investment in south africa - enterprise europe network in bayern

TRANSCRIPT

Investmentin

South Africa

August 2002

Liability disclaimer

The information contained in this guide was collected during late 2001 and early 2002, and isbased on information available at that time. The information is not exhaustive and investorsare advised to take the relevant professional advice before taking any formal action.

KPMG cannot accept responsibility for any errors this guide may contain, whether negligentor otherwise, or take responsibility for any loss sustained by any person that relies oninformation herein, however caused.

© August 2002, KPMG IncThe Southern African member firm of KPMG InternationalISBN 1-875082-36-0 Produced by KPMGAlso available at www.kpmg.co.za

South Africa as an investment location

A dynamic investment location which offers:

■ a new constitution committed to democracy and the preservation of human rights;

■ unsurpassed physical and commercial infrastructures;

■ road, rail, air and sea access to the fastest growing markets in Africa;

■ growth-orientated economic policies;

■ a commitment to the expansion of trade links;

■ protection of intellectual property rights;

■ a commitment to public and private partnership in the expansion of infrastructureprojects in the region; and

■ a package of attractive investment incentives.

i

The protea is South Africa’s

national flower

ii

KPMG senior partner and chairman, Tom Grievewith deputy chairman, Moses Kgosana

About KPMG

KPMG is the world’s third largest business advisory firm, with 103 000 employeesbased in 152 countries and 760 cities. Locally, the firm has over 3 000 employees,based in 14 offices.

International clients include Apple Computer, BMW, BP Amoco, British Airways,Compaq Computer, DaimlerChrysler, Ericsson, Heineken, Hewlett Packard, HondaMotor, Mitsubishi Electric, Motorola, Nestlé, Nokia, PepsiCo, Rolls Royce, RoyalDutch Shell Group, Samsung, Siemens, Sony, TNT, TOTAL, Unilever and Volvo, toname only a few.

Its local client base is no less impressive. KPMG is proud of its 107 year track recordin South Africa which is reflected in our prestigious client listing which includes across-section of the country’s top performing companies, as rated by the FinancialMail’s annual top companies survey. These include six of SA’s top 10 asset leaders –Old Mutual, Stanbic, FirstRand, ABSA, Investec and Nedcor. Of the top 50industrials, KPMG provides services to Sasol, Bidvest, Iscor, Tongaat, PPC,Anglovaal Industries and Unitrans. A total of 91 companies listed on the main boardof the JSE enjoy the professional services of KPMG.

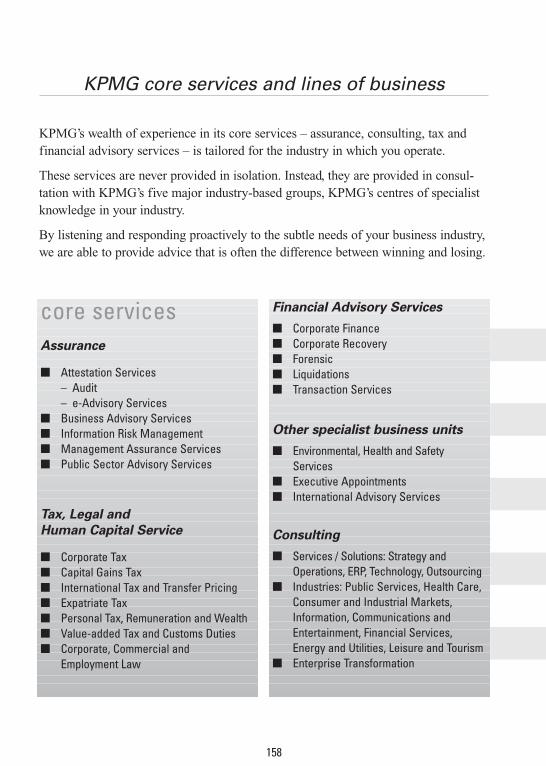

KPMG’s core services – assurance, consulting, tax, legal and human capital services,and financial advisory services – are delivered in conjunction with our five majorindustry-based areas – Financial Services, Industrial Markets, Consumer Markets,Infrastructure and Government, and Owner-Managed Businesses.

Transformation is affecting positively almost everything we do at KPMG. We areproud of our on-going transformation achievements. These include the merger ofKPMG and KMMT, which was completed by 1 April 2002. This merger now allowsour combined firm to radically accelerate our continuing transformation initiativesacross all spectrums of our business. We have a robust transformation strategy thatwas developed through a rigorous consultative process. We are also leading with theestablishment of our transformation advisory board.

Initiatives in our human resources area, which ensure that KPMG’s transformationinitiatives are on track, include recruitment, financial support, and a host ofdevelopment programmes. Black representation stands at 30% while women make up49% of the staff complement and 20% of senior management. Forty per cent ofbursaries have been allocated to previously disadvantaged groups. The vacationtrainee intake from this group stands at about 60%.

iii

Some R12 million was invested during 2001 on corporate social responsibility andvarious transformation initiatives, across a range of exciting educational and otherrelated community initiatives.

This guide has been written primarily to introduce the foreign investor to theformalities and procedures involved in setting up business in South Africa. I hopeyou will find it a useful introduction and look forward to you contacting myself orany of our offices where you will find professionals who will gladly help you set upbusiness in our country.

Tom GrieveSenior partner

iv

Truly South African

Transformation is positively affecting almosteverything at KPMG. Our firm, benefiting from ourambitious initiatives, is starting to truly reflect theSouth African society. Our merger with KMMT,

completed on 1 April 2002, is accelerating the process.

More detail about KPMG as a South African firmembracing transformation in the widest sense can be

found in our Trans[FIRM]motionTM publication or go towww.kpmg.co.za

Investment in South Africa

Page

Introduction ix

Note on the Republic of South Africa xiThis chapter covers issues such as investment climate,trade agreements, employment statistics, prospects for theeconomy and the restructuring of state assets.

KPMG’s corporate social responsibility (CSR) model xviii

Chapter 1 Investment in South Africa 1

Chapter 2 South Africa: A brief survey 31. Geographical description 32. Rainfall 43. Climate and temperature 44. Rivers 45. Vegetation 56. Population 57. Currency 78. Masses and measures 79. Land tenure 710. Minerals and natural resources 711. Business activity and living conditions 812. General welfare and living conditions 913. Public holidays 1014. Infrustructure 11

Chapter 3 Forms of business enterprise 171. Introduction 172. Industrial development 183. Regional industrial development 194. Import and export control 195. Patents, trademarks, designs and copyrights 20

v

6. Immigration and work permits 207. Exchange control and foreign investment 208. Competition 219. Tender preferences on government purchases 2110. Employment of labour and technical factory requirements 2211. Water, waterworks and water pollution 2212. Road transport 2213. Customs and excise 2214. Standards 2315. Industrial research and development 2316. Export trade promotion 2317. Industrial financing 2418. Small business promotion 24

Chapter 4 Companies and close corporations 251. Companies: Law and administration 252. Close corporations: Law and administration 31

Chapter 5 Exchange control 351. Introduction 352. Blocked rands 353. Exchange controls relating to individuals 364. Controls relating to companies resident in South Africa 435. Other regulations 476. Contraventions and penalties 48

Chapter 6 Banking and finance 491. Financial services industry 492. Bank legislation 513. South African Reserve Bank 524. Parastatal institutions 535. Insurance companies 556. International finance organisations 55

Chapter 7 Taxation in South Africa 611. Introduction 612. Income tax 623. Indirect tax 1014. Other taxes 1055. Budget proposal 106

vi

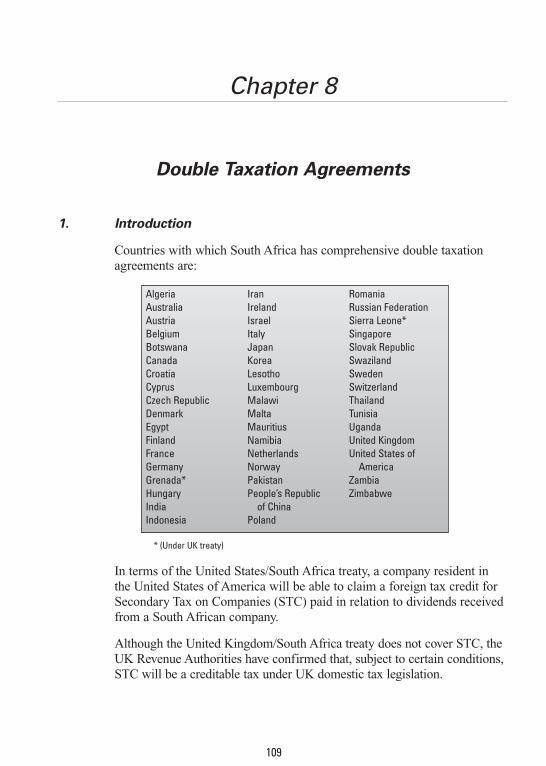

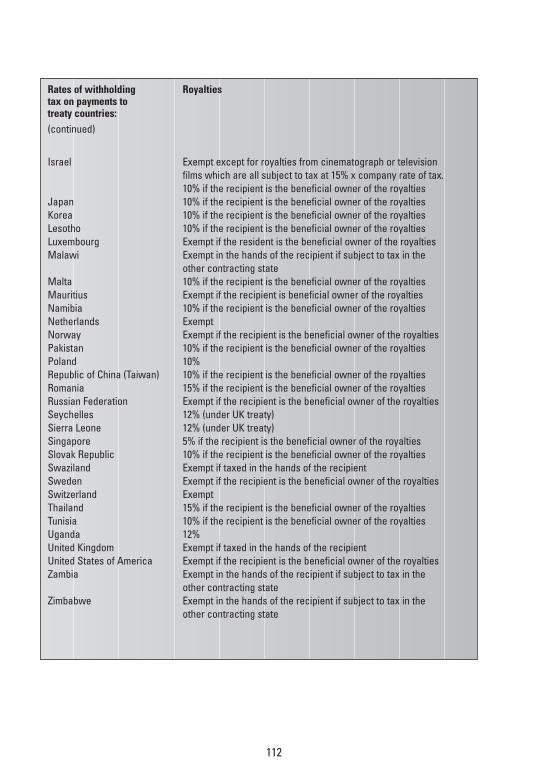

Chapter 8 Double taxation agreements 1091. Introduction 1092. Rates of withholding tax in terms of South Africa’s

