introducing our analytical framework - usaid lensjordanlens.org/sites/default/files/3b. dfs models...

TRANSCRIPT

Value chainCustomer value proposition

Profit model

Introducing our analytical framework

0

Capturing the key aspects of the business models

What cost or operational efficiency benefits does the

service bring to the business?

Who is the target

customer?

Who owns the

customer relationship

and brand?

Data / VASDigital

channel

Physical

channel

What is the value proposition for the target

customer?

What sections of the value chain does the business own vs

outsource to partners?

Accounts

What additional revenue or loyalty benefits does

the service bring to the business?

• s

Shared control

Full control

No control

Completely owns the value chain item. Not dependent

on any partner.

Partly owns the value chain item and/or shares it with

partners

Owns no part of the value chain item. Value chain item

may or may not be necessary to the business model

Color coding legend

Framework: Value Chain in DFS Services

1

Data / VAS Digital ChannelPhysical

Channel

What sections of the value chain does the business own vs outsource to partners?

Who is legally

responsible for the

user accounts?

On whose platform

do user accounts

reside?

Whose brand(s)

do users see?

Who primarily

owns the user

relationship?

Accounts

Who sees and

controls user /

transaction data?

Are these data

being utilized to

offer Value-Added

Services?

Who owns the key

communications

channel (USSD,

SIM, data) used?

Can users interact

with their accounts

at physical touch

points (e.g. ATMs

or agents)?

Who owns these

physical touch

points?

What financial and

strategic cost or

asset is posed by

physical channel?

Bank model: Equity Bank

2

Equity 3.0: the next step in the evolution

• Licensed as Mobile Virtual Network Operator (MVNO)

• Rents space on the comms channel from Airtel

• Issues SIM cards and SIM overlay under Equitel brand

• Offers regular voice, SMS and data services alongside an integrated financial services product

• Free P2P between Equity customers and Orange Money wallets

• 30 day mobile loans up to $2,000 at 1.5% interest

• Customizable goal savings feature

• Free educational content and access to Facebook, Wikipedia

3

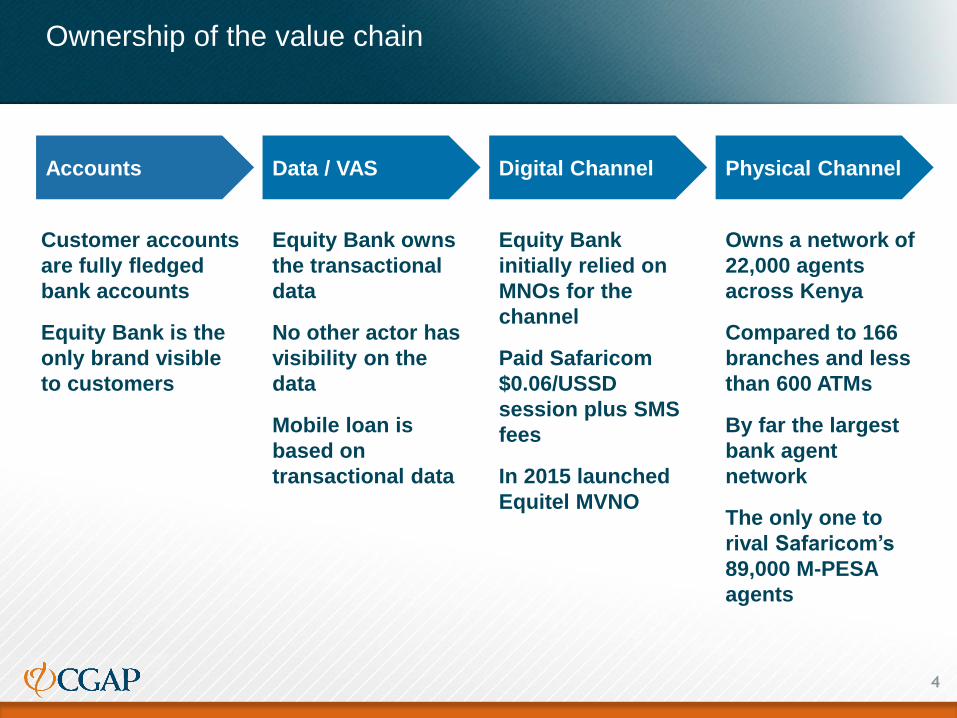

Ownership of the value chain

4

Accounts Data / VAS Digital Channel Physical Channel

Customer accounts

are fully fledged

bank accounts

Equity Bank is the

only brand visible

to customers

Equity Bank owns

the transactional

data

No other actor has

visibility on the

data

Mobile loan is

based on

transactional data

Equity Bank

initially relied on

MNOs for the

channel

Paid Safaricom

$0.06/USSD

session plus SMS

fees

In 2015 launched

Equitel MVNO

Owns a network of

22,000 agents

across Kenya

Compared to 166

branches and less

than 600 ATMs

By far the largest

bank agent

network

The only one to

rival Safaricom’s

89,000 M-PESA

agents

Profit model:

Digital channels drive deposit mobilization, revenue growth

5

Mass deposit mobilization New revenue sources

Transaction fees:

• Total transaction fee revenue grew by

29% in 2015 to $166m

• 8 million transactions per month on

Equitel channel (Aug 2015)

• USSD users average 2 txs / month

while Equitel users now average 21

Customer acquisition:

• From 100,000 depositors in 2001 to

over 8 million in 2015

Deposit mobilization

• Total deposits now $3.1bn

• Agents in Kenya collected $285m in

deposits in Aug 2015 alone

Majority of cash transactions have been shifted to the agent

channel

6Source: Equity Bank Investor Briefing Q3 2015

0

10

20

30

40

3Q 2011 3Q 2012 3Q 2013 3Q 2014 3Q 2015

Number of transactions, in millions

ATM Branch Agency

Agency

51%

ATM27%

Branch22%

Percentage of transactions by type, as

of Sept. 2015

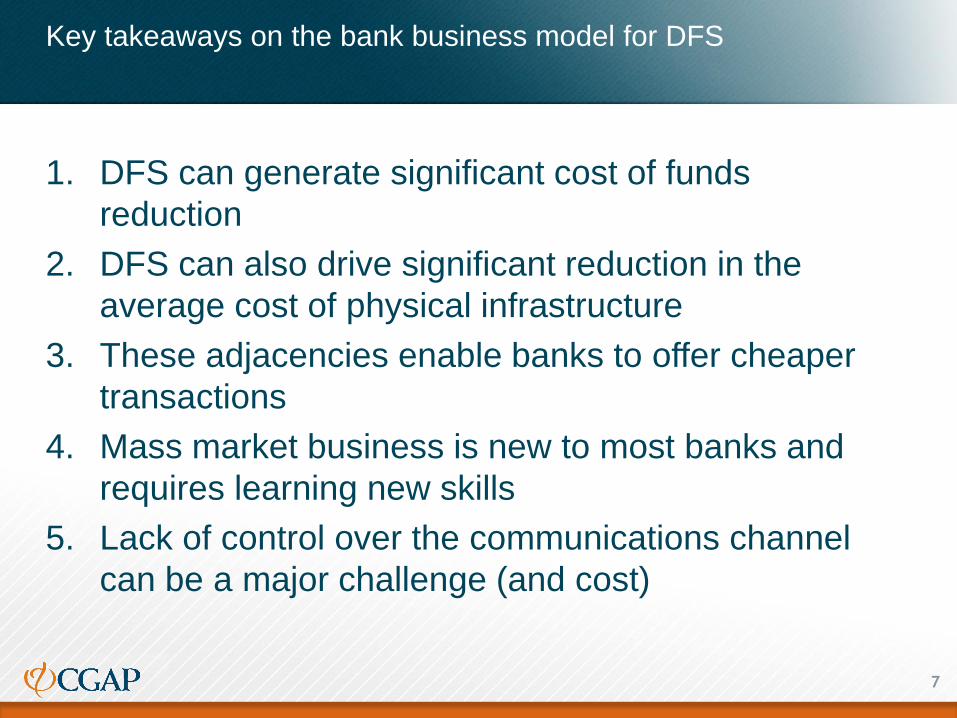

Key takeaways on the bank business model for DFS

1. DFS can generate significant cost of funds

reduction

2. DFS can also drive significant reduction in the

average cost of physical infrastructure

3. These adjacencies enable banks to offer cheaper

transactions

4. Mass market business is new to most banks and

requires learning new skills

5. Lack of control over the communications channel

can be a major challenge (and cost)

