introduction to insurance - iii · explain and clarify these key insurance terms: risk,...

TRANSCRIPT

Chapter 1

Chapter aim

This chapter explores key insurance terms and introduces students to the concept of risk – its different dimensions and its relationship to insurance.

© The Insurance Institute of Ireland 2014 1

Introduction to insurance

Chapter

1

SAMPLE

Cha

pter

1

2 © The Insurance Institute of Ireland 2014

PDI-01 The Nature of Insurance April 2014

ContentsSection Title Learning outcome

AThe concept of risk Explain and clarify these key insurance terms:

risk, uncertainty, frequency, severity, peril, hazard, risk pooling, insurance and co-insurance.

BPeril and hazard

CRisk pooling

DRisk sharing

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 3

Chapter 1

A The concept of riskThere is no universally recognised definition for risk. The word is used in several ways and we need to look at each of these. First, we need a definition of the term in its everyday sense and here we find our first problem.

The Oxford Dictionary defines risk as a situation involving exposure to danger. If we were to ask a group of people for their definition of risk, we would probably get a variety of answers. Some might focus on a fear of uncertainty or danger, while others might refer to the financial consequences of unwanted events, for example, damage to property or incurring a legal liability.

Every person or business faces some degree of risk in their everyday life and we regularly make decisions based on an assessment of risk, such as whether or not it is safe to cross a road. Normally, however, we tend to consider risk in terms of potentially catastrophic events. We may also seek some form of protection from the consequences of such events.

The dictionary definition is helpful to our exploration of risk, but it is also useful to look at other uses of the term:

• the possibility of an unfortunate occurrence

• doubt concerning the outcome of a situation

• unpredictability

• the possibility of loss.

We see that there are two important elements to risk: uncertainty and unpredictability. We can gather these together in the following definition: Risk is the uncertainty of future events and their outcome.

Let us consider for a moment, the risks associated with owning and using a car. Some are more obvious than others. They include the risk of:

• car theft

• damage caused by an accident

• injury to the driver

• injury to others

• damage to property

• prosecution for a motoring offence.

Each of these represents a risk to the owner. For the first five points, it will be possible to insure (transfer) the risk. However, the final situation on the list is not so straightforward. As we will discover in Chapter 2B3, any fine imposed as a criminal penalty is uninsurable, as this would be against public policy.

risk

uncertainty of future events and their outcome:

• the cause of the possible loss

• the thing (or liability) insured, e.g. a factory, house, liability to the public, motor car, individual

• a combination of the thing insured and the cause of the possible loss

SAMPLE

PDI-01 The Nature of Insurance April 2014

4 © The Insurance Institute of Ireland 2014

Cha

pter

1

Just think

Example 1.1

A1 Insurance as a risk transfer mechanism When a risk is insurable, we can view the transaction in financial terms and say that

the owner pays a known premium to an insurer in return for the insurer accepting the future unknown cost of the insured risk. The insurer’s side of the bargain is a series of promises set down in policy wording that defines when it will pay for loss, damage or liability incurred.

Insurance is a risk transfer mechanism. For the one who is insured it brings peace of mind because the uncertainty of possible future loss has been replaced by the certainty of the agreed premium.

What other risks do you face as an individual? Think about the risks to what you own, within the environment in which you live and work and in the wider field.

You may have thought about your car, home, possessions – all tangible assets. Each could be lost, damaged or stolen. Your environment, on the other hand, includes less tangible risks, such as to your health and finances. Various social risks may also arise, e.g. in joining clubs and organisations. Then there is the possibility of unemployment, recession or, wider still, government instability and legislative change. As we consider more and more aspects of our environment, we can see that risk is inherent in most of what we do. External influences are at work to bring about unexpected results (investment performance, competition, promotion at work, public debt). Many of these are not within our control but we may be able to manage their effects.

Although we are considering risk in its generic sense, there are three other ways in which the word is used in the insurance marketplace, as shown in Table 1.1.

