internal revenue bulletin no. 2000–41 bulletin october 10 ... · 2000–41 i.r.b. october 10,...

TRANSCRIPT

INCOME TAX

Rev. Rul. 2000–43, page 333.Charitable contributions; S corporations; section 170-(a)(2). An accrual-basis S corporation may not elect undersection 170(a)(2) of the Code to treat a charitable contribu-tion as paid in the year authorized by the S corporation’sboard of directors if the contribution is paid by the S corpo-ration after the close of the tax year.

Rev. Rul. 2000–44, page 336.Transactions between partner and partnership. A corpo-ration that acquires assets of another corporation in a trans-action described in section 381(a) of the Code succeeds to thestatus of the other corporation for purposes of applying theexception for reimbursements of preformation expendituresand determining whether a liability is a qualified liability underthe regulations regarding the disguised sale provisions of sec-tion 707(a)(2)(B).

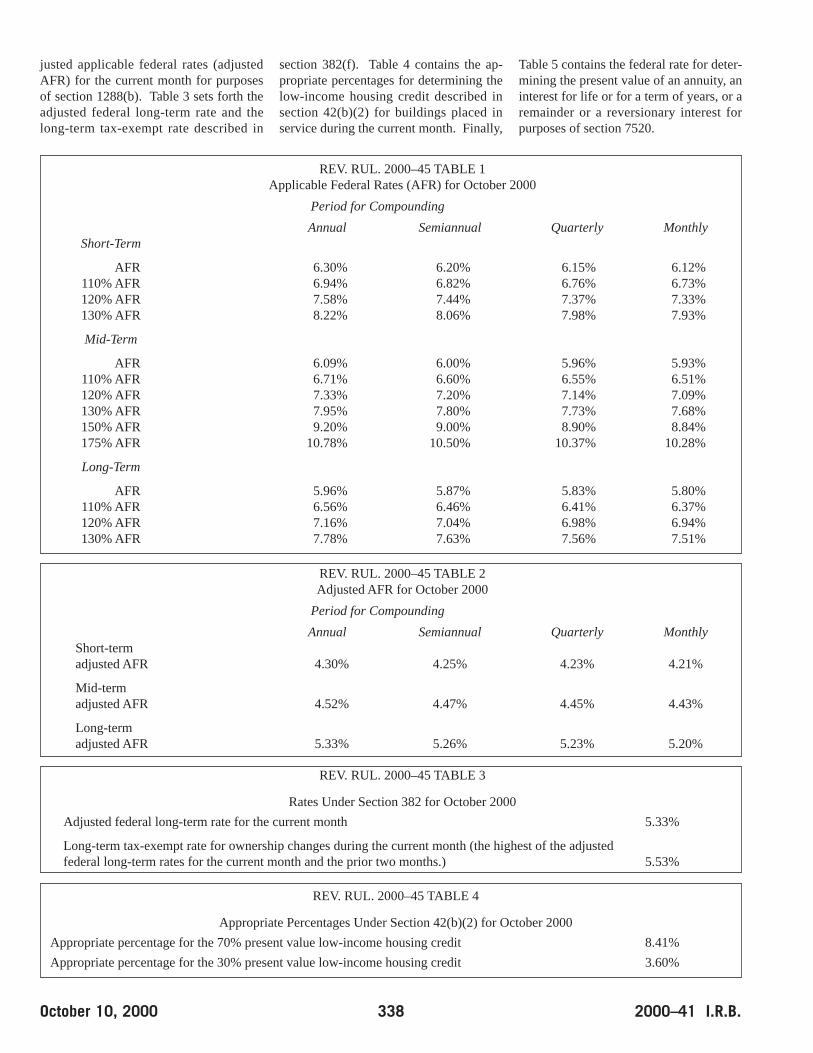

Rev. Rul. 2000–45, page 337.Federal rates; adjusted federal rates; adjusted federallong-term rate, and the long-term exempt rate. For pur-poses of sections 1274, 1288, 382, and other sections of theCode, tables set forth the rates for October 2000.

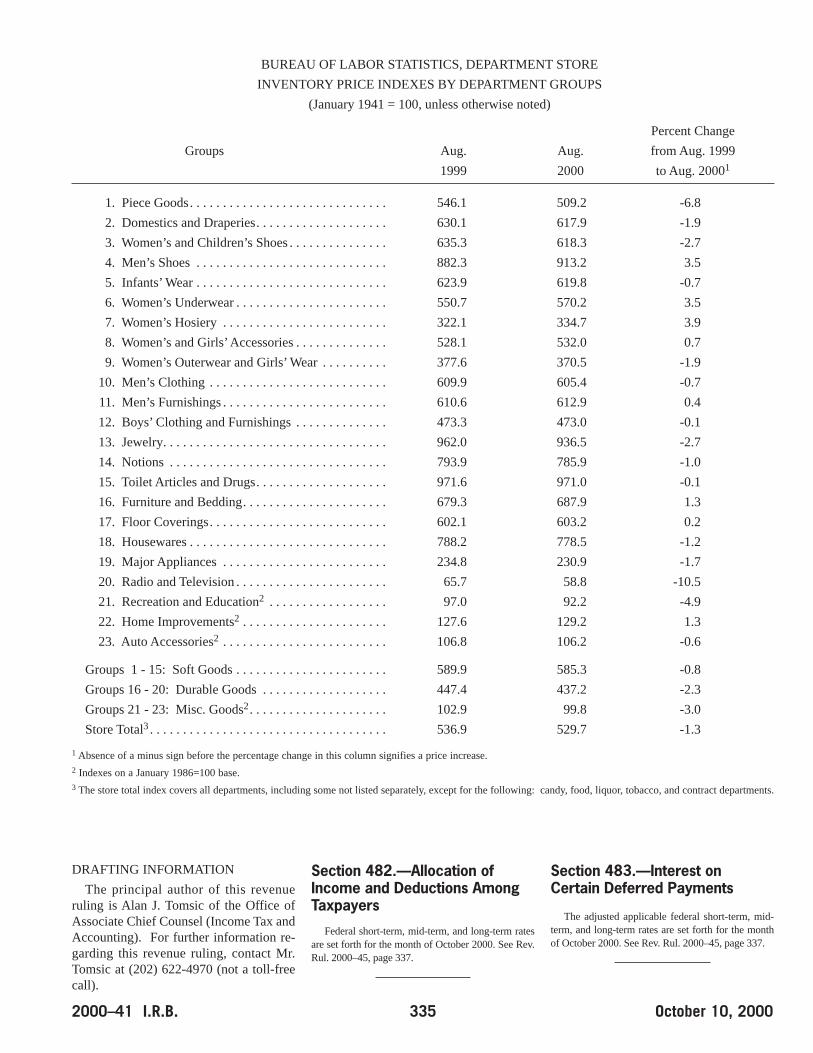

Rev. Rul. 2000–46, page 334.LIFO; price indexes; department stores. The August 2000Bureau of Labor Statistics price indexes are accepted for useby department stores employing the retail inventory and last-in,first-out inventory methods for valuing inventories for tax yearsended on, or with reference to, August 31, 2000.

T.D. 8902, page 323.Final regulations interpret the look-through provisions of sec-tion 1(h) of the Code (relating to collectibles and section1250 capital gain) when an interest in a pass-thru entity issold or exchanged and provide rules for dividing the holdingperiod of an interest in a partnership.

