international accounting standards for life insurance ... · w w w . w a t s o n w y a t t . c o m...

TRANSCRIPT

W W W . W A T S O N W Y A T T . C O M

International Accounting Standards for Life Insurance CompaniesMichael Ross17 July 2003

2

Contents

What is the background? In particular, what is the history, scope and reactions

What is the approach to calculating the reserves under the proposed standard for a life insurer?

What are the implications of the new approach for life insurers?

3

Contents

What is the background? In particular, what is the history, scope and reactions

What is the approach to calculating the reserves under the proposed standard for a life insurer?

What are the implications of the new approach for life insurers?

4

The need for consistent global standards

No-one now questions the need for more effective, more economical and standardised financial reporting worldwide

Historic reporting based on historic cost has often failed to reflect important changes in trading or financial conditionsSeveral types of transactions utilise deferral and matching or ‘smoothing’ approaches e.g. revenue accounting and ‘premium basis’ reserving Many practices also non-transparent with little disclosure

However the global standards now being introduced are intended to present reality from a more consistent but also more volatile market-value-based perspective

5

Towards a global standardThe common and agreed goal - consistent global accounting standards; getting agreement as to ‘how’ is not always so easily achievedThe drive for these latest developments has come primarily from the EU and from stock exchanges around the world

Resistance has come especially from the financial servicesOne of the biggest hurdles is also US GAAP – itself a widely used standard for international groups, but still imperfect

Historically regulators, fiscal authorities and other bodies have also usually based their own requirements on annual audited company accounts (with variations) –will they also in future?

6

Who is involved – international bodies (1)

l The International Organisation of Securities Commissions(IOSCO) - established in 1974, comprises all the major Security Exchange Regulators

l The International Association of Insurance Supervisors (IAIS) founded in 1994 - includes Hong Kong and all other major market regulators from 120 countries

l The International Actuarial Association (IAA) - established in 1895 for individual actuaries, but now re-formed national associations

7

Who is involved International Accounting Standards Board ("IASB")

"To produce a single set of high quality, understandable and enforceable global accounting standards that require high quality, transparent and comparable information in financial statements"

l Insurance project (1997)l Issues paper (Nov 1999)l Comments (May 2000)l Draft Statement of Principles (Dec

2001 – Jul 2002)

Formed in 1973 with the objective ….

l Independent and privately-fundedl 41 International Accounting Standards (“IAS”) or

International Financial reporting Standards (“IFRS”) so farl Already adopted in some countries as domestic standard

and often accepted on stock markets for foreign listed companies

l The Board co-operates with national accounting standard setters to achieve convergence in accounting standards