Table 1.1 Other uses of the term ‘risk’

1. The cause of the possible loss that is insured, e.g. fire, theft or liability risk

2. The thing (or liability) insured, e.g. a factory, house, liability to the public, motor car or individual

3. A combination of 1 and 2, where an insurer will refer to insuring a ‘risk’, which means the thing itself and the cause of the possible loss.

The last of these may not be readily evident, so let us consider Example 1.1.

An insurer is considering a household risk for a house in an area where there has been a series of floods in the past. The insurer is asked: ‘Will you insure this risk?’

In this situation, the insurer is being asked to consider both the physical bricks and mortar and the likelihood of future flood damage (both the thing and the cause of loss). This is what is referred to as the ‘risk’.

insurer

a risk-carrying, regulated entity (product producer)

risk transfer mechanism

acceptance of an unknown future potential risk by an insurer for an agreed premium from an insured

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 5

Chapter 1

Quick question 1

What is the uncertainty element in life assurance products?

Example 1.2

If we were looking at risk in a more general context we would have to consider the upside of risk, e.g. the hope of a favourable financial outcome when setting up a business. However, in the context of insurance, risk is viewed from the perspective of its downside – the possibility of loss rather than gain.

When we consider risk in this way there are three aspects of risk that are important for our studies:

• Uncertainty – ‘Will it ever happen?’ or, as in life assurance, ‘When will it happen?’

• Level of risk – ‘How often will the loss occur and how severe will it be?’

• Risk definition and influential factors – ‘What peril (or contingency) is involved and what are the relevant hazards?’

We will now look at each of these three aspects of risk.

A2 Uncertainty Uncertainty is at the core of the concept of risk. If we always know what is going to

happen, then there is no element of risk. If you know that your house will burn down at 4pm tomorrow, or that on the way home you will have a car accident, there is no risk of the event happening as it is a certainty.

A3 Level of risk This relates to how risk is measured. There is a greater likelihood of some events

happening than others. We know that some events will cost more than others. The level of risk is normally assessed in terms of frequency and severity.

Frequency is often interchangeable with the term likelihood. Severity is often interchangeable with the term impact.

A3a Frequency (likelihood)

This is a predictive aspect of risk that insurers try to gauge from past experience. Before we consider how they do this, read through Example 1.2.

Imagine a house situated beside a river that is prone to overflowing. Past experience (i.e. the known history of the river overflowing) increases the likelihood of this house suffering flood damage.

Now imagine a second house that is 100 metres away from the river bank and on a slight hill. This house is less likely to be flooded because of its position and altitude.

In both cases, we are considering how often flooding might occur (the frequency or likelihood). This is an important facet of risk assessment.

peril

contingency that gives rise to a loss or liability

hazard

any feature that influences the operation of a peril, either in its likelihood of occurrence or its severity

frequency

how often an event will (or is likely to) happen

SAMPLE

PDI-01 The Nature of Insurance April 2014

6 © The Insurance Institute of Ireland 2014

Cha

pter

1

Just think

Think of other risks, both personal and commercial. What factors would influence the possible frequency of a loss occurring?

There are many other possibilities:

• Motor insurance – age and type of vehicle, driving experience of driver (likelihood of risky activity)

• Property insurance – industrial processes (likelihood of fire or explosions)

• Employers liability insurance – unguarded machinery (likelihood of worker injury)

• Bicycle insurance – inadequate security when unattended (likelihood of theft).

Here again in each scenario we have considered only the risk of loss, injury or damage occurring (frequency). We have not yet considered the potential size of any loss.

A3b Severity (impact)

The overall level of risk may change if we consider the potential amount of loss, damage or destruction. In other words, as well as frequency, we must also consider the severity, scale or seriousness of the loss that might occur.

