international cross-listing, firm performance, and top...

TRANSCRIPT

THE JOURNAL OF FINANCE • VOL. LXIII, NO. 4 • AUGUST 2008

International Cross-Listing, Firm Performance,and Top Management Turnover: A Test of the

Bonding Hypothesis

UGUR LEL and DARIUS P. MILLER∗

ABSTRACT

We examine a primary outcome of corporate governance, namely, the ability to iden-tify and terminate poorly performing CEOs, to test the effectiveness of U.S. investorprotections in improving the corporate governance of cross-listed firms. We find thatfirms from weak investor protection regimes that are cross-listed on a major U.S. Ex-change are more likely to terminate poorly performing CEOs than non-cross-listedfirms. Cross-listings on exchanges that do not require the adoption of stringent in-vestor protections (OTC, private placements, and London listings) are not associatedwith a higher propensity to remove poorly performing CEOs.

DOES CROSS-LISTING IN THE UNITED STATES IMPROVE the corporate governance offoreign firms? The “bonding hypothesis” proposed by Coffee (1999, 2002) andStulz (1999) predicts that after listing on a major U.S. stock exchange, foreignfirms become subject to stringent U.S. investor protections that constrain in-siders from expropriating minority shareholders. Because this hypothesis hasimportant implications for the effectiveness of U.S. laws and enforcement aswell as the efficacy of market-based approaches in improving global corporategovernance, it has attracted the recent attention of academics and practitionersalike.

To date, empirical support for the bonding hypothesis is principally drawnfrom the large literature that examines the economic consequences of cross-listing in the United States.1 However, as Leuz (2006) notes, the evidence inmany of these studies is fairly indirect, as it is difficult to attribute the economicconsequences of cross-listing directly to the bonding hypothesis because many

∗Lel is from the Federal Reserve Board and Miller is from Edwin L. Cox School of Business atSouthern Methodist University. We thank an anonymous referee and associate editor; CampbellHarvey (the editor); Mark Carey, Craig Doidge, Art Durnev, Nandini Gupta, David Mauer, ChipRyan, Chester Spatt, and Wendy Wilson; and seminar participants at the 2006 University of NorthCarolina GIA Conference, the 2006 University of Oregon Corporate Finance Conference, the 2006Financial Research Association Conference, the 2006 Utah Winter Finance Conference, LouisianaState University, and the University of Texas at Dallas. We thank Bill Megginson and MeghannaAyyagari for data access and Charles Murry and Laurel Nguyen for excellent research assistance.This paper represents the authors’ opinions and not necessarily those of the Federal Reserve Board.All errors are the sole responsibility of the authors.

1 Karolyi (1998, 2006) and Benos and Weisbach (2004) provide comprehensive surveys. We alsodiscuss the literature in Section II of this paper.

1897

1898 The Journal of Finance

theories of cross-listing have similar economic predictions.2 Moreover, the va-lidity of the bonding hypothesis has been called into question by a number ofrecent studies that document cross-listed firms’ lack of compliance with certainU.S. laws and the low number of enforcement actions by U.S. legal institutions(see, for example, Siegel (2005) and Lang, Raedy, and Wilson (2006)). Therefore,whether U.S. securities laws and regulations improve the corporate governanceof cross-listed firms is under debate as the nascent empirical evidence is pre-dominantly indirect and yields mixed results.

In this paper we pursue a different approach in testing the bonding hypothe-sis and examine a direct outcome of corporate governance: the propensity toreplace poorly performing CEOs. We argue that if cross-listing actually re-sults in increased shareholder protections, we should be able to observe spe-cific outcomes that are consistent with improved corporate governance. Wefocus on the sensitivity of top executive turnover to performance since an ex-tensive body of international research shows that a necessary component ofeffective corporate governance is the ability to identify and replace poorly per-forming CEOs (see, for example, Kaplan (1994), Coffee (1999), Murphy (1999),Volpin (2002), Dahya, McConnell, and Travlos (2002), Gibson (2003), DeFondand Hung (2004)). We compile a database of 70,976 firm-year observations from47 countries from 1992 to 2003 to test the hypothesis that CEOs of cross-listedfirms are more likely to face termination when firm performance is poor. We findthat the relation between CEO turnover and poor performance is stronger forcross-listed firms than non-cross-listed firms, and that the stronger turnover topoor performance relation for cross-listed firms is concentrated in firms listedon major U.S. exchanges (for example, Level 2 and 3 American depositary re-ceipts (ADRs)). Firms that list in the over-the-counter (OTC) market (Level 1),conduct private placements (Rule 144a), or even list in London do not have asignificantly different relation between CEO turnover and performance fromnon-cross-listed firms. Further, we find that the increased relation betweenCEO turnover and poor performance for cross-listed firms is strongest in coun-tries with weak investor protections. Overall, our results are consistent withthe hypothesis that U.S. securities laws and regulations improve the corporategovernance of cross-listed firms.

We also investigate several alternative explanations for our results, includ-ing the potential endogeneities that arise in a study of cross-listing and gover-nance due to the nonrandom nature of the decision to list in the United States.For example, we investigate if our results are due to the notion that better-governed firms are the ones that self-select to cross-list. To do so, we examineseveral specifications that measure the sensitivity of CEO turnover to perfor-mance for cross-listed firms prior to cross-listing. These tests show that therelation of turnover to performance is insignificant (significant) in the pre-cross-listed (post-cross-listed) period, which suggests that our results are notan artifact of the pre-cross-listed governance status of our sample firms. We

2 For further details on other theories that have been argued to generate similar predictions(e.g., market segmentation, investor recognition, increased liquidity, and better information) seethe discussion in Doidge, Karolyi, and Stulz (2004a) and Hail and Leuz (2004).

International Cross-Listing 1899

also examine if other potential control changes around cross-listing such asprivatizations, changes in ownership, M&A events, and changes in the com-position of board of directions can explain our results. We find that our re-sults remain robust to these events. Further, we examine if cross-listing in-duces top management to leave their jobs to pursue employment in the UnitedStates where they are likely to be more highly compensated or if cross-listedfirms terminate poorly performing management because they are able to ac-cess a more international pool of top-management candidates. We find thatfirms that change CEOs tend to replace them with managers from their do-mestic labor pool and that departing CEOs most often get jobs in the localmarket. Therefore, shifts in the labor market also do not appear to explain ourresults.

We subject our tests to a battery of firm- and county-level robustness testsas well. We find our results are robust to country, industry, and year fixedeffects in addition to the possible entrenchment effects of concentrated owner-ship structures. Our findings are also robust when we exclude countries thatcontain the largest portion of our sample, remove observations surroundingthe Asian financial crises, and omit financial and regulated industries. An im-portant methodological note is that all of our analyses control for the recentlyrecognized difficulty in implementing and interpreting interaction effects innonlinear models (see, for example, Ai and Norton, (2003)).

Our results advance the literature in several ways. First, our findings addto the debate on whether U.S. securities laws and enforcement are effective inreaching non-U.S. firms. Second, by showing that CEOs of cross-listed firmsare more likely to face termination when firm performance is poor, our resultsalso contribute to the literature by documenting a specific channel throughwhich cross-listing improves corporate behavior, something that is not well-documented in the literature.3 Finally, our findings also have implications forthe growing literature that examines how global corporate governance can beimproved (see, for example, LaPorta et al. (2000) and Coffee (2002)). This re-search stems from a large number of studies that show that the economic conse-quences for firms located in countries with poor investor protections are severe.4

Given the economic impact of poor investor protections and the correspondingdifficulty in changing a country’s legal structure (i.e., legal convergence), an im-portant question is whether market-based approaches (i.e., functional conver-gence), such as opting-in to a better legal system via cross-listing, can improvecorporate governance. Our finding that cross-listing in the United States is as-sociated with improved corporate governance is consistent with the hypothesisthat the functional convergence of legal systems to a higher global standard ispossible.

The remainder of the paper proceeds as follows. Section I discusses relatedliterature. Section II describes the data. Section III presents the research de-sign. Section IV shows the results and Section V presents robustness tests.Section VI concludes.

3 See, for example, the discussion in Leuz (2006).4 See, for example, LLSV (1997, 1998) as well as the survey by Beck and Levine (2004).

