international conference affordable housing & mortgage financing may 28-29, 2015 local market...

TRANSCRIPT

International Conference Affordable Housing & Mortgage Financing

May 28-29, 2015

Local Market Challengesin

Housing Microfinance

Tariq Mohar – Deputy CEO Tameer Micro Finance Bank Limited

Contents

1. Perspective on Housing Market- International and National

2. Local Housing Edifice

3. Market Challenges

4. Recommendations

Scope

1. Housing includes both; urban and rural.

2. Urban housing has an over-arching impact and forms the central theme of this presentation.

3. Cost of fully developed house in microfinance market is beyond the reach of customer, thus the approach to housing envisages:- Construction of house on an already acquired land / plot. Addition / improvement of an existing house. Upgrade the living in kachi abadees (squatters) or migrate to better

living.

Due to income / saving constraints micro-segments seldom have capacity to construct house in a developed schemes. Mostly it is a phased approach to acquire a house

Dimensions of the Bottom of Pyramid (BOP)Based on annual income / spend pattern

Annual income up to USD 3000 and lessGlobal 1. Consumer 4 billion people2. Market Value 5 trillion USD Geographic Zones Asia + ME E.Europe Latin America Africa 1. Consumer (people in B) 2.86 0.254 0.360 0.4862. Market size (USD in B) 3470 458 509 429 Segmentation USD in billion Pakistan Market 1. Food 2895 49.42. Energy 433 8.0 3. Housing 332 8.7 4. Transportation 179 4.1 5. Health 158 3.6

6. ICT 101 1.17. Water 20 0. 2

As per the study, PakistanHousing market has size ofUSD 8.7 billion at the BOP,

while the figures of the nationalhousing nearly remains same.

Thusthe housing market of people

having annual income above USD 3000 per annum is negligible.

Reference : The Next Four Billion. World Resource Institute – IFC.

Housing globally is at number 3 In Pakistan it stands 2 after the food

Size of Local Housing Market and Responsebased on per year income / spend pattern

National Market

USD 8.7 billion Rs. 870 billion

Micro-housing Market –urban

USD 3.13 billion Rs. 313 billion

Response in terms of total credit

Commercial Banks + DFIs

USD 537 million Rs. 53.7 billionMicrofinance Banks

USD 2.14 million Rs. 214 million

Huge opportunity exists in the housing market . MFBs have negligible response.The nature and challenges of this market impose inertia for micro-housing product.

At 25% debt burden of income ( Rs 313 B), MF credit opportunity for 10 years tenure can be Rs 782 billion

Components of Housing Edifice

Recurring Expenses• Taxes• Utility bill• Repair & Maintenance • Additions

House

• Land/Plot

• Infrastructure

Plot purchased by owner . Infrastructures

are arranged by Developer / Realtor

included in the price.

Investment by actual owner or

Developer / Realtor Power

Gas WaterSewerageRoadsAmenities

Tenant paysrent + utilities

Total investment by owner and pays recurring expenses

MF customer can seldom purchasea fully developed house. Must start from acquiring the plot.

For micro- house loan, rental should match or better monthly Repayment – move to own house.

The house acquisition plan must be spread over longer period to make financing with in the reach of customer. Pooling of family incomes should be encouraged. Objective: migrate tenant to ownership.

