international capital market association european … · market is one of the largest financial...

TRANSCRIPT

International Capital Market Association

European repo market surveyNumber 10 – conducted December 2005

Published March 2006

© International Capital MarketAssociation (ICMA), Zurich, 2006.All rights reserved. No part of thispublication may be reproducedor transmitted in any form or byany means without permissionfrom ICMA.

International Capital MarketAssociationRigistrasse 60P. O. Box CH-8033 Zurichwww.icma-group.org

CONTENTS

Foreword By Hans-Jörg Rudloff, Chairman, ICMA 5

Foreword By Godfried De Vidts, Chairman,European Repo Council 6

Executive Summary 8

Chapter 1: The Survey 10

Chapter 2: Analysis of Survey Results 12

Chapter 3: Conclusion 21

Chapter 4: Five Years of the ICMA Repo Survey 22

Chapter 5: The Work of the European Repo Council 27

About the Author 40

Appendix A: Survey Guidance Notes 41

Appendix B: Survey Participants 46

Appendix C: Summary of Survey Results 50

Appendix D: Global Master Repurchase Agreement (GMRA) Annexes and Legal Opinions 54

ISMA EUROPEAN REPO MARKET SURVEY DECEMBER 2003 I 3

This report has beencommissioned by the InternationalCapital Market Association (ICMA)in particular support of members ofICMA’s European Repo Council(ERC) and in the interests of theinternational capital market as awhole.

Its purpose is to helpparticipants in, and observers of,Europe’s cross-border repo marketto gauge the size of the market.

All statements, opinions andconclusions contained within thisreport are made in a personalcapacity by the author, are his soleresponsibility and do not representthe opinion of ICMA, which hasneither taken an official position onthe issues discussed, statementsmade and conclusions drawnherein nor sought to verify theinformation, statistics, opinions orconclusions provided.

4 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 5

FOREWORD BYHANS-JÖRG RUDLOFFCHAIRMAN, ICMA

The ICMA European repo surveywas established in 2001 to helpparticipants in Europe’s cross-borderrepo market to establish moreaccurately the size and compositionof the market. Whilst the repomarket is one of the largest financialmarkets in Europe and, as arefinancing tool, repo is critical tocapital market operations, before theadvent of the repo survey actualstatistical evidence of market sizewas hard to obtain.

In the 5 years since it began,this survey has become establishedas an essential source of data onthe repo market in Europe, widelyused by market participants toassess their own market share anddetermine their strategies in thisarea. ICMA has been very pleasedby the success of this initiative andwelcomes the publication of this,the 10th report, which contains anoverview of the current state of themarket and an analysis of the keydevelopments which have takenplace over the period since thesurvey started.

6 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

FOREWORD BYGODFRIED DE VIDTS CHAIRMAN, EUROPEANREPO COUNCIL

When the European RepoCouncil (ERC) launched the firstedition of its semi-annual survey ofthe repo markets the outcome wasunsure. Nobody had previouslycompiled data on repo activity and,as a consequence, estimates aboutthe size of the market and the useof various forms of collateral werea matter of guesswork for anybodyinvolved in this increasinglyimportant product area.

The group of market expertsgathered as the European RepoCouncil clearly identified the needfor some co-ordination of statisticsin the repo market, particularly inlight of the newly born currency,the Euro. Repo markets, createdinitially in Belgium and France,quickly became the financing tool

used by the various NationalCentral Banks and with the adventof the European Central Bank repowas confirmed as the main tool forrefinancing operations in Europe asa whole. As each domestic marketjoined what was becoming onehuge single market, we, themarket users were quick tounderstand both the potential andthe challenges.

Working under the aegis ofICMA, the European Repo Councilhas become the industryrepresentative body that hassought to identify shortcomings inall aspects of market infrastructurerelated to repo. The legalframework was put in place at anearly stage with the developmentof the Global Master RepurchaseAgreement (GMRA), now the onlycredible cross-border legaldocumentation to support thisbusiness. Counterparty riskmitigation can only work on asound legal basis and this has beensupported both financially and withtechnical advice from thesupporters of the GMRA.

The ERC has extensivelypromoted the use of repo andgiven guidance to marketparticipants in regular updates atmeetings which are open to ERCmembers and non-members alike.Repo Trading Practice Guidelineshave been produced that havebeen instrumental in thedevelopment of electronic tradingwhile the Best Practice to RepoMargining has helped our support

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 7

officers to understand thesecomplex issues. For a number ofyears the ERC has organisedprofessional repo market courses,widely acknowledged as thebenchmark for training in thissector, with the result that severalhundred successful formerstudents are now working in themarket.

Some of the challengesinherent in creating a single Europewide repo market are still with us.Clearing and settlement issueshave become very much a topic forconferences and discussions in thewholesale market and only now isthe European Commission workingon the creation of the necessaryinfrastructure allowing the marketsto move collateral cross-borderwithout unnecessary friction andloss of efficiency. In Europe we stillneed to work hard on theinfrastructure that will create amuch larger secured market. Tothis end the ERC has been involvedwith the Eurosystem of theEuropean Central Banks, hassupported the work of theGiovannini working group,provided advice to the CESAMEworking group of the EuropeanCommission and various otherindustry groups.

This 10th edition of theEuropean repo market survey is inmany ways a tribute to allparticipants in this market for a jobwell done. Specifically, all themembers of the European RepoSteering Committee deserve our

thanks for their commitment overthe years. Thanks must also go toall the number crunching supportstaff from all the banks, tripartyagents and interdealer brokers whoprovide the data for the survey andof course to the author of thesurvey, Richard Comotto who oftenworks against tight deadlines forits publication.

In conclusion, the ICMAEuropean repo market surveyprovides real evidence of thespectacular growth of the markets,demonstrating the momentum thatEurope’s capital markets have builtover the last 5 years. It is proof tothe financial markets that thisproduct has claimed its rightfulplace among the many toolsused by financial institutions andtheir clients and, with theimplementation of the new CapitalAccord (Basel 2) next year, thebenefits of repo as a collateralmanagement tool are set to beeven more widely recognised.

My hope is that many morefinancial institutions will participatein this European wide survey in thefuture.

8 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

EXECUTIVE SUMMARY

In December 2005, theEuropean Repo Council (ERC) ofthe International Capital MarketAssociation (ICMA) conducted thetenth in its series of semi-annualsurveys of the repo market inEurope.

The latest survey asked asample of financial institutions inEurope for the value of their repocontracts that were stilloutstanding at close of business onDecember 7, 2005. Replies werereceived from 80 offices of 70financial groups, mainly banks.Returns were also made directly bythe principal tri-party repo agentsand automatic repo tradingsystems (ATS) in Europe.

Total repo business

The total value of repocontracts outstanding on the booksof the 80 institutions whoparticipated in the latest surveywas EUR 5,883 billion, compared toEUR 5,319 billion in June 2005 andEUR 5,000 billion in December2004.

It is important to note thatsome of the changes in theseheadline numbers between surveysrepresent the entry and exit ofinstitutions into and out of thesurvey, as well as bank mergersand the consolidation of repo bookswithin banks. The organic year-on-year growth in the European repomarket has therefore beenmeasured by comparing the

aggregate returns from a sample ofinstitutions that have participatedin several surveys. Growthmeasured on this basis wasbetween about 15% and 18% overthe year to December 2005.

Counterparty analysis

The latest survey showed thatthe share of electronic trading roseto a record 24.7% from 21.2% inJune 2005, while the share ofvoice-brokers dropped to a low of21.8% from 24.6% over the sameperiod.

Geographical analysis

The share of reportedoutstanding repo contracts thatwere negotiated anonymously onan ATS and settled with a centralclearing counterparty (CCP)increased to 11.0% from 10.4% inJune 2005, but was still below therecord 11.7% reported inDecember 2004.

Settlement analysis

The share of tri-party reposwas unchanged at 10.4%, stillbelow the peak of 11.2% reachedin December 2003.

Cash currency analysis

The share of the euro fell backto 68.2% from 70.0% in June2005, while that of the poundsterling increased to 12.7% from11.1% over the same period. Forthe first time, the survey

specifically identified the Swissfranc. However, this accounted forjust 0.2%.

Collateral analysis

The share of repo collateralheld by survey participants whichwas issued in countries in theeurozone was virtually unchangedat 68.1%. Within this total,however, the share of collateralissued in Germany jumped to29.9% from 24.8% in June 2005.The share of collateral issued in theUK increased to 13.9% from12.9%. The main counterpartswere reductions in the shares ofcollateral issued in Italy (13.4%from 15.2%), Spain (3.9% from5.6%), the US (2.2% from 3.5%)and other OECD countries (10.1%from 11.2%).

The share of collateral issuedin EU countries accounted for bygovernment bonds was littlechanged at 85.9%. The share ofequity collateral was unchangedat 0.4%.