1900 The Journal of Finance

I. Related Literature

The bonding hypothesis of Coffee (1999) and Stulz (1999) posits that firmscross-listed on a major U.S. stock exchange have better corporate governancethan non-cross-listed firms from the same country, ceteris paribus, since cross-listed firms are subject to strong U.S. investor protections.5 For example, cross-listed firms on U.S. exchanges must adhere to U.S. disclosure practices, whichrequire them to reconcile their net income and shareholder’s equity to U.S.generally accepted accounting principle (GAAP), disclose the identity of ma-jority shareholders (10% or greater), and follow detailed procedures duringtender offers and going private transactions. These firms are also subject tofar-reaching U.S. investor protection laws such as the Foreign Corrupt Prac-tices Act and, more recently, the Sarbanes Oxley Act. Cross-listed firms arealso subject to punishment by U.S. law enforcement, both by the Securitiesand Exchange Commission (SEC) as well as private investor law suits, andto increased scrutiny from intermediaries such as financial analysts and debt-rating agencies.6 In contrast, listing on the OTC market or conducting a privateplacement allows substantial exemptions from these laws and regulations.7

Specifically, the bonding hypothesis predicts that, ceteris paribus: (1) cross-listed firms will have better corporate governance than non-cross-listed firms,(2) the difference in governance between cross-listed firms and non-cross-listedfirms will be greatest in the countries with the weakest investor protections,and (3) cross-listings that require the most stringent U.S. investor protections(i.e., on the NYSE, AMEX, or NASDAQ) will have the largest differences incorporate governance. In this way, cross-listing in the United States representsa market-based approach to increased investor protection.

While in theory a cross-listing in the United States should lead to more ef-fective corporate governance, the ability of a cross-listing to serve as a bondingmechanism is under debate. On the one hand, several empirical studies exam-ine the economic impact of cross-listing in the United States and find evidencethat is consistent with the bonding hypothesis. This line of research finds thatcross-listed firms from weak investor protection countries have larger stock-price reactions (Foerster and Karolyi (1999), Miller (1999)), higher valuation(Mitton (2002), Doidge, Karolyi, and Stulz (2004a)), more scrutiny by financialanalysts (Baker, Nofsinger, and Weaver (2002), Lang, Lins, and Miller (2003)),lower cost of capital (Errunza and Miller (2000), Hail and Leuz (2004)), bet-ter information environments (Bailey, Karolyi, and Salva (2005)), lower votingpremiums (Doidge (2004)), and more access to external finance (Reese andWeisbach (2002), Lins, Strickland, and Zenner (2005)). However, ascribing theevidence contained in many of these studies directly to the bonding hypothesis

5 It is important to note that while firms may choose to cross-list for a variety of reasons, oncethey are listed they become subject to U.S. laws and regulations.

6 Coffee (2002) calls these intermediaries “financial watchdogs.”7 For example, these firms are not required to register under the Exchange or Securities acts and

are therefore exempt from most civil liability provisions and do not have to follow U.S. disclosurepractices (Doidge (2004)).

International Cross-Listing 1901

is difficult given the well-known challenge in distinguishing among the varioustheories of cross-listing and the endogeneity issues inherent to this literature.8

On the other hand, the evidence in several recent studies suggests bondingvia cross-listing in the United States is ineffective. For example, Siegel (2005)finds that the SEC and minority shareholders have rarely enforced U.S. lawsagainst cross-listed firms and Lang, Raedy, and Wilson (2006) find that the ac-counting data of cross-listed firms from weak investor protection environmentsare of lower quality even though cross-listed firms are required to follow nom-inally similar accounting standards as U.S. firms. However, the approaches inthese papers are not without their drawbacks, as Coffee (2002) and Benos andWeisbach (2004) suggest that measuring the incidence of legal actions may un-derstate the deterrent benefit of laws, and Leuz (2006) argues that disclosurequality differences between cross-listed and U.S. firms may not be clear evi-dence against bonding as cross-listed firms are allowed considerable discretionin preparing their financial statements to U.S. GAAP.

Another challenge researchers face when testing the bonding hypothesis isthat it is often difficult to assess the quality of governance from observed mech-anisms of governance because governance mechanisms often substitute or com-plement one another, a finding that Doidge, Karolyi, and Stulz (2004b) empha-size is dependant on the extent of a country’s investor protections. Further, thisissue is likely to be exacerbated for cross-listed firms, given the many financialand regulatory changes that take place around a listing (see, for example, Lang,Lins, and Miller (2003, 2004)).

In this paper, rather than calculating the stock-price consequences, legal en-forcement incidents, or changes in governance mechanisms around a cross-listing to infer improvements in investor protections, we measure a directoutcome of corporate governance: the propensity to replace poorly perform-ing CEOs. Why CEO turnover? Replacing poorly performing CEOs is arguedto be a necessary condition for good corporate governance (Shleifer and Vishny(1989, 1997)) and the sensitivity of top executive turnover to performance as ameasure of the quality of corporate governance has been supported by a largenumber of studies in the United States and abroad, including recent researchby Dahya et. al (2002), DeFond and Hung (2004), Gibson (2003), and Volpin(2002).9

II. Sample Selection and Descriptive Statistics

A. Sample Selection

Our empirical analysis consists of three main parts. First, we investigatewhether the sensitivity of top executive turnover to poor firm performance ishigher for cross-listed firms. In these tests we differentiate cross-listings bytype in order to test whether cross-listings on major U.S. exchanges, which re-quire the strongest governance provisions, have the largest effect. Second, we

8 For example, Sarkissian and Schill (2006) argue that valuation gains to cross-listing aretransitory.

9 For U.S.-based studies see Hermalin and Weisbach (2003) and citations contained therein.

1902 The Journal of Finance

test if the effect of bonding is greatest for firms that are located in the countrieswith the weakest investor protection laws. We do so by examining the sensi-tivity of top executive turnover to poor firm performance across legal originsand investor protection laws. Finally, we conduct a battery of tests designedto gauge the robustness of our results by examining the sensitivity of top ex-ecutive turnover to poor firm performance in the pre-cross-listing period, theeffect of other potential governance changes concurrent with cross-listing, theexclusion of turnover that occurs in the list year, and the departing and en-tering CEOs’ work history. We also rerun our tests excluding countries thatcontain the largest portion of our sample firms, omitting firms with large blockownership, removing observations surrounding the Asian financial crisis, andexcluding financial and regulated firms.

To execute this analysis, we gather data on executive turnover and firm per-formance between 1992 and 2003 from the Worldscope database.10 The initialsample consists of approximately 38,000 firms from 59 countries. We excludefirms with missing firm-specific financial and executive data, firms with noidentifiable top manager, and firms located in countries with missing legal en-vironment data. We also exclude U.S. firms as the bonding hypothesis predictsdifferences between cross-listed and non-cross-listed firms, rather than differ-ences between cross-listed and U.S. firms (see, for example, Leuz (2006)). Fi-nally, we exclude firms that are reported in the Worldscope database only oncebecause we need at least two consecutive years of nonmissing data on com-pany officers and their titles to compute CEO turnover. The resulting sampleincludes 70,976 firm-year observations of 19,091 firms from 47 countries over1992–2003. Every country in our final sample except Zimbabwe has at least onecross-listed firm in the United States . A breakdown of the sample distributionacross countries, cross-listing status, and years is reported in Table I.

We obtain the list of cross-listed firms using several sources including theBank of New York, Citibank, NYSE, and Nasdaq and verify the listing datesusing Lexis–Nexis searches, Form 20-F, etc. Exchange-traded cross-listings aredenoted as Level 2/3, over-the-counter cross-listings as Level 1, and privateplacements as Rule 144a. The data set also takes into account ADR programupgrades, such as from a Level 1 to a Level 2 program, and delistings fromthe U.S. market. We also include direct listings. Most notably, Canadian firmslist their shares on U.S. exchanges directly without issuing ADRs . Given thatthe increased disclosure and securities law provisions required in listing on amajor U.S. exchange are functionally equivalent for ADRs and direct listings,we classify Canadian firms that are traded on both a Canadian and a majorU.S. exchange as Level 2/3 ADRs. However, the exclusion of Canadian firmsfrom the sample does not change our conclusions.

We follow DeFond and Hung (2004) and use the titles CEO, Chief ExecutiveOfficer, and Chief Executive to identify the top manager in each firm. However,

10 We use a total of 37 Worldscope CDROMs during our sample period. Because of delays byfirms in releasing information and Worldscope’s backfilling procedure, Worldscope indicated to usthat multiple CDROMs from each year should be used as they often contain different numbers offirms.

International Cross-Listing 1903

Table IDescriptive Statistics

This table presents the distribution of the sample used in the regression analysis by country,cross-listing status, and year, and descriptive statistics for the main firm-level variables. Panel Adescribes the number of observations, number of firms, and CEO turnover percentage across coun-tries. Panel B presents the distribution of the sample over time. Panel C displays the distributionof the sample by cross-listing status. Panel D presents the summary statistics for the sample usedin the regression analysis. The last column in Panel D reports the median differences of the firmperformance variables between the CEO turnover and nonturnover observations and the relatedresults from a nonparametric test on the equality of medians. CL dummy is 1 if the firm cross-listsin the United States, 0 otherwise. Level 2/3 dummy is 1 if the firm has a Level 2 or Level 3 ADRprogram, 0 otherwise. Level 1 dummy is 1 if the firm has a Level 1 ADR program, 0 otherwise. Rule144A dummy is 1 if the firm has a Rule 144A issuance, 0 otherwise. Lagged Earnings Ratio is the1-year lagged ratio of earnings before interest and taxes to total assets. Lagged Excess Returns isthe 1-year lagged total stock returns in excess of the country average. Total Assets is measured inmillion $U.S. ∗∗∗ indicates significance at the 1% level.

