investing in germany - jll germany-2015-jll.pdf · jll • investing in germany • october 2015 |...

TRANSCRIPT

Published in October 2015

Investing in Germany

JLL • Investing in Germany • October 2015 | 3

Contents

Introduction Investing in Germany 4Overview of Germany 5Germany: 10 sources of competitive advantages 6Legal Overview 7Leasing Overview 8Environmental Overview 10Key tax issues - Acquisition 12Ownership and operation of German real estate 13

City Focus Berlin 14 Cologne 18 Düsseldorf 22 Frankfurt am Main 26 Hamburg 30 Munich 34 Stuttgart 38

Contacts 42

4 | JLL • Investing in Germany • October 2015 4 | JLL • Investing in Germany • October 2015

Berlin

Hamburg

Düsseldorf

MunichStuttgart

Frankfurt

IntroductionInvesting in Germany

4 | JLL • Investing in Germany • October 2015

Germany is one of the largest investment markets in Europe, with an average commercial transaction volume of more than €29 bn (2005-2014). A safe haven for global capital, Germany offers investors a stable financial, political and legal environment that is highly attractive to both domestic and international groups.

This brochure provides an introduction to investing in German real estate. JLL has over 40 years of experience in Germany and today has nine offices covering all major German markets. Our full-service real estate offering is unrivalled in Germany. We look forward to sharing our in-depth market knowledge with you.

Timo Tschammler MSc FRICSInternational DirectorManagement Board GermanyOffice and Industrial, JLL

Germany’s thriving, robust and mature real estate market is one of the cornerstones of the German economy. Detailed knowledge of the law, the real estate market and the players in it has been one of Clifford Chance’s core competences for decades and forms the basis of the most experienced, integrated and largest real estate legal practice in Germany. We will help you achieve your goals and minimise legal risks throughout the lifecycle of your real estate investments, wherever your investment strategy takes you.

Cornelia ThalerPartnerHead of Real Estate GermanyClifford Chance

Cologne

JLL • Investing in Germany • October 2015 | 5 JLL • Investing in Germany • October 2015 | 5

Overview of Germany

Germany has the strongest economy in Europe and one of the largest worldwide. It plays a leading role in the European Union (EU) and benefits from the customs duty exemptions that membership provides. This membership allows Germany to take advantage of free trade between the community’s 28 member states. Germany accounts for 20% of Europe’s GDP (EU-28) and is home to 16% of the total European Union population. The German economy is both highly industrialised and diversified – with an equal focus on services and production.

Germany’s capital city is Berlin, however as a Federal Republic Germany has sixteen “Bundesländer” (federal states) with each having its own state legislature, political institutions and administration. The federal structure ensures the division of authority between the Federal Government and the “Länder”. For this reason there are some differences between the administrative/legislative protocols of the Länder, such as Building Codes or certain tax levels. From an economic perspective, the federal structure, along with the variety of conditions found across the German regions and cities, presents investors with a range of opportunities.

German manufacturing is internationally renowned for its quality and leading-edge design and technology. German chemical, automotive, and machinery & equipment manufacturing industries are globally recognised. Germany’s main trading partners include European countries such as France, the UK,

Italy, and the Netherlands, as well as international markets such as the United States, China and Russia.

‘Made in Germany’ is a synonym for quality. This reputation has been built on the consistent innovation shown by German companies, making them global leaders in the development of new technologies. German dominance in the development of new technologies continues to this day; in 2014 Germany had twice as many patents approved as France and Great Britain combined.

Germany is the leading global force in high-tech solutions with German engineering a globally demanded commodity. This dominance looks set to continue: 11% of all university graduates have an engineering degree.

Environmental research and technologies are also areas in which Germany will continue to lead. Germany’s position as a global pioneer in developing renewable and environmental technologies is a trend that looks set to continue.

Germany places strong emphasis on environmental sustainability and encourages large companies to take part in “corporate sustainability” for a healthy world. National targets aim to reduce CO2 emissions by 80% to 60% in 2050.

6 | JLL • Investing in Germany • October 2015

Germany: 10 sources of competitive advantage

Quality of Living Survey

Rank City Country

1 Vienna Austria2 Zurich Switzerland3 Auckland New Zealand4 Munich Germany5 Vancouver Canada6 Düsseldorf Germany7 Frankfurt Germany8 Geneva Switzerland

Source: MERCER Ranking 2015

The variety of opportunities and competitive occupational costs make Germany an excellent destination for investment.

Germany has the highest GDP and largest population in Europe, with four cities having a population of greater than 1 million.

Premium infrastructure. Germany is Europe’s number one logistics market. An excellent transportation and communications network assures just-in-time delivery.

Germany has nine major international airports: Frankfurt/M, Munich, Düsseldorf, Berlin, Hamburg, Cologne, Leipzig, Hannover and Stuttgart.

Germany has highly developed economic and political legislation, providing the legal framework required to protect investments.

Germany, based on a 2014 survey of more than 20,000 people in 20 countries, is the world’s most popular country.

Economic diversity: Manufacturing and the provision of services provide two distinct, yet complementary, grounds that anchor the strong and stable German economy. The manufacturing sector is one of the largest and strongest in the world. Small and medium-sized enterprises (SME) are also an important part of the German economy, with almost 60% of all employees working in SMEs.

Germany is one of the top three global exporters (alongside China and the US). This supply-side strength is one of the main drivers in making Germany one of the leading destinations for international investors.

1

2

3

4

5

6

Germany has one of the lowest unemployment rates in Europe and worldwide. Alongside this, Germany benefits from an excellent standard of workforce, due to the quality of education and vocational training available.

The renewable energy sector in Germany is the most innovative and successful in the world.

Liquid Markets. Owing to Germany’s federal structure, it has many strong cities; this variety brings with it opportunities for diversification (there are 70 cities with more than 100,000 inhabitants).

7

8

9

10

6 | JLL • Investing in Germany • October 2015

JLL • Investing in Germany • October 2015 | 7

Ownership

In Germany, ownership title is one of the fundamental individual rights, protected by the constitution. The owner of an asset such as real estate has unlimited rights of use, enjoyment of the fruits of its asset (rents, natural resources, interest payments etc), disposal, letting, and the right to bequeath the asset.

The most common form of real estate ownership title is full freehold title. Of lesser importance is condominium ownership (Wohnungseigentum), or quasi-ownership forms such as hereditary building rights (Erbbaurechte) or usufruct rights (Nießbrach). The ownership title of real estate assets are always registered in the land register, as are the most important encumbrances which can rest on real property (such as mortgages).

Full freehold ownership

Full freehold ownership is the ownership over a plot of land. As a matter of law, immovable fixtures, most importantly buildings, are considered an integral part of the land. Thus, whoever is registered as the owner of the freehold in the land register also owns the buildings on the land. Full freehold ownership can be charged either for financing purposes with mortgages or with liens permitting/prohibiting certain conduct (e.g. cable rights, right of way etc).

Ownership title is transferred from one owner to the next through the registration of ownership title in the land register. Registration of the ownership title is based on an agreement between the purchaser and the vendor. This agreement must always be notarised before a notary; if not notarised, an agreement to transfer real estate is void under German law, and a land register will refuse to register the transfer of ownership title. The transfer of ownership title is usually effected some weeks after the commercial closing between the parties has taken place. There are certain legal safeguards in place to ensure that both the purchaser and the vendor of real estate can enter into and execute a transaction involving real estate, despite being unable to close the transaction themselves.

Condominium ownership

Condominium ownership is the result of the separation of individual units in a building. Residential multi-user properties are commonly held in this way,

especially in larger German cities. However, this form of ownership is not common for commercial purposes, such as offices (which are usually owned in full freehold ownership).

Condominium ownership consists of the ownership of a specific part of the building, usually the rooms of the apartment (Sondereigentum), and the co-ownership, together with all other condominium owners, of the communal parts of the building (Gemeinschaftseigentum), such as elevators, staircases and gardens.

The relationship between the condominium owners is governed by a contract, which governs how decisions relating to the whole of the real estate are reached, and how costs are shared. In larger condominiums, there will be a condominium administrator in charge of managing the affairs of the condominium owners.