Maturity analysis

The share of short-dated repos(one month or less) fell to 61.9%from 65.3% in June 2005. For thefirst time, the survey asked for thevalue of repo contracts with morethan 12 months remaining tomaturity: these longer-term reposaccounted for 5.1%. The share offorward-start repos continued tofall, touching 3.2%.

Product analysis

The share of total businessconducted on repo desks that wasaccounted for by securities lendingand borrowing dropped to 17.5%of total business from 19.2% inJune 2005. The share of equitycollateral in this securities lendingand borrowing fell back to 9.7%from 11.4% in June, but this is stillsubstantially higher than the 5.9%recorded in December 2004.

Concentration analysis

In the latest survey, theshares of the top ten, twenty andthirty institutions were smaller at54.3%, 77.0% and 88.6%,respectively, compared to 55.0%,78.2% and 90.1%, respectively, inJune 2005.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 9

10 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

CHAPTER 1: THESURVEY

On December 7, 2005, theEuropean Repo Council (ERC) ofthe International Capital MarketAssociation (ICMA) conducted thetenth in its series of semi-annualsurveys of the repo market inEurope.

The ICMA survey was activelysupported by the ACI – TheFinancial Markets Association, andhas been welcomed by theEuropean Central Bank andEuropean Commission. The surveywas managed and the resultsanalysed on behalf of ICMA by theICMA Centre at Reading Universityin England under the guidance ofthe ERC Steering Committee (“ERCCommittee”).

1.1 What the survey askedThe survey asked financial

institutions in a number ofEuropean centres for the value ofthe cash side of repo and reverserepo contracts still outstanding atclose of business on Wednesday,December 7, 2005.

The questionnaire also askedthese institutions to analyse theirbusiness in terms of the currency,the type of counterparty, contractand repo rate, the remaining termto maturity, method of settlementand source of collateral. Inaddition, institutions were askedabout securities lending andborrowing conducted on their repodesks. For the first time,

institutions were asked to identifytheir Swiss franc repo business andtransactions with a remaining termto maturity of more than one year.

The detailed results of thesurvey are set out in Appendix C.An extract of the accompanyingGuidance Notes is reproduced inAppendix A.

Separate returns were madedirectly by the principal tri-partyrepo agents and automatic repotrading systems (ATS) in Europe.

1.2 The response to thesurvey

The latest survey wascompleted by 80 offices of 70financial groups. This compareswith 81 offices of 74 financialgroups in June 2005 and 76 officesof 69 groups in December 2004.While 7 institutions whichparticipated in the June 2005survey dropped out of the latestsurvey, 6 institutions rejoined.

The institutions surveyed wereheadquartered in 16 Europeancountries, as well as in NorthAmerica (6) and Japan (5). 66institutions were headquartered in13 of the 25 countries of theEU (no institutions from Portugaland Sweden participated in thelatest survey) and 60 wereheadquartered in 11 of the 12countries of the eurozone.However, although someinstitutions were headquartered inone country, the bulk of theirbusiness was conducted in another.

Many institutions provided data fortheir entire European repobusiness. Others provided separatereturns for each office with its ownrepo book. A list of the institutionsthat have participated in ICMA reposurveys is contained in Appendix B.

1.3 The next surveyThe next survey is scheduled

to take place at close of businesson Wednesday, June 14, 2006.

Any financial institution wishingto participate in the next survey candownload copies of the questionnaireand accompanying Guidance Notesfrom ICMA’s web site. The latestforms will be published shortly at thefollowing website: www.icma-group.org/surveys/repo/participate.

Questions about the surveyshould be sent by e-mail [email protected].

Institutions who participate inthe survey receive, in confidence, alist of their rankings in the variouscategories of the survey.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 11

12 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

CHAPTER 2: ANALYSIS OF SURVEY RESULTS

The aggregate results for previous surveys are set out in Appendix C.

Total repo business (Q1)The total value at close of business on December 7, 2005, of repos andreverse repos outstanding on the books of the 80 institutions whichparticipated in the survey was EUR 5,883 billion, of which, 54.6% wererepos and 45.4% were reverse repos.

Table 2.1 – Total repo business 2001 to 2005

The values measured by thesurvey are gross figures, whichmeans that they have not beenadjusted for the double counting oftransactions between pairs ofsurvey participants.

Nor does the survey measurethe value of repos transacted withcentral banks as part of officialmonetary policy operations. Infact, the value of the reposoutstanding between surveyparticipants and the ECB on thesurvey date was EUR273.8 billion,equivalent to 4.7% of the surveytotal (although the central banknumber has no double-counting).Survey participants accounted for69.1% of the outstanding repos tothe ECB. In addition, some survey

participants will have hadoutstanding transactions with theBank of England, DanmarksNationalbank, Sveriges Riksbankand Swiss National Bank.

In order to gauge the year-on-year growth of the European repomarket (or at least of that segmentrepresented by the institutionswhich have participated in thesurvey), it is not valid to simplycompare the total value of reposand reverse repos with the samefigures in previous surveys. Someof the changes represent the entryand exit of institutions into and outof the survey, mergers betweenbanks and the reorganization ofrepo books within banks. Toovercome the problem caused by

Survey Total (EUR bn) Repo Reverse repo2005 December 5,883 54.6% 45.4%2005 June 5,319 52.4% 47.6%2004 December 5,000 50.1% 49.9%2004 June 4,561 50.6% 49.4%2003 December 3,788 51.3% 48.7%2003 June 4,050 50.0% 50.0%2002 December 3,377 51.0% 49.0%2002 June 3,305 50.0% 50.0%2001 December 2,298 50.4% 49.6%2001 June 1,863 49.6% 50.4%

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 13

changes in the sample of surveyparticipants, comparisons weremade of the aggregate outstandingcontracts reported only byinstitutions which had participatedin several surveys. The repobusiness of the 30 institutionswhich have participated in all tensurveys grew by 18.5% year-on-year to December 2005. Over thefirst six months from December2004 to June 2005, the rate ofgrowth was 9.2% and, from June2005 to December 2005, it was8.5%. Of the 67 institutions thatparticipated in all three surveys

from December 2004, growth was15.4% year-on-year to December2005, 5.1% from December 2004to June 2005 and 9.8% from June2005 to December 2005.

The average size of repo booksjumped to EUR74 billion fromEUR66 billion. Of the 67institutions that participated inboth the December 2004 and 2005surveys, there was a clear biastowards growth, with the repobooks of 45 expanding over theyear, 20 contracting and twounchanged.

In December 2005, inter-dealer ATSs took a record share of24.7% of reported business,despite the number of institutionsin the latest survey reporting useof ATSs falling from 53 to 48, thelowest number since June 2002.

The principal automatictrading systems (ATS) operating inEurope provided data directly tothe survey. Returns were receivedfrom BrokerTec, Eurex Repo andMTS. The reported share of reposoutstanding on December 7, 2005,that had been transacted across anATS was EUR759.9 billion

compared to EUR660.2 billion in

June 2005 and EUR568.8 billion in

December 2004, increases of

15.1% and 16.1%, respectively,

and a year-on-year increase of

33.6% to December 2005. The

year-on-year growth rate in ATS

business reported directly is not

too dissimilar to that measured by

the main survey (38.9%), but the

pattern of growth was very

different: in the main survey, ATS

growth was 32.9% between

December 2005 and June 2005,

and only 4.5% between June 2005

and December 2004.

December 2004 June 2005 December 2005share users share users share users

direct 54.5% 76 54.3% 81 53.5% 80of which tri-party 9.8% 34 10.4% 40 10.4% 37voice-brokers 24.2% 55 24.6% 57 21.8% 56ATS 21.3% 50 21.2% 53 24.7% 48

Counterparty analysis (Q1.1)

Table 2.2 – Counterparty analysis December 2004 to December 2005

The value of outstanding repocontracts transacted across ATSsand reported directly by the ATSsin December 2005 was equivalentto 12.9% of the headline total ofEUR5,883 billion from the mainsurvey, whereas the ATS numberfrom the main survey was 24.7%.The difference is likely to be duemainly to double-counting in themain survey (the data provideddirectly by the ATSs count only oneside of each transaction). On theother hand, the main surveyincludes business across at leastone additional ATS (Senaf).

The share of voice-brokerstouched an all-time low of 21.8%in December 2005.

A sub-set of direct repos,equivalent to 10.4% of thetotal outstanding business, wassettled through tri-party repoarrangements. This wasunchanged from June 2005, higherthan in December 2004 (9.8%) butbelow the peak (11.2%) recordedin December 2003. However, thenumber of institutions in thesurvey reporting tri-party repos fellto 37 from a record 40 in June2005.

The main tri-party repo agentsin Europe again contributed data tothe survey. Returns were receivedfrom Bank of New York, Clearstream,Euroclear, and SegaInterSettle(SIS). The total value of outstandingtri-party repo contracts on December7, 2005, reported by these agentswas EUR523.4 billion compared withEUR 315.8 billion in June 2005 andEUR 297.2 billion in December 2004(a substantial increase despite thesmaller sample of tri-party agents inthe latest survey). This compares toEUR604.1 billion reported in themain survey. The reason for thedifference is not obvious. As most tri-party repo in Europe is betweenbanks and customers, the differenceis unlikely to be due to double-counting. It may be that thedifference is tri-party repos betweensurvey participants and tri-partyrepo agents that did not reportdirectly.

