investment banking

DESCRIPTION

‘Investment Banking: The Dream Begins’ is for people who want to understand value. This book can help you get your arms around the many tasks and variables involved in effective valuation of a company and help you decide what kind of help you should enlist to complete a deal.TRANSCRIPT

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

Preface to the Third Edition

‘Investment Banking: The Dream Begins’ is for people who want to understand

value. This book can help you get your arms around the many tasks and variables

involved in effective valuation of a company and help you decide what kind of help

you should enlist to complete a deal.

What’s New About the Third Edition?

Firstly, the third edition of the book has a new Subtitle – The Dream Begins…!!!

Then the book has been thoroughly revised and restructured. The book has been

divided in four major parts with Part I focuses on introduction to investment banking

and discusses in detail about the offerings of investment banking entities with special

focus on equity offerings. It too discusses the private equity in depth. Part II

discusses the financial statements, segregating operating and non-operating items to

determine the core operating profits of the entity, articulation of financial statements

and the key ratios to analyse the financials of the company. Part III discusses the

reasons valuation happens in a business, and the various valuation tools used by

investment bankers. And the last part of the book offers a step-by-step guide for

analyzing and valuing a company in practice. Among the many ways to value a

company, this part focuses particularly on valuation based on comparable companies

and deals – Relative Valuation.

The book acts as the first guide to the capital markets’ aspirants and as a useful

resource and reference for the capital market participants who quickly wish to learn

the valuation of companies or refine and fine-tune their skills and compare the

companies on fundamental basis for mergers, acquisitions, private equity

investments, etc. This book is also highly beneficial for investment banking trainers

providing various training programmes on valuation of companies.

I have tried to keep the book as simple as possible and have tried to explain the

concepts in the plain vanilla language in such a way that you can easily apply them

on your own. This book tries to fulfil an important need as a valuable training

material and reliable handbook for finance professionals. Stay with it, and I believe

the payoff for both beginning and experienced professionals will be huge.

