internal controls and financial reporting quality in privitized companies in uganda: a case of...

TRANSCRIPT

INTERNAL CONTROLS AND FINANCIAL REPORTING QUALITY IN PRIVITIZED

COMPANIES IN UGANDA:

A CASE OF CENTRAL PURCHASING COMPANY LIMITED (CPCL)

ABAS JASPER OLWOL

DBS, Bsc Accts/Finance (Hons)

11/2/501/E/428

SUPERVISOR: Dr Henry Buwule Musoke

PhD, Msc, BBA (Hons)

A DISSERTATION SUBMITTED IN PARTIAL FULFILLMENT OF THE

REQUIREMENTS FOR THE AWARD OF MASTER OF BUSINESS

ADMINISTRATION DEGREE OF NDEJJE UNIVERSITY

SEPTEMBER, 2013

i

DECLARATION

I Abas Jasper Olwol do hereby declare that this dissertation is my own original work and

has not been presented to any institution/University for academic award or otherwise by

any person.

Signature ………………………… Date………………….

Abas Jasper Olwol

Reg No: 11/2/501/E/428

ii

APPROVAL

This dissertation has been submitted for examination with my approval as a University Supervisor

Signature……………………………… Date…………………………………

DR. Henry Buwule Musoke

iii

DEDICATION

I dedicate this research dissertation to the almighty God, my late Father Benjamin Okwenye, my Mother

Ms Leah Okwenye, my Wife Ms Deborah Olwol and Children (Glad, Gloria and Gabriel), brothers and

sisters, my friend Opio Amed Sunday and all those whose desire has seen me where I am now. May God

bless you all

iv

ACKNOWLEDGEMENT

Most of all I thank the Almighty God for being a source of inspiration and for providing me

wisdom and the Grace to complete this research. I am greatly indebted to my Supervisor, Dr. Henry

Buwule Musoke for his guidance, encouragement and patience even when I seemed not to

understand. I also extend my profound appreciation and thanks to family and most especially my

parents the late Benjamin Okwenye and Ms. Leah Okwenye, my wife Deborah and Children,

brothers and sisters Robinson, Dianah, Janet, Night and Gift for having been understanding,

tolerant, supportive for along time. My gratitude also goes to my colleagues especially Opio, Filder,

Nicho, Wanyana, Harriet, Olive, Maureen, Kamukama, Cissy and Linda who assisted and offered

me the academic company I needed during the MBA program, my pastor Moses Kakembo together

with the family of Luzira Healing Springs Church. Special thanks go to the Central Purchasing

Company management for allowing me carry out this research; I also thank all staff especially those

who participated in this research by responding to questionnaires. For all the above various groups

and individuals and many others that I may not have mentioned, in this acknowledgement, I owe

this achievement to you all and I will always remain indebted to you.

v

TABLE OF CONTENTS

DECLARATION………………………………………………………...…..…...Error!

Bookmark not defined.

APPROVAL……………………………………………………………….....…..Error!

Bookmark not defined.

DEDICATION………………………………………………………………...…iii

ACKOWLEDGEMENT…………………………………………………… .….iv

TABLE OF CONTENT……………………………………………………..…..v

LIST OF TABLES…………………..………………………………………....viii

LIST OF FIGURES……………………………………………………………..ix

ABBREVIATIONS AND ACRYOMNS..... …………………………………….x

ABSTRACT........................................................................................................... xi