To return to our earlier example of the two riverside houses, what if the house closest to the river is valued at 0100,000 and the second house further away is valued at 0500,000? We might need to modify our view as to which house represents the greater overall risk, in view of the higher potential severity (seriousness) of loss.

We must therefore consider both frequency and severity when considering the level of risk.

Quick question 2

When considering ‘severity’, what are we trying to determine?

severity

the seriousness (size/consequences) of an event (also referred to as impact)

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 7

Chapter 1

A3c Relationship between frequency and severity

In many risk situations, we see a standard relationship between frequency and severity. There is a high frequency of low-severity losses and a low frequency of high-severity losses. This relationship is illustrated in Figure 1.1.

Figure 1.1: Frequency–severity relationship

The Heinrich Triangle in Figure 1.2 shows that, for every one major injury at work, there are 30 minor ones and 300 non-injury incidents. The triangle was the result of analysing several thousand work incidents and these figures have been confirmed by later studies. The pattern shows that there are few serious incidents and many minor ones.

Figure 1.2: The Heinrich Triangle

The relationship of ‘high frequency/low severity’ and ‘low frequency/high severity’ has also been shown to exist for other areas of risk, including motor accident and property damage.

Severity

Frequency

1Major Injury

30Minor Injuries

300Non-Injury AccidentsSAMPLE

PDI-01 The Nature of Insurance April 2014

8 © The Insurance Institute of Ireland 2014

Cha

pter

1

Table 1.2 illustrates some common examples of this relationship.

Table 1.2 Examples of behaviour for risk types

Business class Type of incident Frequency Severity

Motor Windscreen High Low

Motor Multiple fatalities Low High

Household Accidental breakage High Low

Household Subsidence Low High

Travel Baggage claim High Low

Travel Death overseas Low High

Private medical insurance Broken arm/leg High Low

Private medical insurance Critical illness diagnosis Low High

This table reflects the typical experience of a busy claims department in an insurance company. For example, motor claim handlers deal with large numbers of claims for minor damage to vehicles, but thankfully fewer claims involving serious or fatal injuries.

The different profiles of frequency and severity help insurers predict the overall cost of claims likely to arise for a particular class of business. This enables them to set appropriate premiums and to decide on the level of risk they are prepared to accept.

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 9

Chapter 1

B

Quick question 3

List other examples of a positive (good) hazard.

Example 1.3

Peril and hazardPeril and hazard are important aspects of the concept of risk as they relate to the causes of losses.

B1 Perils (contingencies) and hazards This aspect of risk relates to the cause of losses:

• A peril can be defined as the contingency that gives rise to a loss or liability. It is helpful to use the term ‘contingency’ as this is appropriate to both legal liabilities and damage to property.

• A hazard can be defined as any feature that influences the operation of the peril, either in its likelihood of occurrence or its severity.

At first, the distinction between the two may not be that obvious. However, Example 1.3 should help.

A thatched cottage is insured against fire. Fire is therefore the peril, because it is the insured incident, the primary cause of loss named in the policy. However, the thatched roof has the potential to encourage a fire to spread quickly and result in greater loss should a fire occur. The thatched roof is therefore a hazard.

Not all hazards are negative in their impact. Take for example the fitting of an intruder alarm. This can be viewed as a positive hazard resulting in a premium discount for the insured.

Other examples of perils are:

• Overflow of water tanks and apparatus –This causes damage to buildings and/or contents and is an insurable contingency.

• Lightning –This natural peril can result in damage that can be insured.

• Theft – Both loss of and damage to property in the course of theft can be insured.

Other examples of hazards are:

• A safari holiday – Factors such as the presence of local diseases and the likelihood of injury while engaging in safari activities all increase the possible extent of loss and are therefore hazards in travel insurance.

• A high number of motoring convictions – This increases the likelihood of poor quality driving or even reckless driving, thus affecting motor insurance.SAMPLE

PDI-01 The Nature of Insurance April 2014

10 © The Insurance Institute of Ireland 2014

Cha

pter

1

Just think

Example 1.4

Did you notice the difference between the two types of hazard that we have just considered?

