interoperability as a means to financial inclusion • executive summary 2 executive summary there...

TRANSCRIPT

Interoperability and connected financial ecosystems promise to dramatically extend and

broaden financial inclusion to the world’s poor. Technical solutions are only half the

answer; regulators and central banks first need to create the underlying legal and

regulatory foundations that pave the way toward full interoperability and inclusion.

ericsson White paper284 23-3295 Uen Rev B | November 2016

Interoperability as a means to financial inclusion

INTEROPERABILITY • EXECUTIVE SUMMARY 2

Executive summary

There is increasing international recognition of the importance of financial inclusion for stimulating

economic development and individual livelihoods. Through progressively enabling the most

vulnerable in our society to partake securely and equally in formal and informal economies, we

start to address existing economic disparities and empower the excluded.

Governments and international organizations alike are demonstrating their commitment to

financial inclusion through national and international agreements and policies; one example being

the Maya Declaration on Financial Inclusion signed globally by over 80 institutions from developing

and emerging countries. In addition, in October 2013, the World Bank Group set the target of

reaching universal financial access by 2020 [1] with a special mention of the role that digital

financial services will provide as a means of achieving this goal.

Given the high penetration of mobile phones, mobile commerce has been advocated as a

means for providing financial inclusion. However, access to mobile services alone will not provide

the solution. There must also be a strong regulatory framework for enabling an interoperable

ecosystem that allows easy entry by non-traditional authorized financial service providers. Only

a strong regulatory and policy framework can provide the parameters and environment in which

sector-wide participation can be fostered. Both interoperability and financial inclusion have been

included in various national level policies, with strong examples from Bangladesh, Colombia,

Indonesia, Rwanda and Tanzania. But despite these national and international commitments, full

realization remains elusive.

This paper addresses the importance of considering and potentially mandating interoperability

as a means of achieving a vibrant financial ecosystem, which in turn fosters financial inclusion.

Addressing the potential concerns of competition while promoting innovation, this paper proposes

that an open interoperable system allows traditional and non-traditional authorized financial

service providers to quickly launch products and reach new consumer groups, while achieving

economies of scale and at the same time lowering operating expenditure and startup costs.

Financial interoperability is dependent not on technology, but on forging partnerships and

facilitating market entry [2] within a conducive, defined and stable regulatory environment. It is

clear that to achieve this, there is a role to be played by all members of society, including regulators,

the private sector and international organizations [3].

Financial inclusion is more than just access to financial services – it can provide a transformative

influence on economies and the way populations interact with the world around them,

contributing to financial stability for the poor and fostering entrepreneurship to drive growth

in the developing world.

MAKING FINANCIAL INCLUSION A GLOBAL GOAL

More than one quarter of the world’s population lacks access to formal banking services.

Despite the growth in mobile financial solutions, including 700 million new account holders

between 2011 and 2014, nearly one half of all adults in the developing world still do not have

bank accounts or access to services from financial institutions.

Initiatives such as the World Bank Group’s call for universal financial access by 2020 have

been boosted by the success of e-money solutions, debit cards and low-cost regular bank

accounts. Extending financial access to the world’s poor is seen as a powerful tool in the

fight against extreme poverty, and the principle is embodied in Goal 8 of the United Nations’

Sustainable Development Goals. In addition, the G20’s Financial Inclusion Action Plan has

been revised to further incorporate financial inclusion when assessing financial sectors.

For the conventional banking sector, extending traditional financial services can be

prohibitively expensive; legacy systems, regulatory constraints as well as the standard branch

network model provide little flexibility in how they serve their customer base. A general lack

of high-quality physical infrastructure in developing markets also causes additional problems

for the banking sector. This could lead to additional costs for supplying power with generators

or problems in managing the supply chain. Operational costs can be double those in

developed markets, with bad infrastructure lowering productivity by up to 40 percent.

Financial services need to be accessible, affordable and convenient. Realizing financial

inclusion in emerging markets, for the most part, requires the provision of financial products

and services to users in hard to reach areas, in a cost-effective and secure way. Consequently,

banks have started turning to partnerships with financial and non-financial institutions to

provide financial services to those who previously had little or no access.

