investigating how the steel industry uses the lme to tackle · pdf file ·...

TRANSCRIPT

Robert Fig Senior Business Development Executive

October 2014

Investigating how the steel industry uses

the LME to tackle price volatility Platts 4th Annual Steel Supply Chain Conference

1

Product development:

Reacting to market demand

2

Steel – why is this an important market?

Market size • Huge market potential largely untapped – c.17x larger than the non-ferrous

industry

Risk management • While some of the steel industry hedge risks for currency, energy, base metals,

emissions and shipping, it may be loathe to hedge steel prices

Transparent pricing • Consumers look for transparent pricing which can be provided by the LME

Few steel products • Few steel products on exchange currently available.

The most recyclable and versatile of all metals – widely-used in the physical market

Widely used in the automotive, construction, white goods, ship building and infrastructure industries Use

Non-ferrous market

Approximately 92 million metric tonnes produced per

year

Ferrous market

Approximately 1.6 billion metric tonnes produced per

year

Market potential

Why LME steel contracts?

Associated industry

Future potential to venture into other related markets

(e.g. minor metals, chemicals)

Source: World Steel Association 2012 world production figures

3

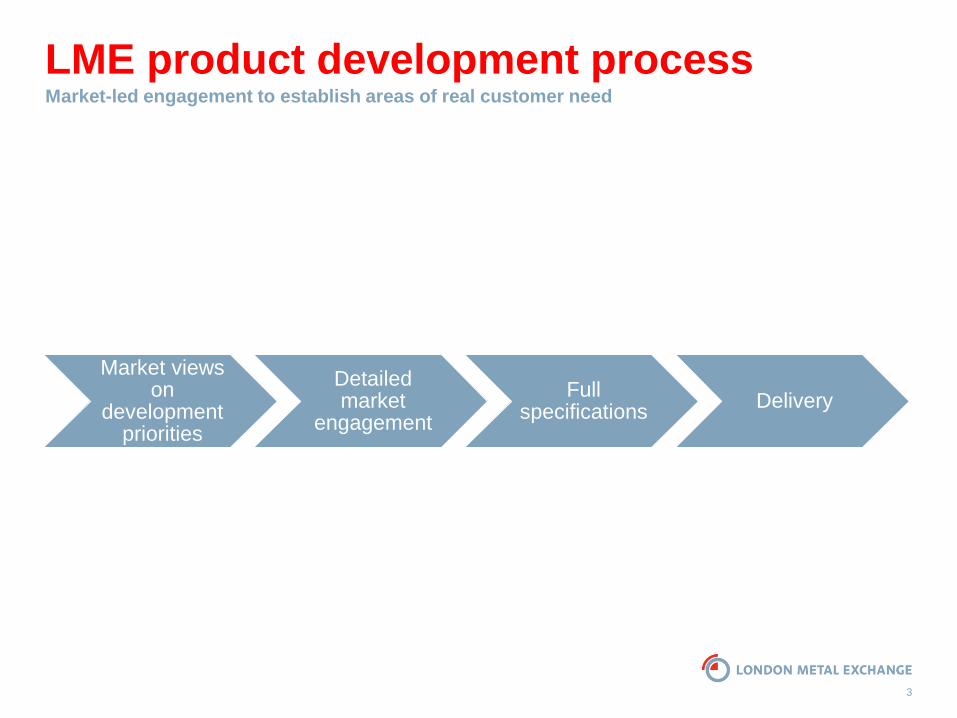

LME product development process Market-led engagement to establish areas of real customer need