This leads us to an important distinction between the types of hazards presented by different risks. Hazards can be physical or moral.

B2 Physical hazard Examples of physical hazard are:

• Security protection at a shop – the higher the quality of the security system, the better the physical hazard presented, as it may prevent a loss altogether

• Construction of a property – the lesser the standard of building construction, the poorer the physical hazard for fire and similar risks, as the building will be less resistant to damage.

Example 1.4 provides a case study demonstrating both good and poor aspects of physical hazard.

Blue Diamond is a company that produces industrial diamonds. It recently purchased a new business unit in an area with a high crime rate. Due to inadequate lighting in the surrounding area, the company installed a camera surveillance system and their vehicles are garaged overnight. As a result of making deliveries nationwide, the garage (part of the business unit) stores 50 litres of gasoline on a continual basis. The company supplies its staff with suitable protective eye equipment in its production processes.

Poor aspects of physical hazard

• Attractiveness of stock, small in size relative to value and not easily traced – high risk of theft loss

• High crime-rate area – increased likelihood of theft loss

• Poor lighting – further increased likelihood of theft loss

• Gasoline in garage – increased likelihood of fire loss with catastrophic potential.

Good aspects of physical hazard

• Camera surveillance system – deterrent to would-be thieves and therefore reduced likelihood of theft loss

• Vehicles garaged overnight – reduced likelihood of motor theft loss

• Suitable protective eye equipment – reduced likelihood of employers liability loss.

physical hazard

influencing factors that are factual characteristics, including any measurable dimension of the risk

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 11

Chapter 1

Example 1.5

B3 Moral hazard Examples of moral hazard include the following:

• Carelessness – A driver’s lack of care can increase the chance of an accident happening and its severity.

• Honesty – A person who has previously been open and upright in their dealings with insurers represents a better moral hazard than one who has made, or is suspected of making, fraudulent or exaggerated claims.

• Social attitudes – Some individuals and sectors of society do not regard cheating insurers as immoral.

Example 1.5 provides a case study that demonstrates moral hazard.

George is a motorist, whose car is a standard model that presents no unusual features. However, George has had two insurance claims in the past and two motoring convictions.

The first claim involved car theft. George told his insurers that the car was recovered in a damaged state after a theft. On investigation, the insurers suspected that the car had not been stolen, but was reported to the Gardaí as a theft because George had only limited cover. His policy covered damage to the car due to theft, but did not include damage resulting from an accident.

The second incident involved a household insurance claim. Following what the insurers believed to be a genuine theft, there were suspicions that extra ‘stolen’ items had been added to the list. There were no receipts available.

His motoring convictions involved driving through a red light and failing to stop when required to do so by a Garda.

Poor aspects of moral hazard

a. Suspicion of fraud – Faking an incident and falsely including non-stolen items in a theft claim are very serious matters.

b. Motoring convictions – While insurers may be prepared to view a minor parking offence generously, the type of offences George had committed demonstrate an irresponsible and careless attitude.

B4 Distinguishing hazards Sometimes, it can be difficult to distinguish between a physical and a moral hazard.

This is because poor moral hazard is often accompanied by some poor physical aspect to the risk. Take the example of the physical hazard of unguarded machinery in a factory or a poorly controlled smoking environment. This clearly arises from the attitude and behaviour of those in charge, which allows for a careless approach to safety.

moral hazard

influencing factors concerned with the attitude and conduct of people. In insurance, usually the person insured but also the insured’s employees and that of society as a whole.