8

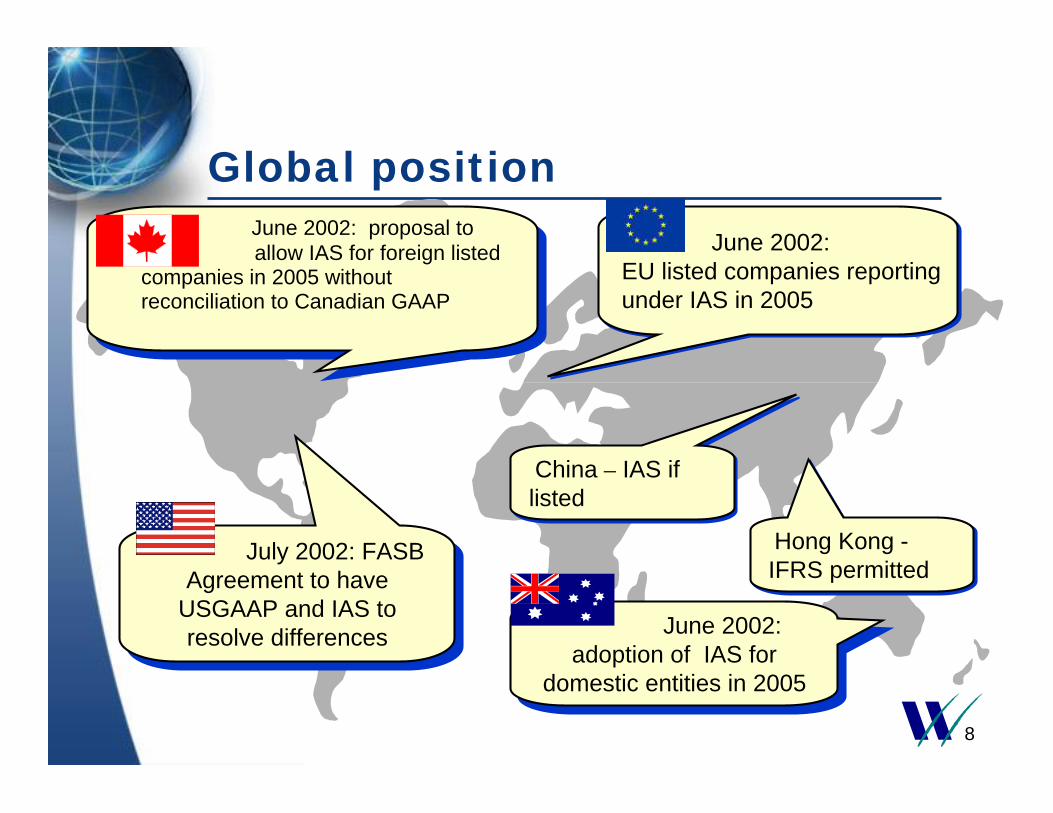

Global positionJune 2002: proposal to allow IAS for foreign listed

companies in 2005 without reconciliation to Canadian GAAP

June 2002: proposal to allow IAS for foreign listed

companies in 2005 without reconciliation to Canadian GAAP

July 2002: FASBAgreement to have

USGAAP and IAS to resolve differences

July 2002: FASBAgreement to have

USGAAP and IAS to resolve differences

June 2002: EU listed companies reporting under IAS in 2005

June 2002: EU listed companies reporting under IAS in 2005

June 2002: adoption of IAS for

domestic entities in 2005

June 2002: adoption of IAS for

domestic entities in 2005

Hong Kong -IFRS permittedHong Kong -IFRS permitted

China – IAS if listedChina – IAS if listed

9

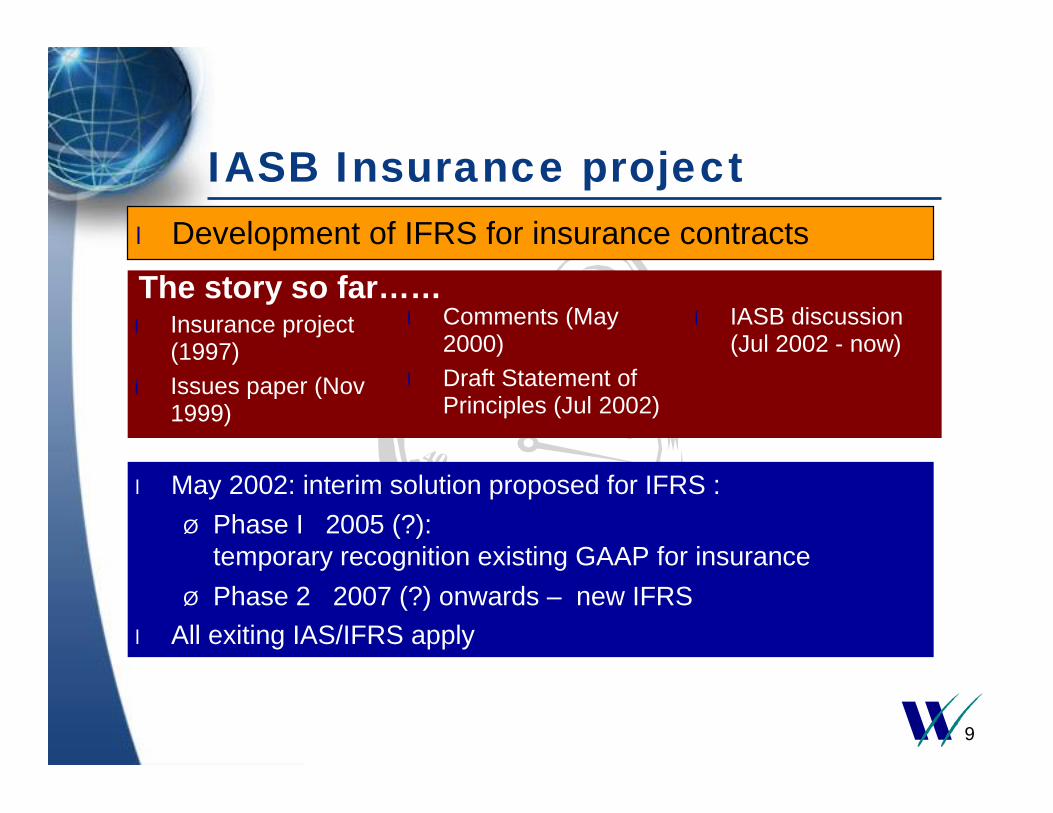

IASB Insurance project

l Insurance project (1997)

l Issues paper (Nov 1999)

The story so far……l Development of IFRS for insurance contracts

l Comments (May 2000)

l Draft Statement ofPrinciples (Jul 2002)

l May 2002: interim solution proposed for IFRS :Ø Phase I 2005 (?):

temporary recognition existing GAAP for insuranceØ Phase 2 2007 (?) onwards – new IFRS

l All exiting IAS/IFRS apply

l IASB discussion (Jul 2002 - now)