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

Contents at a glance

Part I

Investment Banking Chapter 1 The Origin of Investment Banking 25

Chapter 2 The Business of Investment Banks 35

Chapter 3 Equity Offerings & Exits 49

Chapter 4 Private Equity 65

Part II

Financial Statements Chapter 5 Understanding Financial Statements 85

Chapter 6 Cleaning of Financial Statements 133

Chapter 7 Analysing Financial Statements 151

Part III

Valuation

Chapter 8 Valuation Overview 181

Part IV

Relative Valuation

Chapter 9 Comparable Company Analysis 205

Chapter 10 Comparable Deals Analysis 253

Part V

Excel Shortcuts 267

Part I - Investment Banking

Chapter 1: The Origin of Investment Banking

1.0 Introduction 25

1.1 The First Investment Banks 26

1.2 Regulatory Environment 28

1.3 The Recession of 2008 29

1.4 Investment Banking Post Financial Crisis 30

Chapter 2: The Business of Investment Banks

2.1 What is Investment Banking 36

2.2 What Investment Banks Do? 37

2.3 Investment Banking Hierarchy 37

2.4 Functions on Investment Bank 38

2.5 Fund Raising Via Private Equity 42

2.6 Initial Public Offerings (IPOs) 42

Chapter 3: Equity Offerings & Exits

3.0 Introduction 49

3.1 Instruments Involved In Equity Offerings 50

3.2 Parties Involved In Equity Offerings 50

3.3 Initial Public Offerings (IPOs) 52

3.4 Book Building IPO Process 54

3.5 Delisting of Shares 58

3.6 IPO Activity in India 60

Chapter 4: Private Equity

4.1 What Is Private Equity 65

4.2 How Private Equity Works 69

4.3 Need for Private Equity Investments 70

4.3 What Private Equity Firms Look For 73

4.4 Private Equity Process 74

4.5 Private Equity in India 78

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

Part II - Financial Statements

Chapter 5: Understanding Financial Statements

5.0 Introduction 85

5.1 Sourcing the Financial Statements 86

5.2 Location of Company Reports 88

5.3 Understanding Financial Statements 89

5.4 Statement of Financial Position 95

5.5 Income Statement 111

5.6 Statement of Comprehensive Income 118

5.7 Statement of Cash Flows 120

5.8 Statement of Shareholders’ Equity 126

5.9 Articulation of Financial Statements 127

Chapter 6: Cleaning of Financial Statements

6.0 Introduction 133

6.1 Sourcing Non-operating Expenses and Onetime Charges 134

6.2 Typical Non-operating Expenses and Onetime Charges 135

6.3 Special Items 137

6.4 Clean/Adjusted Profits 141

6.5 Adjusted Capital 144

6.6 Using Clean or Reorganised Financials 147

Chapter 7: Analysing Financial Statements

7.0 Introduction 151

7.1 Measuring Performance with Ratios 152

7.2 Categories of Ratios 152

7.3 Liquidity/Short Term Solvency Ratios 152

7.4 Capital Structure and Coverage Ratios 155

7.5 Turnover Ratios/Resource Management 159

7.6 Profitability Ratios 162

7.7 Application of Ratios in Evaluating Performance and Decision

Making 175

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

Part III - Valuation

Chapter 8: Valuation Overview

8.1 Introduction 182

8.2 Approaches to the Business Valuation 183

8.3 The Assets Approach 184

8.4 Comparable Company Analysis 185

8.5 Comparable Deal Analysis 186

8.6 Discounted Cash Flows 187

8.7 Leveraged Buyouts 188

8.8 Breakup Analysis 189

8.10 +VEs and –VEs of Valuation Methodologies 193

8.11 Is There A Best Valuation Tool? 195

8.12 Which Method Results in the Highest Valuation? 198

Part IV - Relative Valuation

Chapter 9 : Comparable Company Analysis

9.1 Introduction 206

9.2 Why Trading Comps Tool is Popular 206

9.3 Uses of Trading Comps 209

9.4 Steps for Trading Comps Valuation Tool 209

9.5 Step I: Selection of Peer Group Companies 210

9.6 Step II: Calculate Enterprise Value 212

9.7 Step III: Making Financials Comparable 222

9.8 Step IV: Calculate Multiples 231

9.9 Step V: Benchmarking & Valuation 239

9.10 Sourcing the Information for Trading Comps 245

9.11 Summary of Multiples 246

9.12 Is Comparable Valuation Better than DCF 250

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

Chapter 10: Comparable Deals Analysis

10.1 Introduction 253

10.2 Steps for Deal Comps Valuation Tool 254

10.3 Step I: Selection of Comparable Deals 256

10.4 Step II: Calculate Enterprise Value 257

10.5 Step III: Source Key Financials 261

10.6 Step IV: Calculate Multiples 262

10.7 Step V: Benchmarking and Valuation 263

Part V - Excel Shortcuts

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

SNAPSHOTS FROM 3RD

EDITION

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

1.4 INVESTMENT BANKING POST FINANCIAL CRISIS

The recovery of investment banking industry has been as dramatic as its decline. At the start of 2009,

the world’s banks and brokers were in a deep hole. They had recorded some US$1 trillion in credit

losses and write-downs of their mortgage holdings in the financial crisis of 2007 and 2008, and markets

were still reeling. The sky cleared in the second half, making 2009 a year of recovery. By the year-end,

the Stock indices across the world shot up by more than 50%, which helped trigger a flood of fund

raising (new stock and bond issues) and M&A activities.

The year 2011 witnessed investment banks generating a total fee of $81 billion, almost consistent with

2010 level. JP Morgan ($5.5 billion), Bank of America Merrill Lynch ($4.9 billion) and Morgan

Stanley ($4.1 billion) were the leading investment banks in 2011; Goldman Sachs ($3.91 billion) fell to

#4, out of top 3, for the first time on the overall investment banking fee basis.

Exhibit 1.1: Top Investment Banks (Fee Collection Basis)

(In $ Million) CY Dec’11 1H June’12

Fee Rank Fee Rank

JP Morgan 5,518 1 2,395 1

Bank of America Merrill Lynch 4,920 2 1,988 2

Goldman Sachs 3,908 4 1,727 3

Morgan Stanley 4,052 3 1,652 4

Citi 3,140 7 1,547 5

Credit Suisse 3,398 5 1,490 6

Deutsche Bank 3,184 6 1,448 7

Barclays 2,799 8 1,323 8

UBS 2,358 9 923 9

The year 2012 started on a bad not in terms of investment banking fee with the total fees declining to

$33.94 billion in the first half of 2012, down by 23% compared with the year ago period. JP Morgan

maintained its lead position in the first six months of 2012 with total investment banking revenues of

$2.4 billion. Bank of America Merrill Lynch was at second position with total fee of $1.99 billion.

