international economics - managing the brazilian real (2013 devaluation)

TRANSCRIPT

Celine Yeo . Harvard Chan . Jonathan Ang . Nicholas Teo . Yeo Ding Run G3

Flow of Presentation

Pre 2013

Pre-2013: A strong real & currency wars

NicholasCelineDing RunJonathanHarvard

Part A

Key Developments that led to the devaluation

Part B

The actions taken by the BCB to manage the ER

Part C

India and it’s economy

Part CMeasures taken to

prevent deflation in India

0

5E+11

1E+12

1.5E+12

2E+12

2.5E+12

3E+12

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 199519961997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Brazil GDP (US $)

1980 - 1984Oil Shock doubles price of imported oil. Lowered terms of trade, high debt and faced austerity from IMF

Cruzado Plan (1986)Readjust wages, freeze prices, rents and exchange rate. Inflation resumed at end of year.

Summer Plan (1989)Avoid inflation in election year. Less revenue for federal governments

New president (1990)Stabilization plan, 18 month freeze to most of private sector assets, liquidity freeze, reduce inflation

Plano Real (1994)New stabilization plan. 1) Introduction

of equilibrium budget

2) Introduction of BZL

3) Monetary Reform

Asian Financial Crisis (1997)Risk adverse as a result of EM exposure, large current account deficits

Luis Re-elected (2006)Strong economic growth under his stewardship

IMF support (1998)$41.5 bn support after crafting fiscal adjustment and structural reform

Slowing Economic Growth (2006)Sluggish consumer spending contributed to lower GDP growth

Govt ConsumptionImports

Household Consumption

InvestmentsExports

12.4%

62.5%

-14.9%

18.7%

21.7%

GDP

Household Consumption 62.5%

Investments 18.7%

Imports 14.9%

Govt Consumption 21.7%

Exports 12.4%

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

GDP Composition 2013

48%

11%

24%

17%

United States

Others

China

Europe

Exports Destinations 2013

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Top Exports of Brazil

5.3%

7%

8.4%

13%

Raw Sugar

Soybeans

Crude Petroleum

Iron Ore

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

The Strong Real Before 2013

Strength of the real (2010 to 2012)

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

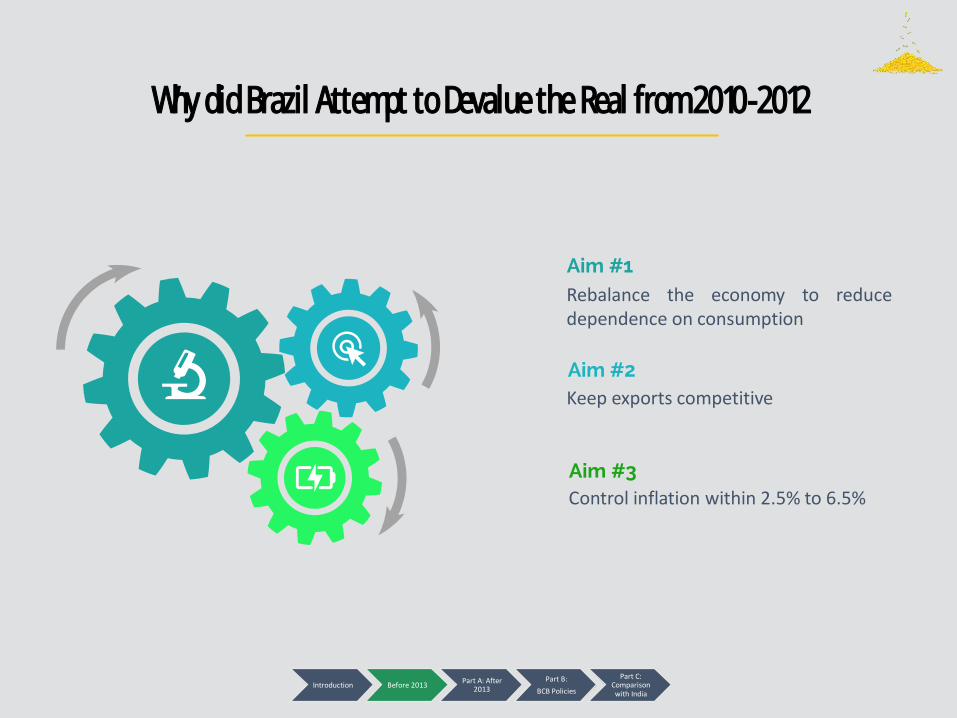

Aim #1Rebalance the economy to reducedependence on consumption

Aim #2

Aim #3

Keep exports competitive

Control inflation within 2.5% to 6.5%

Why did Brazil Attempt to Devalue the Real from 2010 -2012

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Why did Brazil Attempt to Devalue the Real from 2010 -2012

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Demand affected the realBCB decreased Selic rates 2011-

2012 before maintaining a constant rate of 7.25%. However,

it was comparatively higher to other countries, causing hot

money inflow.