Market views on

development priorities

Detailed market

engagement

Full specifications

Delivery

4

Current LME Support to Steel

Industry

5

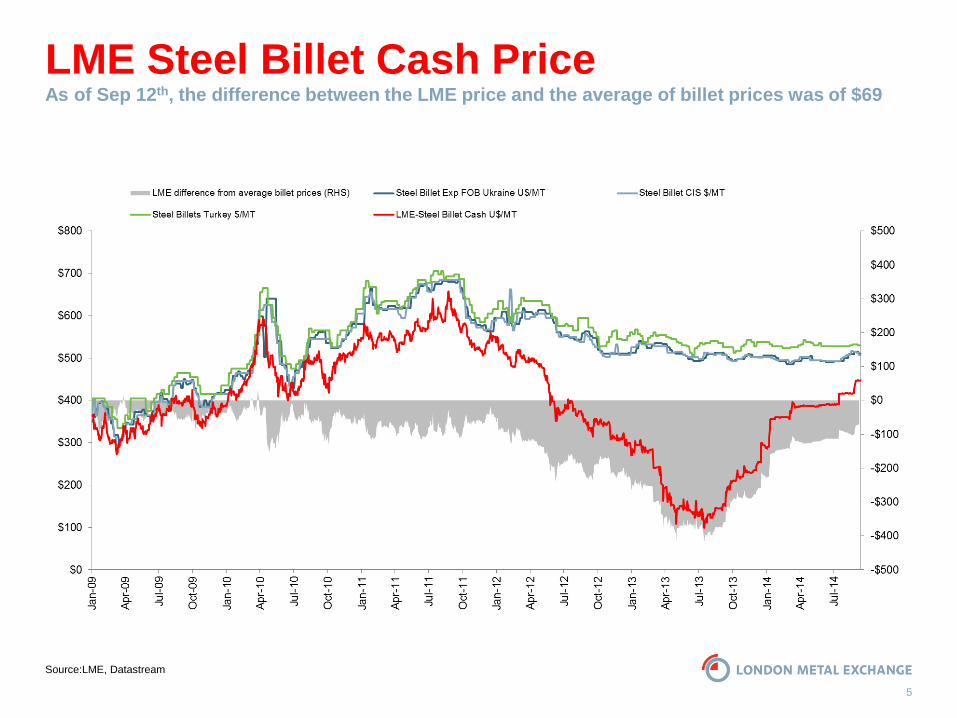

LME Steel Billet Cash Price As of Sep 12th, the difference between the LME price and the average of billet prices was of $69

Source:LME, Datastream

6

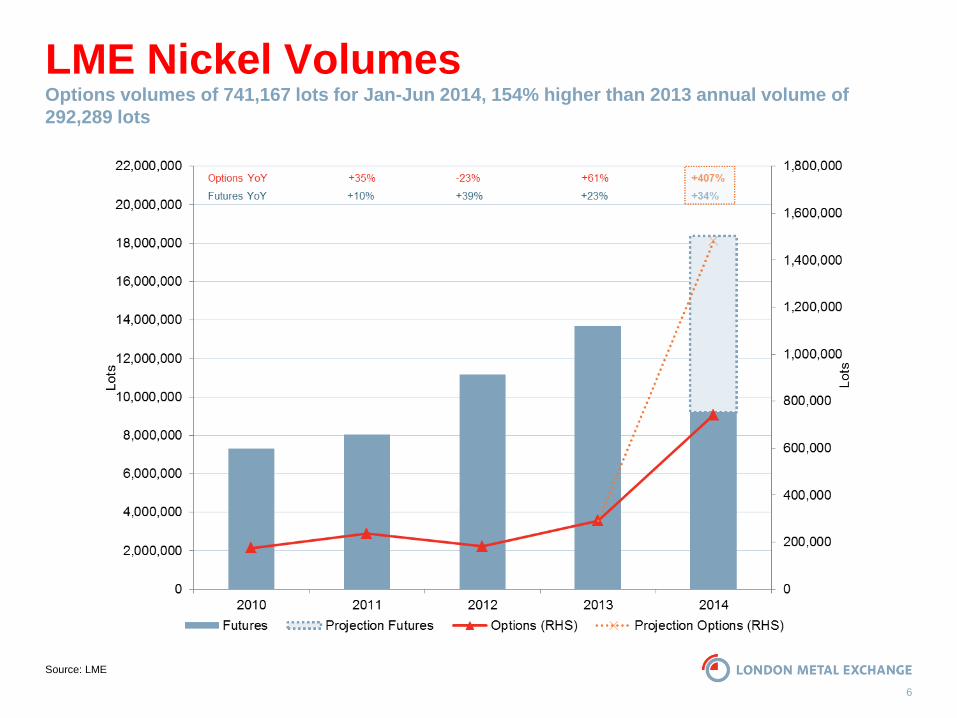

LME Nickel Volumes Options volumes of 741,167 lots for Jan-Jun 2014, 154% higher than 2013 annual volume of

