interagency task force on commodity markets...

TRANSCRIPT

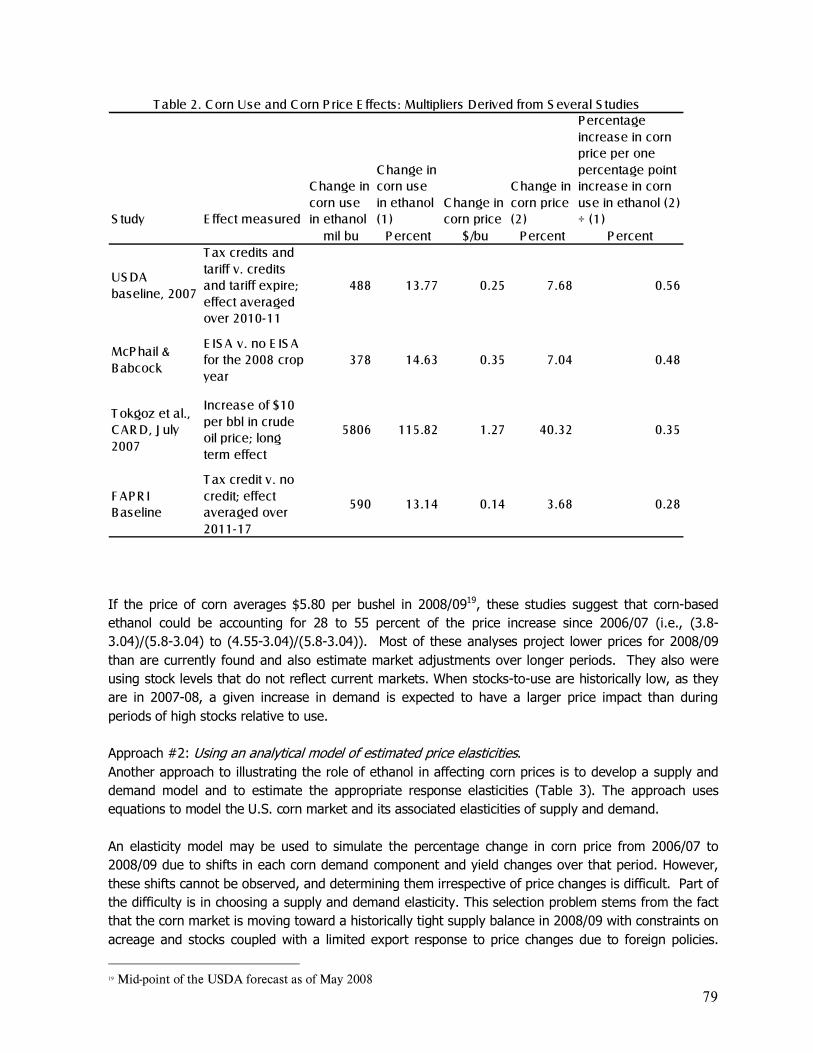

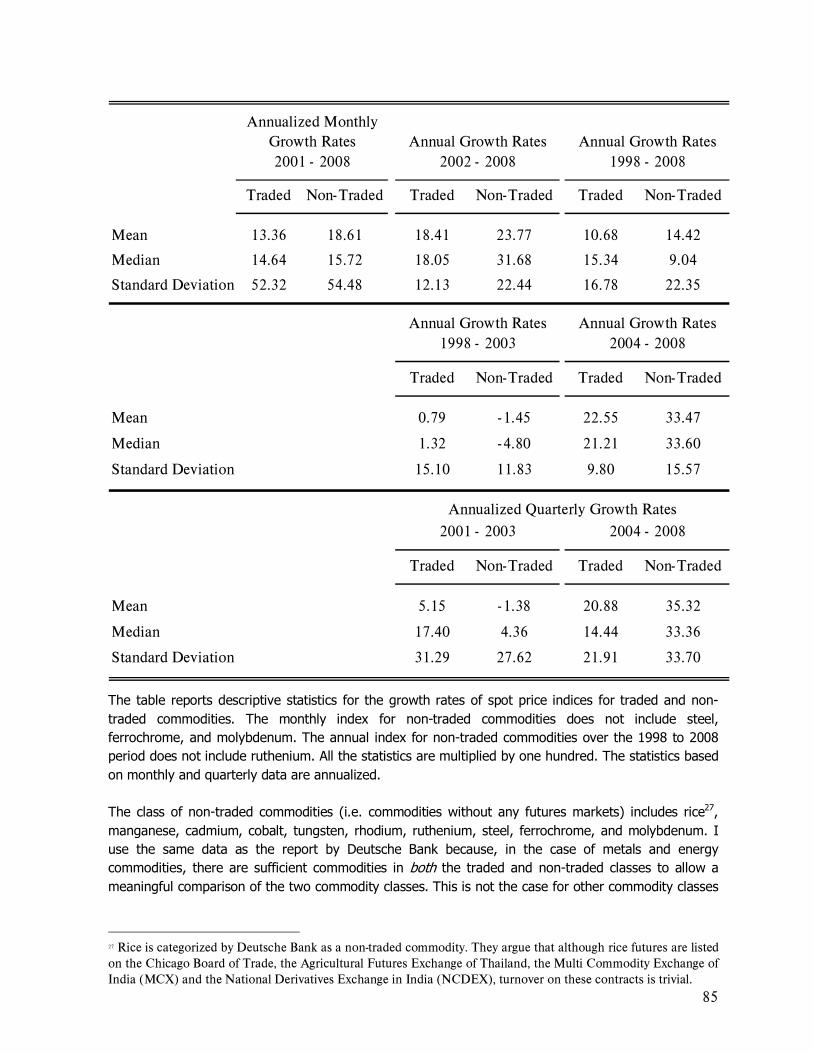

1

Interagency Task Force on Commodity Markets Special Report on Commodity Markets

I. Introduction

II. Executive Summary

III. Commodity Markets

A. Globalization of Commodity Markets and Trading Commodities trading originated in a simpler market environment, wherein a producer � a farmer, for instance � would bring his or her commodity to a local marketplace in order to sell the product to willing buyers. Historically, the prices of commodities were determined by comparatively simpler and more geographically circumscribed supply and demand factors. For example, the prices of grains in a given country were determined principally by local crop yields (i.e., supply) and demand conditions that were a reflection of more limited local, regional, or national needs. Moreover, commodities trading was largely limited to and conducted by producers and users of the commodities, or through their agents. The trading of commodities was a more straightforward affair, and it was a less complicated task to determine prices and identify the underlying causes of swings in the prices of commodities. Today, this is no longer the case. It was the inevitability of commodity price volatility that led to the development of forward markets and futures markets, which enabled producers and users of commodities to manage and transfer the price risks they faced through the use of forward agreements and futures contracts, respectively. The oldest futures exchange that still exists today is the Chicago Board of Trade (CBOT)1, which was established in 1848 and which originally traded contracts on a few agricultural commodities such as wheat, corn, and soybeans. One effect of the advent of futures exchanges was to bring together producers and consumers from more dispersed locations who previously might not have traded together. Though prices of traded commodities still depended on fundamental supply and demand factors, because the markets were less localized, events that occurred farther from the marketplace began to have an effect. In addition, though principally still a market where producers and users came together, the CBOT and other futures markets soon attracted other traders who did not have a direct connection to or use for the commodities they traded. Through their ability and willingness to assume risk, these speculative traders brought additional liquidity and risk transference to the markets. The commodity market model founded by the CBOT and other early exchanges spread, and futures exchanges were established in other major US and international economic centers, trading a wider array of commodity contracts. As economies expanded, so did the need for centralized and efficient marketplaces for trading of commodities and transferring risk. Though futures exchanges were able to attract commodity producers and users from farther afield, the act of trading commodities remained largely a local occupation due to the fact that trading was conducted on a physical �floor� of the exchange by brokers and other traders.

1 The CBOT, together with the Chicago Mercantile Exchange, is today a subsidiary of the CME Group.

2

Up until the 1970s, only so-called �physical� commodities � principally agricultural products and a few metals � were traded on commodity markets. In the United States between 1936 and 1974, the Commodity Exchange Act (CEA) � the federal statute that today still governs commodity futures and options trading in the U.S. � permitted futures exchanges to trade contracts only on agricultural commodities that were specifically enumerated in the Act. In 1974, however, the Commodity Futures Trading Commission Act (CFTC Act) amended the CEA to permit the trading of �contracts for the sale of a commodity for future delivery� and options on such contracts, not only on agricultural commodities, but on all commodities.2 In fact, the CFTC Act also established the Commodity Futures Trading Commission (CFTC) as a new independent regulator for commodity and futures markets. In 1975, the CFTC approved the first futures contracts on non-agricultural commodities.3 The introduction of financial products into the commodity markets not only expanded the types of entities participating in the markets � including banks, insurance companies, and other financial institutions and corporations � but also opened the door for the transformation of commodity markets into something closer to financial markets. In the 1980s and 1990s, further transformation of commodity markets occurred with the advent of electronic trading and other technological innovations that allowed trading to take place away from a physical trading floor. With electronic trading, it became technologically feasible for traders to trade in markets in another region or country. Globalization of commodity trading had arrived. Despite the potential for global commodities trading, regulatory barriers in place in various countries did not readily permit the cross-border trading of commodities. Such regulatory barriers were first to fall in the European Union, which in the 1990s saw a flurry of mergers between previously stand-alone national commodities markets. With increased cross-border activity, it became apparent to exchanges and policymakers in the U.S. that the regulatory structure needed to better enable U.S. commodity markets to compete globally. The Commodity Futures Modernization Act of 2000 (CFMA) streamlined regulatory requirements for exchanges and explicitly clarified the legal uncertainty surrounding the trading of over-the-counter (OTC) derivatives and swaps transactions. In addition, since passage of the CFMA, U.S. commodity markets have been opened gradually to foreign traders and exchanges. Today, in reflection of the global nature of the world economy, commodities markets are truly global markets. Futures, options, and derivatives markets exist in numerous countries in Europe, Asia, Latin America, and the Middle East, and more appear every year, all of them competing for trading volume and liquidity. Although some commodity contracts traded by some exchanges constitute more of a �local� market, the markets for many commodities � including financial commodities, metals, and energy products, including oil � are global markets where trading occurs around the clock by users and traders all over the world. Further, commodity markets have continued to attract a growing array of

2 The CEA defines �commodity� as including an enumerated list of agricultural commodities (e.g., �wheat, cotton, rice, corn, � wool, � fats and oils, � livestock products, ��), plus �all other goods and articles, except onions �, and all services, rights, and interests in which contracts for future delivery are presently or in the future dealt in.� 3 The first financial futures approved by the CFTC included the CBOT�s futures contract on Government National Mortgage Association (Ginnie Mae) certificates, and the Chicago Mercantile Exchange�s futures contract on 90-day U.S. Treasury bills.

3

market participants from around the world � for example, financial investors such as hedge funds, pension funds, and sovereign wealth funds � who increasingly perceive commodities as a separate and diversifying asset class. Prices in commodity markets today continue to reflect supply and demand fundamentals. The difference between today�s global markets and the more localized markets of the past, however, is that those supply and demand fundamentals are more complex. Physical supply and physical aggregate demand without question remain powerful forces on commodity prices, but increasingly supply and demand are globally determined, reflecting a multitude of current and expected factors: geopolitical considerations; increasing demand from China, India, and other emerging economies; national policies on commodity use (e.g., ethanol and biodiesel directives in the U.S. and E.U.) and price subsidization; the use of commodities as a diversifying asset class; and a host of macroeconomic influences including exchange rates, interest rates, commodity price linkages, cost-push and substitution effects. These global factors interact in a complex way to influence commodity prices. Consequently, it sometimes is an increasingly daunting challenge to identify the underlying causes of price changes and volatility.

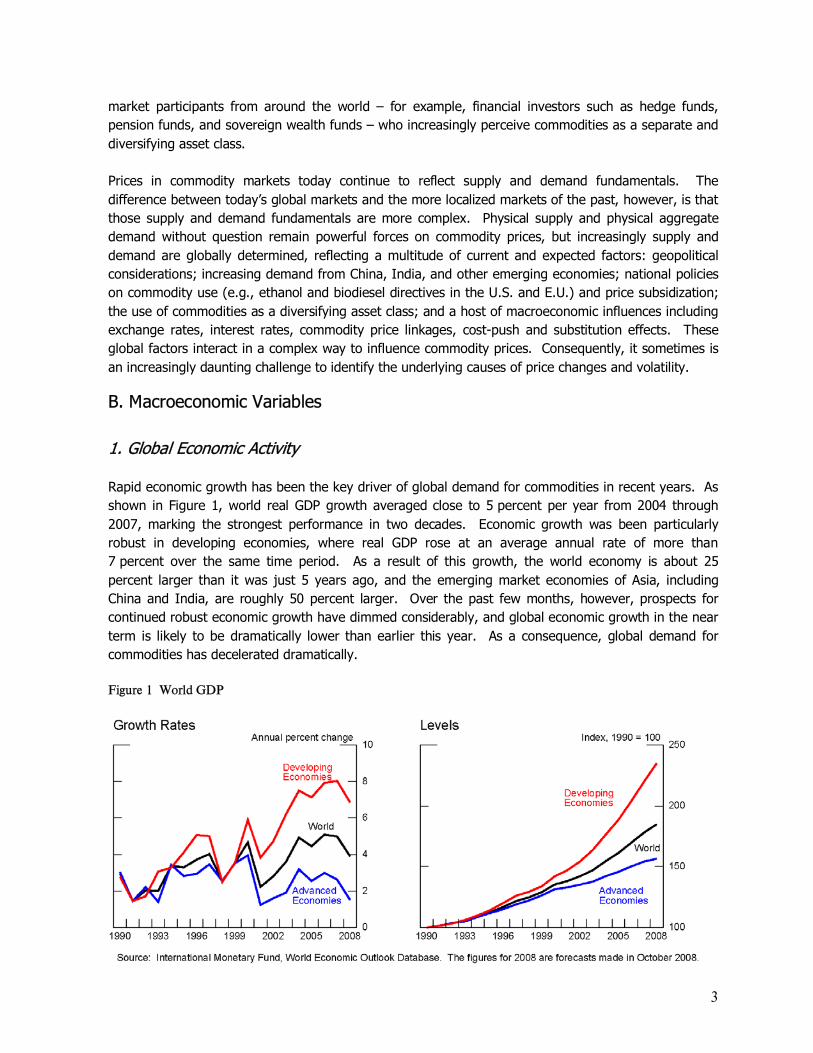

B. Macroeconomic Variables 1. Global Economic Activity Rapid economic growth has been the key driver of global demand for commodities in recent years. As shown in Figure 1, world real GDP growth averaged close to 5 percent per year from 2004 through 2007, marking the strongest performance in two decades. Economic growth was been particularly robust in developing economies, where real GDP rose at an average annual rate of more than 7 percent over the same time period. As a result of this growth, the world economy is about 25 percent larger than it was just 5 years ago, and the emerging market economies of Asia, including China and India, are roughly 50 percent larger. Over the past few months, however, prospects for continued robust economic growth have dimmed considerably, and global economic growth in the near term is likely to be dramatically lower than earlier this year. As a consequence, global demand for commodities has decelerated dramatically. Figure 1 World GDP