ADMINISTRATIVE

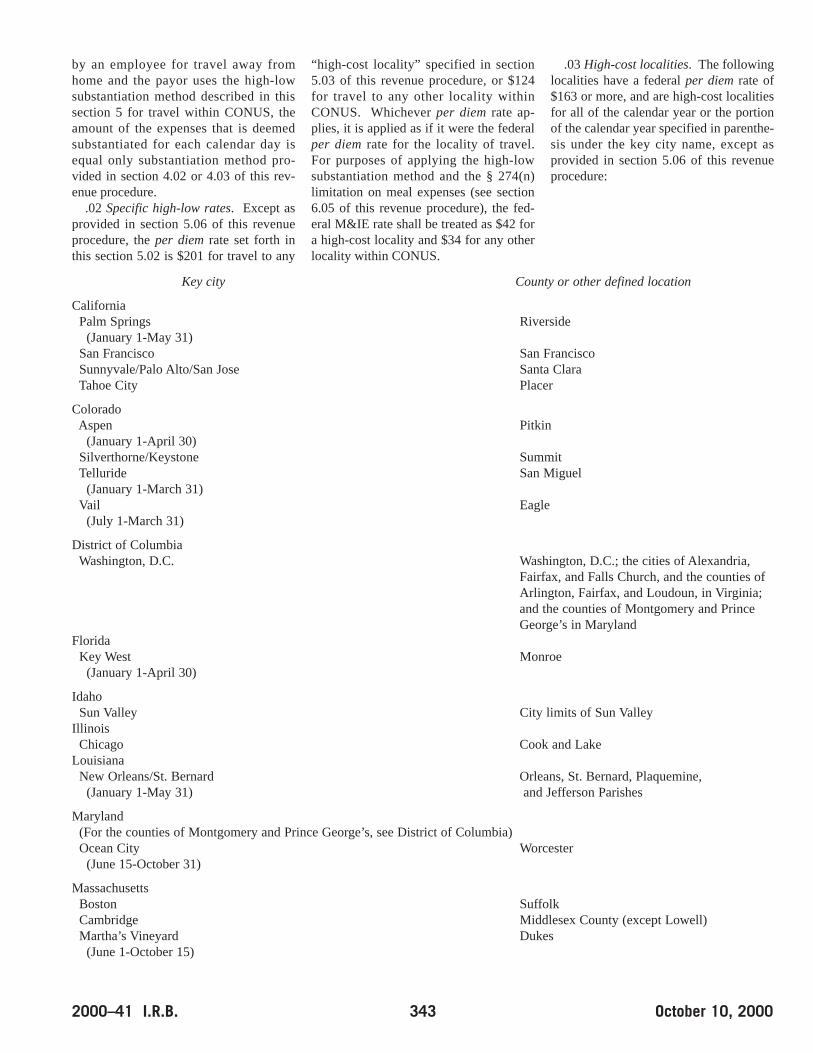

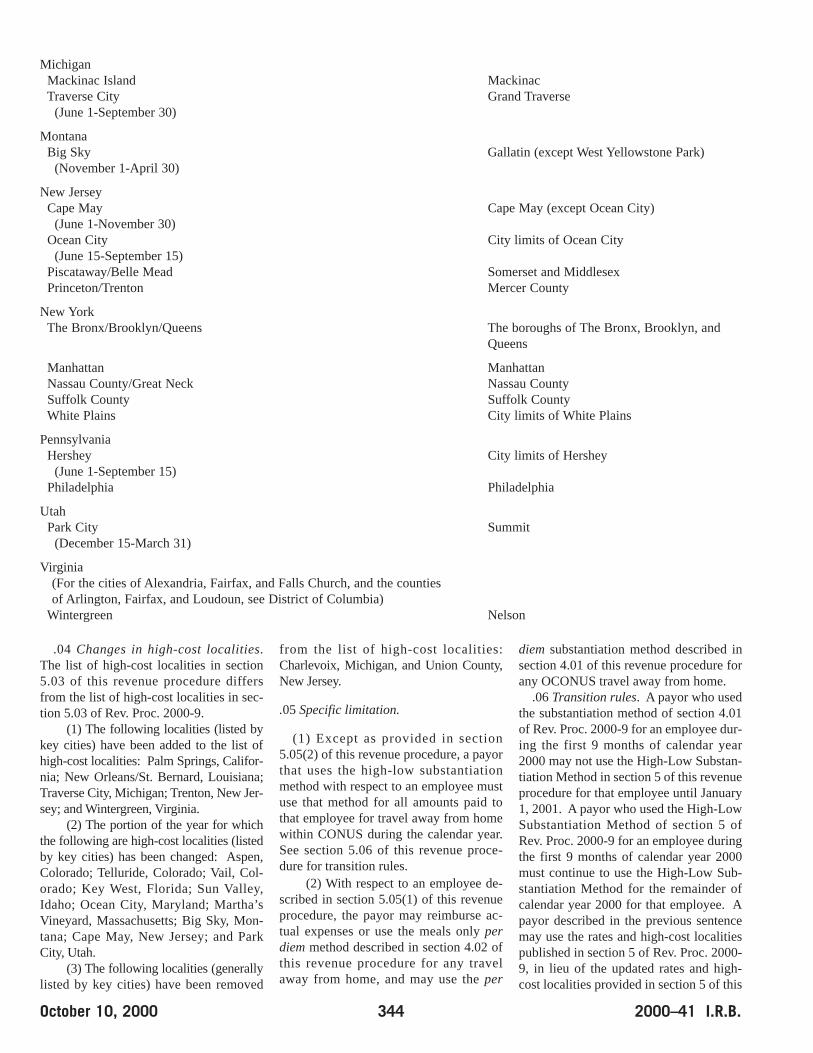

Rev. Proc. 2000–39, page 340.Per diem allowances. This procedure provides optional rulesfor deeming substantiated the amount of certain reimbursedtraveling expenses of an employee as well as for determiningthe amount of deductible meals while traveling away fromhome. Rev. Proc. 2000–9 superseded. Notice 2000–48superseded.

Announcement 2000–81, page 348.This document contains corrections to final regulations (T.D.8892, 2000–32 I.R.B. 158) relating to the removal of tem-porary regulations concerning the Telefile Voice Signaturetest.

Announcement 2000–83, page 348.New Form 8869, Qualified Subchapter S Subsidiary Election,is now available. This form is used by a parent S corporationto elect to treat one or more of its eligible subsidiaries as aqualified subchapter S subsidiary (QSub).

Internal Revenue

bbuulllleettiinnBulletin No. 2000–41

October 10, 2000

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

Department of the TreasuryInternal Revenue Service

Finding Lists begin on page ii.Actions Relating to Court Decisions is on the page following the introduction.

October 10, 2000 2000–41 I.R.B.

The Internal Revenue Bulletin is the authoritative instrumentof the Commissioner of Internal Revenue for announcing offi-cial rulings and procedures of the Internal Revenue Serviceand for publishing Treasury Decisions, Executive Orders, TaxConventions, legislation, court decisions, and other items ofgeneral interest. It is published weekly and may be obtainedfrom the Superintendent of Documents on a subscriptionbasis. Bulletin contents are consolidated semiannually intoCumulative Bulletins, which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform applicationof the tax laws, including all rulings that supersede, revoke,modify, or amend any of those previously published in theBulletin. All published rulings apply retroactively unless other-wise indicated. Procedures relating solely to matters of in-ternal management are not published; however, statementsof internal practices and procedures that affect the rightsand duties of taxpayers are published.

Revenue rulings represent the conclusions of the Service onthe application of the law to the pivotal facts stated in therevenue ruling. In those based on positions taken in rulingsto taxpayers or technical advice to Service field offices,identifying details and information of a confidential natureare deleted to prevent unwarranted invasions of privacy andto comply with statutory requirements.

Rulings and procedures reported in the Bulletin do not havethe force and effect of Treasury Department Regulations,but they may be used as precedents. Unpublished rulingswill not be relied on, used, or cited as precedents by Servicepersonnel in the disposition of other cases. In applying pub-lished rulings and procedures, the effect of subsequent leg-islation, regulations, court decisions, rulings, and proce-

dures must be considered, and Service personnel and oth-ers concerned are cautioned against reaching the same con-clusions in other cases unless the facts and circumstancesare substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisionsof the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions, and Subpart B, Legislation and RelatedCommittee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references tothese subjects are contained in the other Parts and Sub-parts. Also included in this part are Bank Secrecy Act Admin-istrative Rulings. Bank Secrecy Act Administrative Rulingsare issued by the Department of the Treasury’s Office of theAssistant Secretary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The first Bulletin for each month includes a cumulative indexfor the matters published during the preceding months.These monthly indexes are cumulated on a semiannual basis,and are published in the first Bulletin of the succeeding semi-annual period, respectively.

The IRS Mission

Provide America’s taxpayers top quality service by help-ing them understand and meet their tax responsibilities

and by applying the tax law with integrity and fairness toall.

Introduction

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

2000–41 I.R.B. October 10, 2000

It is the policy of the Internal RevenueService to announce at an early datewhether it will follow the holdings in cer-tain cases. An Action on Decision is thedocument making such an announcement.An Action on Decision will be issued atthe discretion of the Service only on un-appealed issues decided adverse to thegovernment. Generally, an Action on De-cision is issued where its guidance wouldbe helpful to Service personnel workingwith the same or similar issues. Unlike aTreasury Regulation or a Revenue Ruling,an Action on Decision is not an affirma-tive statement of Service position. It is notintended to serve as public guidance andmay not be cited as precedent.

Actions on Decisions shall be reliedupon within the Service only as conclu-sions applying the law to the facts in theparticular case at the time the Action onDecision was issued. Caution should beexercised in extending the recommenda-tion of the Action on Decision to similarcases where the facts are different. More-over, the recommendation in the Actionon Decision may be superseded by newlegislation, regulations, rulings, cases, orActions on Decisions.

Prior to 1991, the Service published ac-quiescence or nonacquiescence only incertain regular Tax Court opinions. TheService has expanded its acquiescenceprogram to include other civil tax caseswhere guidance is determined to be help-ful. Accordingly, the Service now may ac-quiesce or nonacquiesce in the holdingsof memorandum Tax Court opinions, aswell as those of the United States DistrictCourts, Claims Court, and Circuit Courtsof Appeal. Regardless of the court decid-ing the case, the recommendation of anyAction on Decision will be published inthe Internal Revenue Bulletin.

The recommendation in every Actionon Decision will be summarized as ac-quiescence, acquiescence in result only,or nonacquiescence. Both “acquies-cence” and “acquiescence in result only”mean that the Service accepts the holdingof the court in a case and that the Servicewill follow it in disposing of cases withthe same controlling facts. However, “ac-quiescence” indicates neither approvalnor disapproval of the reasons assignedby the court for its conclusions; whereas,“acquiescence in result only” indicatesdisagreement or concern with some or all

of those reasons. “Nonacquiescence” sig-nifies that, although no further reviewwas sought, the Service does not agreewith the holding of the court and, gener-ally, will not follow the decision in dis-posing of cases involving other taxpay-ers. In reference to an opinion of a circuitcourt of appeals, a “nonacquiescence” in-dicates that the Service will not followthe holding on a nationwide basis. How-ever, the Service will recognize theprecedential impact of the opinion oncases arising within the venue of the de-ciding circuit.

The Actions on Decisions published inthe weekly Internal Revenue Bulletin areconsolidated semiannually and appear inthe first Bulletin for July and the Cumu-lative Bulletin for the first half of theyear. A semiannual consolidation also ap-pears in the first Bulletin for the follow-ing January and in the Cumulative Bul-letin for the last half of the year.

