introducing wood pellet fuel to the uk etsu …

TRANSCRIPT

INTRODUCING WOOD PELLET FUEL TO THE UK

ETSU B/U1/00623/REP

DTI/Pub URN 01/1014

ContractorRenewable Heat & Power Ltd

Prepared byR.A Cotton A. Giffard

The work described in this report was carried out under contract as part of the DTI Sustainable Energy Programmes, with support from the European Commission’s ALTENER programme. The views and judgments expressed in this report are those of the contractor and do not necessarily reflect those of the DTI or the European Commission.

First published 2001 © Crown copyright 2001

INTRODUCING WOOD PELLET FUELTO THE UK

Executive Summary

Introduction

Wood Pellets are now a major fuel resource for heating in many parts of Europe as well as in the US and Canada. Wood pellet-fired heating also has the potential to make a significant contribution to the energy needs of the UK.

The wood pellet industry has been established in Scandinavia and North America for over 20 years and consequently wood pellet-fired appliances are now highly reliable, with many tens of thousands of systems in operation ranging in size from 10kW up to more than a MW.

Wood pellet boilers and roomheaters are highly automated. They have automatic ignition and are well suited to meet varying load demands. All pellet appliances have thermostatic controls or can be operated on a timer. This means that the level of convenience is equivalent to that of oil fired heating systems, but wood pellets have added environmental and local economic benefits. Because the rate of fuel feed and amount of combustion air are controlled precisely, pellet appliances achieve very high efficiencies (typically 90%+), comparable to that of an oil-fired system.

Wood pellets are compressed wood made usually from sawdust and shavings. However, they can potentially made from any biomass material (e.g. straw, forestry residues, specially grown energy crops etc.) and hence have the potential to be sourced from locally unused material, which can give considerable benefit to the local economy.

At the start of the project “Introducing Wood Pellet Fuel to the UK”, the use of wood-fuel pellets was largely unknown in the UK. There was no fuel- pellet production capacity, nor any pellet appliances on the UK market to burn pellets. This project has addressed a wide range of technical and nontechnical issues to help establish a wood pellet industry in the UK.

Aims and Objectives of the ProjectThe overall aim of the project was to help establish a wood pellet industry in the UK. This aim was achieved by:

• Reviewing the historic growth and current status of the wood pellet industry in other European countries and North America.

• Reviewing UK standards, legislation, and regulations and developing UK voluntary standards for biomass pellets and appliances.

• Identifying and quantifying markets for pellet heating in the UK.

A1..i.

• Organizing a series of workshops, seminars and other events to demonstrate pellet burning appliances in order to raise awareness of the technology.

• Carrying out trial pelletisation of a variety of biomass feedstocks available in the UK and helping to establish fuel pelletising facilities within the UK.

• Helping establish a number of demonstration installations of pellet-fired appliances.

• Undertaking a promotional campaign for wood pellet fuel.

• Compiling resource directories for pellet fuel and pellet burning appliances in the UK.

Summary of the Work Carried OutThe work programme was comprised of three phases:

Phase 1. Reviewing existing pellet markets, the potential market within the UK and the identification and engagement of interested parties in the UK.

A review of how the wood pellet industry became established in other European countries and in North America and the current status of those industries was carried out. Interested parties in the UK were identified and a Biomass Pellet network was established by British BioGen consisting of approximately 250 names of interested individuals. Standards, Legislation and Regulations effecting the production and use of wood pellet fuel in the UK and wood pellet appliances were reviewed. An overview of the potential markets for biomass pellet appliances in the UK was investigated. The first UK Seminar on Wood Pellet Fuel was held in Nottinghamshire in Sept 1999.

Phase 2. Identification of resources and potential heating sites and pelletisation trials

An assessment of biomass resources in the UK was undertaken which looked at the following potential feed-stocks; primary processing residues and secondary raw materials, recovered wood and biomass waste, forestry residues and energy crop products and straw. A more detailed resource survey was carried out in South Wales and the South West. A programme of identification and quantification of markets was carried out in South Wales and the South West. Pelletisation trials were carried out using a range of pelletisation equipment and a range of biomass feedstocks that are found in quantity in the UK.

A1..ii.

Phase 3. Commercialisation of wood pellets, training and promotion campaign

Help was given on commercial considerations in terms of UK pellet production and installation of pellet-fired equipment. A number of training events were given to installers and service engineers on brand-specific pellet burning equipment. A series of events were held where wood pellet technology was explained and demonstrated and a promotional campaign was undertaken to raise general awareness of the use of wood pellet fuel.

Summary of the Main Results

This project has achieved all of the following:

• Development of UK voluntary standards for wood pellet fuel and combustion appliances.

• The first seminar dedicated to wood pellets in the UK was held with experts from Sweden, Austria, the US, Italy and the UK presenting papers. This attracted over 130 people from around the UK and a conference proceedings was published and widely disseminated.

• A database of about 250 individuals in the UK with an interest in wood pellet fuel has been compiled.

• Help was given in the establishment of a number of sources of UK manufactured wood fuel pellets including the construction of a 5tonne/hour pellet mill in South Wales.

• Pelletisation trials on equipment suitable for pellet production in the UK at a number of scales, using a wide variety of biomass materials available in the UK, have been undertaken including preliminary trials using a grass mill for the seasonal production of wood pellet fuel.

• Agreements have been made with a number of pellet stove and boiler manufacturers and UK companies to import equipment into the UK and a number of UK companies are currently developing pellet appliances.

• About a dozen pellet burning appliances are now operating in the UK with many planned to be installed over the next year.

• Six heating engineers have been trained in the general installation of wood pellet-fired appliances and in brand-specific appliances.

• An analysis has been made of the economics of wood pellet fuel in a UK context.

• A general resource assessment has been compiled for the UK and a detailed resource assessment for two specific regions of feedstocks for biomass pellets.

• A promotional campaign is underway, both for brand-specific equipment on a local level and generic promotion of the concept of heating with wood pellets at a national level.

Al.iii

• A centralized information service and website has been set up dealing with all aspects of promoting wood pellet fuel.

• Close links have been established with Trade Associations, “Pellet Clubs” and companies involved with pellet production or pellet appliance manufacture in Europe and North America.

Conclusions

The project “Introducing Wood Pellet Fuel to the UK” has been a success. There are now a number of groups either producing wood pellet fuel or planning to produce wood pellet fuel in the near future. These include a 1 tonne/hr pellet mill currently operating, a 5tonne/hour machine due to start production in towards the end of 2001 and a modified grass mill with capacity for about 6,000 tonnes of wood pellets per annum which has successful produced wood pellets.

There exists a large potential for a low cost feedstock of clean wood waste coming out of the waste sector. However, it is clear from pelletisation trials from this project and elsewhere that a critical issue in the acceptance of these materials is quality control procedures to ensure that there are no contaminates within the feedstock.

The lack of an organization in the UK with a specific remit to promote the use of wood pellet fuel at all levels will retard the expansion of the wood pellet industry in the UK. Most European countries now have a “Pellet Club” - a trade association for the wood pellet industry.

The current Building Regulations (Document J) have not taken account of the coming into being of a class of forced draft appliances of low output such as pellet fueled roomheaters. The present minimum recommended size of 125mm diameter for any solid fueled appliance is inappropriately oversized for most pellet stoves and also represents an unnecessary cost burden.

In general, the economics of wood pellet fuel in the UK look promising. Wood pellet fuel is competitive with oil and LPG in the UK at the time of writing although the higher capital cost of pellet-fired appliances compared to fossil fuel boilers is a major barrier to the expansion of the wood pellet industry in the UK.

The favourable fuel costs coupled to the environmental benefits of heating with wood fuel and the fact that the wood pellet industry could make a substantial contribution to the rural economy, would imply that an emerging wood pellet industry in the UK has a good chance of becoming a major renewable energy sector.

A1.iv

Recommendations

A number of actions are required to help the expansion of the wood pellet industry in the UK over the next few years.

• The introduction by the UK government of a capital grant scheme for biomass heating systems.

• More work on Quality Assurance schemes to ensure that waste wood from the waste handling sector is reliably sorted to exclude any material not complying with the present and likely future European descriptions for “biomass fuel”.

• Generic promotion at all levels of the use of sustainably produced biomass fuels in substitution for fossil fuels.

• Encouragement of R & D by grants to UK appliance and boiler manufacturers to develop new combustion hardware.

• Undertake work with the Building Research Establishment to confirm the suitability of 100mm flues and chimneys for pellet fueled roomheaters.

The wood pellet industry has the potential to be a substantial industry in the UK over the next few years. The examples of other countries suggests that pellet fuel is by its nature sufficiently specialized that it requires its own generic promotion and there are European initiatives to accomplish this which the UK should support.

The role of a Pellet Trade Association, or a specialized sub-section of an existing Trade Association would be the following:

• Run a central information service on all aspects of wood pellet fuel including lists of manufacturers of appliances and suppliers of wood pellet fuel.

• Develop an accredited training programme in wood pellet heating, covering both pellet stoves and central heating systems, similar to that of the CORGI training for gas-fired appliances in the UK and the Heath Education Foundation in North America.

• Represent the Wood Pellet Industry’s interests at National government and local government level.

• Develop and refine standards on pellet fuel and appliances to comply with the latest legislation.

• Co-ordinate all promotional activities of wood pellet fuel.

A1..v.

In addition, an R&D programme is needed on specific activities. These include

• Seasonal conversion of grass mills and sugar beet mills to wood pellet production.

• Distribution and delivery of wood pellet fuel to customers in the UK at various scales.

• Quality Control procedures for wood residues from the waste sector, which may open up new resources for pellet production.

A1..v..i.