4

In addition to the pace of world economic activity, demand for commodities has been further supported in recent years by the composition of growth across countries. As shown in Figure 2, China, India, and the Middle East use substantially more oil and steel to produce a dollar�s worth of real output than the United States. These economies have been among the fastest growing in the world; together they have accounted for about two-thirds of the rise in global use of oil and steel since 2004. Moreover, these economies� use of commodities is still relatively low on a per capita basis, as shown in Figure 3. Over the longer term, as these economies continue to develop and incomes rise, per capita commodity use is likely to increase further. Figure 2 Commodity Intensity

Figure 3 Per Capita Commodity Use

2. Exchange Rates The relationship between exchange rates and commodity prices is complex, and the causality can run in both directions. Typically, a depreciation of the dollar would be expected to lead to a rise in the

5

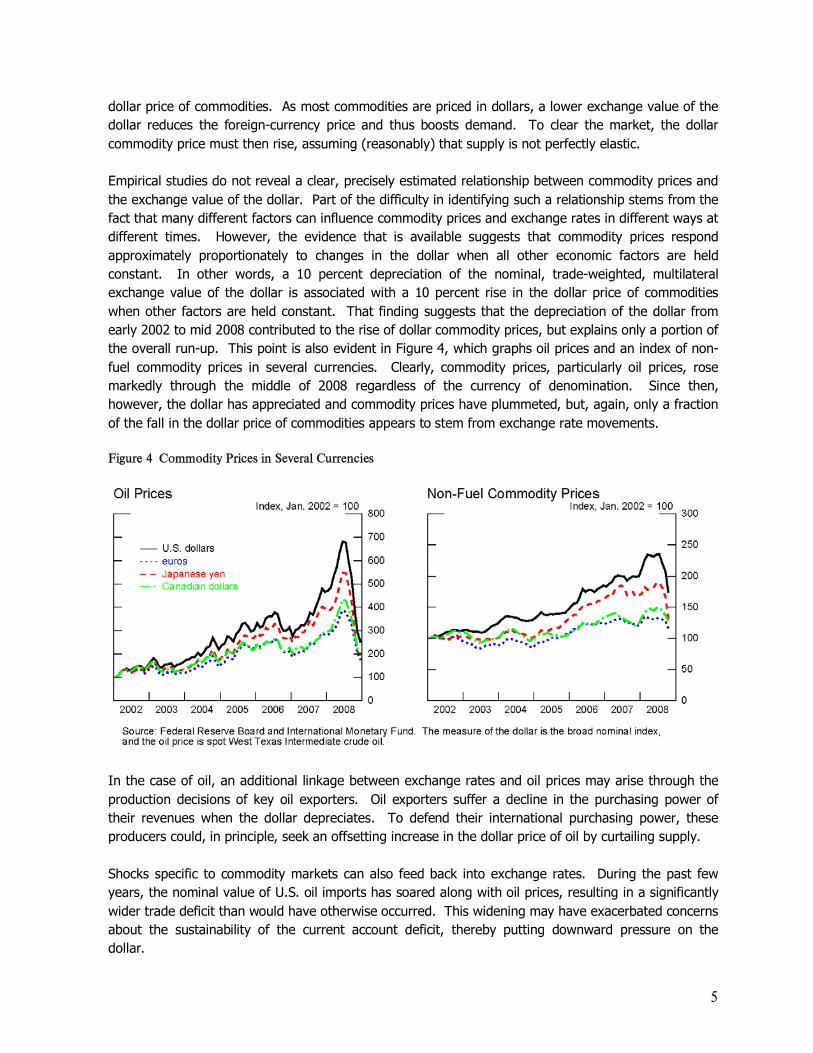

dollar price of commodities. As most commodities are priced in dollars, a lower exchange value of the dollar reduces the foreign-currency price and thus boosts demand. To clear the market, the dollar commodity price must then rise, assuming (reasonably) that supply is not perfectly elastic. Empirical studies do not reveal a clear, precisely estimated relationship between commodity prices and the exchange value of the dollar. Part of the difficulty in identifying such a relationship stems from the fact that many different factors can influence commodity prices and exchange rates in different ways at different times. However, the evidence that is available suggests that commodity prices respond approximately proportionately to changes in the dollar when all other economic factors are held constant. In other words, a 10 percent depreciation of the nominal, trade-weighted, multilateral exchange value of the dollar is associated with a 10 percent rise in the dollar price of commodities when other factors are held constant. That finding suggests that the depreciation of the dollar from early 2002 to mid 2008 contributed to the rise of dollar commodity prices, but explains only a portion of the overall run-up. This point is also evident in Figure 4, which graphs oil prices and an index of non-fuel commodity prices in several currencies. Clearly, commodity prices, particularly oil prices, rose markedly through the middle of 2008 regardless of the currency of denomination. Since then, however, the dollar has appreciated and commodity prices have plummeted, but, again, only a fraction of the fall in the dollar price of commodities appears to stem from exchange rate movements. Figure 4 Commodity Prices in Several Currencies

In the case of oil, an additional linkage between exchange rates and oil prices may arise through the production decisions of key oil exporters. Oil exporters suffer a decline in the purchasing power of their revenues when the dollar depreciates. To defend their international purchasing power, these producers could, in principle, seek an offsetting increase in the dollar price of oil by curtailing supply. Shocks specific to commodity markets can also feed back into exchange rates. During the past few years, the nominal value of U.S. oil imports has soared along with oil prices, resulting in a significantly wider trade deficit than would have otherwise occurred. This widening may have exacerbated concerns about the sustainability of the current account deficit, thereby putting downward pressure on the dollar.

6

3. Interest Rates The relationship between interest rates and commodity prices can vary, as it depends on the interactions of many economic variables. As noted below, a decline in interest rates by itself might be expected to raise commodity prices to some extent, suggesting a negative correlation between these two variables. But if the decline in interest rates is in reaction to a downturn in economic activity, commodity prices may very well fall in response to that weaker demand, resulting in a positive correlation. One mechanism by which declines in interest rates could push up commodity prices is through a reduction in the costs associated with storing commodities. An implication of this hypothesis is that inventories of commodities should tend to rise when interest rates decline. Such increases, however, are not evident in the available data. 4. Prices and Expectations Commodities are traded in global markets that are generally deep and liquid. Commodity prices adjust through markets to equilibrate the amounts supplied and demanded. For some commodities, such as oil, corn and wheat, the quantity consumed changes only modestly in response to price movements; that is, demand is relatively inelastic in the short run. For other commodities the quantity consumed changes more dramatically in response to price movements; demand is relatively elastic. The elasticity of demand for a commodity or good reflects the importance of the commodity to consumers and the availability of substitutes. For example, there are few substitutes for oil, especially for use in transportation. Demand for most goods is more elastic in the long run, as persistent high prices lead consumers and firms to make permanent changes to reduce the quantity used. The change in the quantity of a commodity produced in response to changes in price defines the elasticity of supply. Many agricultural commodities are thought to have inelastic short run supply because of growing seasons and lags in adjustment, but much more elastic long run supply. Oil producers often have more scope than consumers to respond to price changes, although at present the ability to adjust output in the near-term appears to be limited. The elasticity of demand and supply will determine the degree to which changes in supply and demand result in changes in quantity and changes in price. Goods with inelastic short run (one to two years) supply and demand � like many commodities - are likely to experience large swings in price in response to changes in supply or demand. Many of the commodities discussed in this report � most notably oil � are exhaustible resources. Oil is an exhaustible resource with a natural, inexpensive storage solution. This leads owners of oil reserves to base output decisions on both current prices and expectations of future prices. In particular, the pace at which they extract oil will depend on expectations about future prices relative to the risk-adjusted rate of return on other investments. Producers will supply less oil today and instead keep it in the ground if its price is expected to rise in the future by more than the expected return on other investments. Producers will pump more oil when the price is expected to fall (or rise at a rate slower than the return on other investments). Because today�s oil prices reflect expectations about future supply and demand, they can move considerably in response to events or changes in market

7

perceptions about future supplies, even if the events have little apparent connection with the supply or demand for oil today.

C. Instruments and Investors in Commodity Markets For much of the history of derivatives markets in the U.S., trading was primarily limited to hedgers and individual speculators trading on futures exchanges. This situation began to change in the 1980s when financial engineers developed the swap contract, giving hedgers and speculators an alternative to the exchange-traded futures contract to manage or acquire commodity price risks. More recently, commodity index funds, and exchange-traded funds and notes have been created that also allow portfolio managers and individuals to efficiently gain price exposures to individual commodities and commodity indexes through an alternative means to the futures markets. 1. Over-the-Counter Swap Contracts The development of the swap contract began in 1981 when the World Bank and IBM entered into what became known as a currency swap. The swap essentially involved a loan of Swiss francs by IBM to the World Bank and the loaning of U.S. dollars by the World Bank to IBM. The motivation for the transaction was the ability of each party to borrow the funds more cheaply than the counterparty, thereby reducing overall funding costs for both parties. This structure of swapping cash flows ultimately served as the template for swaps on any number of financial assets and commodities. Although currency swaps initially served a lending function, the development of swaps that exchange a fixed rate for a floating rate were found to serve as an effective hedging vehicle in much the same was that futures contracts do. For example, a futures contract is essentially a contract for the buyer of the contract to pay a fixed price in return for receiving delivery of a commodity that will have an uncertain or floating value. The advantage that swaps contracts offered, however, was the flexibility with which counterparties could tailor the terms of the contract to meet their hedging needs. For example, an airline wanting to hedge future jet fuel purchases cannot directly do so with a futures contract since none exists. Such hedging would have to be done as a cross hedge using crude oil, gasoline or heating oil futures. The swap market offers the airline the alternative of entering in to a swap contract that would directly reference a cash price for jet fuel. In addition to permitting the tailoring of contract terms to match such specifications as commodity, grades, and delivery timing and locations, swaps also allow counterparties to execute large positions that might overwhelm liquidity in a market. Thus, a hedger or speculator seeking a commodity exposure can obtain price certainty when negotiating a contract. The party offering the swap, typically a swap dealer, would take on any price risks associated with managing the risk of the commodity exposure. In the early development of swaps markets, investment banks often served in a brokering capacity to bring together parties with opposite hedging needs. The currency swap between the World Bank and IBM was brokered by Solomon Brothers. While brokering swaps eliminates market and credit risk to the broker, the process of matching and negotiating swaps between counterparties with opposite hedging needs could be difficult. As a result, swaps brokers, who took on no market risk, evolved into swaps dealers, who took the contract onto their books. This, of course, exposed the dealer to the risks

8

associated with commodity price movements. However, since a swap dealer is willing to enter into a swap contract on either side of a market, at times they will enter into swaps that create offsetting exposures. Since it is unlikely that a dealer at all times could completely offset the market risks associated with its swap business, dealers will often enter the futures markets to offset the residual market risk. As a result of the growth of the swaps market and the dealers who support the market, we have seen an associated growth in the futures markets related to the commodities for which swaps are offered.