Condominium ownership is freehold ownership, albeit of only a part of a building, and as such can be let, sold on and charged in the same way.

Hereditary building rights

Hereditary buildings rights are a type of quasi-ownership rights to real estate. They are similar to freehold ownership insofar as they entitle the owner to use a plot of land. They can be sold, bequeathed and charged with mortgages and liens. But a hereditary building right is only temporary, and after the term of the hereditary building right has passed, the right ceases to exist and the usage rights are, with all other rights, conferred back to the full freehold owner.

Hereditary ownership rights are brought about by agreement between the full freehold owner and the beneficiary of the hereditary building right. The right needs to be registered in the land register; for the hereditary building right, an additional land register page is formed to register all changes in title to this quasi-ownership right.

Typically, a hereditary ownership right lasts for 99 years, but it is possible to extend this. Hereditary building rights are used by entities which, while allowing third parties to use and redevelop a plot of land on a very long-term basis, hesitate to sell full freehold ownership. The most prominent examples are German municipalities and the Christian churches, both of which make use of hereditary building rights regularly.

In cooperation with

Legal overview

8 | JLL • Investing in Germany • October 2015

Commercial buildings and properties are often let through commercial lease agreements. Commercial leases are governed by special provisions of the German Civil Code. This law leaves most matters up for agreement between the parties, but provides fall-back provisions on which the parties can rely if they do not choose to deviate from the general rule of the law. Some of these provisions are pro-landlord, others are more pro-tenant. In general, German lease law can be said to have a slight bias towards the tenant, more than for example in the UK, but less than in France.

A German lease agreement will always contain provisions on the following issues:

Rent object

This needs to be clearly defined to avoid problems.

Duration

Under German law, the parties are free to agree to a fixed term, or can leave the duration of a lease agreement unspecified. In the latter case, a commercial lease is generally terminable with six to nine months’ notice. If a fixed term is agreed, the term is subject to market practice. Retail properties tend to be let for 10-15 years, whereas office buildings are usually let for an initial term of 5-10 years, and shorter terms thereafter. Other usages can result in different market-standard terms. Contractual renewal options are common, but not a matter of statutory law; they must be agreed by both parties.

The term of a commercial lease can not, as a matter of law, exceed 30 years. After that time, both parties can terminate the lease, even if the contract stipulates a longer period. In practice, there is a legal requirement that leases with a duration of more than one year must meet “written form” requirements. This does not only mean that all material parts of the agreement which form the lease agreement must be in writing, but furthermore that all parts of the lease must form one “deed”. There are different ways to comply with these requirements. If a lease does not comply with the legal requirements of written form, it remains valid and in force, but after one year may be terminated by either party as if the lease had an unspecified term, i.e. with six to nine months’ notice.

Rent

The rent can, and is, freely agreed between the parties of commercial leases. All the usual permutations of rent calculations can be found in Germany (fixed rent, turnover rent, mix of both etc.), including all methods of incentivising tenants (rent-free periods etc.).

The rent review mechanism in Germany links changes in rent to inflation (normally VPI – the German consumer price index). Often this mechanism involves a hurdle rate at which point the change in rent will be triggered; once triggered the passing rent will be amended to reflect the change in VPI. Frequently however, the change in VPI is not fully incorporated in the new rent. For instance a standard rental increase may outline that after a given change in VPI, then the rent will be affected by 90% of this change. It should be noted that rental adjustments, while possible in principle, must allow for an increase as well as a decrease of rent, reflecting the current market situation, to be valid. The only exception is if a rent step-up plan is explicitly agreed upon in advance. But “upward-only” rent reviews are not permissible in German law.

Rent usually consists of the true compensation for the usage of the property, as well as a prepayment by the tenant of costs the landlord has vis-à-vis third parties (e.g. waste disposal, utilities, ground rent etc.). Unless the lease explicitly provides for such costs to be borne by the tenant, the landlord must carry them. It is standard to refer to certain legal provisions listing the most important kinds of ancillary costs. However, in some markets tenants refuse to carry certain costs (e.g. ground tax). In this case, the landlord must deduct these expenses from his income to calculate the true net rent.

Maintenance and repairs

Unless otherwise agreed between the parties, the obligation to perform and pay for maintenance and repairs rests with the landlord. However, it is common for the tenant to take over the execution and costs of certain maintenance and repair works, whereas the landlord will be responsible only for structural issues (Dach und Fach). Alternatively, a landlord can reach an agreement where the tenant will be responsible even for these structural issues; but this is less common. German courts will closely scrutinise such agreements and are not shy of holding such triple-net provisions invalid if agreed upon due to the overwhelming market power of the landlord.

Leasing overview

In cooperation with

JLL • Investing in Germany • October 2015 | 9

Sub-letting / Assignment

Sub-letting is permissible under German law, but usually subject to agreement between the parties which restrict the tenant’s possibilities of sub-letting. The unilateral assignment of a lease by the tenant to a third party is, unless specifically allowed and provided for in the lease agreement, not possible under German law. Unless specifically allowed and provided for, it always requires the consent of the landlord.

In the event of a sale the lease will follow the land, i.e. the purchaser of the real estate automatically becomes, by mechanism of law, landlord in place of the vendor. There are only few exceptions to this rule; most notably, the original landlord will remain responsible for any rent security provided to them by tenants. In the worst case, the tenant can claim back the rent security from the original landlord even if it no longer owns the property and has passed the security on to the acquirer of the property. As a result, there are usually specific agreements relating to such security in purchase agreements.

Acquisition options

Agreements between tenants and landlord which entitle one party to ask for the property to be sold are not uncommon. However, they do require notarisation to be valid.

Tax

German commercial lease agreements are normally subject to VAT, provided that the tenant is an entity which can reclaim VAT. There are certain types of tenants which are not, such as doctors or banks. This can lead to complications in the tax treatment of the property which require specialist advice.

Standard Rental Terms Office Retail Logistics

Rents €/sqm/month €/sqm/month €/sqm/month

Typical lease term 5-10 years 5-10 years (High Street) 3-5 years for existing properties and 7-10 years for new space

Frequency of rent payable Monthly in advance Monthly in advance Monthly in advance

Typical rent deposit (expressed in months) 3-6 months Negotiable Negotiable

Basis of rent increase at review VPI with hurdle rates VPI with hurdle rates VPI with hurdle rates

Frequency of rent increases Annual Indexation Annual Indexation Annual Indexation

10 | JLL • Investing in Germany • October 2015

Green Buildings – Sustainability in Germany

Germany is pursuing an ambitious program of transforming the real estate industry from one of the largest consumers of fossil fuels to an entity governed by the principles of sustainability. The Energieeinsparverordnung 2014 (EnEV 2014) is a piece of legislation which deals with buildings’ energy consumption and efficiency. Under this regulation, old and inefficient heating systems must be replaced by efficient new ones, building insulation must meet certain minimum standards and air conditioning systems must be regularly inspected by experts. Furthermore, all buildings must have energy certificates (Energieausweis), which must be presented when selling or letting a building.

These regulations will be made tougher in the coming years, with the aim of tightening the obligations. New buildings will have to meet ambitious energy efficiency standards; it is also possible that these stringent new regulations could be extended to existing buildings. The new regulations will oblige property owners to state the energy consumption and efficiency of their building when advertising their buildings for purchase or rental purposes. As of 2021, all newly constructed buildings must be so-called minimal-energy buildings, i.e. require zero energy for heating, or even produce energy. Buildings built by public entities will have to achieve this by 2019.

These inititiatives aim to reduce the carbon footprint of buildings, both new and existing. These changes will have important implications for the allocation of the cost burden between landlords, tenants and (via subsidies or tax breaks) the government. Recent laws allow landlords of residential premises

to increase rents as a result of energy efficiency measures, such as added insulation, new heat-insulating windows, more efficient heating systems etc. However, these increases are limited to 11% of the rent. In addition, the tenant’s right to reduce the rent as a result of disturbances and nuisance related to the construction work associated with such measures is now limited to construction activities exceeding three months.