SAMPLE

PDI-01 The Nature of Insurance April 2014

12 © The Insurance Institute of Ireland 2014

Cha

pter

1

We must guard against the tendency of assuming there is an automatically adverse moral aspect to a heavy risk. For example, a fireworks factory represents a very heavy fire risk but it does not follow that there is a poor moral aspect to the risk. Equally, a young driver who is driving a high-performance car will not necessarily drive irresponsibly. However, especially in the latter example, statistics do show that a disproportionately high number of accidents are caused by young drivers. Also, the car itself will be in a high-rating group because of its value and performance. These two aspects comprise a physical hazard because they are measurable; so too would a poor claims history, serious motoring convictions or penalty points.

The significance of these aspects of hazard is that they will influence insurers’ decisions as to the acceptability and pricing of policies. However, as well as contributing to the process of pricing, these factors will also influence decisions by insurers regarding how much of a risk they should accept, and the degree to which the risk should be shared with other insurers or reinsurers.

Quick question 4

Why is it sometimes difficult to distinguish between a physical and moral hazard?

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 13

Chapter 1

C

Example 1.6

Risk pooling

An insurance company gathers together relatively small sums of money from people who want to be protected financially from similar kinds of perils (contingencies). The insurer sets itself up to operate a ‘pool’. Contributions, in the form of premiums from many policyholders, go into this pool. Out of the pool come payments to compensate the losses of the few.

The contributions, or premiums, must be large enough in total to meet the losses incurred in any one year. They must also cover the costs of operating the pool and provide an element of profit for the insurer. At this level of operation the methodology is true of all types of insurance, including private health insurance. Consider Example 1.6.

Risk pooling – a very basic example

Millbrook Insurance Company is a newly established company that will specialise in providing household insurance for apartments. MIC expects to sell 10,000 policies, the net cost of claims is estimated at 01,250,000. Management estimates the costs in running the company (brokerage, salaries, rent, promotion, taxation and cost of reinsurance) would be 01,500,000. Furthermore, the stake holders are expecting a 5 per cent return on their 010,000,000 investment.

Net cost of claims 01,250,000 + expenses 01,500,000 + dividend 0500,000 = Total 03,250,000

Contribution by each of the 10,000 policy holders (premium) = 0325

To operate a pooling system successfully, a number of pools must be established, one for each main group of risks; for example, an individual pool for motor insurance, another for household insurance and yet another for private health insurance. One reason for this is the law of large numbers, which is considered in Section C1.

C1 Law of large numbers In operating the pool, insurers benefit from the law of large numbers. This can

be illustrated by considering the flip of a coin, which results in either a heads or tails outcome. Simple mathematics tells us we should expect to get the same number of heads and tails, because the chance of getting either outcome is 50 per cent. Flipping a coin 20 times may result in any combination of heads and tails, but the sample is too small to be reliable. By flipping the coin 10,000 times, the law of large numbers will operate to give a result more in keeping with the underlying probability of 50 per cent each – or 5,000 heads and 5,000 tails.

risk pooling

basic concept of insurance – that the losses of the few are met by the contributions of many

law of large numbers

the larger the number of similar-type events that occur, the more likely the outcome will match the expected resultSAMPLE

PDI-01 The Nature of Insurance April 2014

14 © The Insurance Institute of Ireland 2014

Cha

pter

1

Applying the principle of large numbers to insurance claims statistics enables the insurer to predict, with some degree of confidence, the future total cost of claims in any one year. This is because insurers provide cover against a large number of similar risks. The final number of actual loss events tends to be very close to the expected number (based on past measured experience). This means that the insurer can calculate likely losses and confidently charge a fixed premium. This has the benefit of fixing the cost for the insured, who now knows what the financial outlay will be for the year, irrespective of the number or size of claims that may occur in the period.

We need to consider terminology at this point as we have begun to use terms such as ‘insured’ and ‘policyholder’. Terms for the same party tend to differ according to the stage in the insurance process and the relationship to other parties.

Table 1.3 Terminology

• Proposer: the person or firm applying for insurance.

• Insured/policyholder: the person or firm that has arranged a contract of insurance with an insurer.