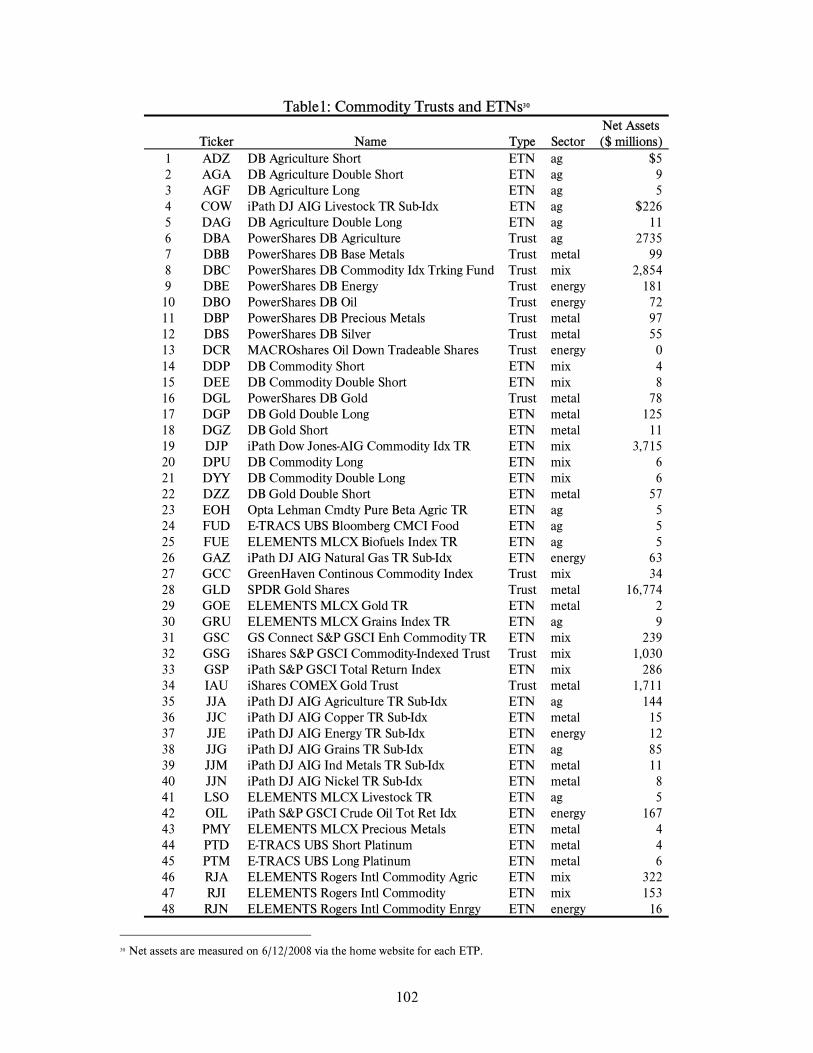

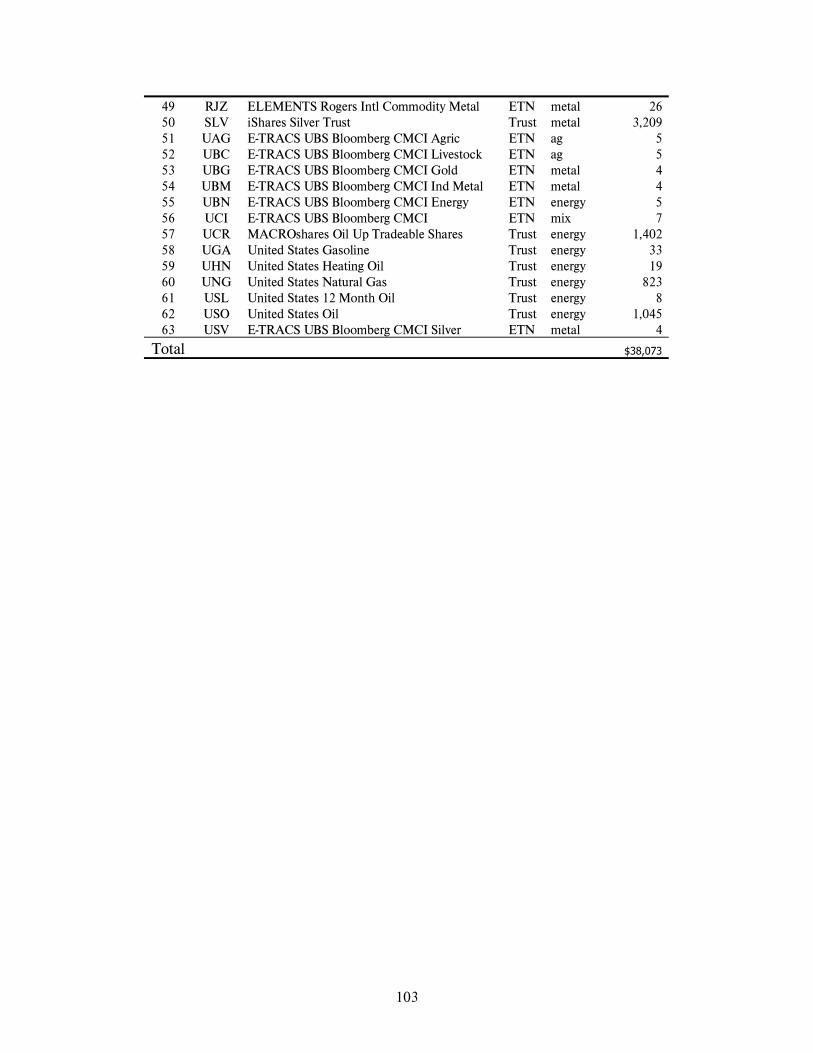

2. Exchange-Traded Products Commodity exchange-traded products, or ETPs, refer to exchange-traded investment vehicles that offer investors exposure to a range of individual commodities, derivatives on commodities, and commodity indexes. The main types of commodity ETPs are commodity trust shares and commodity-linked notes (ETNs). Commodity trusts hold physical commodities or derivatives on these commodities and the investments are held in trust for the benefit of shareholders. Shares in the trust can be bought and sold throughout the day like stocks on a securities exchange through a broker-dealer. The shares of the trust should trade at approximately the same price as the net asset value of its underlying assets over the course of the trading day. If a commodity trust were liquidated, investors would receive their share of the underlying trust assets. Originally marketed as a tool for investors to participate in tradable portfolio or basket products, shares in commodity trusts are held today in large amounts by institutional investors, including mutual funds, and other investors as part of sophisticated trading and hedging strategies. Investors may short sell commodity trusts in the same manner that shares of stock can be sold short. Although commodity trust shares resemble exchanged-traded fund (ETF) shares, there is an important legal distinction between the two. Commodity trust shares are registered by the SEC under the Securities Act of 1933 whereas ETFs are also registered as investment companies under the Investments Company Act of 1940 (�1940 Act�). As such, commodity trusts are not subject to the same regulation of operations that applies to registered investment companies under the 1940 Act. Commodity-linked exchange-traded notes (ETNs) are senior, unsecured, unsubordinated debt securities issued by an underwriting bank or other large issuer. The issuer of the commodity ETN promises to pay a specified return, often linked to the performance of an underlying commodity derivative or commodity index minus an expense ratio. ETNs share both equity and debt attributes. ETNs have a maturity date and are backed only by the credit of the issuer. If investors hold the ETN to maturity, they will receive a cash payment that is linked to the performance beginning on the trade date and ending at maturity. In the event of default, ETN investors would receive their funds only if there was money left over after the secured creditors were paid. ETNs may be bought and held or else sold before maturity by trading them on the exchange. The additional risk of an ETN versus a commodity trust lies in the credit risk of the issuer. The issuer may suffer a decline in its credit rating or the underwriting bank could go bankrupt, adversely affecting the value of the ETN. ETNs do not accrue or pay out interest, unlike traditional debt securities. Investors may short sell ETNs. ETNs are regulated by the SEC under the 1933 Securities Act.

9

Investors can also gain exposure to commodities through three other types of investments: commodity-linked medium term notes, commodity index-linked mutual funds, and commodity index assets under management attributable to institutional investors. Commodity-linked medium term notes (MTNs) are structured products that involve a pre-packaged investment strategy that is based on derivatives, a basket of securities, commodities, or some other underlying security. Commodity-linked MTNs are primarily structures linked to commodity indices and may be associated with agriculture, metals, or other commodities. Commodity index assets under management are based on baskets of commodity futures which replicate the buying of a forward position that is continuously rolled forward in time. The positions are long only and there is no physical ownership of the underlying inventory. A 2008 study conducted by researchers at Barclays4 estimates a total value of $225 billion invested across the various commodity products. They give a breakdown as follows: $46 billion attributed to ETPs, $40 billion for MTNs, $17 billion for index-linked mutual funds, and $122 billion in index assets under management. 3. Commodity Index Funds A more recent development in the derivative market has been the development of commodity index funds. While investors have for years been able to invest in commodity pools, which pooled investors� funds to trade commodities much like mutual funds do for investors in stocks and bonds, commodity index funds offer investors the opportunity to gain a passive exposure to a specified index of commodities. That is, while a pool operator seeks to profit by following a trading strategy that may buy or sell a variety of commodities, the operator of commodity index fund seeks to match a pre-specified index through the acquisition of long futures positions.5 The major attraction of these funds are that they are believed to give investors a commodity exposure that is largely independent or even negatively correlated with the returns on stocks and bonds, and they eliminate margin calls against customers by entering into only long positions and trading on an unleveraged basis. Thus, a pension fund or other portfolio manager can theoretically smooth out the returns of a portfolio by including a commodity index position in the portfolio. Smaller retail investors have also embraced commodity index funds as a cost effective way of investing in a diverse basket of commodities. Moreover, because the funds only enter into long positions and have collected the full price for the commodity positions that they enter into, the risk of margin calls, which would be associated with a futures position, is eliminated.

4. CFTC Special Calls Report To better understand how swaps dealers and index traders use the futures markets to manage their risks, in June 2008, the CFTC issued a special call to swaps dealers and commodity index traders, which included 43 request letters issued to 32 entities and their sub-entities. These entities include

4 Cooper, S., K. Norrish, and A. Sen, July/August 2008, �Piercing the Fog: Facts and Fallacies about Commodity Investment Flows,� Futures Industry. 5 Theoretically an index could include short market positions, however, to date commodity index funds have primarily limited themselves to long positions. Moreover, the funds limit leverage to their customers by limiting the notional value of the fund to the amount of funds collected from its customers.

10

swap dealers engaged in commodity index business, other large swap dealers, and commodity index funds. The special call required all entities to provide data relating to their total activity in the futures and OTC markets, and to categorize the activities of their customers for month-end dates beginning December 31, 2007 through June 30, 2008, and continuing thereafter. On September 11, 2008, the CFTC issued a staff report that summarized the preliminary analysis of data collected through the special calls. The preliminary survey results represent the best data currently available to the staff and the results present the best available snapshot of swap dealers and commodity index traders for the relevant time period.6 In analyzing the total OTC and on-exchange positions for index trading, the report focuses on three quarterly snapshots � December 31, 2007, March 31, 2008, and June 30, 2008 - and has thus far revealed the following: Firstly, the estimated aggregate net amount of all commodity index trading (combined OTC and on-exchange activity) on June 30, 2008 was $200 billion, of which $161 billion was tied to commodities traded on U.S. markets regulated by the CFTC. Of the $161 billion combined total, a significant amount of the OTC portion of that total likely is never brought to the U.S. futures markets. For comparison purposes, the total notional value on June 30, 2008 of all futures and options open contracts for the 33 U.S. exchange-traded markets that are included in major commodity indexes was $945 billion � the $161 billion net notional index value was approximately 17 percent of this total. Secondly, the staff report also presented index trading data for some individual commodities. The total notional value of futures and options open contracts on June 30, 2008 for NYMEX crude oil was $405 billion � the $51 billion net notional index value was approximately 13 percent of this total. The total notional value of futures and options open contracts on June 30, 2008 for CBOT wheat was $19 billion � the $9 billion net notional index value was approximately 47 percent of this total. The total notional value of futures and options open contracts on June 30, 2008 for CBOT corn was $74 billion - the $13 billion net notional index value was approximately 18 percent of this total. The total notional value of futures and options open contracts on June 30, 2008 for ICE-Futures US cotton was $13 billion � the $3 billion net notional index value was approximately 23 percent of this total. Finally, according to the report, of the total net notional value of funds invested in commodity indexes on June 30, 2008, approximately 24 percent was held by �Index Funds,� 42 percent by �Institutional Investors,� 9 percent by �Sovereign Wealth Funds,� and 25 percent by �Other� traders.

D. The Role of Commodity Futures Markets 1. Futures Contract Design

6 As a result of the survey limitations, there may be a margin of error in the precision of the data, which will improve as the staff continues to work with the relevant firms and to further review and refine the data. As entities continue to provide monthly data to the Commission in response to their ongoing obligation to comply with the special call, Commission staff will continue to examine the data, refine the specific requests, and further develop the analysis.