Panel A: By Country

Country No of Obs. No of Firms CEO Turnover %

Argentina 36 18 25.00Australia 2,463 1,001 15.79Austria 530 160 15.09Belgium 711 187 14.21Brazil 348 155 11.78Canada 3,455 1,011 19.28Chile 473 152 18.39China 276 170 19.57Colombia 3 3 33.33Czech Republic 83 42 15.66Denmark 1,146 283 14.22Finland 766 212 13.71France 3,200 1,019 12.25Germany 3,692 1,047 17.39Greece 517 216 15.28Hong Kong 2,028 797 16.18Hungary 114 36 19.30India 1,268 358 13.17Indonesia 1,090 324 24.13Ireland 418 93 14.83Israel 217 90 21.66Italy 1,192 318 18.04Japan 21,009 3,776 14.15Korea 1,704 675 38.40Luxembourg 59 18 15.25Malaysia 2,185 687 13.27Mexico 304 117 17.76Netherlands 1,034 305 19.05New Zealand 294 90 18.71Norway 356 110 18.82Pakistan 459 111 12.64Peru 87 43 24.14Philippines 674 205 20.47Poland 239 83 19.67

(continued)

1904 The Journal of Finance

Table I—Continued

Panel A: By Country

Country No of Obs. No of Firms CEO Turnover %

Portugal 152 62 9.21Singapore 1,304 429 17.02South Africa 1,210 450 16.28Spain 590 163 16.95Sri Lanka 37 14 8.11Sweden 1,359 420 18.91Switzerland 1,413 360 20.74Taiwan 1,241 423 25.56Thailand 898 269 18.04Turkey 316 124 15.19United Kingdom 9,981 2,448 14.59Venezuela 25 11 4.00Zimbabwe 20 6 25.00

Panel B: By Year

Year No of Obs. No of Firms CEO Turnover %

1992 1,602 – 17.851993 4,081 – 17.741994 4,721 – 13.851995 5,369 – 11.511996 6,083 – 12.941997 6,790 – 13.781998 6,359 – 15.851999 6,893 – 14.842000 6,813 – 23.162001 7,712 – 19.852002 9,962 – 17.512003 4,591 – 14.75

Panel C: By Cross-listing Status

Cross-listing Status No of Obs. No of Firms CEO Turnover %

Non-CL firms 65,563 17,729 16.06CL firms 5,413 1,362 19.18Level 2/3 2,088 609 21.50Level 1 2,494 565 16.92Rule 144A 801 188 20.22

Total 70,976 19,091 16.30

Panel D: Summary Statistics

Turnover vs.5th 95th Nonturnover

N Mean Median Percentile Percentile (Medians)

Lagged Earnings Ratio 70,976 0.218 0.052 −0.133 0.202 −0.006∗∗∗Lagged Excess Returns 62,333 −0.011 −0.079 −0.724 0.909 −0.030∗∗∗Total Assets 70,976 259,278 372.651 15.534 494,872 –

International Cross-Listing 1905

many countries use other titles for top managers, which vary across and withincountries. We use two sources to determine the top manager in the rest of thesample. When available, we use the top manager titles used by DeFond andHung (2004) and Gibson (2003). For example, the titles CEO, Chief ExecutiveOfficer, Chief Executive, and President are used to identify the top managerin Argentina. We exclude firms in which the top manager title is shared bytwo officers to prevent a split turnover (Gibson (2003)). For the remaining 15countries not covered in DeFond and Hung (2004) or Gibson (2003) (4.68% ofour sample), we use press accounts, country experts’ opinions, and manual datainspections of manager titles in each country to determine the top manager title.A list of top manager titles used in each country is displayed in the Appendix.11

After the top manager in the firm is identified, we first compare the last namesand the first letter of first names of top managers of the firm over time todetermine whether there was a top manager replacement in any given year.We next hand-check CEO turnover events for the entire sample given thatDefond and Hung (2004) find that first names of managers do not consistentlyprecede their last names in several Asian countries such as Korea and Japan,and Worldscope infrequently contains typos on executive names for foreignfirms.

As in DeFond and Hung (2004) and Gibson (2003), we do not know whether aCEO turnover event is voluntary (for example, due to retirement) because theWorldscope does not provide information on CEO age and tenure, and mediacoverage in English for the sample firms varies substantially across countries.Hermalin and Weisbach (2003) argue that voluntary turnover is unlikely to berelated to performance, and hence not distinguishing between voluntary andforced turnovers events leads to additional noise in the dependent variable,which only affects standard errors. Consistent with their assertion, the empir-ical evidence suggests a similar or more sensitive relationship between CEOturnover and performance for involuntary (forced) replacements (see, for exam-ple, Huson, Parrino, and Starks (2001), Dahya et al. (2002), and Kaplan andMinton (1994)). Therefore, we do not expect this data limitation to alter ourconclusions.

B. Descriptive Statistics

Panel A of Table I provides summary statistics for the sample based on afirm’s country of domicile. Turnover ranges from a low of 4% in Venezuela toa high of 38.4% in Korea, with an average of 16.30%. For comparison, overour sample period the U.S. turnover rate was 12.86%. Similar to other studiesthat employ the Worldscope database, there is a clustering of observations inJapan and United Kingdom. Although our analysis is based on fixed countryeffects to ensure we are comparing CEO turnover differences within countries,in robustness tests reported later in the paper we remove observations fromJapan and the United Kingdom and find that our conclusions are unaffected.

11 We use the terms CEO turnover and top manager turnover interchangeably.

1906 The Journal of Finance

Panel B of Table I shows turnover by year, which ranges from a low of 11.51% in1995 to a high of 23.16% in 2000. Panel C of Table I presents turnover by cross-listing status. The panel indicates that cross-listed firms have higher CEOturnover than non-cross-listed firms (19.18% vs. 16.06%). Of the cross-listedfirms, CEO turnover is greatest for Level 2/3 firms, followed by Rule 144a andthen Level 1 companies (21.50%, 16.92%, and 20.22%, respectively). Panel Cof Table I also shows that 1,362 foreign firms are identified as cross-listed inour sample, of which 609 are exchange-traded cross-listings (Level 2/3), 565are OTC cross-listings (Level 1), and 188 are private placements via Rule 144Aissuance (Rule 144a).

We consider various measures of firm performance, including both operat-ing performance measures and stock-price-based measures. We augment stockprice data from Worldscope with data from Datastream International wherepossible. However, we expect the operating performance measures to be a bet-ter proxy in our international setting, as both Volpin (2002) and DeFond andHung (2004) find that stock returns are not related to CEO turnover in coun-tries whose markets are characterized by high stock-price synchronicity andilliquidity, attributes that make stock-price-based measures less informative.12

For our main tests, we focus on the ratio of accounting earnings before inter-est and taxes (EBIT) to book value of assets (earnings ratio), and the total stockreturns in excess of the country average (excess returns). We follow DeFond andHung (2004) and Volpin (2002) and use EBIT among accounting-based firmperformance measures because it is not influenced by firms’ capital structurepolicies or by differential country-level tax regimes. Similar forms of both vari-ables are used extensively to proxy for firm performance in studies examiningthe sensitivity of CEO turnover to firm performance.13 We lag both performancevariables by 1 year to prevent a possible overlap of the replaced CEO’s perfor-mance with that of the new CEO. Panel D of Table 1 reports sample statisticsof the main performance measures and shows that the lagged performancemeasures are significantly lower in firm-years with CEO turnover than in non-turnover years. In terms of the depth of the sample, the mean (median) numberof years a firm is in our regression analysis is 3.84 (3) years.

We also use sales growth and the change in EBIT to total assets as alterna-tive accounting-based measures of firm performance and obtain qualitativelysimilar results. In addition, we recompute our firm performance measures inwhich industry-adjusted performance is calculated as firm performance minusthe median value of the corresponding two-digit SIC global industry and obtainsimilar results.

12 Harvey (1995) shows that first-order autocorrelations in emerging markets are positive andsignificant and Lesmond (2005) finds that liquidity-related transactions costs in countries withweak legal institutions are higher than in markets with strong legal systems.