10

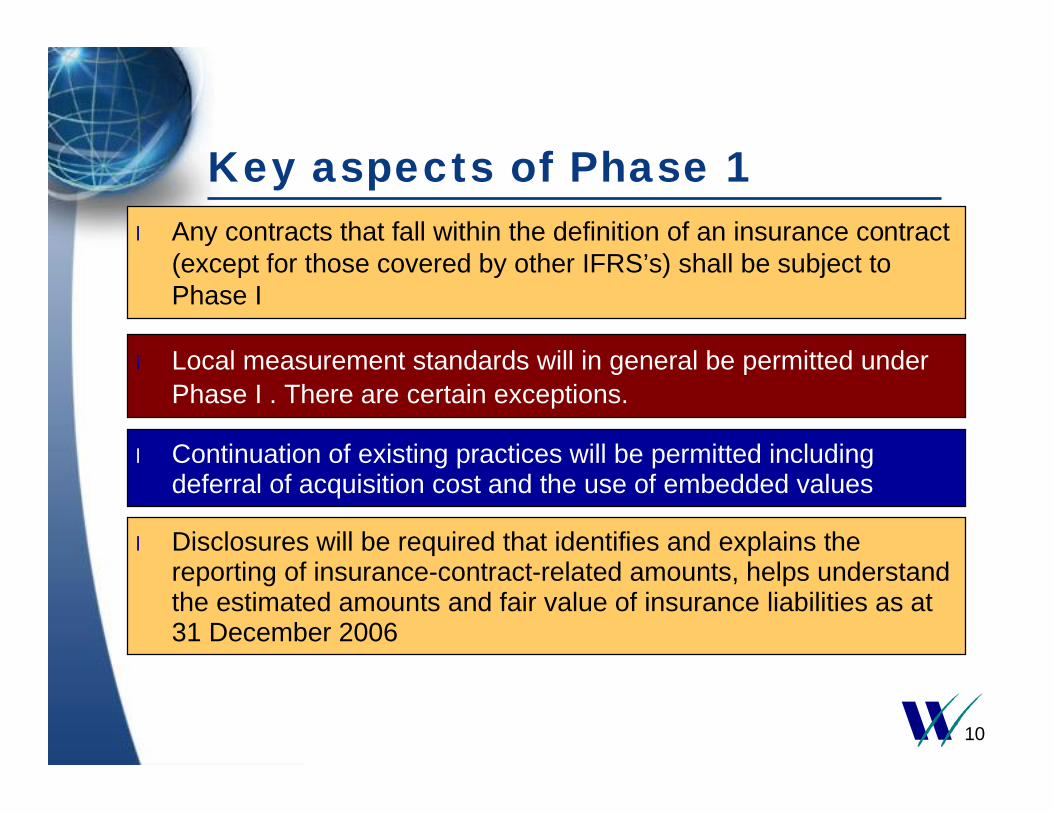

Key aspects of Phase 1l Any contracts that fall within the definition of an insurance contract

(except for those covered by other IFRS’s) shall be subject to Phase I

l Local measurement standards will in general be permitted under Phase I . There are certain exceptions.

l Continuation of existing practices will be permitted including deferral of acquisition cost and the use of embedded values

l Disclosures will be required that identifies and explains the reporting of insurance-contract-related amounts, helps understand the estimated amounts and fair value of insurance liabilities as at 31 December 2006

11

IAS treatment assets and liabilities

2005

Is it an insurance contract?

Liabilities

IAS 39IAS 39

No

Local GAAP

Phase 1: Current GAAP

Yes

Insurance IAS

Phase 2:Insurance IFRS

Yes

IAS 39

Assets

2007?

actuarial reserves fair value fair value/

amortised cost

fair value/amortised cost

12

What is an insurance contract?

Risk is significant if “ a reasonable possibility exists that an event affecting the policyholder will cause a significant change in the present value of the insurer’s net cash flows …”

Ø Determined on contract by contract basisØ Insurance if significant loss

possible in one foreseeable scenario

Ø One way classification: once insurance always insurance

Main issuesl Definition of “significant” and “reasonable possibility”

l Ensure consistency in local markets

l Application of IAS 39 to investment contracts

“contract under which one party (The insurer) accepts significantinsurance risk from another party (the policyholder) by agreeing to compensate the policyholder or other beneficiary if a specified uncertain future event (the insured event ) adversely affects the policyholder or other beneficiary”

13

Insurance contracts and scopeInsurance (significant risk)

Insurance but outside scope

Not insurance

Ø Whole of lifeØ EndowmentsØ AnnuitiesØ Term insuranceØ DisabilityØ HealthØ Credit insuranceØ Reinsurance

Ø Financial guarantees(under discussion) (IAS 37,39)

Ø Product warranties issued directly by a manufacturer or others (IAS 18,37)

Ø Retirement benefit obligations and related assets (IAS 19,26)

Ø Insurance contracts that have little insurance risk

Ø Financial reinsurance

Ø Group contracts where all risks are passed on

Ø Self-insuranceØ GamblingØ Financial

derivatives

14

Phase 1: companies still face a number of issues despite use of local GAAP

Mismatch A&L

UnbundlingAsset

ManagementFees

Embedded derivatives

Participating features

DAC

Disclosure

ReinsuranceLoss

recognition

Amortised cost/

Fair value

15

Phase 2

l Based on the DSOP’s l Identify and measure directly individual assets and

liabilities rather than creating deferrals of inflows and outflows

l Implemented in 2006

16

Presentation13Discount Rates6

Disclosure14Performance-linked insurance contracts

7

Interim Financial Reports12Adjustments for risk and uncertainty

5

Reporting entity and consolidation11Estimating the Amount and Timing of Cash Flows