All of these measures have led to the rise of certificates confirming compliance with applicable energy-efficiency laws, and even stricter standards, in German commercial real estate. For instance, it is now extremely rare for trophy office buildings to be built without such certificates. Common certificates are the German “Deutsches Gütesiegel Nachhaltiges Bauen” (DGNB) and “Bewertungssystem Nachhaltiges Bauen” (BNB), but other certificates such as the US “Leadership in Energy and Environmental Design” (LEED) certificate or the UK’s BREEAM are also present in the German market. These certificates are becoming increasingly important in the minds of many institutional investors. This trend of sustainability in real estate is set to continue.

Contamination of land or buildings

When land becomes polluted or a building becomes contaminated, the responsibility to remediate this usually lies with the owner. However, if the polluter can be identified, they too can be held responsible. Property tenants are usually not held liable, unless they caused the pollution. Under German law, a property owner cannot get out of clean-up liability by selling or abandoning the land (concept of “eternal land-owners clean-up liability”). Indemnification clauses in agreements with property purchasers only allocate liability between the contract parties and significantly not in relationship to the authorities.

Actions to clean up can be brought either by the authorities, or by certain private parties (mainly property owners and neighbours). The procedure can take time and involves an exact evaluation of the issues, agreement of possible remedies, planning and execution of remediation work and monitoring of the results. This usually involves environmental / technical experts. The process is normally carried out in co-operation between the authorities and the party responsible for clean-up.In most German states, if contamination is found it must be reported to the authorities. There is no legal obligation on the owner to actively search for

Environmental Overview

In cooperation with

JLL • Investing in Germany • October 2015 | 11

contamination of the land or buildings. However, for some contaminants (such as asbestos), best management practices adopted by market participants, as well as workplace safety and insurance requirements, have led to thorough investigations of the majority of commercial buildings. There is no automatic obligation to remove contaminants (e.g. asbestos, PCB), unless there is an imminent material threat to human health. Whether or not contaminants can remain in the building depends on the result of an assessment of the danger posed in each individual case.

Environmentally material facilities

Buildings or industrial facilities which may have an adverse impact on the environment and the surroundings, especially local neighbours, require permitting under special environmental laws. These permits deal with environmental hazards and nuisances such as noise, air pollution, waste disposal, wastewater discharge, and many others. Environmental regulation is comprehensive and complex in Germany, as can be expected in a developed, mature industrialised nation; much of it is determined by EU law. Specialised authorities of the Federal States are responsible for the permitting process and compliance monitoring of such facilities, which are governed under the German Federal Emission Protection Act (Bundes-Imissionsschutzgesetz) and many other environmental laws. Depending on the kind of facility, the permitting process can be very time consuming and elaborate and is likely to require several public hearings. Smaller installations are subject to lesser requirements. Non-industrial real property is not usually subject to these permitting requirements.

Germany is pursuing an ambitious program of transforming the real estate industry from one of the largest consumers of fossil fuels to a sector governed by the principles of sustainability.

12 | JLL • Investing in Germany • October 2015

Key tax issues − Acquisition

In cooperation with

Real Estate Transfer Tax

• The transfer of German real estate by way of an asset deal is subject to German Real Estate Transfer Tax (“RETT”).

• The transfer of shares/interest in entities holding German real estate is generally also subject to RETT if, inter alia, a) 95% or more of the shares/interest are directly or indirectly transferred to, or are unified in the hand of, a single purchaser or b) upon a transaction a taxpayer holds an economic participation of at least 95%, directly or indirectly, in a German real estate holding company. Moreover, if German real estate is held by a partnership, RETT is triggered, if within five years 95% or more of the interest in such partnership are directly or indirectly transferred to new partners. However, structures to mitigate RETT might be available.

• The RETT rate depends on the German Federal State in which the property is located and currently ranges between 3.5% to 6.5%.

• The market standard is that RETT is borne by the purchaser. However, parties may also negotiate a deviating provision in a sale and purchase agreement.

Value Added Tax

• The transfer of leased German real estate constitutes (in most cases) a sale of an ongoing business which is not subject to German Value Added Tax (“VAT”) provided, inter alia, the purchaser continues the leasing business of the seller. In such case the purchaser assumes the VAT position of the seller regarding the real estate (including VAT correction obligations, if any).

• In any other case, the sale and transfer of German real estate as well as shares in companies owning German real estate is generally VAT exempt. However, the possibility to opt for VAT might be available in order to allow a deduction of input VAT or to avoid any correction of input VAT in connection with the real estate acquisition in an asset deal.

• The current standard VAT rate is 19%.

Income Tax

• In the case of corporate ownership, rental income derived from German real estate is subject to German Corporate Income Tax (“CIT”) at an effective standard rate of 15.825% (including solidarity surcharge). In the case of individual ownership, German Income Tax (“GIT”) with an individual (progressive) income tax rate up to 47.475% (including solidarity surcharge) on the rental income would apply. In the case of ownership through a partnership structure, income taxation would depend on the relevant partners (companies or individuals).

• Expenses and costs incurred in relation to German real estate (including e.g. depreciation deduction of in general up to 3% p.a. on the acquisition costs of the building) should in principle be deductible for CIT and GIT purposes.

• Interest expenses should generally also be tax deductible. However, the tax deductibility of net-interest expenses is limited under the so-called Interest Barrier Rules (“IBR”) to generally 30% of the tax EBITDA of the relevant year. However, no limitation would apply, inter alia, if the net-interest expenses are less than €3.0m p.a. Other IBR exemptions might be available in the single case.

Withholding Tax

• In principle, no German Withholding Taxation (“WHT”) should apply to (non-profit linked) interest payments and rental revenues. However, in certain circumstances the German tax authorities may order the application of WHT at a rate of 26.375% (including solidarity surcharge).

• Dividends paid by a German corporation are generally subject to German WHT at a rate of up to 26.375% (including solidarity surcharge). The rate might be reduced if a double tax treaty is applicable and might even be reduced to 0% under the European Parent-Subsidiary Directive, if applicable. However, such reductions of WHT are subject to substantial requirements.

JLL • Investing in Germany • October 2015 | 13

Ownership and operation of German real estate

In cooperation with

Trade Tax

• Any commercial trade or business is in principle subject to German Trade Tax (“TT”), if and to the extent the business is operated in Germany through a German permanent establishment or a German permanent representative (“German PE”).

• Generally, TT is levied on the business income calculated based on the profits determined for CIT or GIT purposes. However, certain adjustments are required to determine the TT base (i.e. certain add-backs and deductions are made for TT purposes). This applies in particular to interest expenses, of which 25% minus EUR 100,000 are added back to the tax base. Special TT exemption for real estate companies may also be available on a case by case basis.

• The TT rates currently range from approximately 7% to 17% depending on the municipality in which the German PE is located.

• Non-German resident companies merely leasing German real estate should generally not be subject to TT provided they do not act through a German PE.

VAT

• The leasing and letting of German real estate is subject to VAT, but generally exempt from VAT. However, the possibility to opt for VAT is available under certain circumstances and commonly made use of provided the tenants use the property for businesses which allows the reclaiming of paid VAT as input VAT.

Land Tax

• In general, German real estate owners are subject to Land Tax in Germany. However, it is almost standard that Land Tax is borne by the tenant as an ancillary cost provided the respective lease agreement comprises such a pass-through provision.

• The Land Tax rates range between 1% and 2% of a special property value determined under German Valuation Tax Act (reflecting values as of the year 1964), which is generally substantially lower than the current fair market value of the property.

Capital Gain Tax

• Capital gains realised in connection with the direct sale of a German real estate (i.e. asset deal) should in principle be subject to GIT or CIT (as the case may be) at the standard rates mentioned above. If the capital gain is connected to a German PE, TT also applies.

