invest in yourself • savvy savers • credit • focus on finance

TRANSCRIPT

• Invest in Yourself• Savvy Savers• Credit• Focus on Finance

Invest In Yourself

2@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

Lesson Description

Students are divided into groups to produce name tents. Each of four groups in the classroom produce name tents in a different way to highlight different levels of human capital. They identify ways in which people invest in their human capital. Students analyze unemployment, educational attainment, and median weekly income data for 2011. They work with a partner to analyze the data and write sentences to describe relationships among the variables. As an assessment, students create graphs or charts to illustrate the unemployment, educational attainment and income data. They also use the Occupational Outlook Handbook to identify a possible career and the type of investments in human capital required to obtain that occupation.

Concepts

Human capitalInvestment in human capital

Objectives

Students will:

■■ Define human capital and investment in human capital.

■■ Give examples of investment in human capital.

■■ Describe the relationship between a person’s level of education and income- earning potential.

■■ Describe the relationship between educational attainment and percent unemployment.

Common Core Standards

Grades 6-12 Literacy in History/Social Studies & Technical SubjectsEnglish Language Arts Standards, History/Social Studies, Grades 6-8 and 9-12

■■ Craft and Structure

■■ Integration of Knowledge and Ideas

■■ Craft and Structure

Content Standards

National Standards in Personal Financial Literacy

■■ Standard 1: Earning Income

National Standards in Economics

■■ Standard 13: Income

■■ Standard 15: Economic Growth

3@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

Time Required

45 minutes

Materials

■■ One sheet of chart paper for each pair of students

■■ Two sheets of light-colored construction paper per student plus one sheet for the teacher

■■ One dark-colored marker per student

■■ One copy of Handout 1 for each student

■■ One sheet of chart paper for each pair of students

Procedures

1. Tell students that they will create name tents for display on their desks for the day.

2. Demonstrate how to produce a name tent as follows.

• Fold the piece of construction paper in half, shorter edges (8“) together.

• Crease the center fold. The folded paper should measure 8“ x 5.5“.

• Open the paper to 8“ x 11”.

• Fold the bottom 8” edge to the middle crease. Crease the fold.

• Open the paper to 8“ x 11”.

• Fold the top 8” edge to the middle crease. Crease the fold.

• The paper should now have four sections each measuring approximately 2.75” x 8”.

• Starting from one end of the paper, count down three rectangles. Print your first name in large letters in the rectangle.

• Turn the paper upside-down. Again count down three rectangles and print your first name in large letters in the rectangle.

• Fold the paper to create a tent with the name displayed on both sides.

3. Divide the students into four groups. Explain that each group will have different rules for folding name tents. Describe the rules for each group as follows.

• Group 1: Each of you will remain seated to produce your own name tent, using only one hand, your nondominant hand—that is, the hand with which you do not write—to produce the name tent. You must keep your dominant hand behind your back.

4@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

• Group 2: Each of you will remain seated to produce your own name tent, using only one hand, your dominant hand—that is, the hand with which you write—to produce the name tent. You must keep your nondominant hand behind your back.

• Group 3: Each of you will remain seated to produce your own name tent, using both hands.

• Group 4: Each of you will produce your own name tent while standing and using only one hand—the nondominant hand—to produce the name tent. You must keep your dominant hand behind your back. You may not use the desk, table or chair.

• None of the groups may begin producing name tents until the class is told to begin.

• When each student finishes folding his or her name tent, he or she should raise a hand.

• Students will be timed and will have a maximum of two minutes to make the name tent.

4. Draw the following table on the board and use this to tally students who raise their hands upon completing the name tent.

Time Group 1 Group 2 Group 3 Group 4

30 seconds

60 seconds

90 seconds

120 seconds

5. Distribute a piece of construction paper to each student. Remind them that students in each group must fold name tents according to the rules described and that they are to raise their hands individually when they have finished their name tents. Tell students they may begin. As students raise their hands, record tallies on the board next to the appropriate group number and time segment. If students raise their hands at a time beyond 30 seconds, place the tally mark in the 60- seconds row. If they raise their hand beyond 60 seconds, place the tally mark in the 90-seconds row and so on.

6. After two minutes, ask everyone to stop producing name tents and discuss the following:

• Did any students find it very difficult to produce name tents? (students in Group 4) Why? (Standing and folding with one hand—the nondominant hand—made it nearly impossible.)

5@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

• Ask students in each group what difficulties they encountered making the name tents? (Group 1: hard to fold with one hand, very hard to fold using only nondominant hand, difficult to write with nondominant hand; Group 2: hard to fold with one hand; Group 3: few difficulties; Group 4: hard to fold with one hand, very hard to fold with nondominant hand, very, very hard to fold stand-ing up and difficult to write with nondominant hand)

• In general, which group of students finished most quickly? (Group 3) Why? (Students in this group were able to use both hands and were able to remain seated.)

• In general, which group of students took the longest time to finish? (Group 4) Why? (Students in this group had to use only the nondominant hand and had to stand.)

7. Explain that this activity can be used to introduce the concept of human capital. Human capital is the knowledge, talent, experience, and skills that people pos-sess. Point out that people are able to invest in their human capital by going to school,pursuing additional training and developing skills.

8. Explain that the process of managing income includes saving and investing for the future. An important investment that students make in their future is their investment in human capital—their efforts to acquire and improve their knowledge, talent, experience, and skills.

9. Ask the students how finishing name tents more quickly and producing name tents that are of higher quality might relate to investment in human capital. (Answers will vary, but students might recognize that people with more skills, education and train-ing tend to be more productive.)

10. Explain that people with more skills, education and training tend to be more pro-ductive, and, as a result, earn higher incomes. In the name tent activity, Group 4 represents those with the smallest investment in human capital—high school drop-outs. Thus, they are constrained the most in completing the task representing the reduced amount of education and skills. Group 1 represents those who graduate from high school. Group 2 represents those who pursue additional training follow-ing high school—associate’s degrees, bachelor’s degrees or trade school. Group 3 represents those who pursue advanced degrees. They had the fewest constraints in pursuing the task to represent having more skills and education.

11. Explain that people develop human capital throughout life. Learning to read and compute are examples. Discuss the following and record student examples on the board:

• Give examples of the human capital you possess—that is, the skills, talents and education that you have now. (read, write, compute, play piano, play chess, draw, use various woodworking tools, ability to use a computer, ability to work with others, and so on)

6@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

• What investments did/do you make to develop and maintain this human capi-tal? (practiced reading, completed math homework, practiced piano, joined the chess club, attended a special art class, attended a computer class, made furniture and other wood items, and so on)

• If you want to own your own business in the future, what human capital might you need? (management skills, accounting skills, computer skills, communica-tion skills, etc.)

• What investments might you make to develop this human capital? (pursue a college degree in business or accounting, read professional journals, shadow someone who owns a business, etc.)

12. Distribute a copy of Handout 1: Educational Attainment, Income and Unemploy-ment Data to each student. Ask students to work in pairs. Each pair should write two sentences—one describing the relationship between median income and edu-cational attainment. The other sentence should describe the relationship between unemployment and educational attainment. Ask pairs of students to share their statements. (Answers might include: There is a direct relationship between edu-cational attainment and income. The more education people acquire, the higher their weekly income. There is an indirect relationship between unemployment and educational attainment. The higher the level of educational attainment the lower the percent of unemployment.)

13. Using a computer and projector, display the Occupational Outlook Handbook at www.bls.gov/ooh/. (Note: If computers are available have pairs of students look up the OOH.)

14. Point out that due to a variety of supply and demand factors, the type of post-sec-ondary education you pursue matters as well. Some types of degrees or programs may make it easier for someone to find a job and may translate to higher salaries. For example, engineers are likely to earn high salaries and find employment more readily than some others. Those who pursue training as plumbers and electricians may also find work more easily and may earn higher incomes. Ask the students for evidence of this from the Occupational Outlook Handbook.