• Client: the name given by an intermediary to a person or firm that has appointed them to act on their behalf. This person or firm is known as the intermediary’s client from the time of initial appointment onwards.

C2 Equitable premiums For most types of insurance when deciding on an equitable contribution, insurers

take into account the different elements (the risk itself and its associated hazards) brought into the pool by each of the proposers. In order to ensure that a fair premium is charged and a fair profit can be made, the process of arriving at a premium is a complex one and the correct assessment of risk is extremely important. This process is part of the insurance activity termed underwriting.

In Ireland, however, the system of equitable premiums cannot be applied to private health insurance. The Health Insurance Acts 1994–2013 dictate that there must be an identical contribution to the pool by all policyholders regardless of those factors that would normally give rise to a difference of premium (i.e. age, gender and health record). It follows that for these insurances, the underwriting process applies only to calculating the costs required to run the pool as a whole. Price distinctions are not made on the basis of the different risk characteristics being brought to the pool, but solely on the basis of different levels of cover. This is considered further in Chapter 6.

Quick question 5

Why not set up a single pool so that the greatest possible number of risks can be included?

firm

a regulated entity (as used throughout this textbook to refer to regulated entities providing financial services, including insurers and/or intermediaries)

equitable premiums

the rule that each person wishing to join an insurance pool must be prepared to make a fair contribution

underwriting

process of risk pooling, risk selection (choosing who and what to insure) and assessment of individual risks that meet the insurer’s risk criteria

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 15

Chapter 1

D

Just think

Risk sharing A significant part of an insurer’s job is to manage the pool of money from which valid claims are to be paid. Each insurer will set a range of criteria for the risks they are prepared to accept. The criteria will include maximum limits of acceptance for particular categories of risk. For property insurances, the boundaries would be expressed as a range of acceptable sums insured, which differ according to the trade being carried on in the premises and/or the construction standards of the buildings.

For example, it is always the case that an insurer will be prepared to accept a higher sum insured for an office risk than for a factory where plastics are manufactured.

So what happens when a risk is offered to an insurer but the amounts at risk are greater than the sum the insurer is willing to retain for that category?

We may conclude that the most obvious response is for the insurer to decline to insure the risk. However, the insurer will not wish to do this if the only reason is one of size and in all other respects the risk is of good quality. So, the insurer must find a way to share the risk with others or to insure only part of the risk. There are two ways of doing this – the first is by co-insurance and the second by reinsurance. The following section discusses co-insurance, while reinsurance will be examined in Chapters 3F and 6G.

D1 Co-insurance For property insurances in particular, an insurer may choose to share a risk by means

