internal revenue bulletin no. 2001–28 bulletin · pdf fileenacted in the community...

TRANSCRIPT

INCOME TAX

Rev. Rul. 2001-34, page 31.Federal rates; adjusted federal rates; adjusted feder-al long-term rate, and the long-term exempt rate. Forpurposes of sections 382, 1274, 1288, and other sectionsof the Code, tables set forth the rates for July 2001.

T.D. 8947, page 36.This T.D. removes certain final regulations under section6656 of the Code because amendments to the Code sectionhave made these regulation sections obsolete.

T.D. 8949, page 33.Final regulations relate to the aggregation of stock owner-ship in a corporation of members of a consolidated group.Section 1.1502–34 generally provides that for purposes ofthe consolidated return regulations, the stock ownership ofall members of a consolidated group in another corporationis aggregated in determining the application of certain Codeprovisions. These regulations reflect a technical correctionenacted in the Community Renewal Tax Relief Act of 2000that, in substance, provides that the stock aggregation rulesunder regulation section 1.1502–34 shall apply for purpos-es of section 732(f) of the Code.

T.D. 8950, page 34.Final regulations provide guidance as to the time for filing anapplication for a tentative carryback adjustment by consoli-

dated groups and by certain new members of consolidatedgroups. The amendments also extend the period of time forfiling an application for a tentative carryback adjustment forthe separate return year created by a corporation becominga new member of a consolidated group.

Rev. Proc. 2001–39, page 38.This procedure modifies the definitions of capitation fee andper-unit fee in Rev. Proc. 97–13 (1997–1 C.B. 632) to per-mit automatic increases of those fees according to a speci-fied, objective, and external standard such as the ConsumerPrice Index. Rev. Proc. 97–13 modified.

EMPLOYEE PLANS

T.D. 8948, page 27.Final regulations clarify the circumstances under which anemployer is considered to have significantly reduced retireehealth coverage during the cost maintenance period definedunder section 420(c)(3) of the Code.

EXEMPT ORGANIZATIONS

Announcement 2001–72, page 39.A list is provided of organizations now classified as privatefoundations.

Internal Revenue

bbuulllleettiinnBulletin No. 2001–28

July 9, 2001

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

Department of the TreasuryInternal Revenue Service

Finding Lists begin on page ii.Finding Lists begin on page ii.

(Continued on the next page)

ESTATE TAX

Announcement 2001–74, page 40.This announcement contains revised filing locations forsome states for estate, gift, and generation-skipping trans-fer tax returns.

GIFT TAX

Announcement 2001–74, page 40.This announcement contains revised filing locations forsome states for estate, gift, and generation-skipping trans-fer tax returns.

ADMINISTRATIVE

Announcement 2001-73, page 40.This document contains a correction to Rev. Proc. 2000–39(2000–41 I.R.B. 340) relating to business and travelingexpenses, and per diem allowances.

Announcement 2001-75, page 42.This announcement describes the procedures for requestinga waiver from electronic filing for partnerships that arerequired to electronically file Form 1065, but do not havethe necessary software to file all forms and schedules.

July 9, 2001 2001–28 I.R.B.

July 9, 2001 2001–28 I.R.B.

The Internal Revenue Bulletin is the authoritative instrumentof the Commissioner of Internal Revenue for announcing offi-cial rulings and procedures of the Internal Revenue Serviceand for publishing Treasury Decisions, Executive Orders, TaxConventions, legislation, court decisions, and other items ofgeneral interest. It is published weekly and may be obtainedfrom the Superintendent of Documents on a subscriptionbasis. Bulletin contents are consolidated semiannually intoCumulative Bulletins, which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform applicationof the tax laws, including all rulings that supersede, revoke,modify, or amend any of those previously published in theBulletin. All published rulings apply retroactively unless other-wise indicated. Procedures relating solely to matters of in-ternal management are not published; however, statementsof internal practices and procedures that affect the rightsand duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service onthe application of the law to the pivotal facts stated in therevenue ruling. In those based on positions taken in rulingsto taxpayers or technical advice to Service field offices,identifying details and information of a confidential natureare deleted to prevent unwarranted invasions of privacy andto comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not havethe force and effect of Treasury Department Regulations,but they may be used as precedents. Unpublished rulingswill not be relied on, used, or cited as precedents by Servicepersonnel in the disposition of other cases. In applying pub-lished rulings and procedures, the effect of subsequent leg-islation, regulations, court decisions, rulings, and proce-

dures must be considered, and Service personnel and oth-ers concerned are cautioned against reaching the same con-clusions in other cases unless the facts and circumstancesare substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisionsof the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions, and Subpart B, Legislation and RelatedCommittee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references tothese subjects are contained in the other Parts and Sub-parts. Also included in this part are Bank Secrecy Act Admin-istrative Rulings. Bank Secrecy Act Administrative Rulingsare issued by the Department of the Treasury’s Office of theAssistant Secretary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The first Bulletin for each month includes a cumulative indexfor the matters published during the preceding months.These monthly indexes are cumulated on a semiannual basis,and are published in the first Bulletin of the succeeding semi-annual period, respectively.

The IRS Mission

Provide America’s taxpayers top quality service by help-ing them understand and meet their tax responsibilities

and by applying the tax law with integrity and fairness toall.

Introduction

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

insert missingchildrenBriannaWinslow

andDavid Gosnell

July 9, 2001 2001–28 I.R.B.

Section 42.—Low-IncomeHousing Credit

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, page 31.

Section 280G.—GoldenParachute Payments

Federal short-term, mid-term, and long-termrates are set forth for the month of July 2001. SeeRev. Rul. 2001–34, page 31.

Section 382.—Limitation on NetOperating Loss Carryforwardsand Certain Built-In LossesFollowing Ownership Change

The adjusted applicable federal long-term rate isset forth for the month of July 2001. See Rev. Rul.2001–34, page 31.

Section 420.— Transfers ofExcess Pension Assets toRetiree Health Accounts

26 CFR 1.420–1: Significant reduction in retireehealth coverage during the cost maintenanceperiod.

T.D. 8948

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Minimum Cost RequirementPermitting the Transfer ofExcess Assets of a DefinedBenefit Pension Plan to aRetiree Health Account

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document contains finalIncome Tax Regulations relating to theminimum cost requirement under section420, which permits the transfer of excessassets of a defined benefit pension plan to aretiree health account. Pursuant to section420(c)(3)(E), these regulations provide thatan employer who significantly reduces re-

tiree health coverage during the cost main-tenance period does not satisfy the mini-mum cost requirement of section 420(c)(3).In addition, these regulations clarify the cir-cumstances under which an employer isconsidered to have significantly reduced re-tiree health coverage during the cost main-tenance period.

DATES: Effective Date: These regula-tions are effective June 19, 2001.

Applicability Date:These regulationsare applicable to transfers of excess pen-sion assets occurring on or after Decem-ber 18, 1999. See the Effective Datepor-tion of this preamble.

FOR FURTHER INFORMATION CON-TACT: Janet A. Laufer or Vernon S. Carter(202) 622-6060 (not a toll-free number).

SUPPLEMENTARY INFORMATION:

Background

This document contains final regula-tions (26 CFR Part 1) under section 420of the Internal Revenue Code of 1986(Code). These regulations provide guid-ance concerning the minimum cost re-quirement under section 420. The Rev-enue Reconciliation Act of 1990 (PublicLaw 101–508) (104 Stat. 1388), section12011, added section 420 of the Code, atemporary provision permitting certainqualified transfers of excess pension as-sets from a non-multiemployer definedbenefit pension plan to a health benefitsaccount. A health benefits account is de-fined as an account established and main-tained under section 401(h) of the Code(401(h) account) that is part of the plan.1

One of the conditions of a qualified sec-tion 420 transfer was that the employersatisfy a maintenance of effort require-ment in the form of a “minimum cost re-quirement” under which the employerwas required to maintain employer-pro-vided retiree health expenditures for cov-ered retirees, their spouses, and depen-dents at a minimum dollar level for a5-year cost maintenance period, begin-ning with the taxable year in which thequalified transfer occurs.

The Uruguay Round Agreements Act(Public Law 103–465) (108 Stat. 4809)(December 8, 1994) extended the avail-ability of section 420 through December31, 2000. In conjunction with the exten-sion, Congress modified the maintenanceof effort rules for plans transferring assetsfor retiree health benefits so that employ-ers could take into account cost savingsrealized in their health benefit plans. As aresult, the focus of the maintenance of ef-fort requirement was shifted from healthcosts to health benefits. Under this “ben-efit maintenance requirement,” which ap-plied to qualified transfers made after De-cember 8, 1994, an employer had tomaintain substantially the same level ofemployer-provided retiree health cover-age for the taxable year of the transfer andthe following 4 years. The level of cover-age required to be maintained was basedon the coverage provided in the taxableyear immediately preceding the taxableyear of the transfer.

The Tax Relief Extension Act of 1999(title V of H.R. 1180, the Ticket to Workand Work Incentives Improvement Act of1999) (Public Law 106–170,113 Stat.1860) (TREA-99) extended section 420through December 31, 2005. In conjunc-tion with this extension, the minimumcost requirement was reinstated as the ap-plicable “maintenance of effort” provi-sion (in lieu of requiring the maintenanceof the level of coverage) for qualifiedtransfers made after December 17, 1999.Because the minimum cost requirementrelates to per capitacost, an employercould satisfy the minimum cost require-ment by maintaining the average costeven though the employer defeats the pur-pose of the maintenance of effort require-ment by reducing the number of peoplecovered by the health plan. In response to

Part I. Rulings and Decisions Under the Internal Revenue Code of 1986

1 Section 420(a)(1) and (2) provide that the trust that ispart of the plan is not treated as failing to satisfy thequalification requirements of section 401(a) or (h) ofthe Code, and no amount is includible in the grossincome of the employer maintaining the plan, solely byreason of such transfer. Also, section 420(a)(3) pro-vides that a qualified transfer is not treated as either anemployer reversion for purposes of section 4980 or aprohibited transaction for purposes of section 4975.