11

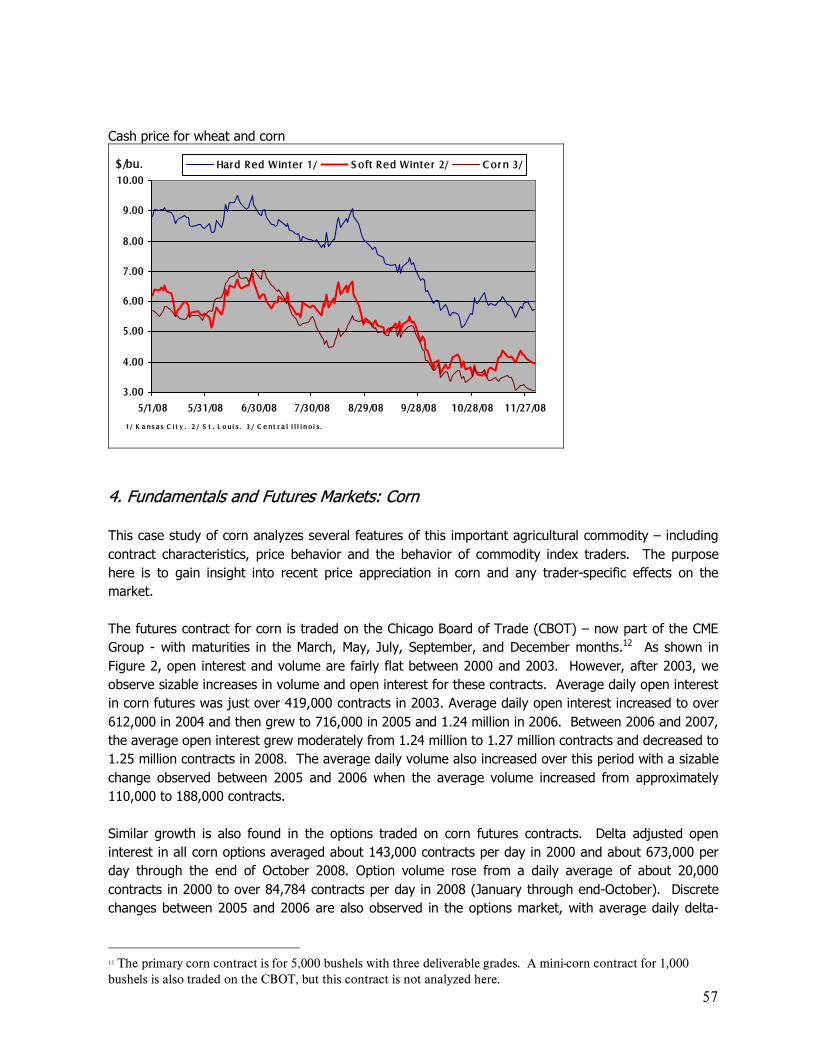

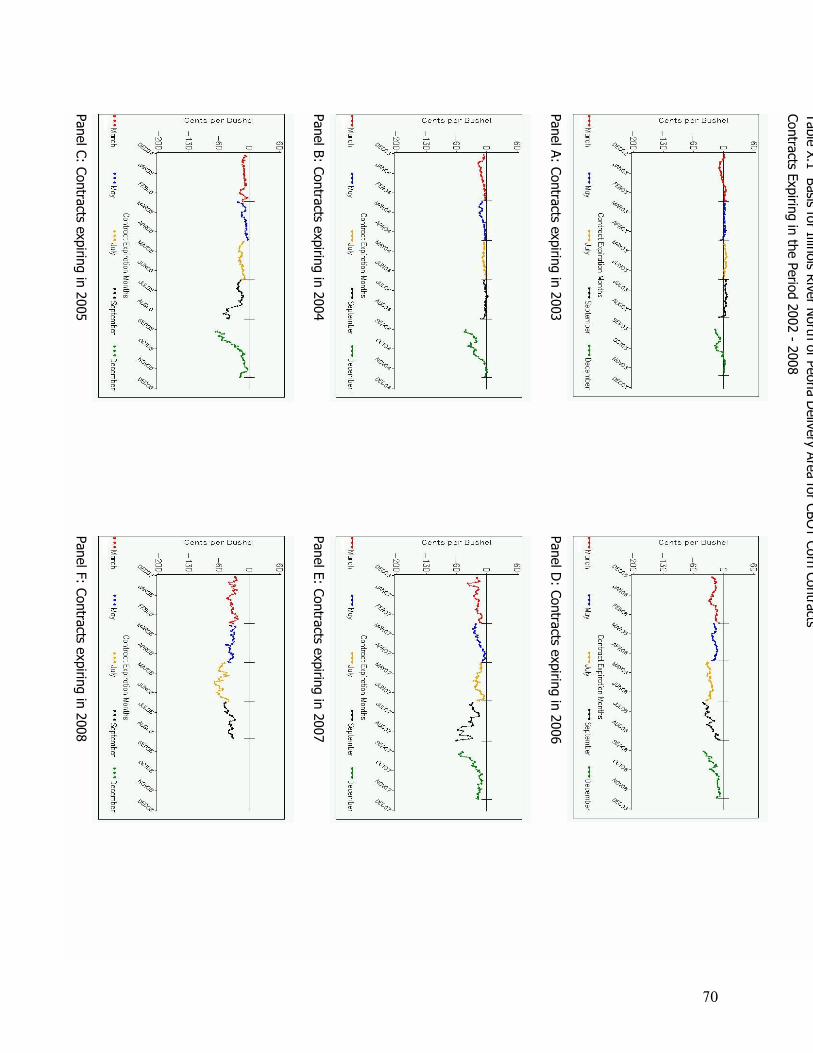

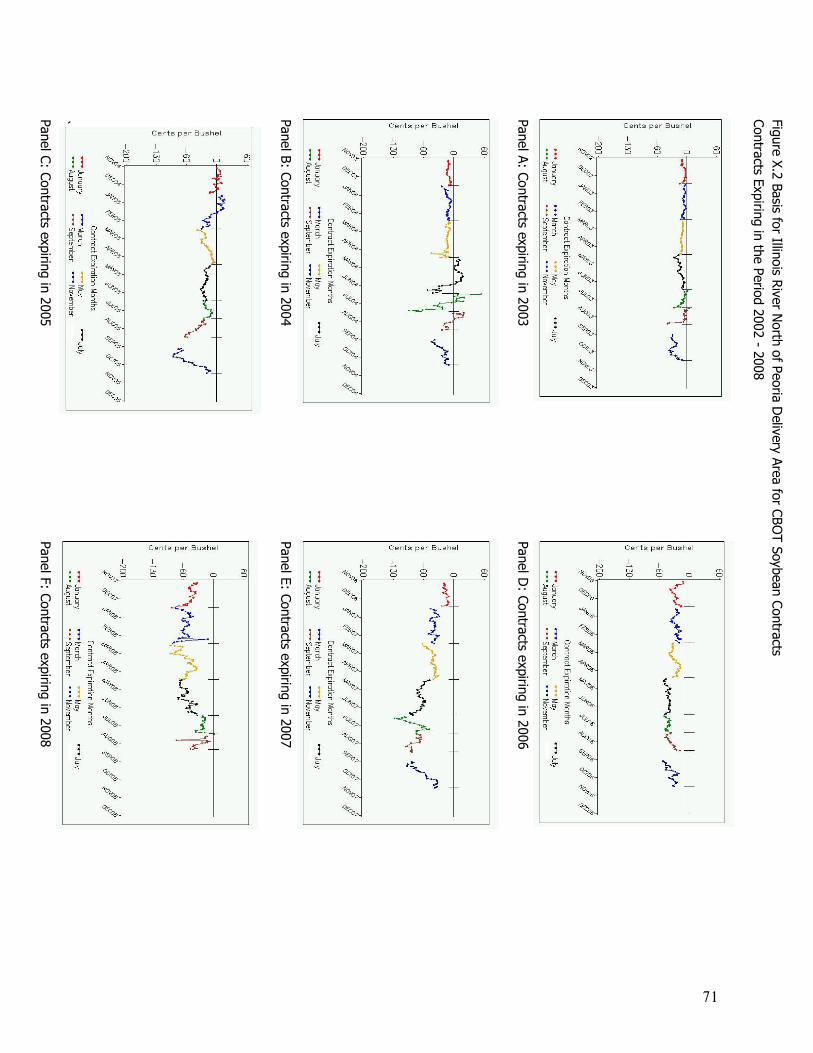

A futures contract is an agreement between two parties to buy and sell a given amount of a commodity at an agreed upon date in the future, at an agreed upon price and at a given location. For example, the Chicago Board of Trade (CBOT) December 2008 corn contract is an agreement to deliver 5,000 bushels of No. 2 yellow corn via a shipping certificate within the Chicago and Burns Harbor, Indiana shipping districts along the Illinois waterway during the first half of December 2008. Similar scenarios hold true for the CBOT�s soybean and wheat contracts. In this regard, the CBOT November 2008 soybean contract calls for the transfer of 5,000 bushels of No. 2 yellow soybeans via a shipping certificate at the same delivery points as for corn during the first half of the contract month. The CBOT wheat contract calls for the delivery of 5,000 bushels of No. 2 soft red winter, No. 2 hard red winter, No. 2 dark northern spring, and No. 2 northern spring wheat using a shipping certificate at either the Chicago; Burns Harbor, Indiana; or Toledo, Ohio; shipping districts. In the case of crude oil, the New York Mercantile Exchange (NYMEX) West Texas Intermediate (WTI) December 2008 oil contract is an agreement to physically deliver 1,000 barrels (42,000 gallons) of oil at Cushing, Oklahoma during the contract month. For all futures contracts, the buyer (or long trader) and the seller (or short trader) agree to a price when they enter into the contract. Unless offset, these contracts require their counterparties to deliver or to take physical delivery of a commodity.7 A party whose contract remains open at its expiration date is obligated to make or take delivery as promised. Futures contracts are standardized so as to facilitate trading between buyers and sellers. The characteristics of a contract specify common commodity grades and quantities that are typically seen in the cash market transactions. The specificity of deliverable grades varies across futures contracts. In general, futures contracts specify deliverable grades that are commonly traded in the cash market. However, the number of deliverable graded varies from contract to contract. This feature is particularly true for agricultural futures contracts. In this regard, weather and disease play important roles in crop development. Adverse growing conditions may reduce the availability of the par grade, thus making delivery difficult. In contrast, favorable conditions may produce and overabundance of higher grades. Crop futures assume average growing conditions. Thus, the futures contracts specify average commodity grades, which reflect crop quality that is realized by most farmers in most crop years. In order to account for the effect of adverse or favorable weather conditions on crop quality, crop futures contracts allow the delivery of additional grades at a premium or discount. For example, lower grades of corn, such as No. 3 yellow corn, are deliverable on the CBOT corn contract at a discount of 1.5 cents per bushel. Dominant futures contracts within a specific group typically are listed on a single exchange. In this regard, livestock products are listed on the Chicago Mercantile Exchange (CME), energy contracts are listed on the NYMEX, and row crop futures are listed on the CBOT. Exceptions do exist, particularly if a similar contract listed by another exchange specifies a different variety or grade of the same underlying commodity. For example, while the CBOT offers the dominant wheat contract, the Minneapolis Grain Exchange and Kansas City Board of Trade both offer their own wheat contracts. The MGE contract specifies No. 2 northern spring wheat, while the KCBT contract calls for the delivery of No. 2 hard red winter wheat. Contract terms and conditions, such as delivery and storage procedures, reflect standard industry practices. While a given futures contract�s terms and conditions mirror common characteristics associated with cash market transactions, futures contracts� terms and conditions generally are not

7 Not all futures contracts require physical delivery.

12

standard across contracts. For example, delivery requirements can vary greatly. The NYMEX crude oil contract requires that the seller physically transfer the crude oil to the buyer in Cushing during the contract month. In contrast, the CBOT corn, soybeans, and wheat futures contracts are physically settled contracts which deliver the commodity to the buyer in the form of a shipping certificate. The delivery instrument (shipping certificate) gives the buyer the right but not the obligation to demand load-out of the commodity whenever desired. The regular firm approved for delivery who issued the shipping certificated loads out the commodity within the timeline mandated by the exchange rules. The shipping certificate represents a claim to a commodity without binding the owner to a specific stock in a specific location. Shipping certificates offer the owner flexibility since there are no timelines in which one must convert the certificate into the physical commodity. During the time an owner holds the certificate he incurs opportunity cost and a set storage cost that must be paid to the regular firm. Additional shipping certificates (SC) features include the holder�s ability to sell the certificate in the cash market, sell it back to the issuing firm, or redeliver the certificate against an expiring short position. 2. Risk Management and Price Discovery Because futures contracts are standardized futures markets are ideal for aggregating a multiplicity of opinions regarding the expected price of a commodity at different points in time in the future. It is often easier for a common view on an expected price to emerge at a futures exchange than among dispersed producers and consumers of a physical (cash) commodity. For that reason, futures markets are an important source of price information - prices are often said to be �discovered� in futures markets and then communicated to participants in certain cash markets. The price discovery function of futures markets is extremely valuable in terms of planning business activities and for allocating commodity price risk. Futures contracts are instruments primarily designed to manage risk - they are identical in all aspects except for the contracted price; they trade on exchanges; and clear through designated clearinghouses. Exchange trading may occur either electronically or on the floor through open outcry; many times electronic and floor trading are conducted simultaneously. For crude oil and each of the row crops, the primary futures contract is physically delivered. Energy traders tend to have a greater array of choices with respect to contracts that are usable for risk management purposes. Besides the dominant physically-delivered contracts, energy traders can take advantage of cash-settled futures, mini-sized contracts, and basis contracts. In contrast, nearly all crop futures are physically delivery. The MGE does offer for trading cash settled corn, soybeans, and wheat contracts based on national index prices. However, none of these MGE contracts achieved significant trading volume since their introduction in early- and mid-2000. Due to their standardization, futures contracts are not so well-suited to allocate the physical commodity. For example, to mainly serve an allocation role, crude oil futures contracts in particular would feature multiple delivery locations. In fact, the figure below shows, only a small number of oil futures contracts result in physical delivery. Similarly, even though some futures contracts, such as those for corn and soybeans, specify a multiplicity of delivery points, the multiple delivery points are intended to facilitate delivery on the contract for the purpose of attaining better convergence between cash and futures prices rather than facilitating the use of the contracts as merchandizing vehicles.

13

3. Hedging and Speculation The distinction between hedging and speculation in futures markets is less clear than it may appear. Traditionally, those with a commercial interest in or an exposure to a physical commodity have been called hedgers, while those without a physical position to offset have been called speculators. In practice, however, hedgers may be �taking a view� on the price of a commodity, and even those who are not participating in the futures market despite having an exposure to the commodity could be considered speculating. Traditional speculators enter into futures contracts with the intention of reversing their positions before they would be required to deliver (short positions) or to accept physical delivery (long positions) of a commodity. As such, speculators serve important market functions � immediacy of execution, liquidity, and information aggregation. Traditional speculators could further be differentiated depending on the time horizons at which they operate. Speculators, known as scalpers or market makers, operate at the shortest time horizon � sometimes trading within a single second. These traders typically do not trade with a view as to where prices are going. Instead, they provide immediacy of execution to a trade. That is, they �make markets� by standing ready to buy or sell at a moment�s notice. These market makers will usually offset their positions soon after entering into them. The goal of a market maker is to buy contracts at a slightly lower price than the current market price and sell them at a slightly higher price, perhaps at only a fraction of a cent profit on each contract. By trading hundreds or even thousands of contacts a day, skilled market makers can earn a profit. The benefit provided by the market maker is the speed, or immediacy, at which a trader attempting to establish or offset a position in the market can do so. Absent a market maker, a market participant would have to wait until the arrival of another party with an opposite trading interest. Other types of speculators take longer-term positions based on their view of where prices may be headed. Speculators known as �day traders� establish positions based on their views of where prices might be moving in the next minutes or hours, while �trend followers� take positions based on price expectations over a period of days, weeks or months. Through their efforts to gather information on underlying commodities, the activity of these traders serves to bring information to the markets and aid in price discovery. These speculators are also important to the market in that they often supply overall liquidity to hedgers in futures market. While hedging and speculation are often considered opposite activities and are generally identified with commercial and non-commercial traders, in practice both commercial and non-commercial traders can bring about the price discovery in futures markets. In essence, futures prices are a reflection of the opinions of all those entering the market. Moreover, the actions of those who can, but choose not to enter the futures market are also quite important for price discovery. For example, a commercial trader holding physical inventory, but choosing not to hedge it in the futures market (by taking a short position) will not only withhold a downward pressure on the price, but may also send a signal that prices are expected to rise in the future. It is important to keep in mind that futures and option trading should be viewed in the context of an overarching risk management strategy. Futures trading may be only one means of hedging price risk. Market participants may be involved concurrently in OTC transactions, trades on exempt commercial

14

markets, and transaction in foreign markets. For example, crude oil traders can hedge cash market positions using a combination of futures, swaps, bilateral forward contracts, and cleared broker and ECM transactions. Grain traders can use a combination of forward and hedge-to-arrive contracts as well as exchange-traded futures and options, and agricultural swaps. Activities that occur in other markets and other instruments can also impact futures markets. There are three potential activities that might impact futures trading on U.S. exchanges: (i) the trading of over-the-counter (OTC) derivatives contracts ; (ii) the trading on exempt commercial markets; and (iii) the trading on foreign boards of trade.