Figure 2.1 – Counterpartyanalysis

14 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Table 2.3 – Numbers of participants reporting particular types of business

Dec-02 Dec-03 Dec-04 Jun-05 Dec-05ATS 48 50 50 53 48anonymous ATS 35 29 36 36 35voice-brokers 65 58 55 57 56tri-party repo 32 32 34 40 37total 82 76 76 81 80

Direct bilateral43.1%

ATS24.7%

Voice-brokered21.8%

Direct tri-party10.4%

Table 2.4 – Geographical analysis December 2004 to December

The share of anonymoustrading across ATSs increasedmarginally to 11.0% from 10.4% inJune 2005, but remains below the11.7% recorded in December2004. The sluggishness ofanonymous trading contrasts withthe rapid growth of electronictrading generally. It may be thatthe share of anonymous electronictrading has been understated bygaps in some key survey returns.The share of anonymous electronictrading could be two or morepercentage points larger thanreported.

Anonymous trading accountsfor 73.8% of the business of themain ATSs.

The composition of tri-partybusiness reported by the tri-partyrepo agents was not too dissimilarfrom the composition of overallactivity reported in the main survey.31.6% of directly-reported tri-partyrepos was domestic (compared with31.4% in June 2005 and 30.5% inDecember 2004) and 61.6% wascross-border with counterpartiesoutside the eurozone (comparedwith 61.4% in June 2005 and62.9% in December 2004).

Figure 2.2 – Geographicalanalysis

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 15

December 2004 June 2005 December 2005

share users share users share usersdomestic 33.9% 36.7% 35.5%cross-border 54.3% 52.8% 53.5%anonymous 11.7% 36 10.4% 36 11.0% 35

Domestic35.5%

Anonymous ATS11.0%

Non-Eurozone23.8%

Eurozone29.7%

Cash currency analysis (Q1.2 and Q1.3)Table 2.5 – Cash currency analysis December 2004 to December 2005

December 2004 June 2005 December 2005EUR 70.4% 70.0% 68.2%GBP 10.9% 11.8% 12.7%USD 11.6% 11.1% 11.3%DKK, SEK 2.2% 2.2% 2.1%JPY 3.6% 3.4% 3.6%CHF n/a n/a 0.2%other currencies 1.3% 1.5% 1.9%cross-currency 1.0% 0.9% 1.1%

The share of euros touched arecord low of 68.2%, while theshare of the pound sterling reacheda record high of 12.7%. The sharesof other currencies remained fairlystable. For the first time, the shareof the Swiss franc was measured.However, the figure of 0.2% is toolow to be credible and seems toreflect the way that some keybanks organize their repo tradingin terms of currency.

The reported share of cross-currency repos remainedinsignificant, but the response rate tothis question remains low (28) andclose examination of survey returnsshows that, in some banks, cross-currency repos account for asignificant share of business. There istherefore likely to be a reportingproblem. In many other institutions,the under-reporting of cross-currencybusiness may reflect the use of tri-party repo for this activity (43.2% oftri-party was cross-currency inDecember 2005) and the problems ofintegrating tri-party reporting.

The share of the euro in ATSbusiness was lower at 92.4%compared to 94.6% in June 2005.The share of sterling rose to 7.4%from 5.1% in June 2005.

There was dramatic shift in thecurrency composition of tri-partybusiness towards the US dollar. Theshare of the dollar jumped to 42.3%in December 2005 from 21.6% inJune 2005 and 24.9% in December2004. The share of the euro fellsharply to 43.6% from 61.1% inJune 2005 and 58.0% in December2004, that of sterling fell to11.5% from 14.2% and 13.3%,respectively. The proportion of cross-currency business also fell sharply to43.2% from 58.5% in June 2005 and59.0% in December 2004.

Figure 2.3 – Currency analysis

16 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Collateral analysis (Q1.8)Table 2.6 – Collateral analysis December 2004 to December 2005

December 2004 June 2005 December 2005Germany 24.9% 24.8% 29.9%Italy 14.7% 15.2% 13.4%France 10.1% 10.1% 10.4%Belgium 3.8% 4.1% 3.6%Spain 5.4% 5.6% 3.9%other eurozone 7.4% 7.6% 6.9%UK 12.0% 12.3% 13.9%DKK, SEK 2.9% 2.5% 2.2%US 2.5% 3.5% 2.2%Accession countries 0.3% 0.4% 0.7%other OECD 13.3% 11.2% 10.1%other 2.7% 2.6% 2.8%equity 0.4% 0.4% 0.4%

Other1.9%

JPY3.6%

DKK,SEK2.1%

USD11.3%

GBP12.7%

EUR68.2%

CHF0.2%

68.1% of repo collateral heldby survey participants was issuedin countries in the eurozone,slightly up from 67.4% in June2005 and 66.3% in December2004. However, within this change,the share of collateral issued inGermany recovered to 29.9% fromthe record low of 24.8% seen inJune 2005, largely at the expenseof the shares of collateral issued inItaly, Spain, the US and otherOECD countries. On the otherhand, the share of collateral issuedin the UK continued to expand andreached a record 13.9%.

Figure 2.4 – Collateral analysis

The share of collateral in themain survey issued by centralgovernments was 85.9%, verysimilar to the 85.7% recorded inJune 2005 and below the share of87.8% in December 2004. Of theremainder, 2.0% of collateral wasGerman pfandbrief.

Business reported by ATScontinued to be dominated bycollateral issued in Germany, Italy,

France and the UK. The share ofGerman collateral increased to43.9% from 40.0% in June 2005,largely at the expense of Italiancollateral (down to 21.3% from27.6%).

There was a big change in thecollateral composition of tri-partybusiness with the share of equityrising sharply to 20.4% from11.9% in June 2005 and 15.5% inDecember 2004. This was not ageneral change in tri-partybusiness. Moreover, it somewhatdistorted the changes in the sharesof other collateral categories. Tri-party repo collateral issued in theEU fell back to 60.1% from 75.4%in June 2005 (this repeated thepattern seen in 2004, when theshare of EU collateral fell back to66.9% in December 2004 from76.5% in June 2004). The share ofcollateral issued in the eurozonefell to 46.8% from 57.8% in June2005 and 52.7% in December2004, and the share of collateralissued in Germany to 13.6%compared to 15.4% in June 2005and 18.0% in December 2004.The share of EU government bondsin tri-party business fell to 23%from 25.7% in June 2005 and44.2% in December 2004.

Contract analysis (Q1.4)The share of reported

outstanding repo contracts takingthe form of classic repos (alsocalled “repurchase agreements”)stayed at the record high of 83.0%reached in June 2005 comparedwith 80.6% in December 2004.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 17

Germany29.9%

Italy13.4%

Spain3.9%

OtherEurozone7%

UK13.9%

DKK,SEK2.2%

US2.2%

OtherOECD10.1%

Others2.8%

Belgium3.6%

France10.4%

Accessioncountries0.7%

Figure 2.5 – Contract analysis

Repo rate analysis (Q1.5)