In addition, Title I of the Employee Retirement In-come Security Act of 1974 (88 Stat. 829), as amended(ERISA), provides that a qualified transfer pursuant tosection 420 is not a prohibited transaction underERISA (ERISA section 408(b)(13)) or a prohibited re-version of assets to the employer (ERISA section403(c)(1)). ERISA also provides certain notificationrequirements with respect to such qualified transfers.

2001–28 I.R.B. 27 July 9, 2001

July 9, 2001 28 2001–28 I.R.B.

concerns regarding this possibility,TREA-99 also added section 420(c)(3)(E), which requires the Secretary of theTreasury to prescribe such regulations asmay be necessary to prevent an employerwho significantly reduces retiree healthcoverage during the cost maintenance pe-riod from being treated as satisfying theminimum cost requirement of section420(c)(3). If the minimum cost require-ment of section 420(c)(3) is not satisfied,the transfer of assets from the pensionplan to the 401(h) account is not a “quali-fied transfer” to which the provisions ofsection 420(a) apply.

On January 5, 2001, a notice of pro-posed rulemaking (REG–116468–00,2001–6 I.R.B. 522) was published in theFederal Register(66 FR 1066). Writtencomments were received on the proposedregulations. A public hearing scheduledfor March 15, 2001, was canceled be-cause no one had requested to speak (66FR 13864). After consideration of all thecomments received on the proposed regu-lations, the regulations are adopted asmodified by this Treasury decision.

Explanation of Provisions

General Framework

Following the approach taken in theproposed regulations, these regulationsprovide that the minimum cost require-ment of section 420(c)(3) is not met ifan employer significantly reduces re-tiree health coverage during the costmaintenance period. Whether an em-ployer has significantly reduced retireehealth coverage is determined by look-ing at the number of individuals (re-tirees, their spouses, and dependents)who lose coverage during the cost main-tenance period as a result of employeractions, measured on both an annualbasis and a cumulative basis.

In determining whether an employerhas significantly reduced retiree healthcoverage, the regulations provide that theemployer does not satisfy the minimumcost requirement if the percentage de-crease in the number of individuals pro-vided with applicable health benefits thatis attributable to employer action exceeds10 percent in any year, or if the sum of theannual percentage decreases during thecost maintenance period exceeds 20 per-cent.

Employer Action

The regulations retain the broad defini-tion of employer action contained in theproposed regulations. Thus, employer ac-tion includes not only plan amendmentsbut also situations in which other em-ployer actions, such as the sale of all orpart of the employer’s business, operate inconjunction with the existing plan termsto have the indirect effect of ending an in-dividual’s coverage.

The proposed regulations contained noexceptions from the rule that treats indi-viduals as losing health coverage by rea-son of employer action if those individu-als’ coverage ends by reason of a sale ofall or part of the employer’s business,even if the buyer provides coverage forsuch individuals (on the implicit assump-tion that a buyer of less than an entire cor-poration rarely undertakes to provide suchcoverage to retirees in these transactions).The preamble to the proposed regulationsspecifically requested comments as to (1)the circumstances, if any, in which buyerscommonly provide the seller’s retirees,and their spouses and dependents, withhealth coverage following a corporatetransaction, and (2) in such cases, criteriathat should apply to the replacement cov-erage in determining whether to treat thoseindividuals as not having lost coverage.

Commentators disagreed with the as-sumption stated in the preamble to theproposed regulations that a buyer acquir-ing a portion of a seller’s business rarelyundertakes to provide retiree health cov-erage to retirees in these transactions andexpressed concern about the approachtaken in the proposed regulations con-cerning individuals who lose retireehealth coverage in such situations. Onecommentator stated that in the case ofbusiness combinations involving organi-zations that contract with the UnitedStates Government, the relevant procure-ment regulations encourage buyers to as-sume a seller’s obligations for retirees’pension and retiree medical benefits.Other commentators expressed a desire toretain flexibility in structuring futurebusiness dispositions so that a buyer ortransferee of a business could undertaketo provide retiree health coverage for theseller’s employees.

Generally, commentators requested thatthe regulations allow an employer whosells or transfers a business to take into

account health coverage that a buyer ortransferee provides to retired employeesof the employer. Various approacheswere suggested, most of them centeringaround allowing an employer to takecredit for retiree health benefits providedby a buyer or transferee that are substan-tially similar to the benefits provided bythe employer.

In cases in which a buyer acquires theentire employer sponsoring the pensionplan that is the subject of the maintenanceof effort requirement under section420(c)(3)(E), no special rule is required,because the buyer as the successor em-ployer maintaining the plan is responsiblefor continuing to satisfy the minimumcost requirements of section 420(c)(3)with respect to that transfer. However,based upon comments received, thesefinal regulations include a special rulethat allows the employer responsible forsatisfying the maintenance of effort re-quirement of section 420(c)(3)(E) to takecredit for a buyer’s or transferee’s provi-sion of retiree health benefits in certainother situations.

Under the final regulations, an em-ployer may, but is not required to, treat re-tiree health coverage as not having endedfor individuals whose coverage is pro-vided by a buyer. In such a case, for theyear of the sale and future taxable years ofthe cost maintenance period, the em-ployer must apply the minimum cost re-quirement contained in section 420(c)(3)by treating the individuals whose cover-age is provided by the buyer as individu-als to whom coverage for applicablehealth benefits is provided during the year(i.e., including all such individuals in thedenominator in the determination of ap-plicable employer cost) and treatingamounts the buyer spends on health bene-fits for those individuals as qualified cur-rent retiree health liabilities. After thebuyer commences providing the retireehealth benefits, action of the buyer is at-tributed to the employer for purposes ofdetermining whether an individual’s cov-erage ends by reason of employer action.Accordingly, if a buyer initially providesretiree health benefits to individuals af-fected by the sale, but later amends itsplan to stop providing benefits to those in-dividuals, the employer must treat thoseindividuals as having lost coverage byreason of employer action.

These final regulations also add a defi-nition of “sale” to clarify that the rule forsales applies as well to other transfers of abusiness. In the case of a transfer, thetransferee is treated as the buyer. Thus,for example, the rule applies in a situationin which an employer spins off all or partof its business, and also applies when acontractor that operates a government-owned facility is replaced by another con-tractor and the replacement contractorhires the employees of the prior contrac-tor to operate the facility.

Effective Date

The proposed regulations provided thatthe 10 percent annual limit would notapply to a taxable year beginning beforeFebruary 5, 2001 (30 days after publica-tion of the proposed regulations in theFederal Register). However, under theproposed regulations, the 20 percent cu-mulative limit applied with respect to costmaintenance periods pertaining to anytransfers made on or after December 18,1999. Thus, if an employer reduced cov-erage by more than 20 percent prior to is-suance of the proposed regulations, theemployer would have failed the cumula-tive test.

Several commentators expressed con-cern about the proposed effective date oftransfers occurring on or after December18, 1999. None of the comments indi-cated that any employers had in fact re-duced coverage by more than 20 percentprior to issuance of the proposed regula-tions, and one of the commentators statedthat as a practical matter, the issue ofretroactivity is moot. However, a numberof the commentators expressed concernover retroactive effective dates in Trea-sury regulations as a matter of principle.

These final regulations, like the pro-posed regulations, provide that the 20 per-cent cumulative test will apply with re-spect to transfers of excess pension assetsoccurring on or after December 18, 1999.In order to address concerns raised bycommentators, however, the final regula-tions take into account any reinstatementof coverage that occurs during the portionof a cost maintenance period that pre-cedes the first day of the first taxable yearbeginning on or after January 1, 2002 (theinitial period). Thus, for purposes of thecumulative test, if an employer reducedretiree health coverage by more than 20

percent, the employer can, before the endof the initial period, resume providingcoverage for individuals who lost cover-age and treat those individuals as not hav-ing lost coverage. However, if an em-ployer reduces retiree health coverage bymore than 20 percent during the initial pe-riod and does not “correct” by again pro-viding coverage for individuals who lostcoverage, the employer would fail the cu-mulative test. Also, the annual test ofsignificant reduction applies only to tax-able years beginning on or after January1, 2002, which reflects a further delayfrom the date in the proposed regulation.

Additional changes

The proposed regulations contained aspecial rule that addresses situations inwhich an employer adopts plan terms thatestablish eligibility for health coveragefor some individuals, but provide thatthose same individuals lose health cover-age upon the occurrence of a particularevent or after a stated period of time. Inthose cases, an individual is not countedas having lost health coverage by reasonof employer action merely because thatindividual’s coverage ends upon the oc-currence of the event or after a certain pe-riod of time, such as when health benefitsare provided to employees retiring as a re-sult of a plant closing only for the periodduring which they receive severance pay(see example 2 of the regulations). As aresult of the changes discussed above thataddress “corrections” through restorationof coverage during the initial period andsale transactions, these final regulationscontain two modifications of the specialrule for contemporaneously-adopted planterms. First, the special rule is not avail-able with respect to an amendment thatrestores coverage before the end of theinitial period. Second, in the context ofan amendment of a buyer’s health plan toprovide retiree health coverage for aseller’s employees, the special rule isavailable only to the extent that any termsthat have the effect of ending an individ-ual’s coverage are the same as the termsof the plan maintained by the seller, andonly if the terms of the seller’s plan thatterminate coverage were adopted contem-poraneously with the provision underwhich the individual became eligible forretiree health coverage under the seller’splan.