13 See Huson et al. (2001), Mikkelson and Partch (1997), Gibson (2003), and Kang and Shivdasani(1995) for the accounting-based measure and Weisbach (1988), Kang and Shivdasani (1995), Defondand Hung (2004), Huson, Parrino, and Starks (2001), and Hadlock and Lumer (1997) for the stock-market-based measure.

International Cross-Listing 1907

III. Research Design

A. Empirical Model

To test our hypothesis that CEO turnover is more sensitive to poor perfor-mance for exchange-traded cross-listed firms than non-cross-listed firms, weestimate a series of probit models that take the form:

Pr (Turnover) = φ[α + β1(FirmPerformance)] + β2(L23)

+ β12(L23∗FirmPerformance) + β3(L1)

+ β13(L1∗FirmPerformance) + β4(R144A)

+ β14(R144A∗FirmPerformance) + δX ] (1)

where φ is the standard normal cumulative distribution, L23 refers to exchange-traded cross-listings, L1 refers to OTC cross-listings, R144A refers to privateplacements, and X is a set of firm control variables, country controls, industrycontrols, and year controls. Note that the cross-listed dummies are time-varyingin that they take the value of 1 in the cross-listing year and can switch back to0 if the firm delists or changes level of cross-listing.

We follow previous research and measure turnover as a binary variable thattakes the value 1 if the top manager is changed in that year. We include firmsize measured as the natural logarithm of the book value of total assets inmillions of U.S. dollars. In the regression analysis, we winsorize the continuousvariables at the 1% level for each country.

It is also important to note that throughout our analysis, we include coun-try fixed effects that ensure we are measuring within-country differencesbetween cross-listed and non-cross-listed firms as well as controlling for un-observed country effects. In addition, we include industry dummies using thetwo-digit SIC code to control for global industry-wide factors that may affectCEO turnover and firm performance. Finally, our regressions include indica-tor variables for each year. Our regressions also correct the standard errorsfor possible serial correlation and heteroskedasticity by clustering at the firmlevel.

We test our second hypothesis, which posits that the difference in the sensitiv-ity of top management turnover to performance between cross-listed firms andnon-cross-listed firms is greatest in the countries with the weakest corporategovernance, by classifying countries into strong and weak investor protectionregimes and comparing coefficients across samples. Alternatively, a randomcountry effects specification could be employed with interaction effects, but inour sample this is inappropriate as it fails the Hausman specification test. Wefocus on three country-level measures of investor protection. The first measure,from La Porta, Lopez-De-Silanes, Shleifer, and Vishny (LLSV) (1997, 1998), iswhether the home country has an English legal origin, which is an overallmeasure of strong investor protections. Following Djankov et al. (2005) we usethe anti-director rights index (ADRI), which is a revised version of the originalADRI index from LLSV (1997) that addresses the coding concerns expressed

1908 The Journal of Finance

in Pagano and Volpin (2005) and Spamann (2006). The ADRI represents thedegree of minority shareholder protection. We also use the anti-self-dealingindex from Djankov et al. (2005), which measures how difficult it is for minor-ity shareholders to thwart the consumption of private benefits by controllingshareholders. Djankov et al. (2005) argue that self-dealing is the central prob-lem of corporate governance in most countries. In unreported tests, we alsoexamine other country-level measures of investor protection from LLSV (1998)and La Porta, Lopez-De-Silanes, and Shleifer (LLS) (2006), such as the ruleof law, burden of proof, disclosure, and private law enforcement indexes. In allinstances, our results are consistent across every measure of high versus lowinvestor protection. Further, the results are robust to using Spamann’s (2006)ADRI.

B. Interpretation of Interactions in Probit Models

Recent research by Ai and Norton (2003) and Powers (2005) emphasizes thedifficulty present in interpreting interactions in nonlinear models. Strikingly,the interaction effect cannot be evaluated by looking at the sign, magnitude, orstatistical significance of the coefficient on the conventional interaction term.Ai and Norton (2003) show that the interaction effect is conditional on the inde-pendent variable, and therefore both the magnitude and statistical significanceof the interaction term can vary across observations. For example, in our probitspecification the correct marginal effect of a change in the interaction variablebetween the L23 dummy and firm performance is

�∂F (u)

∂FirmPerformance�L23

= (β1 + β12) ∗ φ[(β1 + β12) ∗ FirmPerformance + β2 + X δ]

− β1 ∗ φ [β1 ∗ FirmPerformance + δX ] (2)

where F (u) = Pr(Turnover), which is given by equation (1) and u denotes theregression specification. Equation (2) shows that the marginal effect of theinteraction variable may not be zero even when β12 is zero. Thus, the standardcoefficient on the interaction term may have an incorrect magnitude, standarderror, and even sign relative to the true interaction effect.

To ensure our inferences are correct, we use the methodology developedby Norton, Wang, and Ai (2004) to compute the correct marginal effect of achange in the interaction variable between the respective cross-listed dummyand firm performance. We report both the marginal effects and their standarderrors and display the graphs of the distribution of marginal effects and theassociated z-statistics over the entire range of predicted probabilities for ourmain models. In tests where our inferences are unambiguous, we also sum-marize the range of corrected interactions by the mean interaction effect andits significance.

International Cross-Listing 1909

IV. The Effect of Cross-Listing on CEO Turnover

A. By Cross-Listing Type

Table II presents a series of probit regressions that include interactionsbetween firm performance and cross-listing type to test the hypothesis thatcross-listed firms have a higher performance to turnover sensitivity than non-cross-listed firms. Model 1 reports the results for the accounting-based per-formance measure and Model 2 presents the results for the stock-price-basedperformance measure. All regression models include country, industry, and yearfixed effects as well as control for firm size.

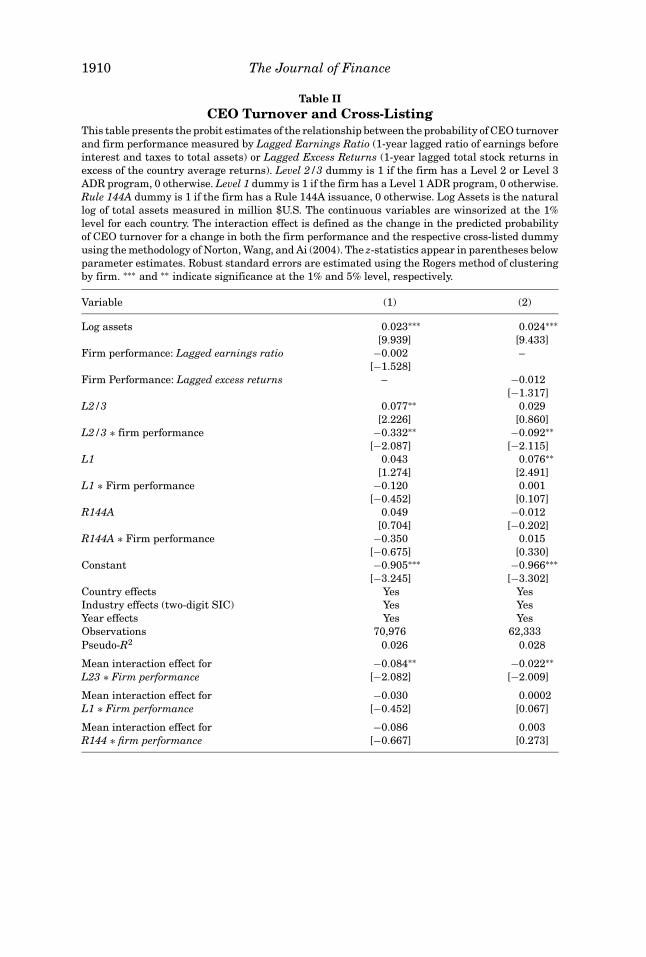

Model 1 shows that the interaction between Level 2/3 and lagged earningsratio is negative and significant (−0.332, t-statistic = −2.087). In contrast,OTC or Rule 144a cross-listings do not have a significantly higher propensityto terminate poorly performing CEOs than non-cross-listed firms’ interaction(coefficient = −0.120, t-statistic = −0.452 and −0.350, t-statistic = −0.675, re-spectively). This finding is consistent with the hypothesis that non-U.S. firmsadopting the strongest governance and reporting requirements by cross-listingin the United States observe outcomes consistent with improved governanceover similar firms that are not cross-listed in the United States. However,given the aforementioned problems with interpreting simple interaction termsin discrete choice models, we follow Ai and Norton (2003) and evaluate the cor-rected marginal effects and their significance at every predicted probability.Figure 1a shows that for major exchange-traded cross-listings, the correctedinteraction effects are overwhelmingly negative across the predicted probabil-ities, while Figure 1b shows that these interaction effects are also significant(less than −1.96) for most probabilities. We summarize the corrected inter-active effect and its significance in the last row of Table II by reporting themean interaction effect and its significance (−0.084, t-statistic = −2.082). Interms of economic significance, the absolute probability of replacing the CEOincreases by 1.34% for Level 2/3 ADRs when we move from the top quartileto the bottom quartile of firm performance. For OTC (Rule144a) cross-listings,the corrected interactive effects, presented in Figures 1c–f and summarizedin the bottom rows of Table II, further confirm that the interaction effectis rarely significant across the range of predicted probabilities (the mean-corrected effect is −0.030, t-statistic = −0.452, and −0.086, t-statistic = −0.667,respectively).

