international financial reporting standards (ifrs) · deloitte consulting llp december 15, 2008....

TRANSCRIPT

Deloitte Consulting LLPDeloitte Consulting LLP

December 15, 2008

International Financial Reporting Standards (IFRS)

SIM

IFR

S v

1.pp

t

- 2 -

Agenda

IFRS Background

Comprehensive View of IFRS Adoption

IFRS Adoption: Downstream Impacts and Strategic Benefits

IFRS Key Takeaways

IFRS Contacts and Resources

Questions & Answers

SIM

IFR

S v

1.pp

t

- 3 -

IFRS Background

- 4 -

What is IFRS?

Key characteristics of IFRS:Principals-based approach with greater weighting on interpretation and application of principles, rather than a rules governed approachGreater emphasis on the substance of transactions and an evaluation of whether the accounting presentation reflects the economic realityRenewed focus on the need for professional judgment in arriving at accounting conclusionsGreater use of fair value as a measurement basis placing emphasis on obtaining reliable measurements

IFRS (International Financial Reporting Standards) is a set of principle-based accounting standards put forth by the London-based International Accounting Standards Board (IASB) that is gaining worldwide acceptance on an accelerating basis.

Countries that require or permit IFRS

Countries seeking convergence with the IASB or pursuing adoption of IFRS

THE MOMENTUM TOWARDS GLOBAL IFRS ADOPTION

- 5 -

IFRS: Today and Tomorrow

Today

Used in over 100 countries and by approximately 40% of the Global Fortune 500

Required for listing companies across all EU countries, starting in 2005

Adoption date announced by large countries like Canada, Brazil and India

Tomorrow

Expected that all major countries will have adopted IFRS to some extent by 2014

Convergence of Japan will be substantially completed

Substantial majority of Global Fortune 500 will report under IFRS

SEC proposed roadmap finalization for US companies expected in early 2009

Global Fortune 500

0

50

100

150

200

250

300

2005 2007

U.S. GAAP IFRS Other

About 40% of the Global Fortune 500 companies currently use IFRS. That number is expected to grow as Canada and Brazil adopt IFRS over the next few years.

IFRS is quickly gaining worldwide acceptance as a global standard for financial reporting

- 6 -

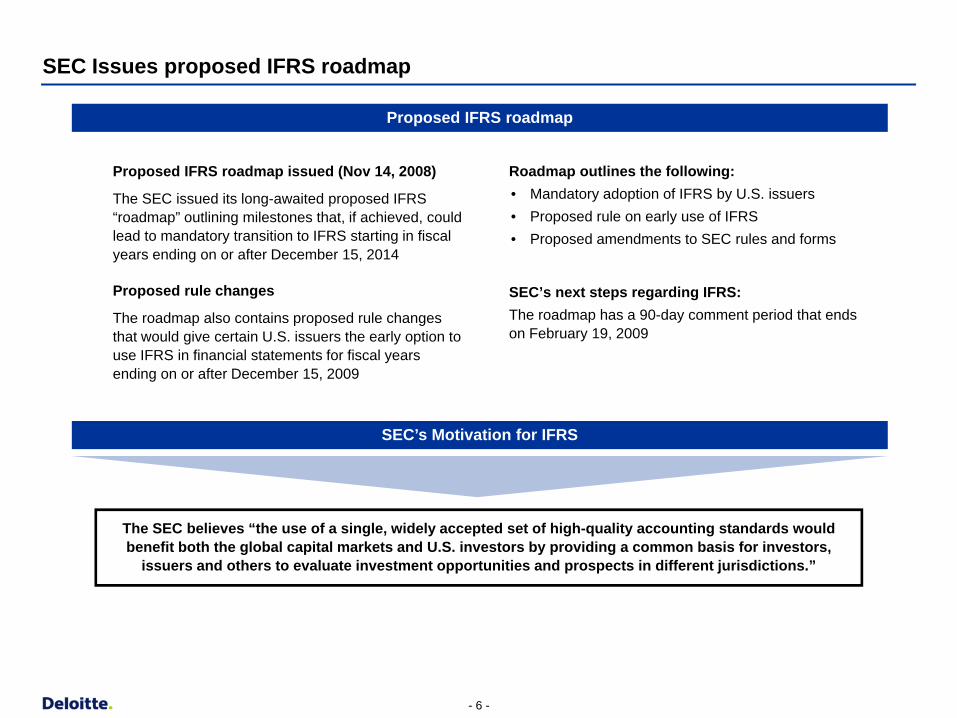

SEC Issues proposed IFRS roadmap

Proposed IFRS roadmap issued (Nov 14, 2008)

