inter temporal choice

TRANSCRIPT

Chapter 10

Intertemporal Choice

In this chapter we model a consumers choice of consumption over time.This is known as intertemporal choice.

10.1 The budget constraint

Assume two periods, say, today and tomorrow denoted 1 and 2 respectively.Denote consumption in the respective periods as (c1, c2) and the money theconsumer will have in each period as (m1,m2). Assume the relative priceof consumption in the two periods is equal to 1.

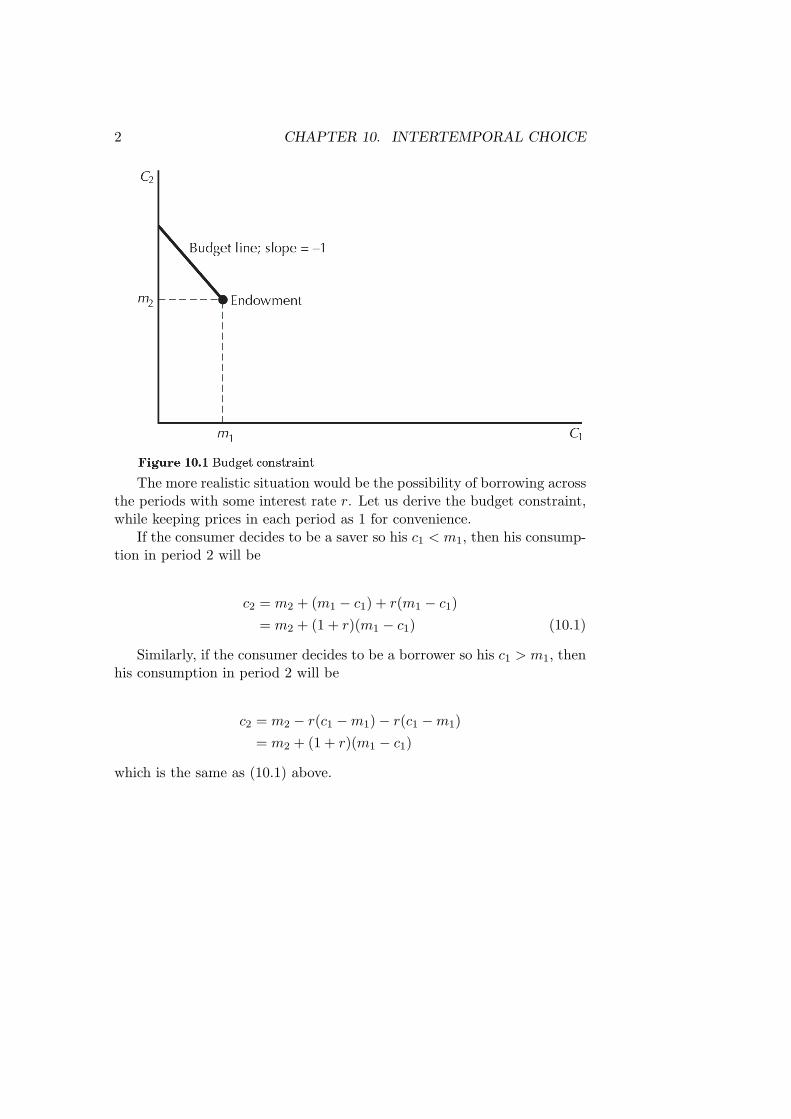

If the consumer can transfer money from period 1 to period 2 by saving(without any interest), but cannot borrow money in period 1 (so he canonely spend a maximum of m1), then the budget constraint looks as follows:

1

2 CHAPTER 10. INTERTEMPORAL CHOICE

The more realistic situation would be the possibility of borrowing acrossthe periods with some interest rate r. Let us derive the budget constraint,while keeping prices in each period as 1 for convenience.

If the consumer decides to be a saver so his c1 < m1, then his consump-tion in period 2 will be

c2 = m2 + (m1 − c1) + r(m1 − c1)= m2 + (1 + r)(m1 − c1) (10.1)

Similarly, if the consumer decides to be a borrower so his c1 > m1, thenhis consumption in period 2 will be

c2 = m2 − r(c1 −m1)− r(c1 −m1)= m2 + (1 + r)(m1 − c1)

which is the same as (10.1) above.

10.1. THE BUDGET CONSTRAINT 3

We can rearrange the budget constraint to get two alternative forms thatare useful, namely, the future value form which sets p2 = 1 and p1 = (1+r)and the present value form which sets p1 = 1 and p2 = 1/(1 + r). So wehave

Future value: (1 + r)c1 + c2 = (1 + r)m1 + m2

and

Present value: c1 + c2/(1 + r) = m1 + m2/(1 + r)

Note that both equations have the forms p1x1 + p2x2 = p1ω1 + p2ω2.The geometric interpretation of present value and future value is given

in Figure 10.2 below.