For the control variables, we find that firm size is positively related to CEOturnover.14 Firm performance (lagged earnings ratio) is negative yet statisti-cally insignificant, a finding that is the result of pooling countries where firmperformance is unlikely to be used to evaluate management.15 The coefficienton L2/3 is positive, indicating that exchange cross-listed firms also have higher

14 In the United States, size is generally thought to capture the effects of CEO and institutionalstock ownership, board composition, managerial depth, and formal succession processes (see, e.g.,Huson et al. (2001)). Gibson (2003) and DeFond and Hung (2004) also find that firm size is positivelyrelated to CEO turnover internationally.

15 When we split by investor protection regimes, the coefficient on lagged earning ratio is negativeand significant in high protection countries.

1910 The Journal of Finance

Table IICEO Turnover and Cross-Listing

This table presents the probit estimates of the relationship between the probability of CEO turnoverand firm performance measured by Lagged Earnings Ratio (1-year lagged ratio of earnings beforeinterest and taxes to total assets) or Lagged Excess Returns (1-year lagged total stock returns inexcess of the country average returns). Level 2/3 dummy is 1 if the firm has a Level 2 or Level 3ADR program, 0 otherwise. Level 1 dummy is 1 if the firm has a Level 1 ADR program, 0 otherwise.Rule 144A dummy is 1 if the firm has a Rule 144A issuance, 0 otherwise. Log Assets is the naturallog of total assets measured in million $U.S. The continuous variables are winsorized at the 1%level for each country. The interaction effect is defined as the change in the predicted probabilityof CEO turnover for a change in both the firm performance and the respective cross-listed dummyusing the methodology of Norton, Wang, and Ai (2004). The z-statistics appear in parentheses belowparameter estimates. Robust standard errors are estimated using the Rogers method of clusteringby firm. ∗∗∗ and ∗∗ indicate significance at the 1% and 5% level, respectively.

Variable (1) (2)

Log assets 0.023∗∗∗ 0.024∗∗∗[9.939] [9.433]

Firm performance: Lagged earnings ratio −0.002 –[−1.528]

Firm Performance: Lagged excess returns – −0.012[−1.317]

L2/3 0.077∗∗ 0.029[2.226] [0.860]

L2/3 ∗ firm performance −0.332∗∗ −0.092∗∗[−2.087] [−2.115]

L1 0.043 0.076∗∗[1.274] [2.491]

L1 ∗ Firm performance −0.120 0.001[−0.452] [0.107]

R144A 0.049 −0.012[0.704] [−0.202]

R144A ∗ Firm performance −0.350 0.015[−0.675] [0.330]

Constant −0.905∗∗∗ −0.966∗∗∗[−3.245] [−3.302]

Country effects Yes YesIndustry effects (two-digit SIC) Yes YesYear effects Yes YesObservations 70,976 62,333Pseudo-R2 0.026 0.028

Mean interaction effect for −0.084∗∗ −0.022∗∗L23 ∗ Firm performance [−2.082] [−2.009]

Mean interaction effect for −0.030 0.0002L1 ∗ Firm performance [−0.452] [0.067]

Mean interaction effect for −0.086 0.003R144 ∗ firm performance [−0.667] [0.273]

International Cross-Listing 1911

Figure 1. The economic significance of the impact of cross-listing on the relationshipbetween CEO turnover and firm performance. The following graphs display the interactioneffects and corresponding z-statistics on the interaction variable between the respective cross-listeddummy and firm performance measure reported in Table II, estimated using Norton, Wang, and Ai(2004). The interaction effect is defined as the change in the predicted probability of CEO turnoverfor a change in both firm performance and the respective cross-listed dummy. Panel A plots thegraphs associated with the lagged earnings ratio measure and Panel B depicts the graphs for thelagged excess returns measure. The lines above and below 0 on the figures located on the right siderepresent the 5% significance levels (±1.96).

1912 The Journal of Finance

Figure 1—Continued.

absolute turnover, a result that is primarily driven by firms from the UnitedKingdom.16

Model 2 of Table II examines the sensitivity of CEO turnover to performanceemploying our alternative firm performance measure, 1-year lagged excess

16 Dahya et al. (2002) show that after the Cadbury Act was passed in 1992, CEO turnoverincreased for U.K. firms.

International Cross-Listing 1913

stock market returns. We find that the interaction between L2/3 and stock-price-based performance is negative and significant, while the interactions be-tween L1 or R144a and stock-price-based performance are insignificant. There-fore, with this alternative performance measure we continue to find that cross-listed firms that are associated with the most stringent U.S. investor protectionsare more likely to terminate poorly performing CEOs.

Overall, the results contained in Table II provide support for the hypothesisthat cross-listing on a major U.S. exchange, which requires the adoption of strin-gent U.S. investor protection laws, results in a significantly higher propensityto terminate poorly performing CEOs than their non-cross-listed counterparts.In addition, firms that cross-list via Level 1 or Rule 144a ADRs do not have anincreased association between CEO turnover and poor firm performance.

In untabulated results, we also split our sample into countries with highand low stock-price informativeness to examine if the CEO turnover to per-formance sensitivity is higher in countries where stock prices are more infor-mative about firm-specific performance. Prior research by DeFond and Hung(2004) and Volpin (2002) argues that only in countries where stock prices areinformative is CEO turnover related to stock market performance.17 However,it is important to note that a significant relation between CEO turnover andperformance in low informativeness countries is possible if stock prices be-come more informative about performance due to cross-listing, something thatFernandes and Ferreira (2006) and Dasgupta, Gan, Ning, (2005) suggest oc-curs. Consistent with DeFond and Hung (2004) and Volpin (2002), we find thatthe interaction between cross-listing types and firm performance is insignif-icant in countries that have below-median stock-price informativeness, whilein countries where stock prices are informative, cross-listing on a major U.S.exchange results in a higher propensity to shed poorly performing CEOs. Theseresults also suggest that the increased CEO turnover to performance sensitiv-ity for cross-listed firms is not driven purely by stock prices becoming moreinformative for cross-listed firms in certain countries.

Overall, the results in Table II provide support for the bonding hypothesis.We find that cross-listed firms have outcomes that are consistent with bettercorporate governance systems than similar non-cross-listed firms. Further, thefindings suggest that governance outcome differences are only significant forthose firms that adopt the strongest U.S. investor protections by listing on amajor U.S. exchange, rather than an OTC listing or private placement. Theseresults provide support for the hypothesis that by cross-listing in the UnitedStates, firms are able to opt-in to superior corporate governance.

B. The Strength of Bonding for Firms in Low Investor Protection Countries

Table III tests the third prediction of the bonding hypothesis that the ef-fect of bonding will be greatest for firms domiciled in the countries with theweakest investor protections. We test this hypothesis by splitting the sample

17 Bushman, Piotroski, and Smith (2004) show that corporate transparency is low in poor investorprotection countries.

1914 The Journal of Finance

Tab

leII

IC

EO

Tu

rnov

er,C

ross

-Lis

tin

g,an

dL

egal

En

viro

nm

ent

Th

ista

ble

pres

ents

the

prob

ites

tim

ates

ofth

ere

lati

onsh

ipbe

twee

nth

epr

obab

ilit

yof

CE

Otu

rnov

eran

dfi

rmpe

rfor

man

ceu

nde

rva

riou

sm

easu

res

ofa

cou

ntr

y’s

lega

len

viro

nm

ent.

Fir

mpe

rfor

man

ceis

mea

sure

dby

Lag

ged

Ear

nin

gsR

atio

,wh

ich

isth

e1-

year

lagg

edra

tio

ofea

rnin

gsbe

fore

inte

rest

and

taxe

sto

tota

lass

ets,

orL

agge

dE

xces

sR

etu

rns,

wh

ich

isth

e1-

year

lagg

edto

tals

tock

retu

rns

inex

cess

ofth

eco

un

try

aver

age

retu

rns.

