement

25%

Ideas ‘bank’

40%

Pro

voke

d C ed C

reativity Challenges framed for virtual t

Systems-driven Virtual boutiques

Talent-driven Ring fenced innovation

it

R&D-driven

yteams

Fast track process

Dedicated resource

Thought leadership

Individual accountability

unit

‘White space’ for free thinkers

Fund incubators

15% 70%5%

Eureka CreativityEureka Creativity

Source: Citi/Principal/CREATE Survey 2011.11

Theme 3

1. The Scorecard: Clients have an Open Mind about Innovation

2. Challenges: Fit-for-purpose innovations requires rigorous processes and robust reality checks

3. Actions: Innovations should seek to deliver ‘best endeavour’ outcomes

“For most of the last decade, asset managers spent a lot of time worrying about almost everything but th i t ”their customers.”

– An Interview Quote

Source: Citi/Principal/CREATE Survey 2011.12

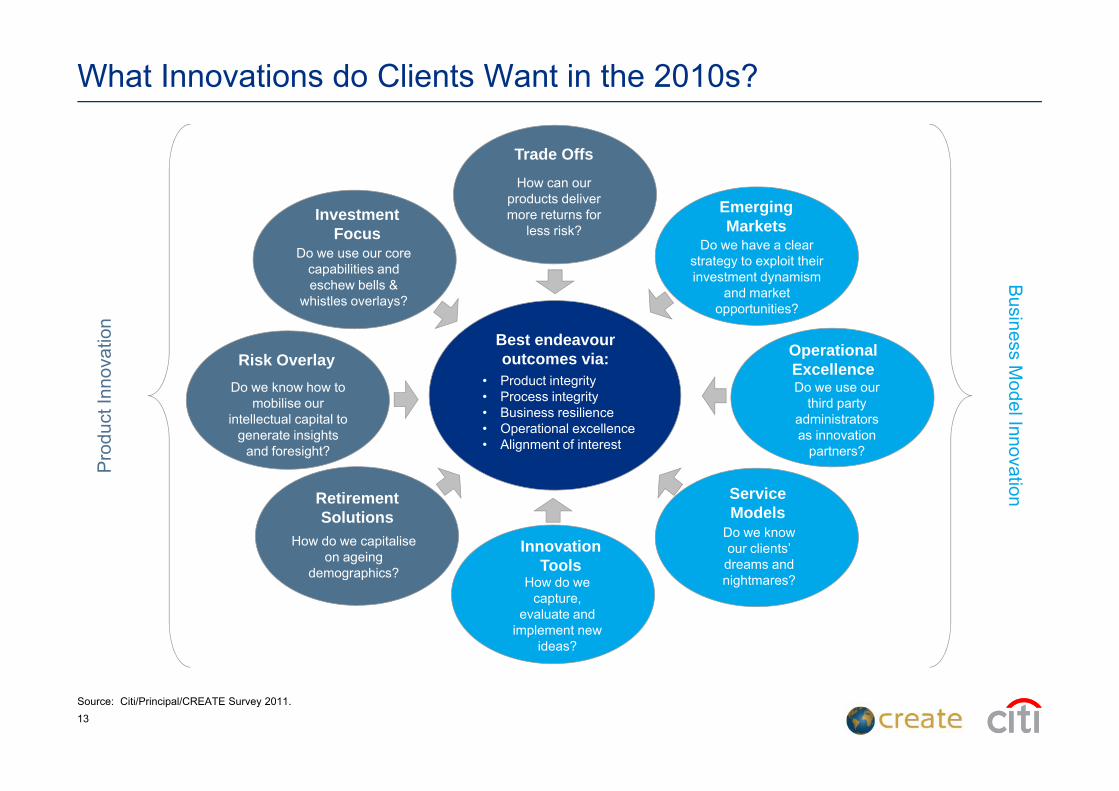

What Innovations do Clients Want in the 2010s?

Trade Offs

How can our products deliver more returns forInvestment Emerging more returns for

less risk?Investment

FocusDo we use our core

capabilities and eschew bells &

whistles overlays?

MarketsDo we have a clear

strategy to exploit their investment dynamism

and market t iti ?