The Commissioner ACQUIESCES inthe following decision:

Kathy A. King v. Commissioner,1

115 T.C. No. 8

Actions Relating to Decisions of the Tax Court

1 Acquiescence relating to whether a nonpetitioning spouse (or former spouse) is entitled to notice and an opportunity to become a party within the meaning of I.R.C.section 6015(e)(4) in a deficiency case where the petitioning spouse (or former spouse) is claiming relief from joint and several liability under section 6015.

Section 1.—Tax Imposed

26 CFR 1.1(h)–1: Capital gains look-through rulefor sales or exchanges of interests in a partnership,S corporation, or trust.

T.D. 8902

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Parts 1 and 602

Capital Gains, Partnership,Subchapter S, and TrustProvisions

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document containsfinal regulations relating to sales or ex-changes of interests in partnerships, Scorporations, and trusts. The regulationsinterpret the look-through provisions ofsection 1(h), added by section 311 of theTaxpayer Relief Act of 1997 and amendedby sections 5001 and 6005(d) of the Inter-nal Revenue Service Restructuring andReform Act of 1998, and explain the rulesrelating to the division of the holding pe-riod of a partnership interest. The regula-tions affect partnerships, partners, S cor-porations, S corporation shareholders,trusts, and trust beneficiaries.

DATES: Effective Date: These regula-tions are effective September 21, 2000.

FOR FURTHER INFORMATION CON-TACT: Jeanne M. Sullivan or David J.Sotos (202) 622-3050 (not a toll-freenumber).

SUPPLEMENTARY INFORMATION:

Paperwork Reduction Act

The collections of information con-tained in these final regulations have beenreviewed and approved by the Office ofManagement and Budget in accordancewith the Paperwork Reduction Act of1995 (44 U.S.C. 3507) under controlnumber 1545-1654. Responses to thesecollections of information are required toverify compliance with section 1(h) andto determine that the tax on capital gainshas been computed correctly.

An agency may not conduct or sponsor,and a person is not required to respond to,a collection of information unless the col-lection of information displays a validcontrol number assigned by the Office ofManagement and Budget.

The estimated annual burden per re-spondent/recordkeeper is 10 minutes.

Comments concerning the accuracy ofthis burden estimate and suggestions forreducing this burden should be sent to theInternal Revenue Service, Attn: IRS Re-ports Clearance Officer, OP:FS:FP, Wash-ington, DC 20224, and to the Office ofManagement and Budget, Attn: DeskOfficer for the Department of the Trea-sury, Office of Information and Regula-tory Affairs, Washington, DC 20503.

Books or records relating to this collec-tion of information must be retained aslong as their contents may become mater-ial in the administration of any internalrevenue law. Generally, tax returns andtax return information are confidential, asrequired by 26 U.S.C. 6103.

Background

Section 311 of the Taxpayer Relief Actof 1997, Public Law 105-34 (111 Stat.788, 831) (the 1997 Act), as modified bysections 5001 and 6005(d) of the InternalRevenue Service Restructuring and Re-form Act of 1998, Public Law 105-206(112 Stat. 685, 787, 800) (the 1998 Act),reduced the maximum statutory tax ratesfor long-term capital gains of individualsin general and provided regulatory author-ity to apply the rules to sales and ex-changes of interests in pass-thru entitiesand to sales and exchanges by pass-thruentities. On August 9, 1999, the IRS pub-lished in the Federal Registera notice ofproposed rulemaking (REG–106527–98,1999–34 I.R.B. 304 [64 F.R. 43117]) relat-ing to the taxation of capital gains in thecase of sales or exchanges of interests inpartnerships, S corporations, and trusts.The regulations interpreted rules added bythe 1997 Act and amended by the 1998Act, and provided guidance relating to thedivision of the holding period of a partner-ship interest. The IRS received no re-quests to speak at a public hearing thatwas scheduled for November 18, 1999,and canceled the hearing. Written com-

ments were received in response to the no-tice of proposed rulemaking. After con-sideration of the comments, the proposedregulations under sections 1(h), 741, and1223 are adopted, as revised by this Trea-sury decision. The comments receivedand revisions made are discussed below.

Explanation of Revisions and Summaryof Comments

1. Look-Through Capital Gain

a. In General

Section 1(h) provides maximum capitalgains rates in three categories: 20-percentrate gain, 25-percent rate gain, and 28-per-cent rate gain. Twenty percent rate gain isnet capital gain from the sale or exchangeof capital assets held for more than oneyear, reduced by the sum of 25-percentrate gain and 28-percent rate gain.Twenty-five percent rate gain is limited tounrecaptured section 1250 gain. Twenty-eight percent rate gain includes capitalgains and losses from the sale or exchangeof collectibles (as defined in section408(m) without regard to section408(m)(3)) held for more than one yearand certain other types of gain.

Capital gain attributable to the sale orexchange of an interest in a pass-thru en-tity held for more than one year generallyis in the 20-percent rate gain category.However, the proposed regulations pro-vide that, when a taxpayer sells or ex-changes an interest in a partnership, S cor-poration, or trust that holds collectibles,rules similar to the rules under section751(a) apply to determine the capital gainthat is attributable to certain unrealizedgain in the collectibles. Furthermore,under the proposed regulations, rules simi-lar to the rules under section 751(a) alsoapply to determine the capital gain attrib-utable to certain unrealized gain in section1250 property held by a partnership whena taxpayer sells or exchanges an interest ina partnership that holds such property.

b. Net Collectibles Loss

Twenty-eight percent rate gain is theexcess (if any) of (i) the sum of col-lectibles gain and section 1202 gain, over

2000–41 I.R.B. 323 October 10, 2000

Part I. Rulings and Decisions Under the Internal Revenue Code of 1986

October 10, 2000 324 2000–41 I.R.B.

(ii) the sum of collectibles loss, the netshort-term loss, and the amount of long-term capital loss carried under section1212(b)(1)(B) to the taxable year. Onecommentator suggested that, when an in-terest in a partnership, S corporation, ortrust is transferred, net collectibles loss aswell as net collectibles gain in propertyheld by such an entity should be takeninto account in determining a taxpayer’soverall collectibles gain or collectiblesloss. The Treasury Department (Trea-sury) and the IRS believe that the pro-posed regulations are consistent with therule in section 1(h)(6)(B), which, in pro-viding look-through treatment with re-spect to collectibles, refers only to “gainfrom the sale of an interest in a partner-ship, S corporation, or trust which is at-tributable to unrealized appreciation inthe value of collectibles . . .” Accord-ingly, the comment is not adopted in thefinal regulations.

c. Limitations with Respect to Section1231 Property

Section 1(h)(7)(B) limits the amountof unrecaptured section 1250 gain recog-nized as a consequence of sales, ex-changes, and conversions described insection 1231(a)(3)(A) to the taxpayer’snet section 1231 gain (as defined in sec-tion 1231(c)(3)) for the taxable year. Theproposed regulations provide that, upon apartner’s transfer of a partnership inter-est, the partner’s allocable share of sec-tion 1250 capital gain (as defined in§1.1(h)-1(b)(3)) is not treated as section1231 gain for purposes of applying thelimitation in section 1(h)(7)(B). Therehas been some confusion regardingwhether the section 1(h)(7)(B) limitationapplies to all unrecaptured section 1250gain, including section 1250 capital gainrecognized on the transfer of a partner-ship interest.

Because the transfer of an interest in apartnership is not described in section1231(a)(3)(A), the limitation provided insection 1(h)(7)(B) is not applicable withrespect to such transfers. Accordingly,under the final regulations (and consis-tent with the proposed regulations),where a partner sells an interest in a part-nership, the partner must take into ac-count the entire allocable share of section1250 capital gain in determining the un-recaptured section 1250 gain under sec-

tion 1(h)(7)(A), without regard to thelimitation set forth in section 1(h)(7)(B).

d. Redemption of a Partnership Interest

Some practitioners have expressed con-cern that the look-through capital gainsprovisions of the proposed regulationsapply to the redemption of a partnershipinterest. To apply the regulations in thecontext of redemptions, it would be nec-essary to import the concepts utilized insection 751(b). Treasury and the IRS be-lieve that this would not be advisable.Accordingly, these regulations do notapply to any transaction that is treated as aredemption of a partnership interest forFederal income tax purposes.

e. Allocating Section 704(c) Gain andLoss

Certain commentators requested thatthe final regulations provide guidancewith respect to the proportionate part ofthe section 704(c) built-in gain or loss thatis transferred to the purchaser when a sec-tion 704(c) partner sells a portion of apartnership interest. This issue is relevantbecause, in determining a taxpayer ’sshare of collectibles gain or section 1250capital gain on the sale of a partnershipinterest, it is necessary to calculate howmuch of such gain would be allocatedwith respect to the partnership interestsold if the underlying collectibles or sec-tion 1250 property held by the partnershipwere sold for their fair market value. Inmaking this determination where a part-ner sells only a portion of its interest in apartnership, it is necessary to determinehow much section 704(c) gain relating tocollectibles or section 1250 property is al-locable to the portion of the partnershipinterest that is sold. Although relevant,Treasury and the IRS believe that thisissue is beyond the scope of these regula-tions. Accordingly, this comment is notaddressed in these regulations.

f. Look-Through Capital Gain Where thePass-Thru Entity Has a Short-TermHolding Period in Collectibles

The final regulations modify the pro-posed regulations to provide that a pass-thru entity’s holding period in the col-lectibles is not relevant in determiningwhether long-term capital gain recog-nized on the sale of an interest in the en-

tity is collectibles gain (taxable at a 28-percent rate). Consistent with the purposeof the look-through provisions containedin section 1(h), these regulations charac-terize a transferor’s long-term capital gainrecognized on the sale of the interest in apass-thru entity by reference to the en-tity’s underlying assets that give rise tosuch gain. Where a transferor recognizeslong-term capital gain on the sale of an in-terest in a partnership, S corporation, ortrust, it would be anomalous to providethe transferor with a better tax result if theentity has a short-term holding period incollectibles than if the entity has a long-term holding period in such property.This rule is not relevant with respect tosection 1250 property. Because all depre-ciation with respect to section 1250 prop-erty held for one year or less is treated asadditional depreciation under section1250(b)(1), such amounts will be treatedas unrealized receivables under section751(c) and thus will give rise to ordinaryincome under section 751(a) upon a dis-position of the partnership interest.