Th

eC

ivil

Law

sam

ple

incl

ude

sfi

rms

loca

ted

inco

un

trie

sw

ith

aF

ren

ch,

Ger

man

,or

Sca

ndi

nav

ian

lega

lsy

stem

.T

he

Com

mon

Law

sam

ple

refe

rsto

firm

slo

cate

din

cou

ntr

ies

wit

hth

eE

ngl

ish

lega

lori

gin

.An

ti-d

irec

tor

righ

tsin

dex

mea

sure

sth

ede

gree

ofm

inor

ity

shar

ehol

der

prot

ecti

on.A

nti

-sel

f-de

alin

gis

anin

dex

ofth

est

ren

gth

ofm

inor

ity

shar

ehol

der

prot

ecti

onag

ain

stse

lf-d

eali

ng

byth

eco

ntr

olli

ng

shar

ehol

der.

All

thes

eco

un

try-

leve

lin

dice

sar

eob

tain

edfr

omD

jan

kov

etal

.(20

05).

Th

em

edia

ns

of3.

5fo

ran

ti-d

irec

tor

righ

tsan

d0.

42fo

ran

tise

lf-d

eali

ng

inde

xu

sed

inD

jan

kov

etal

.(20

05)

are

use

dto

grou

pfi

rms

into

hig

hve

rsu

slo

win

vest

orpr

otec

tion

regi

mes

(low

erth

anor

equ

alto

the

med

ian

refe

rsto

low

gove

rnan

cesu

bsam

ples

).L

evel

2/3

dum

my

is1

ifth

efi

rmh

asa

Lev

el2

orL

evel

3A

DR

prog

ram

,0ot

her

wis

e.L

evel

1du

mm

yis

1if

the

firm

has

aL

evel

1A

DR

prog

ram

,0ot

her

wis

e.R

ule

144A

dum

my

is1

ifth

efi

rmh

asa

Ru

le14

4Ais

suan

ce,0

oth

erw

ise.

Log

Ass

ets

isth

en

atu

rall

ogof

tota

lass

ets

mea

sure

din

mil

lion

$U.S

.Th

eco

nti

nu

ous

vari

able

sar

ew

inso

rize

dat

the

1%le

velf

orea

chco

un

try.

Th

ein

tera

ctio

nef

fect

isde

fin

edas

the

chan

gein

the

pred

icte

dpr

obab

ilit

yof

CE

Otu

rnov

erfo

ra

chan

gein

both

the

firm

perf

orm

ance

and

the

resp

ecti

vecr

oss-

list

eddu

mm

yu

sin

gth

em

eth

odol

ogy

ofN

orto

n,W

ang,

and

Ai(

2004

).T

he

z-st

atis

tics

appe

arin

pare

nth

eses

belo

wpa

ram

eter

esti

mat

es.R

obu

stst

anda

rder

rors

are

esti

mat

edu

sin

gth

eR

oger

sm

eth

odof

clu

ster

ing

byfi

rm.

∗∗∗

and

∗∗in

dica

tesi

gnif

ican

ceat

the

1%an

d5%

leve

l,re

spec

tive

ly.

Pan

elA

:On

e-Ye

arL

agge

dE

arn

ings

Rat

io

Low

An

ti-

Hig

hA

nti

-L

owA

nti

-H

igh

An

ti-

Civ

ilC

omm

onD

irec

tor

Dir

ecto

rS

elf-

Sel

f-L

awL

awR

igh

tsR

igh

tsD

eali

ng

Hig

hD

eali

ng

Var

iabl

e(1

)(2

)(3

)(4

)(5

)(6

)

Fir

m,c

oun

try,

indu

stry

,yea

rco

ntr

ols

Yes

Yes

Yes

Yes

Yes

Yes

Obs

erva

tion

s44

,735

26,2

3741

,007

29,9

6715

,936

55,0

20P

seu

do-R

20.

033

0.02

20.

034

0.02

30.

031

0.02

9M

ean

inte

ract

ion

effe

ctfo

r−0

.341

∗∗∗

0.01

9−0

.333

∗∗∗

0.01

8−0

.328

∗∗∗

−0.0

45L

23∗l

agge

dea

rnin

gsra

tio

[−3.

435]

[0.4

18]

[−3.

339]

[0.3

86]

[−3.

121]

[−1.

023]

Mea

nin

tera

ctio

nef

fect

for

−0.1

120.

040

−0.1

0400

38−0

.023

−0.0

31L

1∗l

agge

dea

rnin

gsra

tio

[−0.

850]

[0.5

40]

[−0.

763]

[0.5

19]

[−0.

154]

[−0.

440]

Mea

nin

tera

ctio

nef

fect

for

−0.1

640.

129

−0.1

830.

058

−0.1

21−0

.076

R14

4∗l

agge

dea

rnin

gsra

tio

[−1.

071]

[0.5

02]

[−0.

975]

[0.3

31]

[−0.

535]

[−0.

497]

International Cross-Listing 1915

Pan

elB

:On

e-Ye

arL

agge

dE

xces

sR

etu

rns

Low

An

ti-

Hig

hA

nti

-L

owA

nti

-H

igh

An

ti-

Civ

ilC

omm

onD

irec

tor

Dir

ecto

rS

elf-

Sel

f-L

awL

awR

igh

tsR

igh

tsD

eali

ng

Hig

hD

eali

ng

Var

iabl

e(1

)(2

)(3

)(4

)(5

)(6

)

Fir

m,c

oun

try,

indu

stry

,yea

rco

ntr

ols

Yes

Yes

Yes

Yes

Yes

Yes

Obs

erva

tion

s39

,809

22,5

1936

,552

25,7

7113

,455

48,8

54P

seu

do-R

20.

033

0.02

30.

034

0.02

40.

032

0.03

0M

ean

inte

ract

ion

effe

ctfo

r−0

.044

∗∗∗

0.01

3−0

.054

∗∗0.

007

−0.0

35∗∗

−0.0

09L

23∗l

agge

dex

cess

retu

rns

[−3.

256]

[0.8

01]

[−2.

077]

[0.5

00]

[−2.

492]

[−0.

655]

Mea

nin

tera

ctio

nef

fect

for

0.00

040.

002

−0.0

090.

003

−0.0

002

−0.0

03L

1∗l

agge

dex

cess

retu

rns

[0.1

48]

[0.1

10]

[−0.

250]

[0.7

51]

[−0.

077]

[−0.

200]

Mea

nin

tera

ctio

nef

fect

for

−0.0

002

0.02

60.

004

0.00

4−0

.004

0.01

4R

144

∗lag

ged

exce

ssre

turn

s[−

0.01

5][0

.931

][0

.267

][0

.250

][−

0.25

3][1

.148

]

1916 The Journal of Finance

by investor protection regimes and examining the interactions between cross-listing types and firm performance, for both accounting- and stock-market-based performance measures (Panels A and B, respectively). Firm, country,industry, and year controls are included in all regressions.

The first two columns in Panel A of Table III split the sample by legal origin, aclassification that proxies for the overall protection of minority shareholders ina country (see, for example, LLSV (1998)). Model 1 shows that in countries withCivil Law tradition, where investor protection is weakest, the corrected interac-tion between Level 2/3 and Lagged Earnings Ratio is negative and significant(−0.341, t-statistic = −3.435). Model 1 also shows that the corrected interac-tions between firm performance and L1 or R144a are insignificant (−0.112,t-statistic = −0.850, and −0.164, t-statistic = −1.071, respectively). Therefore,in countries with poor investor protections, cross-listing on a major U.S. ex-change is associated with an increased CEO turnover to poor firm performancesensitivity. In terms of economic significance, the probability of replacing theCEO increases by 4.36% in absolute terms for Level 2/3 ADRs when we movefrom the top quartile to the bottom quartile of firm performance measured inCivil Law countries.18

Model 2 of Panel A presents the results for Common Law countries, whereinvestor protection is strongest. In these countries, we find that all the interac-tions between cross-listing type and the Lagged Earnings Ratio are statisticallyinsignificant. Further, the difference in the interaction terms between Civil andCommon Law countries is significant (p-value of lower than 0.01). Therefore,the results indicate that the effect of U.S. investor protections is most signifi-cant when the firm’s home country investor protections are weakest. Althoughnot reported, we find that the Lagged Earnings Ratio coefficient is negative andsignificant, which is consistent with previous research that finds accounting-based performance is used for managerial performance evaluation.

To further test if the extent of bonding is dependent on the category of pro-tections investors are afforded in a particular country, we also investigate al-ternative investor protection indices from Djankov et al. (2005). Models 3 and5 report results for countries classified as having weak protection of minorityshareholders and poor safeguards against corporate tunneling. In both models,we find the interactions (both standard and corrected) between Level 2/3 andLagged Earnings Ratio are negative and significant, indicating that in theselow investor protection countries, cross-listing on a major U.S. exchange is as-sociated with increased CEO turnover to poor firm performance sensitivity.Models 4 and 6 report results for the strong investor protection countries. Inboth these models, the interactions between cross-listing type (Level 2/3, L1, orR144a) are insignificant, indicating no difference in the CEO turnover to firmperformance relation in countries that have strong investor protection.19

18 For comparison, Huson et al. (2001) show that going from the top quartile to the lowest quartilein EBIT/TA ratio increases the probability of CEO turnover by 2%.