15. Point out that the income data are given as median income rather than average or

mean income. Discuss the following:

• What is the difference between median and mean? (Students should explain that mean is an average. All terms are added and the sum is divided by the number of terms. Median is the middle number. It is found by placing the terms on a scale from lowest value to highest value, then finding the middle value.)

• Why does it matter? (Average income can be skewed by one outlier number in a very dramatic way. The median income would not be dramatically affected by a single outlier number and is generally favored by economists when looking at groups of numbers, particularly income, where a small number of high earners can skew the number upward.) Note: Clarification is provided below.

7@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

- Assume that you were calculating the average and median incomes for full time students who have not graduated from high school yet and whose incomes are not very high and vary.

- Assume that there are seven students in the group with incomes ranging in $1,000 increments from $1,000 to $7,000. To calculate the average or mean you must add the income of all the people and divide by the number of people in the group. ($1,000 + $2,000 + $3,000 + $4,000 + $5,000 + $6,000 + $7,000) ÷ 7 = $4,000

- To find the median, you should put the numbers in order of value from lowest to highest and pick the middle number. $1,000, $2,000, $3,000, $4,000, $5,000, $6,000, $7,000

- In this case $4,000 is the middle number. In our example $4,000 is both the mean and median, so why should we care which number gets used? Let’s add one person to the group. A father of one of the students who is a doc-tor earning $150,000 per year.

- The calculation for average or mean income now looks like this: ($1,000 + $2,000 + $3,000 + $4,000 + $5,000 + $6,000 + $7,000 + 150,000) ÷ 8 = $22,250

- When we recalculate the average or mean, the average income of the group increased from $4,000 to $22,250. While the number is mathematically correct, it might seem misleading to say that the average income of people in the group is $22,250 because nearly everyone in the group earns far less than that amount.

- The calculation for median income looks like this: $1,000, $2,000, $3,000, $4,000, $5,000, $6,000, $7,000, $150,000

- To calculate the median when you have two middle numbers, you find the number half-way between them by adding them together and dividing by two. Here the median income is $4,500. The median income increased from $4,000 to $4,500. To say that the median income for this group is $4,500 seems to be a more accurate reflection of the people in the group than the mean.

16. Explain that part of the art of planning for your financial future includes making a strong investment in your own human capital. Learning about earning and manag-ing income is an investment in human capital.

17. Optional: Distribute new pieces of construction paper to students who were not able to complete their name tents or to students whose name tents were illegible.

8@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

Closure

18. Review the key points of this lesson by discussing the following:

• What is human capital? (the knowledge, talent, experience, and skills that people have)

• What is investment in human capital? (efforts to acquire and improve human capital)

• How do people invest in human capital? (education, training and practice)

• In general, how does investment in human capital—through education—affect income? (The more education, the greater income people earn.)

Assessment

19. Ask students to work with a partner to create a chart/graph that represents that data from Handout 1. Distribute chart paper and markers to each pair. Have pairs draw their chart or graph on the chart paper. Beneath the graph ask students to write an explanation of the importance of investment in human capital using the data in the table. Have pairs of students display their charts and share them with the class.

20. Have students review the Occupational Outlook Handbook at http://www.bls.gov/ooh/. Have them select an occupation in which they are interested, identify the human capital that they currently possess that would be important for this occupation (reading, mathematics, people skills, writing, etc.), and identify investments in human capital that they must make to attain this occupation (additional training and education, computer skills and so on).

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Invest In Yourself | Financial Fundamentals from the Fed

9

Handout 1: Unemployment Rate, Educational Attainment and Median Weekly Earnings in 2012

Directions: Working with a partner, write two sentences—one describing the relationship between median income and educational attainment. The other sentence should describe the relationship between the rate of unemployment and educational attainment.

Unemployment rate in 2012 (Percent) Educational attainment Median weekly earnings in

2012 (Dollars)

2.5 Doctoral degree $1,624

2.1 Professional degree 1,735

3.5 Master’s degree 1,300

4.5 Bachelor’s degree 1,056

6.2 Associate degree 785

7.7 Some college, no degree 727

8.3 High-school diploma 652

12.4 Less than a high school diploma 471

Note: Data are for persons age 25 and over. Earnings are for full-time wage and salary workers.

SOURCE: Bureau of Labor Statistics, Current Population Survey.

Savvy Savers

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

2

Lesson DescriptionStudents calculate compound interest to identify benefits of saving in interest-bearing accounts. They learn the “rule of 72” and apply it to both investments and debt. They learn that there is a relationship between the level of risk for an investment and the poten-tial reward or return on that investment.

Concepts Compound interestInterestNon-interest bearing accountPrincipalRisk-reward relationshipRule of 72Saving

ObjectivesStudents will:

■■ Explain the difference between a non-interest bearing account and an interest-bearing account.

■■ Calculate interest compounded semiannually.

■■ Explain and demonstrate the Rule of 72.

■■ Describe the risk-reward relationship.

Common Core StandardsGr. 6-12 English Language arts Standards, Literacy in History/Social Studies and Technical Studies

■■ Craft and Structure

■■ Integration of Knowledge and Ideas

■■ Craft and Structure

Content StandardsNational Standards in Personal Financial Literacy

Saving and Investing: Implement a diversified investment strategy that is compatible with personal goals.

■■ Standard 3: Saving

■■ Standard 5: Financial Investing

■■ Standard 4: Using Credit

National Standards in Economics

■■ Standard 12: Interest Rates

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

3

Time Required

45 minutes

Grade Level

9–12

Materials

■■ A copy of Handouts 5.1, 5.2 and 5.3 for each student

■■ Visuals of Handout 5.1—Answer Key, Handout 5.2—Answer Key and Handout 5.3—Answer Key

■■ A calculator for each student

Procedures

1. Begin by asking students the following:

• What does it mean to be a saver? (Answers may vary but may include not spending all of one’s income, having money left after paying expenses, income greater than expenses, etc.)

• What do you suppose it means to be a savvy saver? (Answers may vary but may include being a smart saver, knowing about places to save one’s money, knowing about different savings accounts, etc.)

2. Explain that saving is income not spent. Distribute Handout 1: Maria’s Saving Deci-sion to all students and explain that they may see the difference between a saver and a savvy saver when they examine Maria’s story. Call on a student to read aloud the first paragraph of Handout 1.

3. Explain the following:

• A non-interest bearing account, or zero-interest account, is one in which no interest is paid on the principal—that is, the amount of deposit or account balance.

• Interest is the price of using someone else’s money. When people place their money in a bank, the bank uses the money to make loans to others. In return, the bank pays the account holder interest. There are various types of interest-bearing accounts depending on the amount of interest and how often the interest is paid.

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

4

• Compound interest means that interest is computed on the sum of the origi-nal principal and any accrued (accumulated or earned) interest. For example, an account that pays 5 percent interest “compounded semiannually” means that every six months H of 5 percent, i.e., 2.5 percent, interest is paid on the princi-pal and any accrued interest.

4. Show students how to calculate 5 percent interest compounded semiannually by demonstrating the answers to problems #1 through #3 on Handout 1. (Refer to Handout 1: Maria’s Savings Decision—Answer Key for answers.)

5. Distribute a calculator to each student and instruct students to complete Handout 5.1 (problem #4) on their own.

6. Display a visual of Handout 1 and go over answer #4 on the handout. After review-ing all of the questions on Handout 1, ask students the following:

• What is a non-interest bearing account? (an account or deposit that does not pay interest on the principal)

• What could Maria have bought with the $50.63 of interest she might have earned on her savings? (Answers may vary.)

• Would you classify Maria as a saver or a savvy saver? (saver) Why? (She didn’t invest her money in a way that would give her a return on her investment, i.e. an account that pays interest on the principal.)

• Why would anyone leave the $1,000 in a non-interest bearing account rather than putting it in an interest-bearing account? (Answers may vary but may include that she was financially lazy—not proactive—or that she may not have understood the importance of compound interest.)

