internship report on foreign exchange operation of jamuna bank limited

DESCRIPTION

A Final Internship ReportTRANSCRIPT

A Research ReportOn

Foreign Exchange Operations of Jamuna Bank

1

JAMUNA BANK LIMITED

2

JAGANNATH UNIVERSITY, DHAKA

Report

3

On

4

Prepared To :

A. K. M. Moniruzzaman Ph. D Professor

Department of Management Studies

5

JAGANNATH UNIVERSITY, DHAKA.

Prepared By:

Name : Md. Zakir Hossain ID : 05122353 Sec : A Session : 2005-2006

Department of Management StudiesJAGANNATH UNIVERSITY, DHAKA.

6

Date of Submission: 20th November, 2011

Letter of Transmittal

To A. K. M. Moniruzzaman Ph. DProfessorDepartment of Management studies

7

Jagannath University Dhaka.

Subject: Submission of Internship Report.

Dear Sir,

It is my privilege to let you know that as partial fulfillment of the requirements for the degree of Bachelor of Business Administration (BBA), I have completed my term paper report in the Jamuna Bank Limited. I have to furnish a report based on my practical experience. The report focuses mainly on the foreign exchange operations of Jamuna Bank Limited.

8

It was stimulating opportunity and a valuable experience for me to the real business world. I am grateful for providing me such an opportunity to gather practical experience of working in a private commercial bank, like Jamuna Bank Limited.

Hope that you would be very pleased to accept my report and oblige me.

Sincerely Yours

Md. Zakir HossainID – 05122353Department of Management Studies

9

Jagannath University Dhaka.

ACKNOWLEDGEMENT

10

At first I want to express my gratitude to almighty Allah for giving me the strength, ability and opportunity to complete the report within the schedule time successfully.

My sincere gratitude goes to my respected internship supervisor, Professor A. K. M. Moniruzzaman Ph. D, report would not have been possible and such endeavor really deserves compliment. Thanks to him for giving me the opportunity to prepare this report which I think will enhance my skill and help the practical application of my knowledge in future.

I received cordial cooperation from the officers and members of staffs of jamuna Bank Ltd, Dilkusha / Principal branch, Dhaka and the teachers and staff of Jagannath University of Dhaka. I want to express my cordial gratitude to them for their cooperation without which it would not have been possible to complete the report.

11

I am reallythankful to Mr. Kamal Uddin, SAVP and operation in charge, Jamuna Bank Dilkusha Branch for giving me the excellent opportunity to do my practical coordination in this branch. I would also like to thank to Mr. Shahed Morshed Chowdhury, JAVP, Mr. A S.M Masouk, SEO, Mr. ABM Mazharul Hoque Sikder, EO of Import Division, and Ms. Sapna Habib Srabanti, Officer, Customer Care for giving me the excellent direction with their proper compassionate with me.

12

Executive Summary

13

A few years back also, banks are nothing but a medium whose only task is to collect money from

people who have excess of it and give it to those people who need it.But very recently banks

have diversified their operations into various sectors. Even, they have notification able

contribution in maintaining the global relation among various countries of the world. The JBL is

one of the newest banks of Bangladesh; in fact, it has been doing business just over 10 years in

the country. However, in this short period of time, it has already made a significant impact on the

economic, financial, and social system of Bangladesh. Jamuna Bank Ltd has a long and relishing

heritage. Jamuna Bank Limited (JBL) started its journey in the financial sector of the country as

an investment company back in May 20, 1999. The company operated up to 1999 with 9

branches and thereafter with the permission of the Central Bank converted in a full-fledged

14

schedule private commercial bank in June 2, 1993 with paid up capital of Tk. 39.00 crore to

serve the nation from a broader platform. The Bank and its first Branch at the busiest commercial

hub of the country at 61, Dilkusha commercial Area, Dhaka was opened. My Report titled

“Foreign Exchange Practices in Private Banks: A Case Study of Jamuna Bank Ltd.” is conducted

to describe the section as well as the organization where I was placed as an Intern. The first

chapter gives a broad over view about the origin of the report, objective of the report,

methodology of preparing the report, data collection procedure and its source, scope and

limitations faced while preparing the report. After the first part it has been focused in the second

part of the report. The overview consists of the definition and objective of the bank, historical

background of the banking institutions and banking operations in Bangladesh.

15

The report part started from the third chapter. In that chapter, describe the theoretical framework

of foreign exchange and other foreign exchange activities.The fourth chapter is highlighted of

Jamuna bank with SWOT analysis.The fifth chapter consists General foreign exchange policy of

the bank.The sixth chapter consists of performance evaluation of the bank in 2009.The seventh &

last chapter highlighted with recommendations, problems and Conclusion.

Table of Contents

16

Chapter-1Introduction

1.1 Statement of the research problem 101.2 Objectives of the Study 101.3 Methodology of the Study 111.4 Definition of terms used in the study 12-131.5 Limitation of the study 13

Chapter-2Scenario of Foreign Exchange Operations in Bangladesh.

2.1 Illustrated the international trade in Bangladesh with the help 15

17

of a diagram

2.2 Scenario of Foreign Exchange Operations in Bangladesh. 16-17

Chapter-3

An Overview of Jamuna Bank LTD.

3.1 Background 193.2 Corporate Information 19-203.3 Organization Structure 213.4 Branches information 223.5 Number of employees 233.6 Vision statement of the Bank 23

18

3.7 Mission statement of the Bank 233.8 Product scheme 243.9 Principal Activities 243.10 SWOT analysis of JBL 253.10.1 Identification of Strengths, Weaknesses, Opportunities and

Threats of the JBL26-27

3.10.2 Draw conclusion 273.10.3 Prepare action plan 27

Chapter-4Foreign Exchange: Theoretical Background &

19

Practical Experiences

4.1 Objectives of Jamuna Bank 294.2 Strategies of JBL 294.3 Foreign exchange: its meaning and definition 304.4 Types of foreign exchange 30-314.5 Tools for foreign exchange 31-324.6 General Foreign exchange policy of JBL 33-35

Chapter-5Data Analysis

& Findings

20

5.1 Findings 375.2 Performance of the Bank 38-405.3 Key Financial Indicators 41-465.4 Identified problems for the JBL 47

Chapter-6

Conclusions and Recommendations

6.1 Recommendation for the JBL 496.2 Conclusion 50

Bibliography 51Acronyms 52

21

22

List of Tables and Figures

SL List of Figure Page01 Framework of the overall structure of the total work 1602 Organization Structure of JBL 28

03 Branch Network 2904 SWOT Analysis 3005 The international trade can be illustrated by the following diagram 4406 Types of Foreign Exchange 4907 Profit scenario of JBL 5008 Capital Tire-I 71

23

09 Capital Tire-II 8810 Capital Tire-I & II 9711 Deposit & Deposit Mix 9812 Import Trade 9813 Export Trade 98

SL List of Tables Page

01 Ways of classifying products and services 16

02 Import procedure Flow Chart 3403 Export procedure Flow Chart 4304 Highlights of Jamuna Bank 67

24

05 Capital adequacy ratio 6806 Deposit & Deposit Mix 7307 Import Position 9608 Export Position 10009 Foreign Remittance position 10110 Acronyms 101

25

26

Chapter One

Introduction Chapter One

Introduction

1.1 Statement of the research problem

To write a report it is necessary to select a topic. A well-defined topic reflects what is going on to

be discussed throughout the report. The topic that has been assigned by organization supervisor

is “The foreign exchange operations– the ultimate way to success”. The report has discussed how

the bank can improve the foreign exchange operations.

27

1.2 Objectives of the study

Primary objective:The primary objective of this report is to familiar with the working environment of present

institutions. And also fulfill the requirement of BBA theoretical knowledge gained from the

coursework of the BBA program in a specific field.

Secondary Objective:

To have exposure to the credit operation and other function of Jamuna Bank Limited.

28

To have a clear understanding of the business operation of Jamuna Bank Limited.

To discuss the services offered by Jamuna Bank Limitcd.

To assess and evaluate the growth trends of Jamuna Bank Limited. To evaluate the profitability of Jamuna Bank Limited. To identify the major strength and weakness of Jamuna Bank Limited in respect to

other banks.

To recommend ways and means to solve problems regarding banking of Jamuna

Bank Limited.

29

To get acquainted with the loan structure, size, profile of sector wise outstanding position

of loans and system of loan classification of Jamuna Bank Limited.

1.3 Methodology of the Study

To make the Report more meaningful and presentable, two sources of data and information’s have been used widely.

The “Primary Sources” are as follows:

Face-to-face conversation with the respective officers and staffs of the Branch

Informal conversation with the clients

30

Practical work exposures from the different desks of the four departments of the

Branch covered

Relevant file study as provided by the officers concerned

The “Secondary Sources” are as follows:

Annual Report (2009) of Jamuna Bank Ltd.

Periodicals published by Bangladesh Bank.

Various books, articles, complications etc. regarding general banking function, foreign

exchange operation and credit policies.

FRAMEWORK OF THE OVERALL STRUCTURE OF THE TOTAL WORK

31

Doing work in different department of ABBL

32

Selecting the topic of the study

Preparing outline

Collecting secondary informatio

Analysis of collected data ninformati

Collecting information from ABBL

Dividing the study work

Appointing as an intern

Preparation of the Final Report

1.4 Terms used in Foreign Exchange Operations

Foreign Exchange:

Foreign exchange refers to the process or mechanism by which the currency of one country is

converted into the currency of another country. According to Foreign Exchange Regulation Act

(FERA) 1947, "Anything that conveys the right to wealth in another country is foreign exchange.

Foreign exchange means and includes all deposits, credits and balances payable in foreign

33

currency as well as foreign currency instruments such as drafts, TCs. Bill of Exchange,

promissory Notes and Letters of Credit payable in any foreign currency. ".