2. Determination of Holding Period in aPartnership

a. In General

The proposed regulations provide rulesrelating to the allocation of a dividedholding period with respect to an interestin a partnership. These rules generallyprovide that the holding period of a part-nership interest will be divided if a part-ner acquires portions of an interest at dif-ferent times or if an interest is acquired ina single transaction that gives rise to dif-ferent holding periods under section1223. Under the proposed regulations,the holding period of a portion of a part-nership interest generally is determinedbased on a fraction that is equal to the fairmarket value of the portion of the partner-ship interest to which the holding periodrelates (determined immediately after theacquisition) over the fair market value ofthe entire partnership interest.

Under the proposed regulations, a sell-ing partner generally cannot identify anduse the actual holding period for a portionof the partner’s interest. However, theproposed regulations provide that a sell-ing partner is permitted to identify theportion of a partnership interest sold withits holding period if the partnership is a

publicly traded partnership (as definedunder section 7704(b)), the partnershipinterest is divided into identifiable unitswith ascertainable holding periods, andthe selling partner can identify the portionof the interest transferred.

b. Contributions of Cash by ExistingPartners

The proposed regulations include anexample of a pro rata contribution of cashby partners that results in a divided hold-ing period in those partners’ interests inthe partnership. Commentators suggestedthat it is inappropriate to provide for a di-vided holding period where an existingpartner contributes cash to the partner-ship, particularly where the contributionis pro rata by all of the partners. Accord-ing to these commentators, such an ap-proach may unfairly convert portions oflong-term appreciation of partnership as-sets into a short-term capital gain on thesale of a long held partnership interest.(This conversion occurs regardless ofwhether the partner sells all or a portionof a partnership interest.)

The conversion of long-term apprecia-tion in partnership assets into short-termcapital gain upon the sale of a partnershipinterest as a result of cash contributions tothe partnership is largely the product ofpartners having unitary bases in their part-nership interests. See Rev. Rul. 84-53(1984-1 C.B. 159) (a partner has a singlebasis in a partnership interest). Under thisrule, gain attributable to previously con-tributed or acquired assets may be allo-cated to the short-term portion of a part-nership interest even though the value ofthe short-term portion is no greater thanthe amount of cash contributed to thepartnership. If basis from contributedcash or property could be traced to a seg-regated interest in the partnership, thisconversion of long-term capital apprecia-tion into short-term capital gain would notoccur. Larger problems would arise,however, in the context of partnershiptaxation if a partner were allowed to havea divided basis in a partnership interest.

An aggregate approach to determiningthe holding period of an interest in a part-nership would make it more likely that acontribution of cash would not give rise toa short-term holding period. Under an ag-gregate approach, one could trace con-tributed funds into the partnership and de-

termine whether a new holding periodwas created by reference to whether thefunds were used for capital expenditures(in which circumstance, a short-termholding period generally would be appro-priate) or for operating expenditures ofthe partnership (in which circumstance,no new holding period should be created).On the other hand, to the extent that apartnership interest is a capital asset thatis distinct from the partnership’s assets(an entity approach), its holding periodand basis should be determined indepen-dently and should not be affected by thepartnership’s use of the contributed funds.In choosing the entity approach in theproposed regulations, Treasury and theIRS concluded that tracing funds to theirultimate use in the partnership is not anadministrable means of determiningwhether a contribution to a partnershipcreates a new holding period.

Furthermore, the proposed regulationsare consistent with general rules relatingto the holding period of capital and sec-tion 1231 assets. Where a capital asset(including a capital asset held for one yearor less) or property described in section1231 is contributed to a partnership, sec-tion 1223(1) requires the tacking of theholding period in the partnership interest,whether the partners make pro rata contri-butions of property or instead make non-pro rata contributions that increase theproportionate interests of one or morepartners.

In addition, the proposed regulationsavoid inappropriate results that may occurif cash contributions are ignored after theformation of a partnership. If cash contri-butions were ignored, it would be possiblefor partners to form shelf partnershipswith nominal cash contributions in orderto start their holding period in the inter-ests, where the majority of cash would notbe contributed (and significant operatingassets of the partnership would not be ac-quired) until some time in the future. Thisclearly would not be a proper result.

Based upon the foregoing, Treasury andthe IRS continue to believe that the ap-proach taken in the proposed regulationsis appropriate. However, in response tocomments, Treasury and the IRS have pro-vided one exception, and explicitly grantauthority for another, where the contribu-tion of cash will not create a new holdingperiod in a partnership interest.

If a partner makes cash contributionsand receives cash distributions from apartnership during the one-year period be-fore sale of all or a portion of the interestin the partnership, Treasury and the IRSbelieve it is appropriate that the net cashcontribution to the partnership determinethe portion of the interest that is held forone year or less. Therefore, the final reg-ulations provide that, if a partner makesone or more cash contributions and re-ceives one or more cash distributions withrespect to the partnership during the one-year period ending on the date of the saleor exchange of all or a portion of the part-ner’s interest in the partnership, in apply-ing the rules for determining the partner’sholding period in its partnership interestwith respect to cash contributions, thepartner may reduce the cash contributionsmade during the year by cash distribu-tions received on a last-in-first-out basis,treating all cash distributions as if theywere received by the partner immediatelybefore the sale or exchange. This rulealso applies in determining the holdingperiod of a partnership interest where gainor loss is recognized under section 731(a)upon a distribution by the partnership.

In addition, the final regulations in-clude authority for the Secretary to pro-vide, in published guidance, additionalexceptions to the general holding periodrules with respect to other cash contribu-tions, including de minimiscash contribu-tions, to a partnership. Treasury and theIRS request comments as to the appropri-ate level for a de minimisexception.

c. Treatment of Deemed CashContributions under Section 752(a)

Section 752(a) provides that an in-crease in a partner’s share of partnershipliabilities, or an increase in a partner’s in-dividual liabilities by reason of the part-ner’s assumption of partnership liabilities,shall be treated as a contribution ofmoney by the partner to the partnership.Some practitioners have questionedwhether a partner’s deemed contributionof cash under section 752(a) will give riseto a new holding period in that partner’sinterest in the partnership. A deemed con-tribution of cash resulting from a shiftamong partners in their share of liabilitiesor as a result of a partnership incurringnew debt does not expand the net assetbase of the partners represented by their

2000–41 I.R.B. 325 October 10, 2000

interests in the partnership. Accordingly,it is inappropriate to create a new holdingperiod as a result of such deemed contri-butions. However, to the extent that apartner actually assumes a debt of thepartnership, thus causing an increase inthe net asset base of the partnership, thecreation of a new holding period with re-spect to a portion of the partner’s interestis appropriate.

In addressing a similar issue, the capi-tal account rules regarding the treatmentof liabilities under §1.704–1(b)(2)(iv)(c)attempt to measure the increase or de-crease in a partner’s economic interest inthe partnership resulting from the as-sumption of liabilities by either the part-ner or the partnership. Those rules pro-vide:

(1) money contributed by a partner to a partner-ship includes the amount of any partnership liabili-ties that are assumed by such partner (other than[certain] liabilities . . . that are assumed by a distrib-utee partner [in connection with a distribution ofproperty by the partnership]) but does not includeincreases in such partner’s share of partnership lia-bilities (see section 752(a)), and (2) money distrib-uted to a partner by a partnership includes theamount of such partner’s individual liabilities thatare assumed by the partnership (other than [certain]liabilities . . . that are assumed by the partnership [inconnection with a contribution of property to thepartnership]) but does not include decreases in suchpartner’s share of partnership liabilities (see section752(b)). . .

This rule is incorporated in the finalregulations. The final regulations providethat deemed contributions and distribu-tions of cash under sections 752(a) and(b) will be disregarded in determining apartner’s holding period in its partnershipinterest to the same extent that suchamounts are disregarded under§1.704–1(b)(2)(iv)(c). (Deemed distribu-tions under section 752(b) are relevant asa result of the cash netting rule added inthese final regulations.)

d. Contribution of Section 751 Assets

Commentators noted that, if a partnerhas a short-term holding period in a part-nership interest on account of the contri-bution of assets described in section751(c) or (d) (section 751 assets), therules of section 751(a) in conjunctionwith the proposed regulations cause thesection 751 assets to be counted twice if apartnership interest is sold within 12months of the contribution, once in apply-ing section 751(a) to treat part of theamount received as ordinary income, and

again in determining the selling partner’sshort-term capital gain. In response tothese comments, the final regulations pro-vide that, if a partner recognizes ordinaryincome or loss on account of section 751assets, either under section 751(a) as a re-sult of the sale of all or part of the partner-ship interest or as a result of the sale bythe partnership of the section 751 assets,the section 751 assets shall be disregardedin determining the division of the holdingperiod of an interest in a partnership upona sale of such partnership interest duringthe one-year period following the contri-bution. This rule does not apply if, in theabsence of the rule, a partner would notbe treated as having held any portion ofthe interest for more than one year. Ac-cordingly, if a partner’s only contributionsto a partnership are contributions of sec-tion 751 assets or section 751 assets andcash within the prior one-year period, theadjustment will not be available, and thepartner appropriately will be treated ashaving a short-term holding period withrespect to the entire interest.