4. Publicly Available Data on Futures Markets To provide the public with information on the activity of traders in the futures and options markets, the CFTC publishes a weekly Commitments of Traders (COT) report. The report is released every Friday at 3:30 p.m. Eastern time and contains a summary of trader�s positions as of the close of business on the previous Tuesday for each market in which 20 or more traders hold positions equal to or above the large trader reporting levels established by the CFTC.8 The summary of market activity contained in the weekly COT reports is available in a variety of formats�i.e., long and short format, as well as in futures-only and futures-and-options-combined format�and are available for no charge on the CFTC�s website. The long and short format reports show open interest separately by reportable and non-reportable positions. For reportable positions, additional data is provided for commercial and non-commercial holdings, spreading, changes from the previous report, percents of open interest by category, and numbers of traders. The long report also groups the data by crop year, where appropriate, and shows the concentration of position held by the largest four and eight traders. The CFTC, beginning in 2007, also publishes a Supplemental report for selected agricultural markets showing all the information in the short format report plus the positions of traders classified as Index Traders.9 The information regarding the reportable positions of traders contained in the COT reports is drawn from the reports the CFTC receives daily from clearing members, futures commission merchants, and foreign brokers. Those reports show the futures and option positions of traders that hold positions above specific reporting levels set by CFTC regulations. If, at the daily market close, a reporting firm has a trader with a position at or above the CFTC�s reporting level in any single futures month or option expiration, it reports that trader�s entire position in all futures and options expiration months in that commodity, regardless of size. The aggregate of all traders� positions reported to the CFTC usually represents 70 to 90 percent of the total open interest in any given market. From time to time, the CFTC will raise or lower the reporting levels in specific markets to strike a balance between collecting

8 Reporting levels can be found in section 15.03(b), 17 CFR15.03(b), of the CFTC�s regulations, and can be accessed from the CFTC�s website, www.cftc.gov 9 For more information on the CFTC�s Supplemental report see, �Commodity Futures Trading Commission: Commission Actions in Response to the �Comprehensive Review of the Commitments of Traders Reporting Program� (June 21, 2006),� available at the CFTC�s website, www.cftc.gov.

15

sufficient information to oversee the markets and minimizing the reporting burden on the futures industry. When an individual reportable trader is identified to the CFTC, the trader is classified either as �commercial� or �non-commercial.� All of a trader�s reported futures positions in a commodity are classified as commercial if the trader uses futures contracts in that particular commodity for hedging as defined in CFTC Regulation 1.3(z), 17 CFR 1.3(z). Generally this definition reflects a matching of a futures position with a commercial market risk and does not consider the motivation for entering into a hedge. A trading entity generally gets classified as a �commercial� trader by filing a statement with the CFTC, on CFTC Form 40: Statement of Reporting Trader, that it is commercially ��engaged in business activities hedged by the use of the futures or option markets.� To ensure that traders are classified with accuracy and consistency, CFTC staff may exercise judgment in re-classifying a trader if it has additional information about the trader�s use of the markets. A trader may be classified as a commercial trader in some commodities and as a non-commercial trader in other commodities. A single trading entity cannot be classified as both a commercial and non-commercial trader in the same commodity. Nonetheless, a multi-functional organization that has more than one trading entity may have each trading entity classified separately in a commodity. For example, a financial organization trading financial futures may have a banking entity whose positions are classified as commercial and have a separate money-management entity whose position are classified as non-commercial. In classifying traders as commercial or non-commercial rather than hedgers and non-hedgers, the CFTC recognizes that the ultimate motivations for trading futures by commercial and non-commercial traders cannot be observed. That is, while a commercial trader may be matching a futures position against a cash market price risk, it is not known whether such a trader is doing so on a routine basis in order to minimize ongoing price risks or doing so selectively based on specific market expectations. Thus, some of the trading information captured by the commercial trading category may reflect activity that could be characterized more as speculative rather than hedging.

IV. Select Commodity Markets: Fundamentals and Markets

A. Crude Oil

1. Background The recent, rapid crude oil price rise and fall represent an extension of oil market developments originating in the 1990s. At around that time, relatively high inventories and ample surplus production capacity served to limit oil price fluctuations. When spot market prices moved up or down, futures contracts requiring delivery in distant months generally traded close to $20 per barrel, consistent with a market expectation that producers would ensure that spot prices would eventually return to that level. However, as leading Organization of Petroleum Exporting Countries (OPEC) members shifted towards a tight inventory policy and global oil demand recovered from the slowing effect of Asia�s financial crisis, the global market balance tightened and inventories declined sharply at the beginning of the present decade. Oil prices rose to $30 per barrel in what might be seen as the first leg of the upward trend. By 2003, inventories were drawn down sufficiently such that subsequent increases in global demand stretched oil production to levels near capacity. The large, unexpected jump in world oil consumption

16

growth in 2004, fostered by strong growth in economic activity in Asia, reduced excess production capacity significantly. Into the first half of 2008, despite high prices, world oil consumption growth remained strong, overall non-OPEC production growth continued to slow, and OPEC oil production could not fill the gap. Geopolitical risks created considerable uncertainty about future supplies. Crude oil price declines since mid-July reflect an increasingly clear slowdown in oil consumption growth, higher recent Saudi Arabian oil production, and prospects of higher non-OPEC supplies through 2009. The resulting lower demand for OPEC oil, combined with planned increases in OPEC production capacity, now suggests OPEC surplus crude production capacity could increase to about 3 million barrels per day next year, providing the market with a cushion against supply disappointments and supporting lower oil prices than expected previously. Turmoil in U. S. financial markets point to lower global economic activity and weaker world oil consumption growth and has reinforced the sentiment of a loosening in the global oil balance. EIA�s November release of its Short Term Energy Outlook, reflected a considerable reduction in expected world oil prices for the second half of 2008, with moderate price growth through the first half of 2009. This forecast reflects the clear global downturn and its effects on demand for energy. EIA�s November Outlook recognizes OPEC�s intention to cut crude oil production starting November 1, in response to a perceived supply surplus in the market caused by slowing oil consumption growth and higher non-OPEC supply growth. The result is that the OPEC production cut may limit, but not reverse the recent sharp fall in oil prices.

2. Demand

a. Global Economic Activity

The key driver of oil demand has been robust global economic growth, particularly in emerging market economies. As shown in Figure 1, world GDP growth (with countries weighted by oil consumption shares) has averaged close to 5 percent per year since 2004, marking the strongest performance in two decades.

Figure here. In addition to the pace of world economic activity, oil demand has been further supported by the composition of growth across countries. As shown in Figure 2, China, India, and the Middle East use substantially more oil to produce a dollar�s worth of real output than the United States.

Figure here. These economies are among the fastest growing in the world; together they have accounted for nearly two-thirds of the rise in world oil consumption since 2004. Moreover, these economies still consume relatively little oil on a per capita basis. Over the longer term, as these economies continue to develop and incomes rise, per capita energy use is likely to increase further.

b. Increasing Consumption

17

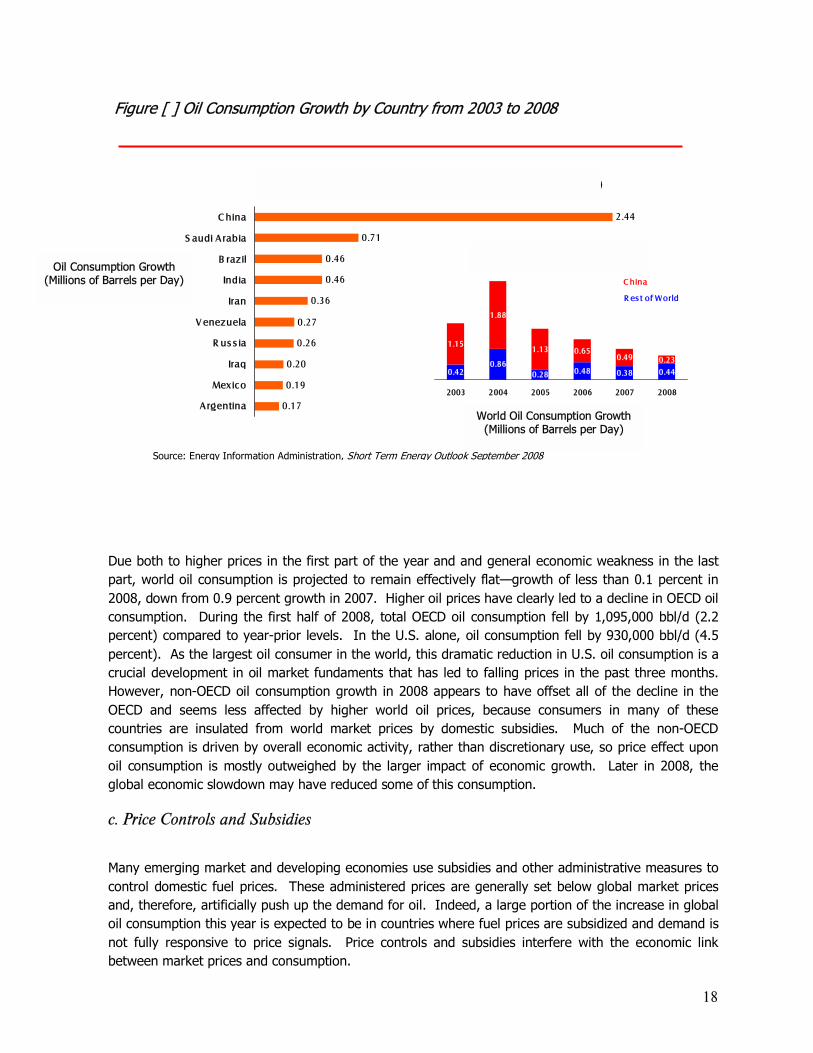

The historical rise in global economic activity has been accompanied by corresponding growth in world oil consumption. Since 2003, world oil consumption growth has averaged 1.4 percent per year. The recent global economic slowdown, however, is expected to result in virtually no growth for 2008, reaching only 85.9 million barrels a day. Non-OECD countries, especially China, Brazil, India, and the Middle East, represent the vast majority of currently expected growth (Figures 3 and 4).

Figure [ ] Annual Growth in World Oil Consumption

2003 2004 2005 2006 2007 2008

Ch

an

ge

fro

m P

rio

r Y

ear

(Mill

ion

Ba

rre

ls p

er

Day

C hina U.S . Other

1.6

2.7

1.41.1

0.9

T otal W orld Oil C ons umption Growth

0.7

Source: Energy Information Administration, Short-Term Energy Outlook September 2008

(est.)

(Million Barrels per Day)

18

Due both to higher prices in the first part of the year and and general economic weakness in the last part, world oil consumption is projected to remain effectively flat�growth of less than 0.1 percent in 2008, down from 0.9 percent growth in 2007. Higher oil prices have clearly led to a decline in OECD oil consumption. During the first half of 2008, total OECD oil consumption fell by 1,095,000 bbl/d (2.2 percent) compared to year-prior levels. In the U.S. alone, oil consumption fell by 930,000 bbl/d (4.5 percent). As the largest oil consumer in the world, this dramatic reduction in U.S. oil consumption is a crucial development in oil market fundaments that has led to falling prices in the past three months. However, non-OECD oil consumption growth in 2008 appears to have offset all of the decline in the OECD and seems less affected by higher world oil prices, because consumers in many of these countries are insulated from world market prices by domestic subsidies. Much of the non-OECD consumption is driven by overall economic activity, rather than discretionary use, so price effect upon oil consumption is mostly outweighed by the larger impact of economic growth. Later in 2008, the global economic slowdown may have reduced some of this consumption.

c. Price Controls and Subsidies

Many emerging market and developing economies use subsidies and other administrative measures to control domestic fuel prices. These administered prices are generally set below global market prices and, therefore, artificially push up the demand for oil. Indeed, a large portion of the increase in global oil consumption this year is expected to be in countries where fuel prices are subsidized and demand is not fully responsive to price signals. Price controls and subsidies interfere with the economic link between market prices and consumption.