Liquidity:

In terms of international trade, liquidity is the ease in which foreign currency is converted into

domestic currency. FX markets, such as the New York Jamuna Exchange, match buyers and

sellers to bring about speedy, orderly transactions.

International Trade:

34

Businesses rely on FX markets to buy currency that is spent to obtain overseas goods.

Corporations will also look to FX markets to convert international earnings back into the

domestic currency.

Imports and Exports:

Businesses all around the world are increasingly depending on buying and selling from other

countries. Although the international trade environment has changed substantially over the last

100 years, the risks have essentially remained the same. Jamuna Bank is ready to assist you with

your trade documentation and adherence to exchange control regulations.

35

SWIFT:Electronic payments are the most commonly used method of transferring any currency.

These payments are most commonly used for imports and exports, but holidaymakers may also

use them. They are done using SWIFT, a worldwide electronic payment and receipts network.

Traveller's Cheques:

If you are travelling out of the country either for business or holiday, you can buy Traveller's

Cheques directly from us.

Letter of credit (L/C):Letter of credit means any arrangement whereby a Bank (the issuing Bank) is committed (on behalf of the buyer/applicant) to pay certain amount at the seller’s disposal under some agreed conditions.

36

Foreign remittance:

Foreign remittance means remittance of foreign currencies from one place/person to another place/person. In broad sense, foreign remittance includes all sale and purchase of foreign currencies on account of Import Export, Travel and other purposes. However, especially foreign remittance means sale & purpose of foreign currencies for the purposes other than export and import. SOUTHEAST Bank Limited performs the remittance function with different countries. It maintains the foreign remittance in the following form:

Foreign Demand Draft Inward Remittance Outward Remittance

37

1.5 Limitation of the study

All the time of preparing my report I tried to gather every details of process but the major limitation is lack of adequate information,

Lack of opportunity to visit more than one branch Sufficient records, publications were not available as per my requirement. Time constraint. Non-cooperative behavior of some officials of the bank. It is my first work, and inexperience was a problem.

38

39

40

Chapter Two Scenario of Foreign Exchange Operations in Bangladesh.

Chapter Two Scenario of Foreign Exchange Operations in Bangladesh.

2.1 The international trade can be illustrated in Bangladesh by the following

diagram

41

Contract of sale (1)

Contract of sale (1)

Exporter (Beneficiary)

Importer(Applicant)

Ships Goods to

(5)

Forwards L/C to

(4)

Presents documents and obtains payment from (6) Recovers Amount from (8)

Applies for opening of L/C (2)

Advising/ negotiating Bank Obtains reimbursement

from (7)

\

Issuing Bank

Opens L/C and send it to (3)

42

43

2.2 Scenario of Foreign exchange operations in Bangladesh

1. Foreign Exchange Regulation (FER) Act, 1947 (Act No. VII of 1947) enacted on 11th March,

1947 in the then British India provides the legal basis for regulating certain payments, dealings in

foreign exchange and securities and the import and export of currency and bullion. This Act was

first adapted in Pakistan and then, in Bangladesh. The Act is reproduced at Appendix-1.

44

Bangladesh Bank is responsible for administration of regulations under the Act. Appendix 4

provides a list of Bangladesh Bank's offices and their jurisdictions.

2. Basic regulations under the FER Act are issued by the Government as well as by the

Bangladesh Bank in the form of Notifications which are published in the Bangladesh Gazette.

Notifications issued by the Bangladesh Government and the erstwhile Government of Pakistan

and the Bangladesh Bank and the erstwhile State Bank of Pakistan are reproduced at Appendices

2 and 3. Directions having general application are issued by the Bangladesh Bank in the form of

notifications, foreign exchange circulars and circular letters.

45

3. Authorized Dealers (ADs) in foreign exchange are required to bring the foreign exchange

regulations to the notice of their customers in their day-to-day dealings and to ensure compliance

with the regulations by such customers. The ADs should report to the Bangladesh Bank any

attempt, direct or indirect, of evasion of the provisions of the Act, or any rules, orders or

directions issued there under.

4. Bangladesh Bank issues licenses normally to scheduled banks to deal in foreign exchange if it

is satisfied that the bank applying for this license has adequate manpower trained in foreign

exchange.

46

5. Licenses with limited scope are also issued to persons or firms to exchange foreign currency

notes, coins and travellers' cheques in places where money changing facilities are required.

6. ADs, on their own, are free to buy and sell foreign currencies forward in accordance with tile

internationally established practices however, in all cases the ADs must ensure that the cover is

intended to neutralize the risks arising from definite and genuine transactions.

7. All remittances from Bangladesh to a foreign country or local currency credited to on resident

Taka accounts of foreign banks or convertible Taka account constitute outward remittances of

foreign exchange

47

8. Lacking of experience related to foreign cxchange policy.

9. Lacking of skill manpower.

10. Lacking of proper knowledge about foreign exchange policy and related items.

48

49

50

Chapter Three

An Overview of Jamuna Bank

Chapter Three

An Overview of Jamuna Bank

51

52

3.1 Background

Jamuna Bank Limited (JBL) is a Banking Company registered under the Companies Act, 1994 with its head office at Printers Building (2nd floor and 8th

floor), 5, Rajuk Avenue, Dhaka-1000. The Bank started its operation from 3rd June 2001.

53

Jamuna Bank Limited is a highly capitalized new generation Bank started its operation with an authorized capital of Tk.1600.00 million and paid up capital of Tk.390.00 million, as of December 2006 Paid up capital of the Bank raised to Tk.1072.5 million and number of branches raised to 29 (Twenty nine).

JBL undertakes all type of banking transactions to support the development of trade and commerce in the country. JBL’s services are also available for the entrepreneurs to set up new ventures and BMRE for industrial units. The Bank gives special emphasis on Export, Import, Trade Finance, SME Finance, Retail Credit and Finance to Women Entrepreneurs.

54

To provide clientele services in respect of International Trade it has established wide correspondent banking relationship with local and foreign banks covering major trade and financial centres at home and abroad.

3.2 Corporate Information of Jamuna Bank

Registered Office:

55

Chini Shilpa Bhaban3, Dilkusha C/A, Dhaka-1000.

Company Registration Number:

C-42780 (2139)/2001External Audior(s)Howladar Yunus & Co

56

Chartered Accountants67, Dilkusha C/A (2nd Floor), Dhaka-1000

Legal Advisor

Mr. Habibul Islam BhuiyanSenior AdvocateBhuiyan Islam & ZaidiAdvocates and BarristersH# 29, Rd# 9/A, Dhanmondi R/A, Dhaka

Number of Branches & SME/ Agri Branches / Centers

57

Total Branches: 52SME/ Agri Branches: 3SME/ Agri Centers: 1

Allied Concern

Jamuna Bank FoundationHadi Mansion (4th Floor), 2, Dilkusha C/A, Dhaka

Subsidiary Company

Jamuna Bank Capital Management Ltd (Proposed)

58

Chini shilpa Bhaban3, Dilkusha C/A, Dhaka-1000

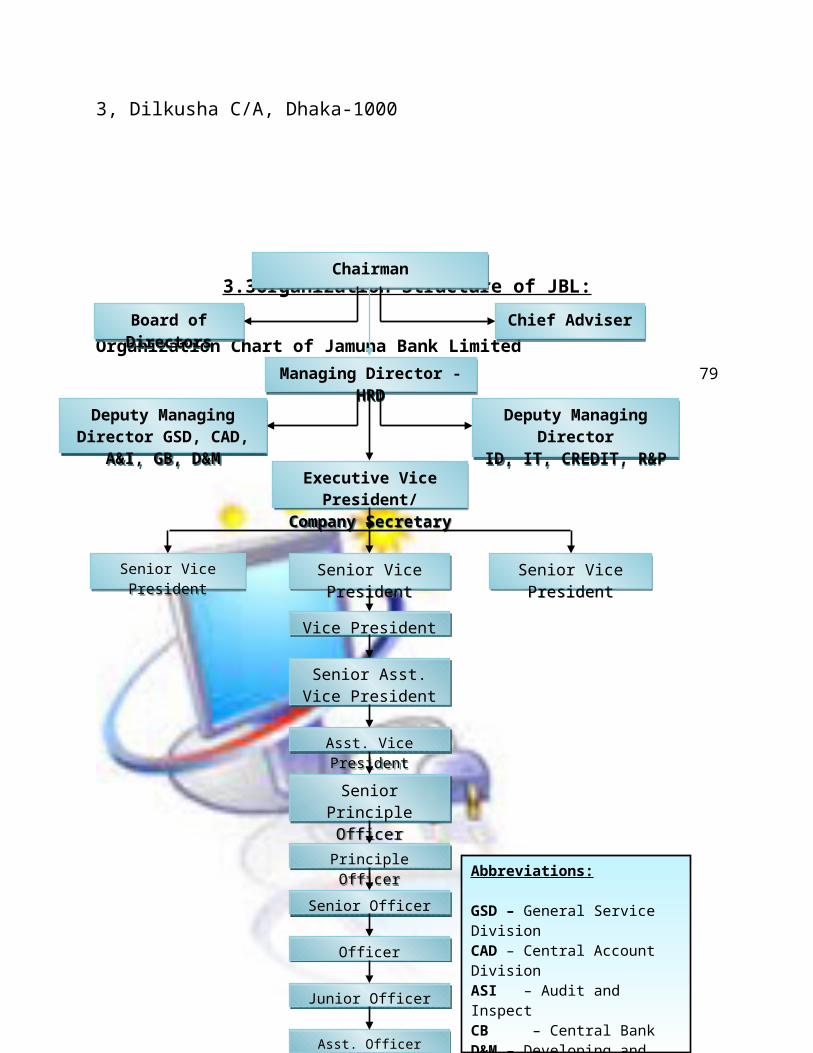

3.3Organization Structure of JBL:

Organization Chart of Jamuna Bank Limited

59

ChairmanChairman

Managing Director - HRDManaging Director - HRD

Executive Vice President/Company Secretary

Executive Vice President/Company Secretary

Chief AdviserChief AdviserBoard of DirectorsBoard of Directors

Deputy Managing DirectorID, IT, CREDIT, R&P

Deputy Managing DirectorID, IT, CREDIT, R&P

Deputy Managing Director GSD, CAD, A&I, GB,

D&M

Deputy Managing Director GSD, CAD, A&I, GB,

D&M

Senior Vice PresidentSenior Vice President Senior Vice PresidentSenior Vice PresidentSenior Vice PresidentSenior Vice President

Vice PresidentVice President

Senior Asst. Vice President

Senior Asst. Vice President

Asst. Vice PresidentAsst. Vice President

Senior Principle Officer

Senior Principle Officer

Principle OfficerPrinciple Officer

Senior OfficerSenior Officer

OfficerOfficer

Junior OfficerJunior Officer

Asst. OfficerAsst. Officer

Abbreviations:

GSD – General Service DivisionCAD – Central Account DivisionASI – Audit and InspectCB – Central BankD&M – Developing and MarketingID – International DivisionR&P – Research & Planning

60

61

Figure: 3.3 Organization chart of JBL

3.4 Branch Information

Branch: 52 & SME / Agri Branch : 4

62

63

3.5 Number of employees

Number of employees in the main branch of Jamuna bank is 65

3.6 Vision statement of the bank

To become a leading banking institution and to play a pivotal role in the development of the country.

64

3.7.Mision statement of the bank

The Bank is committed to satisfying diverse needs of its customers through an array of products at a competitive price by using appropriate technology and providing timely service so that a sustainable growth, reasonable return and contribution to the development of the country can be ensured with a motivated and professional work-force.The bank has some mission to achieve the organizational goals. Some of them are as follows as:

Jamuna Bank Limited provide high quality financial services to strengthen the well being

and success of individual, industries and business communities.

Its aim to ensure their competitive advantages by upgrading banking technology and

information system.

65

JBL intends to play more important role in economic development of Bangladesh and its

financial relations with the rest of the world by interlining both modernistic and

international operations.

JBL encourages investors to boost up share market.

The bank creates wealth for the shareholders.

The bank believes in strong capitalization.

It maintains high standard of corporate and business ethics.

Jamuna Bank Limited extend highest quality of services, which attracts the customers to

choose them first.

The bank creates wealth for the shareholders.

66

The bank maintains congenial atmosphere for which people are proud and eager to word

with Jamuna Bank Limited.

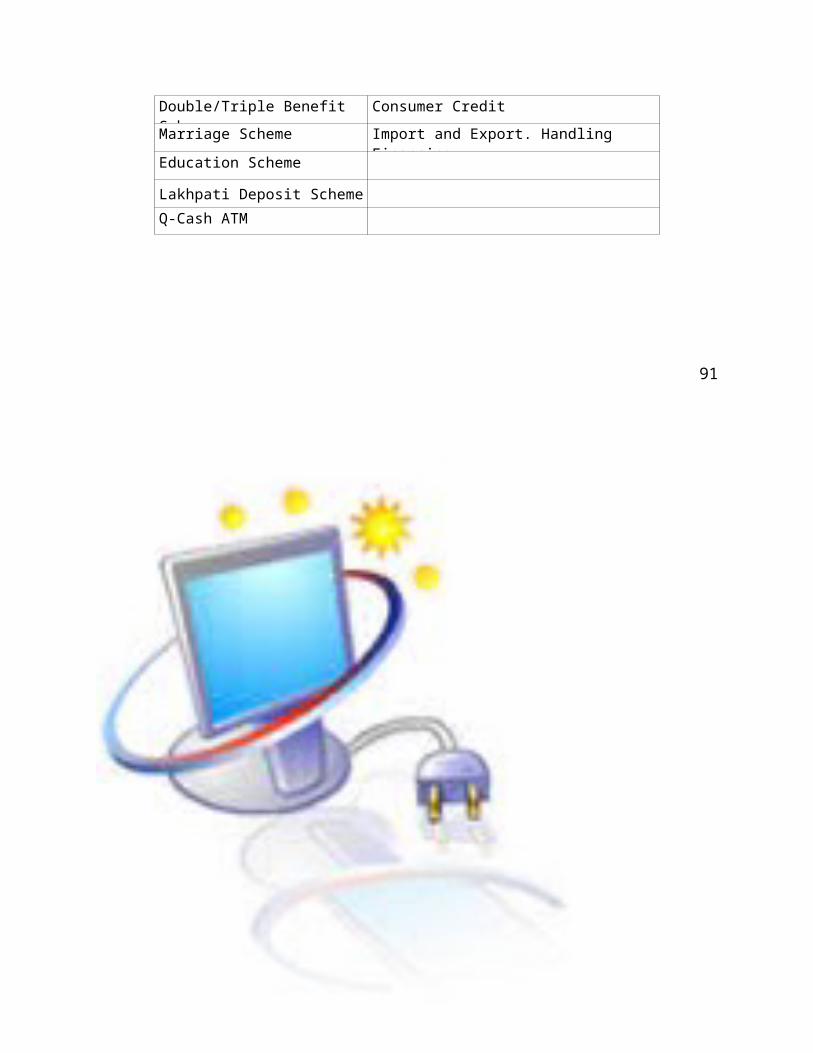

3.8 Product Scheme

The products and services can be classifying in two ways & those arc.

The deposit products & services

The lending products & services

67

Deposits products & services Lending/Investment products & services

Corporate Banking Hi-her Purchase

Personal Banking Lease Finance

Online Banking Personal loan for woman

Monthly Savings Scheme Project Finance

i Monthly Benefit Scheme i Loan Syndication

Double/Triple Benefit Scheme Consumer Credit

Marriage Scheme Import and Export. Handling Financing

Education Scheme

68

Lakhpati Deposit Scheme

Q-Cash ATM

3.9 Principal activities of Jamuna bank Ltd.

The principal activities of the bank are to provide all kind of commercial bank activities

encompass a wide range of services including excepting deposits, making loans, discounting

bills, conducting money transfer and foreign exchange transactions and performing other related

69

services such as safe keeping, collections, issuing guarantees, acceptances and letters of credit to

its customers through its branches in Bangladesh.

3.10 SWOT ANALYSIS OF JBL

In the competitive area of marketing are SWOT analysis is based on product, price, place and

promotion of a financial institution like private Bank. By doing the SWOT analysis it is possible

70

to find out the strengths, Weaknesses, opportunities, and threats of the JBL. From the SWOT

analysis we can figure out on going scenario of the Bank.

SWOT Analysis

SWOT analysis two factors act as prime movers

Internal factors which are prevailing inside the concern which include Strength and

Weakness.

71

Internal FactorsInternal Factors External FactorsExternal Factors

Weakness Weakness OpportunityOpportunityStrength Threats

On the other hand another factor is external factors which act as opportunity and threat.

3.10.1 Identification of Strengths, Weaknesses, Opportunities and Threats of

the JBL

Strength:

1. The bank provides quality service to the clients compared to it other contemporary

competitors.

2. Experienced bankers and corporate personnel have formed the management.

72

3. The bank recently introduce on line banking which enable it to automate all of its

operations. At present, several banking functions are performed by computers. The bank

is also a member of SWIFT (Society for Worldwide Inter bank Financial

Telecommunication) alliance Access which enables the bank to exchange critical

financial messages swiftly and cost effective.

Weaknesses:

1. Delegation of authority is centralized which makes the employee to realize less

responsibility. Thus, the employee morale is deteriorated.

73

2. The credit proposal evaluation process is lengthy. Therefore, sometimes valuable clients

are lost and the bank becomes unable to meet targets.

3. No substantive use of Annual Confidential Report (performance evaluation form of the

employee) to reward or to punish the employee. Hence the employee becomes

ineffective.

4. The bank lacks aggressive advertising and promotional activities to get a broad

geographical coverage.

5. Computer facility for all the officers is not available. Moreover, all the officers have no

computer knowledge.

6. The bank has no any research and development division.

74

Opportunities:

1. The bank can introduce more innovative and modern products and services for then

customers.

2. It can diversity its portfolio by taking new sector.

3. Many branches can be opened to reach the bank’s services to the remote areas.

4. It can recruit more efficient and experienced persons to give fast and efficient service to

the customers

Threats:

1. The common attitude of Bangladeshi clients is default.

75

2. Multinational as well as the fast growing local banks with modern products and services

are capturing huge market within short period a resulting to switch over the existing

customers of the bank.

3. Bangladesh Bank Sometimes requires Private Commercial Banks to be abides by such

rules and regulations which are not suitable for every commercial Bank

3.10.2 Draw conclusion

The bank provides quality service to the clients compared to its other contemporary competitors.

The bank can introduce more innovative and modern products and services for then customers.

76

The common attitude of Bangladeshi clients is default. Delegation of authority is centralized and

the bank has no any research and development division.

Conclusions concerning the company’s overall business situation:

Where on the scale from “alarmingly week” to “exceptionally strong” does the attractiveness of the company’s situation rank?

What are the attractive or unattractive aspects of the company’s situation?

3.10.3 Prepare action plan

77

Use company strengths and capabilities as cornerstones for strategy.

Pursue those market opportunities best suited to company strengths and opportunities.

Correct weaknesses and deficiencies that impair pursuit of important market opportunities or heighten vulnerability to external threats.

Use company strengths to lessen the impact of important external threats.