• If the seller is a corporation, generally 95% of a capital gain from the sale of the shares in a corporation (i.e. share deal) holding German real estate would be exempt from CIT. If the seller is an individual holding the shares as a private asset and has held less than 1% of the shares in the last five years, a capital gain from the sale of shares in a corporation would generally be subject to GIT at a flat rate of 26.375% (including solidarity surcharge). If the individual holds the shares as a business asset or has held more than 1% in the last five years, 40% of the capital gain would be exempt from GIT; the remaining amount would be subject to the individual progressive income tax rate of the seller (and consequently only 60% of the expenses would be deductible). If the capital gain is connected to a German PE, TT also applies.

• In case of non-German residents, Germany may have waived its right to tax capital gains realised from the sale of shares in companies holding German real estate under an applicable double taxation treaty.

•

14 | JLL • Investing in Germany • October 2015

City Focus: BerlinThe Capital of Germany

Berlin is the capital city of Germany and the seat of German government. It is also the largest city in Germany with 3.4 million inhabitants. The wider Metropolitan Region Brandenburg/Berlin is home to roughly 5.9 million inhabitants. Berlin is also a growing city with a forecasted population growth of 3.0% until 2030 (from 2014).

The capital has one of the most modern traffic and transport infrastructure networks in Europe, with long-distance and regional trains as well as the international airport offering comprehensive transport options. The city’s geographical location enables Berlin to serve as an important and attractive trade fair location for central and east European countries. Berlin is also a

competitive business location. Its highly qualified workforce and, excellent universities provide a major reason for companies to locate here.

Berlin is consistently well place in location rankings and continues to offer a high quality of life. The most important companies headquartered in Berlin are: Deutsche Bahn, Siemens, Mercedes Benz, Deutsche Telekom, Zalando and Axel Springer. Berlin is also a growing city and offers an attractive environment for business, living and retail. The project “Berlin Adlershof – City of Science, Business and Media” is a new district occupying 420 hectares in south-east Berlin. It is a location internationally renowned for ‘forward-looking’ companies.

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

16 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 17

Berlin is the main hot spot for international retailers

Berlin is considered the innovation heart of the creative sector and of academic research, and a fashion capital and tourist hotspot in Europe. There can be no doubt that Berlin is one of the most interesting retail locations in Europe. The city offers a breadth and depth of products that is unique both within and beyond Germany. Some ten kilometres of prime location covering more than 1,035,000 sqm of sales space are spread over eight top areas and offer tenants and investors virtually unlimited scope and potential. In addition, Berlin’s tourist appeal is a strong magnet for national and international retail formats. Berlin is not only the most frequently visited city in Germany – it is also among the top three in Europe. In spite of – or maybe because of – its size, Berlin’s is constantly reforming and reshaping. Alexanderplatz Square has been transformed rapidly, with sales space doubling in recent years. Hackescher Markt has turned from an insider’s favourite to an internationally-known location. Friedrichstraße has also found its own niche. The street is now uniquely positioned as a premium location with a strong tourist appeal. As one of the symbols of Berlin, Kurfürstendamm remains in focus for developers and the Potsdamer Platz has become even more attractive with the new 76,000 sqm “Mall of Berlin” that opened in 2014. While nationwide comparison shows that Berlin does not have the highest rents or the highest footfall, the German capital clearly remains No. 1 in terms of international appeal, variety and brand diversity.

Sustained population growth

At year-end 2014, Berlin’s population exceeded 3.4 million as the result of an influx of almost 40,000 inhabitants p.a. The Federal Institute for Research on Building, Urban Affairs and Spatial Development expects further population growth to more than 3.5 million inhabitants by 2030 and Berlin’s City Development Senate projections are even higher, predicting 3.746 million by the same date. The new, young arrivals to Berlin tend to move into the city centre districts. In addition to the traditionally fashionable locations such as Prenzlauer Berg and Kreuzberg, there is increasing demand for locations in the vicinity (such as Neukölln) and less well-developed areas in the Mitte district such as Wedding and Moabit owing to comparatively cheaper rental levels. The influx of young people in the past is now reflected in the high birth rates in those districts. The former newcomers also often attempt to stay in the city centre as young families, which gives rise to high natural increases in population in city centre districts such as Friedrichshain, Kreuzberg and Mitte. This means that Berlin’s population growth in the last few years is also due to

a slight surplus of fertility over mortality. Rents for newly built apartments in city centre locations range between €11.00 and €17.00 per sqm. Since 2011 there has been a new upwards trend with rental growth of 38%. A reduction in the building surplus was followed by a scarcity of supply in certain submarkets and significant rises in rental levels.

Growing demand from business services

The strong economic growth over recent years has driven higher levels of employment – especially in office employment which has grown by around 5% since 2011; much higher than average office employment growth in Germany. As it’s the capital of Germany, demand for Berlin office space until 2005 was mainly driven by government-related companies and institutions. Since then, business and service consultancies, media companies as well as industry identified Berlin as an attractive office location. The most recent trend in the office market is high demand from former pure internet players like Google, Microsoft, Zalando or Rocket Internet who have since 2009 taken up more than 150,000 sqm of office space. We expect this trend to continue and with those companies capturing a significant share of Berlin’s office space in the next few years. Principal demand is concentrated in locations within the inner city suburban train circle, including office markets like Mitte and Europacity/Main Station as well as Mediaspree. Berlin has an extremely high land potential within the inner city which means land prices are kept low in comparison to other cities.

Platform for transport to Eastern Europe

The Logistic Region consists of the city of Berlin and the surrounding agglomeration area. As the region is strongly populated, Berlin is an attractive location for discounter and retail-oriented companies’ warehouses. In contrast, the share of traditional industrial space is relatively low but it is increasing in importance. Excellent infrastructure, with several motorway and railway connections, is fundamental for Berlin’s role as a trade hub, which sees a strong flow of goods, particularly from Eastern European countries.

Berlin is among the top three European cities and the most frequently visited city in Germany.

18 | JLL • Investing in Germany • October 2015

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

City Focus: CologneGermanyʼs Media Hub

Cologne is, with one million inhabitants, Germany’s fourth largest city (after Berlin, Hamburg and Munich) and North Rhine Westphalia’s biggest city. The wider “Rhine-Ruhr” Metropolitan Region comprises more than 10 million inhabitants. Cologne is a growing city with a forecast population growth of around 1% until 2030 (from 2014).

Cologne benefits greatly from its central location and accessibility to the markets of central and western Europe. Cologne has a long tradition as an axis of trade and as such attracts a wide variety of tenants from across the business spectrum. Leading enterprises from the industrial, automotive, media, chemical, pharmaceutical and engineering sectors are located in Cologne.

Because of its centrality and accessibility, Cologne is a successful European economic and globalised area attracting large companies including Ford, Bayer, Stadtwerke Köln, Rewe, AXA and RWE Power. Cologne plays host to a number of TV stations, record labels and publishing houses underlining the importance the city places on the media and creative industries in Germany.

All sectors of the media industry are represented in Cologne, for example WDR, the largest broadcasting station in continental Europe, has its headquarters in Cologne. Local employment structure is characterised by a strong service sector with a focus on insurance companies, financial institutions, industry and professional associations as well as retailers. Cologne is also a transportation hub benefiting from excellent infrastructure.