19 Using alternative measures of investor protection laws from LLS (2006) and LLSV (1998),such as the burden of proof, investor protection, private law enforcement, disclosure, and ruleof law indexes, produces similar conclusions. Further, the results are robust to using Spamann’s(2006) ADRI.

International Cross-Listing 1917

Panel B provides the results for the stock-price-based firm performance mea-sure. As in Panel A, we find across all weak investor protection subsamples,the interaction between firm performance and Level 2/3 is negative and signifi-cant. For example, the mean-corrected interactive effect in Civil Law countriesis −0.044 (t-statistic = −3.256). For other cross-listing types, the interactioncoefficients are insignificant. Further, Models 2, 4, and 6 show that in stronginvestor protection countries, cross-listing does not increase the sensitivity ofCEO turnover to poor firm performance.

Taken together, the results in Table III show that in countries where investorprotections are weakest, adopting the strongest U.S. investor protection provi-sions results in significantly greater propensity to terminate poorly performingCEOs, while in countries that already have strong investor protections, cross-listing does not change the CEO turnover to performance sensitivity. Further,the results show that in weak investor protection countries, only cross-listingsthat require the most stringent of U.S. investor protections (exchange-listedcross-listings) are associated with better governance outcomes. Therefore, theresults provide support for the second and third main predictions of the bondinghypothesis.

C. Sensitivity of CEO Turnover to Performance in the Pre-Cross-Listing Period

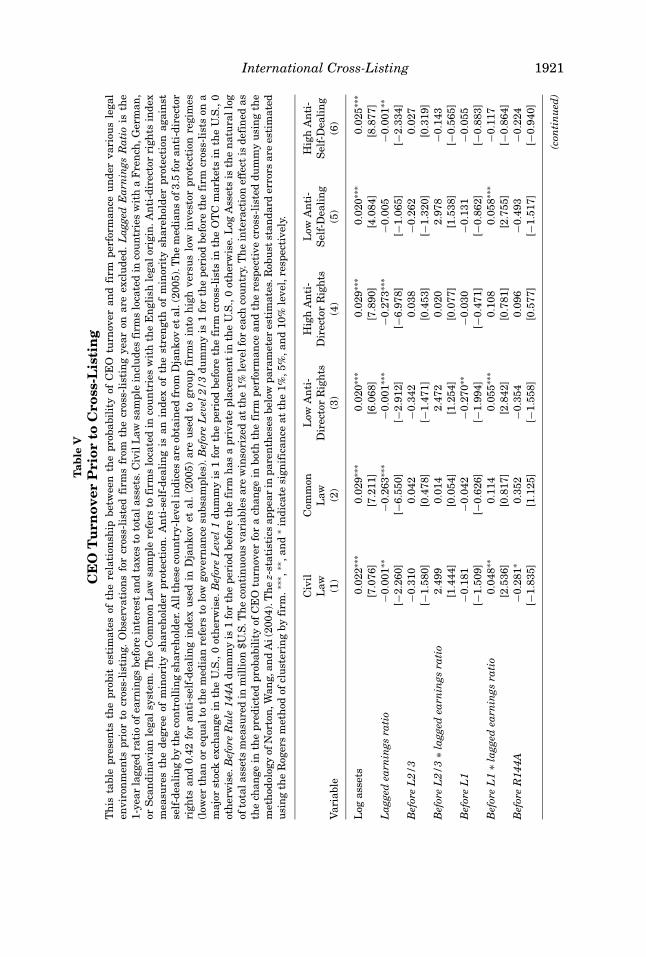

The previous analysis establishes that cross-listed firms on major U.S. ex-changes have outcomes that are consistent with improved corporate gover-nance over non-cross-listed firms. In this analysis, the comparison group isall non-cross-listed firms, which includes firms that may never cross-list aswell as cross-listed firms in their pre-cross-listing period. However, an alterna-tive explanation for our findings is that only the better-governed firms chooseto cross-list on a major U.S. exchange, which would drive our results. Whileour previous tests employed time-varying cross-listing indicator variables thatequal one only after the firm cross-listed, we further examine this issue byperforming two additional tests in which we examine the sensitivity of CEOturnover to performance in the pre-cross-listing period.

In the first test, we examine how the sensitivity of CEO turnover to firmperformance differs before and after cross-listing, where we restrict the sam-ple to firms that will have a cross-listing of the same type during our sampleperiod.20 The advantage of this experiment is that the non-cross-listed compari-son group consists of firms that will have a cross-listing of a similar type duringthe sample period (that is, the pre-cross-listing period of the cross-listed firms).If firms that pursue exchange-traded cross-listings have better governanceprior to cross-listing, then we would expect to find little difference betweencross-listed firms and “to-be” cross-listed firms. Due to space considerations,in this test we focus on the broad Civil versus Common Law classificationsusing the lagged earnings ratio performance measure, but other governance

20 We also examine the comparison groups together with indicator variables for cross-listingtypes (i.e., Level 2/3, Level 1, and Rule144a dummies together) and obtain similar results.

1918 The Journal of Finance

classifications and performance measures produce consistent results.21 Model1 in Table IV shows that the sensitivity of turnover to performance for exchange-traded cross-listings is significantly larger than that for non-cross-listed firmsthat will eventually cross-list on a major exchange in low shareholder protec-tion countries. Therefore, the results suggest that the difference in governanceoutcomes is driven by the post-cross-listing period of cross-listed firms. Thecoefficient on L2/3 also shows that these firms have higher absolute turnoverafter cross-listing. For Level 1 and Rule 144a cross-listings, the interactionsbetween cross-listing type and firm performance are not significantly differentbetween cross-listed and non-cross-listed firms.

The second way we test if the pre-cross-listing governance of our samplefirms is driving our results is to exclude all observations for cross-listed firmsfollowing the cross-listing year and compare the interactions of “to-be” cross-listed firms’ performance to the full sample of non-cross-listed firms. If the pre-cross-listing status of cross-listed firms is driving our results, we might expectto see results in this analysis similar to our full sample tests presented earlier.An advantage of this test is that we are able to use the full sample of non-cross-listed firms. The disadvantage is that there are relatively few observations inthe prelisting period, which is likely to lower the power of the test. Table V showsthat when the post-cross-listing observations are excluded, we no longer findthat cross-listed firms are more likely to terminate poorly performing CEOs.22

We also find in Table V that Before L1 ∗ Lagged Earnings Ratio is positiveand significant, which suggests these firms see an improvement from a verylow level of corporate governance, where well-performing managers are morelikely to leave, to a low level where there is no relation between turnover andperformance.

Overall, the results in Tables IV and V show that when compared to theirpre-cross-listing status, cross-listing on a major U.S. exchange results in sig-nificantly higher CEO turnover to firm performance sensitivity. Therefore, theresults indicate that it is not the pre-cross-listing governance of firms that isdriving the results. Taken together, the evidence in the preceding sections sug-gests that in countries with poor investor protections, cross-listing on a majorU.S. exchange increases the likelihood that firms will have outcomes consistentwith improved corporate governance systems.

D. London Listings

Listing in London is an often-cited alternative for firms that do not wish tosubject themselves to the stringent listing requirements in the United States.23

21 For example, using the excess returns measure, the interaction between performance andLevel 2/3 is also statistically significant (insignificant) in Civil (Common) Law, weak (strong) anti-director rights, and low (high) anti-self-dealing subsamples.

22 We also estimate a two-stage model for self-selection that controls for the decision to list inthe first stage and find that our results are robust to this specification.

23 See, for example, “London Calling” in Forbes Magazine May 8, 2006.

International Cross-Listing 1919

Tab

leIV

CE

OT

urn

over

and

Cro

ss-L

isti

ng:

Fir

ms

wit

ha

Cro

ss-L

isti

ng

ofth

eS

ame

Typ

eT

his

tabl

epr

esen

tsth

epr

obit

esti

mat

esof

the

rela

tion

ship

betw

een

the

prob

abil

ity

ofC

EO

turn

over

and

firm

perf

orm

ance

for

firm

sth

ath

ave

orw

ill

hav

ea

sim

ilar

type

ofA

DR

prog

ram

duri

ng

the

sam

ple

peri

od.T

he

sam

ple

inco

lum

ns

1–2

isli

mit

edto

firm

sth

ath

ave

orw

illh

ave

list

edon

am

ajor

U.S

.exc

han

gedu

rin

gou

rsa

mpl

epe

riod

.Sim

ilar

ly,t

he

sam

ples

inco

lum

ns

3–4

and

5–6

rest

rict

the

sam

ple

tofi

rms

that

list

onth

eO

TC

mar

ket

and

issu

epr

ivat

epl

acem

ents

via

Ru

le14

4aan

ytim

edu

rin

gou

rsa

mpl

epe

riod

,res

pect

ivel

y.L

agge

dE

arn

ings

Rat

iois

the

1-ye

arla

gged

rati

oof

earn

ings

befo

rein

tere

stan

dta

xes

toto

tal

asse

ts.