Bu

Best endeavouroutcomes via:

• Product integrity• Process integrity

y

Risk OverlayDo we know how to

Operational ExcellenceDo we use our

opportunities?

nnov

atio

nsiness M

od

• Process integrity• Business resilience• Operational excellence• Alignment of interest

mobilise our intellectual capital to

generate insights and foresight?

third party administrators as innovation

partners?

Pro

duct

Indel Innovati

Retirement Solutions

How do we capitalise on ageing

demographics?

Innovation Tools

Service Models

Do we know our clients’ dreams and

?

on

demographics?How do we

capture, evaluate and

implement new ideas?

nightmares?

Source: Citi/Principal/CREATE Survey 2011.13

1. Engagement

How often have your asset managers involved you when innovating the products that you buy from them?

Pension Plans’ ResponsesPension Plans Responses

Alpha Seekers Want Strategic Partnership

Returns Seekers Want Arms Length Vendors

Advice Seekers Want Expert Hand-holders

Source: Citi/Principal/CREATE Survey 2011.14

2. Bottom Line

Which of the following fund product features will need to improve most over the next 3 years?

Source: Citi/Principal/CREATE Survey 2011.15

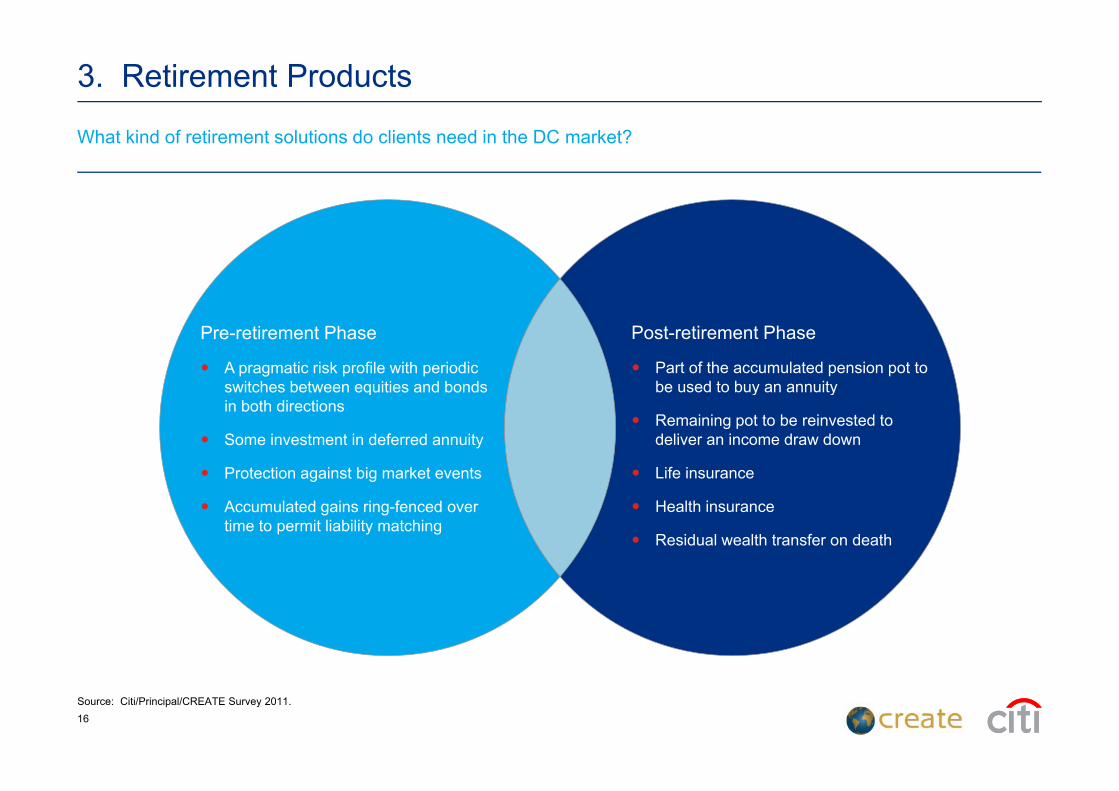

3. Retirement Products

What kind of retirement solutions do clients need in the DC market?