292,289 lots

Source: LME

7

LME Zinc Volumes

Source: LME

8

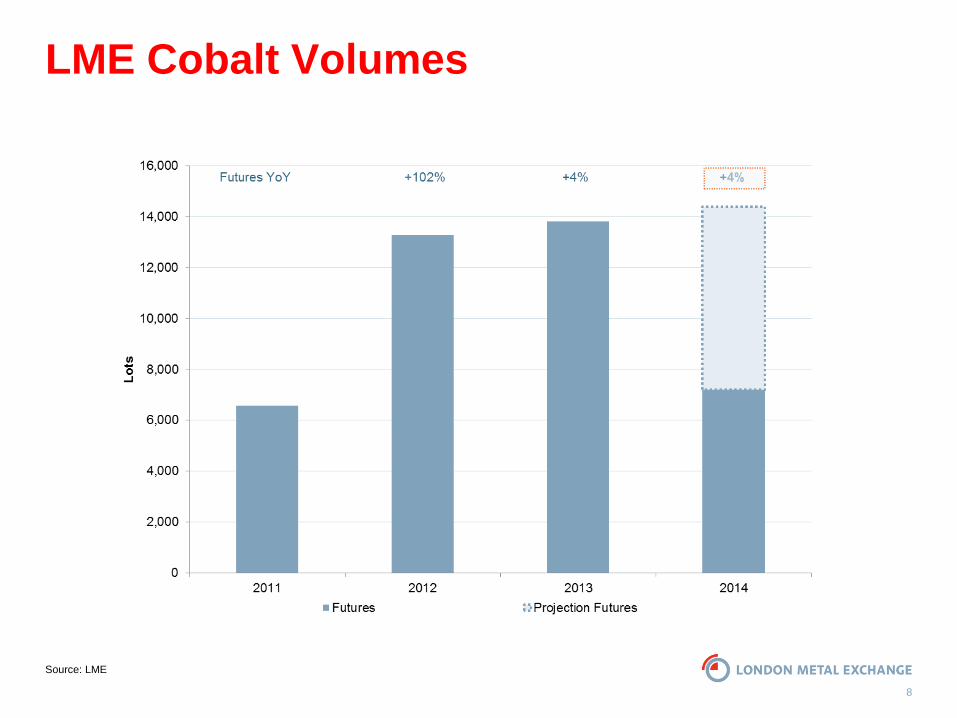

LME Cobalt Volumes

Source: LME

9

Where to now?

10

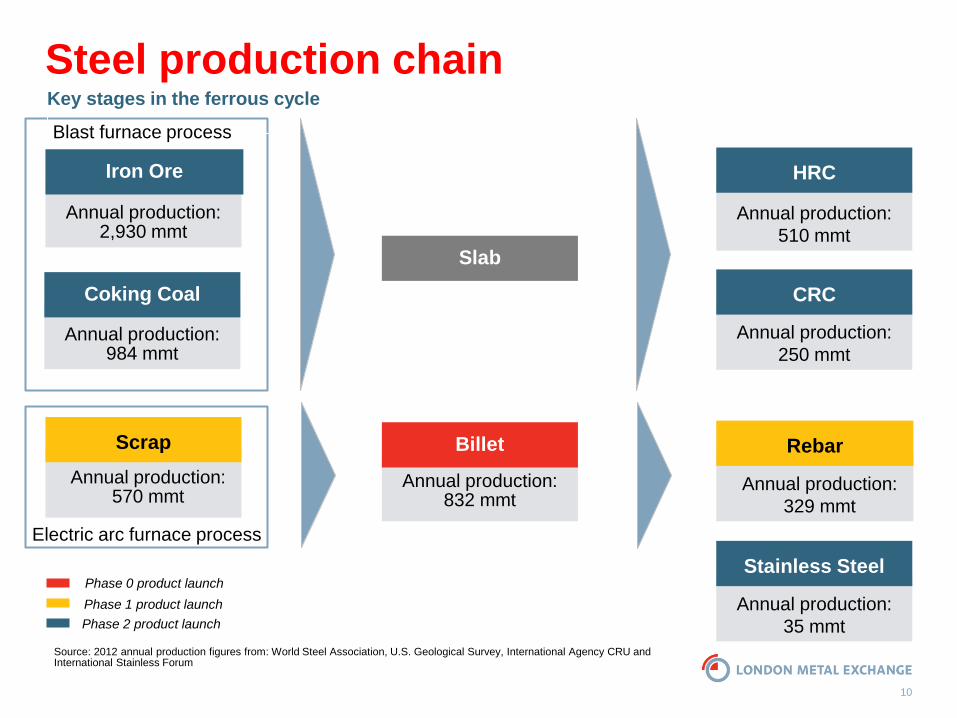

Annual production:

329 mmt

Annual production:

250 mmt

Annual production:

510 mmt

Annual production:

35 mmt

Annual production: 832 mmt

Annual production:

984 mmt

Steel production chain Key stages in the ferrous cycle

Annual production:

2,930 mmt

Iron Ore

Source: 2012 annual production figures from: World Steel Association, U.S. Geological Survey, International Agency CRU and International Stainless Forum

Billet

Coking Coal

HRC

CRC

Rebar

Stainless Steel Phase 0 product launch

Phase 1 product launch

Phase 2 product launch

Annual production: 570 mmt

Scrap

Slab

Blast furnace process

Electric arc furnace process

11

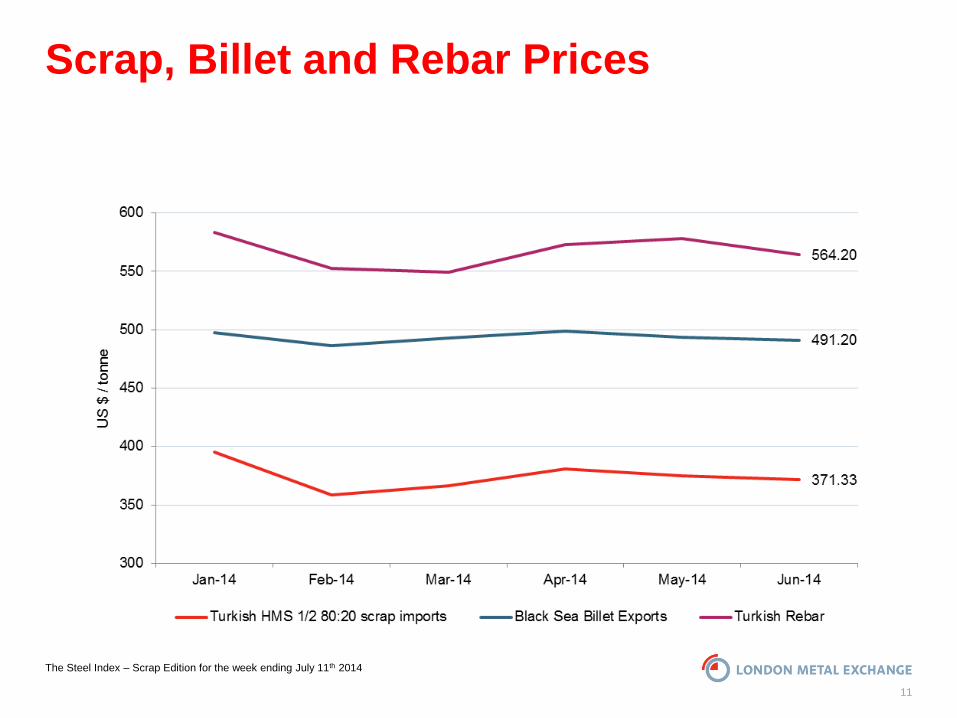

Scrap, Billet and Rebar Prices

The Steel Index – Scrap Edition for the week ending July 11th 2014

12

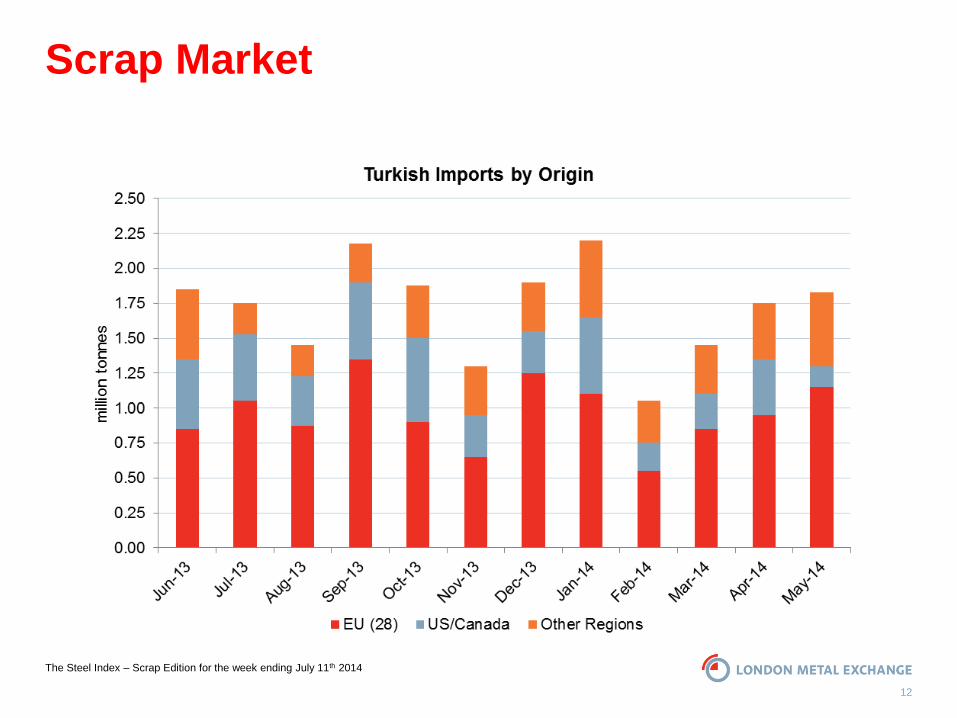

Scrap Market

The Steel Index – Scrap Edition for the week ending July 11th 2014