A similar rule disregarding the contri-bution of section 751 assets does notapply in determining the holding periodof a partnership interest with respect togain or loss recognized under section 731upon a distribution by a partnership.Properly coordinating the holding periodrules with gain or loss determinationsunder section 751(b) would be inordi-nately complex. In addition, where,within a one-year period, a partner con-tributes section 751 assets to a partnershipand receives a cash distribution largeenough to require the recognition of gain,it is likely that the contribution and distri-bution will constitute a disguised sale ofthe section 751 assets to the partnershipunder section 707(a)(2)(B), thus render-ing the holding period rules irrelevantsince the sale of an asset to a partnershipdoes not affect the holding period of aninterest in the partnership.

e. Treatment of Recapture and OtherUnrealized Receivables

An example in the proposed regula-tions treats the portion of a contributedasset that would be recaptured as ordinaryincome under section 1245 upon disposi-tion as non-section 1231 property for pur-poses of the tacked holding period rule insection 1223(1). Some commentators

have raised questions regarding the posi-tion taken in this example. For purposesof these regulations, Treasury and the IRSbelieve that it is appropriate to character-ize all properties and potential gaintreated as unrealized receivables undersection 751(c) and the regulations there-under as separate assets that are not capi-tal assets or property described in section1231. Accordingly, while the example inthe proposed regulations has been elimi-nated, a specific rule has been added inthe final regulations to provide for such aresult. This rule is consistent with therule added in the final regulations regard-ing the holding period exception for con-tributed section 751 assets. As discussedabove, that rule will disregard the contri-bution of section 751 assets (includingproperties and potential gain treated asunrealized receivables under section751(c)) in computing the holding periodof a partnership interest where the interestis sold within one year after contribution.Accordingly, while section 1245 recap-ture (and similar items treated as unreal-ized receivables) will be treated as a sepa-rate asset that is not a capital or section1231 asset, the asset will not give rise to ashort-term holding period where a part-nership interest is sold. This rule also issimilar to the rule contained in § 1.755–1(a), which provides that proper-ties and potential gain treated as unreal-ized receivables under section 751(c) areconsidered separate ordinary income as-sets for purposes of allocating basis ad-justments under section 755.

f. Identification of Publicly TradedPartnership Units

The proposed regulations provide thata selling partner may use the actual hold-ing period of the portion of a partnershipinterest sold if the partnership is a “pub-licly traded partnership” (as definedunder section 7704(b)), the partnershipinterest is divided into identifiable unitswith ascertainable holding periods, andthe selling partner can identify the por-tion of the interest transferred. Commen-tators suggested that it may be appropri-ate to provide that a partner must beconsistent in electing, for holding periodpurposes, to identify units of a publiclytraded partnership that are sold or ex-changed in order to avoid distortion inthe total long-term and short-term capital

October 10, 2000 326 2000–41 I.R.B.

gain recognized. This suggestion isadopted in the final regulations.

g. Conversion from General Partnershipto Limited Partnership

A commentator requested clarificationthat a partner’s holding period in its part-nership interest carries over when a part-nership converts from a general partner-ship to a limited partnership, as describedin Rev. Rul. 84-52 (1984–1 C.B. 157).The ruling concludes that, pursuant tosection 1223(1), there will be no changeto the holding period of any partner’s in-terest in the partnership as a result of sucha conversion. The final regulations do notchange the result set forth in Rev. Rul. 84-52.

h. Other Miscellaneous Issues

The proposed regulations contain an ex-ample which, consistent with Rev. Rul.84–53, states that a partner has a singlebasis in its partnership interest. Certaincommentators suggested that the principlethat a partner has a single basis in its part-nership interest should be set forth in regu-lations, rather than simply relying on Rev.Rul. 84–53. The rules set forth in theseregulations address only holding periodand character issues. In illustrating theoperation of certain of these rules, the ex-ample accurately reflects current law.Treasury and the IRS believe that the in-clusion of a separate rule providing that apartner has a single basis in its partnershipinterest is unnecessary and is beyond thescope of these regulations.

Finally, it was suggested that the finalregulations cross-reference section 83(f),which provides that in determining theholding period of property to which sec-tion 83(a) applies, only the holding periodduring which rights are transferable or arenot subject to a substantial risk of forfei-ture shall be included. Treasury and theIRS currently are studying the extent towhich section 83(a) applies to the issuanceof certain partnership interests (i.e., a prof-its interest in a partnership) in exchangefor services. Section 83(f) is relevant tothe extent that section 83(a) applies withrespect to a partnership interest. However,in order to avoid any implication that sec-tion 83(a) applies to all partnership inter-ests issued in exchange for services, across reference to section 83(f) has notbeen included in the final regulations.

Special Analyses

It has been determined that this Trea-sury decision is not a significant regula-tory action as defined in Executive Order12866. Therefore, a regulatory assess-ment is not required. It also has been de-termined that section 553(b) of the Ad-ministrative Procedure Act (5 U.S.C.chapter 5) does not apply to these regula-tions. It is hereby certified that the collec-tion of information in these regulationswill not have a significant impact on asubstantial number of small businesses.This certification is based upon the factthat the economic burden imposed on tax-payers by the collection of informationand recordkeeping requirements of theseregulations is insignificant. For example,the estimated average annual burden perrespondent is 10 minutes. Therefore, aRegulatory Flexibility Analysis is not re-quired under the Regulatory FlexibilityAct (5 U.S.C. chapter 6). Pursuant to sec-tion 7805(f) of the Internal RevenueCode, the notice of proposed rulemakingpreceding these regulations was submit-ted to the Chief Counsel for Advocacy ofthe Small Business Administration forcomment on its impact on small business.

Drafting Information

The principal authors of these regula-tions are Jeanne M. Sullivan and David J.Sotos of the Associate Chief Counsel(Passthroughs and Special Industries).However, other personnel from Treasuryand the IRS participated in their develop-ment.

* * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR parts 1 and 602are amended as follows:

PART 1— INCOME TAXES

Paragraph 1. The authority citation forpart 1 is amended by adding an entry innumerical order to read in part as fol-lows:

Authority: 26 U.S.C. 7805 * * *Section 1.1(h)–1 is also issued under

26 U.S.C. 1(h); * * *Par. 2. Section 1.1(h)–1 is added to

read as follows:

§1.1(h)–1 Capital gains look-through

rule for sales or exchanges of interests ina partnership, S corporation, or trust.

(a) In general. When an interest in apartnership held for more than one year issold or exchanged, the transferor may rec-ognize ordinary income (e.g., under sec-tion 751(a)), collectibles gain, section1250 capital gain, and residual long-termcapital gain or loss. When stock in an Scorporation held for more than one year issold or exchanged, the transferor may rec-ognize ordinary income (e.g., under sec-tions 304, 306, 341, 1254), collectiblesgain, and residual long-term capital gainor loss. When an interest in a trust heldfor more than one year is sold or ex-changed, a transferor who is not treated asthe owner of the portion of the trust attrib-utable to the interest sold or exchanged(sections 673 through 679) (a non-grantortransferor) may recognize collectiblesgain and residual long-term capital gainor loss.

(b) Look-through capital gain—(1) Ingeneral. Look-through capital gain is theshare of collectibles gain allocable to aninterest in a partnership, S corporation, ortrust, plus the share of section 1250 capi-tal gain allocable to an interest in a part-nership, determined under paragraphs(b)(2) and (3) of this section.

(2) Collectibles gain—(i) Definition.For purposes of this section, collectiblesgain shall be treated as gain from the saleor exchange of a collectible (as defined insection 408(m) without regard to section408(m)(3)) that is a capital asset held formore than 1 year.

(ii) Share of collectibles gain allocableto an interest in a partnership, S corpora-tion, or a trust. When an interest in apartnership, S corporation, or trust heldfor more than one year is sold or ex-changed in a transaction in which all real-ized gain is recognized, the transferorshall recognize as collectibles gain theamount of net gain (but not net loss) thatwould be allocated to that partner (takinginto account any remedial allocationunder §1.704–3(d)), shareholder, or bene-ficiary (to the extent attributable to theportion of the partnership interest, S cor-poration stock, or trust interest transferredthat was held for more than one year) ifthe partnership, S corporation, or trusttransferred all of its collectibles for cashequal to the fair market value of the assetsin a fully taxable transaction immediately

2000–41 I.R.B. 327 October 10, 2000

before the transfer of the interest in thepartnership, S corporation, or trust. If lessthan all of the realized gain is recognizedupon the sale or exchange of an interest ina partnership, S corporation, or trust, thesame methodology shall apply to deter-mine the collectibles gain recognized bythe transferor, except that the partnership,S corporation, or trust shall be treated astransferring only a proportionate amountof each of its collectibles determined as afraction that is the amount of gain recog-nized in the sale or exchange over theamount of gain realized in the sale or ex-change. With respect to the transfer of aninterest in a trust, this paragraph (b)(2)applies only to transfers by non-grantortransferors (as defined in paragraph (a) ofthis section). This paragraph (b)(2) doesnot apply to a transaction that is treated,for Federal income tax purposes, as a re-demption of an interest in a partnership, Scorporation, or trust.