7

8MNO Model: Airtel Money

Airtel Money in Africa

Established in August 2012

– Live in 16 countries

– 12m active customers

– 250,000 active agents

– 7m txns per day

– $70m in txns value per day

9

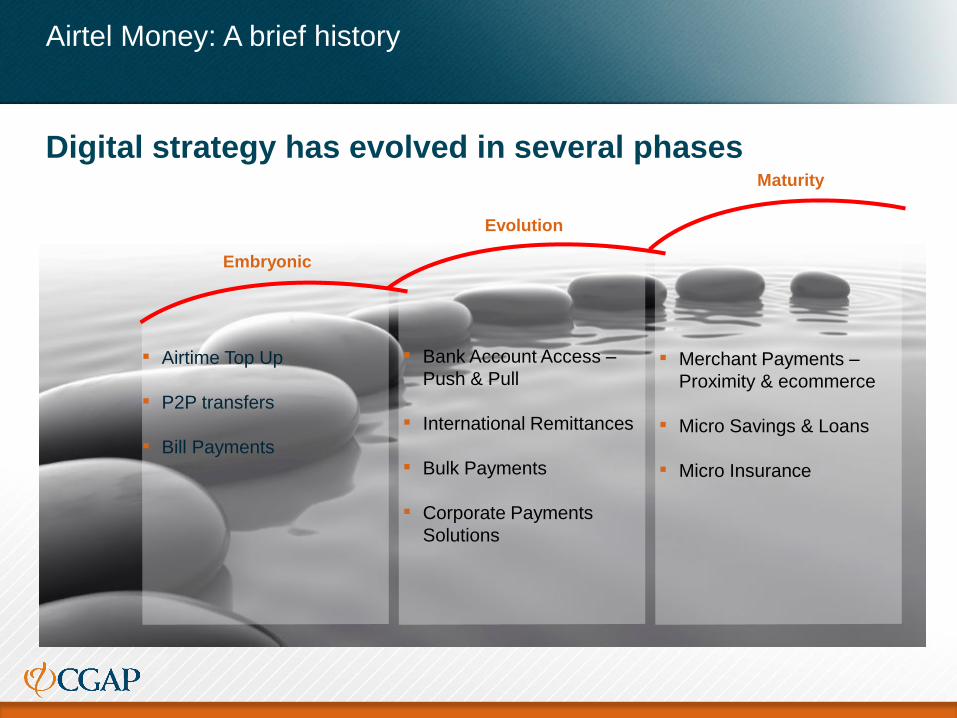

Airtel Money: A brief history

Digital strategy has evolved in several phases

Embryonic

Evolution

Maturity

▪ Airtime Top Up

▪ P2P transfers

▪ Bill Payments

▪ Bank Account Access –

Push & Pull

▪ International Remittances

▪ Bulk Payments

▪ Corporate Payments

Solutions

▪ Merchant Payments –

Proximity & ecommerce

▪ Micro Savings & Loans

▪ Micro Insurance

How are customers using mobile money?

Customer Transactions on mobile money

Source: GSMA State of the Industry 2015

2%

43%

5%

5%

3%

1%

31%

20%

27%

15%

1%

1%

32%

15%

0% 25% 50% 75% 100%

Trx Value

Trx Count

Air Time Bill Pay Bulk Disbursement Cash In Cash Out Merchant Pay P2P Transfers

Active customers conduct an average of 11 transactions/month and maintain

median account balance of $4.70

Ownership of the value chain

12

Accounts Data / VAS Digital Channel Physical Channel

Hosts all customer

accounts on its own

e-money platform

Airtel Money is the

only brand visible to

customers

All customer funds

are held in pooled

accounts at a bank

Airtel Money owns

the transactional

data

No other actor has

visibility on most of

the data

Airtel Timiza mobile

loan is based on

transactional data

Airtel owns the

digital channel

Cross promotions

with voice business

are often used (e.g.

free talk time equal

to P2P amount sent)

Owns a network of

22,000 agents in

Kenya and 20,000 in

Tanzania

Early investment pushes breakeven out past 36 months

Mobile money profitability over time (months)