4

Other assets and liabilities10Measurement: Overall Issues3

Measurement of direct insurance contracts by policyholders

9Overall Approach, Recognition and Derecognition

2

Reinsurance8Scope1

TitleChapterTitleChapter

DSOP contents

(Note) Titles in blue have not yet been published as at April 2003

17

Phase 2: Fair value accounting

Main elementsl Best estimate cash flows plus

‘service margin’ l Discount rate derived from

market : ‘risk free’ plus own credit risk allowance

l Allowance for future premiums restricted

l Profit at inception only if “market evidence”

Required solvency

MVM

Expected value of liability Fair value

liability

Net free asset

Shareholder equity

Required amount

Insurance Supervision

IAS

18

l All cash flows, including embedded options, required to be modelled and discounted at a risk-free rate

l In many cases, deterministic projections may give reasonably reliable answers

l But stochastic modelling needed for:Ø Embedded options and guarantees;Ø Benefits that correlate to economic performanceØ Discretionary bonuses related to company profitsØ Other situations where deterministic projections

are not sufficientl Many scenarios (1,000 – 10,000) needed with associated projections

using market-consistent economic models l Fair value now fully replaces the earlier concept of entity-specific

value, which has been dropped for this IFRS

0.95

1

1.05

1.1

1.15

0 0.2 0.4 0.6 0.8 1

Methods of evaluation

19

Risk, uncertainty and discount rates

l Addition of margins to all assumptions for risk and uncertainty that reflect market’s risk preferences (hereinafter “RSA”s – previously “MVM”s)

l RSAs should always reflect not only undiversifiable risk (systematic risk) but also diversifiable (non-systematic) risk -different to asset pricing theories such as CAPM and APT

l Pre-tax risk free discount rates to be used - consistent with modern financial theory but different to normal practice for embedded values

l Also the credit rating of the company should be included –however this produces a counter-intuitive and contrary answer for liabilities in that it implies reserves should reduce as the risk of bankruptcy increases.

20

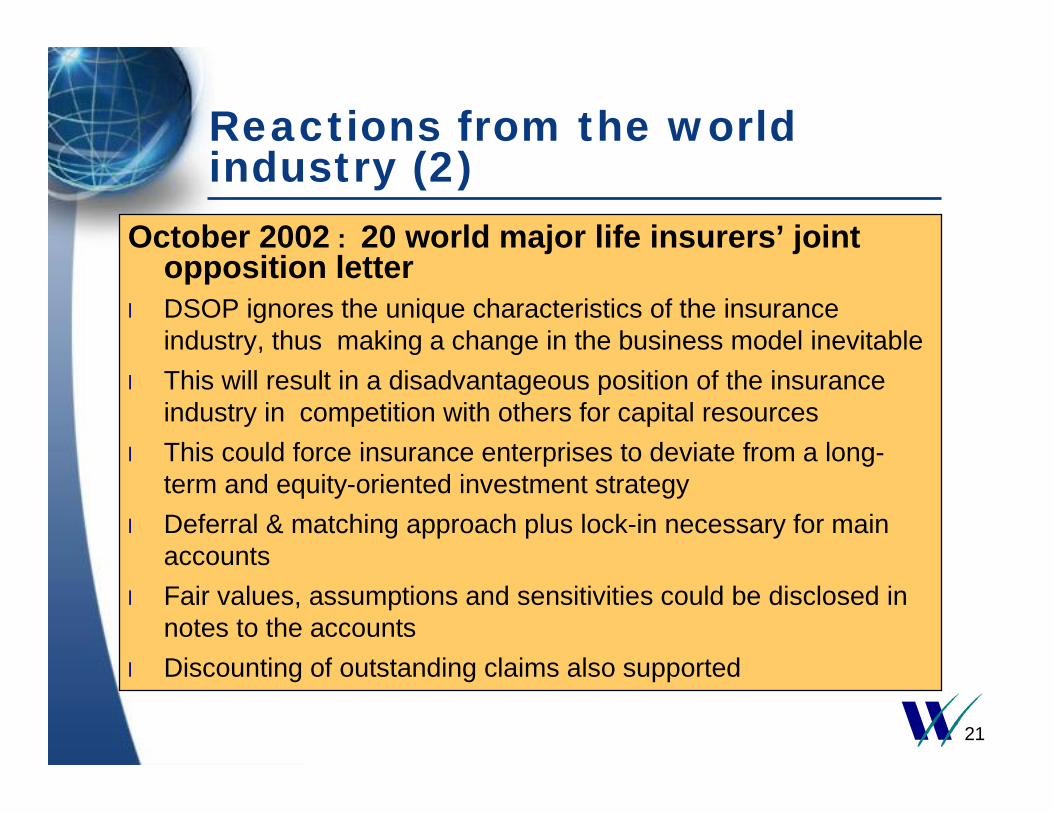

Reactions from the world industry (1)

US (Life), German, Austrian, Japanese (Life) /RAA letter:l Latest joint letter from the above associations submitted February

2003:Ø Phase 1 - opposing several of the major changes in Phase 1

l Scope of Phase 1 and application of IAS 39 should be restrictedl Oppose separation of built in derivatives and use of loss-

recognition tests

Ø Phase 2 – comment thatl the study is hasty and prematurel the associations support deferral and matching method and

most support deferral of acquisition expenses

l the associations oppose reflection of credit risks

21

Reactions from the world industry (2)