Figure [ ] Oil Consumption Growth by Country from 2003 to 2008

T otal Oil C ons umption G rowth, 2003-2008 (Million bbl/d)

0.17

0.19

0.20

0.26

0.27

0.36

0.46

0.46

0.71

2.44

Argentina

Mex ico

Iraq

R us s ia

V enezuela

Iran

India

B razil

S audi Arabia

C hina

0.420.86

0.28 0.48 0.38 0.44

1.15

1.88

1.13 0.650.49 0.23

2003 2004 2005 2006 2007 2008

C hina

R es t of World

Source: Energy Information Administration, Short Term Energy Outlook September 2008

World Oil Consumption Growth (Millions of Barrels per Day)

Oil Consumption Growth (Millions of Barrels per Day)

19

3. Supply

a. Stagnant Production

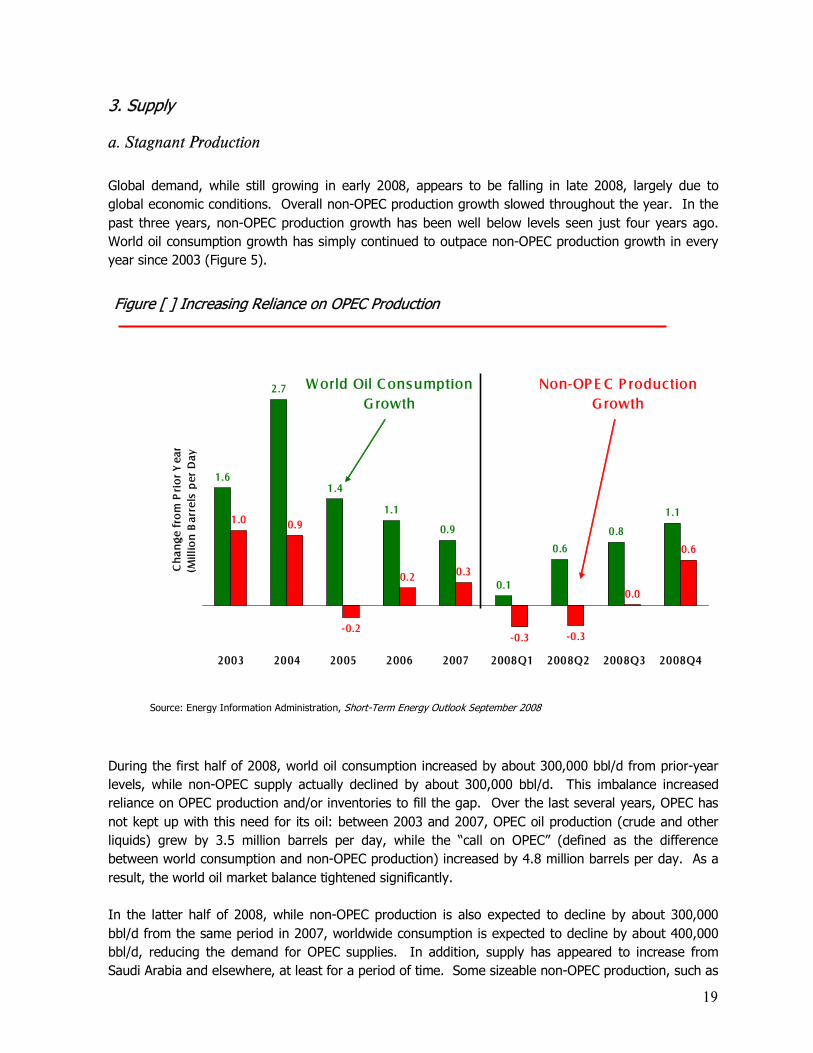

Global demand, while still growing in early 2008, appears to be falling in late 2008, largely due to global economic conditions. Overall non-OPEC production growth slowed throughout the year. In the past three years, non-OPEC production growth has been well below levels seen just four years ago. World oil consumption growth has simply continued to outpace non-OPEC production growth in every year since 2003 (Figure 5).

During the first half of 2008, world oil consumption increased by about 300,000 bbl/d from prior-year levels, while non-OPEC supply actually declined by about 300,000 bbl/d. This imbalance increased reliance on OPEC production and/or inventories to fill the gap. Over the last several years, OPEC has not kept up with this need for its oil: between 2003 and 2007, OPEC oil production (crude and other liquids) grew by 3.5 million barrels per day, while the �call on OPEC� (defined as the difference between world consumption and non-OPEC production) increased by 4.8 million barrels per day. As a result, the world oil market balance tightened significantly. In the latter half of 2008, while non-OPEC production is also expected to decline by about 300,000 bbl/d from the same period in 2007, worldwide consumption is expected to decline by about 400,000 bbl/d, reducing the demand for OPEC supplies. In addition, supply has appeared to increase from Saudi Arabia and elsewhere, at least for a period of time. Some sizeable non-OPEC production, such as

Figure [ ] Increasing Reliance on OPEC Production

1.6

2.7

1.4

1.1

0.9

0.1

0.6

0.8

1.11.0 0.9

-0.2

0.2 0.3

-0.3 -0.3

0.0

0.6

2003 2004 2005 2006 2007 2008Q1 2008Q2 2008Q3 2008Q4

Ch

an

ge

fro

m P

rio

r Y

ear

(Mill

ion

Bar

rels

per

Da

y

W orld Oil C onsumptionG rowth

Non-OP E C P roductionG rowth

Source: Energy Information Administration, Short-Term Energy Outlook September 2008

20

in Brazil and Azerbaijan, has started to come online, leading to an improved perception regarding non-OPEC supply growth for the second half of 2008 in comparison to the first half of the year.

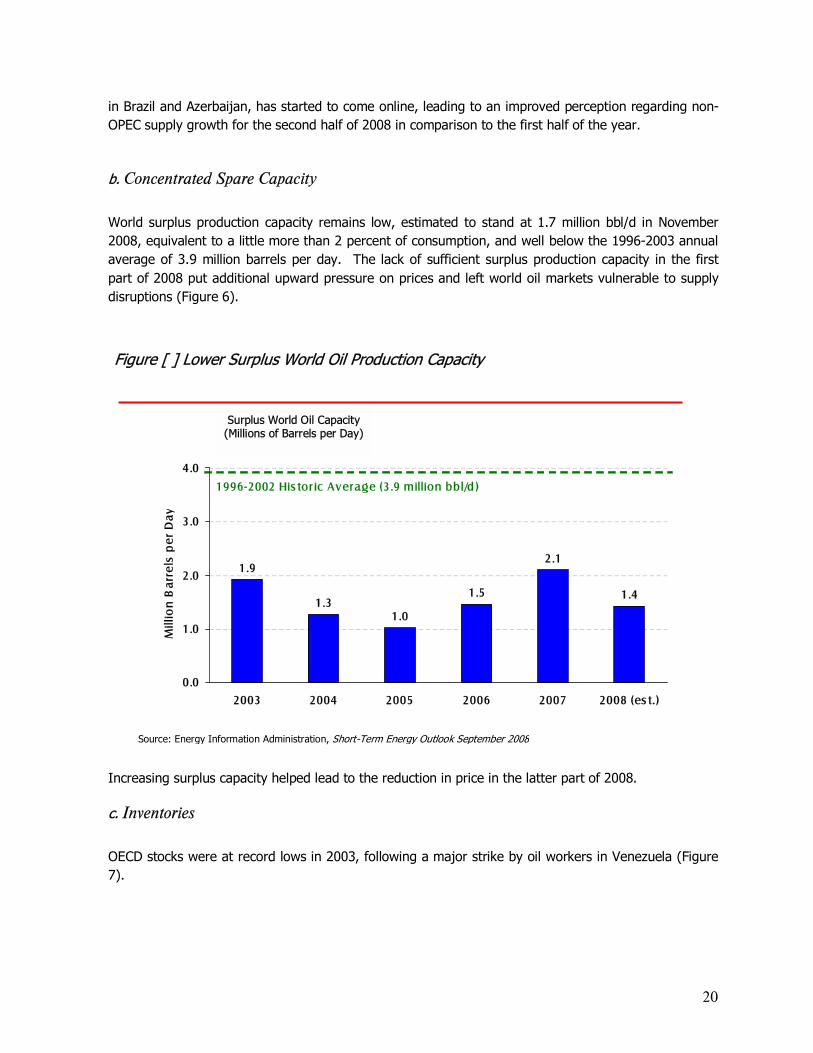

b. Concentrated Spare Capacity

World surplus production capacity remains low, estimated to stand at 1.7 million bbl/d in November 2008, equivalent to a little more than 2 percent of consumption, and well below the 1996-2003 annual average of 3.9 million barrels per day. The lack of sufficient surplus production capacity in the first part of 2008 put additional upward pressure on prices and left world oil markets vulnerable to supply disruptions (Figure 6).

Increasing surplus capacity helped lead to the reduction in price in the latter part of 2008.

c. Inventories

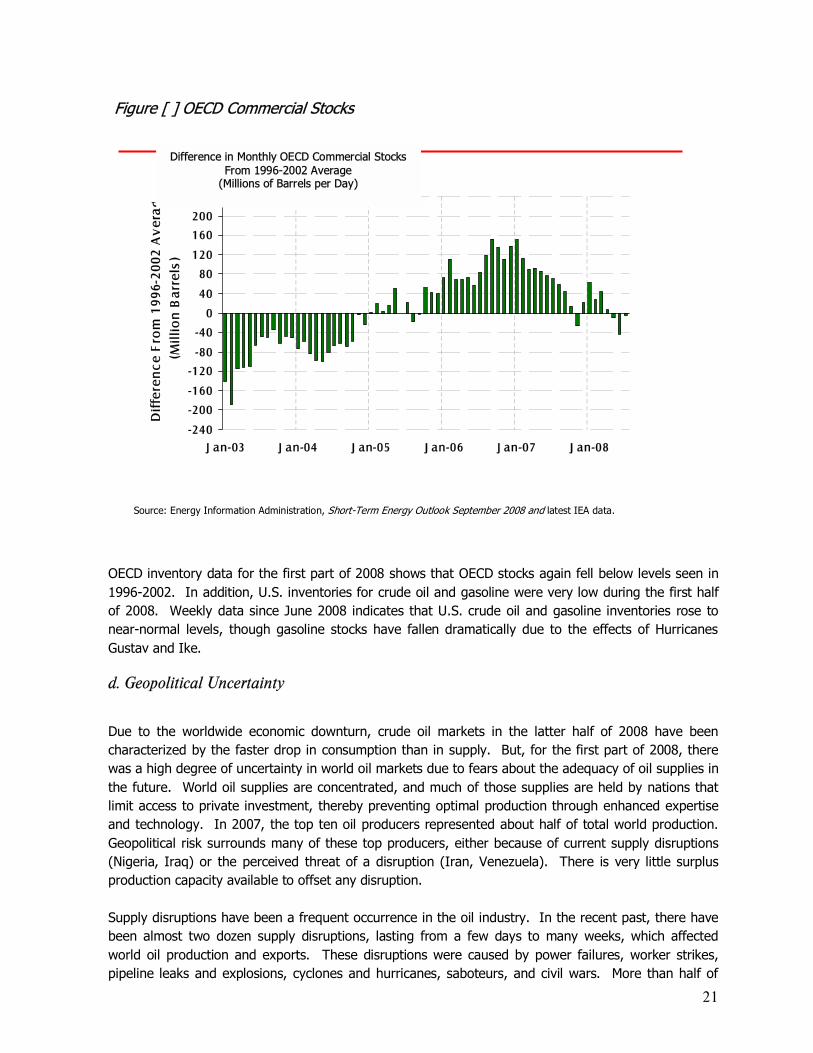

OECD stocks were at record lows in 2003, following a major strike by oil workers in Venezuela (Figure 7).

Figure [ ] Lower Surplus World Oil Production Capacity

1.9

1.31.0

1.5

2.1

1.4

0.0

1.0

2.0

3.0

4.0

2003 2004 2005 2006 2007 2008 (es t.)

Mill

ion

Bar

rels

pe

r D

ay

1996-2002 His tor ic Average (3.9 million bbl/d)

Source: Energy Information Administration, Short-Term Energy Outlook September 2008

Surplus World Oil Capacity (Millions of Barrels per Day)

21

OECD inventory data for the first part of 2008 shows that OECD stocks again fell below levels seen in 1996-2002. In addition, U.S. inventories for crude oil and gasoline were very low during the first half of 2008. Weekly data since June 2008 indicates that U.S. crude oil and gasoline inventories rose to near-normal levels, though gasoline stocks have fallen dramatically due to the effects of Hurricanes Gustav and Ike.

d. Geopolitical Uncertainty

Due to the worldwide economic downturn, crude oil markets in the latter half of 2008 have been characterized by the faster drop in consumption than in supply. But, for the first part of 2008, there was a high degree of uncertainty in world oil markets due to fears about the adequacy of oil supplies in the future. World oil supplies are concentrated, and much of those supplies are held by nations that limit access to private investment, thereby preventing optimal production through enhanced expertise and technology. In 2007, the top ten oil producers represented about half of total world production. Geopolitical risk surrounds many of these top producers, either because of current supply disruptions (Nigeria, Iraq) or the perceived threat of a disruption (Iran, Venezuela). There is very little surplus production capacity available to offset any disruption. Supply disruptions have been a frequent occurrence in the oil industry. In the recent past, there have been almost two dozen supply disruptions, lasting from a few days to many weeks, which affected world oil production and exports. These disruptions were caused by power failures, worker strikes, pipeline leaks and explosions, cyclones and hurricanes, saboteurs, and civil wars. More than half of

Figure [ ] OECD Commercial Stocks

-240

-200

-160

-120

-80

-40

0

40

80

120

160

200

240

J an-03 J an-04 J an-05 J an-06 J an-07 J an-08

Dif

fere

nc

e F

rom

19

96-

20

02

Av

era

g

(Mil

lio

n B

arr

els

)

Source: Energy Information Administration, Short-Term Energy Outlook September 2008 and latest IEA data.

Difference in Monthly OECD Commercial Stocks From 1996-2002 Average

(Millions of Barrels per Day)

22

these resulted in oil production outages exceeding 100,000 barrels per day. The most significant of these to oil markets resulted from the ongoing strife in Iraq and Nigeria. These disruptions have varied in size over time, with Iraq losing more than 500,000 barrels per day of exports in March 2008 and Nigeria reaching more than 1.4 million barrels per day of shut-in production at one point in April 2008. Actual supply disruptions directly affect world oil markets due to a loss of physical barrels available to the market. Concern over the impact of potential supply disruptions is reinforced by the limited amount of spare production capacity available. As long as potential disruptions, either realized (as in Iraq and Nigeria) or perceived (as in concerns about the potential loss of supply from Iran), exceed the amount of additional production capacity that can be brought online quickly, geopolitical concerns will weigh heavily on oil markets.

4. Price-Inelastic Supply and Demand

The short-run demand for oil is relatively price inelastic, meaning the quantity demanded does not change much relative to price changes. Put another way, it takes a very large price increases to significantly reduce the quantity demanded. In the short run, the supply of oil is inelastic as well: the quantity supplied is not responsive to changes in market price, due to low spare capacity, the inability to bring new supplies online quickly, and relatively low inventories to draw down. If both supply and demand are not very responsive to prices, it takes large price increases to return markets to equilibrium if they get out of balance temporarily. As noted previously, world oil production has remained relatively flat in recent years, as global economic growth has kept demand strong. Consequently, oil prices have risen to keep world oil consumption in line with production. As oil demand is very insensitive to moves in oil prices in the near term, the rise in oil prices has been disproportionately large in order to offset the robust, income-driven rise in demand. An implication of these structural features of the oil market is that large and rapid movements in oil prices are not, by themselves, evidence that prices are behaving in a manner that is inconsistent with the fundamentals of demand and supply. Indeed, in such tight market conditions, relatively small changes in demand and supply should be expected to lead to large price swings. That said, there is a significant degree of uncertainty regarding the true state of market fundamentals at any point in time, due to the general lack of reliable and timely data.