Savings

Insurance

Merchant solutions

Credit

Agriculture Energy

Mobile Money

A broad range of services are emerging around mobile money

Some of which are completely new business models

Water

FarajaInsurance

farijika

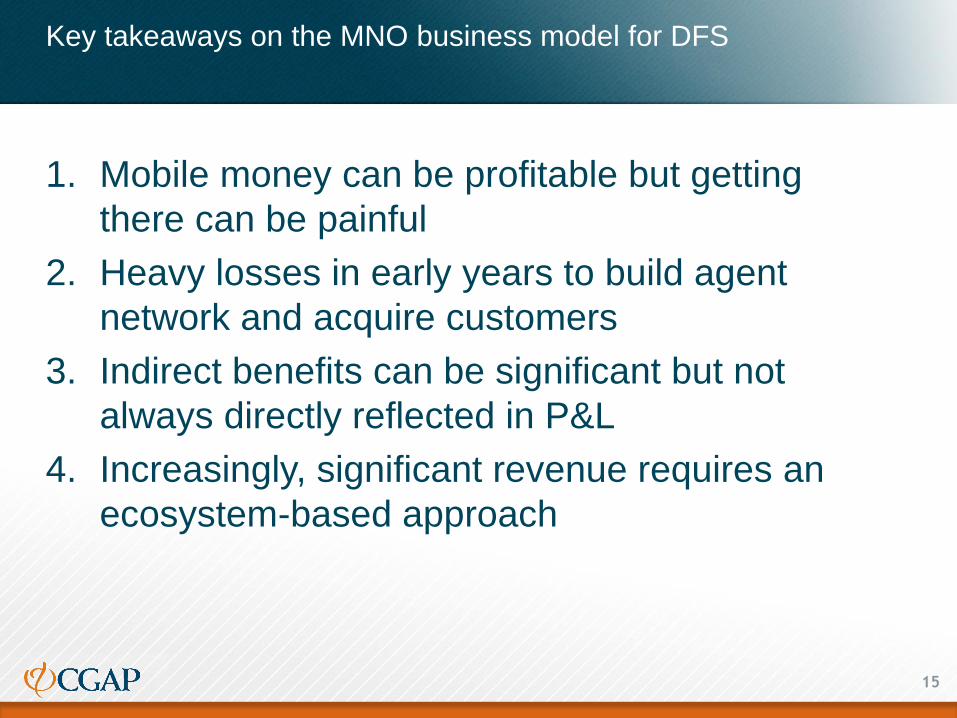

Key takeaways on the MNO business model for DFS

1. Mobile money can be profitable but getting

there can be painful

2. Heavy losses in early years to build agent

network and acquire customers

3. Indirect benefits can be significant but not

always directly reflected in P&L

4. Increasingly, significant revenue requires an

ecosystem-based approach

15

Standalone model: bKash

16

BRAC: 3 service channels

17

bKash: Scale

18

As of October 2015

Accounts 25 million

Active Accounts 10 million

Transactions Per Month 85 million

Value of Transactions Per Month $1.4 billion

Average Transaction Size $16

* Source: Bangladesh Bank statistics, estimates for bKash based on 85%

market share of industry total.