The SEC issued its long-awaited proposed IFRS “roadmap” outlining milestones that, if achieved, could lead to mandatory transition to IFRS starting in fiscal years ending on or after December 15, 2014

Proposed rule changes

The roadmap also contains proposed rule changes that would give certain U.S. issuers the early option to use IFRS in financial statements for fiscal years ending on or after December 15, 2009

Roadmap outlines the following: • Mandatory adoption of IFRS by U.S. issuers• Proposed rule on early use of IFRS• Proposed amendments to SEC rules and forms

SEC’s next steps regarding IFRS:The roadmap has a 90-day comment period that ends on February 19, 2009

The SEC believes “the use of a single, widely accepted set of high-quality accounting standards would benefit both the global capital markets and U.S. investors by providing a common basis for investors,

issuers and others to evaluate investment opportunities and prospects in different jurisdictions.”

Proposed IFRS roadmap

SEC’s Motivation for IFRS

- 7 -

IFRS transition timeline: Adoption by 2014

Regulatory timeline

2009 2010 2011 2012 2013 2014

Nov. 2008 - Proposed roadmap and rules issued. Once finalized, select U.S. filers will be eligible to file IFRS financial statements in 2009.

2011 – SEC to decide whether to mandate use of IFRS for all U.S. issuers on the basis of the progress of milestones. SEC may also decide to allow other issuers to adopt before 2014

Assessment• Technical accounting

• Statutory reporting

• Taxes

• Systems, processes, and controls

• Training and communication plan

• Organizational impacts

• Conversion strategy

Dec. 31, 2014 -Mandated IFRS: Large accelerated filers could be mandated to report financial results using IFRS (accelerated filers in 2015 and non-accelerated filers in 2016)

Jan. 1, 2012 -Beginning of the first comparative IFRS year for companies that will adopt IFRS in 2014

Transition date Reporting date

Illustrative company timeline

IFRS reporting

Conversion• Accounting policies

• Statutory conversions

• Financial statements and disclosures

• System/data enhancements

• Tax structures/ planning

• Auditor coordination

Communication• Board of directors

• Shareholders

• Employees

• Analysts

• Business partners

Business as usual

• Planning, forecasting, and budgeting

• Process refinement

• Execute sustained reporting plan

Capture benefits• Shared services

• Off-shoring and/or outsourcing

• Tax planning

• Systems consolidation

Sustained reporting plan

• Close/reporting process

• Training execution

• Internal control alignment

• Statutory consolidation

• Collateral impacts (e.g., compensation plans, contracts, joint ventures, regulatory requirements)

Dual reporting

U.S. GAAP financial statements (through third quarter 2014)IFRS financial statements