Th

eC

ivil

Law

sam

ple

incl

ude

sfi

rms

loca

ted

inco

un

trie

sw

ith

aF

ren

ch,

Ger

man

,or

Sca

ndi

nav

ian

lega

lsy

stem

.Th

eC

omm

onL

awsa

mpl

ere

fers

tofi

rms

loca

ted

inco

un

trie

sw

ith

the

En

glis

hle

galo

rigi

n.T

his

clas

sifi

cati

onof

lega

lreg

imes

isob

tain

edfr

omD

jan

kov

etal

.(20

05).

Lev

el2/

3du

mm

yis

1if

the

firm

has

aL

evel

2or

Lev

el3

AD

Rpr

ogra

m,0

oth

erw

ise.

Lev

el1

dum

my

is1

ifth

efi

rmh

asa

Lev

el1

AD

Rpr

ogra

m,0

oth

erw

ise.

Ru

le14

4Adu

mm

yis

1if

the

firm

has

aR

ule

144A

issu

ance

,0ot

her

wis

e.L

ogA

sset

sis

the

nat

ura

llo

gof

tota

las

sets

mea

sure

din

mil

lion

$U.S

.Th

eco

nti

nu

ous

vari

able

sar

ew

inso

rize

dat

the

1%le

velf

orea

chco

un

try.

Th

ein

tera

ctio

nef

fect

isde

fin

edas

the

chan

gein

the

pred

icte

dpr

obab

ilit

yof

CE

Otu

rnov

erfo

ra

chan

gein

both

the

firm

perf

orm

ance

and

the

resp

ecti

vecr

oss-

list

eddu

mm

yu

sin

gth

em

eth

odol

ogy

ofN

orto

n,W

ang,

and

Ai

(200

4).T

he

z-st

atis

tics

appe

arin

pare

nth

eses

belo

wpa

ram

eter

esti

mat

es.R

obu

stst

anda

rder

rors

are

esti

mat

edu

sin

gth

eR

oger

sm

eth

odof

clu

ster

ing

byfi

rm.∗

∗∗,∗

∗ ,an

d∗

indi

cate

sign

ific

ance

atth

e1%

,5%

,an

d10

%le

vel,

resp

ecti

vely

.

Exc

han

ge-T

rade

dA

DR

sO

TC

-Tra

ded

AD

Rs

Pri

vate

Pla

cem

ents

Civ

ilL

awC

omm

onL

awC

ivil

Law

Com

mon

Law

Civ

ilL

awC

omm

onL

awV

aria

ble

(1)

(2)

(3)

(4)

(5)

(6)

Log

asse

ts−0

.011

0.02

8∗−0

.006

0.01

30.

148∗

∗∗0.

122∗

∗[−

0.48

1][1

.770

][0

.299

][0

.769

][3

.028

][2

.299

]L

agge

dea

rnin

gsra

tio

1.40

5−0

.134

−0.0

27−0

.122

−0.8

88−2

.495

[0.9

64]

[−0.

509]

[−0.

837]

[−0.

829]

[−0.

705]

[−0.

668]

L2/

30.

631∗

∗∗0.

021

––

––

[3.2

19]

[0.2

03]

L2/

3∗l

agge

dea

rnin

gsra

tio

−2.8

52∗

0.02

1–

––

–[−

1.90

3][0

.067

]L

1–

–0.

194

−0.0

63–

–[1

.547

][−

0.56

7]L

1∗l

agge

dea

rnin

gsra

tio

––

−0.2

660.

094

––

[−0.

449]

[0.2

50]

(con

tin

ued

)

1920 The Journal of Finance

Tab

leIV

—C

onti

nu

ed

Exc

han

ge-T

rade

dA

DR

sO

TC

-Tra

ded

AD

Rs

Pri

vate

Pla

cem

ents

Civ

ilL

awC

omm

onL

awC

ivil

Law

Com

mon

Law

Civ

ilL

awC

omm

onL

awV

aria

ble

(1)

(2)

(3)

(4)

(5)

(6)

R14

4A–

––

–0.

196

−0.7

14[0

.899

][−

1.57

5]R

144A

∗lag

ged

earn

ings

rati

o–

––

–0.

472

3.14

4[0

.303

][0

.796

]C

onst

ant

0.47

3−6

.433

∗∗∗

−11.

514∗

∗∗−6

.577

∗∗∗

−0.7

69−0

.320

[0.6

35]

[−10

.192

][−

40.6

28]

[−18

.563

][−

0.82

8][−

0.42

7]C

oun

try

effe

cts

Yes

Yes

Yes

Yes

Yes

Yes

indu

stry

effe

cts

(tw

o-di

git

SIC

)Ye

sYe

sYe

sYe

sYe

sYe

sYe

aref

fect

sYe

sYe

sYe

sYe

sYe

sYe

s

Obs

erva

tion

s73

71,

567

1,49

61,

656

544

367

Pse

udo

-R2

0.14

70.

061

0.05

90.

067

0.24

20.

171

Mea

nin

tera

ctio

nef

fect

−0.5

65∗

0.00

5−0

.092

0.02

30.

046

0.81

9[−

1.70

2][0

.061

][−

0.63

3][0

.266

][0

.084

][0

.748

]

International Cross-Listing 1921T

able

VC

EO

Tu

rnov

erP

rior

toC

ross

-Lis

tin

gT

his

tabl

epr

esen

tsth

epr

obit

esti

mat

esof

the

rela

tion

ship

betw

een

the

prob

abil

ity

ofC

EO

turn

over

and

firm

perf

orm

ance

un

der

vari

ous

lega

len

viro

nm

ents

prio

rto

cros

s-li

stin

g.O

bser

vati

ons

for

cros

s-li

sted

firm

sfr

omth

ecr

oss-

list

ing

year

onar

eex

clu

ded.

Lag

ged

Ear

nin

gsR

atio

isth

e1-

year

lagg

edra

tio

ofea

rnin

gsbe

fore

inte

rest

and

taxe

sto

tota

lass

ets.

Civ

ilL

awsa

mpl

ein

clu

des

firm

slo

cate

din

cou

ntr

ies

wit

ha

Fre

nch

,Ger

man

,or

Sca

ndi

nav

ian

lega

lsys

tem

.Th

eC

omm

onL

awsa

mpl

ere

fers

tofi

rms

loca

ted

inco

un

trie

sw

ith

the

En

glis

hle

galo

rigi

n.A

nti

-dir

ecto

rri

ghts

inde

xm

easu

res

the

degr

eeof

min

orit

ysh

areh

olde

rpr

otec

tion

.A

nti

-sel

f-de

alin

gis

anin

dex

ofth

est

ren

gth

ofm

inor

ity

shar

ehol

der

prot

ecti

onag

ain

stse

lf-d

eali

ng

byth

eco

ntr

olli

ng

shar

ehol

der.

All

thes

eco

un

try-

leve

lin

dice

sar

eob

tain

edfr

omD

jan

kov

etal

.(20

05).

Th

em

edia

ns

of3.

5fo

ran

ti-d

irec

tor

righ

tsan

d0.

42fo

ran

ti-s

elf-

deal

ing

inde

xu

sed

inD

jan

kov

etal

.(2

005)

are

use

dto

grou

pfi

rms

into

hig

hve

rsu

slo

win

vest

orpr

otec

tion

regi

mes

(low

erth

anor

equ

alto

the

med

ian

refe

rsto

low

gove

rnan

cesu

bsam

ples

).B

efor

eL

evel

2/3

dum

my

is1

for

the

peri

odbe

fore

the

firm

cros

s-li

sts

ona

maj

orst

ock

exch

ange

inth

eU

.S.,

0ot

her

wis

e.B

efor

eL

evel

1du

mm

yis

1fo

rth

epe

riod

befo

reth

efi

rmcr

oss-

list

sin

the

OT

Cm

arke

tsin

the

U.S

.,0

oth

erw

ise.

Bef

ore

Ru

le14

4Adu

mm

yis

1fo

rth

epe

riod

befo

reth

efi

rmh

asa

priv

ate

plac

emen

tin

the

U.S

.,0

oth

erw

ise.

Log

Ass

ets

isth

en

atu

rall

ogof

tota

lass

ets

mea

sure

din

mil

lion

$U.S

.Th

eco

nti

nu

ous

vari

able

sar

ew

inso

rize

dat

the

1%le