Goldman Sachs re-entered in the list of top 3 with total revenues of $1.7 billion ahead of Morgan

Stanley. In terms of investment banking products, Bonds and Equity Markets was lead by JP Morgan,

M&As by Goldman Sachs and Loans by Bank of America Merrill lynch.

Investment banks faced decline in number of deals and fees in almost all parts of the world in the first

six months of 2012 with the exception of Japan where M&As and Debt markets became stronger

compared with year ago period.

2.4 FUNCTIONS OF INVESTMENT BANK

They say that money makes the world go round. And, if it does, investment bankers help direct and

facilitate its flow. Investment banks provide a wide range of financial services to clients. They structure

M&A deals, raise capital (equity or debt) to help companies grow, analyse the prospects of listed

companies, and trade in securities on behalf of clients.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

The core functions of investment banking include —

Raising Capital

Sales and Trading of securities

Mergers & Acquisitions

Research

2.4.1 Raising Capital

The need to raise capital in business lead to the birth of Investment Banks. Investment banks raise

capital either through equity markets or debt markets. Money from equity markets is raised primarily in

form of private equity investments, seed funding, block trades, initial public offerings (IPOs) and

follow public offerings (FPOs), while from debt markets it involves money raising in form of bonds,

mortgage-backed securities and asset backed securities. From just raising money, the role of the

investment banks, in recent times, involves advisory on optimum capital structure.

To act as intermediary between issuers and investors

To provide access to equity and fixed income capital

To create specialized securities and derivatives

Steps in raising capital

Financial & Valuation Modeling

Preparation of Pitch Book

Organizing road shows and investor meets

Due Diligence

Facilitate transaction (valuation and stake to be diluted, structuring of deal)

Collection of fee by Investment Bankers

4.1 WHAT IS PRIVATE EQUITY

Private Equity is a form of investment in equity capital of a company that is not quoted on a public

exchange. In other words, private equity investments are normally focused towards unlisted entities

that cannot or do not want to raise equity in public markets (via IPO route) in near future. Obtaining

PE is very different from raising debt or a loan from a lender, such as a bank. Lenders have a legal

right to interest on a loan and repayment of the capital, irrespective of your success or failure.

Two important features of private equity investing include—

It’s About Capital:

Private equity investing means putting capital into a business to expand, develop new products or fund

changes to ownership and management. Private equity investors do more than buy the rights to share in

a company’s return – they provide working capital.

And More Than Just Capital:

PE investors generally provide their capital in exchange for a sizeable stake in the business. They also

invest their expertise – in management, finance, marketing, strategic direction and networks. By

exercising some control through board seats and management agreements, PE investors can protect and

grow their investments. This alignment of interests and the ability to add value to the business often

means that PE investors can generate higher returns than those available from traditional ‘hands-off’

equity investing.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

4.1.1. Different Equity Funding Stages

Equity investing is often divided into the broad categories described below.

Maturity of Company

−−−−−−−−−−−−−−-−−−−−−−−−−−−−−−−−−−−−−−−−−−−−−−−−−-−−−−−−−

Seed

Stage

Start-up

Stage Expansion Stage

Replacement

Capital Buyout

Angel Investments VC & PE Private Equity

For the purpose of this chapter, PE is the universe of all venture and buyout investing, whether such

investments are made through funds, funds of funds or secondary investments.

Seed Stage: Financing provided to research, assess and develop an initial concept before a business has

reached the start-up phase.

Start-Up Stage: Financing for product development and initial marketing. Companies may be in the

process of being set up or may have been in business for a short time, but have not sold their products

commercially and will not yet be generating a profit.

Expansion Stage: Financing for growth and expansion of a company, which is breaking even or

trading profitably. Capital may be used to finance increased production capacity, market or product

development, and/or to provide additional working capital. This stage includes bridge financing and

rescue or turnaround investments.