• How much interest would Maria have received had the money been deposited in an interest-bearing account for three years? ($1,159.71 - $1,000.00 = $159.71)

• Imagine that instead of $1,000, Maria’s grandmother had given her $10,000. After three years, how much interest would $10,000 have earned on a 5 per-cent compounded semiannually account? ($159.71 x 10 = $1,597.10)

• Why is time—i.e., the number of months you have your money in an interest-bearing account—a very important factor in accumulating savings? (Answers may vary but may include that the sooner you start saving, the sooner you start earning interest not only on your principal but also on accrued interest. Your money works for you over time.)

7. Ask students the following questions:

• How many of you would like for the amount of your savings to double over a period of years? (Answers may vary, but most students will likely want their amount of savings to double.)

• How long would it take for Maria’s $1,000 to double if she kept the money in a non-interest bearing account? (It would never double.)

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

5

• How long do you think it will take for Maria’s $1,000 to double if she puts the money in a savings account that pays compounded interest? (Answers will vary.)

8. Tell students that you are going to show them the Rule of 72, which is an easy way to estimate how long it will take their money to double at a certain interest rate. Tell students that in order to determine how long it will take their money to double at a certain interest rate, they should divide 72 by the interest rate. For example, 72 ÷ 5 = 14.4. Therefore the principal in a savings account that pays 5 percent interest will double in a little over 14 years. Explain that the Rule of 72 assumes people leave their money in an account without taking away from it or adding to it. It isn’t an exact number, but it’s close enough to serve as an estimate.

9. Distribute Handout 2: The Rule of 72 to all students and ask them to complete the handout by following the instructions.

10. When students have completed Handout 2, display a visual of Handout 2: The Rule of 72—Answer Key to review the answers. Discuss the following:

• Does the amount of interest an account pays have much of an impact on how long it will take for your money to double? (Yes.)

• Interest rates vary over time, but savings accounts are considered to be a safe way to save your money because for most savings accounts your principal is guaranteed. Interest rates for savings accounts generally pay in the 2 percent to 4 percent range, depending on current financial conditions in the economy. This reflects the risk-reward relationship.

• The risk-reward relationship is based on the concept that the higher the risk of loss of principal for an investment, the greater the potential reward of an increase in the principal or higher yield on the principal. And the lower the risk of loss of principal for an investment, the lower the potential reward of increased principal or higher yield on the principal. Therefore, savings accounts are considered very low risk; so, their reward, as compared with other invest-ment options, is a relatively low “yield,” or interest rate.

• The Rule of 72 applies not only to investments but also to debt, because it shows approximately how fast your debt will double at a certain rate of interest.

• What rate of interest do credit cards charge? (Answers will vary.)

• Credit card rates of interest vary over time and under different financial condi-tions in the economy, but generally credit cards charge a relatively high rate of interest. Credit cards can charge a high rate because the card companies bear a risk to loan funds to their cardholders.

• If a credit card charges an interest rate of 18 percent, approximately how long would it take for your debt to double if you made no payment on the debt? (4 years)

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

6

Closure

11. Review the key points of this lesson by discussing the following:

• What is a non-interest bearing account? (an account that pays zero interest on the principal)

• What is interest? (the price of using someone else’s money)

• What is compound interest? (Interest is paid on the principal and also on the accrued interest at specific time intervals.)

• What level of interest would you expect a safe account or investment that is low risk to pay—low, medium or high—and why? (low because of the risk-reward principal)

• What does the Rule of 72 indicate? (The rule shows how long it takes to double your money—or your debt—given a specified rate of interest.)

Assessment

12. Give each student a copy of Handout 3: Charlie’s Financial Goal and tell them to follow the instructions on the handout. Display a visual of Handout 3: Charlie’s Financial Goal—Answer Key to review student answers.

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

7

Handout 1: Maria’s Savings Decision

One year ago, Maria received $1,000 from her grandmother with instructions to save it for college two years from now. She deposited the money in her checking account for which she was paid no interest. She had considered putting the $1,000 in a savings account that paid 5 percent interest compounded semiannually, but she never got around to it. How much money did Maria lose by leaving her $1,000 in a non-interest bearing account for 12 months? Follow the steps below to find the answer.

1. Because the interest on the account is compounded semiannually, the interest is added to the principal every six months. Therefore, divide the annual amount of interest—5 percent—by two to determine interest paid at the end of each six-month period. Every six months, the saver would receive .025 (.05 ÷ 2) interest on the principal plus any accumu-lated interest. Multiply the principal (plus any accrued interest) by the interest rate. Round to the nearest hundredth. (For example, $25.625=$25.63.) Note that the principal will change each time interest accrues.

Months Principal (p) Interest (i) p + i

6 $1,000.00 $ $

12 $ $ $

2. Fill in the following chart, which shows these two savings options.

3. Maria lost $__________ by keeping her money in a non-interest bearing account rather than putting it in an account that paid 5 percent compounded semiannually.

Type of account Original Principal Interest after 12 months

Total principal and interest after 12

months

Zero-interest checking account

$1,000.00 $ $

5% compounded semiannually

$1,000.00 $ $

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

8

Handout 1: Maria’s Savings Decision, cont.

Months Principal (p) Interest (i) p + i

6 $1,000.00 $ $

12 $ $25.63 $

18 $ $ $

24 $ 1,076.90 $ $

30 $ $27.60 $

36 $ $ $

4. Now, complete the chart below by using the information from question one for months six and 12, and calculate the interest paid for years two and three in the account that pays 5 percent compounded semiannually. Round to the nearest hundredth. Remem-ber that the principal will change each time interest accrues.

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

9

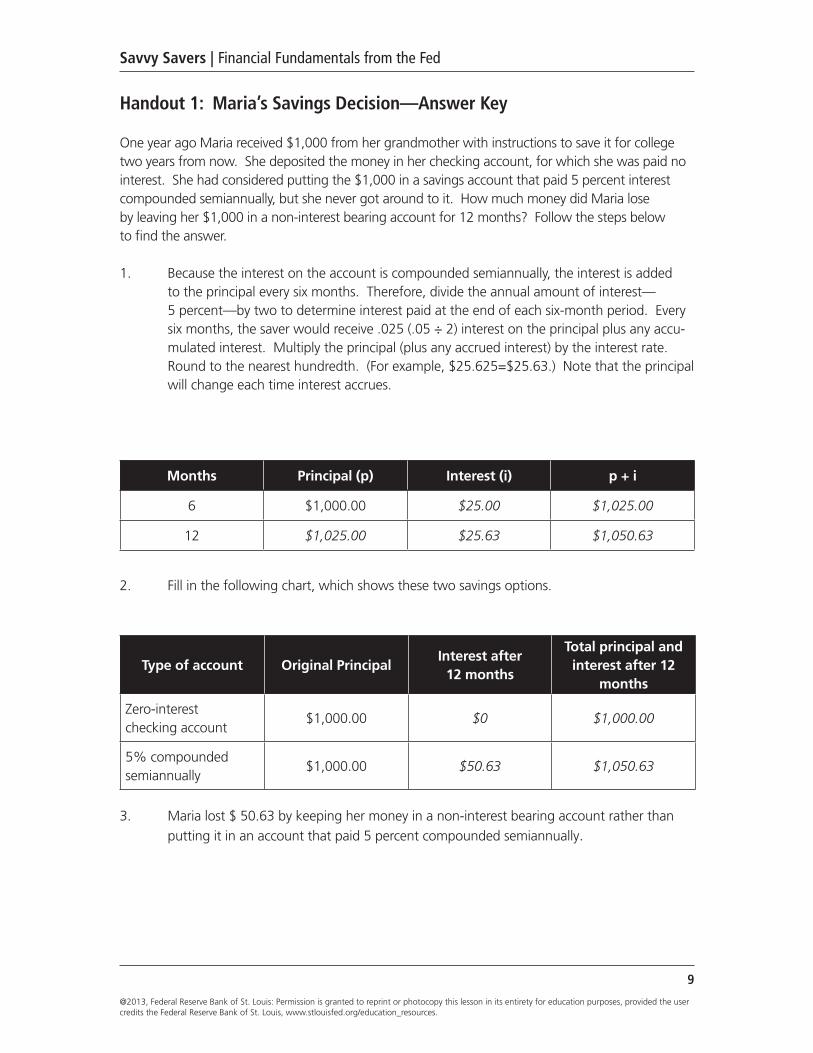

Handout 1: Maria’s Savings Decision—Answer Key

One year ago Maria received $1,000 from her grandmother with instructions to save it for college two years from now. She deposited the money in her checking account, for which she was paid no interest. She had considered putting the $1,000 in a savings account that paid 5 percent interest compounded semiannually, but she never got around to it. How much money did Maria lose by leaving her $1,000 in a non-interest bearing account for 12 months? Follow the steps below to find the answer.