78

79

Chapter Four

Foreign Exchange: Theoretical Background &

Practical Experiences

Chapter Four

Foreign Exchange: Theoretical Background &

Practical Experiences

4.1 Objective of Jamuna Bank

• To earn and maintain CAMEL Rating 'Strong'

•To establish relationship banking and improve service quality through development of Strategic Marketing Plans.

•To remain one of the best banks in Bangladesh in terms of profitability and assets quality.

•To introduce fully automated systems through integration of information technology.

• To ensure an adequate rate of return on investment.• To keep risk position at an acceptable range (including any off balance sheet risk).

80

• To maintain adequate liquidity to meet maturing obligations and commitments.• To maintain a healthy growth of business with desired image.• To maintain adequate control systems and transparency in procedures.

•To develop and retain a quality work-force through an effective human Resources Management System.

• To ensure optimum utilization of all available resources.

•To pursue an effective system of management by ensuring compliance to ethical norms, transparency and accountability at all levels.

4.2 Strategies of JBL

81

•To manage and operate the Bank in the most efficient manner to enhance financial performance and to control cost of fund

•To strive for customer satisfaction through quality control and delivery of timely services

•To identify customers' credit and other banking needs and monitor their perception towards our performance in meeting those requirements.

•To review and update policies, procedures and practices to enhance the ability to extend better service to customers.

•To train and develop all employees and provide them adequate resources so that customers' needs can be reasonably addressed.

•To promote organizational effectiveness by openly communicating company plans, policies, practices and procedures to employees in a timely fashion

•To cultivate a working environment that fosters positive motivation for improved performance

82

• To diversify portfolio both in the retail and wholesale market

•To increase direct contact with customers in order to cultivate a closer relationship between the bank and its customers.

4.3 Foreign Exchange- its meaning and definition:

Foreign exchange refers to the process or mechanism by which the currency of one country is

converted into the currency of another country. Foreign exchange is the means and methods by

which rights to wealth in a country's currency are converted into rights to wealth in another

country's currency. In banks when we talk of foreign exchange, we refer to the general

mechanism by which a bank converts currency of one country into that of another. Foreign Trade

gives rise to foreign exchange.

83

According to Foreign Exchange Regulation Act (FERA) 1947, "Any thing that conveys the right

to wealth in another country is foreign exchange. Foreign exchange means and includes all

deposits, credits and balances payable in foreign currency as well as foreign currency

instruments such as drafts, TCs. Bill of Exchange, promissory Notes and Letters of Credit

payable in any foreign currency. ".

This definition implies that all business activities relating to Import, Export, Outward & Inward

Remittances, buying & selling of foreign commissions, etc. come under the purview of foreign

exchange business. Foreign exchange department of banks plays significant roles through

providing different services for the customers.

84

4.4 Types of Foreign Exchange:

There are mainly three types of transactions which lead to foreign exchange. These are:

a) Import

b) Export

c) Foreign Remittance

85

Foreign Exchange Department

L/C Foreign Remittance

Import Export Foreign Inward Outward

Currency A/C Remittance Remittance

86

4.5 Tools for foreign exchange

Importer (Buyer)/Applicant

The Issuing Bank (Opening Bank)

The Advising Bank/Notifying Bank

Exporter/Seller (Beneficiary)

87

Confirming Bank

Negotiating Bank

The Paying/Reimbursing/Accepting/Remitting Bank.

a) Applicant

The person/body (customer of the bank) who requests the bank (opening bank) to issue letter of

credit. As per instruction and on behalf of the applicant, bank open L/C in line with the terms and

conditions of the sales contract between the buyer and seller.

b) Opening bank/Issuing Bank

88

The bank which open/issue L/C on behalf of the applicant/importer. Issuing bank’s obligation is

to make payment against presentation of documents drawn strictly as per terms of the L/C.

c) Advising/Notifying Bank

The bank through which the L/C is advised/forwarded to the beneficiary (exporter). The

responsibility of advising bank is to communicate the L/C to the beneficiary after checking the

authenticity of the credit. The advising bank acts only as agent of the issuing bank without

having any engagement on their part.

d) Beneficiary

89

Beneficiary of the L/C is the party in whose favor the letter of credit is issued. Usually they are

the seller or exporter.

e) Confirming Bank

The Bank, which under instruction in the letter of credit, adds confirmation of making payment

in addition to the issuing bank. It is done at the request of the issuing bank having arrangement

with them. This confirmation constitutes a definite undertaking on the part of confirming bank in

addition to that of issuing bank.

f) Negotiating Bank

90

The Bank, which negotiate documents and pays the amount to the beneficiary when presented

complying credit terms. If the negotiation of documents is not restricted to a particular bank in

the L/C, normally negotiating bank is the banker of the beneficiary.

g) Reimbursing/Paying Bank

The Bank nominated in the credit by the issuing bank to make payment stipulated in the

document, complying with the reimbursing bank.

91

4.6 General foreign exchange policy of the Jamuna Bank LTD.

Import procedure in Flow Chart:

92

Registration with CCI&E, Import Registration Certificate

Registration of Letter of Credit Authorization Form(LCAF)

Purchase contract with foreign supplier directly or through agent

Yes

93

Opening/Issuance of L/C by the Importer’s Bank

Dispatch/Transmit the L/C to the beneficiary through issuing Bank’s correspondent in the beneficiary’s country

Receipt of import Documents from Negotiating/collecting bank

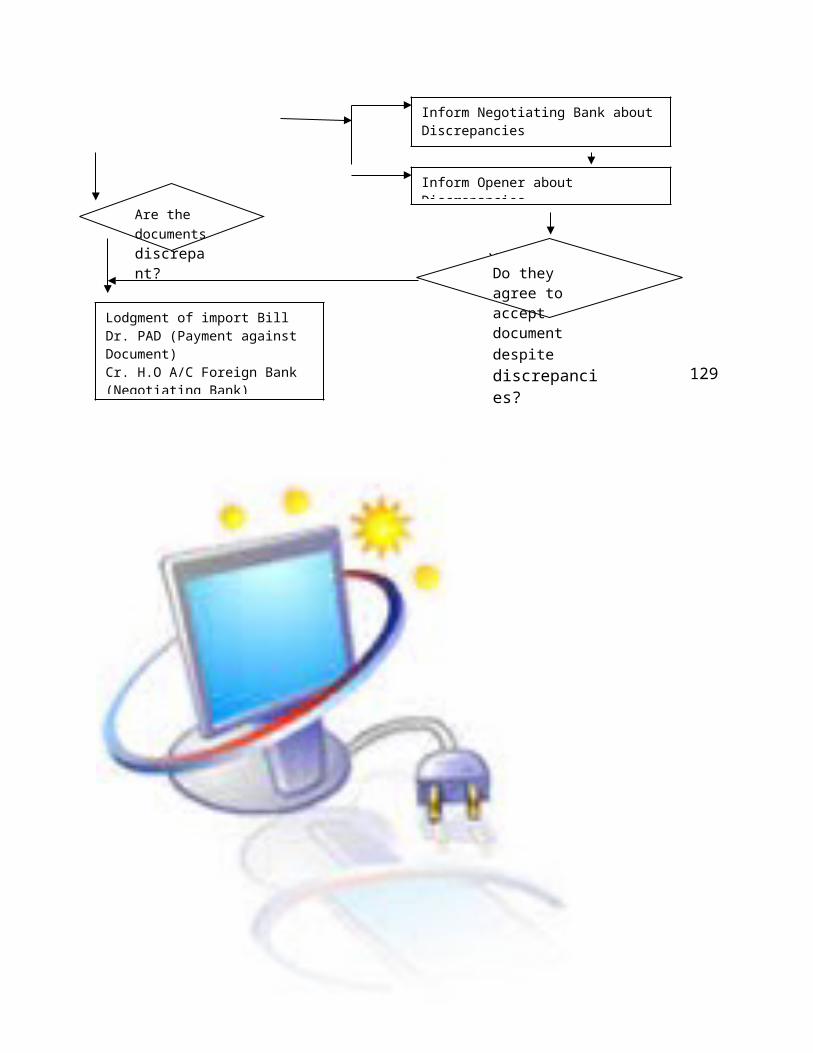

Scrutiny if import Document Inform Negotiating Bank about Discrepancies

Inform Opener about Discrepancies

Are the documents discrepant?

Yes

No

Yes

94

Do they agree to accept document despite discrepancies?