double taxation agreements 111

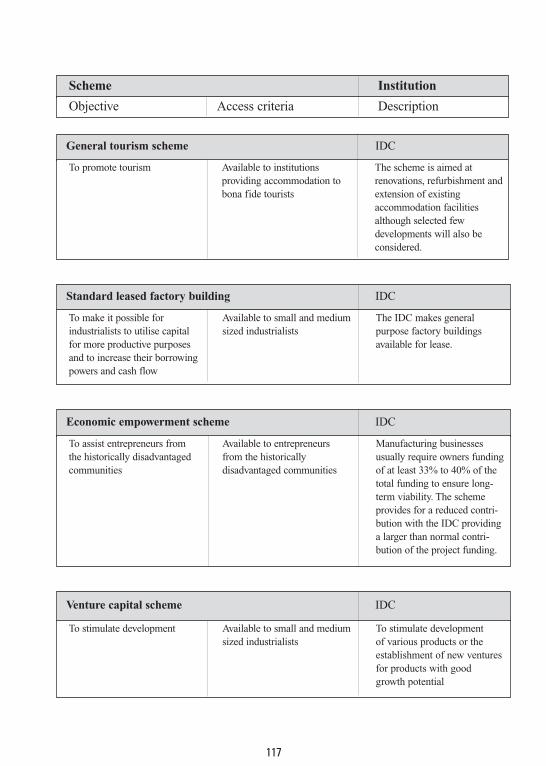

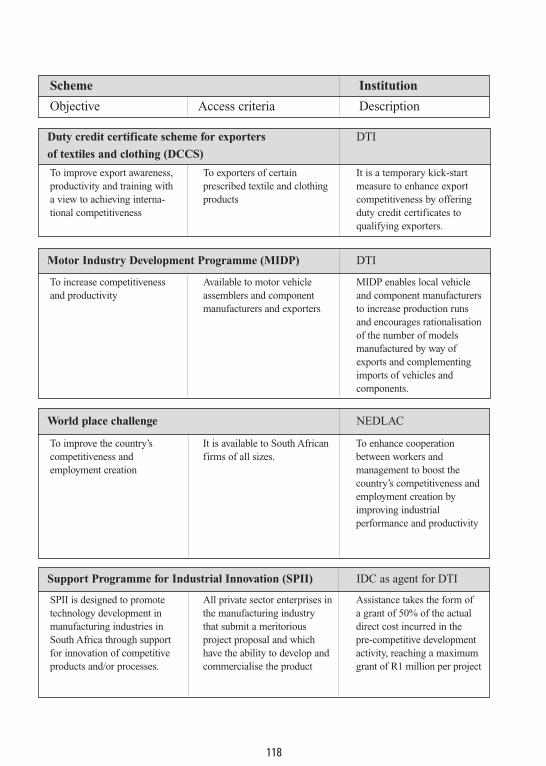

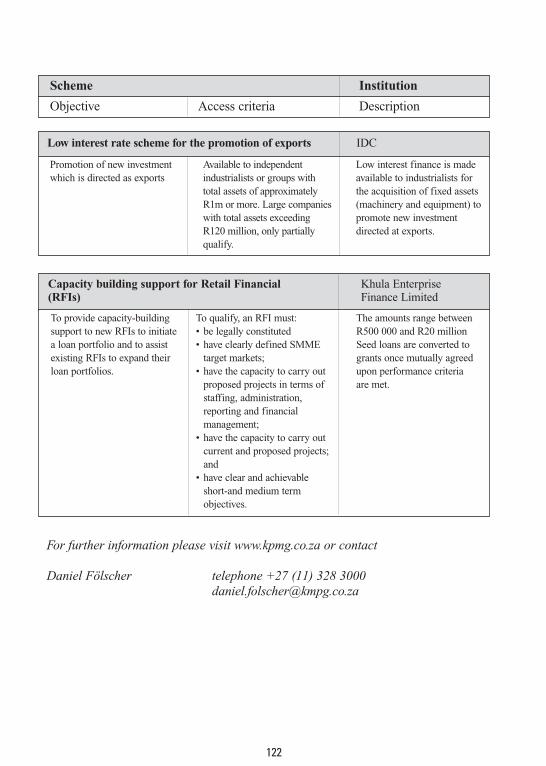

Chapter 9 Incentive schemes 113

Chapter 10 Industrial relations 1231. Introduction 1232. Statutory enactments 1233. Trade unions 1244. The constitution 1255. The Labour Relations Act, 1995 125

Chapter 11 Black economic empowerment 133

Chapter 12 Corporate governance and accounting standards 1371. Corporate governance 1372. Anticipating King II 1373. Accounting standards 142

Chapter 13 Technology 1451. Introduction 1452. Telecommunications 1463. Internet 1474. Information security 1495. Major industry players 150

Chapter 14 Tourism in South Africa 1531. Introduction 1532. Tourism in South Africa 1543. Conclusion 156

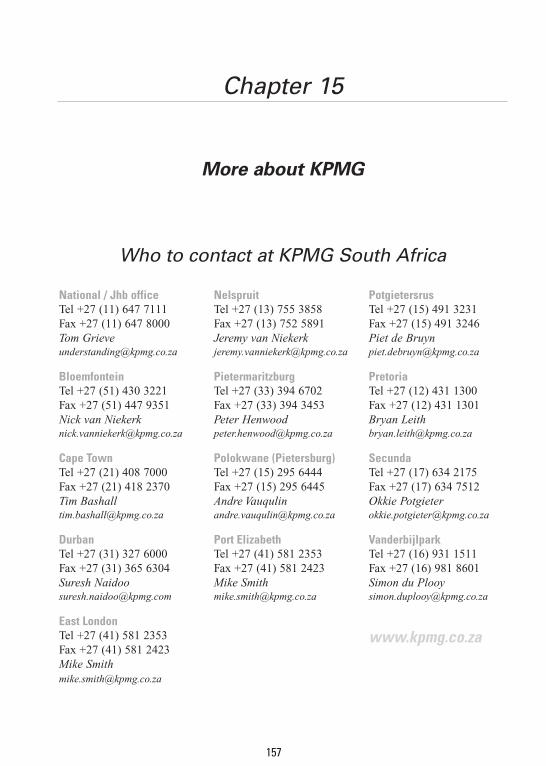

Chapter 15 More about KPMG 157

Who to contact at KPMG South Africa 157Core services and lines of business 158

Chapter 16 Internet sites 161

The next step 163

What do you think 166

vii

viii

South African president, Thabo Mbeki

Introduction

The Republic of South Africa, the Kingdoms of Swaziland and Lesotho and theRepublics of Botswana and Namibia are the signatories to the Southern AfricanCustoms Union Agreement. The latter countries do not fall within the scope of thisguide and information relating to them may be obtained from the KPMG officeslocated in those territories.

The information provided in this guide is for non-residents of South Africa who maybe contemplating investment in the country. It is also hoped that this guide will helpbusiness people resident in Southern Africa.

Foreign investors wishing to invest in South Africa would naturally need to choose a suitable business entity for their enterprise. This may take the form of a company, a branch of an overseas corporation, a close corporation, a partnership or operatingdirectly as individuals in South Africa.

It is intended that this guide should explain, in broad terms, the local requirementsaffecting the establishment and operation of a business enterprise in South Africa. In addition, general information is provided concerning taxation and currencyregulations.

The contents of this guide are not exhaustive. Decisions involving investments or the setting up of operations in South Africa should be made only on the basis ofspecific and detailed advice on the contemplated structure and modus operandi of the proposed undertaking.

