investment company

TRANSCRIPT

CZECH REPUBLIC

ASSESSMENT OF GOVERNANCE OF THE COLLECTIVE INVESTMENT FUND SECTOR

September 2004

Private and Financial Sector Development Department Europe and Central Asia Region The World Bank

ACRONYMS AMC Asset Management Company CIU Collective Investment Undertaking CNB Czech National Bank CSC Czech Securities Commission CZK Czech Koruna (crown) EU European Union FEFSI Fédération Européenne des Fonds et Sociétés d'Investissement FSAP Financial Sector Assessment Program GDP Gross Domestic Product ICI Investment Company Institute IFAC International Federation of Accountants IOSCO International Organization of Securities Commissions MOF Ministry of Finance NAV Net Asset Value OECD Organization for Economic Cooperation and Development OTC Over the Counter PSE Prague Stock Exchange ROSC Report on Observance of Standards and Codes SEC Securities and Exchange Commission (of the US) UCITS Undertakings for the Collective Investment of

Transferable Securities UNIS Union of Czech Investment Companies US United States

Table of Contents Context and Acknowledgements ........................................................................................ 4 Introduction......................................................................................................................... 5 The Czech Collective Investment Fund Sector................................................................... 8

Sector Composition......................................................................................................... 8 Legal Structures .............................................................................................................. 9

Summary of Key Issues and Recommendations............................................................... 12 Key Issues ..................................................................................................................... 12 Key Recommendations ................................................................................................. 14

Conflicts of Interest between Investment (Management) Companies, Depositaries and Unit-Holders ..................................................................................................................... 15

Investment (Management) Companies ......................................................................... 15 Depositaries................................................................................................................... 16 Segregation of Assets.................................................................................................... 18

Supervisory Boards........................................................................................................... 19 Risk Management, Internal Controls & Financial Reporting ........................................... 21 Regulation of Abusive Practices....................................................................................... 23 Regulations for Special Funds .......................................................................................... 26 Tables Table 1: Number of Collective Investment Funds and Assets under Management............ 9 Table 2: Comparison of Legal Forms of Collective Investment Undertakings ................ 11 Table 3: Czech Investment (Management) Companies - Summary Information ............. 17 Table 4: Related Party Transactions ................................................................................. 24 Box Governance of US versus European Funds .........................................................................8 Annex Detailed Assessment ..........................................................................................................28

Context and Acknowledgements In well-developed capital markets, collective investment funds provide a potentially attractive investment option for investors. They provide individual investors with access to a diversified investment portfolio, potentially benefiting from efficient sales and purchases of large blocks of securities. However, collective investment funds also entail some risks. Individual investors lack direct information regarding the investment assets and are therefore obliged to trust the fund managers—and the sector’s governance framework—to ensure that their interests are protected. It is the role of the Government to ensure that such trust is warranted and that investors can feel confident that their interests will be placed ahead of those of the investment managers. These issues are particularly sensitive in the Czech Republic where the 1990’s saw the establishment of collective investment funds in an environment of insufficient regulation, providing fertile ground for widespread governance abuses by fund managers. This assessment of corporate governance of the Czech investment fund sector is the first assessment in a pilot program to analyze the governance of collective investment funds in transition and emerging markets. The assessment has four objectives: (1) identify possible governance weaknesses in the Czech governance framework, (2) consider what provisions should be in place to ensure that governance of investment funds adequately protects investors and other stakeholders, (3) develop a set of benchmarks for assessment of governance of collective investment fund sectors, and (4) conduct a trial assessment of the Czech governance framework against the proposed benchmarks. The assessment thus both highlights the key weaknesses in the Czech collective investment fund sector and also provides a systematic assessment of the Czech framework compared to the benchmarks. The benchmarks and the assessment of the Czech framework against the benchmarks are found in the Annex. However, because this is a pilot assessment, even the final report will likely be no more than “work-in-progress.” Nevertheless, it is expected that the report will play a useful role in contributing to the international public debate on guidelines for strong corporate governance of the collective investment fund sectors in both developed and emerging markets. The collective investment fund governance assessment is one of a series of pilot financial sector governance assessments prepared by the World Bank at the request of the Czech Government. The other financial sector governance assessments include the banking sector and may in the future also cover the insurance and private pension fund sectors. The report draws on other financial sector assessments prepared by the World Bank for the Czech Republic, including a Capital Markets Review in 1999, a Financial Sector Assessment Program (FSAP) Review in 2001, a Corporate Governance Report on Observance of Standards and Codes (ROSC) in 2002 and an Accounting and Auditing ROSC in July 2003.1 The assessment of Czech collective investment fund governance was prepared based on a visit to Prague from January 26, 2004 to February 5, 2004. The Bank Team was led by

1 The completed ROSC reports can be obtained from http://www.worldbank.org/ifa/rosc_cg.html.

Ms. Marie-Renée Bakker, Lead Financial Sector Specialist and Finance and Private Sector Program Coordinator for the New EU Member States. The other team members were Ms. Susan Rutledge, Regional Corporate Governance Coordinator for the Europe and Central Asia Region and Mr. Richard Symonds, Senior Legal Counsel at the World Bank. Advising the Bank Team was Mr. Steffen Matthias, Secretary-General of the Fédération Européenne des Fonds et Sociétés d'Investissement (FEFSI), the industry association for the European investment fund sector. In addition, E-Merit Consulting Services of Prague completed a preparatory template-questionnaire regarding the collective investment fund governance framework in the Czech Republic. The Bank Team met with officials from the Ministry of Finance MOF), the Czech Securities Commission (CSC), the Czech National Bank (CNB), the Prague Stock Exchange (PSE) and its clearing subsidiary, Univyc, the Prague Securities Center, the Union of Investment Companies of the Czech Republic (UNIS) and numerous asset management companies, depositaries, broker-dealers, and members of the financial and legal community. The World Bank would like to express its gratitude for the efforts undertaken by all parties involved to facilitate its work. Introduction All financial institutions have important fiduciary duties to the individuals and corporations who have entrusted their funds to them. However, collective investment funds have particularly strong fiduciary obligations. Fund investors need to be able to focus on the issues of maximizing the return on their capital, not return of their capital. Furthermore investors are entitled to honest and industrious fiduciaries, who abide by fair and ethical principles. The collective investment sector is characterized by complex agency relationships, where the fund operator might misrepresent the quality or value of an asset portfolio--or the nature of the risks involved--or the operator might manage the assets in his own interests rather than in the best interests of the investors. The asymmetry of market power and information available to a fund operator enables such abuses if the corporate governance framework for the collective investment fund sector does not preclude such behavior. A framework for corporate governance comprises of the following three areas: (1) the financial and company laws that constitute the legal framework, (2) the supervisory and enforcement institutions that constitute the regulatory framework and (3) the common business practices that determine the willingness of the financial and corporate sectors to comply with the legal and regulatory framework. The market-place practices also influence the sector’s interest in adopting high standards of corporate social responsibility, which cannot be legislated but are important for the corporate and financial community. More specifically, corporate governance relates to the set of relationships between company management and the company’s supervisory board, shareholders and other stakeholders—and the ways in which conflicts of interest are managed and addressed. With regard to the collective investment fund sector, the report takes as its starting point the objective that the sector should provide all investors with a level playing field when

5

investing in collective investments. Good corporate governance should complement state regulation of the collective investment fund sector and should ensure both transparency and accountability in the sector. Transparency of fund operations is needed to enable investors to make informed and timely decisions. Accountability may lie with the supervisory boards of the asset-management companies or it may lie with the bank depositaries that control the activities of the asset-management companies or self-managed investment companies. In either scheme, investors need to rest assured that a reliable and trust-worthy body is accountable and looking out for the investors’ interests. One of the difficulties in assessing collective investment fund governance is that there are no internationally accepted benchmarks for governance of the collective investment fund sector. The Guidelines for Private Pension Fund Governance prepared by the OECD in 2002 provide a useful starting point.2 Also of relevance are the IOSCO Objectives and Principles of Securities Regulation, specifically Principles 17 to 20 (which touch on governance issues for mutual funds, even though they are more regulatory principles than governance principles)—as well as the methodology developed by IOSCO for assessing compliance with the Principles.3 The European Union (EU) has issued the “UCITS” Directive (initially as 85/611/EEC) which lays out the requirements for undertakings in collective investments in transferable securities.4 The EU is currently reviewing a number of areas related to collective investments, such as the use and function of depositaries,5 which were taken into account in preparing this assessment. In addition, the European collective investment fund industry association, FEFSI, has issued a number of specific principles on issues such as investment policies, business transactions (including affiliated transactions), and investor information, including a model simplified prospectus and a methodology for calculation of the performance and total expense ratio of a collective investment fund.6 The US Securities and Exchange Commission (SEC) has proposed (and already partially adopted) new requirements for governance of investment companies.7 Also, the US investment fund industry association, the Investment Company Institute (ICI), has released recommendations for the directors of investment companies.8 However, none of these recommendations or guidelines provide a comprehensive set of benchmarks for reviewing the governance of a country’s collective investment fund sector.