Local Market Challenges

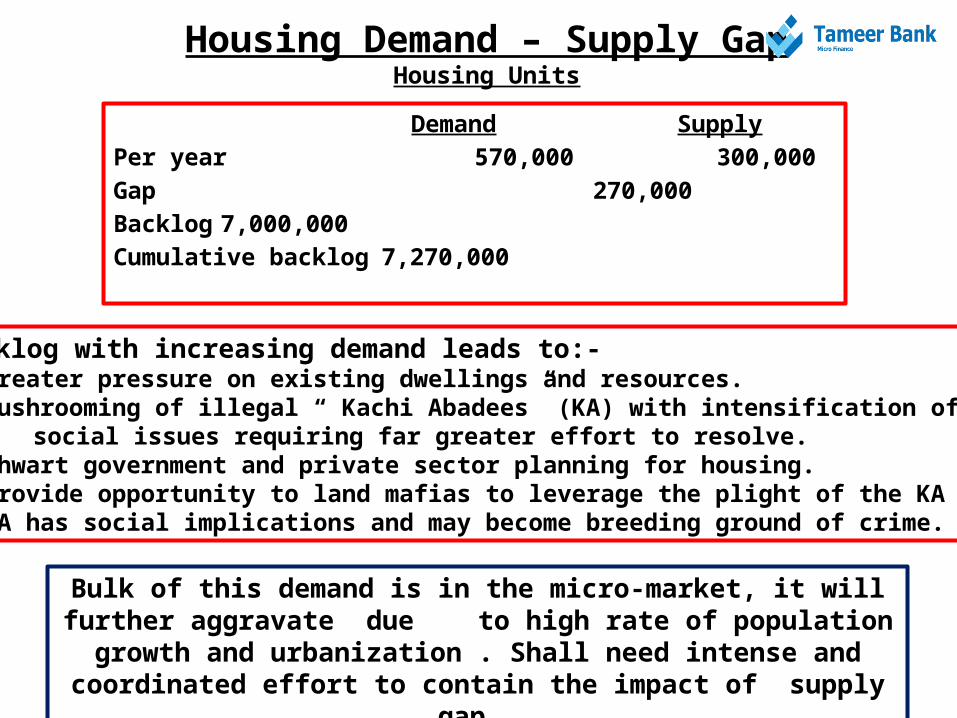

Housing Demand – Supply GapHousing Units

Demand Supply

Per year 570,000 300,000

Gap 270,000

Backlog 7,000,000

Cumulative backlog 7,270,000

Backlog with increasing demand leads to:- Greater pressure on existing dwellings and resources. Mushrooming of illegal “ Kachi Abadees” (KA) with intensification of social issues requiring far greater effort to resolve. Thwart government and private sector planning for housing. Provide opportunity to land mafias to leverage the plight of the KA KA has social implications and may become breeding ground of crime.

Bulk of this demand is in the micro-market, it will further aggravate due to high rate of population growth and urbanization . Shall need intense

and coordinated effort to contain the impact of supply gap.

Speculation kills Micro-housing Schemes

As part of the “ Site and Service Model ” Government develops infrastructures, while people purchase plots to build their own houses. Fixed percentage is dedicated for low income groups. However, these schemes remain non-productive as subsidized plots have lower prices and are purchased by higher income groups for speculation. Genuine customers are denied opportunity. Some of the prominent schemes, that failed to support the MF customers :-

1. KDA Scheme of 200,000 plots in Karachi in 1970 and 1980

2. Prime Minister 3 and 7 marla scheme in 1987.

3. Projects of National Housing Authority.

Failure of such schemes leads to Kachi Abadees (squatter housing / slums) in major urban areas of Pakistan. These Abadees are illegal occupation of government lands, thatprovide main alternative to low income groups, who migrate from rural areas or other

remote locations for economic opportunities in big cities.

Huge backlog has impaired government’s capacity to manage the micro-housing needs. It affords great opportunity for private sector, in case of enabling environments.