Contents Page

Executive Summary1 Introduction 1

2 Standards, Legislation and Regulations 22.1 Review of Industry Standards 22.2 Regulations for Pellet Burning Equipment 22.3 UK legislation & regulations of materials for pellets 2

3 Reports on national pellet markets; Sweden, Austria and the US 5

4 Suppliers of Pellets, Pelletising Equipment and Appliances 5

5 One-day Seminar on Wood Pellets in the UK 6

6 Potential Feed-stocks for Biomass Pelletisation in the UK 76.1 National UK Biomass Residue Resource 76.2 Feedstock for Pelletisation Somerset and Devon 106.3 Feedstock for Pelletisation in South Wales 14

7 The Economics of Biomass Pelletisation in a UK Context 167.1 The Economics of the Heating Market in the UK 167.2 The cost of production of wood pellets in the UK 20

8 Trial Pelletisation 258.1. EcoTre Pellet Mill 268.2. Farm Feed Pellet Mill (25hp) 308.3 Conversion of a Grass Mill to a Wood Pellet Mill 32

9 Market Development Strategy 359.1 Survey of reactions to pellet-fired heating 359.2 Market Development Strategy for Biomass Pellets 36

10 Conclusions 37

11 Recommendations 38

Appendix 1 Commercialisation report

Appendix 2 Codes of Good Practice for Pellet fuel

Appendix 3 Pellet fuel standards in Sweden, Austria and the US

Appendix 4 Codes of Good Practice for roomheaters

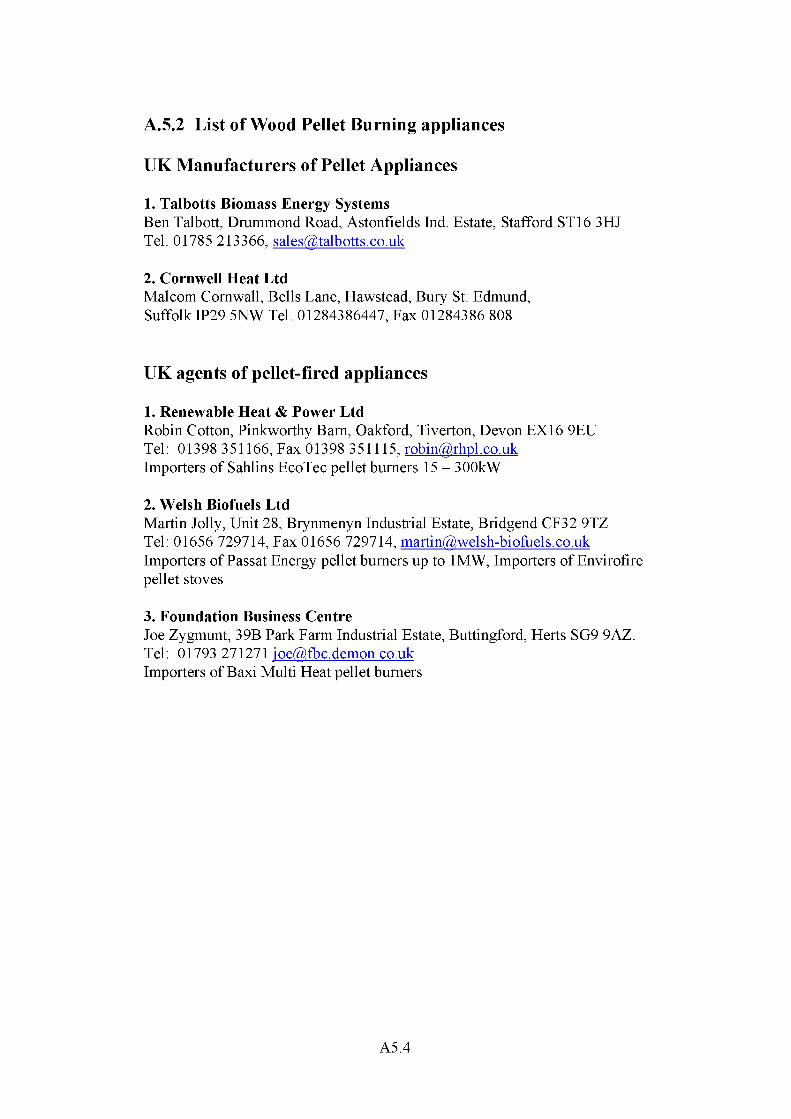

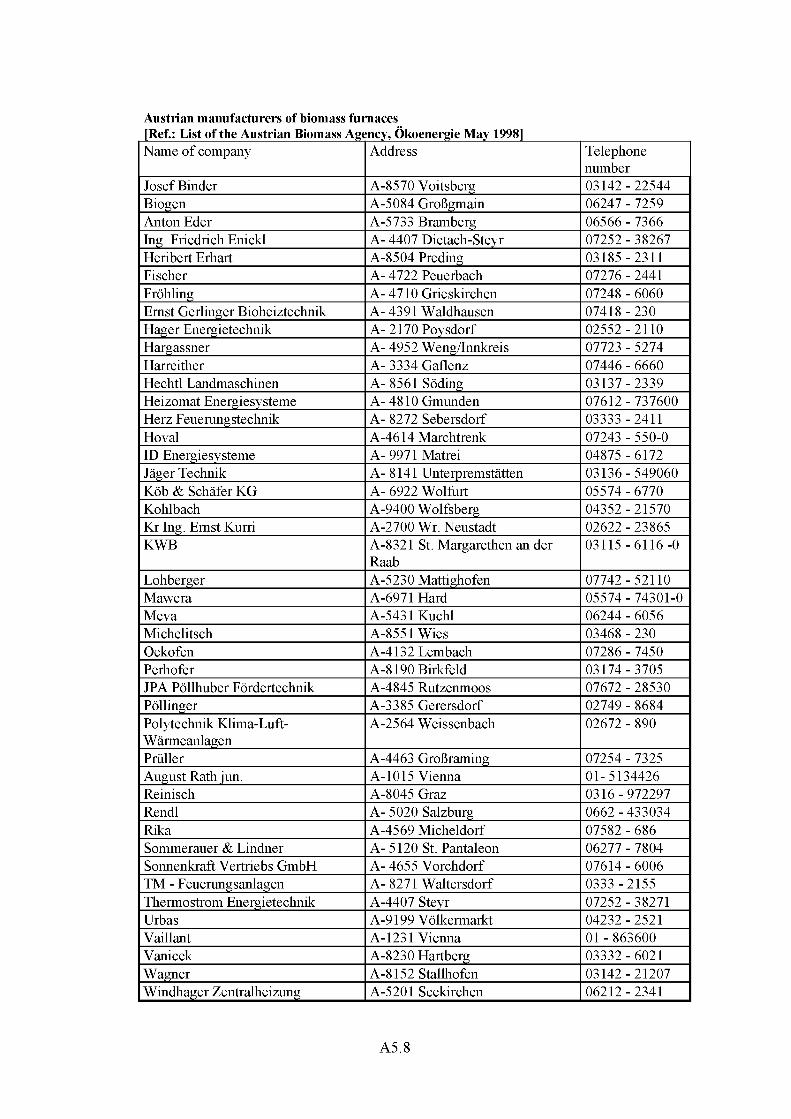

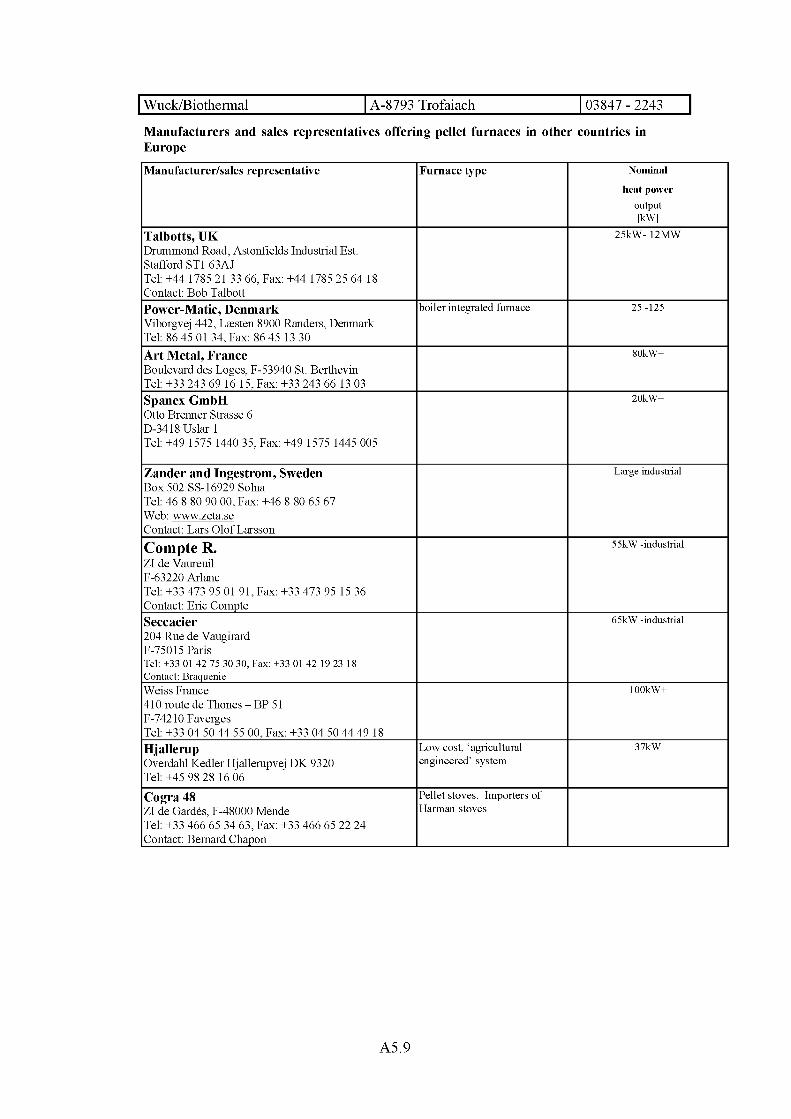

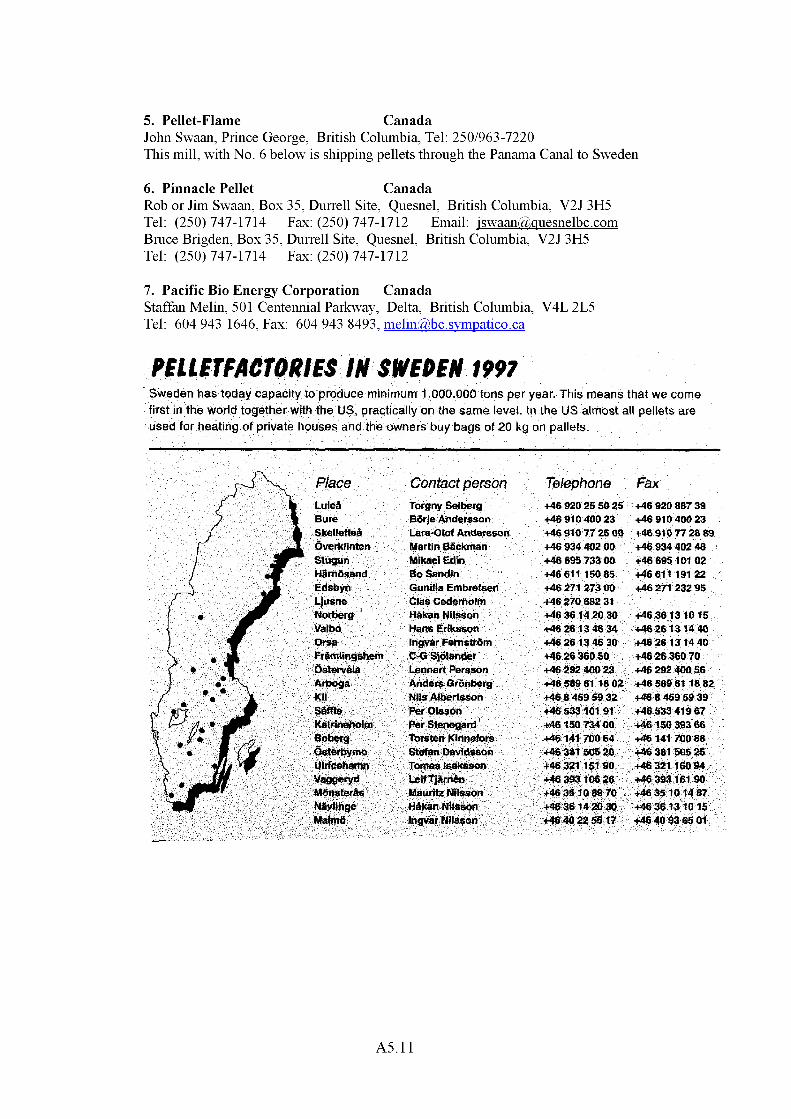

Appendix 5 List of suppliers of pellet mill machinery, pellet suppliers in the UK and abroad and pellet-fired heating appliances (stoves and stoker/boilers)

Appendix 6 Programme for “Introducing Wood Pellet Fuel to the UK” seminar

1. INTRODUCTION

Wood Pellets are now a major fuel source for heating in many parts of Europe as well as in the US and Canada. Wood pellet-fired heating also has the potential to make a significant contribution to the energy needs of the UK.