1.0 INTRODUCTION .......................................................................................... 1

1.1 Background to the study ................................................................................. 1

1.2 Statement of the problem................................................................................ 6

1.3 Objectives of the study...................................................................................... 7

1.3.1 General objective ........................................................................................... 7

1.3.2 Specific objectives ......................................................................................... 7

1.4 Research Questions ......................................................................................... 7

1.4.1 Hypothesis.................................................................................................... 7

1.5 Significance of the study................................................................................. 7

1.6 Conceptual frame work..................................................................................... 8

1.7 Scope of the Study ............................................................................................ 9

1.7.1 Geographical Scope ....................................................................................... 9

1.7.2 Content Scope ................................................................................................ 9

1.7.3 Time scope ..................................................................................................... 9

1.8 Definition of Key Concepts used in this Study................................................ 9

1.9 Organization of the study................................................................................ 11

CHAPTER TWO…………………...…………………………..………………12

LITERATURE REVIEW .................................................................................. 13

2.1 The nature of Internal Controls....................................................................... 13

vi

2.1.1 Preventive Internal controls: ........................................................................ 14

2.2 Financial Reporting Quality.......................................................................... 26

2.3 Internal Controls and Financial Reporting Quality......................................... 33

2.4 Preventive Controls and Financial Reporting Quality .................................... 35

2.4.1 Detective Controls and Financial Reporting Quality................................... 36

2.5. Conclusion .................................................................................................... 38

CHAPTER THREE…………………………………………………………….38

METHODOLOGY ............................................................................................. 39

3.1 Research Design.............................................................................................. 39

3.2 Study Area and Population ............................................................................. 39

3.2.1 Study Area ................................................................................................... 39

3.2.2 Study Population.......................................................................................... 39

3.3 Sampling Design and Sample Size ................................................................. 40

3.3.1 Sampling Design.......................................................................................... 40

3.3.2 Sample Size.................................................................................................. 40

3.4 Data Collection Sources, Methods and Instruments ....................................... 40

3.4.1 Data Sources ................................................................................................ 40

3.4.2 Data collection methods............................................................................... 41

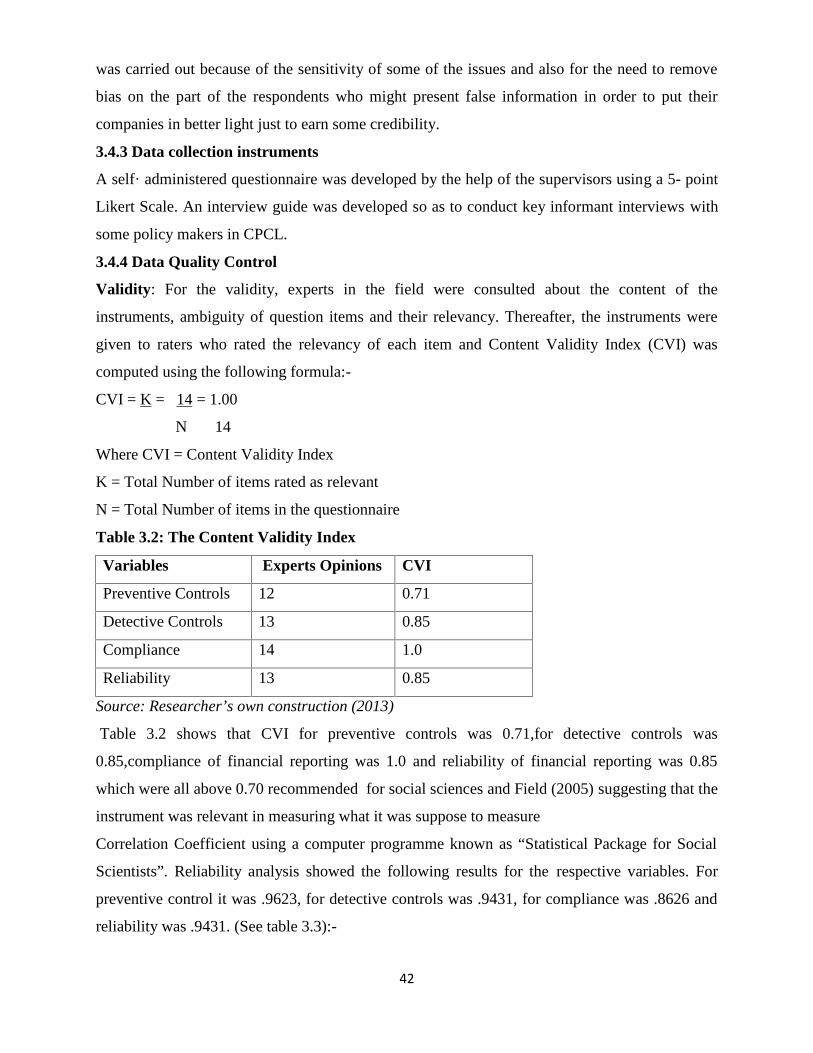

3.4.3 Data collection instruments.......................................................................... 42

3.5 Data Processing and Analysis ......................................................................... 43

3.5.1 Data Processing............................................................................................ 43

3.5.2 Data analysis ................................................................................................ 43

3.6 Ethical Considerations .................................................................................... 43

3.7 Limitation of the Study ................................................................................... 44

CHAPTER FOUR............................................................................................... 45

FINDINGS OF THE STUDY ............................................................................ 45

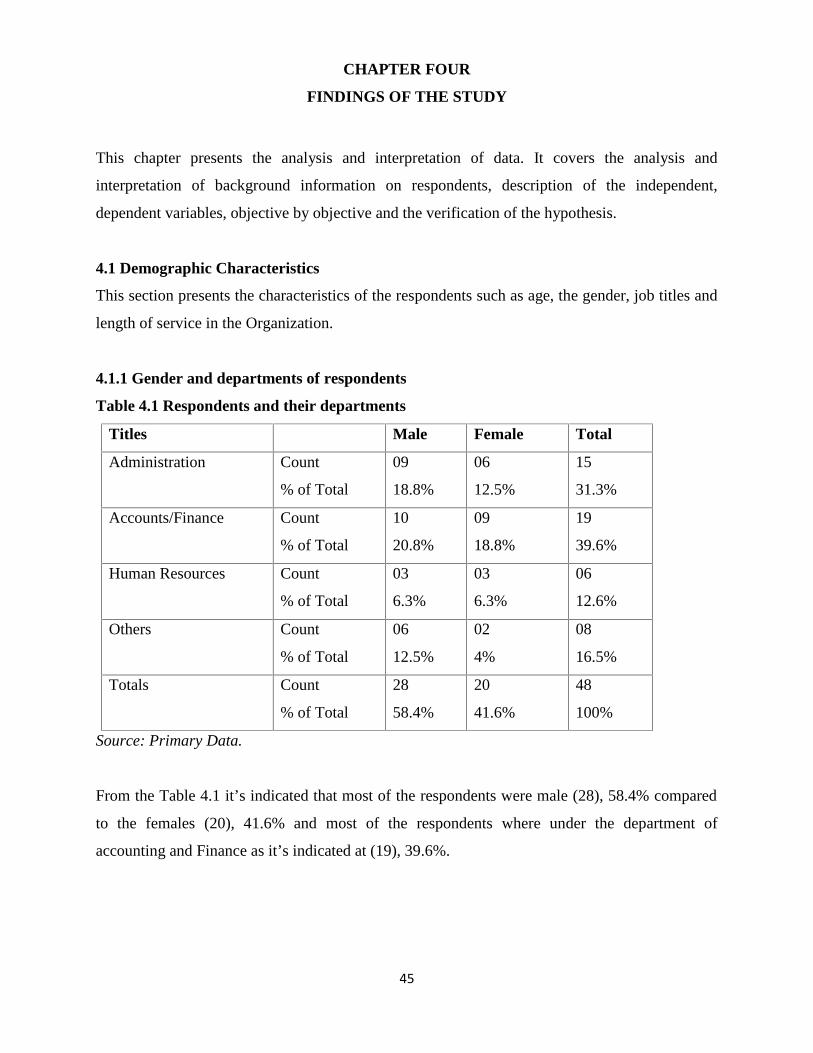

4.1 Demographic Characteristics .......................................................................... 45

4.1.1 Gender and departments of respondents ...................................................... 45

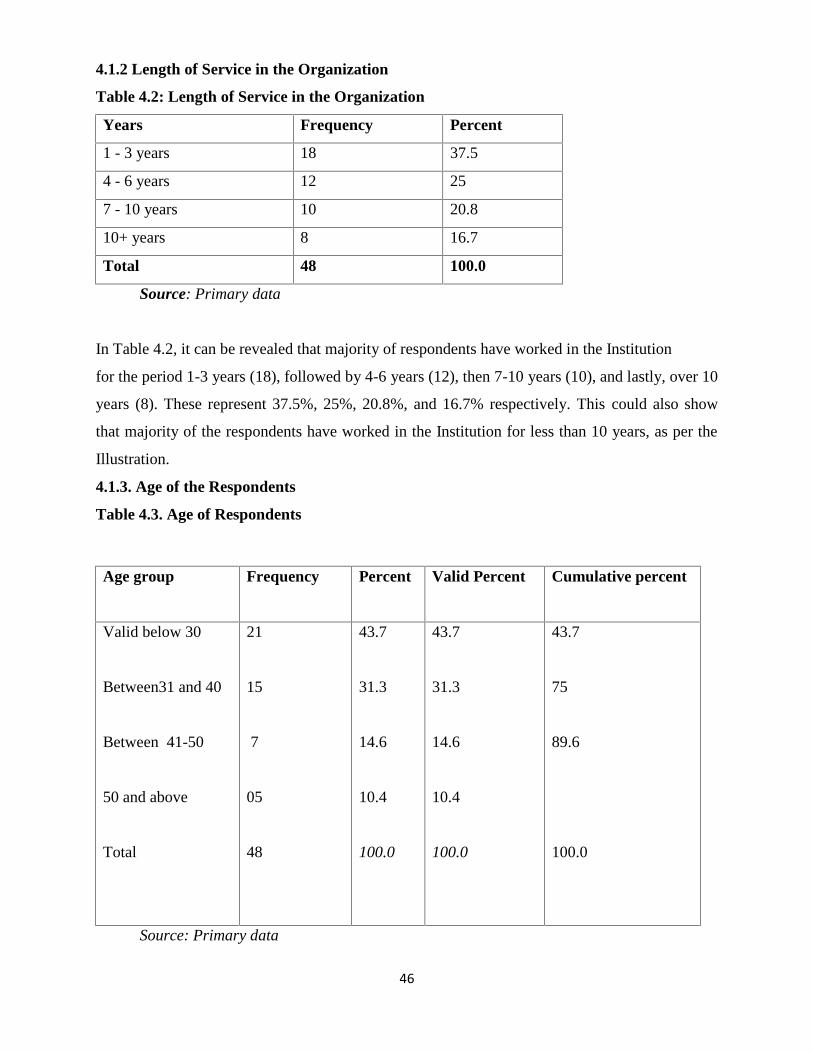

4.1.2 Length of Service in the Organization ......................................................... 46

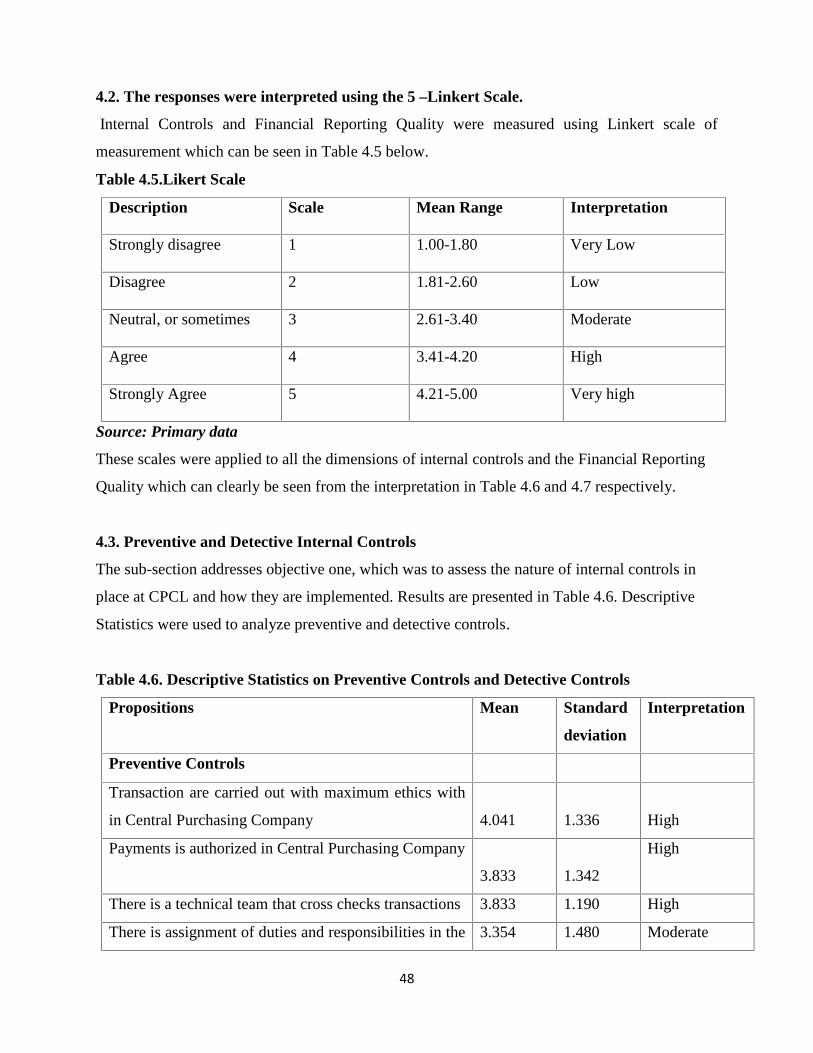

4.3. Preventive and Detective Internal Controls ................................................... 48

4.4. Financial Reporting Quality........................................................................... 52

4.5. Relationship Between Internal Controls and FRQ......................................... 55

vii

4.6. Regression Analysis....................................................................................... 58

4.6.1 Qualitative Data Presentation ...................................................................... 59

4.6.3 Internal controls ........................................................................................... 59

4.6.4. Effectiveness of internal controls................................................................ 60

4.6.5 Accountability procedure............................................................................. 61

4.6.6 Reporting procedure..................................................................................... 61

CHAPTER FIVE…………………...……………………………………....……61

5.0 SUMMARY,CONCLUSIONS AND RECOMMENDATIONS…………62

5.1 Summary of Major Findings ........................................................................... 62

5.1.1. Objective One. ............................................................................................ 62

5.1.2. Objective two .............................................................................................. 62

5.1.3. Objective Three........................................................................................... 63

5.2 Conclusions.................................................................................................... 63

5.3 General Recommendations ............................................................................. 64

5.3.1 Objective one ............................................................................................... 64

5.3.2 Objective Two.............................................................................................. 65

5.3.3 Objective Three............................................................................................ 65

5.5 Recommendation for further research ............................................................ 65

REFERENCES…………………………………………………………………..65

APPENDIX I SELF – ADMINISTERED QUESTIONNAIRE...................... 69