High Demand for Brazilian Debt

The strong real is due to investors buying up high yielding Brazilian debt,

and this may make exports more expensive, hurting the exports.

Brazilian Central Bank (BCB) imposesextra IOF taxes on foreign investors to

reduce buyers and weaken the real. BCB also wants to devalue the real so

that it will not hurt exports.

Strong Real Hurting ExportsThe strong real is hurting the

exports of price-sensitive commodities, the bedrock of Brazil’s economy. BCB has to

devalues its currency to keep exports competitive

Protectionist PoliciesDue to years of protectionist policies, Brazilian manufacturing becomes inefficient and overpriced, losing export competitiveness

Port BureaucracyInefficient port bureaucracy and port infrastructure: turn-around time for containers of 21 days at Santos, compared to 1 or 2 days internationally. This has affected Brazil’s trade.

Reduce Dependence on ConsumptionSince Brazil has current account deficit, it shows that Brazil is dependent on consumption for growth and the source of inflation is from imports. The govt believes that devaluing the real can reduce consumption and reduce inflation.

Competitive devaluation (2009 2013)

1. Competitive devaluation from 2009 – 2013 which became prominent in Sept 2010

2. Fed, BoJ introduced loose monetary policies (i.e. QE) post 2008

3. Coined by Brazil finance minster Guido Mantega

4. Mercantilist approach to support cheaper exports

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Nov 2009Goldman Sachs declares real most overvalued currency in the world

Oct 2010Brazil increases capital controls. Doubles taxes on fixed income assets to 4%. Taxed capital inflows from 2% to 6%

Dec 2009QE1 is announced

Sept 2012QE3 is announced

June 2013Tapering is announced

Nov 2010QE 2 announced

Competitive devaluation (2009 2013) - Timeline

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

What is QE?

What happens

in QE?

Unconventional formof monetary policy

Central Bank prints “new” money or use

electronically created money to buy government securities and other assets

from banks

• Aimed at lowering interest rates

• Banks use these money and lend to

consumers/businesses and buy other assets like bonds

• Creates a virtuous cycle of spending and investment

Competitive devaluation (2009 2013) - Quantitative Easing (QE)

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Competitive devaluation (2009 2013) USA

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

-2013

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Strategies used to devalue currency

1. Use of interest rates – high interest rates mean constrained economic growth but higher foreign capital inflow

2. Foreign currency trades –international reserves used as insurance against crisis to smooth forex rates

3. Intervene with swap operations – To prevent depreciation of domestic currency (BZL to USD)

4. Reverse swap – Selling contacts to limit appreciation of currency (USD to BZL)

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Government carried out 36 currency swap operations between July 2011 to Dec 2012

Does not directly affect supply of foreign currency, affects the exchange rate as to alter demand for forex (short term)

FX purchases of real decreased

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Strategies used to devalue currency Currency Swap Operations

In 2012, BRL sales outweighed U.S dollar purchases inflow

BCB auctions swaps and shorts the USD

Contrato de Swap Cambial com Ajuste Periódico – the swap contracts

When the BCB believes the BRL is too cheap (undervalued) it auctions swaps and effectively goes short the USD, when it believes the real is overvalued

It auctions reverse swaps and goes long the USD– short its own currency.

Foreign reserves do not need to come into play

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Strategies used to devalue currency Currency Swap Operations

2006 – BCB bet on appreciation on USD to contain BRL rise

Flat line – represented no use of swaps

“Free floating” but actually managed currency

Adjusted with swaps

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Strategies used to devalue currency Currency Swap Operations

1. Raised IOF tax in fixed income securities from 4% to 6%

2. Boosted levy on money for margin deposits for futures trades from 0.38% to 6%

3. Measures taken to erode foreigner’s short term demand for investments

4. Between May 2009 to Dec 2012, BCB intervened 62% of all trading days

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Strategies used to devalue currency IOF Tax