The information contained in the following pages is based on company law, taxlegislation and other regulations in force in late 2001 and early 2002. Publications areissued periodically by KPMG dealing with changes occurring in legislation from time to time and are sent to clients and associated offices. This information is alsoavailable at www.kpmg.co.za.

ix

x

Former South African president, Nelson Mandela

Note on the Republic of South Africa

On 27 April 1994, the first general election in which all citizens of the Republic ofSouth Africa took part, was held. Following the general election in which NelsonMandela became president and his party, the African National Congress (ANC), came into power with an over 60% majority, the transitional or interim constitutionbecame the supreme law of the Republic of South Africa. Early in 1997, this interimconstitution was replaced with the final constitution embracing these principles:

■ commitment to a democratic system of government based on universal adult franchise;

■ regular elections;

■ a multi-party system;

■ one citizenship for all;

■ an entrenched constitution;

■ acknowledgement of the fundamental rights of the individual;

■ no discrimination;

■ an independent judiciary;

■ equality before the law;

■ separation of powers to prevent abuses; and

■ three levels of government (president and cabinet; national parliament andprovincial legislatures).

Since the 1994 general election, the government has continued to redress decades ofracial discrimination, especially in education, housing and welfare services.

Unemployment officially stands at 26,4% and is based on the 16,1 million econom-ically active group of people between 15 and 65 years of age. It represents thecountry’s single biggest problem and helps explain the crime rate. The situation hasbeen aggravated by illegal immigration from neighbouring countries whereemployment prospects are poor. Government continues to take major steps toimprove the management and increase the manpower of the police and to enforcethe powers of the courts to deter criminals.

xi

Other problems facing the new government include corruption, particularly atprovincial government levels, legal and illegal immigration from neighbouringterritories, and urbanisation which has created massive informal squatter campsaround established cities.

Investment climate

On the positive side, real economic growth has shown a promising upturn from 1,1% before the election in 1993 to an average of around 6%. The inflation target isexpected to reduce the annual average consumer price index to between 3% and 6%within two to three years. Moves towards a gradual elimination of exchange controlsare under way. Tourism is growing steadily and Cape Town, in particular, has becomeone of the cities favoured by the rich and famous. Generally the investment mood ismore favourable than it has been for many years.

Despite improved investment ratings from international rating agencies, significantinvestment in South Africa has not been forthcoming and for the first time since1998, the country experienced a net outflow of capital. Policy makers are frustratedwith investor’s lack of enthusiasm considering the sound fiscal policies that are inplace and the discipline that has been shown in comparison to other emergingmarkets. The following factors have been identified as hampering foreign directinvestment (FDI):

■ political instability in the region (Zimbabwe);

■ ongoing currency depreciation;

■ the stance taken by the government with regards to the HIV/AIDS epidemic;

■ perceived crime rate;

■ “brain drain”;

■ restrictive labour policies; and

■ difficulty in obtaining a South African work permit.

But growth of our economy has been underpinned by extensive structural reformsdesigned to ensure a more dynamic and resilient economy:

■ Export diversification continues, both in non-traditional manufactured goods,tourism-related trade and growth in services exports. Manufactured exports grewfrom 9% to 20% of gross domestic product (GDP) between 1990 and 2000.

xii

■ The balance of payments is immeasurably stronger and better able to sustainstronger growth – the current account will register a moderate deficit of 0,5% ofGDP in 2002.

■ Real wages and productivity have increased by over 20% since 1994, bringingrising living standards to millions of people and strengthening the competitivenessof industry.

■ The net open forward position has been reduced from some US$24 billion in1998 to just under US$3 billion in January 2002.

■ The budget deficit is expected to be 2,1% of GDP in 2002/03 falling to 1,7% in2004/05.

Primary contributors

The agricultural sector contributes only 4% of the gross domestic product (GDP).The mining sector played an important role in the development of the South Africaneconomy, but its importance has declined in the last decade and currently accountsfor about 6% of GDP. The manufacturing sector accounts for approximately one-fifthof South Africa’s GDP. The contribution of financial services and business increasedfrom about 12% to nearly 18% during the nineties and, given the high level ofbanking and commercial activities in South Africa, this share is expected to expandeven further. Tourism activity is also expanding its relative size and further increasesin the contribution of the tertiary sector to GDP are expected. (Source: www.gov.za/yearbook)

Trade agreements

■ European Union

The SA European Union trade and development cooperation agreement has beenin operation since 1 January 2001. The agreement is extensive and covers a rangeof industries that produce commodities ranging from wines and spirits, stainlesssteel, purifying and filtering equipment, fruit juices, bottled water, fish products,gold, platinum, coal and diamonds, to name only a few.

The success of the agreement is evident in the 35% increase in SA’s exports to the EU in 2001. During the same period, EU exports to SA grew 20% (November 2001).

xiii

After the end of the 10 year transition period of the free trade area, 95% of EUimports from SA would enter the EU market free of duty. SA would be able toretain its tariff barriers for longer. After a transition of 12 years, SA will open86% of EU imports to duty free trade.

■ United States

South Africa, together with other eligible countries, is covered by the UnitedStates Africa Growth and Opportunity Act (AGOA) which affects many industriessuch as clothing and automotive sectors.

The Africa act is meant to provide duty- and quota-free access to the US marketessentially to all products from sub-Saharan African countries. This includespreferential access for some products that were previously considered to beimport-sensitive. It also provides additional security for investors and traders in sub-Saharan African countries with a general system of preference benefits for eight years.

In the apparel industry, the act lifts all existing US import quotas on textiles andapparel products from sub-Saharan Africa and extends duty- and quota-free USmarket access to apparel made in Africa from US yarn and fabric.

The act also extends duty- and quota-free treatment to sub-Saharan Africanapparel made from yarns and fabrics not available or not produced in commercialquantities in the US and for “knit-to-shape” sweaters made in Africa fromcashmere and some merino wool.

It extends duty- and quota- free treatment to apparel made in Africa with Africanor regional fabrics and yarns.

Employment statistics

■ Despite the endeavour of government to uplift the economy, the legacy of the pasthas a huge impact on growth potential. In 2001, there were an estimated 27,1million people aged between 15 and 65 years, of which 16,1 million were econom-ically active; 11,8 million were employed and 4,2 million were unemployed. *

However, the total labour force was projected to be 21% lower in 2015, with theoverall size of the labour force remaining almost stagnant over the next 14 years.This is according to a macro-economic sensitivity analysis of the impact ofHIV/AIDS on the South African economy through 2015 conducted by the Bureauof Economic Research (BER).

xiv

■ The total number of people employed in the formal sector, excluding agriculture,stands at 6,7 million.*

■ All provinces, except KwaZulu-Natal, Mpumalanga and North West, experienced aslight increase between September 2000 and February 2001.*

■ Unemployment is highest among African women and lowest among white men.However, the disparity in gender within population groups is highest among theIndian population.*

■ The previously disadvantaged sector of the community holds 14% of the wealth,but comprises 80% of the population. Unemployment and income distribution aretwo of the major challenges facing modern South Africa – future focus on thesekey issues will go a long way to improving economic growth within the country.Economists believe that annual growth of at least 5% is required to addressunemployment and past social imbalances.

■ With a population growth rate of 2%, the economy could continue to register 3%average real GDP growth – or better – over the next 10 to 15 years. However,sceptics remain negative and sizeable international investments have not beenforthcoming since 1997. In order to increase optimism and create employment,foreign direct investment is a requirement.

Prospects for the economy in the future

There is a need for clean differentiation between South Africa and its neighbours, butthere is also a need for the country to take an active role in the development of itspartners in Africa. The signs are positive. The increasing role of South Africancompanies across the whole economic spectrum in places like Tanzania, Mozambiqueand Gabon is reminiscent of the role played by Singapore and Hong Kong in thedevelopment of regional economies in the Far East. The knowledge of Africa andability to apply African solutions to peculiar problems is perhaps the light that isrequired to fire economic growth.

The government has been particularly pro-active in communicating its vision of anAfrican Renaissance, African Century and a “Marshall Plan” for Africa. The wordssound good and make sense, but economic judgement will be made on delivery, notgood intentions. South Africa is, however, taking the lead and such an approach couldprovide dividends as greater focus becomes placed on employment, investment andgrowth, rather than aid.

xv

* These statistics are taken from Statistics SA’s Study; Labourforce Survey, February 2001.More detail is available at www.statssa.gov.za.

Econometrix has projected the following growth figures for South Africa over thenext ten years:

Amidst this, South Africa’s economy has shown impressive resilience. It is easilyforgotten that the average rate of growth in real GDP between 1994 and 2000 was2,7%. If we exclude 1998, a year of exceptional international turmoil due to the Asianfinancial crisis, average growth was 3,1%. The economy grew by 3,4% in 2000 andabout 2,2% in 2001, underpinned by a moderate recovery of investment and a strongexport performance in the first half of last year.

But of course the South African economy is not immune to internationaldevelopments which have temporarily unsettled growth and inflation trends. Growthfor 2002 is expected to be 1,8% rising to 3,7% in 2003. Against the background of anunexpected depreciation of the rand in the second half of last year, we now expectinflation to pick up moderately this year.

Such figures are attainable if government maintains its current endeavours to winover the international community. Government has laid the following plans to attractinternational investors:

xvi

■ create a welcoming environment for investors;

■ establish a greater distance between South Africa and other African countries inperception, but convergence in economic terms;

■ double the economic growth rate from 2,5% to 5% through a mixture of domesticand foreign investment;

■ liberalise labour policies; and

■ limit bureaucracy for skilled personnel applying for work permits.