Digital financial inclusion – the most promising development has been the dramatic growth

of digital financial services. The rise of mobile money solutions has grown steadily in recent

years and in many areas, such as in Sub-Saharan Africa, this is the only method of accessing

financial accounts for half of the customer base.

Digital financial services build upon a transactional platform that allows payment instruments

(cards, phones and so on) to be connected to storage accounts and potentially allow users

to make payments using any retail agent.

The expansion of mobile phone networks in remote and poorly developed regions allows

mobile phones to be used by financial service providers as an effective distribution channel

to lower operational costs, increase coverage and extend financial services to emerging

markets.

Over-emphasis on IT solutions – many governments and some private-sector providers

around the world continue to rely on IT solution providers to encourage the use of mobile

financial services (MFS). While inclusion must be built on a sound IT infrastructure, the

environment must first be prepared with a supportive regulatory, policy and legal framework.

It is therefore critical that governments and the private sector work together to realize social

and economic targets through meaningful partnerships. These partnerships must first be

established between all regulatory, policy-making and commercial players in the MFS

ecosystem, which in turn will guide IT solution providers in designing products that address

those systemic needs. Instead of deploying IT into a regulatory vacuum, we must create the

environment where the IT solution is purposeful, given each market’s particular context and

requirements.

INTEROPERABILITY • THE POWER OF ACCESS 3

The power of access

INTEROPERABILITY • THE POWER OF ACCESS 4

INTEROPERABILITY

Given the potential significance of the role interoperable ecosystems can play in achieving critical

national and international agendas, it is important to identify what interoperability is and how it

contributes to the realization of financial and social inclusion.

In simple terms, it is about the ability of customers of independent digital financial service

providers to transact and do business with each other. However, interoperability is more than

the ability of various technical platforms to interact, or a feature of the general IT infrastructure;

it speaks to political will and stakeholder relationships – on the motivation and ability of every

player in the ecosystem to feel empowered and enabled to connect and transact.

Interoperability has the potential to lower fees and the cost

per transaction by avoiding duplication of payment

acceptance and point-of-sale (POS) device infrastructure. It

can also increase the value and usage of new payment

infrastructures by allowing users to do business with more

people and services. To achieve this, suitable regulatory

frameworks need to be in place, supported by a strong

political will to motivate the service uptake. The IT

infrastructure in itself must be designed and implemented

not to create needs, but rather to respond to needs within

an enabling environment.

There are both different types of interoperability and

different ways to achieve interoperability. For the purposes

of this paper, we focus on the regulatory and political issues

that are needed to promote interoperability of different retail

payment systems and open up markets to newcomers.

Mobile walletproviders

Retailers andmerchants

Governmentdepartments

Money transferorganizations INGOs and NGOs

Banks Microfinanceinstitutions

Interoperableecosystem

Card terminals and POS

Figure 1: Overview of an interoperable ecosystem

THE PLAYERS

Financial regulators and central banks

Regulators and central banks must create proportionate regulation

and supervision to enable non-banks to compete with traditional

banking players when providing financial services to excluded groups.

Banking and traditional financial service providers

MFS bring risks and opportunities to traditional financial service

providers. There is clearly enormous potential from an untapped market

made available by MFS channels, which allow banks to overcome

infrastructural, geographical or information constraints. In addition,

the wide acceptance for new mobile network operator (MNO) payment

and mobile money systems can increase consumer confidence in

markets where trust in the banking system is low.

MNOs and non-banking players

Here we include MNOs, affiliates and subsidiaries that may issue

e-money and set up customer accounts. Local regulation may require

that they establish a non-bank subsidiary. In many regions, non-

traditional financial service providers are vital players and can often

be the only providers of products and services to the financially

excluded and underbanked.

INTEROPERABILITY • ACHIEVING FINANCIAL INCLUSION 5

Achieving financial inclusionACCESS IS NOT ACTIVITY

Although the number of financially included people has incrementally improved over the past

decade, the number of people who do not have a formal bank account still stands at 2 billion. It

is important to note that addressing financial inclusion is not about simply opening a formal bank

account or signing up for a mobile wallet. Financial literacy, the ability to buy and sell goods, and

fully activating your financial tool to enable and support your financial ambitions are characteristics

of a financially included citizen.

Moving from activated to active wallets requires providing opportunities and options to all sector

players. Key drivers for active wallet use include: connectivity, the expansion of the agent network,

the ability to send and receive funds from different service providers or to different accounts and

customer empowerment [4]. Active wallets require an active, engaged and connected ecosystem.