Replacement Capital: Purchase of shares from another investor or to reduce gearing via their financing

of debt.

Buyouts: A buyout fund typically targets the acquisition of a significant portion or majority control of

businesses, which normally entails a change of ownership. Buyout funds ordinarily invest in more

mature companies with established business plans to finance expansions, consolidations, turnarounds

and sales, or spinouts of divisions or subsidiaries. Financing expansion through multiple acquisitions is

often referred to as a "buy and build" strategy. Investment styles can vary widely, ranging from growth

to value and early to late stage. Furthermore, buyout funds may take either an active or a passive

management role.

5.4 STATEMENT OF FINANCIAL POSITION

SFP or Statement of Financial Position (Popular as Balance Sheet) is the core of the financial

statements. All other statements either feed into or are derived from the ‘Statement of Financial

Position’. SFP gives a snapshot of the company’s financial position at a given point of time – showing

the resources available to the management and the claims against those resources by creditors and

shareholders.

Of the three basic financial statements (Income Statement, Statement of Financial Position, Statement

of Cash Flows), Statement of Financial Position is the only statement, which applies to a single point in

time of a business' fiscal year i.e. Statement of Financial Position is always as on date and not for any

period. E.g. Cash is always as on date, i.e. the company has xxx million cash as on 31 December 2012.

One cannot say that the company has cash of xxx million for 12 months ending 31 December 2012.

“The Statement of Financial Position is just like a photograph: It represents, at a moment in time, the

financial position of the business entity.”

Statement of Financial Position is divided into three sections: Assets, Liabilities and Shareholders’

Equity.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

Statement of Financial Position

Assets = Liabilities + Equity

Resources of the Business Amounts owed to the outside creditors

Capital provided by owners

Current Assets (cash, debtors, inventories etc.)

Non-current Assets

(property, plant,

machinery, investments, intangibles etc.)

Current Liabilities (short

term loans, outstanding expenses etc.)

Non-current Liabilities

(long term loans, pension obligations etc.)

Contributed Capital

(share capital issued, securities premium)

Earned Capital (Retained Earnings)

Why analyze a statement of financial position? It’s the entry point to the inner financial workings of a

company. The numbers contained in this statement give important smoke signals of whether business is

doing good or sliding into trouble.

6.0 CLEANING FINANCIAL STATEMENTS

‘Cleaning’ or ‘Adjusting’ the reported numbers sounds a little strange, doesn’t it? Well, it’s not. Rather

it is the essence of the science of valuation. To analyze and compare the companies, it is appropriate to

add or remove various financial data or apply various computations to get a true economic picture of

the business. Adjusting is what analysts and business valuation professionals do to fully examine assets

and companies as a whole.

Historical financial statements should reflect the true operating performance of the company, so that

the numbers can be used for valuation and comparison purposes. However, the reported financials may

include some non-operating income or expenses and some exceptional gains/incomes or

losses/expenses. Therefore, the historical financials need to be adjusted for those items that, in the

analyst’s judgment, distort the true operating performance of the business. Reported numbers need to

be cleaned, else they may lead to distorted valuations.

Cleaning the reported numbers is a process to see what would have been the

profits of the company, if those exceptional items (expenses/losses/incomes/gains)

were not there.

The objective of cleaning or normalizing historical financial statements is to present the data on a basis

comparable to that of other companies in the industry, thereby allowing the analyst to form conclusions

as to the strength or weakness of the subject company relative to its peers.

There is no exclusive list of such extraordinary or non-operating items; however, typical examples

include restructuring charges, litigation charges, impairment of assets, penalty charges, losses due to

floods or earthquakes or fire, losses due to strikes, insurance claims, losses or incomes from

discontinued operations, and loss or gain on sale of assets.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