There is a wide range of potential biomass feedstocks for fuel use which vary in nature, particle size, shape and moisture content. The use of these feedstocks for the production of wood pellets results in a low moisture, high density fuel of small particle size (commonly 6-12mm diameter). This fuel is well suited to being used in automatic heating systems and allows a consistent fuel quality to be achieved.

The wood pellet industry has been established in Scandinavia and North America for over 20 years and consequently wood pellet-fired appliances are now highly reliable, with many tens of thousands of systems in operation in Europe ranging in size from 10kW up to more than a MW.

Wood pellet appliances are highly automated and have automatic ignition and are well suited to meet variable load demands. All pellet appliances have thermostatic controls and can be operated on a timer. This means that the level of convenience is equivalent to that oil fired heating systems, but wood pellets have added environmental and local economic benefits. Because the rate of fuel feed and amount of combustion air are controlled precisely, pellet appliances achieve very high efficiencies (typically 90%+), comparable to that of an oil-fired system.

Wood pellets are compressed wood made usually from sawdust and shavings. However, they can potentially made from any biomass material (e.g. straw, forestry residues, specially grown energy crops etc.) and hence have the potential to be sourced from locally unused material, which can give considerable benefit to the local economy.

At the start of the project “Introducing Wood Pellet Fuel to the UK”, the use of wood-fuel pellets was largely unknown in the UK. There was no fuel- pellet production capacity, nor any pellet appliances on the UK market to burn pellets. This project has addressed a wide range of technical and nontechnical issues to help establish a wood pellet industry in the UK.

A1..1.

2 STANDARDS, LEGISLATION AND REGULATIONS

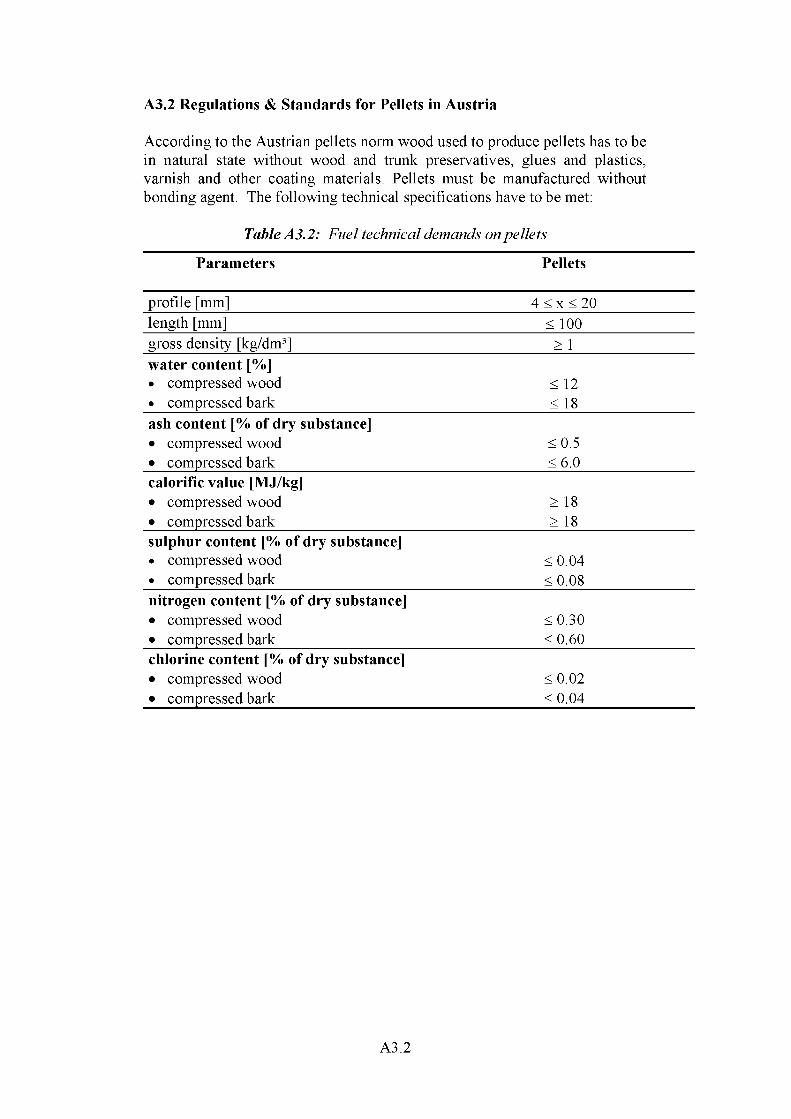

2.1 Review of Industry StandardsStandards on wood pellet fuel have been independently developed in the US, Sweden, Austria and Germany. Although there is some variation between the various standards, there is fairly close agreement on the main characteristics, for example, moisture content, calorific value, etc. These standards have been used as a starting point for the development of a voluntary UK standard.

A Biomass Pellet Technical Committee was set up which was comprised of sixteen people from industry, chosen from about 250 on the project database, who had a broad range of interests in wood pellet fuel e.g. potential pellet producers, heating equipment manufacturers etc. This committee met twice during the project and developed a code of good practice for wood pellets for the UK. This is given in Appendix 2. The Swedish, Austrian standards and US wood pellet standards are given in Appendix 3.

2.2 Regulations for Pellet Burning Equipment.A code of good practice for pellet room heaters (COGPP) has been developed for the UK which has used as a basis the P-mark certification programme in Sweden and the US standard ASTM 1509-95. The former is a voluntary standard existing in Sweden whereby a product can be granted permission to display the P Mark- symbol after certification by SP, the Swedish National Testing and Research Institute. Such certification involves verification that the product fulfils applicable requirements in respect of standards, codes of practice for the sector concerned, regulations etc., and that there is verified and approved continuous inspection and quality control of production.

The certification rules describe the conditions for certification, technical requirements and requirements for continuous inspection and quality control of pellet stoves. The technical requirements include characteristics to guarantee minimum levels of safety, efficiency and reliability as well as maximum emission levels. Details of the COGP for roomheaters are given in Appendix 4.

2.3 Review the UK legislation and regulations of materials for pelletsBritish Biogen, in collaboration with other partners, wrote a position document on the regulations governing materials for pelletisation for submission to DETR/EA. It continues to be difficult to get definitive guidance from EA/DETR until a ruling emerges from the European Court of Justice. There is also work being done by a CEN Technical Committee on “recovered fuels” which is not expected to be completed for some time.

The types of material that may be used to manufacture biofuel pellets and the types of combustion equipment for those pellets, will be heavily influence by the 'waste status' of the material, the types of any material other than biomass that it might contain and the 'traceability' of the material.

A1..2.

So far as legislation and regulation are concerned there are four key issues:

■ Will the material be subject to the new Waste Incineration Directive?■ Is the feedstock defined as a waste?■ Can a waste be made into a fuel that can be burned without a Waste

Incineration Licence?■ Is it desirable to make biofuel pellets out of waste feedstocks?

It is currently somewhat less than clear what feedstock is a waste and what is not, the EU Waste Framework Directive defines it as 'any substance or object ... which the holder discards or intends or is required to discard.'

There is a range of regulations and guidance regarding the definition of waste in the UK. As yet however there is no definitive guidance as to what types of biomass feedstocks are currently defined as waste and if and how those feedstocks might be recycled into a non-waste product.

The draft Waste Incineration Directive however specifically excludes, amongst other materials:

■ vegetable waste from agriculture and forestry■ wood waste with the exception of:

o those that may contain halogenated organic compounds or heavy metals as a result of treatment;

o treated wood originating from building and demolition waste,

The whole area of biomass fuels and waste, and the manufacture of biomass fuels from biomass wastes is currently subject to some debate. As the development of EU standards for solid biofuels moves forward, DG XI have softened their position on the manufacture of fuels from waste and are currently considering when a waste may become a product. In addition, various other rulings of the EU may apply. CEN technical Committee on “Solid Recovered Fuels” (CEN/BT/TF118) are working on these issues.

2.3.1 Waste Management LicensingA pellet mill that takes and recovers waste wood material will need the appropriate Waste Transport and Management Licenses. This involves some cost but may also allow the mill to take in packaging waste for recovery, such as clean pallets, and issue Packaging Recycling Notes (PRNs), which will have some value.

A1..3.

2.3.2 Biofuel Feedstocks:It is important to ensure that biofuels are manufactured from appropriate materials and to sensible product standards to ensure that problems of poor appliance reliability, emissions problems and potential health risks are avoided. This requires the Biofuel Pellets Network and wider industry to take a precautionary approach to the selection of pellet feedstocks.

Although it was initially proposed that there be two categories of feedstock for biofuel manufacture, the final decision made by the Biomass Pellet Technical Committee is that the Voluntary Standard for Biofuel Pellets should only include wood pellets made of 100% pure wood with no materials otherthan Biomass (such as resins used in making plywood, MDF and chip board)

2.3.3 Relevant waste legislation:Council Directive 75/442/EEC, amended by Council Directives 91/156/EEC and 91/692/EEC is commonly known as the Framework Directive on Waste. In the UK waste definitions and controls are legislated for in section 30(1) of the Control of Pollution Act 1974 and its reenactment in sections 75(1) and 75(3) of the Environmental Protection Act 1990.

The Packaging Waste Directive gives provision for the issue of PRN’s. Currently about 50% of all wood packaging now comes under the scheme. PRN's are likely to be issued by wood packaging processors rather than the end user which gives the possibility that pellet mills may be able to issue PRN's.

Following the adoption of the Waste Framework Directive the UK Government has decided to replace UK definitions of waste with that used by the directive. Primary legislation will be required to amend the 1990 act but for the time being the change has been applied through amendments to the Waste Licensing Regulations 1994.

The most recent guidance on the application of waste legislation and regulation is given in joint circular DoE 11/94.

The most recent guidance on waste definitions is given in the DETR note 'The Definition of Waste' of 27/11/98.