Lodgment of import BillDr. PAD (Payment against Document)Cr. H.O A/C Foreign Bank (Negotiating Bank) Ask Negotiating Bank for

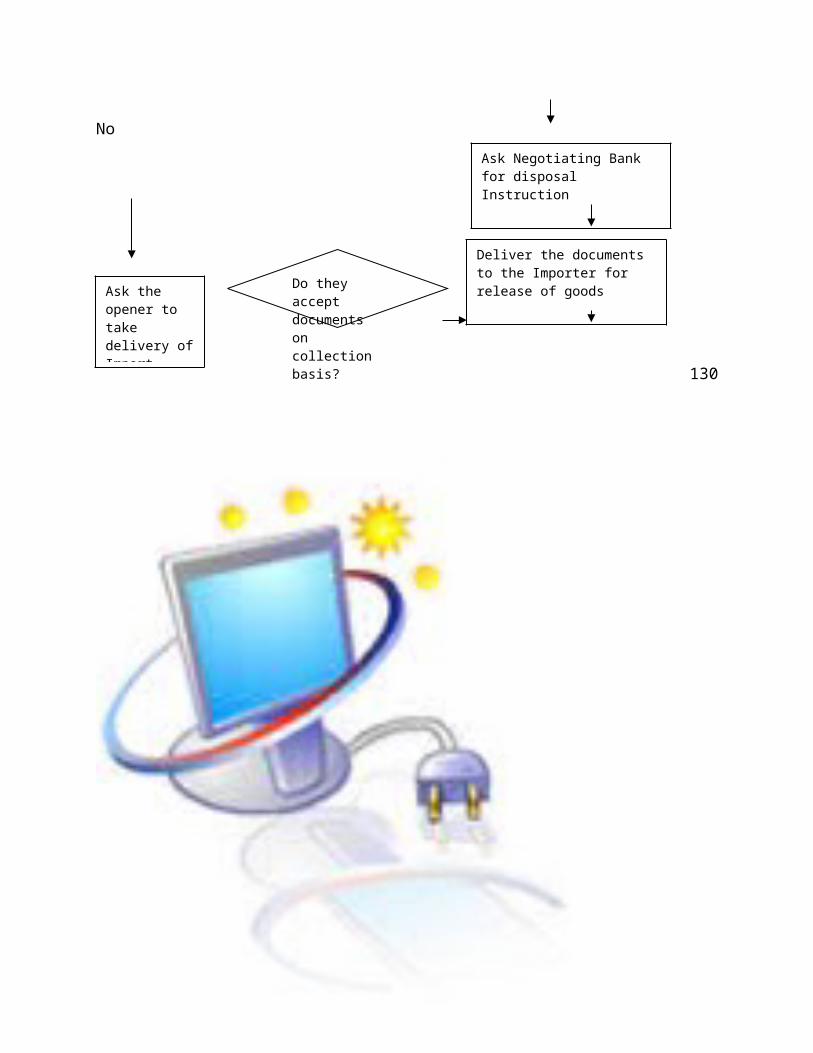

disposal Instruction

Ask the opener to take delivery of Import documents for release of

Deliver the documents to the Importer for release of goods

Do they accept documents on collection basis?

No

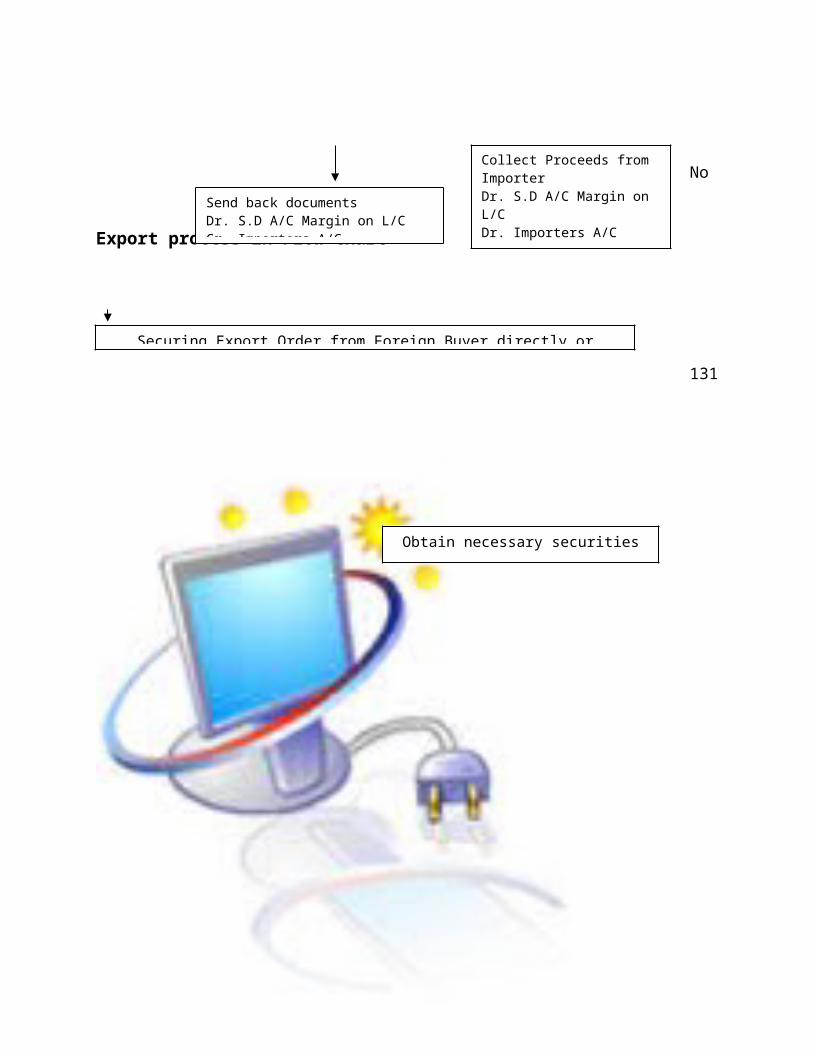

Export process in Flow Chart

95

Send back documentsDr. S.D A/C Margin on L/CCr. Importers A/C

Collect Proceeds from ImporterDr. S.D A/C Margin on L/CDr. Importers A/CCr. H.O Foreign Bank (Collecting Bank)

Securing Export Order from Foreign Buyer directly or through agent

Receiving L/C from buyer’s bank through an advising bank in Bangladesh

Obtain necessary securities

If Yes

If No

96

Certification of EXP from by Authorized Dealer(Bank)

Will the Exporter be allowed any pre- shipment Credit Facility?

Shipment of goods by Exporter

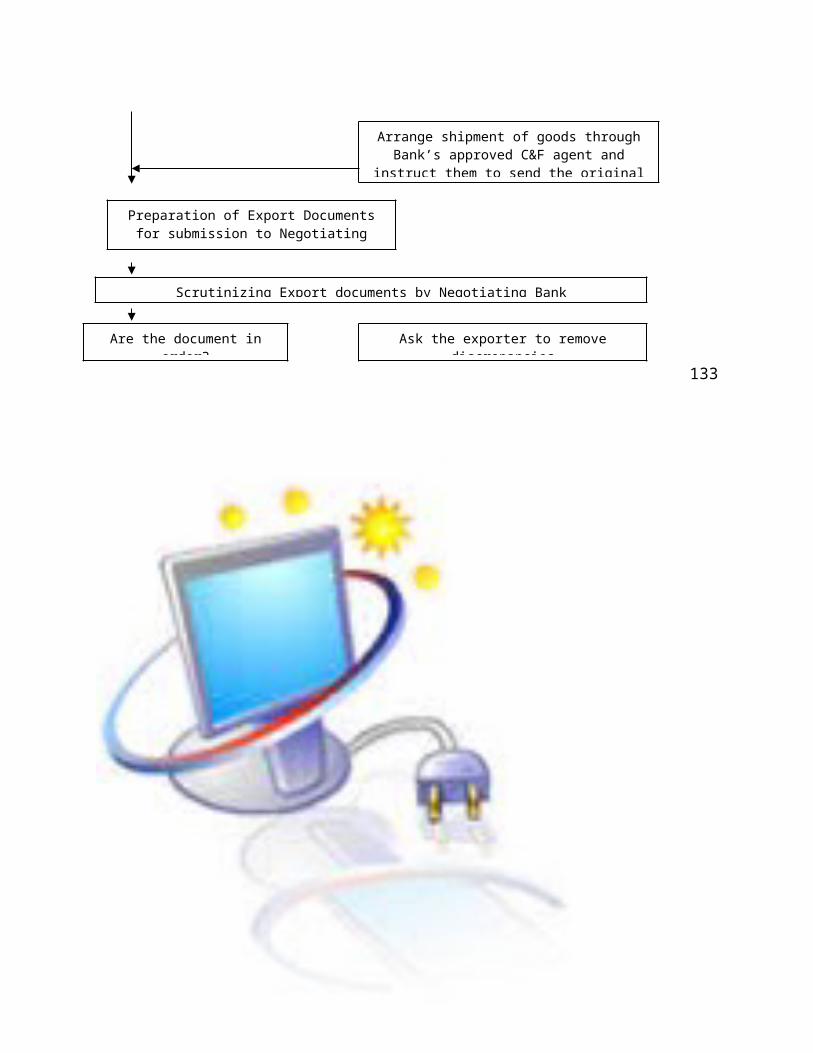

Arrange shipment of goods through Bank’s approved C&F agent and instruct them to send the original Bill of Lading etc. to the Bank Directly

Mark Bank’s Lien on the page of the original L/C

No

Yes No

Yes

97

Preparation of Export Documents for submission to Negotiating Bank

Scrutinizing Export documents by Negotiating Bank

Are the document in order? Ask the exporter to remove discrepancies

Inform opening Bank about discrepancies

Are the discrepancies removed?

Negotiate documents

Despatch documents with reimbursement instruction

Do they allow negotiation?