2 Guidelines for Pension Fund Governance. OECD Secretariat. July 2002. A copy can be found at http://www.oecd.org/dataoecd/22/2/2767694.pdf 3 See the February 2002 report of the International Organization of Securities Commissions. Copies can be found at http://www.iosco.org/pubdocs/pdf/IOSCOPD125.pdf 4 See European Union Directive of 20 December 1985 on the coordination of laws, regulations and administrative provisions relating to undertakings for collective investments in transferable securities (85/611/EEC) as modified by Directives 88/220, 95/26 and 00/64 including the Common Positions adopted on 5 June 2001 (EC23/2001 & 24/2001.) Copies can be downloaded from http://europa.eu.int/scadplus/leg/en/lvb/l24036a.htm. 5 European Commission Communication to the Council and Parliament, Regulation of UCITS Depositaries in the Member States, COM (2004) 207 (30.03.2004) 6 Copies can be found on the FEFSI website www.fefsi.org under “FEFSI standards”. 7 The SEC proposed requirements are summarized at http://www.sec.gov/news/press/2004-5.htm. 8 Corporate collective investment funds are called “investment companies” in the United States under the Investment Company Act of 1940. A copy of the 1999 ICI’s Best Practices for Fund Directors can be found at http://www.ici.org/statements/ppr/rpt_best_practices.pdf.

6

Indeed recent years have witnessed rapidly changing—and improving—standards for regulation. In April 2004 the US SEC proposed regulations to: (1) enhance and modernize the national market system for investment companies , (2) expand the categories of events that trigger prompt disclosure and (3) increase disclosure of investment companies’ policies and practices on market timing and selective disclosure of portfolio holdings.9 The agency has already revised significant disclosure rules and forced the investment companies to adopt new ethics codes and to appoint compliance officers. In June 2004, the SEC adopted new rules requiring that at least 75 percent (rather than 50 percent) of the boards of directors of investment companies should be “independent” members and that the chairman of the board should also be independent.10 In part the impetus for change has come from the rapid growth of the mutual fund sector and the widespread conflicts of interest highlighted by US prosecutors. However, the issues related to governance of collective investment funds are present in all major capital markets. The common occurrence of such issues provide encouragement for systematic review of collective investment fund governance, particularly in those markets (such as the Czech Republic) where corporate governance abuses existed in the past. Although the developments in the US represent positive news for fund investors, the rapidly changing approaches and the absence of internationally agreed principles that could be used as benchmarks have complicated the task of reviewing the Czech collective investment fund sector. The Bank Team therefore kept in mind the historical experience of the Czech Republic in corporate governance development while relying on best practices used in well-regulated and governed capital markets. It should be noted that in the Spring and early Summer of 2004, the Government passed legislation to bring the Czech laws and regulations in compliance with all Directives and regulations of the European Union. In particular, two major pieces of legislation were completed: (1) the Law on Collective Investments, which replaces the old Law Investment Companies and Investment Funds, to comply with the UCITS Directive and (2) the Law on Capital Market Undertakings, which replaces the old Law on Securities. As of June 2004, revisions to the Commercial Code were under way. In addition, the Czech Securities Commission (CSC) had drafted six new regulations related to collective investment funds as well as over 15 regulations concerning other parts of the capital markets. The report focuses on the new legislation that was passed in April 2004 and relevant translated decrees and compares it to the prior laws and regulations. The comparison will provide useful insight into the governance strengths and weaknesses of the Czech collective investment sector. 9 See the April 2004 speech of US Securities and Exchange Commission Chairman William Donaldson, which can found at http://www.sec.gov/news/speech/spch042204whd.htm 10 Other details are also important. The outside directors will have to hold quarterly meetings without fund executives being present, and each board will be required to justify the fund managers it retains. The SEC is also planning in 2004 to complete rules limiting after-hours trading, requiring greater disclosure of some fees and regulating more closely the payments and other compensation paid by funds to the brokerage firms that execute their sales and purchases of securities.