Special Analyses

It has been determined that this Trea-sury decision is not a significant regula-tory action as defined in Executive Order12866. Therefore, a regulatory assess-ment is not required. It has also been de-termined that section 553(b) of the Ad-ministrative Procedure Act (5 U.S.C.chapter 5) does not apply to these regula-tions, and, because the regulations do notimpose a collection of information onsmall entities, the Regulatory FlexibilityAct (5 U.S.C. chapter 6) does not apply.Pursuant to section 7805(f) of the Code,the notice of proposed rulemaking pre-ceding these regulations was submitted tothe Chief Counsel for Advocacy of theSmall Business Administration for com-ment on its impact on small business.

Drafting Information

The principal authors of these regula-tions are Janet A. Laufer and Vernon S.Carter, Office of Division Counsel/Associ-ate Chief Counsel (Tax Exempt and Gov-ernment Entities). However, other person-nel from the IRS and Treasury Departmentparticipated in their development.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 is amendedas follows:

PART 1 – INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by adding a new entryin numerical order to read in part as fol-lows:

Authority: 26 U.S.C. 7805, 26 U.S.C.420(c)(3)(E)***

Par. 2. Section 1.420–1 is added underthe undesignated centerheading “Pension,Profit-Sharing, Stock Bonus Plans, etc.”to read as follows:

§1.420–1 Significant reduction in retireehealth coverage during the costmaintenance period.

(a) In general. Notwithstanding sec-tion 420(c)(3)(A), the minimum cost re-quirements of section 420(c)(3) are notmet if the employer significantly reducesretiree health coverage during the costmaintenance period.

2001–28 I.R.B. 29 July 9, 2001

(b) Significant reduction—(1) In gen-eral. An employer significantly reducesretiree health coverage during the costmaintenance period if, for any taxableyear beginning on or after January 1,2002, that is included in the cost mainte-nance period, either —

(i) The employer-initiated reductionpercentage for that taxable year exceeds10 percent; or

(ii) The sum of the employer-initiatedreduction percentages for that taxable yearand all prior taxable years during the costmaintenance period exceeds 20 percent.

(2) Employer-initiated reduction per-centage. The employer-initiated reductionpercentage for any taxable year is thefraction B/A, expressed as a percentage,where:

A = The total number of individuals(retired employees plus theirspouses plus their dependents)receiving coverage for applica-ble health benefits as of the daybefore the first day of the taxableyear.

B = The total number of individualsincluded in A whose coveragefor applicable health benefitsended during the taxable year byreason of employer action.

(3) Special rules for taxable years be-ginning before January 1, 2002. The fol-lowing rules apply for purposes of com-puting the amount in paragraph (b)(1)(ii)of this section if any portion of the costmaintenance period precedes the first dayof the first taxable year beginning on orafter January 1, 2002—

(i) Aggregation of taxable years. Theportion of the cost maintenance periodthat precedes the first day of the first tax-able year beginning on or after January 1,2002 (the initial period), is treated as asingle taxable year and the employer-ini-tiated reduction percentage for the initialperiod is computed as set forth in para-graph (b)(2) of this section, except thatthe words “initial period” apply instead of“taxable year.”

(ii) Loss of coverage. If coverage forapplicable health benefits for an individ-ual ends by reason of employer action atany time during the initial period, an em-ployer may treat that coverage as not hav-ing ended if the employer restores cover-age for applicable health benefits to that

individual by the end of the initial period.

(4) Employer action—(i) General rule.For purposes of paragraph (b)(2) of thissection, an individual’s coverage for ap-plicable health benefits ends during a tax-able year by reason of employer action, ifon any day within the taxable year, the in-dividual’s eligibility for applicable healthbenefits ends as a result of a plan amend-ment or any other action of the employer(e.g., the sale of all or part of the em-ployer’s business) that, in conjunctionwith the plan terms, has the effect of end-ing the individual’s eligibility. An em-ployer action is taken into account for thispurpose regardless of when the employeraction actually occurs (e.g., the date theplan amendment is executed), except thatemployer actions occurring before thelater of December 18, 1999, and the datethat is 5 years before the start of the costmaintenance period are disregarded.

(ii) Special rule. Notwithstandingparagraph (b)(4)(i) of this section, cover-age for an individual will not be treated ashaving ended by reason of employer ac-tion merely because such coverage endsunder the terms of the plan if those termswere adopted contemporaneously withthe provision under which the individualbecame eligible for retiree health cover-age. This paragraph (b)(4)(ii) does notapply with respect to plan terms adoptedcontemporaneously with a plan amend-ment that restores coverage for applicablehealth benefits before the end of the initialperiod in accordance with paragraph(b)(3)(ii) of this section.

(iii) Sale transactions. If a purchaserprovides coverage for retiree health bene-fits to one or more individuals whose cov-erage ends by reason of a sale of all or partof the employer’s business, the employermay treat the coverage of those individualsas not having ended by reason of employeraction. In such a case, for the remainder ofthe year of the sale and future taxable yearsof the cost maintenance period —

(A) For purposes of computing the ap-plicable employer cost under section420(c)(3), those individuals are treated asindividuals to whom coverage for applica-ble health benefits was provided (for aslong as the purchaser provides retireehealth coverage to them), and any amountsexpended by the purchaser of the businessto provide for health benefits for those indi-viduals are treated as paid by the employer;

(B) For purposes of determiningwhether a subsequent termination of cov-erage is by reason of employer actionunder this paragraph (b)(4), the purchaseris treated as the employer. However, thespecial rule in paragraph (b)(4)(ii) of thissection applies only to the extent that anyterms of the plan maintained by the pur-chaser that have the effect of ending re-tiree health coverage for an individual arethe same as terms of the plan maintainedby the employer that were adopted con-temporaneously with the provision underwhich the individual became eligible forretiree health coverage under the planmaintained by the employer.

(c) Definitions. The following defini-tions apply for purposes of this section:

(1) Applicable health benefits. Applic-able health benefits means applicablehealth benefits as defined in section420(e)(1)(C).

(2) Cost maintenance period. Costmaintenance period means the cost main-tenance period as defined in section420(c)(3)(D).

(3) Sale. A sale of all or part of an em-ployer’s business means a sale or othertransfer in connection with which the em-ployees of a trade or business of the em-ployer become employees of another per-son. In the case of such a transfer, theterm purchasermeans a transferee of thetrade or business.

(d) Examples.The following examplesillustrate the application of this section:

Example 1.(i) Employer W maintains a definedbenefit pension plan that includes a 401(h) accountand permits qualified transfers that satisfy section420. The number of individuals receiving coveragefor applicable health benefits as of the day beforethe first day of Year 1 is 100. In Year 1, EmployerW makes a qualified transfer under section 420.There is no change in the number of individuals re-ceiving health benefits during Year 1. As of the lastday of Year 2, applicable health benefits are pro-vided to 99 individuals, because 2 individuals be-came eligible for coverage due to retirement and 3individuals died in Year 2. During Year 3, EmployerW amends its health plan to eliminate coverage for 5individuals, 1 new retiree becomes eligible for cov-erage and an additional 3 individuals are no longercovered due to their own decision to drop coverage.Thus, as of the last day of Year 3, applicable healthbenefits are provided to 92 individuals. During Year4, Employer W amends its health plan to eliminatecoverage under its health plan for 8 more individu-als, so that as of the last day of Year 4, applicablehealth benefits are provided to 84 individuals. Dur-ing Year 5, Employer W amends its health plan toeliminate coverage for 8 more individuals.

(ii) There is no significant reduction in retireehealth coverage in either Year 1 or Year 2, because

July 9, 2001 30 2001–28 I.R.B.

there is no reduction in health coverage as a result ofemployer action in those years.

(iii) There is no significant reduction in Year 3.The number of individuals whose health coverageended during Year 3 by reason of employer action(amendment of the plan) is 5. Since the number ofindividuals receiving coverage for applicable healthbenefits as of the last day of Year 2 is 99, the em-ployer-initiated reduction percentage for Year 3 is5.05 percent (5/99), which is less than the 10 percentannual limit.

(iv) There is no significant reduction in Year 4.The number of individuals whose health coverageended during Year 4 by reason of employer action is8. Since the number of individuals receiving cover-age for applicable health benefits as of the last dayof Year 3 is 92, the employer-initiated reduction per-centage for Year 4 is 8.70 percent (8/92), which isless than the 10 percent annual limit. The sum of theemployer-initiated reduction percentages for Year 3and Year 4 is 13.75 percent, which is less than the 20percent cumulative limit.

(v) In Year 5, there is a significant reductionunder paragraph (b)(1)(ii) of this section. The num-ber of individuals whose health coverage ended dur-ing Year 5 by reason of employer action (amend-ment of the plan) is 8. Since the number ofindividuals receiving coverage for applicable healthbenefits as of the last day of Year 4 is 84, the em-ployer-initiated reduction percentage for Year 5 is9.52 percent (8/84), which is less than the 10 percentannual limit. However, the sum of the employer-ini-tiated reduction percentages for Year 3, Year 4, andYear 5 is 5.05 percent + 8.70 percent + 9.52 percent= 23.27 percent, which exceeds the 20 percent cu-mulative limit.