No

No

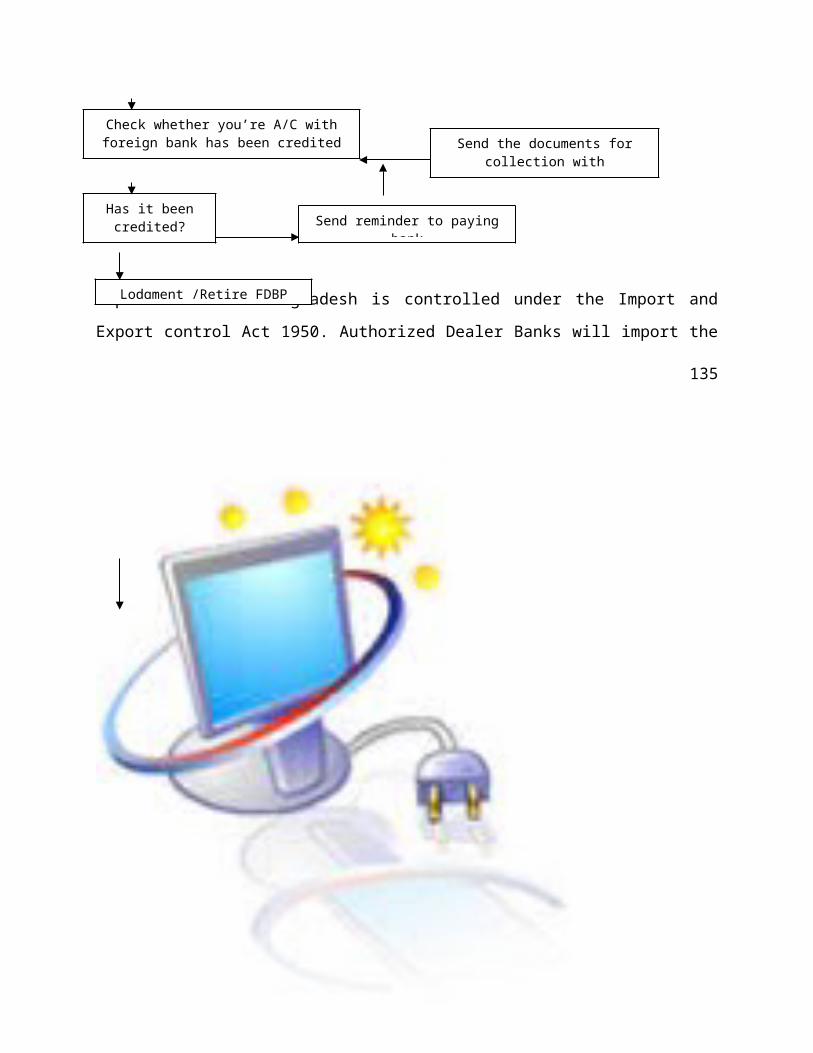

Import trade in Bangladesh is controlled under the Import and Export control Act 1950.

Authorized Dealer Banks will import the goods into Bangladesh following the import policy,

98

Check whether you’re A/C with foreign bank has been credited Send the documents for collection

with reimbursement instruction

Has it been credited?Send reminder to paying bank

Lodgment /Retire FDBP

public notice, F.E. circular and other instructions from competent authorities from time to time.

The import functions of the branch as far I have understood are discussed bellow:

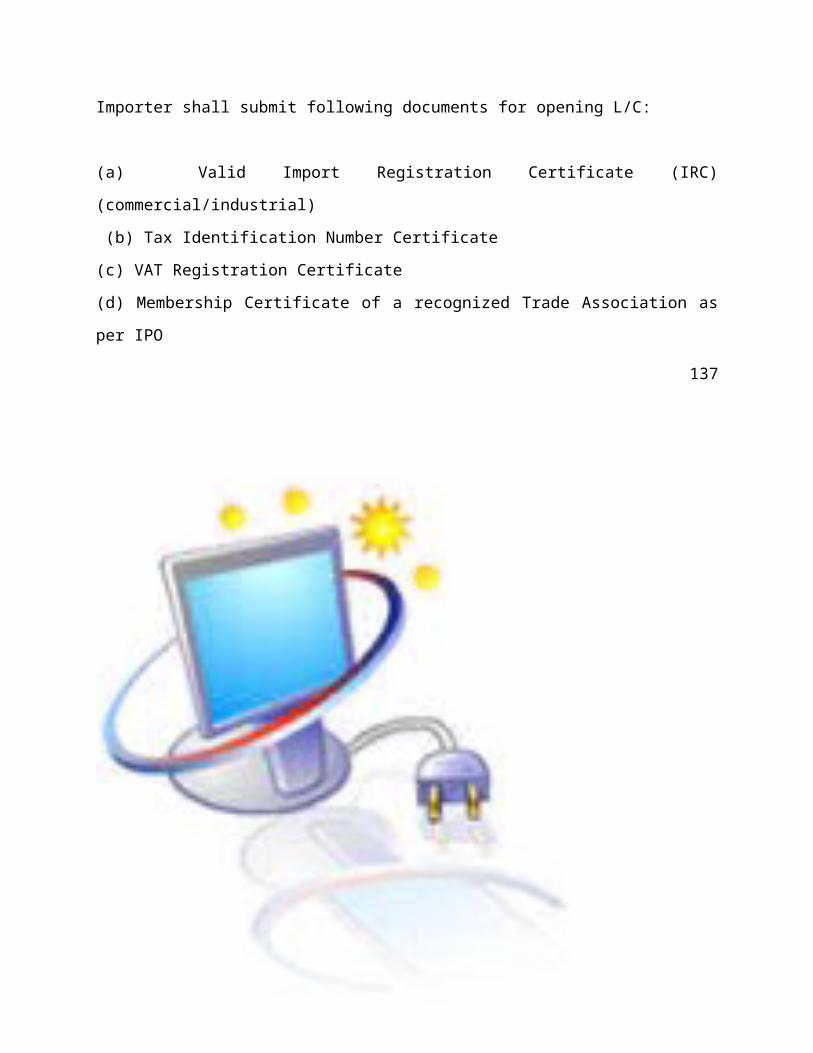

Documentary Requirements for Opening L/C

Importer shall submit following documents for opening L/C:

(a) Valid Import Registration Certificate (IRC) (commercial/industrial)

99

(b) Tax Identification Number Certificate

(c) VAT Registration Certificate

(d) Membership Certificate of a recognized Trade Association as per IPO

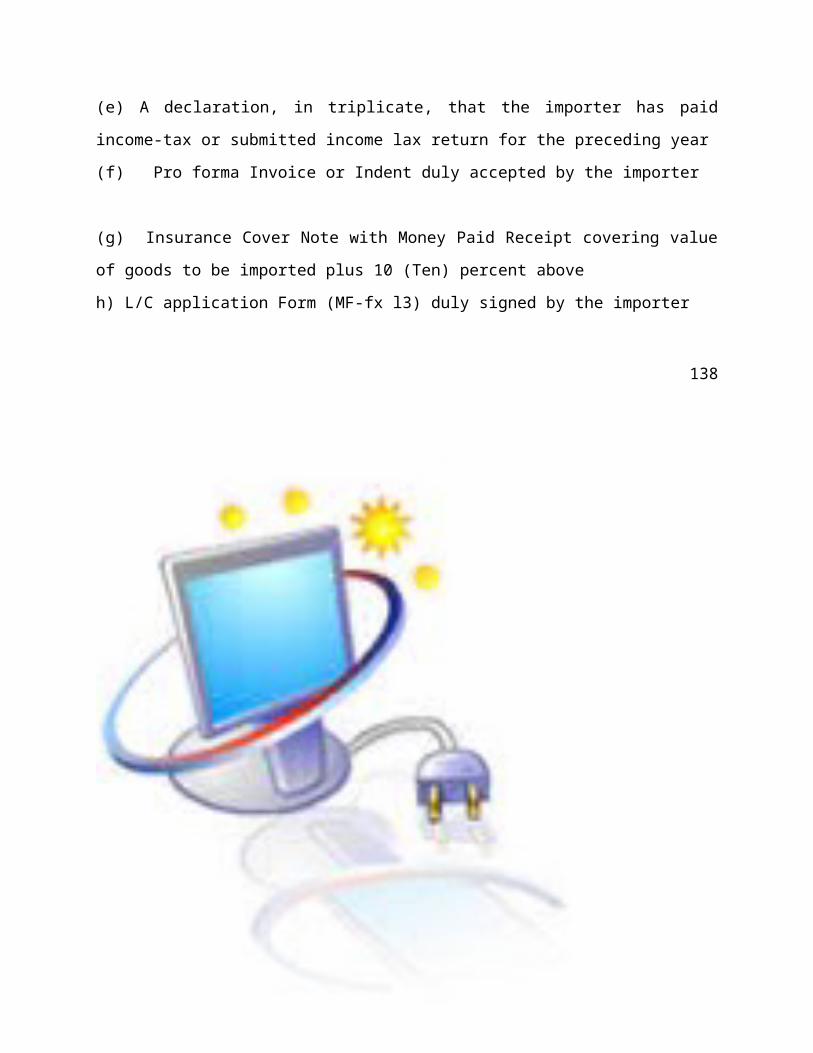

(e) A declaration, in triplicate, that the importer has paid income-tax or submitted income lax

return for the preceding year

(f) Pro forma Invoice or Indent duly accepted by the importer

(g) Insurance Cover Note with Money Paid Receipt covering value of goods to be imported plus