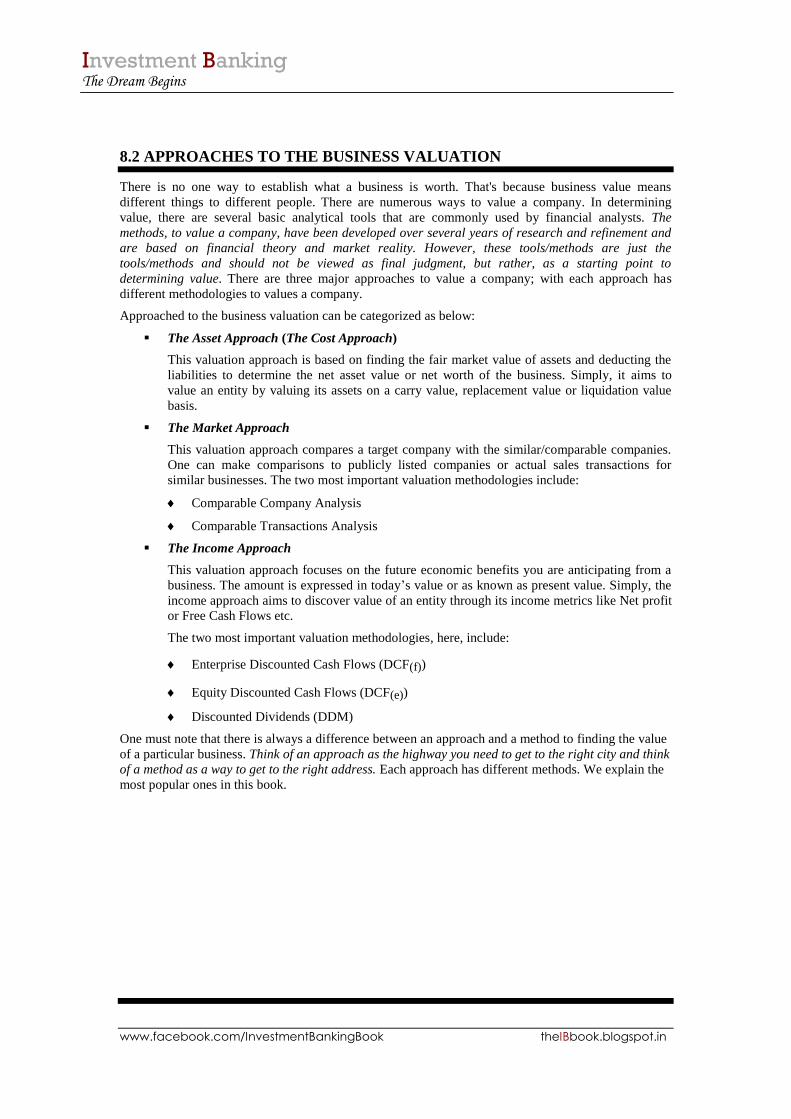

8.2 APPROACHES TO THE BUSINESS VALUATION

There is no one way to establish what a business is worth. That's because business value means

different things to different people. There are numerous ways to value a company. In determining

value, there are several basic analytical tools that are commonly used by financial analysts. The

methods, to value a company, have been developed over several years of research and refinement and

are based on financial theory and market reality. However, these tools/methods are just the

tools/methods and should not be viewed as final judgment, but rather, as a starting point to

determining value. There are three major approaches to value a company; with each approach has

different methodologies to values a company.

Approached to the business valuation can be categorized as below:

The Asset Approach (The Cost Approach)

This valuation approach is based on finding the fair market value of assets and deducting the

liabilities to determine the net asset value or net worth of the business. Simply, it aims to

value an entity by valuing its assets on a carry value, replacement value or liquidation value

basis.

The Market Approach

This valuation approach compares a target company with the similar/comparable companies.

One can make comparisons to publicly listed companies or actual sales transactions for

similar businesses. The two most important valuation methodologies include:

Comparable Company Analysis

Comparable Transactions Analysis

The Income Approach

This valuation approach focuses on the future economic benefits you are anticipating from a

business. The amount is expressed in today’s value or as known as present value. Simply, the

income approach aims to discover value of an entity through its income metrics like Net profit

or Free Cash Flows etc.