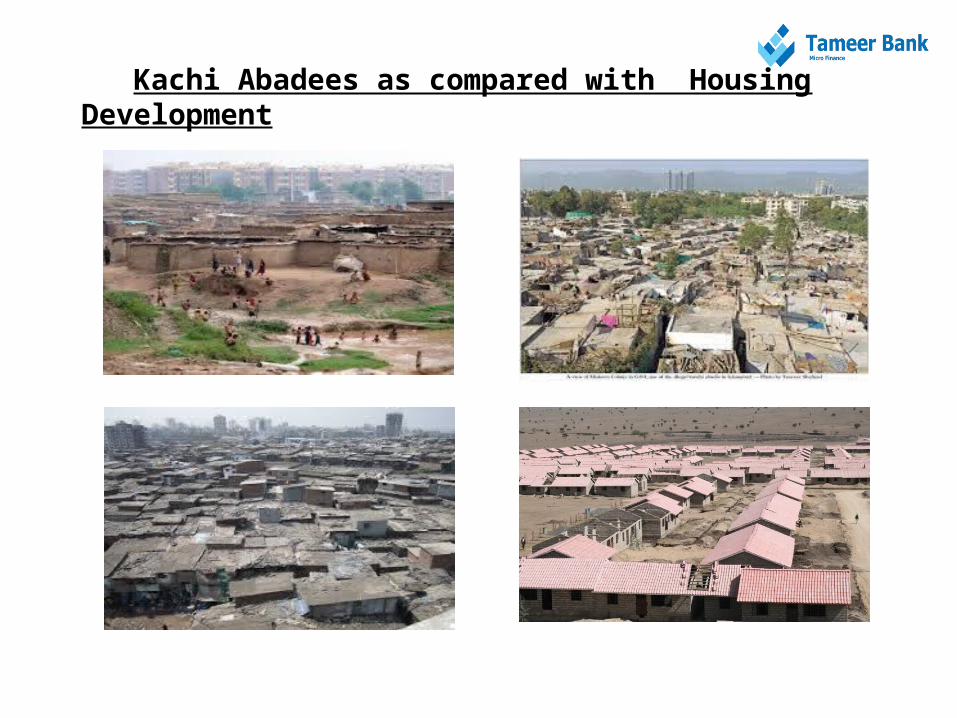

Kachi Abadees as compared with Housing Development

Constraints of Micro-housing Product

Essence of microfinance products:-1. Most of the MF products are based on 12 months tenure with equal monthly installment (EMI).

2. In the absence of documented financial profile, physical assessment / verification of incomes / cash flows (ICF) has accuracy up to a maximum of 24 months.

3. Based on credit behavior and validation of ICF the tenures may be increased to 24 or at best 36 months.

4. Products having tenures beyond 36 months will have inconsistent behavior, primarily due to lack of validity of ICF beyond 24 months.

Above conditions for MF products are more pronounced for micro-housing loan, which has demand for bigger ticket and longer tenures, having following effects:-

1. 12 -24 months is too short a period for recovery of large EMI loan. 2. 36 months make a viable option, yet the size of EMI do not support big ticket size. 3. 60 months can reduce the size of the installment but the ICF does not remain valid. Thus, most of the loan go into default after 24 months. Option for declining balance does not match the long – term cost of funds, which is high for MFBs.

Present regulations allows a housing loan up to USD 5000 or Rs. 500,000 that does not support purchase of house, at best it can help addition / improvement in existing house,

or purchase of plot. Higher markup for longer tenures seeps customer capacity for loan.

Documentation and Ownership Titles MF customers who purchase land / plots from societies / developers do not receive title of

ownership for various reason, thus remain unqualified for house financing despite holding possession.

Ancestral properties with high market value, have multiple ownership due to family succession but the units can not be split for individual title. All co-owners seldom agree to mortgage and surrender the original documents. It remains a difficult proposition for most of the families.

There are properties, which may have valid sale deeds (stamp papers) but are not registered or mutated in the name of the buyer, due to high cost of transfer or bureaucratic hurdles, thus the investment remains locked.

Even clear titles with registration can not be verified by the land department as changes / mutations are not kept up to date, due to reasons of corruption, weak management or oversight. Remedies entail extensive procedure requiring extra cost and influence, which MF customer can not afford.

The recent effort to computerize land records may ease the situation, yet it is to early to make any comment.

Property without clear and verified title is a “dead capital”Except few organizations, ownership titles and related document are not well maintainedeven for high value properties by the land / revenue department. MF customers are more at disadvantage due to weak influence or lack of funds to pursue or bribe.

Operational limitations of Micro- housing Loan

Title search and verification has high cost for processing loans. The end use lacks structured mechanism like commercial banks where partial funds are

released at various stages of the house construction. MF customers decline loans having phased disbursal.

If the end purpose is to be monitored, it has an additional cost, which will further over-burden the cost of acquiring loan and also in conflict with customer behavior.

In case of default, the case is referred to the civil courts, as the jurisdiction of the banking courts precludes MFBs, since they do not fall under the banking companies act of 1962. The procedure in civil courts is tedious and time consuming with high cost.

Even if the case is decided in favor of the bank, the sale of the mortgaged house is not possible due pressure / sympathy of the local community. At best the negotiations can be undertaken to recover the principal with adjustments / waivers.

Where there are multiple owners to a title, the loans are not offered by the MFBs, thus a

huge portion of the property equity stays locked with no economic advantage. People holding ownership of commercial properties in old portions of cities / towns on

goodwill “pugree basis” can not use it as collateral for loan since they are treated as a tenant with no legal status. Similarly the original owner who has given property on “pugree” can not use the same as collateral for any loan / finance.

Commercial banks are shy of housing finance in absence of effective foreclosure laws. MFBs are more at disadvantage in absence of capacity to bear high default and its

related legal recourse to civil courts.