October 2002 : 20 world major life insurers’ joint opposition letter

l DSOP ignores the unique characteristics of the insurance industry, thus making a change in the business model inevitable

l This will result in a disadvantageous position of the insurance industry in competition with others for capital resources

l This could force insurance enterprises to deviate from a long-term and equity-oriented investment strategy

l Deferral & matching approach plus lock-in necessary for main accounts

l Fair values, assumptions and sensitivities could be disclosed innotes to the accounts

l Discounting of outstanding claims also supported

22

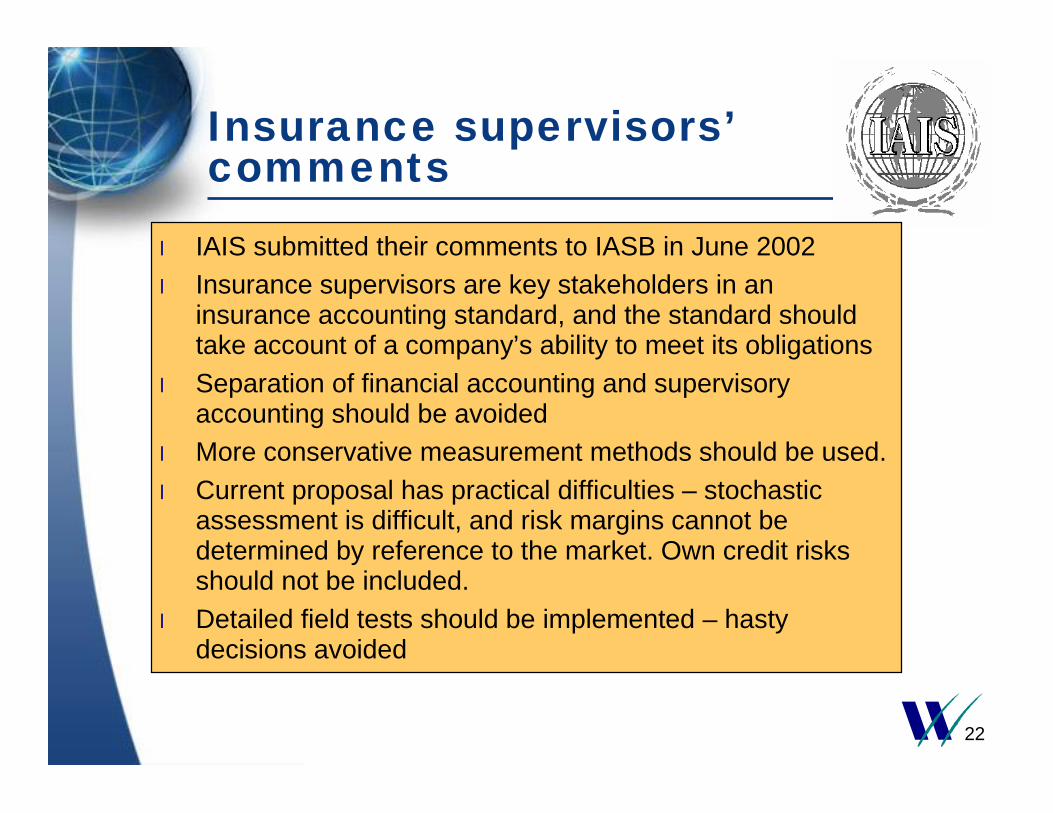

Insurance supervisors’comments

l IAIS submitted their comments to IASB in June 2002l Insurance supervisors are key stakeholders in an

insurance accounting standard, and the standard should take account of a company’s ability to meet its obligations

l Separation of financial accounting and supervisory accounting should be avoided

l More conservative measurement methods should be used.l Current proposal has practical difficulties – stochastic

assessment is difficult, and risk margins cannot be determined by reference to the market. Own credit risks should not be included.

l Detailed field tests should be implemented – hasty decisions avoided

23

IAA’s reaction

l IAA in general favours proposals in DSOPl A sub-group is now developing 23 actuarial standards for

Phase 1l Recent discussions on drafting international actuarial practice

standards for Phase 2 based on DSOP have not progressed very fast

l Another sub-group is exploring various methodologies and worked examples – however there remains strong potential for internal disagreement – as with previous alternative approaches to measurement and control of emergence of profitability

24

Contents

What is the background? In particular, what is the history, scope and reactions

What is the approach to calculating the reserves under the proposed standard for a life insurer?

What are the implications of the new approach for life insurers?