Government also plans to be more pro-active in promoting South Africa throughinitiatives such as the International Marketing Council, the Africa developmentprogramme and an international advisory panel. There is goodwill in the internationalcommunity towards South Africa. There must, however, be recognition thatcompetition for foreign direct investment (FDI) is global and that the wrongs ofapartheid mean little in terms of international shareholder value.

Restructuring of state assets

Apart from new regulatory initiatives and competition policy to stimulate investmentand expand employment through gains in efficiency, the government is engaged inthe restructuring and privatisation of state enterprises.

Most state-owned enterprises, especially in the energy, telecommunications andtransport sectors, have now been corporatised, allowing for management reform andincreased transparency in the allocation of financial resources. The government iscommitted to the further restructuring over time of the four largest state-ownedenterprises, namely Telkom, Eskom, Transnet and Denel.

The objectives of the restructuring of state assets are to extend public services, suchas the roll-out of telephone lines to more people, and to improve the efficiency ofservice delivery.

The restructuring of state enterprises aims to bring capital, technology and renewedcorporate leadership to the utilities sectors, while transferring several non-strategicentities to the private sector. Further economic benefits include a reduction in statedebt, the lowering of interest costs and thus the possibility of a reallocation ofresources towards social spending and infrastructure. Privatisation will also lead toincreased foreign direct investment.

(Reference: www.gov.za/yearbook)

xvii

xviii

KPMG’s corporate social

responsibility

At KPMG, community matters. A three-tiered investment model, consisting of charity,commercial initiatives and community involvement, supports KPMG’s corporate socialresponsibility (CSR) strategy.

The strategy is enduring and invaluable, contributing to programmes as diverse aseducation of people from previously disadvantaged areas, help for the physically andmentally disabled, and hands-on involvement in environmental projects such as therelocation of elephants. KPMG’s philosophy is to lean towards sustainable projectswhere the firm can make a difference, ideally through active involvement.

The old adage, Charity begins at home, is one that KPMG takes seriously and putsinto practice. KPMG is strongly committed to improving the well-being of those lessfortunate, having made significant contributions through corporate social responsibility.

The firm provides more than 150 honorary engagements to charities such as theJohannesburg Child Welfare organisation, and makes financial contributions to manyothers. These include the Association for the Physically Disabled, Boy’s Town, theAvril Elizabeth Homes and the Takalani Project for the Mentally Disabled, SOSChildren’s Village and the Association for the Physically Disabled.

In the spirit of the words of Henry Ford, My best friend is the one who brings out thebest in me, KPMG strives to befriend the community by providing communityinvestments that are uplifting and durable.

KPMG has strengthened its involvement in educational projects implemented someyears ago, which now have enviable reputations. The wisdom of monitoring progress,and providing resources in a focused manner, have borne fruit with an outstandingimprovement in the matric pass rates in the schools that are supported.

Kudung, near Heidelberg, has improved its matric pass rate by 269% between 1997,the year before KPMG’s involvement, and 2000. The neighboring Kgoro-Ya-Thutoschool turned in a 94% improvement between 1999 and 2000.

Apart from resources that are committed to schools, KPMG also invests in universitiesand informal learning centres, through financial donations, honorary audit andaccounting work, time spent lecturing and mentoring, marking examination papers,and other direct donations, particularly of computer equipment. It will spend morethan R4 million on bursaries in 2002. Academic intervention programmes aresupported at several universities.

Building equity for previously disadvantaged communities goes beyond the obviousfor KPMG. Those still learning must be exposed to KPMG’s long-term commitment totransformation; thus the commissioning of the Johannesburg Girls’ School to do theartwork for KPMG’s first corporate social responsibility brochure.

A comprehensive programme aimed at addressing career awareness of theaccountancy profession in schools is now in place.

A two-year academic support programme for previously disadvantaged individualsbegan this year.

It has been said Humans are complex beings. They make deserts bloom and lakes die.KPMG’s commercial initiatives aim to create sustainable and productive environmentsin which all life can blossom.

The firm has continued its involvement in elephant relocation, extending this to the new Transfrontier Park straddling the borders of South Africa, Mozambique and Zimbabwe. The project now also involves the relocation of buffalo, rhino and roan antelope.

The Cape Town office participated enthusiastically in the clean-up of the penguinsfollowing the oil spill off the Cape coast early in 2001. KPMG also sponsoredawareness programmes for a crime-free society.

In a groundbreaking public-private sector initiative to fight cholera in KwaZulu-Natal,KPMG donated more than 12 tons of Jik to families in some of the worst affectedareas in the province. The programme was praised by Professor Ronald Green-Thompson, secretary of the KZN department of health, as one that had a significantimpact in providing safe water, and in educating people on how to protect themselvesfrom the disease.

KPMG also boasts an entirely local art collection. Black artist commissions make uphalf of this inspiring collection, that we continue to invest in.

xix

xx

An example of South Africa’s vast mineral resources is the Phalaborwa Complex inthe Limpopo Province. This geological phenomenon is one of the world’s great

mineral repositories containing large deposits of copper and phosphates, magnetiteas well as the world’s largest deposit of vermiculite. It also hosts important concen-trations of zirconium, nickel and precious metals. This treasure trove is also yielding

titanium, one of the world’s most sought-after metals. Shown above is Foskor’s phosphate plant in the region.

Chapter 1

Investment in South Africa

South Africa is a young developing country and depends heavily on overseasinvestment for its continued growth. The injection of investment funds from abroad isessential to ensure the proper exploitation of the country’s vast natural resources,which will in turn enhance the continued development and advancement of all thepeople living in the sub-continent.

Now, more than ever before, South Africa has many attractions for the foreign investor:

■ South Africa is the most advanced country, both technologically and economically, in Africa.

■ South Africa represents some 80% of Africa’s rail infrastructure.

■ South Africa possesses seven superb deep water ports. These, together with its airports, contribute in no small measure to its claim to be the gateway to sub-Saharan Africa.

■ South Africa generates 70% of the electric power on the African continent.

■ The steady increase in black living standards, together with massive urbanisation, has resulted in this section of the population being recognised aspossessing an enormous amount of disposable income and being responsible forthe major share of consumer spending.

■ The country has a highly sophisticated transport infrastructure, which isconstantly being improved.

■ Communications are efficient and improved technologies are continually beingintroduced into the system.

■ Primary and secondary industries are modern and competitive. The mostadvanced technologies are also employed.

1

■ The country is endowed with a fabulous store of natural mineral resources.

■ South Africa’s vast proven coal reserves have more than made up for its lack of oil.

■ The country is acknowledged as a world leader in “oil from coal” technology with numerous plants presently in operation together with an “oil from off-shore natural gas” operation.

■ The country’s first nuclear power station came on stream in 1984.

■ South Africa is today a net exporter of energy.

■ The country’s climate is probably one of the best in the world with mainlytemperate conditions all year round.

■ Situated as it is on the African continent, South Africa is ideally placed to export to any part of the world.

■ Similarly, South Africa enjoys the many benefits of being within the CentralEuropean time-zones, falling between the Americas and Asia-Pacific.

2

South African cities such as Johannesburgwere built as a result of the discovery of

gold some 100 year ago.

Chapter 2

South Africa: A brief survey

1. Geographical description

South Africa forms the southern most part of the African continent and liesalmost entirely in the southern temperate zone between 22° and 35° south.The country has a surface area of 1 219 090 km2 and is five times the sizeof Great Britain and almost as large as the combined areas of France, Italy,the Netherlands, Belgium and the former West Germany.

South Africa presently consists of nine provinces – Eastern Cape, Free State, Gauteng, KwaZulu-Natal, Mpumalanga, Northern Cape,Limpopo (Northern Province), North West Province and Western Cape.Most of the country is a vast interior plateau with an average altitude ofmore than 1 200 metres.

LIMPOPO

KWAZULU-NATAL

EASTERN CAPE

NORTHERN CAPE

WESTERN CAPE

Polokwane

Durban

East London

Cape Town

NAMIBIA

BOTSWANA

ZIMBABWE

MOZAMBIQUE

REPUBLIC OF SOUTH AFRICA

MPUMALANGAGAUTENG

FREE STATE

LESOTHO

NORTH WESTPROVINCE

Johannesburg

Bloemfontein

Port Elizabeth

Upington

SWAZILANDPretoria/Tshwane

3

There are four major geographical regions: The Coastal Belt between theescarpment and the sea; the Little Karoo, a narrow tableland separatedfrom the Coastal Belt by the Langeberg and Outeniqua mountains; theGreat Karoo, separated from the Little Karoo by the Swartberg andSuurberg mountains; and the Highveld comprising the Northern Cape, theFree State and part of KwaZulu-Natal together with Gauteng and most ofthe Northern Province. The coastline is 3 000 km long and is bordered bytwo oceans, the Atlantic in the west and the Indian in the south and east.Two major current systems, the warm Mozambique in the east and southand the cold Benguela in the west, flow along the country’s shores.