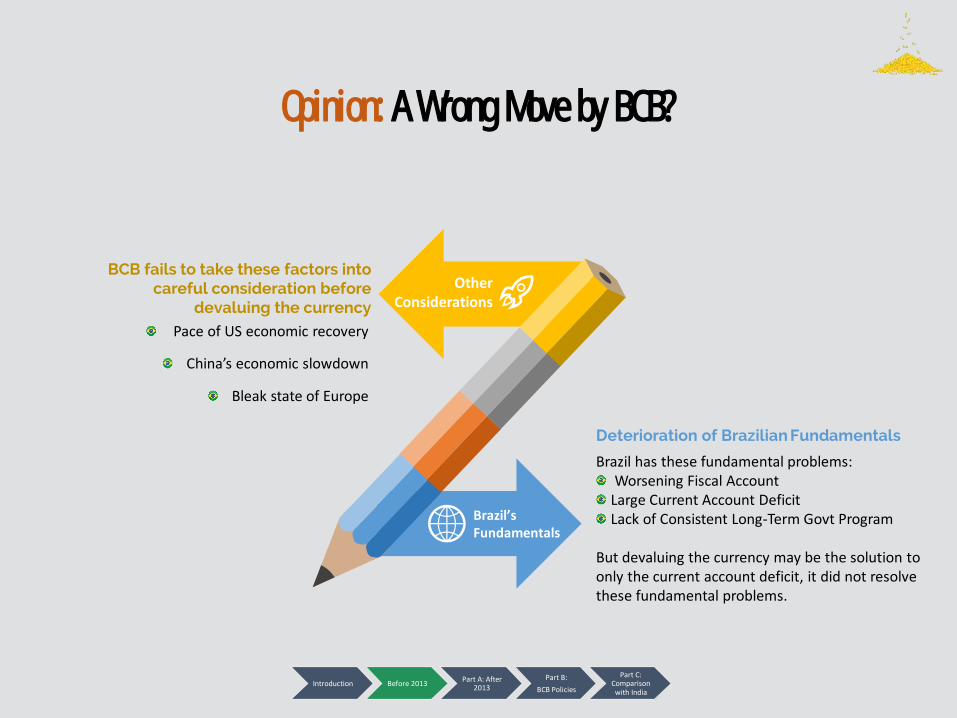

Other Considerations

BCB fails to take these factors into careful consideration before

devaluing the currency

Opinion: A Wrong Move by BCB?

Pace of US economic recovery

China’s economic slowdown

Bleak state of Europe

Deterioration of Brazilian Fundamentals

Brazil has these fundamental problems:Worsening Fiscal Account

Large Current Account DeficitLack of Consistent Long-Term Govt Program

But devaluing the currency may be the solution to only the current account deficit, it did not resolve these fundamental problems.

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Brazil’s Fundamentals

Key economic & financial developments Leading to

Devaluation

Part A

• Stagnant growth• Fiscal shocks

(Govt budget cut and Tax increases)

1.7%

7.7%

2.9%

Europe Stagnating

• Experiencing slowing growth, well below the double-digit growth it chalked up over the past 30 years.

• Slow growth as China begins to address the costs of the rapid growth that include pollution, wasted spending, corruption and finacial frugality.

• China wants to restructure the economy to rely less on heavy investments in real estate, infrastructure, capital-intesive industries and exports abroad.

China’s Slowing Growth

US Gradual Recovery

Gradually recovering from recession

Major Economies 2013

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Key developments that led to devaluation

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Key developments that led to devaluation

Balance of Payments

Current Account

Capital Account

Asset Market Approach

i*

ee

Balance of Payments

Commodity Prices

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Current Account

Commodity Exports

Image Source: MarketLineData Source: IMF, MarketLine

Dependence on commodity exports (Risks)

• Manufactured exports declined from close to 60% to 40% of total exports

• Rising prominence of iron ore and soybeans among exports, economy is more vulnerable to price shocks

• China is Brazil’s main trading partner since 2012; major importer of iron ore

• With slowing growth from china, china demands less imports from brazil. Causing Brazil’s Export to fall further

Current Account

Current Account Deficit

• Current Account Deficit increased

• Reasons for the deficit: Fall in trade surplus

• Import still continued to increase, especially fuel import

• Widening deficit( 4.17% of GDP)weaken currency additional inflation pressure as imports more costly (serious challenge for Brazil, struggling with subdued global economy and productivity shortcomings at home.)

• X-M <0 Current Account Deficit

0

5E+10

1E+11

1.5E+11

2E+11

2.5E+11

3E+11

3.5E+11

Exports of goods andservices (BoP, currentUS$)

Imports of goods andservices (BoP, currentUS$)

Image Source: Rabobank and WorldBankData Source: Rabobank

Current Account

Current Account Deficit

Image Source: Rabobank

• Increase in deficits in the Services Account (High increase of international travelling expenditure)

• Increase in deficits in Income Accounts

Although FDI remained consistent in 2013 at USD64 billion, because of the increase in CA deficit, it can no longer cover the deficit

Current Account

Weak Capital Account

Gross fixed capital formation stood at 5% lower than peak 2011 levelMost other EMs had investment growth, however Brazil has contracted

Investment in Brazil is lower than average compared to other EMs

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Capital Account

Why are there low investments rate in Brazil?

Reliance on FDI

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Poor legal rights, ease of doing businessPoor ratings in time to open a business and prepare and pay taxes

Difficulty in doing business deters FDI

Capital Account

Reliance on FDI Capital Account

In May 2013, there was a riot due to public outcry due to the large sum spent on building stadiums when transportation, healthcare and

education require funds more urgently.Brazil govt was slow in its response to the protests and this has

severely affected investors’ confidence and decapitated FDI in BrazilWith the US signaling a tapering of its monetary policy, the FDI in Brazil

has been severely affected.

Reliance on FDI

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Balance of payments has mainly been funded via capital accountFDIs have been remaining constant but portfolio investment fluctuates greatly

Massive and rapid change in capital inflows affects export competitiveness

Brazil relies on its capital account to finance its BOP. The fluctuations may lead to deeper CA deficit & speculative attacks may occur.