The two most important valuation methodologies, here, include:

Enterprise Discounted Cash Flows (DCF(f))

Equity Discounted Cash Flows (DCF(e))

Discounted Dividends (DDM)

One must note that there is always a difference between an approach and a method to finding the value

of a particular business. Think of an approach as the highway you need to get to the right city and think

of a method as a way to get to the right address. Each approach has different methods. We explain the

most popular ones in this book.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

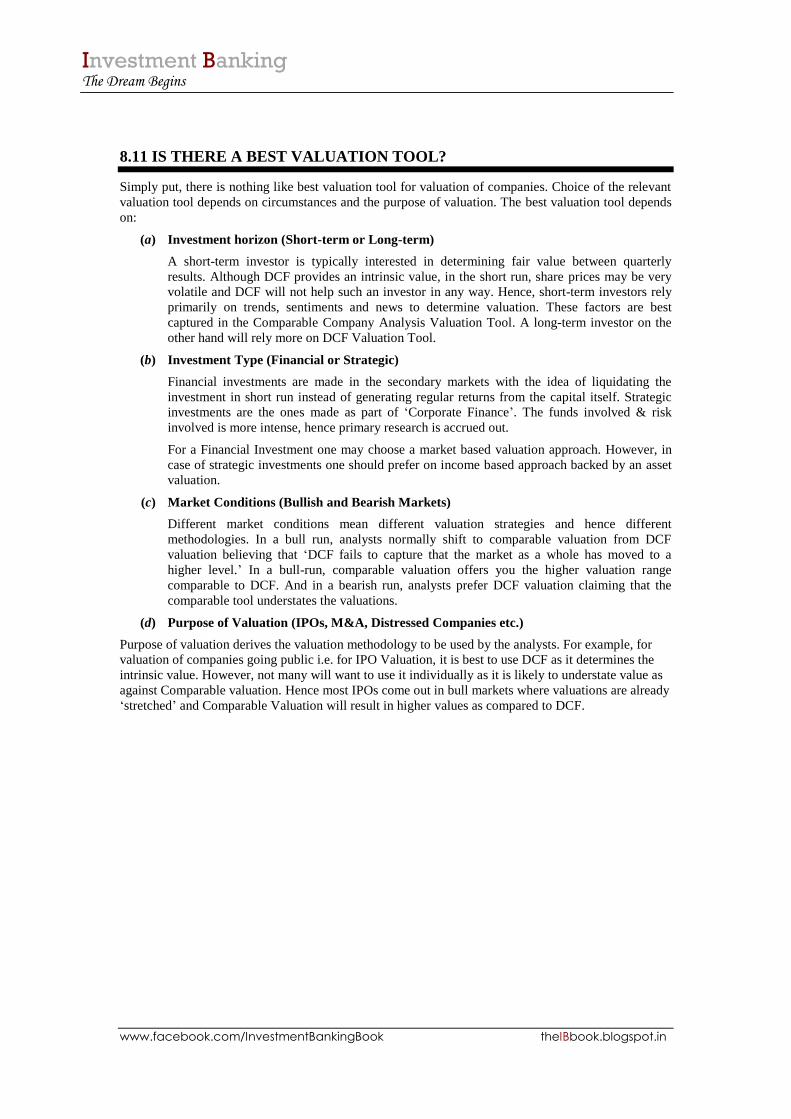

8.11 IS THERE A BEST VALUATION TOOL?

Simply put, there is nothing like best valuation tool for valuation of companies. Choice of the relevant

valuation tool depends on circumstances and the purpose of valuation. The best valuation tool depends

on:

(a) Investment horizon (Short-term or Long-term)

A short-term investor is typically interested in determining fair value between quarterly

results. Although DCF provides an intrinsic value, in the short run, share prices may be very

volatile and DCF will not help such an investor in any way. Hence, short-term investors rely

primarily on trends, sentiments and news to determine valuation. These factors are best

captured in the Comparable Company Analysis Valuation Tool. A long-term investor on the

other hand will rely more on DCF Valuation Tool.

(b) Investment Type (Financial or Strategic)

Financial investments are made in the secondary markets with the idea of liquidating the

investment in short run instead of generating regular returns from the capital itself. Strategic

investments are the ones made as part of ‘Corporate Finance’. The funds involved & risk

involved is more intense, hence primary research is accrued out.

For a Financial Investment one may choose a market based valuation approach. However, in

case of strategic investments one should prefer on income based approach backed by an asset

valuation.