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

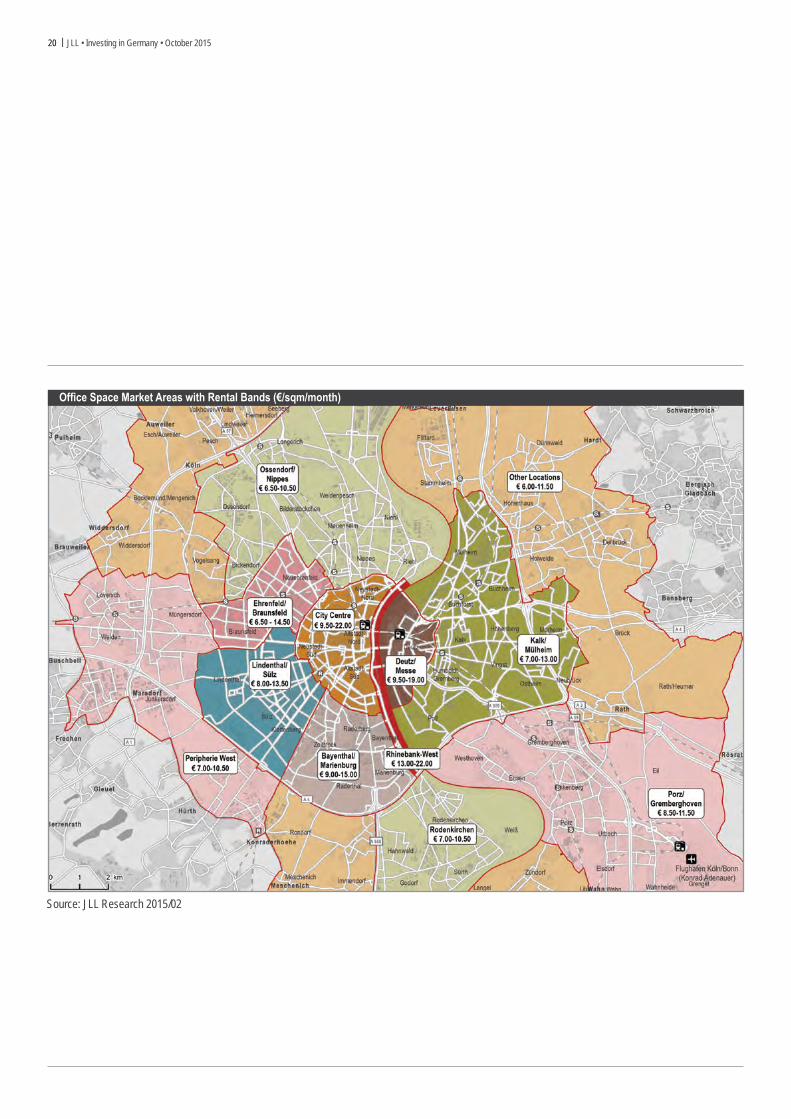

20 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 21

Attractive shopping destination

Cologne is also something of a cultural metropolis, attracting millions of tourists each year with its historic sites and numerous high profile events like Carnival or Christopher Street Day. Tourists and residents alike can indulge in a 3km-long shopping tour through downtown Cologne. No other German city offers a comparable circuit with all major shopping streets forming an almost continuous loop. Schildergasse and Hohe Strasse are among the most visited shopping streets in Germany. Retail premises in the prime locations of Cologne command rents that are among the highest in Germany. However, when compared to other cities, there are only a small number of shopping malls in Cologne. The retail landscape here continues to be characterised by highly functional street level locations. Cologne’s population is continuing to grow with population growth at its highest in locations close to the city centre. The central areas are still relatively affordable and are particularly attractive for newcomers; this includes the large numbers of students who come to the city to study. In the city centre, rental prices have now reached €12.00 to €14.00 per sqm, whilst in peripheral locations, new-build apartments are already being offered below €9.00 per sqm. Rents have been rising again in Cologne since 2011 and have increased by around 6%.

Growing office market

Since 2005 office employment has grown by roughly 20% to almost 260,000 office workers. Cologne has developed as an attractive office location and office employment is expected to grow further in the coming years with a continued focus on business services, trade and media companies.

Logistics

The logistics market in the Cologne Region benefits from the relatively strong purchasing power of the population and well-established infrastructure with several motorways, harbours and the second largest freight airport in Germany.

Retail premises in the prime locations of Cologne command rents that are among the highest in Germany.

22 | JLL • Investing in Germany • October 2015

City Focus: DüsseldorfOne of the Most Dynamic and Influential Business Locations

With 601,000 inhabitants and a further 11.6 million inhabitants located within one hour’s drive, Düsseldorf is one of the most dynamic and influential business locations in Germany. Düsseldorf is also a growing city, with population growth forecast to increase by 2% until 2030 (from 2014). It is also one of the most important German commercial centres, playing a leading role in exporting goods from Germany to foreign trade partners. Due to this strong track record in exporting goods, Düsseldorf has attracted internationally oriented service providers such as banks, insurers, logisticians, media experts and tax consultants. The largest companies are: Metro, C&A Fashion, Henkel, Rheinmetall, Vodafone and Demag Cranes.

Furthermore, businesses from many nations are represented in Düsseldorf such as Fujifilm (Japan), HSBC (UK), L’Oreal (France), TATA Steel (India), Huawei (China) and Statkraft (Norway). Due to this, 40 consulates and 33 foreign chambers of commerce are also based here. Düsseldorf is the state capital of the region North Rhine-Westphalia and is home to all ministries of the provincial government.

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

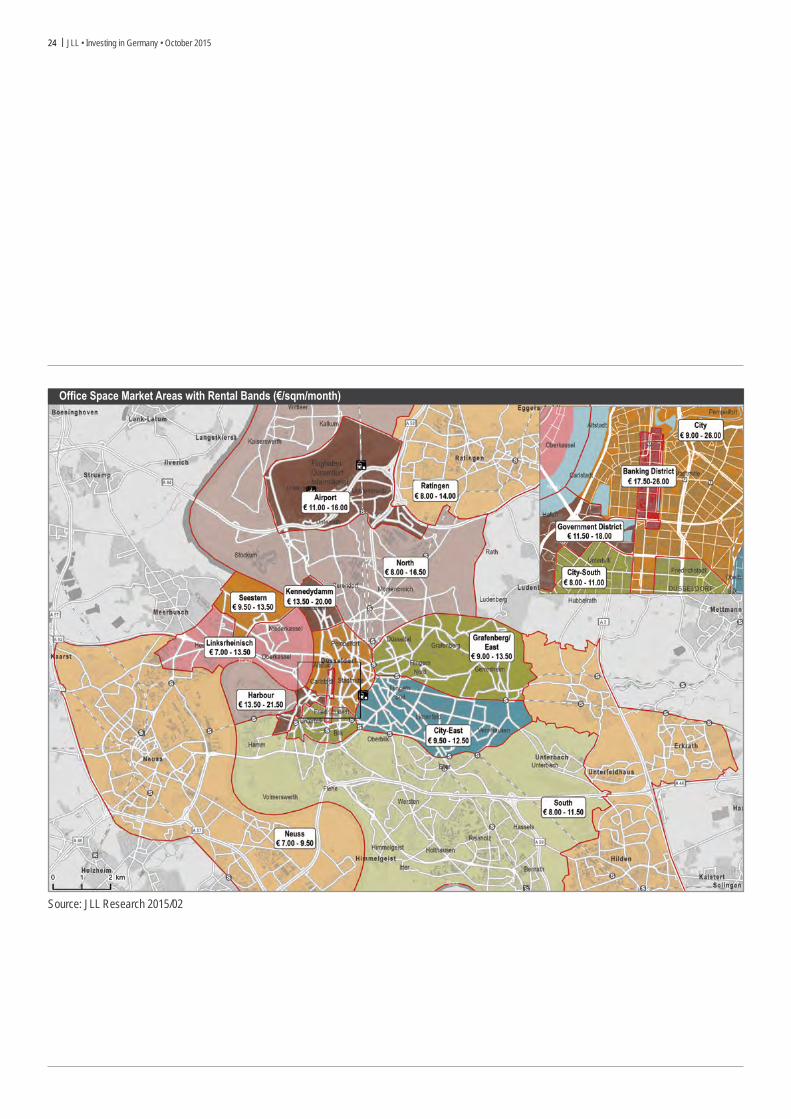

24 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 25

Düsseldorf – a retail metropolis

Düsseldorf is a retail metropolis and one of the top three retail locations in Germany. In recent times it has benefited from the growing interest of international retailers looking to expand, attracting these groups thanks to its mix of luxury, consumer and fashionable locations.

Düsseldorf is famous for its fashion industry. Major companies like Peek & Cloppenburg are headquartered here. The Königsallee or “The Kö” has one of the highest rents for retail space in Germany and is a strong draw for tourists. Königsallee is by far the most heavily frequented luxury shopping location in Germany. Several fashion stores have recently reopened following major refurbishment. With the completion of the landmark project Kö-Bogen in 2013 some additional 19,000 sqm of new retail space have been created in this prominent location between Königsallee and Schadowstrasse.