Capital Account

Large Commercial Outflows

Extremely open capital account – short term capital flows bring instability to economy

Ineffective elimination of capital outflows –reduction of Financial Transactions Tax on fixed income securities from 6% to 0%

These short term portfolio investments lead to instability of the BOP and may lead to currency crisis.

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Capital Account

Balance of Payments - Conclusion

The BOP in Brazil is mainly funded through the capital account

Commodity prices have affect exports and CA is in deficit

The capital account is also contributed to by “hot money” or short term portfolio investments

These factors may lead to an instability of the BOP and a persistent current account deficit. Ultimately, these could lead to a currency crisis.

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Balance of Payments

Asset Market Approach

Asset market approach - Interest Rates i*

• US Fed Funds rates remained constant

• 2013, Federal Reserve has considered tapering its QE Program – Market has expectation of an increase in interest rates

An expectation of the rise in US interest rates also led to a devaluation in Brazilian Real, as brazil experiences capital outflow to US.

Asset market approach - Interest Rates

Brazilian exchange rate expectation

ee

• Brazil’s relys on its capital account, particularly short term portfolio investment

• This “hot money” is expected to flow out with the backdrop of an improving US economy

There is an expectation for the Brazilian real to depreciate due to projected trade account deficit

Asset market theory - Conclusion

Interest rates in USA are expected to rise due to the taper

The trade deficit has created expectations of devaluation

These factors support the devaluation of the real.

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Asset Market

• Brazil has faced persistent high inflation in recent years and this has led to an increase in Selic rate to curb inflation

• Central Bank’s Inflation target is 4.5% with a ± 2% expectation

• Central only managed to hit the high side of 6.5% with interest rate of more than 10%

To curb the high inflation, BCB raised the high Selic rate, this in-turn increase the cost of borrowing, hurting the consumption in the Brazil.

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

The Brazilian Lifestyle

Installment plans on anything

R$ 1000 TV Set24 monthly installment of R$ 41.70

R$ 54 Toy Robot5 monthly installment of R$ 10.80

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

• Steady credit growth in Brazil from the consumer and companies.

• This shows a culture and reliance of credit for consumption.

• At some point, the interest charged will be too much and there will be defaults which will affect consumption in brazil, worsening its economic state.

A Culture of Credit

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

• One of highest Govt Debt in the world and financed with a deficit

• Brazil Govt reliance on debt to finance policies

A Culture of Credit in Govt

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Managing the

ER

Managing the ERPart B

Policy Instruments To Manage the Exchange Rate

Brazilian Central Bank (BCB)

Deepening of Financial Markets

Monetary Policy

- Interest Rate Policy

Macro-Prudential Policy

- Eliminates Reserve Requirement Ratio

Capital Control Management

- Eliminate IOF Tax on Fixed-Income Instruments

Government Fiscal Policies

IPI Tax on Automobiles

*Will not be covered in details

Brazilian Central Bank

(BCB)

Deepening of Financial Markets

Monetary Policy

- Interest Rate Policy

Capital Control Management

- Eliminate IOF Tax on Fixed-Income Instruments

Policy Instruments To Manage the Exchange Rate

Stabilization of the Real

Price Stability Objectives

Maintain Financial Market Stability

Macro-Prudential Policy

- Eliminates Reserve Requirement Ratio

Mitigate Reversal of Short-Term Capital Flows

Inflation Rate TargetingWhen planning monetary policy: BCB sets Selic rate to target inflation at 4.5%, with tolerance range between 2.5% and 6.5%

Set direction and focus for monetary policy

Improves investors’ confidence in Brazil

Achieve stability in exchange rate

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

On 22 Aug 2013, BCB announced $60 billion currency intervention program:

o $500 million worth of currency swap auctions and derivative contracts auctions from Mon-Thu

o $1 billion on spot market through repurchase agreements on Fri

Currency Intervention Program

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

$500 million worth of currency swaps auctions and derivative contracts auctions from Mon-Thu

o Daily auctions of derivative contracts that investors use to place future bets against the Brazilian real.

o These derivative contracts are seen as a method to protect investors' holdings of the local currency, so that they do not rush to sell at the first sign of weakness.

This widens the range of money market instruments, build financial market external resilience and stabilizes the real

Ensure both the stability in exchange rate and Brazilian real liquidity

1. Deepening of Financial Markets via Currency Swap Auctions

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Deepening of Financial

Markets

2. Monetary Policy - Interest Rate PolicyBrazil’s interest rate is known as SELIC (Sistema Especial de Liquidação e de Custódia)

FIs participate with SELIC as custody account holders

Selic – the overnight rate

Selic transaction process through repurchase agreements (Repos)

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Monetary Policy

• Gradual increases as a result of Fed tapering & repatriation of capital• BCB pressured into defending the real through increase of interest rates and the selling of foreign

reserves• Brazil’s vehicle for undertaking OMO – like the FOMC • Objectives:

o Price stabilityo Reduce inflation effectso Guide inflation to its target of 4.5% ± 2%

2

4

6

8

10

12

14

16

2015

2014

2013

2012

2011

2010

2009

2008

2007

2006

Selic Rates

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Monetary Policy

How does it works?• When Selic rate increase, it is more

attractive for international investors who are seeking for high returns.