13

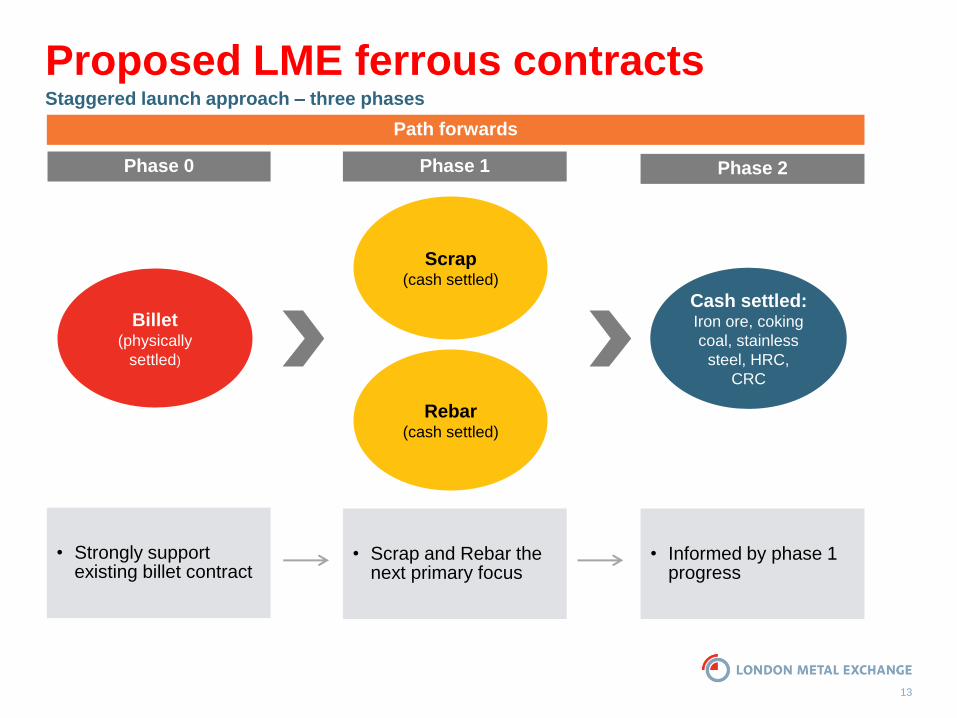

Proposed LME ferrous contracts Staggered launch approach – three phases

Phase 0

• Strongly support existing billet contract

• Scrap and Rebar the next primary focus

• Informed by phase 1 progress

Phase 1 Phase 2

Billet

(physically

settled)

Scrap

(cash settled)

Rebar (cash settled)

Cash settled: Iron ore, coking

coal, stainless

steel, HRC,

CRC

Path forwards

14

Total commitment to a market-led solution Supporting the steel industry

Reacting to clear demand from

underlying participants

Enabling involvement of

active participants

Best-in-class compliance

Developing London as a global steel trading

centre

15

Speculation

Complicated

Pressure off sourcing

Liquidity

Shareholder exposure

Cost

Pricing not hedging

Creating hedging team

What stops companies hedging?