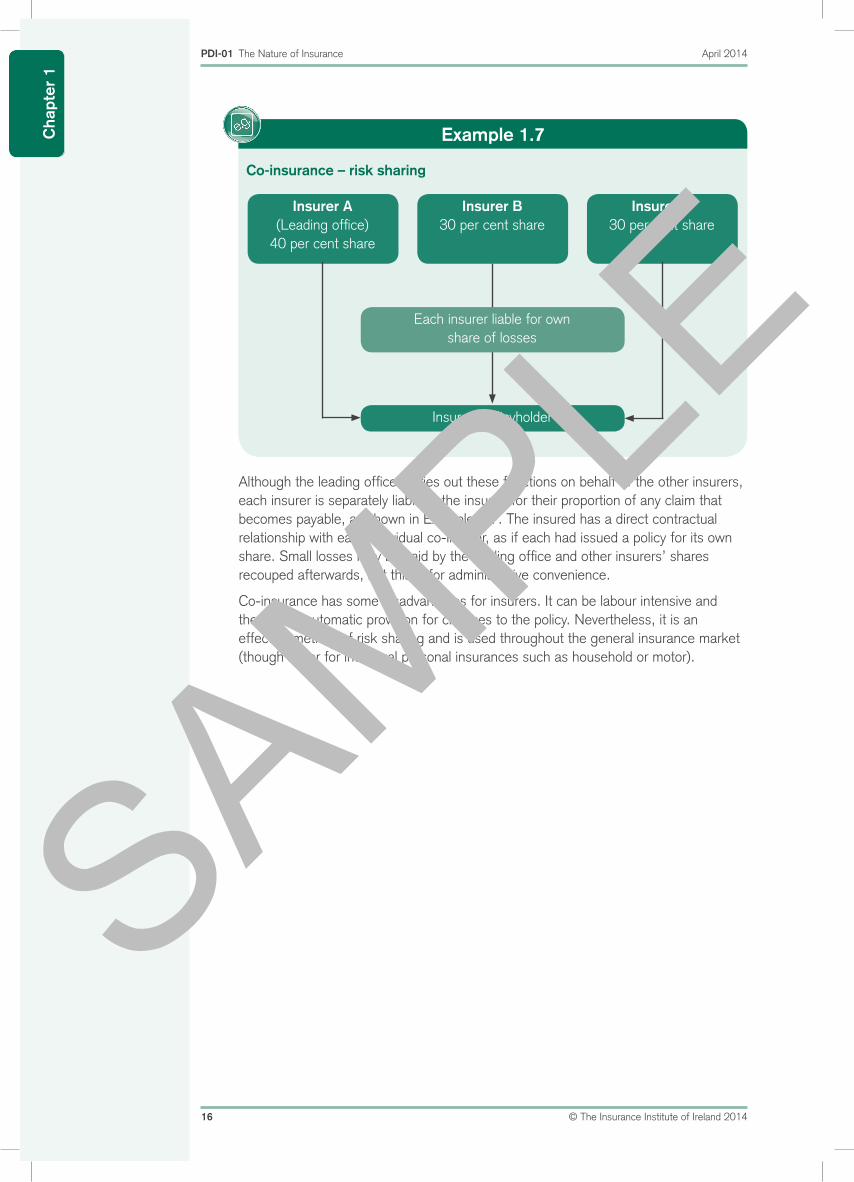

of co-insurance. This involves an insurer agreeing with other insurers on the rating and terms to be applied and issuing what is known as a collective policy. Each insurer receives a stated proportion of the premium and pays the same proportion of any losses that occur. The insurer holding the largest share of the risk is referred to as the ‘leading office’. It is the first insurer named on the policy and may receive a lead office fee from the other co-insurers on more complex risks. The leading office is responsible for issuing the documentation, surveying the risk and pricing renewal business, although the agreement of co-insurers is necessary before this information is conveyed to the policyholder. Another important function of the leading insurer is to review and comment on claims prior to notification of co-insurers. Consider Example 1.7.

co-insurance

proportional risk-sharing between insurers

SAMPLE

PDI-01 The Nature of Insurance April 2014

16 © The Insurance Institute of Ireland 2014

Cha

pter

1

Example 1.7

Insurer A (Leading office)

40 per cent share

Insurer B 30 per cent share

Insurer C 30 per cent share

Each insurer liable for own share of losses

Insured/policyholder

Co-insurance – risk sharing

Although the leading office carries out these functions on behalf of the other insurers, each insurer is separately liable to the insured for their proportion of any claim that becomes payable, as shown in Example 1.7. The insured has a direct contractual relationship with each individual co-insurer, as if each had issued a policy for its own share. Small losses may be paid by the leading office and other insurers’ shares recouped afterwards, but this is for administrative convenience.

Co-insurance has some disadvantages for insurers. It can be labour intensive and there is no automatic provision for changes to the policy. Nevertheless, it is an effective method of risk sharing and is used throughout the general insurance market (though never for individual personal insurances such as household or motor).

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 17

Chapter 1

E SummaryThis chapter introduced the concept of risk and its relationship with insurance. We examined the different aspects of risk and identified how insurance operates as a risk transfer mechanism.