1. Because the interest on the account is compounded semiannually, the interest is added to the principal every six months. Therefore, divide the annual amount of interest— 5 percent—by two to determine interest paid at the end of each six-month period. Every six months, the saver would receive .025 (.05 ÷ 2) interest on the principal plus any accu-mulated interest. Multiply the principal (plus any accrued interest) by the interest rate. Round to the nearest hundredth. (For example, $25.625=$25.63.) Note that the principal will change each time interest accrues.

Months Principal (p) Interest (i) p + i

6 $1,000.00 $25.00 $1,025.00

12 $1,025.00 $25.63 $1,050.63

2. Fill in the following chart, which shows these two savings options.

Type of account Original PrincipalInterest after

12 months

Total principal and interest after 12

months

Zero-interest checking account

$1,000.00 $0 $1,000.00

5% compounded semiannually

$1,000.00 $50.63 $1,050.63

3. Maria lost $ 50.63 by keeping her money in a non-interest bearing account rather than putting it in an account that paid 5 percent compounded semiannually.

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

10

Handout 1: Maria’s Savings Decision—Answer Key, cont.

Months Principal (p) Interest (i) p + i

6 $1,000.00 $25.00 $1,025.00

12 $1,025.00 $25.63 $1,050.63

18 $1,050.63 $26.27 $1,076.90

24 $1,076.90 $26.92 $1,103.82

30 $1,103.82 $27.60 $1,131.42

36 $1,131.42 $28.29 $1,159.71

4. Now, complete the chart below by using the information from question one for months six and 12, and calculate the interest paid for year two and three in the account that pays 5 percent compounded semiannually. Round to the nearest hundredth. Remember that the principal will change each time interest accrues.

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

11

Handout 2: The Rule of 72

The Rule of 72 is a method to determine the number of years it will take for your savings to double in value. Complete the following chart by shading in the bars in chart below. Begin at 0 years, and shade horizontally to the number of years it will take for an amount of money to double for each interest rate. Please use pencil.

0years

10years

20years

30years

40years

50years

2% (72 ÷ 2)

4% (72 ÷ 4)

6% (72 ÷ 6)

8% (72 ÷ 8)

12% (72 ÷ 12)

If your interest rate is . . .

Your money will double in . . .

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

12

Handout 2: The Rule of 72—Answer Key

The Rule of 72 is a method to determine the number of years it will take for your savings to dou-ble in value. Complete the following chart by shading in the bars in chart below. Begin at 0 years, and shade horizontally to the number of years it will take for an amount of money to double for each interest rate. Please use pencil.

0years

10years

20years

30years

40years

50years

2% (72 ÷ 2)

4% (72 ÷ 4)

6% (72 ÷ 6)

8% (72 ÷ 8)

12% (72 ÷ 12)

If your interest rate is . . .

36 years

18 years

12 years

9 years

6 years

Your money will double in . . .

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

13

Handout 3: Charlie’s Financial Goal

1. Charlie is saving to buy a car a year and a half from today. He has $12,000 in a savings account with an interest rate of 4 percent compounded quarterly. How much will Charlie have in his savings account after 18 months? Calculate and fill in the chart below. Round to the nearest hundredth.

2. How long will it take Charlie’s money to double at an interest rate of 4 percent? ______________________

3. Charlie wants to explain the risk-reward relationship to his nephew, who is a sophomore in high school. If you were Charlie, how would you explain the principal of risk-reward?

Months Principal (p) Interest (i) p + i

3 $12,000.00 $ $

6 $ $ $

9 $ $ $

12 $ $ $

15 $ $ $

18 $ $ $

@2013, Federal Reserve Bank of St. Louis: Permission is granted to reprint or photocopy this lesson in its entirety for education purposes, provided the user credits the Federal Reserve Bank of St. Louis, www.stlouisfed.org/education_resources.

Savvy Savers | Financial Fundamentals from the Fed

14

Handout 3: Charlie’s Financial Goal—Answer Key

1. Charlie is saving to buy a car a year and a half from today. He has $12,000 in a savings account with an interest rate of 4 percent compounded quarterly. How much will Charlie have in his savings account after 18 months? Calculate and fill in the chart below. Round to the nearest hundredth.

2. How long will it take Charlie’s money to double at an interest rate of 4 percent? (18 years)

3. Charlie wants to explain the risk-reward relationship to his nephew, who is a sophomore in high school. If you were Charlie, how would you explain the principal of risk-reward? (When you are investing your money, the higher the risk of loss of principal for an invest-ment, the higher the potential reward. So, relatively safe places to put your money—in a savings account at a bank, for example—yield a relatively low reward because the risk of losing your principal is very low.)

Months Principal (p) Interest (i) p + i

3 $ 12,000.00 $ 120.00 $ 12,120.00

6 $ 12,120.00 $ 121.20 $ 12,241.20

9 $ 12,241.20 $ 122.41 $ 12,363.61

12 $ 12,363.61 $ 123.64 $ 12,487.25

15 $ 12,487.25 $ 124.87 $ 12,612.12

18 $ 12,612.12 $ 126.12 $ 12,738.24

Credit

2@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Lesson Description

In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities on an individual’s net worth, monthly budget and balance sheet. Working in groups, students analyze a borrowing scenario and evalu-ate the advantages and disadvantages of using credit.

Concepts

AssetsBudgetCreditLiabilitiesNet Worth

Objectives

Students will:

■ Analyze the impact of purchases financed with credit on a balance sheet.

■ Analyze the effects of debt payments on a budget.

■ Evaluate the advantages and disadvantages of financing various purchases.

Common Core Standards

Gr. 6-12 English Language arts Standards, Literacy in History/Social Studies and Technical Studies