2. Rainfall

South Africa enjoys a summer rainfall. There is a relatively small region, theWestern Cape, where winter rainfall occurs. On the eastern seaboard, therainfall exceeds 1 000 mm per annum but it decreases gradually to less than125 mm in the desert regions of the Northern Cape in the west. The centralplateau enjoys a rainfall varying between 375 mm and 715 mm annually.

3. Climate and temperature

South Africa has a very healthy and invigorating climate which is probablyone of the best in the world. Warm and temperate conditions prevail and theaverage number of hours of sunshine a day throughout the year ranges from

7,5 to 9,4. It is interesting to compare this with London andNew York which enjoy 3,8 and 6,9 hours respectively. In

winter, the sun shines continually and there is norain, except in the Western Cape. Mean annual

temperatures tend to be lower in South Africathan in countries in similar latitudes elsewhere

in the world, mainly being due to thegreater elevation of the sub-continent.

4. Rivers

South Africa’s rivers are not navigable;their fall is steep and their flow erratic.

Accordingly, water conservation enjoys toppriority. The most ambitious scheme to date is

the Orange River project which harnesses thewaters of the Orange River for industrial and

agricultural purposes and also the generation of electric power.

4

During the periods of drought, some remarkable feats of engineering havebeen accomplished. The flow of the Vaal River was reversed for a portionof its length in order to ensure a constant supply of water to the series ofenormous thermal power stations situated in the Northern Province.

The World Bank is presently funding a project which will see the waters ofthe rivers in the mountains of Lesotho being sold to South Africa. Thisambitious project is well advanced.

5. Vegetation

Vegetation in South Africa ranges from desert and semi-desert throughbushveld and savannah to temperate grasslands and forests. The mainvegetation is grass veld which ranges from poor to good, and is prairie-likein the highveld regions. South Africa has more than 17 000 species of wildflowers, the richest variety in the world.

6. Population

According to Census ’96 figures, released in October 1998, on the night of 9 October 1996 there were 40,58 million people in South Africa. This tablereflects how the population is broken down between the major race groups.

According to Statistics SouthAfrica, the country’s mid-1999population estimates stood at43,054 million, of whichwomen constituted some 22million.

A census was again conductedduring 2001, the results ofwhich are expected to beavailable in 2003.(www.statssa.gov.za)

5

The South African population consists of:

■ the Nguni people, who account for two-thirds of the population;

■ the Sotho-Tswana people, who include the Southern, Northern andWestern Sotho (Tswana);

■ the Tsonga;

■ the Venda;

■ Afrikaners;

■ English;

■ Coloureds;

■ Indians; and

■ several different groups of people who have immigrated to SouthAfrica from the rest of Africa, Europe and Asia and who maintain astrong cultural identity.

A few members of the Khoe and the San also remain.

[Source: www.gov.za]

Whites are descended from European settlers; large influxes of all nation-alities having been experienced with the discovery of diamonds and goldin the second half of the 19th century.

Coloureds are the historical result of the intermingling of the variouspopulation groups. Their forebears were the white settlers, the indigenousHottentots, Malay and other slaves from the East and black Africans.Eighty per cent of the coloureds live in the Western Cape Province. Theirlanguage is predominantly Afrikaans. The Cape Malay section of thecoloured population has retained its Muslim traditions including Islam.

The Indian population is descended predominantly from the indenturedlabourers brought to KwaZulu-Natal from India from 1860 onwards towork in the sugar cane fields. They live mostly in KwaZulu-Natal butmany are resident in Gauteng. They speak various Indian languages andthe Hindu and Muslim faiths predominate.

South Africa is a multilingual country and there are eleven officiallanguages. These are English, Afrikaans, Zulu, Xhosa, Sesotho, Siswati,Tsonga, Venda, Pedi, Setswana and Ndebele. The most widely spokenlanguage is Zulu, while Afrikaans is the most widely used. English is themain language of business.

6

7. Currency

The currency unit of South Africa isthe Rand (ZARl=100c). TheCommon Monetary Area (CMA)comprises South Africa, Namibia,Lesotho and Swaziland. The CMAcountries have their own currencies,but trade on parity with the SouthAfrican rand.

8. Masses and measures

The metric system of masses andmeasures is used in South Africa.

9. Land tenure

Except in very special circumstances, all land in South Africa is heldunder freehold title. Land is referred to as “immovable property” and alldeeds affecting ownership of immovable property must be registered at theoffice of the Registrar of Deeds. There are ten deeds registries each withits own territorial jurisdiction.

10. Minerals and natural resources

The country is rich with minerals and natural resources. The mostimportant export minerals are gold, coal, diamonds, iron-ore, platinum,copper, manganese, chromium and uranium.

South Africa is the world’s main supplier of manganese, gold, vanadium,ferrochromium, alumino-silicates and chrome ore, and the second mostimportant supplier of platinum group metals, vermiculite, zirconium,titanium, antimony and asbestos. The country is also the third mostimportant supplier of diamonds and uranium.

In 2001, the South African government introduced a minerals bill into thepublic forum for debate and comment. The primary objective of the mineralsbill is intended to bring the South African minerals industry in line with therest of the world and enable all minerals beneath the surface to belong to thenation. The bill is expected to be enacted as law within 2002.

7

11. Business activity and living conditions

Business in South Africa is conducted on lines very similar to the Britishbusiness system. Many of the fundamental characteristics of South Africanbusiness were derived from British systems, but there are also a great manysubsidiary and associated companies of western European parentcompanies in the country.

Many US parent companies, because of the sanctions campaign againstSouth Africa, disinvested. Most of these subsidiaries were either boughtout by management or purchased by South African conglomerates. A number of US businesses have returned to the country since 1994.

Business is well-organised and the country’s infrastructure operatesefficiently. Statutory controls on banks, insurance and public investmentcompanies are strict and a high degree of investor security in these areas is maintained.

The JSE Securities Exchange enjoys an enviable reputation. The legal,accounting, medical and other professions are well regulated by theirrespective controlling bodies.

The country is well-developed industrially and commercially, and businesstechniques and services are highly sophisticated.

Banking services are comprehensive and the business community is servedby a number of commercial banks, merchant banks, discount houses,general banks and building societies offering a wide variety of up-to-datefinancial facilities. Banking technology is very sophisticated and SouthAfrica has probably one of the most advanced electronic banking systemsin the world.

All types of goods and services are freely available. Prices generallycompare well with those in other parts of the western world.

South Africa was plagued by a very high rate of inflation. However, thecountry’s monetary authorities have, through stringent monetary policies,reduced the inflation rate from around 15% per annum on average, to acurrent figure of about 6–7%.

8

For the overseas visitor, business person or investor, the low value of therand means that prices in South Africa are currently very attractive. Hotelaccommodation compares favourably with the rest of the world and isinexpensive by world standards.

Middle income housing is generally in separate houses or townhouses,flats and apartments.

Transport facilities by rail, road, sea and air are efficient and more thanadequate for the needs of the business community.

Business dress for men is usually a business suit with comparablestandards of dress being observed by women in the world of commerce.

Hours of business vary but are usually from 08:00–08:30 to 16:30–17:00Monday to Friday. Shops open for approximately the same hours and ifhoused in shopping centres are also likely to be open on Saturdays and, inmost areas, on Sunday mornings. Those shops not housed in shoppingcentres are likely to be open until 13:00 on Saturday and closed on Sundays.

All sporting and cultural pursuits are well-catered for and the superbclimate makes for an outdoor lifestyle.

12. General welfare and living conditions

South Africa has many advantages for the investor. The far-reachingconsequences of the country’s divided history complete the picture,however. For example:

■ Social, educational and community welfare services and employmentopportunities are skewed along the lines set by apartheid policies, eventhough these policies no longer apply.

■ Although the country produces more than enough food for a population of its size, poverty and malnutrition are a reality formillions of South Africans.

■ There is a large backlog in the provision of low-cost housing.

■ Literacy and skills among the majority of the economically activepopulation are at a low level.

9

■ Unemployment, officially standing at 26,4%, is based on the 16,1 million economically active group of people between the ages of15 and 65. This has resulted in a high crime rate, particularly in theurban areas.

■ Despite government’s differing views on HIV/AIDS, it is believed to bethe country’s number one killer and government has given substantialfinancial aid to its HIV/AIDS programme. This includes increasing itsspend on provincial health departments for Aids-related illnesses,funding for prevention programmes in schools and communities,hospital treatment and community care programmes. It also includes aprogressive roll-out of the programme to prevent mother-to-childtransmission, medication for prevention of tuberculosis and pneumoniain infected people and treatment of opportunistic infections.

13. Public holidays

South Africa has 12 public holidays. They are:

New Year’s Day – January 1Human Rights Day – March 21Good Friday – Friday before Easter SundayFamily Day – Day after Easter SundayFreedom Day – April 27Workers’ Day – May 1Youth Day – June 16National Women’s Day – August 9Heritage Day – September 24Day of Reconciliation – December 16Christmas Day – December 25Day of Goodwill – December 26

If any of these days fall on a Sunday, the following Monday becomes apublic holiday.

10

14. Infrastructure

South Africa has a solid infrastructure including an extensive roadnetwork, railways, airports, pipelines and harbours. The modern transportsystem plays an important role in South Africa’s national economy as wellas for several other African states which use the South African transportinfrastructure to move their imports and exports.