APPENDIX II INTERVIEW GUIDE:.............................................................. 73

APPENDIX III :( NATURE OF INTERNAL CONTROLS) ......................... 74

APPENDIX IV (NATURE OF FINANCIAL REPORTING QUALITY)..... 75

APPENDIX V KREJICE AND MORGAN (1970) .......................................... 76

APPENDIX VI INTRODUCTORY LETTER…………………………………..76

viii

LIST OF TABLES

Table 3.1: Sample Size ......................................................................................... 40

Table 3.2: The Content Validity Index ................................................................. 42

Table 3.3 Reliability Test Table............................................................................ 43

Table 4.1 Respondents and their departments ...................................................... 45

Table 4.2: Length of Service in the Organization................................................ 46

Table 4.3. Age of Respondents ............................................................................. 46

Table 4.4 Level of Education of the Respondents ................................................ 47

Table 4.5.Likert Scale ........................................................................................... 48

Table 4.6.showing Descriptive statistics controls................................................. 48

Table 4.7 showing Descriptive Statistic of FRQ…………………………...……51

Table 4.8 Relationship between Internal Controls and FRQ……….……....……54

Table 4.9 Relationship between preventive control and Compliance……...….…55

Table 4.9.1 Relationship between preventive control and Reliability……...……55

Table 4.9.2 Relationship between detective control and Compliance……...……56

Table 4.9.3 Relationship between detective control and Reliability...……...……56

Table 4.9.4 Model summary………………………………………....……...……57

Table 4.9.5 Analysis of Variables (ANOVA)……………………………………57

Table 4.9.6 Standardised Coefficient………...………...…………....……...……58

ix

LIST OF FIGURES

Figure 1.1: Conceptual frame work of ICs and FRQ in Privitised Companies in Uganda…...........7

x

ABBREVIATIONS AND ACRYNOMS

ACCA Association of Chartered Certified Accountants

AICPA American Institute of Certified Public Accountants

COBIT Control Objectives for Information and Related Technology

COSO Committee of Sponsoring Organizations

CPCL Central Purchasing Company Limited

CPD Continuing Professional Development

CVI Content Validity Index

FCPA Foreign Corruption Practices Act

FRO Financial Reporting Organizations

GCPC Government Central Purchasing Corporation

HRO Human Resource Organizations

ICPAU Institute of Certified Public Accountants of Uganda

ICS Internal Control System

IFRS International Financial Reporting Standards

IIA-UK Institute of Internal Auditors- United Kingdom

SAC System Audit ability and Control

SAIGA The South African institute of government auditor

SD Standard Deviation

SOX Sarbanes- Oxley Act

SSA Sub Saharan Africa

xi

ABSTRACT

Whereas extensive studies have been carried out to explore and explain internalcontrols and financial reporting quality in Privatized Companies worldwide, very fewof these have focused on Developing Africa and Uganda as a whole. This study assessedinternal controls and financial reporting quality in privatized companies focusing oncentral purchasing company limited (CPCL). A conceptual framework was developedon the internal controls and financial reporting quality of Central PurchasingCompany. The specific objectives were (i) To access the nature of internal controlsused by Central Purchasing Company Limited. (ii) To examine the nature of financialreporting quality at (Central Purchasing Company Limited). (iii) To establish arelationship between Internal Controls and Financial Reporting Quality. Aquantitative correlational cross-section survey and a case study research design wereused to collect data. Stratified and purposive sampling techniques were used to selectthe respondents. Microsoft Excel and SPSS were used to analyze the data and topresent the findings. Findings indicates that, the company had average internalcontrols and most of them were functioning properly .The correlation coefficient ofr=0.914 indicated that there is a strong positive relationship between internal controlsand financial reporting quality. It’s thus recommended that Central purchasingcompany management should ensure that all its internal controls that are implementedare properly functioning and are not undermined by its staff as a way of attainingfinancial reporting quality (B.K. Sebbowa, 2009), .(Gerrit and Mohammad J. 2010). Inconclusion, given the correlation coefficient above it’s evident that there is a strongpositive relationship between internal controls and the financial reporting quality ofthe company. Recommendations were made focusing mainly on the need to improvethe weak areas such as verification of documents an aspect internal control so as toachieve sustainable financial reporting quality.

1

CHAPTER ONE

1.0 INTRODUCTION

This study presents internal controls and financial reporting quality in privatized companies with

Central Purchasing Company as a case study. This Chapter covers the background to the study,

statement of the problem, objectives of the study, research questions, hypotheses, significance of

the study, scope of the study, the conceptual frame work and definition of key terms, and

organization of the study.

1.1 Background to the study

An internal control is a process implemented by an organization structure work and authority

flows, people and management information systems, designed to help the organization

accomplish specific goals or objectives with means of directing, monitoring and measuring of

organization resources. (COSO, 2005).

Internal control activities have been established by practitioners, primarily auditors. Rather than

investigate to control activities themselves, academics focused their research efforts on issues

surrounding the controls using an explicit, or implied, assumption that the properties of the

control activities are known. (Barra & Roberta 2010; Ashton1974; Bodner 1975; Cushing1974;

Doty et al1989; Hornik and Ruf 1997 Simon 1974 and Curtis1998) Aldridge and Colbert (1994)

define internal control as the process designed and effected by those charged with governance,

management and other personnel to provide reasonable assurance about the achievement of the

entity’s objectives with regard to the reliability of financial reporting, effectiveness and

efficiency of operation and compliance with applicable laws and regulations.(Gerrit and

Mohammad J. 2010),

Also internal control is defined as a process designed to provide reasonable assurance regarding

the achievement of financial reporting quality through reliability of financial reporting and

compliance with applicable laws and regulations. (Schaefer& James 2010; Peluchett & Joy

2009).

Internal control is a process effected by an entity's board of directors, management, and other

personnel designed to provide reasonable assurance regarding the achievement of objectives in

2

the following categories: reliability of financial reporting, effectiveness and efficiency of

operations, compliance with applicable laws and regulations.( Stephen H, 2003), Internal

controls have existed from ancient times. It is common knowledge among practicing

accountants, managers and business scholars that good internal controls prevent errors and frauds

leading to unqualified auditors opinion. External auditors may test the effectiveness of internal

controls and place reliance on the underlying records as a basis for the preparation of financial

reports. (ACCA- Managerial Finance Paper 8; 2010; and Panday;2008) .