Growing number of households

Düsseldorf’s population is continuing to grow, largely as a result of inward migration – but also because of the rising birth rate within the city. For the first time since the late 1970s, in 2014 the population exceeded 600,000 inhabitants. With the growth in the numbers of households exceeding population growth, the trend for smaller households in Düsseldorf continues. The average asking rent for accommodation in Düsseldorf is €9.65 per sqm/month, which equates to a rise of more than 4% compared with the same period in 2013. Asking rents for new-build apartments are currently around

€12.70 per sqm. Rents in Düsseldorf have been rising since 2010 (c.20%). New developments have had a great effect on the Düsseldorf rental market over the long-term.

Taking this increase into account, and the fact that the rising trend is currently slowing down in Düsseldorf, there has been rather a moderate rental price increase since 2004, which has been at approximately the same rate as inflation. Whether there is further rental price development in Düsseldorf remains to be seen and depends on the large number of project developments.

Service sector pushes office market

Demand for office space in the region is bolstered by the general importance of the service sector. The share of people employed in this sector in Düsseldorf is extremely high, at over 80%. In addition to its strong service sector, Düsseldorf, as the capital of North Rhine-Westphalia, is known as the “Desk of the Ruhr-Area” which means a significant share of the demand for office space comes from local and regional government.

Logistic platform for Europe

Düsseldorf has an advantageous geographic location for trade – Benelux, France and the remainder of Germany are all easily accessible. Excellent infrastructure is fundamental to Düsseldorf’s role as a trade hub for western and central European business.

Düsseldorf has benefited from the growing interest of international retailers looking to expand and is one of the top three retail destinations in Germany.

26 | JLL • Investing in Germany • October 2015

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

City Focus: Frankfurt am MainA Global Financial Centre

Frankfurt am Main is located in the centre of Germany. With approximately 701,000 inhabitants it is fifth largest city in Germany, after Berlin, Hamburg, Munich and Cologne. The wider metropolitan region, Rhine-Main, comprises over 5.6 million inhabitants and it is the second largest region in Germany. Forecasts for Frankfurt population growth vary: While the German Federal Institute for Research on Building, Urban Affairs and Spatial Development expects the population to decrease by 2% until 2040, the City of Frankfurt itself expects the growing trend (which has been continuously taking place for some 15 years now) to continue, with a forecasted growth of 14% by 2030 (from 2014). Frankfurt is the financial centre of Germany and the largest in continental Europe. The European Central Bank, The German Federal Bank and The German Stock Exchange as well as several large commercial banks like Deutsche Bank and Commerzbank are located in the heart of Frankfurt.

First class infrastructureFrankfurt Central Station is one of the largest stations in Europe, serving approximately 400,000 travellers or those passing through every day. Furthermore Frankfurt Airport numbers amongst the busiest airports worldwide and, in addition to this, the Frankfurter Kreuz motorway junction is one of the busiest in Europe.The Frankfurt Trade Fair is the world’s second largest exposition company. It has a presence in more than 160 countries and generated turnover of 544 million Euros in 2014.Frankfurt offers a high quality of life. The city is also known as a ‘green city’. Protected green areas make up more than 50% of the inner city. Frankfurt has ranked among the top 10 of the global Mercer Quality of Living Survey for many years now.

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

28 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 29

Frankfurt is the financial powerhouse of Europe and home to The European Central Bank, The German Federal Bank and The German Stock Exchange.

High international profile backs retail business

Mention Frankfurt and people think of the airport, the Paulskirche and Goethe, Frankfurter sausages and green sauce, the stock exchange and the book fair and, of course, the imposing skyline. However, the ‘world’s smallest metropolis’ also offers much more. This city combines a metropolitan profile with idyllic features and a distinctive lifestyle. The attractiveness of the city is reflected in key retail and tourism indices. The centrality indices of Frankfurt (111) indicates the above-average attractiveness of its retail location and reflects the strong influx of purchasing power from the surrounding areas. While the city’s above-average purchasing power contributes to strong retail demand, its cultural and recreational offerings also have a strong appeal.

The most important prime locations are concentrated in the city centre, above all such top locations as Zeil, Grosse Bockenheimer Strasse and Goethestrasse. The attractive mix ranges from consumption-oriented, highly frequented shopping areas to chic luxury streets. The consumer-oriented stores are concentrated to the east of the city centre, with the higher quality locations found primarily towards the west. With more than 4.8m visitors, Frankfurt set another record in terms of tourist numbers in 2014.

Continued population growth in the City on the Main

The population threshold of 700,000 was exceeded in 2012 and population growth continued in 2014. Around 9% more people live in the city than five years ago. There are large development zones, e.g. the Am Riedberg area (8 kilometres north-west of Frankfurt‘s city centre), which has attracted not only more than 8,800 residents to date, but also Goethe-University’s natural science faculties and numerous research institutes in Science City. The main driver of population growth is the high level of inward migration. In 2013, some 63,300 moved to the city and just 52,700 moved away. The Federal Institute for Research on Building, Urban Affairs and Spatial Development (BBSR) residential market forecast estimates that by 2025 the city of Frankfurt will require some 3,300 new apartments every year to be able to provide sufficient residential space for its growing population. While, as in other major German cities, Frankfurt’s rental history shows that rents have not always been rising, the upwards spiral in rents has been continuing for nine years now, reaching €12.35 per sqm in 2014 (average asking price for apartments). One of the reasons for this rapid development is attributed to the attractiveness of city life.

Office demand highly concentrated on financial business

Frankfurt is the German centre of the banking and finance industry and competes with other global financial centres like London and Paris. Several hundred national and international banks in addition to many (financial service) advisors shape the office market. Consequently, Frankfurt has the highest share of office employment (43%) of all “Big 7x” German real estate strongholds; a total of about 290,000 work in offices and on a long-term average banks, financial and business services account for around half of total demand. The Frankfurt office market is the most volatile market in Germany but could offer on the other hand the most opportunities. The market consists of an office stock of around 12m sqm. The Frankfurt office market traditionally has the highest prime rents and the only established high-rise office market in Germany. The market structure is characterised by a concentrated prime banking district. Together with the other two sub-markets City and Westend the highest share of demand is concentrated here.

Logistics – in the heart of Germany

Thanks to its central geographic location, the Frankfurt/Rhine-Main region is probably the most accessible region in the whole of Germany and Europe. It is home to the Rhine-Main Airport, the largest airport in continental Europe, and has the junction of the A3 and A5 motorways, the two main north-south links, at its centre. This unique infrastructure underpins the economic potential of the entire region. As an industrial location, the Frankfurt/Rhine-Main region has the second highest density of industrial companies behind the Ruhr area. The most important industrial sectors are the chemical/pharmaceutical industry, the automotive industry and the logistics sector. The airport is the main driver for the logistics market and several airfreight related companies are located in the airport area. Therefore rents for logistics space are generally more expensive compared to other logistic sub-markets in the region.

30 | JLL • Investing in Germany • October 2015

City Focus: HamburgA gateway to the world

With 1.8 million inhabitants, Hamburg is the second largest city in Germany after Berlin. The wider metropolitan region comprises over five million inhabitants with approximately 300,000 commuters to Hamburg. Hamburg is a growing city with a forecasted population growth until 2030 of around 3.5%.

Hamburg is known as a gateway to the world, because of its port, which is one of the most important harbours in Europe. However this reputation also comes from the city’s concentration of foreign trade professionals and internationally oriented service providers, such as bankers, insurers, logisticians, media experts and legal and tax consultants. Hamburg always achieves top positions in location rankings and is peforms equally well in

terms of high quality of life. The largest companies are: Airbus, Lufthansa, Asklepios Kliniken, Beiersdorf, Hamburger Hochbahn and Otto Group.

Many of the companies in Hamburg are involved in foreign trade as import and export traders, several of them as subsidiaries of foreign parent companies, reinforcing Hamburg’s role as a hub for external trade mainly with the Baltic Sea region and China. In addition to this, around 100 consulates are based here, as well as the International Tribunal for the Law of the Sea. The inner city is growing and offers space for working, living and retail. The HafenCity is Europe’s largest inner-city development project: a completely new urban district on an area of 157 hectares.