(c) Market Conditions (Bullish and Bearish Markets)

Different market conditions mean different valuation strategies and hence different

methodologies. In a bull run, analysts normally shift to comparable valuation from DCF

valuation believing that ‘DCF fails to capture that the market as a whole has moved to a

higher level.’ In a bull-run, comparable valuation offers you the higher valuation range

comparable to DCF. And in a bearish run, analysts prefer DCF valuation claiming that the

comparable tool understates the valuations.

(d) Purpose of Valuation (IPOs, M&A, Distressed Companies etc.)

Purpose of valuation derives the valuation methodology to be used by the analysts. For example, for

valuation of companies going public i.e. for IPO Valuation, it is best to use DCF as it determines the

intrinsic value. However, not many will want to use it individually as it is likely to understate value as

against Comparable valuation. Hence most IPOs come out in bull markets where valuations are already

‘stretched’ and Comparable Valuation will result in higher values as compared to DCF.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

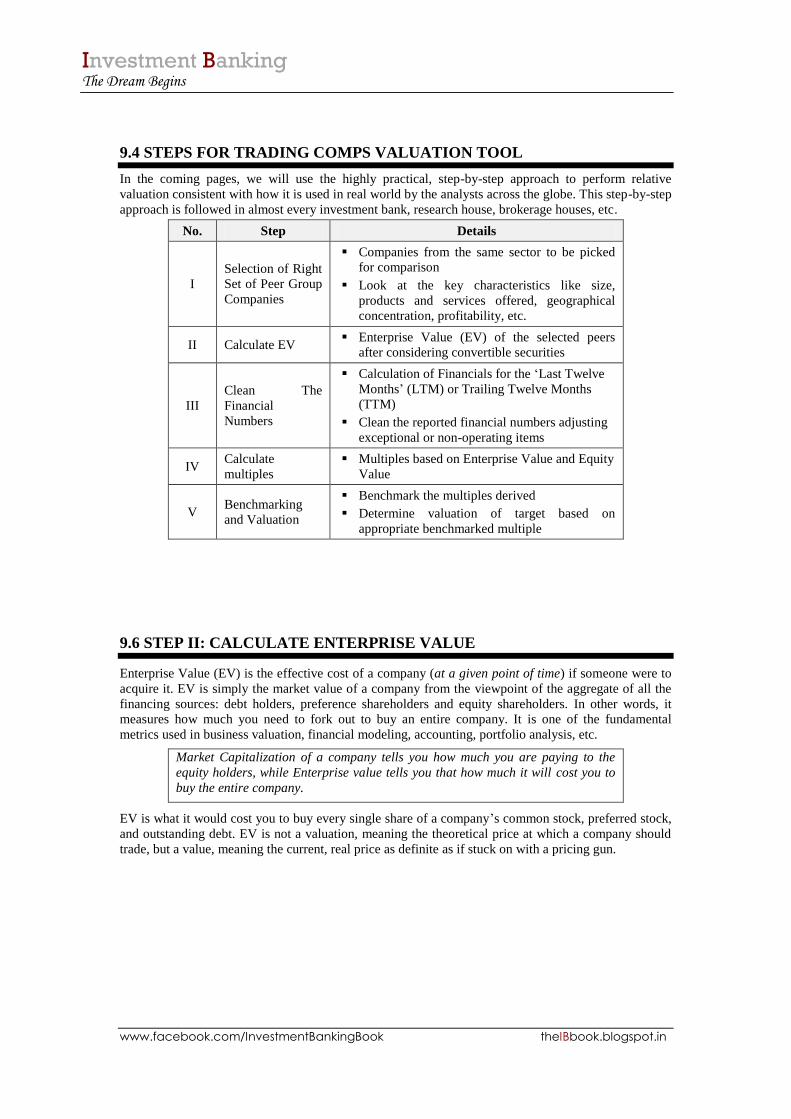

9.4 STEPS FOR TRADING COMPS VALUATION TOOL

In the coming pages, we will use the highly practical, step-by-step approach to perform relative

valuation consistent with how it is used in real world by the analysts across the globe. This step-by-step

approach is followed in almost every investment bank, research house, brokerage houses, etc.