7

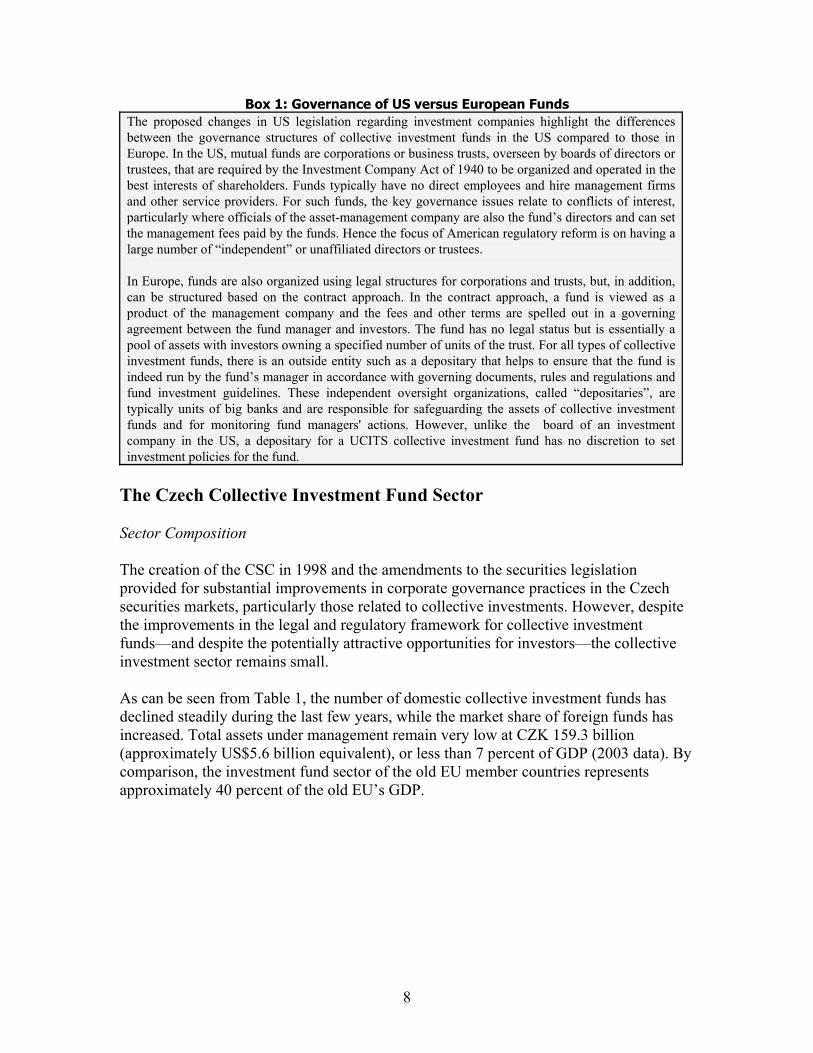

Box 1: Governance of US versus European Funds The proposed changes in US legislation regarding investment companies highlight the differences between the governance structures of collective investment funds in the US compared to those in Europe. In the US, mutual funds are corporations or business trusts, overseen by boards of directors or trustees, that are required by the Investment Company Act of 1940 to be organized and operated in the best interests of shareholders. Funds typically have no direct employees and hire management firms and other service providers. For such funds, the key governance issues relate to conflicts of interest, particularly where officials of the asset-management company are also the fund’s directors and can set the management fees paid by the funds. Hence the focus of American regulatory reform is on having a large number of “independent” or unaffiliated directors or trustees. In Europe, funds are also organized using legal structures for corporations and trusts, but, in addition, can be structured based on the contract approach. In the contract approach, a fund is viewed as a product of the management company and the fees and other terms are spelled out in a governing agreement between the fund manager and investors. The fund has no legal status but is essentially a pool of assets with investors owning a specified number of units of the trust. For all types of collective investment funds, there is an outside entity such as a depositary that helps to ensure that the fund is indeed run by the fund’s manager in accordance with governing documents, rules and regulations and fund investment guidelines. These independent oversight organizations, called “depositaries”, are typically units of big banks and are responsible for safeguarding the assets of collective investment funds and for monitoring fund managers' actions. However, unlike the board of an investment company in the US, a depositary for a UCITS collective investment fund has no discretion to set investment policies for the fund.

The Czech Collective Investment Fund Sector Sector Composition The creation of the CSC in 1998 and the amendments to the securities legislation provided for substantial improvements in corporate governance practices in the Czech securities markets, particularly those related to collective investments. However, despite the improvements in the legal and regulatory framework for collective investment funds—and despite the potentially attractive opportunities for investors—the collective investment sector remains small. As can be seen from Table 1, the number of domestic collective investment funds has declined steadily during the last few years, while the market share of foreign funds has increased. Total assets under management remain very low at CZK 159.3 billion (approximately US$5.6 billion equivalent), or less than 7 percent of GDP (2003 data). By comparison, the investment fund sector of the old EU member countries represents approximately 40 percent of the old EU’s GDP.

8

Table 1: Number of Collective Investment Funds and Assets under Management

egal Structures

or the purposes of this paper, the Czech terminology in the area of collective investment

No. of entitiesAssets (bln.

CZK)Assets (bln.

US$) Share (%)Assets as

% of GDP1999 Open-ended mutual trusts 54.2 1.57 0.28%2000 Investment funds1) 33 20.4 0.53 19.83%

Investment companies2) 36 78.9 2.04 76.68%Open-ended mutual trusts 87Closed-end mutual trusts 7 3.6 0.09 3.50%Total (Czech entities only) 102.9 2.67 100% 0.52%

2001 Investment funds1) 20 12 0.32 14.94%Investment companies2) 21 66.5 1.75 82.81%Open-ended mutual trusts 88Closed-end mutual trusts3) 4 1.8 0.05 2.24%Foreign entities n.a. n.a. n.a.Foreign funds4) 209Total (Czech entities) 80.3 2.11 100% 3.69%

2002 Investment funds1) 8 5.2 0.16 3.49%Investment companies2) 17 107.9 3.30 72.42%Open-ended mutual trusts 92Foreign entities 44 35.9 1.10 24.09%Foreign funds 651Total (Czech entities) 113.1 3.45 75.91%Total (including foreign entities) 149 4.55 100% 6.55%

2003 Investment funds1) 4 2.3 0.08 1.44%Investment companies2) 15 106.7 3.78 66.98%Open-ended mutual trusts 66Foreign entities 49 50.3 1.78 31.58%Foreign funds 723Total (Czech entities) 109 3.86 68.42%Total (including foreign entities) 159.3 5.64 100% 6.29%Source: Czech Securities Commission, Czech National Bank.1) Includes only active investment funds, not investment funds in liquidation2) Includes only active investment companies, not investment companies in liquidation3) There are no more closed-end funds as of 20024) The foreign funds were only allowed in the Czech Republic since the beginning of 2001. The data for 2001 are not available

L Ffunds should be explained. Czech law recognizes two different types of fund structures: (1) an “investment fund,” which has a corporate legal form as a joint stock company and(2) a “unit trust” which does not have a legal personality and is based on contract. The term “unit trust” is used in the new Law on Collective Investments and will be used to describe contractually based funds (under the old Czech law, they were referred to as “mutual trusts”).

9

Unit trusts are managed by asset management companies (called “investment companies” under Czech law.) Investment funds can be self-managed or managed by an asset management company. Table 2 provides a summary of different legal forms for collective investment undertakings. The new legislation on collective investments in the Czech Republic that came into force on May 1, 2004 converts all existing management companies into UCITS-type asset managers. Existing investment funds and mutual trusts are automatically considered “special funds,” and will be required to request authorization from the CSC for transformation into a UCITS-type collective investment undertaking. Since the primary audience for this assessment is the Czech collective investment fund sector, the Czech terminology will be used in the text sections referring to institutions created under Czech law, with several minor changes for the benefit of clarity for non-Czech readers. As a result:

1. “Collective Investment Fund” will refer generically to all types of collective investment funds under Czech law, no matter what their legal form is.

2. “Investment (management) company” will refer to asset management companies. 3. “Corporate investment fund” will refer to collective investment funds organized

as a corporation. 4. “Unit trust” will refer to a collective investment fund organized on a contractual

basis with a legal personality. 5. “Depositary” will refer to the entity which controls the activity of the collective

investment fund under Czech law.

10

Table 2: Comparison of Legal Forms of Collective Investment Undertakings11

Type of Fund Legal Form Type Manager Depositary Title to Assets Investor Interest

Czech Republic

Investment Fund

Corporation Closed Investment Company(the term for asset management company in the Czech law) or is self-managed

Assets must be “controlled” (or supervised) by a depositary

Investment company holds title or investment fund if it is self-managed

Shares

Unit trust

or Mutual Fund

Fund created by Contract

Open or

Closed

Investment Company Assets must be “controlled” (or supervised) by a depositary

Investment company holds title

Units of Participation

UCITS Recognized

Investment Company

(such as SICAV)

Corporation Open or

Closed12

Asset Management Company (AMC) or is self-managed

Assets must be entrusted to a depositary for safekeeping

Determined by national law

Shares

Fund Based on Contract

Fund created by Contract

Open Managed by AMC Assets must be entrusted to a depositary for safekeeping

Determined by national law

Units of Participation

United Kingdom

Unit Trust Trust under Anglo-Saxon law

Open Managed by a Trust Company acting as the Trustee

UK - Assets held by trustee

Trust Company as trustee has legal title

Beneficial Units in Trust

United States

Investment Company Corporation Open or

Closed

Investment Advisor (registered with SEC) or is self-managed

Not obligatory, although assets can be held by a custodian

Title held by investment company

Shares

11 For additional information on the governance of collective investment fund sectors in various OECD countries, see John K. Thompson and Sang-Mok Choi, Governance Systems for Collective Investment Schemes in OECD Countries. OECD, Financial Affairs Division. April 2001. A copy can be found at http://www.worldbank.org/wbi/banking/insurance/contractual/pdf/thompson_choi.pdf 12 Although UCITS funds refer to open-ended funds, there appears to be an exception for exchange-traded funds which can be closed, if the asset manager intervenes to keep the price of the fund within 5% of the NAV. This intervention is considered by the UCITS directive to be the functional equivalent of open-ended redemption, however the exchange listed funds are still closed-end from a legal standpoint.

11

Summary of Key Issues and Recommendations Key Issues The report highlights six key issues concerning governance of the Czech collective investment fund sector. They relate to:

1) Conflicts of Interest between investment (management) companies, depositaries and unit-holders,

2) Supervisory boards, 3) Risk management, internal controls and financial reporting, 4) Regulation of abusive practices, 5) Authority of the Czech Securities Commission, and 6) Regulations for special funds.