SECURITY AND CONFIDENCE

Perceptions of risk and mistrust remain evident in all sectors of society. Improved compliance and

security measures along with appropriate and relevant marketing and awareness campaigns go

far in addressing consumer perception. This can be done through the drafting of appropriate policies

and regulations that outline the national anti-money-laundering requirements and clear data and

consumer protection, privacy and security regulations.

Specifically addressing the concerns of financial regulators through appropriate national

frameworks will help level the playing field and increase market access from various sector players.

Furthermore, work can be done to support these regulators to encourage regulatory revisions. This

can be achieved through the sharing of best practice examples and highlighting the value that

MFS and interoperability bring to national agendas and proactively mitigating these concerns.

Continued regulatory outreach, combined with engagement with and inclusion of the traditional

players is important.

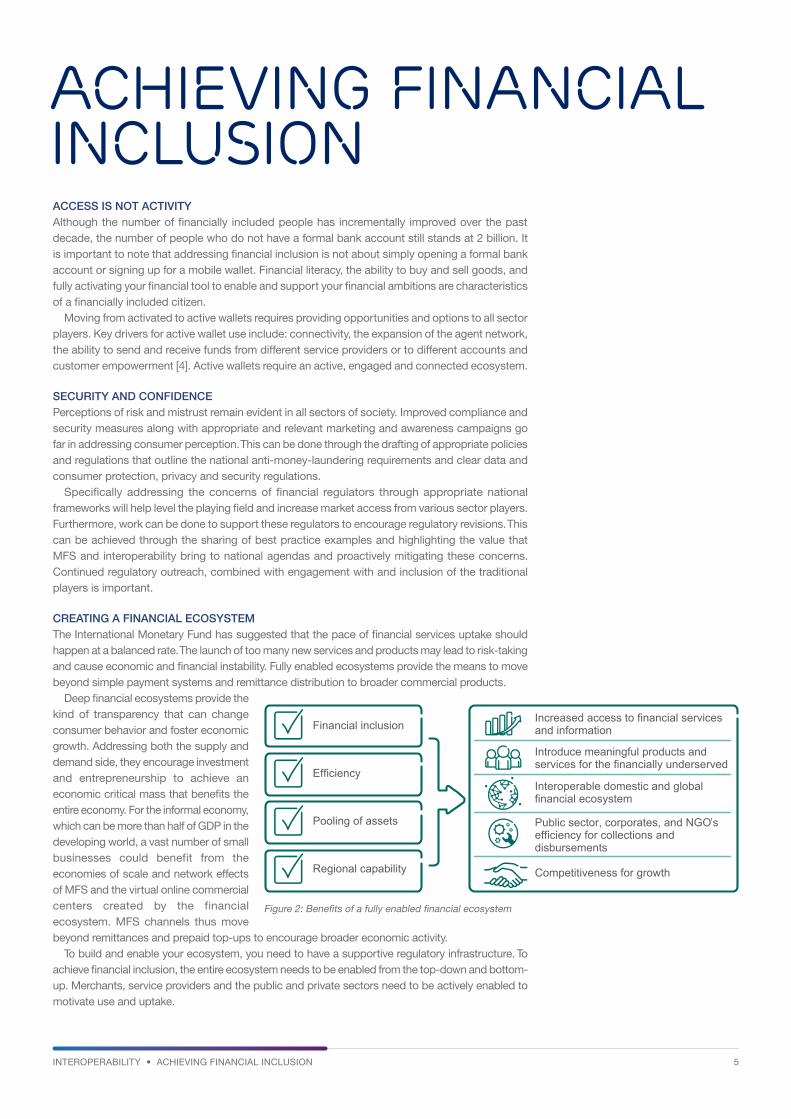

CREATING A FINANCIAL ECOSYSTEM

The International Monetary Fund has suggested that the pace of financial services uptake should

happen at a balanced rate. The launch of too many new services and products may lead to risk-taking

and cause economic and financial instability. Fully enabled ecosystems provide the means to move

beyond simple payment systems and remittance distribution to broader commercial products.