The forthcoming Directive on the Incineration of Waste specifically excludes most biomass feedstocks and may therefore set a precedent for what feedstocks may be used for the production of pellet fuels which are not subject to waste incineration regulations.

The Framework Directive on Waste is under continuous review by the Technical Adaptation Committee with possible implications for biomass feedstock and fuel use.

A1..4.

2.3.4 Non Waste combustion:Currently the combustion of 'non-waste' wood fuel is regulated in the UK by the Clean Air Act 1993 with notice to be given to Local Authorities and basically a requirement that "... furnaces shall be so far as practicable smokeless”'. There are tighter restrictions on appliances and fuels used in urban Smoke Controlled Areas.

3 REPORTS ON NATIONAL PELLET MARKETS; SWEDEN, AUSTRIA AND THE US

Separate reports were compiled on the current markets for wood pellet fuel in Sweden, Austria and the US, which included a historic perspective to show how the industry evolved in each country and the main factors determining the expansion.

The report on the wood pellet industry in Sweden and the report of the wood pellet industry in North America are available from the British Biogen website. A report on wood pellets in Austria is contained in the conference proceedings for the one day seminar “Introducing Wood Pellet Fuel to the UK”, Bought on Sept 1999. This is available from the British Biogen Web site1.

A document entitled “Wood Pellets in Europe” was published in January 2000, funded by the European Commission DG XVII under a Thermic B project2. This report gives details of the wood pellet industries in Sweden, Norway, Germany, Austria and North America.

4 SUPPLIERS OF PELLETS, PELLETISING EQUIPMENT AND APPLIANCES

Three separate databases have been compiled containing a list of suppliers of the following:

a) Wood pellet fuel

b) Equipment for the production of wood pellets

c) Pellet-fired heating appliances (roomheaters and stoker/boilers)

These databases include companies from the EU and the US and are given in Appendix 5.

1 www.britishbiogen.co.uk2 Wood Pellets in Europe, published by the Industrial Network on Wood Pellets, January 2000, EU reference Thermic B DIS/2043/98-AT, edited by UMBERA GmbH, email umbcraVv.via.at

A1..5.

5 ONE-DAY SEMINAR ON WOOD PELLETS IN THE UK

The first seminar dedicated to wood pellets in the UK was held at Bought on pumping station on September 22nd 1999. The one day seminar “Introducing Wood Pellet Fuel to the UK” was organised by Renewable Heat & Power Ltd with British Biogen.

The seminar drew together experts from The US, Sweden, Austria, Italy and the UK to look at how substantial markets for wood pellets have evolved in other countries and to discuss the potential for establishing a pellet fuel market within the UK.

There was strong interest in the seminar and it attracted over 130 people from a wide variety of backgrounds including solid fuel appliance manufacturers, sawmill owners, waste companies, foresters etc. A 45 page seminar proceedings has been published containing papers from leading experts on all aspects of the wood pellet fuels industry from the US, Sweden, Austria, Italy and the UK.

The papers include an overview of wood pellet markets abroad, pellet standards, current economics, the energy balance of pelletising, appliance standards, pellet mill construction and contains contacts for further information. The proceedings were distributed free of charge to all delegates who attended the seminar. The seminar programme is given in Appendix 6. A copy of the conference proceedings is available from the British BioGen Website www.britishbiogen.co.uk.

A1..6.

6 POTENTIAL FEED-STOCKS FOR BIOMASS PELLETISATION IN THE UK

6.1 National UK Biomass Residue ResourceFor the purpose of this section of the report, the potential feed-stocks have been divided into four categories, namely;

1. Forestry and Energy Crop Products2. Straw3. Primary Processing Residues and Secondary Raw Materials4. Recovered Wood and Biomass Waste

6.1.1 Forestry and Energy Crop ProductsForestry and Energy Crop Products include Round wood and whole tree chips, wood brash and residue chips, energy crops; short rotation coppice, miscanthus, whole crop hemp & various others. The recent report “New and Renewable Energy: Prospects for the 21st century: supporting Analysis” by ETSU for the DTI3 suggest the following current and future resources:

Table 1: Estimated Current and Future Forest Residues.

per year)Wood Fuel Resource (1000’s dry tonnes

1998 2013Residues and Residuals 309 660Dedicated Wood Fuels 148 380Broadleaf Woodland 203 203Arboricultural arising 484 484TOTAL 1,144 1,728Source ETSU Report R-122 (rounded to nearest 1000 tonnes)

An estimated 1.1 million dry tonnes of wood is available from forestry residues, thinning operations, whole tree harvesting, broadleaf woodland management and arboricultural arisings. As the UK forestry industry enters a major harvesting phase over the next 20 years, roundwood production is expected to double, along with sawmilling capacity and the forestry residue resource. Energy crops are not yet a major source of wood fuel in the UK with just over 900 hectares planted to date. British Biogen suggest that establishing 125,000ha of energy crops should be a realistic target by 2010 which would producing approximately 1.5 million tonnes of wood fuel per year.

An energy crops scheme has been introduced which gives grants to establish energy crops and to assist the set up of producer groups. A total of £30million has been allocated over 7 years.

3 ‘New and Renewable Energy: Prospects for the 21st century: supporting Analysis’, ETSU R- 122, March 1999, Harwell, Oxon

A1..7

6.1.2 Straw:Straw is probably the largest single resource in the UK at the present time with over 6 million tonnes presently unused and hence, in principle, accessible for energy use. There is a strong geographical variation in the production and usage of straw. For example Wales is net importer of almost 1 million tonnes whilst England produces a surplus of about 4.4million tonnes. The regional distribution of use and production of straw is given in table 2:

Table 2: Regional Distribution of Straw Produced and Used.

(1000’s tonnes per year at 15% moisture) Total straw Total straw Total strawproduced used unused

Yorkshire & Humberside 1,491 877 614East Midlands 1,938 618 1,320East Anglia 1,840 371 1,469South East 2,352 749 1,603West Midlands 950 737 213Grampian 526 253 273Tayside 334 99 235TOTAL 9,431 3,704 5,727Source ETSU Report R-122. Excludes regions with less than 200,000 tonne surplus

While there is clearly an abundance of straw in certain regions and hence would represent a low cost feed-stock and straw is a clean material and so would classify as ‘biomass’, it does have fairly high ash content with a low melting temperature. This means that burning straw may result in ‘clinker’ formation and therefore straw pellets will usually require specialist combustion equipment and be an unsuitable fuel for use in domestic scale appliances which have been designed to operate on fuel with an ash content below 1%.

6.1.3 Primary Processing Residues and Secondary Raw Materials:This includes residues from sawmills, timber production and other wood processing industries which are estimated to have produced some 1.1 million tonnes of sawdust, shavings and off-cuts in 1997. As wood production and sawmilling in the UK grows, so too will processing residue production, perhaps to some 2 million tonnes by 2010.

A1..8.

6.1.4 Recovered Wood and Biomass WasteThis is an interesting category of wood waste as it does includes a substantial amount of good, dry woody material that may be available at low or zero cost but which may also contain materials other than biomass. This feedstock might include;

■ Furniture factory waste■ Wood packaging waste■ Construction industry wood waste■ Wool & cotton waste from textile industry■ Sludge from papermaking.■ Wood panels industry waste■ Demolition wood waste■ Paper and cardboard waste

Total industrial and commercial waste from 'textiles, wood and paper' is estimated at some 9 million tonnes per year. The Environment Agency estimates that perhaps 1 million tonnes of wood packaging waste is produced in the UK each year. Of this about 115 thousand tonnes was recovered for use in 1997, almost all of it in chipboard manufacture.

The DETR have recently published two documents entitled Waste Management Statistics and Waste Strategy 2000, both of which are available via the Internet at:

http://www.environment.detr.gov.uk/wastats/mwb9899/index.htm

http://www.environment.detr.gov.uk/waste/strategy/cm4693/index.htm

From the end of 1999 those recycling wood packaging will be able to issue Packaging Waste Recovery Notes, or PRNs. This is expected to encourage a far greater use of recycled wood packaging in the board industry.

The Landfill Directive will require increasing quantities of 'organic' material to be diverted from landfill, a reduction to 35% of 1995 levels by 2016. How the Directive is to be implemented in the UK remains to be seen but there is increasing emphasis, in the Draft Waste Strategy and elsewhere, on the recovery of material from the waste stream.

Wood pellets have been produced from the fines arising from “clean” wood waste in Durham County and during pelletisation trials on a small scale pellet mill (see section 8). From these trials it has become apparent that quality control procedures are of critical importance to ensure that the resulting feedstock for pellet production are free from materials other than biomass as required by the EU definition of “Biomass” and the UK Code Of Good Practice for pellets.

AE.9.

6.1.5 Conclusions on national biomass feedstocks• The expected rise in UK timber production, the deployment of energy

crops, the application of the Packaging Regulations to wood packaging and the implementation of the Landfill Directive may all be expected to increase the volume of wood and wood residues available.

• Current prices for 'clean woody materials' collected for the pulp and board industries would seem to be in the region of £20 per green tonne. However, some mills require that material of less than 3mm is screened out and some use only virgin chip material.

• There is also a substantial straw resource available that might be used to manufacture pellets for industrial and commercial heat and CHP installations.

• In practice the resource needs to be looked at in detail for particular regions to see what is available where, in what form and at what price.

6.2 Feedstock for Pelletisation in Somerset and Devon

6.2.1 Wood Waste Potential in SomersetThe wood waste potentially available for pelletisation in Somerset has been estimated using the following methods:

• Hand sorting of representative samples of wood waste in the region• Previous work undertaken by Wyvern Waste Ltd (a project partner)• Compilation of a database of approximately 120 companies likely to

produce wood waste and the mail-shot of a questionnaire.

Two “ro-ro” skips of household wood waste from two separate Civic Amenity (CA) sites were sorted by hand into three categories. The two sites were Dimmer and Somerton, both owned by Wyvern Waste Ltd. The total amount of waste sorted was about 6 tonnes. Photograph 1 shows a typical sample of sorted wood waste.

The three categories used were:

(i) Class A: Clean wood waste.This material included clean pallets, joinery waste, unpainted furniture etc. This category specifically excluded chipboard, MDF and any wood waste with paints or preservatives.

(ii) Class B: Processed wood waste.This material included chipboard and MDF and also included some laminated material. The majority of the wood waste consisted of chipboard coated with white finish as is typical in low cost furniture. Again, any wood waste with paints or preservatives was specifically excluded.

A1.10

(iii) Other material ‘Class C’:This class contained all wood material which was excluded from Classes A and B. This included painted material and pressure treated wood, all of which may only be burned with a waste incineration licence.

Table 3: Breakdown of Results

Dimmer CA(tonnes)

Somerton CA(tonnes)

Class A 0.46 0.20Class B 1.64 1.38Class C 1.24 1.06TOTAL 3.34 2.64

Conclusions: The total amount of clean wood waste is around 10% of the total, 50% of the wood waste is in the form of chipboard or MDF and the remaining 40% is painted wood (old doors, windows, pressure treated wood etc).