• This leads to more portfolio capital inflows into Brazil.

• Increasing the demand for real.• Strengthening the real against other

currency.

Increasing Selic Rate via RepoBCB offer $1 billion repos every Friday to pull short-term funds from the financial system. This means that money supply is reduced, in-turn pushing up the Selic rate as a monetary policy instrument to mange its currency stability and at the same time, meet its economic goals.

2. Increasing Selic Rate

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Portfolio Capital Inflows

Value of Real

Selic RateMoney SS

Monetary Policy

3. Macro-Prudential Policy

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Eliminated the local banks reserve requirement on short dollar positions against the real• This increases lending to the economy, increasing the

returns on domestic and forex deposits, resulting in an appreciation of the real

• Objective:o Address financial market instability

Macro-Prudential

Policy

Monetary Policy

Macro-Prudential

Policy

Price StabilityFinancial

Market Stability

• Introduced in June 2013

• By lifting the IOF tax on fixed-income, BCB is aiming to attract more investments and capital inflow into Brazil.

• This will attract more investors seeking higher returns, given that the Selic rate has increase after that.

• The demand for real will increase and the real will strengthen against the USD.

o However, the removal of fixed-income IOF can be a double-edged sword.

o While the removal of fixed-income IOF is aimed at attracting investments and portfolio capital inflow, it canactually increase volatility in the market.

o The initial high IOF of 6% had initially “locked” investors’ capital in Brazil as they are unwilling to withdrawcapital out of Brazil’s fixed-income market as they have to fork out 6% to bring it back in again.

o However, with the IOF reduced to 0%, coupled with the US signaling a tightening of the monetary policy, thishas led to capital flight from Brazil into US which has better near-term prospects.

Reducing Fixed-Income IOF from 6% to 0%

IOF is the Brazilian tax on fixed-income foreign portfolio investments

4. Capital Control Management

How does it works?

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Capital Control

Management

Effectiveness of Policy Instruments

Ensuring Price Stability• Inflation of 6% to 6.5% in 2013• Targeted inflation of 4.5% ± 2%

achieved in 2013

Worsening Current Account Deficit• CAD worsened from -3% in Q3

2013 to -3.7% in Q1 2014• Resulted from declining demand

for its exports

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Effectiveness of Policy Instruments

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

Improving Capital Account• The initial fall in capital flows in Aug 2013

could be attributed to the removal of IOF tax on fixed-income instruments. The initial high IOF could have “locked” investors’ capital in Brazil. With the removal of IOF tax on fixed-income instruments, coupled with US signaling a tightening of its monetary policy, this could have led to the capital flight from Brazil in late Q3 2013.

• Eventually, capital flows increased from from Q4 2013 to Q1 2014, posting an overall increase trend in the capital account.

Stabilization of Brazilian real• Achieved through improving its

capital account via increasing Selic rate, currency swap auctions

ComparisonwithIndia

India Vs BrazilPart C

Nominal GDP of US$1.876Trillion

G IX-M C

16.47%

-3.6%

30.02%

57.11%

Net Importer

High Dependence on Investments

India’s Current Account Deficit (CAD)

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

61

Causes of Downward Pressure on Rupee

High Dependency

on Investments

US Economy Gradual

Recovery

Weak Balance of Payments

Rising Oil Prices

India’s Low

Foreign Reserves

WEAK BALANCE OF PAYMENTS

• Large Current Account Deficit (CAD) since 2003, with a negative growth of 2293% in the last 10 years

• CAD of US$75.8 billion as at 2013• Global Rank of 192, just above Brazil• Large and Persistent CAD implies higher vulnerability

to sudden capital flow reversal, resulting in currency collapse

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

WEAK BALANCE OF PAYMENTS

• Persistent Fiscal Deficit since 1991• Implies Government is spending more than it is receiving• Increase chances of speculative attacks as it is assumed that

the government do not have enough reserves to protect its economy

• Large and persistent twin deficits makes India very susceptible to pressure on its rupee

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

RISING OIL PRICES

• Brent crude oil has rose to a 6-month high of US$115.59 in August 2013

• Almost 79% of India’s crude oil needs are imported

• The rise in oil prices implies that India has to pay an increased amount of USD for the same quantity of oil

• India has to sell more rupees to buy more USD

Value of Rupee

Domestic Money Supply

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

HIGH DEPENDENCY ON INVESTMENTS

• 30% of India’s GDP is on investments• After 2008 Global Financial Crisis, Federal Reserve

cut interest rateo Lower cost of borrowings causes investors to borrow

from US and invest in higher yielding assets in emerging markets like India, strengthening the rupee

o This is how India is able to finance its CAD

• However, speculations of QE tapering caused investors to pull out a record US$10 billion from Indian debt & equity markets