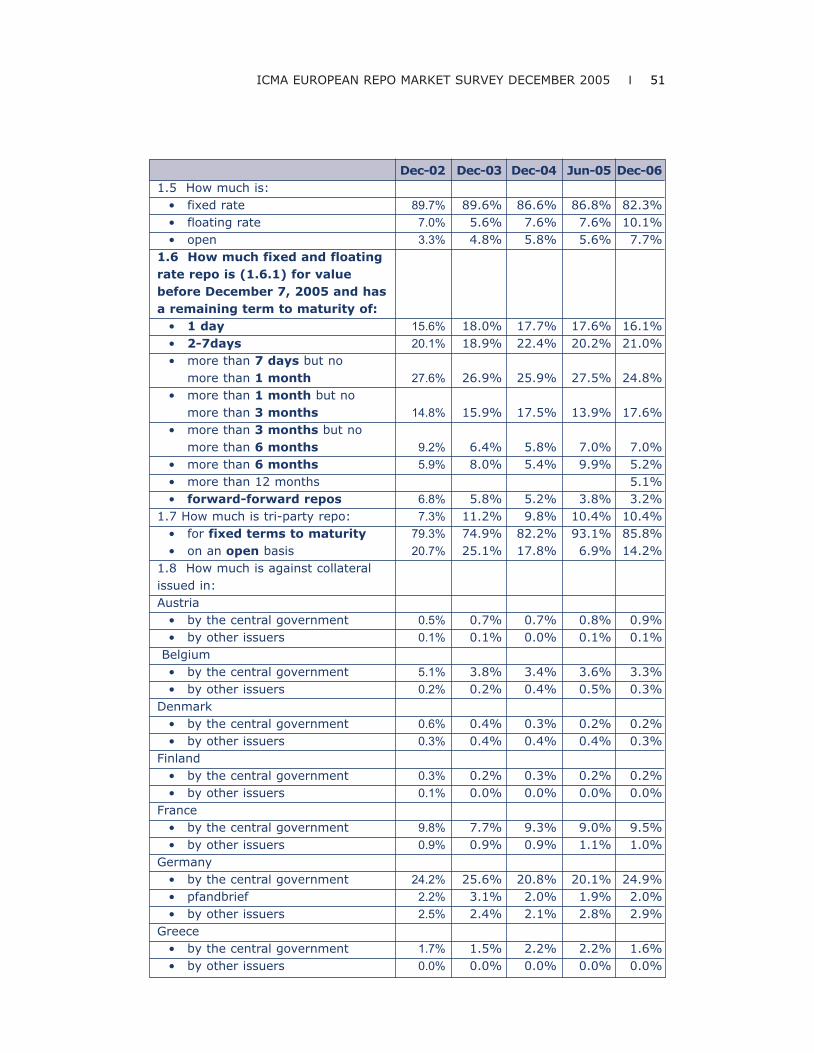

One of the majordevelopments between the Juneand December 2005 surveys wasthe increase in the share offloating-rate repos (typicallyindexed to EONIA), whichincreased to 10.0% from theprevious highs of 7.6% recorded inboth June 2005 and December2004. Floating-rate repos in ATSbusiness accounted for 11.6%compared with 10.1% in June2005.

This growth probably reflectedboth secular and cyclical factors.Interest has been growing infloating-rate repo, in part, becauseof their attraction to customers

such as money market mutualfunds and has been facilitated bythe clarification of floating interestcalculation. More recently, firmershort-term interest rates may havespurred demand.

The proportion of fixed-ratetri-party repo business wasunchanged at 82.1% (compared to84.8% in December 2004): theremainder was largely opencontracts (17.1%).

Figure 2.6 – Repo rate analysis

Although the largest share ofoutstanding repo contractscontinued to have less than onemonth remaining to maturity(61.9%), the proportion has beenfalling since June 2004 (68.1%)and reached its lowest level since

18 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

December 2004 June 2005 December 20051 day 17.7% 17.6% 16.1%2 days to 1 week 22.4% 20.2% 21.0%1 week to 1 month 25.9% 27.5% 24.8%>1 month to 3 months 17.5% 13.9% 17.6%>3 months to 6 months 5.8% 7.0% 7.0%>6 months to 12 months 5.4% 9.9% 5.2%>12 months 5.1%forward-start 5.2% 3.8% 3.2%

Maturity analysis (Q1.6)Table 2.7 – Maturity analysis December 2004 to December 2005

Classic repo83.0%

Documentedsell/buy-back11.5%

Undocumentedsell/buy-back5.5%

Fixed rate82.3%

Open7.7%

Floating rate10%

December 2001 (58.3%).Contracts with between one andthree months remaining tomaturity repeated the seasonalpattern identified in previoussurveys, contracting in June andrecovering in December. Contractswith more than six months havecontinued to recover from the lowrecorded in December 2004.

For the first time, the surveyasked participants to break outcontracts with more than 12months remaining to maturity. Theshare of this reported business was5.1%. One year had previouslybeen seen as a barrier to repo,largely because of tax issues in theUK, but these were recentlyresolved, allowing a longer-termrepo market to develop.

Forward-forward reposcontinued to contract in relativeterms touching a record low of 3.2%.

The bulk of outstandingcontracts reported directly by theATSs had a remaining term tomaturity of one day (77.7%compared to 77.1% in June 2005).The share of ATS business withbetween 2 days and 1 weekremaining to maturity fell to 9.4%from 13.4% in June 2005, butthere was an increase in businesswith remaining terms to maturityof between 1 week and 1 month(8.4% compared to 6.8% in June2005) and more than 1 month(4.5% compared with 1.6%).

There was a major change inthe maturity distribution of tri-party repo business between June2005 and December 2005. In thelatest survey, the share ofoutstanding tri-party contractswith one month or less remainingto maturity fell to 55.2% from71.8% in June 2005 and 74.9% inDecember 2004.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 19

1D 2-7D 8D-1M 1-3M 3-6M 6-12M >12M Forward0

5

10

15

20

25

30

35

Figure 2.7 – Maturity analysis June 2001 to December 2005

Concentration analysis

Table 2.8 – Concentration analysis December 2004 to December 2005

Figure 2.9 – Concentrationanalysis

Although the apparentconcentration of repo business ishigh, this does not mean that thelargest institutions havecommensurate market power. Abetter measure of marketconcentration – often used incompetition analyses – is theHerfindahl Index. The Index for thesurvey was unchanged at 0.043recorded in June 2005.

20 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

December 2004 June 2005 December 2005top 10 58.4% 55.5% 54.3%top 20 80.4% 78.2% 77.0%top 30 91.5% 90.1% 88.6%other 9.5% 9.9% 11.4%

1 The Herfindahl Index is the sum of the squares ofmarket shares divided by the square of the sum ofmarket shares. The higher the index, the lower thedegree of competition. If the index is higher, the morea single institution has a dominant market share and/orthe more insignificant the market shares of all the othersurvey participants. A market in which severalinstitutions have very large market shares can thereforehave a relatively low index.

Top 1054.3%

Top 11-2022.7%

Top 21-3011.6%

Remainder11.4%

Product analysis (Q2)

The share of total businessaccounted for by securities lendingand borrowing conducted on repodesks dropped to 17.7% from19.2% in both June 2004 andDecember 2004. The share of fixedincome securities (as opposed toequity) recovered to 90.3% from88.6% in June 2005, but was stillwell below the 94% reported inDecember 2004.

Figure 2.8 – Product analysis

Repo82.5%

SecuritiesLending17.5%

CHAPTER 3:CONCLUSION

The ICMA survey on December7, 2005 continued to demonstratethe enormous size of the Europeanrepo market by setting theboundary for the minimum size ofthat market at EUR 5,883 billion interms of outstanding contracts. Itagain revealed healthy year-on-year growth, this time of betweenabout 15% and 18%.

The share of electronic tradingadvanced to a record 24.7% ofreported business and there wassome lengthening of the averageterm to maturity of electronicbusiness.

Tri-party repos stabilized at10.4%, below its peak of 11.2% inDecember 2003 but well up on thelevels seen in earlier surveys.

The survey identified asignificant share of repo businessbeyond one year. Although suchlong term repos have been tradedin some European markets forsome time, recent growth is likelyto have been encouraged by taxchanges in the UK. The averageterm to maturity of both deliveryand tri-party repos lengthened,reflecting, in part, seasonal factors(e.g. banks locking in funding overthe year-end with longer termtransactions).

One of the key developmentsin the latest survey was rapidgrowth in floating-rate repos.

Interest in this instrument,traditionally associated with theFrench market and demand frommoney market mutual funds, hasbeen growing for some time. Aboost to business may have beengiven by the clarification(facilitated by the ERC) of theappropriate method of calculatingfloating interest and expectationsof rising short-term interest rates.

The share of the euro hascontinued to decline. The shareof sterling increased and therewas a dramatic increase in theimportance of the US dollar intri-party repo.

German securities reassertedtheir importance as collateral in theEuropean market and there was asurge in the use of equity in tri-party repo. There was no furthergrowth in the share of non-government collateral.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 21

CHAPTER 4: FIVE YEARSOF THE ICMA REPOSURVEY

2001

The first ICMA repo surveytook place on 13 June 2001. It wasnot an auspicious year to start. Thefinancial markets were stillsuffering from the bursting of thedot.com bubble which hadtriggered an abrupt globalslowdown. Subsequently, they werehit by the market disruption causedby the terrorist attack on the US onSeptember 11. Immediatelyfollowing these events, centralbanks rapidly injected liquidity intothe financial system in order tomaintain confidence. Such a cleardirection to short-term interestrates is likely to have encouragedposition-taking and a very largeincrease in repo activity wasrecorded by the survey betweenJune and December. However, it isdifficult to be confident that theincrease recorded by the surveyprovided an accurate measure ofthis change in activity. Lookingback over the run of surveys, theJune 2001 survey looks anomalousand is probably best excluded fromany review of trends.

2002

By early 2002, the marketshad become apprehensive about areversal of the easy monetarypolicy that followed 9/11 given theresilience of the financial systemand expectations of an imminent

global recovery. This concern wasreflected in steepening yieldcurves. However, in April 2002, therelease of poor US economic datasuddenly reversed investorsentiment and started to flattenforward curves in both US dollarsand euros. Despite subsequentlystrong economic data, optimismeroded over the following sixmonths and the fixed incomemarkets priced in sharp downwardrevisions in expected economicgrowth. Pessimism about economicrecovery was aggravated byfurther damage to investorconfidence from a number of high-profile corporate failures (startingwith the collapse of Enron inDecember 2001). Between lateJune and mid-October, creditspreads soared to the highestlevels for over a decade. Notunsurprisingly, the repo marketgrowth recorded in the ICMA reposurvey between December 2001and June 2002 was an anaemic2.9% (this and subsequent growthrates have been recalculated for aconstant sample of participantswho took part in all ten surveys).