Land Infrastructure Construction of house Furnishing Maintenance Improvement /

additions

Size of plot• 20 sq yd• 40 “• 60 * “• 80 “• 120 “Docus/title

• Power • Gas• Water• Sewerage• Road• Amenties

• Design• Structure• Door/

window• Electric• Sanitary• Linkages

• Furniture• Household

Life Cycle of Micro- housing with Related Aspects

• Utilities• Loan instl • Repair /

maint

For family needsand improve Standard of living

Price - various Phases for median size of 60 yds

Rs. 50 – 100 K Rs. 200-300 K Rs. 1- 1.2 M Rs. 100-150 K

Utilities: Rs. 500-800Rental value:4000 -6000

Phase -1 Phase -2 Phase-3 Phase -4

Developer / cooperative societies / NGO Personal ownership

Direct purchase at Phase - 3 having finance need of Rs 1.5 M by MF customernot viable due to size of monthly installment. Loan for various Phases may help to resolve the issue, needs long-term approach.

Presently, most of the loans are used for Phase - 4

Recommendations

Premise of recommendations

1. The demand and related aspects of micro-housing in the country can not be handled by private sector . It would need continuous patronage and support of the government.

2. Informal savings habits in low income segments are well honed , as reflected by the holding of gold / jewelry. This may be leveraged by providing another option

to save for future by investing in acquisition of housing plot / land.

3. The issue of housing is complex and voluminous and will require a comprehensive

approach to provide solutions that can tackle the immediate, mid and long-term

housing needs , and its related issues.

4. Response of MFBs to the micro-housing market needs is negligible , it would need time and resources to make a viable change. A new operating model will have to be designed, which can improve the existing site and service approach of the government by integrating the private sector and civil society. Land mafias will have to be contained.

5. Lyari Expressway Resttelement Project (LERP), Karachi and Saiban make a strong model to migrate Kachi Abadees to formal settlement.

6. Each aspect of the recommendation would require detailed study to dimension its extent and application.

Recommendations

Following recommendations are made with in the purview of the premise:- National Housing Policy. National housing policy do cover general aspects for low income

segments. It should clearly articulate the micro-housing segment in every housing scheme

with intent to:-

a. Where possible, legalize existing kachi abadees and provide additional lands, where required to develop in to an organized housing colony.

b. Migrate kachi abadees to more preferred areas to release the unauthorized holdings of land. LERP at Taiser Town provides a fairly effective working model, which can be improved further.

c. Integrate micro-housing projects into future town planning of every district as part of the provincial housing plan. The public - private partnership should be part of every province, gradually moving down to every district.

d. The existing government model of site and service should be suitably modified based on the public - private partnership, with inbuilt measures to discourage speculation by real estate mafias.

Recommendations - Continued

Strategy. There is a need to have a comprehensive micro-housing strategy based on the following:-

Long-terms: Develop saving product that targets delivery of plot on completion of the tenure. It needs formation of the consortium based on public - private partnership:-

a. Government. To provide guarantee, release and management of land for micro-housing.

b. Microfinance Banks (MFBs). Targeted saving product which confirms allotment of land on completion

of saving tenure.

c. Investor. Inducts capital for development of infrastructures as part of the housing scheme / society which offers developed plots to customers against the saved amounts with the MFBs.

Mid-term.

a. The recent creation of the Mortgage Refinance Company may consider to refinance against land

occupation in kachi abadees to MFBs, with special focus on the high markup to finance addition /

improvement of squatter houses and make them livable.

b. All Kachi Abadees may be surveyed and prioritized based on the status of holding and suitability for

induction of credit, with prospects of land regularization. It will open a new market for MFBs.

Immediate. The SBP prudential regulations may be revised to include loans up to Rs 1 million for micro

-housing. To make the product viable for low income groups. Subsidy / relief in mark-up rates may be

provided

Recommendations - Continued

Housing Design. Housing design must be standardized to keep the price and related profits under watch :-

Adherence to design should be mandatory, whereas furnishing of the of the house should

be the choice of the customer.

Size of the house could be 20, 40, 60, 80, and 120 sq yds, with 60 yds as the standard size.

In case of apartment, the size can be smaller with in these categories . However, the

height should not exceed more than 4 floors as deployments of other facilities will

increase the initial and regular operating cost. Apartments do not provide the culture

for migratory population, and may be considered as a long term option.

General• Micro-housing loan with less than 10 years tenure become unviable, to retain the monthly

installments with in repayment reach, subsidy on mark up should be the main relief for the customer. Pooling of family income should be encouraged.

• Government may reduce the cost of funds for the MFBs by placing its deposits with the MFB at nominal rates compared with the market.

• Monitoring for end use of the loan may be deferred for next 10 years , to allow the mortgages and micro-housing loans to take its spin in the market.

“thank you”