In the United States many organizations have adopted the internal control concepts presented in

the report of the Committee of Sponsoring Organizations of the Tread way Commission

(COSO). Published in 1992.COSO describes internal control as consisting of five essential

components. These components, which are subdivided into seventeen factors, include:The

control environment

Risk assessment

Control activities

Information and communication

Monitoring

The COSO model is depicted as a pyramid, with control environment forming a base for control

activities, risk assessment, and monitoring. Information and communication link the different

levels of the pyramid. As the base of the pyramid, the control environment is arguably the most

important component because it sets the tone for the organization. Factors of the control

environment include employees' integrity, the organization's commitment to competence,

management's philosophy and operating style, and the attention and direction of the board of

directors and its audit committee. The control environment provides discipline and structure for

the other components. (Gerrit & Mohammad J, 2010).

Risk assessment refers to the identification, analysis, and management of uncertainty facing the

organization. Risk assessment focuses on the uncertainties in meeting the organization's

financial, compliance, and operational objectives. Changes in personnel, new product lines, or

rapid expansion could affect an organization. Sebbowa , (2009),

3

Control activities include the policies and procedures maintained by an organization to address

risk-prone areas. An example of a control activity is a policy requiring approval by the board of

directors for all purchases exceeding a predetermined amount. Control activities were once

thought to be the most important element of internal control, but COSO suggests that the control

environment is more critical since the control environment fosters the best actions, while control

activities provide safeguards to prevent wrong actions from occurring. Sarens, G. & De Beelde,

I. (2006b)

Information and communication encompasses the identification, capture, and exchange of

financial, operational, and compliance information in a timely manner. People within an

organization who have timely, reliable information are better able to conduct, manage, and

control the organization's operations.

Monitoring refers to the assessment of the quality of internal control. Monitoring activities

provide information about potential and actual breakdowns in a control system that could make it

difficult for an organization to accomplish its goals. Informal monitoring activities might include

management's checking with subordinates to see if objectives are being met.

A more formal monitoring activity would be an assessment of the internal control system by the

organization's internal auditors.In Hellenistic Egypt there was a dual administration, with one set

of bureaucrats charged with collecting taxes and another with supervising them. The sacking of

Troy was a classic example of the failure of internal controls. Mwindi (2008).

Internal Control System (ICS) is a very important function in the achievement of the

organizational success and successful management functions (The South African institute of

government auditor SAIGA 2003). It further pointed out that when administrative and financial

management decisions go wrong, reference is usually made to ICS to seek out possible reasons.

On the other hand, financial statement is a written report which quantitatively describes the

financial health of a company or an organization which usually includes the income statement,

balance sheet, cash flow statement and the statement of retained earnings. (Myojung; Kim and

Lim 2010).

4

Financial report Quality on the other hand refers to statements prepared to the required

accounting financial reporting standards to show the financial position of the business at the end

of the financial/accounting year and these statements must meet the following characteristics

which include; understandability, comparability, relevance and fair presentation.(Aharony, J and

A. Dotan, 2004) According to Welsch and Chesley(1990) the notes of balance sheets, cash flows

statement, statements of changes in are integral part of financial statements and help users

interpret the statement, elaborated on accounting policies, major financial effects and certain non

quantifiable events that may contribute to the success or failure of the business. The objective of

financial statements is to provide financial information about the reporting entity that is useful to

present and potential equity investors, lenders and other creditors in making decisions in their

capacity as capital providers. (Murray, 2010).

The Financial Accounting Standards Board and the International Accounting Standards Board

releases a joint exposure draft proposing significant changes to how businesses present their

financial statements. Two major objectives of the proposed financial statements are

‘’disaggregation’’ and "cohesiveness." Disaggregation means, simply, that information on the

financial statements will be broken into more detail than is currently done, Cohesiveness means

that financial information expenses on the statement of comprehensive income to specific assets

or liabilities on the balance sheet and to specific cash flows on the statement of cash flows.

(Wagoner, Joel, 2011).

According to Osborne and Gaebler 1992, privatization is the shift of functions, activities and

responsibilities from the public (government) sector to the private sector. It involves a process

where the government gradually and progressively eliminates their involvement in direct service

provision while maintaining responsibility and authority over key functions such as

standardization, certification and accreditation. According to Megginson and Netter 2001,

Privatization is the deliberate sale by a government of state-owned enterprises or assets to private

economic agents.Andrews and Dowling, 1998 describe Privatization as a process by which state

owned enterprises are sold to the private sector

5

In 1991/92 financial year, Uganda had about 140 State-Owned Enterprises covering a diverse

range of activities from trade and commerce, agricultural production and processing,

manufacturing, hotel and tourism, banking, insurance and utility services. Over 85% of these

State-Owned Enterprises were commercial in nature and were considered unlikely to survive in

competition with the emerging private sector without significant continuing government subsidy

(Adam Smith Institute, 2005).

In 1993, privatisation and reform supporting legislature, the Public Enterprises Reform and

Divestiture Statute 1993, Statute No. 9, (thereafter referred to as the PERD 1993 Statute) was

then passed by parliament and enacted to give legal backing to the policy reform objectives. This

was a pre-reform set of activities and an enabling law formulation that legalized the Economic

Reform process. The law served to safe guard outcomes of the operations and future legal

consequences. However some of the enterprises such as Lake Victoria bottling company– a soft

drinks company and Nile Breweries had already been privatised before the law was passed!

The PERD 1993 Statute provided guidelines for the reform and divestiture. It categorized the

enterprises that were to be reformed or divested under the programme, laid down the

implementers and the modes of privatisation that would be used in the process. There were

subsequent amendments to the statute along the way.

Following continued criticism from the World Bank and International Monetary Fund (IMF)

regarding poor performance of public enterprises especially in Sub-Saharan Africa (SSA), many

governments have had to implement Structural Adjustment Reforms to try and improve their

economies and to gain access to financial credit facilities and so did Uganda (Tangri et al. 2001).

In May 1987, Uganda government took a stand to embrace a radical Economic Recovery

Programme (ERP) to improve the performance of the economy and ensure sustainable growth.

This programme introduced privatisation into the economy and this involved rationalization of

state ownership, liberalization, rehabilitation, divestiture, consolidation and liquidation. The

privatisation programme is part of the overall Economic Recovery Programme (ERP) and its

adoption was intended to invigorate the private sector so that it could make the private sector

play a leading role in the development of the economy (Privatisation Unit 2005).

6

The Central Purchasing Company was formed following the divestiture of the Government

Central Purchasing Corporation (GCPC). GCPC had been set up by government to procure

common-user items in bulk and supply these materials to Government at lower prices taking

advantage of economies of scale. GCPC eventually started supplying to the private sector as

well. In June 2000, GCPC was privatized by way of a Management Employee Buyout under

which the former employees of GCPC forfeited their terminal benefits for stock in the company.

The company which was originally owned by eighty six (86) individuals now trades as the

Central Purchasing Company Ltd (CPCL) with its main business being procurement and trading

for both the public and private sector.

The company set up should be designed to realize the objective of the company. However an

evaluation of the company structure, management of staff, financial performance, decision

making structures and levels that procurement function did not portray alignment to the

objectives. For instance Company’s capacity assessment of 1999 conducted by private sector

foundation revealed that most private companies go down in business due to weakness and laxity

in control systems. B.K. Sebbowa, (2009)

1.2 Statement of the problem

Despite the availability of professional staff and their continued development, internal and

external auditor’s contribution in most Companies still experience difficulty in presenting

financial reports that reflect the financial condition and results of operations in rational and

meaningful manner. According to Blackbeard (2006), information is often delayed, inaccurate

and relayed from person to person rather than via reports; making it hard for Organizations to

achieve financial reporting quality .

However despite all the above efforts, the company still struggles with meeting acceptable

financial reporting quality, financial reports are not made timely, accountability for the financial

resources are still wanting, frauds and misuse of the Company’s resources have been unearthed (

Auditors Report,2011). If the Company continues in this direction, decisions made may not be

informed and this may lead to declined performance. While there are many factors that affect

Financial Reporting Quality of privatized Companies, particularly Central Purchasing Company

Limited, Internal Controls may be playing a significant role. It is for this reason that the

7

researcher embarked on this study relating Financial Reporting Quality (Compliance and

Reliability) to Internal Controls, specifically preventive and detective controls in Central

Purchasing Company Limited.