In Chapter 2, we will continue to examine the relationship between insurance and risk. We will consider the main features of insurable risks and the ways in which insurance products provide protection from the main risks faced by individuals and businesses.

Login to iiiConnect via the Member Area Login at www.iii.ie. This resource should form an important element of your study and examination preparation. It includes a personalised learning plan containing a wealth of online supports e.g. interactive e-learning, webinars, automated study planner, exam countdown timer, key points per chapter, online mock exam assessments for Multiple Choice Question exams,

study tips guide and discussion forums.

Study andexamination

supports

SAMPLE

18 © The Insurance Institute of Ireland 2014

SAMPLE

Chapter 1

© The Insurance Institute of Ireland 2014 19© The Insurance Institute of Ireland 2014 19

Chapter 1 Introduction to insuranceC

hapter 1 End of chapter questions1. Provide a definition of ‘risk’.

2. State what it means to say that insurance is a ‘risk transfer’ mechanism.

3. In an insurance context, define what is meant by the level of risk.

4. Briefly describe the usual relationship between frequency and severity.

5. Provide an example of an aspect of insurable risk that is likely to affect the frequency of loss.

6. Define:

• peril

• hazard.

7. Define the term ‘moral hazard’.

8. Define the term ‘physical hazard’.

9. State what is needed for risk pooling to operate effectively.

10. List the two main ways in which insurers share risks.

SAMPLE

PDI-01 The Nature of Insurance April 2014

20 © The Insurance Institute of Ireland 2014

Cha

pter

1

Answers to end of chapter questions1. The uncertainty of future events and their outcome.

2. The accepting of an unknown future potential risk by an insurer for an agreed premium.

3. How often an event happens (frequency) and the extent of damage when it does happen (severity).

4. In many risk situations, we see a standard relationship between frequency and severity. There is a high frequency of low-severity losses and a low frequency of high-severity losses.

5. Any one of the following:

• motor insurance – age and driving experience of the driver (reflecting the likely number of risky manoeuvres)

• property insurance – industrial processes (making fire or explosion a more likely occurrence)

• employers liability insurance (for injury to employees) – unguarded machinery (making the risk of injury more likely)

• bicycle insurance – inadequate security when unattended (resulting in theft being more likely).

6. The definitions are:

• peril – a contingency that gives rise to a loss or liability

• hazard – any feature that influences the operation of the peril, either in its likelihood of occurrence or its severity.

7. The term ‘moral hazard’ refers to the attitude and conduct of people.

8. Physical hazard relates to factual characteristics and includes any measurable dimension of risk.

9. Homogeneous risks properly classified so that the law of large numbers can operate effectively.

10. The two main ways in which insurers share risks are co-insurance and reinsurance.

SAMPLE

Chapter 1 Introduction to insurance

© The Insurance Institute of Ireland 2014 21

Chapter 1 Answers to quick questions

1. Although we know that we will all die at some time, the uncertainty relates to the timing of our death.

2. ‘What is the maximum cost of an incident occurring?’

3. The following are examples but you may have thought of others:

• motor – fitting of an alarm/immobiliser

• household – installing a fire extinguisher/smoke alarm/fire blanket

• commercial theft – use of a commercial firm to provide overnight surveillance.

4. Quite often, poor moral hazard will be accompanied by a poor physical aspect to the risk, which can cause confusion.

5. The law of large numbers only works effectively when there is homogeneity of risk. We cannot simply increase numbers of risks grouped in a pool if it is at the expense of similarity of risk characteristics.

SAMPLE

SAMPLE

Chapter 2

Chapter aim

This chapter explores how risks are classified to determine whether or not they can be insured. It identifies the main characteristics of insurable and uninsurable risks. This provides the basis for identifying the insurable risks faced by consumers and the products developed to provide protection from those risks.

© The Insurance Institute of Ireland 2014 23

Insurability of risks

Chapter

2

SAMPLE