Pre-retirement Phase

A pragmatic risk profile with periodic switches between equities and bonds

Post-retirement Phase

Part of the accumulated pension pot to be used to buy an annuity

in both directions

Some investment in deferred annuity

Protection against big market events

Remaining pot to be reinvested to deliver an income draw down

Life insurance

Accumulated gains ring-fenced over time to permit liability matching

Health insurance

Residual wealth transfer on death

Source: Citi/Principal/CREATE Survey 2011.16

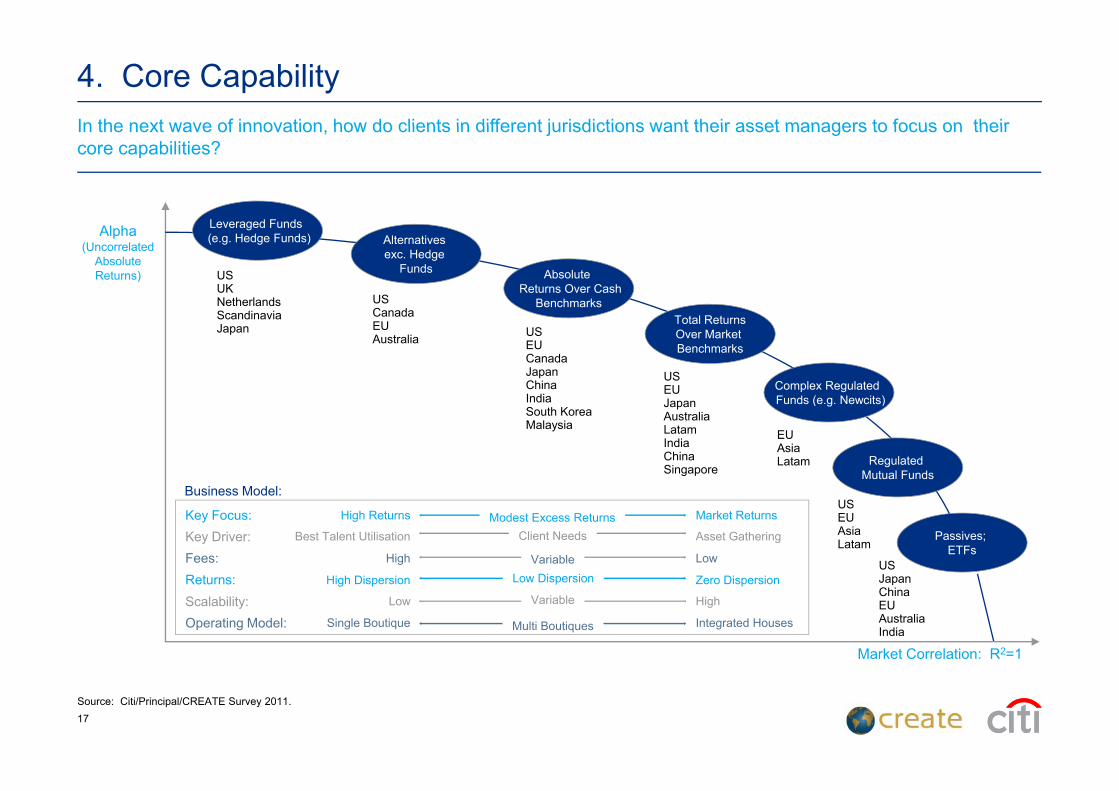

4. Core CapabilityIn the next wave of innovation how do clients in different jurisdictions want their asset managers to focus on theirIn the next wave of innovation, how do clients in different jurisdictions want their asset managers to focus on their core capabilities?

Leveraged Funds (e.g. Hedge Funds) Alternatives

exc. Hedge Funds Absolute

Returns Over Cash Benchmarks

Alpha(Uncorrelated

Absolute Returns)

US

USUKNetherlands Benchmarks

Total ReturnsOver Market Benchmarks

Complex Regulated F d ( N i )

USEU

CanadaEUAustralia US

EUCanadaJapanChinaI di

NetherlandsScandinaviaJapan

Funds (e.g. Newcits)

Regulated Mutual Funds

JapanAustraliaLatamIndiaChinaSingapore

EUAsiaLatam

IndiaSouth KoreaMalaysia

Passives; ETFs

USJ

USEUAsiaLatamKey Driver: Best Talent Utilisation Asset Gathering

Fees: High Low

R t

Key Focus: High Returns Market Returns

Client Needs

VariableL Di i

Modest Excess Returns

Business Model:

Market Correlation: R2=1

JapanChinaEUAustraliaIndia

Returns: High Dispersion Zero Dispersion

Scalability: Low High

Operating Model: Single Boutique Integrated Houses

Low Dispersion

Variable

Multi Boutiques

Source: Citi/Principal/CREATE Survey 2011.17

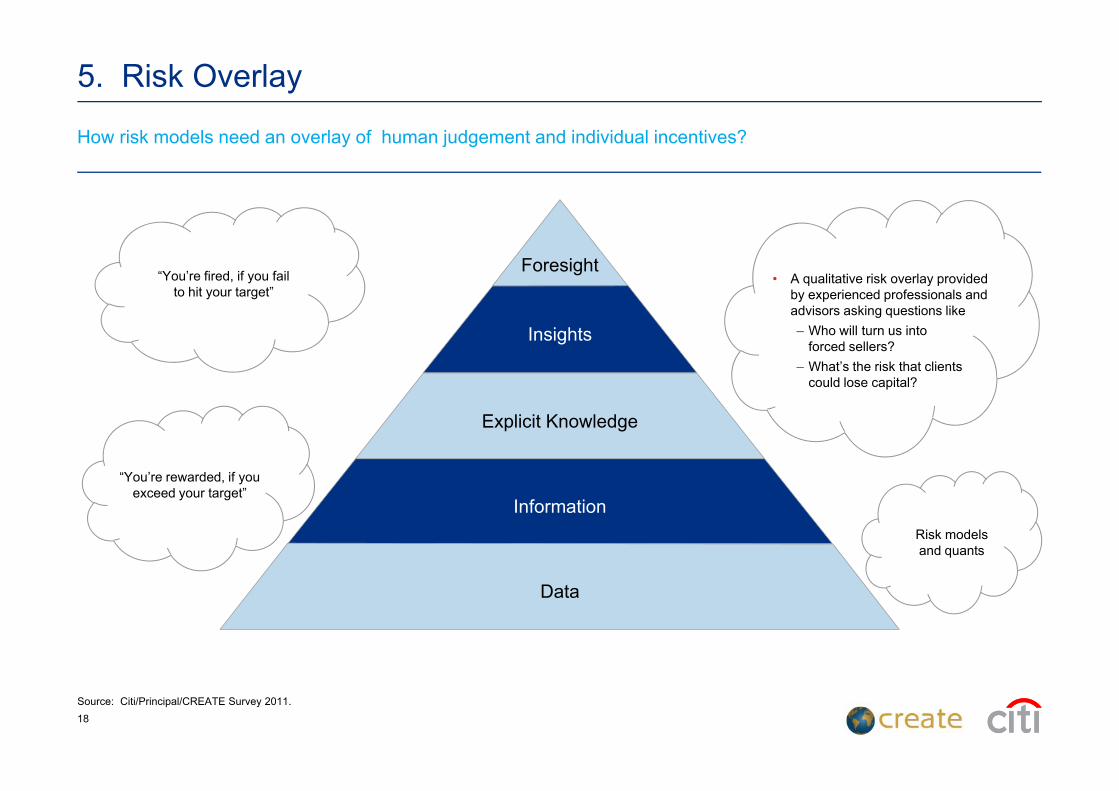

5. Risk Overlay

How risk models need an overlay of human judgement and individual incentives?

Foresight“You’re fired, if you fail

to hit your target”• A qualitative risk overlay provided

by experienced professionals and d i ki ti lik

Insightsadvisors asking questions like– Who will turn us into

forced sellers?– What’s the risk that clients

could lose capital?