Example 2.(i) Employer X, a calendar year tax-payer, maintains a defined benefit pension plan thatincludes a 401(h) account and permits qualifiedtransfers that satisfy section 420. X also provideslifetime health benefits to employees who retire fromDivision A as a result of a plant shutdown, no healthbenefits to employees who retire from Division B,and lifetime health benefits to all employees who re-tire from Division C. In 2000, X amends its healthplan to provide coverage for employees who retirefrom Division B as a result of a plant shutdown, butonly for the 2-year period coinciding with their sev-erance pay. Also in 2000, X amends the health planto provide that employees who retire from DivisionA as a result of a plant shutdown receive health cov-erage only for the 2-year period coinciding with theirseverance pay. A plant shutdown that affects Divi-sion A and Division B employees occurs in 2000.The number of individuals receiving coverage for ap-plicable health benefits as of the last day of 2001 is200. In 2002, Employer X makes a qualified transferunder section 420. As of the last day of 2002, applic-able health benefits are provided to 170 individuals,because the 2-year period of benefits ends for 10 em-ployees who retired from Division A and 20 employ-ees who retired from Division B as a result of theplant shutdown that occurred in 2000.

(ii) There is no significant reduction in retireehealth coverage in 2002. Coverage for the 10 re-tirees from Division A who lose coverage as a resultof the end of the 2-year period is treated as havingended by reason of employer action, because cover-age for those Division A retirees ended by reason ofa plan amendment made after December 17, 1999.

However, the terms of the health plan that limit cov-erage for employees who retired from Division B asa result of the 2000 plant shutdown (to the 2-yearperiod) were adopted contemporaneously with theprovision under which those employees became eli-gible for retiree coverage under the health plan. Ac-cordingly, under the rule provided in paragraph(b)(4)(ii) of this section, coverage for those 20 re-tirees from Division B is not treated as having endedby reason of employer action. Thus, the number ofindividuals whose health benefits ended by reasonof employer action in 2002 is 10. Since the numberof individuals receiving coverage for applicablehealth benefits as of the last day of 2001 is 200, theemployer-initiated reduction percentage for 2002 is5 percent (10/200), which is less than the 10 percentannual limit.

(e) Regulatory effective date. This sec-tion is applicable to transfers of excesspension assets occurring on or after De-cember 18, 1999.

David A. Mader,Acting Deputy Commissioner

of Internal Revenue.

Approved June 12, 2001.

Mark A. Weinberger,Assistant Secretary

of the Treasury (Tax Policy).

(Filed by the Office of the Federal Register on June14, 2001, at 2:45 p.m., and published in the issue ofthe Federal Register for June 19, 2001, 66 FR32897)

Section 467.—Certain Paymentsfor the Use of Property orServices

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, on this page.

Section 468.—Special Rules forMining and Solid WasteReclamation and Closing Costs

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, on this page.

Section 482.—Allocation ofIncome and Deductions AmongTaxpayers

Federal short-term, mid-term, and long-termrates are set forth for the month of July 2001. SeeRev. Rul. 2001–34, on this page.

Section 483.—Interest onCertain Deferred Payments

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, on this page.

Section 642.—Special Rules forCredits and Deductions

Federal short-term, mid-term, and long-termrates are set forth for the month of July 2001. SeeRev. Rul. 2001–34, on this page.

Section 807.—Rules for CertainReserves

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, on this page.

Section 846.—DiscountedUnpaid Losses Defined

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, on this page.

Section 1274.—Determinationof Issue Price in the Case ofCertain Debt Instruments Issuedfor Property

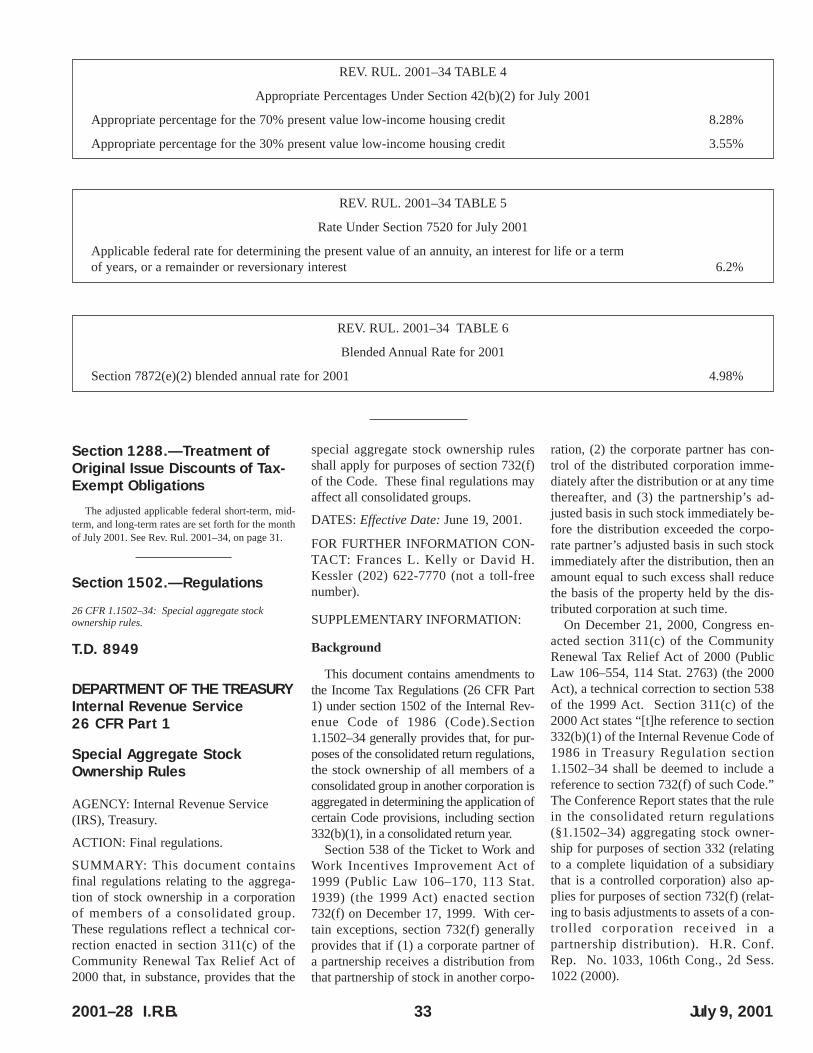

(Also sections 42, 280G, 382, 412, 467, 468, 482,483, 642, 807, 846, 1288, 7520, 7872.)

Federal rates; adjusted federal rates;adjusted federal long-term rate, andthe long-term exempt rate.For purposesof sections 382, 1274, 1288, and othersections of the Code, tables set forth therates for July 2001.

Rev. Rul. 2001–34

This revenue ruling provides variousprescribed rates for federal income taxpurposes for July 2001 (the currentmonth). Table 1 contains the short-term,mid-term, and long-term applicable fed-eral rates (AFR) for the current month forpurposes of section 1274(d) of the Inter-nal Revenue Code. Table 2 contains theshort-term, mid-term, and long-term ad-justed applicable federal rates (adjustedAFR) for the current month for purposesof section 1288(b). Table 3 sets forth the ad-

2001–28 I.R.B. 31 July 9, 2001

justed federal long-term rate and the long-term tax-exempt rate described in section382(f). Table 4 contains the appropriate per-centages for determining the low-incomehousing credit described in section 42(b)(2)

for buildings placed in service during thecurrent month. Table 5 contains the federalrate for determining the present value of anannuity, an interest for life or for a term ofyears, or a remainder or a reversionary inter-

est for purposes of section 7520. Finally,Table 6 contains the blended annual rate for2001 for purposes of section 7872

July 9, 2001 32 2001–28 I.R.B.

REV. RUL. 2001–34 TABLE 1

Applicable Federal Rates (AFR) for July 2001

Period for Compounding

Annual Semiannual Quarterly Monthly

Short-Term

AFR 4.07% 4.03% 4.01% 4.00%110% AFR 4.48% 4.43% 4.41% 4.39%120% AFR 4.90% 4.84% 4.81% 4.79%130% AFR 5.31% 5.24% 5.21% 5.18%

Mid-Term

AFR 5.12% 5.06% 5.03% 5.01%110% AFR 5.65% 5.57% 5.53% 5.51%120% AFR 6.16% 6.07% 6.02% 5.99%130% AFR 6.69% 6.58% 6.53% 6.49%150% AFR 7.73% 7.59% 7.52% 7.47%175% AFR 9.06% 8.86% 8.76% 8.70%

Long-Term

AFR 5.82% 5.74% 5.70% 5.67%110% AFR 6.41% 6.31% 6.26% 6.23%120% AFR 7.01% 6.89% 6.83% 6.79%130% AFR 7.60% 7.46% 7.39% 7.35%

REV. RUL. 2001–34 TABLE 2

Adjusted AFR for July 2001

Period for Compounding

Annual Semiannual Quarterly MonthlyShort-termadjusted AFR 3.16% 3.14% 3.13% 3.12%

Mid-termadjusted AFR 3.87% 3.83% 3.81% 3.80%

Long-termadjusted AFR 5.00% 4.94% 4.91% 4.89%

REV. RUL. 2001–34 TABLE 3

Rates Under Section 382 for July 2001

Adjusted federal long-term rate for the current month 5.00%

Long-term tax-exempt rate for ownership changes during the current month (the highest of theadjusted federal long-term rates for the current month and the prior two months.) 5.01%

Section 1288.—Treatment ofOriginal Issue Discounts of Tax-Exempt Obligations

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, on page 31.

Section 1502.—Regulations

26 CFR 1.1502–34: Special aggregate stockownership rules.

T.D. 8949

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Special Aggregate StockOwnership Rules

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document containsfinal regulations relating to the aggrega-tion of stock ownership in a corporationof members of a consolidated group.These regulations reflect a technical cor-rection enacted in section 311(c) of theCommunity Renewal Tax Relief Act of2000 that, in substance, provides that the

special aggregate stock ownership rulesshall apply for purposes of section 732(f)of the Code. These final regulations mayaffect all consolidated groups.

DATES: Effective Date:June 19, 2001.