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

32 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 33

A retail metropolis for the North

Hamburg is an attractive retail location and because of its polycentric structure the city offers various interesting shopping areas. The core retail areas are located in the city centre with more than 320,000 sqm of retail space Jungfernstieg, Neuer Wall, Spitalerstraße and Mönckebergstraße – these streets are some of the best known retail spots in Germany. But there are also several district locations that offer a full range of retail goods. Hamburg’s city centre is a very attractive shopping destination and has considerable tourist appeal. An extensive variety of goods attracts consumers to the city centre, but several other quarters in Hamburg’s city districts also offer amazing shopping facilities. Hamburg’s centrality index and purchasing power rankings are both well above the German average.

High demand for apartments

Approximately one seventh of Hamburg’s urban area consists of green recreation space. Hamburg’s high quality of life is based on residential estates that are close to green recreational areas and centrally located within the city limits. A low population density and a varied cultural offering combine to offer an appealing lifestyle.

Hamburg City Council estimates the population will have grown to 1.9 million inhabitants by 2030. The proportion of inward migration from abroad into Hamburg has again increased significantly and accounts for around one third of all arrivals. This is due to Hamburg’s relatively sound economic performance, which appeals in particular to workers from Eastern and Southern Europe.

Depending on location, rents for new-build apartments in Hamburg range between €10.50 and €15.00 per sqm and on average €13.20 per sqm. Due to the high demand for apartments, the Hamburg rental market has experienced the strongest uplift of all major German cities since 2007. Since the first half of 2010, rents have risen by almost 50%, which equates to an average rise of 8% p.a. The increasing number of new-builds is still too low to have a noticeable effect on rents, and the rise in demand has not diminished in recent years. It is more likely to be the result of restrictions in spending by an increasing number of households who are no longer prepared to accept rents at any price.

Many different service sector companies drive the office market

Hamburg has high economic diversity. Major clusters are the maritime economy, aviation, and life sciences. But the service sector also plays a relatively important role in Hamburg. Hamburg is the leading media location and a major banking location in Germany. Hamburg has a total office stock of around 14.7m sqm and is therefore the largest after Berlin and Munich. In comparison with the other major German office markets, Hamburg has a traditional low vacancy rate, relatively stable demand (due to the economic diversity) and moderate levels of rent. The balanced business mix has a major impact on the office market. In no other German city is office demand distributed across so many different sectors, with this mix creating market stability.

A centre for the logistics sector

The logistics market benefits from Hamburg’s advantageous geographic location– the North Sea and Baltic Sea are both nearby. Excellent infrastructure is the basis for Hamburg’s role as a trade hub where the flow of goods, especially from the Nordic countries as well as from Asia and the Baltic states, pass through. Hamburg’s harbour is the second biggest seaport in Europe after Rotterdam. Space for warehousing and logistics is in high demand, but supply is very limited.

Hamburg is the second largest city in Germany and centred around one of the most important deep water ports in Europe.

34 | JLL • Investing in Germany • October 2015

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

City Focus: MunichMixture of strong economy and a high quality of life

With 1.5 million inhabitants, Munich is Germany’s third largest city after Berlin and Hamburg. Munich is a growing city. With a forecast population growth until 2025 of 3%, it will be one of the highest growth cities in Germany. The wider metropolitan region comprises 5.5 million inhabitants. Munich is also the city with the lowest unemployment rate (below 5%) and the highest purchasing power in comparison to all other major cities in Germany. The strong mixture of companies of different sizes and varied industries is very important for the economy in Munich. The city is also the number one insurance location in Germany. Other important industries are services, the automobile industry, science, medicine, environmental science and communication-technology.

Munich is in a top position in location rankings, acts acts as a hub for knowledge and offers a high quality of life. The largest companies are: BMW, Bosch, Siemens, MAN and EADS.

Munich’s central location at the southern end of Germany means it is very close to Central, South and Eastern Europe and to the high-performing regions of Austria, Italy and Switzerland.

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

36 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 37

Munich claims the highest rents and multipliers in Germany, ranking among the most important European metropolitan centres.

Munich’s prime retail locations

Munich is a unique city offering a high quality of life. Its highly attractive location is characterised by its proximity to the Alps and the short distance to Italy. The local market for retail property is unique, too. Munich claims the highest rents and multipliers in Germany and also ranks among the most important European metropolitan centres. Investors and retailers constantly compete for the best investment opportunities and shop locations. Prime rents in top locations have recently risen to 360 €/sqm/month, which is the highest in Germany. The prime streets – Kaufingerstrasse and Neuhauser Strasse, Theatinerstrasse, Weinstrasse and Residenzstrasse – are among Germany’s most popular shopping streets. In addition, the Maximilianstrasse is one of Germany’s most prominent luxury shopping miles. In summary, the city centre of Munich has a total retail space of around 450,000 sqm, offering a good balance between prime downtown locations and off-centre borough shopping locations.

Munich – a young and growing city

The Bavarian state capital and Germany’s third largest city, Munich continues to boom. With a population of around 1.5 million inhabitants, there are today almost 8.5% more people living in the city than there were in 2010. Within this five-year period the population has grown by a further 120,000 inhabitants. The reason for this development is the continued positive migration balance in Munich. In the last decade, the influx had reached an average of 10,000 people p.a. but over recent years the migration rate has exceeded up to three times this level. Many of the new arrivals are of an age to start a family, the influx is also creating a significant growth trend in terms of natural population growth, with a rising birth rate and declining mortality. This explains why the city on the Isar is comparatively youthful. The average age is 41.5 years, in comparison the national average is 44.2 years. The population forecast for Munich is 1.7 million inhabitants by 2030, and Munich has the highest population density of all major German cities. Additionally, in the future high volume housing construction will take place. Looking at the city as a whole, average asking rents rose to their current level of almost 16.00 €/sqm. The highest prices were achieved in the southern part of Munich city centre around Lehel and in the historic city centre, as well as in the northeast of the city along the river Isar.

Diversified office market

The office market in Munich is the largest in Germany (20m sqm office stock) and has the highest take up volumes (on average) compared with the other main German office markets. Munich is Germany‘s most important location for the IT and biotech sector with above-average levels of innovation. It has a diversified economic structure and a mixture of large international-oriented and medium-sized companies. Munich is the HQ-Location for six DAX-Companies and for many IT and insurance companies, and is Germany’s leading education and research location. Thanks to this diversity and, according to long-term observation, three quarters of the take-up volume are attributable to eight business sectors. Over the last five years, office employment has grown by 10%; the highest growth rate among the seven major office locations in Germany.

Platform for transport to North & South Europe

The logistic region consists of the city of Munich and the surrounding agglomeration area. As the south-east logistic region of Germany, it is an attractive location for warehouses, retail oriented companies, local industry and other major clusters. An excellent infrastructure with several motorway and railway connections is the basis for Munich’s role as a trade reloading point to both northern and nouthern Europe.