(3) Section 1250 capital gain—(i) Defi-nition. For purposes of this section, sec-tion 1250 capital gainmeans the capitalgain (not otherwise treated as ordinary in-come) that would be treated as ordinaryincome if section 1250(b)(1) included alldepreciation and the applicable percent-age under section 1250(a) were 100 per-cent.

(ii) Share of section 1250 capital gainallocable to interest in partnership.When an interest in a partnership held formore than one year is sold or exchangedin a transaction in which all realized gainis recognized, there shall be taken into ac-count under section 1(h)(7)(A)(i) in deter-mining the partner’s unrecaptured section1250 gain the amount of section 1250capital gain that would be allocated (tak-ing into account any remedial allocationunder §1.704–3(d)) to that partner (to the

extent attributable to the portion of thepartnership interest transferred that washeld for more than one year) if the part-nership transferred all of its section 1250property in a fully taxable transaction forcash equal to the fair market value of theassets immediately before the transfer ofthe interest in the partnership. If less thanall of the realized gain is recognized uponthe sale or exchange of an interest in apartnership, the same methodology shallapply to determine the section 1250 capi-tal gain recognized by the transferor, ex-cept that the partnership shall be treatedas transferring only a proportionateamount of each section 1250 property de-termined as a fraction that is the amountof gain recognized in the sale or exchangeover the amount of gain realized in thesale or exchange. This paragraph (b)(3)does not apply to a transaction that istreated, for Federal income tax purposes,as a redemption of a partnership interest.

(iii) Limitation with respect to net sec-tion 1231 gain. In determining a trans-feror partner’s net section 1231 gain (asdefined in section 1231(c)(3)) for pur-poses of section 1(h)(7)(B), the transferorpartner’s allocable share of section 1250capital gain in partnership property shallnot be treated as section 1231 gain, re-gardless of whether the partnership prop-erty is used in the trade or business (as de-fined in section 1231(b)).

(c) Residual long-term capital gain orloss. The amount of residual long-termcapital gain or loss recognized by a part-ner, shareholder of an S corporation, orbeneficiary of a trust on account of thesale or exchange of an interest in a part-nership, S corporation, or trust shall equalthe amount of long-term capital gain orloss that the partner would recognizeunder section 741, that the shareholder

would recognize upon the sale or ex-change of stock of an S corporation, orthat the beneficiary would recognize uponthe sale or exchange of an interest in atrust (pre-look-through long-term capitalgain or loss) minus the amount of look-through capital gain determined underparagraph (b) of this section.

(d) Special rule for tiered entities.Indetermining whether a partnership, S cor-poration, or trust has gain from col-lectibles, such partnership, S corporation,or trust shall be treated as owning its pro-portionate share of the collectibles of anypartnership, S corporation, or trust inwhich it owns an interest either directly orindirectly through a chain of such entities.In determining whether a partnership hassection 1250 capital gain, such partner-ship shall be treated as owning its propor-tionate share of the section 1250 propertyof any partnership in which it owns an in-terest, either directly or indirectly througha chain of partnerships.

(e) Notification requirements. Report-ing rules similar to those that apply to thepartners and the partnership under section751(a) shall apply in the case of sales orexchanges of interests in a partnership, Scorporation, or trust that cause holders ofsuch interests to recognize collectibles gainand in the case of sales or exchanges of in-terests in a partnership that cause holdersof such interests to recognize section 1250capital gain. See §1.751–1(a)(3).

(f) Examples.The following examplesillustrate the requirements of this section:

Example 1. Collectibles gain. (i) A and B areequal partners in a personal service partnership(PRS). B transfers B’s interest in PRSto T for$15,000 when PRS’s balance sheet (reflecting a cashreceipts and disbursements method of accounting) isas follows:

October 10, 2000 328 2000–41 I.R.B.

ASSETS

Adjusted MarketBasis Value

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 3,000 $3,000Loans Owed to Partnership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,000 10,000

Collectibles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,000 3,000Other Capital Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,000 2,000

Capital Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,000 5,000Unrealized Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0 14,000

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $20,000 $32,000

LIABILITIES AND CAPITAL

Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2,000 $ 2,000Capital:

A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,000 15,000B . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9,000 15,000Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $20,000 $32,000

2000–41 I.R.B. 329 October 10, 2000

(ii) At the time of the transfer, B has held the in-terest in PRSfor more than one year, and B’s basisfor the partnership interest is $10,000 ($9,000 plus$1,000, B’s share of partnership liabilities). None ofthe property owned by PRSis section 704(c) prop-erty. The total amount realized by B is $16,000,consisting of the cash received, $15,000, plus$1,000, B’s share of the partnership liabilities as-sumed by T. See section 752. B’s undivided one-half interest in PRSincludes a one-half interest inthe partnership’s unrealized receivables and a one-half interest in the partnership’s collectibles.

(iii) If PRSwere to sell all of its section 751 prop-erty in a fully taxable transaction for cash equal tothe fair market value of the assets immediately priorto the transfer of B’s partnership interest to T, Bwould be allocated $7,000 of ordinary income fromthe sale of PRS’s unrealized receivables. Therefore,B will recognize $7,000 of ordinary income with re-spect to the unrealized receivables. The differencebetween the amount of capital gain or loss that thepartner would realize in the absence of section 751($6,000) and the amount of ordinary income or lossdetermined under §1.751–1(a)(2) ($7,000) is thepartner’s capital gain or loss on the sale of the part-nership interest under section 741. In this case, thetransferor has a $1,000 pre-look-through long-termcapital loss.

(iv) If PRSwere to sell all of its collectibles in afully taxable transaction for cash equal to the fairmarket value of the assets immediately prior to thetransfer of B’s partnership interest to T, B would beallocated $1,000 of gain from the sale of the col-lectibles. Therefore, B will recognize $1,000 of col-lectibles gain on account of the collectibles held byPRS.

(v) The difference between the transferor’s pre-look-through long-term capital gain or loss (-$1,000)and the look-through capital gain determined underthis section ($1,000) is the transferor’s residual long-term capital gain or loss on the sale of the partner-ship interest. Under these facts, B will recognize a$2,000 residual long-term capital loss on account ofthe sale or exchange of the interest in PRS.

Example 2. Special allocations. Assume thesame facts as in Example 1, except that under thepartnership agreement, all gain from the sale of thecollectibles is specially allocated to B, and B trans-fers B’s interest to T for $16,000. All items of in-come, gain, loss, or deduction of PRS, other thanthe gain from the collectibles, are divided equallybetween A and B. Under these facts, B’s amount re-alized is $17,000, consisting of the cash received,$16,000, plus $1,000, B’s share of the partnershipliabilities assumed by T. See section 752. B willrecognize $7,000 of ordinary income with respectto the unrealized receivables (determined under§1.751–1(a)(2)). Accordingly, B’s pre-look-throughlong-term capital gain would be $0. If PRSwere tosell all of its collectibles in a fully taxable transac-tion for cash equal to the fair market value of the as-sets immediately prior to the transfer of B’s partner-ship interest to T, B would be allocated $2,000 ofgain from the sale of the collectibles. Therefore, Bwill recognize $2,000 of collectibles gain on ac-count of the collectibles held by PRS. B will recog-nize a $2,000 residual long-term capital loss on ac-count of the sale of B’s interest in PRS.

Example 3. Net collectibles loss ignored. As-sume the same facts as in Example 1, except that thecollectibles held by PRShave an adjusted basis of$3,000 and a fair market value of $1,000, and theother capital assets have an adjusted basis of $4,000and a fair market value of $4,000. (The total ad-justed basis and fair market value of the partner-ship’s capital assets are the same as in Example 1.)If PRSwere to sell all of its collectibles in a fullytaxable transaction for cash equal to the fair marketvalue of the assets immediately prior to the transferof B’s partnership interest to T, B would be allo-cated $1,000 of loss from the sale of the col-lectibles. Because none of the gain from the sale ofthe interest in PRSis attributable to unrealized ap-preciation in the value of collectibles held by PRS,the net loss in collectibles held by PRSis not recog-nized at the time B transfers the interest in PRS. Bwill recognize $7,000 of ordinary income (deter-mined under §1.751–1(a)(2)) and a $1,000 long-

term capital loss on account of the sale of B’s inter-est in PRS.

Example 4. Collectibles gain in an S corpora-tion. (i) A corporation (X) has always been an Scorporation and is owned by individuals A, B, andC. In 1996, X invested in antiques. Subsequent totheir purchase, the antiques appreciated in value by$300. A owns one-third of the shares of X stock andhas held that stock for more than one year. A’s ad-justed basis in the X stock is $100. If A were to sellall of A’s X stock to T for $150, A would realize $50of pre-look-through long-term capital gain.

(ii) If X were to sell its antiques in a fully taxabletransaction for cash equal to the fair market value ofthe assets immediately before the transfer to T, Awould be allocated $100 of gain on account of thesale. Therefore, A will recognize $100 of col-lectibles gain (look-through capital gain) on ac-count of the collectibles held by X.

(iii) The difference between the transferor’s pre-look-through long-term capital gain or loss ($50)and the look-through capital gain determined underthis section ($100) is the transferor’s residual long-term capital gain or loss on the sale of the S corpo-ration stock. Under these facts, A will recognize$100 of collectibles gain and a $50 residual long-term capital loss on account of the sale of A’s inter-est in X.