FOR FURTHER INFORMATION CON-TACT: Frances L. Kelly or David H.Kessler (202) 622-7770 (not a toll-freenumber).

SUPPLEMENTARY INFORMATION:

Background

This document contains amendments tothe Income Tax Regulations (26 CFR Part1) under section 1502 of the Internal Rev-enue Code of 1986 (Code).Section1.1502–34 generally provides that, for pur-poses of the consolidated return regulations,the stock ownership of all members of aconsolidated group in another corporation isaggregated in determining the application ofcertain Code provisions, including section332(b)(1), in a consolidated return year.

Section 538 of the Ticket to Work andWork Incentives Improvement Act of1999 (Public Law 106–170, 113 Stat.1939) (the 1999 Act) enacted section732(f) on December 17, 1999. With cer-tain exceptions, section 732(f) generallyprovides that if (1) a corporate partner ofa partnership receives a distribution fromthat partnership of stock in another corpo-

ration, (2) the corporate partner has con-trol of the distributed corporation imme-diately after the distribution or at any timethereafter, and (3) the partnership’s ad-justed basis in such stock immediately be-fore the distribution exceeded the corpo-rate partner’s adjusted basis in such stockimmediately after the distribution, then anamount equal to such excess shall reducethe basis of the property held by the dis-tributed corporation at such time.

On December 21, 2000, Congress en-acted section 311(c) of the CommunityRenewal Tax Relief Act of 2000 (PublicLaw 106–554, 114 Stat. 2763) (the 2000Act), a technical correction to section 538of the 1999 Act. Section 311(c) of the2000 Act states “[t]he reference to section332(b)(1) of the Internal Revenue Code of1986 in Treasury Regulation section1.1502–34 shall be deemed to include areference to section 732(f) of such Code.”The Conference Report states that the rulein the consolidated return regulations(§1.1502–34) aggregating stock owner-ship for purposes of section 332 (relatingto a complete liquidation of a subsidiarythat is a controlled corporation) also ap-plies for purposes of section 732(f) (relat-ing to basis adjustments to assets of a con-trolled corporation received in apartnership distribution). H.R. Conf.Rep. No. 1033, 106th Cong., 2d Sess.1022 (2000).

2001–28 I.R.B. 33 July 9, 2001

REV. RUL. 2001–34 TABLE 4

Appropriate Percentages Under Section 42(b)(2) for July 2001

Appropriate percentage for the 70% present value low-income housing credit 8.28%

Appropriate percentage for the 30% present value low-income housing credit 3.55%

REV. RUL. 2001–34 TABLE 6

Blended Annual Rate for 2001

Section 7872(e)(2) blended annual rate for 2001 4.98%

REV. RUL. 2001–34 TABLE 5

Rate Under Section 7520 for July 2001

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 6.2%

Section 311(d) of the 2000 Act pro-vides that section 311(c) of the 2000 Acttakes effect as if included in the provi-sions of the 1999 Act to which it relates.Thus, the effective date of section 311(c)of the 2000 Act is the same as that for sec-tion 538(a) of the 1999 Act, which is con-tained in section 538(b) of the 1999 Act.

Explanation of Provisions

These final regulations conform § 1.1502–34 to a technical correction en-acted in section 311(c) of the 2000 Actand add a regulation under section 732 re-flecting that correction. These regulationsreflect this statutory provision clarifyingthat the stock aggregation rules under § 1.1502–34 apply for purposes of section732(f).

Because section 311(d) of the 2000 Actprovides that section 311(c) of the 2000Act shall take effect as if it had been in-cluded in the provisions of the 1999 Act,the effective date provisions of section538(b) of the 1999 Act apply to these reg-ulations. Section 538(b) generally pro-vides that the amendments made by sec-tion 538(a) of the 1999 Act apply todistributions made after July 14, 1999. Inthe case of a corporation that was a part-ner in a partnership as of July 14, 1999,the amendments made by section 538(a)of the 1999 Act apply to distributionsmade (or treated as made) to that partnerfrom that partnership after June 30, 2001.In the case of any such distribution madeafter December 17, 1999, and before July1, 2001, the rule of the preceding sentencedoes not apply unless that partner makesan election to have the rule apply to thedistribution on the partner’s income taxreturn for the year in which the distribu-tion occurs.

Special Analyses

It has been determined that this Trea-sury decision is not a significant regula-tory action as defined in Executive Order12866. Therefore, a regulatory assess-ment is not required. Because no noticeof proposed rulemaking is required forthis final regulation, the provisions of theRegulatory Flexibility Act (5 U.S.C.chapter 6) do not apply.

This final rule merely conforms § 1.1502–34 to the statutory amendmentmade by section 311(c) of the 2000 Act.Pursuant to 5 U.S.C. 553, it is determined

that prior notice and comment are unnec-essary and contrary to the public interest.For the same reason, good cause exists fornot delaying the effective date of this finalrule.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 is amendedas follows:

PART 1 — INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by adding entries in nu-merical order to read in part as follows:

Authority: 26 U.S.C. 7805 * * *Section 1.732–3 also issued under 26

U.S.C. 732(f). * * *Section 1.1502–34 also issued under 26

U.S.C. 1502. * * *Par. 2. Section 1.732–3 is added to read

as follows:

§ 1.732–3 Corresponding adjustment tobasis of assets of a distributedcorporation controlled by a corporatepartner.

The determination of whether a corpo-rate partner has control of a distributedcorporation for purposes of section 732(f)shall be made by applying the special ag-gregate stock ownership rules of § 1.1502–34.

§ 1.1502–34 [Amended]

Par. 3. In §1.1502–34, the first sentenceis amended by adding “732(f),” immedi-ately after “351(a),”.

Robert E. Wenzel,Deputy Commissioner of

Internal Revenue.

Approved June 8, 2001.

Mark A. Weinberger,Assistant Secretary

of the Treasury.

(Filed by the Office of the Federal Register on June13, 2001, at 8:45 a.m., and published in the issue ofthe Federal Register for June 19, 2001, 66 FR32901)

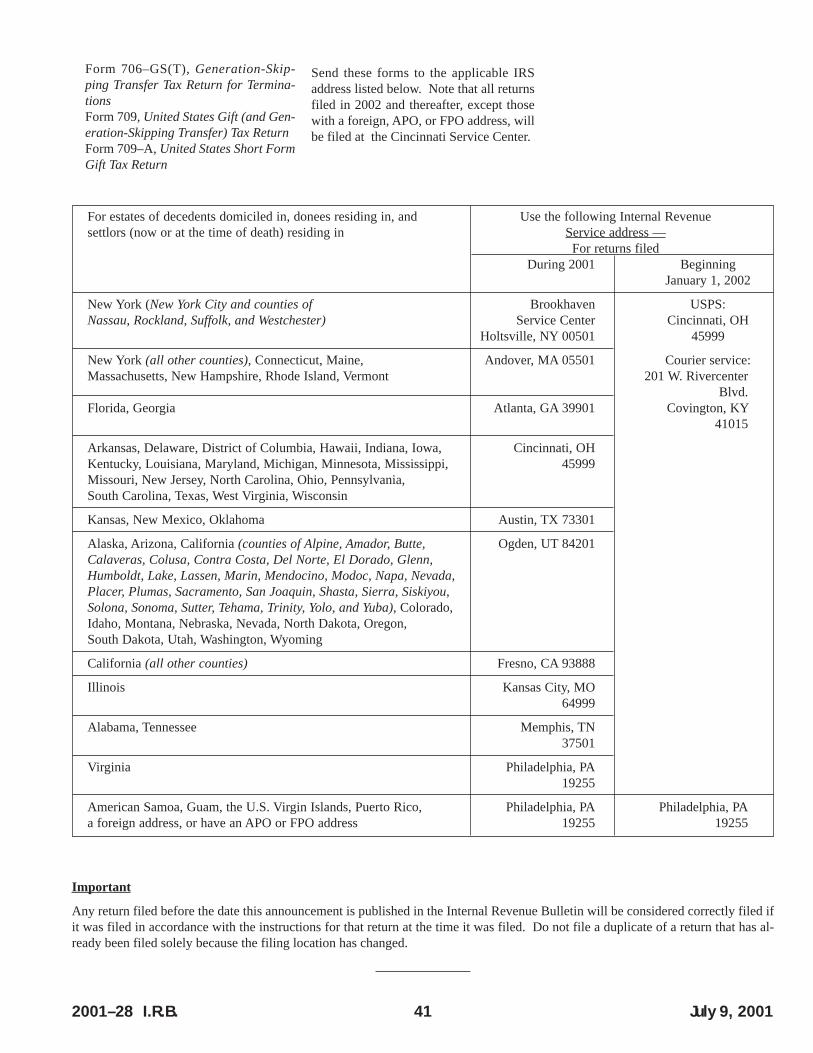

26 CFR 1.1502–78: Tentative carrybackadjustments.

T.D. 8950

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Guidance on Filing anApplication for a TentativeCarryback Adjustment in aConsolidated Return Context

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document containsfinal regulations relating to the filing ofan application for a tentative carrybackadjustment. These regulations provideguidance as to the time for filing such ap-plication by a consolidated group and bycertain corporations for the separate re-turn year created by their becoming amember of a consolidated group. Thesefinal regulations may affect all consoli-dated groups.

DATES: Effective Date:June 22, 2001.Applicability Date:For dates of applic-

ability, see §1.1502–78(e)(2)(v) of theseregulations.

FOR FURTHER INFORMATION CON-TACT: Christopher M. Bass or FrancesL. Kelly (202) 622-7770 (not a toll-freenumber).