Foreign Capital Outflow

Domestic Money Supply

Value of Rupee

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

US Economy Gradual Recovery

• Signs of recovery from the impact of Global Financial Crisis gave rise to expectations of a stronger US dollar

• Resulted in capital inflow into the US Economy• Some of these capital flows out from India to US

Domestic Money Supply

Value of Rupee

Foreign Capital OutflowIntroduction Before 2013

Part A: After 2013

Part B:

BCB Policies

Part C: Comparison with India

Foreign Reserves

• Foreign Reserves grown by a little over 2 times (from US$138 billion in 2005 to US$295 billion in 2013)

• However, CAD have grown by more than 5 times in the same period(from US$12.95 billion to US$74.8 billion)

• Foreign reserves are able to cover CAD from more than 10 times in 2005 to less than 4 times in 2013o India is unable to intervene in its foreign currency

markets as aggressively as beforeo Declining ability to protect its currency from

currency shocks, making it more susceptible to speculative attacks

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013

Number of times Foreign Reserves can cover CAD

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

68

OTHER POLICIES

MACRO-PRUDENTIAL POLICIES

MONETARY POLICIES

FISCAL POLICIES

Measures Taken to Prevent Devaluation

1. FISCAL POLICIES

• The government imposed higher import tax on gold and silver, the largest luxury import, from 6%to 10%

• 20% of every lot of import of gold must be for export purposes

Increased Tax on Silver and Gold Imports

• Increased deposit rates for Non-Resident Indians (NRIs)

• Relaxed FDI’s routes for investments in India (changed from government to automatic) for various sectors such as commodity and retail

Encouraging Capital Inflows

Healthier BOP

Current Account Deficit

Foreign Capital Inflows

More Resistant to Currency

Shocks

2. MONETARY POLICIES

• Reserve Bank of India (RBI) have increased the MSF (interest) rate from 8.25% to 10.25%

• Aim at influencing the multiplier effect, reducing the money creation process and hence reducing money supply

Increasing Marginal Standing Facility (MSF)

Rate

Value of Rupee

Domestic Money Supply

Open Market Sales of Government Securities

• RBI announced the sale of government securities worth Rs 12,000 crore via Open Market Operations to reduce liquidity via reducing money supply

3. CAPITAL CONTROLSIntroduction Before 2013

Part A: After 2013

Part B:

BCB Policies

Part C: Comparison with India

• Amount of money Indians can take out of the country reduced from $200,000 to $75,000 per financial year

Reduction of Outward Remittance

• RBI have reduced LAF (the amount of money that banks are able to borrow from RBI through repos), to a maximum of 1% of its deposits, which amounts to an estimated Rs 75,000 crore

Restricting Liquidity Adjusting Facility (LAF)

Aim to keep the money within the country to avoid volatility

4. OTHER POLICIES

• RBI provided US dollars directly to 3 state-owned oil companies (Indian Oil Pte Ltd, Hindustan Pentroleum Corp, Bharat Petroleum Corp), which have the biggest demand for USD of $400 to $500 million daily

Dollar Aid to State-Owned Oil Companies

Value of Rupee

Domestic Money SupplyIntroduction Before 2013

Part A: After 2013

Part B:

BCB Policies

Part C: Comparison with India

This is to isolate these demands from the market, hence reducing pressure on the rupee

VSBRAZIL INDIA

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

India stabilized its devaluation from a high of 67.39 Rupee per USD to a current value of 62.36 rupee per USD

VALUE OF CURRENCY

Real continued its devaluation from 2.433 to a current value of 3.117 per USD in the same period

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

July 2013 to 5.37% currently

INFLATION RATE

July 2013 to 7.7% currently

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

India achieved a healthier CAD, narrowing the deficit from US$12 billion in July 2013 to US$6.84 billion currently

CURRENT ACCOUNT DEFICIT

US$2.84 billion currently

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

India FDI increased from US$2 billion from July 2013 to US$5.5 billion currently

FOREIGN DIRECT INVESTMENTS

Brazil FDI decreased from US$6 billion to US$2.76 billion currently

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

HOW MUCH OF THE DIFFERENT OUTCOMES ARE ATTRIBUTED TO

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

However external effects like the decrease in oil prices could have improve its current account deficit, leading to an improvement in India’s economy

FDI liberalization & restriction of outward

remittance & cuts in MSF and LAF

Tax on luxury imports & currency

swaps with oil companies

economy in a bid to support the rupee

These policies aim at C and I component of its GDP

Tax of luxury imports reduce M component of GDP

Currency swaps allow the cost of oil imports to be kept low, reducing the

pressure on inflation

India’s policies are well rounded because it addresses its currency pressure issues by targeting both domestic and foreign factors, hence India did not suffer from the side effects by emphasizing too much on one policy.

Introduction Before 2013Part A: After

2013

Part B:

BCB Policies

Part C: Comparison with India

However external effects such as the recent slow growth in China and Europe crisis could have contributed to its economy worsening, which is largely uncontrollable by Brazil.

capital outflow

Selic rate hike & reducing IOF

These policies aim at I component of its GDP

Brazil’s policies are too focused on trying to keep capital from flowing out of the country. This has actually caused its economy to worsen due to conflicting effects• Increasing SELIC rate & reducing fixed-income IOF tax

aim to attract hot money and this should have strengthen the real.