1.3 Objectives of the study

This sub section spells out the general and specific objectives of the study

1.3.1 General objective

The general objective of the study was to find out the effect of internal controls on financial

reporting quality in privatized companies in Uganda, using CPCL as a case study.

1.3.2 Specific objectives

i) To assess the nature of Internal Controls used by CPCL.

ii) To examine the nature and Quality of Financial Reporting at CPCL.

iii) To establish a relationship between Internal Controls and Financial Reporting Quality in

CPCL.

1.4 Research Questions

i) What internal controls are being used by Central Purchasing Company?

ii) What is the nature and quality of financial reporting at CPCL?

iii) What relationship exists between the internal controls and the Financial Reporting Quality?

1.4.1 Hypothesis

There is no significant relationship between Internal Controls and Financial Reporting Quality.

1.5 Significance of the study.

(i) The study may help management of CPCL in setting policies that are relevant to company’s

performance in improving their financial reporting.

(ii) The study may provide information and knowledge to academicians and other researchers

and also the study findings can generate knowledge for the government about why privatized

companies fail to comply with financial reporting requirements. This can help the government to

identify what kind of technical support they should provide the privatized companies before

giving them any funding in order to ensure acceptable quality of financial reports.

8

(iii) The study may provide information that will assist workers of CPCL and other stakeholders

to improve on the existing internal controls in the Company

(iv) The study findings can also help privatized companies in improving their compliance to

financial reporting requirements and thus improving their capability to attract more development

and ensure their company’s sustainability.

1.6 Conceptual frame work

Independent Variable Dependent Variables

Mediating Variables

Source: Conceptualized by Researcher

Figure 1.1 Relationship between internal controls and financial reporting quality.

Fig.1.1 provides a conceptual framework relating internal controls to financial reporting quality.

The independent variables are internal controls and the framework depict two elements of

internal controls, namely preventive controls and detective controls, all conceptualized to have

an effect on financial reporting quality. The dependent variable in this study is the financial

reporting quality which was measured in terms of compliance to International financial reporting

standards and reliability for its purpose. The framework further shows that there are moderating

variables such as company policies and systems, organizations efficiency through experience,

skills, knowledge and ethical behavior of staff ,For example, despite the expected relationship

between internal controls and Financial Reporting Quality, organizational inefficiency can have

an opposite effect.

Financial Reporting QualityInternal Controls

Compliance

Reliability

Preventive ControlsSegregation of Duties

Approvals, Authorizations,and Verifications:

Detective Controls

Reviews of Performance Reconciliations Internal Audit

Company policies andsystems

Organizational

Efficiency

Experience, skillsand knowledge ofStaff

9

1.7 Scope of the Study

This sub section covers geographical scope, content scope and time scope.

1.7.1 Geographical Scope

The study was undertaken at the head office of Central Purchasing Company Ltd located on plot

56 Bell Avenue West, Jinja and two branches in Jinja District and Malaba in Busia District. The

researcher selected Central Purchasing Company Ltd because it was the first Government

Corporation to be sold to its own employees under the privatization unit and pioneer of takeover

by employees in Uganda. The locations were chosen because Jinja and Malaba office are the

only remaining operational offices of Central Purchasing Company Limited.

1.7.2 Content Scope

The study focused on accounting controls and was limited to two dimensions of accounting

controls ( preventive controls and detective controls) as independent variables and financial

reporting quality measured in terms of compliance and reliability of financial reporting as

standards of measurement under internal financial reporting .

1.7.3 Time scope

The study covered the period from 2002 to 2009 in order to review the significance of internal

controls on financial reporting quality so as to come up with the necessary conclusions and

recommendations which would be generalized and applicable to justify the study. The researcher

was interested in this period because it was the time Central Purchasing Company started selling

off its properties in Kampala and laying off employees.

1.8 Definition of Key Concepts used in this Study.

Internal controls: refers to a control environment and control procedures adopted by

management of an entity, to assist in achieving the practicable; the orderly and efficient conduct

of its business, adherence to management policies, safeguarding assets, prevention and detection

of fraud and error, accuracy and completeness of records and timely preparation of reliable

financial information. (ISA 400 Risk assessment and Internal control), Internal controls are those

measures which ensure the accuracy of financial statements through preventive and detective

control. Millichamp, (1996).

10

These are measures which ensure the accuracy of financial statements. Once financial

statements are known to be accurate, there will be increased reliance on the underlying

accounting system as a basis for the preparation of accounting reports. Accounting control may

include authorization, management accounts (profit, loss account and balance sheet) produced

monthly, periodic stocktaking and valuation and reconciliation of bank statements with the cash

book. Millichamp (1996).

Detective Internal Controls: These controls are meant to expose those frauds and errors that

have not been prevented. An audit, both internal and external will serve to detect errors and

frauds, reconciliation of bank accounts, reconciliation of debtors ledgers to their controls

accounts, cash and stock accounts will detect anomalies that need to be investigated and decision

to correct them made by management. Supervision is also a detective control. (Institute of

Chartered Accountants of Britain and Wales, sept.1999).

Administrative Internal Controls are controls that are put in place by management to ensure

operational efficiency, effectiveness and compliance with management policies in all

departments or sections of an organization. Administrative control may include authorization to

use equipment or entry to certain offices, security of all the assets of the organization. Finance

Markets ‘Authority (AMF).January2007.

Financial Reporting. According to Frank wood and Sangster, (1998) financial reporting is

defined as a discipline concerned with the preparation and presentation of financial statements.

While ACCA, (Foulks Lynch, 2005), defines financial reporting as preparation of financial

statement in accordance to accounting standards.

It’s a statements prepared to the required accounting financial reporting standards to show the

financial position of the business at the end of time period and also the operating results by

which the business arrives at this financial position .It is of view that accountants rely on record

keeping systems particularly, double entry to produce meaningful financial reports that

summarize both the past and current financial positions of the organization. Also financial

11

reporting show past and projected finances and these reports are both the sources of tax

information and the means of analyzing the business. Blake J (1999), Brookson (2001.

Financial reporting quality. Financial report is said to be of quality when it meets all its

characteristics like reliability, comparability, relevancy, understandability and also measures a

company's financial performance during a specific accounting period.

Compliance of financial reporting. Compliance refers to practical application of the existing

laws and regulations and internal policies in relations to IFRS framework. Coco indicates that

control comprises: those elements of an organization (including its resources, systems, processes,

culture, structure and tasks) that, taken together, support people in the achievement of the

organization's objectives.

Reliability of financial reporting is all about information being fit for purpose. Where people

have a clear responsibility to do something and they need to use information to do this, it brings

the whole issue of reliability into focus. The purpose for any financial information is aiding

management with clear decision concerning financial matters as reliability is seen as an

important concept in a number of other fields such as engineering and research we are keen to

see if the theory in these areas may help us to understand how reliability relates to audited

financial statements.

1.9 Organization of the study

The Study covered five chapters as follows Chapter one covers the background to the study,

statement of the problem, general objectives of the study, specific objective of the study,

research questions, hypothesis tested, significance of the study, the conceptual frame work, and

scope of the study, definition of key terms and organization of the study.

Chapter two presents a review of related literature on internal controls and financial reporting

quality.

Chapter three is the detailed descriptions of the research methods and instruments employed in

the study.

12

Chapter four is a presentation and discussion of the study findings based on the objectives

aiming at internal control system and financial reporting quality for the last seven years.

Chapter five presents the summary of the results, conclusion and recommendations from the

study.

13

CHAPTER TWO

LITERATURE REVIEW

This chapter comprises the concepts and views of authorities in this area of study that is internal

control and financial reporting quality and the relationship between the two variables of the

study.

2.1 The nature of Internal Controls

There are numerous definitions of internal control, most of them having been drafted by

professional accountants’ organizations.

This is the case for the definition of internal control provided in 1977 by the French Institute of

Chartered Accountants: “internal control is the set of security measures which contribute to the

control of a company. Its aim is to ensure, on the one hand, the security and safeguard of assets

and the quality of information, on the other hand, the application of instructions given by Senior

Management, and to encourage improvements in performance. It is evidenced through the

organization, methods and procedures for each of the company’s activities, so as to ensure the

continuity of that company”. Finance Markets ‘Authority (AMF).January2007.