10 (Ten) percent above

h) L/C application Form (MF-fx l3) duly signed by the importer

100

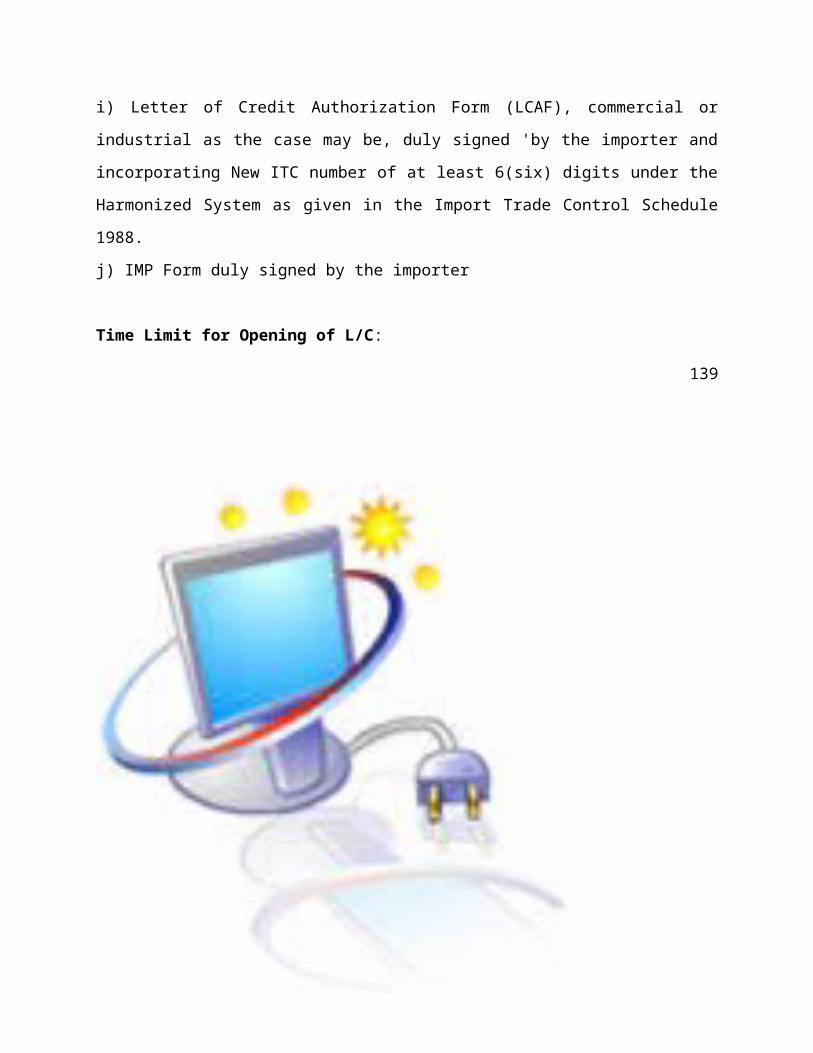

i) Letter of Credit Authorization Form (LCAF), commercial or industrial as the case may be,

duly signed 'by the importer and incorporating New ITC number of at least 6(six) digits under

the Harmonized System as given in the Import Trade Control Schedule 1988.

j) IMP Form duly signed by the importer

Time Limit for Opening of L/C:

L/Cs shall be opened within 150 days from the date of issuance of LCAF.

101

102

Chapter- 5

Data Analysis& Findings

Chapter- 5

Data Analysis& Findings

103

5.1 Findings

104

While working at Jamuna Bank, I have attained to the newer kind of experience. After the

collecting and analyzing of data I have got some findings. These findings are completely from

my personal point of view. Those are given below.

Based on my experience, I can be said that Jamuna Bank should reconsider its services

that better satisfy customer needs and requirements Bank should be more tactful in

dealing with the customers and launch new products that fully meet customer

expectations.

Jamuna Bank Limited has already established a favorable reputation in the banking

industry of the country. It is one of the leading private sector commercial banks in

Bangladesh. The bank has already shown a tremendous growth the profits and deposits

105

sectors.

The bank follow the online banking system to provide the customer better services; but

all the branches of Jamuna bank are not follow the online banking system

During the last 6 years (2004-2010) the average growth of deposits and advance were 33% and 37% respectively, which was 20% in the case of import business. 72% in export business and 36% in guarantee business during the period, shareholders equity grew at the rate of 40%. The bank always fulfills Die provisioning requirements as set by Bangladesh Bank reflecting sound financial health and discipline

The consistent and increasing growth trend of the above mentioned performance indicators has increased depositors' confidence as well as good will/reputation of the bank to a great extent and these have contributed to increase the shareholders value.

106

The Bank’s Human resources Development strategy is to build up quality manpower with

conceptual/managerial Knowledge, skills through designing/arranging of continuous in-

house and outside training programs

The bank focuses on customer-friendly marketing approaches by offering various

efficient delivery of personalized banking services at the clients door steps and caters to

the ever-growing financing needs of clientele at a competitive price

The company philosophy to workout best solutions for customers and clients as a

business and customer friendly Bank

Jamuna bank has an interactive corporate culture & friendly working environment.

107

108

5.2 Performance of the bank:

The incessant fall-out of

international credit market due to world economic meltdown resulting sluggish growth has put

significant pressure on financial performance of banks and financial institutions worldwide.

109

Jamuna Bank Ltd has achieved continuous growth in almost all arenas of its business arenas

despite this economic crisis, facing intensified competition of the industry. The bank remained in

financial strong position with its continued focus on the vision of becoming country’s finest

corporate citizen , providing excellent and need-based customer service.

The bank mobilized deposits of BDT 42356 million as at December 31, 2010 compared to BDT

27307million, till 2009. Total loans and advances stood at BDT 32287million at the end of 2010

that was BDT 21036million at the end of 2009. Import business stood at BDT 46685 million in

2010 compared to BDT 30312 million in 2009. Export business stood at BDT 21407 million in

2010 as against BDT 18617 million in 2009. The bank collected foreign remittance of BDT 5.06

billion in 2010 compared to BDT 4.72 billion in 2009.

110

In 2010, the bank was able to make profit before tax BDT 1.66 billion as compared to 1.28

billion indicating 29.73% growth. Net profit attributable to shareholders stood at BDT 807.52

million. The return on equity remained 18.80% during 2010 and earnings per share (EPS) stood

at BDT at 56.92. Non performing loan (NPL) ratio reduced to 2.54% in 2009 as compared to

2.86% in 2008.

JBL made adequate provision against classified loans which is significantly higher than last year.

Adequate provision made the bank stronger than before. Tier-1 capital stood at BDT 3054.14

million at the end of 2010 compared to that of BDT 2131.02 at the end of 2009. Tier-2 capital

reached to BDT 943.52 million at the end of December 2010 as compared to that of BDT

313.32million at the end of 2009. Return of assets (ROA) increased to 1.89% in 2009 from

111

1.51% in 2009 and return on equity (ROE) also increased significantly to 18.80% from 17.75%

in 2009. The capital adequacy ratio (CAR) increased to 10.48% in 2009 as against that of

10.17% in 2009. Net interest margin (NIM) stood at 3.58% at the end of 2010, suggesting a

healthy growth in net interest income.

112

HIGHLIGHTS OF JAMUNA BANK LIMITED

Amount in Taka ( Except Ratio)

Sl.No. Pa

2010 2009

113

1

2

3

4

5

6

7

8

9

10

11

12

13

Paid up Capital

Total Capital

Capital surplus/(deficit)

Total Assets ( excluding off balance sheet items)

Total Deposits

Total Loans & Advances

Total Contingent Liabilities & Commitments

Advance Deposit Ratio

% of classified loans against Total Loans

Profit after taxation & provisions

Amount of classified loans

Provision kept against Classified loan

Provision surplus / deficit

1,621,882,500

3,997,664,705

880,659,405

48,730,951,557

42,356,203,563

32,287,661,155

14,718,947,868

76.23%

2.20%

923,123,207

710,858,000

465,638,000

-

1,313,265,200

2,444,338,501

392,695,301

31,646,629,499

27,307,936,141

21,036,861,012

9,169,471,638

77.04%

2.84%

479,437,923

598,309,000

296,285,000

114

5.3 Key Financial Indicator:

115

Profit scenario of Jamuna Bank:

In 2009Jamuna Bank Limited posted an operating profit of Tk.1914.25 million as against Tk.1040.20 million in 2008 with a spectacular growth of 84.03 percent over the preceding year. After having made necessary provisions for loans and advances of Tk.351.05 million in accordance with the instruction of Bangladesh Bank Net Income Before Tax (NIBT) stood at Tk.1536.20 million in the year under review against Tk.865.82 million in the preceding year. An amount of Tk.632.26 million has been kept as provision for payment of Tax. Thus Net Income after Tax and provision stood at Tk.923.12 million in 2009 which was Tk.479.44 million in 2008.

116

117

Operating Profit

Year Tk.(Million)

2005 419.94

2006 701.32

2007 824.20

2008 1040.20

2009 1914.25

118

119

Capital Structure:

Jamuna Bank Limited has a conviction of maintaining a strong capital base in carrying on opereat operation on June 03, 2001 with a paid-up capital of Tk.390.00 million divided into 3.90 million

120

ordinary shares of Tk.100 each. The authorized capital of the Bank is Tk.1600 million divided into 16.00 million of Tk.100 each. The Bank's paid-up capital as at 31st December 2009 stood at Tk.1621.88 million. Tk429.00 million was raised through initial public issue of 4.29 million ordinary shares of TkA 00 each with a premiu- each while Tk.214.50 million was raised by issue of Bonus Shares in the ratio of 1:4, i.e. one bonus _s-holding of 8.58 million ordinary shares as on 31.12.2005, for every 4 shares out of profits upto the Thus, as on 31st December 2009, the total shareholder's equity and reserve stood at Tk.3997.66 million!"

