inventory management and receivables (abc, eoq model)

TRANSCRIPT

Presentation onFINANCIAL MANAGEMENT’S

•INVENTORY MANAGEMENT TECHNIQUES•RECEIVABLES AND ITS MANAGEMENT

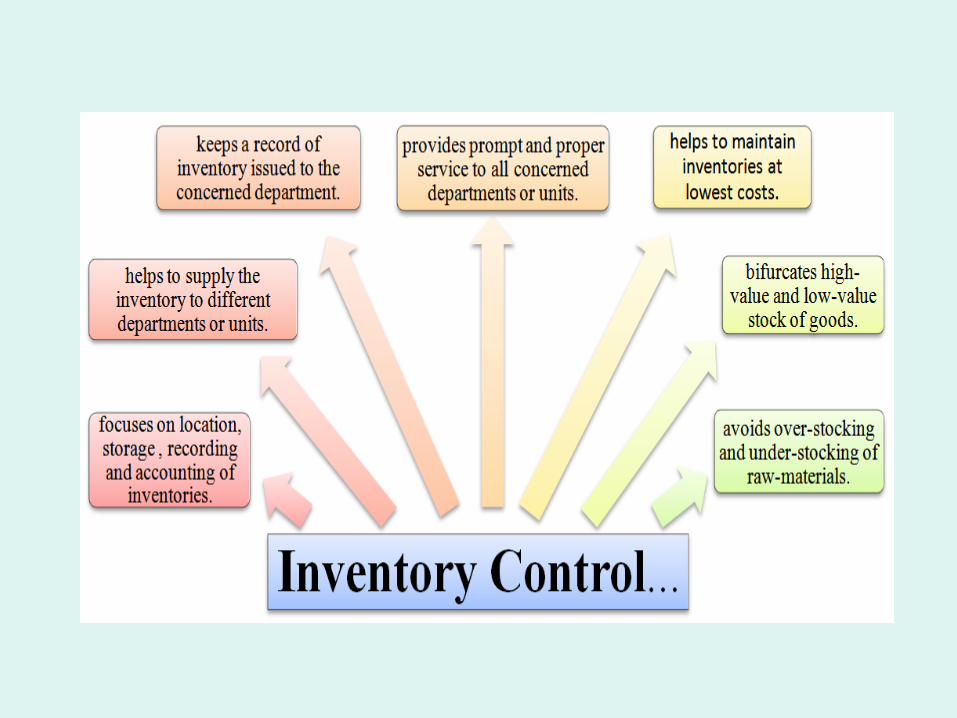

INVENTORY:Meaning & Definit ion

• In a manufacturing organization, in addition to the stock of finished goods, there will be stock of partly finished goods, raw materials and stores.

• The collective name of these entire items is ‘INVENTORY’.

• The term ‘inventory’ refers to the stockpile of production a firm is offering for sale and the components that make up the production.

INVENTORY MANAGEMENT

• Inventories consist of raw materials, stores, spares, packing materials, coal, petroleum products, works-in-progress and finished products in stock either at the factory or deposits.

TECHNIQUES

ABC Analysis of Inventories

• The ABC inventory control technique is based on the principle that a small portion of the items may typically represent the bulk of money value of the total inventory used in the production process, while a relatively large number of items may from a small part of the money value of stores.

• The money value is ascertained by multiplying the quantity of material of each item by its unit price.

• According to this approach to inventory control high value items are more closely controlled than low value items.

• Each item of inventory is given A, B or C denomination depending upon the amount spent for that particular item. “A” or the highest value items should be under the tight control and under responsibility of the most experienced personnel, while “C” or the lowest value may be under simple physical control.

ABC Analysis of Inventories

Pareto Principle

There are no fixed threshold for each class, different proportion can be applied based on objective and criteria. ABC Analysis is similar to the Pareto principle in that the 'A' items will typically account for a large proportion of the overall value but a small percentage of number of items. The Pareto principle states that, for many events, roughly 80% of the effects come from 20% of the causes.

Limitation of ABC Analysis

The ABC system of classification should, however, be used with caution. For ex:

An item of inventory may be very inexpensive. Under the ABC system it would be classified into C category. But it may be very critical to the production process and may not be easily available. But it may be very critical to the production process and may not be easily available. It deserves the special attention of mgmt. But in terms of the ABC framework, it would be included in the category which requires the least attention.

Question on ABC Analysis

• Question: Analyze the following items into ABC categories on the basis of information given below:

• Category A: Rs.5000 & above (Total Value)• Category B: Rs.1500 to Rs.4,999 (Total Value)• Category C: Below Rs.1500

Economic Order Quantity(EOQ MODEL)

Important questions dealt with in EOQ Model

• 1.How much to purchase at any one time?

• 2.Other costs associated with ordering quantity apart from purchase price?

• 3.Material procurement should be done in one lot or installments?

TERMS• Ordering cost- cost incurred by the

company at the time of placing an order.

• For e.g.. Handling and transportation cost, Stationary cost, costs incurred for inviting quotations and tenders.

• The more the frequency of order, the more the Ordering cost.

• Carrying cost- cost of carrying the inventory. Real out of pocket cost, associated with having inventory on hand.

• For e.g.. Warehouse charges, insurance lighting, losses due to handling spoilage, breakage etc.. Along with, amount of interest lost due to the investment in the inventory.

• C.C. increases as the quantity of material in inventory increases.