Internal control is a company’s system, defined and implemented under its responsibility, which

aims to ensure that: Laws and regulations are complied with; the instructions and directional guidelines

fixed by Executive Management or the Management Board are applied, The Company’s internal

processes are functioning correctly, particularly those implicating the security of its assets.

In determining its policies with regard to internal control, and thereby assessing what constitutes

a sound system of internal control in the particular circumstances of the company, the board’s

deliberations should include consideration of the following factors: the nature and extent of the

risks facing the company; the extent and categories of risk which it regards as acceptable for the

company to bear; the likelihood of the risks concerned materializing; the company’s ability to

reduce the incidence and impact on the business of risks that do materialize; and the costs of

operating particular controls relative to the benefit thereby obtained in managing the related

risks. (Institute of Chartered Accountants of Britain and Wales, sept.1999).An internal control is

broadly classified into administrative and accounting controls.

14

Administrative internal controls are controls that are put in place by management to ensure

operational efficiency, effectiveness and compliance with management policies in all

departments or sections of an organization. Administrative control may include authorization to

use equipment or entry to certain offices, security of all the assets of the organization.

Accounting internal controls are those measures, which ensure the accuracy of financial

statements. Once financial statements are known to be accurate, there will be increased reliance

on the underlying accounting system as a basis for the preparation of accounting reports.

Accounting control may include authorization, management accounts (profit, loss account and

balance sheet) produced monthly, periodic stocktaking and valuation and reconciliation of bank

statements with the cash book. Mill champ (1996).This control is further classified into;

Preventive, Detective and Corrective internal controls.

2.1.1 Preventive Internal controls: These are controls that are put in place by management to

prevent the accuracy of errors and frauds in the financial statements. These controls include

internal audit, recruitment of the right people with adequate training and experience in the right

places, segregation of duties, authorization and approval of transactions and surprise cash

accounts in the cash office among many more. Coe, Charles K, Ellis, Curtis (2010)

Separating Approval and Payment. A requirement that an employee who is authorized to

initiate a payment to a vendor is not also authorized to sign vendor payment checks would be a

preventive control. Among other things, such a control is designed to reduce the risk of

unauthorized payments,( Krishnan, J. 2005).

Limiting Access to IT Systems. Controlling access to software programs related to accounting

or payment functions through the use of passwords and access codes is another type of

preventive control. Limiting the persons who can change IT programs reduces the risk of

unauthorized transactions. (Conor, Errol &Divesh, 2006).

Segregation of Duties: One of the building blocks of internal control is segregation of duties.

This concept involves assigning responsibility for different parts of a process to different people

so that no one person can control the entire process. The importance of segregation of duties

stems in part from the fact that collusion between two individuals is less likely than misconduct

15

by a single individual. Segregation also reflects the lower probability that two persons will make

the same error with respect to the accounting for a transaction. Assigning responsibility for

physical access to a supply room to a different person than the individual who is responsible for

maintaining the records of the supplies inventory is an example of segregation of duties. (COSO,

2010).

Approval, verification, and authorization

The first step towards controlling financial reporting is to ensure that all transactions are properly

authorized in accordance with management’s policies. Management authorizes employees to

perform certain activities and execute certain transactions within limited parameters. In addition

management specifies those activities or a transaction that needs supervisory approval before

they are performed or executed by employees. A supervisor’s approval (manual or electronic)

implies that he or she has verified and validated that the activity or transaction conform to

established policies and procedure (Rezaee, I&Zabihellah.B, 2002).

Authorization is the delegation of authority and it may be general or specific. Giving a

department permission to expend funds from an approved budget is an example of general

authorization, specific authorization relates to individual transactions; it requires the signature or

electronic approval by a person with approval authority. Approval of a transaction means that the

approver has reviewed the supporting documentation and is satisfied that the transactions is

appropriate, accurate and comply with the applicable laws, regulations, policies and procedures.

Generally approvers review supporting documents, question usual items and make sure that

necessary information is present to justify the transactions before they sign off on the transaction.

As a general rule, authorizations do both of the following (COSO, 2010).Require advance

approval, require written documentation of approval, Dittenhofer, M. (2001).

2.1.2 Detective internal controls:

These controls are meant to expose those frauds and errors that have not been prevented. An

audit, both internal and external will serve to detect errors and frauds, reconciliation of bank

accounts, reconciliation of debtors ledgers to their controls accounts, cash and stock accounts

will detect anomalies that need to be investigated and decision to correct them made by

management. Supervision is also a detective control, (Hayes et al. 2005).

16

Review of performance : While business firms require ongoing changes in organizations'

activities (Alles et al, 2006), they also provide internal control effectiveness thoroughly

understanding in the way continuous monitoring adequacy is because continuous monitoring

ensures that firms are subject to operational effectiveness, reliability of financial reporting, and

regulatory compliance. Therefore, continuous monitoring adequacy is a component of internal

controls that it serves preventive and detective control, for example, when staff members who

know their work as well, they always perform their duties. In this research, continuous

monitoring adequacy is defined as the sufficient and appropriate process of methodology for

issuing the extent of firm to monitor and evaluate internal control system, involvement of long

and short term action plan that the organization uses to assess their plan on strategic objectives.

The appropriate and sufficient monitoring control includes of a performance by firm's evaluators

who respect, trust, and believe the operational control system. The monitors such as internal

auditors or to whom a company assigns their duty to be continuous or ongoing monitoring by

using a highly a control skills, knowledge, and ability that they can evaluate, summarize, and

control effectively. Hence, continuous monitoring leads to preventive and corrective firms'

control system before all members have gotten an effect on organization's goals. The continuous

monitoring adequacy will provide the strongest support for company reporting, particularly, a

reliance of financial reporting (Shapiro and Matson, 2008)

Communication: Within organization, communication is very important baseline in business

firms for both inside and outside the firms (Duxbury and Neufeld, 1999). However, particular

intra organization communications want more links from the staff members and college to

encourage information and knowledge (Zhang et al, 2005). When firm acquires new information

or company rules of internal control, the senior management will make connections with the

target groups and might be aware of information and consciousness within the firm (Yang and

Maxwell, 2011). Therefore, the role of intra organization communication needs a clear

communication skills, or communication in practice. Effective communications within

organization allows employees to recommend and suggest internal control guidance on practical

performance which is used in the day to day operations of a business (Harvey et al., 2000).

Organization communication has been defined as a comprehensive and thorough of firm

members who are receiving or addressing on particular internal control topics and issues

17

completely, clearly, reliability and timeliness. The potential of intra origination communication

may address or stress on the awareness between organization staffs regarding how a quickly was

relation with internal control information it is. If firm members felt that their behavior had

received incomplete or not clear information that firm sends from the firm particular internal

control policies announcement, they perhaps feel most dissatisfied consequently internal control

doesn't effectiveness (Oberg and Walgenbach, 2008). The control of channel communication

distribution information can help build effectiveness of internal control mechanism (Nunlee,

2005).

Firm must be quickly expanding internal control information to all employees' levels. Moreover,

firm policies should show that its reliability can be assisted by providing internal control actually

happening at the intra communication level within organization (Carlsson et al 2010; Hogard et

al, 2005).) Intra-firm communication possess is sharing information, a potential adapter collect

information before making a decision impact on innovation in finance (Everdingen and Wiernga

2002). On the other hand, intra organization communication should be designed to help both

users and contributors to communicate and share information within organization easily (Yang

and Maxwell, 2011; Bardir et al 2009; Russo and Harrission, 2005; Millson and Wilemon, 2002).

The wide domain of potential intra organization communication related to internal control

effectiveness has a significant criterion such as task performance and respect (Driskill and

Downs, 1995) especially accounting policy and firm member belief or behavior respectively.