Capital Tire-I Capital Tire-II

121

Total capital Tire-I & II

122

CAPITAL ADEQUACY RATIO

123

The Bank adopted BIS risk adjusted capital standards to measure the capital adequacy in line with

set by Bangladesh Bank. According to the instructions contained in Bangladesh Bank's BRPD

Circ dated May 14, 2007 relating to Capital Adequacy every commercial bank operating in the

required to maintain at minimum 9 percent of its risk-weighted assets as capital. Jamuna Bank

Li-maintain Capital Adequacy ratio of 12.83 percent as at 31.12.2009 which was higher than the

require Adequacy Ratio. The amount of capital with break-up is given below:

"Fig in BDT Million"Particulars 2009 2008

124

Tier I Capital 3054.14 2131.02

Paid up Capital 1621.88 1313.27

Non-repayable Share Premium Account - -

Statutory Reserve 816.48503.84

Retained Earnings 615.78 313.91Proposed Bonus Share - -

Tier II capital943.52 313.32

1 % Provision against Unclassified Loans 332.64 213.80

Exchange Equalization Fund 0.33 0.33

Total Capital (Tier I +Tier 11)3997.66 2444.34

125

126

DEPO SITS AND DEPOSIT MIX

In commercial banks operation starts with mobilization of resources i.e. tapping of deposits and

then the said resources are deployed as loans, advances and investments for the purpose of

maximizing wealth which -sans deposits have dominance in commercial bank's operations. That

is why; there is a common saying that deposit is the lifeblood of a bank. The comparative

position of deposit mix of the Bank as on 31.12.2009 and 31.12.2008 is depicted below:

Type of Deposit As on

31.12.2009

As on

31.12.2008

Changes

(+)/(-)

Changes in

% over the

127

year

Current A/C & other 4715.31 3283.21 +1432.10 43.62

Bills Payable 516.31 412.03 +57.59 25.30

Savings Deposit 2891.25 1679.40 +1211.85 72.15

Short term Deposit 25201.52 16360.18 +8841.34 54.04

Fixed Deposit 2762.49 1335.16 +1427.33 93.54

Scheme Deposits 6118.32 4131.80 +1986.52 48.07

Foreign Currency Deposit 151.00 106.16 +44.84 42.24

Total Deposits 151.00 27307.94 +15048.26 55.10

128

129

Import, Export & Remittance Position

Import Trade The total import business handled by the bank in 2009 was Tk.46684.73 million compared to Tk.30311.71 million in the preceding year registering a growth of Tk.16373.02 million being 54.02 percent. A sizable L/C’s were also opened by the bank in the year under review. The import items included industrial raw materials, machinery, consumer goods, fabrics, accessories, food item etc.

130

Export Trade

ImportYear Tk. (Million)2005 121522006 154582007 221922008 303122009 46685

131

The Bank handled export business worth Tk.21406.94 million in the year under report. In 2008 export business handled by the Bank was Tk.1861.43 million. Thus there was an increases of Tk.2789.51 million in export business handled by the Bank, being 14.98 percent over the preceding year. The major export item was Readymade Garments.

132

ExportYear Tk. (Million)2005 65222006 115842007 139902008 186172009 21407

133

Foreign RemittanceTotal foreign remittance in a single year,i.e. in 2009 made a record high to the tune of BDT 5061.30 million compared to that of BDT 4722.90 million in 2008. The Bank has deepened its step on the foreign soils further by establishing more and more remittance arrangements with overseas exchange companies where Bangladeshi expatriates are working. These Include U.K, U.A.E, Kuwait, Baharain, Canada, Italy, France etc. Moreover, for prompt and safe distribution of this hard earned money to their near and dear ones in every corner of the country, the Bank has made an arrangement with Bangladesh Post Office, Western Union and some other agencies.

Particulars Upto Last Date on 23/06/2010

As on 23/06/2010 Total Amount is Crore Tk.

No Amount No. Amount No. Amount

I a. L/C (Cash) 741 447.35 15 5.29 756 452.64

134

mp

ort

b. L/C (BTB Local)

2389 397.23 17 2.82 2406 400.05

c. L/C (BTB Foeign)

890 290.80 3 4.15 893 294.95

Sub Total BTB L/C

3279 688.03 20 6.97 3299 695.00

Total 3992 1135.38 35 12.26 4027 1147.64

Exp

ort

a)Export Bill (Gen)

374 107.16 1 0.67 375 107.83

b) Export Bill (RMGF

2350 711.01 19 5.33 2369 716.33

c) Export Bill (RMGL)

1626 229.87 12 1.88 1638 231.75

Total 4350 1048.03 32 7.88 4382 1055.91

Re Inward 0 51.57 0.00 0 51.57Outward 0 5.30 0.00 0 5.30Total 56.87 - 56.87

135

Banking industry has entered into the new Risk Based Capital Adequacy Framework (Basel II )

arena from 2010. JBL has already taken necessary steps to comply with this accord properly. The

bank will also continue strengthen its position by expanding the core business activities.

136

5.4 Identified Problems for the Jamuna Bank

The main constraint of the study was insufficiency of information that was highly

required for the study. Since the bank officials are very busy with their activities, as a

result it was though to have proper knowledge as was required for the study.

The duration was not enough to cover all aspects of banking.

Lack of depth knowledge and analytical ability for writing import.

137

The data and information related with the topic was not easily available because of

confidentiality of the concern.

Foreign Exchange dealing is a technical job and has a great prospect in our country.

Floating Exchange Rate has been introduced and it has put the banking sector into a new

era. Bangladesh Bank’s total control is not there but there is some risk factor involved in

it. Jamuna Bank Ltd wanted to find whether the process of their foreign exchange

operation is good enough to avoid any unwanted risk and the prospect in foreign

exchange dealing in their present standing,

The office of JBL, Malibagh Branch, and Dhaka is not sufficient enough.

138

In JBL, Malibagh Branch, Dhaka maximum officers are working in a specific desk for a

long time and for this reason they may feel monotony and certainly they are not be able

to know the overall banking activities through they have enough eagerness to know.

Foreign Exchange Section is one of the busiest sections in Bank. Sometimes it is found

that all works are not performed efficiently due to insufficiency to Officer/Staffs.

Training facility isn’t sufficient especially for the lower level officers.

Still now, like most of the branches of JBL, Malibagh Branch, Dhaka, follows the

traditional banking system.

JBL, Malibagh Branch, Dhaka, has no reception section and has no receptionist that may

receive phone calls and complains from customer and supply the enough information.

139

In this branch there is lack of modern equipments.

140

141

Chapter- Six

Conclusion and Recommendations

Chapter- Six

Conclusion and Recommendations

6.1 Recommendations

In view of the facts, the following recommendations are made to the respective concerned for

the consideration and implementation.

► The bank should have standardized system of measuring customer satisfaction.

► Need for integrity of the officials within reasonable limits.

142

► The officials should have a through knowledge of the product.

► The officials should be trained up for their efficiency.

► Reasonable interest rate for all kinds of loan.

► Increasing number of staffs and cash terminals.

► Officials should be more cooperative with the clients.

► Officials should be trained up for self-management.

► Customized new financial product development.

► Officials should be faster during transaction.

► Bank can accept new ideas from the customers for regarding improvement the quality

of their service.

143

►They need to maintain an upgraded guideline for the employees to avoid any kind of

confusion.

►They should enhance their savings facilities by introducing many other saving

schemes, because customers really look for various savings programs.

►Special increment should be given to middle and junior level managers and executives

also to increase their motivation level.

144

6.2 Conclusion

From the beginning of greater change in the world economic structure, banking activities has

becoming an important thing. Now a day the idea of banking is also developed and a huge

number of private commercial banks are just on waiting for business. So it is a matter of think

that how to establish an idea with different techniques, In Bangladesh, Commercial banks are

playing vital role in the development of our economy and financial system. Standard Charted

145

Bank Limited has a strong position in the today’s competitive market. The JBL, Malibagh

Branch, Dhaka also contributing a better proportion of profit in JBL’s total earning. Total

analysis of the bank has the greater opportunity to do better in the future.

Day by day JBL’s area of service is increased all over the country through setting up new

branches at new places. The reliability of the customer on JBL‘s increasing day by day for its

better services. But they may introduce online and ATM services comparing with other

commercial bank to improve their services and to make efficient and easy customer services.

They also may follow the given recommendations in order to improve day by day. Jamuna Bank

Limited may contribute a vital role in the socio-economic prospective and in the development of

our economy.

146

The JBL has been trying to operate its business successfully in Bangladesh since 1999. JBL has

already developed an image of goodwill among its clientele by offering its excellent services.

This success has resulted from dedication, commitment and dynamic

Leadership of its management over the periods. During the short span of time of its operation,

the bank bas successfully grabbed a position as a progressive and dynamic financial institution in

the country. If the bank goes this way. It is expected that in the near future JBL may become one

of the top performers in the banking sector.

Here I observed its deposit figure is strong. The bank should take necessary action for

maintaining .JBL has been able to maintain its recovery position in sector wise credit financing is

147

up to the satisfactory level. At last it should give more emphasis in this sector to acquire more

profit.

References

1.Annual Report of Jamuna Bank Limited, 2005, 2006,2007

148

2. Chowdhury, L.R; A Textbook on Foreign Exchange, Fair Corporation,139, Azimpur,

Dhaka, 1205

3. Foreign Exchange Manual, Jamuna Bank Limited., 1st November,2009

4. Collyer Gary, ICC Uniform Customs And Practice For Documentary Credits ,3rdEdition,

International Chamber Of Commerce, ICC Publication No.600

5. Bangladesh Bank Foreign Exchange Guidelines, Volume-1

6. www.jamunabankbd.com

149

150

Acronyms

151

A/C AccountAD Authorized DealerB/L Bill of LadingBB Bangladesh BankBOE Bill of exchangeC & F Clearing & ForwardingC&F Cost & FreightCC Cash CreditCCI & E Chief Controller of Import & ExportCIB Credit Information BureauCIF Cost Insurance & FreightCRF Clean Report FindingsDD Demand DraftDP Note Demand Promissory NoteEPB Export Promotion BureauERC Export Registration CertificateEXP Export FormFC Foreign CurrencyFDD Foreign Demand DraftFDR Fixed deposit receiptHS Code Harmonized system of codingIBC Inward Bills for CollectionIBCA Inter Branch Credit AdviceIBCT Inter branch Credit TransactionIBDA Inter Branch Debit AdviceIMP Import FormIRC Import Registration CertificateL/C Letter of CreditLCAF Letter of Credit Authorization FormLIM Loan against Imported MerchandiseLTR Loan against Trust ReceiptOBC Outward Bills for CollectionPAD Payment against DocumentPO Payment OrderPSI Pre Shipment InspectionSTD Short Term DepositSWIFT Society for Worldwide Inter bank FinancialTC Travelers ChequeTIN Tax Identification NumberTT Telegraphic Transfer

152

153

154