No. Step Details

I

Selection of Right

Set of Peer Group

Companies

Companies from the same sector to be picked

for comparison

Look at the key characteristics like size,

products and services offered, geographical

concentration, profitability, etc.

II Calculate EV Enterprise Value (EV) of the selected peers

after considering convertible securities

III

Clean The

Financial

Numbers

Calculation of Financials for the ‘Last Twelve

Months’ (LTM) or Trailing Twelve Months

(TTM)

Clean the reported financial numbers adjusting

exceptional or non-operating items

IV Calculate

multiples

Multiples based on Enterprise Value and Equity

Value

V Benchmarking

and Valuation

Benchmark the multiples derived

Determine valuation of target based on

appropriate benchmarked multiple

9.6 STEP II: CALCULATE ENTERPRISE VALUE

Enterprise Value (EV) is the effective cost of a company (at a given point of time) if someone were to

acquire it. EV is simply the market value of a company from the viewpoint of the aggregate of all the

financing sources: debt holders, preference shareholders and equity shareholders. In other words, it

measures how much you need to fork out to buy an entire company. It is one of the fundamental

metrics used in business valuation, financial modeling, accounting, portfolio analysis, etc.

Market Capitalization of a company tells you how much you are paying to the

equity holders, while Enterprise value tells you that how much it will cost you to

buy the entire company.

EV is what it would cost you to buy every single share of a company’s common stock, preferred stock,

and outstanding debt. EV is not a valuation, meaning the theoretical price at which a company should

trade, but a value, meaning the current, real price as definite as if stuck on with a pricing gun.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in

9.9.1 Preference of Multiples

There has been an ongoing debate as to which multiple is used in which situation. There is no fixed

answer to it. However, we can make a note of the following:

EV/Sales multiple is a preferred multiple in case of the young companies, which do not have an

established history of profits. For example while comparing the start-up companies, multiples

based on EBIT or EBITDA might be meaning less if the companies are reporting losses. In such

cases, one is left with two multiples – EV/Sales and EV/Operating Metric.

Amongst profit multiples (EV/EBIT and EV/EBITDA), the multiple of EBITDA has preference in

case of capital intensive industries like manufacturing, oil & gas, industrial goods, telecom etc., as

the amount of depreciation and amortization figure will have a huge impact on EBIT. And in case

of service industry companies, one can use either EBIT or EBITDA multiples.

9.12 IS COMPARABLE VALUATION BETTER THAN DCF

In majority of the cases DCF & trading Comps are complimentary i.e. one provides a sanity check to

the other! However, in times of conflict it is better to rely on DCF. This is because Comps do not truly

attempt to arrive at Intrinsic Value, implying that the market could easily ‘stretch’ valuations based on

peers.

One cannot substantiate whether Apple Inc. is correctly trading at an P/E multiple of 15.60x unless one

can test it through at least one or more methods that Value a company based on its Fundamentals. DCF

ties Stock Value to fundamentals whereas Trading Comps are driven by Sentiments & Consensus

Estimates.

10.1COMPARABLE DEAL ANALYSIS

Comparable Deals Analysis is another multiples-based approach to derive an implied valuation range

for the target company. The process for completing the deal comps is quite similar to the trading comps

method, but the multiples derived from the two methods have different meanings. The multiples form

trading comps are the potential multiples on which the deals can happen or on which the premiums or

discount will be applied while doing a deal, while the multiples derived from the transaction comps are

the historical multiples on which deals had happened and they are inclusive of premium or discounts

given at the time of deal.

Deal Comps are very similar to trading comps analysis except that the deal comps use actual

transaction data instead of publicly traded companies.

Potential buyers or investors look very closely at the deal multiples that have been paid for comparable

acquisitions in past as it gives them an indications for negotiations while closing the deal. Precedent

transactions have a broad range of applications, most notably to help determine a potential sale price

range for a company, or part thereof, in a M&A transaction or PE deal or a JV deal.

Note: One must note that Transaction comps method does not mean that it can be used only for

Mergers and Acquisitions deal. Rather this method is useful for any stake acquisition deal - either

partial stake acquisition or full stake acquisition.

Investment Banking The Dream Begins

www.facebook.com/InvestmentBankingBook theIBbook.blogspot.in