In October 2002, as bondyields reached record lows,investors became nervous aboutthe existence of a bond marketbubble. Hopes of new interest ratecuts built up but cuts did notmaterialise until November 2002 inthe US and December 2002 in theeurozone. This nervousness wasreflected in a contraction in repoactivity between June 2002 andDecember 2002 of 8.2%.

22 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

2003

In March 2003, the onset ofwar in Iraq and a fall in oil pricesrevived optimism in the fixedincome markets, leading to steeperforward curves. Corporateretrenchment and balance sheetrestructuring restored confidencein credit markets at a time wheninvestors regained their riskappetite and began to seek higheryields than those available ongovernment bonds. Corporatebonds rallied strongly into the firsthalf of 2003. Increased riskappetite appeared to be reflectedin repo market growth betweenDecember 2002 and June 2003of 18.4%.

However, unusually low short-term interest rates following cuts inofficial rates by the ECB and Fed inJune 2003 appeared to leave thefixed income markets increasinglyuncertain about further centralbank moves in response to possibledeflationary pressures, particularlyin the US. In the summer, fixedincome markets were hit by asharp global sell-off. Repo marketactivity suffered and growthbetween June and December 2003was only 6.7%.

2004

In March 2004, positivemacroeconomic data in the USbrought forward expectations ofmonetary policy tightening by theFed and led to a renewed sell-off inthe US fixed income market. At this

stage, euro rates decoupled fromUS rates in recognition of the moresluggish economic performance ofthe European economy. However,measures of interest rate VaR inthe investment banking sectorpeaked in Q2 2004 after risingcontinuously since Q2 2002indicating greater position-takingand was reflected in strong banktrading revenues, which mayexplain the robust growth of15.5% recorded in the repo marketbetween December 2003 andJune 2004.

Despite the tightening ofmonetary policy started by the Fedin June 2004, market conditionseased. Long-term yieldsunexpectedly fell, equity pricesrose and credit spreads narrowed.However, weak US employmentdata in July and August 2004caused investors to reassess thelikelihood of further monetarytightening and triggered a globalfixed income rally. Unfortunately,over the remainder of the secondhalf of 2004, lower price volatilityand lower trading income,particularly in fixed-income, weretranslated into a slowdown inthe growth of the repo marketto 5.9%.

2005

Although many financialmarkets retreated in March andApril 2005 due to increased riskaversion and inflation concernsafter new US data rekindled fearsof an early tightening in monetary

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 23

policy, bond prices quicklyrecovered as weak economicprospects in Europe caused long-term yields in the eurozone todecline. German government bondyields hit all-time lows in May. Inthese conditions, the repo marketrecorded comfortable growth of10.9% between December 2004and June 2005.

In the second half of 2005,long-term yields in the eurocontinued to fall and, by September,reached the lowest levels seen for acentury. Subsequently, improvedeconomic growth prospects, helpedby a decline in oil prices, started toreverse the fall in long-term yieldsand, as indicated by a steepening inthe front of the forward curve,raised expectations of an earlytightening of monetary policy by theECB. Against this background, therate of growth recorded in the repomarket in the second half of 2005continued to be steady at 9.2%.

Table 4.1 – Growth rates of asample of survey participantswho have contributed to allten surveys

Trends in the European repomarket

At the level of aggregation andthe frequency at which the surveyis conducted and given the partialnature of the sample ofparticipants, it is difficult to spotand interpret changes in thecomposition of business in theEuropean repo market. However,the run of survey results andanecdotal evidence suggests anumber of broad developmentshave taken place in the structure ofthe market since the survey began.

Counterparties. Electronic repotrading on ATSs has shown cleartrend growth in market share,while the trend in the share ofvoice-brokers has been downward.While electronic trading has beenobserved to prosper in moderatelyvolatile markets, it is not possibleto discern such variation from thesurvey numbers.

Tri-party repo moved up a notchin December 2003 but appears tohave since settled on a plateau interms of market share. There is ahint of a link between the growth ofnon-government bond repo andtri-party repo, which is supportedby anecdotal evidence that mosttri-party collateral is non-government bonds and equity.

24 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Survey date Growth over the previous six months

December 2005 +9.2%June 2005 +10.9%December 2004 +5.9%June 2004 +15.5%December 2003 +6.7%June 2003 +18.4%December 2002 -8.2%June 2002 +2.9%

Figure 4.1- Counterparty analysis

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 25

Figure 4.2 – Geographical analysis

Figure 4.3 – Currency analysis

0

10

20

30

40

50

60

ATS voice-broker direct bilateral direct tri-party

Dec-01Jun-02Dec-02Jun-03Dec-03Jun-04Dec-04Jun-05Dec-05

%

0

10

20

30

40

50

60

domestic cross-border anonymous ATS

Dec-01Jun-02Dec-02Jun-03Dec-03Jun-04Dec-04Jun-05Dec-05

%

Geography. The share of cross-border trading has grown at the expense ofdomestic trading. This would fit with broader developments in the financialmarkets, which have seen cross-border business flows concentrated in majorbanks acting as hubs in their domestic markets for local institutions andproviding cross-border links to major overseas financial centres.

Currency. The share of the euro is on a downtrend, the counterpart to which isgrowth in the shares of sterling and the US dollar. Taking account of exchangerates (the data is all in euros) would, if anything, accentuate these.

0

10

20

30

40

50

60

70

80 Dec-01Jun-02Dec-02Jun-03Dec-03Jun-04Dec-04Jun-05Dec-05

EUR GBP USD DKK, SEK JPY other

%

26 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Figure 4.4 – Collateral analysis

Maturity. There is a clear seasonal pattern in short-dated repos, with the shareof short dates rising in December and falling back in June. It is assumed thatthis pattern reflects banks locking in longer-term financing over year-ends. Theshare of short-term repos with up to three months remaining to maturity hastended to increase at the expense of longer-term repo. Forward-forward reposhave faded in importance. Given their use in interest rate risk-taking, this mayreflect the lack of clear trends in short-term interest rates.

Figure 4.5 – Maturity analysis

Collateral. The share of non-government collateral (as a percentage of EUmarkets) is growing steadily. It is generally assumed that this reflects the growthin credit repo. The share of German collateral, while remaining dominant, hasfluctuated widely. However, the shares of Italian and Belgian collateral, the mainsources of general collateral in the euro repo market, have tended to decline. UKand more especially non-eurozone collateral has taken a growing market share.

0

10

20

30

40 Dec-01Jun-02Dec-02Jun-03Dec-03Jun-04Dec-04Jun-05Dec-05

Belgian Dutch French German Italian Spanish othereurozone

UK Denmark,Sweden

US other

%

0

10

20

30 Dec-01Jun-02Dec-02Jun-03Dec-03Jun-04Dec-04Jun-05Dec-05

1 day 2 days to1 week

1 week to1 month

1-3months

3-6months

over6 months

over6 months

%

CHAPTER 5: THE WORKOF THE EUROPEANREPO COUNCIL

The European Repo Council(ERC) is an important focus for the European repo market. It is the forum where the repo dealer community meets and forges consensus solutions to the continually emerging,practical problems of a rapidlyevolving marketplace. In this role, it has been consolidating and codifying best market practice. Moreover, the contact and dialogue that takes place atthe ERC underpins the strongsense of community and common interest that characterisesthe professional repo market in Europe.

The ERC is also responsible forpromoting the wider use of repo inEurope, particularly among banks,by providing education and marketinformation. It has also proveditself an effective partner to financeministries, treasuries, debtmanagement agencies, centralbanks, regulators and committeesof wise men across Europe, notleast in countries without smoothlyfunctioning repo markets, byexplaining the importance of theinstrument to the efficientfunctioning of financial marketsand helping the authorities tounderstand the positive andnegative implications of their legal,tax and regulatory proposals.Without such a representativebody, the repo market would oftenbe the victim of the unforeseenconsequences of official initiatives.

The origins of the ERC

The ERC was established in December 1999 by the InternationalCapital Market Association (ICMA, which was then called the InternationalSecurities Market Association or ISMA). It had started life back in 1992as the Repo Sub-Committee of ICMA’s Council of Reporting Dealers.ICMA, in association with TBMA (The Bond Market Association, then calledthe Public Securities Association or PSA) and with the assistance of aworking group of repo professionals, had just published the PSA/ISMAGlobal Master Repurchase Agreement (GMRA) to provide legally effectivedocumentation for the nascent cross-border European repo market. TheRepo Sub-Committee was set up as a permanent group to monitor theperformance of the GMRA and address the ongoing needs of the repodealer community.