These issues are summarized below. A more detailed description can be found in the Annex to this paper (Detailed Assessment of the Corporate Governance Framework for Collective Investment Undertakings in the Czech Republic: A Comparison of Rules and Practices Against Proposed Best Practice Benchmarks). Conflicts of Interest between Investment (Management) Companies , Depositaries and Unit-Holders - Over 95 percent of all assets in collective investments are managed by just four investment (management) companies. While these companies are separately incorporated as joint stock companies, each one of them is also owned by the same bank (or banking group) that acts as both broker-dealer and depositary for the funds they manage. Although these arrangements provide some efficiencies for their activities, the common ownership structure could create conflicts of interests and highlights the need for strong supervisory boards and systems of risk management and internal controls. Supervisory Boards – The Czech Commercial Code is due for revision and provides for only weak internal governance of joint stock companies. In particular, the Code fails to establish adequate fiduciary duties for members of supervisory and management boards. As asset managers, Czech investment (management) companies and corporate investment funds should have stronger governance provisions than those that apply to non-financial joint stock companies. Their supervisory boards should also be responsible for ensuring that adequate systems of risk management and internal controls are in place. Risk Management, Internal Controls and Financial Reporting – Major improvements in the internal systems of investment (management) companies and corporate investment funds are mandated by the introduction of the CSC’s regulation on business operations and internal controls of May 2004 – which will be effective as of July 1, 2005. However, while the regulation assigns responsibility to the internal auditors to verify compliance with existing internal risk limits, it does not specifically require investment (management) companies and corporate investment funds to have adequate risk management systems in place. The industry claims to be ahead of the regulator in this area. They argue that the entry of strategic foreign bank owners into the Czech parent banks that own the major investment (management) companies has resulted in the introduction of mature market risk management and internal control systems from abroad. Even if this is the case, however, it is evident that the CSC will still need to build

12

up its own in-house capacity to monitor and review risk management and internal controls of investment (management) companies and corporate investment funds—and develop a credible enforcement track record. Regulation of Abusive Practices – Related-party transactions provide the most fertile ground for abusive practices related to collective investment funds. Both the legal structure governing collective investment funds and the internal rules of such funds must address this issue directly to adequately protect investor interests. The law should provide different regulatory approaches for different types of related party transactions in order to protect investors while maximizing their opportunities for returns. Since most abusive practices are conducted by individuals for their personal benefit, the new Law on Collective Investments should provide appropriate regulatory provisions and sanctions for abusive practices by individuals. Unfortunately, there are large gaps in the new Law regarding the individuals that come within the regulatory structure for abusive practices by related-parties. The result is that many individuals can engage in abusive practices without a real threat of sanction. The attempt to solve this problem through decree does not create a sufficiently strong sanction to deter abusive practices by such individuals. Authority and Capacity of the Czech Securities Commission - While the Czech Securities Commission (CSC) has dramatically improved its institutional capabilities and legal authority in recent years, the CSC still has limited authority to promulgate its own secondary legislation. Instead of receiving a general authority to issue such decrees, the Law on Collective Investments limits the areas in which the CSC can issue decrees. As a result, the CSC lacks the authority to issue decrees related to the important area of sales practices of investment (management) companies and corporate investment funds. Emphasis should also be placed on strengthening the capacity of the CSC to ensure that collective investment funds provide financial reporting to investors in compliance with International Financial Reporting Standards, as far a meaningfully applicable, and the Law on Collective Investments. Regulations for Special Funds - The Law on Collective Investments will allow the creation of both “standard” funds, which not only meet the requirements of the UCITS Directive, but are even more restricted in terms of permissible investments and structures, as well as “special” funds, many of which would not meet the provisions of UCITS-type funds. Special funds will likely include non-transferable (and illiquid) securities, real estate, derivatives, funds of funds and special asset classes, in addition to transferable securities. It is expected that most investment managers will look to special funds as a means of obtaining higher returns, albeit at higher risks, than would be possible with the UCITS-type funds. However, the detailed regulations necessary to provide guidance to market participants have only recently been prepared and are just in the process of implementation. Given the past history in the Czech Republic of the voucher privatization funds and the possible rapid appearance of hedge fund type structures in the Czech Republic (coming either from other EU member states or domestic initiatives) in the post EU accession phase, it is imperative that the CSC and the industry undertake maximum effort to educate investors about the risks associated with investing in such less regulated funds, and to explain the differences in the level of regulation and oversight applicable to both types of funds.

13

Key Recommendations The following recommendations are made based on the evaluation of the Czech collective investment fund sector contained in this assessment:

Strengthen the CSC’s authority to extend “fit and proper” requirements to the appointment of members of the supervisory board of both investment (management) companies and corporate investment funds.

For supervisory board members of investment (management) companies and corporate investment funds, extend the statutory fiduciary obligations to include appropriate regulation of related-party transactions, conflicts of interest, fraudulent activity, holding of incompatible offices, and violation of loyalty duties.

Amend the legislation to clarify that the assets of unit trusts should be legally segregated from those of the investment (management) company, in addition to book entry segregation.

Provide the CSC with adequate powers to enforce the use of applicable accounting standards for collective investment funds (preferably International Financial Reporting Standards, as far as meaningfully applicable) and build the requisite enforcement capacity.

Complete the development of a corporate governance code for investment (management) companies and corporate investment funds and put in place appropriate mechanisms to monitor and enforce compliance (either at the CSC or through the Union of Investment Companies of the Czech Republic, UNIS.)

Implement the regulations recently promulgated to prohibit abusive market practices (such as front-running and preferential sales of fund units.) Establish sanctions for individuals who engage in improper or fraudulent sales activities. Amend the Law on Collective Investments to include a regulatory framework that brings all related party individuals within its reach and that has appropriate sanctions for conduct which violates the law.

Adequately enforce the detailed regulation recently promulgated on requirements for systems of internal controls. Amend the regulation to require that investment (management) companies as well as corporate investment funds put in place the missing elements of integral risk management systems (i.e., in addition to internal controls, an appropriate supervisory structure and an established process for approving new investments strategies and instruments.)

Finish preparation of all regulations needed for implementation of the new legislation on collective investment funds.

Delay the introduction of special funds until the CSC is able to prepare and make effective the necessary regulations affecting special funds.

14

Provide for the creation of an Office of Risk Assessment in the CSC to evaluate potential regulatory problems in all of the areas it regulates, including collective investments.

The Annex to this paper (Detailed Assessment of the Corporate Governance Framework for Collective Investment Undertakings in the Czech Republic: A Comparison of Rules and Practices Against Proposed Best Practice Benchmarks) includes additional recommendations with reference to the specific benchmarks. Conflicts of Interest between Investment (Management) Companies, Depositaries and Unit-Holders Investment (Management) Companies There is an inherent conflict between the obligation of an investment (management) company to maximize profits for its own shareholders and, at the same time, give priority to the economic interests of the investors in the funds it is managing. A fundamental element of investor protection in collective investments is the need for independent “control” (i.e. supervision) of an investment manager’s activities in regards to the investment funds under its care. In order to provide this supervision, the institution of the depositary was created to provide an independent review of the activities of the investment (management) companies. The new Czech legislation contains provisions to ensure that there is independent supervision of the management of the collective investment funds. Heavy emphasis is placed on the role of the depositary in monitoring and supervising the investment decisions of the investment (management) companies. Furthermore, the Law on Collective Investment Funds sets a test of “professional care”, establishing a high level of fiduciary duty on the part of the depositary for a collective investment fund. The liability has been tested in court. In 2003, Plzenska Banka was ordered to pay CZK 1.3 billion (approximately US$52 million equivalent) in damages for its role as depositary in permitting C.S. Fondy to purchase 70 percent of a bankrupt poultry company.13 In unit trusts, inherent conflicts of interest are rife particularly over the level of management fees paid by the trust. The investment (management) company wants to receive high management fees while investors wish to pay lower fees. To further protect investors’ interests, the CSC should follow the provisions in the EU Recommendation on Some Contents of the Simplified Prospectus14 and require that a fund disclose the Total Expense Ratio, as calculated in the Recommendation, in the fund’s prospectus, periodic reports, annual reports and marketing materials. The CSC will also need to create a mechanism to monitor the calculation of the Total Expense Ratio to ensure its accuracy. The CSC should also have the authority to request investment (management) companies