Transport in South Africa is coordinated by the Department of Transport(www.transport.gov.za). The new policy shifts government from operationsto policy, planning and regulation. It bases delivery of infrastructure andservices on public-private partnerships and promotes the contracting out ofbus and rail services while drawing the taxi industry into the formaltransport system.

The National Department of Transport began the Moving South Africaproject in June 1997, with a mandate to “develop a strategy to ensure thatthe transportation system of South Africa meets the needs of South Africain the 21st Century and therefore contributes to the country’s growth andeconomic development”. The project encompassed a 14-month process totake the goals of the 1996 White Paper on National Transport Policy anddevelop a twenty-year strategy to achieve them.

14.1 Public transport

South Africa has inherited a public passenger transport system that isunder-performing against its obligation to achieve national goals. Keydevelopment goals are not being met, including basic mobility, basicaccess, and social integration. Workforce mobility is restricted, creatingfriction around national efforts to create employment opportunities.Current spatial distribution leaves commuters and other residents distantfrom key services that they need, and the system’s overall inefficiency iscreating high requirements for subsidy.

There are three main forms of public transport in the country:

■ taxi (vans);

■ rail; and

■ bus.

11

14.2 Roads

On 1 March 1998, motorists in South Africa were introduced to the newformat driving license, replacing the license previously printed or affixedto pages in identity documents. The new license is termed credit cardformat (CCF) as it resembles in shape and size, a conventional bank credit card.

The national road system provides links to all the major centres in thecountry as well as to neighbouring countries. These roads include around1 400km of dual-carriage freeway, 292km of single carriage freeway and4 401km of single-carriage main road with unlimited access.

14.2.1 Fuel prices

Recent fuel price trends are as follows:

The increase in fuel prices can be attributed to:

■ depreciation of the rand; and

■ increase in the dollar rate per barrel.

Government has cut South Africa’s roadworks budgetfrom R1,5 billion to R550m per annum which raisessome concerns as to the ongoing maintenance of theroads in the light of inevitable deterioration of theroads over time.

To maintain South Africa’s major roads, the following national routes havebeen converted to toll roads:

■ N1 (primary Johannesburg / Cape Town route) – 6 toll plazas

■ N2 (primary Cape Town / Durban route) – 5 toll plazas

■ N3 (primary Johannesburg / Durban route) – 4 toll plazas

■ N4 (primary Johannesburg / Pietersburg route) – 5 toll plazas

2000 1999 1998 1997

Petrol 25% 25% 4% 9%

12

14.2.2 N3 construction project

The contract for the R2,5 billion upgrade of the N3 highway betweenDurban and Johannesburg was awarded to the N3 Toll Road. The contractis for the construction, financing, operation and maintenance of 420km oftoll road between Cedara in KwaZulu-Natal and Heidelberg in Gauteng,plus the development of associated facilities under a 30-year concessioncontract to be managed by Sanra.

14.2.3 Arrive Alive

The problem of road safety is very simple: Between 9 600 and 10 000people die on South African roads every year. Almost 150 000 people areinjured in the approximately 500 000 crashes that occur each year. Besidesthe traumatic emotional cost this has on the social fabric of society, theCouncil for Scientific and Industrial Research (CSIR) estimates that thiscosts R11,9 billion to the country’s economy.

The Arrive Alive road safety campaign was initiated as a short-terminitiative to reduce the carnage on South Africa’s roads. The first campaignran from 1 October 1997 to the end of January 1998 with subsequentcampaigns following. (www.transport.gov.za/projects/arrive)

The main objectives of the campaign are:

■ to reduce the number of road traffic accidents in general – andfatalities in particular – by 5% when compared to the same period theprevious year;

■ to improve road user compliance with traffic laws; and

■ to forge an improved working relationship between traffic authorities atthe various levels of government.

14.3 Rail

The rail network in South Africa falls under the control of Spoornet(www.spoornet.co.za) and the South African Rail Commuter Corporation(SARCC). Spoornet provides rail transport mainly for goods andcontainers, but also transport for passengers on the long-haul routesbetween major cities. The SARCC, in turn, is responsible for providingcommuter services in the six major urban centres.

13

14

Spoornet’s rail infrastructure represents some 80% of Africa’s railinfrastructure, including 31 700km of single track, 3 500 locomotives and124 000 wagons. There are nine major rail routes that cover, amongstothers, the following main geographic locations:

■ Johannesburg

■ Cape Town

■ Durban

■ Port Elizabeth

■ East London

■ Bloemfontein

■ Kimberley

14.3.1 Spoornet

Spoornet is a South African company that operates in the freight logisticsand passenger markets in southern Africa. In line with industry forces,Spoornet has committed itself to a vision of world-class freight logisticsand accepted the challenge of being a world leader in this field, fulfillingits responsibilities to South Africa.

Spoornet is the largest division of Transnet, a state-owned company with adiverse portfolio that includes port management and services, pipelines,road haulage and air carrier divisions. Transnet was created in 1990 as aresult of government policy to commercialise its transport businessinterests and deregulate the transport industry in South Africa.

Spoornet is the largest heavy haulier and transporter of general freight inthe Southern African region. Spoornet enhances its rail offerings with anumber of logistics services, each solution flexible and customised tomatch the customer’s unique requirements. The freight business structureincludes two specialised business units:

■ COALlink, benchmarked as a world best heavy haul operator; and

■ OREX which provides dedicated services for the export of iron ore onthe Sishen-Saldanha line.

The general freight business is managed by dedicated business managers.

In the domestic passenger market, Spoornet provides safe and cost-effective transportation to more than five million people each year. Theflagship luxury Blue Train is a five-star hotel on wheels, offering gueststhe best of modern technology and superior service.

14.3.2 SA Rail Committee Corporation (SARCC)

SARCC’s mandate is to ensure that, at the request of the NationalDepartment of Transport or any local government body designated as atransport authority, rail commuter services are provided in the publicinterest. These services are currently provided under contract by MetrorailServices in terms of an operating agreement.

14.4 Harbours

By far the largest, best-equipped and most efficient network of ports onthe African continent, South Africa’s seven commercial ports have asignificant role to play. They are not only conduits for the imports andexports of South Africa and neighbouring countries, but also serve as hubsfor traffic emanating from or destined to the East and West African coasts.

Portnet (www.portnet.co.za), a division of Transnet Ltd, manages andcontrols all seven commercial ports on the South African coastline –Durban, Richards Bay, East London, Port Elizabeth, Mossel Bay, CapeTown and Saldanha Bay. Another deepwater port designed primarily forcontainers, the Port of Ngqura (Coega Industrial Zone), in the PortElizabeth area, has been given the go-ahead by the South Africangovernment (www.coega.co.za). It is expected that the port will becommissioned in 2005.

The South African Marine Corporation (Safmarine) and Unicorn andGriffin Shipping are the country’s largest shipping lines. Their fleets ofcontainers, oil tankers, general cargo and bulk cargo vessels provideservices between South African ports and the major ports of the world.

14.5 Pipelines

Since its inception in 1965, Petronet manages, operates and maintainsSouth Africa’s strategic network of 3 000km of high pressure petroleumpipelines. Products transported are crude oil, leaded and unleaded petrol,diesel, aviation turbine fuel, alcohol and gas.

15

14.6 Air

The Airports Company South Africa (www.airports.co.za) operates all nineof the state airports – Bloemfontein, Cape Town, Durban, East London,George, Johannesburg, Kimberley, Port Elizabeth and Upington. The Johannesburg, Cape Town and Durban airports are classified asinternational airports.

South African Airways (SAA), Comair (British Airways), Nationwide, SAExpress and SA Airlink operate scheduled domestic and/or internationalair services within South Africa, with Africa and to Europe, North andSouth America, Australia, and the Middle and Far East.

SAA (www.flysaa.co.za) is Africa’s leading airline and their mission is tobe the carrier of choice in the markets they serve. On 1 April 1999 SouthAfrican Airways, formerly a division of Transnet, entered a new era ofprivatisation and was renamed South African Airways (Pty) Ltd. SAA isthe largest airline in Africa and annually carries more than five millionpassengers to 32 international destinations. In addition to passenger flights,SAA operates four dedicated freighters both within South Africa andabroad. SAA also provides technical maintenance for certain other interna-tional airlines.

While operating on a code-share basis in various instances, South Africa isalso well-connected through regular scheduled flights on among others ofthe world’s leading airlines, including: British Airways, Virgin Atlantic andQantas.

16

Chapter 3

Forms of business enterprise

1. Introduction

Business enterprises in South Africa may be conducted by individuals,partnerships of individuals, trusts, close corporations, South Africancompanies or branches of foreign companies (“external companies”).

Factors such as the duration of business activities, the type of businesscapital requirements, income tax requirements, accounting requirementsand number of members will be taken into account in determining themost suitable method of operation.

The most common vehicle for conducting business operations in SouthAfrica is the private [(Pty) Ltd] company and there is no minimum equitycapital requirement for companies. The formation and regulation ofcompanies and close corporations are dealt with in Chapter 4.