The amount of time spent on sorting approximately 6 tonnes of waste was approximately 12 person hours, indicating that one person could sort % tonne in one hour. This is clearly a major problem in making economically viable the use of wood waste as raw material for pelletisation.

It should be noted that the wood waste in Sample 1 (Dimmer) had been heavily compacted and broken up into relatively small pieces, whereas Sample 2 (Somerton) had not been crushed and whole pallets were included in the sample. The time taken to sort Sample 2 was approximately half that of Sample 1 i.e. the uncrushed wood waste was much easier to sort.

The exercise of hand sorting waste wood and talking to people in the recycling/waste recovery business gave valuable insights into the commercial viability of utilising such wood waste materials. It is strongly argued that for wood waste from civic amenities to be used as commercial fuel (i.e. not under an incineration licence), sorting at source will be necessary.

A questionnaire was written and sent to about 120 companies in Somerset who were likely to produce significant quantities of wood waste. These included, Carpenters, Joiners, Sawmills, fencing manufacturers, packaging manufacturers etc. It also included some less obvious company types such as companies dealing with aircraft spares (two in Somerset) and paper mills all of which currently dispose of large quantities of wooden pallets to landfill.

The responses from the questionnaires, together with previous work by Gavin Leslie of Wyvern Waste Ltd, have been used to make an estimation as to the total wood waste available in Somerset. This is summarised in figure 1. It should be noted that there are additional companies producing significant

A1.11

quantities of wood waste who did not respond to our questionnaire. For example we later learned of a door manufacturer producing about a thousand tonnes of clean waste per year.

Tonnes Annual Available Wood Waste in Somerset

Figure 1: Annual available wood waste in Somerset

Photographs 2 shows waste pallets outside a packaging company in Somerset which are currently sent to landfill. This is typical of a number of companies in South West.

6.2.2 Wood Waste Potential in DevonThe questionnaire was then sent to 125 companies in Devon who were likely to produce significant quantities of wood waste. The response in general was lower than that of the mail-shot in Somerset, with only 21 companies replying. However, a significant number of sites where substantial quantities of wood waste are produced have been identified.

In particular, two large sawmill sites each producing approximately 2000 and 2500 tonnes/year of clean wood residues in the form of green slab wood and sawdust have been identified. The current price obtained for these residues is £5/tonne and £15/tonne respectively. In addition, ten sites have been identified, where between 75 to 200 tonnes/year of clean wood residues are produced. The current prices obtained for the materials are between +£ 15/tonne to -£30 (i.e. they pay to dispose of it). There are also several companies who have thousands of tonnes of clean pallets per year which they currently pay to dispose of to landfill. In Plymouth there is a recycling operation for wood waste where material is sorted to exclude painted material, then chipped as raw material for a board mill.. The chips are screened with all fines passing a 3mm screen sent to landfill. A sample of these fines was pelletised but it was clear from microscopic examination of the material that

A1.12

the chipping process concentrates contaminates such as paint and the resulting pellets are clearly not a biomass fuel.

6.2.3 Summary of resultsA large resource of clean wood residues in Devon and Somerset has been identified, amounting to over 10,000 tonnes per year, and we have compiled a database of almost 250 companies who currently produce some wood residues. In particular, about 20 sites have been identified where there is material in quantities of greater than 100 tonnes per year of clean wood residues, where the price currently obtained for this material is sufficiently low to make it suitable to be pelletised economically. Extrapolating the results from the sample of companies who replied to the total number of companies who were approached, this would imply a resource of about 50,000 tonnes per year, although this figure could be very much greater.

The smallest pellet mill that has been commercially successful in the US and in Sweden has been at a production rate of 5000 tonnes/year. Therefore, it is concluded that there is sufficient raw material in the South West, even excluding forestry residues, SRC and other agricultural materials (e.g. straw, flax etc).

However, the overriding conclusion from resource surveys is that although there is considerable resource, there is no single concentration of potential feedstock to justify the considerable investment required to set up a pellet mill facility. This problem has led to the idea of a Mobile Pellet Mill. The thought behind this is that, rather than transport low density raw materials to a central facility, the pellet mill would visit a number of sites throughout the year spending perhaps a few days or weeks at each site to pelletise the stored raw material and then either bagging on site or transporting the high density pellets in bulk to a local bagging plant.

A mobile pellet mill would allow a secure supply of locally produced pellets to be available to support the emerging market for wood pellet appliances. This idea could be extended beyond the South West to supply markets in other parts of the country to kick-start the industry there, in anticipation of fixed larger scale pellet mills once pellets are established in an area. The database of companies producing wood residues in Devon & Somerset is available on request.

A1.13

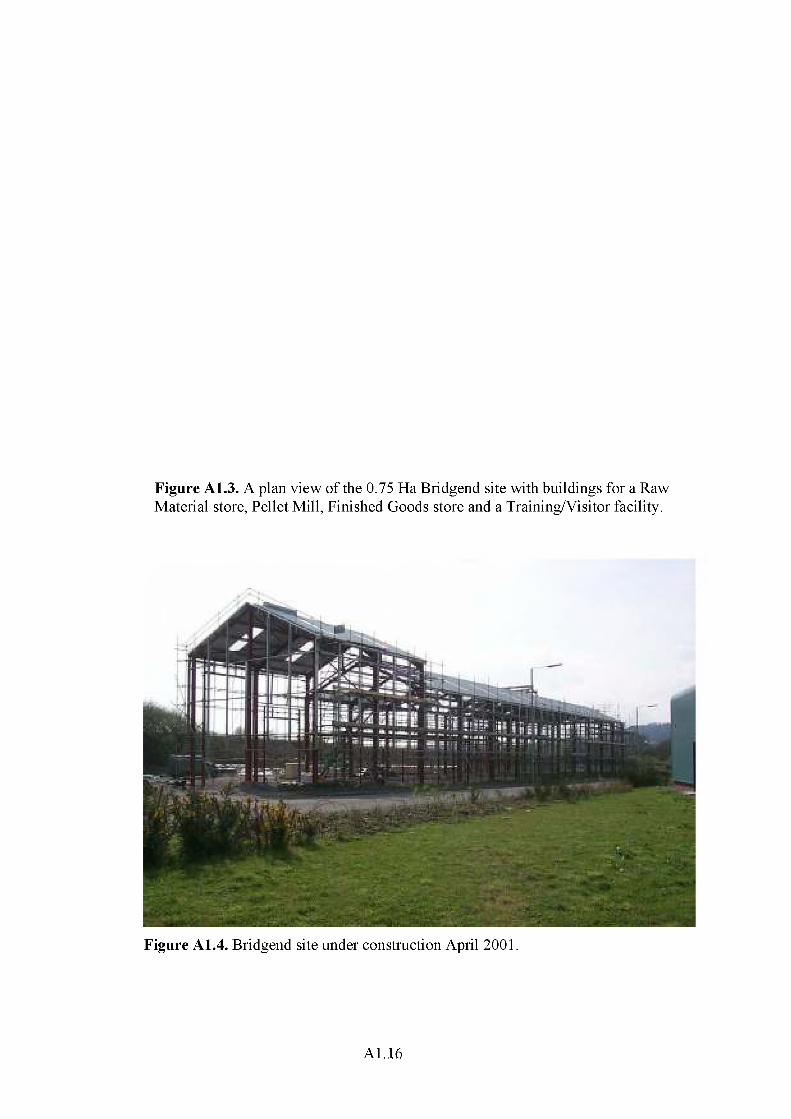

6.3 Feedstock for Pelletisation in South Wales

The construction of a wood pelletisation plant near Bridgend in South Wales is currently underway. A detailed study has been carried out to identify and quantify the potential feed-stocks of waste wood for pelletisation in South Wales. The plant is being designed to initially take 5,000 tonnes of waste wood per year on a single shift operation.

A database has been compiled containing approximately 250 wood-working companies located within 20 miles of Bridgend, South Wales. Each company in the database belongs to one of 5 categories:

(i) Furniture and joinery(ii) Wood component manufacturer(iii) Shed and fencing(iv) Retail(v) Sawmills

In addition, the resource has been split into 4 types:

(i) Sawdust waste(ii) Shavings(iii) Wood chips(iv) Off-cuts

A sample of 32 companies was chosen which contained approximately prorata numbers from each category: 19 Furniture and joinery companies, 8 Wood component manufacturers, 2 Shed and fencing companies, 1 Retail company and 2 Sawmills. From this representative sample, the total wood waste resource suitable for pelletisation in the Bridgend was estimated. The results are as follows.

Table 4: Wood waste resource suitable for pelletisation in the Bridgend area

Total waste wood Total available wasteresource wood resource

Sample of 32 companies 11,170 tonnes/year 8,775 tonnes/yearTotal of 250 companies 89,360 tonnes/year 70,260 tonnes/year

A breakdown of the resource by category and resource type is shown in figures 1 and 2 respectfully. The estimated total resource (from approximately 250 companies) by type in the region is given below.

A1.14

Table 5: The estimated total resource by type in the Bridgend area

Total waste woodresource

Total available waste wood resource

Sawdust waste 23,440 tonnes/year 15,096 tonnes/yearShavings 13,920 tonnes/year 12,584 tonnes/yearChips 16,400 tonnes/year 12,312 tonnes/yearOff-cuts 35,600 tonnes/year 30,208 tonnes/year

Furniture and Joinery

Companies

WoodComponent

Manufacturers

Shed and Fencing

Materials Companies

RetailCompanies

□ Total Resource

□ Available Resource

Figure 2: A breakdown of the resource by category for the 32 sampled companies.

□ T otal Resource

BResource Available

Sawdust Waste Shavings Off-cuts

Figure 3: A breakdown of the resource by resource type for the 32 sampled companies

A1.15

7 THE ECONOMICS OF BIOMASS PELLETISATION IN A UK CONTEXTThe economics of producing wood pellet fuel and establishing a wood pellet industry in the UK are complex. The following analysis looks at the two components determining the economic viability of wood pellet fuel in the UK, namely;

■ The economics of the heating market in the UK i.e. a comparison of competing heating fuels, which will in turn determine the maximum price that wood pellet fuel may be able to command, and

■ The cost of production of wood pellets in the UK

7.1. The Economics of the Heating Market in the UK

There are two key factors which effectively set a maximum price that wood pellets can be produced for in the UK to be competitive in purely economic terms:

a) The world market price of wood pellets andb) The price of fuel oil in the UK.

The price of oil is a critical measure because the replacement of fuel oil is seen as the major market in which wood pellets can hopefully compete within the UK in the near future.

It should be emphasised at the outset that domestic consumers may be willing to pay a premium for pellets over oil since:

(i) Pellets are a renewable source of energy - much easier to use than logs or chips

(ii) Pellets are an indigenous source of energy(iii) Pellets are not as susceptible to large price fluctuations that can

occur with the world oil market - i.e. they have greater long term price stability

A recent study has looked at the public attitude to pellet fuel in relation to other domestic fuels in Austria, Sweden and the USA4.