Explicit Knowledge

“You’re rewarded, if you

Informationexceed your target”

Risk models and quants

Data

Source: Citi/Principal/CREATE Survey 2011.18

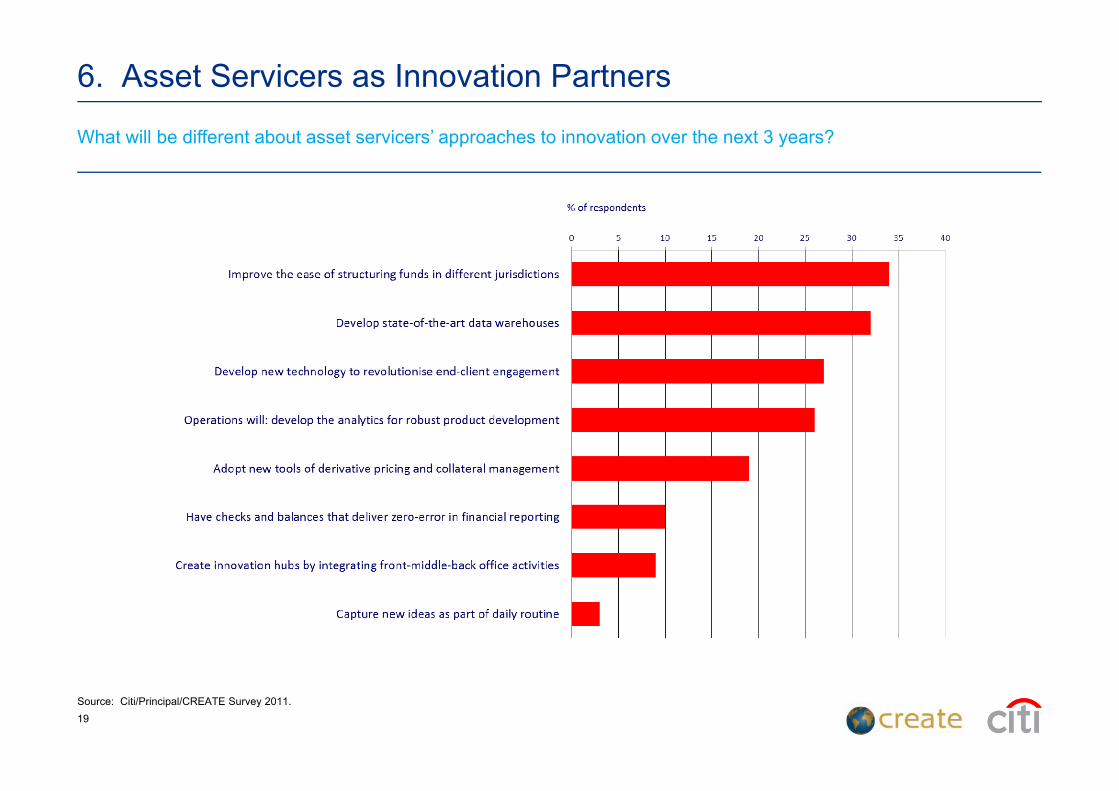

6. Asset Servicers as Innovation Partners

What will be different about asset servicers’ approaches to innovation over the next 3 years?

Source: Citi/Principal/CREATE Survey 2011.19

Conclusions

Client engagement and alignment is keyClient engagement and alignment is key

Simplicity and value for money

Best endeavours and focus on outcomes

Risk is front and centre of investors’ thoughts

Environment of TalentEnvironment of Talent

Avoid ‘hobbies’

Any questions?

How Are YOU Tackling Innovation?

Who leads innovation in your firm? Who leads innovation in your firm?

How are the effects measured?

How is innovation encouraged?

What do you think is the area of your y ybusiness which will be most impacted by innovation in next five years?

Where will it come from: Clients, Products, or Operations?

How will regulation affect the pace of innovation?

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice based on your particular circumstances from an independent tax advisorshould seek advice based on your particular circumstances from an independent tax advisor.Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the information contained herein and the existence of and proposed terms for any Transaction.Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that g y g g , g ( y y ) y p , y y gfrom the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction. We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also request corporate formation documents, or other forms of identification, to verify information provided.Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without

© 2011 Citibank, N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances.

Citi b li th t t i bilit i d b i ti W k l l ith li t fi i l i tit ti NGO d th t t fi l ti t li t h d l i d t t d d dCiti believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our ownenvironmental footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position Statement, the first USfinancial institution to do so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology, and other carbon-emissionreduction activities; (c) committing to an absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of carbon neutral power for ouroperations over the last three years; (e) establishing in 2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of electric power projects; (f) producing equityresearch related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understandingand solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy & mitigation