IFRS preparation

- 8 -

Comprehensive View of IFRS Adoption

- 9 -

Broad View of IFRS

IFRS may impact many aspects of a company’s business

Technical accounting and reporting

Taxes

Systems, processes, and controls

Organizational impacts on people, training and communications

Collateral impacts may include

Debt covenant calculations

Bonus plan calculations

Dividend management

Contingent consideration

Revenue contracts

Tax returns

Joint ventures

Regulatory requirements

Financing arrangement

Investor, employee, and analyst communications

- 10 -

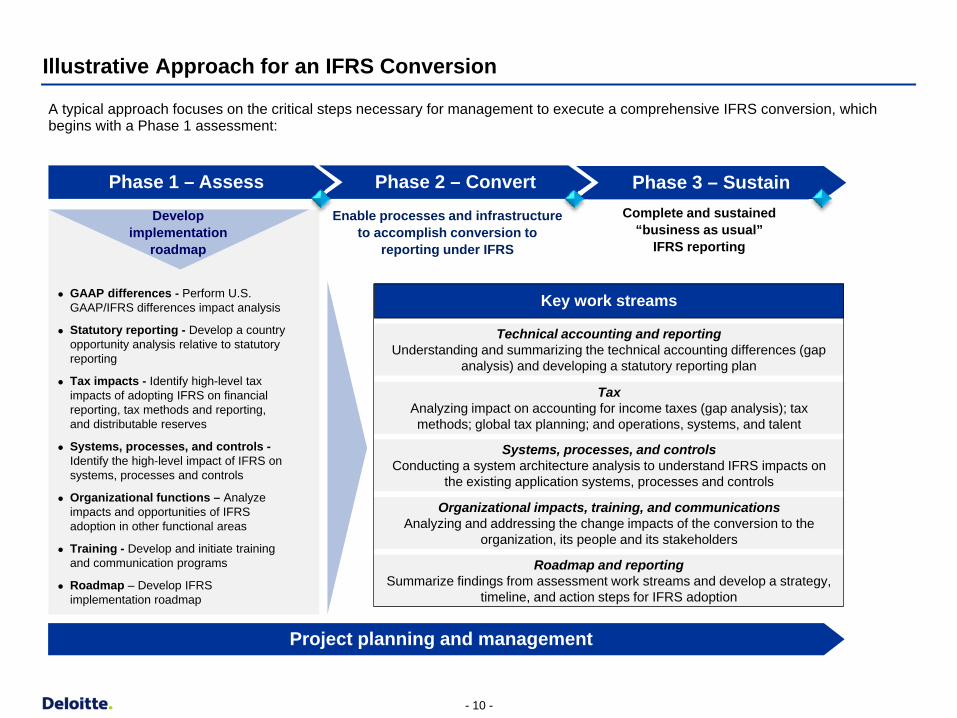

Complete and sustained “business as usual”

IFRS reporting

Enable processes and infrastructure to accomplish conversion to

reporting under IFRS

Phase 1 – Assess Phase 2 – Convert Phase 3 – Sustain

GAAP differences - Perform U.S. GAAP/IFRS differences impact analysis

Statutory reporting - Develop a country opportunity analysis relative to statutory reporting

Tax impacts - Identify high-level tax impacts of adopting IFRS on financial reporting, tax methods and reporting, and distributable reserves

Systems, processes, and controls -Identify the high-level impact of IFRS on systems, processes and controls

Organizational functions – Analyze impacts and opportunities of IFRS adoption in other functional areas

Training - Develop and initiate training and communication programs

Roadmap – Develop IFRS implementation roadmap

A typical approach focuses on the critical steps necessary for management to execute a comprehensive IFRS conversion, which begins with a Phase 1 assessment:

Project planning and management

Technical accounting and reportingUnderstanding and summarizing the technical accounting differences (gap

analysis) and developing a statutory reporting plan

TaxAnalyzing impact on accounting for income taxes (gap analysis); tax methods; global tax planning; and operations, systems, and talent

Systems, processes, and controlsConducting a system architecture analysis to understand IFRS impacts on

the existing application systems, processes and controls

Organizational impacts, training, and communications Analyzing and addressing the change impacts of the conversion to the

organization, its people and its stakeholders

Roadmap and reportingSummarize findings from assessment work streams and develop a strategy,