It should also be noted that for domestic and small commercial heating, wood pellets offer convenience that is approaching that of oil heating e.g. convenient fuel handling, stoves and boilers which are self igniting, clean burning etc. although hoppers must be loaded from a few days to weeks depending on the system design and demand for heat. Pellet burners require weekly ash removal, although automatic ash removal is becoming available. This is an important factor which should be taken in to account when

4 J.Vinterback et al, “Pellet consumers in Austria, Sweden and the United States”, Bioenergy ’98: Expanding Bioenergy Partnerships

A1.16

comparing with other traditional log wood fuel. In comparison to wood-chips, pellets are viewed as having the advantages of being small, dense, homogenous particles of uniform size which flow easily. Because of these advantages the capital cost per kW of appliances is lower for pellets, largely because the handling systems are simpler and lighter e.g. chips require a heavier drive train and feed screw. This is of course offset by the cost involved in pelletisation which means that, generally speaking, for larger systems, chips may be the preferred option.

In addition, due to the high density of wood pellets they do not have the same restrictions as chips on transport distances. Pellets have been shipped form Canada to Sweden, whereas wood chips can really only be transported economically within a local region (say 40-50 miles radius).

7.1.1 The price of fuel oil and the world market for pelletsThe following is a brief analysis of the economics of virgin wood pellets. There are two bench-marks which effectively set an upper price level for wood pellets:

7.1.1.1 World Commodity PriceThere is a world commodity price of about £80 per tonne delivered in bulk to a UK port equipped with grain handling facilities. If a UK pellet manufacturer charges significantly more than £80 per tonne bulk for pellets, the user can simply get pellets shipped in at lower cost from abroad.

A list of pellet suppliers, together with contact details is given in Appendix 2. A number of these companies were contacted to get budget prices for imported pellets. The main motivation for this work was to establish the cost of importing relatively small quantities of pellets to ensure a secure supply until local sources of pellets are established.

Pellets are available at lower cost in the Ukraine and Estonia. However, transportation costs are likely to make the cost of importation impractical.

A lower grade of 10mm diameter pellet for commercial/industrial firing is being made in Holland from “clean” wood from the MSW stream. Although they are unsuitable for domestic appliances and do not conform to the British Biogen Code of Good Practice, these pellets are quoted at £45/tonne FOB Amsterdam. The market for these pellets was large district heating schemes in Sweden however the Swedish authorities are currently moving to ban such fuels.

A1.17

7.1.1.2 The price of fuel oilThe price of fuel oil (domestic heating oil) is crucial to the future of the pellet industry in the UK since this is seen as the major market which wood pellets will hopefully compete against in the UK in the near future.

The importance of the price of fuel oil was shown clearly in Sweden. In 1991 Sweden introduced a ‘carbon’ tax of 27.4 Euros per tonne of CO2 whilst at the same time reducing the then ‘energy’ tax by 50%. Overnight it was cheaper to burn wood pellets than coal, oil or gas. The pellet industry has grown substantially since then and now burns almost V2 million tonnes of indigenous wood pellets annually. Figure 4 shows the growth in the Swedish pellet mill capacity since 1995.

Wood Pellet Capacity in Sweden

1,200

1,000

g 800 a = o^ 600©©® 400

200

01995 1996 1997 1998 1999 2000

Figure 4: Wood Pellet Capacity in SwedenSource: Wood pellets in Europe, Report by the Industrial Network on Wood pellets Jan 2000.

Figure 5 shows the price pellets can command at retail to be equivalent to fuel oil (in terms of equal p/kWh) as a function of fuel oil price5. The current price of fuel oil is about 20 -25 pence per litre (retail price for domestic consumers, excluding VAT) although this price did exceed 25p/litre in early 2000 in certain parts of the UK.

5 This graph assumes an energy density of fuel oil of 36MJ/litre (10 kWh/litre), and an energy density of wood pellets of (18MJ/kg).

A1.I8

Equivalent fuel costs: Pellets vs Fuel Oil

p/litre for Fuel Oil (retail)

Figure 5: Equivalent Fuel costs for heating oil and wood pellets

It can be seen from the graph that an oil price 20p/litre is equivalent to about £100 per tonne for wood pellets. Therefore it is concluded that wood pellets are likely to be close to being competitive in purely economic terms with fuel oil at current prices. However, it should be noted that the current price of fuel oil in Sweden, for example, is equivalent to almost 45p/litre.

There are other factors here that need to be considered. Firstly, it is not yet clear how pellets will be sold in the UK. It is clear that for large installations pellets will be sold in bulk - either large bags (500kg or 1 tonne bags) or will be air handled in bulk. However, it is likely that for domestic situations, certainly initially, pellets will be sold in bags through pellet stove appliance suppliers, stove shops, garages, DIY chains etc. This will mean that the price to the consumer will be substantially higher than the price paid to the pellet manufacturer. Also the cost of bagging pellets can be significant additional cost (estimated to be about £15 per tonne for use of bagging machine, pallets, bags and labour. The current retail price of bagged pellets in the US, where fuel oil has about the same cost as the UK, is about $170 per US ton, corresponding to about £125 per metric tonne at the exchange rate at the time of writing.

This analysis has only looked at the fuel costs - and has not considered the cost of the heating appliance. Pellet heating systems are considerably more expensive than oil systems and so this is a major barrier - therefore pellets must either be cheaper or some capital grant scheme is needed to overcome the differential cost between oil-fired and pellet appliances.

A1.19

7.2 The cost of production of wood pellets in the UK

Biofuel pellets can be manufactured from a wide range of biomass materials. In practice, the viability and value of a particular feed-stock depends on

a) The composition of the feed-stock i.e. whether it is clean virgin biomass or whether it has other materials in it and, if so, the nature of those materials and

b) How much processing it needs before pelletising e.g. drying wet material and breaking down lumpy material is expensive.

c) The quality of the resulting pellets

7.2.1 Costs of Pelletising WoodThe processes and costs involved in pelletisation are:

1. Raw material for pelletisation2. Transport of raw material to pellet mill3. Sorting of material and reduction of material to correct particle size4. Drying of the raw material5. Conditioning material e.g. adding lignin/soyabean oil6. Pelletising7. Bagging and storage8. Transport of pellets

The other major cost is that of debt service on the pellet mill and depreciation of equipment. Clearly the type of material being used will greatly determine the price that can be paid for it: i.e. how much processing it needs before pelletising. e.g. dry and fine material will clearly cost less to pelletise than wet, lumpy material.

7.2.2 Cost of the pellet production processThe following is a compilation of the costs involved in pelletising wood, derived mostly from US and Canadian sources with some additional information from Swedish and UK sources.

None of the figures given are from audited sources, but rather from informal guidelines offered by the Pellet Fuel Institute in the US, supplemented by the general openness and kindness of various individual plant operators.

7.2.2.1 Raw MaterialsRHP have carried out extensive surveys on the prices paid for raw materials, talking to pellet mill owners in Sweden, the US and Canada.

The highest cost anywhere of materials for pelletisation was quoted at £23/tonne in 1998 for a mixture of green sawdust and kiln dried shavings in Sweden. This is an artificial price set by the timber companies who generally own the pellet mills. The price has more to do with the Swedish corporate tax system than a supply/demand equilibrium..

A1.20

The next highest price for raw materials quoted was along the Columbia River in Oregon where there are huge sawmills but also board mills with a great appetite for raw materials for making chipboard which uses sawdust as filler. This pellet mill was paying about £20/tonne for generally kiln dried material probably about 15%mc. The mill owners stated that it was only just possible to break even at this price.

The lowest price quoted for raw materials was in British Columbia where kiln dried material costs £4.60/tonne. This mill is able to ship across the Atlantic and to the Eastern US by railroad by virtue of its low cost raw materials, the shipping cost by sea being about £16.40/tonne.

From the above, a tentative conclusion might be that raw material for wood fuel pellets must not exceed £20/tonne and at that price must be well reduced in particle size and with a low mc. The average price for raw materials in the US appears to be less than half that amount. Chipboard manufactures in the UK pay around £ 18-25/tonne delivered for chips with some variation dependent on average moisture content from individual sources..

7.2.2.2 Particle Size of raw materialsThe final hammer mill screen prior to material entering a pellet mill with one quarter inch dies, making a standard stove pellet, would be 3/16” or 4.8mm. Thus if the raw materials are pallets, furniture or other large size material, there will need to be a “hogging mill” ahead of the final hammer mill. If pallets are being used there will need to be magnetic separation of fastenings.

7.2.2.3 Moisture contentA drier will generally be required as raw material with a moisture content of more than about 16%mc will not pelletise well and the pellets will tend to disintegrate. In addition, pellets would not meet the required calorific value of 4.7kWh/kg or the required 10% moisture content. Careful sampling of typical raw material streams before planning a pellet mill is required to ensure adequate drier capacity and allowance must be made for the fuel needed, usually natural gas, but this can be other waste materials such as bark.

7.2.2.4 Costs for the UK MarketSawmills in the UK can generally sell all the off-cuts that they produce, especially the larger off-cuts, for fire wood etc. The saw dust/shavings have a more limited market but most of this goes for farm animal bedding but also the manufacture of wood pellets for cat litter. Sawmills would not like to lose the fairly lucrative business in selling wood off cuts etc., for which they can obtain up to £20 per tonne, but this is seasonal. Most would be prepared to sell at around £10 to £15 per tonne if a regular all year round outlet were available.