(COSO). 2007

Risk assessments: At present, every business firms requires risk assessment to avoid and mitigate

firm risk purposes. Risk management system consists of manager's style and his philosophy,

linked with business strategy, and objective setting in operating (Arena et al., 2010). The risk

management today has moved from the entity area of the firm to the corporate cover the firm

(Arena et al., 2010, Power, 2009). The sufficient and appropriated risk management procedure

may present internal control effectiveness by senior executive management and board of director

policies. Hence, the senior management and board of director must understand risk appetite more

as the consequence organizational process (Power, 2009). The clear and sufficient accounting

policies can make appropriate internal control effectiveness (COSO, 2004). Therefore, risk

management efficiency is intended to reflect that firm has been updated rules, standard of work,

18

guidance, and especially a quality of compliance. However, organizations using a weaker risk

management process focused on control compliance and experience are with more difficulty

(Arnold et al., 2011). The outcome of risk management efficiency on the internal effectiveness is

reliability of financial reporting. Hence, risk management efficiency is a part of the internal

control effectiveness. Therefore, internal control system is stemmed from the attitude and

behavior of senior executive management and Board of Directors' behavior that must

transparency, integrity, accountability, and competiveness, (B.K. Sebbowa, 2009).

Reconciliations. Independently comparing two sets of records that relate to the same transaction

and analyzing any differences is a detective control. Reconciling the cash account balance on the

company’s books to its bank records could identify whether any payments recorded by the com-

pany were not received by its bank, or whether any withdrawals reported by the bank were not

accounted for by the company, (B.K. Sebbowa, 2009).

Internal Audit, Whittington & Pany (2001) suggest that internal auditing is performed as part of

the monitoring activity of an organization. It involves investigating and appraising internal

controls and the efficiency with which the various units of the organization are performing their

assigned functions. An Internal Auditor is normally interested in determining whether a

department has a clear understanding of its assignment, is adequately staffed, maintains good

records, properly safeguarding cash, inventory & other assets and cooperates harmoniously with

other departments. The internal auditor normally reports to the top management. (Gupta, 2001)

on the other hand asserts that “Internal audit is an independent appraisal function established

within an Organization to examine and evaluate its activities as a service to the organization”.

The objective of internal audit is to assist members of the organization in the effective discharge

of their responsibilities. According to Gupta “the scope of internal audit is determined by

management”. This may however, impair the internal auditor’s objectivity and hampers his

independence, it is quite hard to report negatively on someone who determines the scope your

work. Although at a Seminar organized by the Institute of Certified Public Accountants of

Uganda (ICPAU), Sebbowa, 2009 in his presentation “The role of Internal Audit function in

Organizations”, states that “Independence is established by organizational and reporting

structure” and that “Objectivity is achieved by an appropriate mindset”. Sebbowa, 2009 also

19

defines “Internal auditing is an independent, objective assurance and consulting activity designed

to add value and improve an organization’s operations.ICPAU,(2009).

It helps an organization accomplish its objectives by bringing a systematic, disciplined approach

to evaluate and improve the effectiveness of risk management control and governance

processes”. He further mentions the principles of Internal audit to include; Integrity, Objectivity,

Confidentiality and Competency. However, given that Internal Auditors are appointed by

management, report to management, and are employees of an organizations, their objectivity is

usually highly compromised Adams, M. B. (2006).

In accordance to Institute of Internal Auditors (IIA-UK; 1997), independence is applicable to all

categories of auditors. This means the opportunity granted to the auditors to report directly to the

top authority. Woolf (1986), says, although an internal auditor is an employee of the enterprise

and cannot therefore be independent of it, he should be able to plan and carryout his work as he

wishes and have access to the highest level of management. However, Millichamp (1993) says,

effective internal audit should be carried out by an independent personnel though they are

employees appointed by management, for them to work efficiently, they should have scope to

arrange priorities and activities have un restricted access to records, assets and personnel.

Adams, M. B. (1994)

According to Bhatia (2003), Internal Auditing is the review of operations and records sometimes

undertaken within the business by especially assigned staff. It’s also an independent appraisal

function established within an organization to examine and evaluate the effectiveness, efficiency

and economy of managements control system (Subramaniam, 2006). Its objective is to provide

management with re-assurance that their internal control systems are adequate for the need of the

organization and are operating satisfactorily (Reid & Ashelby, 2002). It is a component of the

internal controls set-up by management of an enterprise to examine, evaluate and report

operations of accounting and other controls. The quality and effectiveness of internal audit

procedures in practice are necessary since internal auditors cover a wide variety of assignments,

not all of which will relate to accounting areas in which the external auditor is interested. For

example, it’s common these days for internal audit to undertake the extensive and continuous

task of setting management goals and monitoring its performance (Woolf, 1996).

20

Emasu (2010) notes that “The effectiveness of internal audit function partly depends on; legal

and regulatory framework, placement of the function and its independence, existence of audit

committees, resources allocated to the function and professionalism of internal audit staff”. It is

however a bitter reality that internal audit departments are rarely adequately facilitated.

Regarding the size and facilitation of the Internal Audit Function, Gerrit and Mohammad (2010),

found evidence in support of the monitoring role of the Internal Audit Function. They

specifically, found evidence that management ownership is positively related to the relative size

of the Internal Audit Function, which is inconsistent with traditional agency theory arguments

that predict a negative relationship, but more in line with recent studies on earnings management.

This finding suggests that increased management ownership may influence the board of directors

to support larger Internal Audit Functions to allow them to closely monitor managers’

performance. It is also plausible that management with higher share ownership is motivated to

invest in larger Internal Audit Function for better monitoring of earnings and for signaling to the

board of directors that, despite their high stake in earnings, they are convinced that appropriate

use of resources has to be assessed on a regular basis. Gerrit and Mohammad also believe that

the proportion of independent board members to have a negative effect on Internal Audit

Function size. This finding may indicate a substitution effect, which means that independent

board members may be considered as an alternative monitoring mechanism to the Internal Audit

Function. They further assert that the control environment has a significant effect on the relative

size of the Internal Audit Function. Specifically, a supportive control environment characterized

by formalized integrity and clear ethical values, a high level of risk and control awareness, the

perception that risk management is important and the fact that responsibilities with respect to risk

management and internal control are clearly defined is associated with a relatively larger Internal

Audit Function. ACCA (2010)

Using a US sample, Wallace & Kreutzfeldt (1991) found that companies with internal audit

departments are observed to be significantly larger, more highly regulated, more competitive,

more profitable, more liquid, more conservative in their accounting policies, more competent in

their management and accounting personnel, and subject to better management controls. Carey et

al. (2000) found that agency variables do not explain the voluntary use of internal audit by

21

Australian family firms. More recently, a study by Goodwin-Stewart & Kent (2006), using a

sample of Australian listed companies, shows that the existence of an Internal Audit Function is

positively associated with firm size and commitment to risk management. Sarens & De Beelde

(2006) also show that the risk and control awareness have an influence on the scope of the

Internal Audit Function. These results suggest that when management is aware of risks and

control activities, they are more likely to understand the role of the Internal Audit Function in

monitoring risk and control activities, thus it is more likely that they will support a relatively

larger Internal Audit Function (Sarens & De Beelde, 2006a; Selim & McNamee, 1999). Meigs et

al (1988) holds that there must be a strong internal control system and the internal auditor must

verify the operations of the system in much the same way, as the external auditor. It involves the

investigation, recording, identification and review of compliance tests of control, they also

argued that effective internal audit procedures provide sufficient relevant and reliable evidence in

order to detect and prevent fraud. ACCA (2009/2010)

Kochan (1993), considers auditing procedures in one company and describes steps taken in

implementing a quality assurance system, she discusses the use of internal audits as an essential

part of ISO 9000 certification process. Boakye-Bonsu (1999) asserts that internal audit

procedures are seen as ends in themselves rather than a means towards a specific objective, with

such an approach our rambler would undoubtedly get lost. Internal audit procedure is a form and

content manual that includes audits notes and responsibilities, documentation standards, local

reporting standards and targets, training requirements and expectations and performance

measures and indicators (Watts, 1999). Effectiveness is the achievement of goals and objectives

using factor measures provided for in determining such achievement. However, it has been

traditional in internal auditing that determination of internal auditing effectiveness can be

accomplished by evaluating the quality and effectiveness of internal auditing procedures that

result in determination by the internal auditors of the character and the quality of effectiveness of

the auditee’s control operations and if the auditing procedures are effectively carried out, then

the evaluative results are positive (Dittenhofer, 2001). Maitin (1994) says efficiency and

effectiveness of internal audit procedures is not a simple task, successful operation is governed

by the extent to which the element of internal audit procedures receive attention which include;

expertise, independence, objectivity and totality. Effectiveness of internal audit procedures is a

measure of the ability of the programme to produce a desired effect or results that can be

22

qualitatively measured (Harvey, 2004). Zabihollah (2001) argues that, there should be effective

internal audit procedures to ensure reliability of financial statements, operational reports

safeguarding corporate assets and effective organizational controls. Benston (2003) further

supplements that perception and ownership, organization and governance framework, legislation,

improved professionalism and resources were identified as functions in the public sector derived

from the effectiveness of the internal audit procedures. How far internal audit procedures

succeed in their effort of effectiveness is mainly judged by three factors that include; frequency

of irregularities committed by the staff in the organization in form of errors or fraud, the

promptness with which such irregularities are detected by the authorities and the planning which

makes possible repetition of such irregularities in future more difficult (Reid & Ashelby, 2002).