Example 5. Sale or exchange of partnership in-terest where part of the interest has a short-termholding period. (i) A, B, and C form an equal part-nership (PRS). In connection with the formation, Acontributes $5,000 in cash and a capital asset with afair market value of $5,000 and a basis of $2,000; Bcontributes $7,000 in cash and a collectible with afair market value of $3,000 and a basis of $3,000;and C contributes $10,000 in cash. At the time ofthe contribution, A had held the contributed prop-erty for two years. Six months later, when A’s basisin PRSis $7,000, A transfers A’s interest in PRStoT for $14,000 at a time when PRS’s balance sheet(reflecting a cash receipts and disbursementsmethod of accounting) is as follows:

ASSETS

Adjusted Market Basis Value

Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 22,000 $22,000Unrealized Receivables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0 6,000

Capital Asset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,000 5,000Collectible . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,000 9,000

Capital Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,000 14,000Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 27,000 $42,000

October 10, 2000 330 2000–41 I.R.B.

(ii) Although at the time of the transfer A hasnot held A’s interest in PRS for more than oneyear, 50 percent of the fair market value of A’s in-terest in PRSwas received in exchange for a capi-tal asset with a long-term holding period. There-fore, 50 percent of A’s interest in PRShas along-term holding period. See §1.1223–3(b)(1).

(iii) If PRS were to sell all of its section 751property in a fully taxable transaction immediatelybefore A’s transfer of the partnership interest, Awould be allocated $2,000 of ordinary income.Accordingly, A will recognize $2,000 ordinary in-come and $5,000 ($7,000 - $2,000) of capital gainon account of the transfer to T of A’s interest inPRS. Fifty percent ($2,500) of that gain is long-term capital gain and 50 percent ($2,500) is short-term capital gain. See §1.1223–3(c)(1).

(iv) If the collectible were sold or exchangedin a fully taxable transaction immediately beforeA’s transfer of the partnership interest, A would beallocated $2,000 of gain attributable to the col-lectible. The gain attributable to the collectiblethat is allocable to the portion of the transferred in-terest in PRSwith a long-term holding period is$1,000 (50 percent of $2,000). Accordingly, Awill recognize $1,000 of collectibles gain on ac-count of the transfer of A’s interest in PRS.

(v) The difference between the amount of pre-look-through long-term capital gain or loss($2,500) and the look-through capital gain($1,000) is the amount of residual long-term capi-tal gain or loss that A will recognize on account ofthe transfer of A’s interest in PRS. Under thesefacts, A will recognize a residual long-term capitalgain of $1,500 and a short-term capital gain of$2,500.

(g) Effective date. This section ap-plies to transfers of interests in partner-ships, S corporations, and trusts thatoccur on or after September 21, 2000.

Par. 3. Section 1.741–1 is amendedby adding paragraphs (e) and (f) to readas follows:

§1.741–1 Recognition and character ofgain or loss on sale or exchange.

* * * * *(e) For rules relating to the capital

gain or loss recognized when a partnersells or exchanges an interest in a part-nership that holds appreciated col-lectibles or section 1250 property withsection 1250 capital gain, see §1.1(h)–1. This paragraph (e) applies totransfers of interests in partnerships thatoccur on or after September 21, 2000.

(f) For rules relating to dividing theholding period of an interest in a part-nership, see §1.1223–3. This paragraph(f) applies to transfers of partnership in-terests and distributions of propertyfrom a partnership that occur on or afterSeptember 21, 2000.

Par. 4. Section 1.1223–3 is added

under the undesignated center heading“General Rules for Determining CapitalGains and Losses” to read as follows:

§1.1223–3 Rules relating to the holdingperiods of partnership interests.

(a) In general. A partner shall nothave a divided holding period in an in-terest in a partnership unless—

(1) The partner acquired portions ofan interest at different times; or

(2) The partner acquired portions ofthe partnership interest in exchange forproperty transferred at the same time butresulting in different holding periods(e.g., section 1223).

(b) Accounting for holding periods ofan interest in a partnership—(1) Gen-eral rule. The portion of a partnershipinterest to which a holding period relatesshall be determined by reference to afraction, the numerator of which is thefair market value of the portion of thepartnership interest received in thetransaction to which the holding periodrelates, and the denominator of which isthe fair market value of the entire part-nership interest (determined immedi-ately after the transaction).

(2) Special rule. For purposes of ap-plying paragraph (b)(1) of this section todetermine the holding period of a part-nership interest (or portion thereof) thatis sold or exchanged (or with respect towhich gain or loss is recognized upon adistribution under section 731), if a part-ner makes one or more contributions ofcash to the partnership and receives oneor more distributions of cash from thepartnership during the one-year periodending on the date of the sale or ex-change (or distribution with respect towhich gain or loss is recognized undersection 731), the partner may reduce thecash contributions made during the yearby cash distributions received on a last-in-first-out basis, treating all cash distri-butions as if they were received immedi-ately before the sale or exchange (or atthe time of the distribution with respectto which gain or loss is recognizedunder section 731).

(3) Deemed contributions and distrib-utions. For purposes of paragraphs(b)(1) and (2) of this section, deemedcontributions of cash under section752(a) and deemed distributions of cashunder section 752(b) shall be disre-

garded to the same extent that suchamounts are disregarded under§1.704–1(b)(2)(iv)(c).

(4) Adjustment with respect to con-tributed section 751 assets. For purposesof applying paragraph (b)(1) of this sec-tion to determine the holding period of apartnership interest (or portion thereof)that is sold or exchanged, if a partner re-ceives a portion of the partnership interestin exchange for property described in sec-tion 751(c) or (d) (section 751 assets)within the one-year period ending on thedate of the sale or exchange of all or aportion of the partner’s interest in thepartnership, and the partner recognizesordinary income or loss on account ofsuch a section 751 asset in a fully taxabletransaction (either as a result of the sale ofall or part of the partner’s interest in thepartnership or the sale by the partnershipof the section 751 asset), the contributionof the section 751 asset during the one-year period shall be disregarded. How-ever, if, in the absence of this paragraph, apartner would not be treated as havingheld any portion of the interest for morethan one year (e.g., because the partner’sonly contributions to the partnership arecontributions of section 751 assets or sec-tion 751 assets and cash within the priorone-year period), this adjustment is notavailable.

(5) Exception. The Commissioner mayprescribe by guidance published in the In-ternal Revenue Bulletin (see §601.-601(d)(2) of this chapter) a rule disregard-ing certain cash contributions (includingcontributions of ade minimisamount ofcash) in applying paragraph (b)(1) of thissection to determine the holding period ofa partnership interest (or portion thereof)that is sold or exchanged.

(c) Sale or exchange of all or a portionof an interest in a partnership—(1) Saleor exchange of entire interest in a part-nership. If a partner sells or exchangesthe partner’s entire interest in a partner-ship, any capital gain or loss recognizedshall be divided between long-term andshort-term capital gain or loss in the sameproportions as the holding period of theinterest in the partnership is divided be-tween the portion of the interest held formore than one year and the portion of theinterest held for one year or less.

(2) Sale or exchange of a portion of aninterest in a partnership—(i) Certain

publicly traded partnerships. A sellingpartner in a publicly traded partnership(as defined under section 7704(b)) mayuse the actual holding period of the por-tion of a partnership interest transferredif—

(A) The ownership interest is dividedinto identifiable units with ascertainableholding periods;

(B) The selling partner can identify theportion of the partnership interest trans-ferred; and

(C) The selling partner elects to use theidentification method for all sales or ex-changes of interests in the partnershipafter September 21, 2000. The sellingpartner makes the election referred to inthis paragraph (c)(2)(i)(C) by using theactual holding period of the portion of thepartner’s interest in the partnership firsttransferred after September 21, 2000, inreporting the transaction for federal in-come tax purposes.

(ii) Other partnerships. If a partnerhas a divided holding period in a partner-ship interest, and paragraph (c)(2)(i) ofthis section does not apply, then the hold-ing period of the transferred interest shallbe divided between long-term and short-term capital gain or loss in the same pro-portions as the long-term and short-termcapital gain or loss that the transferorpartner would realize if the entire interestin the partnership were transferred in afully taxable transaction immediately be-fore the actual transfer.

(d) Distributions—(1) In general. Ex-cept as provided in paragraph (b)(2) ofthis section, a partner’s holding period ina partnership interest is not affected bydistributions from the partnership.

(2) Character of capital gain or lossrecognized as a result of a distributionfrom a partnership. If a partner is re-quired to recognize capital gain or loss asa result of a distribution from a partner-ship, then the capital gain or loss recog-nized shall be divided between long-termand short-term capital gain or loss in thesame proportions as the long-term andshort-term capital gain or loss that thedistributee partner would realize if suchpartner’s entire interest in the partnershipwere transferred in a fully taxable trans-action immediately before the distribu-tion.

(e) Section 751(c) assets. For purposesof this section, properties and potential

gain treated as unrealized receivablesunder section 751(c) shall be treated asseparate assets that are not capital assetsas defined in section 1221 or property de-scribed in section 1231.

(f) Examples. The provisions of thissection are illustrated by the followingexamples:

Example 1. Division of holding period—contri-bution of money and a capital asset. (i) A con-tributes $5,000 of cash and a nondepreciable capitalasset A has held for two years to a partnership (PRS)for a 50 percent interest in PRS. A’s basis in thecapital asset is $5,000, and the fair market value ofthe asset is $10,000. After the exchange, A’s basisin A’s interest in PRSis $10,000, and the fair mar-ket value of the interest is $15,000. A received one-third of the interest in PRSfor a cash payment of$5,000 ($5,000/$15,000). Therefore, A’s holdingperiod in one-third of the interest received (attribut-able to the contribution of money to the partnership)begins on the day after the contribution. A receivedtwo-thirds of the interest in PRSin exchange for thecapital asset ($10,000/$15,000). Accordingly, pur-suant to section 1223(1), A has a two-year holdingperiod in two-thirds of the interest received in PRS.