• However, with the gradual recovery of the US economy, the reduction of fixed-income IOF actually backfired and led to more outflow of portfolio capital from Brazil. This further weakens the real.

• The increasing selic rate also increased the cost of borrowings for both consumers and businesses, impeding domestic growth in Brazil.

India is able to lessen the external effects on its economy more than that of Brazil. • India, being a net importer, is able to directly control demands

for imports by raising taxes. • Brazil on the other hand, are not able to increase demands

from its exports apart from depreciating its currency.

However, we cannot deny that the policies implemented indeed have an impact on its currencies.

Our group feels that in terms of managing its exchange rate, India’s policies have managed it better than Brazil’s policies.

Conclusion

References• Liquidity and Reserve Requirements in Brazil – Patrice Robitaille, June 2011

• The Legacy of the Real Plan: A stabilization without economic growth. (n.d.). Retrieved March 28, 2015, from http://www.ufrgs.br/ppge/pcientifica/2001_06.pdf

• Brazil Real Posts Longest Losing Streak in 8 Weeks After Tax. (n.d.). Retrieved March 28, 2015, from http://www.bloomberg.com/news/articles/2010-10-19/brazil-steps-up-action-in-currency-war-even-as-mantega-seeks-ceasefire

•Wattret, K. (n.d.). BNP Market Outlook. Retrieved March 28, 2015, from http://bnpparibasinvestindia.com/files/1007_MM.pdf

•Fernandes, G. (n.d.). Interventions in the Brazilian Foreign Exchange Market: An Empirical Investigation of the Determinants. Retrieved March 28, 2015, from https://www.itau.com.br/_arquivosestaticos/itauBBA/contents/common/docs/Itau_WP9_FX_may13.pdf

•Ogier, T. (2011, September 23). Brazil vows continued currency intervention. Retrieved March 28, 2015, from http://www.emergingmarkets.org/Article/2906418/Brazil-vows-continued-currency-intervention.html

•Tabak, B. (2013, July 1). Official Intervention through Derivatives: Affecting the foreign exchange demand. Retrieved March 28, 2015, from http://www.bcb.gov.br/pec/wps/ingl/wps317.pdf

• The limits of Brazil’s FX intervention programme. (2014, August 25). Retrieved March 28, 2015, from http://blogs.ft.com/beyond-brics/2014/08/25/guest-post-the-limits-of-brazils-fx-intervention-programme

• OECD: Brazil (BRA) Profile Of Exports, Imports And Trade Partners. (N.p., 2015). Retrieved March 23, 2015, from

• http://atlas.media.mit.edu/profile/country/bra/

• The World bank. (N.p., 2015). Retrieved March 24, 2015, from http://www.worldbank.org/en/country/brazil

• Brazil Exports, Imports & Trade | Economy Watch. (N.p., 2015). Retrieved March 21, 2015,

• http://www.economywatch.com/world_economy/brazil/export-import.html

• Commercial Banks In Brazil | Economy Watch. (N.p., 2015). Retrieved March 23, 2015, from http://www.economywatch.com/banks/commercial-banks/latin-america-and-caribbean/brazil-banks.html

• Holanda Barbosa Filho, Fernando, and Samuel Abreu Pessôa. International Macroeconomic Impacts On The Brazilian Economy. 1st ed. Retrieved March 25, 2015 from http://www.oecd.org/eco/International-Macroeconomic-Impacts-on-the-Brazilian-Economy-paper.pdf

• Holland, Marcio. Capital Account Management In Brazil. 1st ed. Brazil: (N.p., 2015). Retrieved March 21, 2015 from https://www.imf.org/external/np/seminars/eng/2013/macro2/pdf/mh.pdf

• Wikipedia- List Of Banks In The Americas. (N.p., 2015). Retrieved March 25, 2015 from http://en.wikipedia.org/wiki/List_of_banks_in_the_Americas

• Brazil Economy Profile 2014. (N.p., 2014). Retrieved March 25, 2015 from http://www.indexmundi.com/brazil/

• Lorman, Herwin. Country Report Brazil. Rabobank. (N.p., 2014). Retrieved March 24, 2015 from • https://economics.rabobank.com/publications/2014/february/country-report-brazil/

• Country Profile Series: Brazil In-Depth PESTLE Insights. 1st ed. MarketLine, 2014. Print. Retrieved March 24, 2015

• BBC News- Brazil Profile - Timeline. (N.p., 2015). Retrieved March 20, 2015 from http://news.bbc.co.uk/2/hi/americas/1231075.stm

• Biller, David, and Arnaldo Galvao. China, Brazil Sign $30 Billion Swap Accord To Bolster BRICS. Bloomberg. (N.p., 2013). Retrieved March 24, 2015 from http://www.bloomberg.com/news/articles/2013-03-26/china-brazil-sign-currency-swap-agreement-for-30-billion