25

Calculation of fair value liabilities

l Market value, for deep and liquid marketsØ Must be supportable

l Professional assessment, otherwiseØ Must be consistent with

current market pricesØ Must be consistent with

budgets and forecasts

l Discounted future cash flows

l Similar contracts groupedl Reinsurance separate

Approach

Method

l Claimsl Surrendersl Loansl Administration and

maintenance expensesl Premiums

Cash flow items

l Must be explicitl Current and not locked inl Cover all future events

Ø optionsØ legislative changes

l Best estimates plus RSA’s

Assumptions

26

Market Risk Preferences (“RSA’s”)

l Cover all risks, including operational and defaultl Risk types

Ø Non-diversifiable, systematic, parameter / model mis-estimation risksØ Diversifiable, unsystematic, randomness / volatility risks

l Market data reflects some non-diversifiable

Two approaches to RSA’sl Cash flow adjustment

Ø Adjust the cash flows to reflect the risk. E.g. increase the mortality charge

l Risk discount rate adjustmentØ Lower the discount rate to reflect the risk

27

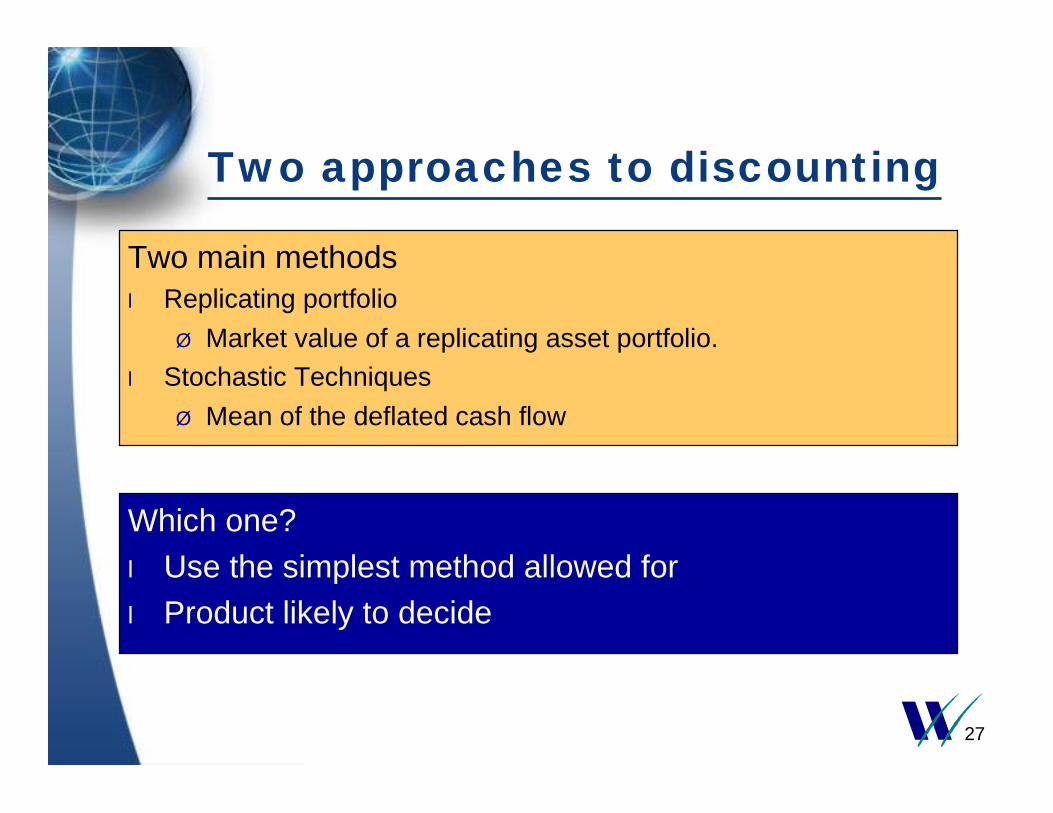

Two approaches to discounting

Two main methodsl Replicating portfolio

Ø Market value of a replicating asset portfolio.l Stochastic Techniques

Ø Mean of the deflated cash flow

Which one?l Use the simplest method allowed forl Product likely to decide

28

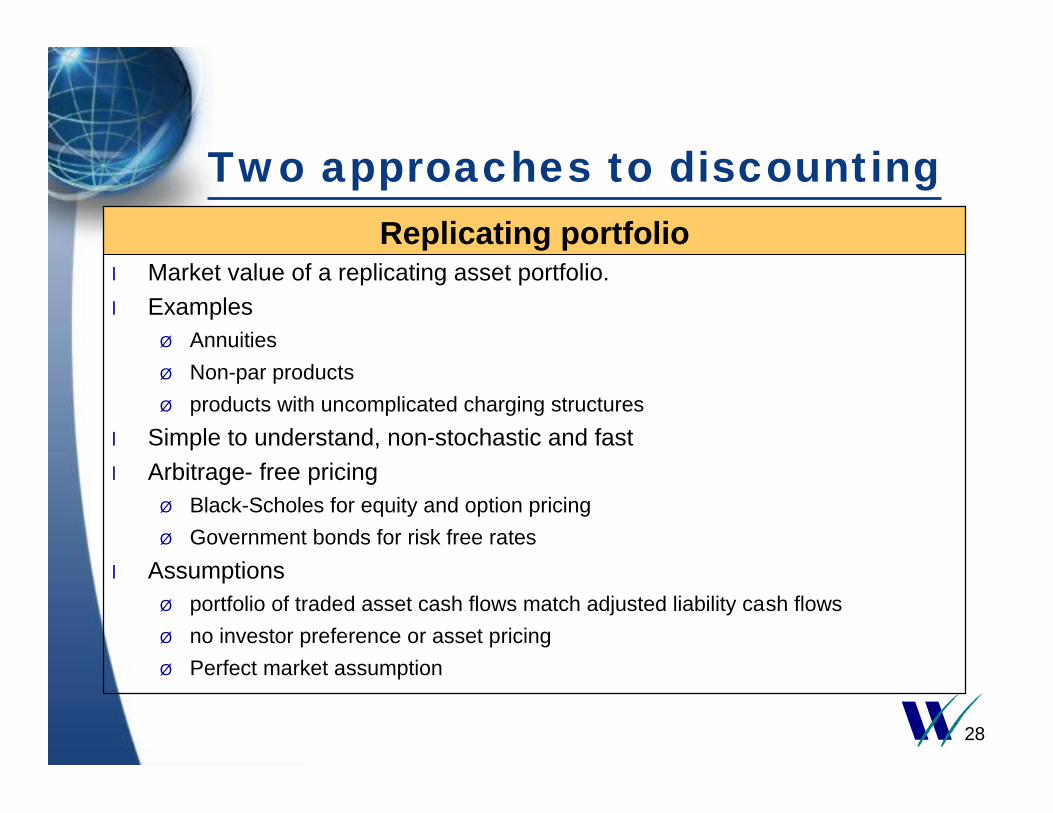

Replicating portfoliol Market value of a replicating asset portfolio.l Examples

Ø AnnuitiesØ Non-par products Ø products with uncomplicated charging structures

l Simple to understand, non-stochastic and fastl Arbitrage- free pricing

Ø Black-Scholes for equity and option pricingØ Government bonds for risk free rates

l AssumptionsØ portfolio of traded asset cash flows match adjusted liability cash flowsØ no investor preference or asset pricingØ Perfect market assumption