■ Key Ideas and Details

■ Integration of Knowledge and Ideas

Content Standards

National Standards in Economics

■ Standard 2: Effective Decision-Making

National Personal Financial Literacy

■ Standard 1: Buying Goods and Services

■ Standard 4: Using Credit

Grade Level

9-12

Time Required

50 minutes

3@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Materials

■ A copy of Handouts 1 and 3 for each student

■ A copy of Handout 2, one scenario for each group

■ A copy of Handouts 1, 2, and 3 Answer Keys

■ Visuals 1 and 2

Procedures

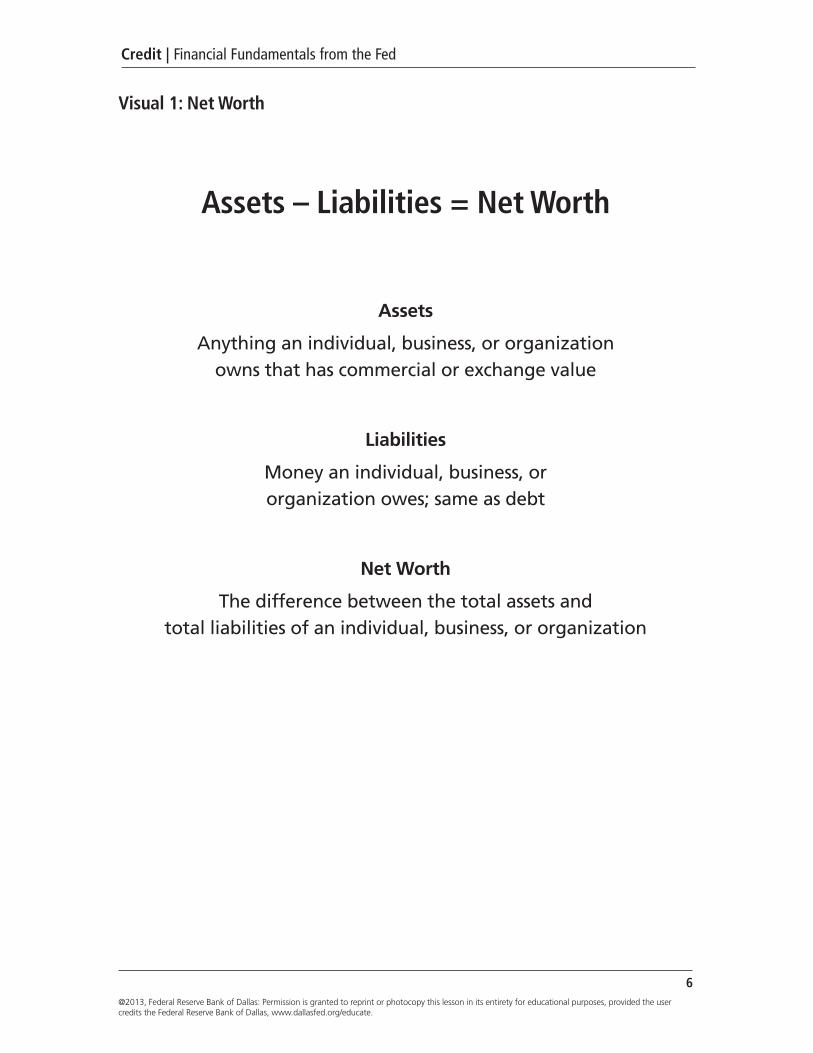

1. Display Visual 1: Net Worth. Use the visual and the information below to discuss net worth.

• Assets – anything an individual or business owns that has commercial or exchange value. Examples include land, buildings, stocks and vehicles.

• Liabilities – money an individual or organization owes; same as debt. Exam-ples include mortgages, car loans, credit card balances and student loans.

• Net Worth – the difference between total assets and total liabilities. Net worth is a way to measure a person’s wealth.

Ask students how a person could increase his or her net worth. Answers should include:

• By increasing total assets

• By decreasing total liabilities

Emphasize that people often use credit to purchase new assets, such as a house or a car, though credit also increases an individual’s liabilities; new liabilities decrease net worth. Credit involves a promise to repay in the future.

2. Distribute Handout 1: Sandra’s Balance Sheet. Have the students complete the worksheet by sorting the items into assets and liabilities. Use Handout 1: Sandra’s Balance Sheet–Answer Key to discuss the suggested answers. Extend the discussion by asking students the following questions.

• How would the balance sheet and net worth be affected if Sandra borrowed $3800 to buy a new car? (The car would be listed as a new asset, even though it will begin to decline in value over time. The loan is a new liability.)

• How would the balance sheet and net worth be affected if Sandra took out $12,000 in student loans to pay for college? (Even though a college degree can increase future earning potential, a college education does not have a market (or resale) value, so it is not considered an asset on her balance sheet. However, the student loan is a new liability.)

4@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

• How would the balance sheet and net worth be affected if Sandra charged $450 on a credit card to pay for spring break trip with her friends? (Because many of the expenses of the trip are consumed [lodging, food and transporta-tion], they do not add new assets. The credit card balance is a new liability.)

Remind students that net worth is a measure of wealth and that every additional loan or liability decreases wealth, whereas increasing assets increases net worth.

3. Display Visual 2: Monthly Budget. Use the visual and the information below to dis-cuss how a budget allows a person to accurately track income and expenses.

• Budgets allow people to account for all sources of income, including jobs, investments and other regular income.

• Budgets help people track and categorize expenses, including food, clothes, entertainment, transportation and gas, etc.

• Budgets allow people to plan for regular (or monthly) expenses, such as loan payments, utility bills and rent, as well as allocate money to savings.

4. Remind students that Sandra added three loans to her balance sheet. In addition

to affecting her net worth, each loan will have an impact on her monthly budget. Use Visual 2 and the information below to discuss the impact of borrowing deci-sions on a budget.

• How would her budget be affected if Sandra borrowed $3800 to buy a car—a loan that adds a $120 monthly car payment for 48 months? (She must add that expense to her monthly budget. For the entire term of the loan, Sandra has to increase income or reduce other expenses to offset the $120 payment.)

• How would her budget be affected if she took out $12,000 in student loans to pay for college, therefore adding a $125 monthly loan payment for 120 months? (She must add that expense to her monthly budget. For the entire term of the loan, Sandra has to increase income or reduce other expenses to offset the $125 payment.)

• How would her budget be affected if Sandra charged $450 on a credit card to pay for a spring break trip and pays off the balance in 10 months with a $50 monthly payment? (For 10 months, Sandra must add the expense to her monthly budget. She must increase income or reduce other expenses to offset the $50 payment.)

5. Divide students into four groups. Give each group one scenario from Handout 2: Use Credit Wisely, and ask students to read the scenario and consider the advan-tages and disadvantages of borrowing. After discussing the advantages and dis-advantages, as well as the impact on the person’s balance sheet and budget, each group should make a recommendation and select a spokesperson to explain the recommendation to the class. (For larger classes, assign scenarios to more than one group and solicit responses from each group.)

5@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

6. Ask the spokesperson from each group to read the group’s scenario, explain some of the advantages and disadvantages of borrowing and make a recommendation. Use the Handout 2–Answer Key suggested discussion points to assist students if necessary. Allow all four groups to present.

Closure

7. Review the important content by asking the following question.

• How does the use of credit–a loan–affect a borrower’s balance sheet? (Debt increases the person’s liabilities, which reduces their net worth, or wealth.)

• How does the use of credit–a loan–affect a borrower’s budget? (Loans require repayment. A borrower must decide if the payments are currently and in the future affordable considering all other obligations.)

Assessment

8. Distribute a copy of Handout 3: Assessment to each student, and ask them to complete it. Use Handout 3: Assessment—Answer Key to discuss student responses.

6@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Visual 1: Net Worth

Assets – Liabilities = Net Worth

Assets

Anything an individual, business, or organization owns that has commercial or exchange value

Liabilities

Money an individual, business, or organization owes; same as debt

Net Worth

The difference between the total assets and total liabilities of an individual, business, or organization

7@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Visual 2: Monthly Budget

Sources of Income Current Income

Total Income

Current Savings

Available to Save (Income - Expenses)

Spending Categories Current Expenses

Total Expenses

8@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 1: Sandra’s Balance Sheet

Sandra is a high school senior. By paying off her car and starting a savings account, Sandra believes that she is well on the way to wealth creation. Use the balance sheet below to calculate Sandra’s net worth. Put the items below in the appropriate section of the chart and use the formula Assets –

Liabilities = Net Worth to calculate her wealth.

Description Amount

Owed to her mother for extra cell phone charges $250

Current value of a savings bond that her uncle gave her $150

Balance on a car loan $1,500

Savings account from summer job $750

DVD collection $200

Car $3,500

Balance on prom dress $200

Assets Amount

Liabilities Amount

Total assets

Total liabilities

Assets – Liabilities = Net Worth

9@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 1: Sandra’s Balance Sheet—Answer Key

Description Amount

Assets Amount

Current value of a savings bond that her uncle gave her $150

Savings account from summer job $750

DVD collection $200

Car $3,500

Liabilities Amount

Owed to her mother for extra cell phone charges $250

Balance on a car loan $1,500

Balance on prom dress $200

Total assets $4,600

Total liabilities $1,950

Assets – Liabilities = Net Worth $2,650

10@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 2: Use Credit Wisely

Patrick’s Prom Problem

Patrick is planning for his senior prom. He is taking the girl he has been dating since homecoming. He would like to take her to a nice restaurant before the dance, but he only has enough money in savings to rent his tux and buy the tickets to the dance. Dinner at the dance is included in the price of the prom tickets, but he really wants to go to a fancy dinner. He recently got a credit card to use for emergencies. Should he use the credit card to buy dinner? If he uses the credit card he will have to pay the amount he charges in the future with interest.