13 See Prague Post on April 2, 1997, “1.3 billion Kc disappearing act wins little applause” http://www.praguepost.cz/archive/busi42b.html 14 EU Commission Recommendation of 27 April 2004 on Some Contents of the Simplified Prospectus as Provided for in Schedule C of Annex I to Council Directive 85/611/EEC (2004/384/EC)

15

to correct excessively high fees. At a minimum, investment (management) companies should be required to explain why the fees are so high and how the fee levels compare with customary levels in other financial systems. Depositaries There is a similar conflict of interest between the duty of the depositary both to maximize profits for its own shareholders and to put the interests of the shareholders in a corporate fund or unit-holders in a contract based fund first. This has frequently been resolved by creating a fiduciary-type duty in the law for the depositary vis-à-vis investors; by requiring the depositary to be independent of the asset management company; and by requiring the depositary to be a regulated financial institution, most commonly a bank.15 The Czech legislation has adopted a number of these safeguards to reduce the dangers of a conflict of interest, such as the requirement that a collective investment fund use a depositary; that the depositaries have legal duties to investors; and that only banks are permitted to be depositaries. However, there are serious concerns as to the independence of the depositaries from the corporate investment funds or investment (management) companies. As found in many small financial sectors worldwide, the Czech collective investment fund sector is tightly interconnected. As seen in Table 3 below, four major investment (management) companies are responsible for over 95 percent of all assets under management through collective investment funds (excluding the private pension funds.) The four investment (management) companies are subsidiaries of four major banks, with Ceska Sporitelny alone accounting for over 40 percent of total assets under management in the Czech collective investment fund sector. The Bank Team was advised that each investment (management) company directs the vast majority of its trading to the broker-dealer of its parent bank and each company uses the parent bank as its depositary. It should be noted that having an asset-management company and a depositary in the same banking group is a common feature of universal banking systems and is seen widely in western Europe. This has not been considered to be a serious problem by the legal and financial community. Throughout Europe, the depositary and asset-management company are subject to regulation by the securities regulator, as they are in the Czech Republic by the CSC. In addition, if the depositaries are banks, they are also regulated by the banking regulator, as they are in the Czech Republic by the Czech National Bank. Moreover, “Chinese walls” between the various entities and departments within the entities are also thought to ensure that potential conflict within such structures are properly regulated without major problems. Indeed, the UCITS Directive has been interpreted in practice to require that depositaries be separate from the asset-management companies but not necessarily that they be “independent” from the asset-management companies. Nonetheless, concern has developed at the EU that different countries in the European Union address the issue of depositaries and asset-management companies in

15 The governance of banks in the Czech Republic will be covered in a separate study.

16

different ways,16 and the EU is moving to harmonize depositary regulation and operations among its member states.

Table 3: Czech Investment (Management) Companies - Summary Information

Investment (Management) Company

Major Shareholders Depositary Assets under Management (CZK millions)

Inv. spol. České spořitelny, a.s. Česká spořitelna (100%) Česká spořitelna 49,227

Investiční kapitálová společnost KB, a.s.

Komerční banka (100%) Komerční banka 29,562

ČSOB inv. spol., a.s. 100% control by ČSOB group

ČSOB 26,459

ŽB - Trust, inv. spol., a.s. Živnostenská banka (100%) Živnostenská banka

6,632

ČP Invest inv. spol., a.s. ČP Finanční holding (100%)

Deutsche Bank 3,261

Prosperita inv. spol., a.s. M. Kurka (50%) M. Kurka (50%)

ČSOB 752

AKRO inv. spol., a.s. n.a. Commerzbank 270

InvestAGe, inv. spol., a.s. J&T Banka, a.s. (100%) Komerční banka 146

MAPIS, inv. spol., a.s. Proxy Finance, a.s. (100%) Komerční banka 142

Pioneer česká inv. spol., a.s. Pioneer International Corp (100%)

ČSOB 57

Citicorp, inv. spol., a.s. Citibank Overseas Investment Corp (100%)

Citibank, a.s. n.a.

Credit Suisse Asset Management inv. spol., a.s.

CS Asset Management Holding Europe (100%)

HVB Bank n.a.

Inv. spol. Jupiter Invest, a.s. Epic Securities, a.s. (100%) Citibank, a.s. n.a.

J&T Asset Management, inv. spol., a.s.

J&T Banka, a.s. (100%) Komerční banka n.a.

Total 116,508 Source: Czech Securities Commission (www.sec.cz); UNIS (www.uniscr.cz.)”Inv. Spol”. refers to investiční společnost. All data are for 2002. Nevertheless, as the IOSCO principles concerning collective investment funds also recognize, the independence of depositaries from their client asset- management companies is an important factor in determining the level of investor protection, in particular in emerging markets. For example, in the private pension fund sector, independent depositaries are commonly used and the requirement for a depositary is included in the OECD principles on private pension fund governance. The role of the depositary is critical in ensuring good corporate governance of pension funds. It is the

16 See for example, the March 2004 EU Communication regarding Regulation of UCITS depositaries in the Member States: Review and Possible Developments. A copy can be found at http://europa.eu.int/comm/internal_market/en/finances/mobil/ucits/docs/com-2004-207/com-2004-207_en.pdf

17

depositary that provides an independent check on the net asset value (NAV) calculation of the asset management company. Indeed, in the Czech private pension funds, which provide a “Third Pillar” for the pension system, asset-management companies are obliged to use independent bank depositaries. Segregation of Assets One of the primary concerns in the area of conflicts of interest between an asset-management company, a depositary and investors is the segregation of the assets of the fund from those of the management company and the depositary. Fund assets should be physically or legally separated from the assets of the asset management company or the depositary. However, under Czech law, legal title to the securities in a unit trust is held by the investment (management) company. Dematerialized securities are held at the Securities Center17 where separate accounts are set up for each unit trust to hold all dematerialized securities in the portfolio of the trust. A list of investors in each unit trust is also maintained by the Securities Center. Nonetheless, title is held by and the accounts are held in the name of each investment (management) company with only a notational reference to the applicable unit trust. This system creates some risk for depositaries. Under the old law, the securities of a unit trust held by the Securities Center could be pledged or used as collateral for a bank loan by the investment (management) company managing the trust without the knowledge of the depositary. In such a case, the depositary would be legally responsible for such conduct regarding the securities in the unit trust, even though the depositary lacked the authority to implement the necessary “control”. The new Law on Collective Investments attempts in part to address this issue of insufficient authority of depositaries to “control” the assets under their care. The new legislation requires the depositary to approve all transactions before final settlement and delivery of the securities (referred to as ex ante approval). As to physical assets, under the old law, the bank depositary could have acted as custodian for the physical assets held by a unit trust . If it did, the assets were required to be kept in a segregated account. Under the new Law, the investment (management) company must turn over to the depositary all assets for custody or other safekeeping. These assets must be kept in accounts separate from the depositary’s own accounts. The fact that the investment (management) company has title to the assets appears to give it the power to direct the Securities Center to transfer assets from the accounts of the unit trusts into the management company’s own accounts, or otherwise dispose of them, prior to notification to the depositary. However, the Bank Team found that the legal and financial community was unanimous in its view that the assets were safe from misuse by the investment (management) company; that the notification and approval procedures to the depositary under the new law were adequate; and that, under the new law, the assets 17 Clearing and settlement services are provided by Univyc, a subsidiary of the Prague Stock Exchange, and share registration is maintained by the Prague Securities Center, which is a “contributory organization” of the Ministry of Finance. The MOF has the authority to appoint the Director of the Securities Center. While the Securities Center is administratively part of the MOF, the supervision of the Center is carried out by the Czech Securities Commission.