There are no marked administrative advantages or disadvantages tooperating a South African company rather than conducting a branchoperation and both are subject to the Companies Act. There may be a taxadvantage to being a branch operation, depending on the parent company’scountry of domicile.

There may be certain disadvantages relating to branch operations, viz.disclosure. The financial statements of a parent company as well as thoseof its branch are required to be lodged with the Registrar of Companies,although in certain circumstances one may apply for an exemption.

The legal liabilities of branches are not limited. In the case of a subsidiarycompany, the liability of the parent is limited to the amount of capitalcommitted, together with any guarantees it has given on behalf of that subsidiary.

Most types of business can be started with a minimum of formalities.Certain activities, such as banking and insurance, are strictly controlled.

17

Licences are required for some activities, but there is generally nodifficulty in obtaining the required licence.

Business enterprises whose expected turnover will exceed R300 000 perannum are required to register for value added tax (VAT). All persons andbusinesses must register for income tax purposes. There is no generalobligation to register a business or business name other than for legalprotection of that name.

A prospective industrialist requires certain governmental consent should he wish to establish a new industrial enterprise. Some of the governmentdepartments which advise on and regulate the setting up or expansion ofindustries are listed below.

2. Industrial development

Investment South AfricaBox 782084 Tel: +27 (12) 428 7905Sandton 2146

Investment South Africa was established on 1 April 1996 by theDepartment of Trade and Industry to fulfil the functions of investmentpromotion and facilitation. Investment South Africa is part of thegovernment’s strategy which strives for technology transfer, job creation,value added export potential and international competitiveness in terms ofSouth Africa’s comparative advantage in the global business community.

Working closely with the private sector, provincial government and thevarious investment promotion agencies, Investment South Africa focuseson promoting South Africa as the premier corporate and industrial relocation destination in Africa.

Department of Trade and IndustryDirectorate: Industrial Development and Investment Centre (IDIC)Private Bag X84 Tel: +27 0861 843384Pretoria 0001 www.dti.pwv.gov.za

The Department of Trade and Industry (Directorate: IndustrialDevelopment) has issued a brochure Establishing a manufacturing concernin South Africa. This publication is issued as a “do it yourself ” guide toprospective industrialists, both local and foreign. We acknowledge theassistance which we derived from it and can do no better than to quotefreely from it.

18

It sets out in some detail the various state services and certain aspects ofstate policy. It also identifies directives issued by those institutions whichaffect their implementation.

In the end, the decision to establish or expand any enterprise rests entirely with the industrialist. He must determine the viability of such an undertaking.

3. Regional industrial development

Enterprise OrganisationPrivate Bag X86 Tel: +27 0861 843384Pretoria 0001 www.dti.pwv.gov.za

On 1 May 1991, a new incentive scheme for regional industrialdevelopment was introduced. The scheme makes provision for the paymentof an establishment grant (two years) and a profit incentive (three years).

A prime requirement is for the entity to be incorporated either as a companyor a close corporation. It must have its own tax base. Only new secondaryindustries or expansions of similar existing operations are eligible. Theymust be engaged in manufacturing, processing or assembling and achieve atleast 25% added value in order to be eligible for the concessions.

Details of the scheme can be obtained from the Board for RegionalIndustrial Development.

4. Import and export control

Department of Trade and IndustryDirectorate: Import and Export ControlPrivate Bag X192 Tel: +27 0861 843384Pretoria 0001 www.dti.pwv.gov.za

Import and export control on commodities is being phased out. However,certain products are still subject to control.

Undertakings wishing to import or export goods which are subject tocontrol must apply for permits to the Director (Imports and Exports),before placing the order for such goods.

All enterprises which import or export goods are also required to registerwith the Commissioner of Customs and Excise.

19

5. Patents, trademarks, designs and copyright

Department of Trade and IndustryOffice of the Registrar:Patents, Trade Marks, Designs and CopyrightPrivate Bag X400 Tel: +27 0861 843384Pretoria 0001 www.dti.pwv.gov.za

This directorate administers legislation concerning patents, trade marks,designs and copyright.

6. Immigration and work permits

Department of Home AffairsPrivate Bag X114 Tel: +27 (12) 314 8911Pretoria 0001 www.homeaffairs.dbs1.gov.za

Persons wishing to immigrate to South Africa or work here have to applyfrom abroad and await the outcome of their applications before makingarrangements to leave for South Africa. More information on this issue isavailable from the South African diplomatic missions or direct from theDirector General, Department of Home Affairs.

7. Exchange control and foreign investment

The South African Reserve BankExchange Control DivisionBox 3125 Tel: +27 (12) 313 3911Pretoria 0001 www.resbank.co.za

Exchange control in South Africa is administered by the South AfricanReserve Bank with the assistance of banks appointed as authorised dealersin exchange. Any enquiry or request of an exchange control nature should,in the first instance, be submitted to a South African commercial bankwhich will, if necessary, confer with the Reserve Bank.

20

8. Competition

Competition CommissionPrivate Bag X720 Tel: +27 (12) 482 9000Pretoria 0001 www.compcom.co.za

The Competition Commission is a statutory body which was established inorder to advise the government concerning competition policy.

The act governing the commission allows it to make provision for themaintenance and promotion of competition in the economy as well as theprevention of, or control of, restrictive practices. The acquisition ofcontrolling interests in businesses or undertakings as well as the investi-gation of monopolistic conditions arising from concentrations ofownership, fall within the ambit of this board’s powers.

9. Tender preferences on government purchases

Directorate: Government PurchasesPrivate Bag X84 Tel: +27 0861 843384Pretoria 0001 www.dti.pwv.gov.za

In awarding tenders for the supply of goods to government and semi-government institutions, tender price preferences are granted for locallymanufactured products. The preferences are based on:

■ local content;

■ the bearing of the South African Bureau of Standards (SABS) mark;

■ manufacture in decentralised areas;

■ locally manufactured electronic systems and components; and

■ black economic empowerment considerations.

21

10. Employment of labour and technical factory requirements

Department of ManpowerPrivate Bag X117 Tel: +27 (12) 309 4000Pretoria 0001 www.manpower.gov.za

The nearest local office of the department should be consulted regardingstatutory regulations affecting the employment of labour. Registration withthe Workmen’s Compensation Commissioner and the UnemploymentInsurance Fund is required. All factory building plans must be approved bythe factory inspector.

11. Water, waterworks and water pollution

Department of Water Affairs and ForestryPrivate Bag X313 Tel: +27 (12) 336 7500Pretoria 0001 www.dwaf.gov.za

This department controls all aspects of water usage, waterworks and waterpollution. All enquiries should be directed to the regional director of theDepartment of Water Affairs and Forestry concerned.

12. Road transport

Department of TransportPrivate Bag X193 Tel: +27 (12) 309 3000Pretoria 0001 www.transport.gov.za

Applications for public and private road carrier permits must be directed to the local Road Transportation Board in the area where theconveyance originates.

13. Customs and excise

Department of FinanceCommissioner for Customs and ExcisePrivate Bag X21 Tel: +27 (11) 241 5500Marshalltown 2107 www.sars.gov.za

Registration with the local controller of Customs and Excise is requiredfor all factories subject to excise duties and for all enterprises whichimport on a regular basis.

22

14. Standards

South African Bureau of Standards (SABS)Private Bag X191 Tel: +27 (12) 428 7911Pretoria 0001 www.sabs.co.za

Information regarding existing specifications for products, specificationsfor new products and guidance on quality control generally is availablefrom the bureau.

15. Industrial research and development

Council for Scientific and Industrial Research (CSIR)Box 395 Tel: +27 (12) 841 2911Pretoria 0001 www.csir.co.za

The CSIR is responsible for the promotion of scientific and industrial research.

16. Export trade promotion

Department of Trade and IndustryDirectorate: Export Trade PromotionPrivate Bag X84 Tel: +27 0861 843384Pretoria 0001 www.dti.pwv.gov.za

In order to promote export trade, the government offers certain incentivesand assistance to exporters. Full particulars may be obtained from thedirectorate. To qualify for this assistance, an undertaking has to beregistered as an exporter with the directorate.

Credit Guarantee Insurance Corporation of Africa LtdBox 125 Tel: +27 (11) 889 7000Randburg 2125 www.creditguarantee.co.za

This corporation provides short, medium and long term credit insurancefor exporters and for domestic credit transactions.

23

17. Industrial financing

Industrial Development Corporation of South Africa Ltd (IDC)Box 784055 Tel: +27 (11) 269 3000Sandton 2146 www.idc.co.za

The IDC is a statutory institution offering an extensive range of financingfacilities to assist private entrepreneurs in the establishment and expansionof economically viable manufacturing industries in South Africa. Forfurther information on the IDC, see Chapter 6 (4.4).

18. Small business promotion

Business Partners LimitedBox 7780 Tel: +27 (11) 480 8700Johannesburg 2000 www.businesspartners.co.za

Business Partners Limited was founded with the specific purpose ofdeveloping small business undertakings of all population groups withinSouth Africa’s Common Monetary Area. For this purpose, BusinessPartners offers a wide range of aid programmes to small businessmenmainly in the fields of financing, the provision of business sites andadvisory services.