By 1999, the pace of change in the repo market led ICMA to transformthe Repo Sub-Committee into a self-standing body operating under ICMAauspices. The Sub-Committee became the International Repo Council(IRC), a body of ICMA members active in the international repo market.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 27

Representing the repo market

The list of official initiatives towhich the ERC has had to respond is long, but the mostconstant topic has perhaps been the implementation of therecommendations of theGiovannini Group on the removal ofbarriers to greater efficiencyin European financial markets,not least the fragmented regionalclearing and settlementinfrastructure. This has involvedthe ERC in regular contact with theEuropean Commission and ECB,the various bodies created totackle the Giovannini barriers suchas the Clearing and Settlement

Advisory and Monitoring ExpertGroup (CESAME), as well as theinfrastructure providers: thenational and international clearingand settlement depositories(ICSDs), and the central clearingcounterparties (CCPs).

The ERC is represented on theECB Money Market Contact groupand the Bank of England’s StockLending and Repo Committee(SLRC). It has also establishedlinks with numerous other privatesector groups across a wide range of market issues, not least,the ACI and, more recently, the International Swaps andDerivatives Association (ISDA).

28 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Its governing board is the International Repo Committee (IRCCommittee), which consists of two representatives appointed by regional repocouncils, which in turn comprise those IRC members that are active in the repomarket of a particular geographic area. The regional repo councils are to beestablished by the IRC Committee for those geographic regions in which itconsiders there to be a reasonable number of ICMA members active in therepo market and a reasonable level of repo dealing. So far, the ERC is the onlyregional repo council that has been formed, but the IRC is in the process ofconsidering whether to establish Asian and Japanese Repo Councils.

Membership of the ERC is open to any ICMA member who hascommenced, or has undertaken to commence, a dedicated repo activity, iswilling to abide by the rules applicable to members of the IRC and hassufficient professional expertise, financial standing and technical resourcesto meet its obligations as a member of the IRC. Membership of the ERC isgranted by the IRC Committee in consultation the ERC Steering Committee.

The ERC meets twice a year (usually in February/March and September)at different financial centres across Europe. The Steering Committee nowcomprises 19 members elected annually and meets four times a year.

More information about the ERC and IRC is available on www.icma-group.org.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 29

Repo documentation

A core responsibility of the ERCand one of its original raison d’êtres isto assist ICMA in maintaining thelegal documentation which underpinsthe safe functioning of the cross-border repo market, specifically, theGlobal Master RepurchaseAgreement (GMRA). Since the firstversion of the GMRA was published in1992 (as the PSA/ISMA GMRA orGMRA 1992), revisions have beenbrought out in 1995 (the TBMA/ISMAGMRA or GMRA 1995) and 2000(GMRA 2000) to take account ofmarket developments andincorporate improvements suggestedby experience. Thus, the GMRA 1995incorporated lessons learnt in theBarings crisis of 1995, in particular,the need for more time to liquidatecollateral. The GMRA 2000 reflectedthe experience of the LTCM, Russianand Asian crises of 1997-98 and theneed to liquidate illiquid collateral incrisis conditions.

The legal work in maintainingthe GMRA is the responsibility of theLegal Department of ICMA, with theassistance of the law firm FreshfieldsBruckhaus Deringer. However, theERC provides the practicalperspective that must inform thelawyers if the agreement is tocontinue to be used by the marketand keep its position as the generallyaccepted market standard for cross-border repos. An example of the roleof the ERC in this process is given byits equities working group during2002-03 in the adaptation of theEquity Annex to the GMRA 2000.

One of the regular items ofbusiness on the agenda of the ERC isthe annual updating of the legalopinions, covering the 1995 and2000 versions of the GMRA as well asthe GMRA 1995 amended by theamendment agreement to the GMRA1995. The legal opinions cover boththe enforceability of the nettingprovisions of the GMRA in differentjurisidictions, as well as the GMRA asa whole. The opinions also addressthe issue of recharacterisation risk(in respect of both the transfer ofsecurities and the transfer of margin)and are commissioned by ICMA,partly in conjunction with TBMA.Currently, opinions for 28 countrieshave been secured by ICMA aloneand 24 jointly by ICMA and TBMA. Inaddition, ICMA is commissioning newlegal opinions in three additionaljurisdictions, which are currentlybeing reviewed and is monitoringlegal developments in anotherfive jurisdictions with a view toascertaining at what stage a cleanopinion can reasonably be expectedfor each of these jurisdictions . At thebehest of the ERC, ICMA alsodecided to extend the scope of the2006 update opinions for 21countries to also cover insurancecompanies, hedge funds and mutualfunds as parties to the GMRA (inaddition to the companies, banksand securities dealers alreadycovered by the current opinions).The annexes to the GMRA deal withthe adaptation of the standardagreement to particular types oftransactions (e.g. buy/sell-backs,equity and money market collateral,and agency transactions) or to

30 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

particular markets (e.g. Australia,Canada and Italy). Three annexes tothe GMRA and supporting legalopinions have been produced for theUK gilts market by the Bank ofEngland, for the Australian marketby the Australian Financial MarketsAssociation (AFMA) and for Japanesesecurities by the Japanese SecuritiesDealers Association. A full list of the opinions that have beencommissioned or secured in recentyears and the current list of annexesto the GMRA 1995 and the GMRA2000 are set out in Appendix D.

In October 1999, new repodocumentation in the form of theEuropean Master Agreement (EMA)was published jointly by theEuropean Banking Federation, theEuropean Savings Bank Group andthe European Association of Co-operative Banks. This was designedto provide a harmonised form ofagreement that could be usedwithin all the domestic markets thatwere part of the eurozone byallowing a choice of legal regimeand language. It also sought tocombine the documentation forrepos and securities lending, andhad ambitions to include foreignexchange and derivatives.However, some felt that the EMAcould be employed to documentcross-border transactions withinthe eurozone. The EMA receivedthe endorsement of the ECB.

Although many in the repomarket were dismayed at thethought that the standardisation ofcross-border repo documentation

achieved by the GMRA could start tounravel, the ERC took an impartialand pragmatic approach by insistingthat it was up to market participantsto make commercial decisions onwhich documentation to use, but italso sought to ensure that therewas no legal or operational basisrisk between the two agreements.

In July 2004, followingdiscussions with the ERC, ISDAannounced that, in the absence ofclear market demand, it would notproceed to expand its 2002agreement to include repos. In thesame month, following discussionswith the International SecuritiesLending Association (ISLA), theERC decided that there was noclear need for a stock lendingannex to the GMRA. However, theERC reiterated the need for closerco-operation between marketassociations with a view toultimately promulgating a single,multi-product agreement thatwould include repos.

Codifying best market practice

One of the tasks which regionalrepo councils may undertake is thepublication of area-specific tradingguidelines and recommendations.The ERC published its Repo TradingPractice Guidelines with effectfrom October 1, 2003. TheGuidelines do not restrict theflexibility of parties in the negotiationof particular transactions, but arerecommendations as to whatconstitutes best market practice forall types of participant (dealers,

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 31

inter-dealer brokers and ATSs) in theEuropean wholesale repo market.They are the product of discussionwithin the ERC Steering Committeeand consultation with ICMA, TBMAand ACI, and with dealers andbrokers active in the market.

A similar initiative has been thepublication in August 2001 of a BestPractice Guide to RepoMargining, which drew on the workof “Market Usances” working groupof the German ACI. The Guide wasrevised and republished inSeptember 2005.

ERC Repo Trading PracticeGuidelines

The sort of issues addressedby the Guidelines can be seenfrom the section headings:

1 Conduct of Business2 Legal Agreement3 Confidentiality4 Screen Guidelines5 Recommended Time Frames

for Pricing Transactions6 General Collateral Repo

Allocations7 Recommended Delivery Size8 Marking to Market9 Confirmation of Forward

Repos10 Obligation to Make Coupon

Payment11 General Collateral12 Business Day Convention

A copy of the full Guidelinescan be downloaded from theICMA website.

Best Practice Guide to RepoMargining

The Guide answers thefollowing questions:

1 What prices are used?2 How is the mark-to-market

calculated?3 At what value date is the

margin call performed?4 What deadlines are

stipulated for margin calls?5 What collateral has to be

accepted?6 How is interest paid on cash

margin?7 At which margin level is a

margin call carried out? Doesthe margin call only coverthe threshold or is the assetsecured up to 100%? Isthere a “Minimum TransferAmount”? To what extent domulti-branch contracts,netting, the spreading of thethreshold over differentbranches and mixedcollateral classes (equity andbond business) impactmargin call procedures?

8 Is a substitution of margincollateral possible?

9 Which trades have to beincluded in the daily “mark-to-market”?

10 How are forward tradesincluded in marking tomarket?

11 How should future dividendsand/or coupon paymentsaffect the margining process?

12 Is a trade “repricing”acceptable?

13 What happens if margincollateral is not delivered(event of default)?

14 Should margin collateral bereturned automatically?

15 How to handle “haircuts”?

A copy of the full Guide can bedownloaded from the ICMAwebsite.