Deep financial ecosystems provide the

kind of transparency that can change

consumer behavior and foster economic

growth. Addressing both the supply and

demand side, they encourage investment

and entrepreneurship to achieve an

economic critical mass that benefits the

entire economy. For the informal economy,

which can be more than half of GDP in the

developing world, a vast number of small

businesses could benefit from the

economies of scale and network effects

of MFS and the virtual online commercial

centers created by the financial

ecosystem. MFS channels thus move

beyond remittances and prepaid top-ups to encourage broader economic activity.

To build and enable your ecosystem, you need to have a supportive regulatory infrastructure. To

achieve financial inclusion, the entire ecosystem needs to be enabled from the top-down and bottom-

up. Merchants, service providers and the public and private sectors need to be actively enabled to

motivate use and uptake.

Financial inclusionIncreased access to financial servicesand information

Introduce meaningful products andservices for the financially underserved

Interoperable domestic and globalfinancial ecosystem

Public sector, corporates, and NGO’sefficiency for collections anddisbursements

Competitiveness for growth

Efficiency

Pooling of assets

Regional capability

Figure 2: Benefits of a fully enabled financial ecosystem

INTEROPERABILITY • WITH OR WITHOUT INTEROPERABILITY 6

With or without interoperabilityRISKS TO BE CONSIDERED

It is important to consider the effects of regulation on the promotion of financial ecosystems

and interoperability at an early stage. Competitive issues need to be contemplated at the

outset, even when the number of users is low. The rise in use and popularity of a service

may lead to the dominance of one actor, which can hinder new players from entering the

market and thus reducing competition as well as raising prices and fees [5]. This early

dominance can reduce market efficiency over time and inhibit interconnection with new

products, thus causing lower innovation as well as limiting the growth of both the new and

old services.

So, what part should regulation play – and when is it best to regulate? There are arguments

suggesting that enforcing interoperability of financial services at too early a stage could

impede the willingness of firms to enter the market. A good case can be made for ensuring

at an early stage that interoperability is technically possible without mandating it.

Regulators should put in place policies that incentivize the provider where necessary,

and include appropriate provisions to enable and support ecosystem development.

Governments also need to ensure that these provisions are balanced and that they both

drive and protect sector investment in MFS.

Special case of MNOs – MNOs raise specific concerns since they control the

communications infrastructure that mobile financial service providers require. This is

especially true when the owner of the communication infrastructure is themselves providing

a service using that infrastructure. Regulators may be concerned that MNOs may have the

ability and will to foreclose competing providers. The solution to this issue will often depend

on country-specific concerns and context, which will require the cooperation of

telecommunications, financial and competition regulators.

INTEROPERABILITY IN PRACTICE

Many international and national commitments have been made toward achieving

interoperability and financial inclusion. The implementation of these commitments has

often varied due to various national interests, awareness and regulatory maturity and

models. There is no “one size fits all” – interoperability should be responsive to the national

and regional peculiarities.

National and regional context – interoperability takes on many different shapes and is

included in national frameworks in different ways. For example, within Colombia, the

financial inclusion law [6] contains a clause mandating MNOs to give financial institutions

fair access to their networks: the same provision in the decree is applicable to the low-

value payment systems. This sets up a series of principles that will allow users of specific

mobile money providers to make payments and transactions using any POS terminals,

ATMs or any other mechanism provided by any financial sector interacting with any other

financial institution. This broad and inclusive approach to interoperability is similar to that

of Tanzania, which defines interoperability as a situation in which payment instruments

belonging to a given electronic payment scheme may be used in another electronic payment

scheme installed by another bank or financial institution [7].

Within Myanmar, entities that offer MFS should be able to provide interoperable services

with other MFS providers. This interoperability needs to be at various levels and tailored to

market demands, including the needs of the agent, customer or mobile platform level [8].

These strong examples go a long way to realizing interoperability, encouraging competition

and the low cost launch of new services.

Not enforcing interoperability – there are successful examples of regions that have

chosen not to enforce interoperability from the start. The Kenyan market, for instance,

continues to divide opinions in this regard. While there is a huge increase in digital payments

INTEROPERABILITY • WITH OR WITHOUT INTEROPERABILITY 7

and allied transactions enabled by investments from dominant sector providers, the jury

is out on if indeed the lack of effective enforcement of interoperability policies and

regulations has supported financial inclusion in its true sense.