A small business undertaking is defined as an independent enterprise withgross assets not exceeding R10 million (see Chapter 9 on page 117 forincentive details).

For further information, please visit www.kpmg.co.za or contact:

Colin Esslemont telephone +27 (11) 647 7185 [email protected]

Cristina von Eckardstein telephone +27 (11) 647 7182 [email protected]

24

Chapter 4

Companies and close corporations

1. Companies: Law and administration

1.1 Company legislation

All companies are subject to the provisions of the Companies Act 1973, as amended, which follows closely on British company legislation. Varioustypes of companies are allowed by the act:

■ companies having a share capital which includes incorporated profes-sional bodies and the word “incorporated” forms the last work of theirname – these companies must provide unlimited liability of itsdirectors in terms of section 53(b) of the Companies Act – this type ofcompany can only be formed where it is allowed by the professionalbody; and

■ companies not having a share capital and having the liability of itsmembers limited by its memorandum of association – a company’smemorandum may provide for unlimited liability of its directors.

1.2 Public and private companies

Companies having a share capital are either “Private” (Proprietary)Limited or “Public” Limited.

■ A “private” company is a company which by its articles of association:

– restricts the right to transfer its shares; and

– prohibits any offer to the public of its shares and debentures.

■ A “public” company is generally one which wishes to raise capitalfrom the public and therefore the above restrictions applicable to aprivate company are absent.

25

1.3 Establishment of a South African company

The Companies Act is administered by the Registrar of Companies who islocated in Pretoria. Incorporation is achieved by:

■ reserving the company’s name with the Registrar of Companies – it is advisable to put forward alternative names, in order of preference, when making application – stamp duty for reserving a name is R50 –the name of the company must be in line with its main object;

■ lodging the memorandum and articles with the Registrar of Companies –the memorandum must state, inter alia:

– the name of the company;

– the company’s main object – it can, however, contain unlimited ancillary objects; and

– the amount of share capital (authorised capital) – it is not necessaryto issue shares to the amount of the authorised capital (see below) –share capital may consist of shares having a par value or shareshaving no par value, but may not have both par value and no parvalue shares of the same class;

■ lodging the written consent of the auditors;

■ lodging a return of directors and officers, ie secretary (if applicable)and all directors;

■ lodging notice of situation of registered office; and

■ lodging application for Certificate to Commence Business.

A standard form of memorandum and articles which can be adapted to thecompany’s individual needs, if necessary, is available. Registration takesapproximately two weeks, from date of lodging.

1.4 External companies (branch of a foreign company)

As an alternative to the registration of a South African company, a branchof a company incorporated outside South Africa can establish a place ofbusiness in South Africa and become registered as an external company.

26

In order to achieve the registration of an external company as a branch of aforeign company, the following must be lodged:

■ two notarially certified (each paged to be signed) copies of thememorandum and articles of association of the foreign company;

■ two notarially certified translations thereof (each page to be signed), if the memorandum and articles of association are not in one of theofficial languages of the Republic;

■ a certificate from the notary certifying that he is a qualified notary;

■ a certificate from the translator certifying that he is an official translator;

■ names and personal details of the directors of the external company;

■ the consent of the auditor of the company’s branch in South Africa;

■ the name and personal details of a South African resident who isauthorised to accept service on behalf of the company;

■ the year end of the foreign company; and

■ the issued share capital of the foreign company.

Also required is a South African resident public officer who will beresponsible for all tax affairs of the branch, for example, submitting taxreturns, VAT and PAYE.

1.5 Shareholders

■ The minimum number of shareholders for a private company is oneand the maximum is fifty, excluding persons who are in theemployment of the company or past employees of the company whowere members on termination of their employment.

■ The minimum number of shareholders for a public company is seven,unless wholly owned, and the maximum is unlimited.

■ It is not necessary for any shares to be held by a South African resident.

27

1.6 Share capital

■ Par value shares of any denomination, or no par value shares.

■ Different classes of shares are permitted with different rights, iepreference shares and redeemable preference shares.

■ There is no minimum amount of share capital which must besubscribed for by the shareholders.

■ Foreign investors should take note of the exchange control restrictionsrelating to local financial assistance which apply to foreign controlledSouth African resident companies (see Chapter 5).

■ Foreign investors should also be aware that thin capitalisation rulesapply if the debt:equity ratio exceeds 3:1 (see Chapter 7).

■ Shares may be issued at par value with or without a premium.

1.7 Directors

■ Minimum number of directors for a public company is two.

■ Minimum number of directors for a private company is one.

■ Directors need not be resident in South Africa.

■ For ease of administration, a South African resident director isdesirable if only for the signing of returns, for example.

■ A director may, depending on the articles of association, appoint analternate director to act in his place and stead.

■ There is no share qualification for directors.

1.8 Company secretary

Every public company must appoint a company secretary who is required,in terms of section 268(g)(d) of the Companies Act, 1973, as amended, tocertify in the annual financial statements that the company has lodged withthe Registrar of Companies all such returns as are required of a publiccompany and that all such returns are true, correct and up-to-date.

28

29

1.9 Public officer

Every company must appoint a South African resident to be its publicofficer who will be responsible under the Income Tax Act for all thecompany’s tax affairs.

1.10 Registered office and postal address

■ Every company and external company must have a “registered office”in South Africa which is a street location.

■ The Registrar of Companies must also be notified of the postal addressof every company and external company.

■ The statutory registers of the company, for example, must be kept atthe registered office of the company unless the Registrar of Companies is otherwise notified.

1.11 Financial statements

■ All companies, including external companies, must keep properfinancial records which must be retained in the Republic.

■ Their annual financial statements must be subject to independent audit.

■ Only public companies and external companies are required to lodgetheir annual financial statements, together with copies of the financialstatements of their subsidiaries, irrespective of whether subsidiaries arepublic or private companies, with the Registrar of Companies.

■ External companies must also lodge the financial statements of the foreigncompany as a whole. Exemption from lodging annual financial statementsfor an external company can be applied for on various grounds.

1.12 Financial year

■ On incorporation, a company must choose a date on which to close its financial year.

■ A subsidiary must have the same financial year end as its holding company.

■ Changes can, however, be effected subsequently, provided the Registraris notified before the expiry of the current year end.

1.13 Annual general meetings

■ Every company, except an external company, must hold an annual general meeting.

■ The first annual general meeting must be held within eighteen monthsof the date of incorporation.

■ Subsequent annual general meetings must be held within nine months,depending on the articles of association, of the year end of the companyand within fifteen months of the preceding annual general meeting.

1.14 Stamp duty

1.14.1 Authorised share capital

■ Stamp duty is payable on the amount of authorised share capital of the company on incorporation.

■ Stamp duty is payable at the rate of R5 per R1 000 or part thereof onthe nominal value of the authorised share capital.

■ In the case of no-par value shares, stamp duty is payable at the rate ofR5 per 1 000 shares authorised.

1.14.2 Issued share capital

■ Stamp duty on the issue of shares is payable within 21 days of issue ofthe share certificate. The share certificate must be issued within twomonths of date of issue.

■ Stamp duty is payable at the rate of 5c per R20 or part thereof on thepar value and premium of shares issued.

■ Stamp duty is payable at the rate of 5c per R20 or part thereof of thevalue attributable to no-par value shares issued.

1.15 Costs

■ The cost of incorporating a South African company in September 2001was approximately R9 000.

■ The cost of registering an external company in September 2001 was approximately R4 500.

30

■ This amount does not include stamp duty, VAT and disbursements.

1.16 Shelf companies

KPMG forms and holds shelf companies for the convenience of theirclients. The advantage of this is that the company is already registered and is available immediately.

1.17 Registration number

A company must display its registration number on all official stationeryand documentation and at the registered office of the company.

2. Close corporations: Law and administration

A close corporation is a form of business enterprise designed for ease of operation. It is regulated by the Close Corporation Act of 1984, asamended, the provisions of which commenced on 1 January 1985.

2.1 Nature of the close corporation

■ A close corporation is a simple business entity with a separate legalstatus from its members or owners.

■ It indicates its status by most commonly displaying the letters CC orBK, but similar lettering in all 11 official languages may be used.

■ Close corporations must display their registration numbers on allofficial stationery and documentation.

■ A close corporation may easily be converted to a company.

2.2 The act and regulations

■ The act is administered by the Registrar of Close Corporations who islocated in Pretoria.

■ The Close Corporation Act and its regulations are expressly designedto be relatively simple to administer for ease of operation.

31

2.3 Membership

■ Only natural persons may be members of a close corporation.

■ The maximum number of members is 10.

■ No company or other juristic person can directly or indirectly, whetherthrough a nominee or otherwise, hold a member’s interest in the corporation.

■ The names and initials of all members must appear on all officialstationery of the corporation.

2.4 Interest of members

■ Close corporations do not have share capital.

■ Members hold an interest in the corporation.

■ A member’s interest is expressed as a percentage of the total members’ interest.

■ A certificate of membership is issued to each member showing that member’s interest.

■ A member acquires his interest by either making a contribution incash, or by way of property (both corporeal and incorporeal), or forservices rendered or by purchase from an existing member.

2.5 The founding statement and incorporation

Incorporation is simple.