Think about Patrick’s balance sheet and budget. What are some advantages and disadvantages to borrowing? Should Patrick borrow?

11@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 2: Use Credit Wisely, cont.

Debra’s Degree Dilemma

Debra graduated from high school and is halfway through a program to become a dental hygienist. She expects to earn about $55,000 after she graduates, but there are no guarantees. Right now she needs a student loan to finish the last year of her associate’s degree. She is confident that her summer internship in a dentist’s office will lead to a full-time job.

Think about Debra’s balance sheet and budget. What are some advantages and disadvantages to borrowing? Should Debra borrow?

12@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 2: Use Credit Wisely, cont.

Carlos’ Comic Conundrum

Carlos has collected comic books for years. He regularly attends conventions and trade shows and is knowledgeable about the books’ values on the open market. At the latest show, a dealer that he knows well showed him a particularly rare edition comic that is in mint condition. The dealer has offered him a fair price, and Carlos expects the value of the comic to increase steadily over the next several years. Carlos does not have the money right now, but if he charges the purchase, he can pay off the balance in three months and pay less than $5.00 in finance charges.

Think about Carlos’s balance sheet and budget. What are some advantages and disadvantages to borrowing? Should he borrow?

13@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 2: Use Credit Wisely, cont.

Veronica’s Vehicle Vexation

Veronica graduated from college last month, and she has a great new job. She has just moved into her new apartment and bought some furniture. She has been driving the same car since her freshman year, but it is still in good shape. She would like to buy a new car, but the furniture pur-chase used up her savings. She could still get a loan, but she will have to finance the car for 72 months, resulting in several thousand dollars in extra finance charges.

Think about Veronica’s balance sheet and budget. What are some advantages and disadvantages to borrowing? Should she borrow?

14@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 2: Use Credit Wisely—Answer Key

Suggested discussion points

Should Patrick borrow?Advantage—by borrowing he increases his ability to consume something that he cannot presently affordDisadvantage—borrowing negatively impacts his balance sheet by adding a new liability with no new asset

Considerations:

• He got the credit card for emergency situations, not for consumption. By using the card for dinner, he will be changing his initial strategy. Is this advisable? Why or why not?

• How will he adjust his budget in the future to pay off the credit card? Does he have sufficient income?

• How much will it cost to borrow the money? What interest rate will he pay? How long will it take to pay off the charge? How much will the dinner eventually cost him?

Should Debra borrow?Advantage—by borrowing she has the opportunity to complete her degree and possibly earn more moneyDisadvantage—by borrowing she adds the burden of the student loan payment if she does not get the expected job

Considerations:

• Debra should research the terms of the student loan and calculate the total cost of borrowing.

• Can Debra manage the required loan payments with her expected new salary? How will the payments affect her anticipated budget?

• If she fails to get the job that she expects, does she have a plan to make the loan payments in a different employment situation?

• The higher income she expects could allow her to begin to save, thus positively affecting her balance sheet by increasing her assets and net worth.

Should Carlos borrow?Advantage—by borrowing he is presented the opportunity to purchase an asset that may increase in value over timeDisadvantage—by borrowing he is presented the risk of misjudging the market and purchasing an asset that loses value

Considerations:

• Investing in collectables requires knowledge of the market and careful consideration of pur-chases. If the asset increases in value, his net worth will increase. However, Carlos could have misjudged the market, and the asset could lose value.

15@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 2: Use Credit Wisely—Answer Key, cont.

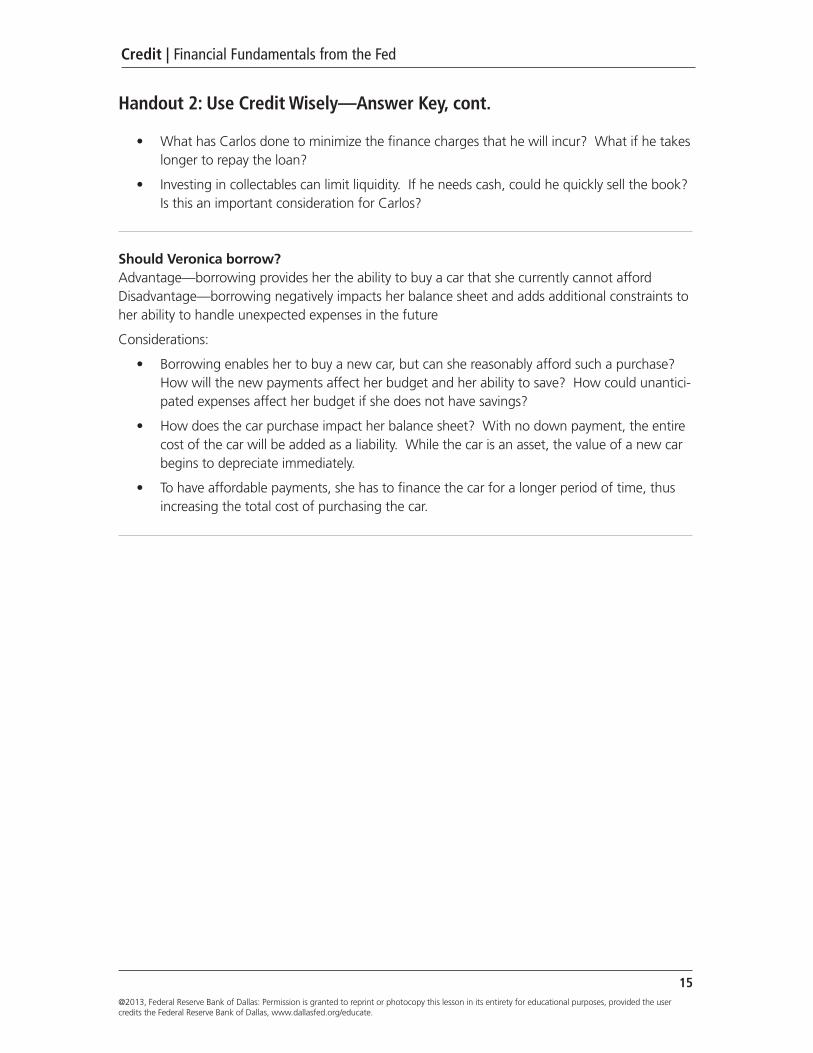

• What has Carlos done to minimize the finance charges that he will incur? What if he takes longer to repay the loan?

• Investing in collectables can limit liquidity. If he needs cash, could he quickly sell the book? Is this an important consideration for Carlos?

Should Veronica borrow?Advantage—borrowing provides her the ability to buy a car that she currently cannot affordDisadvantage—borrowing negatively impacts her balance sheet and adds additional constraints to her ability to handle unexpected expenses in the future

Considerations:

• Borrowing enables her to buy a new car, but can she reasonably afford such a purchase? How will the new payments affect her budget and her ability to save? How could unantici-pated expenses affect her budget if she does not have savings?

• How does the car purchase impact her balance sheet? With no down payment, the entire cost of the car will be added as a liability. While the car is an asset, the value of a new car begins to depreciate immediately.

• To have affordable payments, she has to finance the car for a longer period of time, thus increasing the total cost of purchasing the car.

16@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 3: Assessment

1. Review Tony’s assets and liabilities below, and classify each as one or the other.A $350 loan from parents for a new iPad Mini B. $500 savings bond C. $400 in a checking account D. $65 cash E. $3000 car loan

2. Using the information above, compute Tony’s net worth.

3. Review the items below and construct a monthly budget for Tony. Include sections for total income, total expenses and amount available for savings.

A. After-tax monthly income from part-time job: $675B. Entertainment expenses (movies, dates, dinners out with friends, etc.): $400C. Monthly payment on car loan: $200D. Monthly payment to parents for iPad loan: $50

4. Given his current income and expenses, is it possible for Tony to add a new monthly ex-pense—a $50 date night with his girlfriend—to his budget? Why or why not?

5.