(ii) Six months later, when A’s basis in PRSis$12,000 (due to a $2,000 allocation of partnershipincome to A), A sells the interest in PRS for$17,000. Assuming PRSholds no inventory or un-realized receivables (as defined under section751(c)) and no collectibles or section 1250 prop-erty, A will realize $5,000 of capital gain. As deter-mined above, one-third of A’s interest in PRShas aholding period of one year or less, and two- thirdsof A’s interest in PRShas a holding period equal totwo years and six months. Therefore, one-third ofthe capital gain will be short-term capital gain, andtwo-thirds of the capital gain will be long-term cap-ital gain.

Example 2. Division of holding period—contri-bution of section 751 asset and a capital asset. Acontributes inventory with a basis of $2,000 and afair market value of $6,000 and a capital assetwhich A has held for more than one year with abasis of $4,000 and a fair market value of $6,000,and B contributes cash of $12,000 to form a partner-ship (AB). As a result of the contribution, one-halfof A’s interest in AB is treated as having been heldfor more than one year under section 1223(1). Sixmonths later, A transfers one-half of A’s interest inAB to C for $6,000, realizing a gain of $3,000. IfAB were to sell all of its section 751 property in afully taxable transaction immediately before A’stransfer of the partnership interest, A would be allo-cated $4,000 of ordinary income on account of theinventory. Accordingly, A will recognize $2,000 ofordinary income and $1,000 of capital gain ($3,000- $2,000) on account of the transfer to C. BecauseA recognizes ordinary income on account of the in-ventory that was contributed to AB within the oneyear period ending on the date of the sale, the in-ventory will be disregarded in determining the hold-ing period of A’s interest in AB. All of the capitalgain will be long-term.

Example 3. Netting of cash contributions anddistributions. (i) On January 1, 2000, A holds a 50percent interest in the capital and profits of a part-

nership (PS). The value of A’s PS interest is $900,and A’s holding period in the entire interest is long-term. On January 2, 2000, when the value of A’s PSinterest is still $900, A contributes $100 to PS. OnJune 1, 2000, A receives a distribution of $40 cashfrom the partnership. On September 1, 2000, whenthe value of A’s interest in PS is $1,350, A con-tributes an additional $230 cash to PS, and on Octo-ber 1, 2000, A receives another $40 cash distribu-tion from PS. A sells A’s entire partnership intereston November 1, 2000, for $1,600. A’s adjustedbasis in the PS interest at the time of the sale is$1,000.

(ii) For purposes of netting cash contributionsand distributions in determining the holding periodof A’s interest in PS, A is treated as having receiveda distribution of $80 on November 1, 2000. Apply-ing that distribution on a last-in-first-out basis to re-duce prior contributions during the year, the contri-bution made on September 1, 2000, is reduced to$150 ($230 - $80). The holding period then is de-termined as follows: Immediately after the contri-bution of $100 on January 2, 2000, A’s holding pe-riod in A’s PS interest is 90 percent long-term($900/($900 + $100)) and 10 percent short-term($100/($900 + $100)). The contribution of $150 onSeptember 1, 2000, causes 10 percent of A’s part-nership interest ($150/($1,350 + $150)) to have ashort-term holding period. Accordingly, immedi-ately after the contribution on September 1, 2000,A’s holding period in A’s PS interest is 81 percentlong-term (.90 x .90) and 19 percent short-term((.10 x .90) + .10). Accordingly, $486 ($600 x .81)of the gain from A’s sale of the PS interest is long-term capital gain, and $114 ($600 x .19) is short-term capital gain.

Example 4. Division of holding period whencapital account is increased by contribution. A, B,C, and D are equal partners in a partnership (PRS),and the fair market value of a 25 percent interest inPRSis $100. A, B, C, and D each contribute an ad-ditional $100 to partnership capital, thereby in-creasing the fair market value of each partner’s in-terest to $200. As a result of the contribution, eachpartner has a new holding period in the portion ofthe partner’s interest in PRSthat is attributable tothe contribution. That portion equals 50 percent($100/$200) of each partner’s interest in PRS.

Example 5. Sale or exchange of a portion of aninterest in a partnership. (i) A, B, and C form anequal partnership (PRS). In connection with theformation, A contributes $5,000 in cash and a capi-tal asset (capital asset 1) with a fair market value of$5,000 and a basis of $2,000; B contributes $7,000in cash and a capital asset (capital asset 2) with afair market value of $3,000 and a basis of $3,000;and C contributes $10,000 in cash. At the time ofthe contribution, A had held the contributed prop-erty for two years. Six months later, when A’s basisin PRSis $7,000, A transfers one-half of A’s interestin PRSto T for $7,000 at a time when PRS’s bal-ance sheet (reflecting a cash receipts and disburse-ments method of accounting) is as follows:

2000–41 I.R.B. 331 October 10, 2000

October 10, 2000 332 2000–41 I.R.B.

(ii) Although at the time of the transfer A has notheld A’s interest in PRSfor more than one year, 50percent of the fair market value of A’s interest inPRSwas received in exchange for a capital assetwith a long-term holding period. Therefore, 50 per-cent of A’s interest in PRShas a long-term holdingperiod.

(iii) If PRSwere to sell all of its section 751 prop-erty in a fully taxable transaction immediately be-fore A’s transfer of the partnership interest, A wouldbe allocated $2,000 of ordinary income. One-half ofthat amount ($1,000) is attributable to the portion ofA’s interest in PRStransferred to T. Accordingly, Awill recognize $1,000 ordinary income and $2,500($3,500 - $1,000) of capital gain on account of thetransfer to T of one-half of A’s interest in PRS. Fiftypercent ($1,250) of that gain is long-term capitalgain and 50 percent ($1,250) is short-term capitalgain.

Example 6. Sale of units of interests in a partner-ship. A publicly traded partnership (PRS) has own-ership interests that are segregated into identifiableunits of interest. A owns 10 limited partnership unitsin PRSfor which A paid $10,000 on January 1,1999. On August 1, 2000, A purchases five addi-tional units for $10,000. At the time of purchase, thefair market value of each unit has increased to$2,000. A’s holding period for one-third($10,000/$30,000) of the interest in PRSbegins onthe day after the purchase of the five additionalunits. Less than one year later, A sells five units ofownership in PRSfor $11,000. At the time, A’sbasis in the 15 units of PRSis $20,000, and A’s capi-tal gain on the sale of 5 units is $4,333 (amount real-ized of $11,000 - one-third of the adjusted basis or$6,667). For purposes of determining the holdingperiod, A can designate the specific units of PRSsold. If A properly identifies the five units sold asfive of the ten units for which A has a long-termholding period and elects to use the identification

method for all subsequent sales or exchanges of in-terests in the partnership by using the actual holdingperiod in reporting the transaction on A’s federal in-come tax return, the capital gain realized will belong-term capital gain.

Example 7. Disproportionate distribution. In1997, A and B each contribute cash of $50,000 toform and become equal partners in a partnership(PRS). More than one year later, A receives a distri-bution worth $22,000 from PRS, which reduces A’sinterest in PRSto 36 percent. After the distribution,B owns 64 percent of PRS. The holding periods of Aand B in their interests in PRSare not affected by thedistribution.

Example 8. Gain or loss as a result of a distribu-tion—(i) On January 1, 1996, A contributes prop-erty with a basis of $10 and a fair market value of$10,000 in exchange for an interest in a partnership(ABC). On September 30, 2000, when A’s interest inABC is worth $12,000 (and the basis of A’s partner-ship interest is still $10), A contributes $12,000 cashin exchange for an additional interest in ABC. A isallocated a loss equal to $10,000 by ABCfor the tax-able year ending December 31, 2000, thereby reduc-ing the basis of A’s partnership interest to $2,010.On February 1, 2001, ABC makes a cash distribu-tion to A of $10,000. ABCholds no inventory or un-realized receivables. (Assume that A is allocated nogain or loss for the taxable year ending December31, 2001, so that the basis of A’s partnership interestdoes not increase or decrease as a result of such allo-cations.)

(ii) The netting rule contained in paragraph (b)(2)of this section provides that, in determining theholding period of A’s interest in ABC, the cash con-tribution made on September 30, 2000, must be re-duced by the distribution made on February 1, 2001.Accordingly, for purposes of determining the hold-ing period of A’s interest in ABC, A is treated as hav-ing made a cash contribution of $2,000 ($12,000 -

$10,000) to ABCon September 30, 2000. A’s hold-ing period in one-seventh of A’s interest in ABC($2,000 cash contributed over the $14,000 value ofthe entire interest (determined as if only $2,000 werecontributed rather than $12,000)) begins on the dayafter the cash contribution. A recognizes $7,990 ofcapital gain as a result of the distribution. See sec-tion 731(a)(1). One-seventh of the capital gain rec-ognized as a result of the distribution is short-termcapital gain, and six-sevenths of the capital gain islong-term capital gain. After the distribution, A’sbasis in the interest in PRSis $0, and the holding pe-riod for the interest in PRScontinues to be dividedin the same proportions as before the distribution.

(g) Effective date. This section appliesto transfers of partnership interests anddistributions of property from a partner-ship that occur on or after September 21,2000.

PART 602—OMB CONTROLNUMBERS UNDER THEPAPERWORK REDUCTION ACT

Par. 5. The authority citation for part602 continues to read as follows:

Authority: 26 U.S.C. 7805.Par. 6. In § 602.101, paragraph (b) is

amended by adding an entry in numericalorder to the table to read as follows:

§602.101 OMB Control numbers.

* * * * *(b) * * *

ASSETS

Adjusted Market Basis Value