Note that the budget line always passes through (m1,m2), since this isalways an affordable consumption pattern, and the slope of the budget lineis −(1 + r).

4 CHAPTER 10. INTERTEMPORAL CHOICE

10.2 Comparative statics

If a consumer is initially a lender and the interest rate increases, then sheor she will remain a lender (see Figure 10.4). also note that if the consumeris a borrower and the interest rate falls, then he or she will remain borrower.

10.3. THE SLUTSKY EQUATION AND INTERTEMPORAL CHOICE5

A borrower on the other hand is made worse off by an increase in theinterest rate if he remains a borrower (see Figure 10.5). so it is possiblethat the borrower can switch to becoming a lender if interest rates rise.

10.3 The Slutsky equation and intertemporal choice

Note that raising the interest rate is like raising the price of of consumptiontoday as compared to consumption tomorrow. Writing out the Slutskyequation, we have

4c1

4p1=4cs

1

4p1+ (m1 − c1)

4cm1

4m

(?) (−) (?) (+)

The substitution effect always works in the opposite direction to the pricechange. If we assume that consumption today is a normal good, then

6 CHAPTER 10. INTERTEMPORAL CHOICE

the last term is positive. The sign of the whole expression will depend on(m1−c1), that is, whether the consumer is a borrower (−ve) or lender (+ve).If the consumer is a borrower, then the total change will unambiguouslybe negative - for a borrower, an increase in interest rates means he or shemust pay more interest tomorrow, which induces the consumer to lowerconsumption in the first period.

For the lender, the total effect of a rise in interest rates is ambiguous.

10.4 Inflation

It is easy to modify the above model to deal with inflation. Let’s put inprices as p1 = 1 and p2 as the price of consumption tomorrow. Setting themonetary value of endowment in period 2 as p2m2, the amount of moneythat the consumer can spend in the second period is given by

p2c2 = p2m2 + (1 + r)(m1 − c1)

and the amount of consumption available in the second period is

c2 = m2 +1 + r

p2(m1 − c1)

Recalling p1 = 1, then given some inflation rate π, we have P2 = 1 + π,which gives us

c2 = m2 +1 + r

1 + π(m1 − c1)

We could create a new variable ρ, the real interest rate, and define it by

1 + ρ =1 + r

1 + π

so the budget constraint becomes

c2 = m2 + (1 + ρ)(m1 − c1)

Lastly, note that ρ ≈ r − π when π is not too large.

10.5. PRESENT VALUE 7

10.5 Present value

Assume have $100 in a bank account earning 10% interest per year. the inthe next year, this $100 will grow to $110. $100 is the present value while$110 is the future value of your bank account. Hence,

FV = (1 + r)PV

It follows that

PV = FV/(1 + r)

10.6 Use of present value

Present value is the only correct way to convert a stream of payment’s intotoday’s dollars. Present value is often used in decisions on investment.

Denote an income stream as (M1,M2) and payment stream as (P1, P2).If the present value of the income stream from an investment exceeds thepresent value of its costs, then it is a good investment - it will increase thepresent value of your endowment.

An equivalent assessment uses the net present value. If (M1−P1,M2−P2) is the next cash flow for periods 1 and 2, then the net present value(NPV) is

NPV = M1 − P1 +M2 − P2

1 + r

10.7 Bonds

Securities are financial instruments that promise certain patterns of pay-ment schedules.

Let’s look at the bond, which are a way to borrow money, usuallyissued by governments and corporations. The borrower (who issues thebond) promises to pay a fixed amount of dollars (the coupon) each period

8 CHAPTER 10. INTERTEMPORAL CHOICE

until a certain date T (the maturity date), at which point the borrowerwill pay an amount F (the face value) to the holder of the bond.

Thus the bond has a payment stream which looks like (x, x, x, ..., F ). Ifthe interest rate is constant, the present discounted value of such a bond is

PV =x

1 + r+

x

(1 + r)2+ · · ·+ F

(1 + r)T

Note that the present value of a bond will decline if the interest rateincreases.

An interesting kind of bond is a bond that makes payments forever.These are called consols or perpetuities. Consider a consol that promisesto pay x a year forever. The present value of such a bond will be

PV =x

1 + r+

x

(1 + r)2+ . . .

We can factor out 1/(1 + r) to get

PV =1

1 + r

[x +

x

(1 + r)+

x

(1 + r)2+ . . .

]

The term in the brackets is just the x plust the present value. So we have

PV =1

1 + r[x + PV]

=x

r

10.8 Taxes

Please see the text.