Tony’s Transportation Trouble

Tony’s car is becoming increasingly unreliable. Twice in the past month, he has paid for expensive repairs. Tony drives almost 20 miles to work each way, and public transportation is not located close to his house or job. He has been saving to buy a more reliable car, but the re-pair bills have kept him from saving in the past month. He has found a reliable used car. When he talked to the loan officer at his bank, he found that he could get a loan with payments that are well within his budget.

Think about Tony’s balance sheet and budget. Discuss some advantages and disadvantages to borrowing. Include a recommendation on whether he should borrow.

17@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 3: Assessment—Answer Key

Suggested answers

1. Review Tony’s assets and liabilities below, and classify each as one or the other.A $350 loan from parents for a new iPad Mini (Liability)B. $500 savings bond (Asset)C. $400 in a checking account (Asset)D. $65 cash (Asset)E. $3000 car loan (Liability)

2. Using the information above, compute Tony’s net worth.

Assets: ($500 + $400 + $65 =) $965Liabilities: ($350 + $3000 =) $3350Net worth: (965-3350 = ) $-2385

3. Review the items below and construct a monthly budget for Tony. Include sections for total income, total expenses and amount available for savings.

A. After-tax monthly income from part-time job: $675B. Entertainment expenses (movies, dates, dinners out with friends, etc.): $400C. Monthly payment on car loan: $200D. Monthly payment to parents for iPad loan: $50

Total income = $675Total expenses = $650 ($400 + $200 +50)Total income – total expenses = $25 available to save

4. Given his current income and expenses, is it possible for Tony to add a new monthly expense—a $50 date night with his girlfriend—to his budget? Why or why not?

No, not currently. Because he only has $25 left after he pays his expenses, he would not have enough money each month to add a new $50 expense. He would need to add $25 in income or decrease expenses by $25—or some combination of the two—to add a new $50 expense.

18@2013, Federal Reserve Bank of Dallas: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Dallas, www.dallasfed.org/educate.

Credit | Financial Fundamentals from the Fed

Handout 3: Assessment—Answer Key, cont.

5.

Tony’s Transportation Trouble

Tony’s car is becoming increasingly unreliable. Twice in the past month, he has paid for expensive repairs. Tony drives almost 20 miles to work each way, and public transportation is not located close to his house or job. He has been saving to buy a more reliable car, but the repair bills have kept him from saving in the past month. He has found a reliable used car. When he talked to the loan officer at his bank, he found that he could get a loan with payments that are well within his budget.

Think about Tony’s balance sheet and budget. Discuss some advantages and disadvantages to borrowing. Include a recommendation on whether he should borrow.

Should Tony borrow?

Advantages—reduction of repair expenses, thus, freeing money for affordable loan paymentsDisadvantages—obligation of a monthly car payment, which may be burdensome if other expenses arise or his income decreasesConsiderations:

• Has he considered all the possible budget implications of the car purchase? In addition to the new payment, he should consider other expenses that might change, like insurance or fuel costs.

• Rather than buying a car, could he move closer to work so that he can walk or use public transportation, thus enabling him to continue saving for a car?

• Will the down payment deplete savings that he needs for unexpected expenses? Will the new payment allow him to continue some saving?

• Is his job secure? Could he make the payment if he lost his job?

Focus on Finance

2@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.

Focus on Financial Services | Financial Fundamentals from the Fed

Lesson Description

Students are introduced to the importance of financial services through the “Banking for Safety” online video. They read information about services offered through financial institutions and identify their own service preferences. Students compare institutions listed and choose the one that best meets their needs as an assessment.

ConceptsAccountATMAutomatic bill paymentBalanceBanking relationshipDebit cardDirect depositElectronic paymentFeesFinancial servicesOnline banking

ObjectivesStudents will:

■■ Identify the types of financial services available through financial institutions.

■■ Compare services offered by different financial institutions.

■■ Identify their criteria for selecting financial services and choose an institution that meets their criteria

■■ Explain the importance of developing a relationship with a financial institution.

Common Core StandardsGr. 6-12 English Language arts Standards, Literacy in History/Social Studies and Technical Studies

■■ Key Ideas and Details

■■ Integration of Knowledge and Ideas

Content StandardsNational Standards in Economics

■■ Standard 2: Decision Making

■■ Standard 10: Institutions

National Standards in Personal Financial Literacy

■■ Standard 3: Saving

■■ Standard 4: Credit

3@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.

Focus on Financial Services | Financial Fundamentals from the Fed

Grade level

9-12

Time Required

45 minutes

Materials

■■ Computer access to online video “Lessons from a Storm: Banking for Safety” at: http://www.bos.frb.org/consumer/lessons-from-a-storm

■■ A copy of Handouts 1, 2, and 3 for each student

Lesson Procedure

1. Ask students if they remember hearing about Hurricane Katrina, a storm that affected several communities along the southeast coast of the United States. In 2005, New Orleans experienced major destruction from the storm, which left eighty percent of the city under water. Explain that the storm caused flooding from the Mississippi River and caused most of the city’s residents to evacuate to other loca-tions. Ask the following questions:

• If you were in this situation and had to evacuate, what would you be worried about? (Answers will vary. Students may say they would be worried about their family leaving safely; packing things to take with them; finding a new place to live; going to a new school and other concerns.)

• Would you be worried about having enough money for your move and reloca-tion? (Answers will vary. Some students may mention that money would be an important concern, others may not have considered it.)

2. Tell students that they will watch a video that shows some of the financial problems people experienced when they relocated after the hurricane. Ask them to listen for ways to avoid these problems in emergency situations.

3. Show the seventeen-minute video “Banking for Safety” at: http://www.bos.frb.org/consumer/lessons-from-a-storm (available in English and Spanish).

4. After watching the video, ask the following questions for review:

• Why was it difficult for many workers in New Orleans to get their paychecks after Hurricane Katrina hit the city? (Answers will vary. Students should sug-gest that many people had to evacuate, therefore they did not have regular addresses. If those workers didn’t have bank accounts, their employers did not know where to send the paychecks.)

• How did workers without bank accounts get the money they needed? (Answers will vary. Many workers relied on check-cashing businesses. These

4@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.

Focus on Financial Services | Financial Fundamentals from the Fed

businesses were close by, accepted utility payments, and sold money orders, stamps and envelopes. However, these businesses charged high fees, or payments for their services.)

• Why did Natesha decide to open a bank account? (Answers will vary. Students may say because it was cheaper than using the check-cashing business, which charged $35 a month. They may also comment that it was safer, as Natesha no longer carried her cash around with her. Students may say it was more conve-nient, since Natesha’s paycheck was automatically deposited into her account.)

• What responsibilities come with having a bank account? (Answers may vary. Students should suggest that account holders need to keep track of depos-its and withdrawals, writing amounts down to have a current balance of the money in the account. They should make sure they don’t overdraw their account, letting the balance fall below zero, or they may have to pay fees to the bank. They should also review their monthly statement to make sure it agrees with their own records.)

• What are electronic payments? (Payments sent by computer which transfer money between banks, individuals and businesses.)

• What are the advantages to using electronic payments? (Answers will vary. Advantages include secure transactions, the convenience of funds being directly deposited, and a quick and easy way to pay bills.) Give examples of types of electronic payments that are directly deposited. (Answers will vary. Examples include paychecks, social security, tax refunds, and pensions.)

• As an account holder, what financial services were provided to Natesha? (Answers will vary. Students should suggest automatic deposit of her paycheck, automatic bill pay, and online banking services.)

• Name some ways Natesha used online banking. (Answers may vary. She used it to check her current balance; to see when her phone and utility bills were scheduled to be paid; and to pay other bills directly.)

• What are the benefits of online banking? (Answers will vary. Students may suggest that this service is free, fast, safe and convenient.)

5. Discuss the fact that banks and credit unions are examples of financial institutions, which are organizations that collect and pool small amounts of funds together so that larger investments can be made. Banks and credit unions collect deposits from customers and use the deposits to make loans to other customers. Ask students the following questions:

• Why is it important to have a relationship with a financial institution? (Answers will vary. Students may suggest that this type of relationship can give you finan-cial security by helping you keep track of your money and offering payment services. It can also help in case of emergencies or if you need a loan.)