timeline, and action steps for IFRS adoption

Key work streams

Develop implementation

roadmap

Illustrative Approach for an IFRS Conversion

- 11 -

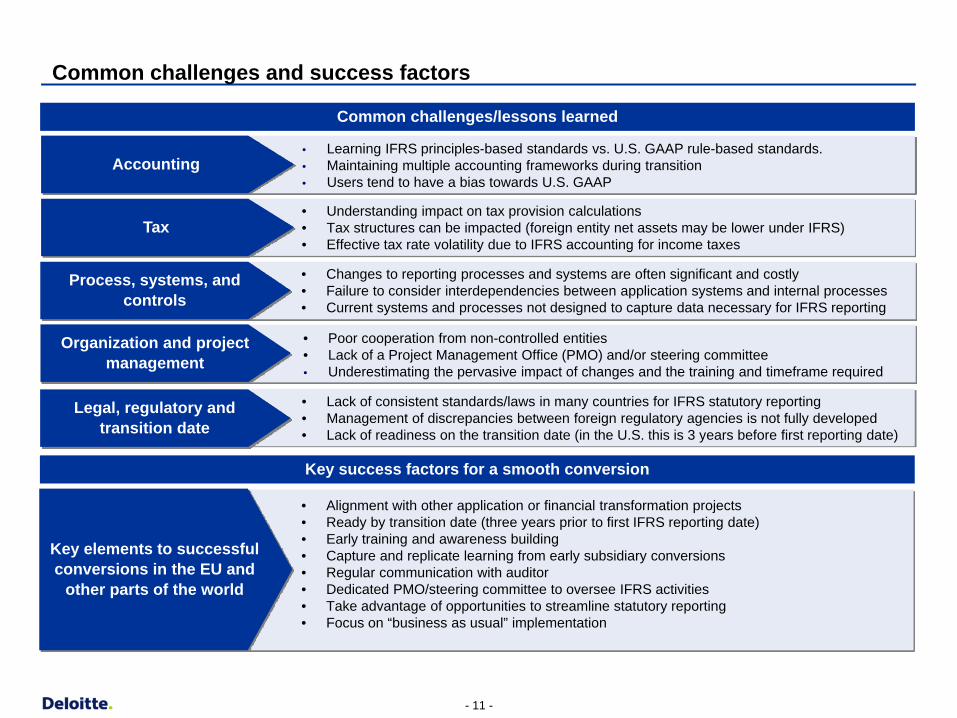

Accounting

Process, systems, and controls

Legal, regulatory and transition date

Key elements to successful conversions in the EU and

other parts of the world

• Learning IFRS principles-based standards vs. U.S. GAAP rule-based standards. • Maintaining multiple accounting frameworks during transition • Users tend to have a bias towards U.S. GAAP

• Changes to reporting processes and systems are often significant and costly • Failure to consider interdependencies between application systems and internal processes• Current systems and processes not designed to capture data necessary for IFRS reporting

• Lack of consistent standards/laws in many countries for IFRS statutory reporting• Management of discrepancies between foreign regulatory agencies is not fully developed• Lack of readiness on the transition date (in the U.S. this is 3 years before first reporting date)

• Alignment with other application or financial transformation projects• Ready by transition date (three years prior to first IFRS reporting date)• Early training and awareness building• Capture and replicate learning from early subsidiary conversions• Regular communication with auditor• Dedicated PMO/steering committee to oversee IFRS activities• Take advantage of opportunities to streamline statutory reporting• Focus on “business as usual” implementation

Common challenges/lessons learned

Tax• Understanding impact on tax provision calculations• Tax structures can be impacted (foreign entity net assets may be lower under IFRS)• Effective tax rate volatility due to IFRS accounting for income taxes

Organization and project management

• Poor cooperation from non-controlled entities• Lack of a Project Management Office (PMO) and/or steering committee• Underestimating the pervasive impact of changes and the training and timeframe required

Key success factors for a smooth conversion

Common challenges and success factors

SIM

IFR

S v

1.pp

t

- 12 -

IFRS Adoption: Downstream Impacts and Strategic Benefits

- 13 -

IFRS Adoption: Downstream Impacts and Strategic BenefitsIFRS adoption, while a significant regulatory event, is also an opportunity and potential catalyst for Finance and IT organizations to create global standards and achieve benefits.

5199

18 H

ot T

opic

IFR

S D

eck

v 1.

ppt

- 14 -

IFRS Adoption: Downstream Impacts and Strategic BenefitsPolicy & Process

Consider the impact on accounting/finance processes (inventory valuation, capitalization of costs, revenue recognition)

Implications of new disclosure requirements

Changes to existing close calendar

Changes to current consolidation logic

Potential for new performance metrics and/or KPIs to measure results of operations

Management reporting packages and global reporting packages

Treasury and cash management activities could be impacted

Legal and debt covenants will need to be reviewed for impact

IFRS can be a lever to help reduce the diversity of accounting policiesWith its consistency requirements, IFRS could be a catalyst to standardize management reporting and provide opportunities for streamlining statutory and tax reporting processesIFRS can facilitate efforts to minimize manual processes, especially with off-line adjustments and spreadsheetsIFRS can drive improvements in Integrated Performance Management

Assess impacts on accounting/finance processes

Determine impact of IFRS to key financial accounts

Analyze IFRS impacts to close, consolidation, reconciliation processes and current consolidation logic