SUPPLEMENTARY INFORMATION:

Background

This document contains amendments tothe Income Tax Regulations (26 CFR Part1) under section 1502 of the Internal Rev-enue Code of 1986 (Code) relating to thefiling of an application for a tentative car-ryback adjustment. The amendments pro-vide guidance as to the time for filing anapplication for a tentative carryback ad-justment by a consolidated group. Theamendments also extend the time for fil-ing an application for a tentative carry-back adjustment by certain corporationsfor the separate return year created bytheir becoming new members of a consol-idated group.

On January 4, 2001, a temporary regu-lation (T.D. 8919, 2001–6 I.R.B. 505) waspublished in the Federal Register(66 FR713). On this same day, a notice of pro-

July 9, 2001 34 2001–28 I.R.B.

posed rulemaking (REG–119352–00,2001–6 I.R.B. 525) cross-referencing thetemporary regulation and a notice of pub-lic hearing were published in the FederalRegister (66 FR 747). No comments orrequests to speak were received from thepublic in response to the notice of pro-posed rulemaking. Accordingly, the pub-lic hearing scheduled for April 26, 2001was canceled in the Federal Register(66FR 19104) on April 13, 2001. The pro-posed regulation is adopted as amendedby this Treasury Decision, and the corre-sponding temporary regulation is re-moved.

Explanation of Provisions

The amendments adopted by this Trea-sury decision provide a general rule for allcorporations filing consolidated returnsstating that the provisions of section6411(a) shall apply to determine the timefor filing an application for a tentativecarryback adjustment by a consolidatedgroup. In addition, the amendments pro-vide a special rule for applications filedby certain corporations that become newmembers of a consolidated group, extend-ing the period of time for filing an appli-cation for a tentative carryback adjust-ment resulting from losses or creditsarising in the new member’s last separatereturn year. For these purposes, the sepa-rate return year is treated as ending on thesame date as the end of the current taxableyear of the consolidated group.

Until Form 1139 (Application for aTentative Carryback Adjustment) is modi-fied to reflect the changes made by thisregulation, an application for a tentativecarryback adjustment filed under the spe-cial rule must include additional informa-tion in the form of a statement, “Filedpursuant to Treas. Reg. section1.1502–78(e)(2),” in red, at the top of thecurrent Form 1139. In addition, the Form1139 must state, in red, the “year end” ofthe consolidated group that the new mem-ber joins. In response to the changesmade by this regulation, IRS Service Cen-ters developed a procedure to assist inprocessing applications filed under§1.1502–78(e)(2). This procedure re-quires that the additional information, asset forth above, be included on the Form1139. This procedure supplements exist-ing guidelines for filing and processingForm 1139.

The proposed regulation (66 FR 747)was issued as §1.1502–78T(g). This finalregulation adopts the substance of theproposed regulation and renumbers suchprovision as §1.1502–78(e).

Special Analyses

It has been determined that this Trea-sury decision is not a significant regula-tory action as defined in Executive Order12866. Therefore, a regulatory assess-ment is not required. It is hereby certifiedthat this regulation will not impose a sig-nificant economic impact on a substantialnumber of small entities because it affectsa relatively small number of corporationsand few, if any, of those corporations arelikely to be small businesses. Therefore,a Regulatory Flexibility Analysis underthe Regulatory Flexibility Act (5 U.S.C.chapter 6) is not required. Pursuant tosection 7805(f) of the Code, the notice ofproposed rulemaking that preceded theseregulations was submitted to the ChiefCounsel for Advocacy of the Small Busi-ness Administration for comment on itsimpact on small business.

Drafting Information

The principal authors of these regula-tions are Christopher M. Bass andFrances L. Kelly, Office of the AssociateChief Counsel (Corporate). However,other personnel from the IRS and Trea-sury Department participated in their de-velopment.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 is amendedas follows:

PART 1 — INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by removing the entriesfor sections 1.1502–78(b) and1.1502–78T and by adding an entry in nu-merical order to read in part as follows:

Authority: 26 U.S.C. 7805 * * *Section 1.1502–78 also issued under 26

U.S.C. 1502, 6402(k), and 6411(c). * * *Par. 2. Section 1.1502–78 is amended by

adding paragraph (e) to read as follows:

§1.1502–78 Tentative carrybackadjustments.

* * * * *(e) Time for filing application—(1)

General rule.The provisions of section6411(a) apply to the filing of an applica-tion for a tentative carryback adjustmentby a consolidated group.

(2) Special rule for new members—(i)New member. A new member is a corpo-ration that, in the preceding taxable year,did not qualify as a member, as defined in§1.1502–1(b), of the consolidated groupthat it now joins.

(ii) End of taxable year. Solely for thepurpose of complying with the twelve-month requirement for making an appli-cation for a tentative carryback adjust-ment under section 6411(a), the separatereturn year of a qualified new membershall be treated as ending on the samedate as the end of the current taxable yearof the consolidated group that the quali-fied new member joins.

(iii) Qualified new member. A newmember of a consolidated group qualifiesfor purposes of the provisions of thisparagraph (e)(2) if, immediately prior tobecoming a new member, either—

(A) It was the common parent of a con-solidated group; or

(B) It was not required to join in the fil-ing of a consolidated return.

(iv) Examples. The provisions of thisparagraph (e)(2) may be illustrated by thefollowing examples:

Example 1. Individual A owns 100 percent of thestock of X, a corporation that is not a member of aconsolidated group and files separate tax returns ona calendar year basis. On January 31 of year 1, Xbecomes a member of the Y consolidated group,which also files returns on a calendar year basis. Xis a qualified new member as defined in paragraph(e)(2)(iii)(B) of this section because, immediatelyprior to becoming a new member of the Y consoli-dated group, X was not required to join in the filingof a consolidated return. As a result of its becominga new member of Group Y, X’s separate return forthe short taxable year (January 1 of year 1 throughJanuary 31 of year 1) is due September 15 of year 2(with extensions). See §1.1502–76(c). Group Y’sconsolidated return is also due September 15 of year2 (with extensions). See §1.1502–76(c). Solely forthe purpose of complying with the twelve-month re-quirement for making an application for a tentativecarryback adjustment under section 6411(a), X’staxable year for the separate return year is treated asending on December 31 of year 1. X’s applicationfor a tentative carryback adjustment is therefore dueon or before December 31 of year 2.

Example 2. Assume the same facts as in Example1 except that immediately prior to becoming a newmember of Group Y, X was a member of the Z con-solidated group. Because X was required to join inthe filing of the consolidated return for Group Z, X

2001–28 I.R.B. 35 July 9, 2001

is not a qualified new member as defined in para-graph (e)(2)(iii) of this section. X’s items for theone-month period will be included in the consoli-dated return for Group Z. Group Z’s application fora tentative carryback adjustment, if any, continues tobe due within 12 months of the end of its taxableyear, which is not affected by X’s change in status asa new member of Group Y.

(v) Effective date. The provisions ofthis paragraph (e)(2) apply for applica-tions by new members of consolidatedgroups for tentative carryback adjust-ments resulting from net operating losses,net capital losses, or unused businesscredits arising in separate return years ofnew members that begin on or after Janu-ary 1, 2001.

§1.1502–78T [Removed]

Par. 3. Section 1.1502–78T is removed.

Robert E. Wenzel,Deputy Commissioner

of Internal Revenue.

Approved June 13, 2001.

Mark A. Weinberger,Assistant Secretary

of the Treasury.

(Filed by the Office of the Federal Register on June21, 2001, at 8:45 a.m., and published in the issue ofthe Federal Register for June 22, 2001, 66 FR33462)

Section 6302.—Mode or Time ofCollection

26 CFR 1.6302–1: Use of Government depositariesin connection with corporation income andestimated income taxes and certain taxes of tax-exempt organizations.

T.D. 8947

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Parts 1, 31, 301, and602

Penalties for Underpayments ofDeposits and OverstatedDeposit Claims

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations and removalof final regulations.

SUMMARY: This document makes con-forming amendments to certain final reg-ulations to reflect the removal of finalregulations, relating to the penalty for un-derpayment of deposits of taxes and thepenalty for overstated deposit claims.These regulations are obsolete due toamendments to section 6656 of the Inter-nal Revenue Code. The removal of theseregulations will not affect taxpayers.

DATES: The amendments and removal ofthese regulations is effective June 15, 2001.

FOR FURTHER INFORMATION CON-TACT: Robin M. Tuczak (202) 622-4940(not a toll-free number).

SUPPLEMENTARY INFORMATION:

Background and Explanation ofProvisions

This document removes two sectionsfrom the Procedure and AdministrationRegulations (26 CFR part 301) relating topenalties for underpayment of Federal taxdeposits and overstated deposit claimsunder section 6656 of the Internal Rev-enue Code.The Omnibus Budget Recon-ciliation Act of 1989, Public Law101–239 (103 Stat. 2106, 1989) amendedsection 6656, modifying the penalty ratesrelating to a failure to make a Federal taxdeposit and removing the penalty relatingto overstatement of Federal tax deposits.These changes have rendered§§301.6656–1 and 301.6656–2 obsolete.

Section 301.6656–1 was revised and§301.6656–2 was added by T.D. 7925(1984–1 C.B. 261), published in the Fed-eral Register for December 13, 1983(LR–311–81, 1982–1 C.B. 570), 48 FR5453). Section 301.6656–2 was added toimplement changes made by the Eco-nomic Recovery Tax Act of 1981, PublicLaw 97–34 (95 Stat. 172, 1981). Section301.6656–1 was revised to remove out-dated provisions relating to deposits madebefore January 1, 1970, based on the lawin effect for those deposits.