A1.21

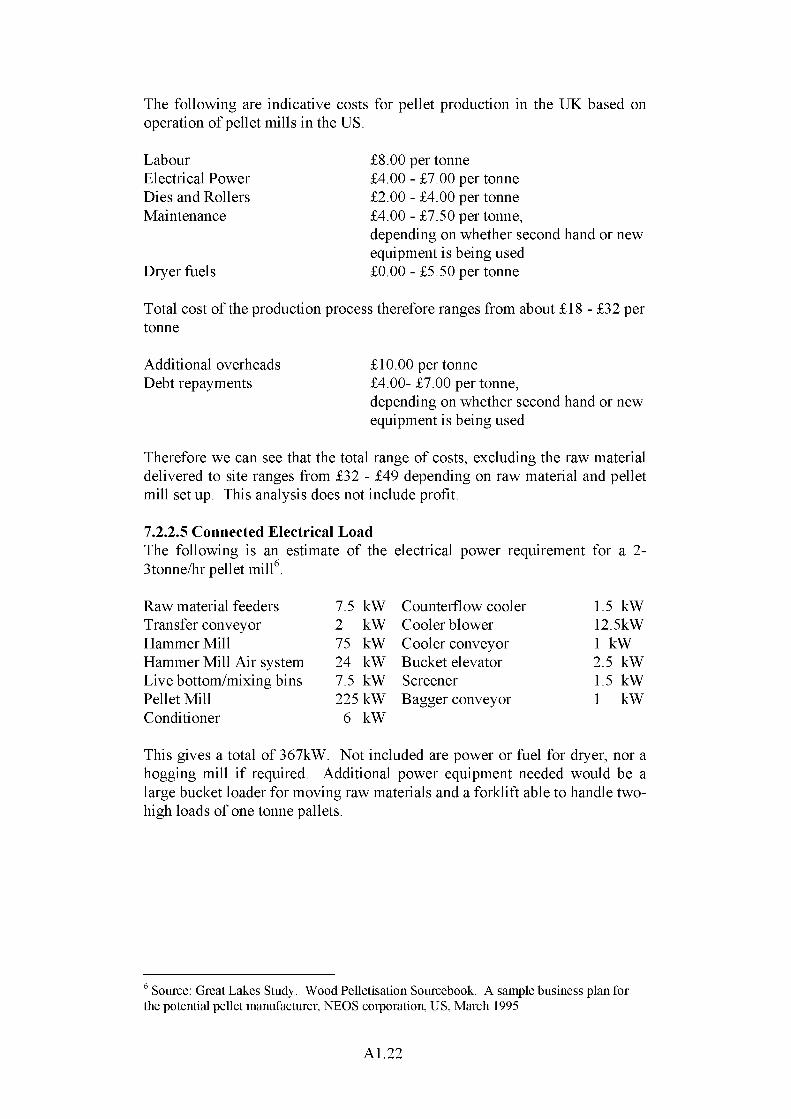

The following are indicative costs for pellet production in the UK based on operation of pellet mills in the US.

LabourElectrical Power Dies and Rollers Maintenance

Dryer fuels

£8.00 per tonne£4.00 - £7.00 per tonne£2.00 - £4.00 per tonne£4.00 - £7.50 per tonne,depending on whether second hand or newequipment is being used£0.00 - £5.50 per tonne

Total cost of the production process therefore ranges from about £18 - £32 per tonne

Additional overheads £10.00 per tonneDebt repayments £4.00- £7.00 per tonne,

depending on whether second hand or new equipment is being used

Therefore we can see that the total range of costs, excluding the raw material delivered to site ranges from £32 - £49 depending on raw material and pellet mill set up. This analysis does not include profit.

7.2.2.5 Connected Electrical LoadThe following is an estimate of the electrical power requirement for a 2- 3tonne/hr pellet mill6.

Raw material feeders 7.5 kWTransfer conveyor 2 kWHammer Mill 75 kWHammer Mill Air system 24 kWLive bottom/mixing bins 7.5 kWPellet Mill 225 kWConditioner 6 kW

Counterflow cooler 1 5 kWCooler blower 12.5kWCooler conveyor 1 kWBucket elevator 2 5 kWScreener 1 5 kWBagger conveyor 1 kW

This gives a total of 367kW. Not included are power or fuel for dryer, nor a hogging mill if required. Additional power equipment needed would be a large bucket loader for moving raw materials and a forklift able to handle two- high loads of one tonne pallets.

6 Source: Great Lakes Study. Wood Pelletisation Sourcebook. A sample business plan for the potential pellet manufacturer, NEOS corporation, US, March 1995

A1.22

7.2.2.6 Capital CostsA pro-forma business plan and spreadsheet has been published which includes a sample costing for capital equipment for a nominal 3.5tonnes per hour capacity. This dates from 1995 but what follows has been up-dated in the light of comments from the Pellet Fuel Institute. The contractors wish to thank Averill Cook, the President of the PFI, for his help generally with many aspects of this project.

Three buildings, two metal, one wood Front end loader Primary grinder Blending hopper Live bottom bin Conveyors Hammer mill Rotary drum dryer Installation of above New ring-die pelletiser (inc controls)Steam boiler Pellet cooler Pellet screener Installation of above Bagging bin Bagging system Installation Fork lift (propane)Total

If £1 = $1.5 Total with contingency = £575,000.

Another actual figure, eight years old, derived from the construction of a 2 ton per hour mill on a greenfield site was $1.2million = £800,000. It should be remembered that land is generally much cheaper in North America than in theUK.

7.2.2.7 Pellets from Recycled Material - (not RDF)If we now look at recycled material the world price is considerably lower. For example pellets from recycled material (formally known as “class B pellets”) can be bought for £45 per tonne FOB Amsterdam. This reflects the very low (or negative) value of the raw materials.

This appears to be consistent with the above figures as this price covers the cost of pelletisation. Pellet mills are presumably taking their profit out of money paid to handle the waste material i.e. the avoided cost of putting the waste in landfill. This class of pellet is potentially very important to the UK, since it is these sorts of materials which we have in large quantities. Their use in larger installations will depend on clarification of the regulations concerning waste materials by the CEN committee and the DETR.7.2.3 Energy Balance. How much energy is used in making pellets?

$ 65,000 $ 65,000 $ 20,000 $ 6,000 $ 12,000 $ 14,000 $ 32,000 $ 200,000 $ 117,000 $ 120,000 $ 15,000 $ 18,000 $ 12,000 $ 111,500 $ 4,000$ 25,000 $ 7,500$ 18,000 $862,000

A1.23

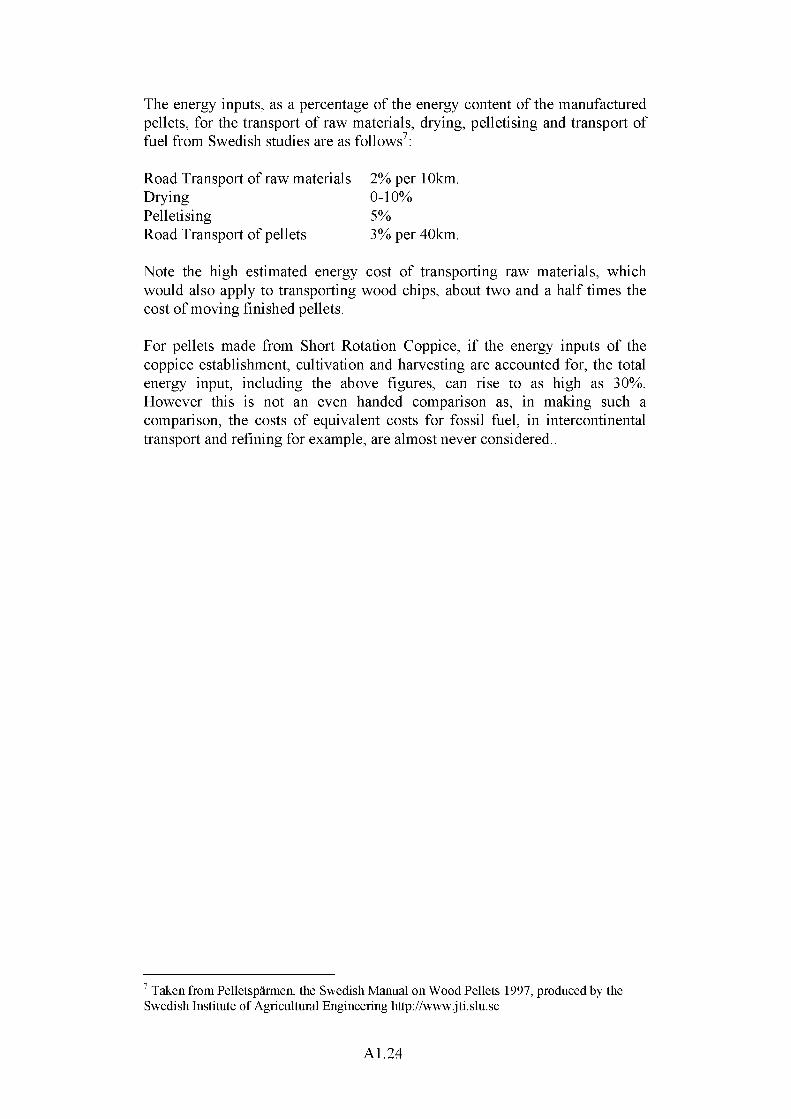

The energy inputs, as a percentage of the energy content of the manufactured pellets, for the transport of raw materials, drying, pelletising and transport of fuel from Swedish studies are as follows7:

Road Transport of raw materialsDryingPelletisingRoad Transport of pellets

2% per 10km.0-10%5%3% per 40km.

Note the high estimated energy cost of transporting raw materials, which would also apply to transporting wood chips, about two and a half times the cost of moving finished pellets.

For pellets made from Short Rotation Coppice, if the energy inputs of the coppice establishment, cultivation and harvesting are accounted for, the total energy input, including the above figures, can rise to as high as 30%. However this is not an even handed comparison as, in making such a comparison, the costs of equivalent costs for fossil fuel, in intercontinental transport and refining for example, are almost never considered..

7 Taken from Pelletsparmen, the Swedish Manual on Wood Pellets 1997, produced by the Swedish Institute of Agricultural Engineering http://www.jti.slu.se

A1.24

8 TRIAL PELLETISATION

The main problem facing a potential pellet industry in the UK at the beginning of the project was how to establish secure supplies of locally made price- competitive wood pellets without an established market.

The construction of a full-scale pellet mill in the UK on a purely commercial basis would not be viable since it cannot be predicted how fast the market for wood pellets will grow from a starting point of zero. Therefore, other ways were investigated. It is interesting that the establishment of pellet supplies is happening by different routes in the three regions of this study; South Wales, The South West and Durham County.

In Wales, since this is a favoured region (Objective 1) and the new Welsh Assembly are supporting sustainable development, the construction of a 5tonne/hour pellet mill has been capitalized largely through grant funding. In Durham County, pellet production has occurred through the waste sector, driven by the need to find alternative sources for clean waste wood which would otherwise go to landfill.

In the South West, several avenues have been explored which have entailed the modification of an animal feed mill for wood pellet production. This has enabled local wood pellets to be manufactured with a very low capital investment.

This section details pelletisation trials on three types of pellet mill using a wide variety of raw materials that are found in quantity in the UK. No combustion trials have taken place by the project partners, since the majority of materials used in pelletisation trials were pure biomass. The density, bulk density and moisture content were measured for all pellets produced (details below).

A database containing information on the composition of biomass and waste materials can be found at www.ecn.nl/phyllis

A1.25

8.1. EcoTre Pellet Mill

8.1.1 BackgroundThe first pelletisation trials using a variety of feed-stocks available within the chosen areas was carried out using equipment manufactured by the Italian company EcoTre Slr. They have developed a pellet mill which has considerable innovation, part of which has been patented. The aim of the development was to minimise energy consumption 8. The project partners were introduced to the technology when a representative from EcoTre was invited to speak at the Seminar held on 22nd Sept, in Nottinghamshire, UK.

Parts of the mill are novel which marks a departure from traditional pellet manufacturing designs. Specific electric consumption ranges from0.025kWh/kg to 0.045kWh/kg depending on the type of wood, according to company literature. The mechanical design and logistics are also new. The pelletiser has two grooved dies and pellets are drawn from outside towards inside each die. The system operates without any additives to the material to be pelletised and the maximum operating temperature of the dies is claimed to be 55 to 60°C.