Ownership of the value chain

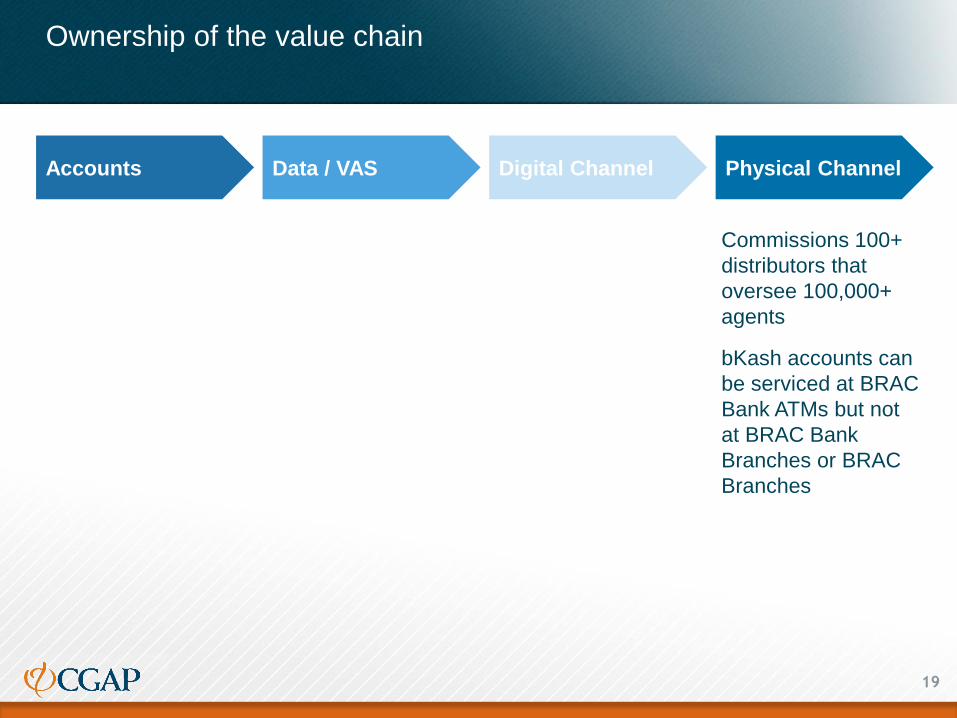

19

Accounts Data / VAS Digital Channel Physical Channel

Commissions 100+

distributors that

oversee 100,000+

agents

bKash accounts can

be serviced at BRAC

Bank ATMs but not

at BRAC Bank

Branches or BRAC

Branches

bKash: Profit model

20

Fees

Interest

2014 Audit

Months

30-42

REVENUE

$84 Million

Agent

Comm-

issions

USSD

Corporate

COSTS

$79 Million

PROFIT

$5 Million

800 staff

110,000 agents

Key takeaways on the standalone business model for DFS

• Startup - neither MNO or Bank - can scale

• Challenging profit model:

• No existing business lines to cut cost

• No adjacencies or cross-sell

• Profitability relies on transaction fees

• Strategy and sequencing key:

• Early scale and profitability come from sharp

focus on basic payments

• Medium term pivot towards broader array of

services; connected services21

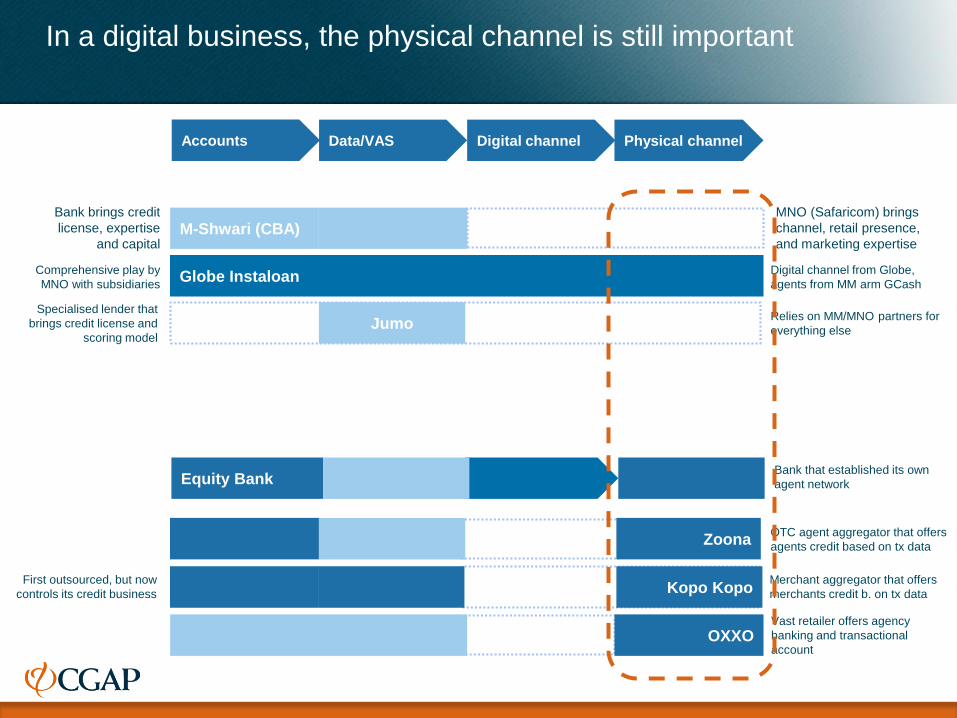

Accounts Data/VAS Digital channel Physical channel

In a digital business, the physical channel is still important

OXXOVast retailer offers agency

banking and transactional

account

M-Shwari (CBA)MNO (Safaricom) brings

channel, retail presence,

and marketing expertise

Bank brings credit

license, expertise

and capital

ZoonaOTC agent aggregator that offers

agents credit based on tx data

Globe InstaloanComprehensive play by

MNO with subsidiaries

Digital channel from Globe,

agents from MM arm GCash

JumoSpecialised lender that

brings credit license and

scoring model

Relies on MM/MNO partners for

everything else

Kopo KopoFirst outsourced, but now

controls its credit business

Merchant aggregator that offers

merchants credit b. on tx data

Equity BankBank that established its own

agent network

Accounts Data/VAS Digital channel Physical channel

DFS business models are not static but evolve (rapidly)

Tim

e

Equity 2.0

OXXO 1.0

Equity 3.0

OXXO 2.0

Offered retail network as

agency provider for banks

Issuing card based accounts

under joint brand, mining tx

data for loyalty, analytics

Est. own agent network for

cash in/out to accounts

Secured own MVNO

license, mining transaction

data for advanced products