18

were clearly the property of the investors. The local community also confirmed that the assets are not part of the property of the investment (management) company or the depositary; nor would they be part of the bankruptcy estate of the investment (management) company or depositary. Moreover, the new Law on Collective Investments holds the depositary responsible for the custody or safekeeping of the assets of unit trusts and corporate investment funds and if that safekeeping were breached, the depositary would be liable. Furthermore, the new Law on Capital Market Undertakings provides for the creation of a Central Depository of Securities to take the place of the Securities Center. The Central Depository is not yet operational and thus it is not clear what its procedures will be. Nonetheless, it may provide for more extensive notification and authority to the depositary of a corporate investment fund and unit trust. It would also be helpful if the legislation could clarify that assets of unit trusts should be legally segregated from those of the fund manager, in addition to their physical segregation or book-entry segregation at the Securities Center. Supervisory Boards The potential for conflicts of interest between an investment management company or corporate investment fund and a depositary in the same banking group also highlights the need for well-functioning supervisory boards of investment (management) companies and corporate investment funds. The Czech Republic relies on a dual-board structure commonly found in corporate legislation based on the German law. The dual-board structure places primary responsibilities with the company’s management board. However, even in Germany, shareholders associations such as DSW (Deutsche Schutzvereinigung fur Wertpapierbesitz) have emphasized the need for a strong strategic and supervisory role to be played by the company’s supervisory board.18 The issue is important. Modern corporations, both in America and Europe, are accountable to a myriad of stakeholders, covering not only shareholders but diverse groups such an environmental and human rights non-government organizations (NGOs.) A modern corporation must find the most appropriate balance between short-term profit objectives and its medium-term obligations for corporate social responsibility. Determination of the appropriate balance falls to the supervisory board, which should set the tone for the company’s business culture and corporate ethics and thus leave the day-to-day running of the company to the management board. At its core, corporate governance concerns two issues: transparency and accountability. While the management board plays an important role in achieving transparency and accountability, ultimately it is the responsibility of a company’s supervisory board to ensure that both are achieved. The Czech Commercial Code provides some guidance for corporate supervisory boards. However the fiduciary duties of board members—both of supervisory and management boards—is generally defined as the requirements that they conduct their duties with due care, due diligence and in the best interests of the company. The Czech Commercial Code includes the requirements for due care and due diligence but fails to adequately specify

18 Information on other European Shareholders’ Associations can be found on the website of Euroshareholders at http://www.wfic.org/esh/.

19

the duty of loyalty—that the board members should conduct their activities in the company’s interests. Similarly in the old Czech legislation, the fiduciary duties of “senior officers” (who are by definition members of the management board) sets a higher standard than for other corporations. Senior officers must meet the test of “professional care” suitable for financial intermediaries and other institutions active in the financial sector. However, under the new Law on Collective Investments, members of supervisory boards are not defined as “senior officers” and thus are not covered by the regulatory system that applies to members of the management board or other “senior officers.” Therefore, although they should be responsible for ensuring that the investment (management) companies or corporate investment funds maintain systems of risk management and internal controls that fully protect investors’ interests,19 there is no specific obligation to do so. The new legislation requires that investment (management) companies and corporate investment funds place the interests of investors in priority ahead of its own interests. However, it may be helpful to require that investment (management) companies and corporate investment funds act “honestly and fairly” (as specified in the most recent UCITS Directive)20 in the interests of both the collective investment funds they manages and the integrity of the market. Investment (management) companies and corporate investment funds should also be obliged to actively take measures to avoid conflicts of interest. When such conflicts cannot be avoided, the investment managers should ensure that the collective investment funds are treated fairly. In addition to the rules of conduct provisions for investment (management) companies and corporate investment funds, it is important that the supervisory authorities be satisfied with the business reputation and professional experience of the directors of the investment (management) company, corporate investment fund and depositary (as well as those of significant shareholders in any of these entities.) The new legislation provides for substantive discussion of such “fit and proper” rules, but they only apply to senior officers and individuals holding over 10 percent of the stock of the corporate investment fund or investment (management) company (or an interest that is deemed controlling.) They do not apply to members of the supervisory board. Such “fit and proper” rules are important in ensuring that the Czech collective investment fund sector includes reputable officials not only as key officers and management directors, but also as members of the supervisory board.21 To supplement the legislative provisions, it would be helpful if a corporate governance code could be developed for collective investment fund managers and other institutional investors, such as private pension funds. The general corporate governance code for listed

19 To ensure that the compliance officer (or compliance unit) is fully effective, it is recommended that the officer (or the unit) report to both the management and the supervisory boards of the AMC. 20 See Article 5h of EU Directive 2001/107/EC for further detail on rules of conduct for management companies of UCITS funds. 21 This is less of an issue for depositaries as only licensed banks can be depositaries, and there are adequate fit and proper tests for bank managers in place (even though there are weaknesses in the supervisory board oversight exercised over bank management, as documented in the forthcoming separate assessment of corporate governance of banks.)

20

companies in the Czech Republic was developed in 2001, with the assistance of an advisor from the U.K. Know-How Fund. The code is currently in the process of being updated but has not been adopted as part of the listing standards of the Prague Stock Exchange. However, even if a general corporate governance code were adopted in the near future, it would still be helpful if a special code could be prepared for the collective investment funds sector with possible application to private pension funds. The Bank Team was informed that discussions and preparation for such a special code are already underway. With or without a corporate governance code, serious consideration should also be given to including other provisions that would strengthen the role of supervisory boards of investment (management) companies and corporate investment funds in protecting minority shareholders’ interests. One key way would to establish a minimum number of non-executive and independent directors on their supervisory boards. Risk Management, Internal Controls & Financial Reporting As noted above, the close ownership ties between investment (management) companies or corporate investment funds and depositaries highlight the importance of robust systems of risk management, including internal controls. A risk management system should include three key elements:

1) An appropriate supervisory structure, 2) A strong set of internal controls, and 3) An established process for approving new investment strategies and instruments.

In collective investment funds, it is clear that internal controls must be established and maintained for accounting, NAV calculation, customer records, segregation of assets and regulatory compliance. A compliance officer has been found to be one of the best institutions for achieving this. In addition, the risk management system should include detailed provisions on internal controls to protect investors’ interests and ensure that investment policies set forth in the prospectus are followed and that trading and investment strategies do not entail risks beyond those disclosed in the prospectus. While asset segregation is in practice ensured through the mandatory use of the central securities registry, until very recently there were no regulatory requirements for investment (management) companies and corporate investment funds to maintain adequate internal controls. The supervisory structure might include a designated senior officer in the investment (management) company or corporate investment fund who maintains a significant level of independence from the officers who make the investment decisions. The senior officer should regularly report to the supervisory board of the investment (management) company or the corporate investment fund on the fund investments and exposures and ensure that the information is provided to the board in a complete and readily understandable way so that the board can make informed decisions. The system of internal controls used by each investment (management) company and corporate investment fund will depend on the degree of complexity and sophistication of