5. Analysis of Crude Oil Futures Markets (update using additional data10

a. Broad Trends in the Participant Structure of Crude Oil Futures Markets

According to the publicly-available Commitments of Traders (COT) reports, activity in the West Texas Intermediate (WTI) light sweet crude oil contracts has grown steadily since 2000. In the last three and a half years alone, open interest across all available contract maturities (the

10 This section largely summarizes findings in an upcoming CFTC research paper analyzing changes in the level and composition of end-of-day open interest in the U.S. crude oil futures market. See Bόyόk�ahin, Haigh, Harris, Overdahl and Robe: �Market Growth and Trader Participation in Futures Markets,� CFTC � Office of the Chief Economist Working Paper, Fall 2008.

23

number of contracts open at the end of each day) in WTI futures and futures-equivalent (or �adjusted�) option contracts traded on the New York Mercantile Exchange (NYMEX) more than tripled from around 900,000 contracts in January 2004 to more than 2.75 million contracts in late August 2008. During the same period, the number of large traders also grew substantially � it almost doubled (from approximately 220 reporting traders in January 2004 to just under 400 in June 2008) before dropping back to 331 large option and futures traders as of late August 2008. These figures speak to the competitiveness and depth of the crude oil futures markets in the U.S. The COT reports also present the breakdown of the overall open interest between commercial and non-commercial traders grouped into long, short, and spread positions. While all types of positions have grown during the last three and a half years, the COT data suggests that it is the spread positions of non-commercial traders that have had the fastest growth rate. While overall open interest has tripled since 2004, non-commercial spread positions have increased six-fold. Notably, spread positions involve long positions in one month combined with short positions in another month so that spread traders are speculating on differences between futures prices in different months rather than the overall price level of crude oil. Since 2005, both the long and short positions of non-commercial traders have increased. Over that time period, the positions of non-commercial traders have been net long and have increased nominally; however, the proportion of those positions has been relatively constant as a share of the annual average open interest over the last few years.

b. Detailed Structure of Crude Oil Futures Markets

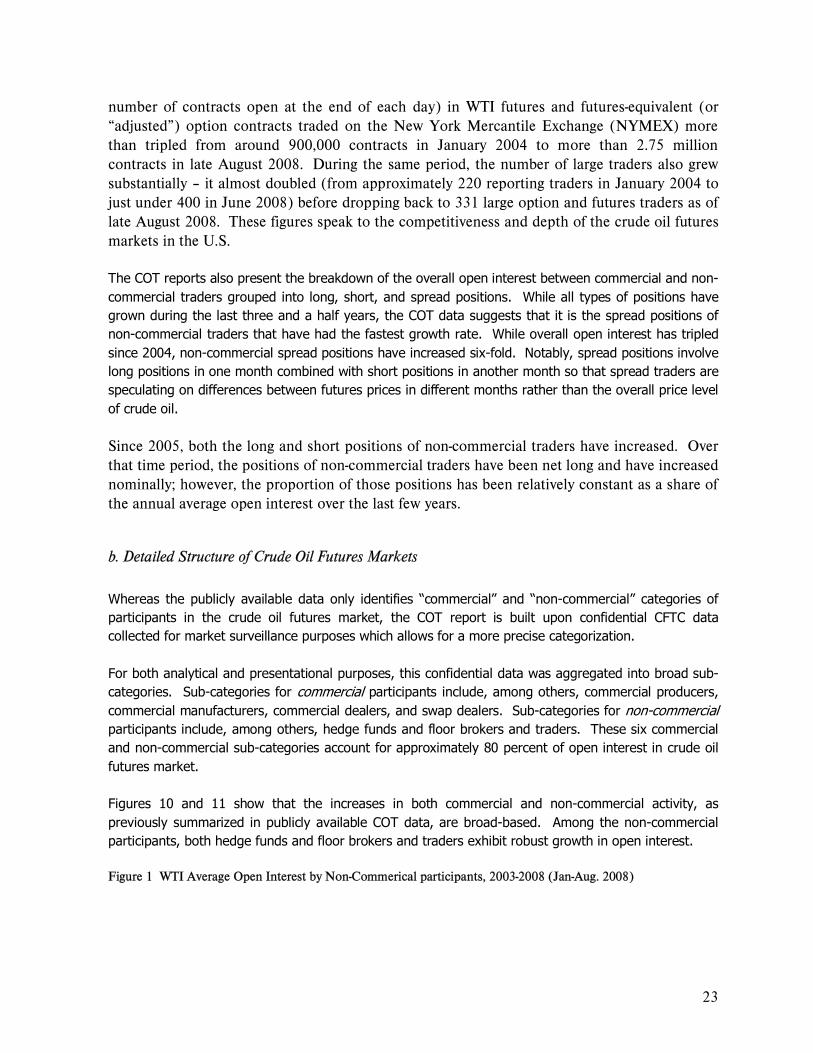

Whereas the publicly available data only identifies �commercial� and �non-commercial� categories of participants in the crude oil futures market, the COT report is built upon confidential CFTC data collected for market surveillance purposes which allows for a more precise categorization. For both analytical and presentational purposes, this confidential data was aggregated into broad sub-categories. Sub-categories for commercial participants include, among others, commercial producers, commercial manufacturers, commercial dealers, and swap dealers. Sub-categories for non-commercial participants include, among others, hedge funds and floor brokers and traders. These six commercial and non-commercial sub-categories account for approximately 80 percent of open interest in crude oil futures market. Figures 10 and 11 show that the increases in both commercial and non-commercial activity, as previously summarized in publicly available COT data, are broad-based. Among the non-commercial participants, both hedge funds and floor brokers and traders exhibit robust growth in open interest. Figure 1 WTI Average Open Interest by Non-Commerical participants, 2003-2008 (Jan-Aug. 2008)

24

20032004

20052006

20072008

F loor B rokers

Hedge F unds

-

250,000

500,000

750,000

1,000,000

S our ce: Büyük ş ahin et al, C FT C , 2008

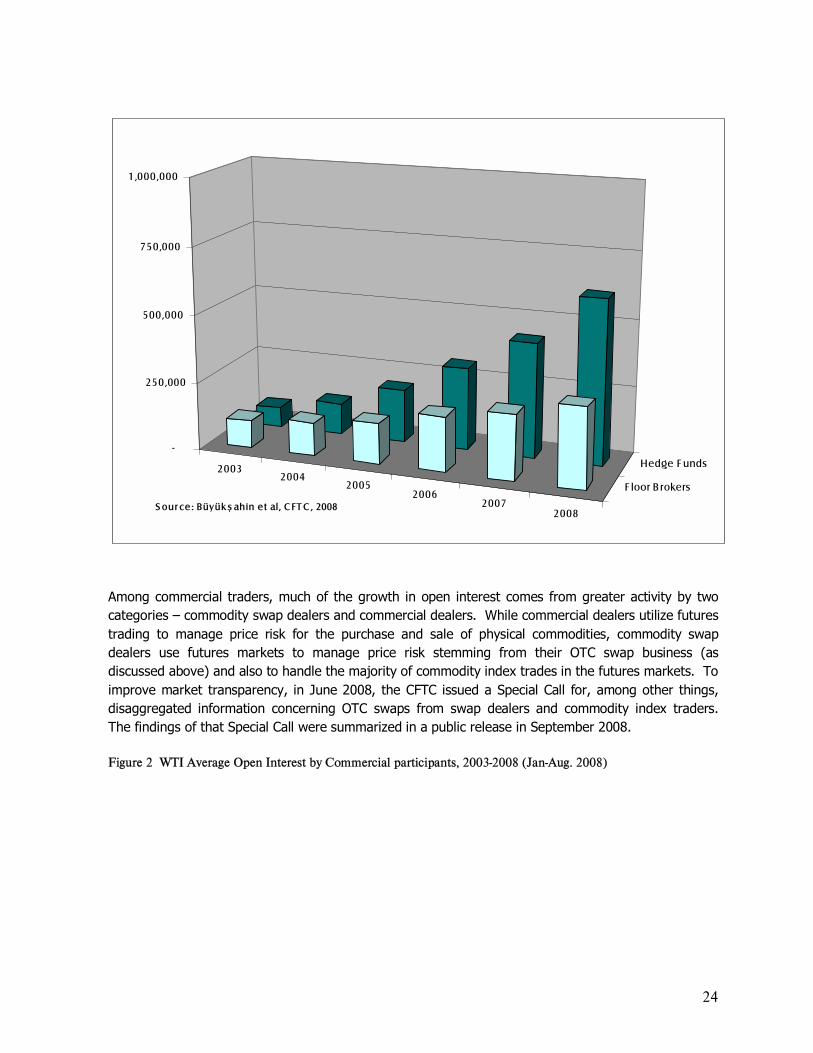

Among commercial traders, much of the growth in open interest comes from greater activity by two categories � commodity swap dealers and commercial dealers. While commercial dealers utilize futures trading to manage price risk for the purchase and sale of physical commodities, commodity swap dealers use futures markets to manage price risk stemming from their OTC swap business (as discussed above) and also to handle the majority of commodity index trades in the futures markets. To improve market transparency, in June 2008, the CFTC issued a Special Call for, among other things, disaggregated information concerning OTC swaps from swap dealers and commodity index traders. The findings of that Special Call were summarized in a public release in September 2008. Figure 2 WTI Average Open Interest by Commercial participants, 2003-2008 (Jan-Aug. 2008)

25

20032004

20052006

20072008

Manufacturers

Producers

Comm. Dealers

S w ap Dealers

-

250,000

500,000

750,000

1,000,000

S ource: Büyük ş ahin et al, C F T C , 2008

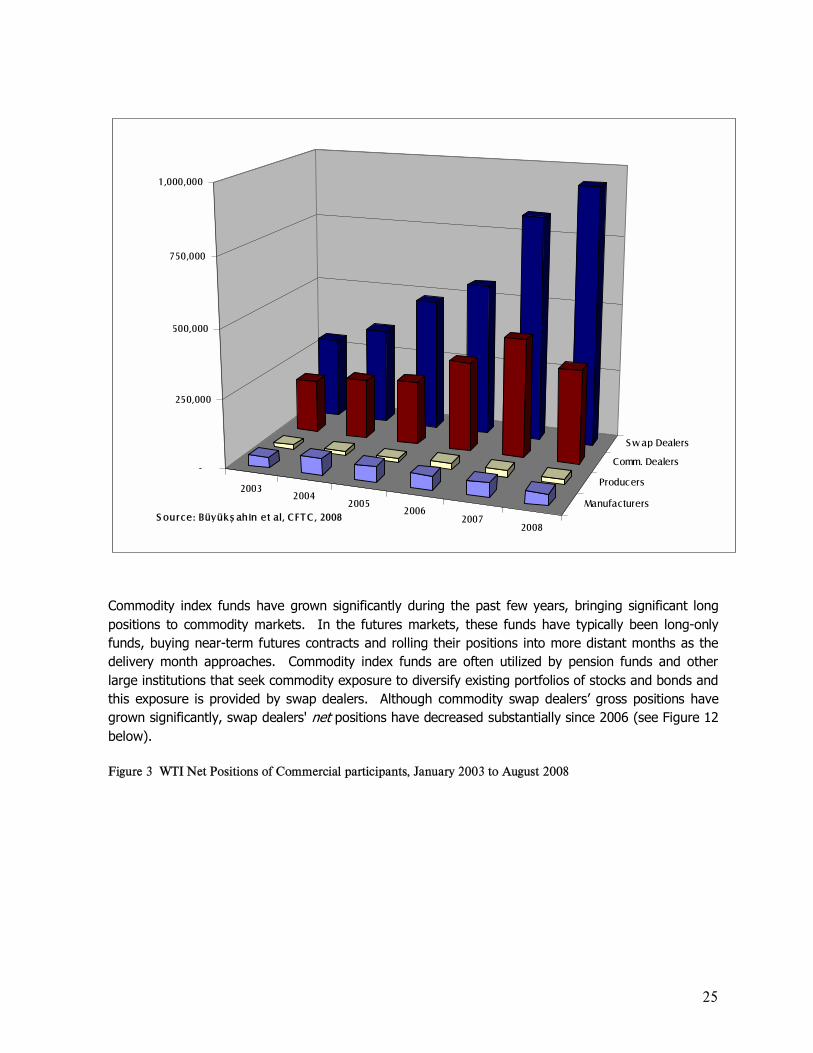

Commodity index funds have grown significantly during the past few years, bringing significant long positions to commodity markets. In the futures markets, these funds have typically been long-only funds, buying near-term futures contracts and rolling their positions into more distant months as the delivery month approaches. Commodity index funds are often utilized by pension funds and other large institutions that seek commodity exposure to diversify existing portfolios of stocks and bonds and this exposure is provided by swap dealers. Although commodity swap dealers� gross positions have grown significantly, swap dealers' net positions have decreased substantially since 2006 (see Figure 12 below). Figure 3 WTI Net Positions of Commercial participants, January 2003 to August 2008

26

20032004

20052006

20072008

Manufac turers

Producers

Comm. Dealers

S w ap Dealers (100,000)

(80,000)

(60,000)

(40,000)

(20,000)

-

20,000

40,000

60,000Manufacturers

Producers

Comm. Dealers

S w ap Dealers

S ource: Büyük ş ahin et al, C FT C , 2008

This suggests that flows from commodity index funds have been offset by other swap dealer activity and thus have not necessarily contributed to the price increases in crude oil during the first half of 2008. In fact, across all maturities, the aggregate position of swap dealers in WTI crude oil futures contracts was only marginally net long as of the end of August 2008.