32 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Harmonising market conventions

The efforts of the ERC topromote the development of anorderly repo market often involvethe clarification of marketconventions, a decision on which oftwo competing conventions shouldapply, modification of conventionsor the introduction of newconventions, and the amendmentof market practices.

One of the very first initiativesby the ERC was the definition inMay 2001 of European generalcollateral. This list is available onthe ICMA website.

Another example is theclarification of the rules on fixingday counts. Given that repoinvolves both cash and collateral,there is an inherent conflictbetween money market and bondmarket conventions. Confusionover day count conventions wasalso created by the emergence ofan active market in forward-startrepos, for which it is necessary tofix the start and end of the forward-forward period. Some participantsopted to fix both forward datesfrom the spot date: others chose tofix the far forward date from thenear forward date. In September2003, the ERC clarified that moneymarket conventions should apply inthe repo market (i.e. the modifiedfollowing business day conventionand the end/end rule). In the caseof forward-start repos, this meansfixing the far forward date from thenear forward date.

The ERC has also helped toharmonise the convention on thecalculation of interest for repospriced at floating rates (typicallyEONIA) after the idiosyncraticpractices of the well-establishedFrench market (not compoundinginterest) caused confusion fornewer users in other Europeanmarkets. Similarly, the ERC wasable to highlight and seek aresolution of the differences thatemerged between the practices ofICSDs and the market in the fixingof the EONIA for the last day ofinterest accrual on a floating-raterepo (the former applied the S-2fixing to the calculation of the lasttwo days of interest accrual).

In a recent case, the ERC hadto modify market convention inorder to deal with the unusualcircumstances of negative reporates. The market convention hasbeen that, in the event of a failureto deliver collateral at the start of arepo, the transaction should onlybe cancelled by mutual agreementand interest should continue toaccrue on the purchase price untilthe scheduled repurchase date oruntil the non-failing party applies a“mini close-out” under paragraphs10(g) or (h) of the GMRA. However,if a piece of collateral trades at anegative repo rate and the sellerfails to deliver the collateral at thestart of a transaction, theconvention means that interestaccrues to the failing seller! Theconvention could thereforeencourage the selling of collateralthat is trading at negative repo

rates by parties with no intentionof delivering. After muchdiscussion, the ERC proposed anamendment to subsection G of theICMA rule book with effect fromJanuary 1, 2005 to the effect that,where repo rates are negative,

the buyer can terminate the

transaction at any time during the

term of the transaction and that,

for every day that the seller fails to

deliver, the repo rate should be

deemed to be zero.

Other issues concerning conventions or market practices dealtwith by the ERC

Unilateral termination of failed repos in the French market

The ERC has conveyed market concern at the practice in the Frenchmarket of unilaterally cancelling failed transactions in the event of afailure to deliver collateral at the start of the transaction. It is generalmarket practice that a failed transaction remains in force unless it expiresor the non-failing party calls a “mini close-out” under the GMRA, and thatthe failing party must pay the non-failing party the interest accruedduring the period before the transaction expires or is closed out.

In response to representations by the ERC and others, Euroclear Franceintroduced in 2006 a “recycling” facility in its RGV settlement system whichautomatically re-enters for seven calendar days the second leg of a repo withan original term to maturity of one week or more that has failed to settle dueto technical reasons. If a transaction continues to fail for seven calendar daysor it has a term to maturity of less than one week, it is recommended thatthe parties mutually agree to terminate the transaction, manually calculatethe payments including interest due to the non-failing party and confirm thetermination by fax. For technical reasons, it has not been possible to recycletransactions with terms of less than one week, which unfortunately includesthe active tom/next repo market.

Forced settlement in Greek bonds

The ERC is currently in discussion with the Greek primary bond dealers’association about procedures introduced by the Bank of Greece at the behestof the primary dealers’ association to deal with failed transactions in Greekgovernment bonds. These procedures do not allow bond transactions to failand instead force an auction at penal rates at the end of the daily settlementcycle. The risk of a forced auction reduced liquidity in the Greek repo market,with some dealers refusing to accept Greek government bonds as part of theeuro-denominated general collateral basket. Forced settlement in Greece isone of a number of examples of problems inadvertently caused for the repomarket by initiatives in the cash bond market.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 33

34 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

Buy-in rules for failed deliveries of bonds

In the cash bond market, failure to deliver bonds can trigger a “buy-in” by the non-failing party. The rules for buy-ins are set out in Rule 454of the ICMA rule book. In the repo market, however, different rules apply.A failed repo can be allowed to expire or the non-failing party can call a“mini close-out” under paragraph 10(g) or (h) the GMRA. The ultimateeffect of both rules is similar but the timing of a buy-in used to be muchlonger than a mini close-out (a minimum of 12 business days as opposedto five). This difference in rules gave rise to a basis risk in cases where aparty buying a bond in a cash trade and repoing it out suffered a fail onthe cash trade or a party selling a bond in a cash trade and reversing it insuffered a fail on the reverse repo. Following approaches by the ERC, theICMA agreed, with effect from January 1, 2004, to amend its buy-in rulesby shortening the minimum period until a buy-in to five business days.

Confirmation of the second leg of a buy/sell-back

The ERC has sought to reform the market practice of confirming thesecond leg of a buy/sell-back separately from the first leg and delayingthe second confirmation until two days or less before the repurchasedate. This practice allowed mismatched trades in long-term sell/buy-backs to remain undetected for long periods of time. At the request of theERC, the ICMA published a letter in April 2004 calling on firms active inbuy/sell-backs to confirm both legs of a transaction at the same timepromptly at the start of the transaction.

Promoting market development

The ERC has on occasiontaken a pro-active role inpromoting the introduction into therepo market of functionalities andfacilities to enhance marketefficiency.

A functionality that would bewelcomed by repo dealers is thewider availability of rights ofsubstitution outside the tri-partyrepo market and/or a GC financingfacility similar to that in the US

market whereby dealers can tradeagainst a standardised basket ofcollateral which allows them toallocate collateral on a net basis atthe end of the day. So far, littleprogress has been made in theEuropean market as a whole, butEurex Repo appears to have hadsome success with its the Euro GCPooling facility.

The ERC has been activelyinvolved with the EuropeanBanking Federation in the creationand promotion of Eurepo. This is a

euro repo rate index launched onMarch 4, 2002, to provide abenchmark for secured euromoney market transactions. It ishoped that Eurepo will serve notonly as a valuation rate but alsoprovide the settlement rate forderivative contracts on repo. TheERC is represented on the EurepoSteering Committee.

The emergence of an activemarket in forward-start reposbrought to the fore the problem ofhow to deal with the divergence ofcash and collateral values beforethe forward purchase date. Thesolution developed in the ERC andincorporated in Annex I of theGMRA 2000 is to allow thepurchase price or nominal value ofcollateral to be adjusted by mutualagreement prior to the forwardpurchase date or to allow a marginto be called before that date.

The ERC has promoted theavailability of tri-party reposervices as a useful facility formany participants and a means ofreducing operational risk. It hasworked closely with tri-party repoproviders and has also tackledobstacles such as accountingdifficulties with the use of tri-partyrepo in Italy.

Another infrastructuredevelopment that has taken centrestage on the ERC’s agenda hasbeen electronic trading acrossautomatic repo trading systems(ATSs). In general, the role of theERC has been to inform and update

members, and to liaise with theATS providers to ensure that theirsystems provide stable and orderlytrading venues. Occasionalproblems have arisen which theERC has sought to address such asthe introduction of buy/sell-backson MTS Germany. On the otherhand, ATSs have been able toassist the ERC with theintroduction of uniform tradingdays in the eurozone.

Similarly, the ERC has beensupportive of central clearingcounterparties (CCPs) and hasencouraged the development of awider range of central clearingservices. It has also pressed allregulators to recognise the benefitsof netting through a CCP with azero risk weighting. The ERC hassupported initiatives to integratethe clearing infrastructure inEurope, while not pre-judging theultimate configuration of providers.It welcomed in principle the jointventure between Clearnet and theCassa di Compensazione eGuarantia (CCG) to introduce aCCP in Italy, and the introduction ofa CCP in Spain, but expresseddisappointment that suchinitiatives did nothing to promotecross-border clearing andsettlement in Europe.

The ERC is often called upon toadvise on emerging repo marketsor repo markets undergoingreform. The ERC has beenparticularly active in recent monthsin Russia.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 35

One of the major obstacles toa smooth functioning repo marketis inappropriate tax treatment. Taxissues have been an issue tackledby the ERC in several Europeanmarkets including Spain. The ERChas also assisted the Japan Centerfor International Finance in itswork on the local tax issues holdingback repo in Japan.

Tackling operational issues

The ERC also frequently has todeal with operational issues thatare periodically thrown up in themarket.