Without regulatory direction, guidance, and leadership, Kenya and similar countries which

are taking the lead in digital payment are unlikely to have a fully interoperable system,

which in turn may impact the drive for financial and economic inclusion. A typical example

is that of a customer holding multiple accounts with several different providers.

Interoperability issues arise when one account holder wishes to transfer money to someone

with an account at a different provider.

Most dominant providers who claim interoperability have achieved some level of that

through bilateral contracts between key players. This, however, is not interoperability in

the true sense.

In an effort to address this problem, Kenya decided to allow non-banks like M-PESA to

establish exclusive contracts with the agents in their distribution network [9]. The rationale

is that this ought to provide wider coverage for consumers and build trust. However, what

this promotes is wider exclusivity rather than interoperability. In reality, each network of

agents is, in every respect, unconnected to and independent of the others in the country.

However, there is some progress being made in the sector as banks have recently been

allowed to create agent networks under the condition that they are not permitted to require

exclusivity.

Mandating interoperability – regulators have two basic methods of encouraging

interoperability: setting standards for interconnectivity and enforcing interoperability.

Enforcing interoperability can happen by either setting interconnection charges or requiring

the unbundling of platform provision from the provision of accounts. This is not an easy

task and one that sees an overlap between regulation of telecom services and that of

account providers.

The Rwandan government, recognizing the importance and value of interoperability as

a means of achieving financial inclusion, coupled with an ambitious plan to position Rwanda

as the first truly digital economy in Africa, has recently taken a significant step toward

nationwide interoperability through the setting up of a national interconnecting switch.

When established, financial and payment service providers will be required to connect

to this central switch. This innovative use of new information and technical software has

been driven by the Ministry of Finance and Economic Planning for Rwanda with strong

involvement and guidance from the financial regulator.

Within Rwanda, there is a clear opportunity for interoperability between financial

institutions and the MNOs with a focus on financial inclusion. The regulatory approach

adopted in Rwanda is particularly interesting; not only is it clear that there is a strong

political will to address financial inclusion, but there is also a strong understanding of the

value of interoperability in realizing that goal. Financial institutions and MNOs will be

interconnected to offer services to virtually all banked and unbanked customers to achieve

interoperability and to substantially increase the financial services outreach to the unbanked

communities [10].

INTEROPERABILITY: WHICH PATH TO TAKE?

There is a choice to be made by regulators when deciding how best to foster economic

and social inclusion through the efficient and wide distribution of MFS. Limited or full

interoperability may happen regardless of regulatory oversight. However, in these cases it

will often depend on the will of individual players to negotiate and establish a number of

bilateral agreements. This requires enormous effort and persistence by key players who

may not necessarily have financial inclusion or the easy entry of new financial service

providers as their top priority.

Considering the dynamics of competition early on is essential. As is the role that

policymakers, supervisors and regulators play in fostering financial inclusion. It could also

be useful to examine case studies comparing mandated interoperability with more market-

driven approaches.

It should also be noted that the advantages of interoperability such as lowered costs,

customer value, efficiency and increased competition may be shared unfairly among the

various players. Early entrants to a market may see enforced interoperability as a disincentive

INTEROPERABILITY • WITH OR WITHOUT INTEROPERABILITY 8

if it means that it will prevent them from recouping their investments.

Regulators can choose between the following three approaches:

> enforce early interoperability

> let the market establish itself with little regulatory involvement

> encourage and incentivize the market toward interoperability

This last option means guiding the market by establishing interoperability as a policy

objective and setting a timeline in which the market must move to interoperability before

it is enforced by regulation. The best choice will often depend on each market’s context

and objectives.

INTEROPERABILITY • CONCLUSION 9

ConclusionInteroperability supports financial inclusion, as it reduces the duplication of services and makes

service delivery more efficient. Furthermore, given that it facilitates cooperation between sector

players, it contributes to market access and service reach. In doing this, it addresses some of

the barriers the consumer may face, including high user fees and limited access.

An interoperable approach requires cooperation between payment service sectors as well as

other sector players. This depends not on IT solutions but on political will and a strong regulatory

approach. The facilitation of interoperability needs to be done under the umbrella of safe,

supportive and enabling regulations and policies. This regulatory development can be encouraged

through strong government leadership and direct regulator and market engagements, the

proliferation of best case practices and multi-sectoral mobilization.