38 | JLL • Investing in Germany • October 2015

Retail High Streets with Key Data (€/sqm/month) % is percentage of chain stores in each location

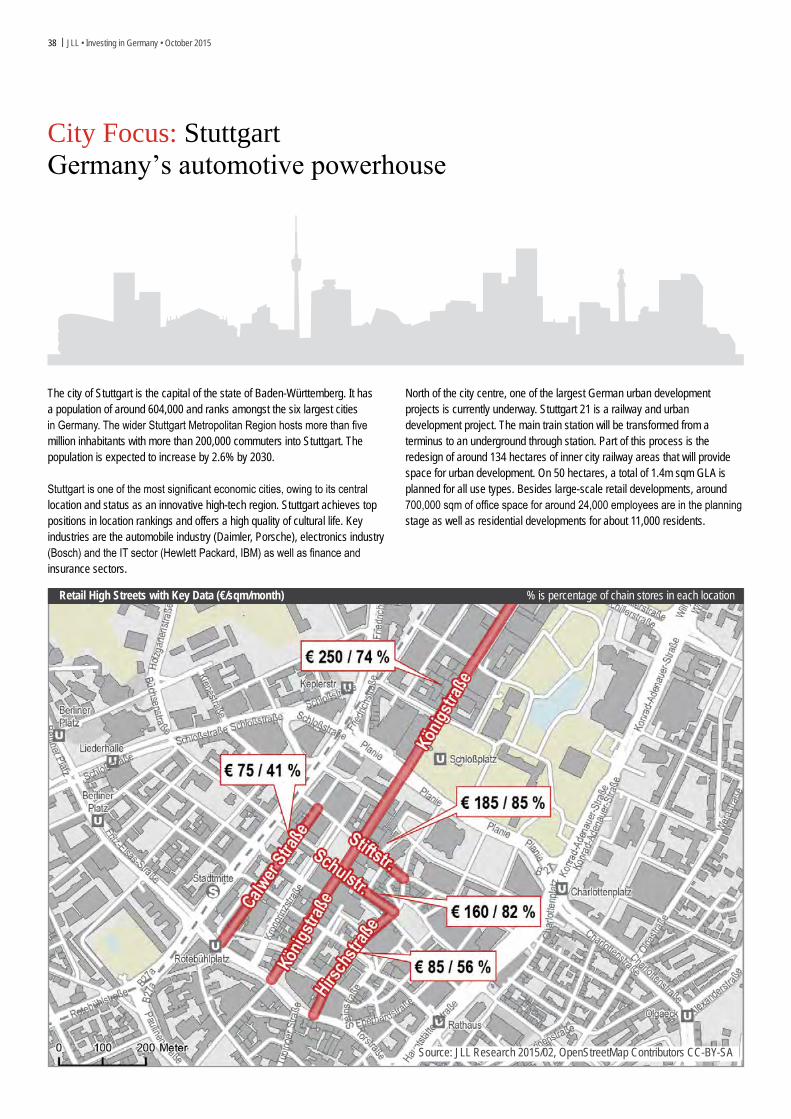

City Focus: StuttgartGermanyʼs automotive powerhouse

The city of Stuttgart is the capital of the state of Baden-Württemberg. It has a population of around 604,000 and ranks amongst the six largest cities in Germany. The wider Stuttgart Metropolitan Region hosts more than five million inhabitants with more than 200,000 commuters into Stuttgart. The population is expected to increase by 2.6% by 2030.

Stuttgart is one of the most significant economic cities, owing to its central location and status as an innovative high-tech region. Stuttgart achieves top positions in location rankings and offers a high quality of cultural life. Key industries are the automobile industry (Daimler, Porsche), electronics industry (Bosch) and the IT sector (Hewlett Packard, IBM) as well as finance and insurance sectors.

North of the city centre, one of the largest German urban development projects is currently underway. Stuttgart 21 is a railway and urban development project. The main train station will be transformed from a terminus to an underground through station. Part of this process is the redesign of around 134 hectares of inner city railway areas that will provide space for urban development. On 50 hectares, a total of 1.4m sqm GLA is planned for all use types. Besides large-scale retail developments, around 700,000 sqm of office space for around 24,000 employees are in the planning stage as well as residential developments for about 11,000 residents.

Source: JLL Research 2015/02, OpenStreetMap Contributors CC-BY-SA

40 | JLL • Investing in Germany • October 2015

Source: JLL Research 2015/02

Office Space Market Areas with Rental Bands (€/sqm/month)

JLL • Investing in Germany • October 2015 | 41

Stuttgart is one of the most significant economic cities because of its central location and is called a significant, innovative high-tech region in Europe.

Sustained population growth

Population development in Stuttgart has stayed positive with a growth of 0.7% over the last five years, in contrast to the population decrease throughout Germany. Similar to other major cities, population growth is closely linked to the economic situation, which generates influx via the creation of new jobs. The global interdependence of the Stuttgart economy has a direct effect on residential market demand. An above-average proportion of the new arrivals are single person households. In the future, the proportion of large households with three or more people will reduce further and the proportion of single and two-person households will increase, and therefore demand for small apartments will continue to rise. However, the trend for family apartments in the city is evident in the residential market due to the high birth rates in the city centre districts.

Stable Office Market Conditions

Strong economic growth in the past years has been the main driver of the demand for office space. Although plenty of new-built offices have been completed, they have been unable to satisfy the high demand. In particular, the city centre lacks large-scale contiguous office space, leading to an increase in prime rents of about 3% in the past 12 months. Stuttgart is a strong office-market with low volatility in prime rents and has the lowest vacancy rate among the seven most important office markets in Germany.

Stuttgart as a hot spot for international retailers

Stuttgart is an attractive retail location enjoying high demand from national and international retailers. The city structure offers various interesting shopping areas. The core retail areas are located in the city centre. Königsstraße, Calwer Straße, Hirschstraße and Stiftstraße are the best known retail spots in Stuttgart. With the Gerber and Milaneo shopping centres, the city centre of Stuttgart has benefited from two more major retail hotspots. Centrality index and purchasing power in Stuttgart are significantly above the German average.

A centre for the industrial sector

The Stuttgart industrial and logistics market comprises the cities Stuttgart and Heilbronn as well as the administrative districts Ludwigsburg, Böblingen, Esslingen, Göppingen, Heilbronn and Rems-Murr-Kreis. With 155,000 companies, it is the top-selling industrial-region in Germany and one of the most successful in Europe. The most important industries for industrial space demand in the metropolitan region are automotive, manufacturing and electrical engineering. Excellent infrastructure is the basis for Stuttgart’s role as a trade hub. Large ongoing investments are made in the region to maintain and improve the train and motorway infrastructure.

42 | JLL • Investing in Germany • October 2015

Contacts

Timo TschammlerInternational DirectorManagement Board Germany, Office and Industrialtel +49 69 2003 [email protected]

Marcus LuetgeringInternational DirectorHead of Office Investment Germanytel +49 89 290088 158 [email protected]

Joerg RitterInternational DirectorManagement Board Germany, Retailtel +49 69 2003 [email protected]

Willi WeisNational DirectorHead of Industrial Investment Germanytel +49 69 2003 [email protected]

Marin MarinovNational DirectorTeam Leader Acquisition Services Germanytel +49 69 2003 [email protected]

Dr. Konstantin KortmannNational DirectorTeam Leader Residential Investment Germanytel +49 69 2003 [email protected]

Fraser BowenRegional DirectorEMEA Capital Marketstel +44 207 399 [email protected]

Helge ScheunemannNational DirectorHead of Research Germanytel +49 40 350011 [email protected]

Steve CollinsInternational Director (Washington DC)International Capital Group (Americas)tel +1 202 7195 [email protected]

Alistair MeadowsInternational Director (Singapore)International Capital Group (Asia Pacific)tel +65 6494 [email protected]

Fadi Moussalli Regional Director (Dubai),International Capital Group (Middle East and North Africa)tel +971 50 425 [email protected]

Matthew RichardsInternational DirectorInternational Capital Group (Europe)tel +44 207 399 [email protected]

JLL • Investing in Germany • October 2015 | 43

Dr. David ElshorstPartnerReal Estatetel +49 69 7199 [email protected]

Dr. Christian KeilichPartnerReal Estatetel +49 69 7199 [email protected]

Dr. Gerold M. JaegerPartnerReal Estatetel +49 69 7199 [email protected]

Stefan LöchnerPartnerReal Estatetel +49 69 7199 [email protected]

Thorsten SauerheringPartnerTaxtel +49 69 7199 [email protected]

Thomas ReischauerPartnerReal Estatetel +49 69 7199 [email protected]

Cornelia ThalerPartnerReal Estatetel +49 69 7199 [email protected]

Reinhard Scheer-Hennings, M.C.J.PartnerReal Estatetel +49 211 4355 [email protected]

Christian Trenkel, Maître en droitPartnerReal Estatetel +49 89 21632 [email protected]

Copyright © JONES LANG LASALLE GmbH, 2015.

No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle GmbH. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.

In cooperation with