• Why should you shop around and compare the services of financial institutions? (Answers will vary. Students may say you should compare to find the financial institution that offers the accounts and services you need the most.)

5@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.

Focus on Financial Services | Financial Fundamentals from the Fed

6. Ask students if any of them currently have a savings or checking account with a finan-cial institution. (Answers will vary.) Explain that these are accounts at banks or credit unions in which the owner deposits funds. The owners can then make withdrawals or write checks on the accounts and use an ATM (Automatic Teller Machine) card or debit card to withdraw funds and access their money when needed.

7. Ask students who have these accounts what services or features their accounts offer. (Answers will vary. Students may mention many of the services Natesha received with her account.) Explain to students that different account holders may want different features, depending on their banking habits and preferences.

8. Distribute a copy of Handout 1: Making the Best Financial Institution Choice, and Handout 2: Consider Your Financial Preferences to each student. Ask students to read through the various services offered at financial institutions and rank the sug-gested features according to their own preferences for financial services by number-ing the blanks from 1-7 (with 1 as the top choice).

9. When students have completed Handout 1, ask the following questions:

• What were your top-ranked features? (Answers will vary.)

• Why did you choose these features over others? (Answers will vary.)

Closure

10. Review the important content in this lesson by asking the following questions:

• What types of financial services do financial institutions provide? (They accept customers deposits and keep those deposits safe. They provide easy access to funds through ATM cards, debit cards, and checks. They provide loans. They often pay interest on deposits.)

• Give examples of financial institutions in your community. (Banks and credit unions)

• Why is it important to compare services provided by different financial institu-tions? (Different institutions offer different services and charge different fees. It is important to choose an institution that provides the combination of services and fees that best meet your preferences.)

• What are some important criteria to consider when choosing a financial institu-tion? (Answers will vary, but may include customer service, access to ATMs, atmosphere, rate of interest paid, level of fees charged, hours of operation, location, convenience, and so on.)

• Why is it important to develop a relationship with a financial institution? (Answers will vary but may include that your money is safe, it is easy and conve-nient to conduct transactions, access to loans and other services, and so on.)

6@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.

Focus on Financial Services | Financial Fundamentals from the Fed

Assessment

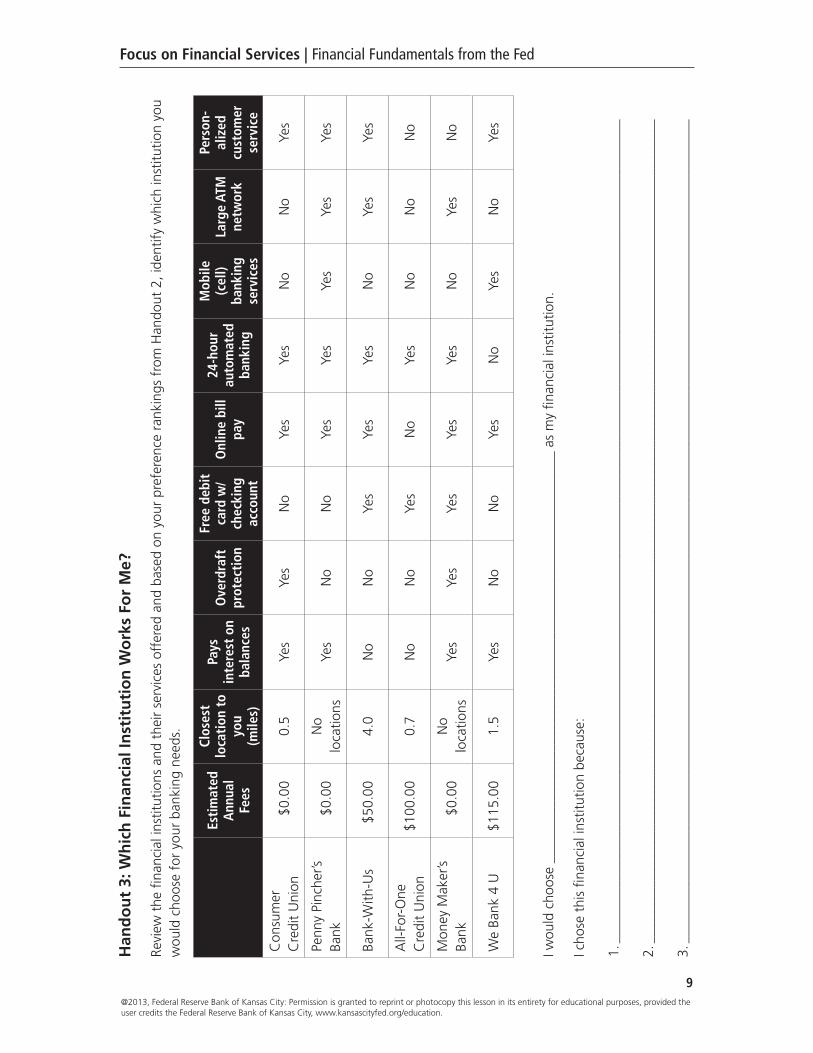

11. Distribute Handout 3: Which Financial Institution Works for Me?, as an assessment. Tell students to read through the list of banks and credit unions, looking for the features they ranked highly in Handout 2. Ask them to compare the institutions that match most of their preferences, narrowing down to the one institution that seems to best meet their preferences. They should list their final choice and the reasons that led them to this choice.

12. As an optional assessment, assign writing a one-page essay that explains what a financial institution is, what services it provides, why those services are useful to them as a customer, and why it is valuable to have a relationship with a financial institution.

7@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.

Focus on Financial Services | Financial Fundamentals from the Fed

Handout 1: Making the Best Financial Institution Choice

How do you decide on the financial institution that’s right for you? Here are some factors to consider:

Atmosphere

Some people enjoy banking where many employees know them by name. If this is important to you, consider a smaller community bank or credit union. Larger regional institutions may have more loca-tions, but staff may not know you personally.

Convenience

Different people have different banking habits. Will you visit your financial institution weekly, or will you conduct most of your banking business online or by phone? Will you need a bank or credit union that is close to home, work, or both? Will you use your ATM card frequently? Consider these questions before making a decision.

Cost

State and Federal Truth-in-Savings Acts require banks and credit unions to disclose all account fees in advance. Use this information to comparison shop. Fees may vary based on your account balance, the number of transactions you make, and other accounts you may have at the same institution. Consider how large a balance you plan to maintain in your bank account. Many financial institutions waive various checking account fees with a large enough balance or a regular direct deposit. Con-sider the number of transactions you will complete monthly, including check writing, ATM use, debit transactions, plus any automatic debits you set up for regular payments (such as for your cellphone, utilities, and car payment.) Some institutions charge for certain transactions, while others allow you a limited number of free transactions. Review the account features to know whether you will be charged for out-of-network ATM use or for automatic overdraft protection on your account.

Customer Service

Most financial institutions have personal bankers to help with specific customer service issues, such as opening and closing accounts, credit questions, and investment opportunities. Some banks and credit unions have 24 hour/7 days a week access to customer service by phone or online. Consider whether these additional services are important to you before making a decision.

Mobility

Today, more than 50 percent of all bank customers do their banking online. Inquire about mobile ser-vices offered, how online banking works at the particular institution, and what fees may be charged. In the United States, there are a number of “branchless banks” for people looking only for online banking services. Many financial institutions offer apps for tablets or cellphones to assist you in doing your banking.

Reputation

Many financial institutions have been in business for years. Is this longevity important to you? Do other peoples’ opinions about particular banks or credit unions matter to you? If so, check out the history and reputation of the institutions you are considering.

Incentives

Some financial institutions offer rewards or incentives for starting an account or maintaining a steady balance. Other banks and credit unions pay higher interest rates as an incentive. Consider whether a checking account that pays interest, or an account without interest but lower fees, is your best value.

8@2013, Federal Reserve Bank of Kansas City: Permission is granted to reprint or photocopy this lesson in its entirety for educational purposes, provided the user credits the Federal Reserve Bank of Kansas City, www.kansascityfed.org/education.