Government and national regulators should:

> address the challenges that perceived competition within the private sector represents–within

and between financial institutions and payment service providers and the role that regulation

plays in encouraging technology for good within existing business models

> facilitate new market entry and encourage the growth and expansion of non-traditional financial

service providers, in particular MNOs, in a compliant and secure way

> encourage sector players to participate and engage in the interoperable network–merchants,

agents, MNOs and consumers alike

> incentivise the market and encourage services providers to recognise the need for interoperability

as part of their service, for example, through tax relief

> take the lead in encouraging consumers to transact digitally, for example by providing

government services online and discounts for individuals who pay for these services through

their wallet solutions

> ensure that the role of IT infrastructure can be appropriately positioned to realize an

interconnected society – a society where IT infrastructure deployment reflects purpose-built

regulations and policies, with tailored solutions designed around an agreed goal

Mobile financial services must evolve from being solely a tool for transferring money to being

the means of empowering the world’s poor with access to banking, credit and insurance markets.

In this way, the goal of true financial and economic inclusion can be achieved.

INTEROPERABILITY • REFERENCES 10

References[1] The World Bank: UFA2020 Overview: Universal Financial Access by 2020, August 18, 2016,

available at: http://www.worldbank.org/en/topic/financialinclusion/brief/achieving-universal-

financial-access-by-2020

[2] The World Bank, Championing interoperability for financial inclusion: carrot or stick?, July 27,

2016, Lammer, T, available at: http://blogs.worldbank.org/psd/championing-interoperability-

financial-inclusion-carrot-or-stick

[3] The World Bank, World Bank Group and a Coalition of Partners Make Commitments to

Accelerate Universal Financial Access, April 17, 2015, available at: http://www.worldbank.org/

en/news/press-release/2015/04/17/world-bank-group-coalition-partners-make-commitments-

accelerate-universal-financial-access

[4] CGAP, Empower the Customer to Choose and Use Financial Services, April 28, 2015, Koning,

A and Valenzuela, M, available at: https://www.cgap.org/blog/empower-customer-choose-and-

use-financial-services

[5] CGAP, Addressing Competition Bottlenecks in Digital Financial Services, October 15, 2015,

Sitbon, E, available at: https://www.cgap.org/blog/addressing-competition-bottlenecks-digital-

financial-services

[6] International Monetary Fund, IMF Working Paper: Financial Inclusion, Growth and Inequality:

A Model Application to Colombia, September 2014, Karpowicz ,I, available at: https://www.imf.

org/external/pubs/ft/wp/2014/wp14166.pdf

[7] Bank of Tanzania, Electronic Payment Schemes, May 2007, available at: http://www.bot.go.tz/

PaymentSystem/Docs/e_Schemes%20Guidelines%20June%202007.pdf

[8] Central Bank of Myanmar, Regulation on Mobile Financial Services (FIL/R/01/03-2016), March

30, 2016, available at: http://www.cbm.gov.mm/sites/default/files/regulate_launder/_fil-r-01_

mobile_financial_services_regulation_eng_final_website_4-4-2016_-5.pdf

[9] CGAP, Regulating Banking Agents, March 2011, Tarazi, M, Breloff, P, available at: https://www.

cgap.org/sites/default/files/CGAP-Focus-Note-Regulating-Banking-Agents-Mar-2011.pdf

[10] IGC, The Regulation of Mobile Money in Rwanda, August 2013, Argent, Hanson, Gomez,

available at: http://www.theigc.org/wp-content/uploads/2014/09/Argent-Et-Al-2013-Working-

Paper.pdf

INTEROPERABILITY • FURTHER READING & GLOSSARY 11

Global Standard-Setting Bodies and Financial Inclusion: The Evolving Landscape – GPFI

http://www.gpfi.org/publications/global-standard-setting-bodies-and-financial-inclusion-

evolving-landscape

Mobile Banking and Financial Inclusion: The Regulatory Lessons - Klein, M. & Mayer, C.

https://www.microfinancegateway.org/library/mobile-banking-and-financial-inclusion-

regulatory-lessons

Further reading

© 2016 Ericsson AB – All rights reserved

MFS mobile financial services

MNO mobile network operator

POS point-of-sale

Glossary