Assess the need for new performance metrics or KPIs and impacts to data analytics necessary to benchmark performance against competitors

Analyze impact of IFRS to statutory and consolidated reporting

Evaluate opportunities to improve tax and treasury

Review legal and debt covenants for required changes

Potential Downstream Impacts

Key Assessment Activities

Strategic Benefit Opportunity

Policy & Process

5199

18 H

ot T

opic

IFR

S D

eck

v 1.

ppt

- 15 -

IFRS Adoption: Downstream Impacts and Strategic BenefitsGovernance & Controls

Assess overall governance framework and determine changes required to ensure policies are documented, updated and monitored for compliance

Assess governance around decision rights and determine need to establish new decision-making process

Assess span of control and identify changes required to support IFRS

Evaluate process level controls around changes to financial reporting structures

Evaluate the impact on current financial reporting structures

IFRS can facilitate the automation of processes to improve controls

Leading finance functions are moving towards a more centralized operating model, IFRS presents opportunities to simplify and standardize processes and drive enforcement across your organization

IFRS will provide an opportunity to strengthen the integrity of your control framework

Limited scope approach may create control challenges (spreadsheet risks)

Increased importance of clarity in policies and governance with shift to principles based approach

Alignment of internal audit approach with new processes

Systems change control and integration issues

Decision rights and governance around new decision-making processes

Potential Downstream Impacts

Key Assessment Activities

Strategic Benefit Opportunity

Governance & Controls

5199

18 H

ot T

opic

IFR

S D

eck

v 1.

ppt

- 16 -

IFRS Adoption: Downstream Impacts and Strategic BenefitsOrganization & People

Key Assessment Activities

Assess stakeholders readiness for change and determine communication needs by stakeholder group

Assess roles, reporting relationships and responsibilities

Identify changes required to finance operating model

Identify leadership role in driving change throughout organization

Determine revisions to training and learning materials and identify stakeholders who will require training

Identify key process owners and business owners impacted by change

Review current incentive compensation programs to ensure alignment with IFRS driven reporting structures

IFRS can be a catalyst for creating Centers of Excellence

Training is more comprehensive than most assume and will be required for implementation of principle-based approach

Assessment of skill sets and identification of competency “gaps”

Change management support for changes in processes, organization and systems

Alignment of performance objectives and incentive compensation programs with new reporting structures

Strategic Benefit Opportunity

Potential to consolidate accounting and/or statutory reporting into a Center of Excellence (COE)

Uniform standards will provide potential to increase operational effectiveness across Finance

Potential to enhance / optimize Finance operating model

Potential Downstream Impacts

Organization & People

- 17 -

IFRS and TechnologyEach systems infrastructure is a specific combination of components and the magnitude of IFRS impact will depend upon how far anorganization has standardized systems and data, and what projects are underway

Regardless of company size and scope, IFRS will have an impact on systems

Even if you have an integrated platform, there are still important considerations for IFRS

Although major software vendors support IFRS, conversion is much more than just “flipping a switch.” An upgrade or adjustments to an existing implementation plan to accommodate the migration may be required

In any case, changes to systems do not occur overnight and will require coordinated efforts from IT and Finance

A roadmap exercise is critical and should be done ASARP (As Soon As Reasonably Possible)

Planning and Calculation Engines

ReportingData Warehouse

ETL

Extract

Transform

Load

Validate

Standardize

Normalize

General Ledger

Chart(s) of Accounts

Multi-Ledgers

ReportingCapabilities

Data Standards

BudgetingPlanning

TransferPricing

Industry Specific Applications

CapitalCalculation

Source Systems

Accounts Payable

Accounts Receivable

Assets

Inventory

Purchasing

Projects

Payroll

Management Reporting

Regulatory Reporting

Business Unit Reporting

Tax Reporting

Local GAAP Reporting

Financial Reporting

Illustrative Systems Infrastructure

Key Considerations

- 18 -

Upstream Data Must Be Evaluated

Potential Impacts

Key Assessment Activities

Differences in the accounting treatment between current accounting standards and IFRS will create a need for new input data

Current data and transactions may not have all needed attributes or qualities

Sub-ledgers within the ERP system may have additional functionality to support IFRS which is currently not being utilized and could be implemented