The work of the internal auditor should appear to be properly planned, controlled, recorded and

reviewed. Examples of the due professional care by the internal auditor are the existence of an

adequate audit manual, general internal audit plans, procedures for controlling individual

assignments and satisfactory arrangements for reporting and following up. Earnest and Young

(1995),

The need for an internal audit function will vary depending on company-specific factors

including the scale, diversity and complexity of the company’s activities and the number of

employees, as well as cost/benefit considerations. Senior Management and the board may desire

objective assurance and advice on risk and control. An adequately resourced internal audit

function (or its equivalent where, for example, a third party is contracted to perform some or all

of the work concerned) may provide such assurance and advice. There may be other functions

within the company that also provide assurance and advice covering specialist areas such as

health and safety, regulatory and legal compliance and environmental issues.

In the absence of an internal audit function, management needs to apply other monitoring

processes in order to assure itself and the board that the system of internal control is functioning

as intended. In these circumstances, the board will need to assess whether such processes provide

sufficient and objective assurance. Kombo & Tromp (2009)

Assurance. When undertaking its assessment of the need for an internal audit function, the board

should also consider whether there are any trends or current factors relevant to the company’s

23

activities, markets or other aspects of its external environment that have increased, or are

expected to increase, the risks faced by the company. Such an increase in risk may also arise

from internal factors such as organizational restructuring or from changes in reporting processes

or underlying information systems. Other matters to be taken into account may include adverse

trends evident from the monitoring of internal control systems or an increased incidence of

unexpected occurrences. http://audit.unlv.edu/InternalControls.htm

The importance of internal controls

A company’s system of internal control has a key role in the management of risks that are

significant to the fulfillment of its business objectives. A sound system of internal control

contributes to safeguarding the shareholders’ investment and the company’s assets.

Internal control (as referred to in paragraph 20) facilitates the effectiveness and efficiency of

operations, helps ensure the reliability of internal and external reporting and assists compliance

with laws and regulations. Kochan, A. (1993).

Effective financial controls, including the maintenance of proper accounting records, are an

important element of internal control. They help ensure that the company is not unnecessarily

exposed to avoidable financial risks and that financial information used within the business and

for publication is reliable. They also contribute to the safeguarding of assets, including the

prevention and detection of fraud. I. M. Pandey (2010).

A company’s objectives, its internal organization and the environment in which it operates are

continually evolving and, as a result, the risks it faces are continually changing. A sound system

of internal control therefore depends on a thorough and regular evaluation of the nature and

extent of the risks to which the company is exposed. Since profits are, in part, the reward for

successful risk taking in business, the purpose of internal control is to help manage and control

risk appropriately rather than to eliminate it. (Institute of Chartered Accountants of Britain and

Wales, sept.1999)

Does the company have clear objectives and have they been communicated. So as to provide

effective direction to employees on risk assessment and Control issues? For example, do

objectives and related plans include? Measurable performance targets and indicators? Are the

24

significant internal and external operational, financial, compliance and other risks identified and

assessed on an ongoing basis?

Significant risks may, for example, include those related to market, credit, liquidity,

technological, legal, health, safety and environmental, reputation, and business probity issues. Is

there a clear understanding by management and others within the company of what risks are

acceptable to the board?

Internal control will also be evaluated by the external auditors. External auditors assess the

effectiveness of internal control within an organization to plan the financial statement audit. In

contrast to internal auditors, external auditors focus primarily on controls that affect financial

reporting. External auditors have a responsibility to report internal control weaknesses (as well as

reportable conditions about internal control) to the audit committee of the board of directors.

(Nigel Turnbull, Rank Group Plc)

Internal control must be evaluated in order to provide management with some assurance

regarding its effectiveness. Internal control evaluation involves everything management does to

control the organization in the effort to achieve its objectives. Internal control would be judged

as effective if its components are present and function effectively for operations, financial

reporting, and compliance. The boards of directors and its audit committee have responsibility

for making sure the internal control system within the organization is adequate. This

responsibility includes determining the extent to which internal controls are evaluated. Two

parties involved in the evaluation of internal control are the organization's internal auditors and

their external auditors. (Tim Row bury Internal, Audit Consultant)

At the specific transaction level, internal control refers to the actions taken to achieve a specific

objective (e.g., how to ensure the organization's payments to third parties are for valid services

rendered.) Internal control procedures reduce process variation, leading to more predictable

outcomes. Internal control is a key element of the Foreign Corrupt Practices Act (FCPA) of 1977

and the Sarbanes–Oxley Act of 2002, which required improvements in internal control in United

States public corporations. Internal controls within business entities are also referred to

as operational controls.

25

Limitations of internal controls

Internal controls are procedures and policies to be followed when carrying out financial

transactions. Policies are mere guides to action to ensure consistency in treatment of similar item

at different times; being guides they are subject to personal error of judgment. It is in the interest

of the organization that set procedures are followed when handling financial transactions.

Internal controls can offer only reasonable assurance that management objectives are reached,

this is because of certain inherent limitations as follows;- Menon, K. & Williams, J. D. (1994),

Due attention is devoted to day to day operational matters, but at the finalization stage of

financial reports, major adjustments are passed which may contain errors and fraud.

Internal controls can lead to internal rigidities that delay decisions and financial reports. Internal

controls already in use may prevent creativity because procedures were set and must be followed

without deviation. Collusion among staff can be used to undermine the internal control

procedures leading to loss of assets.

Management resistance to controls. In a situation where management does not support internal

control procedures, it may override controls to its own advantage. Internal controls work well

where management support is evident.

Management support could arise in form of staff recruitment policies, reviews of financial

information and taking corrective action where deviation from control procedures is reported,

Sarens, G. & De Beelde, I. (2006b).

Some internal control procedures are not cost effective; the cost of a control is disproportionate

to the cost of potential loss due to errors and fraud.

The effectiveness of internal control system is always affected due to carelessness, distraction

and misunderstanding of instructions. Human weaknesses tone down the effectiveness of internal

control systems, Emasu (2007).

Changing business environment may cause inadequacy in procedural conduct of business and

thereby compliance with procedures becomes difficult. (M.S. Ramaswamy, 1997).

In the control activities, Authority usually flows from the Board of Director to general

management.

26

General management therefore exercises delegated authority to ensure that all transactions both

financial and non financial are authorized.

Separation of duties is implemented to prevent intentional and unintentional errors and

misstatements. Duties such as custody of assets should be separate from authorization; posting

of ledgers should be separate from payments and receipting of cash, ( Subramanian, N. 2006)..

Documentation and record keeping provide proof for the accuracy of transactions. Transactions

must be supported by third party invoices, receipts and claim forms. Every transaction has to be

recorded permanently in the books of the organization, Ogneva, M., K. R. Subramanyam, and K.

Raghunandan. 2007.

Unauthorized access to some offices like cash, computer and stores is implemented to avoid loss

of portable assets and also to avoid deliberate damage to say computer programs. (KPMG Audit

Manual, 1988)

2.2 Financial Reporting Quality.

According to Collins and Collins (1978), a financial report is a means of portraying financial

accountability. In order for an organization to review the financial activities of the past year and

make plans for the future it prepares and publishes annual accounts or financial reports.

According to Samuel (1991), these are outputs of an accounting system and they are prepared at

the end of the year, hence the name final accounts. According to Horne (1998), the financial

reports should include a narrative description of the organization’s activities and audited

financial statements. He argues that these enable the stakeholders to see the organization’s

performance and the overall financial situation of the organization. Samuel (1991), states that

managers and accountants are usually required to defend the results shown in the financial