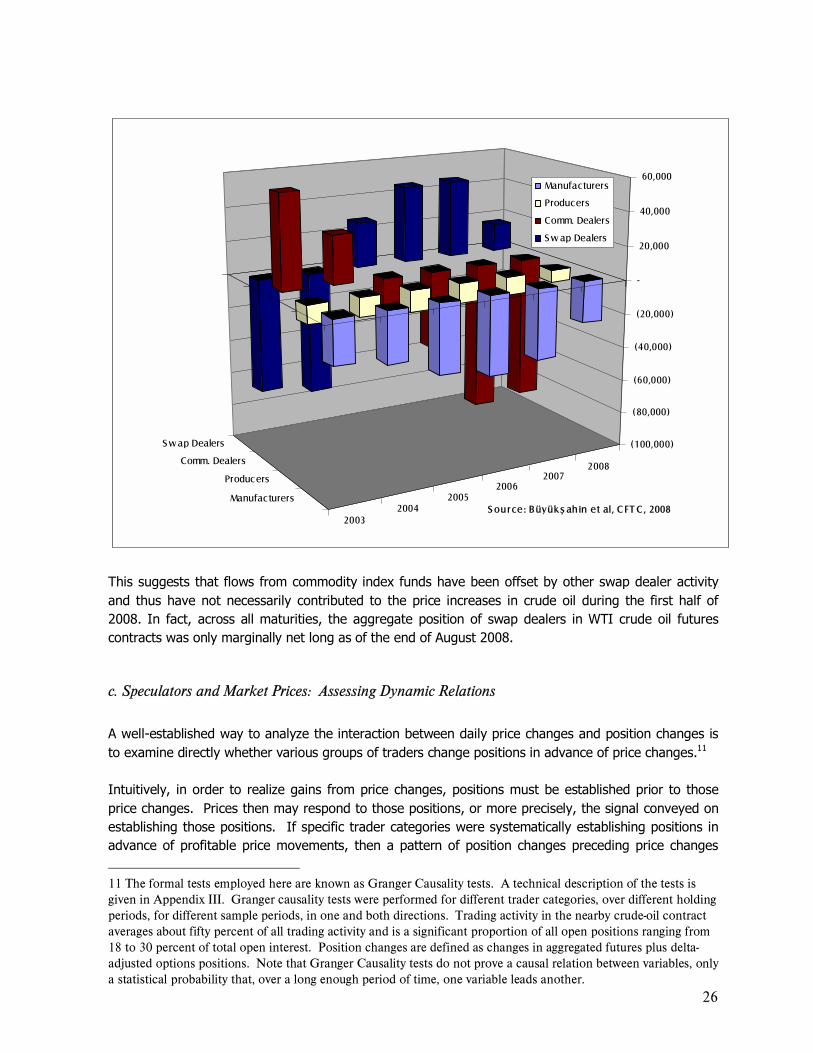

c. Speculators and Market Prices: Assessing Dynamic Relations

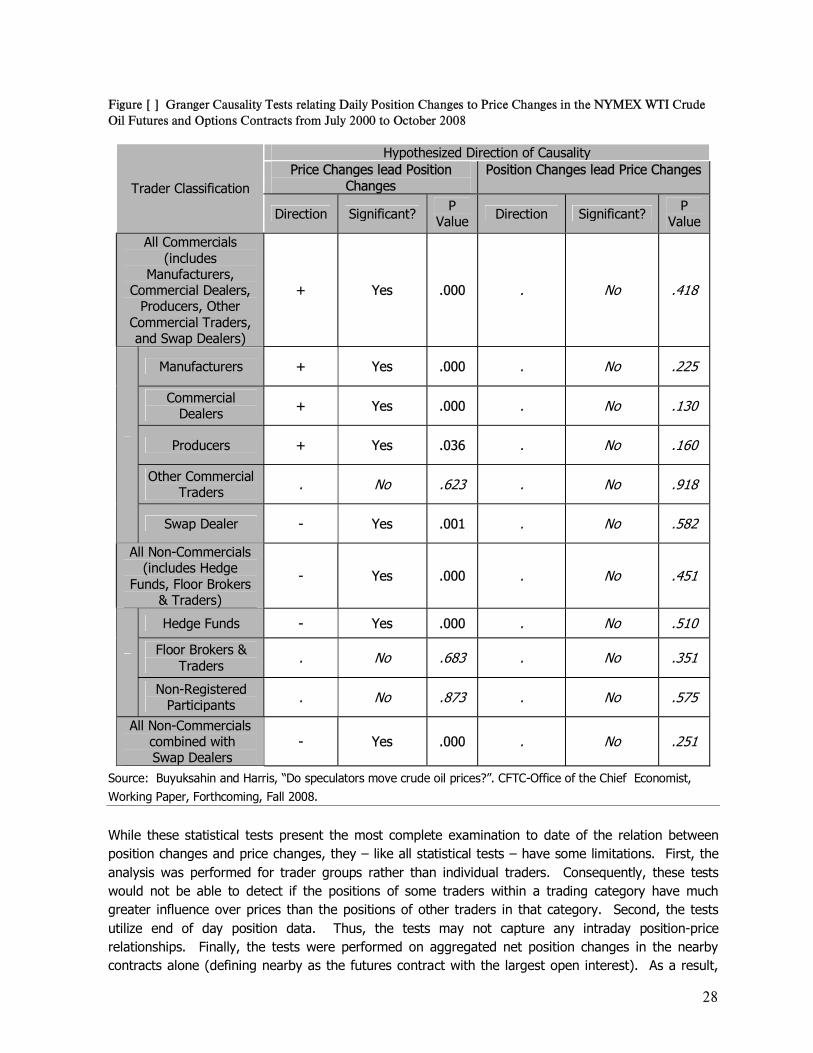

A well-established way to analyze the interaction between daily price changes and position changes is to examine directly whether various groups of traders change positions in advance of price changes.11 Intuitively, in order to realize gains from price changes, positions must be established prior to those price changes. Prices then may respond to those positions, or more precisely, the signal conveyed on establishing those positions. If specific trader categories were systematically establishing positions in advance of profitable price movements, then a pattern of position changes preceding price changes

11 The formal tests employed here are known as Granger Causality tests. A technical description of the tests is given in Appendix III. Granger causality tests were performed for different trader categories, over different holding periods, for different sample periods, in one and both directions. Trading activity in the nearby crude-oil contract averages about fifty percent of all trading activity and is a significant proportion of all open positions ranging from 18 to 30 percent of total open interest. Position changes are defined as changes in aggregated futures plus delta-adjusted options positions. Note that Granger Causality tests do not prove a causal relation between variables, only a statistical probability that, over a long enough period of time, one variable leads another.

27

would emerge. Conversely, evidence of price changes leading position changes would suggest that some market participants actively adjust their positions to reflect new information. Price changes that systematically precede position changes indicate reactive behavior by a particular trading group. Figure [ ] displays the analysis of daily price changes and position changes by various trader groups and combinations of trader groups between January 2003 and October 2008. Over the full time period, there is little evidence that daily position changes by any of the trader sub-categories systematically precede price changes. This result holds for all potential categories of speculators�for non-commercial traders in total, for hedge funds and swap dealers individually, and for the positions of non-commercial traders combined with swap dealers. A reaction in the positive direction indicates that trader positions increase (decrease) following a price increase (decrease) on the previous day. A reaction in the negative direction indicates that trader positions decrease (increase) following a price increase (decrease) on the previous day. These results are representative and have been subject to a variety of robustness checks.

28

Figure [ ] Granger Causality Tests relating Daily Position Changes to Price Changes in the NYMEX WTI Crude Oil Futures and Options Contracts from July 2000 to October 2008

Hypothesized Direction of Causality Price Changes lead Position

Changes Position Changes lead Price Changes

Trader Classification

Direction Significant? P Value Direction Significant? P

Value All Commercials

(includes Manufacturers,

Commercial Dealers, Producers, Other

Commercial Traders, and Swap Dealers)

+ Yes .000 . No .418

Manufacturers + Yes .000 . No .225

Commercial Dealers + Yes .000 . No .130

Producers + Yes .036 . No .160

Other Commercial Traders . No .623 . No .918

Swap Dealer - Yes .001 . No .582

All Non-Commercials (includes Hedge

Funds, Floor Brokers & Traders)

- Yes .000 . No .451

Hedge Funds - Yes .000 . No .510

Floor Brokers & Traders . No .683 . No .351

Non-Registered Participants . No .873 . No .575

All Non-Commercials combined with Swap Dealers

- Yes .000 . No .251

Source: Buyuksahin and Harris, �Do speculators move crude oil prices?�. CFTC-Office of the Chief Economist, Working Paper, Forthcoming, Fall 2008.

While these statistical tests present the most complete examination to date of the relation between position changes and price changes, they � like all statistical tests � have some limitations. First, the analysis was performed for trader groups rather than individual traders. Consequently, these tests would not be able to detect if the positions of some traders within a trading category have much greater influence over prices than the positions of other traders in that category. Second, the tests utilize end of day position data. Thus, the tests may not capture any intraday position-price relationships. Finally, the tests were performed on aggregated net position changes in the nearby contracts alone (defining nearby as the futures contract with the largest open interest). As a result,

29

the tests do not reflect a systematic effect of position changes at different maturities on either the prices of the nearby futures contract or on the whole term structure of futures prices. That said, if the actions of particular groups of traders had systematically driven the recent oil price increases, the tests performed should have made it quite apparent. Again, it is useful to note that while the tests do not find that that changes in daily positions systematically lead changes in prices, such a finding would not necessarily imply that position changes were responsible for the price changes. Nevertheless, the lack of significant position changes leading price changes is informative. Taken as a whole, these tests are consistent with the view that current oil prices are being driven by fundamental supply and demand factors.

B. Select Agricultural Commodities - Corn, Wheat, and Soybeans

1. Background A number of long-term, slowly evolving trends have affected the global supply and demand for food commodities. The impact of these trends has been to slow growth in production and to strengthen demand. The resulting tightening of the global supply and demand balance has gradually put upward pressure on agricultural prices. Many of these long-term trends have been amplified by the more recent developments that have put additional upward pressure on world prices. These developments include rising energy costs, a series of policy changes in the United States and abroad, a weakening dollar, and changes in the profiles of commodity market participants.

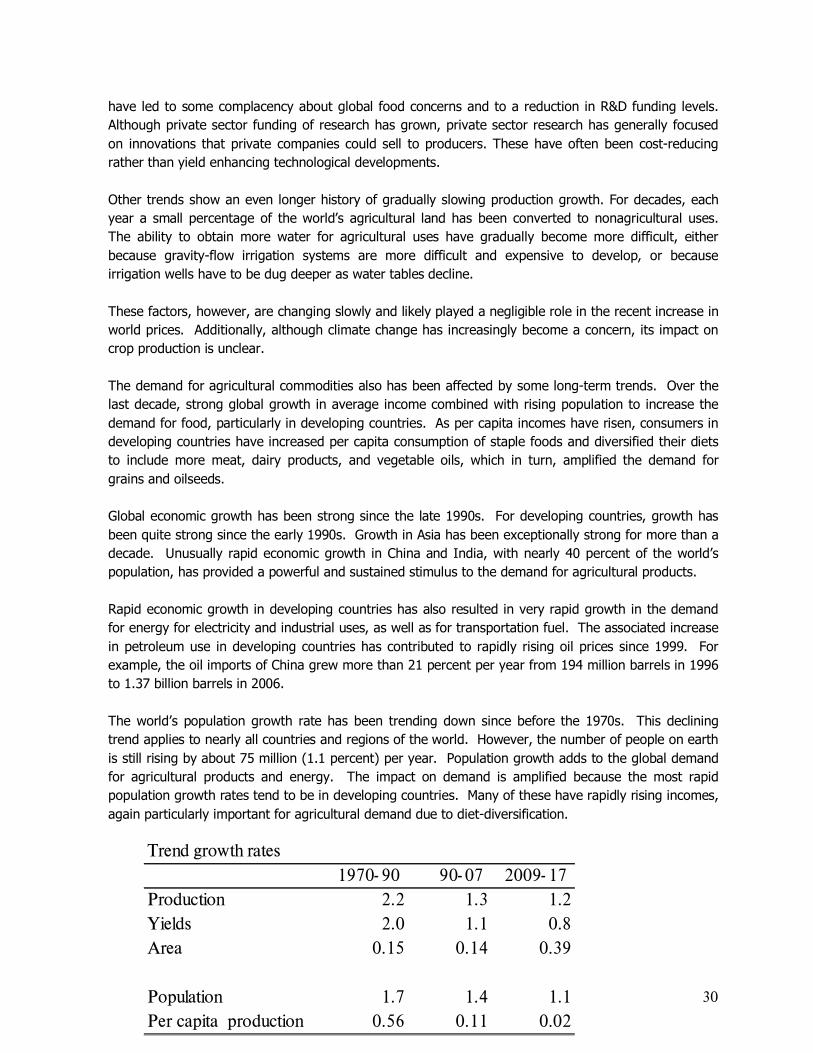

2. Long-Term Trends in Supply and Demand The annual growth rate of aggregate world grains and oilseeds production has been slowing. Between 1970 and 1990, production rose an average 2.2 percent per year. Since 1990, the growth rate has declined to about 1.3 percent. USDA projects this rate will decline to 1.2 percent per year between 2009 and 2017. Growth in productivity, measured in terms of average aggregate yield, has contributed much more to the growth in production globally than has expansion in the area planted to grains and oilseeds. Global aggregate yield growth averaged 2.0 percent per year from 1970 to 1990, but declined to 1.1 percent between 1990 and 2007. Yield growth is projected to continue declining over the next 10 years to less than 1.0 percent per year. The growth rate for area harvested has averaged only about 0.15 percent per year during the last 38 years. USDA projects that crop prices will remain strong during the next decade. The continued higher prices will provide the incentive for producers to respond by increasing the area allocated to crops. Some of this expanded area planted will come from land converted to cropland from non-cropland uses, such as pasture and forest. Area harvested also will increase as a result of more intensive use of existing cropland, generally from double-cropping and reduced fallow area. Reduced agricultural research and development by governmental and international institutions may have contributed to the slowing growth in crop yields. Stable food prices during the last two decades

30