Section 301.6656–1 reflects that, at thetime it was revised, the penalty for under-payment of deposits was five percent ofthe amount of the underpayment withoutregard to the period during which the un-derpayment continued, absent reasonablecause. The Omnibus Budget Reconcilia-tion Act of 1986, Public Law 99–509 (100Stat. 1874, 1986) amended section 6656

to impose a ten percent penalty for under-payment. The Omnibus Budget Reconcil-iation Act of 1989 further amended thissection to provide for a penalty that isequal to an applicable percentage of theamount of the underpayment based on theduration of the underpayment. This regu-lation does not reflect the most recentamendments to section 6656. Further-more, all relevant information regardingunderpayment penalties is put forth in thecode section or in other published guid-ance. This regulation does not provideany additional guidance regarding thecurrent underpayment penalties as setforth in section 6656 and therefore maybe removed.

Section 301.6656–2 explains and ex-pands upon former section 6656(b), Over-stated Deposit Claims. The OmnibusBudget Reconciliation Act of 1989 re-moved former section 6656(b), makingthis regulation obsolete.

In addition, §301.6656–3 is redesignatedas §301.6656–1. Further, §§1.6302–1(d)and 1.6302–2(d) of the Income Tax Regula-tions and §§31.6302–1(m)(1) and31.6302(c)–4(a) of the Employment TaxRegulations are revised to remove refer-ences to the removed regulations under sec-tion 6656.

Effect on other Documents

The final regulations §§301.6656–1and 301.6656–2 published in the FederalRegister for December 13, 1983(LR–311–81, 48 FR 5453), are removedas of June 15, 2001.

Special Analyses

It has been determined that the removalof these regulations is not a significantregulatory action as defined in ExecutiveOrder 12866. Therefore, a regulatory as-sessment is not required. Because this rulemerely removes regulatory provisionsmade obsolete by statute, prior notice andcomment and a delayed effective date areunnecessary and contrary to the public in-terest. 5 U.S.C. 553(b)(B) and (d) Becauseno notice of proposed rulemaking is re-quired, the Regulatory Flexibility Act (5U.S.C. chapter 6) does not apply.

Drafting Information

The principal author of the removal ofthe regulations is Robin M. Tuczak of the

July 9, 2001 36 2001–28 I.R.B.

Office of Associate Chief Counsel, Proce-dure and Administration (AdministrativeProvisions and Judicial Practice Division).

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR parts 1, 31, 301,and 602 are amended as follows:

PART 1—INCOME TAXES

Paragraph 1. The authority citation forpart 1 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * * Par. 2. In §1.6302–1, paragraph (d) is

revised to read as follows:

§1.6302–1 Use of Governmentdepositaries in connection withcorporation income and estimatedincome taxes and certain taxes of tax-exempt organizations.

* * * * *(d) Failure to deposit. For provisions

relating to the penalty for failure to makea deposit within the prescribed time, seesection 6656.

Par. 3. In §1.6302–2, paragraph (d) isrevised to read as follows:

§1.6302–2 Use of Governmentdepositaries for payment of tax withheldon nonresident aliens and foreigncorporations.

* * * * *(d) Penalties for failure to make de-

posits. For provisions relating to thepenalty for failure to make a deposit withinthe prescribed time, see section 6656.* * * * *

PART 31—EMPLOYMENT TAXESAND COLLECTION OF INCOME TAXAT SOURCE

Par. 4. The authority citation for part31 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *

Par. 5. In §31.6302–1, paragraph(m)(1) is revised to read as follows:

§31.6302–1 Federal tax deposit rules forwithheld income taxes and taxes underthe Federal Insurance Contributions Act(FICA) attributable to payments madeafter December 31, 1992.

* * * * *(m) * * *(1) Failure to deposit penalty.

For provisions relating to the penalty forfailure to make a deposit within the pre-scribed time, see section 6656.* * * * *

Par. 6. In §31.6302(c)–4, paragraph (a)is revised to read as follows:

§31.6302(c)–4 Cross references.

(a) Failure to deposit. For provisionsrelating to the penalty for failure to makea deposit within the prescribed time, seesection 6656.* * * * *

PART 301—PROCEDURE ANDADMINISTRATION

Par. 7. The authority citation for part301 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *

§§301.6656–1 and 301.6656–2[Removed]

Par. 8. Sections 301.6656–1 and301.6656–2 are removed.

§301.6656–3 [Redesignated as§301.6656–1]

Par. 9. Section 301.6656–3 is redesig-nated as new §301.6656–1.

PART 602—OMB CONTROLNUMBERS UNDER THEPAPERWORK REDUCTION ACT

Par. 10. The authority citation for part602 continues to read as follows:

Authority: 26 U.S.C. 7805.

Par. 11. In §602.101, paragraph (b) isamended by removing the entries for301.6656–1 and 301.6656–2 from the table.

Robert E. Wenzel,Deputy Commissioner

of Internal Revenue.

Approved June 1, 2001.

Mark A. Weinberger,Assistant Secretary

of the Treasury.

(Filed by the Office of the Federal Register on June14, 2001, at 8:45 a.m., and published in the issue ofthe Federal Register for June 15, 2001, 66 FR32541)

Section 7520.—Valuation Tables

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, page 31.

Section 7872.—Treatment ofLoans With Below-MarketInterest Rates

The adjusted applicable federal short-term, mid-term, and long-term rates are set forth for the monthof July 2001. See Rev. Rul. 2001–34, page 31.

2001–28 I.R.B. 37 July 9, 2001

July 9, 2001 38 2001–28 I.R.B.

26 CFR 601.601: Rules and regulations.(Also Part I, §§ 103, 141, 145; 1.141–3, 1.145–2.)

Rev. Proc. 2001–39

SECTION 1. PURPOSE

This revenue procedure modifies thedefinitions of capitation fee and per-unitfee in Rev. Proc. 97–13, 1997–1 C.B. 632,to permit an automatic increase of thosefees according to a specified, objective,external standard that is not linked to theoutput or efficiency of a facility (for ex-ample, the Consumer Price Index).

SECTION 2. BACKGROUND

.01 Rev. Proc. 97–13 sets forth condi-tions under which a management contractdoes not result in private business useunder § 141(b) of the Internal RevenueCode. The revenue procedure also ap-plies to determinations of whether a man-agement contract causes the test in § 145(a)(2)(B) to be met.

.02 Section 3 of Rev. Proc. 97–13 de-fines various terms, including capitationfee, periodic fixed fee, and per-unit fee.

.03 Section 3.02 of Rev. Proc. 97–13defines a capitation fee as a fixed periodicamount for each person for whom the ser-vice provider or the qualified user as-sumes the responsibility to provide allneeded services for a specified period solong as the quantity and type of servicesactually provided to covered personsvaries substantially. A capitation fee mayinclude a variable component of up to 20percent of the total capitation fee de-signed to protect the service provideragainst risks such as catastrophic loss.

.04 Section 3.05 of Rev. Proc. 97–13defines a periodic fixed fee as a stateddollar amount for services rendered for aspecified period of time. The definitionof periodic fixed fee provides that thestated dollar amount may automaticallyincrease according to a specified, objec-

tive, external standard that is not linked tothe output or efficiency of a facility.

.05 Section 3.06 of Rev. Proc. 97–13defines a per-unit fee as a fee based on aunit of service provided specified in thecontract or otherwise specifically deter-mined by an independent third party, suchas the administrator of the Medicare pro-gram, or the qualified user.

.06 Neither the capitation fee definitionnor the per-unit fee definition expresslycontemplates an automatic increase basedon a specified, objective, external stan-dard not linked to the output or efficiencyof the facility.

.07 This revenue procedure clarifiesthat a capitation fee and a per-unit feemay be determined using an automatic in-crease according to a specified, objective,external standard that is not linked to theoutput or efficiency of a facility (for ex-ample, the Consumer Price Index).

SECTION 3. SCOPE

This revenue procedure applies when,under a management contract, a serviceprovider provides management or otherservices involving property financedwith proceeds of an issue of state orlocal bonds subject to § 141 or § 145(a)(2)(B).

SECTION 4. MODIFICATIONS

.01 Section 3.02 of Rev. Proc. 97–13 ismodified to add the following text imme-diately before the last sentence:

A fixed periodic amount may includean automatic increase according to aspecified, objective, external standardthat is not linked to the output or effi-ciency of a facility. For example, theConsumer Price Index and similarexternal indices that track increases inprices in an area or increases in rev-enues or costs in an industry are objec-tive, external standards.

.02 Section 3.06 of Rev. Proc. 97–13 ismodified to add the following text at theend:

A fee that is a stated dollar amountspecified in the contract does not fail tobe a per-unit fee as a result of a provi-sion under which the fee may automati-cally increase according to a specified,objective, external standard that is notlinked to the output or efficiency of afacility. For example, the ConsumerPrice Index and similar external indicesthat track increases in prices in an areaor increases in revenues or costs in anindustry are objective, external stan-dards.

SECTION 5. INQUIRIES

For further information regarding thisrevenue procedure, contact David Whiteat (202) 622-3980 (not a toll-free call).

SECTION 6. EFFECT ON OTHERDOCUMENTS

This revenue procedure modifies Rev.Proc. 97–13, 1997–1 C.B. 632.

SECTION 7. EFFECTIVE DATE

This revenue procedure is effective forany management contract entered into,materially modified, or extended (otherthan pursuant to a renewal option) on orafter July 9, 2001. In addition, an issuermay apply this revenue procedure to anymanagement contract entered into prior toJuly 9, 2001.

DRAFTING INFORMATION

The principal authors of this revenueprocedure are Mary Truchly and RebeccaHarrigal, Office of Chief Counsel.