21

the investment strategies to be implemented. However, one key issue is the need for functional segregation between the individuals responsible for entering into the investment transactions and those responsible for the “back-office” operations, that is, processing the transactions, calculating exposure, monitoring risk, performing reconciliations (and correcting errors) and reporting the transactions. In particular, the system of internal controls should include rules to track personal investment transactions by employees and officers of investment (management) companies and corporate investment funds to ensure that all such transactions can be monitored and reconstructed, if necessary. Focus should also be placed on the depositary banks’ information technology systems to eliminate the operational risk of losing data due to poorly planned computer systems. The framework for internal controls should also ensure that the prices for transactions are verified independently of those who are responsible for trade execution. Alternatively, the calculations should be regularly verified by the internal audit department of the investment (management) company or corporate investment fund. Where investments are made in complex or sophisticated derivative instruments, the investment manager should also conduct stress testing and scenario analysis so that the consequences of extreme market shocks can be measured against the current market, thus providing a benchmark for measurement of unusual risks. The system of risk management should furthermore provide for a process by which new investment instruments or strategies are evaluated and approved. The approval process should establish appropriate parameters, controls and limits to ensure that the risks are well-understood and fall within the fund’s accepted level of risk tolerance.22 The new Law on Collective Investments requires a corporate investment fund and investment (management) company to adopt a system of internal controls pursuant to the decrees issued by the CSC. The CSC issued a regulation on business execution and internal controls for investment (management) companies and corporate investment funds in May 2004 (Regulation No. 347 “On the manner of complying with the rules for careful execution of business and the rules for the organization of the internal operations of investment companies and investment funds”.) Moreover, some provisions have already been put in place to ensure external review of the internal control systems of investment (management) companies. For example, the legislation requires that each unit trust maintain its own financial statements (even though the funds are not “legal entities” but only tax-paying units.) Furthermore, the financial statements must be audited by an independent auditor and Czech practice is for the auditor to complete a review of the internal controls and financial statements of each of the unit trusts. In addition, both the Czech National Bank, as supervisor for the banking sector, and the CSC, as regulator for the capital markets, conduct onsite and offsite inspections of the bank depositaries and their inspections include reviews of the depositaries’ internal control procedures. The CSC also conducts its own onsite and offsite inspections of the collective investment funds. Nevertheless, the UCITS Directive requires the CSC to introduce an explicit requirement for investment (management) companies to establish and maintain adequate risk

22 See also Risk Management Process:Guidelines for UCITS Managers, which can be found at http://www.foa.co.uk/publications/riskmanpro.pdf

22

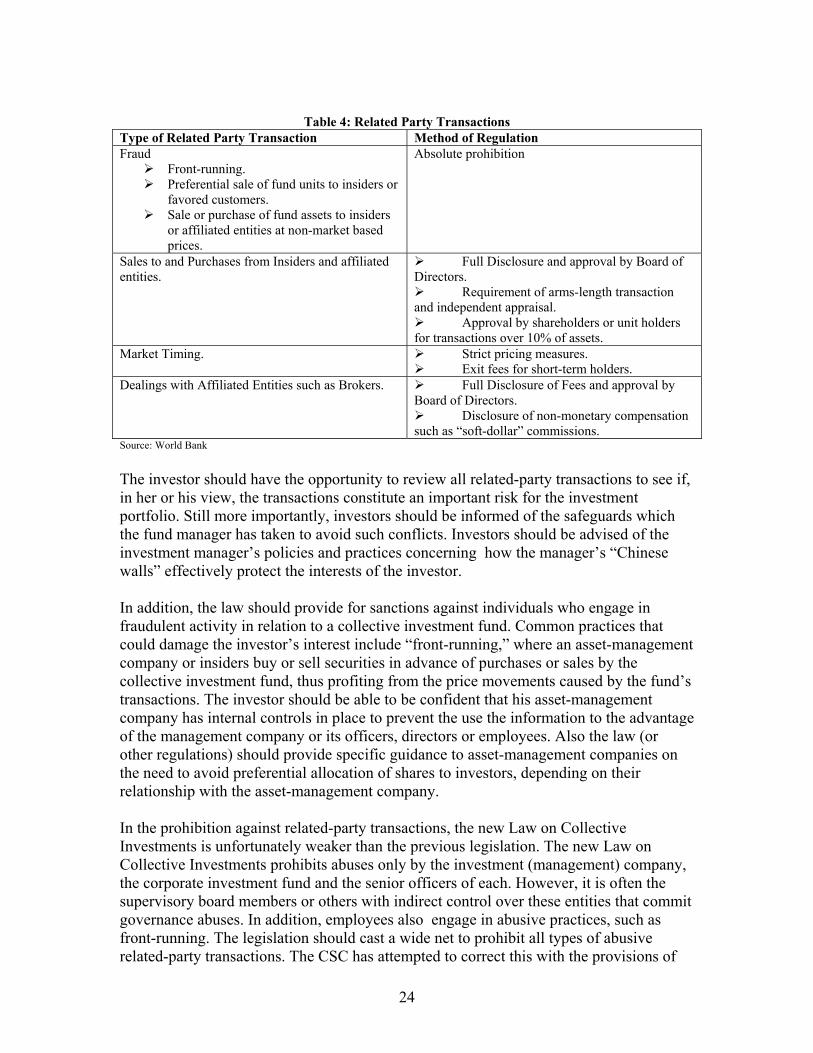

management systems. However, the Decree of May 5th, 2004, on the Method for Fulfilling the Rules of Cautious Business Practice only deals with this issue indirectly. It should set out the requirement in a separate section in detail, including an explanation of how to calculate the risk. The EU Recommendation on the Use of Financial Derivative Instruments for UCITS23 would provide a good basis for preparing a methodology to measure risk and establishing the obligation to disclose risk measurements. This will become all the more important when the volume of assets under management grows and the use of more complex fund of funds structures intensifies, especially for smaller locally owned investment managers. Explicitly requiring the use of a modern risk management system will also serve to set a standard for the pension fund management companies, which hitherto are under a much weaker regulatory structure. Regulation of Abusive Practices Legislation for collective investments should provide detailed guidance to prohibit certain common practices through which an investment (management) company or corporate investment fund can conduct its activities in the interest of its management —or its board members—rather than in the interest of the investors. Related-party transactions constitute the single most abused area with respect to conflicts of interest and investors in collective investment funds are concerned about potential conflicts of interest between those individuals and entities managing the collective investment fund and the companies in which the fund makes equity investments. Each type of related party transaction can be regulated in a different manner so as to balance the protection of investors against the benefits to investors that can come from some related-party transactions. As shown in Table 4, different types of related-party transactions can be regulated in different ways.

23 EU Commission Recommendation of 27 April 2004 on the Use of Financial Derivative Instruments for UCITS (2004/383/EC)

23

Table 4: Related Party Transactions

Type of Related Party Transaction Method of Regulation Fraud

Front-running. Preferential sale of fund units to insiders or favored customers. Sale or purchase of fund assets to insiders or affiliated entities at non-market based prices.

Absolute prohibition

Sales to and Purchases from Insiders and affiliated entities.

Full Disclosure and approval by Board of Directors.

Requirement of arms-length transaction and independent appraisal.

Approval by shareholders or unit holders for transactions over 10% of assets.

Market Timing.

Strict pricing measures. Exit fees for short-term holders.

Dealings with Affiliated Entities such as Brokers.

Full Disclosure of Fees and approval by Board of Directors.

Disclosure of non-monetary compensation such as “soft-dollar” commissions.

Source: World Bank The investor should have the opportunity to review all related-party transactions to see if, in her or his view, the transactions constitute an important risk for the investment portfolio. Still more importantly, investors should be informed of the safeguards which the fund manager has taken to avoid such conflicts. Investors should be advised of the investment manager’s policies and practices concerning how the manager’s “Chinese walls” effectively protect the interests of the investor. In addition, the law should provide for sanctions against individuals who engage in fraudulent activity in relation to a collective investment fund. Common practices that could damage the investor’s interest include “front-running,” where an asset-management company or insiders buy or sell securities in advance of purchases or sales by the collective investment fund, thus profiting from the price movements caused by the fund’s transactions. The investor should be able to be confident that his asset-management company has internal controls in place to prevent the use the information to the advantage of the management company or its officers, directors or employees. Also the law (or other regulations) should provide specific guidance to asset-management companies on the need to avoid preferential allocation of shares to investors, depending on their relationship with the asset-management company. In the prohibition against related-party transactions, the new Law on Collective Investments is unfortunately weaker than the previous legislation. The new Law on Collective Investments prohibits abuses only by the investment (management) company, the corporate investment fund and the senior officers of each. However, it is often the supervisory board members or others with indirect control over these entities that commit governance abuses. In addition, employees also engage in abusive practices, such as front-running. The legislation should cast a wide net to prohibit all types of abusive related-party transactions. The CSC has attempted to correct this with the provisions of