A continuous source ofconcern has been failure to delivercollateral. The ERC has tried towork with the various CSDs totackle the underlying technicalcauses of fails in the cross-bordermarkets. It has also attempted tohelp mitigate the impact of fails byencouraging market participants totake precautions such as theshaping (or breaking up) of bonddeliveries into parcels of EUR 50million, GBP 50 million, USD 50million or JPY 5 billion. A letterrecommending this practice waspublished by ICMA in December2003. On the other hand, the ERChas argued against proposals bysome authorities to imposepenalties for failure to deliver as anunduly draconian response to agenerally technical problem.

A number of the operationalproblems tackled by the ERC havebeen created by changes to

securities settlement systems.Examples are the problems causedby the introduction of the ExpressII settlement system in Italy andnew procedures in the Greeksecurities settlement system (seeabove). The ERC tries to ensurethat the authorities are aware ofthe problems and support theirefforts to develop solutions.

More generally, the ERC hasaddressed the consequences of the fragmented clearing andsettlement system in Europe byencouraging greater co-operationbetween the ICSDs. In 2003, itchaired a meeting between theICSDs and some central banks todiscuss the problem of settlingGerman and other bond transactionsover the Bridge betweenClearstream and Euroclear.Following this meeting, the ICSDsagreed to upgrade the Bridge toallow real-time intra-day settlement.

Given the fragmentation ofclearing and settlement in Europe,the ERC has had a special interestin the intra-day securitiesborrowing facilities offered by theICSDs. It has been involved inintensive discussions to improvethe availability of these facilitiesand reduce their cost.

Keeping the market updated

The ERC takes an active role insupporting efforts to promote thedevelopment of the European repomarket by providing a venue forinformation about market

36 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

initiatives to be presented to therepo dealer community. In thisrole, the meetings of the ERC havereceived presentations, amongother things, on:

ERC meeting: September 21,2005

• EONIA swap index project.• Repo trade matching.• The tax treatment of long-term

repos.• Settlement between the ICSDs

and the German CSD.• Changes to the collateral

framework of the ECB.• The activities of the European

Commission’s Clearing andSettlement Advisory andMonitoring Expert Group(CESAME).

ERC meeting: March 17, 2005

• The evolution of securitieslending and borrowinginfrastructure for overnight andintra-day borrowing.

• Reform of the Bank of England’soperations in the sterling moneymarket.

• Update on the work of CESAME,and the legal and tax expertsgroups, on clearing andsettlement.

• Electronic broking by ICAP.• Access to central bank liquidity

in Switzerland.• Settlement initiatives in Europe.• Discussions in the EU

Committee on Payments andSettlement Systems (CPSS) oncross-border collateralisation.

• The Securities OperationsCommittee’s project to reduceoperational risk.

ERC meeting: October 21,2004

• The reduction of operational riskin repo.

• Eurex Euro General CollateralPooling project.

• Bloomberg electronic repotrading platform.

ERC meeting: March 16, 2004

• The electronic repo market inthe eurozone.

• Monte Titoli’s Express IIsettlement system.

• Eurepo.

ERC meeting: September 25,2003

• The Securities Account Certaintyproject.

• The EURIBOR-ACI Short-TermEuropean Paper (STEPS) TaskForce report.

• Equity Finance.• Clearstream’s Bond Advanced

Management for Borrowing andLending (BAMBL) programme.

• The merger of LCH andClearnet.

ERC meeting: February 10,2003

• Cross-border collateral pool taskforce.

• Developments in the Japaneserepo market.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 37

• The Giovannini Report II.• The collateral initiative by

SWIFT.

ERC meeting: September 18,2002

• Use of ABS in repo transactions.• Communication of the EU

Commission on clearing andsettlement.

Educational initiatives

Perhaps one of the most widelyknown initiatives of the ERC hasbeen its educational programme.With the backing of ICMA and theACI, the ERC has run the ICMA-ACIProfessional Repo Market courseeach November since 2002.

The Professional Repo Marketcourse is designed to reinforce thedevelopment of the European repomarket by enhancing theprofessional competence of juniorrepo dealers. However, the marketfocus of the course has also provedpopular with middle and back office staff, regulators, systemsdevelopers and others. The course isdelivered by a unique combinationof academics, experienced marketpractitioners, legal professionals andofficials. The syllabus is organisedand the academic faculty providedby the ICMA Centre at the Universityof Reading. The syllabus changesslightly each year to reflect newdevelopments.

So far, the Professional RepoMarket course has been run in

Brussels (2002, hosted by FortisBank), Frankfurt (2003, hosted byDeutsche Bank), Munich (2004,hosted by HypoVereinsbank) andMilan (2005, hosted by BancaIntesa). In 2006, the course will berun in Madrid.

In October 2005, a specialcourse was run in Hong Kong. This was sponsored by ICMA,TBMA and the ACI. At the invitationof local organisations, anothercourse will be staged this year inBeijing.

The sponsorship of ICMA, ACIand host bank means that coursescost as little as EUR 200 to attend.They attract between 200 and 300delegates. (Anyone interested inattending other educational eventsshould check the ICMA website fordetails).

In addition to its ProfessionalRepo Market course, the ERC hasalso participated in other events.In October 2003, several membersgave presentations at a centralbank conference for the EUAccession countries organised bythe ECB and ICMA and hosted bythe Banca d’Italia.

Repo survey

Last but not least, the ERC hasof course initiated a semi-annualsurvey of the European repomarket. The tenth survey tookplace on December 7, 2005, andthe results are available in thisreport.

38 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

The ERC survey provides theonly regular authoritative pictureof the European repo market and isunique in the detail it offers. It hasestablished the massive scale andrapid growth of repo activity inEurope, and offers importantinsights into the structure of themarket and market trends, notleast, the progress of electronictrading and tri-party repo.

Participants in the surveyreceive in confidence their ownrankings in the various categoriesof the survey and, for many ofthem, the results provide anindependent check on their marketposition.

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 39

ABOUT THE AUTHOR

This report was compiled byRichard Comotto, who is a VisitingFellow at the ICMA Centre at theUniversity of Reading in England,where he is responsible forteaching modules on moneymarkets (including the repomarket) and risk management inthe Centre's postgraduate financeprogrammes. He also lectures onrepo and securities lending onICMA’s Operations CertificationProgramme, and is Course Directorof the ICMA-ACI annualProfessional Repo Market Course.

The author acts as anindependent consultant providingresearch and training on theinternational money, securities andderivatives markets to professionalmarket associations, governmentagencies, regulatory authorities,banks, brokers and financialinformation services.

The author has written anumber of books and articles on arange of financial topics, includingthe foreign exchange and moneymarkets, swaps and electronictrading systems. He takesparticular interest in the impact of‘electronic brokers’ on the foreignexchange market and in the morerecent introduction of electronictrading systems into the bond andrepo markets.

The author served for tenyears at the Bank of England,within its Foreign ExchangeDivision and on secondment to theInternational Monetary Fund inWashington DC.

40 I ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005

APPENDIX A: SURVEYGUIDANCE NOTES

The following extract is basedon the Guidance notes issued toparticipants conjunction with thesurvey that took place onDecember 7, 2005

The data required by thissurvey are: the total value of therepos and reverse repos booked byyour repo desk that are stilloutstanding at close of business onWednesday, December 7, 2005,and various breakdowns of theseamounts.

Branches of your bank in othercountries in Europe may be askedto complete separate returns. Ifyour repo transactions are bookedat another branch, please forwardthe survey form to that branch. Ifbranches of your bank in othercountries run their own repobooks, please copy the survey formto these branches, so that they canalso participate in the survey.Please feel free to copy the surveyform to other banks, if youdiscover that they have notreceived it directly.

General guidancea) Please fill in as much of the

form as possible. For each questionthat you answer, you will receiveback your ranking in that category.

b) If your institution does nottransact a certain type of repobusiness, please enter ‘N/A’ in therelevant fields. On the other hand,

if your institution does that type ofbusiness but is not providing thedata requested by the survey,please do not enter anything intothe relevant field.

c) You only need to givefigures to the nearest million.However, if you give figures withdecimal points, please use fullstops as the symbols for thedecimal points, not commas. Fornil returns, please use zeros, notdashes or text.

d) Please do not re-format thesurvey form, ie change its lay-out,and do not leave formulae in thecells of the underlyingspreadsheet.

e) Include all classic repos,sell/buy-backs and similar types oftransaction (e.g. pensions livrées).There is a separate question (seequestion 2) on securities lendingand borrowing transactions(including securities lending andborrowing against cash collateral).

f) Exclude repo transactionsundertaken with central banks aspart of their official money marketoperations. Other repotransactions with central banks,e.g. as part of their reservemanagement operations, should beincluded.

g) Give the value of the cashwhich is due to be repaid on allrepo and reverse repo contracts(not the market value or nominalvalue of the collateral) that are still

ICMA EUROPEAN REPO MARKET SURVEY DECEMBER 2005 I 41

outstanding at close of business onWednesday, December 7, 2005.This means the value oftransactions at their repurchaseprices.