Behavior of Carrying Cost & Ordering Cost

• Both C.C and O.C are variables costs , however their behavior is exactly opposite of each other.

• If orders are frequent, O.C will be more. • As quantity ordered increases, C.C will

Increase.• The optimum level of inventory at which

both the O.C and C.C is minimum is called as Economic order quantity. Also called as economic lot size.

Fixation Of Level• Not to purchase too much or too little.

• Setting accurate timing of purchase.

• Objective- To avoid overstocking, avoiding shortage of material, ordering the material at right time.

Maximum Level• Maximum level is the highest level of

material beyond which the inventory of material is not allowed to rise.

• Maximum level=Re order level + Re order quantity-(minimum consumption* minimum re order period)

Minimum Level• In order to avoid shortage of material.

• If production is held up due to shortage of material, there will be huge loss to the company.

• Stock should not fall below this level.

• Minimum level=Ordering level-(average rate of consumption* re order period)

Re order level• This level is fixed for deciding the time of placing an

order.

• If the stock reaches this level, fresh order is placed, so that by the time the material is procured the level of material may fall up to minimum level but not below that.

• Re order level=maximum usage per period* maximum re order period.

Or • Re order level=minimum level + consumption

during the time required to get fresh deliveries.

Average level• Average level=(maximum level + minimum level)/2

• Average level=Minimum level + reorder quantity/2

Working notes:

• Number of orders= total inventory requirement/order size.

• Average Inventory = order size/2.

• Total carrying cost = Average inventory * carrying cost per unit.

• Total ordering cost =Number of orders *cost per order.

• Total cost = cost of items purchased+ total carrying and ordering cost.

Assumptions1. The rate at which the firm use inventory is

steady over times.

2. Both O.C. and inventory C.C are known and they are fixed per unit.

3.The purchasing cost per unit is known and it remains constant.

4.The quantity ordered is delivered immediately.

Question:Two components, A and B are, used as follows: Normal usage 50 units each per week

Minimum usage 25 units each per week

Maximum usage 75 units each per week

Re- Order quantity A:300 UNITS;B:500 UNITS

Re- Order period A:4 TO 6 WEEKSB:2 TO 4 WEEKS

Calculate for each component:

a) Re order level

b) Minimum level

c) Maximum level

d) Average stock level

Receivables and management of Receivables

• Receivables is known as when firm makes an ordinary sale of goods or service and does not receive payment, it grant trade credit and creates accounts receivable which would be collected in future.

• “In simple terms it known as sales of good and service in credit and make an promissory note to receive payment later.”

Receivables

Objectives Of Receivables• Creating, preserving and collecting A/R.• Establishing and communicating credit

policies.• Evaluation of customers and setting credit

lines.• Maintaining up-to-date records of

accounts receivables.

Reasons To Offer Credit• Competition• Market share• Promotion• Credit availability to customers• Customer convenience• Profit

Receivables management• Receivables management refers to the

decision a business makes regarding to the overall credit, collection policies and the evaluation of individual credit applicants.

• It is also called trade credit management.

• It refers to the planning, organizing and controlling of receivables.

Significance & Purpose of Receivables management

• The basic purpose of firm's receivable management is to determine effective credit policy that increases the efficiency of firm's credit and collection department and contributes to the maximization of value of the firm. The specific purposes of receivable management are as follows:

• To evaluate the creditworthiness of customers before granting or extending the credit.

• To minimize the cost of investment in receivables.• To minimize the possible bad debt losses.• To minimize the cost of running credit

and collection department.• To maintain a trade off between costs and benefits

associated to credit policy.

The management of Receivables involves crucial decision in 3 areas:

Credit Policies• It provides the framework to determine

whether or not to extend credit to a customer and how much credit to extend.

• Two broad dimensions:-• Credit standards• Credit analysis

Credit Standards• It represents the basic criteria for the

extension of credit to customers.• The quantitative basis of establishing

credit standards are:-• Credit ratings• Average payment period• Financial ratios

Following Factors are considered while deciding the credit standards

• Collection costs• Investments in receivables or the average

collection period.• Bad debt expenses.• Sales volume

Credit Analysis• The second aspect of credit policies of a firm is credit analysis.• Two basic steps are involved in the credit investigation process:-• Obtaining credit information internal sources:- filling up of various forms internal records external sources:- financial statements bank references trade references• Analysis of credit information quantitative qualitative It must be clear that the main purpose of credit analysis is to assess the credit

worthiness of the customers.

Credit Terms• The terms under which goods are sold

on credit are referred as credit terms.• Credit terms specify the repayment terms

of receivables.• Components of credit terms:-• Credit period• Cash discount • Cash discount period

Collection Policies• They refer to the procedures followed to

collect account receivables when they become due after the expiry of the credit period.

• Their purpose should be the speed up the collection of dues.

• Various steps to collect dues from customer by firm are:- letter, telephone calls etc.

Question: Following information of a company are as under:

2011 2012

(Rs.) (Rs.)

Net Sales 10,00,000 15,00,000

Receivables 2,00,000 2,50,000

Calculate:

(a)Receivables Turnover

(b)Calculate the average size of investment in receivables an improved receivables turnover of 7 times on budgeted sales volume Rs.17,50,000 for the year 2003.

Question:Credit sales of company (Year 2012)

4,00,000Receivables(1.1.2012)

43,000Receivables(31.12.2012)

29,000Suppose 360 days in a year. Calculate

average period of Receivables.