24

Decree of May 5th, 2004, On the method of fulfilling the rules of cautious business practices. An investment (management) company or corporate investment fund is required to establish provisions regulating related-party transactions in its internal regulations. Nonetheless, there does not appear to be any sanction against an individual for violating the internal regulations, other than dismissal by the investment (management) company or corporate investment fund. The regulations in the Decree of May 5th will have no serious effect unless they are backed up by the possibility of severe sanctions for their breach. Authority of the Czech Securities Commission (CSC) In many ways, the CSC has substantial authority. The CSC has the power to levy sizeable fines of up to CZK 100 million (approximately US$4 million.) The fines can be imposed directly by the CSC without requiring that the court imposes the fines. Similarly, the CSC can ban investment (management) company board members and controlling shareholders, if the CSC views the proposed board member “is prevented from proper discharge of the office by some other activity” or an investor as not being suitable for the “sound and prudent management” of the corporate investment fund or investment (management) company’s transparent and credible activity, or if the “interconnection of the applicant with the investment (management) company or corporate investment fund would impede effective performance of supervision.” However, on one key issue, the CSC is lacking in authority. The CSC does not have full authority to directly issue its own regulations providing the necessary guidance for the capital markets. As a result, much of the secondary legislation needed to ensure good corporate governance in the capital markets—and the collective investment fund sector—is missing, such as the ability to regulate sales practices and fee determination practices and disclosures. In addition, the CSC should be able to issue regulations providing guidance on the methods by which investment (management) companies and corporate investment funds should vote at the shareholders’ meetings of companies they are invested in. The new Laws on Capital Market Undertakings and Collective Investments give the CSC some of the requisite authority, however, they do not go far enough. Another important area in which the CSC needs additional authority is in ensuring accurate and reliable financial reporting of the collective investment funds. While the Ministry of Finance (or eventually a new Accounting Standards Board to be created) sets the accounting rules for collective investment funds, at the moment neither the Ministry nor the CSC has explicit legal authority to ensure adequate enforcement of such rules. Legal changes to the Accounting Law and the Law on Collective Investments are needed to give the CSC the requisite authority in this respect (e.g., covering issues such as access to external auditors’ working papers, ability to impose meaningful penalties for infractions and authority to request correction of erroneous financial statements and/or audit reports.) Additionally, sufficient resources should be set aside to ensure that the CSC quickly builds up the capacity to effectively undertake the enforcement function. This will be particularly important once the use of International Financial Reporting Standards, as appropriate, are required for collective investment funds. In addition, membership of the European Union has brought the Czech Republic under the EU’s “single passport” rules under which the home country supervisor of a UCITS fund selling units in the Czech Republic will be responsible for supervision and

25

regulation of the fund, rather than the host country supervisor (e.g., the CSC). Nonetheless, the CSC will be responsible for the regulation of the offer and sale of these foreign funds to investors in the Czech Republic. The CSC will need to develop a set of rules for the regulation of the marketing of these funds. Also, it will be important for the CSC to maintain close co-operation with foreign supervisory authorities in order to properly oversee non-domestic funds and fund operators. Learning from the experience of the US mutual funds industry which has recently been plagued by a wave of scandals and abuses, it may also be helpful for the CSC to establish a special department to monitor risks in the areas that it regulates, including fund practices, such as the Office of Risk Assessment and Strategic Planning of the US SEC. The Office is specifically responsible for assessment of developments in the market in general and anticipating potential problems in the US mutual fund sector, among other areas. Regulations for Special Funds The new Law on Collective Investments has created two types of funds: (1) UCITS-type funds where moneys are invested in transferable securities in accordance with the UCITS Directive applicable in the European Union and (2) “special funds” that would be outside the remit of the UCITS-based regulations. In light of the limited liquidity of the Czech capital markets, where most trading is concentrated in as few as three companies and trading margins are thin, the strong interest of investment managers lies with creating special funds. The Bank Team found that both Czech and foreign investment managers were planning to offer special funds, once the requisite legislation has been approved. Since the funds would be outside the UCITS-based restrictions, the special funds would allow investment managers to offer pooled investments in illiquid and sometimes speculative securities and assets, such as real estate and exchange-traded and OTC derivatives that are not purchased for hedging purposes. The special funds would allow high levels of risk with commensurate levels of reward. In other countries, notably Australia, property funds have been the subject of corporate governance abuses (where the fund manager was able to “dump” investments in illiquid properties into the fund.) Special care needs to be taken before allowing the public the opportunity to invest in any collective investment funds invested in real estate. Although a decree has been issued on the valuation of assets, including those of a special fund, it is not detailed enough, particularly in the areas of valuation of financial and commodity derivatives, especially if they are OTC in character. Moreover, the marketing regulations for such funds are critical to ensuring investor protection, but, as previously stated, the CSC does not have the authority to issue such regulations. At the same time, not all issues have been resolved regarding the old legislation. The old Law on Investment Companies and Investment Funds required that all existing funds, including the former voucher privatization funds, convert their structure from joint stock companies (as was permitted under the former legislation) to open-ended mutual trusts, which are regulated by contracts between unit holders and the investment (management )companies and have no status as legal entity. The Bank Team was advised that at least one, and perhaps two, of the former voucher privatization funds have not been converted into the requisite fund structure due to ongoing litigation in which minority shareholders

26

of the privatization fund joint stock company have argued that their interests will be damaged by the transformation of the fund’s legal structure. The lack of resolution of such legal issues from the past privatization program will likely create some investor uncertainty over the new funds, particularly special funds for which the detailed regulations are still being developed.

27

ANNEX Detailed Assessment of the Corporate Governance Framework for Collective Investment Undertakings in the Czech Republic: A Comparison of Rules and Practices Against Proposed Best Practice Benchmarks.24 GOVERNANCE OF COLLECTIVE INVESTMENT UNDERTAKINGS (CIUs) BOARD OF DIRECTORS The legal and regulatory regime should designate an entity that is accountable to the investor and to the supervisory authority. The entity should be responsible for assuring that investor rights are respected and act as the entity against whom redress for violation of investors’ rights may be sought. Within a corporate structure, the management board should be responsible for the policy formulation, implementation and performance of the corporate CIU and asset management companies. In its general activities, the management board should oversee the preparation of the prospectus, annual reports and implementation of investment policy. It should also oversee the risk management system, internal controls and compliance functions of the corporate CIU and asset-management company. In addition the management board should be responsible for the formulation and implementation of a code of ethics for its officers, management, employees, and external advisors. The supervising board–be it a “supervisory board” under a dual board structure or a “board of directors” under a unitary board structure—should operate independently of the management board. Depending on the structure of governance of the collective investment schemes concerned, this may be achieved through appointment of independent directors and/or audit committees. Description In its provisions relating to corporations, the Commercial Code provides for the

creation of a board of directors (management board) to act as the primary managerial unit of the corporation and a supervisory board to act as a control entity for the benefit of the corporation as a whole. Under the Commercial Code, these entities are charged with conducting their affairs with prudent care. The Law on Investment Companies and Investment Funds, No. 248/1992 has additional qualifications for members of the two boards. In order to obtain a license as a corporate investment fund or investment (management) company, a corporation must obtain approval from the CSC. The CSC as part of that review approves the members of the board of directors (management board) and supervisory board pursuant to a methodology that it has issued. In order to reinforce the independence of the board members, Section 29 provides for specific incompatibilities which would render an individual unqualified to be a member of the board of directors (management board) or supervisory board, such as government service, or a position on the board of another corporate investment fund or

24 Following international practice, the benchmarks use the EU terminology, rather than the Czech terminology. As a result, they refer to “collective investment undertakings” (CIUs) which are the entities participating in the collective investment fund sector. Under international practice, a CIU generally has one of the following legal forms: (1) a “contract-based fund” which does not have a legal personality and is organized and managed by a “management company”, (2) an “investment company” which is a fund in corporate form, which may be self-managed or managed by a management company, or (3) a “unit trust” organized under the common law in which the asset management role is carried out by the trustee of the trust. However, when the discussion deals with Czech organizations, it will use Czech terminology as modified in this assessment.

28