Part III. Administrative, Procedural, and Miscellanous

2001–28 I.R.B. 39 July 9, 2001

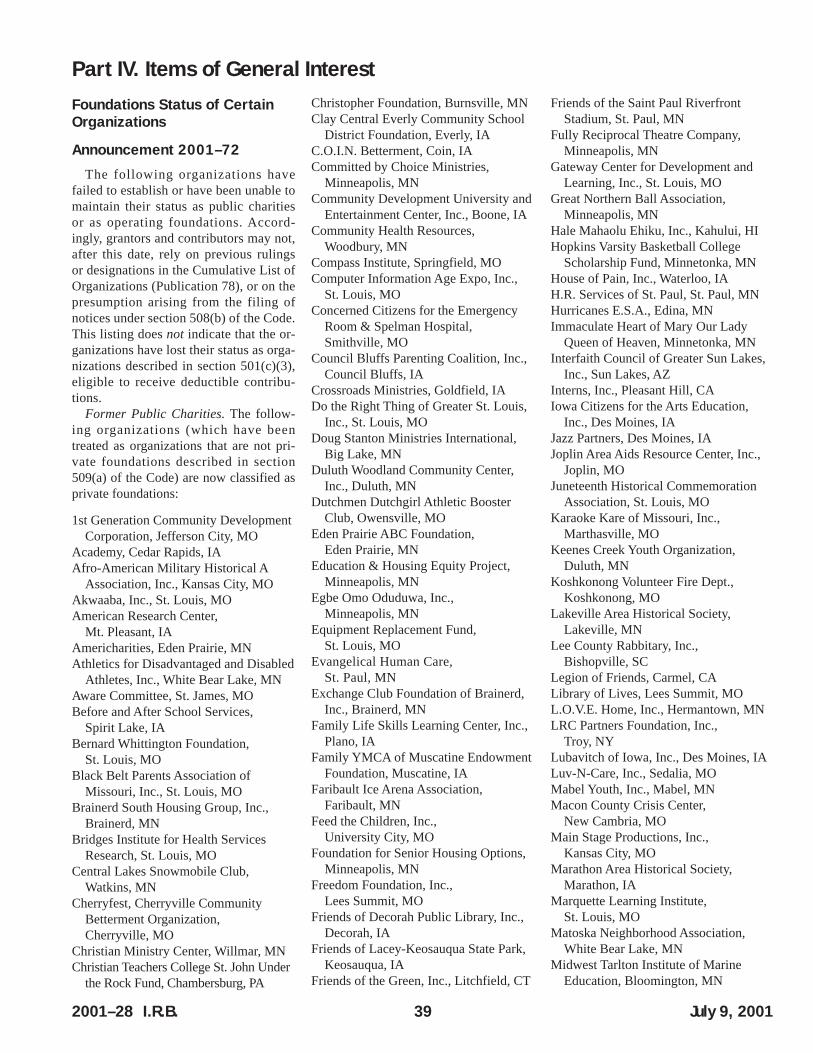

Foundations Status of CertainOrganizations

Announcement 2001–72

The following organizations havefailed to establish or have been unable tomaintain their status as public charitiesor as operating foundations. Accord-ingly, grantors and contributors may not,after this date, rely on previous rulingsor designations in the Cumulative List ofOrganizations (Publication 78), or on thepresumption arising from the filing ofnotices under section 508(b) of the Code.This listing does not indicate that the or-ganizations have lost their status as orga-nizations described in section 501(c)(3),eligible to receive deductible contribu-tions.

Former Public Charities.The follow-ing organizations (which have beentreated as organizations that are not pri-vate foundations described in section509(a) of the Code) are now classified asprivate foundations:

1st Generation Community DevelopmentCorporation, Jefferson City, MO

Academy, Cedar Rapids, IAAfro-American Military Historical A

Association, Inc., Kansas City, MOAkwaaba, Inc., St. Louis, MOAmerican Research Center,

Mt. Pleasant, IAAmericharities, Eden Prairie, MNAthletics for Disadvantaged and Disabled

Athletes, Inc., White Bear Lake, MNAware Committee, St. James, MOBefore and After School Services,

Spirit Lake, IABernard Whittington Foundation,

St. Louis, MOBlack Belt Parents Association of

Missouri, Inc., St. Louis, MOBrainerd South Housing Group, Inc.,

Brainerd, MNBridges Institute for Health Services

Research, St. Louis, MOCentral Lakes Snowmobile Club,

Watkins, MNCherryfest, Cherryville Community

Betterment Organization, Cherryville, MO

Christian Ministry Center, Willmar, MNChristian Teachers College St. John Under

the Rock Fund, Chambersburg, PA

Christopher Foundation, Burnsville, MNClay Central Everly Community School

District Foundation, Everly, IAC.O.I.N. Betterment, Coin, IACommitted by Choice Ministries,

Minneapolis, MNCommunity Development University and

Entertainment Center, Inc., Boone, IACommunity Health Resources,

Woodbury, MNCompass Institute, Springfield, MOComputer Information Age Expo, Inc.,

St. Louis, MOConcerned Citizens for the Emergency

Room & Spelman Hospital, Smithville, MO

Council Bluffs Parenting Coalition, Inc.,Council Bluffs, IA

Crossroads Ministries, Goldfield, IADo the Right Thing of Greater St. Louis,

Inc., St. Louis, MODoug Stanton Ministries International,

Big Lake, MNDuluth Woodland Community Center,

Inc., Duluth, MNDutchmen Dutchgirl Athletic Booster

Club, Owensville, MOEden Prairie ABC Foundation,

Eden Prairie, MNEducation & Housing Equity Project,

Minneapolis, MNEgbe Omo Oduduwa, Inc.,

Minneapolis, MNEquipment Replacement Fund,

St. Louis, MOEvangelical Human Care,

St. Paul, MNExchange Club Foundation of Brainerd,

Inc., Brainerd, MNFamily Life Skills Learning Center, Inc.,

Plano, IAFamily YMCA of Muscatine Endowment

Foundation, Muscatine, IAFaribault Ice Arena Association,

Faribault, MNFeed the Children, Inc.,

University City, MOFoundation for Senior Housing Options,

Minneapolis, MNFreedom Foundation, Inc.,

Lees Summit, MOFriends of Decorah Public Library, Inc.,

Decorah, IAFriends of Lacey-Keosauqua State Park,

Keosauqua, IAFriends of the Green, Inc., Litchfield, CT

Friends of the Saint Paul RiverfrontStadium, St. Paul, MN

Fully Reciprocal Theatre Company,Minneapolis, MN

Gateway Center for Development andLearning, Inc., St. Louis, MO

Great Northern Ball Association,Minneapolis, MN

Hale Mahaolu Ehiku, Inc., Kahului, HIHopkins Varsity Basketball College

Scholarship Fund, Minnetonka, MNHouse of Pain, Inc., Waterloo, IAH.R. Services of St. Paul, St. Paul, MNHurricanes E.S.A., Edina, MNImmaculate Heart of Mary Our Lady

Queen of Heaven, Minnetonka, MNInterfaith Council of Greater Sun Lakes,

Inc., Sun Lakes, AZInterns, Inc., Pleasant Hill, CAIowa Citizens for the Arts Education,

Inc., Des Moines, IAJazz Partners, Des Moines, IAJoplin Area Aids Resource Center, Inc.,

Joplin, MOJuneteenth Historical Commemoration

Association, St. Louis, MOKaraoke Kare of Missouri, Inc.,

Marthasville, MOKeenes Creek Youth Organization,

Duluth, MNKoshkonong Volunteer Fire Dept.,

Koshkonong, MOLakeville Area Historical Society,

Lakeville, MNLee County Rabbitary, Inc.,

Bishopville, SCLegion of Friends, Carmel, CALibrary of Lives, Lees Summit, MOL.O.V.E. Home, Inc., Hermantown, MNLRC Partners Foundation, Inc.,

Troy, NYLubavitch of Iowa, Inc., Des Moines, IALuv-N-Care, Inc., Sedalia, MOMabel Youth, Inc., Mabel, MNMacon County Crisis Center,

New Cambria, MOMain Stage Productions, Inc.,

Kansas City, MOMarathon Area Historical Society,

Marathon, IAMarquette Learning Institute,

St. Louis, MOMatoska Neighborhood Association,

White Bear Lake, MNMidwest Tarlton Institute of Marine

Education, Bloomington, MN

Part IV. Items of General Interest

Minnesota Aviation History andEducation Center, Inc., St. Paul, MN

Mission-A Catholic Worker Community,St. Cloud, MN

Missouri Black Bass Unlimited, Inc.,Clinton, MO

Mt. Pleasant Neighborhood, St. Louis, MO

National Native American War MemorialComplex, Incorporated, Chapter Oak, IA

Network for Prep., Inc., Bettendorf, IANew Harmony Care Center, Inc.,

Richfield, MNNguzo Saba Community Studio,

St. Paul, MNNisswa Enhanced Reading Foundation,

Nisswa, MNNorth Lilbourn Development, Inc.,

Lilbourn, MONorthland Opera Theater Experience,

Duluth, MNNorthside Economic Development

Council, Inc., Minneapolis, MNOne Small Step, St. Paul, MNParents Together Network, Inc.,

Marion, IAPatch, Ballwin, MOPaths Unlimited, Minneapolis, MNPeople Place, Minneapolis, MNPhilip & Adeline Woods Memorial Fund,

Yanceyville, NCPilot Grove Community Athletic

Association, Pilot Grove, MOPlayground, Inc., Buffalo, MOPort Morris Neighborhood Development

Corporation, Bronx, NYPresbyterian Homes-Wedum Affordable

Housing, Inc., Arden Hills, MNQuite Light Opera Company,

St. Joseph, MNRalls County Community 2000, Inc.,

Perry, MORecover America, Inc., Joplin, MORecovery Road, Inc., St. Paul, MNRed Wing Public Schools Foundation,