Two approaches to discounting

29

Example 1 - non linked annuityReplicating portfoliol Series of risk free

(government issued ) zero coupon bonds precisely matching the liability outflow.

l Sum the market values of the matching zero coupon bonds3,800

4,000

4,200

4,400

4,600

4,800

5,000

5,200

1 2 3 4 5 6 7 8 9 10

Expected cashflow Risk Adjusted Cash flow

Year Expected cashflow

Adjusted for risk

Risk Adjusted Cash flow

Investment Market value of

investment1 4,957 10 4,967 1 year zero 4,730 2 4,909 20 4,929 2 year zero 4,471 3 4,856 31 4,887 3 year zero 4,222 4 4,796 55 4,851 4 year zero 3,991 5 4,729 59 4,788 5 year zero 3,752 6 4,654 75 4,729 6 year zero 3,529 7 4,571 93 4,664 7 year zero 3,315 8 4,479 112 4,591 8 year zero 3,107 9 4,378 132 4,510 9 year zero 2,907 10 4,267 154 4,421 10 year zero 2,714

46,596 741 47,337 36,738

Assumptionsl Assume a risk free rate of

5%l Flat yield curvel All cash flows at end of year

30

Replicating portfolio

l a zero coupon bond l a purchased call option, which on

maturity of the bond, gives the insurer the option to buy the FTSE index at the level at which it stood at policy inception

l Market value of zero coupon easily obtained and if risk free no further adjustment for risk would be required

l Price of the call option may not be risk free thus an adjustment for risk would be required

Guaranteed Equity Bond Payoff Profile

-

4,000

8,000

12,000

16,000

20,000

0% 20% 40% 60% 80% 100% 120% 140% 160% 180%

FTSE as a % of Initial level

Polic

yhol

der b

enef

it ($

)Example 2 - Guaranteed Equity Bond

Product descriptionl The product is an index-linked

single premium guaranteed equity bond.

l The benefit at the end is a return of the initial investment plus any increase in the level of the FTSE 100 index over the period.

Replicating portfolio can be constructed as a combination of:

Prices for these can be obtained from the market

31

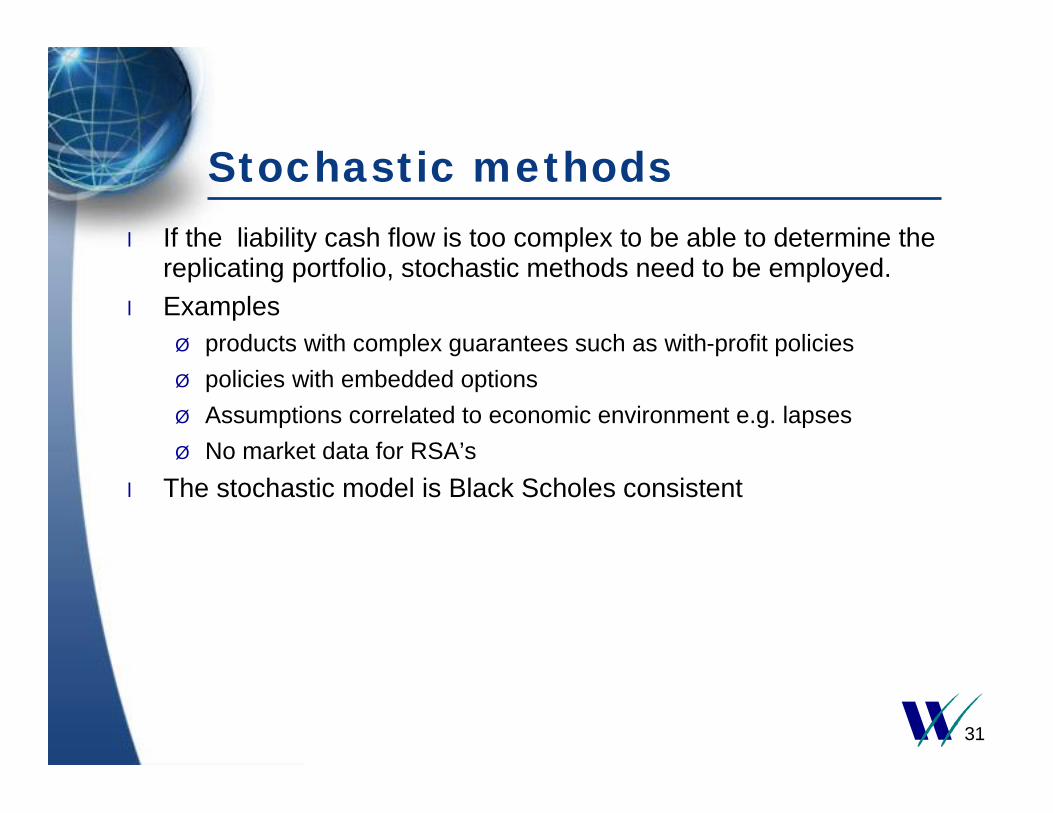

Stochastic methodsl If the liability cash flow is too complex to be able to determine the

replicating portfolio, stochastic methods need to be employed.l Examples

Ø products with complex guarantees such as with-profit policiesØ policies with embedded optionsØ Assumptions correlated to economic environment e.g. lapsesØ No market data for RSA’s

l The stochastic model is Black Scholes consistent

32

Stochastic methodsl Most commonly discussed stochastic method is the “State Price

Deflator method”l Deflators can be best described as stochastic discount rates and

can be used to calculate fair value of liabilities as followsØ a stochastic asset model is run, the output from which will include a

deflator for each time period of each scenarioØ The liability cash flows are projected and adjusted for non-financial riskØ for each simulation the deflator is applied to the relevant cash flow at

each point in time and the values are summed across all projection steps to obtain a deflated value

Ø the fair value of the liability is the mean value of the deflated cash flows.

33

Example 3 - non-linked annuityExample 1 but using state price deflators instead of the deterministic method

YearRun 1 Run 2 Run 3 Run 4 Run 5

1 4,967 0.9867 0.9124 0.8993 1.0011 0.94332 4,929 0.8613 0.9410 0.8248 0.9826 0.94683 4,887 0.8022 0.9097 0.7677 0.9504 0.94704 4,851 0.8126 0.8085 0.7423 0.8850 0.85275 4,788 0.7215 0.8197 0.6831 0.8658 0.85346 4,729 0.6579 0.8094 0.6663 0.7991 0.78647 4,664 0.6279 0.7635 0.6288 0.7623 0.74938 4,591 0.6347 0.6799 0.5552 0.7773 0.72999 4,510 0.5854 0.6637 0.5506 0.7057 0.670010 4,421 0.5007 0.6986 0.5236 0.6680 0.6824

Deflated Value 34,270 38,054 32,586 39,938 38,806

Risk-adjusted

Deflators

Number of simulations Fair value5 36,731

100 36,755500 36,744 1000 36,733 5000 36,739

Deterministic 36,737

l The average over the five runs equals 36,731 compared to the deterministic value of 36,737.Ø Reflecting the random statistical error resulting from such a

small number of simulationsl Results converge as the number of stochastic simulations

increases

34

Contents

What is the background? In particular, what is the history, scope and reactions

What is the approach to calculating the reserves under the proposed standard for a life insurer?

What are the implications of the new approach for life insurers?

35

Getting to grips with fair valuel High level audit of productsl Assessment of financial

impactl Methodology and

assumptionsl Data capturel Systemsl Stochastic modellingl Market consistent asset

model

Implementation

Communication

Management

Other uses

36

Getting to grips with fair value

Implementation

Communication

l Day-one impact and volatility

l Enhanced disclosurel Can we explain results to

our board, customers, shareholders and analysts?

Management

Other uses

37

Getting to grips with fair value

Implementation

Communication

Management

l What are the unacceptable risks?

l Should we change the asset allocation?

l Should we modify the bonus policy?

l Should we transfer risk?l Should we change the

product mix/design?l How should we modify

corporate governance?Other uses

38

Getting to grips with fair value

Implementation

Communication

Management l Regulatory capital?l Capital allocation?l Internal performance

measure?Other uses

39

Summaryl IAS is coming and planning will be required before

2005

l Complex issues to address for with-profits

l Attitude to risks may change

l Wider applications than just the accounts

l Impact on day 1 results will depend on nature of the business

l Volatility of profits is likely to increase