The low-temperature die operation claimed by EcoTre would offer several advantages: no fumes or vapours, direct pellet bagging without additional cooling devices; simplicity and lower investment costs.

It was therefore decided that these claims by the manufacturer should be tested and that trial pelletisation should be carried out using a of range of raw materials which are found in large quantities in the South West of England and other areas of the UK. A total of four samples (approximately half a tonne each) were tested which included mixed softwood sawmill slab wood which had been chipped, Short Rotation Coppice (SRC) poplar stems felled one year and stored outside, SRC willow stems chipped green and chipped kiln dried oak from a flooring mill. To the authors knowledge SRC has not been pelletised before.

8.1.2. Pelletising Wood with the EcoTre Pelletiser.

a) IntroductionThe design of ring die pelletisers was originally inspired by the need to pelletise animal feeds such as grass and grain. The forces involved in pelletising wood are greater, as the density of the finished pellet is greater and the material is harder than cereals. Traditional machines have a revolving ring die penetrated by numerous holes, generally between 6 & 12mm diameter, through which the feed-stock is forced to form pellets.

A schematic of the EcoTre pellet mill is shown in figure 6.

8 Emidio TOSI, EcoTre System s.r.l., Via delle Cantine 12, I-50040 Settimello (FI)

A1.26

LEGENP

1 nngiwG feeder s pellet^ df di istfe2 PELLETIZER WITH PELLET CUTTING DEVICES3 PNEu*1flTTC PELLETS EXTRACTOR4 PELLETS BELT C&flJEYQR

I------ > SAlVnuST Ahln POWDERS CHCtilie e*p PELLETS CIRCUIT

Figure 6: A schematic of the basic EcoTre pellet mill set-up

Inside the die are two or three revolving rollers almost in contact with the inner surface of the die and material is fed in to this inner cavity being trapped at the pinch points between the rollers and die, whence it is extruded outwards through tapered die holes.

Both the ring die and the rollers are “overhung”, that is outside the forward shaft bearings. In pelletising wood the forces on the shaft are greater than envisaged in the original design and machines are called on to operate at the absolute limit of their capability and shaft failures at the stress concentration outside the forward bearing are not uncommon. Bearing replacement costs are a significant expense. There is often difficulty in achieving the pellet density required by the Standards that have been adopted for wood fuel pellets.

The EcoTre system has set out to address these problems by placing the die, or dies, between the bearings of the shafts and by using massively heavier shafts and pressure lubricated bearings. Also the rollers are outside the ring die allowing for placement of up to six rollers around a single die, or ten rollers around a two-die machine with the pellets being extruded inwards.

b) The EcoTre SystemThe machine observed had a 600mm die and four rollers. It was observed over one and a half days pelletising dry beechwood sawdust, hay and the four samples of wood chips from UK sources. An additional run was done using as a feedstock, reground wood pellets that were outside the moisture content limits of the UK Standard.

Material to be pelletised is dumped into a circular receiving hopper which has a swept floor with an opening into a short screw conveyor which introduces the material into an air handling system. This introduces the material into an

AE27

EcoTre “refining mill” (patent pending) which is a 7kW paddle fan combined with a small hammer mill discharging through a screen. Screen size can be changed as appropriate to the die hole diameter.

From the refining mill, material is air conveyed to a storage hopper and then by belt conveyor to a smaller feed hopper directly above the mill. Conditioning water can be introduced at the entry to the mill. Finished pellets are extracted from the inner cavity of the die by pulsed suction and air handled to a screen for removal of fines, which are returned onto the belt conveyor.

c) Wood samplesA. Mixed softwood sawmill slabwood chipped to 50mm chips for

a board millB. Short Rotation Coppice (SRC) poplar stems felled one year and

stored outsideC. SRC willow stems chipped green.D. Chipped kiln dried oak from a flooring mill.E. Wood pellets made from samples B and C

d) Results of Pelletisation trialsSamples of the raw material were taken immediately prior to the pelletisation trials. In addition samples of the raw materials were taken after they had passed into the refining mill but before they entered the pelletiser. This was to determine at which stages in the pelletisation process a reduction in moisture was taking place. Lastly samples of pellets were taken. The results are given in table 6.

All moisture contents were determined from samples taken at the time of pelletisation. These samples were stored in air-tight containers and analysed at the RHP offices. Samples were oven dried at 110°C for 1.5 hours and weighed on a verified spring balance with 500g full scale and a sensitivity of one gramme.

Table 6. Results of pelletisation trials

Sample Moisture content Raw Material

Moisture content After refining mill, before pelletiser

Moisture content of Pellets

Bulk Density of final pellets

Ratio of average length to diameter of pellets

A 45% 26% 17% 530kg/m3 1.5 : 1B 44% 31% 17% 468kg/m3 1 : 1C 36% 32% 17% 458kg/m3 1.2 : 1D 11% 11% 11% 665kg/m3 2.5 : 1E 17% 12% 11% 605kg/m3 2 : 1

It can be seen that the raw materials for A, B and C are of high moisture content and that although pellets were produced the moisture content of the

A1.28

pellets are far too high to be acceptable. It was also noted that the percentage of moisture reduction varied considerably from sample to sample.

A possible explanation for the different amounts of decrease between the samples is the different feed rates used for the refining mill. The slower the feed rate, the longer would have been the exposure of the material to air blast in the handling system. Sample A was much coarser than B and C and had to be fed very slowly as the chips were larger than the specification for the refining mill. Sample B contained some twigs, which C did not, entailing a somewhat slower feed rate. Sample D had a very slow feed rate.

It should be noted that the ambient temperature was 23°C. It is surmised that moisture losses in the refining mill will depend heavily on ambient temperature and relative humidity.

From the figures in table 6 it can be seen that samples D & E are close to the UK standards for wood fuel pellets. The ratio of length to diameter gives some idea of the fragility of the pellets. Damp pellets have little cohesive strength and hence tend to break into short lengths (of the order of the diameter), whereas high quality, low moisture content pellets tend to be long and ‘pencil-like’ in shape.

It should be noted that no fine tuning of the system was attempted. The same die speeds were used for samples regardless of the nature of the samples. The same die was used as for hay.

e) Power consumptionSample E was produced at a peak rate of 16litres/minute, which, at a bulk density of 605kg/m3 as measured, is a production rate of 581kg/hour. Amperage draw was 82A at 380V three phase.

f) Preliminary conclusionsIn general the equipment performed well, although in the author’s opinion the claims about moisture reduction from raw material to pellets is somewhat exaggerated by the manufacturers. There does appear to be significant advantages in using an air handling system. However we believe under likely UK ambient conditions of cool damp air, that there is no possibility of making wood fuel pellets that conform to the British Biogen Code of Good Practice without the use of a drier. A large Ecotre mill is currently being installed in Massachusetts and results from operation of it will be available from the authors as they become available.

The main conclusion is that the EcoTre system looks very promising, although there are some aspects which, in the authors opinion, need addressing. In particular, for operation in the UK, with the climate and likely raw materials to be used, a drier is essential. The authors believe that the EcoTre system is a serious candidate for anyone contemplating the purchase of a pellet mill.

A1.29

8.2. Farm Feed Pellet Mill (25hp)

8.2.1 BackgroundWood pellets as a fuel are very new to the UK with no market at present in the South West. Therefore, as a business investment, a large scale pellet mill is not possible without grant aided capitalization, or at the very least would be speculative for anyone investing in pellet production. Therefore, two ideas have been researched to try and overcome this barrier:

Firstly, the idea of modifying small-scale, low-cost pelletising equipment used in the feed industry to produce relatively small quantities of pellets. Wood pellets for fuel have never been made on small scale equipment (say 25hp) before and therefore a research and development (R&D) programme is currently underway to see if this is possible and if so, how the pellet machine will perform.

The second idea, is to modify an existing grass mill for pelletising wood residues. The details of these preliminary trials are given in the next section.

Research has concentrated on modifying relatively low cost pelletising equipment which was originally designed for animal feed for use with wood as a raw material. There are three major variables in the design of a pellet mill.

1. The area of contact between the die and roller for a given power of machine

2. The ratio of the die holes to undrilled metal area on the inside of the die

3. The geometry of the die hole itself. This geometry is of crucial importance to the performance of the machine, production rate and quality of pellets. The optimum geometry of the die is also highly dependant on the type of material that is being pelletised. For example, a die used for grain will not produce good wood pellets (or wood pellets at all) as different compression ratios are required. The geometry also varies between hard and soft wood, moisture content of the wood and particle size of the raw material.

It is found that if the compression is too high the die will plug up with compressed wood and the machine will not function. If the compression is too low the pellets are not of sufficient density and will fall apart.

A major advantage of using small scale equipment is that it is relatively easy to make modifications to the die since it is small and relatively inexpensive, whereas for large scale pellet machines each die costs several thousands of pounds. In comparison, for a small machine, a die geometry can be tested and one modification can be made in a single day. In this way it is hoped that the optimization of the die for the small machine can make it more efficient and compensate to some extent for the lack of power in the mill drive.

A1.30

A series of trials has been carried out. Three feedstocks have been chosen and a die optimized for each one.

a) Soft Wood Fines from the waste sector.A sample of soft wood fines from Plymouth was tested. This material was from a waste stream of mainly clean wood waste which is sent to be made into chip board. The resulting fines from the reduction process are not suitable for chipboard and are currently sent to landfill. This material contained approximately 2% paint residues which would be unacceptable as a biomass fuel (this must be burnt with an incineration licence). The sorting could be vastly improved but there is certainly an issue of quality control.

This material was pelletised using a 7.5mm die. After approximately 1 week of modifying the die, a successful die geometry was achieved with the correct amount of taper. Pellets of the correct density were made.

b) Kiln dried oak sawdust.The use of hard wood was found to be more difficult as is well known in the North American industry. Although pellets were successfully made in small quantities it was felt that oak material was too hard for a machine of this power. Therefore no further tests were made.

c) Soft wood sawdust from a sawmillTwenty 30kg bags of clean, softwood sawdust from a small Devon Sawmill weres used in the trials giving a total of 600kg. The moisture content of the sawdust was measured to be 18-20%, slightly varying from bag to bag. A drying machine suitable for sawdust was constructed to reduce the moisture content. Pelletisation trials using material with known moisture content ranging from 8% up to 15% was carried out.

Photograph 3 shows clean soft wood sawdust at approximately 10-11% moisture content being pelletisated using a 25hp Farm Feed Ltd Pellet Press. These pellets are of reasonable quality having an absolute density greater than 1000kg/m3 and a moisture content of about 9% (since there is a reduction of 1 or 2% in the pellet pressing).

Clean soft wood sawdust at approximately 10-11% moisture content was successfully pelletised using a 25hp Farm Feed Ltd Pellet Press. These pellets were of reasonable quality having an absolute density greater than 1000kg/m3 and a moisture content of about 9% (since there is a reduction of 1 or 2% in the pellet press).