• The end of poverty? (2013, February 28). Retrieved March 22, 2015, from http://www.economist.com/blogs/americasview/2013/02/social-spending-brazil

• Grounded. (2013, September 28). Retrieved March 22, 2015, from http://www.economist.com.libproxy.smu.edu.sg/news/special-report/21586667-having-come-tantalisingly-close-taking-brazil-has-stalled-helen-joyce-explains

• Going for broke. (2013, October 18). Retrieved March 22, 2015, from http://www.economist.com.libproxy.smu.edu.sg/blogs/americasview/2013/10/public-finances-brazil

• An ever-deeper hole. (2013, June 10). Retrieved March 22, 2015, from http://www.economist.com.libproxy.smu.edu.sg/blogs/americasview/2013/06/brazils-public-finances

• Stuck in the mud. (2013, June 8). Retrieved March 22, 2015, from http://www.economist.com.libproxy.smu.edu.sg/news/americas/21579048-feeble-growth-has-forced-change-course-governments-room-manoeuvre-more

• A fall from grace. (2013, June 8). Retrieved March 22, 2015, from http://www.economist.com.libproxy.smu.edu.sg/news/leaders/21579007-how-squander-inheritanceand-how-easily-it-could-be-restored-fall-grace

• Looking for change. (2013, October 18). Retrieved March 22, 2015, from http://www.economist.com.libproxy.smu.edu.sg/news/briefing/21625661-under-dilma-rousseff-brazils-economy-has-stalled-she-promises-reignite-growthbut-faces#

• Why Brazil needs change. (2014, October 18). Retrieved October 22, 2015, from http://www.economist.com/news/leaders/21625780-voters-should-ditch-dilma-rousseff-and-elect-cio-neves-why-brazil-needs-change

• Has Brazil blown it? (2013, September 28). Retrieved March 22, 2015, from http://www.economist.com/news/leaders/21586833-stagnant-economy-bloated-state-and-mass-protests-mean-dilma-rousseff-must-change-course-has

• RBI opens special window for forex purchase by oil companies. (n.d.). Retrieved March 28, 2015, from http://businesstoday.intoday.in/story/rbi-opens-special-window-for-forex-purchase-by-oil-companies/1/198183.html

• The PRS Blog. (n.d.). Retrieved March 28, 2015, from http://www.prsindia.org/theprsblog/?p=3009

• India’s reliance on imported energy threatens long-term recovery - FT.com. (n.d.). Retrieved March 28, 2015, from http://www.ft.com/intl/cms/s/0/c20792e2-1b84-11e3-b678-00144feab7de.html#axzz3V22V1e4g

• India | Economic Indicators | Data List By Country. (n.d.). Retrieved March 28, 2015, from http://www.tradingeconomics.com/india/

• Collapsing Asian Currencies? Why is the Indian Rupee Depreciating? (n.d.). Retrieved March 28, 2015, from http://www.globalresearch.ca/collapsing-asian-currencies-why-is-the-indian-rupee-depreciating/5350017

• RBI steps in to ease rupee volatility. (2013, July 15). Retrieved March 28, 2015, from http://www.thehindu.com/business/Economy/rbi-steps-in-to-ease-rupee-volatility/article4918136.ece

• Gold duty raised to record 10 percent as imports revive. (2013, August 13). Retrieved March 28, 2015, from http://in.reuters.com/article/2013/08/13/india-tax-finmin-idINDEE97C03J20130813?type=economicNews

• Key 2013 FDI Policy Changes in India - India Briefing News. (2014, February 20). Retrieved March 28, 2015, from http://www.india-briefing.com/news/key-2013-foreign-direct-investment-policy-changes-in-india-7902.html/

Getting RealWith

The REAL

History & Backdrop

Short term fiscal adjustment

Introduction of new currency

De-indexation of economy

Floating of currency with floor value

The Real Plan

Short term fiscal austerity implemented

Cut expenditures while creating tax over financial transactions to increase revenue

In June 1994, fiscal surplus was 2.6%

(i) Short term fiscal adjustment

Unit of real value (URV) was introduced, while cruzerio real continued to be used as legal tender

The URV was an average of inflation indexes in Brazil

Pushed to find a sustainable price set

Market mechanisms were respected

(ii) Introduction of Real

June 1994, 5150%

Dec 2000, 10%

Fighting inflation

Conjunction of bringing inflation down + short run demand in durable goods forced government to slow down economy

Controlled domestic credit & increased interest rates

ER thus became overvalued

Current account deficit due to high ER

Net ST capital inflows financed BOP

Current account deficit increased by 958.85% between 1994 to 1995

Effects of the Real Plan Demand Expansion

Eliminated inflation

Exchange rate trap brought SR macroeconomic inconsistency

BOB keeps inflation target, lets levels of output and unemployment be determined by supply side

High trade openness which affects import inputs

Must hold economic growth target while stabilization of ERManage ER against speculators (dirty floating)

Bring FDIs that can impact future exports

Overall Effectiveness