Transformation layer may need to be adjusted

Over time the potential for acquisitions of companies using IFRS will increase; altering ETL tools to provide required data elements could make integrations more efficient

Understand the existing system landscape for all impacted business units and subsidiariesIdentify missing data elements due to differences in accounting treatmentAssess required enhancements to legacy systemsIdentify changes to ‘In Flight’ projects

- 19 -

General Ledger is More Than Adding Accounts

Potential Impacts

Key Assessment Activities

Differences in the accounting treatment between current accounting standards and IFRS will likely drive changes to general ledger design

Multinational companies may ultimately realize a need to re-develop their general ledger platforms to enable compliance with multiple financial reporting requirements (statutory, industry / regulatory and tax)

Multi-ledger accounting functionality within newer releases of ERP may be considered for long-term solutions

Changes to IFRS will likely necessitate redesigned accounting, reporting, consolidation, and reconciliation processes, which may impact configuration

Assess high level changes to chart of accounts based upon differences between IFRS and GAAP(s)

Analyze reconciliation process between sub ledgers and general ledger; assess accounting, reporting, closing/consolidation, and reconciliation processes

Assess journal entry methods and templates

- 20 -

Data Standards & Warehouses May Be Affected

Potential Impacts

Key Assessment Activities

IFRS has more extensive disclosure requirements, requiring regular reporting and usage of financial data that may not be standardized in current data models

Increased need for documented assumptions, sensitivity analyses may expand the scope of information managed by financial systems

Reporting warehouse feeds to calculation engines may need to be adjusted in a standardized way to support reporting processes

Data governance functions and meta data repositories (potentially including data dictionary, ETL & business intelligence tools) may require adjustment

Identify changes in information requirements due to IFRS and assess impacts on existing data model

Assess readiness of data governance function and meta data repositories to be updated to reflect new data definitions

Confirm impact of any data definition changes on third parties

- 21 -

Reporting Changes Are More Than New Formats

Potential Impacts

Key Assessment Activities

The differences that arise in the accounting treatment between current accounting standards and IFRS will create a need for changes in reporting

Assumption changes from period to period may require detailed support for derivation and rationale for changes, requiring additional reports

External reporting templates will likely require revisions to reflect IFRS requirements

Changes to data structures may impact KPI production and balanced scorecards

New information delivery tools may be required to meet all requirements

Evaluate external reporting templates to identify changes required to support disclosures

Identify information sets that would be needed to meet IFRS reporting and disclosure requirements

Assess business intelligence environment’s readiness for identified IFRS changes

- 22 -

System Considerations and Potential Impacts Vary“F

lexi

bilit

y”/ C

ompo

sitio

n of

Sys

tem

s En

viro

nmen

t

Mature, but flexibly architected Systems

“Legacy” or Mixed Systems Environment

ERP starting now or under way

Mature ERP Install

Systems Impact of IFRS

Systems complexity could require significant design / implementation efforts, limiting the time to implement robust IFRS capabilities. Decisions could end up tactical if delayed

Numerous choices are available. Decisions should be made based on future system flexibility and business adaptability

Upgrade or targeted & efficient enhancements. Upstream & downstream systems are the focus

Robust technical capabilities allow various solutions to IFRS requirements. Decisions driven by pragmatism

- 23 - US

Con

sulti

ng R

epor

t Tem

plat

e_R

EL2

_032

508.

pot

Key Takeaways

IFRS adoption generally can’t be accomplished by Finance alone; other functions (IT, HR, Marketing etc.) must be included

Major business transformation and/or technology initiatives either in progress or under consideration should evaluate IFRS adoption plans as ‘requirements’

Consistency of adoption can be better enabled by leveraging process and technology

Collection of new / additional data elements may be required to support disclosures

Potential modifications to sub-ledgers is likely to support some of the more challenging IFRS requirements

Mapping U.S. GAAP results into IFRS and adding top-side adjustments and process can work but is sub-optimal

Training is consistently under estimated and extends beyond finance

Communications should include both internal and external stakeholders

Implementation is a project in it’s own right and requires change management as well as centralized, dedicated program management

IFRS represents an opportunity to transform global financial reporting

- 24 -

Questions and Answers

Copyright © 2008 Deloitte Development LLC. All rights reserved.